transfer pricing landscape in india an update - amazon...

TRANSCRIPT

© 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co.

18 December 2009

Transfer Pricing landscape in IndiaAn Update

ICAI - SIRC, Chennai

B S R & Co.

2B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Setting the Context

Snapshot on Indian Regulations

Existing and Emerging Controversies

Recent Judicial Rulings

Finance Act 2009 - Amendments

Direct Tax Code - Proposals

010101

020202

030303

040404

050505

060606

© 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co.B S R & Co.

3B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

What are tax heads worried about

Transfer Pricing emerging as the single largest tax risk facing Transfer Pricing emerging as the single largest tax risk facing MNCs todayMNCs today

Withholding taxWithholding tax

Permanent establishment issuesPermanent establishment issues

DTAADTAA

Indirect taxIndirect tax

Provident fundProvident fund

4B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

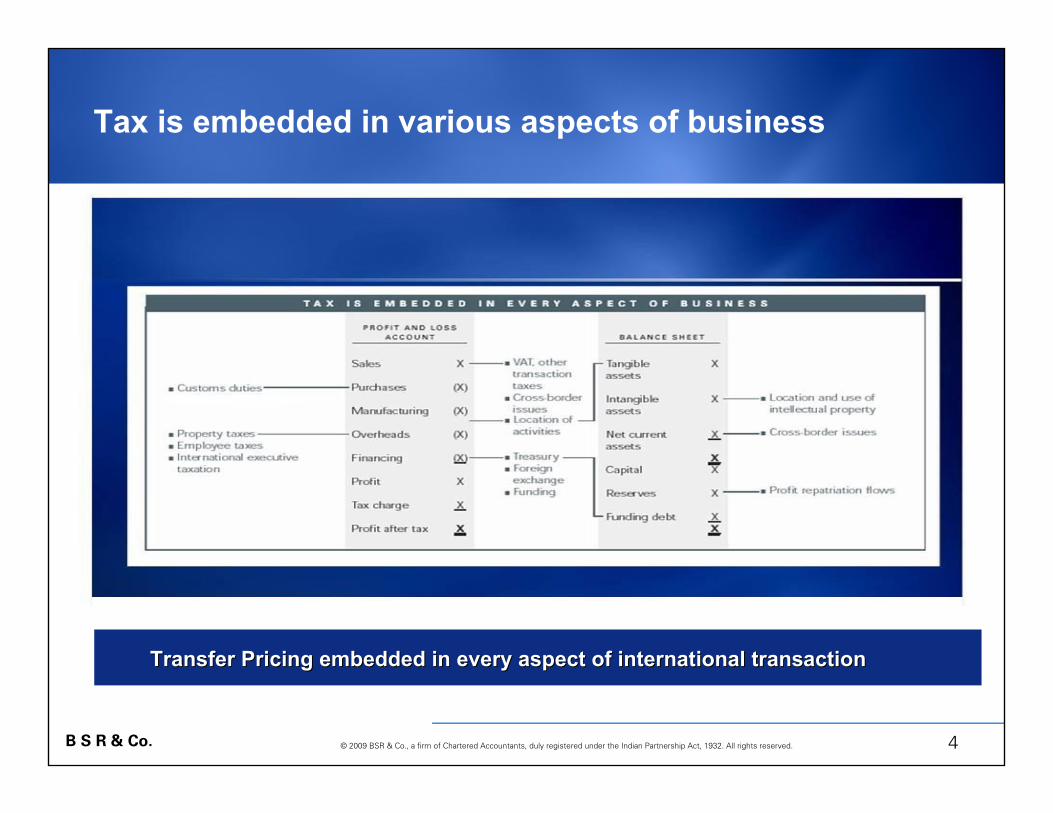

Tax is embedded in various aspects of business

Transfer Pricing embedded in every aspect of international transTransfer Pricing embedded in every aspect of international transaction action

5B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Toughest Tax authorities for Transfer Pricing

UK

Canada

China

Korea

India

France

Australia

Japan

Germany

USA

India and China are expected to top the charts soon

6B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Transfer Pricing In India

© 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co.

7B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Snapshot of Indian Transfer Pricing Regulations

Relatively new legislation - Introduced with effect from April 1, 2001

International transactions between associated enterprises need to satisfy the arm’s length criterion (ALP - price applied between independent enterprises in uncontrolled conditions)

Compliance Requirementsi. Maintenance of contemporaneous documentation (to

substantiate ALP)ii. Annual filing of Accountant’s Report (Form 3CEB)

Steep Penalties – Can be upto 3 times the tax sought to be evaded

Concept of Arithmetic mean

Limited judicial precedence

Assessment procedure stringent

8B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Approach to Transfer Pricing

Typical International Transactions:Import of components; Payments towards technology support; Export of finished products, Reimbursement of expenses

Remuneration based on FAR analysis:Assists in economic characterization and determination of compensation

Most Appropriate Method (MAM):To be used for testing arm’s length Price

• Aggregative approachBenchmarking in public databases required to analyse the arm’s length margin earned by comparable independent companies

• Transaction specific approachTransactions such as technical payouts, management fee cross charges Cost benefit analysis necessary

Net Profit Margins

Analysis allocation of profit / loss

GPM (on costs) benchmarked

GPM (on sales) benchmarked

Prices of each transaction is benchmarked

Approach

Manufacturing & Service functions – Product comparability not critical

Transfer of Intangibles or multiple transactions

Service function; Contract manufacturing

Distribution Function

Direct method – Product comparability critical

Functions

Profit Split

Transactional Net Margin (TNMM)

Cost Plus

Resale Price

Comparable Uncontrolled Price (CUP)

Method

Analysis of prescribed methods

9B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Why do you need aTransfer Pricing documentation in India?

...Tax Exposure

Provision

...

Strengthen the Appeal

Legal Requirement

Burden of proof

Penalty Protection

© 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co.

10B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

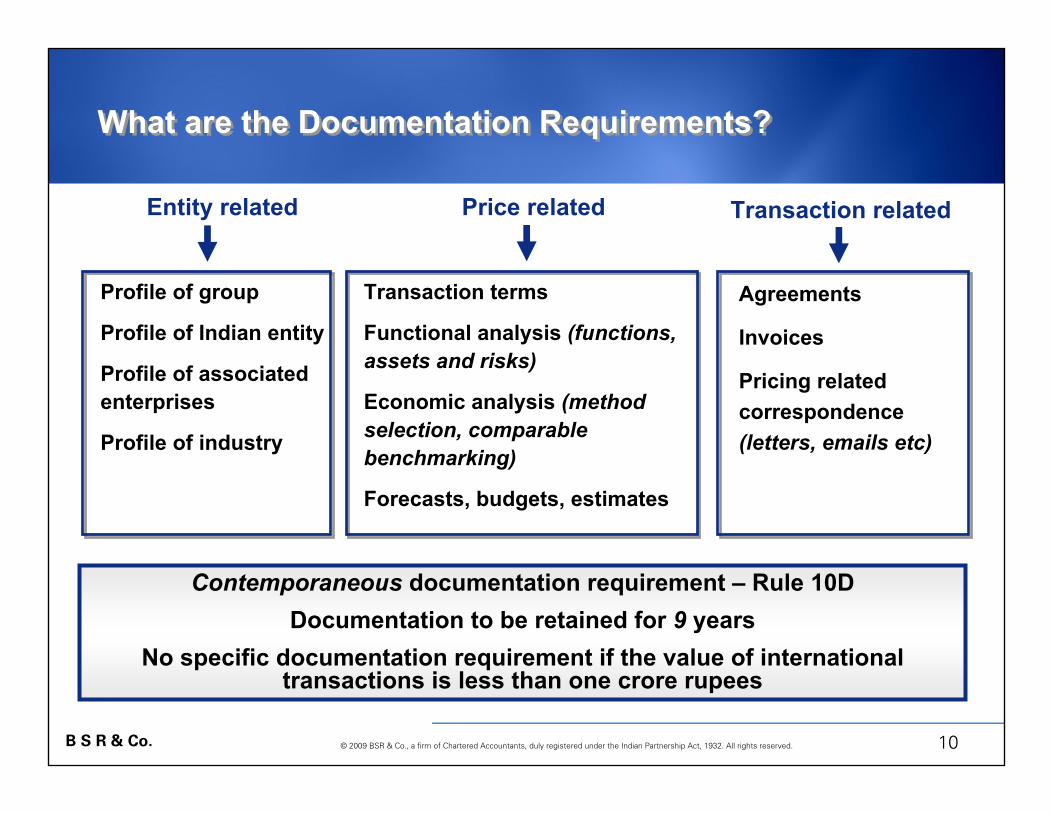

Entity related Price related Transaction related

Profile of group

Profile of Indian entity

Profile of associated enterprises

Profile of industry

Transaction terms

Functional analysis (functions, assets and risks)

Economic analysis (method selection, comparable benchmarking)

Forecasts, budgets, estimates

Agreements

Invoices

Pricing related correspondence (letters, emails etc)

Contemporaneous documentation requirement – Rule 10D Documentation to be retained for 9 years

No specific documentation requirement if the value of international transactions is less than one crore rupees

What are the Documentation Requirements?What are the Documentation Requirements?

11B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

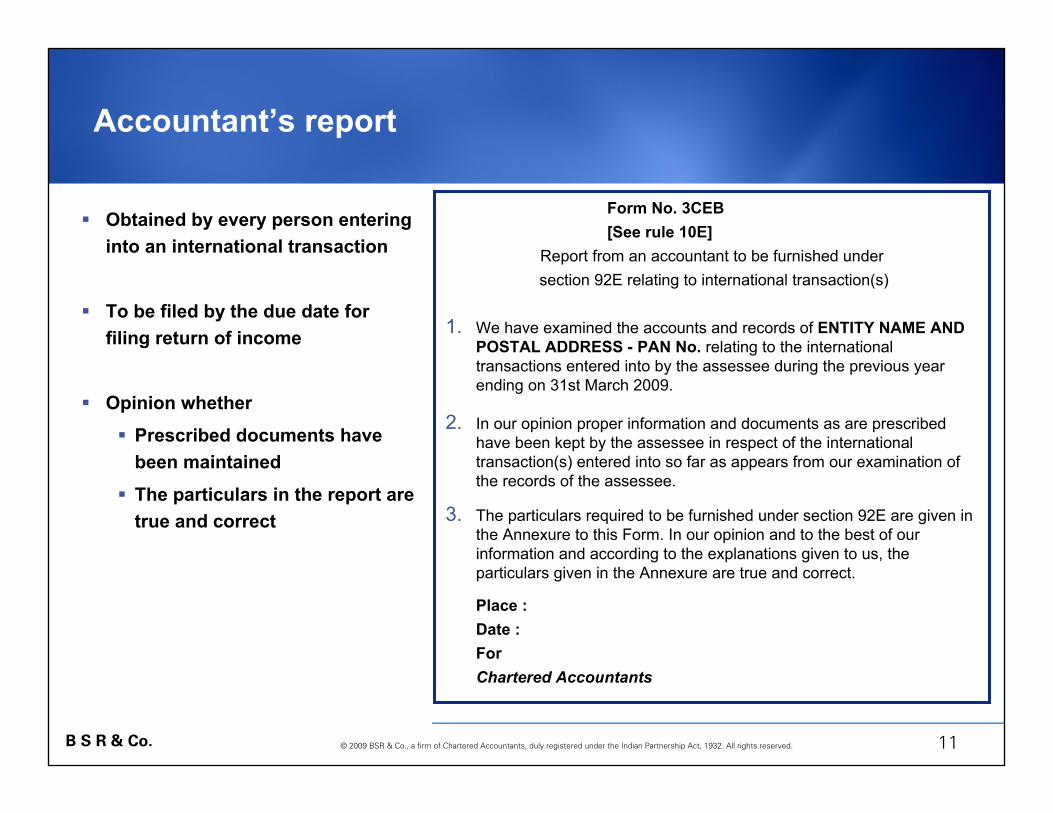

Accountant’s report

Obtained by every person entering into an international transaction

To be filed by the due date for filing return of income

Opinion whetherPrescribed documents have been maintainedThe particulars in the report are true and correct

Form No. 3CEB [See rule 10E]

Report from an accountant to be furnished undersection 92E relating to international transaction(s)

1. We have examined the accounts and records of ENTITY NAME AND POSTAL ADDRESS - PAN No. relating to the international transactions entered into by the assessee during the previous year ending on 31st March 2009.

2. In our opinion proper information and documents as are prescribed have been kept by the assessee in respect of the international transaction(s) entered into so far as appears from our examination of the records of the assessee.

