transition to ifrs - · pdf file3. background to the adoption of ifrs calendar managing the...

TRANSCRIPT

1

Carrefour GroupCarrefour GroupTransition to IFRSTransition to IFRS

16th 16th DecemberDecember 20042004

2

AgendaAgenda

1.1. Background to the adoption of IFRS Background to the adoption of IFRS

2.2. How IFRS will impact Carrefour and the food retail How IFRS will impact Carrefour and the food retail sectorsector

3

Background to the adoption of IFRSBackground to the adoption of IFRS

CalendarCalendar

Managing the transition to IFRS at CarrefourManaging the transition to IFRS at Carrefour

How IFRS differsHow IFRS differs……to French GAAPto French GAAP

and to US GAAPand to US GAAP

…… and the consequencesand the consequences

4

Calendar

30 June 2004 30 June 2005

The first publication of Carrefour accounts under IFRS will be for the six months to 30th June 2005 (with pro forma accounts for the same period to 30th June 2004)

5

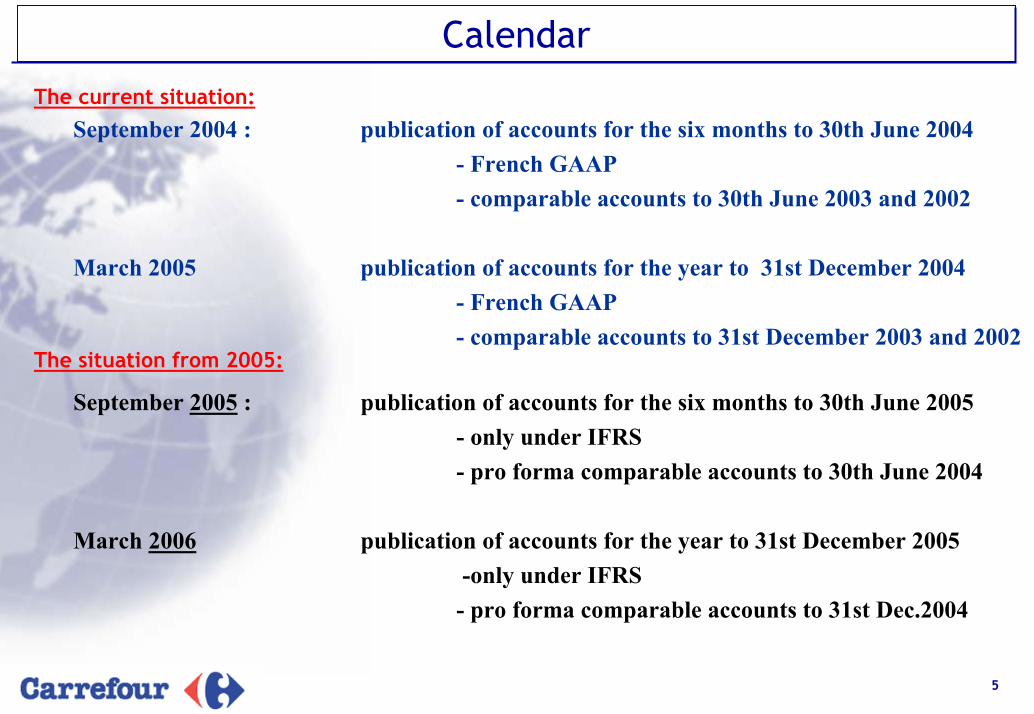

Calendar

September 2004 : publication of accounts for the six months to 30th June 2004- French GAAP- comparable accounts to 30th June 2003 and 2002

March 2005 publication of accounts for the year to 31st December 2004- French GAAP- comparable accounts to 31st December 2003 and 2002

The current situation:

The situation from 2005:

September 2005 : publication of accounts for the six months to 30th June 2005- only under IFRS- pro forma comparable accounts to 30th June 2004

March 2006 publication of accounts for the year to 31st December 2005-only under IFRS- pro forma comparable accounts to 31st Dec.2004

6

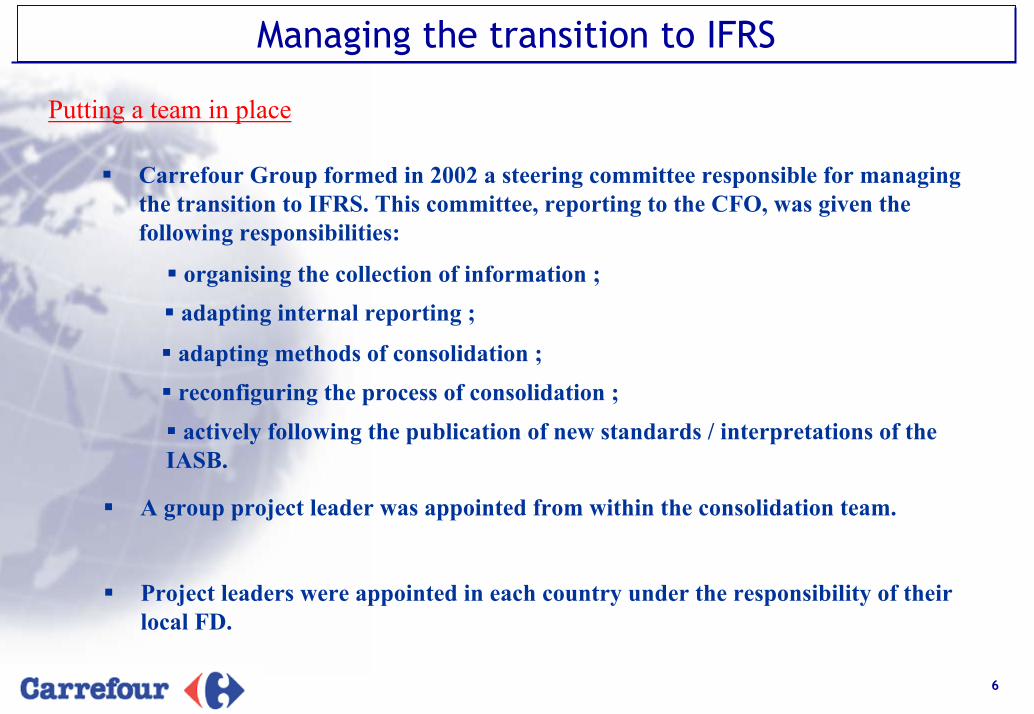

Managing the transition to IFRS

Putting a team in place

Carrefour Group formed in 2002 a steering committee responsible for managing the transition to IFRS. This committee, reporting to the CFO, was given the following responsibilities:

organising the collection of information ;adapting internal reporting ;

adapting methods of consolidation ;reconfiguring the process of consolidation ;actively following the publication of new standards / interpretations of the

IASB.

A group project leader was appointed from within the consolidation team.

Project leaders were appointed in each country under the responsibility of their local FD.

