transfer pricing documentation - bcasonline.org · transfer pricing (tp) ... the relevant...

TRANSCRIPT

Transfer Pricing

Documentation

March 2015

1

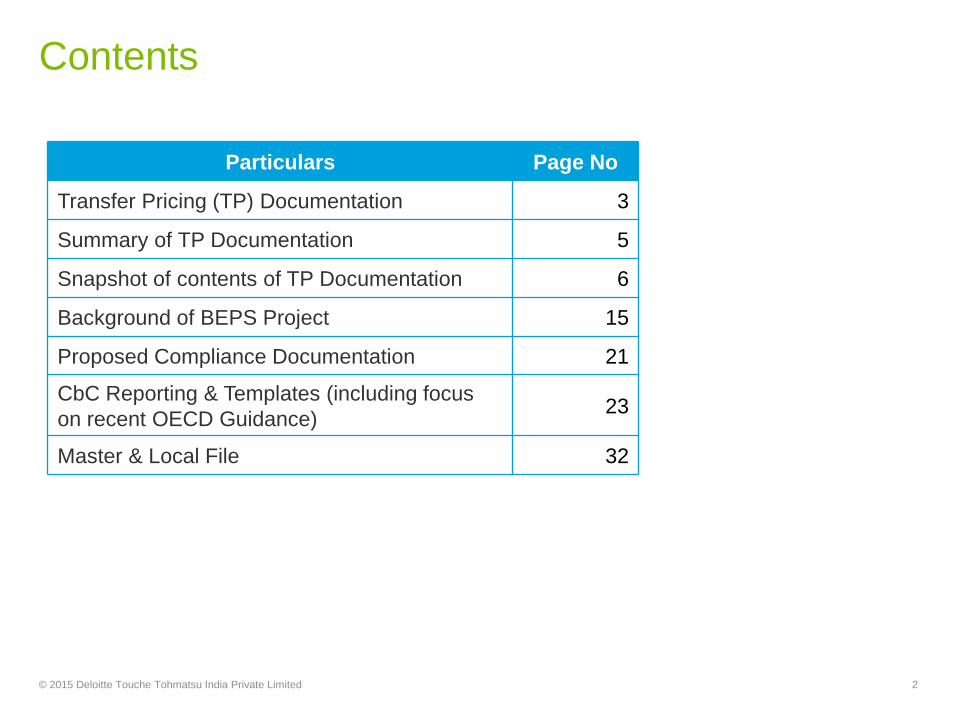

Contents

© 2015 Deloitte Touche Tohmatsu India Private Limited 2

Particulars Page No

Transfer Pricing (TP) Documentation 3

Summary of TP Documentation 5

Snapshot of contents of TP Documentation 6

Background of BEPS Project 15

Proposed Compliance Documentation 21

CbC Reporting & Templates (including focus

on recent OECD Guidance)23

Master & Local File 32

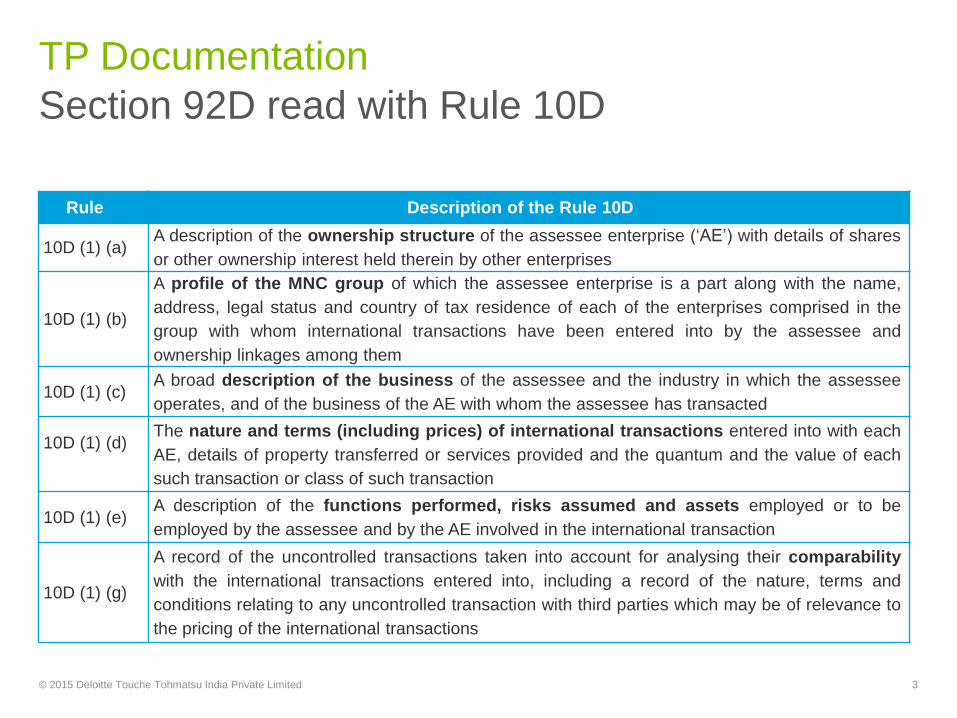

Section 92D read with Rule 10D

TP Documentation

3

Rule Description of the Rule 10D

10D (1) (a)A description of the ownership structure of the assessee enterprise („AE‟) with details of shares

or other ownership interest held therein by other enterprises

10D (1) (b)

A profile of the MNC group of which the assessee enterprise is a part along with the name,

address, legal status and country of tax residence of each of the enterprises comprised in the

group with whom international transactions have been entered into by the assessee and

ownership linkages among them

10D (1) (c)A broad description of the business of the assessee and the industry in which the assessee

operates, and of the business of the AE with whom the assessee has transacted

10D (1) (d)The nature and terms (including prices) of international transactions entered into with each

AE, details of property transferred or services provided and the quantum and the value of each

such transaction or class of such transaction

10D (1) (e)A description of the functions performed, risks assumed and assets employed or to be

employed by the assessee and by the AE involved in the international transaction

10D (1) (g)

A record of the uncontrolled transactions taken into account for analysing their comparability

with the international transactions entered into, including a record of the nature, terms and

conditions relating to any uncontrolled transaction with third parties which may be of relevance to

the pricing of the international transactions

© 2015 Deloitte Touche Tohmatsu India Private Limited

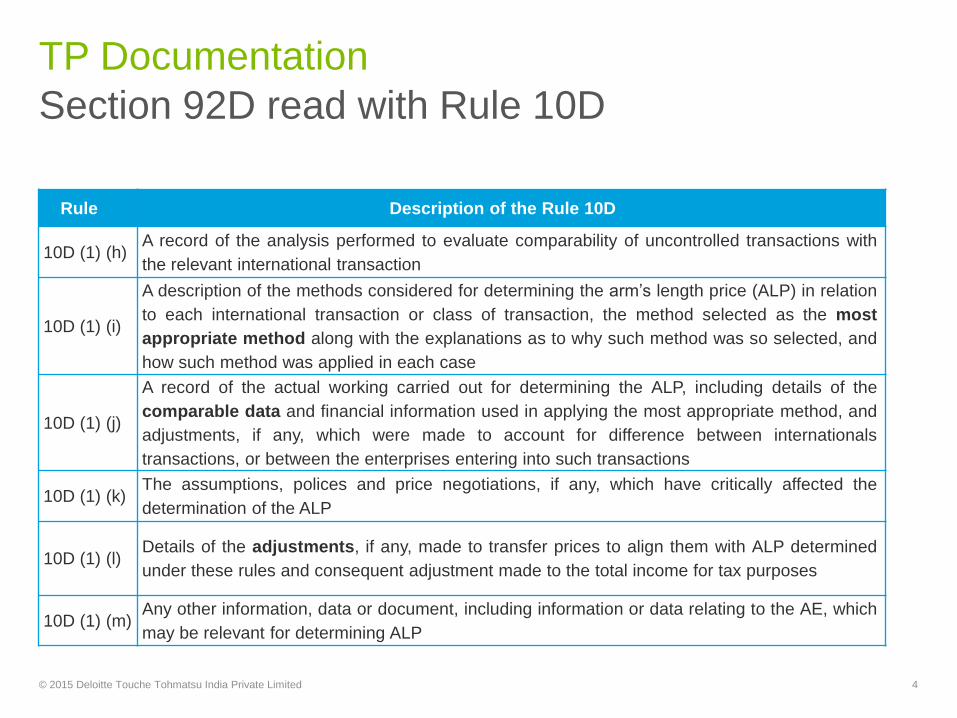

Section 92D read with Rule 10D

TP Documentation

© 2015 Deloitte Touche Tohmatsu India Private Limited 4

Rule Description of the Rule 10D

10D (1) (h)A record of the analysis performed to evaluate comparability of uncontrolled transactions with

the relevant international transaction

10D (1) (i)

