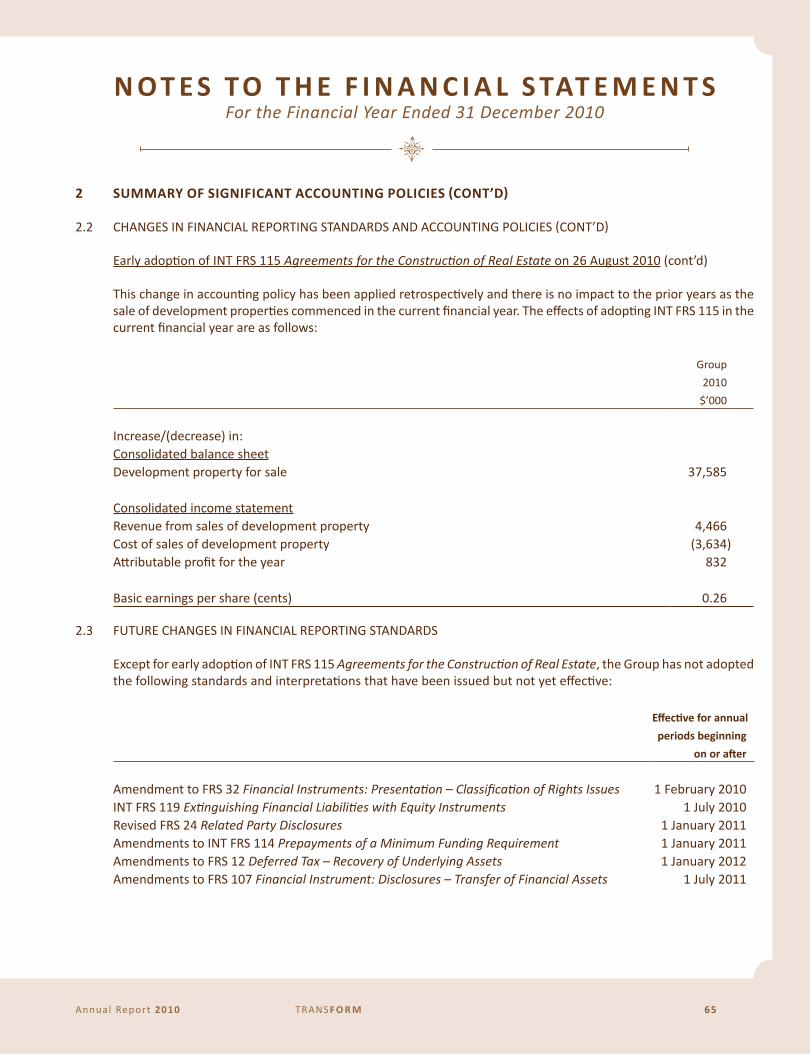

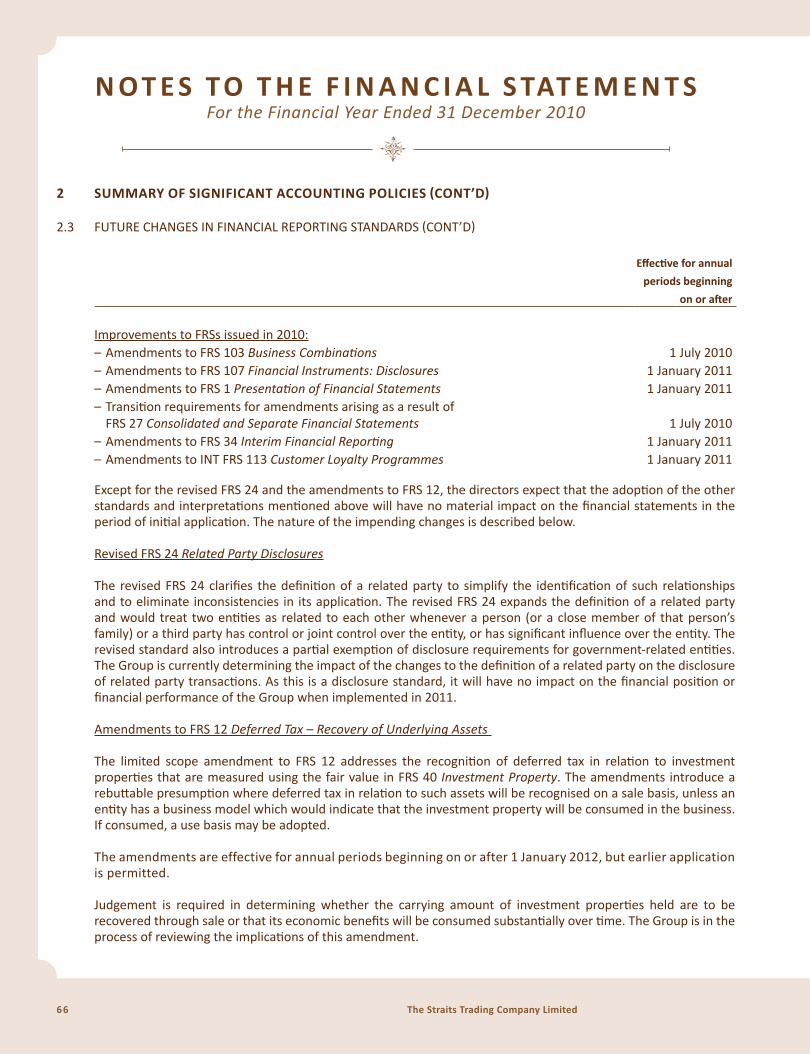

transform -...

TRANSCRIPT

TRANSFORMAnnuAl RepoRt 2010

C O N T E N T S04.

Chairman’s Statement

10. Board of Directors

14. Key Personnel

18. Group Financial Highlights

22. Corporate Information

23. Corporate Social

Responsibility

28. Business Review

37. Corporate Governance

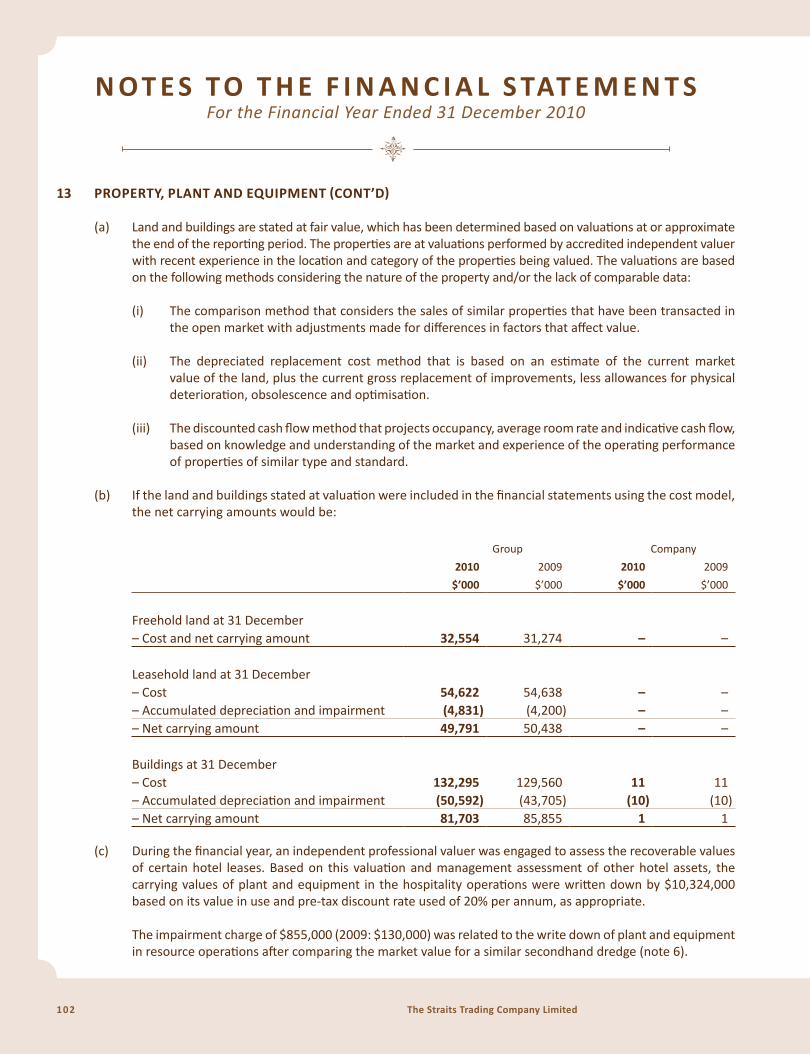

45. Financial Report

Annual Report 2010 tRAns F O R m 1

Change, in its essence, is cultivated through the process of

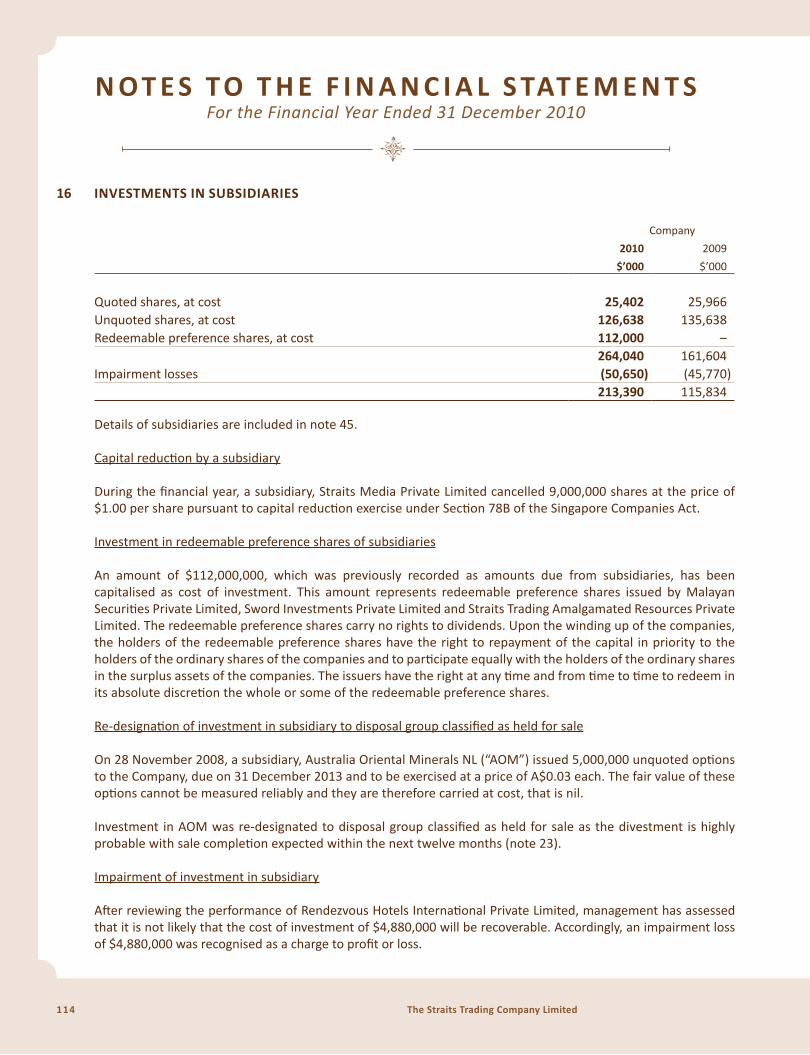

time. And Straits Trading’s vision to become a Corporate

Transformer is by no means any different. Some successes

are achieved overnight, but building a legacy takes time.

Building upon last year’s theme of transformation, this year’s

annual report is an extension of the origami concept to

symbolise our ongoing process of transformation and growth.

Just as it takes time and skill to craft a single piece of paper

into a work of art, we dedicate our efforts to constantly

mould and develop our investments into businesses of

enhanced value. With each experience bringing us closer to

fulfilling our vision, we invite you to join us once again as we

continue this journey of transformation.

O R i G a m i

t R A n s F O R mJust as the unassuming caterpillar morphs into

a majestic butterfly, we seek to nurture our investments and transform them to businesses that deliver greater yield.

2 The Straits Trading Company Limited

The Butterfly is a symbol of transformation.

