transnet pipelines tariffs 2010/2011 - decision & reasons - nersa

TRANSCRIPT

IDMS No. 45374

NATIONAL ENERGY REGULATOR OF SOUTH AFRICA In the matter regarding

TRANSNET LIMITED’S TARIFF APPLICATION FOR:

A 51.3% ALLOWABLE REVENUE INCREASE FOR ITS PETROLEUM PIPELINES SYSTEM FOR 2010/11

THE DECISION

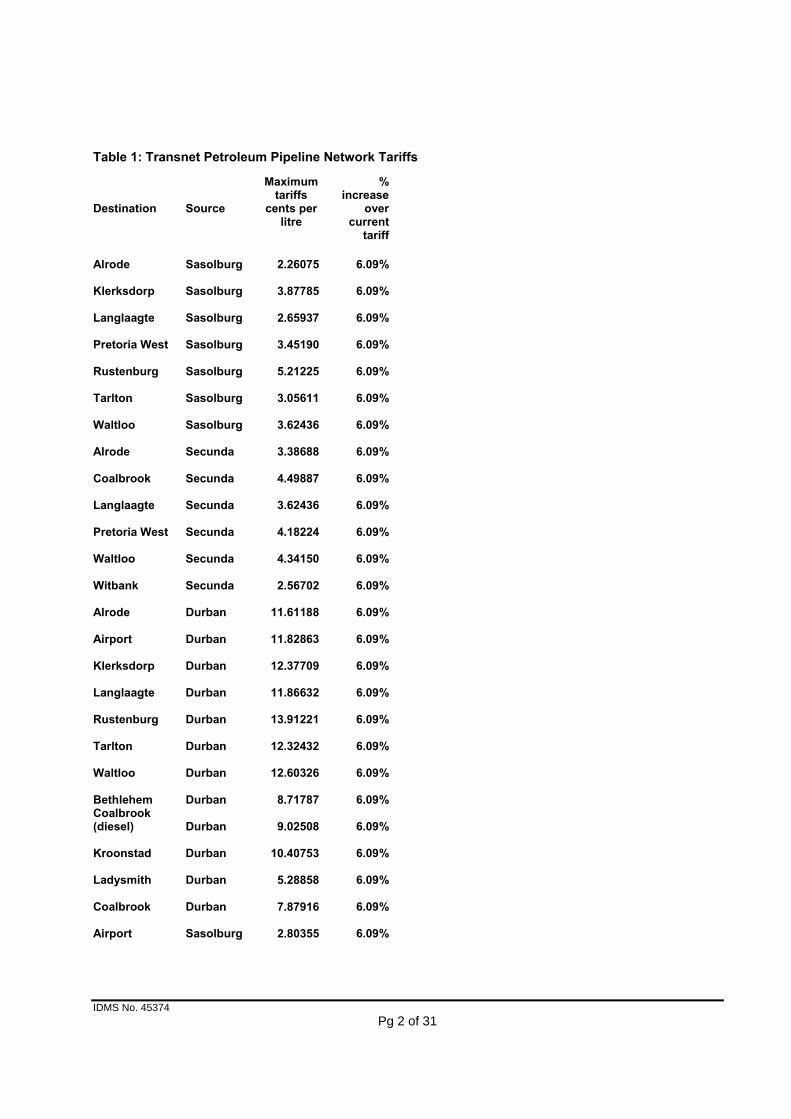

On 25 March 2010 the Energy Regulator amended Transnet Limited’s licence to operate its

petroleum pipeline system by setting tariffs as a condition of that licence. The maximum

tariffs, set out in Table 1, are exclusive of VAT and will apply with effect from 1 April 2010.

(a) The tariffs in Table 1 will be adjusted, if necessary, after applying the claw back

mechanism contemplated in the Tariff Methodology for the Petroleum Pipelines

Industry adopted by the Energy Regulator (“the Methodology”) at the next tariff

review.

(b) The tariffs will enable the applicant to realise an 11.86% increase in Allowable

Revenue compared to the 2009/10 tariff period (an increase from R1,093.93 million

in 2009/10 to R1,223.63 million in 2010/11).

(c) The tariffs in Table 1 represent a 6.09% across-the-board increase over the 2009/10

tariffs without further tariff restructuring. The Energy Regulator will continue its

investigation and consultation process on tariff restructuring during 2010 and the

results of the investigation will be considered in the next tariff period.

