trans-pacific partnership agreement: likely impact on the

TRANSCRIPT

Trans-Pacific Partnership Agreement: Likely Impact on the U.S. Economy and on Specific Industry Sectors

May 2016

Publication Number: 4607

Investigation Number: TPA-105-001

Plan for the presentation

• Brief overview of the Agreement and the analytical framework

• Presentation of economic model results

• Highlights of TPP effects by industry

– Food and agricultural industries

– Manufacturing, natural resources and energy

– Services

2

Overview of TPP and the analysis

• Largest U.S. trade agreement: 12 countries accounting for 36% of global GDP

• Comprehensive agreement covering trade in goods and services, rules of origin, trade remedies, customs facilitation, SPS, TBTs, FDI, IP, government procurement, competition policy, and labor and environmental standards, and more

• The USITC report reviews and assesses all 30 chapters of the agreement

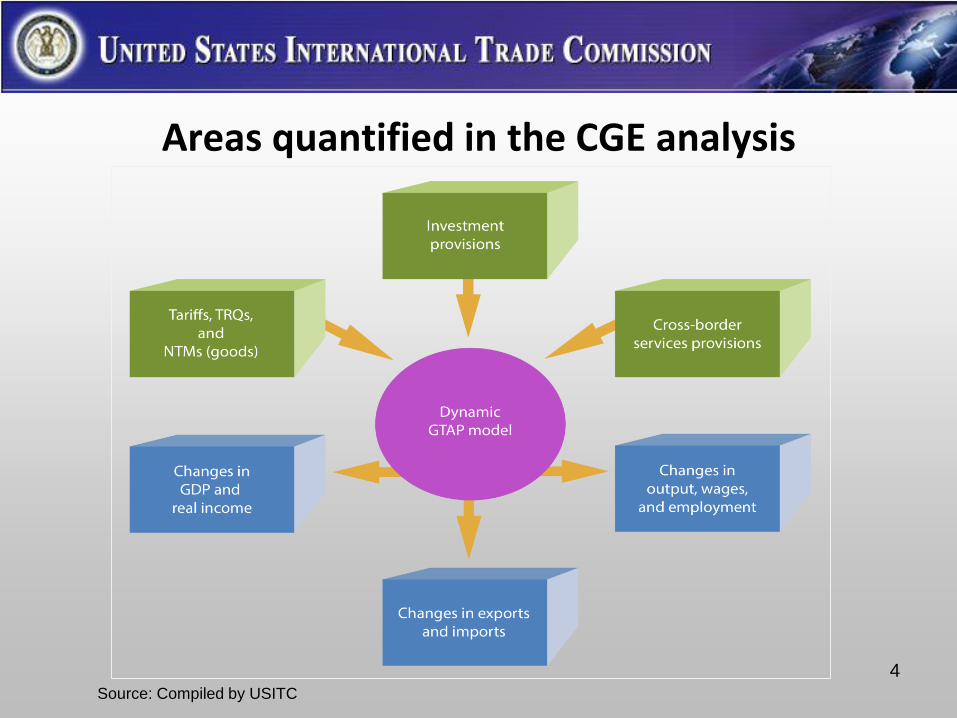

• The CGE analysis is limited to certain aspects of the agreement– Tariffs, TRQs, and NTMs on goods trade

– NTMs on cross-border services trade

– FDI provisions affecting investment in goods and services

• Other provisions are often cited by industry as delivering important benefits (e.g., IP, SOEs, gov’t procurement). Many of these are difficult to quantify