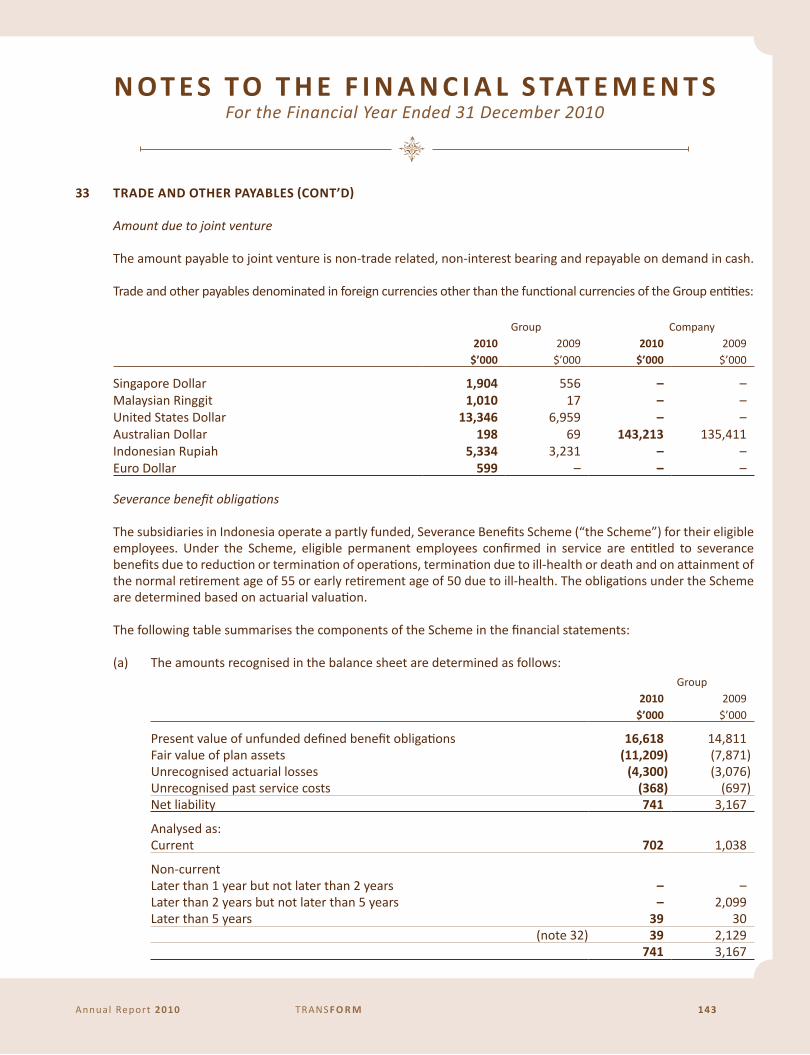

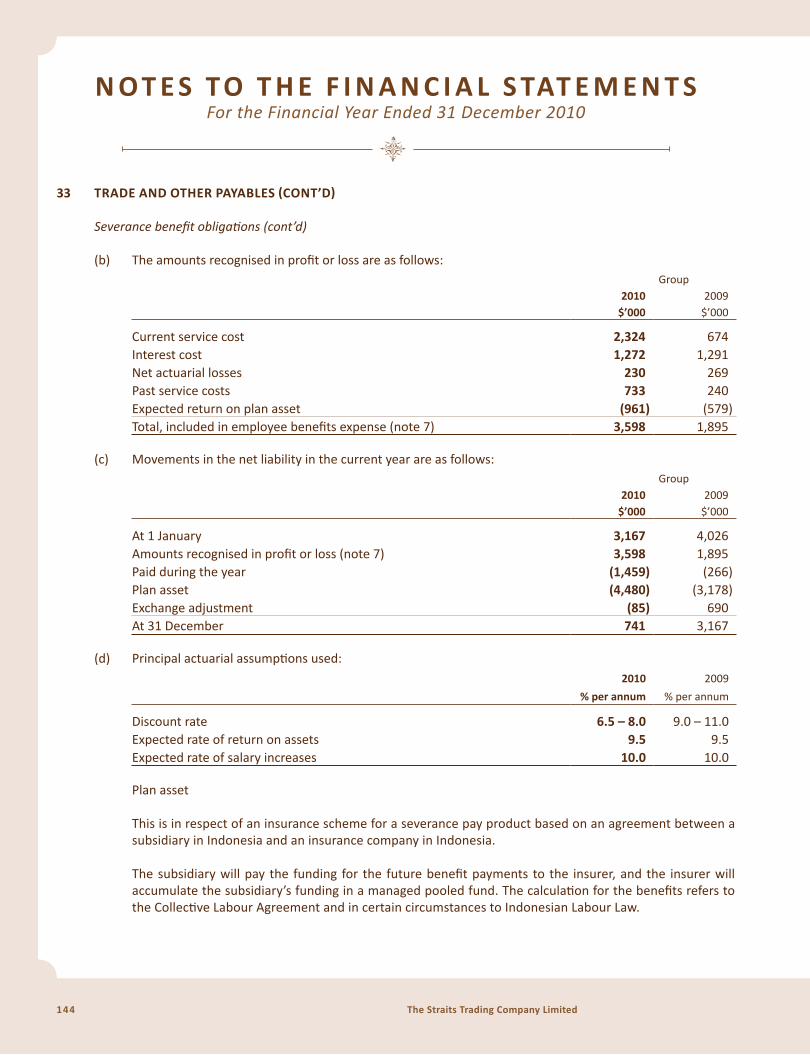

A metamorphosis that represents eminence and beauty, it is the process

of change in its most elegant form.

Annual Report 2010 tRAns F O R m 3

Chew Gek KhimExecutive Chairman

The Straits Trading Company Limited

4 The Straits Trading Company Limited

ChAirmAn’S S TaT E m E N T

2010 saw Straits Trading Company Limited (STC) continue its transformation and growth, with total revenues increasing by

41.5% to S$1.4 billion from S$971.6 million in 2009. This jump in revenues arose mainly from our resources and hospitality divisions.

The recovery in the global economy from the global financial crisis also saw global tourism pick up, resulting in improved occupancies in Asia and Australia, contributing to improved

revenue from our hospitality division.

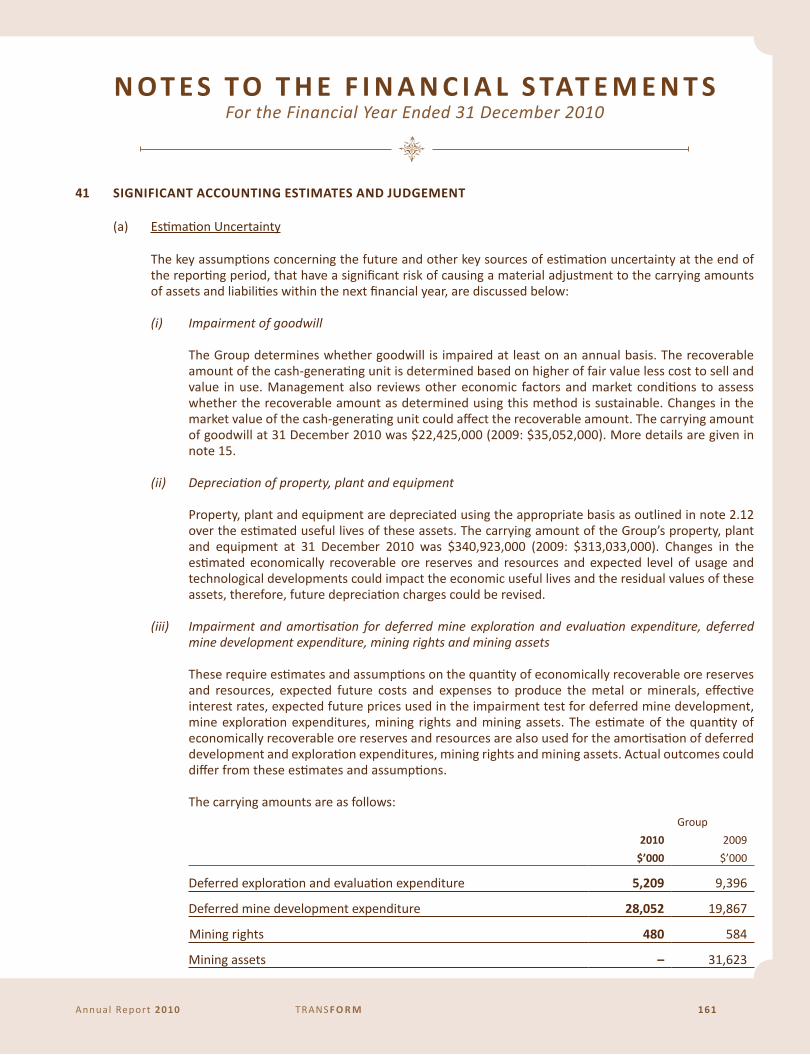

The strong demand for tin, which is extensively used in the electronics industry, saw average tin prices rise to US$20,362 per tonne in 2010 from US$13,469 per tonne in 2009. mSC therefore benefited from higher sales from tin mining and smelting due to higher tin prices on a higher business volume.

The recovery in the global economy from the global financial crisis also saw global tourism pick up, resulting in improved occupancies in Asia and Australia, contributing to improved revenue from our hospitality division.

As articulated in previous years, STC’s objective is to reposition each business as an “engine of growth”. As part of this transformation, and in order to ensure longer term sustainability, the Board decided that a cautious stand should be taken with regard to those aspects of the businesses that were underperforming. hence after careful deliberation, the Board decided to adopt a prudent stance and make provisions for certain underperforming hotel contracts and non-tin investments in the accounts.

As a consequence of these exceptional impairment provisions of S$95.3 million made for the resource and hospitality divisions in 2010, profit before tax for the STC Group fell 87.2% to S$23.9 million for 2010 from S$187.4 million for 2009 and earnings per share fell to 8.6 cents for 2010 from 48.9 cents for 2009. Excluding exceptional items, the decrease was 43.7% to S$13.3 million in 2010 from S$23.6 million in 2009, largely as a result of losses from our hospitality division and lower contributions from property development and financial assets.

notwithstanding the significant provisions for impairments, STC managed to turn in a profit, resulting in net asset value per share increasing to S$3.52 as at 31 December 2010 from S$3.43 as at 31 December 2009.

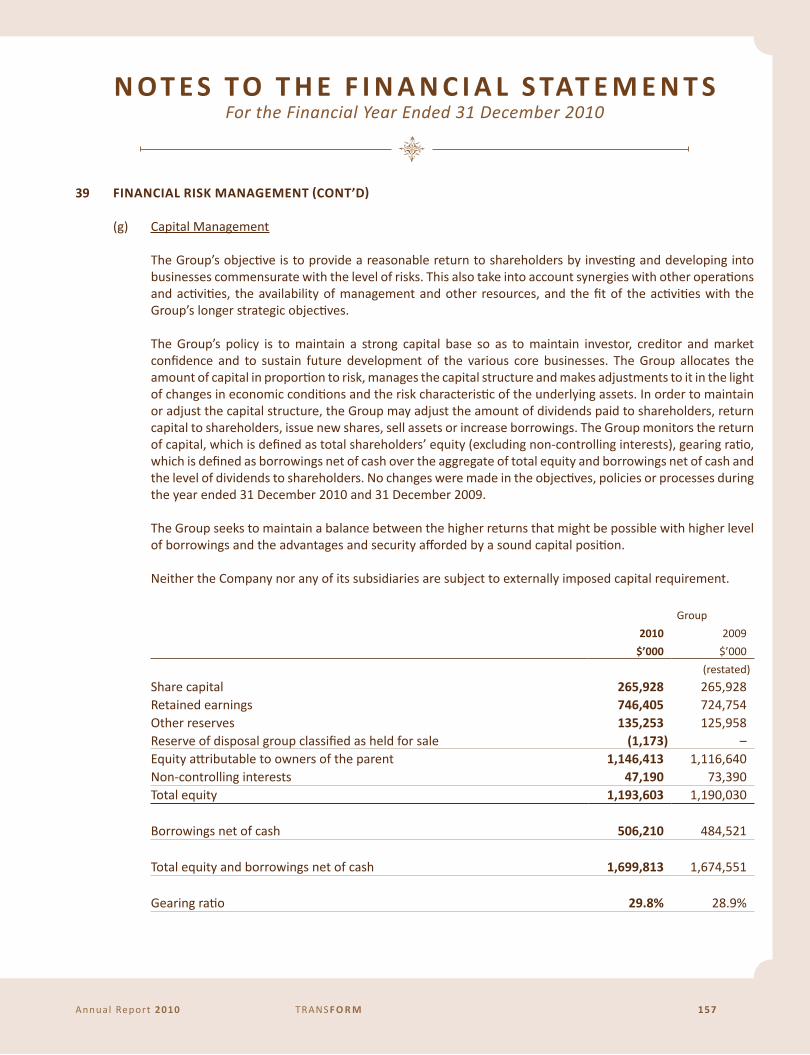

Fiscal discipline continues to be a key tenet and we have kept a tight rein on our borrowings to maintain a strong financial position. As a result, our net gearing ratio increased marginally to 29.8% as at 31 December 2010 from 28.9% as at 31 December 2009. Excluding net borrowings of the mSC Group, the net gearing ratio was a conservative 18.0% as at 31 December 2010, a slight increase from 17.1% as at 31 December 2009.

PROPERTyin 2009, an analytical review of the Group’s real estate portfolio was undertaken in 2009 with the objective of maximising value and in the same year, the redevelopment of STC’s flagship Straits Trading Building at 9 Battery road was completed and 44 units of Gallop Gables were sold.

in 2010, we articulated and implemented the strategy to reposition STC as a niche developer and owner of high-end lifestyle properties.

Annual Report 2010 tRAns F O R m 5

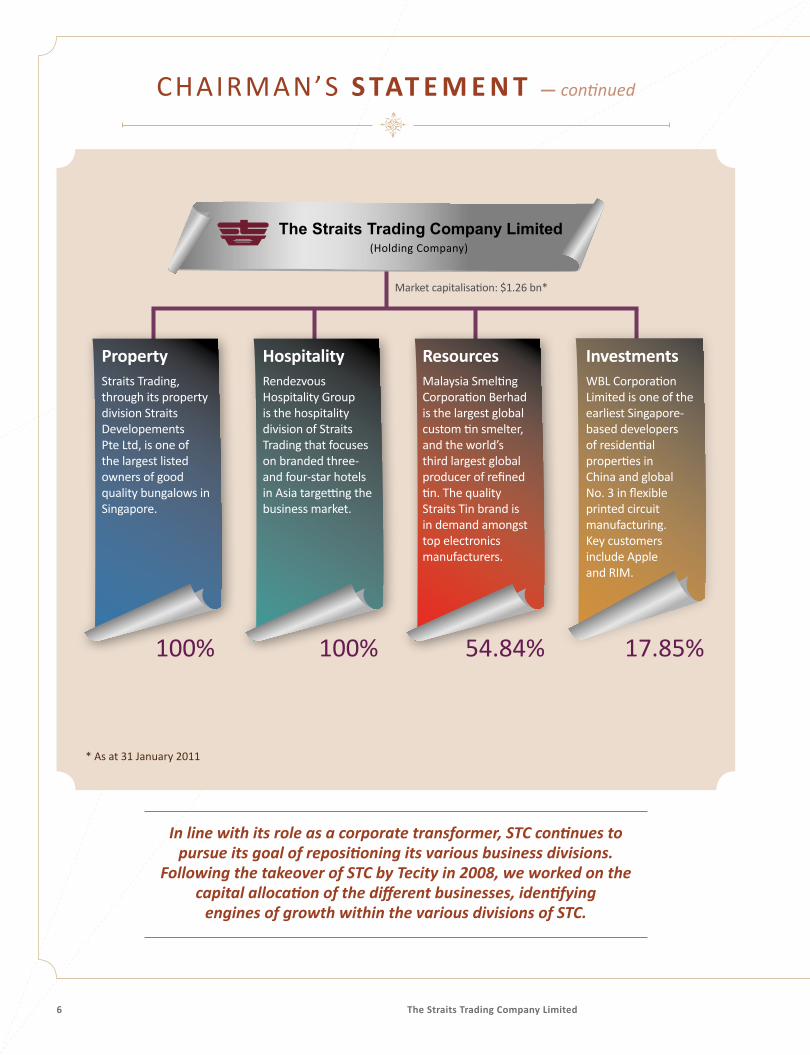

In line with its role as a corporate transformer, STC continues to pursue its goal of repositioning its various business divisions.

Following the takeover of STC by Tecity in 2008, we worked on the capital allocation of the different businesses, identifying

engines of growth within the various divisions of STC.

* As at 31 January 2011

17.85%54.84%100%100%

market capitalisation: $1.26 bn*

investmentsWBL Corporation Limited is one of the earliest singapore-based developers of residential properties in China and global no. 3 in flexible printed circuit manufacturing. Key customers include Apple and rim.

Resourcesmalaysia Smelting Corporation Berhad is the largest global custom tin smelter, and the world’s third largest global producer of refined tin. The quality Straits Tin brand is in demand amongst top electronics manufacturers.

Hospitality rendezvous hospitality Group is the hospitality division of Straits Trading that focuses on branded three- and four-star hotels in Asia targetting the business market.

PropertyStraits Trading, through its property division Straits Developements Pte Ltd, is one of the largest listed owners of good quality bungalows in Singapore.