IDMS No. 45374

Pg 2 of 31

Table 1: Transnet Petroleum Pipeline Network Tariffs

Destination Source

Maximum tariffs

cents per litre

% increase

over current

tariff

Alrode Sasolburg

2.26075 6.09%

Klerksdorp Sasolburg

3.87785 6.09%

Langlaagte Sasolburg

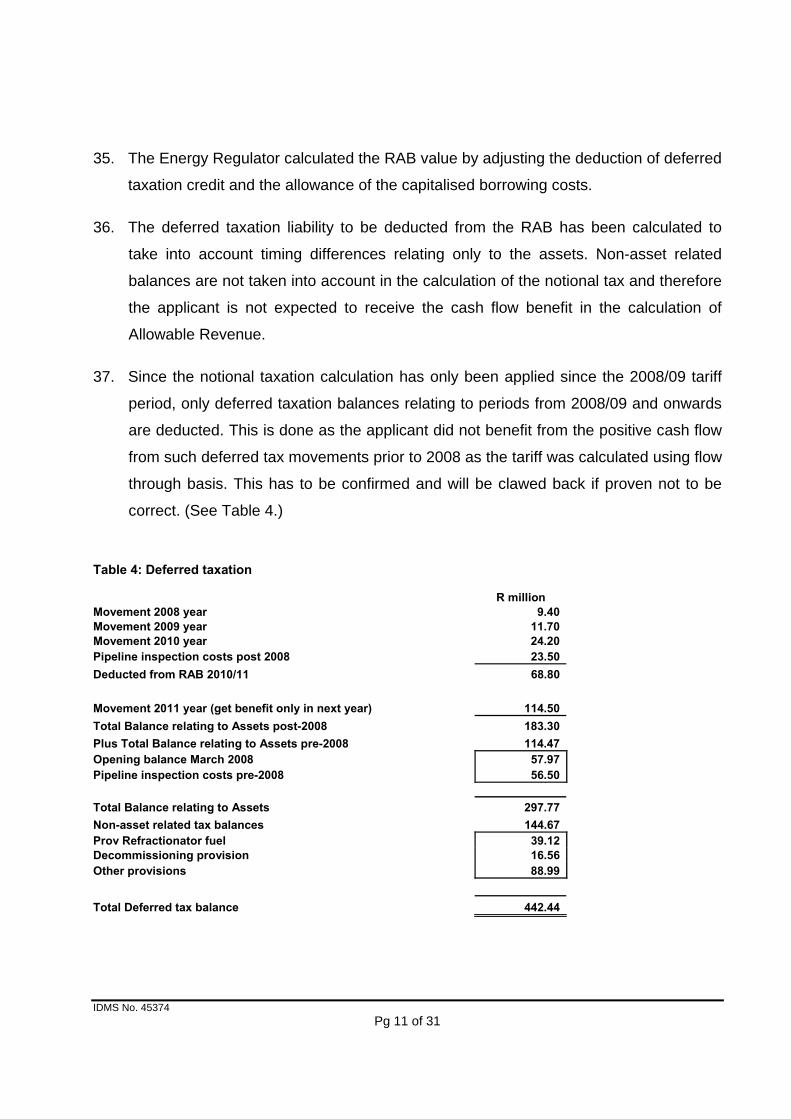

2.65937 6.09%

Pretoria West Sasolburg

3.45190 6.09%

Rustenburg Sasolburg

5.21225 6.09%

Tarlton Sasolburg

3.05611 6.09%

Waltloo Sasolburg

3.62436 6.09%

Alrode Secunda

3.38688 6.09%

Coalbrook Secunda

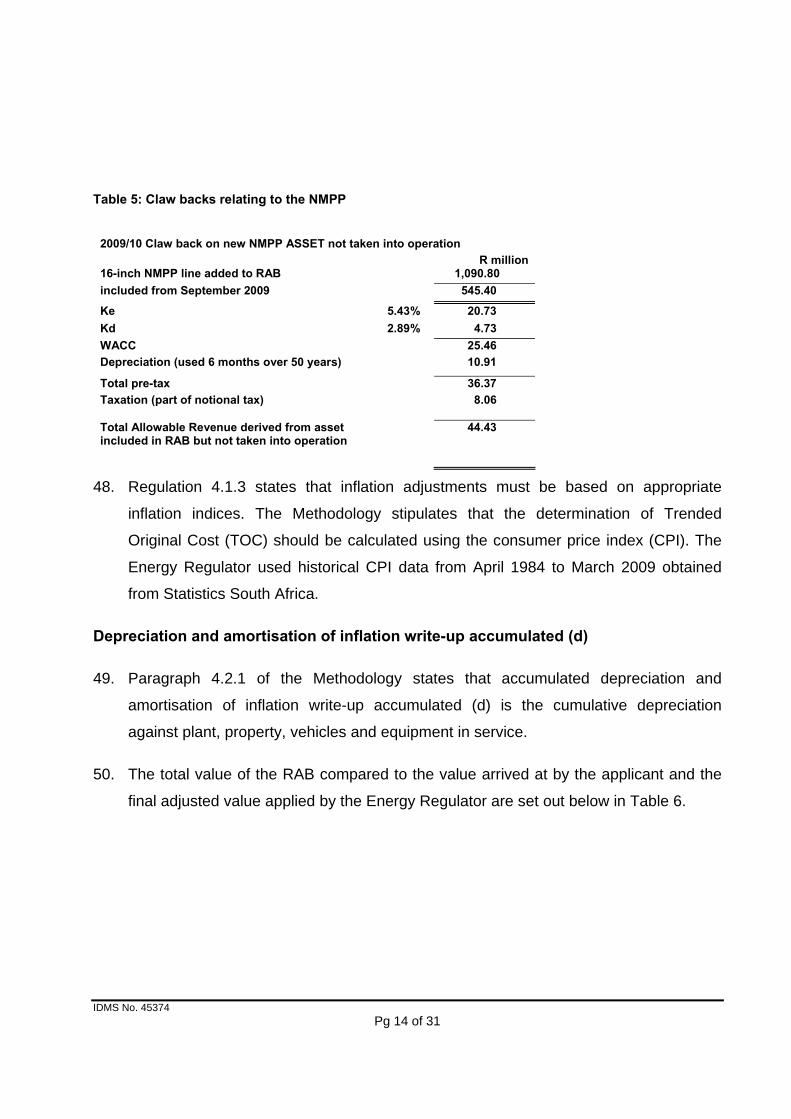

4.49887 6.09%

Langlaagte Secunda

3.62436 6.09%

Pretoria West Secunda

4.18224 6.09%

Waltloo Secunda

4.34150 6.09%

Witbank Secunda

2.56702 6.09%

Alrode Durban

11.61188 6.09%

Airport Durban

11.82863 6.09%

Klerksdorp Durban

12.37709 6.09%

Langlaagte Durban

11.86632 6.09%

Rustenburg Durban

13.91221 6.09%

Tarlton Durban

12.32432 6.09%

Waltloo Durban

12.60326 6.09%

Bethlehem Durban

8.71787 6.09% Coalbrook (diesel) Durban

9.02508 6.09%

Kroonstad Durban

10.40753 6.09%

Ladysmith Durban

5.28858 6.09%

Coalbrook Durban

7.87916 6.09%

Airport Sasolburg

2.80355 6.09%

IDMS No. 45374

Pg 3 of 31

(d) The increase in Allowable Revenue is reduced by claw back adjustments to the

value of R64.91 million arising from excess revenue accrued in previous years. (e) The Energy Regulator has used the applicant’s inflation adjusted 2006 modern

equivalent asset value (MEAV) Regulatory Asset Base (RAB) value for this tariff

period on an interim basis. The applicant’s starting regulatory asset base (SRAB)

has recently been verified and determined; and any consequential tariff adjustments

will be made in the next tariff period.

(f) The Energy Regulator has used the applicant’s estimated depreciation for this tariff

period only. The applicant’s depreciation will be determined once the SRAB

verification findings have been assessed. The depreciation amount allowed may

change depending upon the outcome of the SRAB verification.

(g) The Allowable Revenue includes a pre-tax claw back of R27.62 million (reduction of

Allowable Revenue) in respect of the final claw back relating to the 2008/09 tariff

period.

(h) The applicant’s operational expenses for the 2009/10 tariff period will be investigated

during the current tariff period and any adjustments will be made in the next tariff

review.

IDMS No. 45374

Pg 4 of 31

Reasons for Decision

The application 1. On 16 November 2009, Transnet Limited submitted an application for increases in

its allowable revenue for its petroleum pipeline tariffs (“the application”), licensed for

operation by the Energy Regulator on 29 March 2007 under licence number

PPL.p.F3/20/1/2006. This tariff application was made in terms of section 23 of the

Petroleum Pipelines Act, 2003 (Act No. 60 of 2003), (hereinafter referred to as “the

Act”).

