total banking system of jamuna bank limited

DESCRIPTION

Intern Report on Jamuna Bank Limited.TRANSCRIPT

1 | P a g e

1.0 Introduction

It’s simple enough to say that Bank is financial organization that deals with money. But it is the

precise most definition about bank. In modern age it is impossible to think a country without

bank. Banks play diversified role in an economy. Banking plays very significant contribution

towards socio-economic development of a country. This sector is considered to be like the life

blood the economy as well. As one of the most important components of the financial system it

forms the core of the money market and plays very pivotal role in mobilizing resources for

productive investments in a country which in turn contributes to economic development. The

efficiency of the sector is very important for overall development of the country. The most

important task that is done by a bank is building of capital. That is the key factor of the

development of an economy. An Industrialized nation’s build their industrial sector with the help

of banking sector. The growth of the economy also depends on the performance of the banking

sector. Banks secure money of the society. Government takes various monetary policies. These

policies are implemented with the help of banking sector. It is impossible to do foreign trade

without the help of bank. Banks provide services that help the business sector a lot to carry on

the business.

Jamuna Bank Limited (JBL) is a Banking Company registered under the Companies Act, 1994

with its Head Office at Chini Shilpa Bhaban, 3 Dilkusha C/A, Dhaka-1000. The Bank started its

operation from 3rd June 2001. Jamuna Bank Ltd. is a third generation bank in Bangladesh. It is

playing an important role to develop the business sector. The growth of this bank is very good.

Its motto is to provide a prompt and quick service to the clients. Jamuna Bank Ltd. has

implemented well structured online banking systems that make it easier to provide prompt

services to the customer.

This report has been prepared in the light of practical as well as theoretical knowledge.

Also it is prepared under the guidance and supervision of the core teacher. During the internship

program I have got a good idea about the bank and that is depicted in the report.

2 | P a g e

1.1 Origin of the Report

The BBA (Bachelor’s of Business Administration) internship program is required course for the

students who are graduating from East West University. It is a three credits hour course with the

duration of 3 Months. Students who have completed all the required courses are eligible to for

this course. In this internship program, I was attached to do my internship by rotation to all

departments of Jamuna Bank Limited, Shatinagar Branch, Dhaka. Both the academic supervisor

assigned me on this project. The report is on “Overall Banking System of JAMUNA Bank

Limited”.

1.2 Objective of the Study

The objectives of the report is to make us known the practical situation of commercial banks of

Bangladesh in overall activities and prepare me to face the complex situation of banking in this

country .The primary objective of this report is to commonly with the requirement of JBL.

However the objectives of this study are something broader. Objectives of the study are

summarized in the following manner.

General objectives:

The general objective is to prepare and submit a report on “Overall Banking System of Jamuna

Bank Limited”.

3 | P a g e

Specific objectives:

To apply theoretical knowledge in the practical field.

To present an overview of JAMUNA Bank Ltd

To develop our skill on the banking sector

To earn valuable knowledge about the general banking system

To know the customer service of banking sector.

To observed the practice of modern technology in banking sector.

Practical knowledge about transaction.

To assess the strength and weakness.

To identify possible areas of improvement

1.3 Methodology of the study

At the time of my internship period, I tried to use both primary and secondary data that I have

gathered from different sources. For preparing this report primarily I got some data from face to

face conversation of different employees of JBL Shantinagar branch and some from different

reports and features of the bank. Sometime I have undergone group discussion, asked some

questionnaires to the responsible officer of that work and interviewed with some of them. I

observed different parties and their transaction from a very close eye .all of this observation and

data are included in this report.

Source of data:

These sources are as follows:

Primary source:

Primary data are collected through two ways. These are:

4 | P a g e

a) Questionnaire: some primary data are collected by taking interview and by discussion with the

executives and officer of JBL.

b) Observation: Here primary data are collected through spending three month in the JBL during

the working hour. Here I observed the total banking process of JBL.

Secondary source:

Secondary data are collected from the following sources:

a) annual reports of JBL

b) Published documents

c) Official files

d) Data available with the website of JBL.

e) Different publication of Bangladesh bank and Bangladesh economic reviews.

f) Outlets of Bangladesh Institute of Bank Management.

1.4 Scope of the study

The report commences with the outline of the organization in focus, presenting the mission and

vision, individual department job responsibilities. For conducting this study an overall

knowledge of the total banking system will necessary because the departments banking are

linked with each other due to some partial proceeding. The scope of the organization part covers

the organization structure, background, objective, function, departmentalization and business

performance of JBL as a whole.

The main part covers the operation scenario of a branch of JBL. This refers how the bank helps

the customer in general banking and foreign exchange banking. It also covers loan and advances

facilities of JBL, credit appraisal system, and activities of credit department.

5 | P a g e

1.5 Limitation of the Study

Three months is not enough to know about commercial banking operation through I have been

received maximum assistance from the every individual of the JBL Shantinagar Branch.

Definitely, I could not produce an outstanding report for the time limitations. Due to the time

limit, the scope and dimension of the study has been curtailed.

The Term paper is likely to have following limitations:

Since the ideal size of data could not be taken, suggested operating process may not be useful

without appropriate modifications.

Due to shortage of time, the accuracy of information may not have been completely perfect.

The Operating Process is a theoretical suggestion. Only a practical application of this may

justify its effectiveness that could not be done due to time limitation.

Lack of comprehension of the respondents was the major problem that created many

confusions regarding verification of conceptual question.

Confidentiality of data was another important barrier that was faced during the conduct of

this study. Every organization has their own secrecy that is not revealed to others. While

collecting data on JBL, personnel did not disclose enough information for the sake of

confidentiality of the organization.

Rush hours and business was another reason that acts as an obstacle while gathering data.

6 | P a g e

7 | P a g e

2.1 Overview of Jamuna Bank

Jamuna Bank Limited is a banking company registered under the companies Act 1994 with its

Head office at Chini Shilpa Bhaban (2nd floor, 3rd floor & 8th floor), 3, Dilkusha, C/A, Dhaka-

1000. The bank started its operation from 3rd June 2001.

Jamuna Bank Limited is a highly capitalized new generation Bank with an Authorized

Capital and Paid-up Capital of Tk.10000 million and Tk.4488 million respectively. The Paid-up

Capital has been raised to 840 million and the total equity of the bank stands at 8325 million as

on December 31, 2012.

JBL undertakes all types of banking transactions to support the development of trade and

commerce of the country. JBL’s services are also available for the entrepreneurs to set up new

ventures and BMRE of industrial units. The Bank gives special emphasis on Export Import,

Trade Finance, SME Finance, Retail Credit and Finance to Woman Entrepreneurs.

To provide clientele services in respect of international Trade it has established wide

correspondent banking relationship with local and foreign banks covering major trade and

financial centers at home and abroad.

Jamuna Bank Ltd., the only Bengali named new generation private commercial was established

by a group of winning local entrepreneurs conceiving an idea of creating a model banking

institution with different outlook to other the valued customers, a comprehensive range of

financial services and innovative products for sustainable mutual growth and prosperity. The

sponsors are reputed personalities in the field of trade, commerce and industries. The Bank is

8 | P a g e

being managed and operated by a group of highly educated and professional team with

diversified experience in finance and banking. The scenario of banking business is changing

environment. Jamuna Bank Ltd. Has already achieved tremendous progress within only two

years. The Bank has already ranked the top out as a quality service provider & is known for its

reputation.

Organizations are open system that needs careful management. Jamuna Bank discreetly pursues

the principles of openness, disclosure and compliance to regulatory authorities, transparency in

performance, integrity in dealings, ethics in banking and accountability to the shareholders in

corporate governance. Jamuna Bank is pledge-bound to keep it free from the clutches of loan

default culture. All our units are the centers of excellence. Our underlying commitment to

professionalism and a single-minded devotion to service to our customers characterizes our style

in all operations. We involve with the changing needs of our customers and the processes go on.

The Bank ensures orderly relations between clearly defined functions of the Board of Directors

and the management. Their role remains sharply bifurcated .The Board formulates policies and

frames procedures. Be management implements them and acts within norms. The management

enjoys full independence in managing the banking industry, especially its credit portfolio without

any undue influence from outside. It, however, functions in a reutilized, efficient, suitable and

dynamic way to foster progress, promote general welfare of the society and infuse its people to

serve the nation. In corporate governance, we strictly comply with the requirement of companies

Act-1994, Bank Companies Act 1991, rules and regulation of Bangladesh Bank and other

regulatory authorities.