(holding Company)

ChAirmAn’S S TaT E m E N T — continued

6 The Straits Trading Company Limited

2010 saw the repositioning of MSC as a pure tin smelter and producer. MSC continues

to pursue its strategy into 2011 by focusing efforts into making MSC a vertically integrated player in the tin space with both

mining and smelting businesses.

in 2010, Taiko-Straits Developments Sdn Bhd, a joint venture between Taiko Development Sdn Bhd and STC launched the Thompson-Flora Tropika residences in ipoh comprising 47 luxurious freehold bungalows. A review of our land bank in malaysia has led us to formulate clear plans for the development of residential/commercial projects in various states in malaysia, which will be announced in due course.

STC also initiated development work on two of our five remaining plots of vacant bungalow land in Singapore. The completion of these bungalows in 2011 will make STC one of the listed companies with the largest portfolio of “good class” bungalows in Singapore, the supply of which is currently limited in Singapore.

in 2011, we will complete our Five Chancery project which comprises 12 high-end Strata Bungalows near the premier Anglo Chinese School (ACS). in addition, we have invested in 14 units of The holland Collection, a well-located high-end luxury freehold residential development.

maLaySia SmELTiNG CorporatIon Berhad (MSC)2010 saw the repositioning of mSC as a pure tin smelter and producer. mSC continues to pursue its strategy into 2011 by focusing efforts into making mSC a vertically integrated player in the tin space with both mining and smelting businesses.

Following the successful secondary listing of mSC on the Singapore Exchange on 27 January 2011, STC’s shareholding in mSC decreased from 72% to 54%. mSC’s successful listing makes it the first company in 13 years to be listed in both Singapore and malaysia. Cross-listing on both exchanges stopped in the late 1998[*] after Singapore and malaysian firms were delisted from each other’s exchanges after the split between Kuala Lumpur

Stock Exchange and the Stock Exchange of Singapore. This will help position mSC for growth in its core business of tin. it is my sincere hope that this secondary listing will be the corporate exemplification and a logical continuation of improved governmental, diplomatic and political ties between Singapore and malaysia.

Further details of the business of mSC can be found in the section headed “Business review” under the segment headed “Perform”.

RENDEzvOuS HOSPiTaLiTy Group (rhG)Against the backdrop of a strong rebound in global tourism, the revenue for the hospitality division increased in 2010 from 2009.

however, this was not reflected in profitability and a review of the performance of our hospitality division led us to focus on its management and operations.

To recapitulate, the strategy for rhG as articulated last year was to focus on being a branded three-and-a-half to four-and-a-half star business hotel chain in key cities, targeting the business market. rhG will persevere with this strategy of focusing on the business traveler and the corporate segment; working to improve its product and service in the three-and-a-half to four-and-a-half star market.

Annual Report 2010 tRAns F O R m 7

ChAirmAn’S S TaT E m E N T — continued

however, a sound strategy requires proper execution and sound implementation to achieve the desired objective. in this regard, a management board comprising senior executives and advisors was formed to oversee the hospitality business with a view to creating a clearer brand, identifying areas of inefficiency, improving operational effectiveness and creating a leaner and nimbler organisation in the process so as to ultimately raise the operating performance of this division.

2011 will therefore mark a year of change for the hospitality division and work is already underway as we streamline the business and increase productivity. The Board of STC has made a prudent assessment of the business and appropriate provisions have been taken in the accounts for the financial year ended 2010.

Following an assessment of our hotel properties, the Company decided that one of the approaches to transform the business is to invest in value accretive capital expenditure. We are in the process of refurbishing our hotels (as detailed in the business review section) and it is anticipated that upon completion, our hospitality division will have a stronger brand presence, better customer experience and

increased occupancies and rates resulting in improved profitability.

WBL CORPORaTiON LimiTEDin 2009, we consolidated our investments into one company, WBL Corporation Limited, and increased our shareholdings in WBL to 18.9% as at 31 December 2009. All four of WBL’s core divisions comprising Technology, Automotive, Property and Engineering and Distribution continued to perform profitably for the financial year ended 30 September 2010. WBL paid out a total dividend of 10 cents per share in 2010, compared with 8.5 cents in 2009.

DiviDENDSWe have maintained our interim dividend payout of two-cents per share.

uNLOCKiNG vaLuEin line with its role as a corporate transformer, STC continues to pursue its goal of repositioning its various business divisions. Following the takeover of STC by Tecity in 2008, we worked on the capital allocation of the different businesses, identifying engines of growth within the various divisions of STC. in 2009 we worked on repositioning the Property Division as a niche developer and owner of high-end lifestyle properties. in 2010, we repositioned mSC as a vertically integrated player in the tin space. 2011 will see us working on repositioning rhG as a branded three-and-a-half to four-and-a-half star business hotel chain targeted at the business market and focusing on improving its operational efficiency.

We have also announced that STC is considering a secondary listing on the main market of Bursa malaysia Securities Berhad (Bursa listing). This is in line with our view that the proposed Bursa

In 2009 we worked on repositioning the Property Division as a niche developer and

owner of high-end lifestyle properties. In 2010, we repositioned MSC as a vertically integrated

player in the tin space. 2011 will see us working on repositioning RHG as a branded three-and-a-half to four-and-a-half star business hotel chain targeted at the business market and focusing

on improving its operational efficiency.

8 The Straits Trading Company Limited

listing will enhance the public profile of STC, and provide us with an additional channel to raise capital for future expansion of our significant business activities in both Singapore and malaysia.

2011 aND BEyONDThe global landscape in 2011 will be challenging. Japan’s devastating earthquake, tsunami and deepening nuclear crisis, the unexpected and slowly spreading tide of political unrest and change in the middle East, the growing deficit and financial problems confronting Europe as well as the rising prices of food and fuel will affect the global economy, but the impact and extent of each of these different events on the economy and business remain to be seen.

however, we remain cautiously optimistic about the performance of the Company. With most of our repositioning and write-offs done in 2010, and having put in place the infrastructure roadmaps for realising our vision of transforming our investments into businesses of enhanced value, we are hopeful of a positive performance in 2011.

CHaNGES TO THE ExECuTivE TEamWe are pleased to welcome mr Quah Ban huat into STC as the Chief investment Officer and are sorry to see mr iqbal Jumabhoy leave rhG to pursue his personal interests. We wish to thank mr Jumabhoy for his hard work and contributions to the Group. mr Eric Teng’s responsibilities have expanded to cover both the Property and hospitality divisions.

i wish to thank my fellow Directors, all the Company’s shareholders, advisors, business associates, financiers, clients and customers for their strong and consistent support and all staff for their commitment and professionalism as we continue to transform and grow.

Chew Gek KhimExecutive Chairman28 march 2011

* reference from the Monetary Authority of Singapore, “Deputy Prime Minister Lee’s reply to Parliament question on CLOB, dated 12 October 1998”.

Annual Report 2010 tRAns F O R m 9

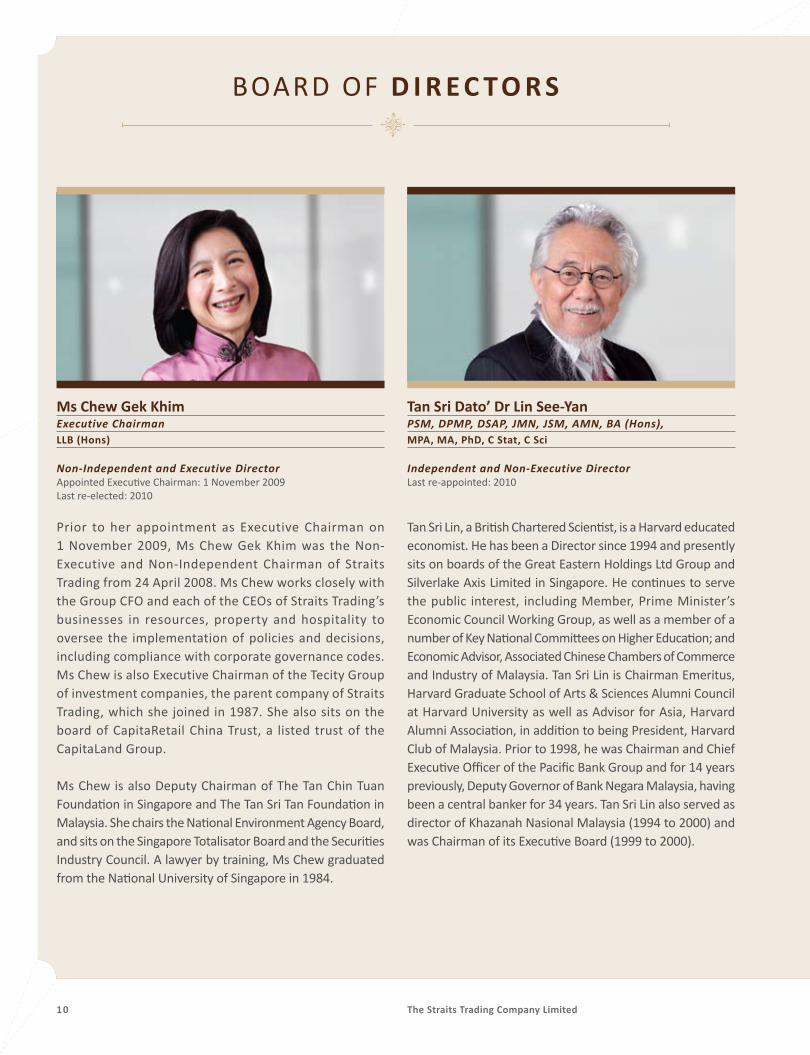

Ms Chew Gek KhimExecutive ChairmanLLB (Hons)

Non-Independent and Executive DirectorAppointed Executive Chairman: 1 november 2009Last re-elected: 2010

Tan Sri Dato’ Dr Lin See-yanPSM, DPMP, DSAP, JMN, JSM, AMN, BA (Hons),Mpa, Ma, phd, C Stat, C Sci

Independent and Non-Executive DirectorLast re-appointed: 2010

Prior to her appointment as Executive Chairman on 1 november 2009, ms Chew Gek Khim was the non-Executive and non-independent Chairman of Straits Trading from 24 April 2008. ms Chew works closely with the Group CFO and each of the CEOs of Straits Trading’s businesses in resources, property and hospitality to oversee the implementation of policies and decisions, including compliance with corporate governance codes. ms Chew is also Executive Chairman of the Tecity Group of investment companies, the parent company of Straits Trading, which she joined in 1987. She also sits on the board of Capitaretail China Trust, a listed trust of the CapitaLand Group.

ms Chew is also Deputy Chairman of The Tan Chin Tuan Foundation in Singapore and The Tan Sri Tan Foundation in malaysia. She chairs the national Environment Agency Board, and sits on the Singapore Totalisator Board and the Securities industry Council. A lawyer by training, ms Chew graduated from the national University of Singapore in 1984.

Tan Sri Lin, a British Chartered Scientist, is a harvard educated economist. he has been a Director since 1994 and presently sits on boards of the Great Eastern holdings Ltd Group and Silverlake Axis Limited in Singapore. he continues to serve the public interest, including member, Prime minister’s Economic Council Working Group, as well as a member of a number of Key national Committees on higher Education; and Economic Advisor, Associated Chinese Chambers of Commerce and industry of malaysia. Tan Sri Lin is Chairman Emeritus, harvard Graduate School of Arts & Sciences Alumni Council at harvard University as well as Advisor for Asia, harvard Alumni Association, in addition to being President, harvard Club of malaysia. Prior to 1998, he was Chairman and Chief Executive Officer of the Pacific Bank Group and for 14 years previously, Deputy Governor of Bank negara malaysia, having been a central banker for 34 years. Tan Sri Lin also served as director of Khazanah nasional malaysia (1994 to 2000) and was Chairman of its Executive Board (1999 to 2000).

BOArD OF D i R E C TO R S

10 The Straits Trading Company Limited

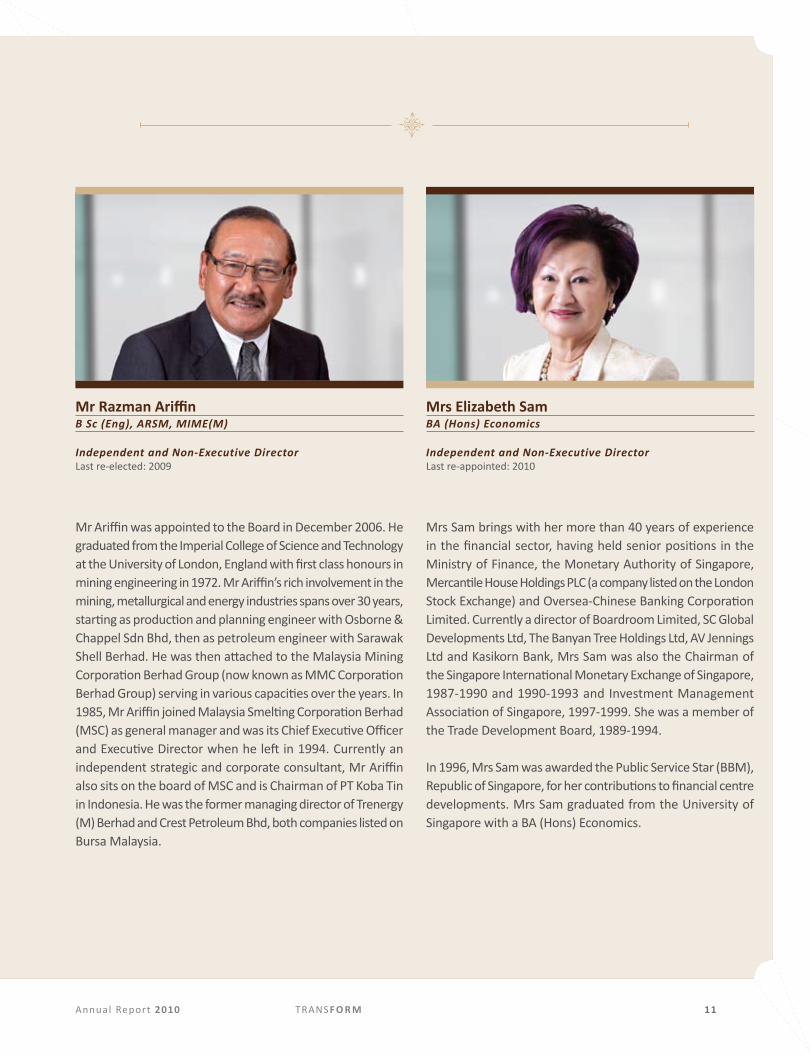

mrs Elizabeth SamBA (Hons) Economics

Independent and Non-Executive DirectorLast re-appointed: 2010

mrs Sam brings with her more than 40 years of experience in the financial sector, having held senior positions in the ministry of Finance, the monetary Authority of Singapore, mercantile house holdings PLC (a company listed on the London Stock Exchange) and Oversea-Chinese Banking Corporation Limited. Currently a director of Boardroom Limited, SC Global Developments Ltd, The Banyan Tree holdings Ltd, AV Jennings Ltd and Kasikorn Bank, mrs Sam was also the Chairman of the Singapore international monetary Exchange of Singapore, 1987-1990 and 1990-1993 and investment management Association of Singapore, 1997-1999. She was a member of the Trade Development Board, 1989-1994.

in 1996, mrs Sam was awarded the Public Service Star (BBm), republic of Singapore, for her contributions to financial centre developments. mrs Sam graduated from the University of Singapore with a BA (hons) Economics.