3

Areas quantified in the CGE analysis

4

Source: Compiled by USITC

Existing FTAs

Americas Asia/Oceania

U.S. Canada Mexico Chile Peru Australia Brunei Japan Malaysia N. Z. Singapore

Canada 1989

Mexico 1994 1994

Chile 2004 1997 1999

Peru 2009 2009 2012 2009

Australia 2005 2009

Brunei 2006 2010

Japan 2005 2007 2012 2015 2008

Malaysia 2012 2010 1992 2006

New Zealand 2006 1983 2010 2010

Singapore 2004 2006 2009 2010 1992 2002 1992 2001

Vietnam 2014 2010 1995 2008 1995 2010 1995

5Source: WTO, RTA-IS database; World Bank, Global PTAs Library

42 of 66 bilateral pairs are already covered by FTAs

Barriers to trade: new FTA partners

60 5 10 15 20 25 30 35 40 45

Agriculture & food

Manufacturing

Natural resources &energy

Services

Agriculture & food

Manufacturing

Natural resources &energy

Services

Agriculture & food

Manufacturing

Natural resources &energy

Services

Agriculture & food

Manufacturing

Natural resources &energy

Services

Agriculture & food

Manufacturing

Natural resources &energy

Services

Agriculture & food

Manufacturing

Natural resources &energy

USA

Bru

nei

Jap

anM

alay

sia

New

Ze

alan

dV

ietn

am

Aga

inst

U.S

. exp

ort

s

AVE before TPP

AVE in 2032

Barriers to trade: existing FTA partners

70 10 20 30 40 50 60 70

Services

Agriculture and food

Manufacturing

Natural resources and energy

Services

Agriculture and food

Manufacturing

Natural resources and energy

Services

Agriculture and food

Manufacturing

Natural resources and energy

Services

Agriculture and food

Manufacturing

Natural resources and energy

Services

Agriculture and food

Manufacturing

Natural resources and energy

Services

Agriculture and food

Manufacturing

Natural resources and energy

Au

stra

liaC

anad

aC

hile

Mex

ico

Per

uSi

nga

po

re

Aga

inst

U.S

. exp

ort

s

AVE before TPP

AVE in 2032

Methodology for modeling investment provisions

8

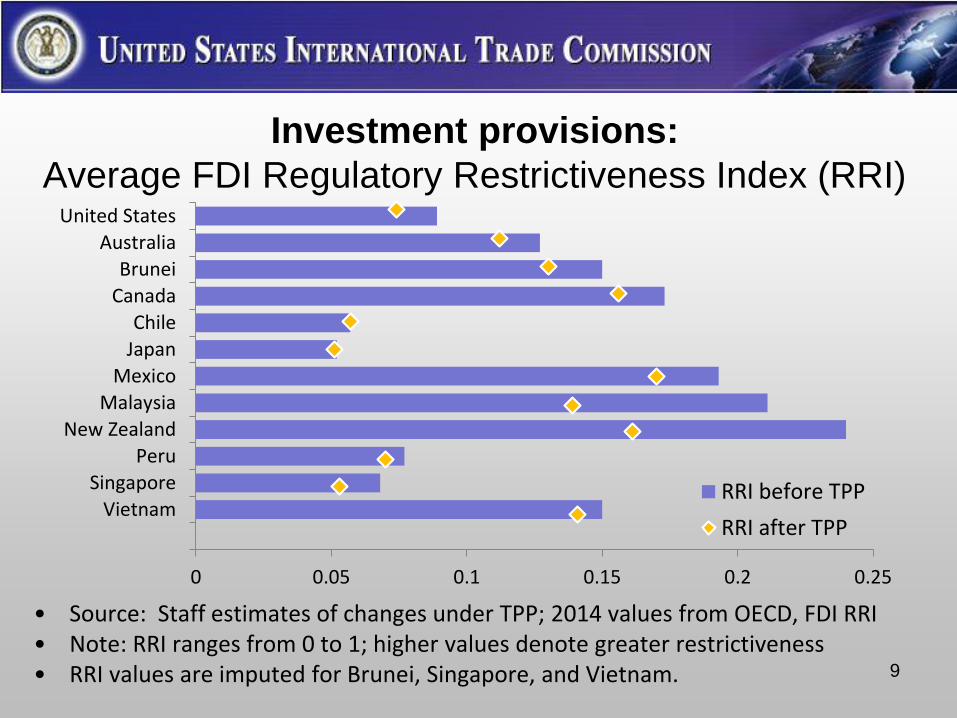

Investment provisions:

Average FDI Regulatory Restrictiveness Index (RRI)

9

• Source: Staff estimates of changes under TPP; 2014 values from OECD, FDI RRI• Note: RRI ranges from 0 to 1; higher values denote greater restrictiveness• RRI values are imputed for Brunei, Singapore, and Vietnam.

0 0.05 0.1 0.15 0.2 0.25

United States

Australia

Brunei

Canada

Chile

Japan

Mexico

Malaysia

New Zealand

Peru

Singapore

VietnamRRI before TPP

RRI after TPP

10

Reduced investment barriers raise productivityHost country productivity gain from TPP’s reduction

in host country RRI, percentage

Note: Economy-wide productivity gains are calculated as share-weighted averages of

sector gains using sales shares

0 0.5 1 1.5 2

United States

Australia

Brunei

Canada

Chile

Japan

Mexico

Malaysia

New Zealand

Peru

Singapore

Vietnam

AGGREGATE MODEL RESULTS

11

Interpreting the modeling results

12Source: USITC estimates

Annual Economy-wide Effects of TPPChanges Relative to Baseline in 2032 and 2047

13

2032 2047

Billion $ Percent Billion $ Percent

Real income 57.3 0.23 82.5 0.28

Real GDP 42.7 0.15 67.0 0.18

Employment (FTEs, thousands) 128.2 0.07 174.3 0.09

Capital stock 171.5 0.18 343.5 0.24

Source: USITC estimates.Note: Dollar values are in 2017 prices.

