toreador research & trading -...

TRANSCRIPT

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Individual Security Analysis For Macro Market Insights

Presented By:

Rafael Resendes

Toreador Research and Trading

Toreador Research & Trading

Global Investment Research Insights

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

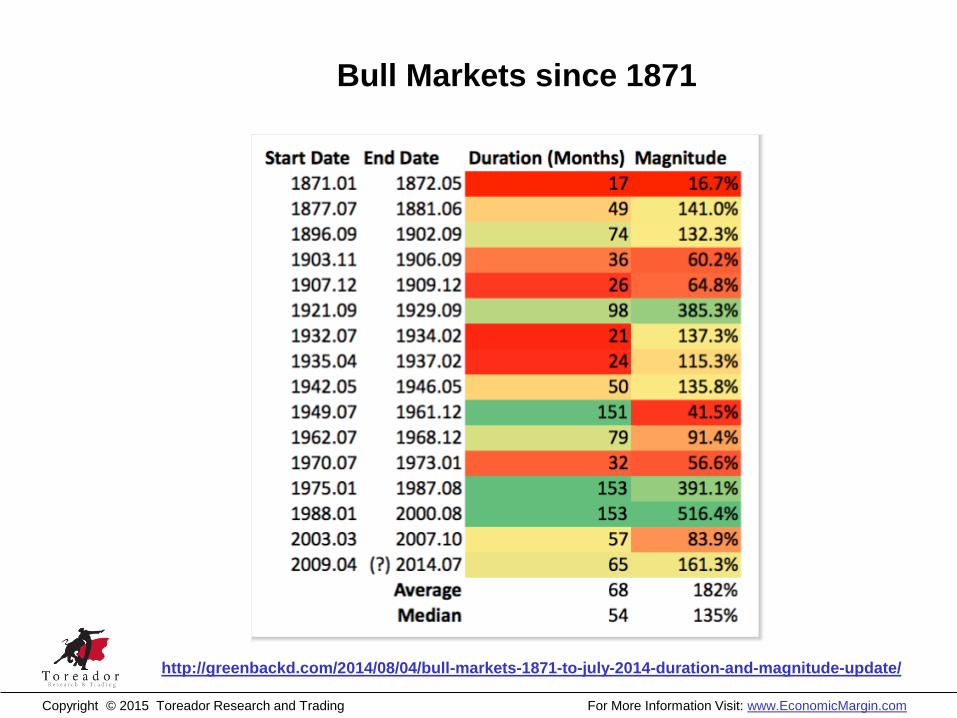

Bull Markets since 1871

http://greenbackd.com/2014/08/04/bull-markets-1871-to-july-2014-duration-and-magnitude-update/

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

http://www.businessinsider.com/santelli-meltdown-on-cnbc-2014-7

Has the world gone

mad?

What is an equity

investor to do?

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Understanding Intrinsic Value

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Getting to Performance Management

Company A Company B

Working Capital 100 0

Gross Plant 0 100

Total Assets 100 100

Cost of Capital 10% 10%

EBITDA 20 20

Cash Yield(EBITDA / Assets)

20% 20%

Are these firms really similar?

Simplistic accounting based analysis shows that these firms have similar

risk and return characteristics. However the asset compositions of each

firm indicates they have very different underlying economics.

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

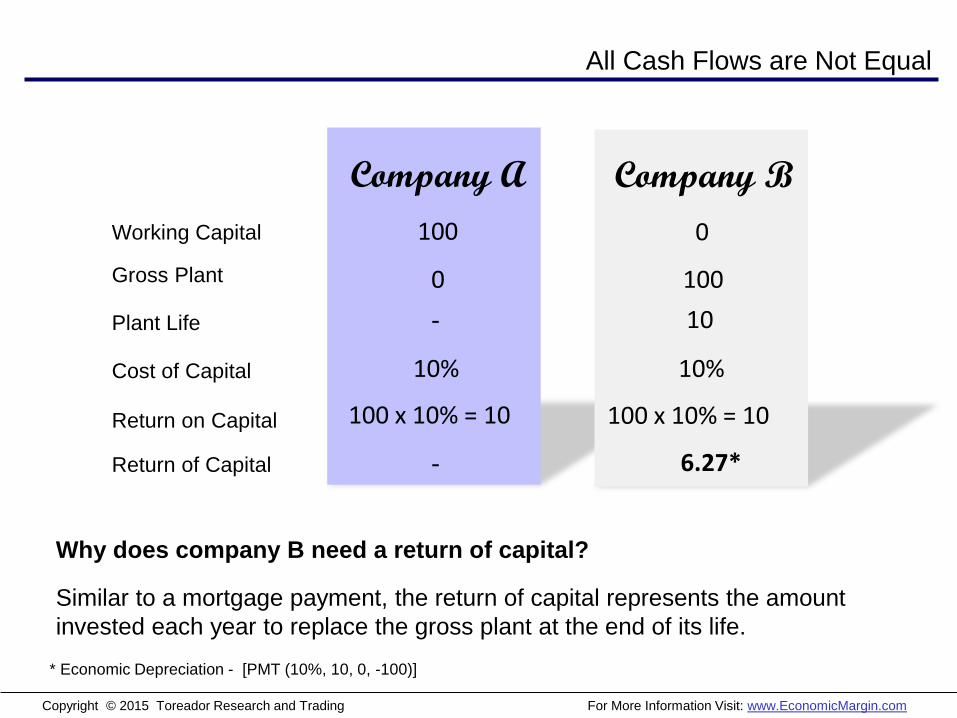

All Cash Flows are Not Equal

Company A Company B

Working Capital 100 0

Gross Plant 0 100

Plant Life - 10

Cost of Capital 10% 10%

Return on Capital 100 x 10% = 10

Return of Capital - 6.27*

* Economic Depreciation - [PMT (10%, 10, 0, -100)]

Why does company B need a return of capital?