Mr razman ariffinB Sc (Eng), ARSM, MIME(M)

Independent and Non-Executive DirectorLast re-elected: 2009

mr Ariffin was appointed to the Board in December 2006. he graduated from the imperial College of Science and Technology at the University of London, England with first class honours in mining engineering in 1972. mr Ariffin’s rich involvement in the mining, metallurgical and energy industries spans over 30 years, starting as production and planning engineer with Osborne & Chappel Sdn Bhd, then as petroleum engineer with Sarawak Shell Berhad. he was then attached to the malaysia mining Corporation Berhad Group (now known as mmC Corporation Berhad Group) serving in various capacities over the years. in 1985, mr Ariffin joined malaysia Smelting Corporation Berhad (mSC) as general manager and was its Chief Executive Officer and Executive Director when he left in 1994. Currently an independent strategic and corporate consultant, mr Ariffin also sits on the board of mSC and is Chairman of PT Koba Tin in indonesia. he was the former managing director of Trenergy (m) Berhad and Crest Petroleum Bhd, both companies listed on Bursa malaysia.

Annual Report 2010 tRAns F O R m 11

mr David Goh Kay yongBA (Hons), SM (MIT), CFA

Non-Independent and Non-Executive DirectorLast re-elected: 2009

mr Goh is the Chief investment Officer and Chief Strategist of the Tecity Group of investment companies, the parent company of Straits Trading Company. mr Goh started his investment career as an investment Analyst with Great Eastern Life in 1986, and taught at the nanyang Technological University (nTU), Singapore in the Bachelor of Business Financial Analyst programme in 1991. After joining Tecity Group in 1997, he remained from 1997-2003 as Adjunct Associate Professor of Finance at nTU. Presently the non-executive chairman of Yeoman Capital management Pte Ltd (an exempt fund manager), mr Goh also serves as director of Pastamatrix international Pte Ltd, Stewardship Capital Pte Ltd, Stewardship Equity Pte Ltd, and nPE Print Communications Pte Ltd. mr Goh holds a Bachelor of Arts (hons) degree in Economics from York University, Canada; a master of Science in management (System Dynamics, Finance and Strategy) from massachusetts institute of Technology’s Sloan School of management, as well as a CFA Charter.

BOArD OF D i R E C TO R S — continued

Ms Chew Gek hiangB Acc (Hons), CPA

Non-Independent and Non-Executive DirectorLast re-elected: 2009

An accountant by training, ms Chew has been with the Tecity Group of private investment companies, the parent company of Straits Trading Company, since 1991. As Executive Director and head of Finance, she is actively involved in the investment activities of the Tecity Group and is responsible for its securities trading portfolio. She also oversees the human resource and administrative functions in the Tecity Group. Currently serving on the advisory panel of the GST review Board, ms Chew is also a Council member of The Tan Chin Tuan Foundation in Singapore and The Tan Sri Tan Foundation in malaysia. She is also President of noah’s Ark CArES (Companion Animal rescue and Education Society), a non-profit animal welfare society which champions responsible pet ownership and active sterilisation and microchipping of stray dogs and cats in Singapore and Johor.

ms Chew graduated from the national University of Singapore in 1986. She joined Ernst & Young (London) in 1987 to pursue her chartered accountancy, and was admitted to the institute of Chartered Accountants in England and Wales in October 1990.

12 The Straits Trading Company Limited

mr yap Chee KeongB acc, FCpa

Lead Independent DirectorLast re-elected: 2010

mr Yap Chee Keong was appointed as the Lead independent Director of Straits Trading Company with effect from 1 november 2009. mr Yap is an independent non-executive director of Capitamalls Asia Limited and the chairman of its audit committee. he is also an independent non-executive director of hup Soon Global Corporation Limited and Tiger Airways holdings Ltd and chairs the remuneration committee of Tiger Airways holdings Ltd. in addition, he serves as a Board member of the Accounting and Corporate regulatory Authority and as a non-executive director of SPi (Australia) Assets Pty Ltd and chairman of Singapore District Cooling Pte Ltd. mr Yap was previously Chief Financial Officer of the Singapore Power Group (SP) where he was also responsible for corporate planning and strategic investments as well as oversight of the overseas investments of SP which included its Australian investments. Prior to SP, mr Yap worked as the chief financial officer and in other senior management roles in several multinational and listed companies. mr Yap has 25 years of experience in senior management, strategic planning, merger and acquisitions, corporate finance, treasury, financial management and risk management functions in diverse industries. mr Yap holds a Bachelor of Accountancy from the national University of Singapore and is a Fellow of the institute of Certified Public Accountants of Singapore and CPA Australia.

mr Tham Kui SengBa (hons), engineering Science

Independent and Non-Executive DirectorLast re-elected: 2010

mr Tham is a director of raffles medical Group Ltd, Global Logistic Properties Limited, SPi (Australia) Assets Pty Ltd and Capitaland China holdings Pte Ltd. he also serves on the Board of The housing and Development Board (hDB) and chairs Em Services Private Limited. mr Tham was the former Chief Corporate Officer of CapitaLand Limited overseeing the corporate services functions of the listed real estate group, a position he held from 2002 until 31 December 2008. he also served as the Chief Executive Officer of CapitaLand residential Limited and before that, the Chief Operating Officer of Pidemco Land Limited.

Annual Report 2010 tRAns F O R m 13

mrs maureen LeongGroup Chief Financial Officer

The Straits Trading Company Limited

mrs maureen Leong joined The Straits Trading Company Limited (STC) as its Group Chief Financial Officer (CFO) in September 2009. As Group CFO, mrs Leong has overall responsibility for the Group’s financial functions, including treasury, tax, insurance, risk management and capital management of STC and its group of companies. mrs Leong was appointed to the Board of mSC, a subsidiary of STC, listed on both the main Boards of Bursa and SGX-ST, as a non-independent and non-Executive Director in December 2009.

mrs Leong has more than 30 years of experience in corporate planning and finance, project financing, mergers and acquisitions, treasury, tax, financial management and risk management functions in various industries. She started her career with DBS Bank Ltd before moving on to Deloitte & Touche. Prior to joining STC, mrs Leong was with Sembcorp industries Ltd, where her last appointment was Executive Vice President of Group mergers and Acquisitions, Group Performance management and Corporate Planning of the Sembcorp Group of companies. She was appointed Director, Group Finance of Sembcorp marine Ltd between 2007 and 2008, and Group CFO of Sembcorp Logistics Ltd from 2004 to 2006, after having served as Group CFO of Sembcorp Utilities Pte Ltd. Both Sembcorp industries Ltd and Sembcorp marine Ltd are listed on the main board of SGX-ST.

mrs Leong holds a First Class honours degree in Accountancy from the University of Singapore and is a Fellow of both the institute of Certified Public Accountants of Singapore and CPA Australia.

mr Quah Ban HuatChief Investment Officer

The Straits Trading Company Limited

mr Quah Ban huat was appointed Chief investment Officer (CiO) of The Straits Trading Company Limited (STC) on 1 march 2011. As the CiO, mr Quah is responsible for overseeing the development and execution of investment strategy for STC. in addition, he is also in-charge of all investor relations matters of the Group.

Prior to joining STC, mr Quah was the Chief Financial Officer of the Trustee-manager of rickmers maritime from 2006 to 2010. mr Quah had also worked as the Chief Financial Officer and thereafter the Financial Adviser of City Gas Pte. Ltd., a wholly-owned subsidiary of Temasek holdings (Private) Limited, an investment holding company of the Government of Singapore. After having spent several years in London, mr Quah joined Deutsche Bank in Singapore as their regional Business Area Controller for the investment banking arm. From 2000, he held various key finance positions including Chief Financial Officer at Growasia.com and Group Finance Director of the imC Group, which holds, among others, interests in transportation, real estate and natural resources.

mr Quah has more than 22 years of experience in finance and accounting, including fund raising, listing and initial public offerings, investments, financing and tax planning. he is a member of the institute of Chartered Accountants in England and Wales and a fellow member of the Association of Chartered Certified Accountants.

KEY P E R S O N N E L

14 The Straits Trading Company Limited

yBhg. Dato’ Seri Dr mohd ajib anuarGroup Chief Executive Officer

Malaysia Smelting Corporation Berhad (MSC)

YBhg. Dato’ Seri Dr mohd Ajib Anuar, a malaysian, was first appointed to the Board of mSC, a subsidiary of The Straits Trading Company Limited, as a non-independent non-Executive Director in July 1986, and has been Chief Executive Officer and Executive Director of mSC since June 1994. he has more than 39 years of experience and expertise in the global tin and mineral resources industry. Currently, he serves as the Chairman of the Kuala Lumpur Tin market, the President of the malaysian Chamber of mines and the Chairman of the malaysian Tin industry (research and Development) Board as well as a Director of iTrL Ltd and iTri innovation Ltd, UK (the research and development body of the world’s tin industry).

Prior to his appointment as CEO of mSC, YBhg. Dato’ Seri Dr mohd Ajib Anuar spent 23 years in malaysia mining Corporation Berhad Group of Companies (now known as mmC Corporation Berhad Group of Companies), serving in various senior positions including as the General manager of the Finance Department, Director of Business Development and managing Director of mmC’s international marketing Division. he also served as the President of iTri Ltd, UK (2002-06), the Deputy Chairman of the Kuala Lumpur Commodity Exchange (1988-93) as well as Chairman of the malaysian Futures Clearing Corporation (1990-93).

he holds the professional qualification of the Association of Chartered Certified Accountants, United Kingdom.

mr Eric TengChief Executive Officer (Property & Hospitality)

& Advisor (Marketing and Communications)The Straits Trading Company Limited

mr Eric Teng was first seconded to head Straits Trading’s Property division from its parent company, the Tecity Group on 1 February 2009 before his permanent transfer on 1 January 2010. in his current appointment, mr Teng is responsible for driving the Property division’s strategy, investment, development and operations for Singapore, malaysia and Australia.

On 1 February 2011, mr Teng’s responsibilities was expanded to cover the hospitality division and concurrently, is the Chief Executive Officer of rendezvous hospitality Group (rhG).

mr Teng joined the Tecity Group in 2005 and has remained as an Advisor to the Tan Chin Tuan Foundation, Tan Sri Tan Foundation in malaysia and the Tecity Group after he had relinquished his role as the Chief Executive Officer of both Foundations upon his transfer to Straits Trading.

Before joining the Tecity Group in 2005, mr Teng has distinguished himself in the advertising, marketing and communications industry, where he had worked for more than 20 years.

mr Teng has held leadership positions in various charity and trade organisations, including the YmCA, national Council of Social Service (nCSS), the Tsunami reconstruction and Facilitation Committee (TrFC), and the national Volunteer and Philanthropy Centre (nVPC) and the Association of Accredited Advertising Agents (4As).

For his voluntary contributions, mr Teng was awarded the Public Service medal (PBm) in 2001 by the Singapore Government.

A marketer by training, mr Teng holds professional qualifications in marketing and an mBA from the nUS Business School.

Annual Report 2010 tRAns F O R m 15

i n F O R meffective communication remains the cornerstone of our organisation, and is achieved when the sum of all parts come together. Forging closer ties with

our customers and shareholders will enable us to make informed decisions and move towards a common goal.

16 The Straits Trading Company Limited

The Star is a symbol of direction. Like the north Star that illuminates the

night, it is a constellation that offers guidance and navigation.

Annual Report 2010 tRAns F O R m 17

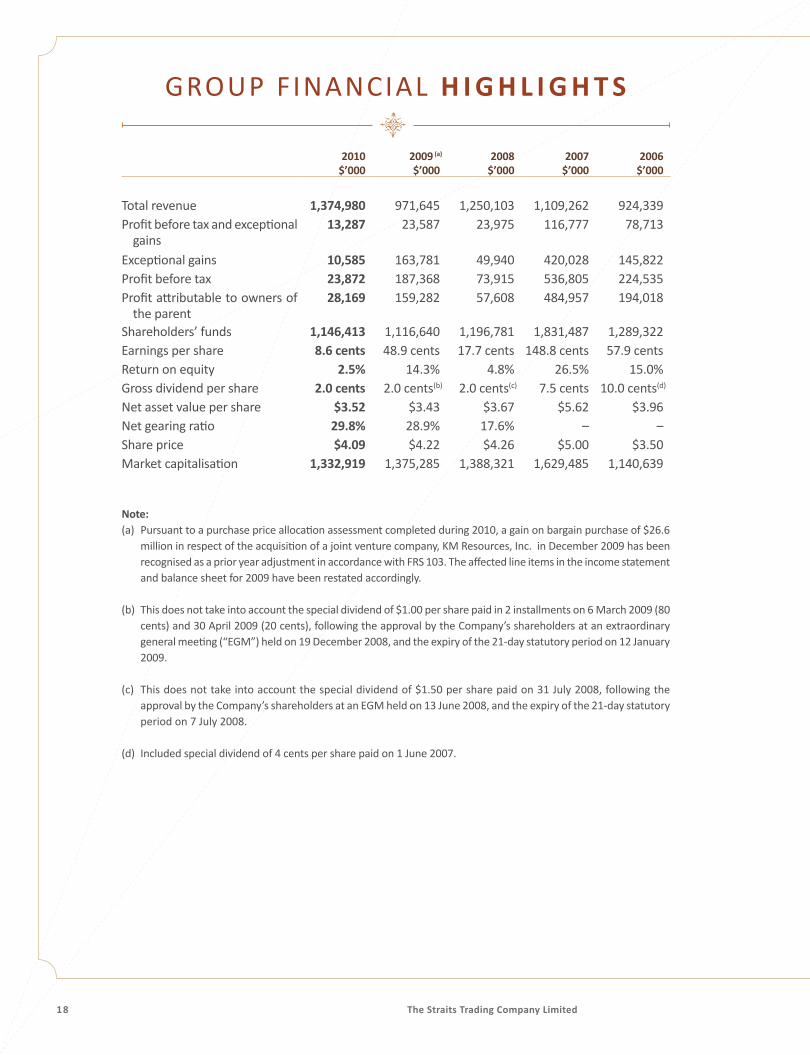

GrOUP FinAnCiAL H i G H L i G H T S

2010 2009 (a) 2008 2007 2006$’000 $’000 $’000 $’000 $’000

Total revenue 1,374,980 971,645 1,250,103 1,109,262 924,339Profit before tax and exceptional

gains13,287 23,587 23,975 116,777 78,713

Exceptional gains 10,585 163,781 49,940 420,028 145,822Profit before tax 23,872 187,368 73,915 536,805 224,535Profit attributable to owners of

the parent28,169 159,282 57,608 484,957 194,018

Shareholders’ funds 1,146,413 1,116,640 1,196,781 1,831,487 1,289,322earnings per share 8.6 cents 48.9 cents 17.7 cents 148.8 cents 57.9 centsreturn on equity 2.5% 14.3% 4.8% 26.5% 15.0%Gross dividend per share 2.0 cents 2.0 cents(b) 2.0 cents(c) 7.5 cents 10.0 cents(d)

net asset value per share $3.52 $3.43 $3.67 $5.62 $3.96net gearing ratio 29.8% 28.9% 17.6% – –share price $4.09 $4.22 $4.26 $5.00 $3.50market capitalisation 1,332,919 1,375,285 1,388,321 1,629,485 1,140,639

Note:(a) Pursuant to a purchase price allocation assessment completed during 2010, a gain on bargain purchase of $26.6

million in respect of the acquisition of a joint venture company, Km resources, inc. in December 2009 has been recognised as a prior year adjustment in accordance with FrS 103. The affected line items in the income statement and balance sheet for 2009 have been restated accordingly.