Broad Sector-level Effects of TPPChanges Relative to Baseline in 2032

14

Exports Imports Output Employment

Billion $ Percent Billion $ Percent Billion $ Percent Percent

Agriculture and food 7.2 2.6 2.7 1.5 10.0 0.5 0.5

Manufacturing, natural resources, and energy

15.2 0.9 39.2 1.1 -10.8 -0.1 -0.2

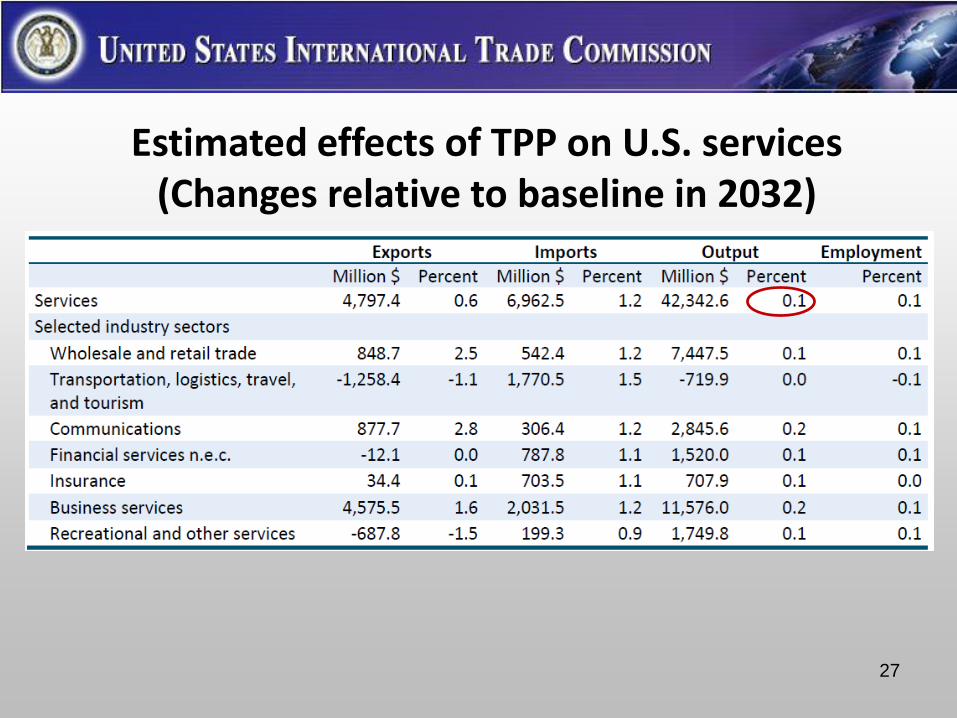

Services 4.8 0.6 7.0 1.2 42.3 0.1 0.1

Source: USITC estimates.Note: Dollar values are in 2017 prices.

Effects of TPP on U.S. Trade by PartnerChanges Relative to Baseline in 2032

15

Exports Imports

Billion $ Percent Billion $ Percent

Trade with TPP partners 57.2 5.6 47.5 3.5

New FTA partners 34.6 18.7 23.4 10.4

Existing FTA partners 22.6 2.7 24.2 2.1

Trade with the world 27.2 1.0 48.9 1.1

Source: USITC estimates.Note: Dollar values are in 2017 prices.

FOOD AND AGRICULTURE

16

Exports Imports Output Employ-

ment

Million $ % Million $ % Million $ % %

Agriculture and food (total) 7,227 2.6 2,734 1.5 10,015 0.5 0.5

Selected industry sectors:

Sugar, sweeteners and SCP 130 4.3 132 2.4 518 0.4 0.4

Dairy products 1,846 18.0 349 10.3 1,839 1.3 1.1

Beef meat 876 8.4 419 5.7 615 0.5 0.4

Pork meat products 219 1.9 94 4 180 0.3 0.3

Poultry meat products 174 1.3 -17 -3.6 266 0.6 0.6

Rice -13 -0.3 15 1.6 -18 -0.1 0.0

Wheat -2 0.0 18 1.5 -8 0.0 -0.7

Corn grain -31 -0.1 3 1.3 207 0.3 0.4

Processed foods 1,540 3.8 427 1.1 2,397 0.8 0.7

Fresh fruit and vegetables 575 2.0 119 0.5 172 0.2 0.3

Seafood 74 2.2 232 0.9 -52 -0.2 -0.2

17

Effects of TPP on U.S. food and agriculture(Changes relative to baseline in 2032)