9 | P a g e

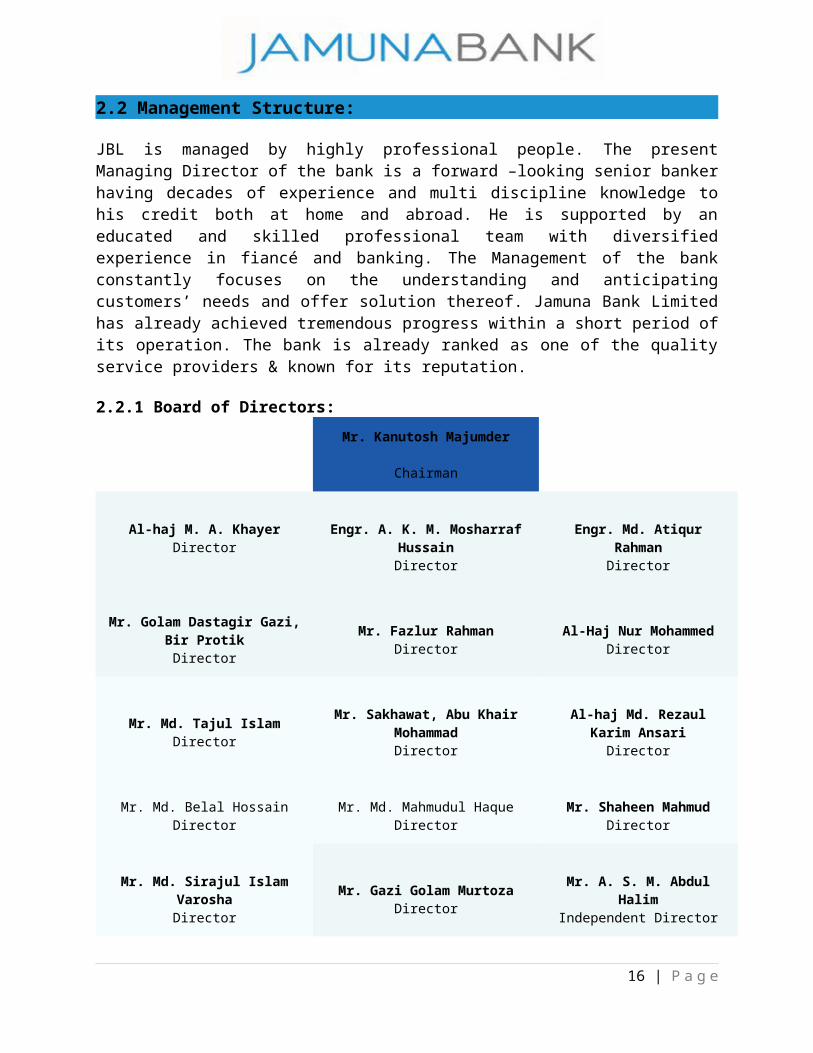

2.2 Management Structure:

JBL is managed by highly professional people. The present Managing Director of the bank is a forward –looking senior banker having decades of experience and multi discipline knowledge to his credit both at home and abroad. He is supported by an educated and skilled professional team with diversified experience in fiancé and banking. The Management of the bank constantly focuses on the understanding and anticipating customers’ needs and offer solution thereof. Jamuna Bank Limited has already achieved tremendous progress within a short period of its operation. The bank is already ranked as one of the quality service providers & known for its reputation.

2.2.1 Board of Directors:

Mr. Kanutosh Majumder

Chairman

Al-haj M. A. KhayerDirector

Engr. A. K. M. Mosharraf Hussain Director

Engr. Md. Atiqur RahmanDirector

Mr. Golam Dastagir Gazi, Bir Protik

Director

Mr. Fazlur RahmanDirector

Al-Haj Nur MohammedDirector

Mr. Md. Tajul IslamDirector

Mr. Sakhawat, Abu Khair Mohammad

Director

Al-haj Md. Rezaul Karim AnsariDirector

Mr. Md. Belal HossainDirector

Mr. Md. Mahmudul HaqueDirector

Mr. Shaheen MahmudDirector

Mr. Md. Sirajul Islam VaroshaDirector

Mr. Gazi Golam MurtozaDirector

Mr. A. S. M. Abdul HalimIndependent Director

Narayan Chandra SahaIndependent Director

Chowdhury Mohammad MohsinIndependent Director

Md. Rafiqul IslamIndependent Director

Shafiqul AlamManaging Director

2.2.2 Audit committee

10 | P a g e

In line with the guidelines of Bangladesh Bank, an Audit Committee of the Board of Directors has been formed to assist the Board with regards to Audit and Internal Control system of the Bank.

Members

Mr. A. S. M. Abdul Halim, Independent Director & Chairman

Mr. Golam Dastagir Gazi, Bir Protik, Director

Al-haj Md. Rezaul Karim Ansari, Director

Mr. Md. Sirajul Islam Varosha, Director

Mr. Md. Rafiqul Islam, Independent Director

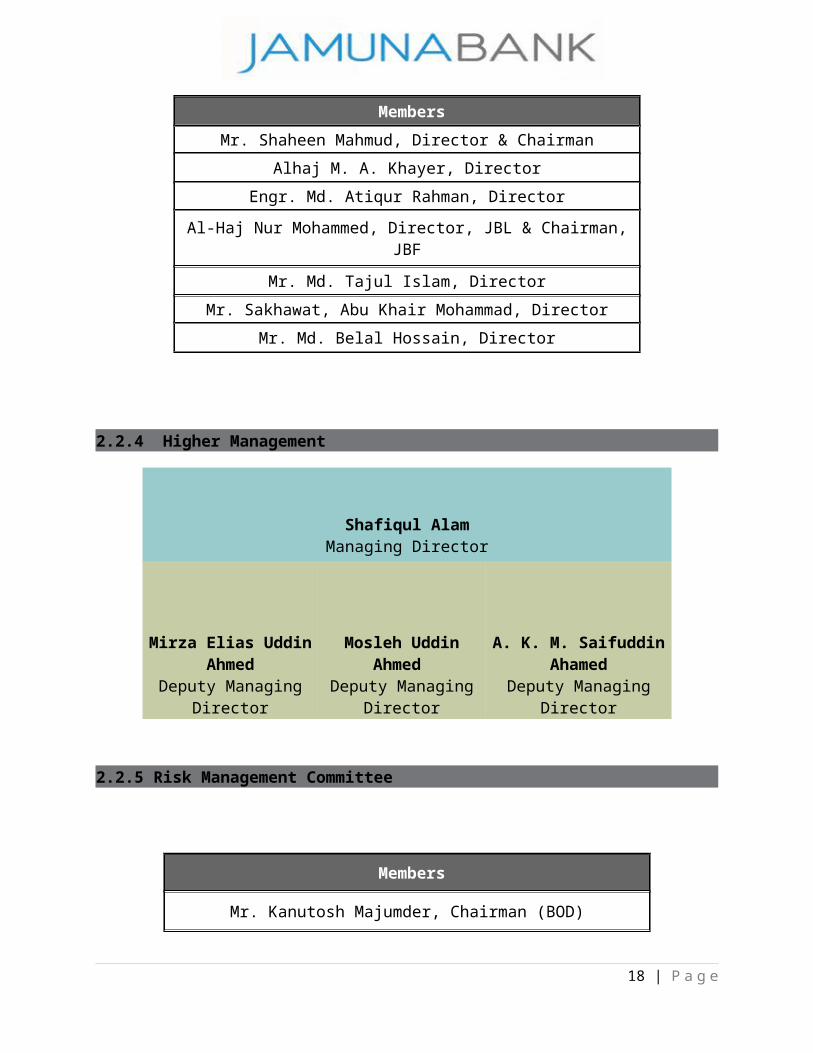

2.2.3 Executive Committee

All routine matters beyond delegated powers of Management are decided upon by or routed through the Executive Committee subject to ratification by the Board of Directors. The Chairman of this Committee is being selected by rotation. Currently, the Executive Committee of Board of Directors is constituted with the following members:

Members

Mr. Shaheen Mahmud, Director & Chairman

Alhaj M. A. Khayer, Director

Engr. Md. Atiqur Rahman, Director

Al-Haj Nur Mohammed, Director, JBL & Chairman, JBF

Mr. Md. Tajul Islam, Director

Mr. Sakhawat, Abu Khair Mohammad, Director

Mr. Md. Belal Hossain, Director

2.2.4 Higher Management

11 | P a g e

Shafiqul AlamManaging Director

Mirza Elias Uddin Ahmed

Deputy Managing Director

Mosleh Uddin Ahmed Deputy Managing

Director

A. K. M. Saifuddin Ahamed

Deputy Managing Director

2.2.5 Risk Management Committee

Members

Mr. Kanutosh Majumder, Chairman (BOD)

