trading and research in r with bloomberg -...

TRANSCRIPT

Trading and research

in R with Bloomberg

Peter Garnry, CFA

CopenhagenR – UseR Group Meetup

2015-05-13

Background

• Loved mathematics and physics in high school

• Bachelor in business (CBS / Warwick) – why?

• Co-founded a financial software company (2007-2010)

• Head of Equity Strategy, Saxo Bank (2010-)

• CFA (2011-2014); to please my educational ego

• Active R programmer since 2011

R in Saxo Bank

FX options pricing models

Multi-asset trading models

Middle-office risk management

Firm-wide risk management

Business intelligence

Research recommendation engine

CFD order flow analysis

The importance of R in finance

• JPMorgan CIO unit lost $6.2B in

2012 due to the “London Whale”

• VaR model underpinning the

hedging strategy was run in Excel!

• If this level of standard was found

in bridge construction…nobody

would drive over a bridge

The physics of Wall Street

Louis Bachelier

Ed Thorp

Maury Osbourne Benoît Mandelbrot

Fischer Black James D. Farmer

The king of quants

Jim Simons

• Only three losing quarters 1993-2005

• 40% p.a. after 5%/44%

• Trades everything that’s liquid

• Time-bound trades

Quantitative trading

• Rules for signal generation and

risk management

– Minimal or no human intervention

• Identify statistically significant and

hopefully repeatable signals

• Low-frequency to high-frequency

Trading strategies

• Forecasting

– Models (super- or unsupervised) attempting to predict the

direction in the future

• Mean reversion

– Trading the spread between two instruments (co-integration)

– Gaps, relative value etc.

• Momentum

– Builds on slow diffusion of information

• High frequency trading

– Exploits market microstructure, market making

Backtesting

• Test trading performance and risk

on historical data

• Remove hindsight bias

– How did you feel on September 16,

2008?

• Statistical performance tests for

comparison between signals

• Forecasting models: three-step…

– Training, validation, test

Backtesting pitfalls

• Training and testing on the same data

– Time series cross-validation (Hyndman) or “forecast evaluation with

rolling origin”

• Survivorship bias (expensive to eliminate)

• “Trade on the close” + ignoring price impact

• Unreasonable participation rate + strategy capacity

• Overfitting statistical model

• Bootstrapping provides more robust result

– Reshuffle historical returns or cross-sectional sample with replacement

over time

What bootstrapping looks like…

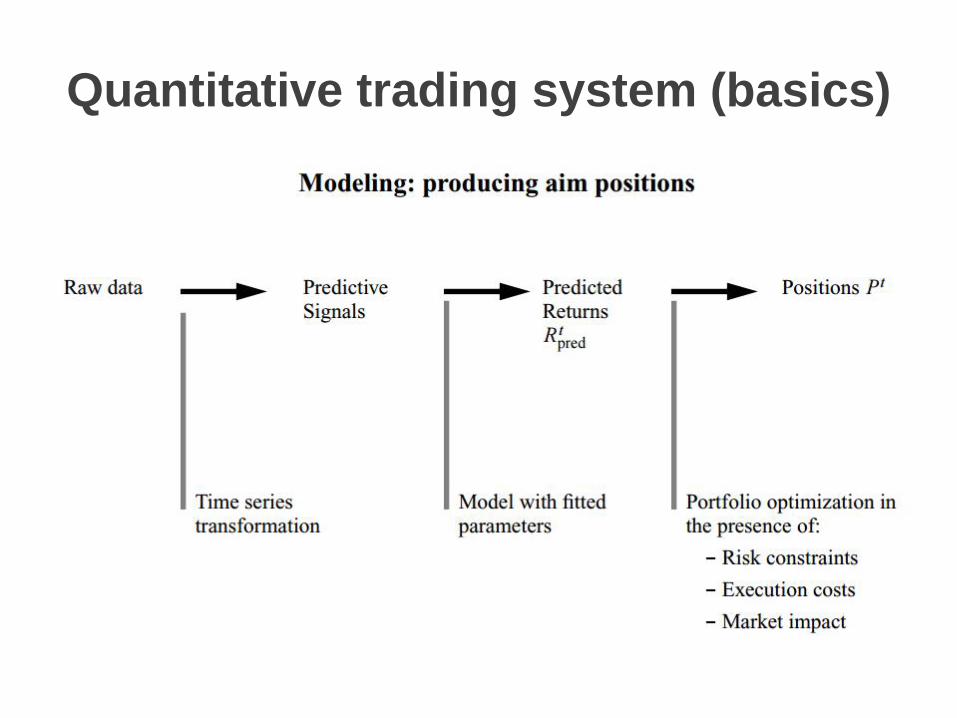

Quantitative trading system (basics)

