topic 8: managing quality - s3.studentvip.com.au · acct2522 page 55 the non-conformance to...

TRANSCRIPT

Measures of customer value: Cost, time and …….. QUALITY

Quality of the entire customer experience including customer service, payment options•Customers may be internal or external to the firm•

Quality: The extent to which a product or service meets customers' needs and expectations

Performance•Aesthetics•Serviceability•Features: Characteristics of the product which differentiates it from similar products•Reliability: Does the product perform at constant level for the time it is expected to (warranty period)?

•

Durability: How long does the product last?•Quality of Conformance: Does the product conform to its design specifications?•Fitness for use: Any obvious design flaws? Eg. Faulty antenna•

Dimensions of Quality - Products

Dimensions of Quality - ServicesServices are consumed as they are produced

Responsiveness: Promptness and willingness to help○

Assurance: Having knowledge and ability to evoke trust○

Performance•

Aesthetics•Features: Eg. Some airlines provide pyjamas, better quality blankets and amenities•Reliability: Is the service always given of the same quality?•Quality of conformance: Is the service performed as advertised•Fitness of use: Eg. Provision of criminal services such as tax evasion advice•

Two Stage Approach to Quality: Enhancing Customer Value

Quality can be broken down into the quality of design and the quality of conformance•

Customers may want/expect mobility for home phones○

Quality of design: Does the design meet customer expectations •

Quality of conformance: Can the firm produce the product?•

Illustration:

Topic 8: Managing QualitySaturday, 2 May 20154:08 PM

ACCT2522 Page 54

Screen clipping taken: 2/05/2015 5:00 PM

Quality Measurement Views/Approaches

Traditional View

Contemporary View Contemporary View 2

Quality Goal Minimise Cost of Quality

Zero Defects Zero Defects

Basis for improvement Evaluation

Information on cost of quality

Direct Measurement: defect rate

<-- Both

Quality Decision Minimise cost of quality

Optimise direct measures: minimise defect rate

Quality costs get management attention. Direct measures approach zero defects

Total Quality Management (TQM)

A comprehensive structure approach to achieving continuous improvement in processes to meet customers' 'expectations

•

Employees need to be trained for this

Employees have authority to make decisions such as stopping production if machine is faulty

All employees are committed to improving quality (not just inspectors)○

All processes in designing and manufacturing need to be of high quality

High quality inputs?□

High quality machinery?□

All aspects of process need to be considered

Process view adopted○

Quality Management system such as ISO 9000 series○

Other features of TQM (holistic approach)•

Costs of Quality (COQ)

Financial Measures

Prevention - Preventing non-conformities from occurring in the first place○

Appraisal - identifying defective (non-conformities) products○

Conformance Costs - ensure product quality meets standard•

Conformance costs are discretionary

Internal Failure - Products that fail to conform to quality standard after production but are corrected before delivery to customer

○

External Failure - Poor quality products are delivered to customers (eg litigation for damages)

○

Non-Conformance Costs - incurred when products are not up to standard•

Monitor these measures with a cost of quality report

ACCT2522 Page 55

The non-conformance to conformance ratio should be as low as possible as it is better to prevent non-conformances than to correct them as they occur

•

Using COQ info to manage Quality

Identify Problems•

Largest Cost items

However, in the short term as shown in the graphs below, both conformance and non-conformance costs will increase.

□

Spending more on conformance costs (prevention and appraisal)

Prioritise improvements according to:○

Match quality-related expenses to customer needs (example C)○

Keep track of quality cost

Evaluate effectiveness of quality program

Monitoring in order to:○

Improve Quality•

COQ and ABM

An exception is if it is a regulatory requirement to inspect products○

Appraisal and failure activities are non-value added so we eliminate them•

Prevention activities can add value if performed efficiently so we try to reduce and select those activities to make them more efficient

•

Increasing Appraisal Costs in the short run

ACCT2522 Page 56

Here, your prevention costs are low. As you're appraisal costs increase, internal failures will be recognised more often and corrected which will in turn, minimise external failure costs.

Here, prevention costs are increased but appraisal costs are still high and so are internal failures but external failures are essentially eliminated.

Traditional View of Optimising Quality: Juran's Economic conformance level (ECL) or Acceptable Quality Level (AQL)

As the rate of conforming increases, conformance costs increase at an increasing rate and non-conformance costs decrease at a decreasing rate.

According to Juran, the optimal point is the one which minimises total COQ

Contemporary View

ACCT2522 Page 57

Conformance cost curve becomes flatter (decreases) over time because firms become better and improving quality with limited resources

•

Non-conformance costs become steeper (increases) over time as if you produce defective products, you lose more and more customers (sales) as your reputation is damaged

•

Ultimately, the curves will intersect at a 100% conformance level where there are no defects•

Traditional ECL View v Contemporary View

Traditional (minimise COQ) Contemporary View (minimise defects)

Driven by efficiency Driven by customer need (usually no defects)

Improving quality will increase time and cost

Improving quality reduces time and cost

Some defects are acceptable None are acceptable

Inspect for quality and rework if necessary

Quality should be designed and built in (easy to manufacture and meets customer expectations)

Quantity is just as important Quantity is irrelevant without quality

Direct (non-financial) Measures of Quality (DMOQ)

Often physical terms - eg diameter of hole drilled in product○

Eg Average customer waiting time at macas

This can be broken down in individual activities

Internal or external - may be from customers or firms perspective○

Measures the attributed of the produce, service or process•

Which Measures are more Useful?