Engr. A. K. M. Mosharraf Hussain, Director

Mr. Fazlur Rahman, Director

Mr. Md. Mahmudul Haque, Director

Mr. Gazi Golam Murtoza, Director

12 | P a g e

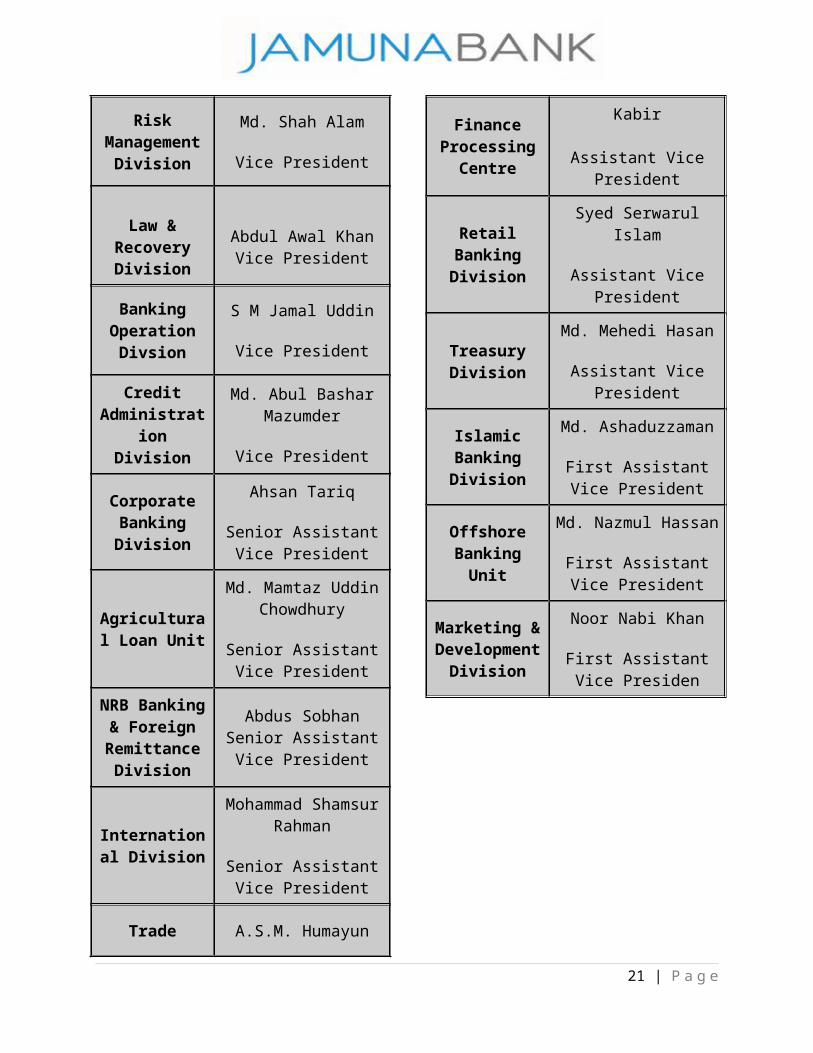

2.2.6 Divisional Heads

Division Name and Designation

Credit Risk Management

Division

Md. Habibur Rahman

Senior Executive Vice President

1. Human Resources Division

2. PR & Brand Communication

Division

Mahbubul Huq Choudhury

Executive Vice President

Anti Money Laundering

Division

Khandaker Khalidur Rahman

Executive Vice President

Information & Communication

Technology Division

Ahmed Nawaz

Senior Vice President

Internal Control & Compliance

Division

Ahamed Sufi

Senior Vice President

Card & ADC Division

Mr. Md. Mohi Uddin

Senior Vice President

Financial Administration

Division

Ashim Kumer Biswas

Senior Vice President

Division Name and Designation

1. Board's Secretariat

2. Share Division

Malik Muntasir Reza Senior Vice President

Monitoring Division

Md. Belal Hossain

Senior Vice President

General & Common Services Division

S.M. Ashafuddoullah

Vice President

Capital Market Operation

M.M. Mostafa Bilal

Vice President

SME DivisionAshif Khan

Vice President

Risk Management

Division

Md. Shah Alam

Vice President

Law & Recovery Division

Abdul Awal KhanVice President

Banking Operation

Divsion

S M Jamal Uddin

Vice President

Credit Administration

Division

Md. Abul Bashar Mazumder

Vice President

13 | P a g e

Corporate Banking Division

Ahsan Tariq

Senior Assistant Vice President

Agricultural Loan Unit

Md. Mamtaz Uddin Chowdhury

Senior Assistant Vice President

NRB Banking & Foreign

Remittance Division

Abdus SobhanSenior Assistant Vice

President

International Division

Mohammad Shamsur Rahman

Senior Assistant Vice President

Trade Finance Processing

Centre

A.S.M. Humayun Kabir

Assistant Vice President

Retail Banking Division

Syed Serwarul Islam

Assistant Vice President

Treasury Division

Md. Mehedi Hasan

Assistant Vice President

Islamic Banking Division

Md. Ashaduzzaman

First Assistant Vice President

Offshore Banking Unit

Md. Nazmul Hassan

First Assistant Vice President

Marketing & Development

Division

Noor Nabi Khan

First Assistant Vice Presiden

14 | P a g e

2.3 Organogram of JBL

15 | P a g e

Chairman

Managing Director (MD)

Deputy Managing Director

Senior Executive Vice President

Executive Vice President

SVPSVP (Credit)SVP (HRD)SVP (Board Secretary)

Vice

SAVP

Senior Executive Vice President Senior Executive Vice President

Executive Vice President

SVPSVP (Credit)

Assistant Vice

First Assistant Vice President

Jr. Assistant Vice

Senior Executive

Executive officer

First executive officer

Officer

First Officer

2.4 Corporate Mission, Vision & Motto

2.4.1 Vision:

To become a leading banking institution and to play a pivotal role in the development of

the country.

To stand out as a pioneer banking institution in Bangladesh.

To contribute significantly to the national economy.

2.4.2 Mission:

The Bank is committed to satisfying diverse needs of its customers through an array of

products at a competitive price by using appropriate technology and providing timely service so

that a sustainable growth, reasonable return and contribution to the development of the country

can be ensured with a motivated and professional work-force.

Jamuna Bank Limited aims to become one of the leading Banks in Bangladesh by prudence, flair

and quality of operations in their banking sector. The bank has some mission to achieve the

organizational goals. Some of them are as follows as:

Fast & accurate customer service and Innovative banking at competitive price.

High quality financial services with the help of latest technology.

Deep commitment to the society and the growth of national economy.

Attract and retain quality human resource, High standard business ethics.

Balanced growth strategy, Steady return on shareholders’ equity

2.4.3 Motto:

The Bank will be a confluence of the following three interests:

Of the Bank : Profit Maximization and Sustained Growth.

Of the Customer : Maximum Benefit and Satisfaction.

Of the Society : Maximization of Welfare

16 | P a g e

2.5 Strategies of Jamuna Bank Ltd

To manage and operate the Bank in the most efficient manner to enhance financial

performance and to control cost of fund.

To strive for customer satisfaction through quality control and delivery of timely

services.

To identify customers' credit and other banking needs and monitor their perception

towards our performance in meeting those requirements.

To review and update policies, procedures and practices to enhance the ability to extend

better service to customers.

To train and develop all employees and provide them adequate resources so that

customers' needs can be reasonably addressed.

To promote organizational effectiveness by openly communicating company plans,

policies, practices and procedures to employees in a timely fashion.

To cultivate a working environment that fosters positive motivation for improved

performance

To diversify portfolio both in the retail and wholesale market

To increase direct contact with customers in order to cultivate a closer relationship

between the bank and its customers.

2.6 Objectives of Jamuna Bank Ltd

To earn and maintain CAMEL Rating 'Strong'

To establish relationship banking and improve service quality through development of

Strategic Marketing Plans.

To remain one of the best banks in Bangladesh in terms of profitability and asset quality.

To introduce fully automated systems through integration of information technology.

To ensure an adequate rate of return on investment.

To keep risk position at an acceptable range (including any off balance sheet risk).

To maintain adequate liquidity to meet maturing obligations and commitments.

To pursue an effective system of management by ensuring compliance to ethical norms,

transparency and accountability at all levels.

17 | P a g e

2.6 Offers of Jamuna Bank Ltd

Term loans especially to develop small scale enterprises and also attach special

importance to technical and advisory support in order to enabling them to run their

enterprises successfully.

Full-fledged commercial banking services including collection of deposit, shortterm trade

finance, working capital finance in processing and manufacturing units and financing and

facilitating international trade.

Technical support to Small Scale Industries (SSIs) in order to enable them to run their

enterprises successfully.

Micro Credit to the urban poor through linkage with NGOs with a view to facilitating

their access to the formal financial market for the mobilization of resources is another

diversification of our services.

In order to perform the above tasks, Jamuna Bank Ltd. works closely with its

Clients, the regulatory authorities, the shareholders (GOB), banks and other financial

institutions.

2.7 Corporate social responsibilities of Jamuna Bank

Jamuna Bank is the 3rd generation junior most bank. From the beginning, the bank is keen to

serve the society and welfare of the people as the corporate social responsibilities. To make

effective contribution by these CSR activities, the governing body of the bank established

Jamuna Bank Foundation in the year of 2007. The bank has appeared as a satisfactory bank to

the central bank. Jamuna Bank every year spends portion of its profit for backward people of the

country.

18 | P a g e

CSR activities of Jamuna Bank foundation are:

Anti-drug Movement

Blood Donation Program

Medical college & Hospital along with free Eye camp and Dental camp

Scholarship giving ceremony

Providing free Treatment

Qirat competition

Relief distribution for Disaster affected people

Discussion on Significance of Ramadan & Lifestyle of Prophets

Blanket & Cloth distribution among cold-hit distressed people

Sewing Training Center

Establishment of Free Primary School

Providing Computer Training by Jamuna Bank Foundation

Tree Plantation & Distribution

Annual School Sports Day & Award-giving Ceremony

Donating in Nimtoli Tragedy

Donating for Development of Sports for the country

Monthly Donating for BDR Tragedy

Donating in Liberation War Museum

19 | P a g e

20 | P a g e

3.1 JBL Personal Banking Services

Personal Banking services of Jamuna Bank offer wide-ranging products and services matching

the requirement of every customer. Transactional accounts, savings schemes or loan facilities

from Jamuna Bank Ltd. make available you a unique mixture of easy and consummate service

quality.

Products of Jamuna Bank Ltd. can be divided into two parts. They are

a) Deposit product

b) Loan products.

a) Deposits products are divided into three parts

1) Transactional Accounts

2) Fixed Deposit Receipts

3) Special Deposit Scheme

1) Transactional Accounts

i) Savings account

Bank considers it as Low cost liability product. The cost of Capital is Only Five percent. Savings

Bank Account may be opened in the name of adult individual who are mentally sound and also

jointly in the names of two or more persons payable to either or both or all of them or to the

survivor or survivors.

ii) Current Deposits

CD Stands for current Deposits. It is cost free. No interest given by the bank on this kind of

account. As it has no cost and more over bank charges on different services, the target of the

bank is to increase the number of current account clients. It can be opened by the name of any

organization and not in personal name. Current account is most suitable for private, traders,

merchants, exporters and importer. One can enjoy maximum flexibility and convenience he or

she opens a current account with JBL.

21 | P a g e

iii) Short Term Deposits.

This is also another low cost product. Anyone can open deposit like this one. Generally these

accounts are opened by Government, Companies or Administration persons. To get the interest

deposit need to keep for a minimum of seven days. Deposits under this category is withdraw

able at a minimum of 7 (seven) days notice.

iv) Special Savings Accounts:

JBL offer Special Savings Accounts to attract different type of segments in the competitive

markets. These are Grihini savings account, student savings account and senior Citizen Saving

Account, Which provide better interest rates and specialized services for particular groups.

v) Resident Foreign Currency Deposit (RFCD) Accounts

Persons ordinarily resident in Bangladesh may open and maintain RFCD accounts with foreign

exchange brought in at the time of their return from travel abroad. Any amount brought in with

declaration to Customs Authorities in form FMJ and up to US$5000 brought in without any

declaration. Balance in these accounts shall be freely transferable abroad. Fund from these

accounts may also be issued to account-holders for the purpose of their foreign travels in the

usual manner.

2) Fixed Deposit Receipts

Generally JBL offers Fixed Deposit for 3 months, 6 months and 12 months tenors at attractive

interest rates.

