transportation consulting - georgia institute of technologyjjb/classes/6340/talk/chainalytics.pdffor...

TRANSCRIPT

Confidential

Transportation Consulting

April 8 2013

© 2010- 2013 Chainalytics

Confidential 2

Agenda

CHAINalytics Overview

Transportation Benchmarking

Transportation Modes in the Supply Chain

Lane Matching

Transportation Modeling/Planning

Opportunities at Chainalytics

© 2010- 2013 Chainalytics

Confidential 3

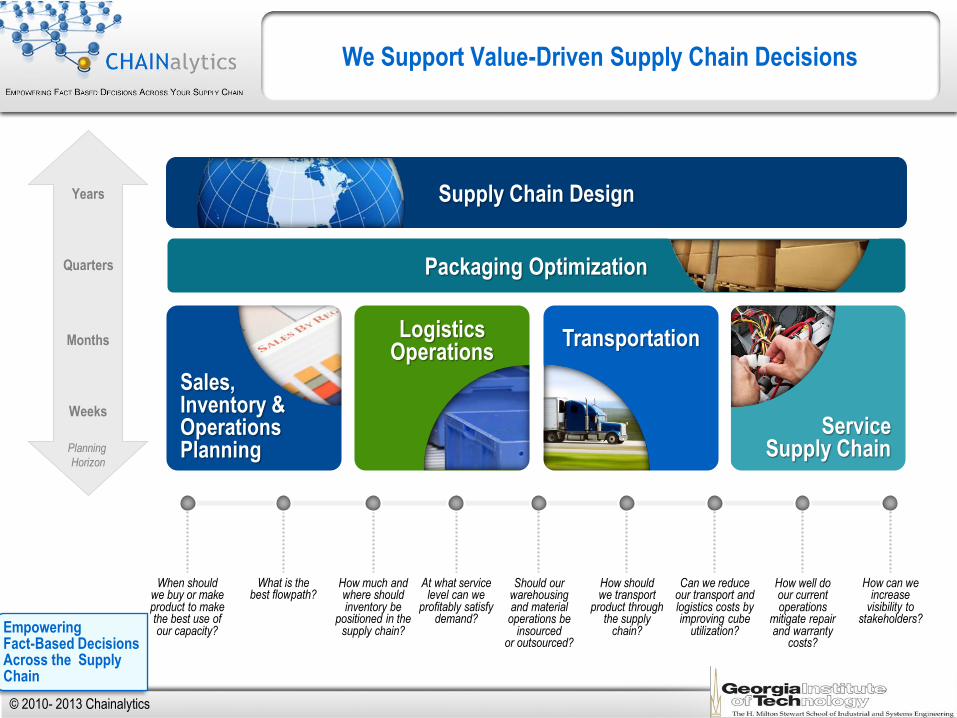

Years

Quarters

Months

Weeks

Planning

Horizon

We Support Value-Driven Supply Chain Decisions

Supply Chain Design

Packaging Optimization

Sales, Inventory & Operations Planning

Transportation Logistics Operations

Service Supply Chain

At what service level can we

profitably satisfy demand?

How should we transport

product through the supply

chain?

How much and where should inventory be

positioned in the supply chain?

Can we reduce our transport and logistics costs by improving cube

utilization?

Should our warehousing and material operations be

insourced or outsourced?

When should we buy or make product to make the best use of our capacity?

What is the best flowpath?

How well do our current operations

mitigate repair and warranty

costs?

How can we increase

visibility to stakeholders?