Similar to a mortgage payment, the return of capital represents the amount

invested each year to replace the gross plant at the end of its life.

100 x 10% = 10

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

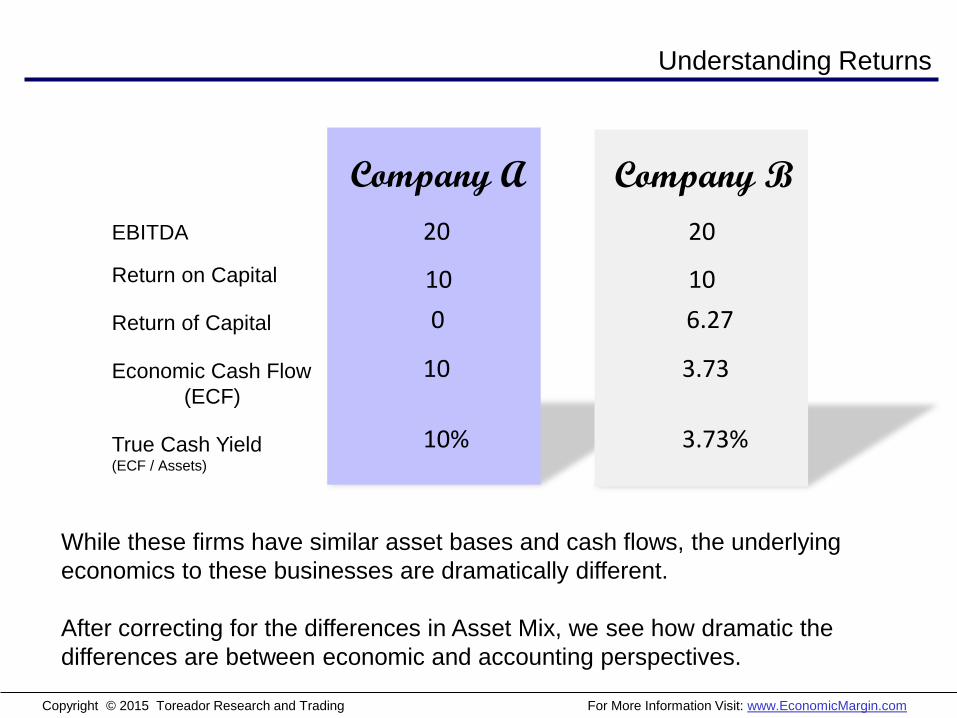

Understanding Returns

Company A Company B

EBITDA 20 20

Return on Capital 10 10

Return of Capital 0 6.27

Economic Cash Flow

(ECF)

10 3.73

True Cash Yield(ECF / Assets)

While these firms have similar asset bases and cash flows, the underlying

economics to these businesses are dramatically different.

After correcting for the differences in Asset Mix, we see how dramatic the

differences are between economic and accounting perspectives.

10% 3.73%

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

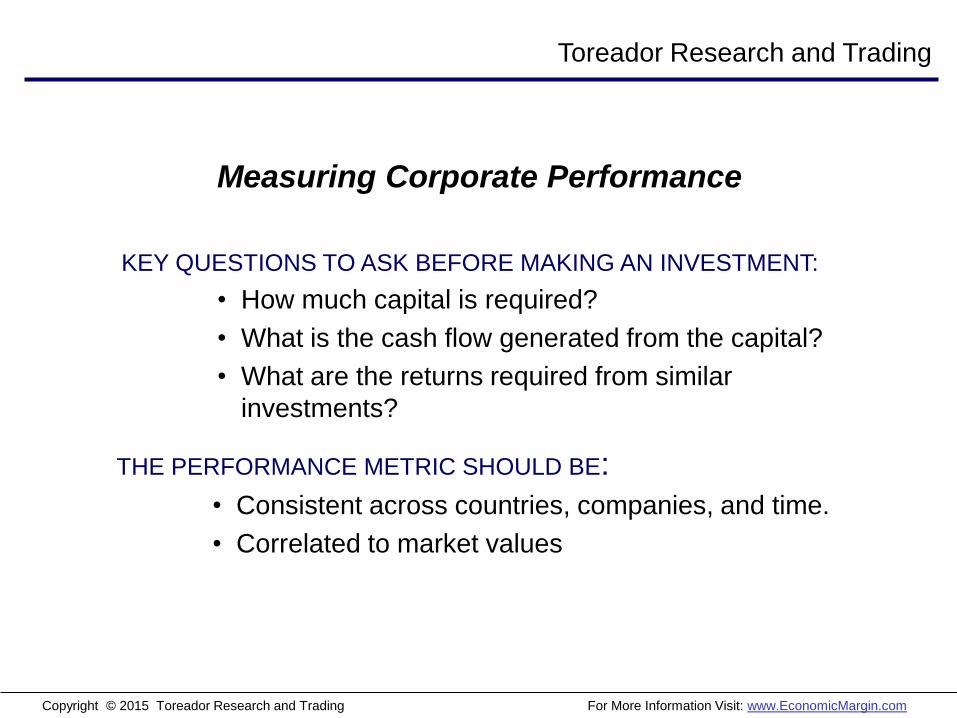

KEY QUESTIONS TO ASK BEFORE MAKING AN INVESTMENT:

• How much capital is required?

