transfer pricing in india - skpgroup.com · winner of india tax firm of the year 2016 at the asia...

TRANSCRIPT

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Transfer Pricing in India

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Evolving Transfer Pricing Regulations in India

Legislation and Trends

Critical issues in India

Advance Pricing Agreements vis-à-vis Safe Harbour Provisions

Secondary Adjustments - Rationale and Impact

New Era of Alignment and Transparency

BEPS Project Action Plans - 4, 8-10 and 13

Impact of Enhanced Documentation on MNEs

Strategies to Navigate

Future of Transfer Pricing Landscape

Key Takeaways

Our Story

Coverage

215-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Evolving Transfer Pricing Regulations in India

315-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Evolution of Transfer Pricing Regulations in India

415-11-2017

Introduction of Transfer Pricing

2001

Domestic Transfer Pricing

APA and Safe Harbour

2012

BEPS Action Plan 13

Secondary Adjustment

Safe Harbour rationalised

20172015/16

Alignment with global regulations

Easing of transfer pricing scrutiny

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

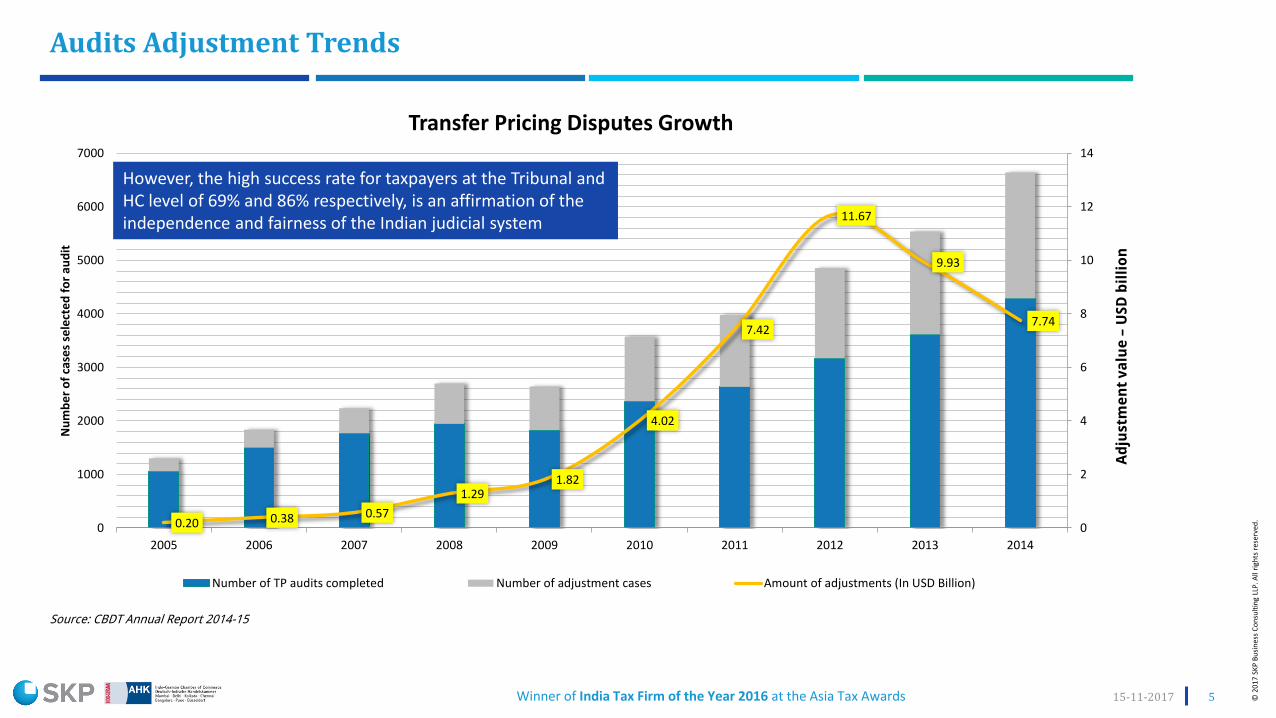

Audits Adjustment Trends

515-11-2017

0.20 0.38 0.57

1.291.82

4.02

7.42

11.67

9.93

7.74

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

1000

2000

3000

4000

5000

6000

7000

Nu

mb

er

of

case

s se

lect

ed

fo

r au

dit

Transfer Pricing Disputes Growth

Number of TP audits completed Number of adjustment cases Amount of adjustments (In USD Billion)