Empowering Fact-Based Decisions Across the Supply Chain

© 2010- 2013 Chainalytics

Confidential 4

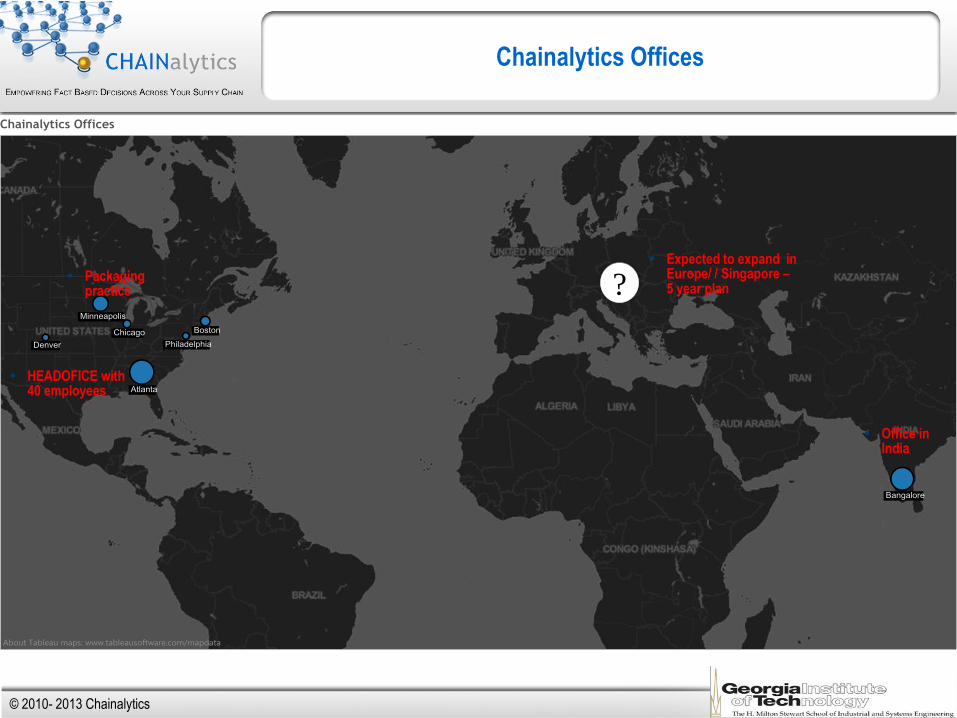

Chainalytics Offices

?

HEADOFICE with 40 employees

Packaging practice

Expected to expand in Europe/ / Singapore – 5 year plan

Office in India

© 2010- 2013 Chainalytics

Confidential 5

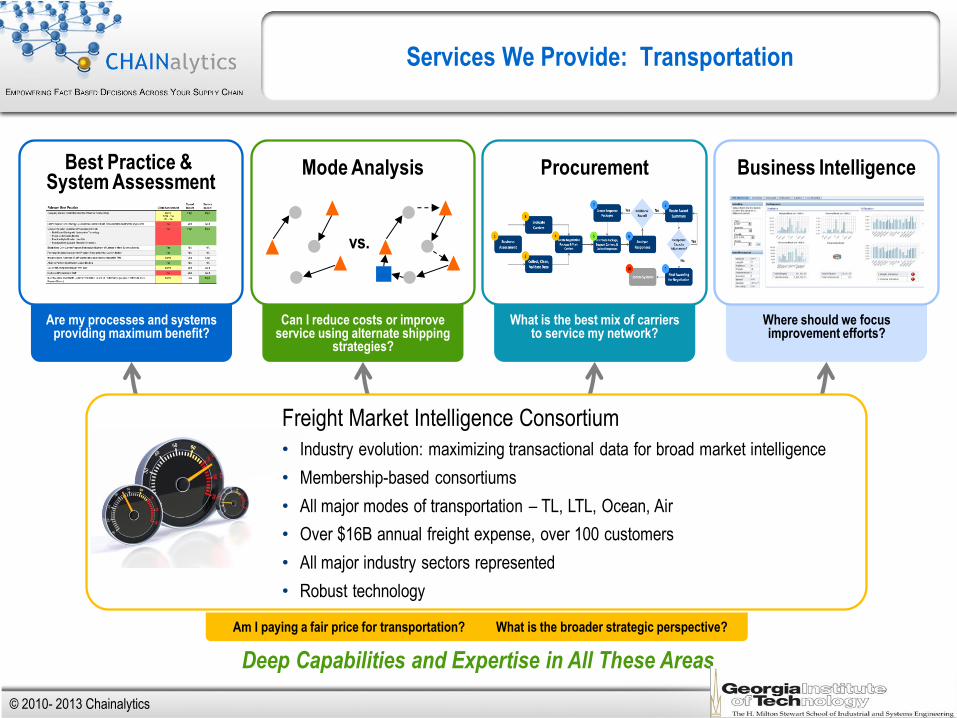

Where should we focus improvement efforts?