COQ DMOQ

Focus on consequence which associates quality with $ Focus on process

Rank Problems Timely

Highlight trade-off between conform and non-conform costs

Understandable for all employees

Aggregated -- > easier to assess Identify root causes of problems

awareness, monitoring and prioritising Facilitates direct solutions and feedback

Disaggregated

awareness, monitoring and prioritising

ACCT2522 Page 58

Combining the Two

COQ for prioritising○

Tools such as fishbone and pareto diagram○

Early stages of quality improvement•

DMOQ for direct feedback ○

COQ still important to monitor performance and impact on bottom line○

Later stages•

Variability: Another Aspect of Quality

Affects customer perception○

Variability in amount of chilli powder used and spiciness of powder□

Eg. Kettle Chips

Variability multiplies○

Processes are harder to manage○

A lack of consistency in product or service quality•

Monitored using Statistical Process Control Chart (SPC)○

Variability management is very important•

Any quality measure that lies outside the upper and lower control limits needs to be investigated as it is not considered to be random error.

The traditional assumption is that an outcome is only costly if it lies outside the upper and lower control limits. Is this a fair assumption?

The contemporary view says no even if customers are not complaining as any variation will carry hidden quality costs such as lost customers/sales.

ACCT2522 Page 59

QLF Formula

L = k (Y-T)2

L: Unit Lossk: multiplier (proportionality constant)Y: Actual value of characteristicT: Target value

K = c/d2

c: Loss associated with a unit produced at the specification limitd: distance from target value to specification limit

If the variation is beyond the upper and lower limits, you will incur a cost c as customers will request a replacement

ACCT2522 Page 60

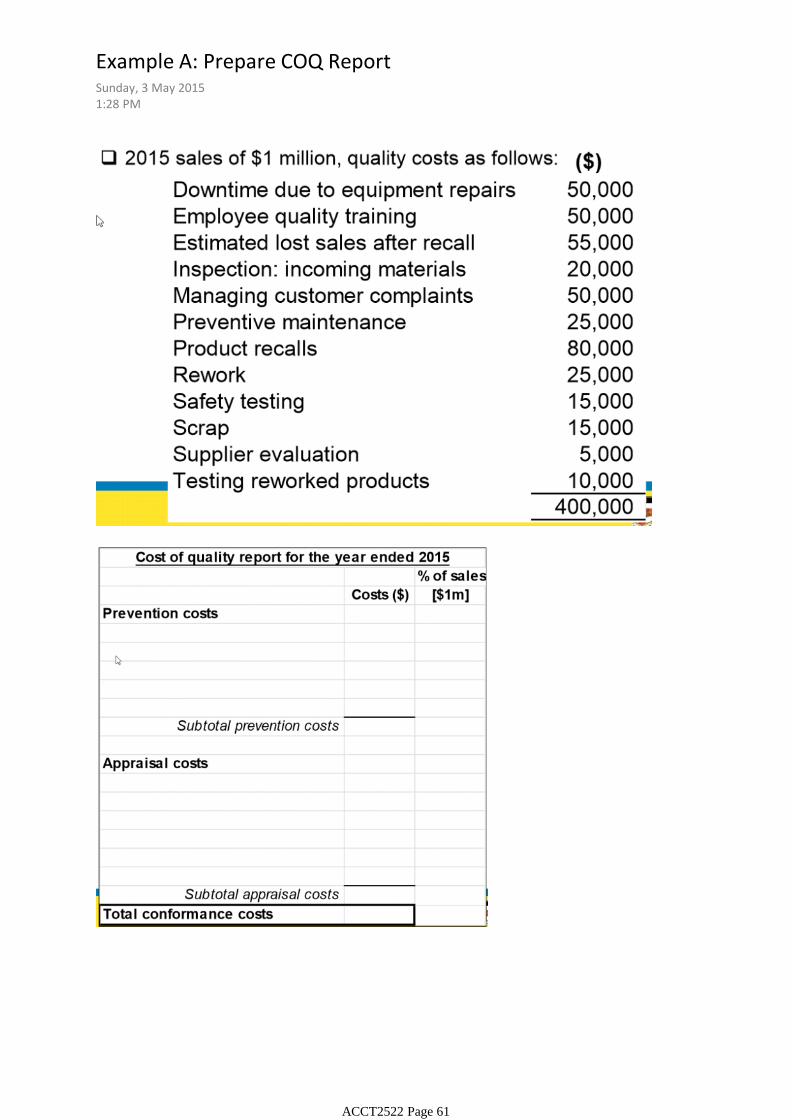

Example A: Prepare COQ ReportSunday, 3 May 20151:28 PM

ACCT2522 Page 61

ACCT2522 Page 62

Example B: Identify types of Quality CostsSunday, 3 May 20151:28 PM

ACCT2522 Page 63

ACCT2522 Page 64

Example C: Assigning quality cost to the importance placed on features by customersSunday, 3 May 20151:30 PM

ACCT2522 Page 65

Example D: DMOQ - internal/external?Sunday, 3 May 20157:34 PM

ACCT2522 Page 66

Example E: Variability and Process ManagementSunday, 3 May 20158:31 PM

ACCT2522 Page 67