topic 2: the relationship between microeconomics and...

TRANSCRIPT

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

Topic 2: The relationship between Microeconomics

and Management AccountingAna Mª Arias Alvarez

University of OviedoDepartment of Accounting

School of Business AdministrationCourse: Financial Statement Analysis and Management Control

Bachelor’s Degree in Economics

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

2.1. Basic concepts of the theories of production andcosts: a practical approach.

2.2. Necessary information to achieve scale, technicaland allocative efficiency.

2.3. Determining the costs of products and services.

2/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

Q

L

Q

L1 L2 L3

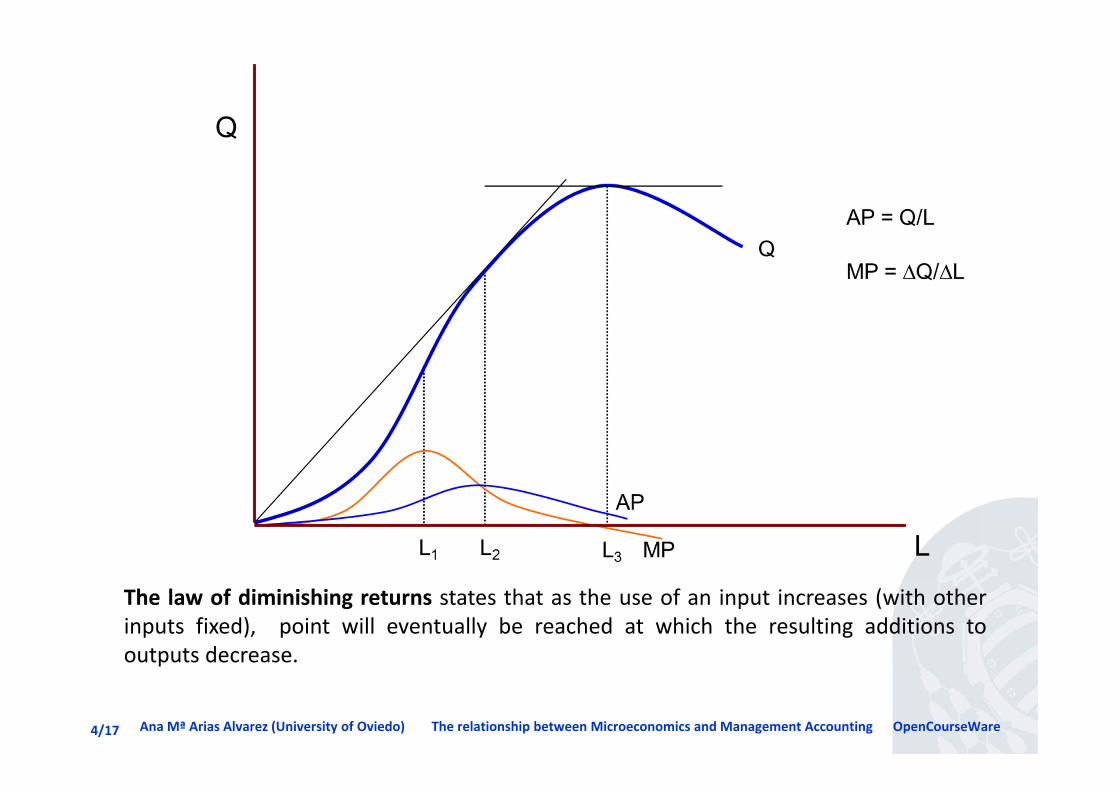

THE PRODUCTION FUNCTION

2.1: BASIC CONCEPTS OF THE THEORIES OF PRODUCTION AND COSTS: A PRACTICALAPPROACH.

3/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

The law of diminishing returns states that as the use of an input increases (with otherinputs fixed), point will eventually be reached at which the resulting additions tooutputs decrease.