A description of the methods considered for determining the arm‟s length price (ALP) in relation

to each international transaction or class of transaction, the method selected as the most

appropriate method along with the explanations as to why such method was so selected, and

how such method was applied in each case

10D (1) (j)

A record of the actual working carried out for determining the ALP, including details of the

comparable data and financial information used in applying the most appropriate method, and

adjustments, if any, which were made to account for difference between internationals

transactions, or between the enterprises entering into such transactions

10D (1) (k)The assumptions, polices and price negotiations, if any, which have critically affected the

determination of the ALP

10D (1) (l)Details of the adjustments, if any, made to transfer prices to align them with ALP determined

under these rules and consequent adjustment made to the total income for tax purposes

10D (1) (m)Any other information, data or document, including information or data relating to the AE, which

may be relevant for determining ALP

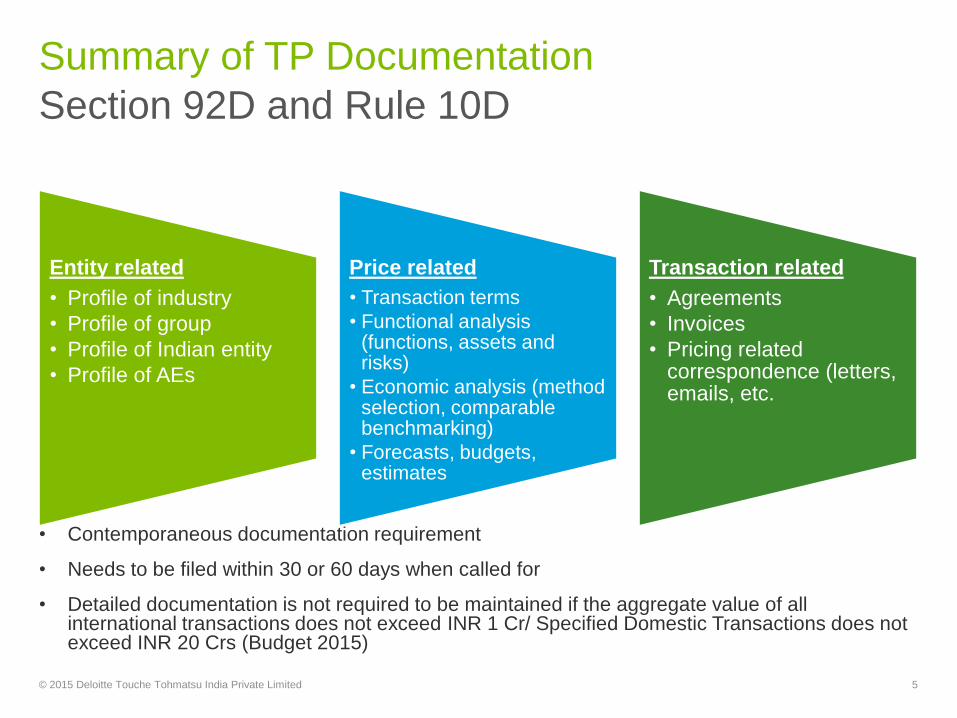

Section 92D and Rule 10D

Summary of TP Documentation

• Contemporaneous documentation requirement

• Needs to be filed within 30 or 60 days when called for

• Detailed documentation is not required to be maintained if the aggregate value of all international transactions does not exceed INR 1 Cr/ Specified Domestic Transactions does not exceed INR 20 Crs (Budget 2015)

© 2015 Deloitte Touche Tohmatsu India Private Limited 5

Entity related

• Profile of industry

• Profile of group

• Profile of Indian entity

• Profile of AEs

Price related

• Transaction terms

• Functional analysis (functions, assets and risks)

• Economic analysis (method selection, comparable benchmarking)

• Forecasts, budgets, estimates

Transaction related

• Agreements

• Invoices

• Pricing related correspondence (letters, emails, etc.

Snapshot of contents of TP

Documentation

6© 2015 Deloitte Touche Tohmatsu India Private Limited

Executive Summary

• Introduction about the company

• Overview of the business:

‒ Main activities of the group

‒ Main activities of the company

• Economic Analysis:

‒ Summary of International transactions and SDT

‒ TP method

‒ Value of transaction

‒ Margin of the company

‒ Margin of comparable companies

• Conclusion (whether the transactions are in accordance with the arm‟s length standard,

as required under the TP regulations or not)

© 2015 Deloitte Touche Tohmatsu India Private Limited 7

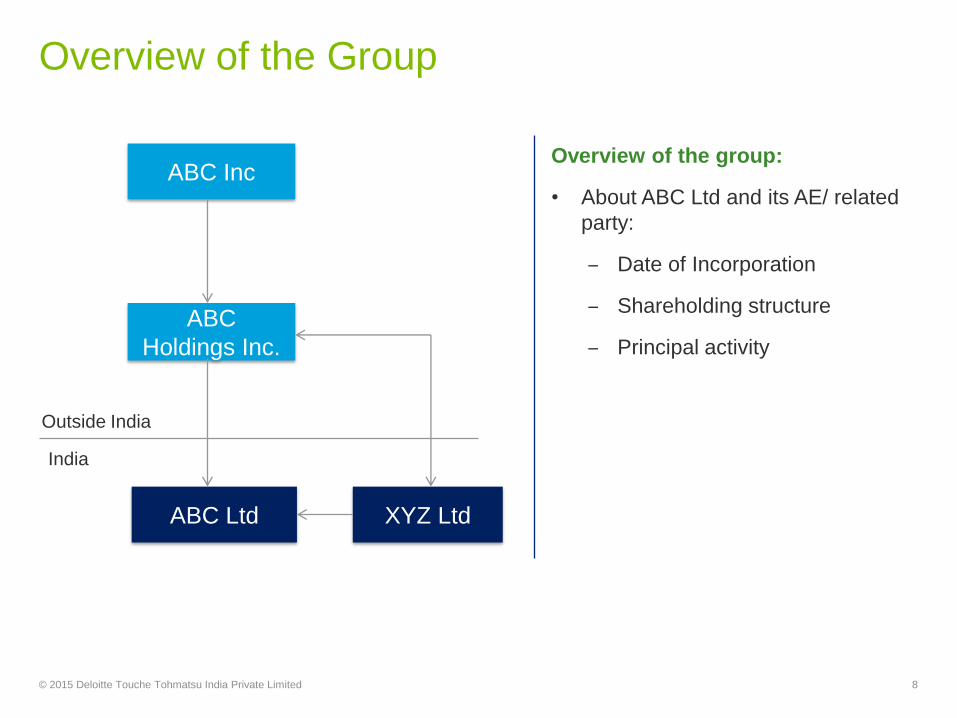

Overview of the Group

Overview of the group:

• About ABC Ltd and its AE/ related

party:

‒ Date of Incorporation

‒ Shareholding structure

‒ Principal activity

© 2015 Deloitte Touche Tohmatsu India Private Limited 8

ABC Inc

ABC

Holdings Inc.

ABC Ltd XYZ Ltd

Outside India

India

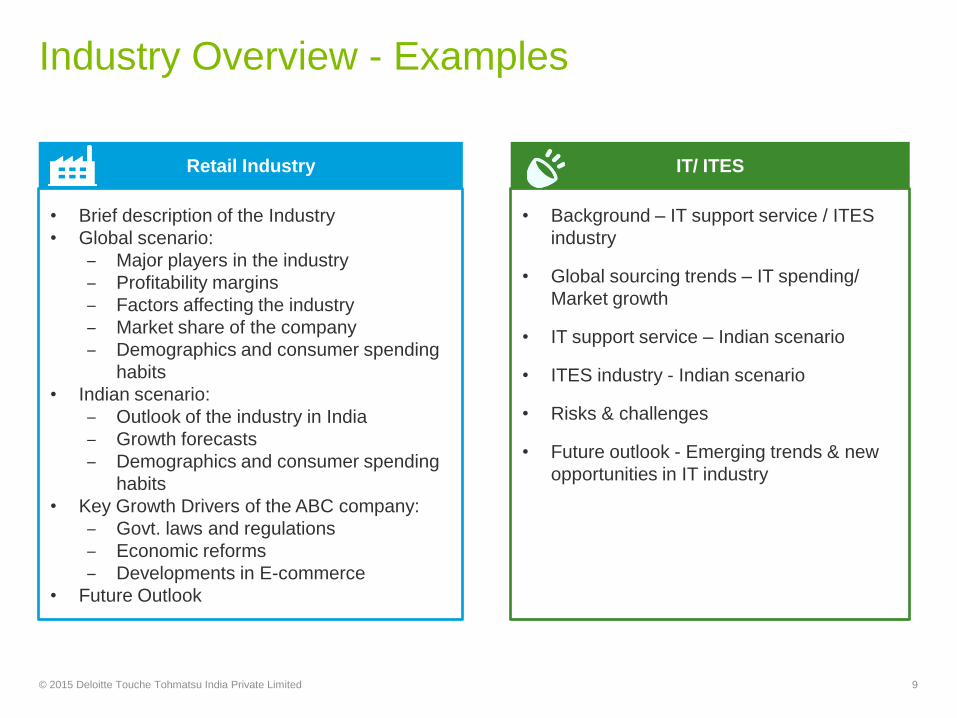

Industry Overview - Examples

© 2015 Deloitte Touche Tohmatsu India Private Limited 9

Retail Industry

• Brief description of the Industry

• Global scenario:

‒ Major players in the industry

‒ Profitability margins

‒ Factors affecting the industry

‒ Market share of the company

‒ Demographics and consumer spending

habits

• Indian scenario:

‒ Outlook of the industry in India

‒ Growth forecasts

‒ Demographics and consumer spending

habits

• Key Growth Drivers of the ABC company:

‒ Govt. laws and regulations

‒ Economic reforms

‒ Developments in E-commerce

• Future Outlook

IT/ ITES

• Background – IT support service / ITES

industry

• Global sourcing trends – IT spending/

Market growth

• IT support service – Indian scenario

• ITES industry - Indian scenario

• Risks & challenges

• Future outlook - Emerging trends & new

opportunities in IT industry

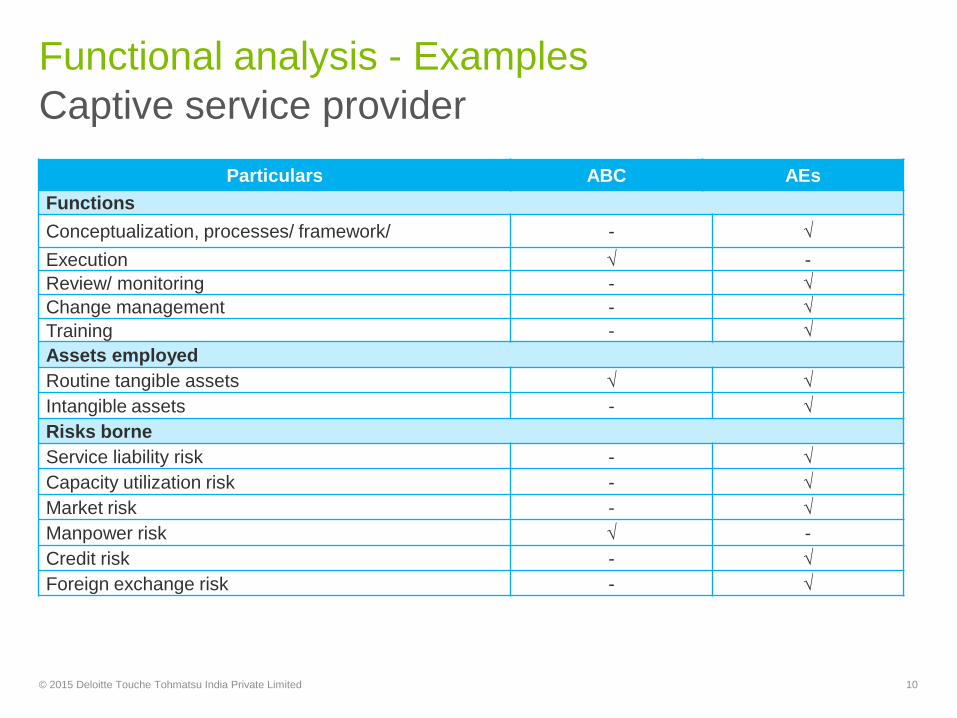

Captive service provider

Functional analysis - Examples

© 2015 Deloitte Touche Tohmatsu India Private Limited 10

Particulars ABC AEs

Functions

Conceptualization, processes/ framework/ - √

Execution √ -

Review/ monitoring - √

Change management - √

Training - √

Assets employed

Routine tangible assets √ √

Intangible assets - √

Risks borne

Service liability risk - √

Capacity utilization risk - √

Market risk - √

Manpower risk √ -

Credit risk - √

Foreign exchange risk - √

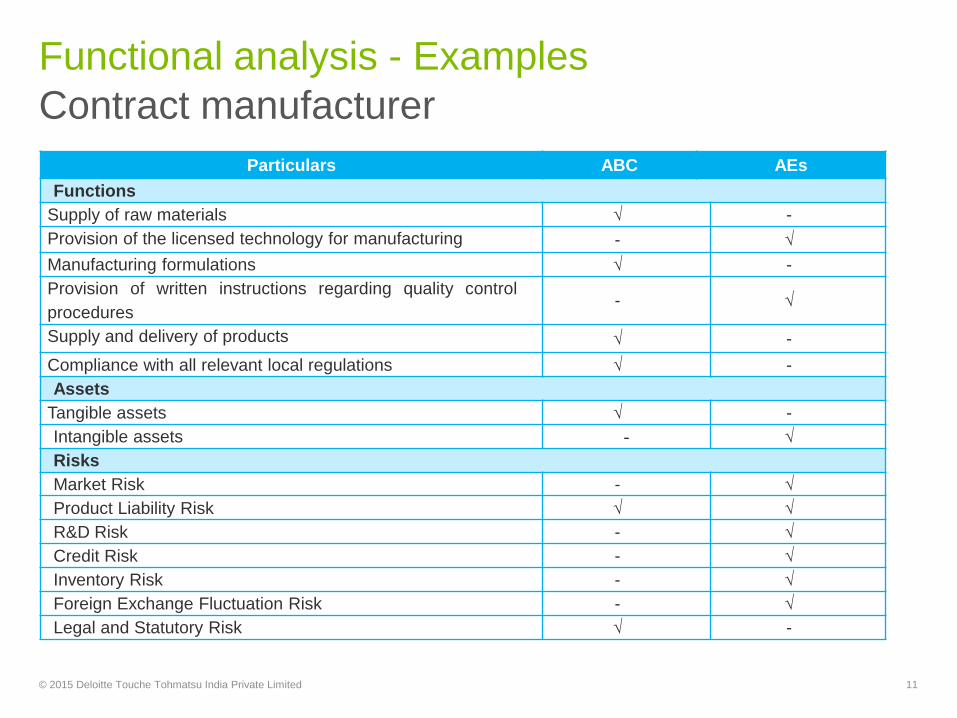

Contract manufacturer

Functional analysis - Examples

© 2015 Deloitte Touche Tohmatsu India Private Limited 11

Particulars ABC AEs

Functions

Supply of raw materials √ -

Provision of the licensed technology for manufacturing - √

Manufacturing formulations √ -

Provision of written instructions regarding quality control

procedures- √

Supply and delivery of products √ -

Compliance with all relevant local regulations √ -

Assets

Tangible assets √ -

Intangible assets - √

Risks

Market Risk - √

Product Liability Risk √ √

R&D Risk - √

Credit Risk - √

Inventory Risk - √

Foreign Exchange Fluctuation Risk - √

Legal and Statutory Risk √ -

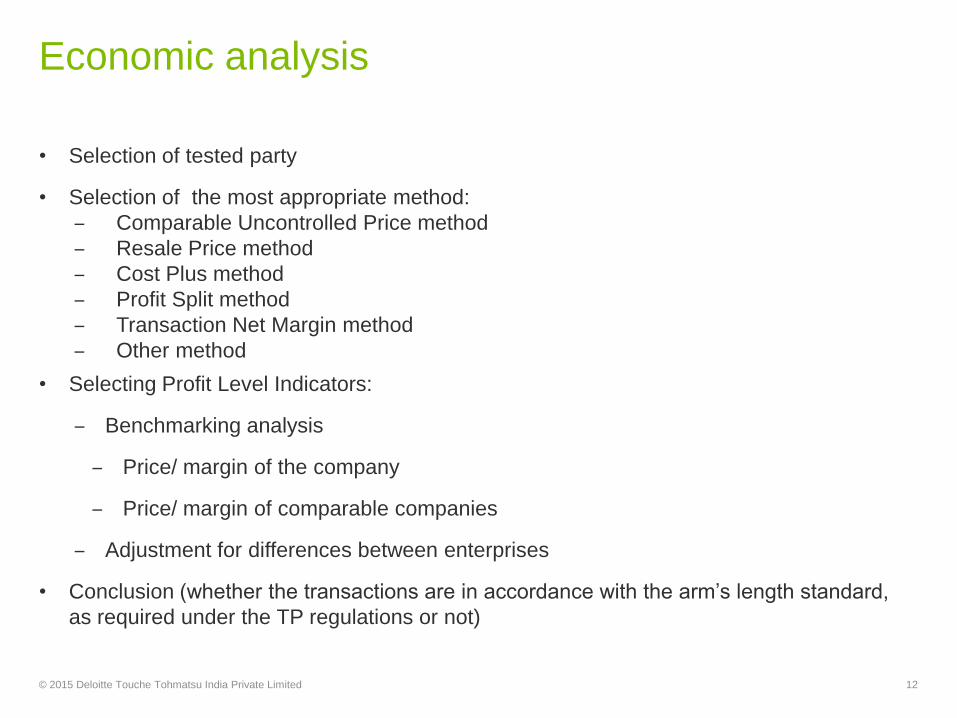

Economic analysis

• Selection of tested party

• Selection of the most appropriate method:

‒ Comparable Uncontrolled Price method

‒ Resale Price method

‒ Cost Plus method

‒ Profit Split method

‒ Transaction Net Margin method

‒ Other method

• Selecting Profit Level Indicators:

‒ Benchmarking analysis

‒ Price/ margin of the company

‒ Price/ margin of comparable companies

‒ Adjustment for differences between enterprises

• Conclusion (whether the transactions are in accordance with the arm‟s length standard,

as required under the TP regulations or not)

© 2015 Deloitte Touche Tohmatsu India Private Limited 12

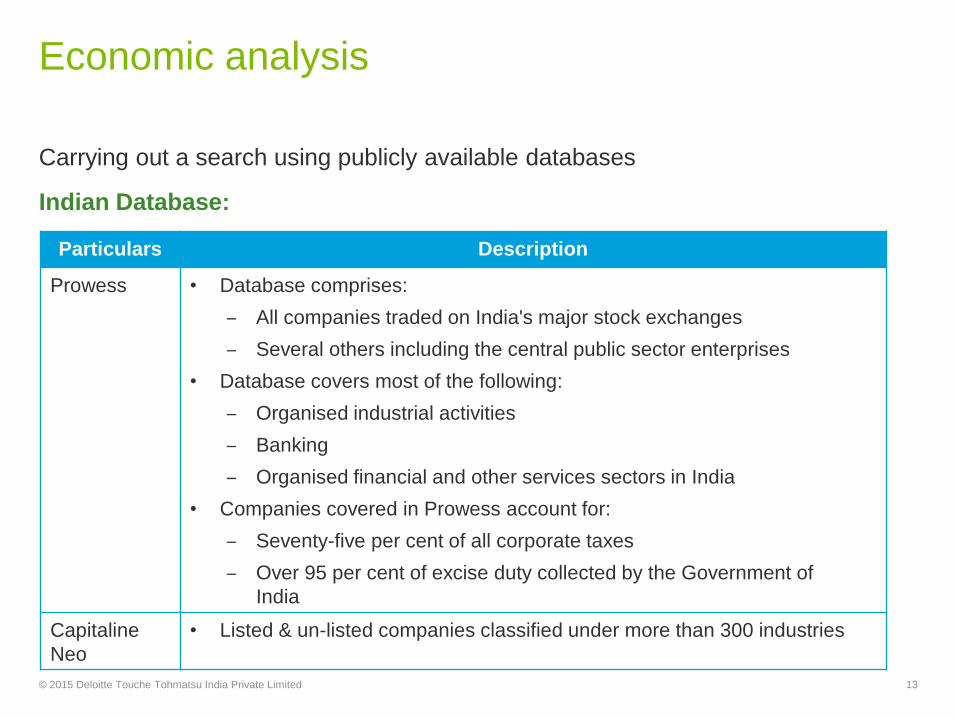

Economic analysis

Carrying out a search using publicly available databases

Indian Database:

© 2015 Deloitte Touche Tohmatsu India Private Limited 13

Particulars Description

Prowess • Database comprises:

‒ All companies traded on India's major stock exchanges

‒ Several others including the central public sector enterprises

• Database covers most of the following:

‒ Organised industrial activities

‒ Banking

‒ Organised financial and other services sectors in India

• Companies covered in Prowess account for:

‒ Seventy-five per cent of all corporate taxes

‒ Over 95 per cent of excise duty collected by the Government of

India

Capitaline

Neo

• Listed & un-listed companies classified under more than 300 industries

Economic analysis

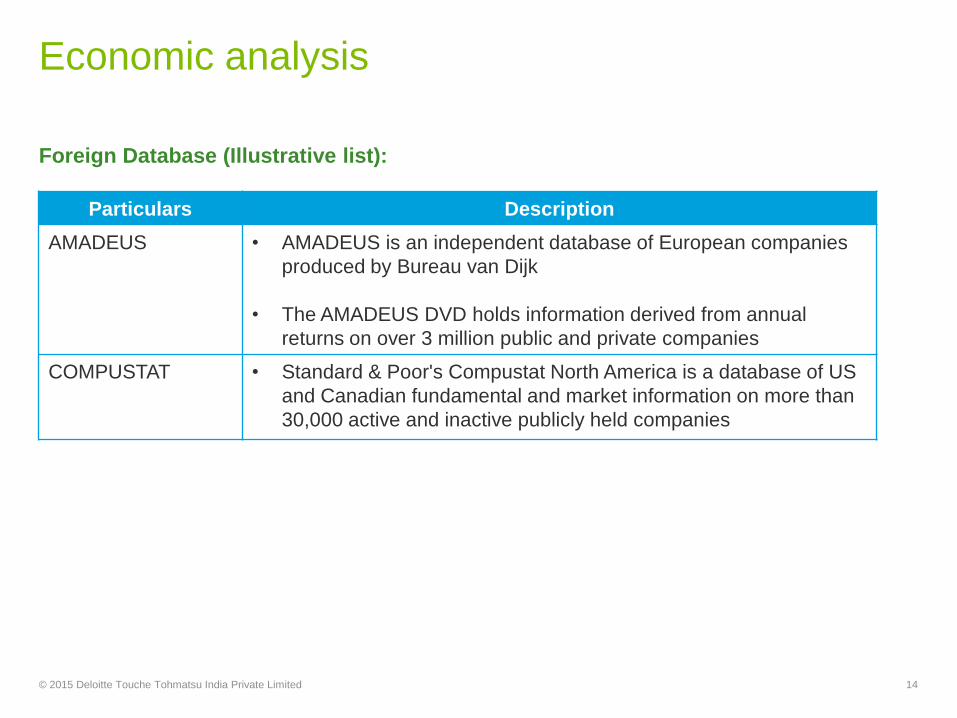

Foreign Database (Illustrative list):

© 2015 Deloitte Touche Tohmatsu India Private Limited 14

Particulars Description

AMADEUS • AMADEUS is an independent database of European companies

produced by Bureau van Dijk

• The AMADEUS DVD holds information derived from annual

returns on over 3 million public and private companies

COMPUSTAT • Standard & Poor's Compustat North America is a database of US

and Canadian fundamental and market information on more than

30,000 active and inactive publicly held companies

Background of BEPS

Project

15© 2015 Deloitte Touche Tohmatsu India Private Limited

© 2015 Deloitte Touche Tohmatsu India Private Limited

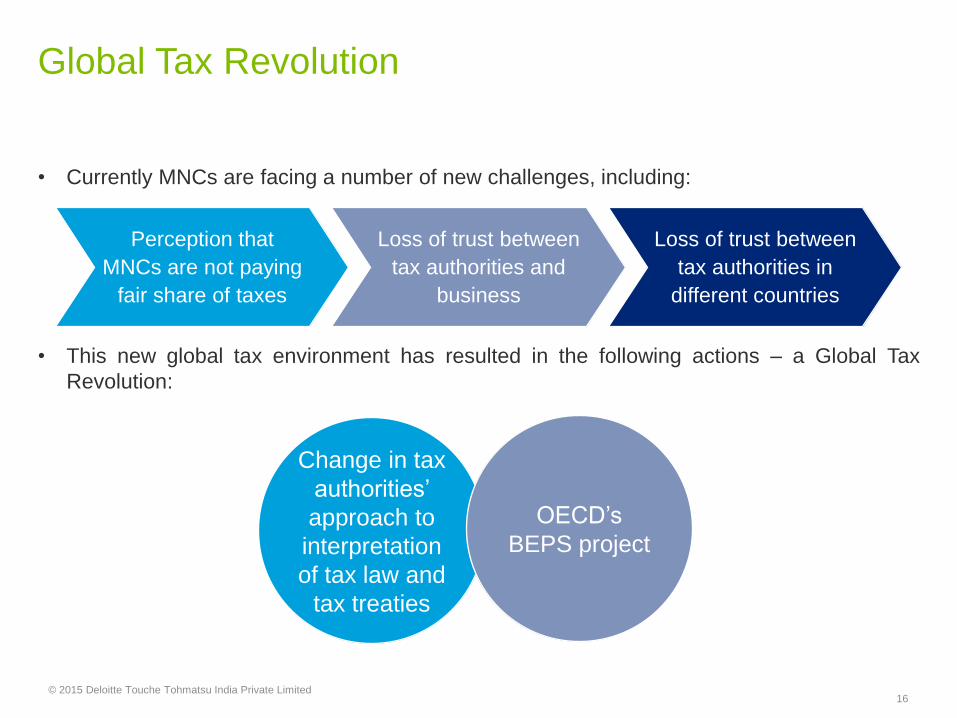

• Currently MNCs are facing a number of new challenges, including:

• This new global tax environment has resulted in the following actions – a Global Tax

Revolution:

Global Tax Revolution

Perception that

MNCs are not paying

fair share of taxes

Loss of trust between

tax authorities and

business

Loss of trust between

tax authorities in

different countries

OECD‟s

BEPS project

Change in tax

authorities‟

approach to

interpretation

of tax law and

tax treaties

Changing

behaviours of

tax authorities

re tax treaties

and tax laws

OECD‟s

BEPS project

16

© 2015 Deloitte Touche Tohmatsu India Private Limited

Introduction to BEPS

• 19 July 2013: OECD released its Action Plan in regard to Base Erosion and Profit Shifting

(BEPS), to coincide with the G20 Finance Leaders meeting in Moscow

• Action Plan:

− Is ambitious : it consists of 15 specific actions “to prevent corporations from paying

little or no tax” (OECD press release)

− Is consensus-based : it has been “signed off” (at the political level) by all 34 OECD

member countries and the 8 G20 countries which are not OECD members

− Has a relatively short timetable : all actions are to be completed by December 2015

(with many of the actions having earlier deadlines)

17

BEPS objectives: a new global tax environment

18© 2015 Deloitte Touche Tohmatsu India Private Limited

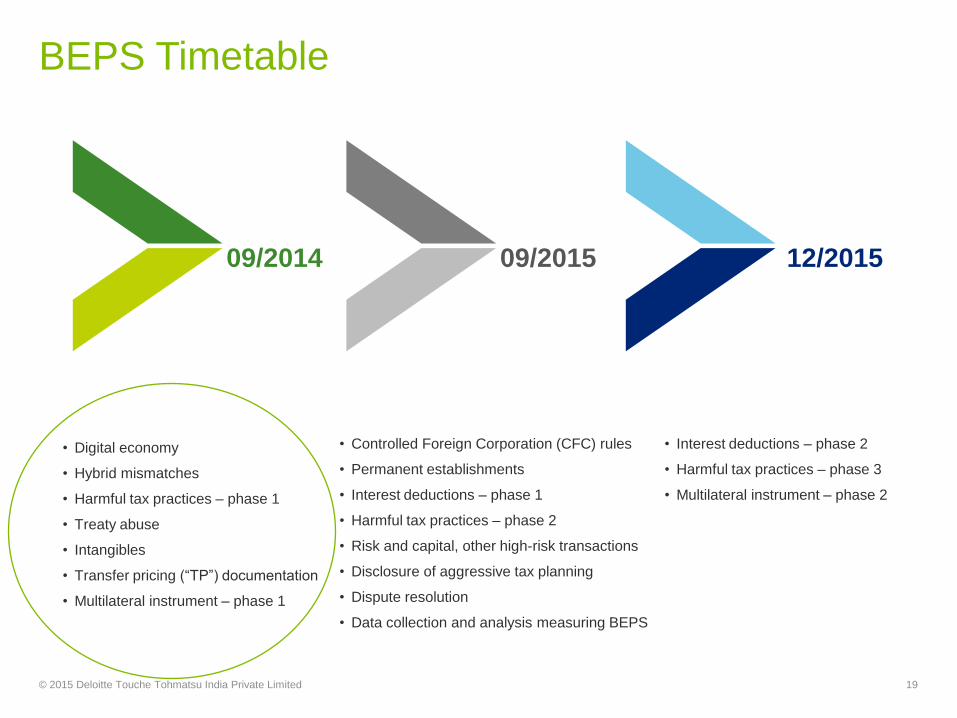

BEPS Timetable

09/2014 09/2015 12/2015

• Digital economy

• Hybrid mismatches

• Harmful tax practices – phase 1

• Treaty abuse

• Intangibles

• Transfer pricing (“TP”) documentation

• Multilateral instrument – phase 1

• Controlled Foreign Corporation (CFC) rules

• Permanent establishments

• Interest deductions – phase 1

• Harmful tax practices – phase 2

• Risk and capital, other high-risk transactions

• Disclosure of aggressive tax planning

• Dispute resolution

• Data collection and analysis measuring BEPS

• Interest deductions – phase 2

• Harmful tax practices – phase 3

• Multilateral instrument – phase 2

19© 2015 Deloitte Touche Tohmatsu India Private Limited

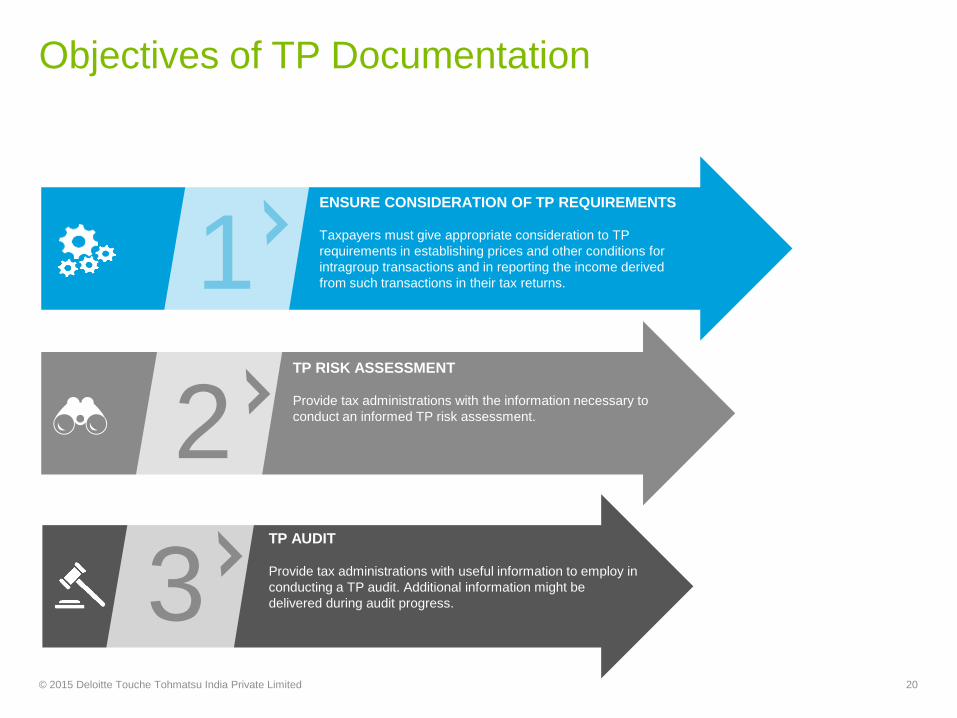

Objectives of TP Documentation

1

2

3

ENSURE CONSIDERATION OF TP REQUIREMENTS

Taxpayers must give appropriate consideration to TP

requirements in establishing prices and other conditions for

intragroup transactions and in reporting the income derived

from such transactions in their tax returns.

TP RISK ASSESSMENT

Provide tax administrations with the information necessary to

conduct an informed TP risk assessment.

TP AUDIT

Provide tax administrations with useful information to employ in

conducting a TP audit. Additional information might be

delivered during audit progress.

20© 2015 Deloitte Touche Tohmatsu India Private Limited

Proposed Compliance

Documentation

21© 2015 Deloitte Touche Tohmatsu India Private Limited

© 2015 Deloitte Touche Tohmatsu India Private Limited

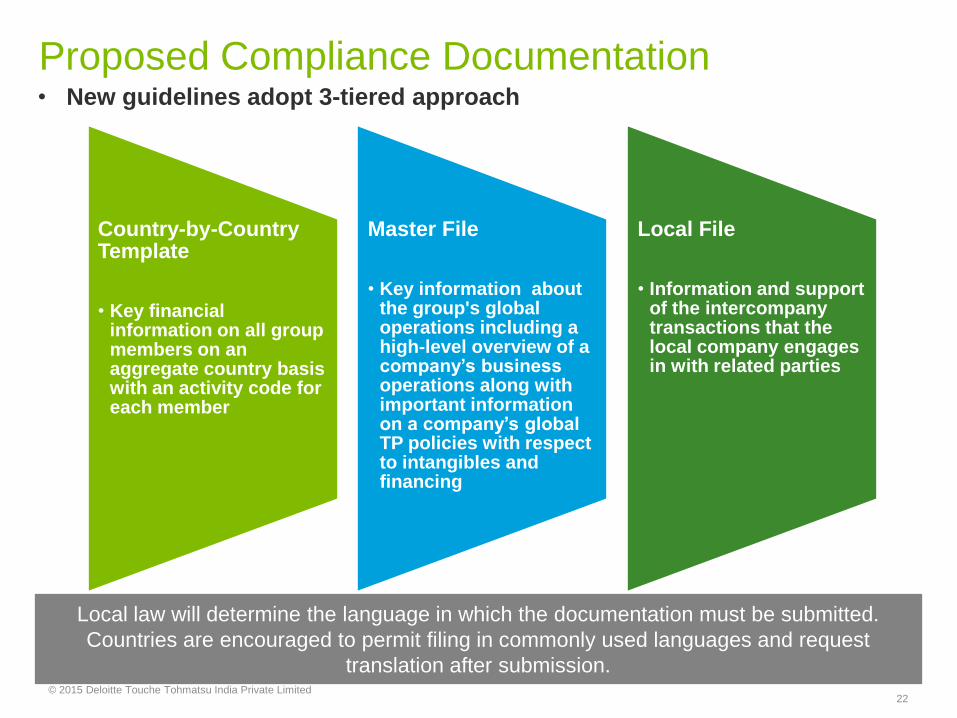

Proposed Compliance Documentation• New guidelines adopt 3-tiered approach

Country-by-CountryTemplate

• Key financial information on all group members on an aggregate country basis with an activity code for each member

Master File

• Key information about the group's global operations including ahigh-level overview of a company’s business operations along with important information on a company’s global TP policies with respect to intangibles and financing

Local File

• Information and support of the intercompany transactions that the local company engages in with related parties

Local law will determine the language in which the documentation must be submitted.