• What is the cash flow generated from the capital?

• What are the returns required from similar

investments?

THE PERFORMANCE METRIC SHOULD BE:

• Consistent across countries, companies, and time.

• Correlated to market values

Measuring Corporate Performance

Toreador Research and Trading

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

EARNINGS ARE A POOR PROXY FOR ECONOMIC PROFITABILTY

• Cash Flow

• Cost of Capital

• Inflation

ACCOUNTING RATIOS MIX/CONFUSE MANY DIFFERENT RATIOS

• Asset Life

• Asset Mix

• Asset Age

• Capital Structure

• Growth

ACCOUNTING RULES DISTORT MANY ASPECTS OF ECONOMIC REALITY

• Leases

• Research and Development

• Revaluations/Goodwill Written Off

• Accelerated Depreciation

Toreador Research and Trading

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Toreador Valuation Framework

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

• Properly understanding how well a company is performing

• Asset characteristics

• Risk

• Incorporating time tested concepts such as competition and risk

• Ability to value thousands of companies to create market insights

• An actual ability to explain how markets tend to work

A Useful Micro/Macro Valuation Approach Requires:

The Toreador Valuation Approach…

Toreador Research and Trading

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Economic Margin Framework

Operations Based Cash Flow:

+ Net Income

+ Depreciation & amortization

+ After Tax Interest Expense

+ Rental Expense Net Int. Adj.

+ R & D Expense

± Non-Recurring Items

Inflation Adjusted Invested Capital:

+ Total Assets

+ Accumulated Depreciation

+ Gross Plant Inflation Adjustment

+ Capitalized Operating Rentals

+ Capitalized R & D

- Non Debt Current Liabilities

- Revaluations

Capital Charge:

Return on and Return of Capital

that captures company specific

economic circumstances.

Economic Margin Calculation Details

(Country Specific COC)

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Economic Margin Framework

Given 5% WACC, What Must Project Yield To Break Even?

Investment:

PV

Life = 10 years

N

PMT = ?Salvage:

$5,000FV

$10,000

Annual Economic Charge = $898

FV (Salvage Value)

N (Life) 0% 50% 100%

7 $1,728 $1,114 $500

10 $1,298 $898 $500

13 $1,065 $728 $500

* Calculated using the Payment function [PMT (5%, 10, 0, -10,000)]

EM =Cash Flow – Capital Charge

Invested Capital

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

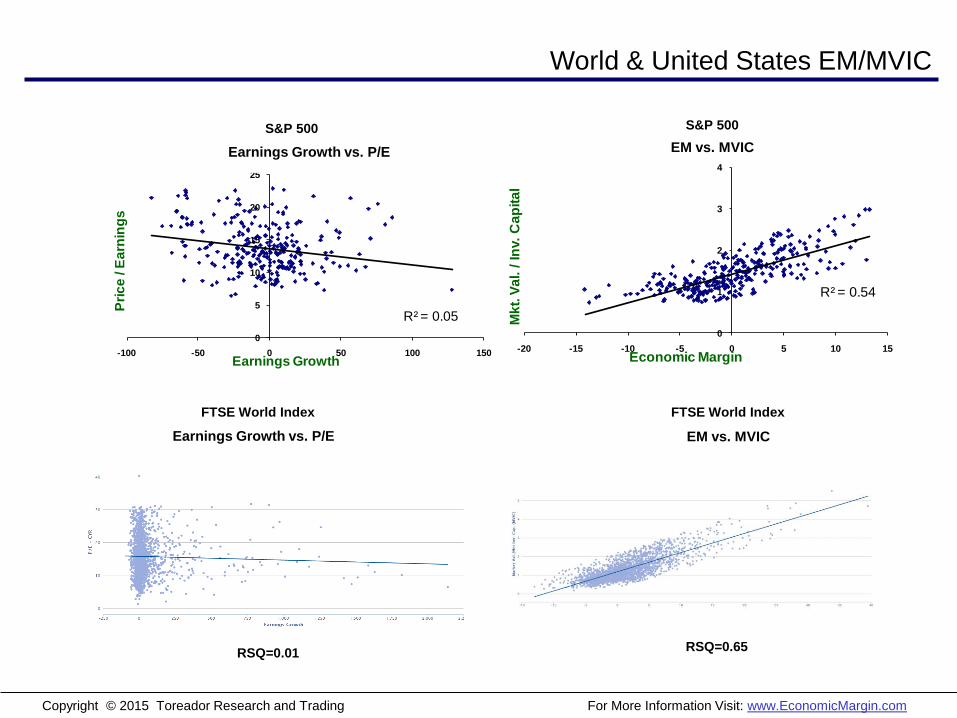

World & United States EM/MVIC

R² = 0.05

0

5

10

15

20

25

-100 -50 0 50 100 150

Pri

ce

/ E

arn

ing

s

Earnings Growth

Earnings Growth vs. P/E (United States 2009)Earnings Growth vs. P/E

R² = 0.54

0

1

2

3

4

-20 -15 -10 -5 0 5 10 15

Mk

t. V

al. /

In

v.