The biggest driver of change is increased export opportunities in Japan and Vietnam

• New TPP partners are expected to account for over 70% of the additional food/ag exports

• Greater access to Japan’s high-priced market which demands goods the U.S. can competitively supply

• Vietnam reducing very high tariffs on food/ag products; incomes rising rapidly

Biggest change with existing FTA partners is in dairy

• Additional $1.2 billion in dairy exports to Canada due to additional TRQ access (though market would remain highly managed) and close proximity

18

MANUFACTURING, NATURAL RESOURCES AND ENERGY (MNRE)

19

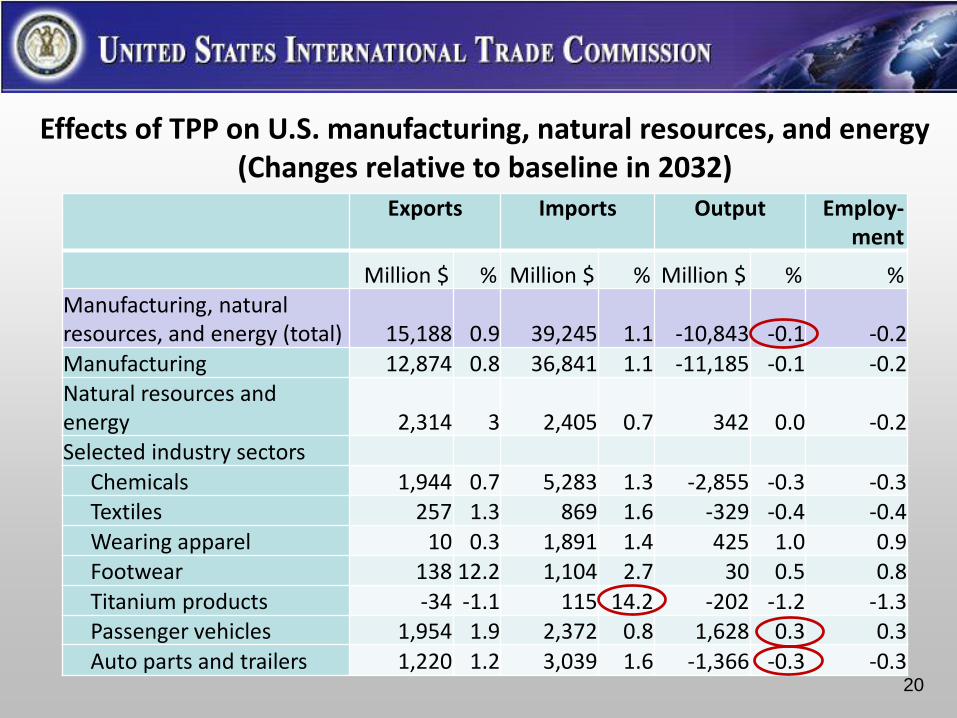

Exports Imports Output Employ-ment

Million $ % Million $ % Million $ % %Manufacturing, natural resources, and energy (total) 15,188 0.9 39,245 1.1 -10,843 -0.1 -0.2

Manufacturing 12,874 0.8 36,841 1.1 -11,185 -0.1 -0.2Natural resources and energy 2,314 3 2,405 0.7 342 0.0 -0.2Selected industry sectors

Chemicals 1,944 0.7 5,283 1.3 -2,855 -0.3 -0.3Textiles 257 1.3 869 1.6 -329 -0.4 -0.4

Wearing apparel 10 0.3 1,891 1.4 425 1.0 0.9Footwear 138 12.2 1,104 2.7 30 0.5 0.8

Titanium products -34 -1.1 115 14.2 -202 -1.2 -1.3Passenger vehicles 1,954 1.9 2,372 0.8 1,628 0.3 0.3

Auto parts and trailers 1,220 1.2 3,039 1.6 -1,366 -0.3 -0.320

Effects of TPP on U.S. manufacturing, natural resources, and energy(Changes relative to baseline in 2032)