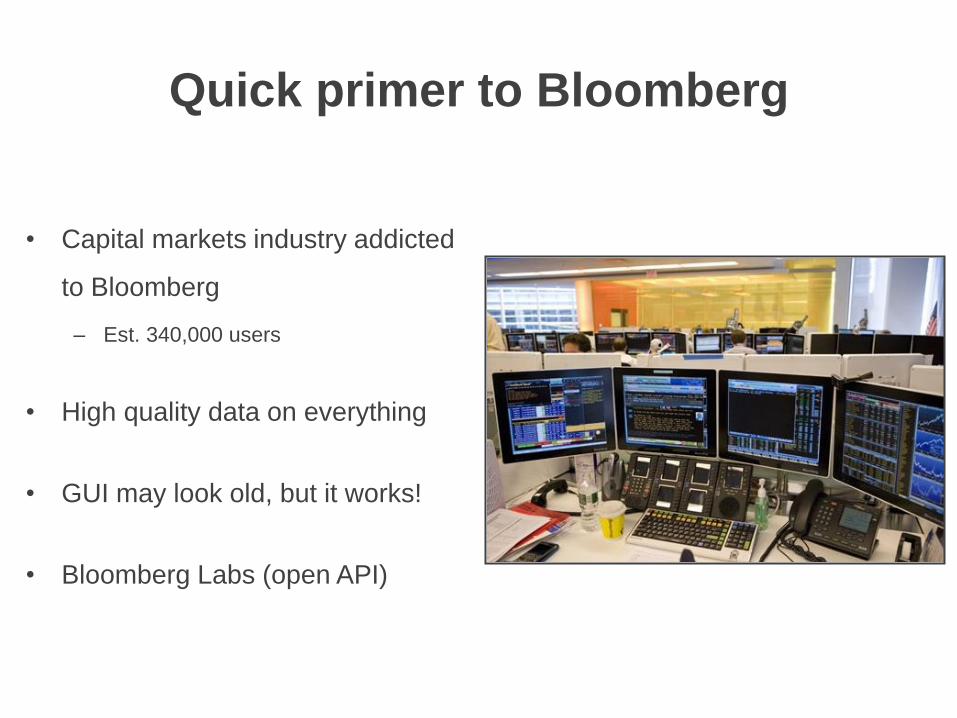

Quick primer to Bloomberg

• Capital markets industry addicted

to Bloomberg

– Est. 340,000 users

• High quality data on everything

• GUI may look old, but it works!

• Bloomberg Labs (open API)

Why data matters

• Corporate actions (splits, dividends etc.)

• Potential outliers distorting statistical models

• Winners/losers on gaps-on-open strategy sensitive to this!

Source: Bloomberg

Apple daily share price unadjusted for corporate actions

RbbgExtension

• Package extends the functions in the Rbbg package

– Connects Bloomberg with R

• Simplifies data queries on fundamental and price data

• Functions to eliminate survivorship bias

• Solves quirky data issues (active vs. inactive tickers)

• Future add-ons: Point-in-Time (equities), options, commodity

seasonality

– Cheaper than Compustat

Enough talk…show me code!

• Load S&P 100 tickers, get OHLCV since Jan 1, 2014

• Tickers > 1 + Fields > 1 = array(time, tickers, fields)

– Why not output data in a list?

Plot data using ‘quantmod’

Apple earnings

• Load historical earnings for Apple

• Plot EPS since 2005 + earnings surprise in %

It’s that easy…

VWAP strategy

• Strategy: long/short the price-to-vwap spread on close

– Long lowest spread (20 pos), short highest spread (20 pos)

– Execution orders < 30 secs before close

– Close positions on next day’s open (overnight bet)