(b) This does not take into account the special dividend of $1.00 per share paid in 2 installments on 6 march 2009 (80

cents) and 30 April 2009 (20 cents), following the approval by the Company’s shareholders at an extraordinary general meeting (“EGm”) held on 19 December 2008, and the expiry of the 21-day statutory period on 12 January 2009.

(c) This does not take into account the special dividend of $1.50 per share paid on 31 July 2008, following the approval by the Company’s shareholders at an EGm held on 13 June 2008, and the expiry of the 21-day statutory period on 7 July 2008.

(d) included special dividend of 4 cents per share paid on 1 June 2007.

18 The Straits Trading Company Limited

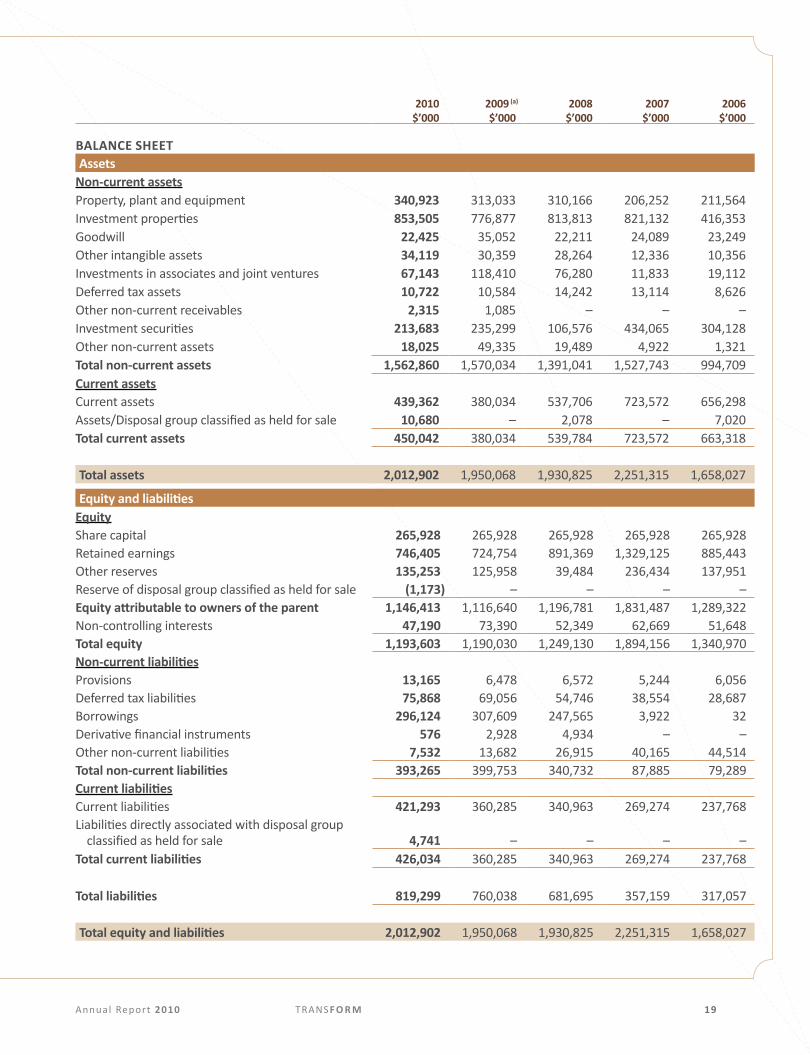

2010 2009 (a) 2008 2007 2006$’000 $’000 $’000 $’000 $’000

BaLaNCE SHEETassets

Non-current assetsProperty, plant and equipment 340,923 313,033 310,166 206,252 211,564investment properties 853,505 776,877 813,813 821,132 416,353Goodwill 22,425 35,052 22,211 24,089 23,249Other intangible assets 34,119 30,359 28,264 12,336 10,356investments in associates and joint ventures 67,143 118,410 76,280 11,833 19,112Deferred tax assets 10,722 10,584 14,242 13,114 8,626Other non-current receivables 2,315 1,085 – – –investment securities 213,683 235,299 106,576 434,065 304,128other non-current assets 18,025 49,335 19,489 4,922 1,321Total non-current assets 1,562,860 1,570,034 1,391,041 1,527,743 994,709Current assetsCurrent assets 439,362 380,034 537,706 723,572 656,298Assets/Disposal group classified as held for sale 10,680 – 2,078 – 7,020Total current assets 450,042 380,034 539,784 723,572 663,318

Total assets 2,012,902 1,950,068 1,930,825 2,251,315 1,658,027

equity and liabilitiesEquity share capital 265,928 265,928 265,928 265,928 265,928retained earnings 746,405 724,754 891,369 1,329,125 885,443Other reserves 135,253 125,958 39,484 236,434 137,951reserve of disposal group classified as held for sale (1,173) – – – –equity attributable to owners of the parent 1,146,413 1,116,640 1,196,781 1,831,487 1,289,322non-controlling interests 47,190 73,390 52,349 62,669 51,648Total equity 1,193,603 1,190,030 1,249,130 1,894,156 1,340,970non-current liabilitiesProvisions 13,165 6,478 6,572 5,244 6,056Deferred tax liabilities 75,868 69,056 54,746 38,554 28,687Borrowings 296,124 307,609 247,565 3,922 32Derivative financial instruments 576 2,928 4,934 – –Other non-current liabilities 7,532 13,682 26,915 40,165 44,514total non-current liabilities 393,265 399,753 340,732 87,885 79,289Current liabilitiesCurrent liabilities 421,293 360,285 340,963 269,274 237,768Liabilities directly associated with disposal group

classified as held for sale 4,741 – – – –total current liabilities 426,034 360,285 340,963 269,274 237,768

total liabilities 819,299 760,038 681,695 357,159 317,057

total equity and liabilities 2,012,902 1,950,068 1,930,825 2,251,315 1,658,027

Annual Report 2010 tRAns F O R m 19

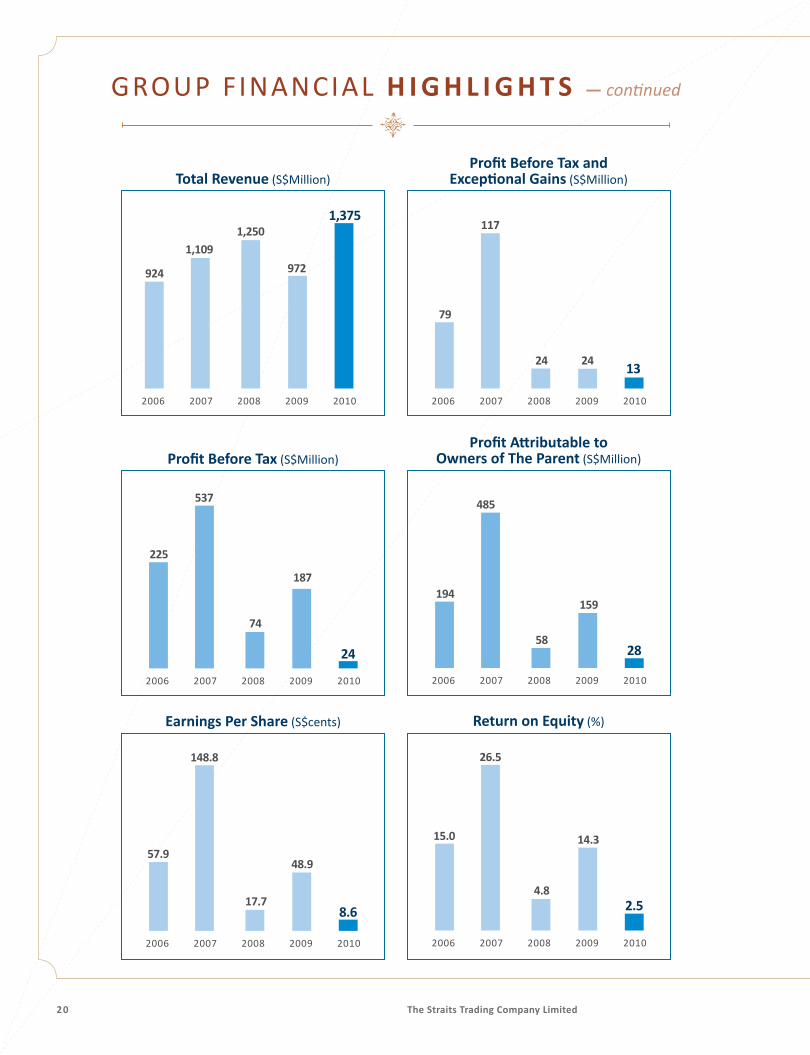

GrOUP FinAnCiAL H i G H L i G H T S — continued

Total Revenue (S$million)

2006 2007 2008 2009 2010

1,375

972

1,250

924

1,109

profit Before tax (S$million)

2006 2007 2008 2009 2010

24

187

74

537

225

profit attributable to Owners of The Parent (S$million)

485

2006 2007 2008 2009 2010

28

159

58

194

Earnings Per Share (S$cents)

2006 2007 2008 2009 2010

8.6

48.9

17.7

148.8

57.9

Return on Equity (%)

2006 2007 2008 2009 2010

2.5

14.3

4.8

26.5

15.0

profit Before tax and exceptional Gains (S$million)

2006 2007 2008 2009 2010

132424

117

79

20 The Straits Trading Company Limited

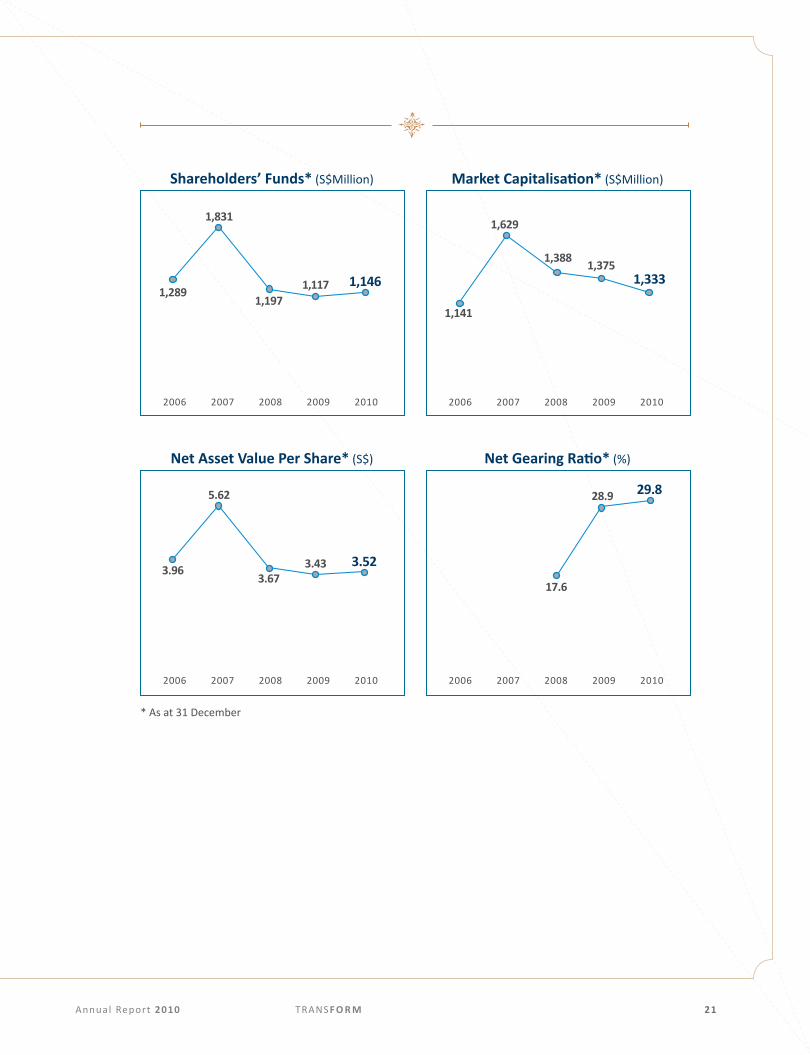

* As at 31 December

Shareholders’ Funds* (S$million)

2006 2007 2008 2009 2010

1,1461,1171,197

1,831

1,289

Market Capitalisation* (S$million)

2006 2007 2008 2009 2010

1,3331,375

1,388

1,629

1,141

Net asset value Per Share* (S$)

2006 2007 2008 2009 2010

3.523.433.67

5.62

3.96

net Gearing ratio* (%)

2006 2007 2008 2009 2010

29.828.9

17.6

Annual Report 2010 tRAns F O R m 21

(THE STRaiTS TRaDiNG COmPaNy LimiTED aND iTS SuBSiDiaRiES)

CoRpoRAte i N F O R m aT i O N

BOaRD OF DiRECTORSMs Chew Gek KhimExecutive ChairmanLLB (Hons)

Tan Sri Dato’ Dr Lin See-yanPSM, DPMP, DSAP, JMN, JSM, AMN, BA (Hons),MPA, MA, PhD, C Stat, C Sci

Mr razman ariffinB Sc (Eng), ARSM, MIME(M)

mrs Elizabeth SamBA (Hons) Economics

Ms Chew Gek hiangB Acc (Hons) , CPA

mr David Goh Kay yongBA (Hons), SM (MIT), CFA

mr yap Chee Keong B Acc, FCPA

mr Tham Kui Seng BA (Hons), Engineering Science

SECRETaRiESmrs maureen Leong B Acc (Hons), FCPA

ms Sng Kiat HuangLLB (Hons)

KEy PERSONNELmrs maureen LeongGroup Chief Financial OfficerThe Straits Trading Company Limited

mr Quah Ban HuatChief Investment OfficerThe Straits Trading Company Limited

yBhg. Dato’ Seri Dr mohd ajib anuarGroup Chief Executive Officermalaysia Smelting Corporation Berhad

mr Eric TengChief Executive Officer (Property & Hospitality) & Advisor (Marketing and Communications)The Straits Trading Company Limited

REGiSTERED OFFiCE9 Battery road #28-01Straits Trading Buildingsingapore 049910

CORPORaTE OFFiCES9 Battery road #28-01Straits Trading Buildingsingapore 049910Tel : (65) 6513 9288Fax : (65) 6534 7202E-mail : [email protected] : www.stc.com.sg

2 Lebuh Pasar BesarGround Floor, Straits Trading Building50050 Kuala LumpurTel : (03) 2698 7126Fax : (03) 2693 7542E-mail : [email protected]

SHaRE REGiSTRaRSTricor Barbinder Share registration Services(A division of Tricor Singapore Pte. Ltd.)