The applicant 2. Transnet Limited (hereinafter referred to as “the applicant” or Transnet), is a public

company registered and incorporated as such in terms of the company laws of the

Republic of South Africa pursuant to the Legal Succession to the South African

Transport Services Act, 1989 (Act No 13 of 1989). The applicant’s company

registration number is 1990/000900/06 and its registered head office is at 47th Floor,

Carlton Centre, 150 Commissioner Street, Johannesburg. Transnet operates the

country’s rail network (Transnet Freight), its ports (National Ports Authority),

petroleum and gas pipelines (Transnet Pipelines) and other operations such as the

South African Ports Operations and Transwerk. Transnet Pipelines is a division of

Transnet Limited that operates petroleum pipelines and a gas pipeline.

3. Transnet Limited is a diversified transport and logistics group wholly owned by the

South African Government.

4. Through its Transnet Pipelines division the applicant operates approximately

2,775 km of pipelines conveying refined petroleum products, crude oil and gas as

well as a storage facility for petroleum products at Tarlton near Krugersdorp. It is the

IDMS No. 45374

Pg 5 of 31

dominant pipeline operator in South Africa and has a de facto monopoly of the

pipeline conveyance of petroleum from Durban to inland destinations.

5. This decision concerns only the petroleum pipelines activities of Transnet.

6. On 12 September 2007, Transnet Limited was granted a construction licence

(Licence Number PPL.p.F1/74-75/2007) to construct a 24-inch diameter petroleum

products pipeline from Durban to Jameson Park and pipelines from Jameson Park to

Alrode/Langlaagte and from Kendal to Waltloo, inclusive of accumulation facilities at

Durban and Jameson Park. The applicant has named this project the New Multi-

Products Pipeline (NMPP).

The decision-making process 7. A public version of the tariff application received on 16 November 2009 was

published on the NERSA website on 24 November 2009. This version excluded

certain information that the Energy Regulator had decided was confidential.

8. Notices inviting the public to comment on the tariff application were placed in the

Sowetan, Independent Newspapers (Business Report) and Business Day on

24 November 2009.

9. The following stakeholders commented on Transnet’s tariff application: BP Southern

Africa (Pty) Ltd. (BPSA), Chevron South Africa (Pty) Limited (Chevron), Engen

Petroleum Limited (Engen), Petroline RSA (Proprietary) Limited (Petroline) and

Sasol Oil (Pty) Limited (Sasol).

10. The comments from stakeholders were published on the NERSA website on

20 January 2010.

11. In order to process the application, the Energy Regulator requested additional

information from Transnet. In view of the time involved in obtaining the information

IDMS No. 45374

Pg 6 of 31

from Transnet and completing the analysis, the Energy Regulator was not in a

position to publish a draft tariff determination for this tariff application. The Energy

Regulator will issue minimum information requirements for future tariff applications.

12. On 9 February 2010 the Energy Regulator published a Discussion Document for

public comment about selected matters pertaining to Transnet’s application.

13. The matters raised in the Discussion Document and on which stakeholders’

comments were requested included:

• the starting regulatory asset base (SRAB);

• tariff design; and

• the beta.

14. Comments from the following stakeholders were received: Transnet, Total South

Africa (Pty) Limited (Total), Sasol and Petroline.

15. A public hearing on the tariff application was held on 4 March 2010. The following

entities presented their views at the hearing: Transnet, BPSA, Total, Sasol and

Petroline.

Applicable law 16. The Energy Regulator derives its mandate to set tariffs for petroleum pipelines from

the Act.1

17. The manner in which tariffs must be set is prescribed by regulation (see GN R342

Government Gazette No. 30905 of 4 April 2008).

18. In terms of section 28 of the Act, tariffs set by the Energy Regulator to be charged by

licensees must be based on a “systematic methodology applicable on a consistent

1 See sections 4(f) and 28 of the Act.

IDMS No. 45374

Pg 7 of 31

and comparable basis”2. To this end the Energy Regulator approved a Tariff

Methodology for the Petroleum Pipelines Industry (hereinafter “the Methodology”)

that outlines the approach taken in this decision. On 26 November 2009, the

Methodology was revised (4th Amendment of the Methodology) after following the

appropriate administrative processes. The Methodology is available on the NERSA

website.3

Overview of the application 19. Transnet applied for an increase in its allowable revenue of 51.3% for the period

1 April 2010 to 31 March 2011. In its application, Transnet also performed a

calculation using the NERSA approved Tariff Methodology (available at that time

and which has subsequently been amended) and the calculation resulted in an

Allowable Revenue increase of 17.9%. The main difference between the two

methodologies applied by the applicant is attributable to the determination of the

cost of equity (Ke) and claw backs.

20. Transnet plans to bring into use a part of its NMPP project at a cost of R2,075 million

in June 2010. Therefore a pro rata value of 75% of the cost has been included in the

RAB in the 2010/11 tariff period. These assets were also planned to be taken into

operation in September 2009 and were taken pro rata (50%) into the RAB

calculation for the 2009/10 tariff period. Since the implementation has been

postponed to this tariff period (June 2010), a claw back will be applied on the value

included in the previous period.

21. The applicant applied for Allowable Revenue of R1,655.6 million (51.3% increase).

Transnet states in its application that it arrived at the Allowable Revenue by

deviating from the Tariff Methodology. When following its interpretation of the

Methodology, Transnet arrived at an Allowable Revenue of R1,289.85 million (17.9%

increase).

2 Section 28(2)(a) of the Act 3 www.nersa.org.za

IDMS No. 45374

Pg 8 of 31

22. The application did not include pipeline tariffs; it only requested an Allowable

Revenue.

ASSESSMENT OF THE APPLICATION

Calculation of Allowable Revenue

23. The formula for the calculation of Allowable Revenue (AR) is:

Allowable Revenue = (RAB x WACC) + E + T + D + F ± C Where: RAB = Regulatory Asset Base

WACC = weighted average cost of capital

E = Expenses: maintenance and operating expenses for the tariff period

under review

T = Tax: estimated tax expense for the tariff period under review

D = Depreciation: the charge for the tariff period under review

F = approved revenue addition to meet debt obligations for the tariff period

under review

C = Claw-back adjustment (to correct for differences between actuals and

forecasts in formula elements as well as efficiency gains and volume

differences) from a preceding tariff period in relation to the latest

estimates for that tariff period

24. Data as supplied by Transnet was used for most of the calculations performed in this

determination. Where this was not the case, the reasons for not using the applicant’s

data are supplied throughout the assessment.

IDMS No. 45374

Pg 9 of 31

25. The values of several of the components in the Allowable Revenue formula provided

in the Methodology had to be calculated for the purpose of assessing the applicant’s

tariffs.

26. NERSA’s calculations lead to an increase of 11.86 % in Allowable Revenue from

R1,093.93 million for 2009/10 to R1,223.63 million for the 2010/11 tariff period.

27. This increase would have been higher (20.1% instead of 11.86%) if not reduced by the

claw back provisions arising from excess revenue allowed in previous years.

28. Appendix A presents the NERSA calculated Allowable Revenue in comparison with

the Allowable Revenue as calculated by Transnet in its application.