7

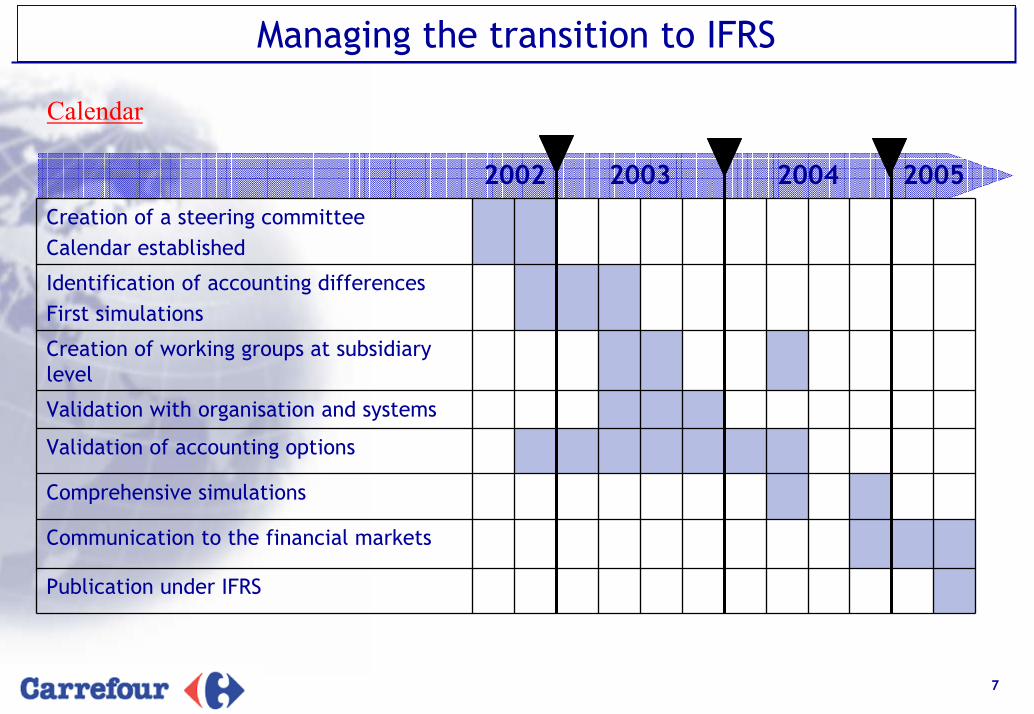

Managing the transition to IFRS

Calendar

Creation of working groups at subsidiary level

Communication to the financial markets

Identification of accounting differencesFirst simulations

Validation of accounting options

Creation of a steering committeeCalendar established

20042003 2005

Publication under IFRS

Comprehensive simulations

Validation with organisation and systems

2002

8

Managing the transition to IFRS

Training

For senior directors

The members of the Audit committee as well as the Supervisory Board are aware of the issues associated with the transition to IFRS.

Presentations have been given to the different regional Executive Committees.

For the accounting and finance teams

Training was given to more than 200 people between April and September 2003 in partnership with an outside consultant.

Training on the complete package of IFRS changes was given in March/April 2004.

For the rest of the company

Our property, merchandising and human resources teams have also been made aware of the issues associated with the transition to IFRS.

9

Managing the transition to IFRS

Adaptation of tools / systems

Development of a new consolidation process, and a user guide

Definition of group policies

Development of a new tool to help subsidiaries review property agreements.

Adaptation software by our Treasury department

Adaptation of our reporting tools

10

The main principles adopted

The opening financial statements reported under IFRS will begin from the 1st January 2004.

Most of the IFRS standards will be applied retrospectively (as if they have always been applied).

The impact of restating the accounts using IFRS will be accounted for in the opening financial statements from the 1st January 2004.

11

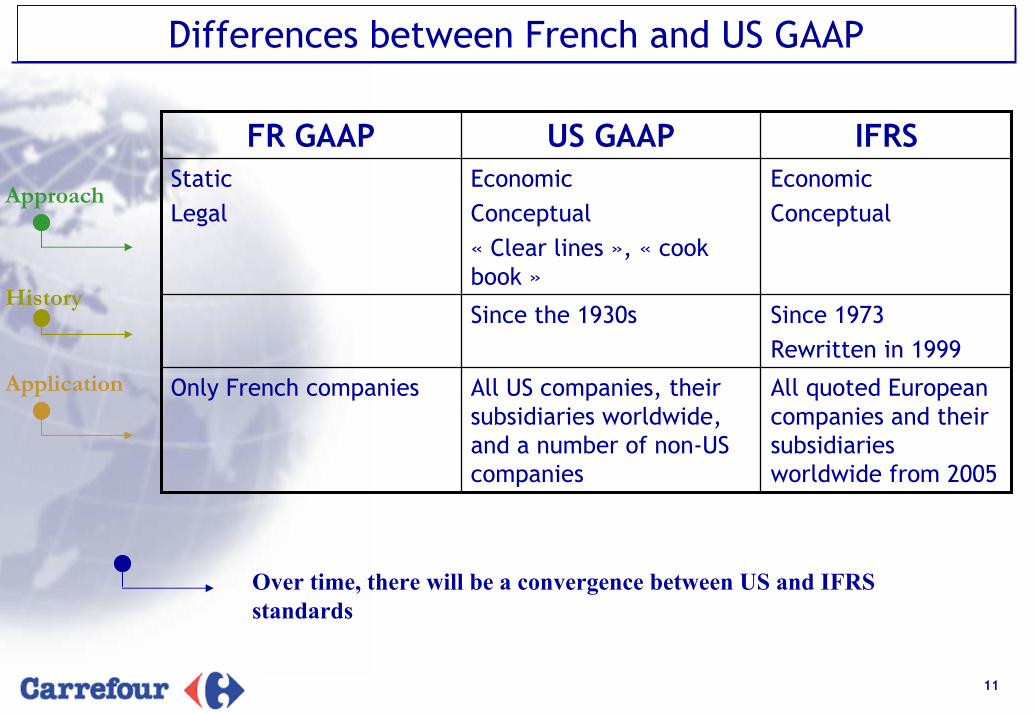

Differences between French and US GAAP

Only French companies

StaticLegal

FR GAAPEconomicConceptual

EconomicConceptual« Clear lines », « cook book »

Since 1973Rewritten in 1999

Since the 1930s

All quoted European companies and their subsidiaries worldwide from 2005

All US companies, their subsidiaries worldwide, and a number of non-US companies

IFRSUS GAAP

Approach

History

Application

Over time, there will be a convergence between US and IFRS standards

12

Consequences

Adopting IFRS standards makes comparisons between European corporateseasier.

However, flexibility in interpreting the new standards means that there will be a divergence of approach with regard to certain issues (for example, revaluation of assets, segment reporting).

The simultaneous adoption of the new standards by all European corporates has encouraged exchanges of information between companies.

13

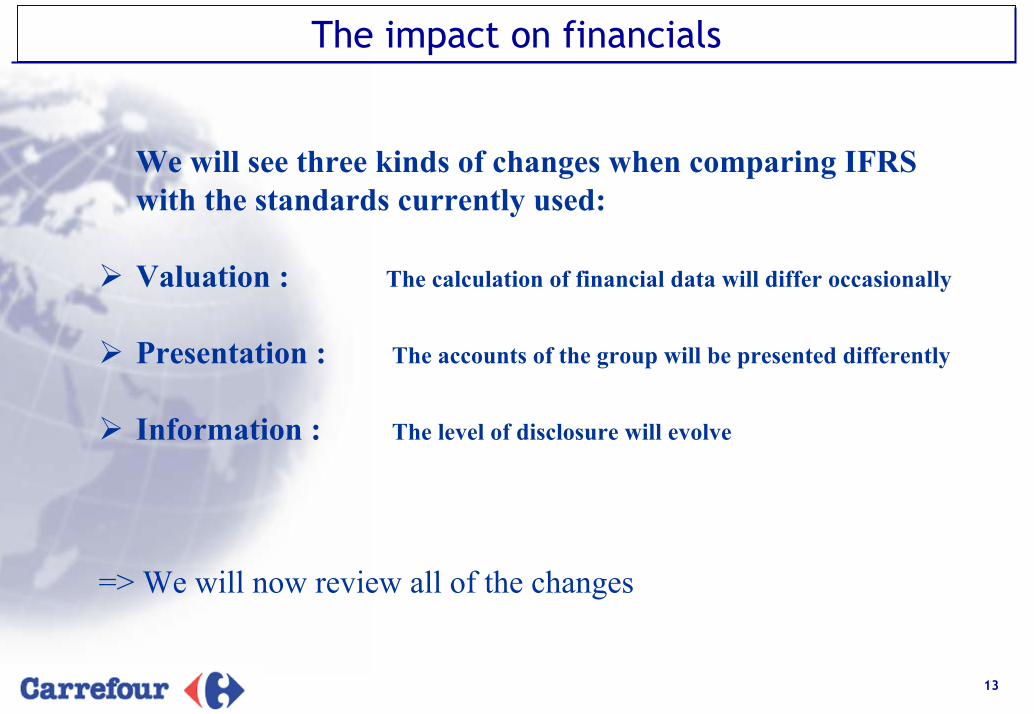

The impact on financials

We will see three kinds of changes when comparing IFRS with the standards currently used:

Valuation : The calculation of financial data will differ occasionally

Presentation : The accounts of the group will be presented differently

Information : The level of disclosure will evolve

=> We will now review all of the changes

14

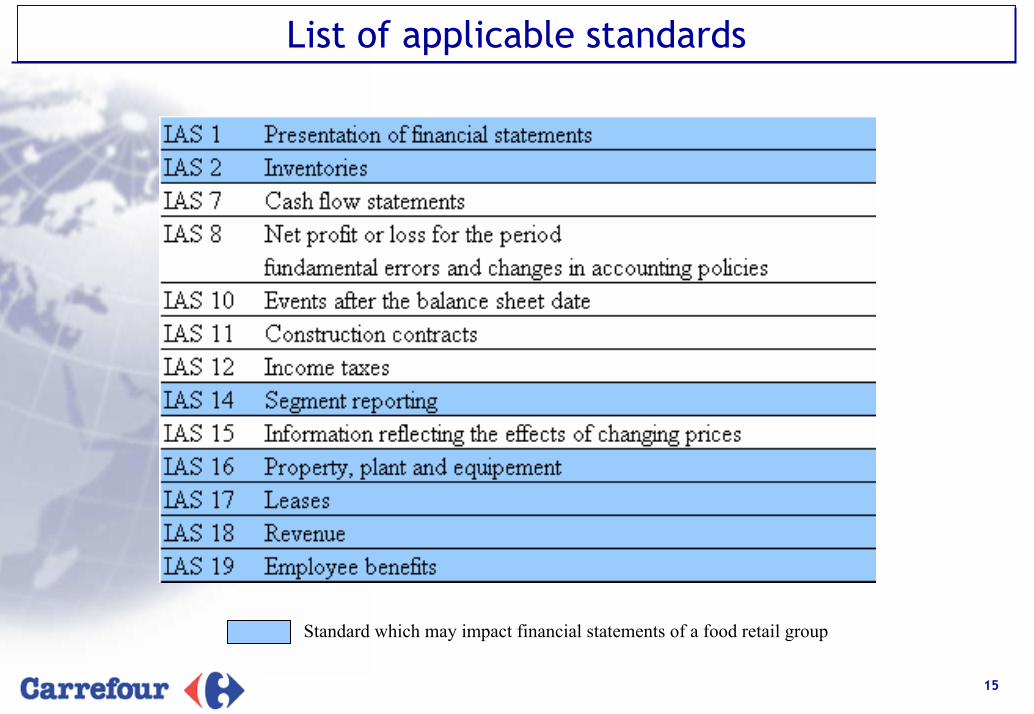

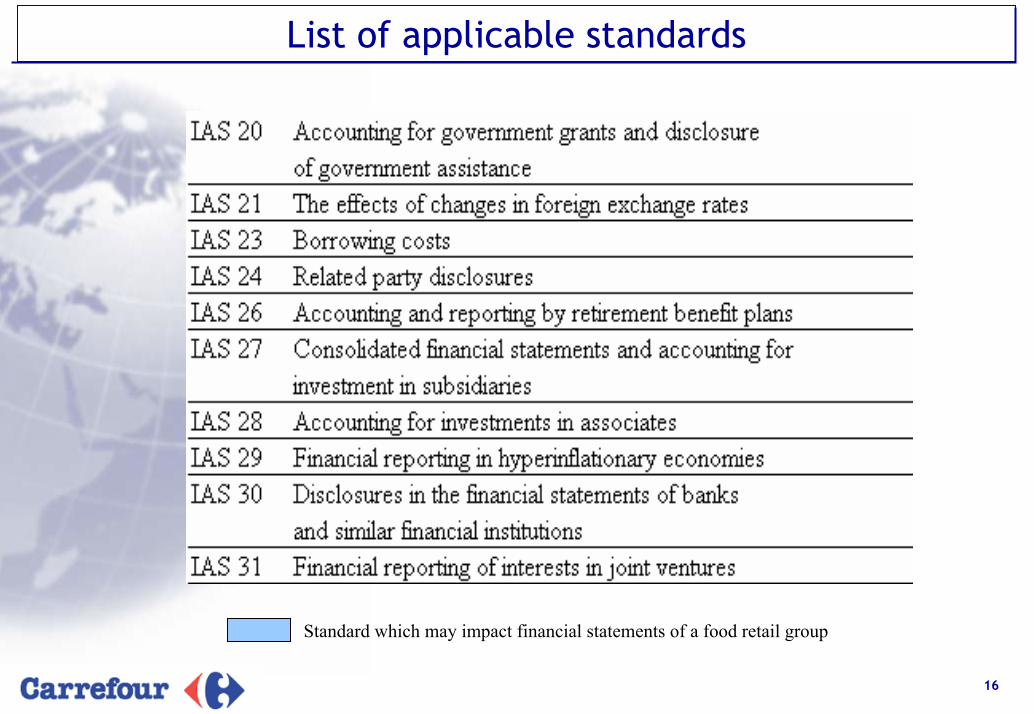

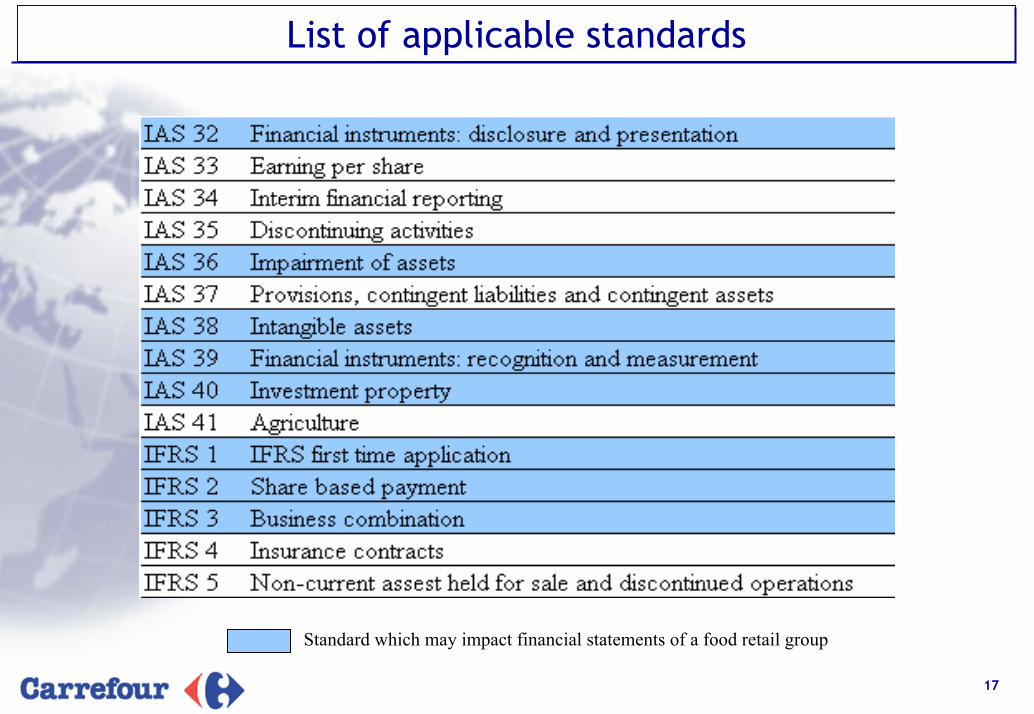

Review of IFRS standardsReview of IFRS standards

List of the standards which are applicable to CarrefourList of the standards which are applicable to Carrefour

Presentation of the principal standards which are likely to Presentation of the principal standards which are likely to impact companies operating in the food retail sectorimpact companies operating in the food retail sector

15

List of applicable standards

Standard which may impact financial statements of a food retail group

16

List of applicable standards

Standard which may impact financial statements of a food retail group

17

List of applicable standards

Standard which may impact financial statements of a food retail group

18

IAS 27 : Business combination

Principle

Different subsidiaries must be fully consolidated where there is a controlling interest.

What Carrefour has decided

Within Carrefour, financial subsidiaries as well as insurance companies which are controlled by the group have been until now consolidated by the equity method.In the future, these companies will be fully consolidated.