FDR for One month 8.00 %

FDR for Three month 10.00 – 10.75 %

FDR for Six month 10.00 – 10.75 %

FDR for Twelve months 10.00 – 10.50 %

22 | P a g e

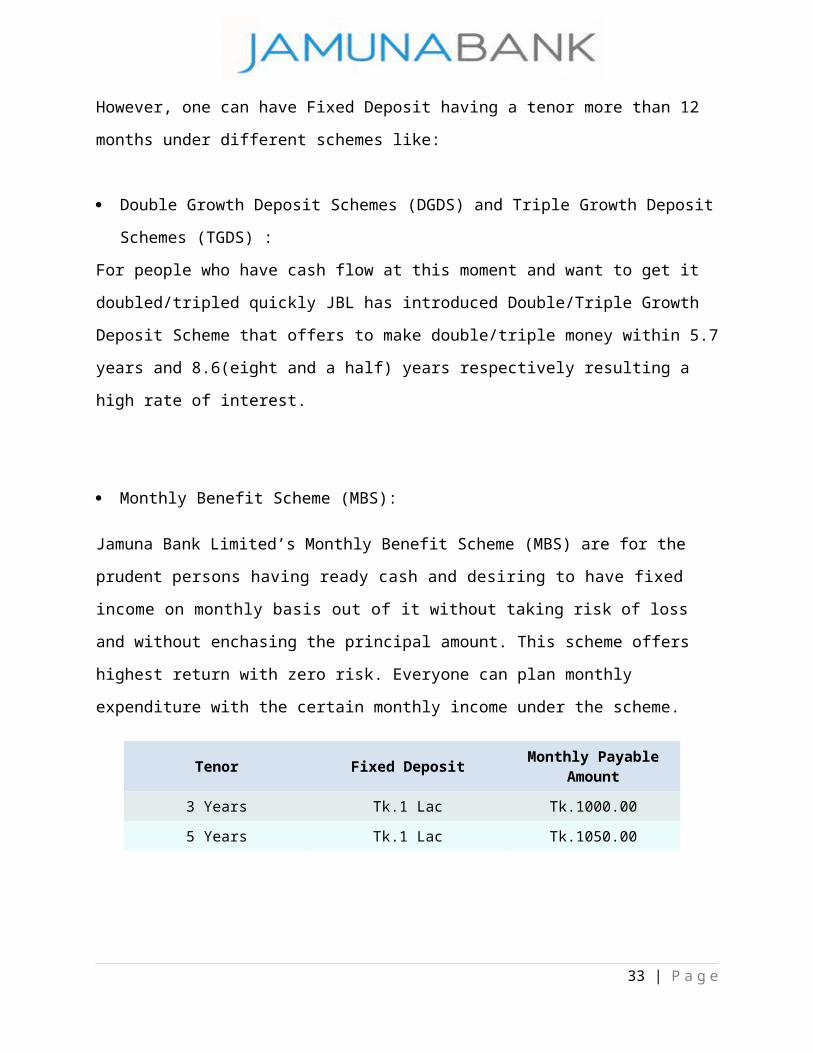

However, one can have Fixed Deposit having a tenor more than 12 months under different

schemes like:

Double Growth Deposit Schemes (DGDS) and Triple Growth Deposit Schemes (TGDS) :

For people who have cash flow at this moment and want to get it doubled/tripled quickly JBL

has introduced Double/Triple Growth Deposit Scheme that offers to make double/triple money

within 5.7 years and 8.6(eight and a half) years respectively resulting a high rate of interest.

Monthly Benefit Scheme (MBS):

Jamuna Bank Limited’s Monthly Benefit Scheme (MBS) are for the prudent persons having

ready cash and desiring to have fixed income on monthly basis out of it without taking risk of

loss and without enchasing the principal amount. This scheme offers highest return with zero

risk. Everyone can plan monthly expenditure with the certain monthly income under the scheme.

Tenor Fixed Deposit Monthly Payable Amount

3 Years Tk.1 Lac Tk.1000.00

5 Years Tk.1 Lac Tk.1050.00

Pension Deposit Scheme: JBL Pension Deposit Scheme is designed for better future after retirement

Education Savings Scheme: Education is a basic need of every citizen. Every parent wants to

impart proper education to their children. Education is the pre-requisite for socio-economic

development of the country. As yet, there is no arrangement of free education to the citizens

from the government level. As such, there should be pre-arrangement of fund to ensure

higher education’s the children. Otherwise higher education may be hindered due to change

of economic condition, income of the parents at the future time when higher education shall

be required. Today's higher education is becoming expired day by day. Parents can get relief

and can have peace of mind if they can arrange the necessary fund for higher education of

their children. As such, JBI, has introduced 'Education Savings Scheme' which offers you an

23 | P a g e

opportunity to build up your cherished fund' by monthly deposit of small amount it at your

affordable capacity or initial lump sum deposit to yield handsome amount on a future date to

meet the educational expenses. Under this Scheme you have the different attractive options to

avail the future benefit i.e. withdrawal of the total amount accumulated in lump sum or

withdrawing monthly benefit to meet educational expense keeping die principal amount

intact or to withdraw both principal and accumulated profit monthly for a certain period.

3) Special Deposit Scheme

Monthly Savings Scheme (MSS): It’s good to save for rainy days and for prosperous

future. Savings can meet up any emergences. JBL has introduced Monthly Savings

Scheme (MSS) that allows saving on a monthly basis and getting a handsome return upon

maturity. If anyone wants to build up a significant savings to carry out you’re cherished

Dream, JBL MSS is the right solution.

Lakhpati Deposit Scheme: To become a lakhpati is a dream to most of the people of

Bangladesh especially to the lower and lower middle class income group. They

experience their expectations and wants are enormous in nature in our small span of life.

To meet our deposit and wants we need right plan. Keeping the above in mind JBL has

introduced "Lakhopati Scheme" which has flexibility report of maturity and monthly

installment as per affordable capacity.

Millionaire Deposit Scheme: JBL offer a deposit scheme which makes a customer

millionaire after certain time. It’s a dream for small savers to be a millionaire. This

dream can come to reality if saver has a calculated savings plan.

Kotipoti Deposit Scheme: To become ‘Kotipati' is simply a dream for the most of the

populace of Bangladesh. It is realizable for high income group who have strong

determination and savings habit. If you decide and plan to save money from your regular

income, you can own Tk1.00 crore easily by making a planned savings. In this regard,

JBL has introduced “Kotipati” Deposit Scheme” offering the savings plan fit to your

income and to execute your dream to be a Kotipati by monthly deposit at your affordable

24 | P a g e

capacity. You can take advantage of the “Kotipati Deposit Scheme” from JBL and plan

for your golden future accordingly.

Marriage Deposit Scheme: Marriage of children, especially daughter is a matter of great

concern to the parents. Marriage of children involves expense of considerable amount.

Prudent parents make effort for gradual building of fund as per their capacity to

meet the matrimonial expense of their children specially daughters. Parents get

relief and can have peace of mind if they can arrange the necessary fund for

marriage of their children, no matter whether they survive or not till the marriage

occasion. It can be a great help to the parents if there is any scope of deposit of a

modest mount as per their financial capacity, which groves very fast at high rate of

interest yielding a sizeable amount on maturity. With this end in view JBL has

introduced Marriage Deposit Scheme, which offers you an opportunity to build - up

your cherished - fund by monthly deposit of serial, amount at your affordable capacity.

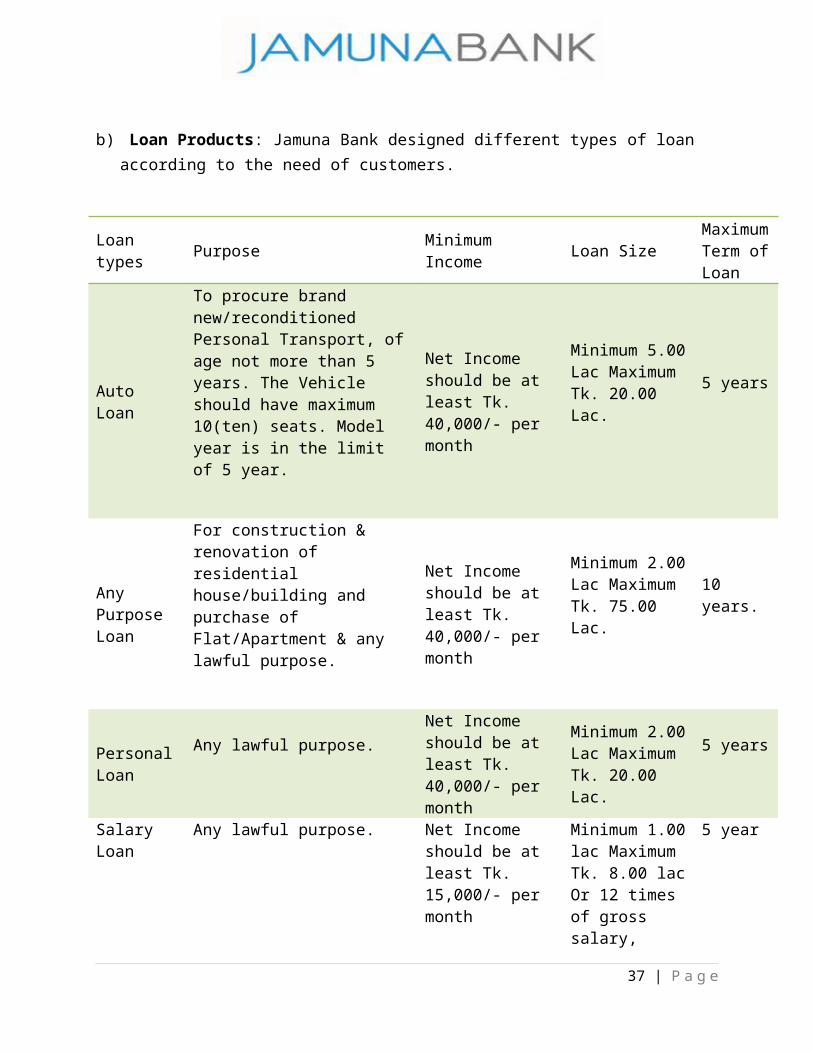

b) Loan Products: Jamuna Bank designed different types of loan according to the need of customers.

Loan types Purpose Minimum Income Loan SizeMaximum Term of Loan

Auto Loan

To procure brand new/reconditioned Personal Transport, of age not more than 5 years. The Vehicle should have maximum 10(ten) seats. Model year is in the limit of 5 year.

Net Income should be at least Tk. 40,000/- per month

Minimum 5.00 Lac Maximum Tk. 20.00 Lac.

5 years

Any Purpose Loan

For construction & renovation of residential house/building and purchase of Flat/Apartment & any lawful purpose.

Net Income should be at least Tk. 40,000/- per month

Minimum 2.00 Lac Maximum Tk. 75.00 Lac.

10 years.

Personal Loan

Any lawful purpose. Net Income should be at least Tk. 40,000/- per month

Minimum 2.00 Lac Maximum Tk. 20.00 Lac.

5 years

25 | P a g e

Salary LoanAny lawful purpose.