Ca

pit

al

Economic Margin

EM vs. MVIC (United States 2009)EM vs. MVIC

S&P 500 S&P 500

Earnings Growth vs. P/E EM vs. MVIC

FTSE World Index FTSE World Index

RSQ=0.01RSQ=0.65

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Linking Performance to Value

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

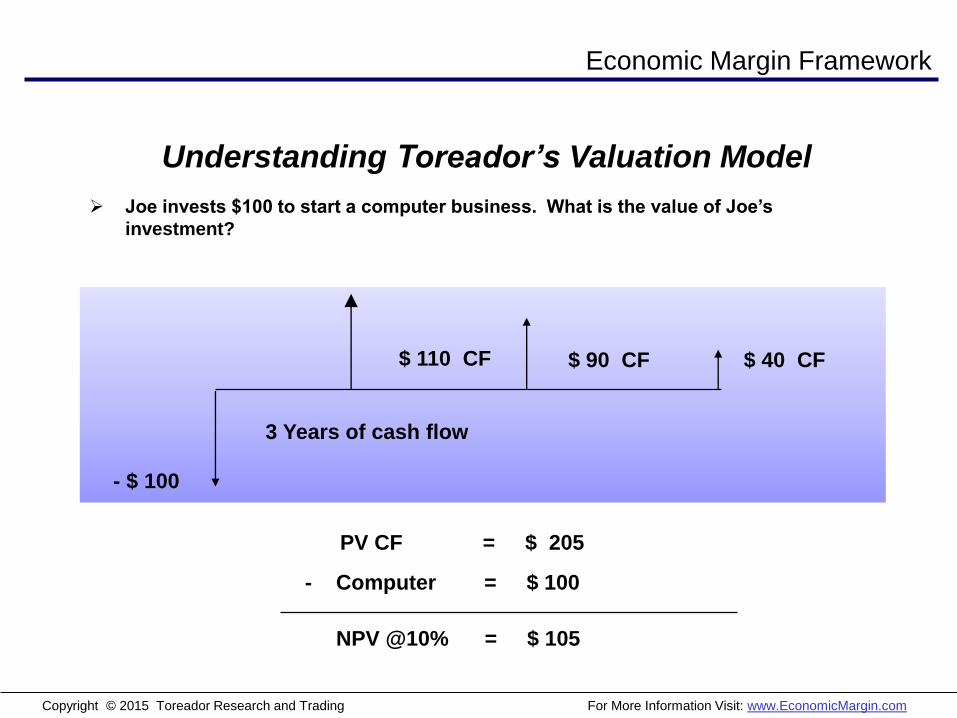

Economic Margin Framework

Joe invests $100 to start a computer business. What is the value of Joe’s

investment?

$ 90 CF

- $ 100

3 Years of cash flow

$ 110 CF $ 40 CF

PV CF = $ 205

NPV @10% = $ 105

- Computer = $ 100

Understanding Toreador’s Valuation Model

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

A New Approach: Linking Performance to Value

Yr 1 Yr 2 Yr 3

+ Cash Flow 110 90 40

- Capital Charge 40 40 40

= Economic Profit 70 50 0

x PV Factor .91 .83 .75

= Economic Value 64 + 41 + 0 = 105

____ ____ ____

If EM=0, it Creates No Value Regardless of its EPS or Cash Flow!

Economic Margin = 70% 50% 0%

Economic Margin Framework

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Effects of Competition and Decay

Capturing Franchise Value: Economic Margin Decay

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Capturing Franchise Value: Economic Margin Decay