What is the best mix of carriers to service my network?

Can I reduce costs or improve service using alternate shipping

strategies?

Are my processes and systems providing maximum benefit?

Services We Provide: Transportation

Procurement Mode Analysis

vs.

Best Practice & System Assessment

Business Intelligence

Deep Capabilities and Expertise in All These Areas

Am I paying a fair price for transportation? What is the broader strategic perspective?

Freight Market Intelligence Consortium

• Industry evolution: maximizing transactional data for broad market intelligence

• Membership-based consortiums

• All major modes of transportation – TL, LTL, Ocean, Air

• Over $16B annual freight expense, over 100 customers

• All major industry sectors represented

• Robust technology

© 2010- 2013 Chainalytics

Confidential 6

Some of Our Clients

FOOD AND

BEVERAGE

RETAIL

HOME/OFFICE

DURABLES

HEALTHCARE

HOME/OFFICE

NON DURABLES

LSP Chemical/Process Auto/Industrial Packaging Utilities/

Telecomm/Media

OTHER

INDUSTRIES

SERVED

• 62 of the Fortune 500

• 9 of the Top 15 US Retailers

• 13 of AMR’s Top 25 Supply Chains

• 5 of the Top 20 Global Forest and Paper Companies

• 8 of the World’s 25 Largest Food & Beverage Mfgs

• 9 of the Top 10 Consumer Goods Supply Chains., SC Digest

© 2010- 2013 Chainalytics

Confidential 7

Agenda

CHAINalytics Overview

Transportation Benchmarking

Transportation Modes in the Supply Chain

Lane Matching

Transportation Modeling/Planning

Opportunities at Chainalytics

© 2010- 2013 Chainalytics

Confidential 8

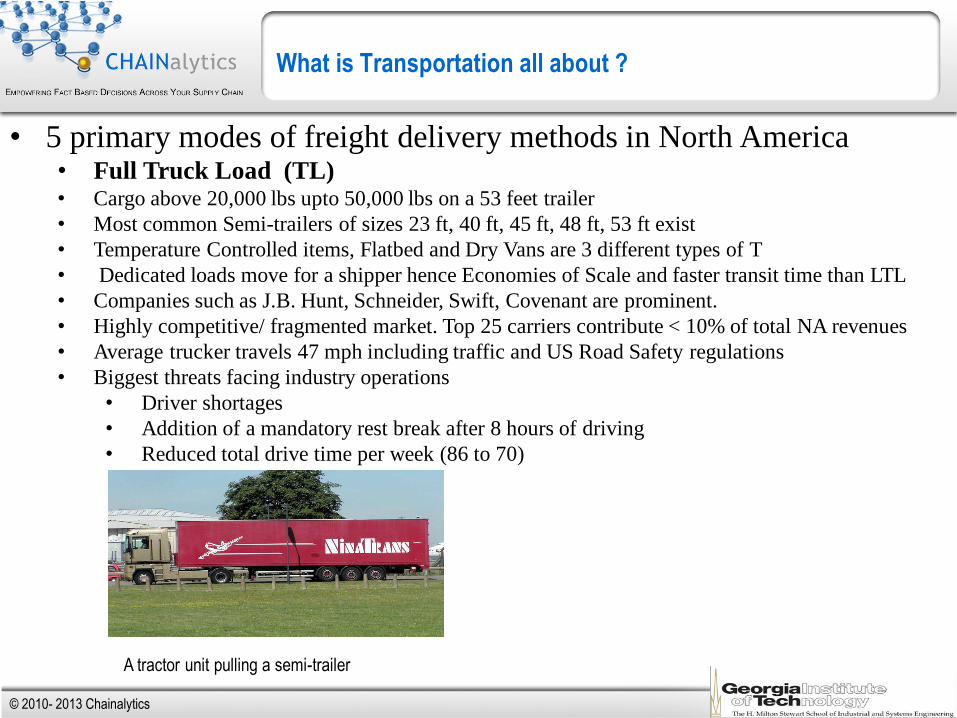

What is Transportation all about ?