In order to give meaning to the financial statements :We will show on the balance sheet, on a separate line, the debt which has been integrated.Within the profit and loss account, the sales of these companies will be presented in « Other revenues ».

19

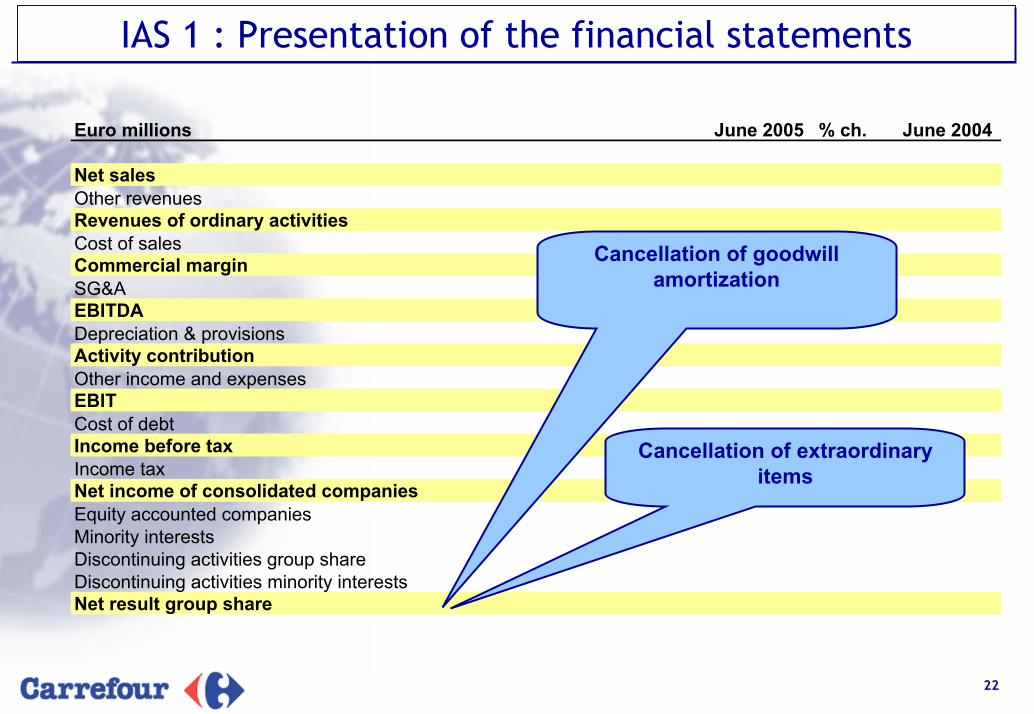

IAS 1 : Presentation of the financial statements

Principle

No requirement for standard presentation of the balance sheet and the profit and loss account.

Cancellation of the concept of extraordinary income.

Choice of presentation of profit and loss account by » nature » or by « purpose ».

What Carrefour has decided

The presentation of the balance sheet remains the same.

New presentation of the profit and loss account (see following page).

The P&L presentation by « nature » has not changed.

20

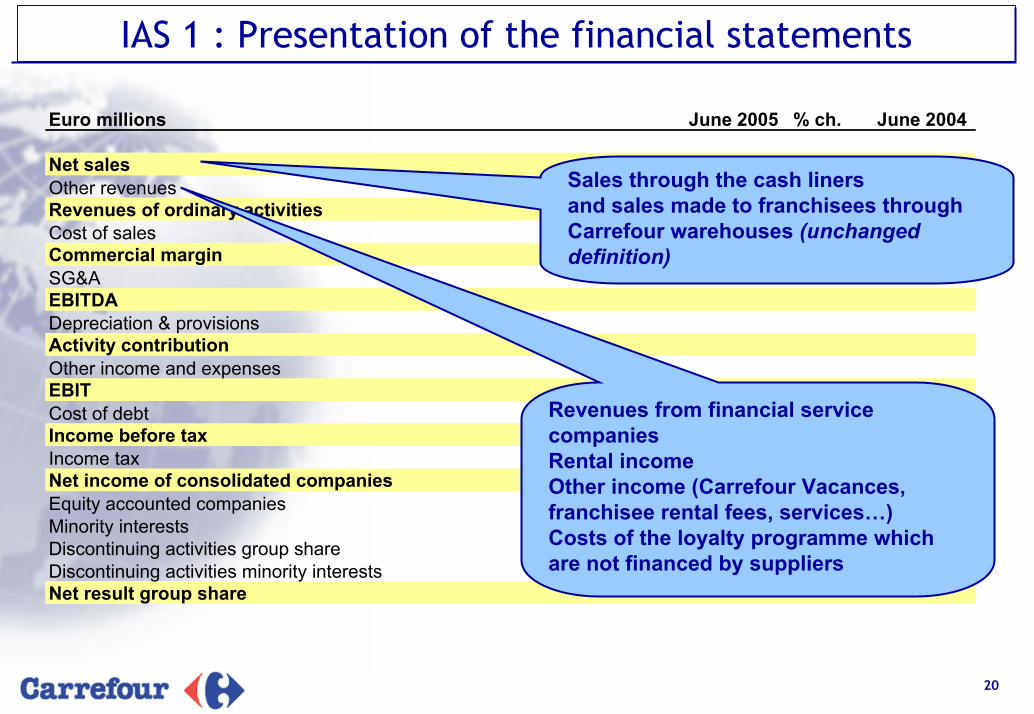

IAS 1 : Presentation of the financial statements

Euro millions June 2005 % ch. June 2004

Net salesOther revenuesRevenues of ordinary activitiesCost of salesCommercial marginSG&AEBITDADepreciation & provisionsActivity contributionOther income and expensesEBITCost of debtIncome before taxIncome taxNet income of consolidated companiesEquity accounted companiesMinority interestsDiscontinuing activities group shareDiscontinuing activities minority interestsNet result group share

Revenues from financial service companiesRental incomeOther income (Carrefour Vacances, franchisee rental fees, services…) Costs of the loyalty programme which are not financed by suppliers

Sales through the cash linersand sales made to franchisees through Carrefour warehouses (unchanged definition)

21

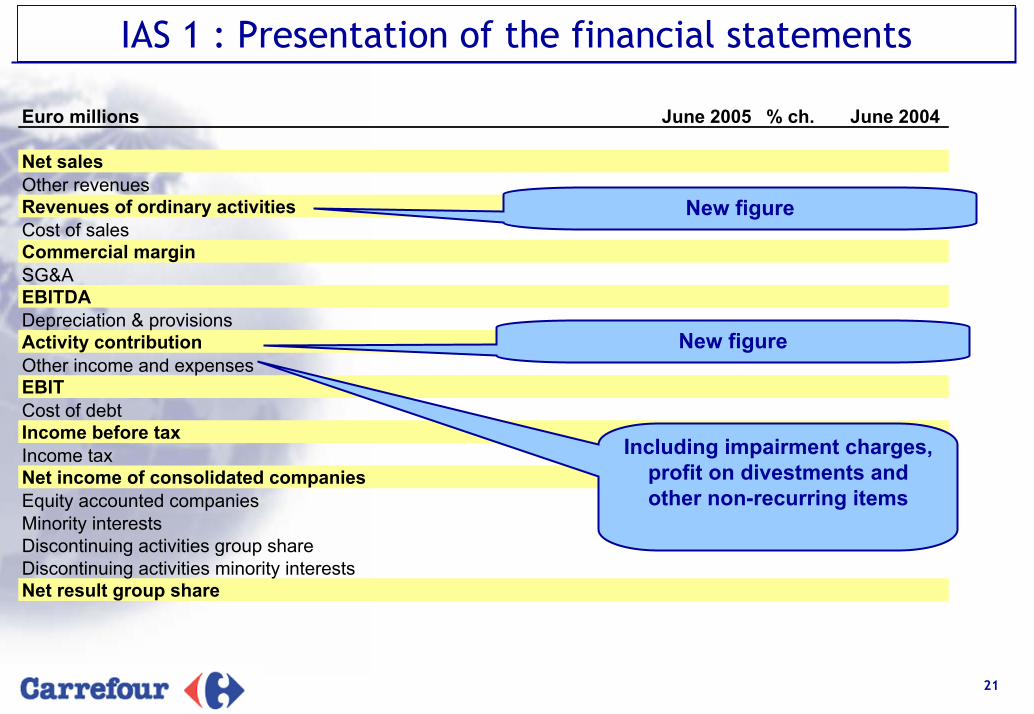

IAS 1 : Presentation of the financial statements

Euro millions June 2005 % ch. June 2004

Net salesOther revenuesRevenues of ordinary activitiesCost of salesCommercial marginSG&AEBITDADepreciation & provisionsActivity contributionOther income and expensesEBITCost of debtIncome before taxIncome taxNet income of consolidated companiesEquity accounted companiesMinority interestsDiscontinuing activities group shareDiscontinuing activities minority interestsNet result group share