Regulatory Asset Base (RAB) 29. The Methodology prescribes the RAB value determination as follows:

Regulatory Asset Base = Trended Original Cost of Property, Plant, Vehicles &

Equipment (V) – depreciation and amortisation of inflation write-up accumulated up

to the commencement of the tariff period under review (d) + Net Working Capital (w)

± deferred tax (dtax). The formula for determining the RAB is:

RAB = V – d + w ± dtax Where: V = Value of property, plant, vehicles and equipment

d = depreciation accumulated up to the commencement of the tariff period

under review

w = net working capital

dtax = deferred tax

30. The relevant regulation pertaining to the determination of the Regulatory Asset Base is

regulation 5(2) of the Regulations made in terms of the Petroleum Pipelines Act

(Government Notice No. R342 of 4 April 2008).

IDMS No. 45374

Pg 10 of 31

31. The applicant submitted that the value of its operating non-current Assets (V-d) is

R5,526.8 million based on the 2006 modern equivalent asset valuation (MEAV)

performed by AD Little adjusted for inflation using inflation indices obtained from the

Bureau for Economic Research (BER).

32. During this tariff period capital asset expenditure (CAPEX) projects to the value of

R2,075 million will be taken into operation (which are part of the New Multi-Product

Pipeline (NMPP) project from June 2010 and hence 75% (R1,556 million) of that value

has been admitted to the RAB. (See Table 2 for the value of Capital Expenditure.)

Table 2: Capital expenditure

Value (V-d) (R m)

Net borrowing

Cost (R m)

Capitalized value (R m)

Working Capital (w)

(R m)

Deferred taxation

(R m)

Total RAB (R m)

New NMPP 16 inch- Pro rata (9/12) 1,327.10 229.44 1,556.54 87.00 (28.60) 1,614.94 New NMPP 16 inch-100% 1,769.46 305.92 2,075.38 116.00 (38.13) 2,153.25

33. The applicant estimates its working capital (w) during the tariff review period to be

R372.6 million or R342.10 million using the NERSA methodology. NERSA calculated

the working capital to be R334.87 million in line with the calculated Allowable

Revenue.

34. The applicant therefore submits that its average Regulatory Asset Base (RAB) is

R6,080.90 million (R5,929.70 million based on NERSA approved Methodology). (See

Table 3.)

Table 3: Transnet application

R million Transnet application 2010/2011

Network Component

Value (V-

d) Net borrowing

Cost Working Capital

(w) Deferred taxation Total RAB

a b c d e=a+b+c-d 5,526.80 217.40 372.60 (36.00) 6,080.80

IDMS No. 45374

Pg 11 of 31

35. The Energy Regulator calculated the RAB value by adjusting the deduction of deferred

taxation credit and the allowance of the capitalised borrowing costs.

36. The deferred taxation liability to be deducted from the RAB has been calculated to

take into account timing differences relating only to the assets. Non-asset related

balances are not taken into account in the calculation of the notional tax and therefore

the applicant is not expected to receive the cash flow benefit in the calculation of

Allowable Revenue.

37. Since the notional taxation calculation has only been applied since the 2008/09 tariff

period, only deferred taxation balances relating to periods from 2008/09 and onwards

are deducted. This is done as the applicant did not benefit from the positive cash flow

from such deferred tax movements prior to 2008 as the tariff was calculated using flow

through basis. This has to be confirmed and will be clawed back if proven not to be

correct. (See Table 4.)

Table 4: Deferred taxation

R million Movement 2008 year 9.40 Movement 2009 year 11.70 Movement 2010 year 24.20 Pipeline inspection costs post 2008 23.50 Deducted from RAB 2010/11 68.80

Movement 2011 year (get benefit only in next year) 114.50 Total Balance relating to Assets post-2008 183.30 Plus Total Balance relating to Assets pre-2008 114.47 Opening balance March 2008 57.97 Pipeline inspection costs pre-2008 56.50 Total Balance relating to Assets 297.77 Non-asset related tax balances 144.67 Prov Refractionator fuel 39.12 Decommissioning provision 16.56 Other provisions 88.99 Total Deferred tax balance 442.44

IDMS No. 45374

Pg 12 of 31

38. Note that the deferred taxation credit which accrues during the current (2010/11) tariff

period is not deducted from the asset base as the applicant will only receive the cash

flow benefit thereof in years to come and therefore the applicant should not be

penalised for it during this tariff period.

Valuation of property, plant, vehicles and equipment (V)

39. The Regulations require the use of historic cost.

40. Section 4.1.2 of the Methodology states that non-current assets are to be valued on

the Trended Original Cost (TOC) basis or in accordance with Regulation 4(7)(b) -

Regulations made in terms of the Petroleum Pipelines Act (Government Notice No. R

342 of 4 April 2008).

41. When determining the RAB the Energy Regulator considered regulation 4(7)(b) of the

Regulations, which states that:

“...for assets in operation at the time of promulgation of these Regulations and for

which historical cost records do not exist, an estimated value that the Authority

accepts as most closely approximating their historical cost…”

42. The applicant has used the modern equivalent asset valuation (MEAV) to calculate its

RAB which is not in compliance with the Regulations.

43. The Energy Regulator has been confronted with this situation before and decided

previously that:

“the Energy Regulator has used the applicant’s inflation adjusted 2006 modern

equivalent asset value (MEAV) Regulatory Asset Base (RAB) for this tariff period

only and on an interim basis. The starting RAB (SRAB) will be determined in due

course and these tariffs may be adjusted thereafter if warranted;”4

4 NATIONAL ENERGY REGULATOR OF SOUTH AFRICA, in the matter regarding, TRANSNET LIMITED’S TARIFF APPLICATION FOR: A 74.42% TARIFF INCREASE FOR THE PETROLEUM PIPELINES NETWORK FOR 2009/10 (AS REVISED ON 26 FEBRUARY 2009), 30 April 2009, page 3.

IDMS No. 45374

Pg 13 of 31

44. A verification exercise to determine a suitable SRAB has been undertaken, however

only on a high level basis thus far. The Energy Regulator is still analysing the results.

Initial indications are that the RAB will be lower than the RAB values used in the

2008/09 and 2009/10 tariff determinations.

45. For the 2010/11 tariff period, the Energy Regulator will continue to use the MEAV

values as supplied by Transnet. Once the necessary detailed calculations have been

performed and assessed, it is the intention of the Energy Regulator to use these

amounts to recalculate the Allowable Revenues for 2008/09, 2009/10 and 2010/11. If,

as expected, there is a resulting reduction in the RABs for 2008/09, 2009/10 and

2010/11, then a claw back will be made in the 2011/12 tariff year.