MNRE Products

• U.S. production in all sectors modeled

would increase over time in baseline

• Direct impact of TPP relative to baseline is

likely to be limited

• Only a relatively small value of U.S. MNRE

trade with TPP partners is currently dutiable

– Some individual industries (e.g., titanium metal)

may experience more adverse impacts from TPP,

while others (e.g., passenger vehicles) may

benefit from TPP 21

Passenger vehicles and parts—Provisions

• Tariff reductions– U.S. tariffs on Japanese imports not reduced at all until year 15,

eliminated by year 30

– Vietnam and Malaysia tariffs on U.S. exports eliminated by year 13

• Rules of origin– Lower RVC relative to NAFTA could negatively affect U.S. parts

production

• Side letters– Japan—details specific NTM reductions, and trade remedies

– Malaysia—removes local content requirements and preferential taxes

by 2021, promise to consider U.S. safety and emissions standards

22

Passenger vehicles and parts—Effects

23

• Vehicles – Increased U.S. demand leads to more vehicles produced,

imported, and exported– Vehicle exports increase to Japan, Vietnam, and Malaysia– Canada and Mexico supply most new imports through

2032; in later years Japan accounts for a significant share of the increase

• Parts – Predicted increase in U.S. vehicle production drives

increased imports of parts. Import increase comes primarily from North America and Japan (somewhat)

– Parts exports also increase; most growth to Canada and Mexico, as part of North American supply chains

SERVICES

24

Services Trade is Liberalized in TPP

Services trade is liberalized by provisions in 5+ chapters:

• Investment—mode 3 commercial presence

• Cross-border Trade in Services—mode 1 cross-border trade is free, except for specific NCMs taken

• E-commerce—dataflow provisions for all sectors except financial services

• Financial Services—banking, insurance, electronic payment services, etc.

• Telecommunications services—Dataflow, FDI and standards

• IP, SOEs, Government Procurement, Regulatory Coherence…

25

Liberalization would lower costs for cross-border services trade

• For sectors with a high level of product innovation, such as digital sectors, where the negative list approach is most helpful

• For those sectors that would benefit most from the dataflow provisions such as communications and business services

• For sectors where a TPP partner improved its commitments by reducing NCMs, such as professional services (Brunei, Malaysia, Chile, Japan, and New Zealand)

26

27

Estimated effects of TPP on U.S. services (Changes relative to baseline in 2032)

E-Commerce Provisions Could Increase Competitiveness of U.S. firms

• Cross-border data and information flows ensured: except for legitimate public policy reason (not trade advantage)

• Forced localization measures prohibited: cannot require data servers to be located in-country

• Other key provisions:– Customs duties on digital products prohibited

– Personal privacy and online consumer protection

– Electronic customs forms, signatures, and paperless trading

– Software code does not have to be disclosed

– Cooperation on cybersecurity and SME e-commerce

28

CROSS-CUTTING AND PROCEDURAL PROVISIONS AND OTHER PROVISIONS ADDRESSING RULES AND NON-TARIFF MEASURES

29

Overview• These chapters are often cited by industry as containing important

interlocking benefits that reduce overall trade costs (Investment, IP, SOEs, TBT, Customs Admin, Government Procurement)

• Broad range of topics, mostly qualitative analysis

• Seven chapters not included in existing U.S. FTAs:

– Temporary Entry for Business Persons

– State-owned Enterprises

– Cooperation & Capacity Building

– Competitiveness & Business Facilitation

– Development

– Small and Medium-sized Enterprises

– Regulatory Coherence

30

Sanitary and Phytosanitary (SPS) Measures

• Likely to significantly benefit U.S. firms investing in and exporting to the region

• Would require modern, science-based food safety regulations

• Most provisions subject to dispute resolution

• “WTO-Plus”: clarifies and significantly builds on provisions of the WTO SPS Agreement, and includes provisions that are entirely new for U.S. trade agreements

• Letter exchanges between the United States and other TPP parties have already resolved specific outstanding SPS market access issues for U.S. beef and other products

31

Technical Barriers to Trade (TBT)

• Significant benefits for U.S. firms investing in and exporting to TPP parties

• Cross-cutting provisions applicable to all goods sectors, would require open, transparent systems of standards and regulatory-setting in TPP countries

• Seven sector-specific annexes detailing particular standards, regulatory, and conformity assessment provisions• Wine/Distilled Spirits; ICT Products; Pharmaceuticals; Cosmetics;

Medical Devices; Proprietary Formulas for Prepackaged Foods and Food Additives; Organic Products

• WTO-Plus: clarifies and significantly builds on provisions of the WTO TBT Agreement and existing U.S. FTAs

• Many TBT provisions are entirely new for all TPP parties

Thank You

33