8 Cross Street #11-00 PWC BuildingSingapore 048424

auDiTORSErnst & young LLPOne raffles Quaynorth Tower, Level 18Singapore 048583

Partner-in-charge : mrs Lim Siew Koon(Appointed with effect from financial year ended 31 December 2010)

PRiNCiPaL BaNKERSUnited Overseas Bank Limited

DBS Bank Ltd

Oversea-Chinese Banking Corporation Limited

malayan Banking Berhad

Standard Chartered Bank

22 The Straits Trading Company Limited

CoRpoRAte soCiAl R E S P O N S i B i L i T y

WHaT WE mEaN By CSRWe see CSr as a vital part of corporate life. it determines how we relate to the world around us. We firmly believe that following a course of Corporate Social responsibility will create value for the company and for all our stakeholders. We shall continue to take the view and needs of all our staff and stakeholders into account in plotting our path forward.

OuR STaRTiNG aPPROaCH TO CSRin line with the philosophy of giving of Tan Chin Tuan Foundation, our sister company and philanthropic arm of Tecity Group, the company decided not to focus on any one segment of society or a particular charity, but rather, support projects or causes that are viable, sustainable, and well-managed with definable social outcomes.

With the help of Tan Chin Tuan Foundation, nine charities that fulfil the following guidelines were identified and shortlisted for our consideration:• Causes that are within TCTF’s funding

parameters• Donation is needed and will be well managed

towards directly helping beneficiaries• healthy reserves • responsiveness to donor, keen to build bridges

and goodwill

Three charities were eventually selected and officially adopted on 4 may 2010, at the official opening of our flagship building, the Straits Trading Building:1) Children’s Cancer Foundation2) Club Rainbow Singapore3) Society for the Physically Disabled

To mark the building’s official opening, STC, Tan Chin Tuan Foundation and 34 business partners donated more than S$330,000 (or S$83,000 each charity) to these three adopted charities and The Straits Times School Pocket money Fund.

In line with StC’s tradition of giving and beyond our commitment to maximise returns for our shareholders, StC is determined to contribute to the wider

community. the Company, together with its parent company, tecity Group, officially launched its Corporate Social responsibility (CSr) programme to support

the underprivileged at the official opening of its flagship building, Straits trading Building, on 4 May 2010.

Annual Report 2010 tRAns F O R m 23

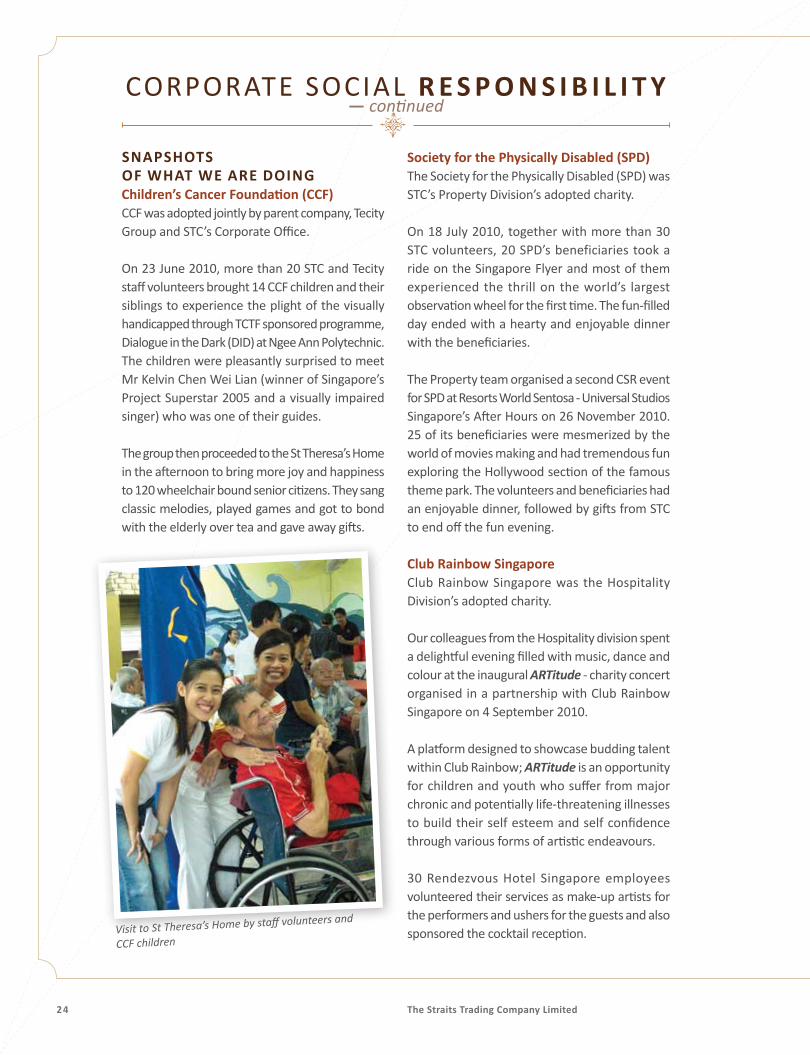

SNaPSHOTS OF WHaT WE aRE DOiNG Children’s Cancer Foundation (CCF)CCF was adopted jointly by parent company, Tecity Group and STC’s Corporate Office.

On 23 June 2010, more than 20 STC and Tecity staff volunteers brought 14 CCF children and their siblings to experience the plight of the visually handicapped through TCTF sponsored programme, Dialogue in the Dark (DiD) at ngee Ann Polytechnic. The children were pleasantly surprised to meet mr Kelvin Chen Wei Lian (winner of Singapore’s Project Superstar 2005 and a visually impaired singer) who was one of their guides.

The group then proceeded to the St Theresa’s home in the afternoon to bring more joy and happiness to 120 wheelchair bound senior citizens. They sang classic melodies, played games and got to bond with the elderly over tea and gave away gifts.

Society for the Physically Disabled (SPD)The Society for the Physically Disabled (SPD) was STC’s Property Division’s adopted charity.

On 18 July 2010, together with more than 30 STC volunteers, 20 SPD’s beneficiaries took a ride on the Singapore Flyer and most of them experienced the thrill on the world’s largest observation wheel for the first time. The fun-filled day ended with a hearty and enjoyable dinner with the beneficiaries.

The Property team organised a second CSr event for SPD at resorts World Sentosa - Universal Studios Singapore’s After hours on 26 november 2010. 25 of its beneficiaries were mesmerized by the world of movies making and had tremendous fun exploring the hollywood section of the famous theme park. The volunteers and beneficiaries had an enjoyable dinner, followed by gifts from STC to end off the fun evening.

Club Rainbow Singapore Club rainbow Singapore was the hospitality Division’s adopted charity.

Our colleagues from the hospitality division spent a delightful evening filled with music, dance and colour at the inaugural ARTitude - charity concert organised in a partnership with Club rainbow Singapore on 4 September 2010.

A platform designed to showcase budding talent within Club rainbow; ARTitude is an opportunity for children and youth who suffer from major chronic and potentially life-threatening illnesses to build their self esteem and self confidence through various forms of artistic endeavours.

30 rendezvous hotel Singapore employees volunteered their services as make-up artists for the performers and ushers for the guests and also sponsored the cocktail reception.

CoRpoRAte soCiAl R E S P O N S i B i L i T y — continued

Visit to St Theresa’s Home by staff volunteers and

CCF children

24 The Straits Trading Company Limited

A fun-filled day at Singapore Flyer for staff volunteers and SPD’s beneficiaries

Staff volunteered as make-up artists for Club Rainbow Singapore charity concert

Annual Report 2010 tRAns F O R m 25

p e R F O R mWe will continue to develop winning strategies and

capitalise on new opportunities that will enable us toscale new heights of growth, thereby creating greatervalue for our customers and delivering higher returns

to our shareholders.

26 The Straits Trading Company Limited

The Mountain is a symbol of strength and stability.

Conquering its imposing presence is an allusion to overcoming obstacles, while reaching its apex a sign of achievement

and success.

Annual Report 2010 tRAns F O R m 27

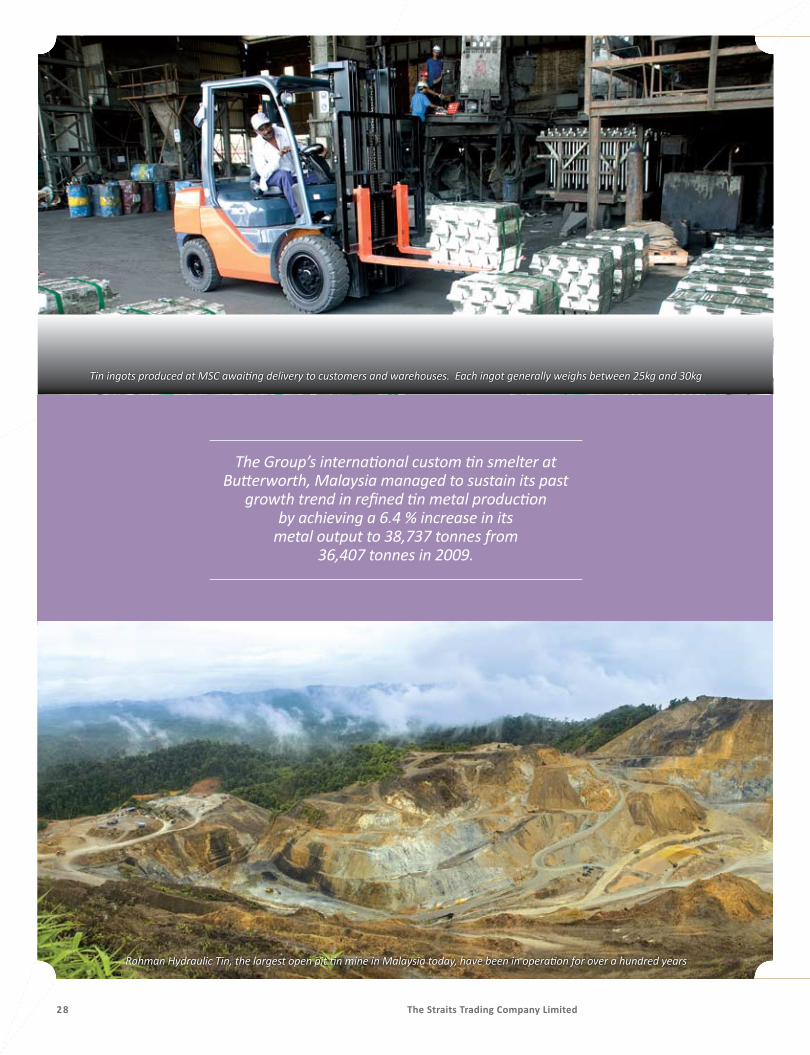

The Group’s international custom tin smelter at Butterworth, Malaysia managed to sustain its past

growth trend in refined tin metal production by achieving a 6.4 % increase in its

metal output to 38,737 tonnes from 36,407 tonnes in 2009.

Rahman Hydraulic Tin, the largest open pit tin mine in Malaysia today, have been in operation for over a hundred years

Tin ingots produced at MSC awaiting delivery to customers and warehouses. Each ingot generally weighs between 25kg and 30kg

28 The Straits Trading Company Limited

Business R E v i E W

Following the strategic decision made in 2009 to reposition the malaysia Smelting Corporation Berhad (mSC) Group to focus on its original core tin business, extensive efforts were undertaken in 2010 to strengthen the Group’s financial and development resources to achieve its long-term objective in growing its tin business, as well as to improve on the operating performance of its existing mining and smelting operations.

The Group therefore has been actively pursuing divestment programmes for its non-tin assets which include investments in various mining assets that have interests in gold, copper, nickel, zinc, silver and coal.

London metal Exchange (LmE) prices for tin and some other base and precious metals such as copper and gold recovered strongly to new record highs in 2010. This was underpinned by improving supply/demand fundamentals amid a more positive macroeconomic backdrop. The surge in tin prices towards the later part of the year presented both opportunities as well as challenges in managing the Group’s smelting and funding requirements.

in the early part of 2011, mSC successfully undertook a secondary listing of its shares on the Singapore Exchange Securities Trading Limited (SGX-ST) to help enhance shareholders’ value. This secondary listing has enabled the Company

— r e S o u r C e S —

MSC’s secondary listing on SGX-ST in January 2011

to raise S$43.75 million from the issuance of 25 million new shares. The dual listing of the Company in malaysia and Singapore marks an important milestone for the Group and will enhance the liquidity and provide a much wider platform for mSC to access capital to help generate a sustainable long term growth.

TiN miNiNG aND SmELTiNG OPERaTiONSThe Group’s turnover in 2010 was higher boosted by a higher metal production as well as tin prices, and was a record rm2.7 billion compared with rm1.8 billion in 2009.

The Group’s international custom tin smelter at Butterworth, malaysia managed to sustain its growth trend in refined tin metal production by achieving a 6.4 % increase in its metal output of 38,737 tonnes from 36,407 tonnes in 2009. Together with Koba Tin, the Group’s two smelting facilities produced in aggregate approximately 45,381 tonnes of tin metal in 2010 (43,862 tonnes in 2009). This has propelled the mSC Group to become the second largest supplier of tin metal globally. The Group’s tin mining operations carried out at the rahman hydraulic Tin Sdn. Bhd (rhT) in Perak, malaysia and at PT Koba Tin in Bangka, indonesia performed well in 2010. Production of tin-in-concentrates at rhT totalling 1,769 tonnes was up by 5% over the previous year due to higher operating efficiencies. At PT Koba Tin, the production from small scale mining operations ceased altogether resulting in a decrease of its overall metal production from 7,455 tonnes in 2009 to 6,644 tonnes in 2010. This was partially offset by a start up of several new gravel pump mining operations in 2010, which is expected to provide mSC Group with greater control over its output and environmental management going forward.