46. Assets that will be brought into use in the tariff period under review will be three

16-inch pipelines5 with a cost of R2,075 million constructed as part of the NMPP

project. Commencement of operation is expected at the end of June 2010. Therefore

a pro rata value of 75% of the cost has been included in the RAB.

47. An asset valued at R1,090 million should have been in operation as of

September 2009 as per the 2009/10 tariff application. This asset was not taken into

operation at that date and it forms part of the R2,075 million NMPP project to be taken

into operation in July 2010. Since this asset was not taken into operation at the

projected date, a claw back for 2009/10 has been made which will reduce the

Allowable Revenue in this decision. This claw back calculation is set out below in

Table 5.

5 (i) from Jameson Park to Alrode; (ii) from Alrode to Langlaagte; and (iii) from Kendal to Waltloo.

IDMS No. 45374

Pg 14 of 31

Table 5: Claw backs relating to the NMPP

2009/10 Claw back on new NMPP ASSET not taken into operation R million 16-inch NMPP line added to RAB 1,090.80 included from September 2009 545.40

Ke 5.43% 20.73 Kd 2.89% 4.73 WACC 25.46 Depreciation (used 6 months over 50 years) 10.91

Total pre-tax 36.37 Taxation (part of notional tax)

8.06

Total Allowable Revenue derived from asset included in RAB but not taken into operation

44.43

48. Regulation 4.1.3 states that inflation adjustments must be based on appropriate

inflation indices. The Methodology stipulates that the determination of Trended

Original Cost (TOC) should be calculated using the consumer price index (CPI). The

Energy Regulator used historical CPI data from April 1984 to March 2009 obtained

from Statistics South Africa.

Depreciation and amortisation of inflation write-up accumulated (d)

49. Paragraph 4.2.1 of the Methodology states that accumulated depreciation and

amortisation of inflation write-up accumulated (d) is the cumulative depreciation

against plant, property, vehicles and equipment in service.

50. The total value of the RAB compared to the value arrived at by the applicant and the

final adjusted value applied by the Energy Regulator are set out below in Table 6.

IDMS No. 45374

Pg 15 of 31

Table 6: Summary of the RAB values

Application NERSA

decision Regulated Asset Base (V-d) 5,526.80 5,526.80 Net borrowing costs 217.40 186.20 Deferred taxation (35.90) (68.80) Working capital (w) 372.60 334.87

Regulated Asset base (RAB) 6,080.90 5,979.07

Net working capital (w)

51. According to the Methodology, net working capital is to be determined by the following

formula:

Net working capital = inventory + receivables + operating cash + minimum cash balance – trade payables.

52. Table 7 presents the Energy Regulator’s determination and compares it with

Transnet’s calculation. The differences are due to the higher receivables based on a

higher Allowable Revenue used by the applicant.

Table 7: Net working capital

Net working capital (w) Application NERSA Decision Allowable Revenue 1,655.60 1,223.63 Operational expenditure 661.80 661.80 -Inventory 234.30 234.30 -Receivables 138.30 100.57 -Operating cash 81.80 81.59 -Less payables (81.80) (81.59) Total working capital 372.60 334.87

Number of days Receivables/AR 30.49 30.00 Number of days Cash/Opex 45.11 45.00 Number of days Payables 45.11 45.00

IDMS No. 45374

Pg 16 of 31

Weighted average cost of capital (WACC)

53. Section 5.1 of the Methodology prescribes the formula to determine the WACC.

54. The gearing used to calculate the WACC is a function of the RAB as defined by the

Methodology. Capital work in progress (CWIP) has been specifically excluded from

the RAB in accordance with the Regulations. A 30% minimum debt level has been

used as required by the Methodology.

55. NERSA’s calculations have yielded a real WACC of 4.43 % (detailed calculation in

Table 8). Following various written and verbal presentations by the applicant and other

parties and the fact that Financial and Industrial Index (FNDI) data is only available

from 1995, the Energy Regulator did not follow the Methodology but used the Allshare

Index (ALSI) as a basis to calculate the market return (Rm) for this tariff period.

Table 8: WACC calculation

WACC Calculation Applicatio

n NERSA

decision

MRP 5.48% 7.30% Industry beta 0.85 0.52 Adjustment for beta 0.15 Adjusted beta 0.85 0.67 Risk-free 1 (Rf1) – post-tax 3.61% 0.49% Cost of equity (Ke) real 8.27% 5.38% Small company adjustment (25%) 2.07% 0.00%

Cost of equity (Ke) real 10.34% 5.38% Cost of debt (Kd) pre-tax 10.89% 10.89% Cost of debt (Kd) post-tax 7.84% 7.84% Projected CPI 2010/11 5.50% 5.50% Cost of debt (Kd) real pre-tax 5.11% 5.11%

Cost of debt (Kd) real post-tax 2.22% 2.22% Debt ratio 30.00% 30%

Equity ratio 70.00% 70%

WACC 7.90% 4.43%

Corporate Taxation Rate 28.00% 28.00%

IDMS No. 45374

Pg 17 of 31

Cost of equity (Ke)

56. The cost of equity is determined as per paragraph 5.6 of the Methodology which

prescribes that the risk-free rate should be the average of the monthly market-to-

market risk-free rate for the preceding 300 months for all Government bonds with at

least a 10-year maturity as at 12 months before the commencement of the tariff period

under review. This results in a real post-tax risk-free rate of 0.49%.

57. All economic data used is as of a year prior to the tariff period under review, in

accordance with the Methodology.

58. Transnet claims in its application that the Energy Regulator has made an error in the

Methodology regarding the risk-free rate by applying an interest tax shield to the risk-

free rate in the cost of equity.

59. Calculating Ke using risk-free (Rf) pre-tax: Transnet submits that theoretically the

Methodology is incorrect to use a post-tax Rf to calculate the market risk premium

(MRP) and eventually the Ke. The Methodology consistently treats all values on a

post-tax real basis to perform calculations. It is true that the Methodology gives the

difference between pre- and post-tax risk-free quantum back to the applicant in the

calculation of the MRP as MRP is calculated using this “post-tax” risk-free rate to

calculate the premium earned by the equity markets. The “gap” between market return

(Rm) and risk-free (Rf) post-tax is then higher and results in a higher MRP which

probably explains some of the differences pointed out by the applicant in paragraph

5.1.2 of the application. This higher MRP “benefit” is obviously enhanced (if the beta is

greater than 1 or reduced (if the beta is less than 1) by the beta applied to the MRP.

In short, the Methodology gives some of the taxation deduction from the Rf back in a

higher MRP, but this higher MRP is enhanced or reduced by multiplying it with a beta

greater or less than 1.

Inflation

60. The Energy Regulator calculated the average inflation to be 9.18% using 300 months

of data up to March 2009 sourced from Statistics South Africa.