Including impairment charges, profit on divestments and other non-recurring items

New figure

New figure

22

IAS 1 : Presentation of the financial statements

Euro millions June 2005 % ch. June 2004

Net salesOther revenuesRevenues of ordinary activitiesCost of salesCommercial marginSG&AEBITDADepreciation & provisionsActivity contributionOther income and expensesEBITCost of debtIncome before taxIncome taxNet income of consolidated companiesEquity accounted companiesMinority interestsDiscontinuing activities group shareDiscontinuing activities minority interestsNet result group share

Cancellation of extraordinaryitems

Cancellation of goodwill amortization

23

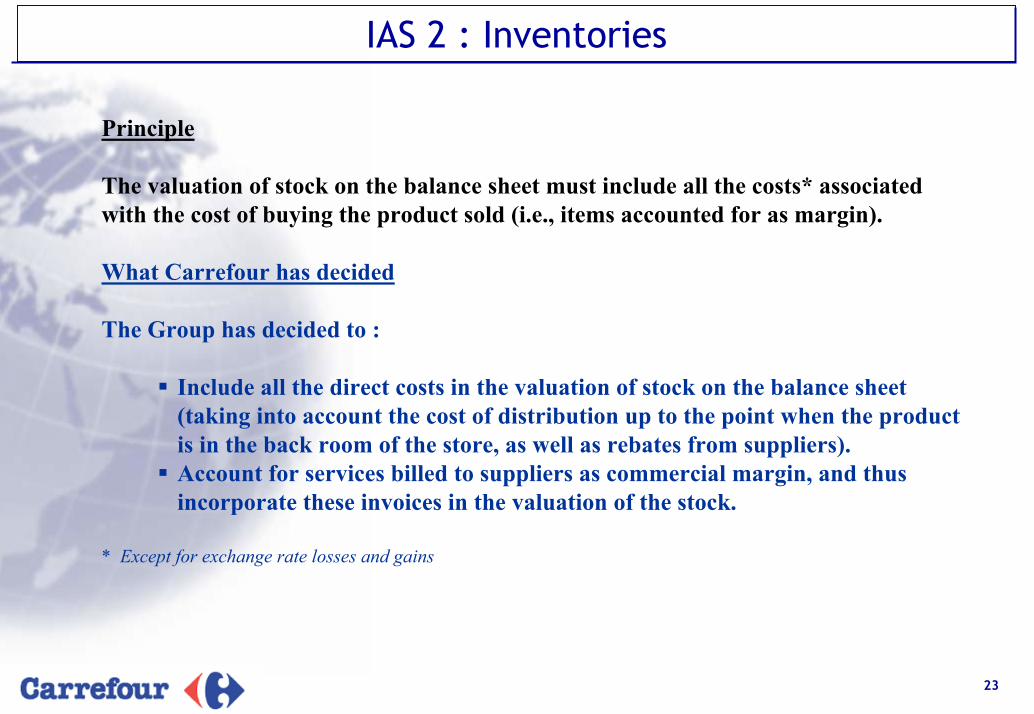

IAS 2 : Inventories

Principle

The valuation of stock on the balance sheet must include all the costs* associated with the cost of buying the product sold (i.e., items accounted for as margin).

What Carrefour has decided

The Group has decided to :

Include all the direct costs in the valuation of stock on the balance sheet (taking into account the cost of distribution up to the point when the product is in the back room of the store, as well as rebates from suppliers).Account for services billed to suppliers as commercial margin, and thus incorporate these invoices in the valuation of the stock.

* Except for exchange rate losses and gains

24

IAS 2 : Inventories

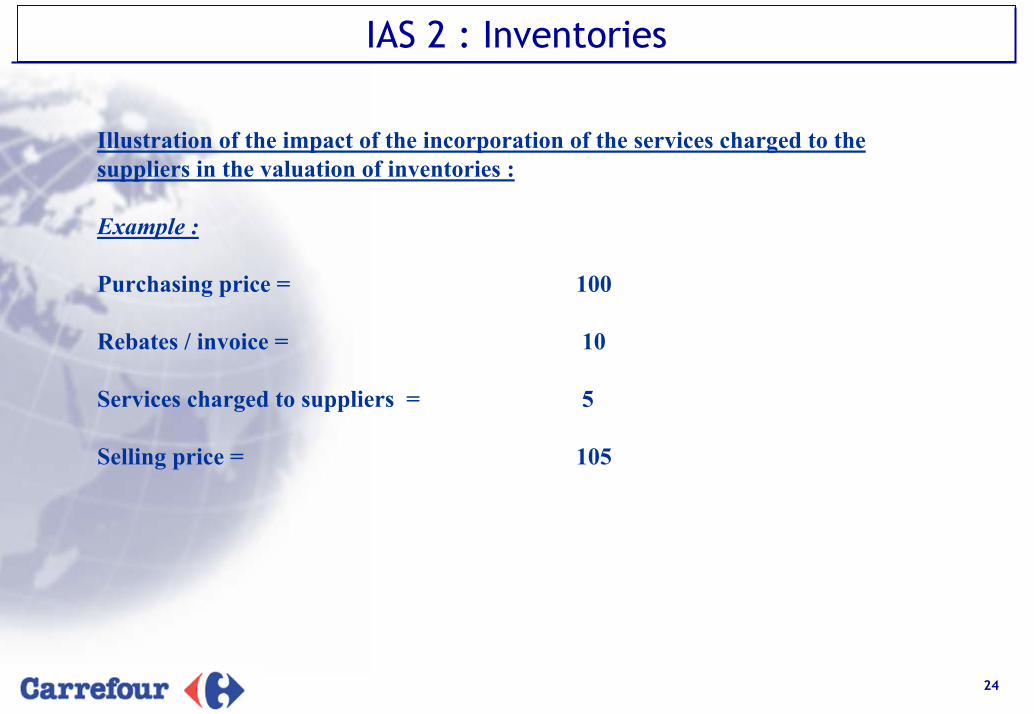

Illustration of the impact of the incorporation of the services charged to the suppliers in the valuation of inventories :

Example :