Ad

just

me

nt

va

lue

–U

SD

bil

lio

n

Source: CBDT Annual Report 2014-15

However, the high success rate for taxpayers at the Tribunal and HC level of 69% and 86% respectively, is an affirmation of the independence and fairness of the Indian judicial system

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

• Revenue paints all licensees of brands with same brush; seeks reimbursement of excess advertisement, marketing and sale promotion (AMP) expenses

Marketing Intangibles

• Revenue applies arbitrary commission, resulting in supernormal operating profits on cost

Procurement, Marketing Functions and PE Issues

• Revenue inflicts high profits margins for contract R&D, IT, ITES, and KPO service providers

Contract Service Providers

• Revenue imputes guarantee fees charges based on credit worthinessInbound Corporate Guarantees

• Revenue challenges the actual receipt of services as well as the benefit of the same Intra-Group Services

Critical Transfer Pricing Issues in India

615-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Advance Pricing Agreements

715-11-2017

Concept of Advance Pricing Agreements (APA) introduced in India by the Finance Act, 2012

Average time for conclusion of unilateral APA is around 1.5 - 2 years (as compared to global standard of around 3 years)

More than 800+ applications have been filed till date - 90% of pre-filing applications got converted to ‘formal’ APA

applications and 85% of the applications are for unilateral APA

APAs concluded so far pertain to various segments like captive service centres in India, manufacturing activities,

telecommunication services, oil exploration services, management cross charges, healthcare, media, etc.

184 APAs concluded till Nov 2017, including 13 bilateral APAs – 5 with Japan, 8 with United Kingdom

Indian Revenue has clarified that absent the provisions of corresponding adjustment in TP matters (generally embodied

in Article 9(2) in any tax treaty) India shall not entertain any bilateral APA with respect to transactions involving such

country

Future of Indo-German Bilateral APA is hanging absent corresponding transfer pricing adjustments clause in the DTAA

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

APA Filing Key Statistics | 2012-13 (FY) – 2016-17 (FY)

5 4

55

88

152

5 3

53

80

141

0 1 28 11

0

20

40

60

80

100

120

140

160

2013 2014 2015 2016 Total

Total APA Unilateral APA Bilateral APA

815-11-2017

Year 1 | 2013 Year 2 | 2014 Year 3 | 2015 Year 4 | 2016 Year 5 | 2017

146 Applications 232 Applications 206 Applications 132 Applications 99 Applications

117 U 192 U 14 B 113 U 19 B 78 U 21 B29 B 206 U 26 B

To

tal

AP

As

Sig

ne

d

Source: Annual Report 2016-17 – Ministry of Finance

AP

As

Fil

ed

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Safe Harbour Rules

915-11-2017

Introduced in 2013, original safe harbour rules hardly received any positive response as compared to the phenomenalsuccess of Advance Pricing Agreement (APA)

Taking a cue from the above there was a rationalisation to the Safe Harbour Rules in 2017

Eligible Transaction Earlier Safe Harbour Revised Safe Harbour

Software Development and ITeS 20.00% - 22.00% 17.00% - 18.00%

Knowledge Process Outsourcing 25.00% 18.00% - 24.00%

Intra-Group LoansSBI Base Rate + (150-300 b.p.) SBI Base Rate + (175 – 425 b.p.)

6m LIBOR + (150 – 400 b.p.)

Corporate Guarantee 1.75% - 2.00% 1.00%

Research and Development Services 29.00% - 30.00% 24.00%

Manufacture and Export of Auto Components 8.50% - 12.00% 8.50% - 12.00%

Low Value Intra-Group Services NA 5.00%

Revised Safe Harbour provisions are made applicable with a upper turnover threshold of USD 31 million for all contract services

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Implications of Reduced Safe Harbour Rates vis-à-vis APAs

1015-11-2017

Putting a threshold for eligibility – revised safe harbour is meant to benefit SME contract service provider entities

Tax authorities can now concentrate more on complex and high-value transactions under APAs and for scrutiny -considering the risk based assessment selection