Historical Decay Analysis – Russell 1000® Index

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

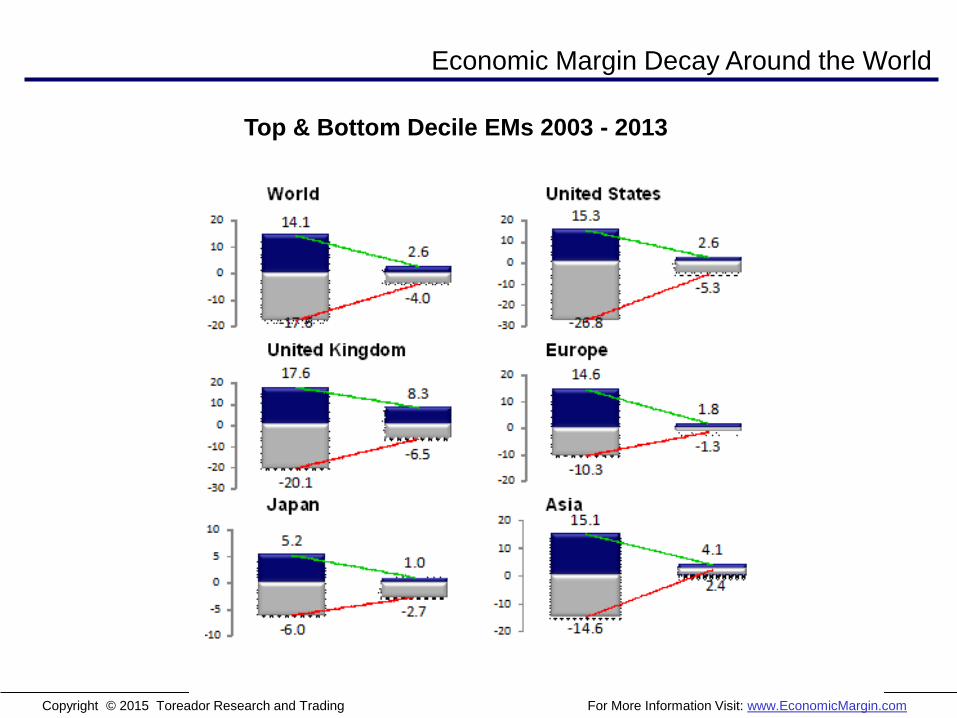

Economic Margin Decay Around the World

Top & Bottom Decile EMs 2003 - 2013

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Valuation – Cost of Capital

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

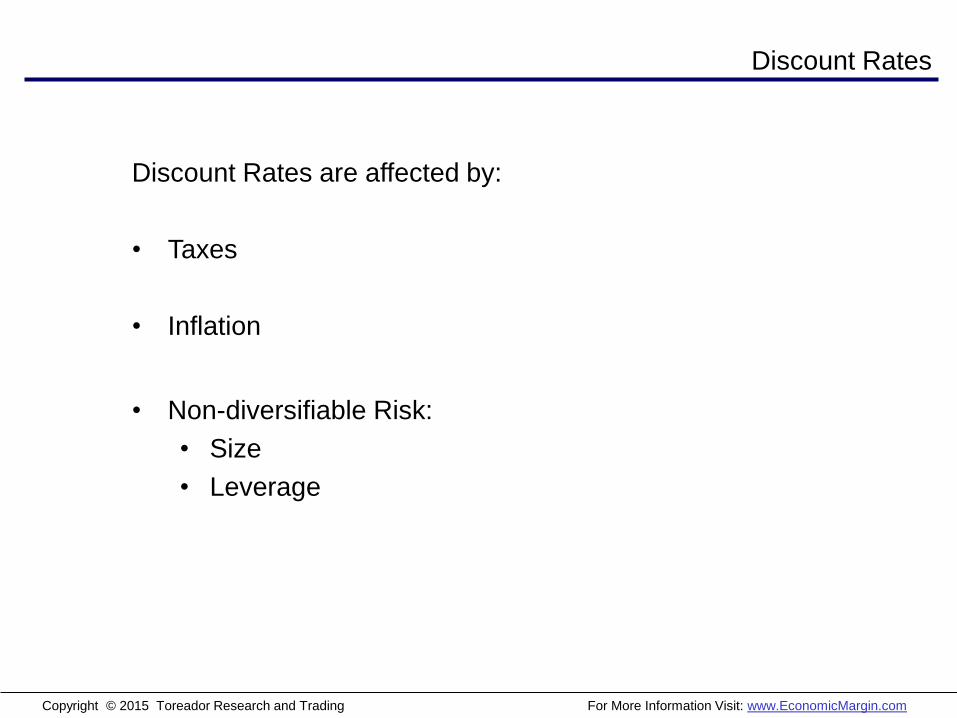

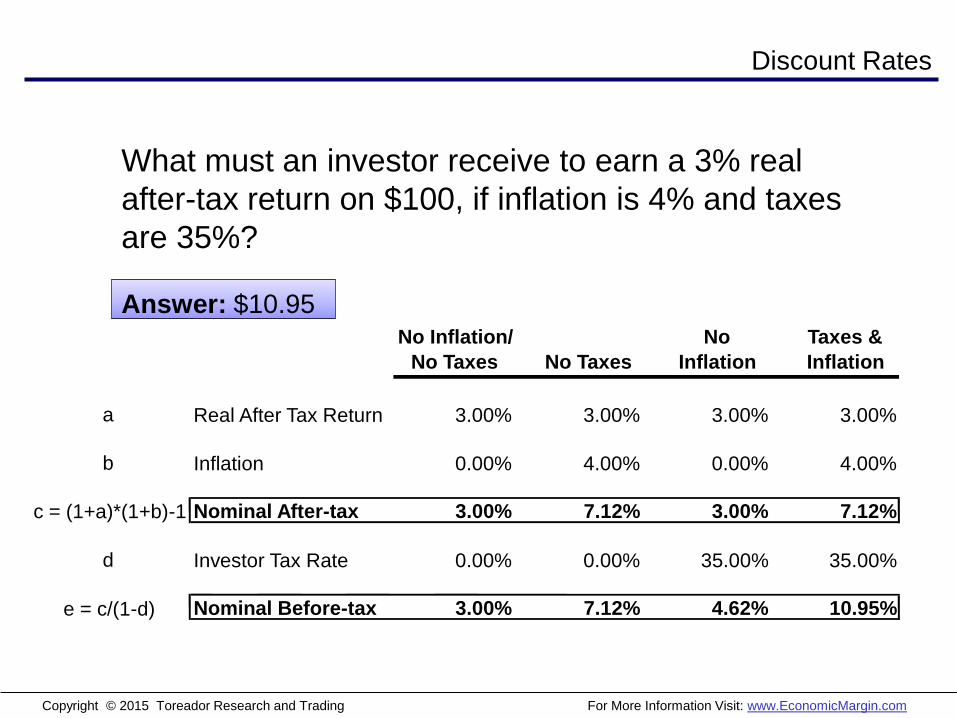

Discount Rates

Discount Rates are affected by:

• Taxes

• Inflation

• Non-diversifiable Risk:

• Size

• Leverage

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

No Inflation/

No Taxes No Taxes

No

Inflation

Taxes &

Inflation

a Real After Tax Return 3.00% 3.00% 3.00% 3.00%

b Inflation 0.00% 4.00% 0.00% 4.00%

c = (1+a)*(1+b)-1 Nominal After-tax 3.00% 7.12% 3.00% 7.12%

d Investor Tax Rate 0.00% 0.00% 35.00% 35.00%

e = c/(1-d) Nominal Before-tax 3.00% 7.12% 4.62% 10.95%

What must an investor receive to earn a 3% real

after-tax return on $100, if inflation is 4% and taxes

are 35%?