Annual Report 2010 tRAns F O R m 29

Business R E v i E W — continued

rationalisation efforts were undertaken in respect of the Group’s other tin interests held through its subsidiary, PT mSC which is developing on-shore tin operations in indonesia, and its 18.54 % interest investment in Tmr Ltd/PT Tenaga Anugerah (PT TA), which undertakes off-shore tin mining operations in indonesia. These investments are expected to generate positive results in 2011. The Group continues to pursue opportunities by identifying, developing and expanding its tin resources in malaysia and indonesia.

dIveStMent oF non-tIn iNvESTmENTSAt the end of 2009, the Group’s non-tin investments comprised a 22.1% interest in a listed gold and copper associate in Australia, BCD resources nL; a 18.22% interest in a Canadian listed nickel associate, Asian mineral resources Limited (Amr); a 30% interest in an unlisted Km resources inc which owns a polymetallic mine (producing copper, zinc, gold and silver in concentrates) in the Philippines; a 76.91% interest in an Australian listed subsidiary, Australia Oriental minerals nL (AOm); and a 53% effective interest in a coal development project in indonesia.

The divestment of the Group’s interest in BCD was completed in December 2010 and the Group ceased to be a shareholder.

Amr has been actively pursuing equity and debt funding to complete the nickel mine project in Vietnam. Pending the conclusion of the proposed fund raising exercise, mSC will continue to evaluate its options on how best to maximise its value by divesting its investment in Amr.

The agreement for the sale of the coal development project in indonesia has been executed and the disposal is expected to be completed in the first half of 2011.

The divestment of the Group’s interest in Km resources inc. may take a bit longer than expected. The mine has performed very well to date and is expected to contribute significantly to mSC’s earnings. As a result of rising copper, gold and silver and zinc prices, the valuation of Km resources inc. has also risen and mSC is seeking to enhance shareholder value by ensuring it sells the project at prices reflecting this increase in value.

FiNaNCiaL RESuLTSThe Group achieved a higher rm 76.01 million pre-tax profit before exceptional items, a 69.5 % increase for the year compared with rm 44.84 million recorded in 2009. This was mainly contributed by a better performance of the Group’s tin business both in malaysia and indonesia. After providing for exceptional items totalling rm154.48 million, the Group recorded a loss before tax of rm78.46 million compared with a Group net profit before tax of rm109.84 million in 2009. The exceptional items mainly comprised the loss incurred on the disposal of investments in BCD, and impairment provisions on the Group’s non-tin assets. The 2009 net profit included a surplus of rm65 million on the valuation of the Group’s interest in Km resources inc.

mSC is optimistic on the long-term prospects of the tin industry and believes the Group will be able to capitalize on the strong global tin market fundamentals and the current uptrend in tin prices to better its performance.

The Group will focus on increasing its tin reserves and resources through investments in explorations and acquisition of new tin mining projects in malaysia and indonesia, as well as brownfield developments at its existing mines. The Group will also continue with the ongoing efforts to improve operating efficiencies.

30 The Straits Trading Company Limited

— p r o p e r t y —

The Holland Collection

Five Chancery

SiNGaPORE2010 was a fruitful year for the Straits Trading Company (STC) property division, including Straits media, which delivered total revenue of S$57.8 million. Although this was lower than 2009 due to a lower number of residential units sold, we saw higher rental revenues from both our commercial and residential properties as a result of securing higher renewals.

We saw progress in the construction of our two new Good Class Bungalows (GCBs) along Cable road and 12 luxury strata bungalows at Five Chancery along Chancery Lane, with both developments on target, and expected completion dates at the end of third quarter of 2011.

The implementation of both the Five Chancery and the new GCB projects articulated our strategy to reposition STC as a niche developer and owner of high-end lifestyle properties.

We are pleased that our flagship Straits Trading Building has secured 96% occupancy in 2010. Occupancy for China Square Central was strong as

occupancy improved 94% in 2010 as compared to 85% in 2009. Our master Lease agreement for China Square Central would expire in march 2012.

We have continued our policy of divesting completed non-core residential properties. Selected units in Gallop Green and Gallop Gables were sold at their valuation in 2010 as investor demand for well-located and exclusive homes, built near desirable amenities such as the Singapore Botanic Gardens and the upcoming Farrer road mrT, remain extremely keen.

Annual Report 2010 tRAns F O R m 31

32 The Straits Trading Company Limited

We are pleased that our flagship Straits Trading Building has secured 96% occupancy in 2010.

Occupancy for China Square Central was strong as occupancy improved 94% in 2010

as compared to 85% in 2009.

Business R E v i E W — continued

maLaySia

As part of our review of our land bank in malaysia, feasibility studies have been conducted on our existing land parcels to help formulate clear plans for the development of residential/commercial projects in various states in malaysia. This is in line with our strategy in malaysia of developing land where there is strategic and commercial value while disposing off those that are non-core and non-strategic.

Sale of the Thompson-Flora Tropika residences in ipoh, comprising 47 luxurious freehold bungalows along the prime Jalan Dr Tun ismail by Taiko-Straits Developments Sdn Bhd, a joint venture between Taiko Development Sdn Bhd and STC is progressing on schedule.

perth, auStraLIa

A major project which we are evaluating will be a residential development at rendezvous Observation City, Perth, which would offer luxurious waterfront living along Scarborough Beach. We are targeting to finalise plans by June 2011 for submission to the relevant authorities for development approval.

The Thompson-Flora Tropika Residences -Showhome

Annual Report 2010 tRAns F O R m 33

Business R E v i E W — continued

We would actively seek opportunities for both development and completed projects

that either offers attractive yields, recurrent income and/or capital appreciation

in Singapore and overseas.

STRaiTS mEDia

Sales revenue for Straits media Pte Ltd, the company’s media advertising subsidiary, increased 34% from S$3.5 million in 2009 to S$4.7 million in 2010. net advertising profit also doubled to S$0.6 million in 2010 from S$0.3 million in 2009. This was mainly due to increased revenues collected from existing sites at hotel rendezvous, Keppel Distripark, Tangs Plaza as well as two new sites acquired in the fourth quarter of 2010.

in conclusion, although the year saw new cooling measures by the Government on the property market being implemented, with the latest on 14 January 2011, we believe that the near term outlook for Singapore’s property market would remain stable although any increase in property prices would be contained.

Property which forms a very substantial part of our assets would continue to be an important “engine of growth” for STC as a niche developer and owner of high-end lifestyle properties. We would actively seek opportunities for both development and completed projects that either offers attractive yields, recurrent income and/or capital appreciation in Singapore and overseas.

The Thompson-Flora Tropika Residences

34 The Straits Trading Company Limited

— h o S p I ta L I t y —

Rendezvous Hotel Adelaide, Penthouse Suite

With the strong rebound in global tourism, the revenue for the hospitality division - rendezvous hospitality Group (rhG) - has increased to S$146.7 million in 2010 from S$127.9 million in 2009. The operating environment however remained competitive and difficult and the Group’s hotel operations reported an operating loss of S$14 million in 2010, compared to an operating loss of S$8.5 million in 2009. This adverse operating result was due in part to the strengthening of Australian dollar against the Singapore dollar as well as challenging management contracts and leases.

Consequently, the Board made a prudent assessment of the business and appropriate provisions have been taken in the accounts for the financial year ended 2010. in addition, efforts were initiated in 2010 to streamline the operations of rendezvous hospitality Group (rhG), strengthen its service efficiency and improve operational effectiveness. in 2011, the Group would continue this effort and take advantage of efficiencies arising from the consolidation of hotel operations and prudent and appropriate capital expenditure. hotel management contract expansion would be carried out in high growth hotels and cities.

in 2010, the Group continued to own, lease and manage 14 hotels in the region, namely:

• in Singapore and China – rendezvous hotel Singapore and rendezvous merry hotel shanghai

• in australia - rendezvous Observation City hotel, Perth; rendezvous hotel, Adelaide; rendezvous hotel melbourne; rendezvous Stafford hotel, Sydney; rendezvous hotel, Brisbane; rendezvous reef resort, Port Douglas; The marque hotel, Perth; The marque hotel, Sydney; The marque hotel, Canberra (lease expiring november 2011 and will be closed for redevelopment)

• in New zealand – rendezvous hotel Auckland; the Marque Hotel, Christchurch

Key highlights for the year by region are as follows:

SiNGaPORE aND SHaNGHai

The Singapore economy rebounded by 15% in 2010, from the -1.3% in 2009 due to the global financial crisis. Coupled with the strong rebound of Asian economies, 2010 was a record year for visitors’ arrival to Singapore.

rendezvous hotel Singapore benefitted with significant increase to its Average Occupancy rates and Average Daily rate. in order to meet future demand and improve its revenue, plans were initiated to refurbish the hotel in 2010 and work has just begun in march 2011.

rendezvous merry hotel Shanghai had a mixed year, benefitting from the World Expo between April to October but saw a slowdown in occupancy after October.

Annual Report 2010 tRAns F O R m 35

Business R E v i E W — continued

Rendezvous Observation City Hotel, Perth

auSTRaLia

rhG’s footprint in Australia remained focused on being a branded three-and-a-half to four-and-a-half star business hotel chain in key cities, targeting the business travellers and the corporate segment.

With the business environment in Australia improving, rhG has been working to improve its product and service and increase its marketing awareness through strategic marketing partnership. This has resulted in an increase on our Average Daily room rate and/or Occupancy for most of the properties.

Capital expenditure plans to refurbish and/or upgrade were drawn up for rendezvous Observation City hotel, Perth, The marque hotel in Brisbane and Perth; and rendezvous hotel melbourne and when completed, is expected to increase market share and revenue.

Yield management was implemented to help better manage costs and the various channels for room reservation to improve revenue.

Whilst rendezvous hotel, Adelaide continued to be a leader in Adelaide’s five star accommodation market targeted at business travellers, rendezvous reef resort, Port Douglas faced another challenging year due to the natural disasters in Queensland, rate parity with the US dollar and poor local weather conditions.

The marque hotel, Canberra will be closed for redevelopment by the owner when the lease expires on 30 november 2011.

NEW zEaLaND

The marque hotel in Christchurch which is a new property commenced business on 18 march 2010 with good awareness and exposure created in the local market through targeted publicity. Unfortunately, as a consequence of the earthquake in Christchurch in September 2010 and the more recent one in February 2011, it is expected to resume operations only in first half of 2012.

Growth at the rendezvous hotel Auckland was marginal but for 2011, the plans to gear up which include capital expenditure plans for improvement and upgrade have been made to leverage on the advantage of the rugby World Cup in September 2011.

From the above assessment, it is apparent that however sound is our strategy, it will still require a proper process of execution and implementation to achieve the desired objective. in this regard, a management board comprising senior executives and advisors was formed to oversee the hospitality business with a view to creating a clearer brand, identifying areas of inefficiency, improving operational effectiveness and creating a leaner and nimbler organisation in the process, so as to ultimately raise the operating performance of this division.

investing in value accretive capital expenditure will be one of the approaches to transform the business, hence, a capital expenditure budget has been set aside for the refurbishment of our hotels and it is anticipated that upon completion, our hospitality division will have stronger brand presence, better customer experience and increased occupancies and rates resulting in improved profitability.

2011 will therefore mark a year of transformation for the hospitality division and work is already underway as we streamline the business and reduce wastage and inefficiencies.

36 The Straits Trading Company Limited

Annual Report 2010 TRAns f o r m 37

r e p o r t o n c o r p o r at e g o v e r n a n c e

The Straits Trading Company Limited (the “Company”) is committed to high standards of corporate governance. This report describes the Company’s corporate governance policies and practices during the financial year ended 31 December 2010 (“FY2010”) with specific reference to the Code of Corporate Governance 2005 (the “Code”).

Board’s Conduct of Affairs

The Board, comprising a majority of independent Directors, provides policy direction, entrepreneurial leadership, approves the development and implementation of corporate strategies, and ensures that the necessary financial and human resources are in place for the Company to meet its objectives.

The Board also sets the Company’s values and standards, and ensures its obligations to all stakeholders are met and understood. While the Board remains responsible for providing oversight in the preparation and presentation of the financial statements, it has delegated to the Management the task of ensuring that the financial statements are drawn up and presented in compliance with the relevant provisions of the Singapore Companies Act, Cap. 50 and the Singapore Financial Reporting Standards.

With the appointment of the CEOs for each of the discrete business units, the Board has appointed the Chairman as Executive Chairman to oversee the Management, and the Lead Independent Director to ensure continued good governance. Supported by four Board Committees, namely the Audit Committee, Remuneration Committee, Nominating Committee and Finance Committee, the Board also approves the Group’s appointment of Board members, key business initiatives, major investments and funding decisions, and interested person transactions.

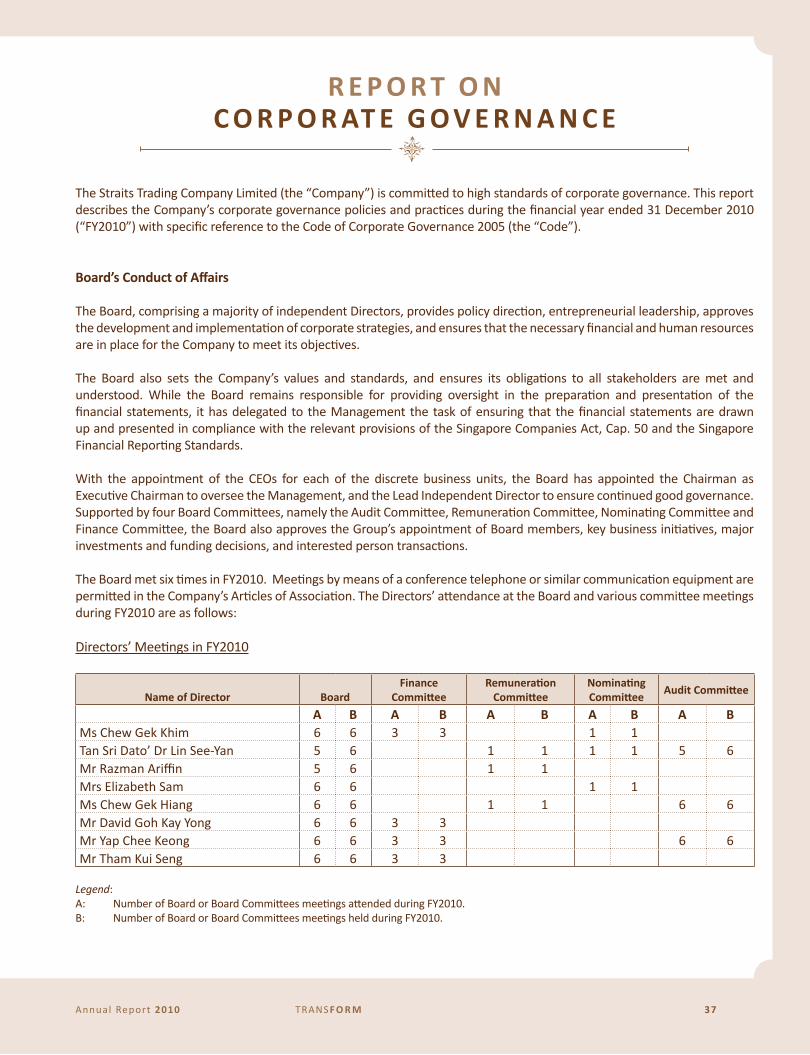

The Board met six times in FY2010. Meetings by means of a conference telephone or similar communication equipment are permitted in the Company’s Articles of Association. The Directors’ attendance at the Board and various committee meetings during FY2010 are as follows:

Directors’ Meetings in FY2010

Name of Director BoardFinance

CommitteeRemuneration

CommitteeNominating Committee

Audit Committee

a B a B a B a B a BMs Chew Gek Khim 6 6 3 3 1 1Tan Sri Dato’ Dr Lin See-Yan 5 6 1 1 1 1 5 6Mr Razman Ariffin 5 6 1 1Mrs Elizabeth Sam 6 6 1 1Ms Chew Gek Hiang 6 6 1 1 6 6Mr David Goh Kay Yong 6 6 3 3Mr Yap Chee Keong 6 6 3 3 6 6Mr Tham Kui Seng 6 6 3 3

Legend:A: Number of Board or Board Committees meetings attended during FY2010.B: Number of Board or Board Committees meetings held during FY2010.