Offering a safe harbour for low value adding intra-group services – one of the most litigation prone transactions is a positive move and it seems to be in line with the BEPS Action Plan 8-10

However, considering various excluded services there is still caution/clarification required in this area

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Secondary Adjustments

1115-11-2017

Once Secondary Adjustment Provisions are triggered the Indian Co. is required to ensure the primary adjustment is recovered from the AE within the time limit

Interest to be imputed in case of failure to repatriate within the time limits mentioned above

Nature of Primary Adjustment Time Limit for Repatriation

Suo-moto adjustment made in return of income

90 days from the due date of filing of a return of income

Advance Pricing Agreement (APA) entered

Safe Harbour Rule (SHR) exercised

Mutual Agreement Procedure (MAP) entered under a Double Taxation Avoidance Agreement (DTAA)

Transfer Pricing Adjustment made by the relevant authority in the relevant order90 days from the date of order (order by the assessing officer or the relevant appellate authority)

Currency of International Transaction Interest Base Rate Spread Effective Interest

Indian Rupee 1 year marginal cost of funds (for SBI Lending Rate) 325 basis points 11.25% p.a.

Foreign Currency 6-month London Inter-Bank Offered Rate (LIBOR) 300 basis points 4.42% p.a

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Secondary Adjustments

1215-11-2017

Indian entity renders captive marketing and sales support services for the group

Remuneration in the form of commission based on percentage of sales.

Indian entity net results are losses – unable to achieve desired levels of sales

Comparable third party commission arrangements not available in the group

Set of comparable sales support companies in India showing a net 8-10% profits

In order to continue with the arrangement and to avoid falling under the ambit of secondary adjustment provisions in India, the group would need to decide whether it should:

1. Increase the commission rate so that Indian entity reaches to an arm’s length rate of margins

2. Record the increased commission income as a receivable in the books of accounts itself

3. Re-evaluate the remuneration model for future years – commission based to cost plus basis, depending specific facts of the case

Overseas Parent Co.

Indian Subsidiary

Providing marketing and sales support services on commission basis

Relook inter-company transactions for the presence of any potential primary adjustments (non arm’s length conditions) and determine the consequential impact of secondary adjustments

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

New Era of Alignment and Transparency | BEPS Project

Action Plan 4 Limiting Interest Deductions Action Plan 8-10 Aligning Value CreationAction Plan 13 CbCR

1315-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Applicability

From AY 2018-2019 (Section 94B Introduced)

Applicable to Indian Companies and Indian Permanent Establishments (PE) of foreign entities

Not Applicable to companies engaged in banking and insurance

Applicable for debt extended by foreign related party; or by third party lender (if backed by implicit or explicit guarantee given; or deposit placed, by foreign related party)

Restricts deduction in respect of expenditure by interest (or of similar nature) paid to non-resident associated entities to 30% of EBITDA (earning before interest, taxes, depreciation and amortisation)

Threshold limit: interest expenditure exceeds USD 0.16 million

Interest over the 30% limit could be carried forward and set-off for up to 8 subsequent years

Action Plan 4 | Limiting Interest Deductions (India’s Perspective)

1415-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Limiting Interest Deductions (Computation Mechanism for Disallowance)

1515-11-2017

Set-Off of Excess Interest – whether treatment same as un-absorbed depreciation or carried forward loss?

Particulars Scenario 1 Scenario 2 Scenario 3 Scenario 4

EBITDA 100 100 100 -100

30% of EBITDA (a) 30 30 30 NA

Interest paid to AE (b) 15 20 20 10

Interest paid to Non-AE (c) 25 40 10 10

Total Interest (d=b+c) 40 60 30 20

Total Interest in excess of 30% of EBITDA

10 30 0 20

Excess Interest to be disallowed and carried forward (lower of b or e)

10 20 0 10

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Action Plans 8 to 10 | Aligning Transfer Pricing with Value Creation

1615-11-2017

India’s stand on economic activity based transfer pricing gets further strengthened

‘Aligning rewards with the actual conduct’ and ‘substance over form’ have been raised by revenue authorities and adjudicated by the tax tribunals in India

More focus on intangibles – returns generated should be correctly shared with companies who in reality perform value adding functions or bear the actual risks in development of those intangibles

Transfer pricing cannot remain a merely principle driven tax compliance activity any more. It will touch upon the entire domain of the business, starting from the strategy to the ground level operations.

