transparency 15 -1 © 2006 south-western chapter 15 choice of business entity: other considerations...

TRANSCRIPT

Transparency 15 -1Transparency 15 -1© 2006 South-Western© 2006 South-Western

Chapter 15Chapter 15

Choice of Business Entity:Other Considerations

Choice of Business Entity:Other Considerations

©2006 South-Western College Publishing, Cincinnati, Ohio©2006 South-Western College Publishing, Cincinnati, Ohio©2006 South-Western College Publishing, Cincinnati, Ohio©2006 South-Western College Publishing, Cincinnati, Ohio

Kevin MurphyKevin MurphyMark HigginsMark Higgins

Kevin MurphyKevin MurphyMark HigginsMark Higgins

Transparency 15 -2Transparency 15 -2© 2006 South-Western© 2006 South-Western

IntroductionIntroduction

Employee compensation Pension plans Stock options Fringe benefits

Tax liabilityTax creditsAlternative minimum

taxInternational Considerations

There are two major areas in which tax issues play a major role in deciding the business form of an organization

Transparency 15 -3Transparency 15 -3© 2006 South-Western© 2006 South-Western

Deferred Compensation Plans

Deferred Compensation Plans

General tax consequences are:Employers take a current deduction for the

amounts contributedEmployees may defer recognition of income

Deferred compensation plans are designed to encourage employers to donate toward employees’ retirement funding.

Transparency 15 -4Transparency 15 -4© 2006 South-Western© 2006 South-Western

Employee Pension PlansEmployee Pension Plans

Contributory versus noncontributory Qualified versus nonqualified

Contributions made to nonqualified may not be deferred or deducted

To be qualified, a plan must Cover workers 21 or older Be in writing Be made to a trust Be made exclusively for the benefit of employees Not discriminate in favor of highly paid employees Limit the amount of allowed contributions and/or benefits

Transparency 15 -5Transparency 15 -5© 2006 South-Western© 2006 South-Western

Employee Pension PlansEmployee Pension Plans

Defined contribution versus defined benefitDefined contribution plans (money purchase

plan or profit-sharing plan) have limits on the amount of contributions made limited to the lesser of $42,000 or 25% of taxable

compensation

Defined benefit plans have limits on the amount of retirement benefits paid Cannot exceed the smaller of $170,000 or 100% of

average of the highest 3 years’ compensation

Transparency 15 -6Transparency 15 -6© 2006 South-Western© 2006 South-Western

Other Pension Plans Keogh

Other Pension Plans Keogh

Designed for self-employed taxpayers not covered by an employer’s plan

For self-employed or owner-partnerDefined contribution plans

Employees: lesser of $42,000 or 25% of compensation Owners: lesser of $42,000 or 20% of net SE income up

to $210,000

Defined benefit plans Maximum payment limited to $170,000 or 100% of

average compensation for the highest 3 consecutive years

Transparency 15 -7Transparency 15 -7© 2006 South-Western© 2006 South-Western

Individual Retirement Accounts

Individual Retirement Accounts

Open to all taxpayers Two kinds

Conventional (Traditional)Roth

Total contributions to all IRAs may not exceed $4,000 per person per yearTaxpayers age 50 or older may contribute

up to $4,500

Transparency 15 -8Transparency 15 -8© 2006 South-Western© 2006 South-Western

Traditional IRATraditional IRA

Contributions limited to lesser of $4,000 ($4,500 if age 50 or older) or amount of earned income Married filing joint may contribute up to $8,000

($9,000 if 50 or older) totalFully deductible if not covered by an employer’s

plan If covered, maximum deduction equals:

(Maximum contribution) X [1 - {(AGI - phase-out) / $10,000}]