Countries are encouraged to permit filing in commonly used languages and request

translation after submission.

22

CbC Reporting &

Templates (including focus

on recent OECD Guidance)

23© 2015 Deloitte Touche Tohmatsu India Private Limited

© 2015 Deloitte Touche Tohmatsu India Private Limited

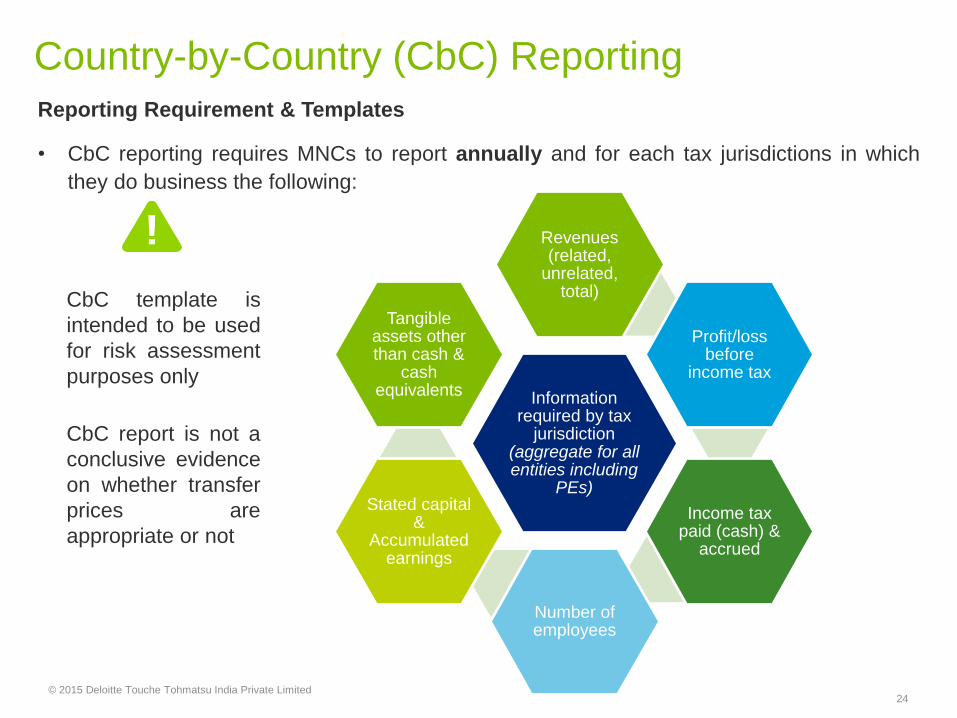

Country-by-Country (CbC) Reporting

Reporting Requirement & Templates

• CbC reporting requires MNCs to report annually and for each tax jurisdictions in which

they do business the following:

Information required by tax

jurisdiction (aggregate for all entities including

PEs)

Revenues (related,

unrelated, total)

Profit/loss before

income tax

Income tax paid (cash) &

accrued

Number of employees

Stated capital &

Accumulated earnings

Tangible assets other than cash &

cash equivalents

CbC template is

intended to be used

for risk assessment

purposes only

CbC report is not a

conclusive evidence

on whether transfer

prices are

appropriate or not

24

© 2015 Deloitte Touche Tohmatsu India Private Limited

CbC Reporting

Sources of Financial Data

• Flexibility to choose organized sources as long as source is consistently used from year

to year

− If using statutory P&L, amounts should be translated to functional currency of the

reporting company at average exchange rate for the year

• Include description of source and explanation for changes in sources

• Not necessary to reconcile revenue, profit and tax reporting in the CbC template to the

consolidated P&L

• Not necessary to make adjustments for differences in accounting principles applied

among tax jurisdictions

28

© 2015 Deloitte Touche Tohmatsu India Private Limited

CbC Reporting

Recent OECD Guidance on CbC Reporting Implementation (1/2)

• OECD on February 6, 2015 released guidance on the implementation of TP

documentation and CbC reporting. Guidance provides answers to taxpayers‟ questions

regarding the:

− timing of preparation and filing of the CbC report

− which companies will be subject to the reporting requirements

− the use of the CbC report by jurisdictions

− the mechanisms for government-to-government exchange of CbC reports

• Timing of preparation and filing:

− The first CbC reports will be required to be filed for MNE fiscal years beginning on

or after January 1, 2016.

− MNCs will be allowed 1 year from the close of the fiscal year to which the CbC

report relates to prepare and file the CbC report, the first CbC reports would be filed

by 31 December 2017.

− It should be noted that the MNE fiscal year relates to consolidated reporting period

for financial statement purposes, not to taxable years or the financial reporting

periods of individual group entities.

29

© 2015 Deloitte Touche Tohmatsu India Private Limited

CbC Reporting

Recent OECD Guidance on CbC Reporting Implementation (2/2)

• Threshold:

− The guidance requires CbC reporting by MNCs with annual consolidated group

revenues above EUR 750 million.

• Use of the CbC report by jurisdictions:

− In terms of the appropriate use of the information in the CbC report, the guidance

states that jurisdictions will commit to use the CbC report for assessing high-level

TP and other BEPS risks, but should not propose adjustments to income on the

basis of an income allocation formula based on CbC report data.

− However, jurisdictions would not be prevented from using the CbC report

information as the basis for making additional inquiries into the MNC‟s TP

arrangements, which arguably is the goal of the OCED‟s current CbC initiative.

• Mechanisms for government-to-government exchange of CbC reports:

− The countries participating in the BEPS project have agreed that they will have in

place and be prepared to enforce legal protections of the confidentiality of the

information in the CbC report equivalent to those under the Multilateral Convention

on Mutual Administrative Assistance in Tax Matters, a tax information exchange

agreement (TIEA) or a tax treaty.

30

© 2015 Deloitte Touche Tohmatsu India Private Limited

CbC Reporting

Key Considerations / Implications

• Presents organized view of where the MNC earns income and pays taxes

• Presents where people and assets are located in relation to the income earned and

taxes paid

− High priority for countries that cannot get information under current rules

− Intended for risk assessment

• Will template result in

− Value chain analysis with people and tangible assets as the driver?

− Greater use of profit splits?

− Increased emphasis on Location Specific Advantages?

− Profit comparison between countries with similar functional and risk profile?