A tractor unit pulling a semi-trailer

• 5 primary modes of freight delivery methods in North America • Full Truck Load (TL) • Cargo above 20,000 lbs upto 50,000 lbs on a 53 feet trailer

• Most common Semi-trailers of sizes 23 ft, 40 ft, 45 ft, 48 ft, 53 ft exist

• Temperature Controlled items, Flatbed and Dry Vans are 3 different types of T

• Dedicated loads move for a shipper hence Economies of Scale and faster transit time than LTL

• Companies such as J.B. Hunt, Schneider, Swift, Covenant are prominent.

• Highly competitive/ fragmented market. Top 25 carriers contribute < 10% of total NA revenues

• Average trucker travels 47 mph including traffic and US Road Safety regulations

• Biggest threats facing industry operations

• Driver shortages

• Addition of a mandatory rest break after 8 hours of driving

• Reduced total drive time per week (86 to 70)

© 2010- 2013 Chainalytics

Confidential 9

Less- Than-Truckload

Less- Than-Truckload (LTL) -

Generally moves freight >150 Lbs & < 20,000 lbs

The LTL market is much smaller than TL ($27B vs. ~$320B)

LTL is a much more concentrated market than TL

Top 25 LTL carriers = 88% of total LTL Revenues (top 6 = 50%)

Top 25 TL carriers ≤ 10% of total TL Revenues

While TL is mainly driven by distance, LTL is influenced by many factors that interact with each other, such as:

Freight Class

Weight

Distance

Pricing is based off of different tariffs with a negotiated discount that can apply to all, or portions, of a network

Freight All Kinds (FAK) classification(Class 50 – 500) dominates and can obscure cost drivers

For the most part, lower the freight class (aka NMFC class) lower the freight charge.

Low density and High value shipments have highest freight class.

2000 lbs of ping pong balls vs. 2000 lbs of plasma TV vs. 2000 lbs of standard shrink wrapped 4 x 4 pallet

GUESS ????