Answer: $10.95

Discount Rates

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

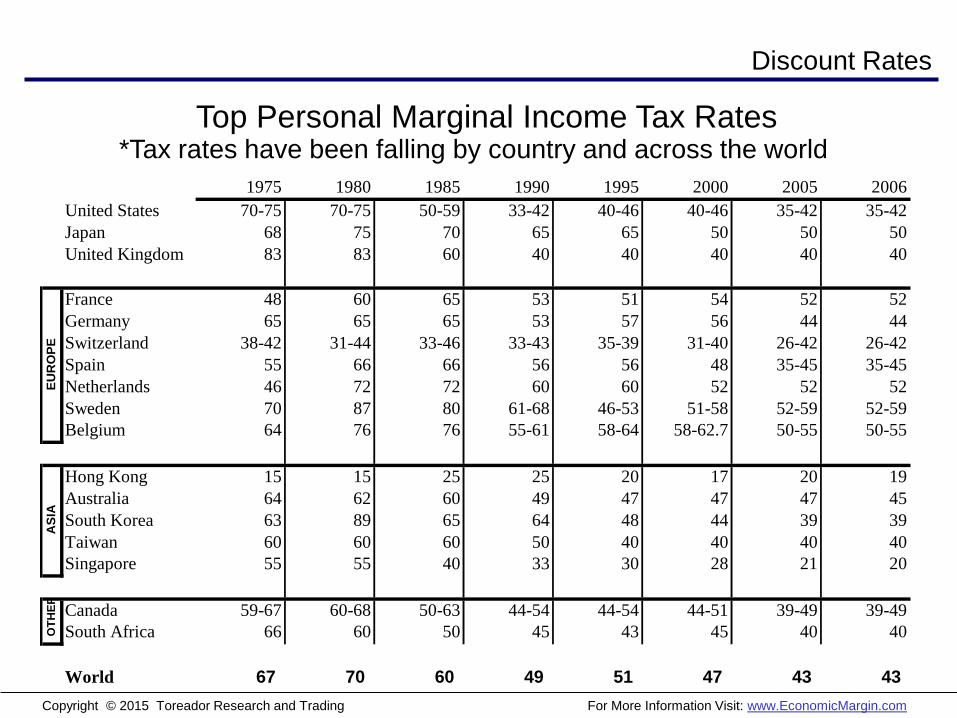

Discount Rates

*Tax rates have been falling by country and across the world

1975 1980 1985 1990 1995 2000 2005 2006

United States 70-75 70-75 50-59 33-42 40-46 40-46 35-42 35-42

Japan 68 75 70 65 65 50 50 50

United Kingdom 83 83 60 40 40 40 40 40

France 48 60 65 53 51 54 52 52

Germany 65 65 65 53 57 56 44 44

Switzerland 38-42 31-44 33-46 33-43 35-39 31-40 26-42 26-42

Spain 55 66 66 56 56 48 35-45 35-45

Netherlands 46 72 72 60 60 52 52 52

Sweden 70 87 80 61-68 46-53 51-58 52-59 52-59

Belgium 64 76 76 55-61 58-64 58-62.7 50-55 50-55

Hong Kong 15 15 25 25 20 17 20 19

Australia 64 62 60 49 47 47 47 45

South Korea 63 89 65 64 48 44 39 39

Taiwan 60 60 60 50 40 40 40 40

Singapore 55 55 40 33 30 28 21 20

Canada 59-67 60-68 50-63 44-54 44-54 44-51 39-49 39-49

South Africa 66 60 50 45 43 45 40 40

World 67 70 60 49 51 47 43 43

EU

RO

PE

AS

IAO

TH

ER

Top Personal Marginal Income Tax Rates

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Discount Rates

WORLD US

1980-89 1990-99 2000-08 1980-89 2000-08

Real After-Tax Equity Rate 3.0% 3.0% 3.0% 3.0% 3.0%

Inflation 5.0% 2.3% 1.7% 4.9% 2.4%

Nominal After-Tax Equity Rate 8.2% 5.3% 4.8% 8.0% 5.5%

Tax-Rate 60% 51% 43% 55% 39%

Nominal Before-Tax Equity Rate 20.3% 10.9% 8.4% 17.8% 8.9%

Lower inflation and investor tax rates have dropped required

equity rates by approximately half from 1980 levels.

Going forward, where will the current government fiscal policies

take us?

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Discount Rates

Median Market Derived Discount Rates By Country

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Discount Rates

Discount Rates: Size & Leverage Effect

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Does Intrinsic Value Make Sense?

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Source: AFGView client databases 1991-2014

Valuation Metric Quintile Analysis – Russell 1000® Index

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

-15%

-10%

-5%

0%

5%

10%

15%

F A

A vs. F Percent to Target – Current Spreads: Global and US Analysis

AFG International Backtest Database: Percent to Target - Current [Global Quintile By Sector] from 12/31/91 to 12/31/14

Universe Size: 5,200 to 14,100 Companies - Global Analysis | All Sectors | All Cap | ADRs Excluded

COUNTRY ANALYSIS

‘

SECTOR ANALYSIS SIZE/STYLE

‘

SECTOR ANALYSIS SIZE/STYLE INDEX/ADR

AFG International Backtest Database: Percent to Target - Current [Global Quintile By Sector] from 12/31/91 to

12/31/14 Universe Size: 2,200 to 5,400 Companies - United States | All Sectors | All Cap | ADRs Included