31

Master & Local File

32© 2015 Deloitte Touche Tohmatsu India Private Limited

© 2015 Deloitte Touche Tohmatsu India Private Limited

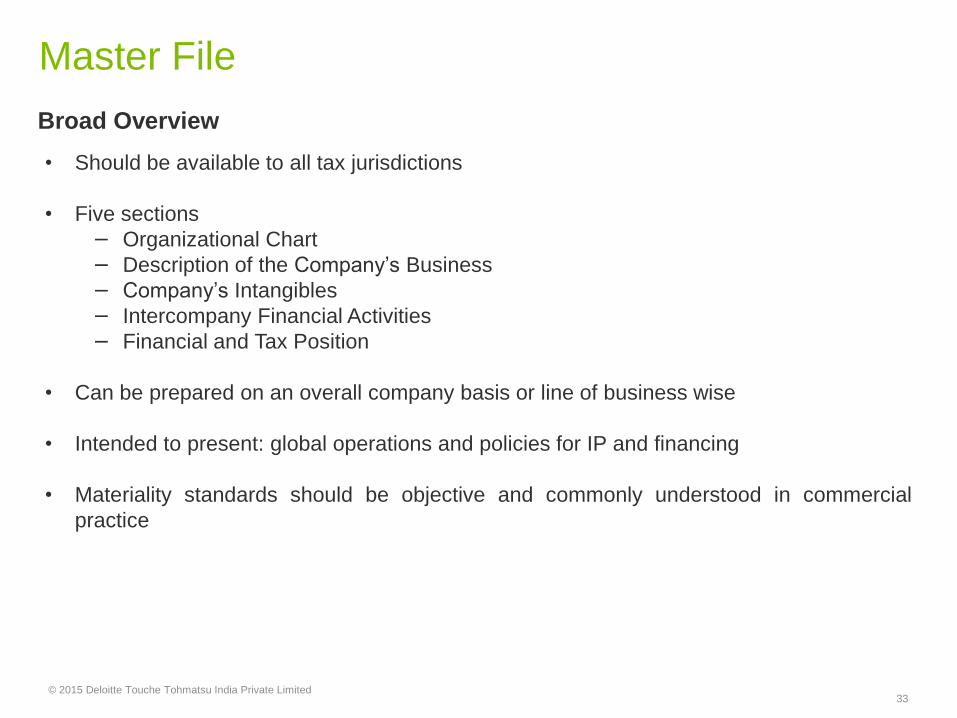

Master File

Broad Overview

• Should be available to all tax jurisdictions

• Five sections

− Organizational Chart

− Description of the Company‟s Business

− Company‟s Intangibles

− Intercompany Financial Activities

− Financial and Tax Position

• Can be prepared on an overall company basis or line of business wise

• Intended to present: global operations and policies for IP and financing

• Materiality standards should be objective and commonly understood in commercial

practice

33

© 2015 Deloitte Touche Tohmatsu India Private Limited

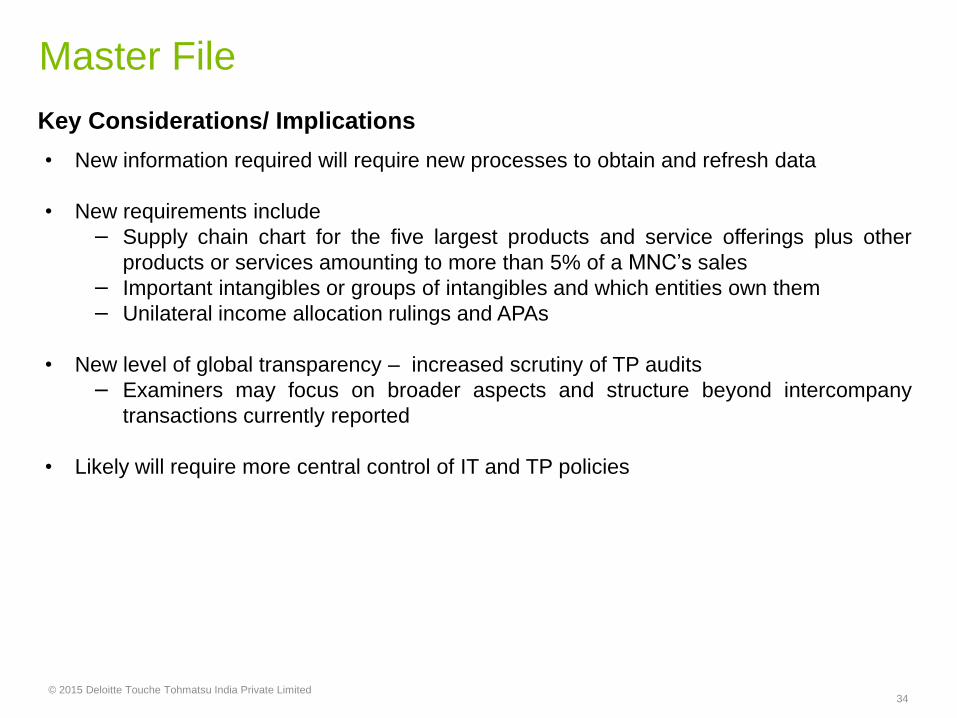

Master File

Key Considerations/ Implications

• New information required will require new processes to obtain and refresh data

• New requirements include

− Supply chain chart for the five largest products and service offerings plus other

products or services amounting to more than 5% of a MNC‟s sales

− Important intangibles or groups of intangibles and which entities own them

− Unilateral income allocation rulings and APAs

• New level of global transparency – increased scrutiny of TP audits

− Examiners may focus on broader aspects and structure beyond intercompany

transactions currently reported

• Likely will require more central control of IT and TP policies

34

© 2015 Deloitte Touche Tohmatsu India Private Limited

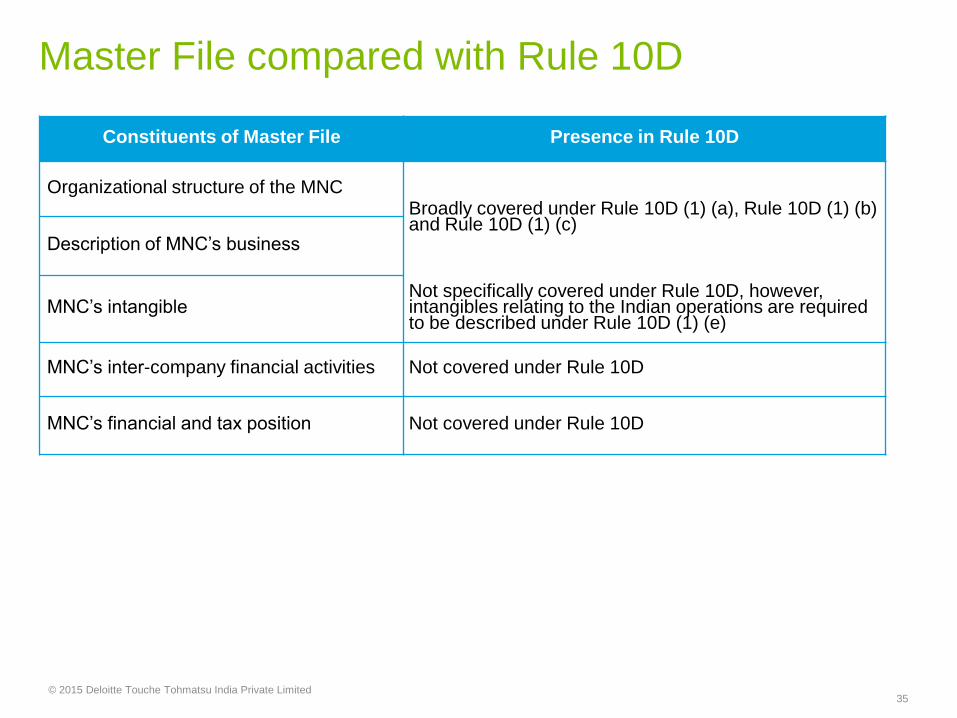

Master File compared with Rule 10D

Constituents of Master File Presence in Rule 10D

Organizational structure of the MNCBroadly covered under Rule 10D (1) (a), Rule 10D (1) (b) and Rule 10D (1) (c)

Description of MNC‟s business

MNC‟s intangibleNot specifically covered under Rule 10D, however, intangibles relating to the Indian operations are required to be described under Rule 10D (1) (e)

MNC‟s inter-company financial activities Not covered under Rule 10D

MNC‟s financial and tax position Not covered under Rule 10D

35

© 2015 Deloitte Touche Tohmatsu India Private Limited

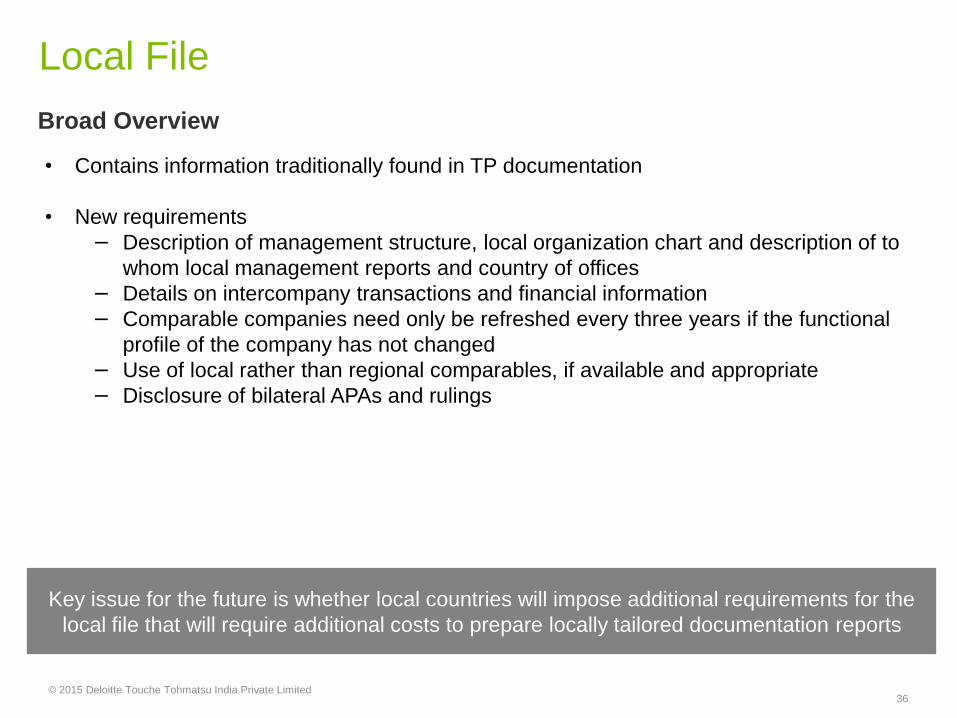

Local File

Broad Overview

• Contains information traditionally found in TP documentation

• New requirements

− Description of management structure, local organization chart and description of to

whom local management reports and country of offices

− Details on intercompany transactions and financial information

− Comparable companies need only be refreshed every three years if the functional

profile of the company has not changed

− Use of local rather than regional comparables, if available and appropriate

− Disclosure of bilateral APAs and rulings

Key issue for the future is whether local countries will impose additional requirements for the

local file that will require additional costs to prepare locally tailored documentation reports