3. The particulars required to be furnished under section 92E are given in the Annexure to this Form. In our opinion and to the best of ourinformation and according to the explanations given to us, the particulars given in the Annexure are true and correct.

Place :Date :ForChartered Accountants

12B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Compliance Compliance -- A step by step approachA step by step approach

Financial AnalysisInternal

Accountants’ Report Documentation

External

Functional, Assets & Risk Analysis

Comparable Analysis

Choice of Appropriate Method

Profit Level Indicator

13B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

• Preparation of project plan • Search strategy

• Access to local & global database

• Analysis of internal comparables

• Judicious identification of arm’s length range

• Understand existing costing mechanism

• Determination of billing methodology

Pre-project planning

Stage 2Stage 3

Stage 4

Functional analysis -

Information gathering

Comparable data /

Industry Analysis

Economic Analysis

• Interviews• Questionnaires

• Discussions with Management

• Characterisation of each entity

• Agreement reviews

Stage 5

• Consultation with management

• Finalization of Transfer pricing documentation

Issuance of Transfer Pricing Documentation

Stage 1

Key to dos before finalizing Documentation

Two Key analysis

14B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Systematically meeting the transfer pricing challenge ...

Transfer Pricing Rules & Regulations

Global / Local Transfer Pricing Team

Man

agem

ent S

uppo

rt Policy /Business Model

TP DocumentationCentral Core Country

AgreementsTangiblesFinancing

IntangiblesServices

Systems / Operating ProceduresIT

Price SettingCost Allocation

Value Chain

Day-to-Day OperationsInvoicing

DocumentationAccounting

Communication

15B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Maintenance of Transfer Pricing Documentation Statute of Limitation – An illustration – March 2009

Section 92D and Rule 10D(5)

Date till which documentation is required to be maintained

31 Mar 20187

Section 149(1)(b)Limitation for reassessment (where income escaping assessment is equal to or greater than INR 100,000)

31 Mar 20166

Section 149(1)(a)Limitation for reassessment (where income escaping assessment is less than INR 100,000)

31 Mar 20145

Second Proviso to Section 153(1)

Limitation for completion of tax audit (scrutiny by the Assessment Officer)

31 Dec 20124

Section 92CA(3A) read with Second Proviso to Section 153(1)

Limitation for completion of the transfer pricing audit (scrutiny by the Transfer Pricing Officer)

31 Oct 20123

Proviso to section 143(2)(ii)Limitation for initiating a transfer pricing audit by the tax administration

30 Sep 20102

Section 139(1) read with Section 92E

Deadline for maintaining documentation, filing tax return and accountant’s report

30 Sep 20091

Relevant Provision Compliance Timeline S.No.

16B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Transfer Pricing Priorities - Today

Compliance• Documentation Penalty

• Filing and Disclosure of RPT

• Compliance Costs

• Internal / External Audit

Planning • Loss Utilization

• Foreign Tax Credits

• Intellectual Property

• Business Restructuring

Controversy • Assessments

• Advance Pricing Agreements

• Litigation

• DRP / CIT (A)

• ITAT

• HC

• SC

Operations• Tax Efficient Supply Chain

Management (TESCM)

• Process Benchmarking

• Capital Efficiency

17B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Transfer Pricing Controversy In India Current and Future Issues

© 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co.

18B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

TP Audit

Audit Process

File tax return and Accountant’s Report (30th September)

Reference to be made to TP Officer (‘TPO’) by the Assessing Officer (‘AO’); Compulsory Reference to be made by AO

if international transactions exceed INR 150 million for AY 2005-06 onwards (Internal guidelines)

Appeal can be made against the order of AO as order of

TPO included within the order of the AO

Notice to be issued by the TPO – TPO calls for supporting documents and evidence

Rectification application can bemade against the order of TPO

for apparent mistakes

Based on results of above mentioned procedure assessing officer passes the order

Appeal Procedure

Appeal to Commissioner of Income Tax

Passes an order

Income Tax Appellate Tribunal

High Court – only on matters related to law

Supreme Court

Constitutional Bench

DRP Mechanism-Finance Act 2009

19B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

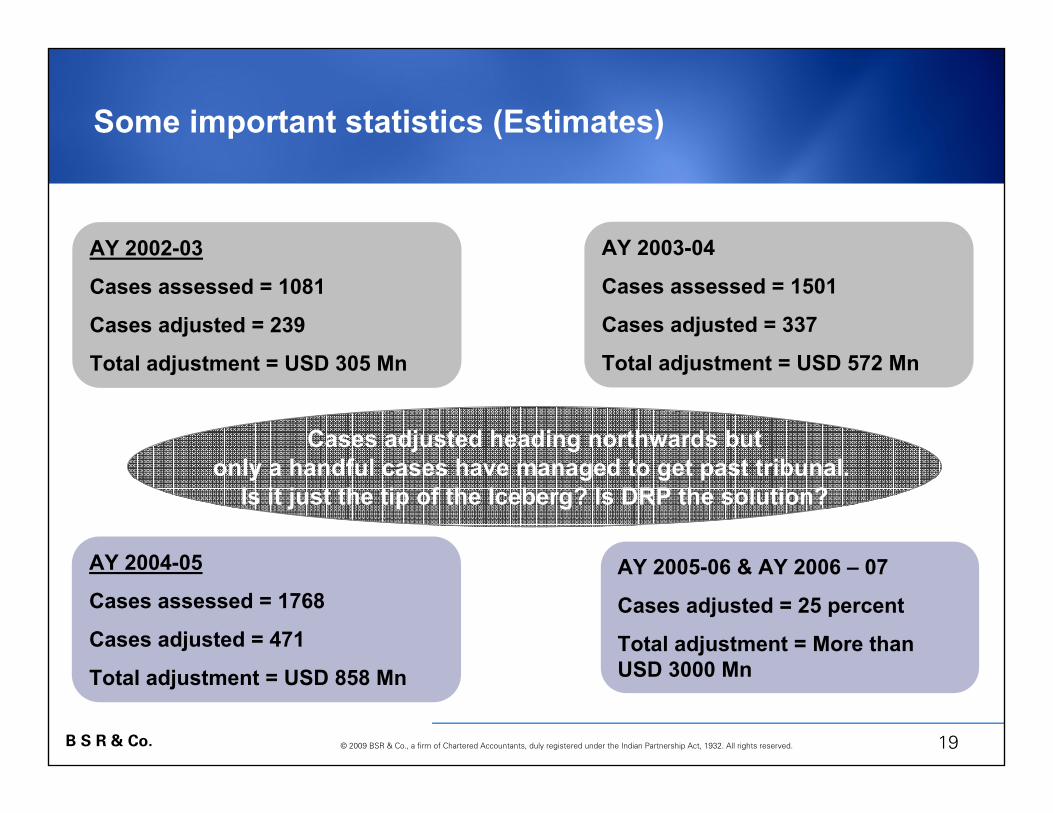

Some important statistics (Estimates)

Cases adjusted heading northwards butonly a handful cases have managed to get past tribunal.

Is it just the tip of the Iceberg? Is DRP the solution?

AY 2002-03

Cases assessed = 1081

Cases adjusted = 239

Total adjustment = USD 305 Mn

AY 2004-05

Cases assessed = 1768

Cases adjusted = 471

Total adjustment = USD 858 Mn

AY 2003-04

Cases assessed = 1501

Cases adjusted = 337

Total adjustment = USD 572 Mn

AY 2005-06 & AY 2006 – 07

Cases adjusted = 25 percent

Total adjustment = More than USD 3000 Mn

20B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

• Finance Act 2009 and DTC – Focus on transfer pricing

• Increase in audit threshold (from USD 1.25 million to 3.75 million)

• Scrutiny audit time increased from 33 months to 45 months from the end of financial year

• Steep expansion of specialist officers [No. of Transfer Pricing Officers (TPOs) from 18 to 80]

• Coordinated All-India Transfer Pricing (TP) approach

• Creation of special TP administration at CIT (A) and Tribunal level

• Training to TPOs on international TP laws and practices

• Co-ordination between Customs and Transfer Pricing authorities

• Significant adjustments to companies in IT, Pharmaceuticals, Financial services, Automobiles and Chemicals Sector

Increased administrative focus from Indian Revenue

Audit Statistics

2021222324252627

AY 02-03 AY 03-04 AY 04-05 AY 05-06Assessment Year

% o

f cas

es

adju

sted

0

200

400

600

800

1000

1200

Amt o

f adj

(USD

M

il)

% of cases adj Amt of Adj (USD Mil)

21B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Transfer Pricing audits in China

22B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Aggressive Audit Environment – Key Triggers

Consistent losses / low margins of the assessee attributable to inter-company transactions

Significant changes in profitability of the assessee and its AEs

High Royalty / Technical fee payouts, Cost recharges, Management Fees, Cost allocations. – Need to pass the ‘benefit test’

Losses incurred by routine distributors

Low mark-ups for services

Contributors to Aggressive Audits:Mounting fiscal demand on Government

Need to Preserve tax base during recession

Competitiveness needs business restructuring

Unprecedented sharing of information between revenue authorities

23B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

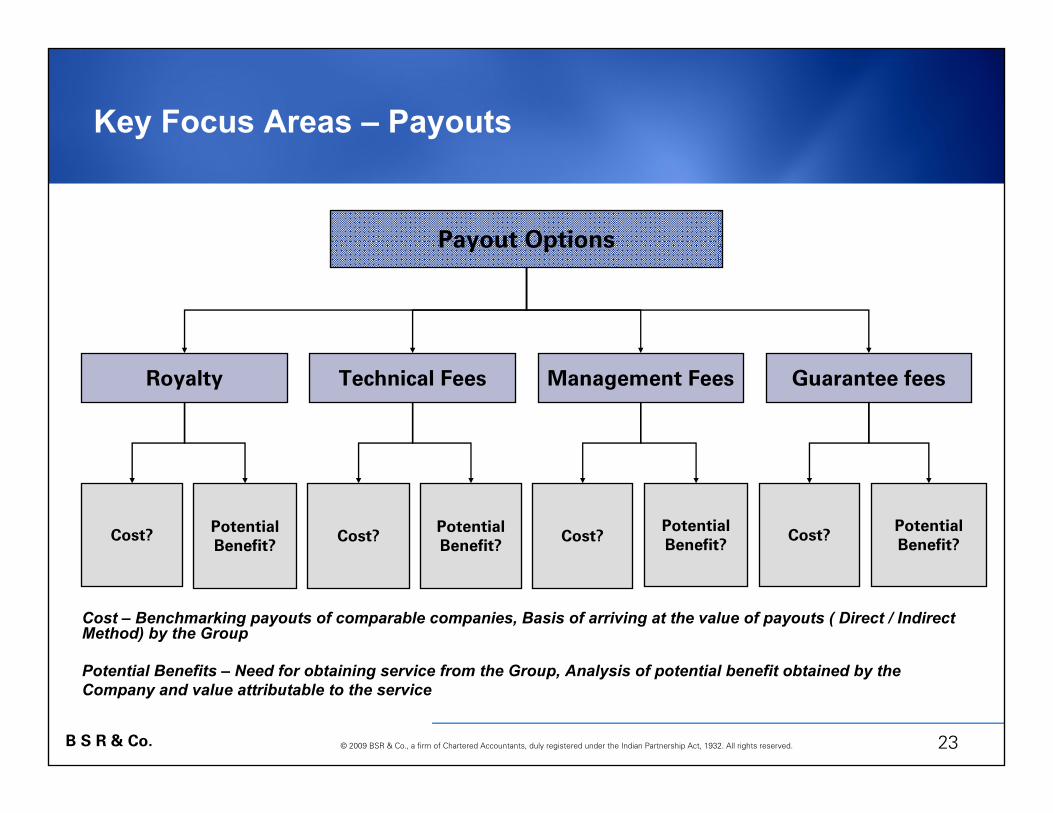

Key Focus Areas – Payouts

Cost? Potential Benefit?

Royalty Technical Fees

Cost? Potential Benefit?

Management Fees Guarantee fees

Cost?Potential Benefit?

Potential Benefit?

Cost?