Net Income should be at least Tk. 15,000/- per month

Minimum 1.00 lac Maximum Tk. 8.00 lac Or 12 times of gross salary, whichever is lower

5 year

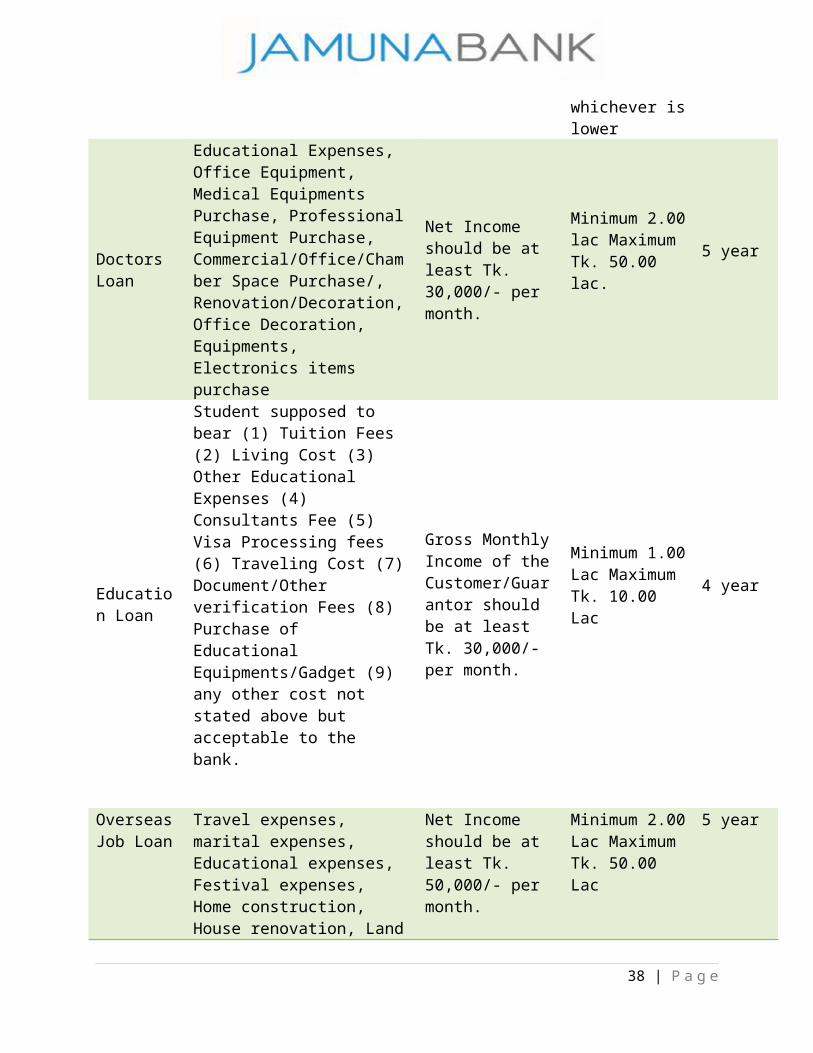

Doctors Loan

Educational Expenses, Office Equipment, Medical Equipments Purchase, Professional Equipment Purchase, Commercial/Office/Chamber Space Purchase/, Renovation/Decoration, Office Decoration, Equipments, Electronics items purchase

Net Income should be at least Tk. 30,000/- per month.

Minimum 2.00 lac Maximum Tk. 50.00 lac.

5 year

Education Loan

Student supposed to bear (1) Tuition Fees (2) Living Cost (3) Other Educational Expenses (4) Consultants Fee (5) Visa Processing fees (6) Traveling Cost (7) Document/Other verification Fees (8) Purchase of Educational Equipments/Gadget (9) any other cost not stated above but acceptable to the bank.

Gross Monthly Income of the Customer/Guarantor should be at least Tk. 30,000/- per month.

Minimum 1.00 Lac Maximum Tk. 10.00 Lac

4 year

Overseas Job Loan

Travel expenses, marital expenses, Educational expenses, Festival expenses, Home construction, House renovation, Land purchase, Transport purchase, Office equipment, Professional equipment purchase, office space purchase, shop space purchase, Office decoration, Household durables/equipments/electronics purchase.

Net Income should be at least Tk. 50,000/- per month.

Minimum 2.00 Lac Maximum Tk. 50.00 Lac

5 year

26 | P a g e

3.1.1 Other services of Personal Banking Division

Personal Banking Division (PBD) issues both VISA Debit Cards and VISA Credit Cards.

VISA is the renowned Card brand in the earth. Jamuna Bank Limited is a principal member of

VISA Worldwide. Remittance Cell is another successful wing of the Personal Banking Division.

Product range includes:

VISA Debit Cards - You can now avail the convenience of VISA Debit Card. It is the easiest and

the most secured way of utilizing your money for 24/7 retail purchases as well as cash

withdrawal.

VISA Credit Cards - The JBL Credit Card gives you a fast, convenient and reliable way to pay,

24 hours a day, wherever you are in the world. VISA Classic, VISA Gold.

International Credit Cards – JBL International Credit Cards (VISA) allows you flexibility and

convenience when you travel internationally. The VISA International card entitles you to

exclusive discounts worldwide. VISA Dual (Gold)

JBL Remittance Cell – “Remit Fast” is the motto of JBL Remittance Cell. It provides the best &

faster services to its customers and connects the world through the renowned money exchange

agencies. Such as Placid Nk Corporation, Moneygram Payment System Inc., Raffles Exchange

Ltd.UK, Euro Bangla Money Transfer (UK) Ltd., Moneylink,UK, Homelink Remit (UK) Ltd.,

Rumana Money Services. Customers can avail improved pricing on remittance.

3.2 JBL Corporate Banking Services

Corporate Banking of Jamuna Bank Limited offers customized corporate banking solution for

both its local Business Houses as well as Multinational Companies. The axiom of JBL’s

Corporate Banking services is to nurture Relationship Banking by maintaining strong

relationship with premier corporate business houses of the country providing their requirement

based financial and other banking services. JBL’s Corporate Banking Division is well equipped

with skilled and experienced personnel who have vast exposure in this area and who being

Relationship Managers maintain one to one relationship with all corporate business houses

having relationship with the Bank. Relationship Managers are relentless in meeting the exact

need and any emergency requirement of the corporate customers.

27 | P a g e

JBL’s Corporate Banking exposure is concentrated in diversified areas of business that include:

Spinning

Textile

Garments

Garments Accessories

Iron & Steel

Cement

Building Materials

Furniture & Furniture materials

Edible Oil

Food & Beverage items

Various Trading

Ship Building

Ship Breaking

Infrastructure Building &

Construction

Electronics & Electrical Equipments

Agro & Agro Products

Transport

Real Estate

Telecommunication

28 | P a g e

3.3 Islami Banking Activities

Besides conventional banking, Jamuna Bank Limited is carrying Islami Banking activities based

on Islami Shaiah principles. The first Islami Banking branch of the Bank opened on October 25,

2003 at Nayabazar in Dhaka. Afterwards it’s second branch opened on November 27, 2004 at

Jubilee Road in Chittagong. Jamuna Bank Limited is committed to conduct business of it’s

Islami Banking branches strictly complying Shariah requirements. To achieve this goal a Shariah

Supervisory Committee has been constituted with renowned Islami scholars of the country and

senior banker having Islami Banking experiences in depth knowledge of conventional and Islami

Banking. All activities of Islami Banking branches are carried out under the guidance of this

Committee. A separate division has also been created at Head Office.

3.4 NRB Banking

Jamuna Bank Ltd is one of the fast growing private commercial bank in the country having wide

Branch & Associate network throughout the Country. All the branches are running with real-time

Online and ATM facilities to settle their transaction from remote areas. JBL have dedicated NRB

Banking Dept. to ensure personalized services to the valued customers at branch & Head Office

Level. JBL have an admirable Remittance Tie-up with a good number of world renowned

Exchange Houses and Banks throughout the World to facilitate the Remittance services to the

Beneficiaries. Besides JBL have 87+ Branch network and 1,800 ATM outlets (own & shared)

throughout the Country. JBL have also a strong Remittance Settlement/distribution Network with

different Associate Banks & BEFTN (Bangladesh Electronic Fund Transfer Network) covering

more than 8000 remote locations throughout the Country. To ensure JBL’s reach to the doorstep

of JBL’s valued customers / Beneficiaries JBL have arranged M-Remittance facilities with

Grameenphone, Banglalink, ROBI.

Main purpose is to cater to the needs of NRBs & their beneficiaries offering deposit and loan &

investment products and services. Prioritizing the needs of NRBs, JBL are in process to offer

different personalized products & services by establishing JBL own Exchange Houses in

29 | P a g e

different Countries like UK, USA, Malaysia, Singapore, Italy, Spain, Australia, Japan, etc. To

serve the NRBs in the best possible manner, Jamuna Bank Limited has deployed NRB

community consultants in Exchange Houses around the globe. They encourage potential

customers to use legal channels to remit their money to the loved ones as well as to invest their

savings in the productive sectors.

JBL have wide range of Correspondent Banking Network & Remittance drawing arrangement

with different International reputed Money Transfer Companies & Exchange Houses throughout

the world to facilitate Bangladesh bound Remittance Globally. JBL value JBL’s customers to

provide prompt & efficient services offering best competitive price for their hard-earning

Foreign Currencies.

3.5 SME Banking

SME means Small and Medium Enterprises. Small & Medium Enterprise (SME) plays a pivotal

role in the economic growth and development of a country. Actually, SME works as the platform

for job creation, income generation, and development of forward and backward industrial

linkages and fulfillment of local social needs. SMEs occupy a unique position in the economy of

Bangladesh. To keep these facts in mind JBL lunched several products for customers. These are:

1. Jamuna Bonik

SME clients are being involved in foreign trade, their network has been expanded throughout the

world. To facilitate the foreign trade transactions of the SME clients, Jamuna Bank is offering a

product named ‘Jamuna Bonik’.

2. Jamuna Chalantika

To operate business with extra ease, term loan is not always the only solution. Keeping this

capital requirement for your business, Jamuna Bank is offering a package of working capital

solution [50% term loan & 50% revolving credit (cash credit) facility] to run the business

smoothly.