Business arrangements would need a close evaluation:

Captive high end R&D services in India remunerated on cost plus basis

Limited Risk Distribution in India, remunerated with a guaranteed low level margins

Indian distributor performing excessive brand building and not getting remunerated from the group for such activities

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Action Plan 13 and Enhanced Documentation Requirement

1715-11-2017

Indian Transfer Pricing Regulations introduced a three-tiered standardised approach to documentation in lines with Action Plan 13

of BEPS (w.e.f. FY 16-17) under Section 92D and Section 286 of the Income Tax Act 1961

• Local country TP documentation

• To be prepared by each local entity and submitted to local Tax Authority

• In place in India since 2001

Local File

(Rule 10D)

• High level blue print of multinational group’s global operations

• Contents like value drivers, supply chain model, Intangibles details, Group financing, etc.

• Prepared centrally; submitted with Tax authorities of all countries

• Ideally prepared by ultimate parent for consolidation

Master File

(Rule 10DA)

• Multinationals having consolidated annual revenue > Euro 750 million

• Summary data and economic activity in each country

• Prepared by ultimate parent for consolidation purposes

• Submitted with tax authority of ultimate parent

• Shared with other tax authorities through automatic exchange of information

CbC Report

(Rule 10DB)

Penalties for non-compliance are huge

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Master File (u/s 92D - Rule 10DA)

1815-11-2017

Master FileOrganisational

Structure

Description of Group’s

business (es)

Group’s important

profit drivers

Intangible property

strategy and policy

Intercompany financial

activities and policy FAR of key

group entities

Description of Supply chain

Group’s financial and tax positions

Effective date- 1st April 2016 (applicable for FY 2016-17 and onwards) Threshold:

1) Consolidated group revenue > INR 500 Cr (Euro 65.4 Mi.); AND

2) Aggregate value of international transactions > INR 50 Cr (Euro 6.5 Mi.) ORTransactions related to intangible property > INR 10 Cr (Euro 1.3 Mi.)

Compliance:

1) Filing in Form 3CEAA (Part A &

B) by 30th November (for FY

16-17 it is 31st Mar 2018)

2) Intimation in Form 3CEAB

(1 March 2018)

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Country by Country Reporting (u/s 286 - Rule 10DB)

1915-11-2017

CbCR

Overview of allocation of income,

taxes and business activities (no of employees and

tangible assets)- tax jurisdiction wise

List of all constituent entities including

main business activity – tax jurisdiction wise

Additional information

Effective date- 1st April 2016 (applicable for FY 2016-17 and onwards) Threshold:

Consolidated group revenue > INR 5500Cr (Approx. Euro 750 Mi.)

Compliance:

1) Intimation in Form 3CEAC (31 Jan

2018)

2) Filing in Form 3CEAD by 30th

November (for FY 16-17 it is 31st Mar

2018)

3) Intimation in Form 3CEAE for

multiple constituent group entities in

India No timeline mentioned in the

rules. It needs to be clarified by the

CBDT.

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Entire global scope is present before the Indian tax authority – would lead to more questions and detailed enquiries at the time of audit

Migrating from old transfer pricing requirements (country specific documentation) to new requirements could be daunting – initial years are crucial

In cases where Master File has been prepared for other jurisdiction, aligning the same with Indian requirements

Uncertainties over tax authorities’ approach on rise

Increased disclosure will have impact on other tax areas – treaty benefits, PE profit attributions, anti-abuse provisions

Countries (such as India) where on ground quantum are huge (market size, human resources, customer/vendor base) would gain more force

Combined Contents of Master File and CbCR having far reaching implications

Sum of the parts is more powerful than individual parts

Enhanced Documentation Requirement | Impact on MNEs Operating in India

2015-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Positives

Opportunity to streamline transfer pricing policies, processes and documentation

Opportunity for tax optimisation, if there are present leakages

Bringing in efficiency – avoiding duplications, efficient benchmarking and updations

Help in explaining the group transfer pricing story to aggressive tax jurisdictions

Inputs for business strategic decision making

Approaching the reality – there are positives also

Enhanced Documentation Requirement | Impact on MNEs Operating in India

2115-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Potential questions from Revenue authorities after perusing Master File / CbCR

Inbound Arrangements

Enhanced Documentation Requirement | Impact on MNEs Operating in India

2215-11-2017

Scenario Potential Questions

Payment of royalty by Indian subsidiary

Whether entity charging royalty is actually carrying out any economic activity [Development, Enhancement, Maintenance, Protection, Exploitation (DEMPE) functions]?