Payout Options

Cost – Benchmarking payouts of comparable companies, Basis of arriving at the value of payouts ( Direct / Indirect Method) by the Group

Potential Benefits – Need for obtaining service from the Group, Analysis of potential benefit obtained by the Company and value attributable to the service

24B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Key Focus Areas – Management Payouts

Typical forms of payouts: Royalty, Technical fee, Management fee, Guarantee fee

Transfer pricing requirement: Under the transaction specific approach it is necessary to anlayse potential “cost-benefit” and maintain appropriate documentation to substantiate arm’s length nature of payouts

– Costs – Benchmarking payouts of comparable companies, Basis of arriving at the value of payouts ( Direct / Indirect Method) by the Group

– Potential Benefits – Need for obtaining service from the Group, Analysis of potential benefit obtained by the Company and value attributable to the service

Other Regulatory Considerations: FEMA / RBI ceilings (illustrative)

USD 1 million per projectTechnical Consultancy support

USD 2 million – lump sum payments 5 percent (domestic) / 8percent (exports) for recurring payments

Technical FeeRoyalty

Ceiling – Automatic routeTransactions

Regulatory ceilings cannot be considered as CUP for defending the arm’s length nature of the Payout – Need for Potential ‘Cost-Benefit’ documentation

25B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

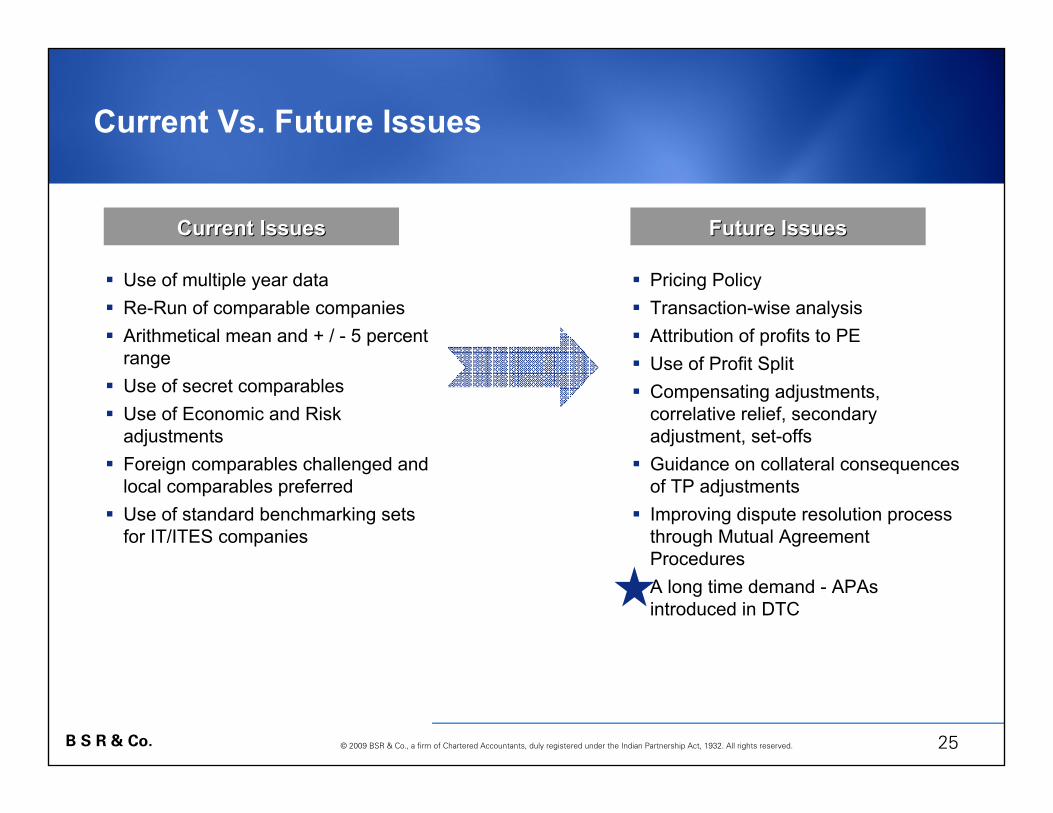

Current Vs. Future Issues

Use of multiple year dataRe-Run of comparable companies Arithmetical mean and + / - 5 percent rangeUse of secret comparables Use of Economic and Risk adjustmentsForeign comparables challenged and local comparables preferredUse of standard benchmarking sets for IT/ITES companies

Pricing Policy Transaction-wise analysis Attribution of profits to PEUse of Profit Split Compensating adjustments, correlative relief, secondary adjustment, set-offsGuidance on collateral consequences of TP adjustmentsImproving dispute resolution process through Mutual Agreement ProceduresA long time demand - APAs introduced in DTC

Current IssuesCurrent Issues Future IssuesFuture Issues

26B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

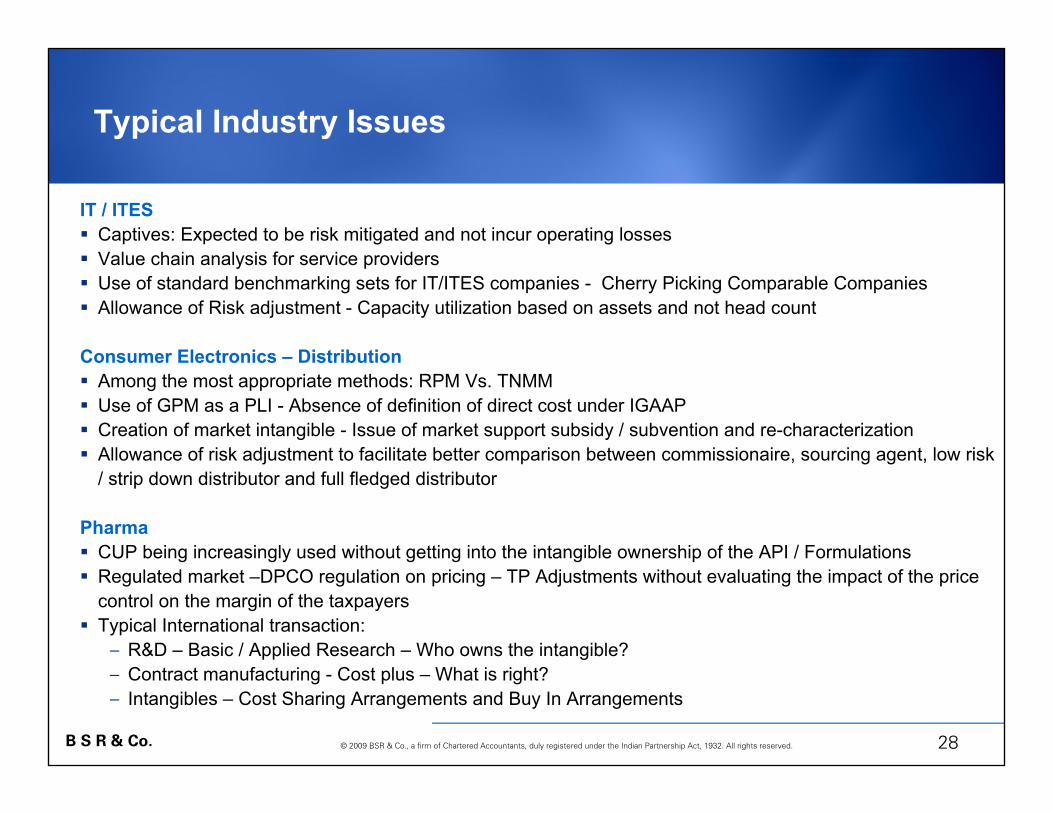

Typical Industry issues

© 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co.

27B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Industry Specific Regulations

Industry specific Regulations and Transfer Pricing: Certain industries there are regulations that govern the activities and the prices charged by the members of the industry.

Pharma: Drug Price Control Order (DPCO) and the National Pharmaceutical Pricing Authority (NPPA) have power to control the drug prices, if found excessive (Hoechst Marion Roussel Ltd. vs JCIT)

Port operations: Tariff Authority of Major Ports - (TAMP) regulates the Tariff w.r.t to container operations and handling and therefore the end price to the customer is fixed

Telecom Sector: TRAI – Telecom Regulatory Authority of India has wide-ranging powers to issue directions on Tariff charged by telecom service providers

Oil and Gas: Administered Pricing mechanism and also subsidy provided to PSU vis-à-vis competitive conditions faced by private multinational players

Transfer Pricing Authorities do not factor suchIndustry Regulations

28B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Typical Industry Issues

IT / ITESCaptives: Expected to be risk mitigated and not incur operating lossesValue chain analysis for service providersUse of standard benchmarking sets for IT/ITES companies - Cherry Picking Comparable CompaniesAllowance of Risk adjustment - Capacity utilization based on assets and not head count

Consumer Electronics – Distribution Among the most appropriate methods: RPM Vs. TNMMUse of GPM as a PLI - Absence of definition of direct cost under IGAAPCreation of market intangible - Issue of market support subsidy / subvention and re-characterization Allowance of risk adjustment to facilitate better comparison between commissionaire, sourcing agent, low risk / strip down distributor and full fledged distributor

PharmaCUP being increasingly used without getting into the intangible ownership of the API / FormulationsRegulated market –DPCO regulation on pricing – TP Adjustments without evaluating the impact of the price control on the margin of the taxpayers Typical International transaction:

– R&D – Basic / Applied Research – Who owns the intangible? – Contract manufacturing - Cost plus – What is right?– Intangibles – Cost Sharing Arrangements and Buy In Arrangements

29B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Typical Issues – Auto Industry

Recessionary economy: Significant impact expected on auto industry

Pricing pressures on automobiles results in push back on component suppliers – cost pressure

Capital intensive and high fixed cost

Start up costs, Idle capacity - Resulting in initial year losses

High initial import content with steady localisation, Forex losses

Dependent on technical support from Group - High tech fee / royalty payouts

Internal comparables need to be analyzed - Pricing of similar transactions with third parties

Local documentation preferred to Group global documentation by revenue authorities

Limited industry guidance or judicial precedence

Issues with Indian benchmarking

What do Ford, Toyota, Honda, Volvo, Skoda have in common in India?Transfer Pricing Adjustment!

30B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Auto Industry Trends and Impact of Transfer Pricing

Well established players (primarily Indian players) earning higher margins vs-a-vis foreign players most of whom are new entrants

New entrants incur initial year losses due to high import content, forex issues, start up costs and idle capacity

New players will be benchmarked with Indian players without cognizance of years of presence or industry / economic dynamics

Impact on transfer pricing

7

8

9

10

Profit Margin

(percent)

2006 2007 2008 2009

Years

Auto Ancillary

AllEngine parts

Auto - Foreign / New players

-10

-5

0

5

10

2006 2007 2008

Years

Pro

fit

mar

gin

(p

erce

nt)

Hyundai Motors -1996

General Motors -1994

Honda Siel - 1995

Ford India - 1995

Auto - Established / Domestic Players

-10

-5

0

5

10

15

2006 2007 2008 2009

Years

Pro

fit

mar

gin

(p

erce

nt)

Tata Motors -1945

Mahindra andMahindra -1945

HindustanMotors - 1942

Maruti SuzukiIndia Ltd. -1984

31B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Recent Rulings in India

© 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co.