4/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

€

Q

TC

VC

FC

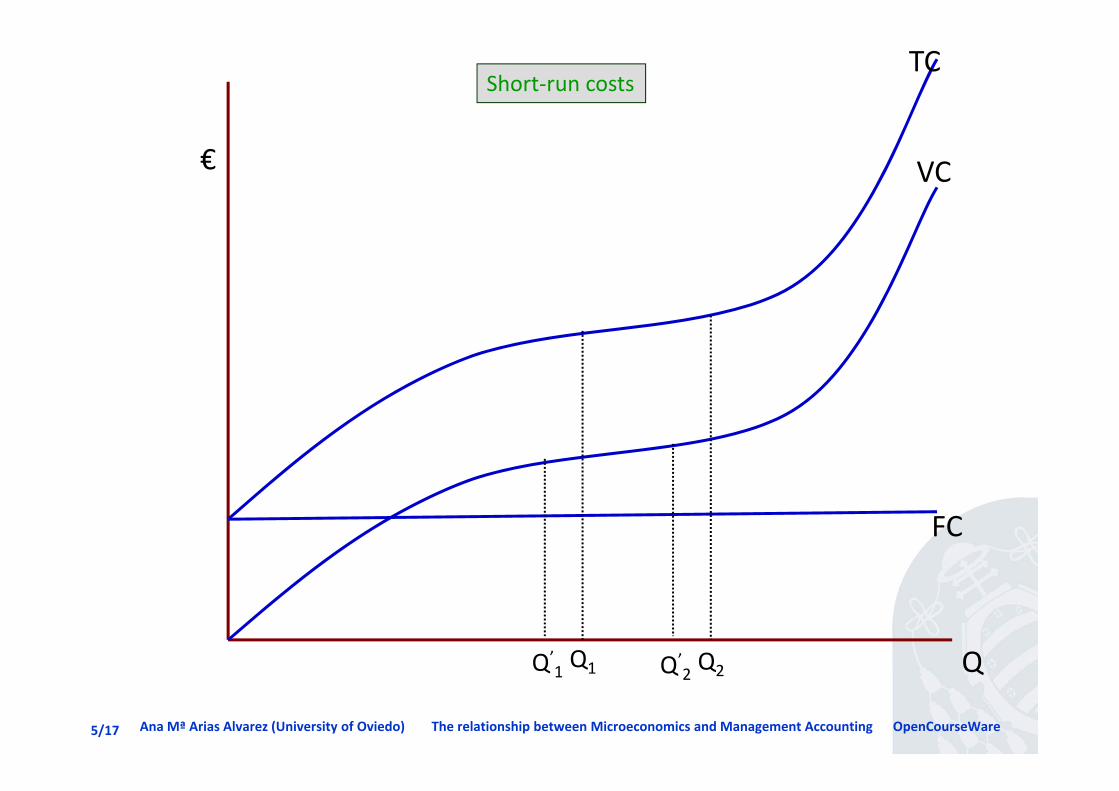

Short‐run costs

Q1 Q2Q’1 Q’

2

5/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

€

Q

ATC

AVC

AFC

MC

Q0Q’0

6/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare7/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

Task: try to solve problem 2.1.