Transparency 15 -9Transparency 15 -9© 2006 South-Western© 2006 South-Western

Deductible IRAPhase-out Beginnings

Deductible IRAPhase-out Beginnings

Tax Year Married Single

2005 $70,000 $50,000 2006 $75,000 $50,000 2007 $80,000 $50,000

Transparency 15 -10Transparency 15 -10© 2006 South-Western© 2006 South-Western

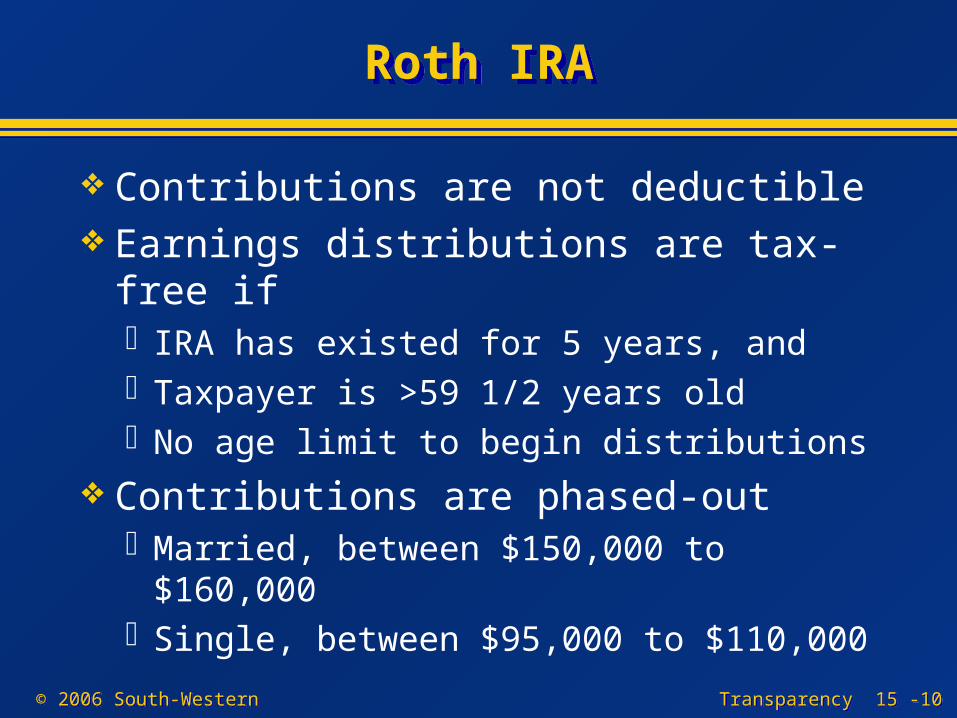

Roth IRARoth IRA

Contributions are not deductible Earnings distributions are tax-free if

IRA has existed for 5 years, andTaxpayer is >59 1/2 years oldNo age limit to begin distributions

Contributions are phased-outMarried, between $150,000 to $160,000Single, between $95,000 to $110,000

Transparency 15 -11Transparency 15 -11© 2006 South-Western© 2006 South-Western

Converting IRAs to Roth IRAsConverting IRAs to Roth IRAs

May convert traditional IRAs to Roth IRAsIf AGI < $100,000

Must pay tax due on amount distributed, but no penalty for early distribution

If AGI > $100,000, must pay 10% penalty

Transparency 15 -12Transparency 15 -12© 2006 South-Western© 2006 South-Western

IRA WithdrawalsIRA Withdrawals

TraditionalMust begin distributions by age 70 1/2Distributions are taxable

Both IRAs - penalty free withdrawals forDeath or disabilityMedicalQualified higher education expensesFirst time home purchases

Transparency 15 -13Transparency 15 -13© 2006 South-Western© 2006 South-Western

Open to any entity Must cover all employees who

Are at least 21 years oldHave worked during the year and for 3 of the last 5

years

Have received at least $450 in compensation Maximum contributions

For owners: lesser of $42,000 or 20% of net SE income up to $210,000

For employees: lesser of $42,000 of 25% of compensation

Other Pension PlansSimplified Employee Pension

(SEP)