38 The Straits Trading Company Limited

Board Composition and Guidance

The Board comprises eight Directors, seven of whom are non-executive. The Nominating Committee considers Tan Sri Dato’ Dr Lin See-Yan, Mr Razman Ariffin, Mrs Elizabeth Sam, Mr Yap Chee Keong and Mr Tham Kui Seng to be independent. The Directors provided objective and independent judgment to the decision making of the Board. The non-executive Directors of the Company participated constructively and reviewed the Group’s operations, budgets and strategies. They also assessed the effectiveness of the Board’s processes and activities in meeting set objectives and corporate governance standards.

The Board as a group have the core competencies, such as accounting or finance, business or general management, legal and industry knowledge, and strategic planning experience. Key information on the Directors are set out in pages 10 to 13.

Executive Chairman

The Board is led by Ms Chew Gek Khim as the Executive Chairman. Ms Chew assumed the Chair on 24 April 2008 and was appointed Executive Chairman on 1 November 2009.

As Chairman of the Board, Ms Chew’s duties include leading the Board, setting the Board agenda and ensuring that all Directors receive sufficient relevant information (both financial and non-financial) to enable them to participate and contribute effectively in Board discussions and decisions. She aims to promote constructive relations between the Board members, and between the Board and the Management, and ensures effective communication with shareholders. Ms Chew also advocates high standards of corporate governance.

As the Executive Chairman, Ms Chew takes on executive oversight of the Management of the business units and is assisted by senior key personnel within the Company. The Management is responsible for the daily management of the businesses and implementation of the Board’s policies and decisions as well as ensuring compliance with the corporate governance policies of the Company as these relate to the respective business units. The Management reports to the Board and is managed through the strategies adopted and monitored through the key performance indicators set for them.

Lead Independent Director

In line with the recommendations set out in the Code, Mr Yap Chee Keong, currently an independent and non-executive Director as well as the Audit Committee Chairman, was appointed the Lead Independent Director of the Company on 1 November 2009.

As the Lead Independent Director, Mr Yap’s role includes being available to shareholders to address any of their concerns and acting as the principal liaison between the independent Directors and the Executive Chairman on critical issues.

r e p o r t o n c o r p o r at e g o v e r n a n c e

Annual Report 2010 TRAns f o r m 39

Board Membership

The Company has adopted a formal and transparent process for the appointment of new Directors through the Nominating Committee which reviews the background of all appointees and makes recommendations accordingly to the Board for approval.

The Nominating Committee, chaired by Mrs Elizabeth Sam, comprises three Directors, the majority of whom are independent, including the Chairman. The other members of the Nominating Committee are Ms Chew Gek Khim and Tan Sri Dato’ Dr Lin See-Yan.

In accordance with Guideline 4.1 of the Code, the Chairman of the Nominating Committee is not directly associated with any substantial shareholder of the Company. The functions of the Nominating Committee include the evaluation of the Board’s effectiveness, each Director’s contributions and independence, as well as making recommendations on the appointment and re-nomination of Directors for the Board and Board Committees. The role and functions of the Nominating Committee are set out in its Terms of Reference.

Board performance

The Company has in place a process to assess the Board’s effectiveness as a whole. The evaluation is carried out annually with each Director making his assessment by providing feedback to the Nominating Committee through a Board assessment questionnaire.

Access to Information

Information and data are important to the Board’s understanding of the Group’s businesses and essential to preparing the Board members for effective meetings. Where required, the Management supplements the meeting papers with presentations on active operations and strategic issues to provide Directors with a better understanding of the Group’s operations. Senior management were also invited to attend the meetings to answer enquiries from the Directors.

The Directors have separate and independent access to the services of the company secretaries, who are responsible for ensuring that Board procedures are followed and applicable rules and regulations are complied with. The company secretaries also assist the Chairman by ensuring good information flows within the Board and its committees, and between senior management and non-executive Directors. The company secretaries attended all board meetings and their appointments or removals are subject to the Board’s approval.

In the furtherance of their duties and if the Management’s explanations are not satisfactory, the Directors may seek independent professional advice at the Company’s expense.

r e p o r t o n c o r p o r at e g o v e r n a n c e

40 The Straits Trading Company Limited

Procedures for Developing Remuneration Policies

The Board has a Remuneration Committee comprising three non-executive Directors, the majority of whom are independent. Mr Razman Ariffin chairs the Remuneration Committee and Tan Sri Dato’ Dr Lin See-Yan and Ms Chew Gek Hiang are the other two members.

The functions of the Remuneration Committee include the recommendation of a framework of remuneration for the Board and senior executives of the rank of senior vice president and above, and the recommendation of specific remuneration package for the Executive Chairman, for the Board’s approval. The role and functions of the Remuneration Committee are set out in the Terms of Reference of the Remuneration Committee.

Level and Mix of Remuneration

The Company adopts a performance-based approach to compensation where employees’ remuneration is linked to individual and corporate performances. The Remuneration Committee sees the importance of a market competitive remuneration strategy to attract, retain and motivate employees to high performance that creates value for the shareholders. Remuneration is determined according to the following general components: salary, contractual bonus and incentive bonus.

During the year under review, the Remuneration Committee met, discussed and approved the compensation for the senior executives of the Group. Presently, the Company does not have any share option scheme.

Taking into account the performance of the Group and the responsibilities and performance of the Directors, directors’ fees (for the Board and the various Board Committees) were set in accordance with a remuneration framework comprising responsibility fees and attendance fees. The Executive Chairman does not receive directors’ fees. Non-executive Directors are paid directors’ fees, subject to approval at the annual general meeting. The non-executive Directors have no service contracts. No individual Director fixes his own remuneration.

r e p o r t o n c o r p o r at e g o v e r n a n c e

Annual Report 2010 TRAns f o r m 41

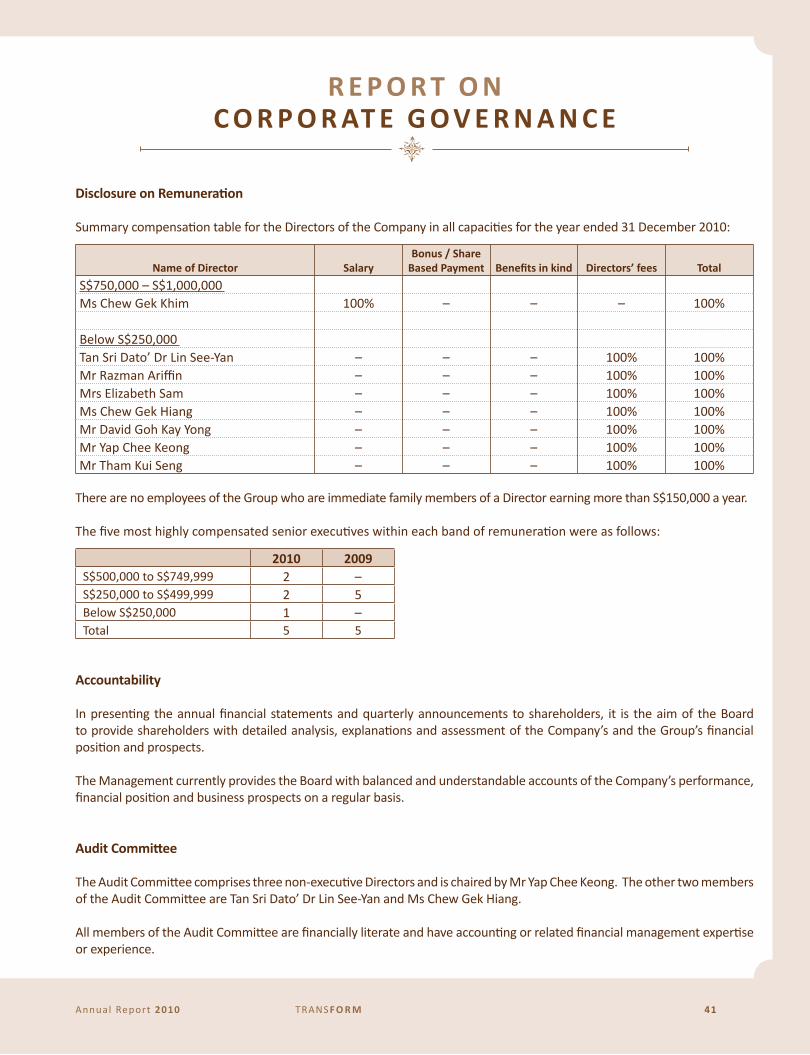

Disclosure on Remuneration

Summary compensation table for the Directors of the Company in all capacities for the year ended 31 December 2010:

Name of Director SalaryBonus / Share

Based Payment Benefits in kind Directors’ fees Total

S$750,000 – S$1,000,000Ms Chew Gek Khim 100% – – – 100%

Below S$250,000Tan Sri Dato’ Dr Lin See-Yan – – – 100% 100%Mr Razman Ariffin – – – 100% 100%Mrs Elizabeth Sam – – – 100% 100%Ms Chew Gek Hiang – – – 100% 100%Mr David Goh Kay Yong – – – 100% 100%Mr Yap Chee Keong – – – 100% 100%Mr Tham Kui Seng – – – 100% 100%

There are no employees of the Group who are immediate family members of a Director earning more than S$150,000 a year.

The five most highly compensated senior executives within each band of remuneration were as follows:

2010 2009S$500,000 to S$749,999 2 –S$250,000 to S$499,999 2 5Below S$250,000 1 –Total 5 5

Accountability

In presenting the annual financial statements and quarterly announcements to shareholders, it is the aim of the Board to provide shareholders with detailed analysis, explanations and assessment of the Company’s and the Group’s financial position and prospects.

The Management currently provides the Board with balanced and understandable accounts of the Company’s performance, financial position and business prospects on a regular basis.

Audit Committee

The Audit Committee comprises three non-executive Directors and is chaired by Mr Yap Chee Keong. The other two members of the Audit Committee are Tan Sri Dato’ Dr Lin See-Yan and Ms Chew Gek Hiang.

All members of the Audit Committee are financially literate and have accounting or related financial management expertise or experience.

r e p o r t o n c o r p o r at e g o v e r n a n c e

42 The Straits Trading Company Limited

The role of the Audit Committee is documented in a Charter (Terms of Reference) approved by the Board. The Charter, amended by the Board in 2005 to facilitate the Company’s compliance with the Code, defines the purpose, authority and responsibilities of the Committee. The Company has a whistle-blowing procedure in place for staff to raise matters of impropriety in confidence and for appropriate follow-up action to be taken, where necessary. The Audit Committee is authorised to investigate any matters specified in the Charter.

In performing its functions, the Audit Committee reviews the overall scope of both internal and external audits and the assistance given by the Company’s officers to the auditors. It meets with the Company’s internal and external auditors to discuss the results of their respective examinations and their evaluation of the Company’s system of internal accounting and financial controls on a quarterly basis. The Audit Committee reviews interested person transactions to ensure that they are carried out on normal commercial terms and are not prejudicial to the interests of the Company and its minority shareholders. The Audit Committee also reviews the consolidated financial statements and the auditors’ report, as well as related announcements to shareholders and The Singapore Exchange Securities Trading Limited before submission to the Board.

Finance Commitee

The Finance Committee comprises the following Directors:

Ms Chew Gek Khim (Chairman)Mr David Goh Kay YongMr Yap Chee KeongMr Tham Kui Seng

Established on 23 February 2010, the Finance Committee’s responsibilities include reviewing and recommending to the Board for approval the annual business plans and budgets for business units and entities within the Group. It also reviews and approves certain transactions of the Group within its delegated authority limits, such as financing plans and borrowings, acquisitions and disposals and capital expenditure.

Internal Controls and Risk Management

The Board recognises its role in ensuring that the Management maintains a sound system of internal controls to safeguard shareholders’ investments and the Group’s assets. The Group has adopted a group-wide risk assessment process, which identifies the key risks facing each major business unit, the potential impact and likelihood of those risks occurring, the control effectiveness and action plans being taken to mitigate those risks.

The Board appreciates that risk management is an on-going process in which the senior management and the operational managers continuously participate to evaluate and monitor the significant risks. The internal audit department regularly reviews all significant control policies and procedures and highlights all significant matters to the senior management and the Audit Committee. The Audit Committee has reviewed the Group’s risk assessment process and is satisfied that there are adequate internal controls in place to manage the significant risks identified.

The Group’s subsidiary, Malaysia Smelting Corporation Berhad, has established a risk management structure, which depicts the lines of reporting and responsibility at its Board, Audit Committee and Management levels.

r e p o r t o n c o r p o r at e g o v e r n a n c e

Annual Report 2010 TRAns f o r m 43

Internal Audit

The Company has its own in-house internal audit department that is independent of the activities it audits. The internal auditors report directly to the Chairman of the Audit Committee on audit matters and reports to the Executive Chairman on administrative matters.

The Audit Committee met with the external and internal auditors, without the presence of Management, on a quarterly basis in FY2010.

In discharging its functions, the Audit Committee is provided with adequate resources, has full access to and co-operation by the Management and the internal auditors, and has full discretion to invite any Director or executive officer to attend its meetings. All major findings and recommendations are brought to the attention of the Board of Directors.

The Audit Committee reviewed all non-audit services provided by the firm of external auditors to the Company and was satisfied that the nature and extent of such services will not prejudice the independence and objectivity of the external auditors.

Having reviewed the independence of the external auditors, the Audit Committee has recommended that Ernst & Young LLP be nominated for re-appointment as auditors at the forthcoming annual general meeting to be held on 28 April 2011. Ernst & Young LLP have indicated their willingness to accept re-appointment.