IDMS No. 45374

Pg 18 of 31

Market risk premium (MRP)

61. The applicant determined a market risk premium (MRP) of 5.48% for the period

01 April 1984 to 31 March 2009 based on the difference between the Allshare Index

total real return versus a pre-tax real risk-free rate on which monthly excess MRP

returns were annualised by compounding them and averaging the annualised MRP

over a specified 25-year period.

62. Transnet arrived at a MRP of 7.13% using the NERSA approach using ALSI instead of

the FNDI (as per the Methodology).

63. The Energy Regulator calculated a MRP of 7.30%.

64. The market return (Rm) was calculated by the Energy Regulator using the JSE ALSI

index data, converted from a nominal to a real value for the previous 300 months

(April 1984 to March 2009). This yielded a result of 16.45%. The average month-to-

month CPI over the same period (April 1984 to March 2009) is 9.18%. The CPI data

used is sourced from Statistics South Africa. The average real market risk premium

(MRP) over 300 months is 7.30 %.

65. The Methodology requires the Energy Regulator to use the Financial and Industrial

Index (FNDI). The Energy Regulator deviated from the Methodology in calculating the

Rm value as data for the FNDI is only available for 15 of the 25 years. Furthermore, it

represents a move towards consistency across the three industries (electricity,

petroleum pipelines and piped gas) in determining the Rm value.

Beta (β)

66. The Energy Regulator does not calculate the beta for proxy companies but uses

publicly available data sourced from an independent source, Zacks. The Energy

Regulator has initiated a review of the calculation of the beta in order to enhance the

approach in future.

IDMS No. 45374

Pg 19 of 31

67. The Energy Regulator used the procedure set out in Note 3 of the Methodology to

calculate beta, as at 12 months prior to the commencement of the tariff period under

review.

68. To determine the beta, the following companies were used as proxies:

68.1 El Paso Energy Corporation 68.2 Enbridge Inc 68.3 EQT Corporation 68.4 Magellan Midstream Holdings, Limited Partnership

68.5 Plains all American Pipeline, Limited Partnership 68.6 Provident Energy Trust.

69. These proxy companies are all North American pipeline companies that are in the

petroleum transportation industry.

70. Transnet has included the proxy companies’ short-term and long-term interest-bearing

debt when determining their gearing and in the weighting formula in relation to the size

of the debt.

71. For the purposes of determining the beta, the Energy Regulator applied the minimum

gearing of 30% as specified in the Methodology.

72. The levered (industry) beta is calculated to be 0.52 as at 12 months prior to the

commencement of the tariff review period in accordance with the Methodology.

73. Currently the debt ratio applied to lever the raw beta is a very low 30%. Once the

applicant’s new NMPP project is completed and taken into operation, and with it, its

corresponding debt, the gearing is expected to increase substantially with a

concomitant impact on the beta.

74. To account for South African business conditions, a risk component of 0.15 was

deemed to be appropriate to add to the industry beta yielding a beta of 0.67. (See

Table 9 below.)

IDMS No. 45374

Pg 20 of 31

Table 9: Risk components

Risk Component Value Industry beta - Calculated industry beta – using 6 proxy North American firms as determined by the ER

as prescribed in the Methodology.

0.52

Size of company. - A beta factor adjustment is proposed to accommodate the fact that Transnet Pipelines

excluding CWIP is considered to be relatively small in comparison with the proxy companies.

0.15

TOTAL BETA 0.67

75. Transnet, in its application, added 25% to the Ke before adjustments. The Energy

Regulator added a risk component of 0.15 to the industry beta in accordance with the

Methodology. (See Table 11 for a comparison.)

76. Beta adjustments: as per the NERSA Methodology, the economic and risk factors are

compensated by adjusting the beta. The Transnet application deals with these factors

by adding them to the WACC. Although this may be a different approach to use, the

results are very close. (See Table 10).

77. The resultant real cost of equity is 5.38%.

Table 10: WACC calculation comparison

Application NERSA Decision

NERSA Decision with risk factors

outside beta A C C Risk free over 25 years (Rf) post-tax 3.61% 0.49% 0.49% MRP 5.48% 7.30% 7.30% Industry beta 0.85 0.52 0.52 Adjustment for beta - 0.15 - Adjusted beta 0.85 0.67 0.52 Risk free 1 (Rf1) – post-tax 3.61% 0.49% 0.58% Cost of equity (Ke) real 8.27% 5.38% 4.37% Small company adjustment (25%) 2.07% 0.00% 1.09% Cost of equity (Ke) real 10.34% 5.38% 5.47% Cost of debt (Kd) real post-tax 2.22% 2.22% 2.22% Debt ratio 30.00% 30.00% 30.00% Equity ratio 70.00% 70.00% 70.00% WACC 7.90% 4.43% 4.49%

IDMS No. 45374

Pg 21 of 31

Consumer price index (CPI)

78. The CPI used in calculating the MRP is the average of the month-to-month CPI from

April 1984 to March 2009 (9.18%) using Statistics South Africa data. The CPI used in

calculating the real cost of debt is a forecasted CPI for the next 12 months (5.5%)

obtained from BER.

Cost of debt (Kd)

79. The applicant estimates a weighted average cost of debt (WACD) for the end of

March 2010 to be 10.77% and for the end of March 2011 to be 11.01% yielding an

average of 10.89%, resulting in a post-tax real cost of debt of 2.22% for financial year

2010/11.

Expenses (E)

80. The Energy Regulator has used Transnet’s estimated expenses of R661.8 million. Any

difference between estimated expenses and actual expenses will be subject to a

give-back or claw-back in the next tariff period

Tax (T)

81. Paragraph 7.1 of the Methodology states that each licensee must make a once-off

election between the use of either (a) “flow through” (actual tax) payment, or

(b) “normalised” (notional tax) payment.

82. Transnet elected to use the normalised (notional) tax approach in its tariff application

and arrived at a sum of R192.5 million. Transnet states that using the Methodology the

tax that would apply is R90.1 million.

83. Taxation was calculated using a normalised tax expense for the tariff period under

review.

84. The South African corporate tax rate (Tr) is 28%. Notional taxation is calculated by

using the following formula:

IDMS No. 45374

Pg 22 of 31

Tr*Tr - 1

allowance tax excl NPBT Tax ⎥⎦⎤

⎢⎣⎡=

85. Tax penalties and interest on tax due are not allowed.

86. Calculated in this fashion the notional tax is R109.66 million as per Table 11.

Table 11: Notional tax calculation

NPBT excl tax allowance={(RAB*WACC)+E+D(historic & write up)+F+-C}-{E+D(historic)}

Using Application numbers NERSA decision (R million)

Ke a 225.27 Kd(real) b 39.82 WACC c=a+b 265.09 E d 661.80 D (historic) e 170.20 D (write-up) ee 81.80 F f 0 C [claw back excl tax claw back] g (64.91)

Allowable revenue before tax allowance h=c+d+e+ee+f+g 1,113.98

Tr j 28%

NPBT excl tax allowance={(RAB*WACC)+E+D+F+-C}-{E+D(historic)} [Note interest not deducted to allow tax shield] k=h-d-e

281.98 Allowable revenue pre tax 1,113.98 Tax={(NPBT excl tax allowance)/(1-Tr)}*Tr l={k/(1-j)}*j 109.66 Total Allowable Revenue m=h+l 1,223.63

Depreciation and amortisation of inflation write-up (D)

87. The Methodology states that the depreciation amount calculated on a straight line

basis over the service life of each of the assets or classes of assets in the RAB for the

tariff period under review is included in the Allowable Revenue.