© 2010- 2013 Chainalytics

Confidential 10

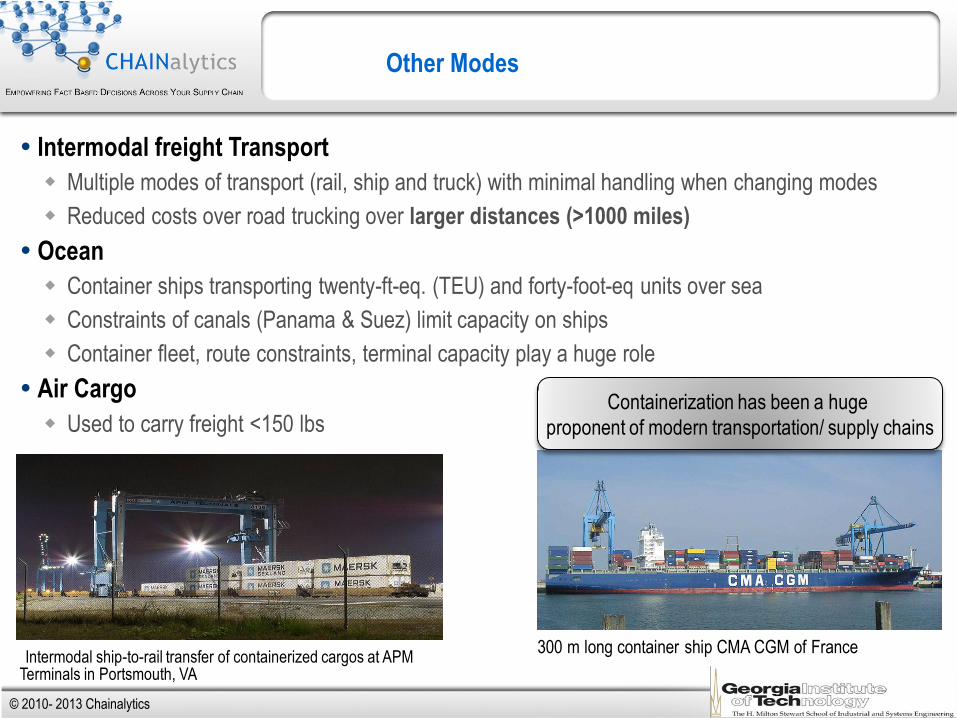

Other Modes

Intermodal freight Transport

Multiple modes of transport (rail, ship and truck) with minimal handling when changing modes

Reduced costs over road trucking over larger distances (>1000 miles)

Ocean

Container ships transporting twenty-ft-eq. (TEU) and forty-foot-eq units over sea

Constraints of canals (Panama & Suez) limit capacity on ships

Container fleet, route constraints, terminal capacity play a huge role

Air Cargo

Used to carry freight <150 lbs

Intermodal ship-to-rail transfer of containerized cargos at APM Terminals in Portsmouth, VA

300 m long container ship CMA CGM of France

Containerization has been a huge

proponent of modern transportation/ supply chains

© 2010- 2013 Chainalytics

Confidential 11

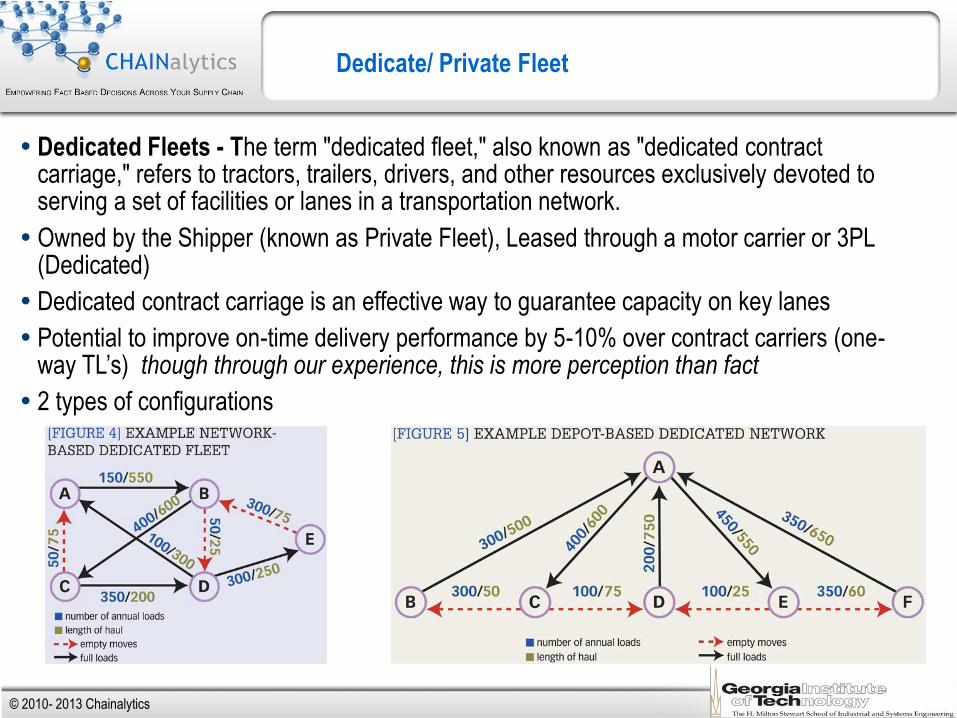

Dedicate/ Private Fleet

Dedicated Fleets - The term "dedicated fleet," also known as "dedicated contract carriage," refers to tractors, trailers, drivers, and other resources exclusively devoted to serving a set of facilities or lanes in a transportation network.