32B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

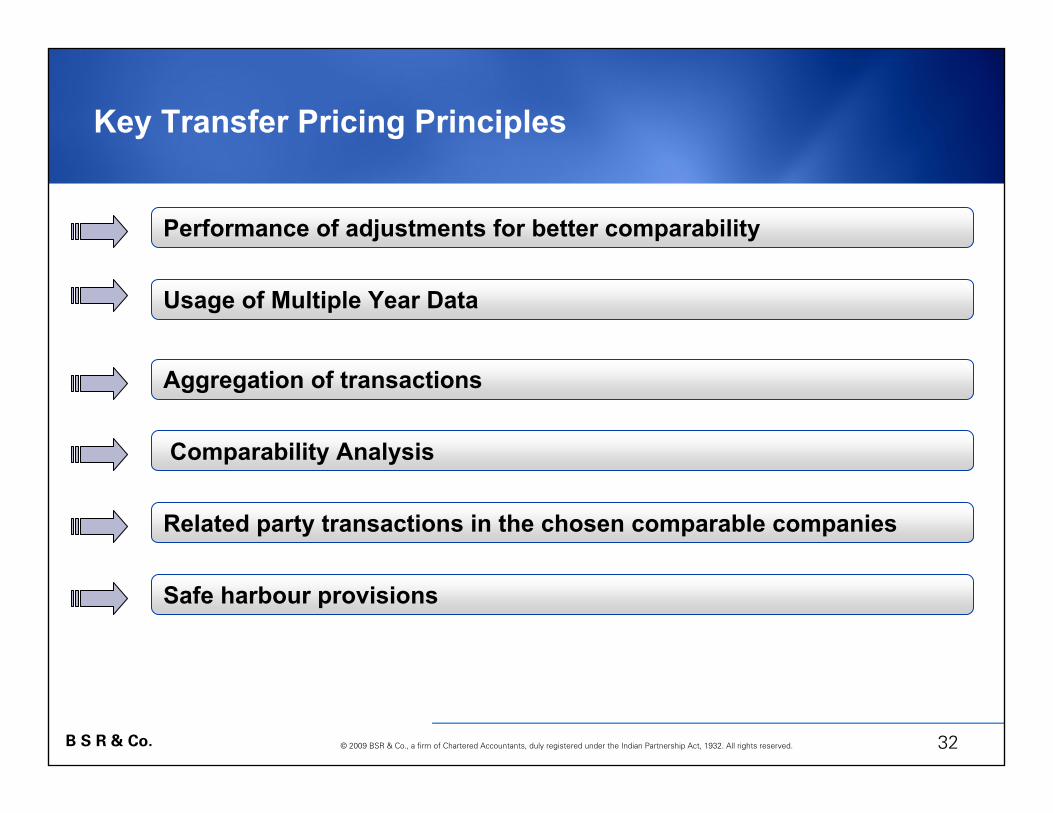

Performance of adjustments for better comparability

Usage of Multiple Year Data

Aggregation of transactions

Comparability Analysis

Related party transactions in the chosen comparable companies

Key Transfer Pricing Principles

Safe harbour provisions

33B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

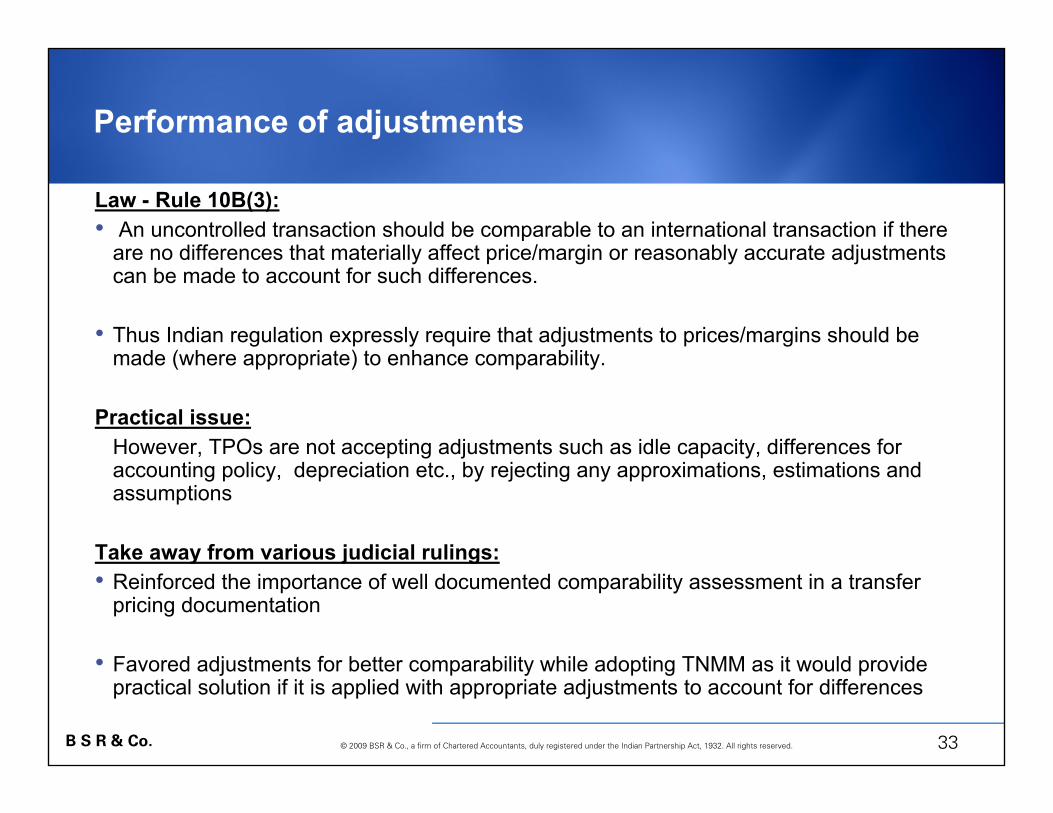

Performance of adjustments

Law - Rule 10B(3):• An uncontrolled transaction should be comparable to an international transaction if there

are no differences that materially affect price/margin or reasonably accurate adjustments can be made to account for such differences.

• Thus Indian regulation expressly require that adjustments to prices/margins should be made (where appropriate) to enhance comparability.

Practical issue:However, TPOs are not accepting adjustments such as idle capacity, differences for accounting policy, depreciation etc., by rejecting any approximations, estimations and assumptions

Take away from various judicial rulings: • Reinforced the importance of well documented comparability assessment in a transfer

pricing documentation

• Favored adjustments for better comparability while adopting TNMM as it would provide practical solution if it is applied with appropriate adjustments to account for differences

34B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Performance of Adjustments – (1/2)Performance of Adjustments – (1/2)

This ruling lays down certain important principles to undertake adjustments in proper and fit cases for the purpose of comparability analysis. This judgment is significant for the companies in start-up stages and recognizes that differences in business models and higher cost incurred during the start-up phase calls for economic adjustments.Adjustments should be factored into the comparability analysis and for the purpose of comparability analysis, the taxpayer cannot be expected to obtain details that are not available in the public domain.

Skoda Auto India Pvt Ltd

Pune ITAT

Tribunal has accepted that depreciation cost may be adjusted to eliminate material differences in the ‘asset profile’ of the taxpayer vis-à-vis comparables based on sufficient evidence on record, thereby enabling use of cash profit as the Profit Level Indicator

Schefenacker Motherson Ltd Delhi ITAT

Adjustment needs to be made to the margins of the comparable companies to eliminate differences on account of different functions, assets and risks. More specifically, adjustment needs to be made for, (a) difference in risk profile, (b) difference in working capital position, and (c) difference in accounting policies.An adjustment on account of difference in risk profiles may be derived by subtracting the risk free ‘bank rate’ from the PLR.

Philips Software Centre Pvt LtdBangalore ITAT

35B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Performance of Adjustments – (2/2)Performance of Adjustments – (2/2)

The Tribunal stated that depending on specific facts and circumstances of the case which cannot be the same for all companies, the final set of comparables may need to eliminate differences by making adjustments.

Some adjustments noted in the Tribunal’s order were adjustments for working capital, risk and R&D expenses.

Mentor Graphics (Noida) Pvt. Ltd.

Delhi ITAT

The Tribunal held that while comparing under the TNMM, those differences having material effect on price must be taken into consideration with an idea to make reasonable and accurate adjustment to eliminate such differencesWhile applying TNMM, necessary adjustments for differences on account of FAR analysis must be made to enhance comparability.if the differences between comparables and the tested party cannot be subjected to an evaluation, then transaction may be eliminated for purpose of comparison.Potential comparables with abnormal profit / losses need to be excluded.

E-Gain Communication Pvt. Limited

Pune ITAT

36B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

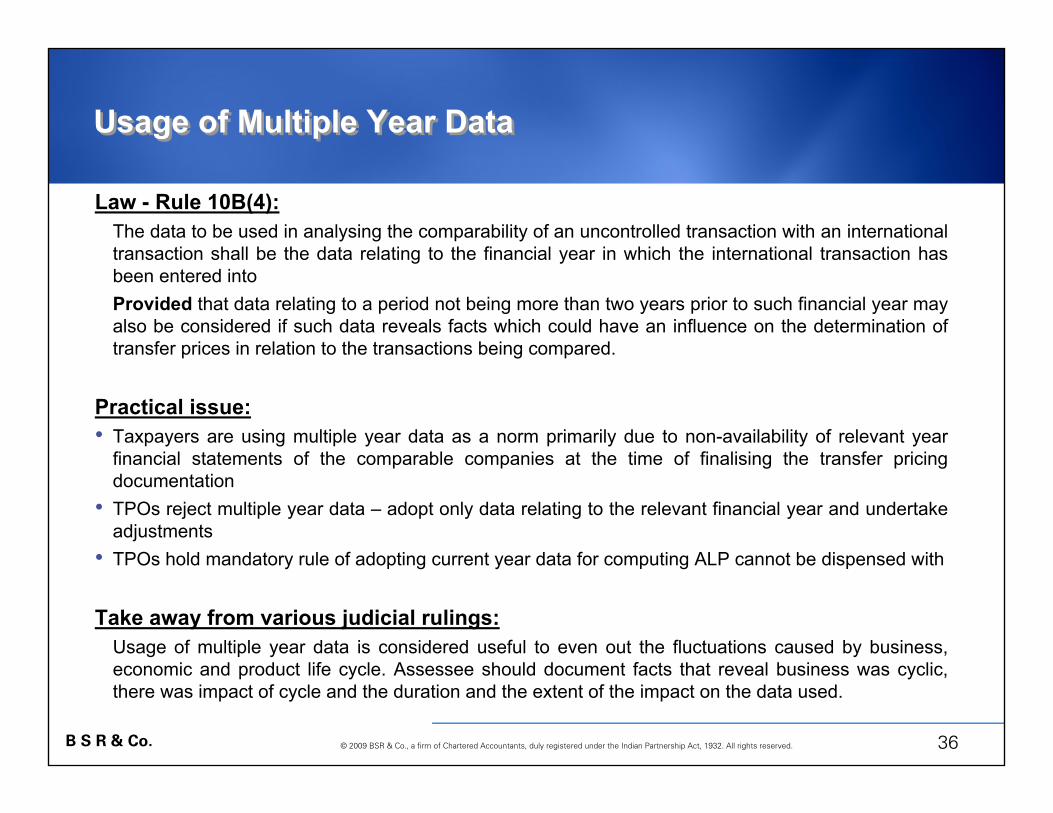

Law - Rule 10B(4):The data to be used in analysing the comparability of an uncontrolled transaction with an international transaction shall be the data relating to the financial year in which the international transaction has been entered into Provided that data relating to a period not being more than two years prior to such financial year may also be considered if such data reveals facts which could have an influence on the determination of transfer prices in relation to the transactions being compared.

Practical issue:• Taxpayers are using multiple year data as a norm primarily due to non-availability of relevant year

financial statements of the comparable companies at the time of finalising the transfer pricing documentation

• TPOs reject multiple year data – adopt only data relating to the relevant financial year and undertake adjustments

• TPOs hold mandatory rule of adopting current year data for computing ALP cannot be dispensed with

Take away from various judicial rulings: Usage of multiple year data is considered useful to even out the fluctuations caused by business, economic and product life cycle. Assessee should document facts that reveal business was cyclic, there was impact of cycle and the duration and the extent of the impact on the data used.

Usage of Multiple Year DataUsage of Multiple Year Data

37B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Usage of Multiple Year DataUsage of Multiple Year Data

The mandatory and absolute requirement of law for use of the current financial year data cannot be dispensed with even if the relevant data was not available with the appellant in the electronic data base at the time of preparation of the TP report.The TPO is empowered to determine the ALP by using the current financial year data available at the time of transfer pricing proceedings and to conduct the comparability analysis by using such data. The OECD Guidelines in Para 1.49 to 1.51 have acknowledged the use of multiple year data under special circumstances. Use of multiple year data is considered useful to smooth out the fluctuations caused by business/economic/product life cycle. However, the mere claim that there exists a cycle is not sufficient.multiple year data should be used only when it adds value to the transfer pricing analysis.

Customer Services India (P) Ltd. Delhi ITAT

Under Indian transfer pricing regulations, for comparability purposes, consideration of subsequent year data or average profits not permitted

In relation to comparability analysis, though the OECD guidelines allowed use of profits for the period under consideration, previous or next year or average of such profits, however, under the Indian TP regulations, Rule 10B (4) there was no provision for consideration of data for a subsequent assessment year.

Honeywell Automation India Limited

Pune ITAT

38B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Aggregation of transactions:• As per transfer pricing principles, International transactions are required to be tested on a stand alone

basic unless they are inextricably linked• In many cases the aggregation approach has been challenged by the TPO’s and they are inclined to adopt

transaction specific approach. • There are rulings in favour and against the aggregation approach

Comparability analysis:• Rule 10B(2) The comparability of an international transaction with an uncontrolled transaction shall be

judged with reference to the following, namely:—– The specific characteristics of the property transferred or services provided in either transaction;– Functions performed, assets employed, risks assumed– Contractual terms– Conditions prevailing in the markets

• In-depth analysis of comparables is critical• In the TNMM approach the Function, Assets and Risk analysis (FAR) of the independent comparable

companies need to be undertaken before finalizing the benchmarking analysis.