88. Depreciation is to be calculated by using the method given in the example in Note 4 of

the Methodology: Method to Determine Depreciation.

89. The applicant estimated its depreciation expense to be R252 million (historic

depreciation R170.2 million and amortisation of write-up balances of R81.80 million).

IDMS No. 45374

Pg 23 of 31

The Energy Regulator has in the interim accepted the depreciation expense as

provided by the applicant pending finalisation of the SRAB as discussed above.

Approved revenue addition to meet debt obligations (F)

90. Section 9 of the Methodology provides for an addition to the Allowable Revenue to put

an entity in a position to meet its debt obligations. It also states that if the applicant

does not seek such an adjustment, the Energy Regulator will not consider such an

adjustment.

91. Transnet did not apply for any additional revenue or “F factor” for this purpose and the

Energy Regulator has not allocated any additional revenue for this purpose.

92. Notwithstanding the above NERSA performed certain checks and is satisfied that

Transnet Pipelines will have an interest cover ratio, in this tariff period, within the

range published by NERSA (1.5 to 4) taking into account those elements of the NMPP

project included in the RAB.

Claw back adjustment (C)

93. The claw back adjustment was determined using the formula as stated in paragraph

10.1 of the Methodology.

Volume Adjustment (VA)

94. Paragraph 10.2 of the Methodology allows for compensation arising from differences

in projected and actual volumes.

95. Transnet’s volume projection for the 2008/09 tariff period was 17,827 million litres. The

Transnet actual volume for that period was 16,965 million litres. The difference is

862 million litres.

96. The applicant also states that the previous tariff decision was only implemented on

6 August 2009. The total revenue earned by the applicant in the 2008/09 financial year

IDMS No. 45374

Pg 24 of 31

was R1,194.4 million versus the calculated Allowable Revenue of R1,250.39 million.

The total volume adjustment in the claw back is therefore R55.99 million which is a

result of volume differences, late price implementation and differences in the volume

mix. An amount of R27.4 million has already been allowed in the 2009/10 year leaving

a balance of claw back amounting to R28.59 million.

Expenses

97. An in-depth review on Transnet’s expense allocation was conducted for the following

three periods:

- 12 months ending March 2008

- 12 months ending March 2009

- 6 months ending September 2009

98. In the 2008/09 tariff decision the Energy Regulator allowed expenses to the value of

R483.1 million as per the application. The actual expenses for that period amount to

R471.18 million. This difference between expenses claimed and expenses actually

incurred to the value of R11.92 million has therefore been clawed back.

99. Included in the corporate head office cost allocation in the tariff periods 2008/09 to

2010/11 is social investment costs. According to paragraph 6.4.9 of the Methodology,

these are not allowed unless demonstrated to be of benefit to the consumer. These

amounts are therefore also clawed back as the applicant failed to demonstrate such

benefit.

R million 2008/09 2009/10 2010/11 Social investment costs 14.09 13.61 -

F-Factor adjustment (FA)

100. The applicant did not claim any F-factor adjustment.

Debt cost adjustment

IDMS No. 45374

Pg 25 of 31

101. Paragraph 10.5 of the Methodology allows for an adjustment if there is a difference

between the estimated cost of debt in the Allowable Revenue and the actual cost of

debt for that tariff.

102. The formula used to determine the debt cost adjustment is:

Debt cost adjustment = Allowable Revenue recalculated with actual cost of debt - Allowable Revenue projected6

103. In the 2008/09 tariff decision, a debt ratio of 45% was used. In the claw back

calculations for the 2009/10 tariff decision, it was decided that the CWIP should not be

allowed as RAB and subsequently should also not influence the Debt/Equity ratios

used in calculating returns. The effect therefore would be that in 2008/09 the

proportion of return on equity in the WACC would be higher and subsequently the

proportion of the return on debt in WACC would be lower. This is set out in Table 12

below.

Table 12: Net WACC return claw back

NERSA

approved (Rfd)

(R million)

Final Transnet actual as

per 2010/2011

application (R million)

Total actual claw

back for 2008/09

(R million)

Claw back allowed in 2009/2010

(as per 2009/2010

Rfd) (R million)

Total claw back to be allowed in

2010/11 (R million)

Claw back requested by Transnet in

2010/11 application (R million)

Debt cost adjustment 187.70 130.50 (57.20) 19.10 (76.30) (76.30) Equity cost adjustment 201.10 276.40 75.30 3.60 71.70 71.70 Net WACC return claw back 388.80 406.90 18.10 22.70 (4.60) (4.60)

104. The claw back on excess reduction of RAB as a result of deferred taxation for the

2009/10 period is reflected in Table 13.

6 Note: All other factors and quantum in estimated Allowable Revenue remain the same.

IDMS No. 45374

Pg 26 of 31

Table 13: Claw back on excess reduction of RAB by deferred taxation (2009/10)

Claw back on "excess" reduction of deferred taxation in 2009/10 tariff year

As in 2009/10 tariff decision Should be Claw back

R million Deferred taxation balance deducted from RAB 230.15 Should be: Movement 2008 year 9.40 Movement 2009 year 11.70 Pipeline inspection costs post-2008 23.50 Deferred taxation balance deducted from RAB 230.15 44.60 185.55

% Ke 5.43% 10.08 Kd 2.89% 5.36 Total Pre tax claw back 15.44

Depreciation adjustment

105. In the interim the Energy Regulator accepts Transnet’s latest estimate for its

depreciation (R232.50 million) compared with what it estimated in its 2008/09 tariff

application (R251.7 million). The credit difference of R19.2 million together with the

claw back of R6.9 million claimed in the 2009/10 tariff application, totalling

R26.1 million is clawed back. This credit claw back is due mainly to the increased

remaining life of certain assets classes.

106. However, since these values are based on the applicant’s MEAV asset values and not

the correct SRAB values, this amount will have to be reconsidered in future and

possibly adjusted when the SRAB verification exercise is concluded and implemented.

Taxation

107. Transnet claimed an amount of R61.40 million for the actual taxation paid during the

2008/09 tariff period (higher than the value of taxation allowed in the 2008/09 tariff

determination) on the basis that the flow through taxation method was used in

determining the taxation. This amount has been disallowed as the notional taxation

calculation was used in the said tariff determination.