8/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

Q

L

TP

L0Q

LL0

AP

MP

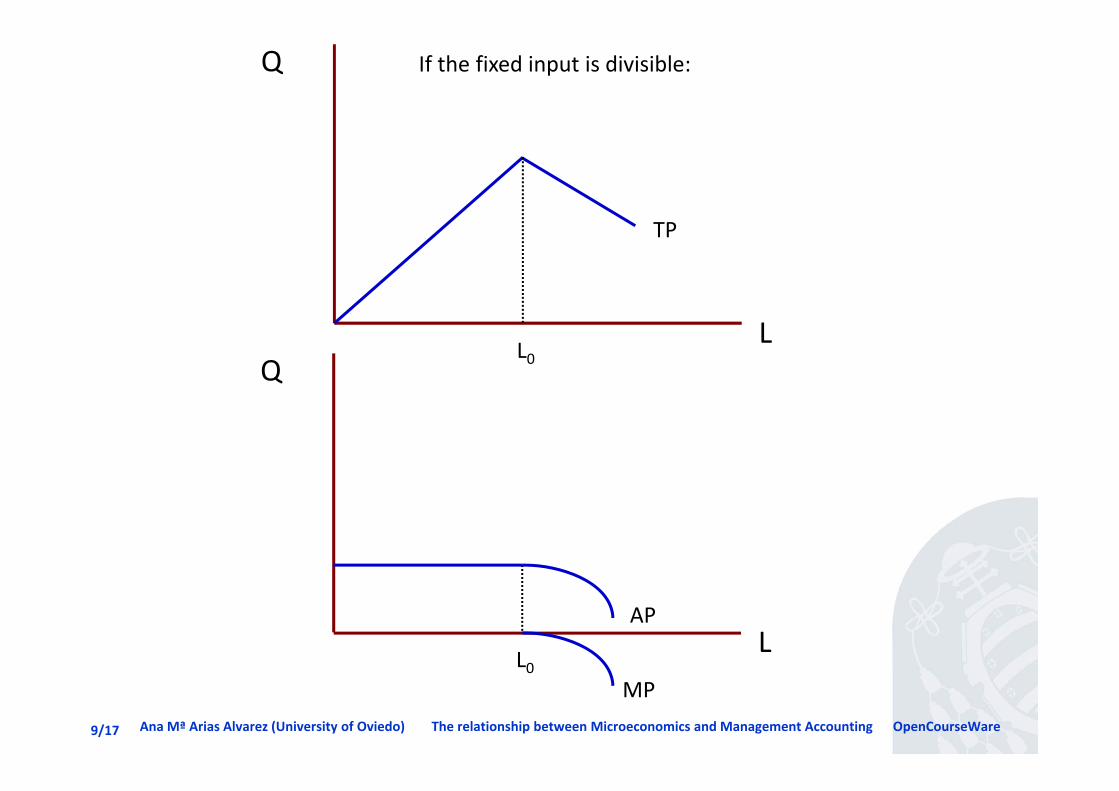

If the fixed input is divisible:

9/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

€

Q€

Q

L0

TC

TVC

L0

AVC= MC

AVCMC

TFC

ATC

AFC

10/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

2.2: NECESSARY INFORMATION TO ACHIEVE SCALE, TECHNICAL ANDALLOCATIVE EFFICIENCY.

Scale efficiency means that firms are of the appropriate size. Profit is at a maximum wheremarginal revenue equals marginal cost. If the firm is operating under perfect competition, thatis achived if the firm is operating at the minimum of its long‐run average cost curve.

Technical efficiency: A technically efficient position is achieved when the maximum possibleimprovement in outcome is obtained from a set of resource inputs. An intervention istechnically inefficient if the same (or greater) outcome could be produced with less of onetype of input.

Allocative efficiency describes the use of inputs in the proportion that minimizes the cost ofproduction, given input prices.

Economic efficiency comprises both technical efficiency and allocative efficiency.