Purchasing price = 100

Rebates / invoice = 10

Services charged to suppliers = 5

Selling price = 105

25

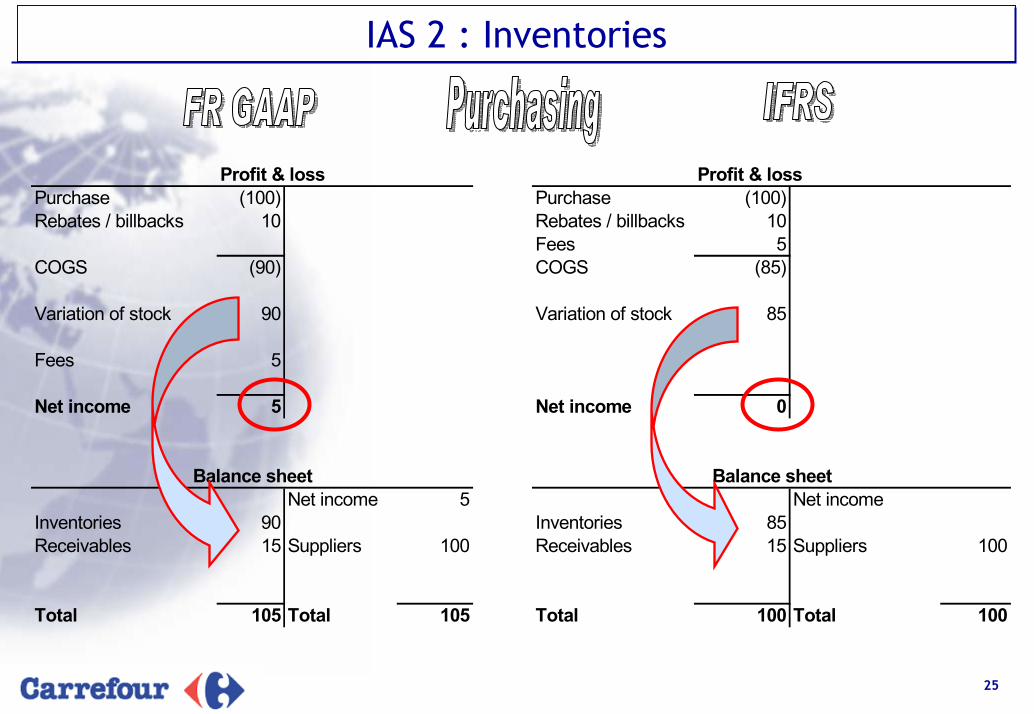

IAS 2 : Inventories

Profit & loss Profit & lossPurchase (100) Purchase (100)Rebates / billbacks 10 Rebates / billbacks 10

Fees 5COGS (90) COGS (85)

Variation of stock 90 Variation of stock 85

Fees 5

Net income 5 Net income 0

Net income 5 Net incomeInventories 90 Inventories 85Receivables 15 Suppliers 100 Receivables 15 Suppliers 100

Total 105 Total 105 Total 100 Total 100

Balance sheet Balance sheet

26

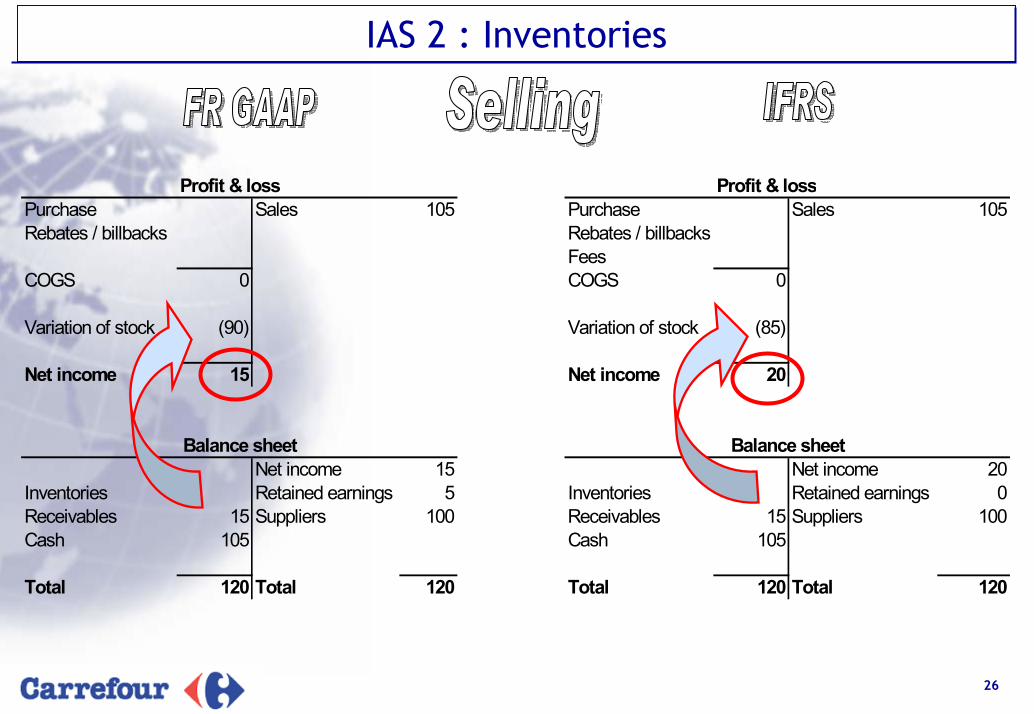

IAS 2 : Inventories

Profit & loss Profit & lossPurchase Sales 105 Purchase Sales 105Rebates / billbacks Rebates / billbacks

FeesCOGS 0 COGS 0

Variation of stock (90) Variation of stock (85)

Net income 15 Net income 20

Net income 15 Net income 20Inventories Retained earnings 5 Inventories Retained earnings 0Receivables 15 Suppliers 100 Receivables 15 Suppliers 100Cash 105 Cash 105

Total 120 Total 120 Total 120 Total 120

Balance sheet Balance sheet

27

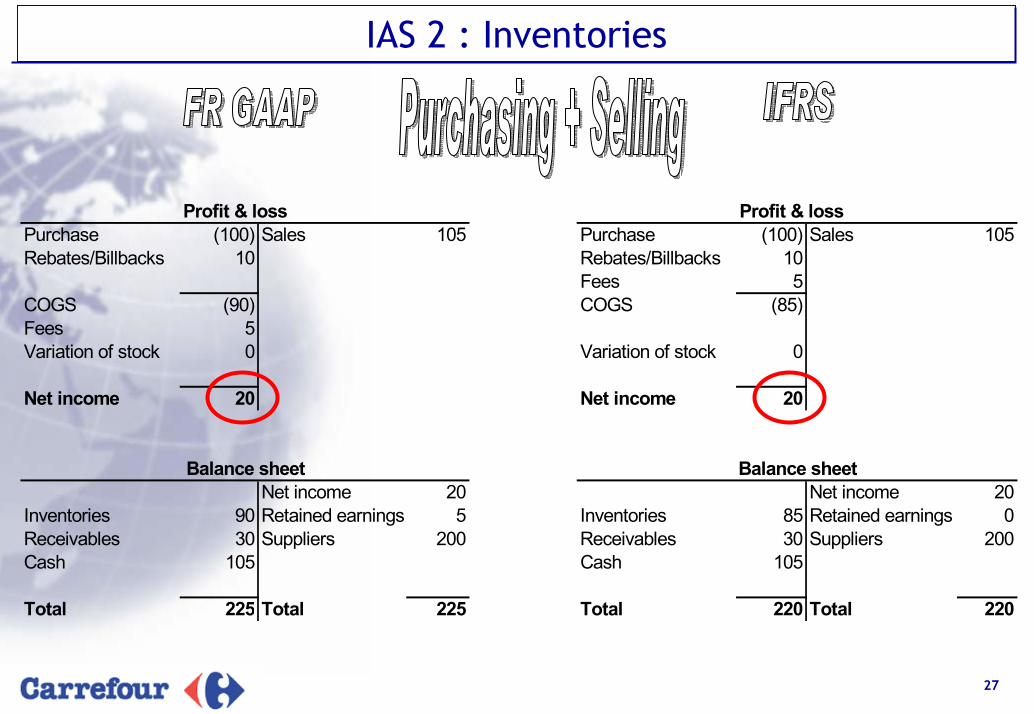

IAS 2 : Inventories

Profit & loss Profit & lossPurchase (100) Sales 105 Purchase (100) Sales 105Rebates/Billbacks 10 Rebates/Billbacks 10

Fees 5COGS (90) COGS (85)Fees 5Variation of stock 0 Variation of stock 0

Net income 20 Net income 20

Net income 20 Net income 20Inventories 90 Retained earnings 5 Inventories 85 Retained earnings 0Receivables 30 Suppliers 200 Receivables 30 Suppliers 200Cash 105 Cash 105