IDMS No. 45374

Pg 27 of 31

Time value of money

108. Transnet received more revenue (R77.60 million) for the 2008/09 and 2009/10 tariff

periods than estimated and should therefore compensate the consumer for the time

value of money. The Energy Regulator’s calculation of the real WACC of 4.43% (see

Table 8) multiplied by the net claw back (R62.16 million) for 1 year is used to calculate

a time value of money of R2.75 million (see Table 14).

109. A taxation claw back is not included in the time value of money calculation as the

taxation would only be paid in the year the revenue is actually earned (2010/11).

IDMS No. 45374

Pg 28 of 31

Claw back summary

110. A summary of the claw back adjustment is presented in Table 14.

Table 14: Summary of the claw back adjustments

R million Application Difference NERSA

Decision Claw back 68.80 (133.71) (64.91)

Volume 28.60 (0.01) 28.59 Cost of debt (76.30) 0.00 (76.30) Cost of equity 71.70 0.00 71.70 Depreciation (26.10) 0.50 (25.60) Operational expenses 2008/09 (11.92) Social investment expenses disallowed for 2008/09 (14.09) Taxation (incl in notional total tax) 61.40 (61.40) - Total claw back 2008/09 59.30 (60.91) (27.62) Social investment expenses disallowed for 2009/10 (13.61) (13.61) Claw back on "over" deduction of deferred taxation in 2009/10 tariff year 15.44 15.44 Total Allowable Revenue on 16-inch NMPP not taken into operation (36.37) (36.37) Subtotal before time value of money 59.30 (95.45) (62.16) Time value of money @WACC (this year’s WACC) 9.50 (12.25) (2.75) Taxation (incl in notional total tax) 0.00

Tariff structure

111. The Energy Regulator commenced setting tariffs in the 2007/08 financial year. The

basis for determining tariffs prior to 2007/08 could not be established.

112. In the 2008/09 tariff decision, the Energy Regulator went some way towards correcting

the imbalances in the inherited historical tariffs, given the information limitations within

which it had to work.

IDMS No. 45374

Pg 29 of 31

113. After the adjustments in 2008/09, intended as a step towards moving from an

unknown historical basis to a known systematic basis, some stakeholders requested

the Energy Regulator not to continue with tariff restructuring until a full consultation

was held. No tariff restructuring was included in the 2009/10 tariff determination.

114. On 31 August 2009, a discussion paper on the 2009/10 Transnet Tariff Structure and

Design (2009) was published by the Energy Regulator. This was followed by a

workshop with stakeholders held on 18 September 2009 on the topic of tariff design.

115. Subsequently NERSA published a Discussion Document on certain matters pertaining

to the application by Transnet Limited for the Setting of its 2010/11 Petroleum Pipeline

Tariffs on 9 February 2010 and written comments thereon were received from

Transnet, Total, Sasol and Petroline.

116. At the NERSA public hearing held on 4 March 2010 Transnet, BPSA, Total, Sasol and

Petroline presented their views on the tariff application and the Discussion Document.

117. Stakeholders have different and opposing views on an appropriate tariff structure for

the industry.

118. In light of the opposing views submitted by various stakeholders and insufficient time

to fully investigate issues raised at the public hearing, the Energy Regulator will

continue its investigations and consultations on tariff structuring during 2010 with the

intention of reaching a well informed position on tariff structuring in time for the next

tariff period.

119. The year to year percentage change in Allowable Revenue will therefore be applied to

the historical tariffs. These tariffs will only be applicable for Transnet’s financial year 1

April 2010 until 31 March 2011.

120. The applicant forecasts a 6.87% increase in the volumes for the 2010/11 tariff period

above the volumes for the 2009/10 tariff period (from 16,774 mega litre in 2009/10 to

17,927 mega litre for 2010/11). When taking the increase in volumes into

consideration in converting the Allowable Revenue increase of 11.86% to a tariff

IDMS No. 45374

Pg 30 of 31

increase, the tariff increase based on a percentage increase over the historic tariffs is

6.09%.

Economic impact

121. The economic impact of the tariff increase in the inland region of South Africa is

expected to be limited. For example, if the Minister of Energy decides to use the

pipeline tariff as a proxy for the cost of transporting fuel from Durban to Johannesburg,

as has been the case in the past, then we expect the consequential petrol price rise to

be 0.7 cents per litre. Such an increase is within the range of monthly petrol price

adjustments Gazetted by the Minister of Energy in recent months. In the month of

January 2010 it was 9 cents per litre decrease, in February 18 cents per litre increase

and in March 2010 6 cents per litre increase.

122. The increase for all tariffs is 6.09% which is below the current inflation rate for January

2010 of 6.2% as published by Statistics South Africa.

123. The tariffs set in this decision are maximum tariffs thus permitting the licensee to

discount.

Other matters

124. In the 2010 budget, the Minister of Finance announced a national fuel levy of 7.5 cents

a litre to contribute to the funding of the New Multi-Product Petroleum Pipeline

(NMPP) between Durban and Gauteng. How this will impact on Transnet Pipelines is

not yet known. No adjustment for the levy has been made during this tariff period

(2010/11).

Conclusion

125. On the conspectus of the facts and evidence, it is appropriate and in compliance with

the requirements of the National Energy Regulator Act, 2004 (Act No. 40 of 2004) to

make the decision set out above. It finds a reasonable balance between the interests

of customers on the one hand and the interests of investors on the other hand.

IDMS No. 45374

Pg 31 of 31

Appendix A: The Allowable Revenue as determined by NERSA is presented in the last column.

Tariff Methodology

Transnet Application NERSA

Decision Allowable Revenue = (RAB x WACC) +E+T+D+F+C Amount (Rm)

or % Amount

(Rm) or %

Regulatory Asset Base (RAB)

Value of assets (V) – accumulated depreciation (d) - Deff taxation

5,708.30 5,644.20

Net Working Capital (W) 372.60 334.87

RAB = V – d + W 6,080.90 5,979.07

WACC Components

Inflation: average over 25 years 9.180%

Inflation: 12 months forecasted 5.50% 5.50%

Rf 3.61% 0.49%

Market return (Rm) Not provided 17.73%

MRP (Market risk premium) 5.48% 7.30%

Proxy industry beta 0.52

Beta adjustment

0.15

Total beta

0.85

0.67

Cost of debt (Kd) 2.22% 2.22%

Cost of equity (Ke) (real) 10.34%

Includes a 25% small company

adjustment

5.38%

WACC 7.90% 4.43%

Expenses 661.80 661.80

Tax 192.50 109.66

Depreciation 252.00 252.00

Claw back adjustment 68.80 (64.91)

Allowable Revenue

1,655.73

1,223.63