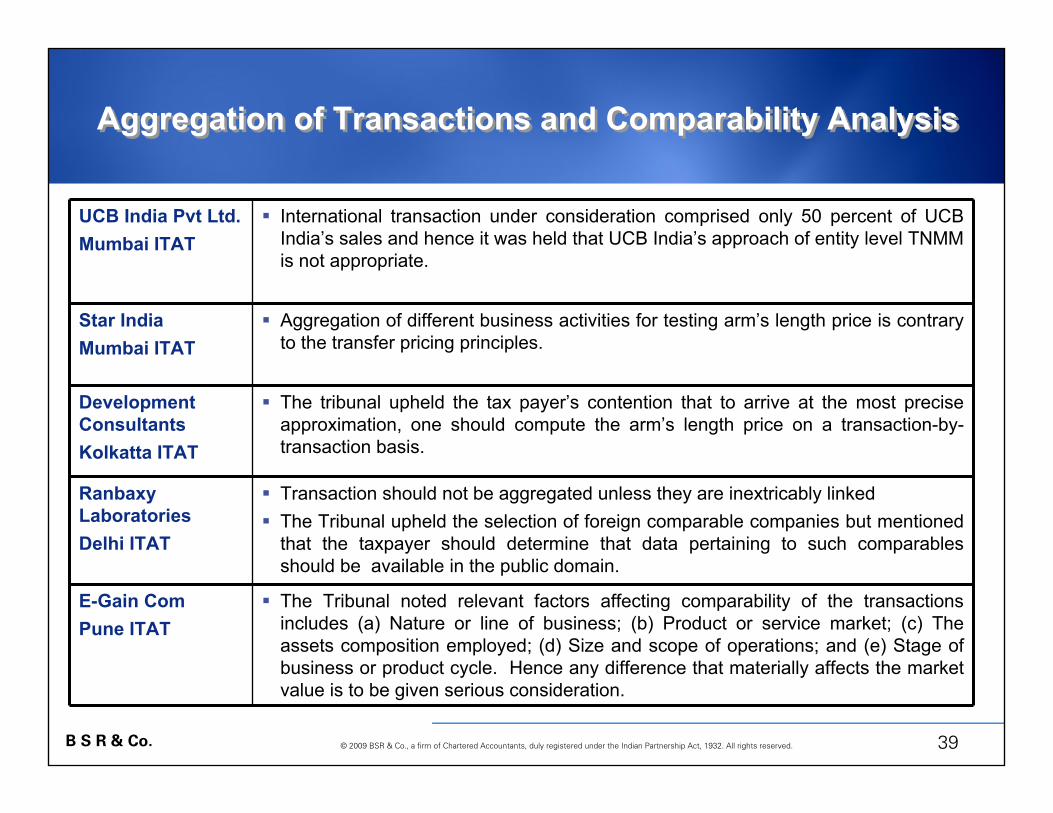

Aggregation of Transactions and Comparability Aggregation of Transactions and Comparability

39B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Aggregation of Transactions and Comparability AnalysisAggregation of Transactions and Comparability Analysis

International transaction under consideration comprised only 50 percent of UCB India’s sales and hence it was held that UCB India’s approach of entity level TNMM is not appropriate.

UCB India Pvt Ltd. Mumbai ITAT

The Tribunal noted relevant factors affecting comparability of the transactions includes (a) Nature or line of business; (b) Product or service market; (c) The assets composition employed; (d) Size and scope of operations; and (e) Stage of business or product cycle. Hence any difference that materially affects the market value is to be given serious consideration.

E-Gain ComPune ITAT

Transaction should not be aggregated unless they are inextricably linkedThe Tribunal upheld the selection of foreign comparable companies but mentioned that the taxpayer should determine that data pertaining to such comparables should be available in the public domain.

Ranbaxy LaboratoriesDelhi ITAT

Aggregation of different business activities for testing arm’s length price is contrary to the transfer pricing principles.

Star IndiaMumbai ITAT

The tribunal upheld the tax payer’s contention that to arrive at the most precise approximation, one should compute the arm’s length price on a transaction-by-transaction basis.

Development ConsultantsKolkatta ITAT

40B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Related Party and Safe Harbour Provisions*

Related party – Law Rule 10A(a)• Rule 10 A (a) provides the meaning of the term “uncontrolled transaction” i.e., it means a

transaction between enterprises other than associated enterprises, whether resident or non resident.

• It is given that arm’s length standard shall be substantiated when the transactions between persons are in uncontrolled conditions.

Practical IssueCan a single rupee of related party transaction be the basis for rejecting a comparable company ? – There are ruling both in favour and against such exclusions

Safe harbourPrior to latest amendment, the proviso to section 92C (2) stated that in the event that more than one arm’s length price is determined based on the MAM applied then the ALP would be the arithmetic mean of such prices, or, at the option of the assessee, a price which may vary from the arithmetic mean by an amount not exceeding 5% percent of such arithmetic mean.

* Amended Subsequently by Finance Act 2009

41B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Related Party and Safe Harbour Provisions*Related Party and Safe Harbour Provisions*

The Tribunal disregarded the selection of comparable companies since they had entered into transaction with either parent company or subsidiary company.

Mentor GraphicsDelhi ITAT

The safe harbour +/- 5 percent variance benefit be allowed as a ‘standard deduction’, if the margins from the controlled transaction falls outside the said tolerance range.

Development ConsultantsKolkatta ITAT

The Tribunal held that an entity can be taken as uncontrolled if its related party transaction do not exceed 10 to 15 percent of total revenue.The tribunal confirmed the availability of safe harbor provisions at the option of the taxpayer.

Sony IndiaDelhi ITAT

Rule 10A (a) - For the purpose of comparability analysis, the comparable “uncontrolled transaction” means a transaction between enterprises other than associated enterprises, whether resident or non-resident; Companies with even a single rupee of transactions with associated enterprises cannot be considered as comparablesDevelopment Consultants squarely applies – 5 percent Standard deduction

Philips Software Bangalore ITAT

* Amended Subsequently by Finance Act 2009

42B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

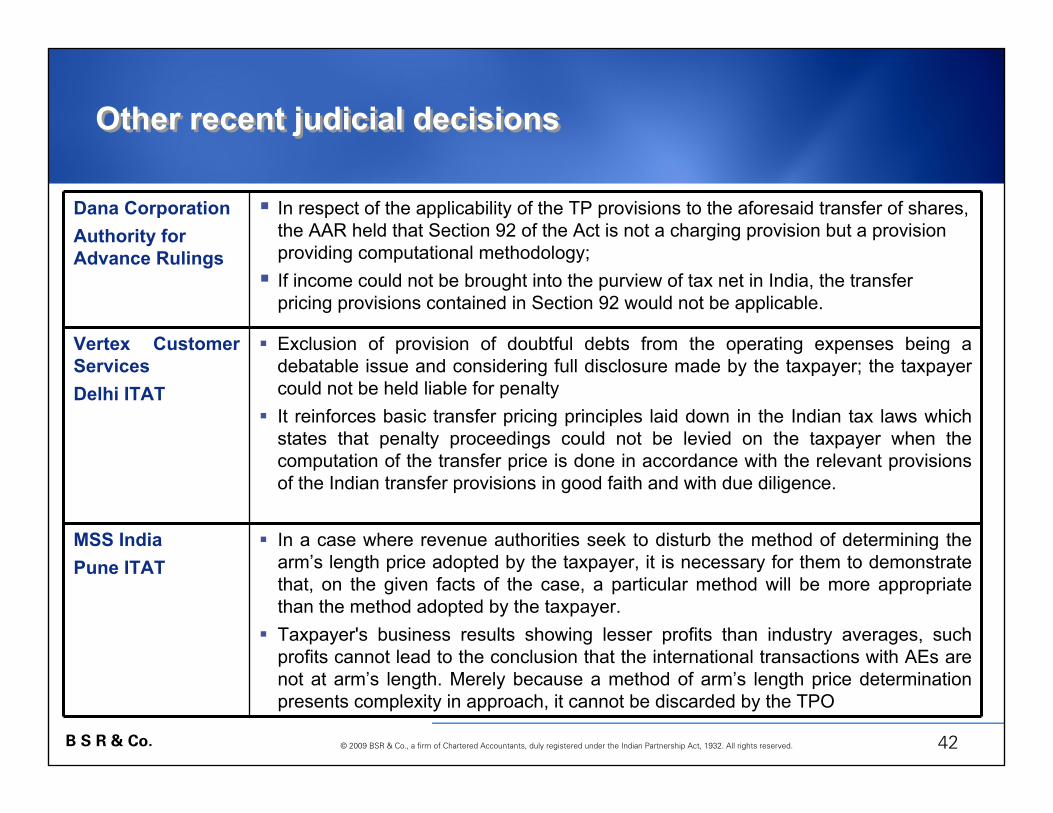

Other recent judicial decisions Other recent judicial decisions

In a case where revenue authorities seek to disturb the method of determining the arm’s length price adopted by the taxpayer, it is necessary for them to demonstrate that, on the given facts of the case, a particular method will be more appropriate than the method adopted by the taxpayer.Taxpayer's business results showing lesser profits than industry averages, such profits cannot lead to the conclusion that the international transactions with AEs are not at arm’s length. Merely because a method of arm’s length price determination presents complexity in approach, it cannot be discarded by the TPO

MSS IndiaPune ITAT

Exclusion of provision of doubtful debts from the operating expenses being a debatable issue and considering full disclosure made by the taxpayer; the taxpayer could not be held liable for penaltyIt reinforces basic transfer pricing principles laid down in the Indian tax laws which states that penalty proceedings could not be levied on the taxpayer when the computation of the transfer price is done in accordance with the relevant provisions of the Indian transfer provisions in good faith and with due diligence.

Vertex Customer ServicesDelhi ITAT

In respect of the applicability of the TP provisions to the aforesaid transfer of shares, the AAR held that Section 92 of the Act is not a charging provision but a provision providing computational methodology;If income could not be brought into the purview of tax net in India, the transfer pricing provisions contained in Section 92 would not be applicable.

Dana CorporationAuthority for Advance Rulings

43B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Customer Services - Delhi

Schefenacker Motherson - Delhi

Skoda Auto – Pune

MSS India – Pune

Adjustment Multiple year data

RPT

Honeywell – Pune

UCB India – Mumbai

Safe Harbour

Philips Software - Blore

Sony India – Delhi

Develop. Consult. - Kol

Star India - Mumbai

E-Gain – Pune

Cargill - Delhi

Ranbaxy – Delhi

Mentor Graphics – Delhi

Aztec - Blore

Comparability Standard

Ruling

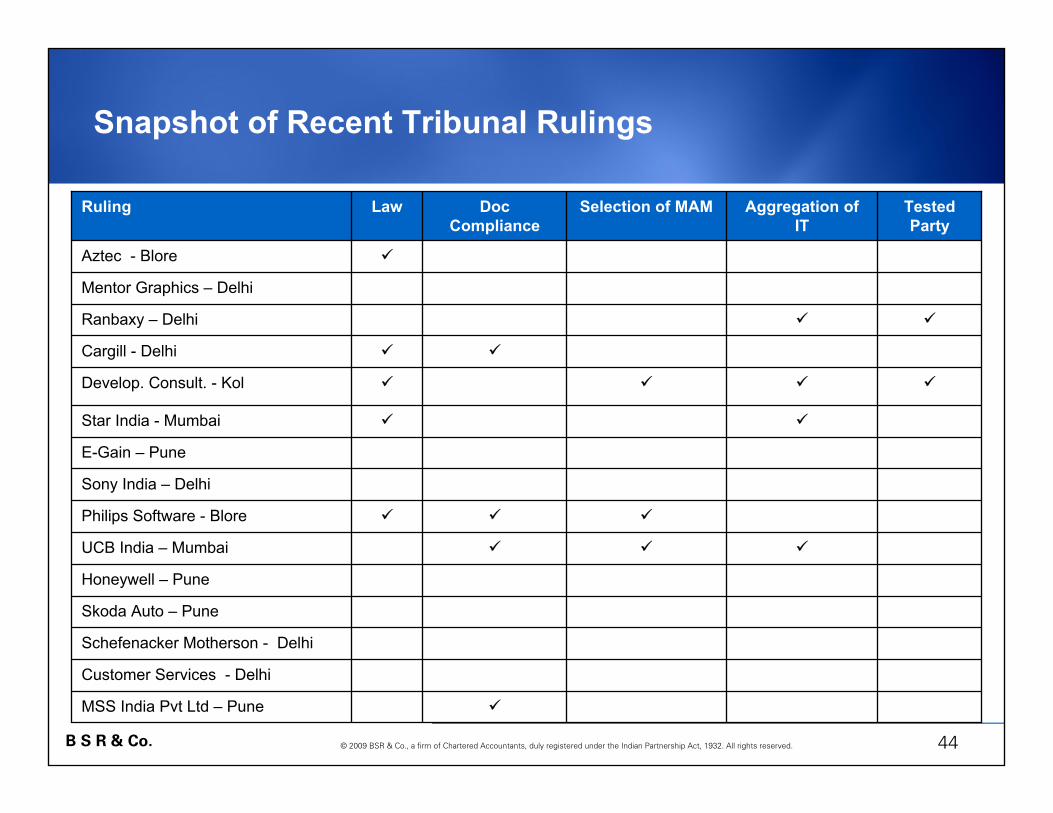

Snapshot of Recent Tribunal Rulings

44B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Schefenacker Motherson - Delhi