Other Pension PlansSimplified Employee Pension

(SEP)

Transparency 15 -14Transparency 15 -14© 2006 South-Western© 2006 South-Western

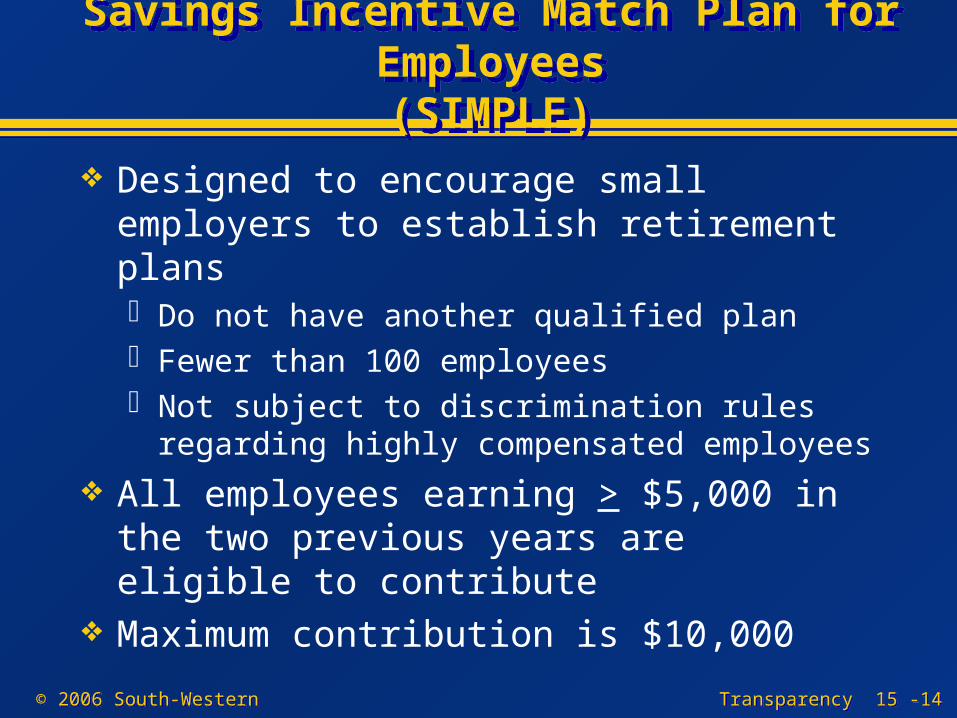

Savings Incentive Match Plan for Employees(SIMPLE)

Savings Incentive Match Plan for Employees(SIMPLE)

Designed to encourage small employers to establish retirement plansDo not have another qualified planFewer than 100 employeesNot subject to discrimination rules regarding highly

compensated employees

All employees earning > $5,000 in the two previous years are eligible to contribute

Maximum contribution is $10,000

Transparency 15 -15Transparency 15 -15© 2006 South-Western© 2006 South-Western

DistributionsDistributions

From a qualified pension plan, Keogh, SEP, IRA, or SIMPLEMay begin the year taxpayer reaches age 59 and

1/2, but must begin the year taxpayer reaches age 70 and 1/2 (except for Roth IRAs)

Must be an annuity May elect lump-sum for Keogh

Required minimum distribution based on taxpayer’s life expectancy

Taxable amount depends on whether taxpayer has basis: capital recovery concept

Transparency 15 -16Transparency 15 -16© 2006 South-Western© 2006 South-Western

PenaltiesPenalties

Three major penalty provisions exist to ensure proper compliance with the rules and requirements of pension plansContributions made in excess of limits are subject

to 10% penalty (6% for IRAs)Early withdrawals are subject to penalty of 10%

May be waived if distribution is due to death, disability, or certain medical, education or home purchase expenses

A 50% penalty is imposed for failure to begin receiving required minimum distribution by age 70 and 1/2 from plans other than Roth IRAs

Transparency 15 -17Transparency 15 -17© 2006 South-Western© 2006 South-Western

Stock OptionsStock Options

All stock options have three important datesGrant date: the date an employee gets the optionExercise date: the date the employee trades the

option for stockSale date: the date the employee sells the stock

A stock option is the right to buy a share of stock at a fixed price within a specified period of time or on a specified date.