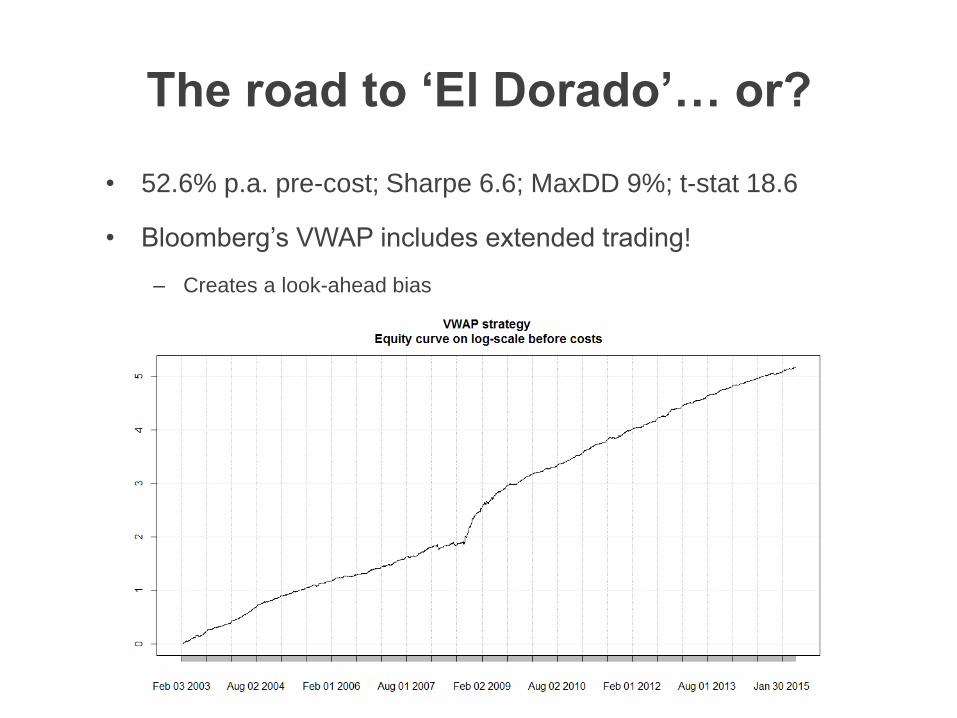

The road to ‘El Dorado’… or?

• 52.6% p.a. pre-cost; Sharpe 6.6; MaxDD 9%; t-stat 18.6

• Bloomberg’s VWAP includes extended trading!

– Creates a look-ahead bias

Pairs trading

• Market neutral strategy, first statistical arbitrage strategy

• Invented in the early 1982/83 by Gerry Bamberger at

Morgan Stanley’s quantitative group

– David Shaw came from same group, founded D.E. Shaw

• Find two time-series that co-integrates e.g. the regression

model’s residuals are stationary

– Typically pairs are found by correlation/co-integration grid search

across clusters (GICS or agglomerative hierarchical clustering)

• Very profitable strategy in 1980s and 1990s, but its has

slowly been arbitraged

Pairs trading

• Example on Coca-Cola and PepsiCo

– Almost identical companies with same product and geography

• Two years of data with the last three months out-of-sample

Momentum

• Premier market anomaly, accepted that as an

add-on to the famous three-factor model

• Robust factor over time, across countries and

asset classes

– Even across frequencies

• Dual-momentum is latest fashion (Gary

Antonacci)

– Implemented in ETFs

• Test momentum on Russell 1000

– Survivorship free vs bias

Few lines of code

34.4% vs 16.1% annualised

Monte carlo simulation

Signal strength

Momentum conclusions

• Code shows how easy it is to do quick trading research in R.

– Where R really shines compared to (Python), Java, C++

• Next step is subtracting trade cost, calculate strategy

capacity etc.

• Shows the importance of survivorship free data set

• Weak signal correlation but enough to beat the market

– But mean return is not significant (t-stat 1.23)

– Academia often finds momentum to be significant?