Customer Services - Delhi

Skoda Auto – Pune

Doc Compliance

Selection of MAM

MSS India Pvt Ltd – Pune

Honeywell – Pune

UCB India – Mumbai

Philips Software - Blore

Sony India – Delhi

Develop. Consult. - Kol

Star India - Mumbai

Aggregation of IT

Tested Party

E-Gain – Pune

Cargill - Delhi

Ranbaxy – Delhi

Mentor Graphics – Delhi

Aztec - Blore

LawRuling

Snapshot of Recent Tribunal Rulings

45B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Synopsis – Some key industry specific rulings

Skoda AutoSchefenacker Motherson

Auto

Sony IndiaConsumer Electronics -Distribution

Mentor GraphicsMorgan StanleyPhilips SoftwareEgainDevelopment ConsultantsComputer Services

IT / ITES

Ranbaxy LaboratoriesUCB

Pharma

RulingIndustry

46B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Key Takeaways from Recent Rulings

No need to establish diversion of profits outside India to determine applicability of the TP provisions

Detailed FAR analysis for tested party and comparable companies is crucial

International transactions should not be aggregated unless they are inextricably linked

Least complex entity to be selected as the tested party

Adjustments be made to improve comparability

Use multiple year data where the business is cyclic and the trend has impacted the business results

Recent rulings reaffirm basic Recent rulings reaffirm basic Transfer Pricing principlesTransfer Pricing principles

47B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Key Takeaways from Recent Rulings

Unquestionable inference – taxpayers must have a robust documentation with sound FAR analysis and well developed economic analysis to justify the transfer prices

Mere finding of faults with the approach adopted by TPO - will not help to delete the adjustments at the appellate level

Taxpayer maintains strong documentation - it becomes increasingly challenging for the TPOs to disprove the same.

Considering the factual nature of the transfer pricing disputes - the rulings have a limited precedent value in case there are variation in facts

48B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Recent updates Amendments in Finance Act 09 & Direct Tax Code Proposals

© 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co.

49B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Anti Avoidance &

Thin capitalizationIntroduction of

Dispute Resolution Panel

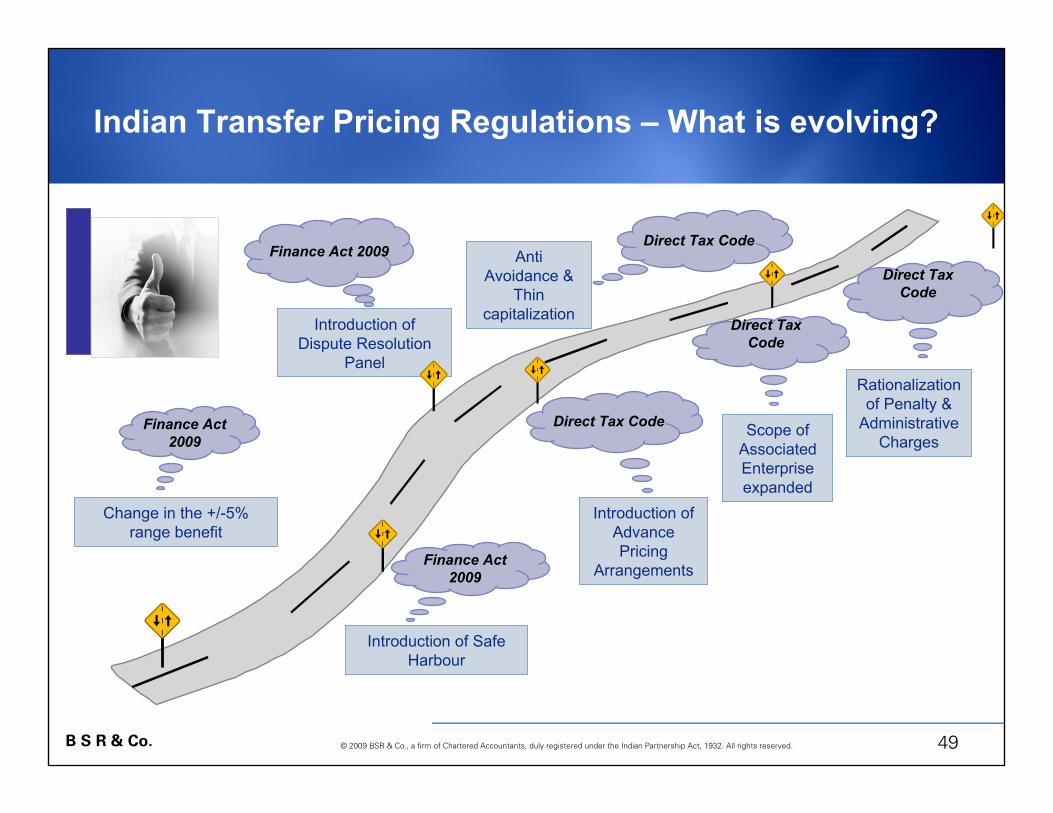

Indian Transfer Pricing Regulations – What is evolving?

Finance Act 2009

Finance Act 2009

Change in the +/-5% range benefit

Direct Tax Code

Introduction of Advance Pricing

Arrangements

Direct Tax Code

Scope of Associated Enterprise expanded

Finance Act 2009

Introduction of Safe Harbour

Direct Tax Code

Direct Tax Code

Rationalization of Penalty &

Administrative Charges

50B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Snapshot of changes

Finance Act 09

Determination of Arm’s Length Price –Concept of +/- 5 percent variance

Introduction of Safe Harbour Rules

Creation of Dispute Resolution Panel

51B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

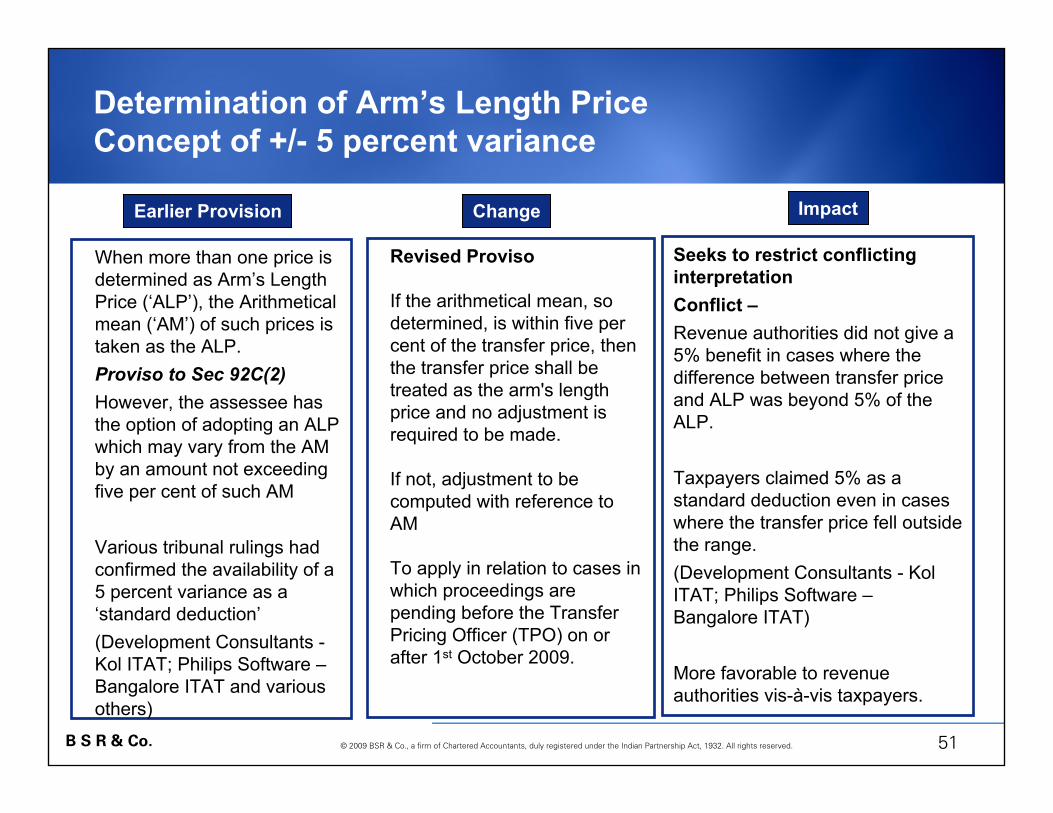

Determination of Arm’s Length PriceConcept of +/- 5 percent variance

When more than one price is determined as Arm’s Length Price (‘ALP’), the Arithmetical mean (‘AM’) of such prices is taken as the ALP.Proviso to Sec 92C(2)However, the assessee has the option of adopting an ALP which may vary from the AM by an amount not exceeding five per cent of such AM

Various tribunal rulings had confirmed the availability of a 5 percent variance as a ‘standard deduction’(Development Consultants -Kol ITAT; Philips Software –Bangalore ITAT and various others)

Revised Proviso

If the arithmetical mean, so determined, is within five per cent of the transfer price, then the transfer price shall be treated as the arm's length price and no adjustment is required to be made.

If not, adjustment to be computed with reference to AM

To apply in relation to cases in which proceedings are pending before the Transfer Pricing Officer (TPO) on or after 1st October 2009.

Seeks to restrict conflicting interpretationConflict –Revenue authorities did not give a 5% benefit in cases where the difference between transfer price and ALP was beyond 5% of the ALP.

Taxpayers claimed 5% as a standard deduction even in cases where the transfer price fell outside the range.(Development Consultants - KolITAT; Philips Software –Bangalore ITAT)

More favorable to revenue authorities vis-à-vis taxpayers.

Earlier Provision Change Impact

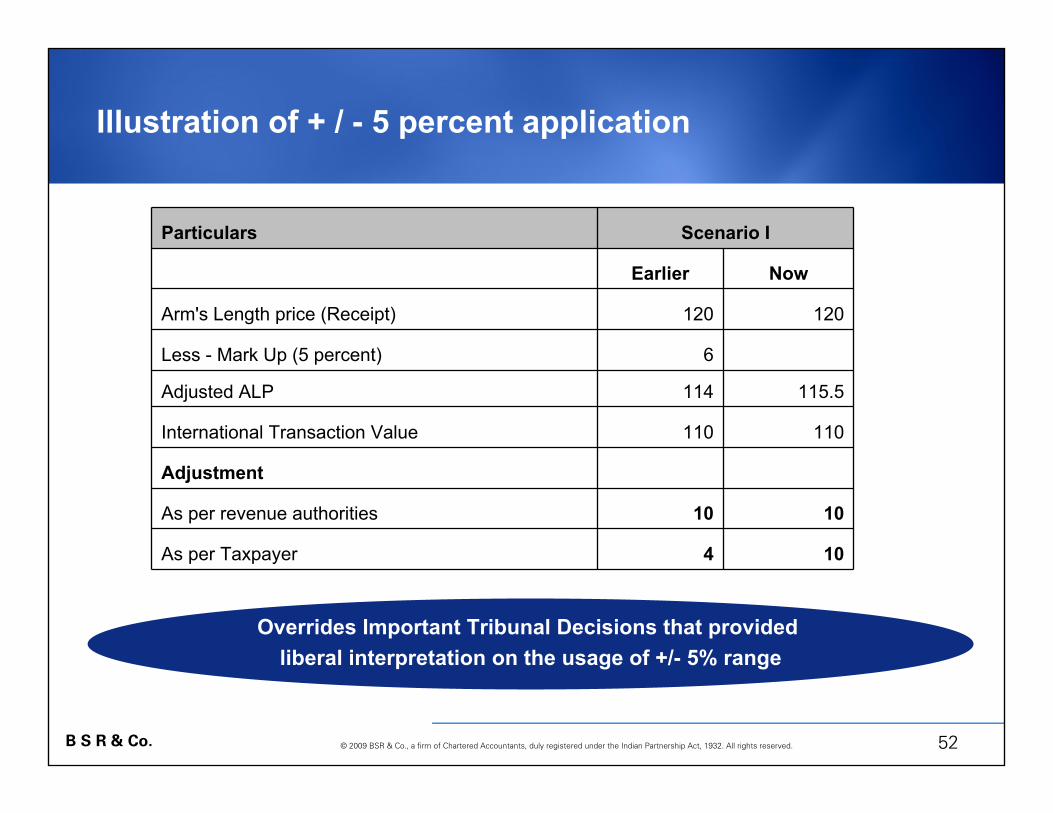

52B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

104As per Taxpayer

1010As per revenue authorities

Adjustment

110110International Transaction Value

115.5114Adjusted ALP

6Less - Mark Up (5 percent)

120120Arm's Length price (Receipt)

NowEarlier

Scenario IParticulars

Illustration of + / - 5 percent application

Overrides Important Tribunal Decisions that provided liberal interpretation on the usage of +/- 5% range

53B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Safe Harbour Provisions

• Considering the increase in transfer pricing litigation, Central Board of Direct Taxes (CBDT) is to formulate safe harbour provisions. - Applicable from 1 April 2009

• Aim to reduce the impact of judgemental errors in transfer pricing

• Safe harbour has been defined to mean ‘circumstances’in which the revenue authorities shall accept the transfer pricing declared by the taxpayer.