36

© 2015 Deloitte Touche Tohmatsu India Private Limited

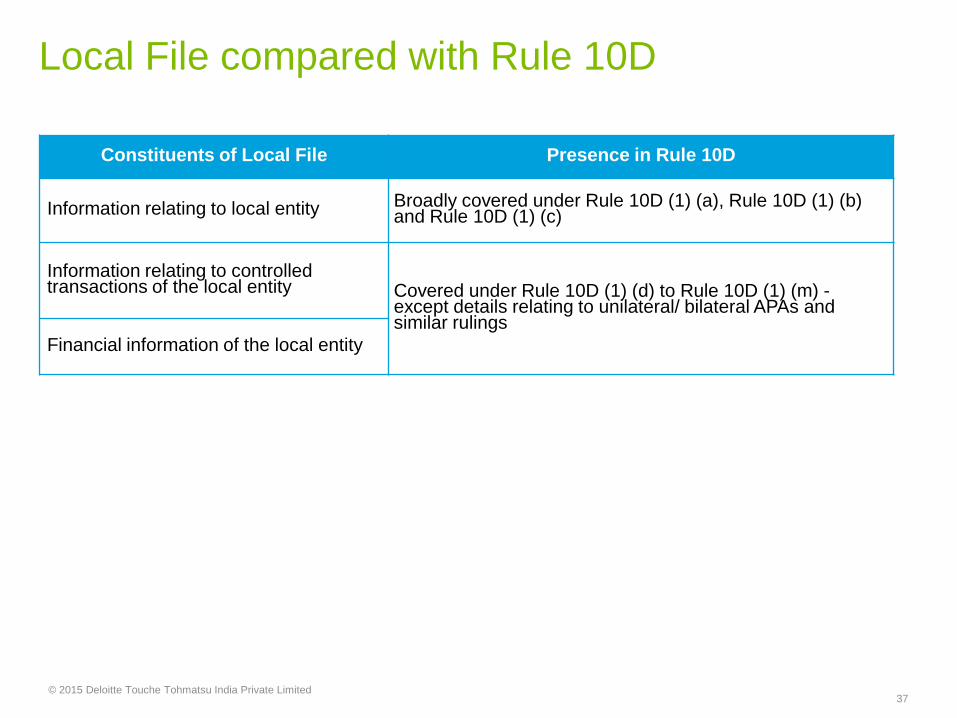

Local File compared with Rule 10D

Constituents of Local File Presence in Rule 10D

Information relating to local entity Broadly covered under Rule 10D (1) (a), Rule 10D (1) (b) and Rule 10D (1) (c)

Information relating to controlled transactions of the local entity Covered under Rule 10D (1) (d) to Rule 10D (1) (m) -

except details relating to unilateral/ bilateral APAs and similar rulings

Financial information of the local entity

37

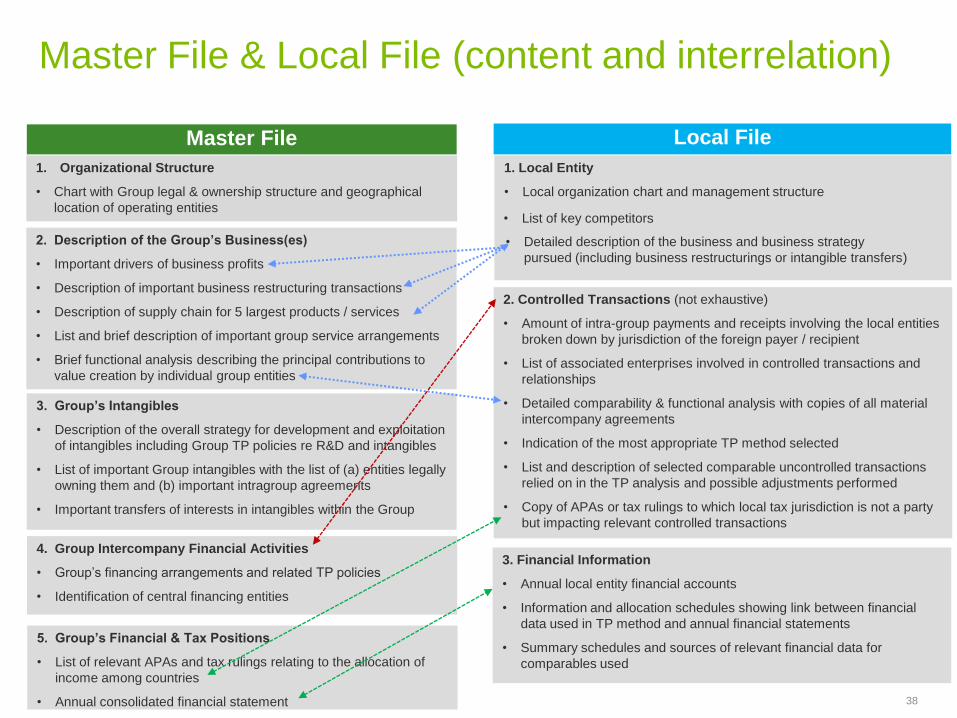

Master File & Local File (content and interrelation)

© 2014 Deloitte Tax & Consulting

Master File

1. Organizational Structure

• Chart with Group legal & ownership structure and geographical

location of operating entities

2. Description of the Group’s Business(es)

• Important drivers of business profits

• Description of important business restructuring transactions

• Description of supply chain for 5 largest products / services

• List and brief description of important group service arrangements

• Brief functional analysis describing the principal contributions to

value creation by individual group entities

4. Group Intercompany Financial Activities

• Group‟s financing arrangements and related TP policies

• Identification of central financing entities

5. Group’s Financial & Tax Positions

• List of relevant APAs and tax rulings relating to the allocation of

income among countries

• Annual consolidated financial statement

1. Local Entity

• Local organization chart and management structure

Local File

• Detailed description of the business and business strategy

pursued (including business restructurings or intangible transfers)

• List of key competitors

2. Controlled Transactions (not exhaustive)

• Amount of intra-group payments and receipts involving the local entities

broken down by jurisdiction of the foreign payer / recipient

• List of associated enterprises involved in controlled transactions and

relationships

• Detailed comparability & functional analysis with copies of all material

intercompany agreements

• Indication of the most appropriate TP method selected

• List and description of selected comparable uncontrolled transactions

relied on in the TP analysis and possible adjustments performed

• Copy of APAs or tax rulings to which local tax jurisdiction is not a party

but impacting relevant controlled transactions

3. Group’s Intangibles

• Description of the overall strategy for development and exploitation

of intangibles including Group TP policies re R&D and intangibles

• List of important Group intangibles with the list of (a) entities legally

owning them and (b) important intragroup agreements

• Important transfers of interests in intangibles within the Group

3. Financial Information

• Annual local entity financial accounts

• Information and allocation schedules showing link between financial

data used in TP method and annual financial statements

• Summary schedules and sources of relevant financial data for

comparables used

38

© 2015 Deloitte Touche Tohmatsu India Private Limited

Compliance Issues

Compliance Issues

Penalties

Confidentiality

Other Issues

Contemporane-ous

Documentation

TimeframeMateriality

Retention of Documents

Frequency of Documentation

Updates

Language

39

Deloitte refers to on or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a

legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited

and its member firms

This material and the information contained herein prepared by Deloitte Touche Tohmatsu India Private Limited (DTTIPL) is intended to provide general

information on a particular subject or subjects and is not an exhaustive treatment of such subject(s). None of DTTIPL, Deloitte Touche Tohmatsu Limited, its

member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this material, rendering professional advice or services. The information

is not intended to be relied upon as the sole basis for any decision which may affect you or your business. Before making any decision or taking any action that

might affect your personal finances or business, you should consult a qualified professional adviser.

No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this material.

©2015 Deloitte Touche Tohmatsu India Private Limited

Member of Deloitte Touche Tohmatsu Limited

40