30 | P a g e

3. Jamuna Green

To save our beloved earth from the disaster of Green House Effect, Jamuna Bank is offering

ECO friendly product ‘Jamuna Green’. Under this product, one can get finance for ETP plants in

different sectors, Eco friendly vehicles, Eco friendly fields (reduce CO2 emission), Bio

Fertilizer, Bio gas plants, Solar plants and Eco friendly any other business. Mode of finance shall

be Term Loan mainly.

4. Jamuna Jantrik

When any SME client wants to puchase any machine or vehicle for business, Jamuna Bank is

there with the offer of ‘Jamuna Jantrik’ thorugh which the client can get a lease finance facility.

5. Jamuna Nari Uddogh

About fifty percent of our total population is women and many of them have succeeded as a

business entrepreneur. To give incomparable ladies some extra ease and to help them to get

financial freedom, Jamuna Bank Ltd. is offering a product ‘Jamuna Nari Uddogh’.

6. Jamuna NGO Shohojogi

From the very beginning, one of the goals of Jamuna Bank Ltd. is to provide services to the

under privileged people of remote areas. Keeping that idea in mind, the Jamuna Bank Ltd. has

come forward with a product for SME customers named ‘Jamuna NGO Shohojogi’. ‘Jamuna

NGO Shohojogi’ ensures wholesale financing through the reputed NGOs in the country whose

past records are remarkable, repayment behaviors are satisfactory, growth rates are significant

and above all loan monitoring & recoveries are above 95%.

31 | P a g e

7. Jamuna Shachchondo

Who does not want a easy life? For the financial ease in business, Jamuna Bank is offering

‘Jamuna Shachchondo’ product through which one can enjoy both overdraft and term loan

facilities.

8. Jamuna Swabolombi

As an entrepreneur, definitely one needs working capital to run your business smoothly. To get

this working capital without Collateral Jamuna Bank Ltd. has ‘Jamuna Swabolombi’ – Collateral

free Term Loan in its basket. Just come with proper documents & get it.

3.6 International Banking

3.6.1 Corresponding Banking:

Jamuna bank is maintaining correspondent banking relationship with 234 international Bank

around 100 Countries in 818 different strategic locations worldwide to ensure the best &

steadfast trade services. Presently we have 23 Nostro Accounts in different Major Currencies like

USD, GBP, EURO, JPY, CHF, SAR, CAD & ACU Dollar with Various World reputed Bank.

As they have wider Correspondent Network with sustainable Credit limit & good relationship

globally, we can provide the following Services smoothly:

L/C Advising

L/C Confirmation

Bank Guarantee

Hajj Guarantee

Purchasing/Discounting/Negotiating of export bills

Off Shore Banking Services

Trade payment settlement

Cash Letter Services

Foreign Remittance

32 | P a g e

3.6.2 SWIFT services:

Jamuna Bank Limited is the member of SWIFT (Society for Worldwide Inter-bank Financial

Telecommunication). SWIFT is a member owned co-operative, which provides a fast and

accurate communication network for financial transactions such as Letters of Credit, Fund

transfer etc. By becoming a member of SWIFT, the bank has opened up possibilities for

uninterrupted connectivity with over 5,700 user institutions in 150 countries around the world.

3.6.3 Trade Finance:

International Trade forms the major business activity undertaken by Jamuna Bank Ltd. The Bank

with its worldwide correspondent network and close relationships with key financial institutions

provides an extensive trade services network to handle your transactions efficiently. Our key

branches throughout the country and Offshore Banking Unit (OBU) are staffed by personnel

experienced in International Trade Finance. These offices are the focal point for processing

import and Export transactions for both small and large corporate customers. We offer a

complete range of Trade Finance services. Our professionals will work with you to develop

solutions tailored to meet your requirements, through mobilizing our full range of trade services

locally, and drawing on our global resources. We can offer you professional advice on all aspects

of International Trade requirements, namely:

Issuing, advising and confirming of Documentary Credits.

Pre-shipment and post-shipment finance.

Negotiation and purchase of Export Bills.

Discounting of Bills of Exchange.

Collection of Bills.

Foreign Currency Dealing etc.

3.6.4 Offshore Banking:

An Offshore banking Unit (OBU) of a Bank is a deemed foreign branch of the parent bank

located within Bangladesh, and shall undertake International Banking business involving foreign

currency denominated assets & liabilities. An offshore bank is simply a bank based in a

33 | P a g e

jurisdiction outside of your country of residence. Accordingly, Jamuna Bank Limited has started

its OBU operation on 22nd April 2010 having following objectives:

To widen and diversify JBL’s area of services to the foreign investors as they do not have

the opportunity of availing credit facilities from different Financial Instittution in

Bangladedsh.

To diversify the sources of foreign exchange earnings by increasing export of Bangladesh

throgh the EPZs.

To encourage and foster establishment and development of industries and commercial

enterprises in EPZs in order to wider and strengthen the economic base of Bangladesh.

Jamuna Bank Limited offers the following range of Offshore Banking Services:

Foreign Currency Deposites( Non Resident entitles and NRBs)

Loan in Foreign Currencies

Credit Facilities including Trade Financing

Negotiation/Purchase of Export Bills

Discounting of Export Bills

Corporate Treasury Services.

Competitive interest rates

Easy international transfers

Fee free accounts

3.7 Online Banking

Jamuna Bank Limited has introduced real-time any branch banking on April 05, 2005. Now,

customers can withdraw and deposit money from any of its Branches. Their valued

customers can also enjoy 24 hours banking service through ATM card from any of Q-

cash ATMs located at Dhaka, Chittagong, Khulna, Sylhet and Bogra. All the existing

customers of Jamuna Bank Limited will enjoy this service by default.

34 | P a g e

3.8 Q-Cash Round The Clock Banking

Jamuna Bank Q-Cash ATIM Card enables the costumers to withdraw- cash variety of banking

transactions 24 hours a day. Q-Cash ATMs are conveniently located covering major

shopping centers, business and residential areas in Dhaka and chittagong. ATMs in Sylhet,

Khulna and other cities will soon start be introduced. The network will expand to cover the

whole country within a short span of time.

35 | P a g e

36 | P a g e

4.1 Introduction

All business concerns to earn a profit through selling either a product or service. A bank does not

produce any tangible product to sell but does offer a variety of financial services to its customers.

General banking is the starting point of all the banking operations. It is the development, which

provides day to day services to the customers. Every day it receives deposits from the customers

and meets their demand for cash by honoring cheques. It opens new accounts, remit funds, issue

bank drafts and pay orders etc. Since bank is confined to provide the service every day, general

banking is also known as “Retail Banking”. The JBL offers various types of general banking

components. They are very essential tools for the bank to serve the customers. To attract new

customers the bank has to launch new components or re-furnished their existing products.

4.2 Functions of General Banking

4.2.1 Account Opening Section

A Person is treated as a customer when he or she opens an account on that bank. Then it becomes a contractual banker customer relationship. The account opening section of any commercial bank is a very important section because; the more customers open bank account the more customers’ base creates. This section takes care of all the relevant duties related to the opening of an account. There are different types of account facilities provided by a commercial bank. For example, saving Account, Current Account, Fixed Deposit Receipt, Short Term Deposit Account, Cash Credit Account.

4.2.1.1 Procedure of Opening of an Account:

Banker’s his to maintain some common principles and procedures for open all most all deposit

accounts. Major information is essential for identification of the account holders individually so

that banker can discharge his obligations to everyone correctly and to the extent due. It is said

that, there is no banker customer relationship if there is no A/C of person in that bank. By

opening a banker and customer create a contractual relationship. However, selection of customer

for opening an account is very crucial of a bank.

37 | P a g e

The following instruction to be followed while opening account: -

Introduction of Account to be obtained from a respectable client acceptable to bank.

The introduction shall be obtained in writing in the respective column of Account opening

form.

For opening savings bank account of individual either singly or jointly, passports and identity

cards may be accepted for introduction, but subsequently proper introduction may be

obtained.

Introduction of Current Account by members of the staff may be allowed but shall be

discouraged as far as possible.

38 | P a g e

Applicant fills up the relevant application

form in the prescribed manner

She/he is required to fill up the specimen

signature card

For individual introduction is

needed by an account holder.

The authorized officer scrutinizes the introduction

and examines the documents submitted

Issuance of deposit slip and the deposit

must be made in cash

After depositing the cash one cheque

book & pay-in-slip book is issued

Account is opened

Current Account shall preferably be introduced by another Current Account holder

acceptable to bank.

Introduction of Account holder of other branch may be accepted with caution. In that case the

introducer’s signature must be verified by authorized officer of that branch and authenticated

by a forwarding letter.

Photographs of account holder must be attested by the introducer.

Letter of thanks be issued to introducer in Bank’s standard specimen.

4.2.1.2 Current Deposit Account

A Current Deposit Account may be opened by individual, firm, company and club,

association, body corporate etc.

Funds in the Current Deposit Account is payable on demand.

No interest is payable on balances of Current Deposit Accounts.

Current Deposit Account may be opened with a minimum initial balance of Tk.5,000/-

Minimum balance to be maintained in the account is Tk.1,000/-

Customer willing to open Current Deposit Account shall fill up the Account Opening

Form (AOF) applicable to him/ her and Specimen Signature Card (SS Card). The customer will

sign in the space provided under “Yours faithfully” and on the specimen signature cards.

In case of proprietorship and partnership firms the relevant account opening form is to be

filled in and signed by the proprietor/ partner in their individual capacity in the space provided

under “Yours faithfully” and on the specimen signature card in their official capacity.

In all other cases including companies etc. the persons opening the account shall fill in

the relevant Account Opening Form and sign the Form in the space provided under “Yours

faithfully” and in the specimen Signature Card in their official capacity.

Introduction of acceptable clients to be obtained as per guidelines.

The Manager’s approval for opening account shall be obtained by the concerned staff

member.

Signatures of the account holder shall be admitted by affixing the stamp “Signature

admitted” and signing by the authorized officer. The introducer’s signature shall be verified by

affixing the stamp “Signature verified” near the signature by authorized officer.

39 | P a g e

Blank space of the Specimen Signature Card should be closed by drawing parallel lines.

The particulars of the Account Opening Form shall be entered in the Account Opened

and Closed Register as per sequence provided by the computer system.