11/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

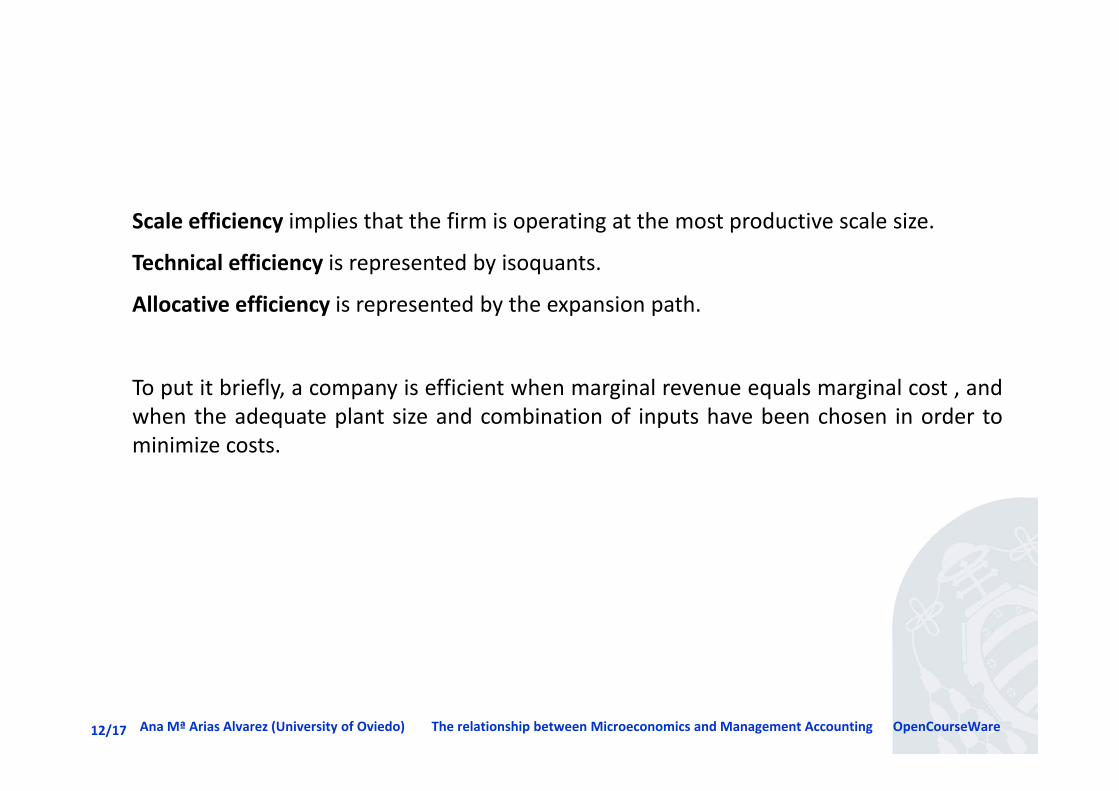

Scale efficiency implies that the firm is operating at the most productive scale size.

Technical efficiency is represented by isoquants.

Allocative efficiency is represented by the expansion path.

To put it briefly, a company is efficient when marginal revenue equals marginal cost , andwhen the adequate plant size and combination of inputs have been chosen in order tominimize costs.

12/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

K

LwC1

rC1

Q1

Q2

Q0

Q3

wC0

rC0

wC2

rC2

wC3

rC3

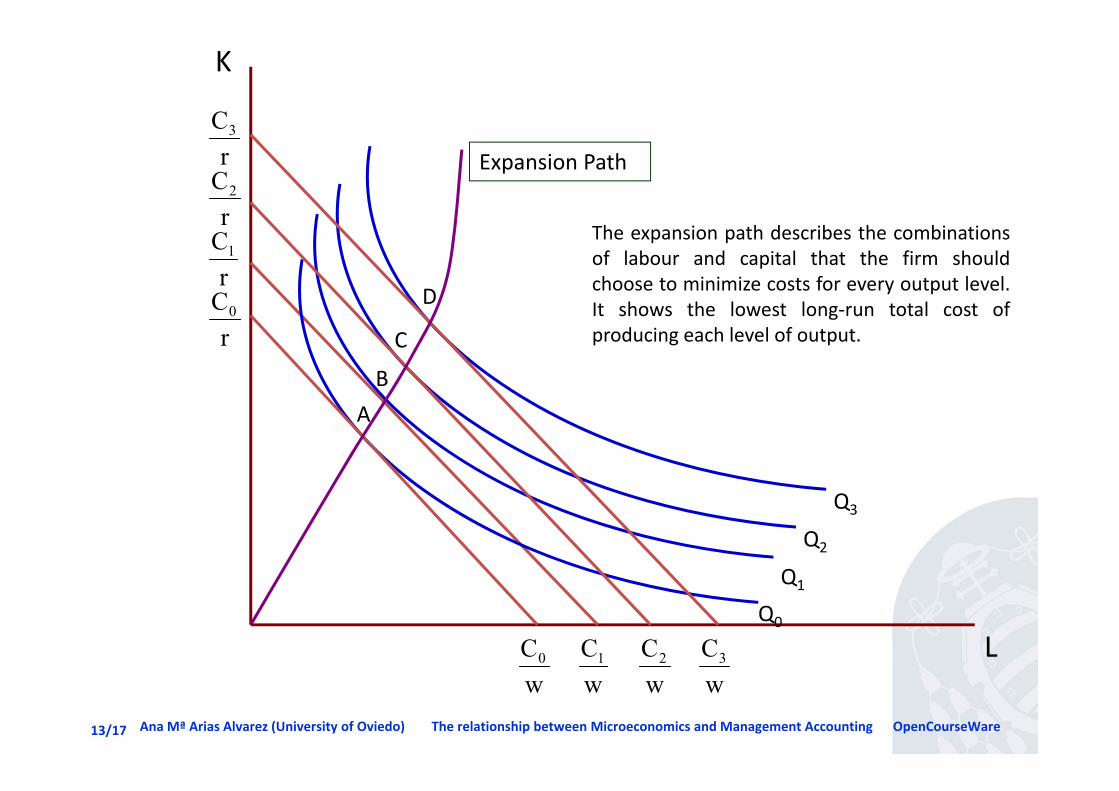

Expansion Path

AB

C

D

The expansion path describes the combinationsof labour and capital that the firm shouldchoose to minimize costs for every output level.It shows the lowest long‐run total cost ofproducing each level of output.