Global Analysis United States Analysis

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

After Such A Long Run, We have Reached

The Stare Down

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Valuation Trends

• Plot standardized valuation levels vs warning bands

• Categories: US, International, Size (Large, Mid, Small), Leverage,

Style (Value, Growth), & Sectors

• Period: 12/31/1991 to 1/31/2015

• US Traded Stocks

Valuation and Market Cycles

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

US Equities: ALL

Upside %: December 1991- Jan 2015

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

INTL Equities: All

Upside %: December 1991- Jan 2015

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

US Equities: Mid

Upside %: December 1991- Jan 2015

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

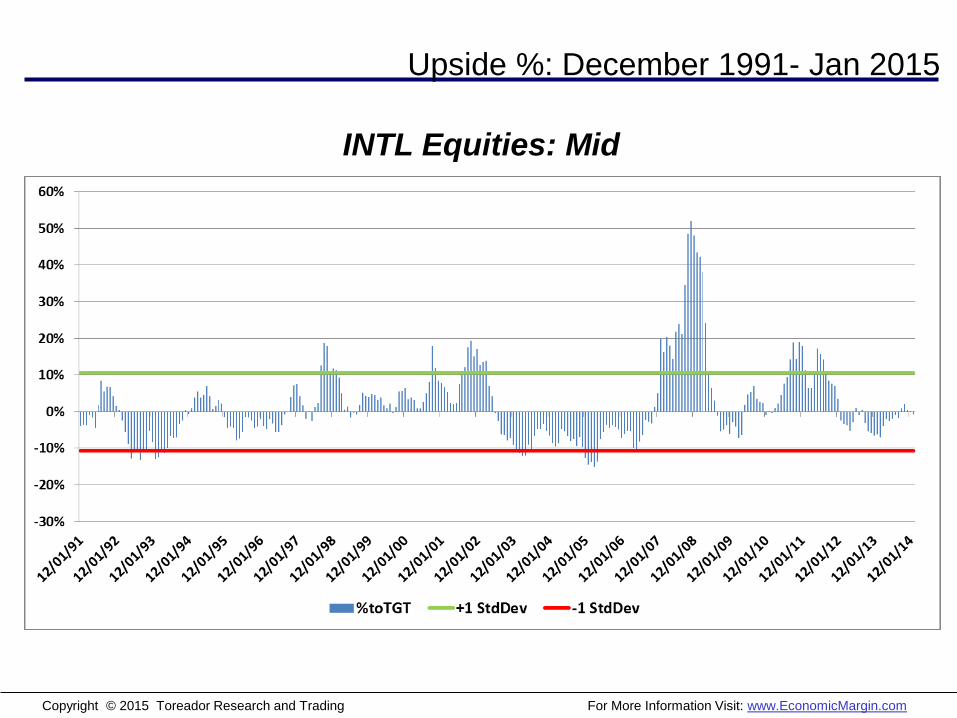

INTL Equities: Mid

Upside %: December 1991- Jan 2015

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

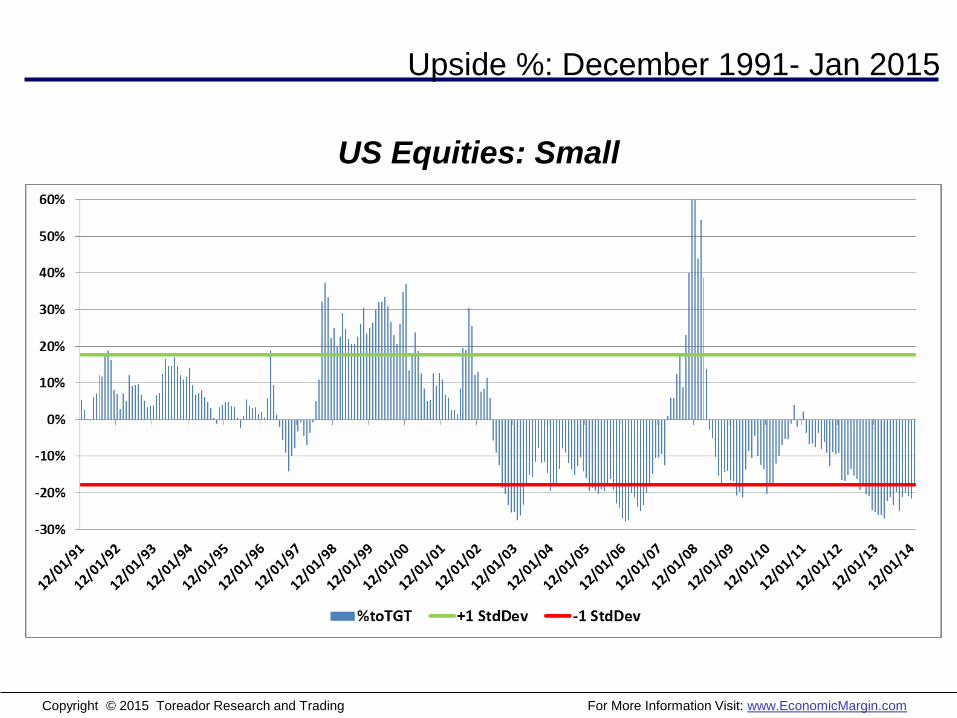

US Equities: Small

Upside %: December 1991- Jan 2015

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

INTL Equities: Small

Upside %: December 1991- Jan 2015

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

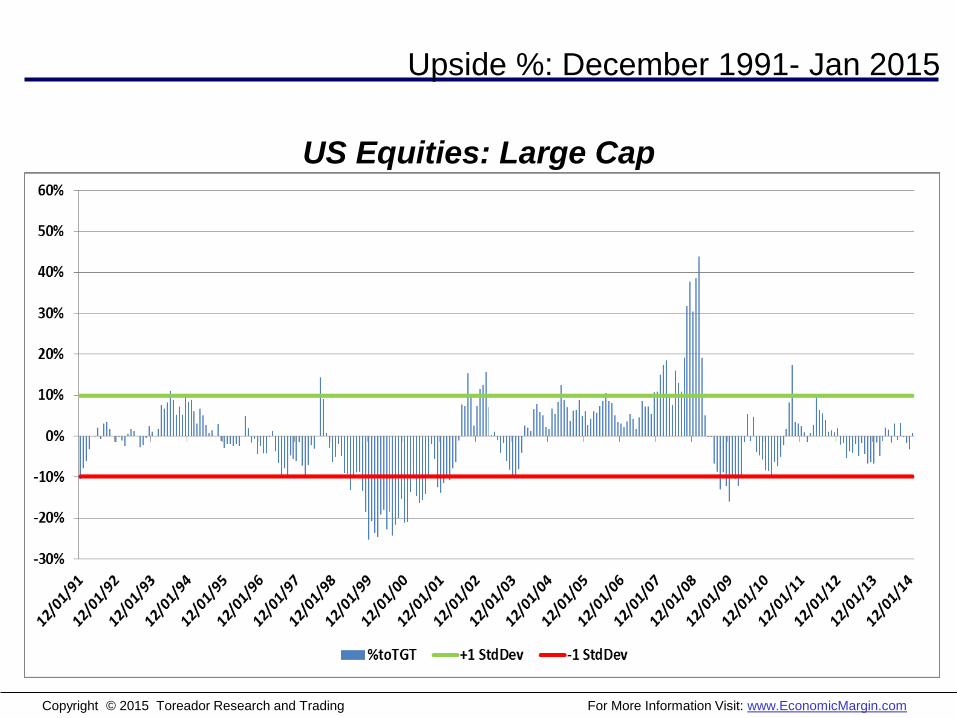

US Equities: Large Cap

Upside %: December 1991- Jan 2015

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

INTL Equities : Large

Upside %: December 1991- Jan 2015

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

US vs. Intl Upside Characteristics

• As measured by Percent to Target, US and Intl

Large Cap equities appear similarly valued for

upside potential

• International Equities have slightly higher

upside than US equities, though this has

varied over the past 6 months with US equities

at times appearing to have slightly higher

upside

• International QE Programs provide a support

catalyst for Intl equities that no longer exists

for US stocks, increasing Intl attractiveness

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

US vs. Intl

• US and Intl Cost of Capital have converged over the last 20 years

• International QE maybe be the catalyst that brings the rates together again in the

near future.

• From an equity risk premium perspective, international equities offer much more

attractive risk/return opportunities

Implied Future Returns

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

US vs. Intl Implied Future Returns

• Though upside as measured by Percent to Target is similar for US and

Intl Large Cap stocks, implied future returns are more favorable for

Intl stocks

• As of Jan 30, 2015 the market derived rate of return to Intl equities was

approximately 100bps higher than for US equities

• If we increase the cost of capital for US stocks by 100 bps, they

become approximately 15% over-valued, making Intl equities quite a

bit more attractive on a relative basis.

• As measured from an Equity Risk Premium perspective, International