Transparency 15 -18Transparency 15 -18© 2006 South-Western© 2006 South-Western

Stock OptionsStock Options

There are two kinds of stock optionsNonqualified stock options

Tax treatment depends on whether the option has a readily ascertainable fair market value

Incentive stock options No tax consequences until the sale date

Transparency 15 -19Transparency 15 -19© 2006 South-Western© 2006 South-Western

Nonqualified Stock Options With Ascertainable FMV

Nonqualified Stock Options With Ascertainable FMV

At the grant dateEmployee has ordinary income = FMV of optionCorporation has deduction = income recognized

At the exercise dateEmployee basis in the stock = exercise amount paid +

income recognizedHolding period begins

At the sale dateEmployee has capital gain = sales price less

basis

Transparency 15 -20Transparency 15 -20© 2006 South-Western© 2006 South-Western

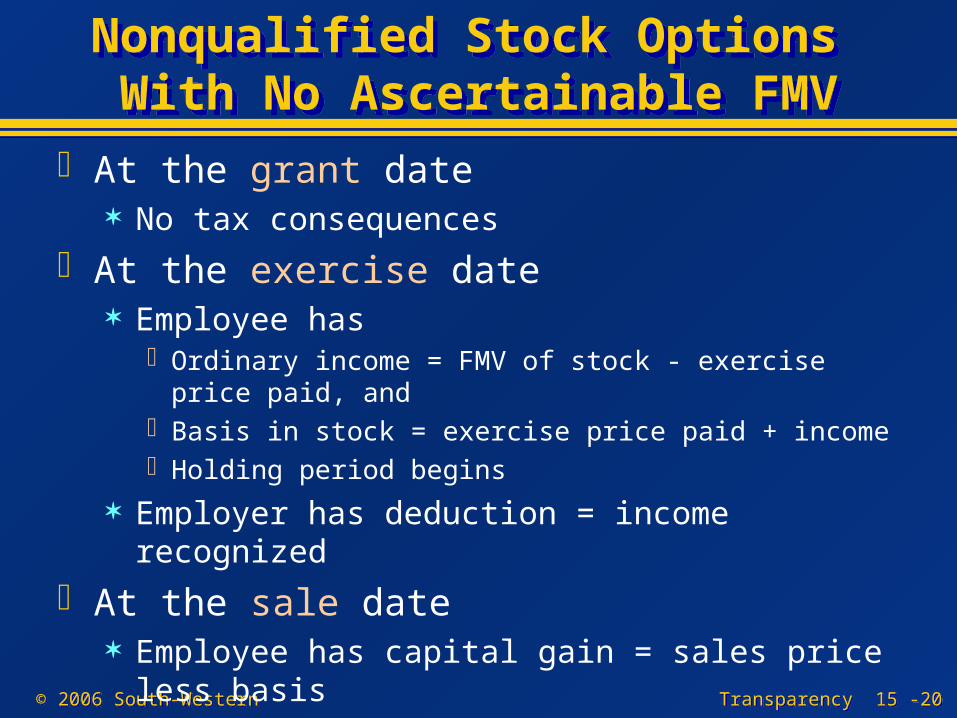

Nonqualified Stock Options With No Ascertainable FMVNonqualified Stock Options With No Ascertainable FMV

At the grant date No tax consequences

At the exercise date Employee has

Ordinary income = FMV of stock - exercise price paid, andBasis in stock = exercise price paid + incomeHolding period begins