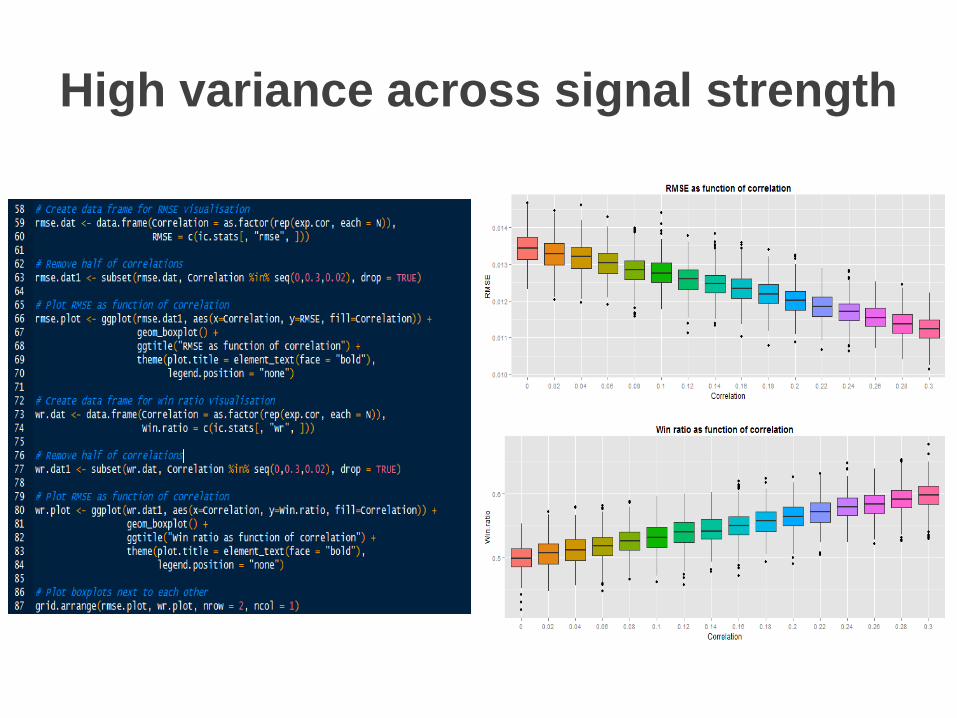

Let’s understand signal strength

• Generate 500 random bivariate normal distributions…

• …over a sequence of expected correlations

• Basically simulating forecasts against actual returns

• Asset with daily mean of 3 bps (7.9% p.a.)

High variance across signal strength

Why multiple strategies work…

Multi-layered signals

• Signal correlation is an important measurement of a model’s

predictive power

– Don’t expect strong signals

• Return variance reduces with signal strength and number of

strategies (depending on signal cross correlations)

• What to do when multiple signals disagree?

– And if the frequency is different?

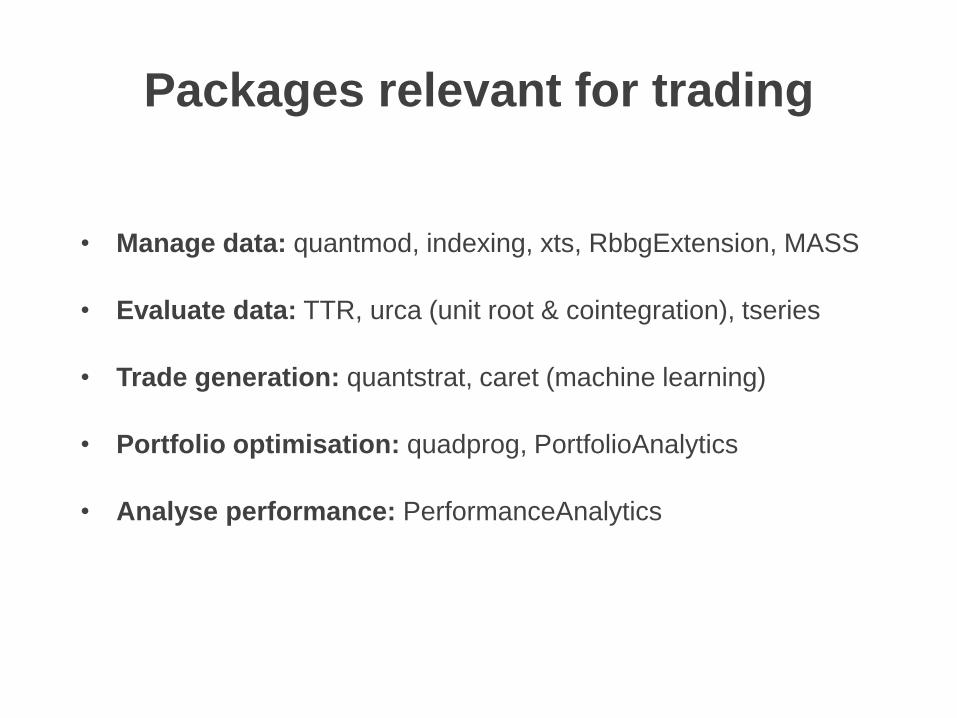

Packages relevant for trading

• Manage data: quantmod, indexing, xts, RbbgExtension, MASS

• Evaluate data: TTR, urca (unit root & cointegration), tseries

• Trade generation: quantstrat, caret (machine learning)

• Portfolio optimisation: quadprog, PortfolioAnalytics

• Analyse performance: PerformanceAnalytics

“In this business it’s easy to confuse

luck with brains”

Jim Simons (1996)