Equities become even more appealing

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Discount Rates

5.25

6.586.17

9.73

7.157.53

6.15

0

2

4

6

8

10

12

US Canada UK Germany Japan Europe ex. UK&GER Asia ex. JPN

GLOBAL EQUITY RISK PREMIUMS

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Conclusions

• Don’t be a hero – Large Cap stocks domestically and

internationally are likely the best equity class at the

moment

• International QE programs are likely to provide an

ongoing trend to reduce cost of capital globally back

towards US levels, making international equities

particularly attractive

• Strategically, any weakness internationally should be

exploited to ensure portfolios are at least market

neutral internationally

• Specific stock picks should consider both valuation

and momentum – those interested, attend our portfolio

workshop – March 31st at the St Regis

Copyright © 2015 Toreador Research and Trading For More Information Visit: www.EconomicMargin.com

Disclaimers

The Applied Finance Group, Ltd. certifies that the views expressed in this report accurately reflect the firm's models. The information in this

report is based on material we believe to be accurate and reliable, however, the accuracy and completeness of the material and conclusions

derived from said material are not guaranteed. The information is not intended to be used as the primary basis of investment decisions, and

The Applied Finance Group, Ltd. makes no recommendation as to the suitability of such investments for any person. Any opinions and

projections expressed herein reflect our judgment at this date and are subject to change without notice. Due to individual investor

requirements, this information should not be construed as advice meant to meet the investment needs of any investor. This information is

not an offer to buy or sell, or a solicitation of an offer to buy or sell any securities.

The Applied Finance Group, Ltd, its owners, employees and/or customers may have positions in the securities whose information is

available on this report. No part of this report may be reproduced, copied, redistributed or posted without prior consent of The Applied

Finance Group, Ltd.

Russell Investment Group is the source and owner of the Russell Index data contained or reflected in this material and all trademarks and

copyrights related thereto. Recipient of this Russell Index data is prohibited from making any further redistribution of the Russell Index data

included in this material. Russell Investment Group is not responsible for the formatting or configuration of this material or for any

inaccuracy in AFG’s presentation thereof..

All the information contained in this report is the property of The Applied Finance Group, Ltd. © 2012.

Contact Us

Illinois

The Applied Finance Group, Ltd.

105 W. Adams, Suite 2105

Chicago, IL 60603

(312) 362-9903

California

The Applied Finance Group, Ltd.

7493 N. Ingram Ave., Suite 104

Fresno, CA 93711

(559) 436-4270

Toreador Research and Trading