Employer has deduction = income recognized

At the sale date Employee has capital gain = sales price less basis

Transparency 15 -21Transparency 15 -21© 2006 South-Western© 2006 South-Western

Nonqualified Stock Options Substantially Restricted

Nonqualified Stock Options Substantially Restricted

At the grant date No consequences

At the exercise date When restrictions lapse, employee has

Ordinary income = FMV - exercise priceBasis in the stock = exercise amount paid + incomeHolding period begins

Employer has deduction = income

At the sale date Employee has capital gain = sales price less basis

Consequences of grant and exercise date may be reversed with Sec. 83(b) election

Transparency 15 -22Transparency 15 -22© 2006 South-Western© 2006 South-Western

Incentive Stock Options (ISO)

Incentive Stock Options (ISO)

Requirements for ISO treatmentMust be part of a qualified stock planOption must be exercised within ten years

of date of grantOption price must be > FMV of the stock at

date of grantOption cannot be transferableFMV of the ISOs granted in a year cannot

exceed $100,000

Transparency 15 -23Transparency 15 -23© 2006 South-Western© 2006 South-Western

Incentive Stock OptionsIncentive Stock Options

Tax consequencesNo consequences on the grant or exercise

datesAt the exercise date

Employee has basis in stock = amount paid

At the sale date Employee has capital gain = sales price less basis

Employer never has deduction

Transparency 15 -24Transparency 15 -24© 2006 South-Western© 2006 South-Western

Reasonableness of Compensation

Reasonableness of Compensation

To be deductible, compensation must beReasonable in amountPaid for actual employee services

Unreasonable compensation of shareholder-employees may be reclassified as dividends

Transparency 15 -25Transparency 15 -25© 2006 South-Western© 2006 South-Western

Income Tax CreditsIncome Tax Credits

A tax credit is a direct reduction in the tax liability of a taxpayer.

Most are nonrefundable They exist to provide specific tax relief Business credits are available to all

entities

Transparency 15 -26Transparency 15 -26© 2006 South-Western© 2006 South-Western

Business Tax CreditsBusiness Tax Credits

Research and Experimental CreditEncourages research in new technologyCredit = 20% of incremental expenditures

less base amount

Rehabilitation Tax CreditIncentive for restoring and saving older

buildingsMust hold buildings for 5 yearsCredit is 10% or 20% of cost depending on

type of building

Transparency 15 -27Transparency 15 -27© 2006 South-Western© 2006 South-Western

Child Care Cost CreditEncourages companies to provide child care for

employeesCredit = 25%(Qualified child care expenses) +

10%(Qualified child care resources) Qualified child care expenses = amounts used to

acquire, construct, or expand property + costs of training care givers

Limited to $150,000 per year

General Business CreditOverall limit on group of business credits

Business Tax CreditsBusiness Tax Credits

Transparency 15 -28Transparency 15 -28© 2006 South-Western© 2006 South-Western

Reporting Tax CreditsReporting Tax Credits

Reduces tax liability dollar for dollar Reported:

at the corporate levelby owners of flow-through entitieson the individual return of a sole-proprietor

Alternative Minimum Tax (AMT)

Alternative Minimum Tax (AMT)

Taxpayer must pay at least the minimum amount of tax

Figured separately from regular income tax Requires keeping a separate set of records Not required for small corporations with

average gross receipts of less than $5,000,000

Transparency 15-29Transparency 15-29

The alternative minimum tax is designed to impose a minimum amount of tax that a

taxpayer must pay.