13/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

Q3Q0

€/unit

Q

LAC

Q1

AC1

Q2

AC2

SACSMCSAC

SAC

SAC

SACSAC

SAC SAC

The relationship between short‐run and long‐run cost:

AC0

14/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

€

QQ1 Q2

TC1 TC2 TC3

A

C

B

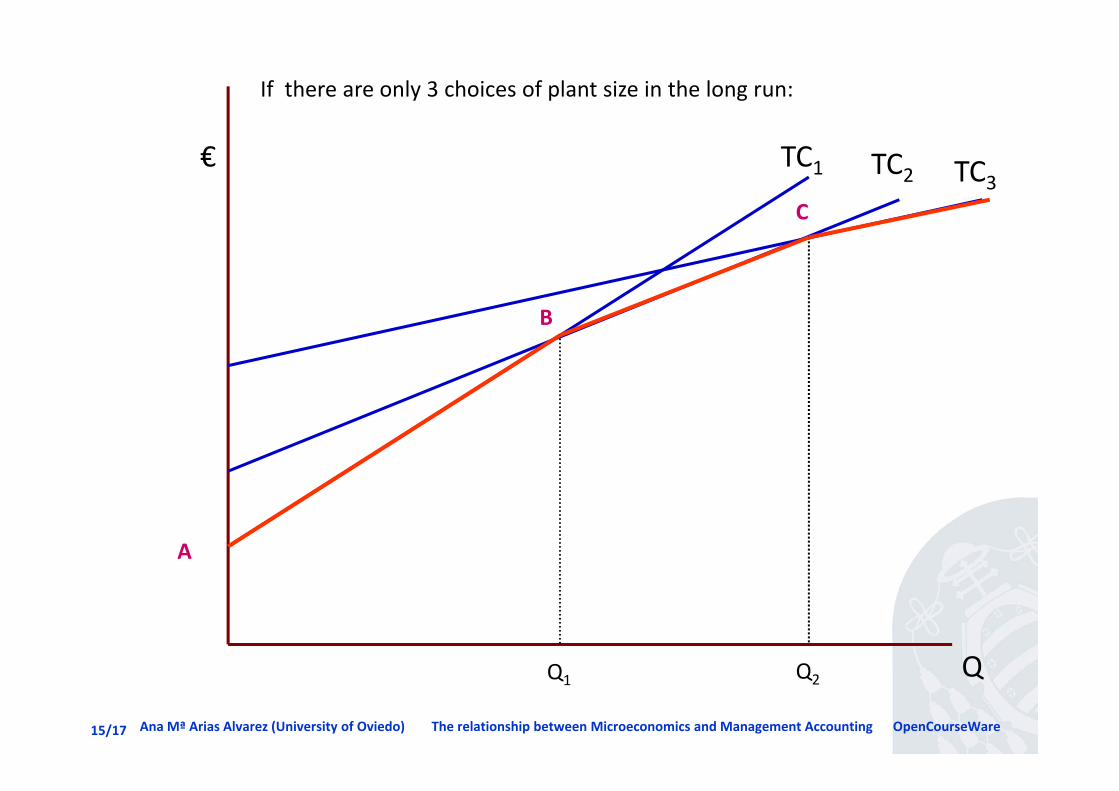

If there are only 3 choices of plant size in the long run:

15/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

Task: try to solve problem 2.2.

16/17

Ana Mª Arias Alvarez (University of Oviedo) The relationship between Microeconomics and Management Accounting OpenCourseWare

2.3: DETERMINING THE COSTS OF PRODUCTS AND SERVICES.

How can cost information be of assistance in providing answers to questions about theconsequences of following particular courses of action:

1) Make or buy decisions: relevant costs should be taken into account (those expectedfuture costs that differ among alternative courses of action).

2) Determining the long‐run optimum production plan: the difference betweenrevenues and variable costs should be maximized taking into account technical andmarket restrictions.

3) How many units must be sold to break‐even? Costs should be separated into theirfixed and variable elements in order to calculate break‐even point.

4) Pricing decisions: should a company sell a product at a price below total cost?

17/17