Internationally safe harbours have taken various forms

• Exclusion of certain classes of transactions based on quantitative thresholds

• Stipulation of margins / pricing norms for specified industries / functions (USA, Singapore)

• Specifying thresholds whereby the onerous documentation requirement is reduced (Brazil)

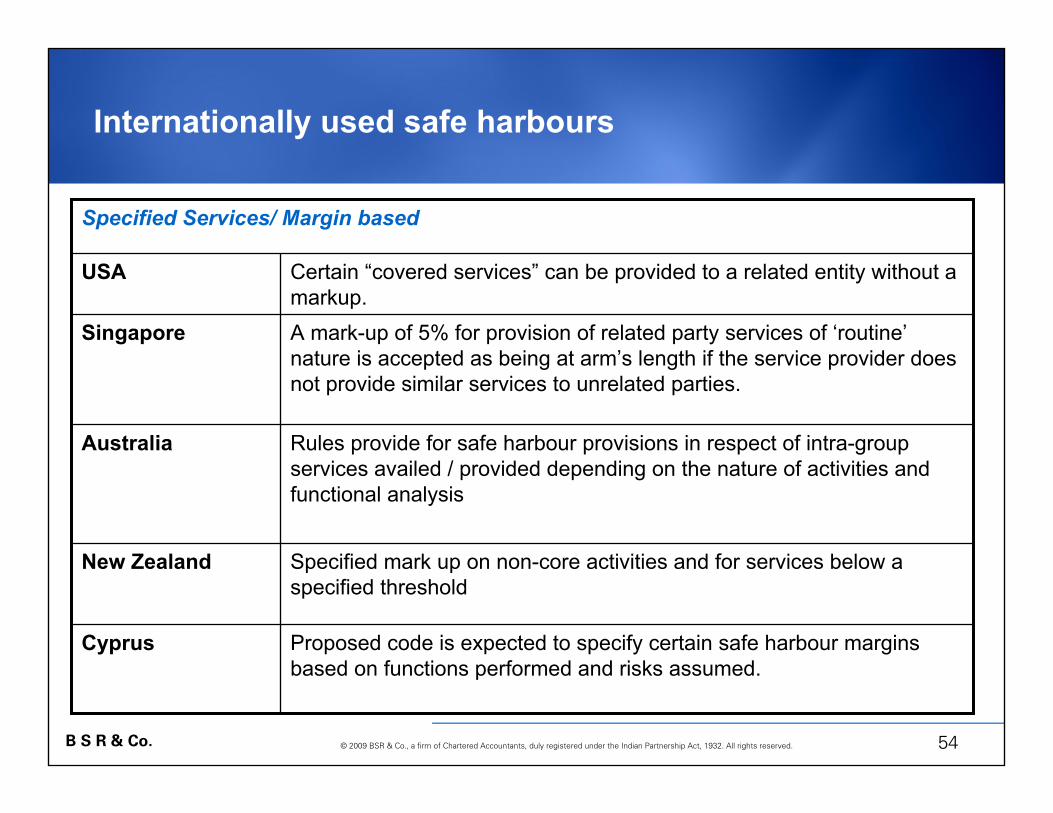

54B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Internationally used safe harbours

Proposed code is expected to specify certain safe harbour margins based on functions performed and risks assumed.

Cyprus

Specified mark up on non-core activities and for services below a specified threshold

New Zealand

Specified Services/ Margin based

Rules provide for safe harbour provisions in respect of intra-group services availed / provided depending on the nature of activities and functional analysis

Australia

A mark-up of 5% for provision of related party services of ‘routine’nature is accepted as being at arm’s length if the service provider does not provide similar services to unrelated parties.

Singapore

Certain “covered services” can be provided to a related entity without a markup.

USA

55B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Internationally used safe harbours

Price based

Specified industry

Relief from detailed documentation requirement

Taxpayer is exempted from detailed documentation if the taxpayer has a minimum of 5% net profit on its total export revenues to related parties or whose export revenue in the calendar year does not exceed 5% of its total revenue in the same period.

Brazil

Africa, Germany, Netherlands - Prescribe acceptable levels of debt equity ratios for related party loans

Others –

If annual revenue is below the specified threshold, transfer pricing documentation need not be maintained. However, other documentation may be called for during audit.

Taiwan / India

Transfer pricing rules will apply to exports only if the average export price is lower than 90% of the average price of similar goods / services sold under similar circumstances in the domestic market.

Brazil

Law provides for ‘safe harbours’ for traditional Maquiladaros (contract manufacturers) with a requirement as regards profit or return on foreign owned assets

Mexico

56B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

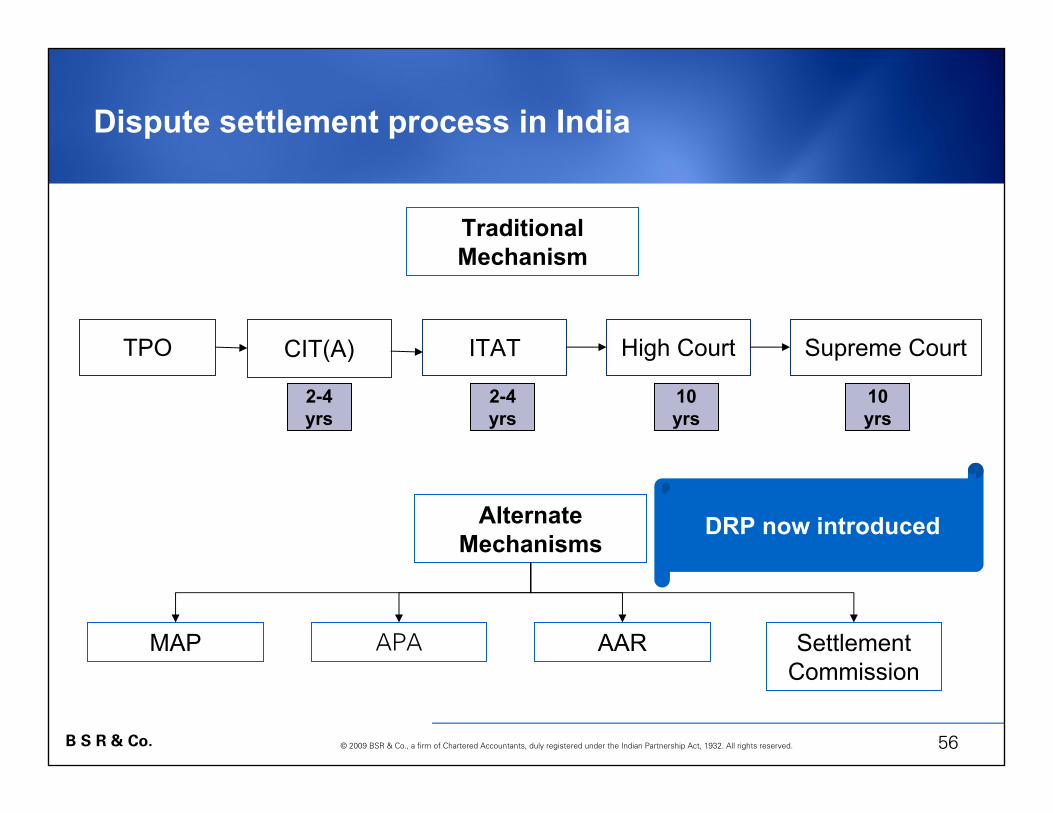

Dispute settlement process in India

Alternate Mechanisms

MAP Settlement Commission

AARAPA

TPO CIT(A) ITAT High Court Supreme Court

Traditional Mechanism

2-4 yrs

2-4 yrs

10yrs

10yrs

DRP now introduced

57B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

DRP Mechanism

• When a TP adjustment is proposed, AO will issue draft order to taxpayer

• Taxpayer will confirm or file objections with AO and DRP within 30 days

• DRP will issue guidance to AO after having regard to evidences, further enquiries etc within 9 months from the date draft order was issued to taxpayer

• Panel may confirm, reduce or enhance the proposed transfer pricing adjustments. It cannot set aside the proposed adjustment for further enquiry

• In case of differences within DRP, opinion of the majority stands

• AO shall pass the order in conformity with directions of DRP, within one month without granting any additional opportunity to the taxpayer

• Appeal by taxpayer lies before the Appellate Tribunal and DRPs order is binding on the revenue and no appeal lies for the revenue

• CBDT to frame rules - The Central Board of Direct Taxes has notified the Income-tax (Dispute Resolution Panel) Rules, 2009 on 20 November

58B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

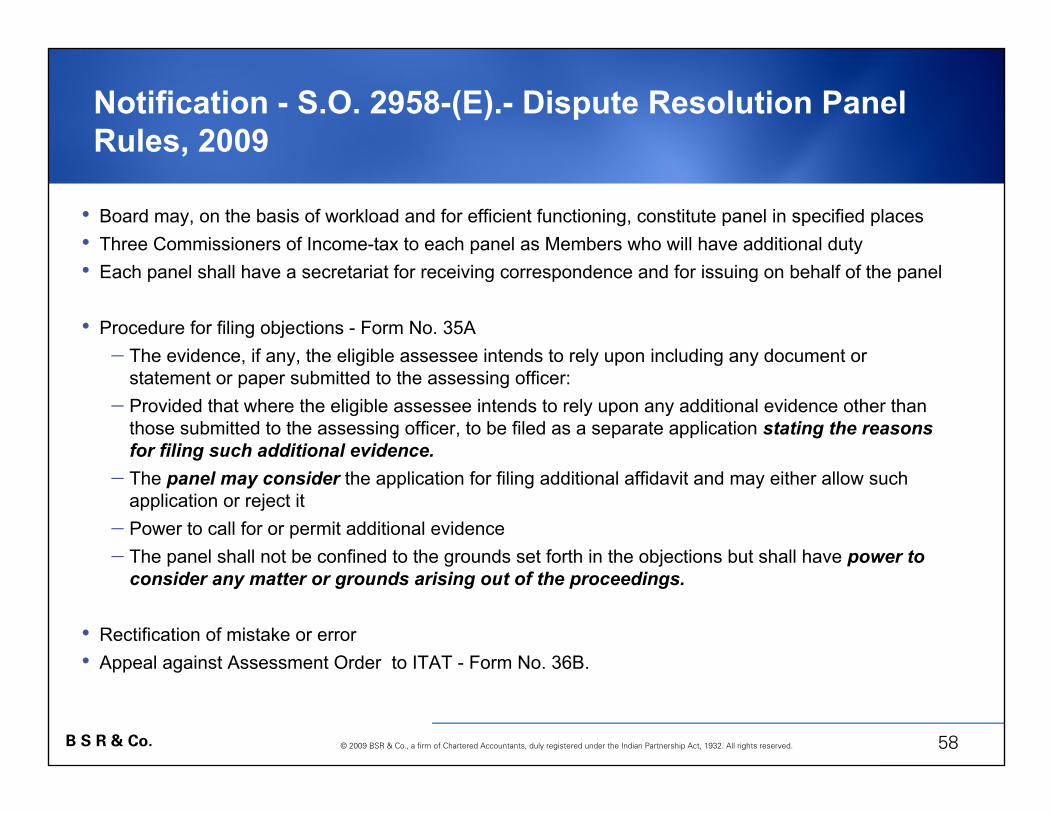

Notification - S.O. 2958-(E).- Dispute Resolution Panel Rules, 2009

• Board may, on the basis of workload and for efficient functioning, constitute panel in specified places • Three Commissioners of Income-tax to each panel as Members who will have additional duty• Each panel shall have a secretariat for receiving correspondence and for issuing on behalf of the panel

• Procedure for filing objections - Form No. 35A− The evidence, if any, the eligible assessee intends to rely upon including any document or

statement or paper submitted to the assessing officer:− Provided that where the eligible assessee intends to rely upon any additional evidence other than

those submitted to the assessing officer, to be filed as a separate application stating the reasons for filing such additional evidence.