Total 225 Total 225 Total 220 Total 220

Balance sheet Balance sheet

28

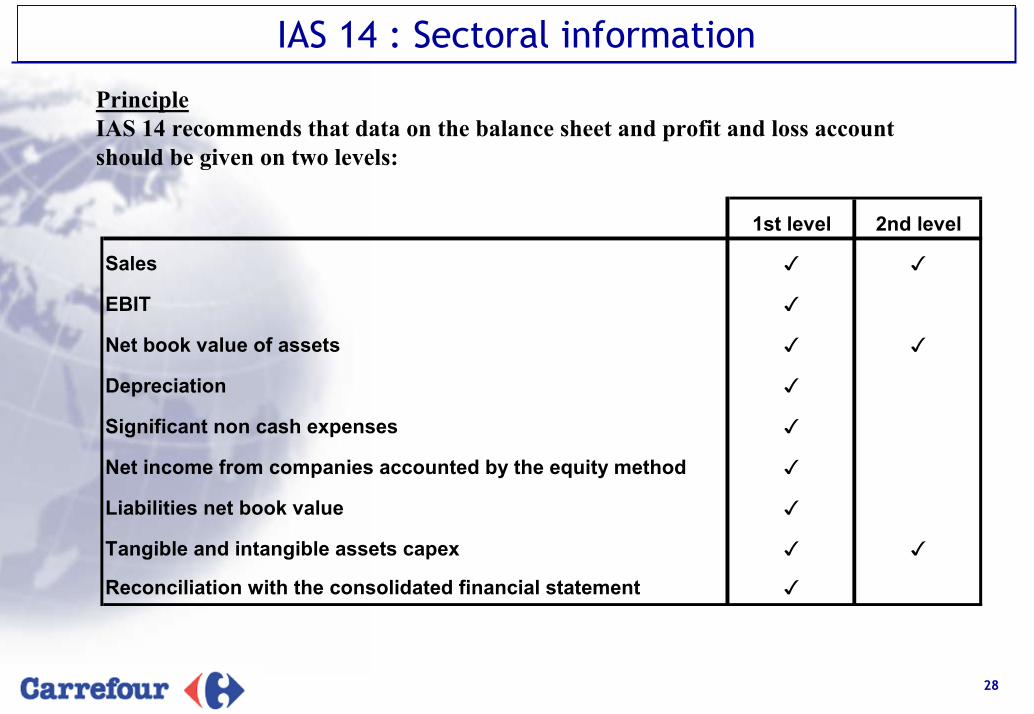

IAS 14 : Sectoral information

PrincipleIAS 14 recommends that data on the balance sheet and profit and loss account should be given on two levels:

1st level 2nd level

Sales ✓ ✓

EBIT ✓

Net book value of assets ✓ ✓

Depreciation ✓

Significant non cash expenses ✓

Net income from companies accounted by the equity method ✓

Liabilities net book value ✓

Tangible and intangible assets capex ✓ ✓

Reconciliation with the consolidated financial statement ✓

29

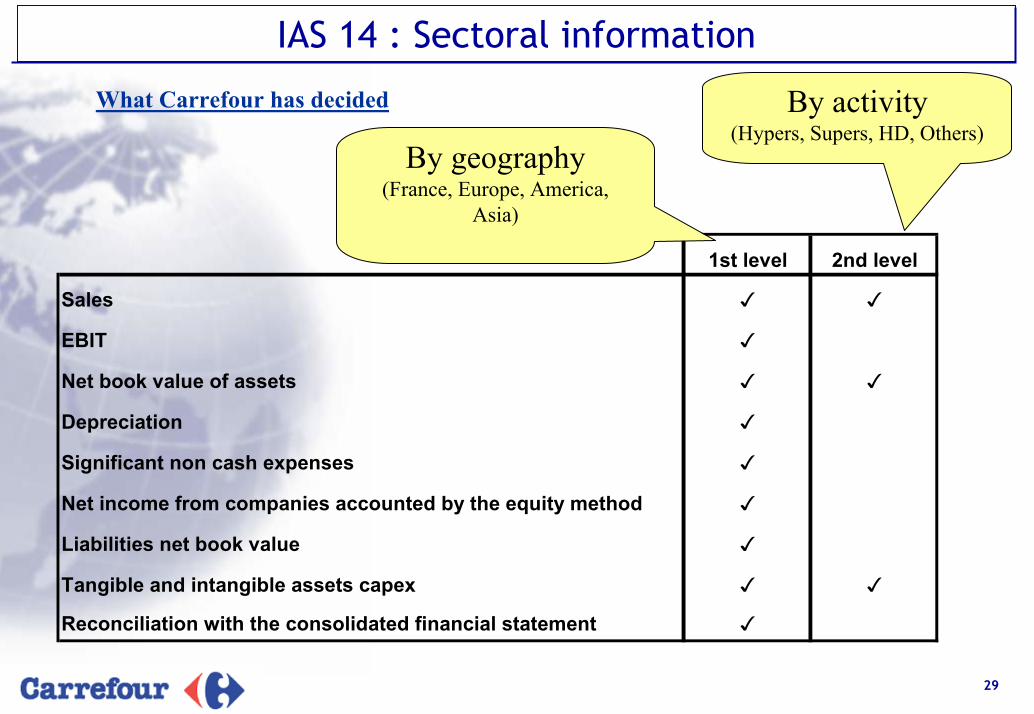

IAS 14 : Sectoral information

1st level 2nd level

Sales ✓ ✓

EBIT ✓

Net book value of assets ✓ ✓

Depreciation ✓

Significant non cash expenses ✓

Net income from companies accounted by the equity method ✓

Liabilities net book value ✓

Tangible and intangible assets capex ✓ ✓

Reconciliation with the consolidated financial statement ✓

What Carrefour has decided By activity(Hypers, Supers, HD, Others)

By geography(France, Europe, America,

Asia)

30

IAS 16 : Fixed assets

Principle / possible options

The residual value of a fixed asset can be recognised at the end of its depreciable life (and thus depreciation is limited to the purchase price minus the residual value).

A revaluation of fixed assets (by category) is also possible.

Depreciation can be calculated by each component of a fixed asset where the cost of that component is significant.

31

IAS 16 : Fixed assets

What Carrefour has decided

Given that the Group typically retains its assets, the residual value of fixed assets, once depreciated, is nil (fixed assets are thus fully depreciated).

The Group has opted not to revalue fixed assets (maintaining historical cost).

The Group has already applied the principle of calculating depreciation by each component of a fixed asset.

32

IAS 16 : Fixed assets

What Carrefour has decided (more)

Carrefour Group considers that adopting IFRS standards does not justify a change to the length of time over which assets are depreciated (given that French GAAP is similar to IFRS in requiring that assets be appreciated over their economic life or faster).

However, within the framework of the creation of Carrefour Property, our pan-European real estate holding company, the group is currently studying the possibility of adjusting the deprecation period for buildings (currently it is 20 years).

This analysis should be completed in 2005, with any new policy adopted in 2005 and with 2004 accounts restated on a pro forma basis.

33

IAS 17 : Rental agreements

Principle

IAS 17 requires that all the rental agreements must be reviewed. If it is apparent from the review of a contract that the most of the risks and rewards linked to the property are transferred to the renter, the contract must be considered as a financial lease (recognised as an asset and as a debt).

=> The definition of a financial lease is wider than under French GAAP.

What Carrefour has decided

More than 2000 contracts reviewed.

Credit lease contracts have already been restated in the consolidated accounts.

Since 2001, all new « sale & lease-backs » contracts conform with IAS 17.

The impact of applying IAS 17 will be limited.

34

IAS 18 : Revenue recognition

Principle

IAS 18 defines sales as the gross inflow of economic benefits arising from the ordinary operating activities of a company.

For sales to be recognised, most of the property risks and rewards of goods or services must be transferred to the customer.

What Carrefour has decided

The composition of sales is unchanged (sales through checkouts and sales made to franchisees through Carrefour warehouses).

Additional revenues (revenue from financial services, Carrefour Voyages, franchisee income…) will be shown in a separate line at the top of the profit and loss account.

35

IAS 19 : Employee benefits

Principle

IAS 19 concerns all benefits which might form part of an employee’s remuneration and requires that all the benefits accruing to employees are calculated on a « fair value » basis whatever their nature or due date.

IFRS requires that companies recognise a greater number of employee benefits that are accounted for than under French GAAP.

What Carrefour has decided

The Group already accounts for its pension obligations.

Taking into account its social legislation, Belgium is the main country affected by this standard, although the impact is relatively small.