The customer shall be provided with Deposit Slip in corporating the Account Number

and be advised to make the initial deposit in the account. The amount of initial deposit shall be

entered in the Account Opening Form.

Cheque Book shall be issued on request on completion of all formalities including initial

deposit. Cheque series to be entered in the Account Opening Form at the bottom right and

authenticated by authorized officer.

After posting of all particulars of the account including cheque series, one authorized

officer shall check/ verify the same in the computer screen and record it in the form with

signature.

Manager/ Authorized Officer shall apply sufficient intelligence and common sense to

ascertain genuineness of the account holder. No account shall be opened without approval of

the Manager.

Clear instruction regarding operation of the account shall be noted on the Account

Opening Form and Specimen Signature Card especially in respect of death of inability of the

account holders, or the person operating the account. The account holder shall confirm the

instructions under specimen signature.

An indemnity shall be obtained from the customer if he/ she signs in language other than

English/ Bengali.

Illiterate persons shall be discouraged to open Current Account. If opened withdrawal

shall be allowed on personal appearance of the account holder.

The account opening form shall be sent to the respective computer terminal for posting

and S.S. Card shall be retained serially in the S.S. Card Box under custody of Cheque Passing

Officer.

One of the photographs of the Account Holder is to be pasted with AOF and another one

with S.S. Card. AOF to be retained in serial order in Pasting File.

A letter of thanks to be sent to the account holder as well as to the introducer.

All new accounts opened during the day shall be personally checked by the Manager at

the close of business of each day.

40 | P a g e

Checking officer shall particularly see the introduction, initial deposit in cash or cheque,

nature of business of the account holder, Trade License, Partnership Deed/ Memorandum of

Articles of Association, Resolution etc.

Similar Accounts should be noted in the AOF and care should be taken while making

posting of transactions in such accounts.

The Computer Program used by bank shall provide reference of clients. Branch Manager

must ensure that their computer system provides reference of client.

Classified Deposit Ownership Program to be maintained in the Computer System for

facilitating periodical returns to Bangladesh Bank.

Bank shall provide monthly statement of account to clients as per computer system of the

branch.

If minimum balance of the account falls below Tk.1,000/- once during the half-year,

incidental charge will be recovered as per Head Office Circular.

Bank at its discretion may close any account with prior notice to the account holder.

In case of closure of account by the account holder, branch shall recover closing charges

as per schedule of charges.

4.2.1.3 Bank Deposit Account

Savings Bank Account may be opened in the name of adult individual who are mentally

sound and also jointly in the names of two or more persons payable to either or both or all of

them or to the survivor or survivors.

Savings Bank Account may be opened in the name of a minor also.

Saving Bank Account may be opened in the names of clubs, societies, association and

similar institutions and even by government and semi-government offices.

Account shall be opened with at-least a minimum initial deposit of Tk.2,000/-.

Interest at the rates fixed by Head Office from time to time is applied half-yearly on the

balances held on daily product basis.

41 | P a g e

Not more than one account is allowed to be opened in the same name. But this will not be

applicable to parents willing to open more than one account in his/ her name in respect of each

minor child.

Savings Bank Account shall not be allowed to be overdrawn under any circumstances.

Account opening formalities like Current Account should be followed.

Savings Bank Account should not be allowed to be operated like Current Account

Not more than 25% of the balance can be withdrawn without 7 days notice. Withdrawals

in the account shall be allowed twice in a week.

No interest shall be paid to such accounts in the month for violation of the above rules.

Bank shall provide monthly-computerized statement of accounts to account holders

instead of passbook.

Bank may at its discretion close any account with prior notice for repeated return of

cheques due to insufficient balance.

Bank may recover charges up to a maximum of Tk.100/- per instances of cheque return.

4.2.1.4 Short Term Deposit Account (STD)

Deposits held in this account are payable on short notice. Normally corporate bodies, bank and financial organizations invest their funds temporarily. Now-a-days, private individuals having sound financial means also open this type of deposit accounts. The following rules shall apply:

Deposits held in STD Account are payable in 7 (Seven) days notice.

Cheque books may be issued to account holders for withdrawal of funds.

Repeated withdrawal without notice shall be discouraged.

Interest is payable on balance held on daily product basis as per computer program used by

bank.

For opening STD Account, AOF used for Current Deposit Account shall be used.

Other formalities are similar to Current Deposit Accounts.

Minimum balance requirement for accruing interest is Tk.100,000 (Taka one lac) only.

42 | P a g e

4.2.1.5 Fixed Deposit Account

Fixed Deposit is neither transferable nor negotiable.

Fixed Deposit Account may be opened by individuals, firms, companies, corporate body etc.

Fixed Deposit Account shall be opened for a fixed period ranging from 3 months to 36 months

or above as determined by Head Office from time to time.

Rate of interest payable to Fixed Deposit Accounts shall be approved/ advised by Head Office

from time to time.

Interest on deposits shall normally be payable on maturity along with principal.

Customers may however, have the option of withdrawing interest accrued after every six

months provided that the account is for more than 24 months period.

Interest ceases to accrue on overdue Fixed Deposit Account. Branch may, however, allow

interest to exceptionally valued clients on deserving cases with concurrence of Head Office.

FDR may be encased before maturity on written request of the depositor. For payment of

interest, branch shall follow Head Office instruction in this regard from time to time.

In case of FDR in joint names, written consent of all holders shall be obtained before

premature encashment, irrespective of instruction provided for operation of the account.

Duplicate FDR may be issued in case of loss of FDR reported by the holder. An indemnity

bond executed by the depositor(s) shall be obtained on Bank’s standard form. A remark

“DUPLICATE ISSUED IN LIEU OF ORIGINAL REPORTED LOST” is to be typed on top

of the duplicate FDR. The original number should be used and comments to this effect be

recorded in AOF, S.S. Card and FD Issue Register.

Extra care shall be taken in case duplicate FDR is proposed for lien to any bank.

Each FDR of the same depositor will be treated as separate contract.

Account Opening Form for Fixed Deposit Account contains relevant columns for mentioning

all terms including rate and term of deposit and operational instruction. The bottom part of the

form shall be used as credit voucher for the deposit. Specimen Signature Card duly signed by

the depositor to be obtained with clear instruction for operation of the account.

Nominee form may be obtained if the depositor desires to nominate any body to receive the

proceeds of his account in case of his death. Nominee’s Signature and one copy of photograph

duly attested by the depositor to be obtained.

43 | P a g e

The signature of the depositor is to be admitted by authorized officer both in AOF and S.S.

Card.

Particulars of the account shall be entered in the FD Account Opening Register and a control

number be allotted in computer sequence order with oblique against the printed number of

FDR. The complete number shall be quoted/ mentioned in all references.

On completion of all formalities, including deposit of fund, FDR shall be issued and signed by

two authorized officers. The FDR shall be delivered to depositor against acknowledgement on

the reverse of the counter foil.

The AOF will be retained in file and the S.S. Card shall be kept in S.S. Card Box under

custody of the concerned authorized officer.

The particulars of the account shall be posted in the computer system on completion of all

formalities including receipt of deposit. One authorized officer shall check/ verify the

particulars in the computer screen and record his comments on the AOF to this effect with

signature.

Renewal of Fixed Deposit Account shall be allowed on written request of the depositor, if no

intimation is received, the account shall be deemed to have renewed under the existing terms

and conditions automatically.

FDR can be accepted as security against credit facility.

Offer of special interest rate on deposits is subject to Head Office approval.

4.2.1.6 Documentation

The following documents duly completed shall be obtained from the customer at the time of

opening different types of accounts as applicable:

1. Individual/ joint.

Account opening form as applicable duly filled in.

Specimen Signature Card.

Two photographs duly attested by introducer.

Nominee Form (if nomination given by the account holder).

Mandate or Authority Form (if a third person is authorized to operate the account).

44 | P a g e

2. Proprietorship Firm

Account Opening Form.

Specimen Signature Card.

Copy of Trade License

Two photographs duly attested by introducer.

Proprietorship Rubber Stamp against all signatures of the proprietor.

3. Partnership Concern

Account Opening Form.

Specimen Signature Card.

Copy of Trade License

Partnerships Deed

Two photographs of each partner duly attested by introducer.

Partnership Rubber Stamp against all signatures of partners operating the accounts.

Partnership letter.

4. Private Limited Company.

Account Opening Form.

Specimen Signature Card.

Copy of Trade License.

Copy of Memorandum and Articles of Association duly attested by the Managing

Director/ Chairman of the Co.

Certificate of Incorporation.

List of Director as per return of Joint Stock Company with signature.

Resolution of the Board for opening account with the bank.

Photographs of each of the authorized signatories.

45 | P a g e

5. Public Limited Company

Account Opening Form.

Specimen Signature Card.

Copy of Trade License.

Photograph of Directors and account operators other than Director.

Certified copy of Memorandum and Articles of Association.

Certificate of commencement of business.

List of Directors as per returns of Joint Stock Company with their signature.

Resolution of the Board for opening account with the Bank.

Certification of incorporation.

6. Clubs/ Association/ Society etc. (Non-Trading Concerns)

Account opening Form for current account or SB accounts.

Specimen Signature Card.

Certified copy of Bye laws/ constitution of the organization.

List of the Executives of Managing Committee with their signature and present and

permanent address.

Resolution of the Committee for opening account with the bank.

2 Photographs of each operator of the account.

7. Corporation/ Autonomous Bodies/ Govt. Organization

Account Opening Form as applicable.

Specimen Signature Card.

Copy of the Act or Ordinance Showing authority to open account.

Letter from the authorized persons in absence of the Board.

8. Account of Constituted Attorney

Account Opening Form (As applicable)

Specimen Signature Card

Power of Attorney

46 | P a g e

A copy of Power of Attorney shall be taken and entered in the Power of Attorney Register in

serial order. The serial number is to be noted along with Banks name on the Power of Attorney.

Original may be returned and the copy to be attached with Account Opening Form.

4.2.2 Issuing Cheque Book

A. Issue of fresh cheque book

Fresh cheque book is issued to the account holder only against requisition on the prescribed

requisition slip attached with the cheque book issued earlier, after proper verification of the

signature of the account holder personally or to his duly authorized representative against proper

acknowledgment.