− The panel may consider the application for filing additional affidavit and may either allow such application or reject it

− Power to call for or permit additional evidence − The panel shall not be confined to the grounds set forth in the objections but shall have power to

consider any matter or grounds arising out of the proceedings.

• Rectification of mistake or error • Appeal against Assessment Order to ITAT - Form No. 36B.

59B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

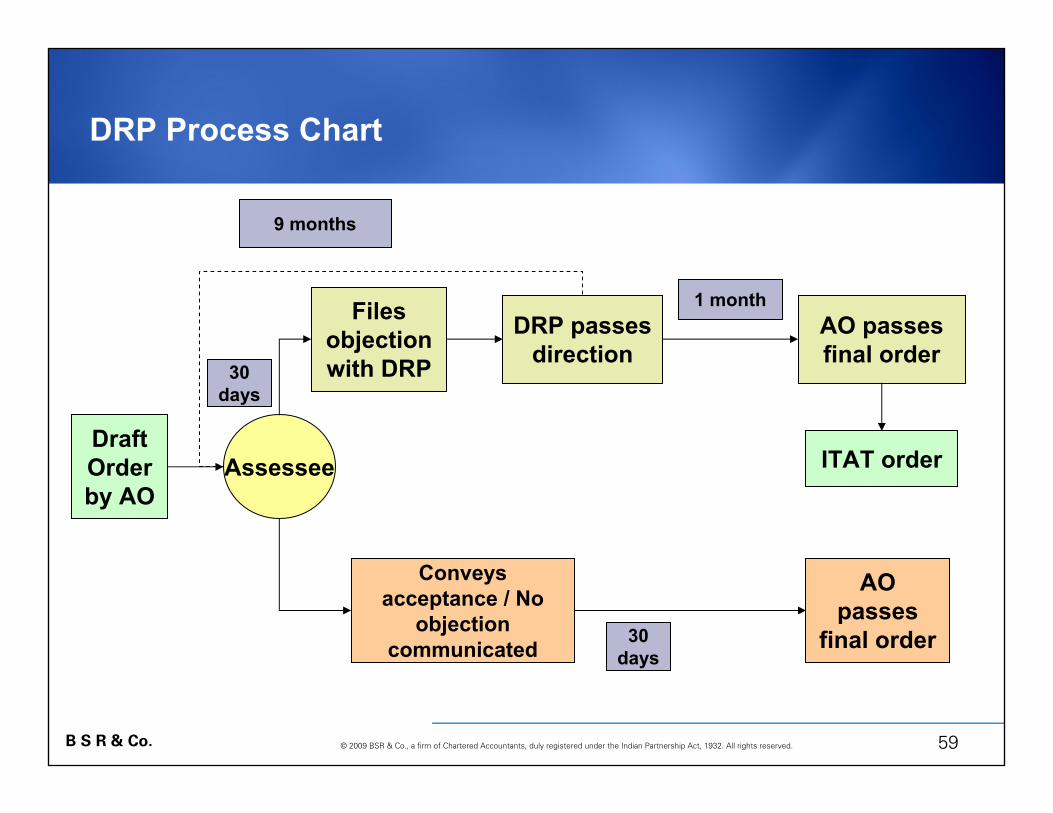

DRP Process Chart

Draft Order by AO

ITAT order

Files objection with DRP

Conveys acceptance / No

objection communicated

DRP passes direction

AO passes final order

Assessee

AO passes

final order

30 days

9 months

1 month

30 days

60B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

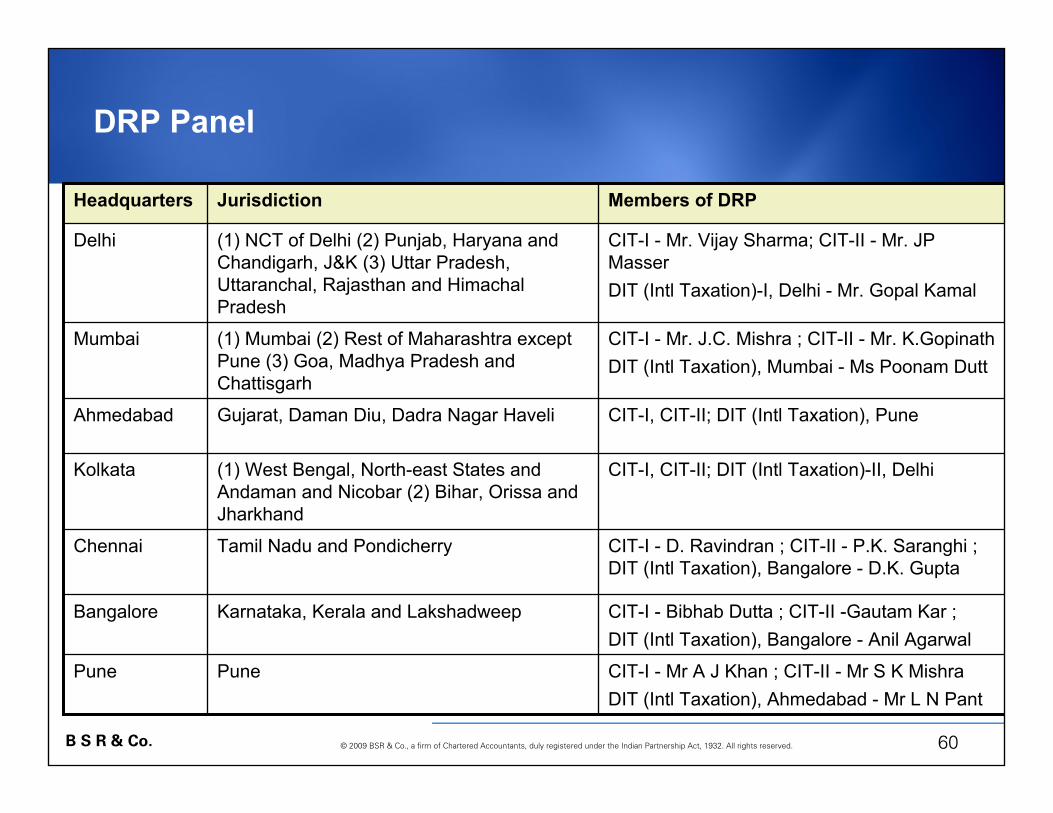

CIT-I - Mr A J Khan ; CIT-II - Mr S K Mishra DIT (Intl Taxation), Ahmedabad - Mr L N Pant

PunePune

CIT-I - Bibhab Dutta ; CIT-II -Gautam Kar ; DIT (Intl Taxation), Bangalore - Anil Agarwal

Karnataka, Kerala and LakshadweepBangalore

CIT-I - D. Ravindran ; CIT-II - P.K. Saranghi ; DIT (Intl Taxation), Bangalore - D.K. Gupta

Tamil Nadu and Pondicherry Chennai

CIT-I, CIT-II; DIT (Intl Taxation)-II, Delhi(1) West Bengal, North-east States and Andaman and Nicobar (2) Bihar, Orissa and Jharkhand

Kolkata

CIT-I, CIT-II; DIT (Intl Taxation), PuneGujarat, Daman Diu, Dadra Nagar HaveliAhmedabad

CIT-I - Mr. J.C. Mishra ; CIT-II - Mr. K.Gopinath DIT (Intl Taxation), Mumbai - Ms Poonam Dutt

(1) Mumbai (2) Rest of Maharashtra except Pune (3) Goa, Madhya Pradesh and Chattisgarh

Mumbai

CIT-I - Mr. Vijay Sharma; CIT-II - Mr. JP Masser DIT (Intl Taxation)-I, Delhi - Mr. Gopal Kamal

(1) NCT of Delhi (2) Punjab, Haryana and Chandigarh, J&K (3) Uttar Pradesh, Uttaranchal, Rajasthan and Himachal Pradesh

Delhi

Members of DRPJurisdiction Headquarters

DRP Panel

61B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Potential Benefits and Open issues

Potential BenefitsSpecialist panel

Speedy resolution – Time-bound

Direct appeal to ITAT by assessee

Department cannot appeal against the DRP directions

No demand till AO issues final order based on directions of DRP

Open IssuesDRP yet to become functional

If AO does not make a reference to TPO – Appeal only to CIT(A)

If AO does not file a reply – appeal will lie before CIT(A)?

Does 144C need to be complied with in case of remand by ITAT

If DRP does not give directions within the period mandated ?

Revision proceedings

62B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Advance Pricing Arrangement

Upfront determination of an arm’s length price (ALP)

The Board would be empowered to make further adjustments to the price determined as per the transfer pricing rules.

APA term would be limited to a maximum term of five consecutive financial years.

The APA would be binding on the taxpayer and the tax authorities, and only in respect of the international transactions for which the agreement is sought.

63B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

(2) Evaluation and

Analysis

(4) Competent Authority

(3) Negotiation

(1) Pre Filing /

Filing

APA Administration

(5) Drafting of the

APA

APA Process

64B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Pros and Cons of entering into an APA

May affect established working relationships with local tax authorities

Cooperative process with experienced professionals considering the case

Exposes all aspects of the business because of voluntary nature of the process

Flexibility developing practical approaches for complex problems

Changes in the business during the APA term may reduce its applicability or necessitate modification/potential revocation

Ability to discuss considerations in a pre-filing meeting, which some countries permit on an anonymous basis

Can take multiple years to finalize Reduces the need for documentation and costs associated with audit and appeals over APA term

Initial APA submission preparation cost may be high relative to annual documentation costs

Low annual reporting cost and certainty with respect to outcome of covered transactions during the APA term

ConsPros

65B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Proposals relating to TP Assessment – DTC

Dispute Resolution Mechanism retained – However only for cases of adjustments exceeding INR 2.5 million.

Form 3CEB lodged directly with the TPO instead of the AO.

Selection of TP audit through risk management strategy framed by the Board. Such strategy or criteria will not be made public.

Change in timelines of submission of certificate, commencement and completion of scrutiny

Best judgement assessment if assessee does not cooperate

66B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Other proposals

Definition of Associated Enterprises widened –Threshold criteria reduced:-

Direct and indirect participation – 10% from 26%loan to asset ratio – reduced to 26% from 51%nomination of director – more than 1/3rd from half

Concept of impermissible avoidance arrangements introduced – thin capitalization.

Safe Harbor provisions retained

Penalty provisions eased

67B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Parting thoughts

Formation of Dispute Resolution Panel, Safe Harbour Mechanism, APA procedure, Risk based assessments are welcome steps in the right direction

Effectiveness of the above proposals would depend on the global best practices adopted by the revenue authorities and the preparedness of the taxpayers.

68B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Questions

69B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Thank YouContact detailsContact details

Name :A. PradeepName :A. Pradeep

Designation :Senior ManagerDesignation :Senior Manager

Email :Email :[email protected]@kpmg.com

Tel: +9940017061Tel: +9940017061

B S R & Co. © 2009 B S R and Co, a firm of Chartered Accountants. All rights reserved.

70B S R & Co. © 2009 BSR & Co., a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.B S R & Co. © 2009 B S R and Company, a firm of Chartered Accountants, duly registered under the Indian Partnership Act, 1932. All rights reserved.

Mumbai

Kamala Mills Compound,448, Senapati Bapat Marg,Lower Parel,Mumbai 400 013Tel +91 22 3983 6000Fax +91 22 24913132

New Delhi

Building No.10, Tower B, 8th Floor, DLF Cyber City,Phase – II,Gurgaon 122002 HaryanaTel +91 124 3074000Fax +91 124 2549101

Bangalore

Solitaire, 139/26, 3rd Floor, Inner Ring Road,Kormangala,Bangalore 560071Tel +91 80 3980 6000Fax +91 80 3980 6999

Hyderabad

8-2-618/2Reliance Humsafar, 4th Floor,Road No. 11, Banjara Hills,Hyderabad 500 034Tel +91 40 6630 5000Fax +91 40 6630 5299

Chennai

No. 10 Mahatma Gandhi Road, Nungambakam, Chennai 600 034Tel +91 40 3914 5000Fax +91 40 3914 5999

Kolkata

Park Plaza, 6TH FloorBlock F, 71 Park StreetKolkata 700 016Tel +91 33 2217 2858Fax +91 33 2217 2868

Pune

703, Godrej Castlemaine, Bund Garden,Pune 411 001Tel +91 20 305 85764/65Fax +91 20 305 85775

Kochi

4/F, Palal Towers M.G.Road, Ravipuram, Kochi 682 016 Tel +91 484 309 4120 Fax +91 484 309 4121