Transparency 15 -30Transparency 15 -30© 2006 South-Western© 2006 South-Western

Basic AMT ComputationBasic AMT Computation

Regular taxable income+/- Adjustments + Preferences

Tentative alternative minimum taxable income - Allowable exemption amount

Alternative minimum taxable income (AMTI)times Tax rate (20% Corporate; 26% or 28% individual) Tentative minimum tax before credits

Transparency 15 -31Transparency 15 -31© 2006 South-Western© 2006 South-Western

AMT AdjustmentsAMT Adjustments

Purpose is to account for effect of special alternative rates or calculations

Most reverse due to timing differencesExamples:

Required use of completed contract method No gain deferral for installment sales Recalculation of NOL; limited NOL deduction Depreciation under ADS versus MACRS

Not all apply to all entities Corporations must compute Adjusted Current Earnings (ACE) Individuals must limit itemized deductions, delete personal

exemption, report income from ISOs

Transparency 15 -32Transparency 15 -32© 2006 South-Western© 2006 South-Western

AMT PreferencesAMT Preferences

Apply to all taxpayers Always added in the computation of AMTI

Are permanent differences and do not reverse

Add back:Percentage depletion in excess of basisLimitation of intangible drilling costsTax-exempt interest from private activity bondsExcess depreciation over straight-line for property

acquired before 1987 42% of gain exclusion on small business stockReserves for bad debts of financial institutions

AMT ExemptionsAMT Exemptions

Designed to eliminate taxpayers with relatively moderate income and small amounts of adjustments and/or preferences

Phased-out at rate of 25 cents for every dollar of AMTI over base

Entity Initial exemption Base

Corporation $40,000 $150,000

Single & HoH 35,750 112,500

Married, joint 49,000 150,000

Married, separate 24,500 75,000

Transparency 15-33Transparency 15-33

Transparency 15 -34Transparency 15 -34© 2006 South-Western© 2006 South-Western

AMT Minimum Tax CreditAMT Minimum Tax Credit

Calculated each year in which AMT applies

Designed to avoid double jeopardy caused by timing differencesDeducted from regular taxAmount is the difference between actual

AMT and what AMT would be without the reversal adjustments

Transparency 15 -35Transparency 15 -35© 2006 South-Western© 2006 South-Western

International TaxInternational Tax

U.S. citizens, resident aliens, and domestic corporations pay U.S. tax on worldwide income

Non-resident aliens and non-domestic corporations pay U.S. tax only on income earned in the U.S.

Transparency 15 -36Transparency 15 -36© 2006 South-Western© 2006 South-Western

Tax TreatiesTax Treaties

U.S. government makes tax treaties with most foreign governmentsDetermine how citizens and non-citizens

are taxed.Try to prevent double taxation.

Transparency 15 -37Transparency 15 -37© 2006 South-Western© 2006 South-Western

Organizational Structures for Foreign Operations

Organizational Structures for Foreign Operations

Foreign subsidiaryU.S. parent owns > 50%

Parent usually not taxed until income brought into the U.S.

Subpart F income is taxed as earned like conduit entity

interest, dividends, rent, royalties

Transparency 15 -38Transparency 15 -38© 2006 South-Western© 2006 South-Western

Foreign Tax CreditForeign Tax Credit

Taxpayer may take credit for foreign tax paidOr, may elect to exclude up to $80,000 of

foreign earned income

Credit is limited to amount of U.S. tax that would have been paid on foreign incomeExcess may be carried back 1 years,

forward 10

Transparency 15 -39Transparency 15 -39© 2006 South-Western© 2006 South-Western

Other International IssuesOther International Issues

If appreciated property is transferred to foreign entities, must report income = gain “as if sold”.

Transfer pricing methods are used to set the price allowed.

Transparency 15 -40Transparency 15 -40© 2006 South-Western© 2006 South-Western

Taxation of Non-resident Aliens

and Foreign Corporations

Taxation of Non-resident Aliens

and Foreign Corporations Income is U.S. trade or business

income if two tests are met. Asset use test: Income is derived from

assets used in active conduct of business in the U.S.

Business activities test: U.S. business is a material part of income

Non-business income is taxed at a flat 30% rate.

Transparency 15 -41Transparency 15 -41© 2006 South-Western© 2006 South-Western

End of Chapter 15End of Chapter 15