47 | P a g e

Requisition slip filled properly along with

the cheque book number.

Banker Verifies the Slip

Banker issues new cheque book if every

thing in the right from.

Enter the new cheque book number in the

register book against the specific customer’s

name.

Procedure of issuance of a fresh cheque:

A customer who opened a new a/c initially deposits minimum required money in the account.

The account opening from is sent for issuance of a cheque book.

Respected officer first draws a cheque book

Officer than scaled it with branch name.

In-Charge officer enters the number of the cheque book in cheque issue register.

Officer also enters the customer’s name and the account number in the same register.

Account number is then writes down on the face of the cheque book and on every leaf of the

cheque book including requisition slip.

There is a special technique to sign every leaf of the cheque book with the help of carbon

paper. So officer’s signature prints the reverse side of the leaf.

The name of the customer is also written down on the face of the cheque book and on the

requisition slip.

The word “Issued on” along with the date of issuance is written down on the requisition.

Number of cheque book and date of issuance is also written on the application from.

Next, the customer is asked to sign in the cheque book issue register.

Then the respected officer signs on the face of the requisition slip put his initial in the

register and hand over the cheque to the customer.

B. Issue of New Cheque Book (For old Account)

All the procedure for issuing a new cheque book for old account is same as the procedure of new

account. Only difference is those customers have to submit the requisition slip of the old cheque

book with date, signature and his/her address. Computer posting is than give to the requisition

slip to know the position of account and to how many leaf/leaves still not used. The number of

new cheque book is entered on the back of the old requisition slip and is signed by the officer.

48 | P a g e

C. Procedure of issuance of a new cheque book:

If the cheque is handed over to any other person then the account holder the bank

addressing the account holder with details of cheque book issues an

acknowledgement slip. This acknowledgement slip must be signed by the account

holder and returned to the bank. Otherwise the bank will not honor any cheque from

this cheque book.

At the end of the day all the requisition slips and application forms are sent to the

computer section to give entry to these new cheque.

Then cutting the cheque book issuing) charge.

4.2.3Transfer of an Account

The account submits an application mentioning the name of the branch to which he

wants the account to be transferred.

His signature cards, advice of new account and all relevant documents are sent to

that branch through registered post.

The balance standing at credit in customer’s account is sent to the other branch

through Inter Branch Credit Advice (IBCA)

No exchange should be charged on such transfer.

Attention is also given in this connection.

4.2.4 Closing the Account

Upon the request of a customer, an account can be closed. After receiving an application from

the customer to close an account, the following procedure is followed by a banker. The customer

should be asked to draw the final cheque for the amount standing to the credit of his a/c less the

amount of closing and other incidental charges and surrender the unused cheque leaves. The a/c

should be debited for the account closing charges etc. and an authorized officer of the bank

should destroy unused cheque leaves.

49 | P a g e

In case of joint a/c, the application for closing the should be signed by all the joint holders.

A banker can also close the account of his customer or stop the operation of the account under

following considerable circumstances:

Death of Customer.

Customer’s insanity and insolvency.

Order of the court (Garnishee order)

Specific charge for fraud forgery.

4.2.5 Cash section

4.2.5.1Receipt and Payment of cash

Among the services provided by the bank, cash receipt and payment is the most vital and

physical function. Generally customer comes to bank to withdraw the money from their account

and deposit his savings in their accounts.

4.2.5.2 Cash Deposit

Money deposited in cash by the constituents at the cash counter of the bank excluding that of

government transaction is known as Bank Receipt (Cash). Different types of forms are used for

cash deposits for different types of accounts. Particulars of some forms are furnished below:

Current or Savings account pay in slip

Application for fixed deposit receipt

Credit voucher

Draft or mail transfer application form

T.T. Pay order application form Call deposit application form

Demand loan pays in slip.

50 | P a g e

4.2.5.3 Cash Payments

Banks payment includes all kinds of payments excluding those of treasury section. Extreme

precautions must be taken at all levels through, which instruments like cheque, drafts, etc, are

disposed of. All the instruments received at the general banking counter will be preliminary

checked by the dealing officer who will enter the instruments in the respective ledger. In case of

cheque the following particulars will be scrutinized.

Date (Whether post dated or anti dated)

Amount in word and figure

Crossed or Open

Bearer or Order

Style of signature as available in the ledger

Prohibitory order or stop payment of checks.

The Cash officer will follow the following procedures at the time of payments of checks/other

instruments over the cash counter.

1. The client will submit the instruments in the computer department first. The computer officer

and cheque passing authorized officer will verify the instrument and posted the instruments.

Then it will be send to the cash counter.

2. After getting the instrument the cash officer will verify the instruments and if necessary the

cash officer can tell the clients to sign in the backside of the instruments.

3. The officer will enter the check in the cash payments register where the denomination of

notes and coins will also be recorded.

4. The cash officer will give the amount to the clients at the cash counter and told the clients to

count it immediately and if needed any quarry.

5. All checks, drafts, debit vouchers etc. must be branded with “Cash Paid” stamp with the

current date.

6. After payment the cash department for the purpose of clean cash book will send the

vouchers.

7. The head of the cash department is responsible for all debit vouchers being branded with the

cash Paid date stamp immediately they are paid and the manager must supervise him/her in

this matter as any laxity is extremely dangerous.

51 | P a g e

4.2.6 Account Section

This is the most confidential department of a bank. Recording all kinds of transactions of the

branch, confirming their accuracy and preparing statements are the main job of this department.

Now a day under computerized banking system, the jobs of accounts department become very easy.

Now the computer directly prepares the clean cash statement on party ledger vouchers. The

function of the accounts department can be divided into two parts:

a) Daily function

b) Periodical functions

Daily functions:

The routine daily tasks of the accounts departments are as follows:

Record the daily transactions in the cash book.

Record the daily transactions in general and subsidiary ledger.

Prepare the daily position of the branch comprising of deposit and cash.

Prepare the daily statement of affairs showing all the assets and liability of the branch as

per ledger and subsidiary ledger separately.

Pay all expenditure on behalf of the branch.

Make salary statement and pay salary.

Checking whether all the vouchers are correctly passed to ensure the conformity with

the `Activity Report'; if otherwise making it correct by calling the respective official to

rectify the voucher.

Records inter branch fund transfer and providing accounting treatment in this regard.

Periodical Tasks:

The routine periodical tasked performed by the department are as follows:

Prepare the monthly salary statements for the employees.

Publish the basic data of the branch.

Prepare the weekly position for the branch, which is sent to the Head Office to maintain

Cash Reserve Requirement.

Prepare the monthly position for the branch, which is sent to the Head Office to maintain

52 | P a g e

Account SectionIBTA General Section

liquidity requirement.

Prepare the weekly position for the branch comprising of the breakup of sector wise deposit,

credit etc.

Preparing the budget for the branch by fixing the target regarding profit and deposit so as to

take necessary steps to generate and mobilize deposit.

JAMUNA bank instead of recording transactions in a journal initially, these are directly recorded

and posted in the ledger separating debit and credit by slip and voucher system. Records of all

the transactions of every department are kept here as well with other respective branch.

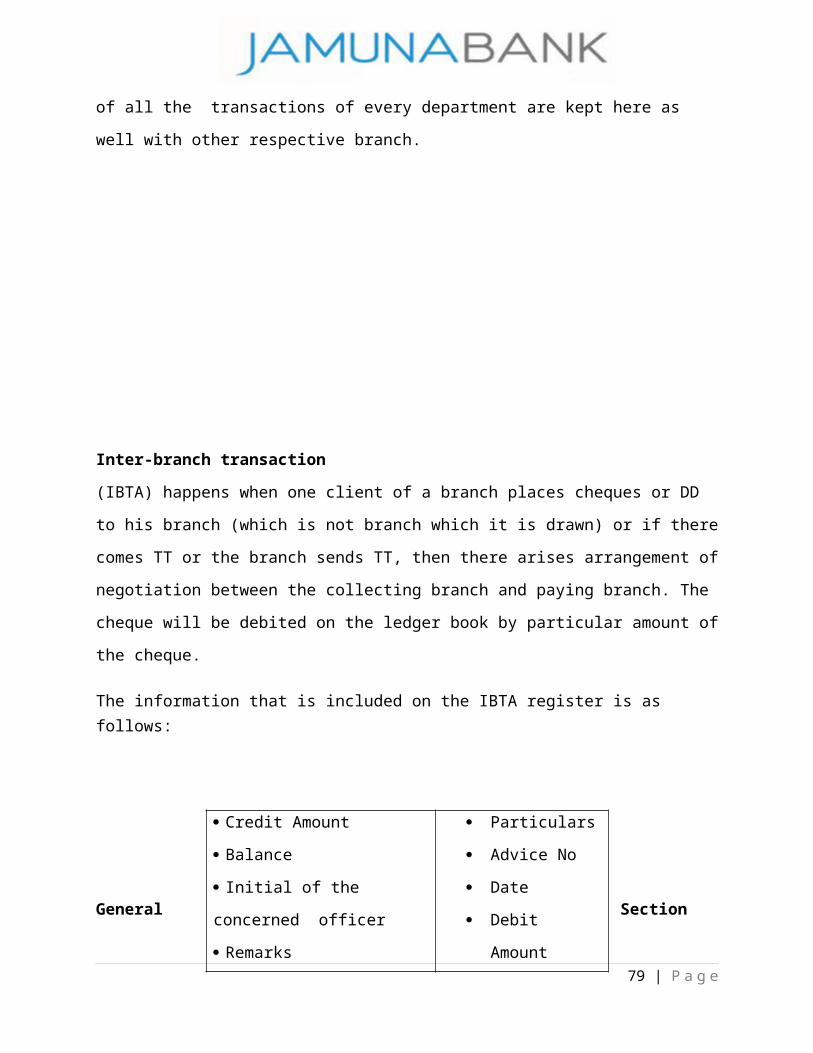

Inter-branch transaction

(IBTA) happens when one client of a branch places cheques or DD to his branch (which is not

branch which it is drawn) or if there comes TT or the branch sends TT, then there arises

arrangement of negotiation between the collecting branch and paying branch. The cheque will be

debited on the ledger book by particular amount of the cheque.

The information that is included on the IBTA register is as follows:

53 | P a g e

Credit Amount