36

IAS 36 : Asset depreciation

Principle

IAS 36 ensures that assets are booked at a value which does not exceed their recoverable value. The standard makes uniform impairment tests for all categories of assets.

Impairment tests are undertaken:

Systematically for non amortized assets (goodwill…).

In case of any sign of a loss of value for the other fixed assets.

What Carrefour has decided

The Group has already realized (since 2000) impairment tests on its main assets (constructions and goodwill).

As a consequence, the adoption of the standard IAS 36 has no impact on the Carrefour opening balance sheet.

37

IAS 38 : Intangible assets

Principle

The definition and terms of accounting of intangible assets under IFRS are based on the notion of control of the asset and not only on the legal notion of property as it is defined under French accounting principles.

Goodwill amortization is cancelled (replaced by impairment tests).

What Carrefour has decided

No material reclassifying of intangible assets as goodwill.

Only earnings per share before goodwill remains.

38

IAS 32/39 : Financial instruments

Considering their late adoption, the standards IAS 32 and 39 do not need to be applied in 2004.

Given that Carrefour Group has not opted for the early application of IAS 32 and 39, only the 2005 accounts will be impacted by these standards (no 2004 pro forma). Although the Group has chosen not to adopt the standards IAS 32 and 39 from 2004, the Carrefour Group has already taken measures to limit the impacts of their application:

Carrefour’s cash flow management and control systems have been adapted in order to take into account the constraints of documentation imposed by the new standards;

Considering the debt coverage policy of the Group, the application of the standards IAS 32 and 39 should not have a significant impact.

Other than the application of the standards 32 and 39, the financial result will be affected by changes of classification within the income statement (example: classification of suppliers discounts as commercial margin rather than financial income).

39

IAS 40 : Investment property

Principle

For buildings which count as «investment property» (property held for rents or to enhance the corporate value), IAS 40 gives the possibility of revaluing the buildings of investment at fair value.

Whatever option the company chooses, the standard requires the fair value of these assets to be disclosed in the notes.

What Carrefour has decided

Shopping malls constitute investment property.

The Group has not opted to revalue its investment property.

The fair value of these buildings will be given in the notes, calculated on the basis of multiple of rents.

40

IFRS 1 : First adoption of IFRS

Principle

IFRS 1 is about how IFRS standards should be adopted. This standard offers several options among which:

Possibility of resetting to zero translation adjustments accumulated up to January 1st, 2004 (transfer of translation adjustments in undistributed profits);

Transfer on January 1st, 2004 of translation adjustments in undistributed profits (reserves);

No retrospective restatement of group consolidation booked before January 1st, 2004 ;

No restatement of group consolidation made before January 1st, 2004 (which would have led to new accounting for the Carrefour / Promodès merger).

41

IFRS 1 : First adoption of IFRS

What Carrefour has decided

The Carrefour Group has decided:

Possibility of applying IAS 32 and IAS 39 on January 1st, 2005 with no pro forma comparison in 2004.

adopting the standards IAS 32 and 39 on January 1st, 2005 with no pro forma comparison in 2004.

Possibility of proceeding to partial assets revaluations on January 1st, 2004.

No asset revaluation.

Possibility of booking any shortfall related to social commitments in opening shareholder equity.

All social commitments will be accounted for in the opening shareholder equity.

42

IFRS 2 : Stock options plans

Principle

Under IFRS, there is an obligation to book as an expense the fair value of the remuneration arising from stock option plans granted to employees, in return for an increase of shareholder equity, as and when they are used (the period during which they are used corresponds to the period in which they are granted).

Such a principle does not exist at present under French standards.

What Carrefour has decided

The stock options granted since November, 2002 will be booked from now as “employee expenses”. The expense will be spread from the date of allocation to the first date of possible exercise.

43

Treasury shares (IAS 32)

Principle

Under IFRS, treasury shares must be written off against shareholder equity.

What Carrefour has decided

Treasury shares held to serve stock-option plans were classified until now as transferable securities of investment and were included in the calculation of the net debt. In case of any loss of value, a reserve was allocated against profit.Under IFRS, treasury shares will be written off against shareholder equity and share price movements will not affect financial statements.

44

ConclusionConclusion

The transition to the IFRS standards will have limited impact on Carrefour for the following reasons:

Conservative options have been chosen (no revaluation…)

Historically careful accounting policy applied by the Group (Carrefour always applied standards close to US standards and thus IFRS when it was compatible with the French standards, for example: impairment tests…)

The adoption of certain standards has already been anticipated (IAS 17 since 2002)

Nevertheless, changes to definitions make a review necessary

45

ConclusionConclusion

Income statement :

Some reclassifying line with line (example: supplier discounts from financial income to commercial margin …)

Nevertheless the EBIT should remained relatively stable as % of sales

The main impact on the group share of net income will be the cancellation of goodwill amortization.

46

ConclusionConclusion

Balance sheet :

The main impact in terms of presentation is the change from the equity method to a global consolidation of financial companies (however this impact will be isolated)

Operating working capital will improve because of the incorporation in stocks of suppliers’ services

The amount of provisions will be impacted by the application of the standard IAS 19 (Belgium)

Treasury shares will be cancelled from shareholders equity

Finally, some items will be reclassified

47

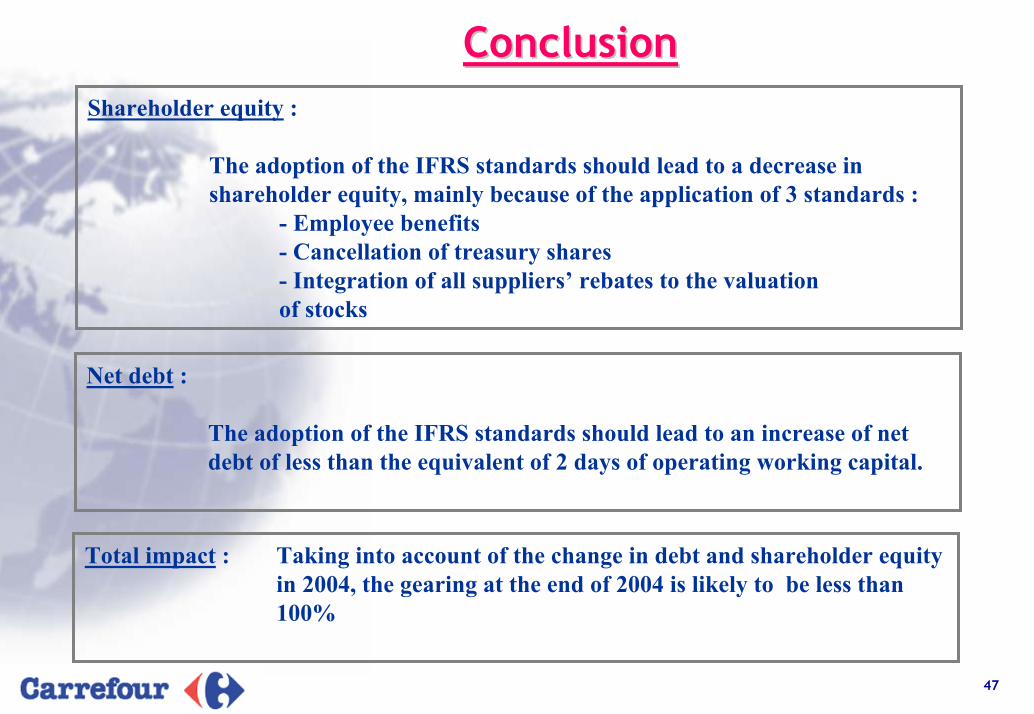

ConclusionConclusionShareholder equity :

The adoption of the IFRS standards should lead to a decrease in shareholder equity, mainly because of the application of 3 standards :

- Employee benefits- Cancellation of treasury shares- Integration of all suppliers’ rebates to the valuation of stocks

Net debt :

The adoption of the IFRS standards should lead to an increase of net debt of less than the equivalent of 2 days of operating working capital.

Total impact : Taking into account of the change in debt and shareholder equityin 2004, the gearing at the end of 2004 is likely to be less than100%