Whether Indian entity received any economic benefit from availing the brand/technology

Contract R&D/captive services rendered by Indian subsidiary

More enquiries on following aspects:- Department wise bifurcation of employees- Qualification of employees- Services defined under inter-company agreement- Role played by Indian entity in entire value chain

Whether remuneration for the Indian entity matches with the FAR contribution it makes? Profit split more suitable?

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Strategies for Initial Preparedness

Prepare group’s global map and plot transfer pricing legal requirements in each individual country

Determine applicability of CbCR and master file for every group entity

Define roles and responsibilities within the group to comply with country specific and group level requirements

Perform skill gap analysis – in-house capabilities and transfer pricing specialist help

Evaluate the preparedness of data collation systems in the group

Define a system for real time/periodic monitoring of data

Prepare a calendar for compliances, transfer pricing benchmarking searches and updates

Enhanced Documentation Requirement | Strategies to Navigate

2315-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Strategies to Mitigate Risk and Being Future Ready

Appropriate interpretation of group wide data collated

Perform what-if analysis for the potential questions/inquiries from the tax authorities

Make appropriate changes in the transfer pricing policy, where required

Define a system to gather real time evidences that will support the policy - developing justifications

Design a system of regular communication between tax teams and business strategy/operations team

Systems in place to track additional information i.e. addition of new entity in the group, supply chain changes, etc.

Give a harmonised picture between

CbCR, Master file, and local files

Year-on-Year disclosures in transfer pricing documentation

Aim for a fine balance between

Protect trade secrets and provide sufficient information

Standardisation and customisation

Enhanced Documentation Requirement | Strategies to Navigate

2415-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Use of technology for collation of data and use of data analytics for transfer pricing risk detection

Collating information through exchange of information and coordinated audit by representatives from two or more jurisdictions

Tax and business and operations team should work in sync as there could be use of subject matter expert witnesses during audit

Not to treat transfer pricing as year end compliance exercise

Having substance based transfer pricing policy with emphasis on establishing fundamentals of transfer pricing instead of legal arguments

Reviewing inter-company transfer pricing policy on regular intervals

Evaluating option of Advance Pricing Agreements

Seeking timely advice of transfer pricing experts

Transfer pricing documentation is no more a standard data driven exercise. It is designing and telling a story.

Enhanced Documentation Requirement | Future of Transfer Pricing Landscape

2515-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Key Takeaways

2615-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Plot and re-look at shareholding and operating structure of your group

Having a tax-efficient transfer pricing policy for the group as a whole

Adequate implementation of the transfer pricing policy

Impact of transfer pricing policy on other areas

Ensure coherence and compliance of local and global laws

Required enhanced documentation in place – on ground details would be crucial

Timely assessment of transfer pricing risks for any change in the business and taking measures to mitigate the same

Key Takeaways

2715-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Our Story

2815-11-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

SKP Today

2915-11-2017

The contents of this presentation are intended for general marketing and informative purposes only and should not be construed to becomplete. This presentation may contain information other than our services and credentials. Such information should neither beconsidered as an opinion or advice nor be relied upon as being comprehensive and accurate. We accept no liability or responsibility to anyperson for any loss or damage incurred by relying on such information. This presentation may contain proprietary, confidential or legallyprivileged information and any unauthorised reproduction, misuse or disclosure of its contents is strictly prohibited and will be unlawful.

DisclaimerMumbai

Pune

Hyderabad

New Delhi

Chennai

Bengaluru

Toronto

Chicago

Dubai

Connect with us

Subscribe

www.skpgroup.com

SKP Business Consulting LLP is a member firm of the "Nexia International" network. Nexia International Limiteddoes not deliver services in its own name or otherwise. Nexia International Limited and the member firms of theNexia International network (including those members which trade under a name which includes the wordNEXIA) are not part of a worldwide partnership. For the full Nexia International disclaimer, please click here.

Icons designed by Freepik © 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

3015-11-2017