Owned by the Shipper (known as Private Fleet), Leased through a motor carrier or 3PL (Dedicated)

Dedicated contract carriage is an effective way to guarantee capacity on key lanes

Potential to improve on-time delivery performance by 5-10% over contract carriers (one-way TL’s) though through our experience, this is more perception than fact

2 types of configurations

© 2010- 2013 Chainalytics

Confidential 12

Agenda

CHAINalytics Overview

Transportation Benchmarking

Transportation Modes in the Supply Chain

Lane Matching

Transportation Modeling/Planning

Opportunities at Chainalytics

© 2010- 2013 Chainalytics

Confidential 13

Truckload Benchmarking

Chainalytics Created the Freight Market Intelligence Consortium

A collaborative membership based group for confidentially sharing transportation rate information for the

purpose of benchmarking against the market (each other)

FMIC Goals

Build a representative model of the market – 10 % of actual freight spend by over 100 member companies

Isolate and Quantify impact of individual freight characteristics - Origin, destination, distance, loading

conditions, service requirements, regional imbalances…

Use of econometric modeling to predict the cost per load for TL freight, given characteristics of the freight

Data driven validation of FACT vs. Myth. Provide a valuable score-card for review within an organization

Identify need and plan procurement – Change the carriers and choose the best bid on lanes

High accuracy of rates provides input to Supply Chain Network design exercises

© 2010- 2013 Chainalytics

Confidential 14

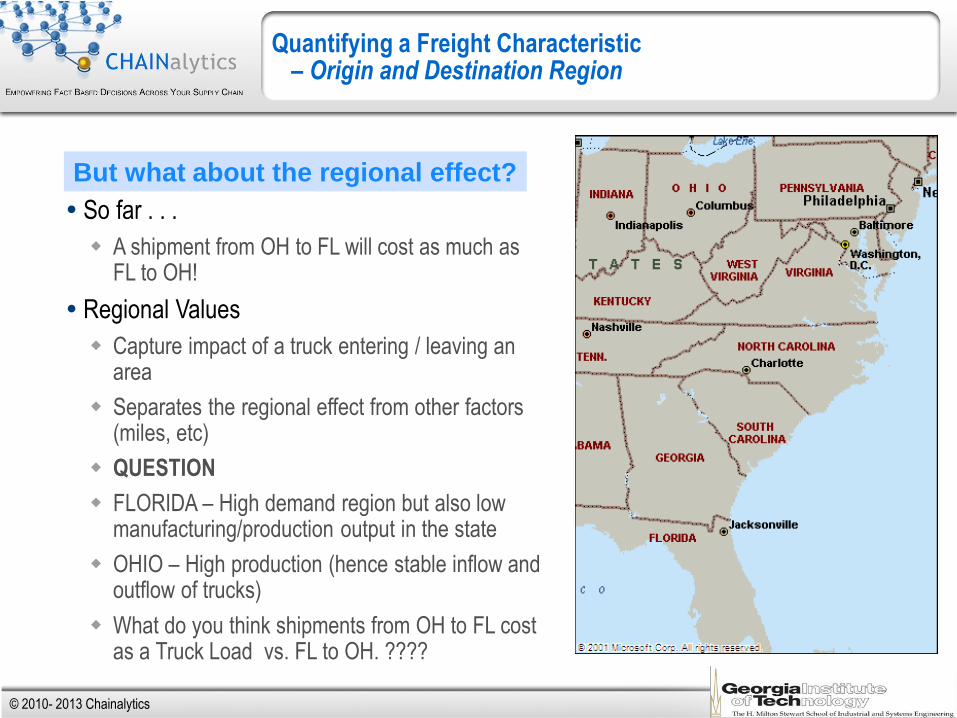

Quantifying a Freight Characteristic – Origin and Destination Region

So far . . .

A shipment from OH to FL will cost as much as FL to OH!

Regional Values

Capture impact of a truck entering / leaving an area

Separates the regional effect from other factors (miles, etc)

QUESTION

FLORIDA – High demand region but also low manufacturing/production output in the state

OHIO – High production (hence stable inflow and outflow of trucks)

What do you think shipments from OH to FL cost as a Truck Load vs. FL to OH. ????

But what about the regional effect?

© 2010- 2013 Chainalytics

Confidential 15

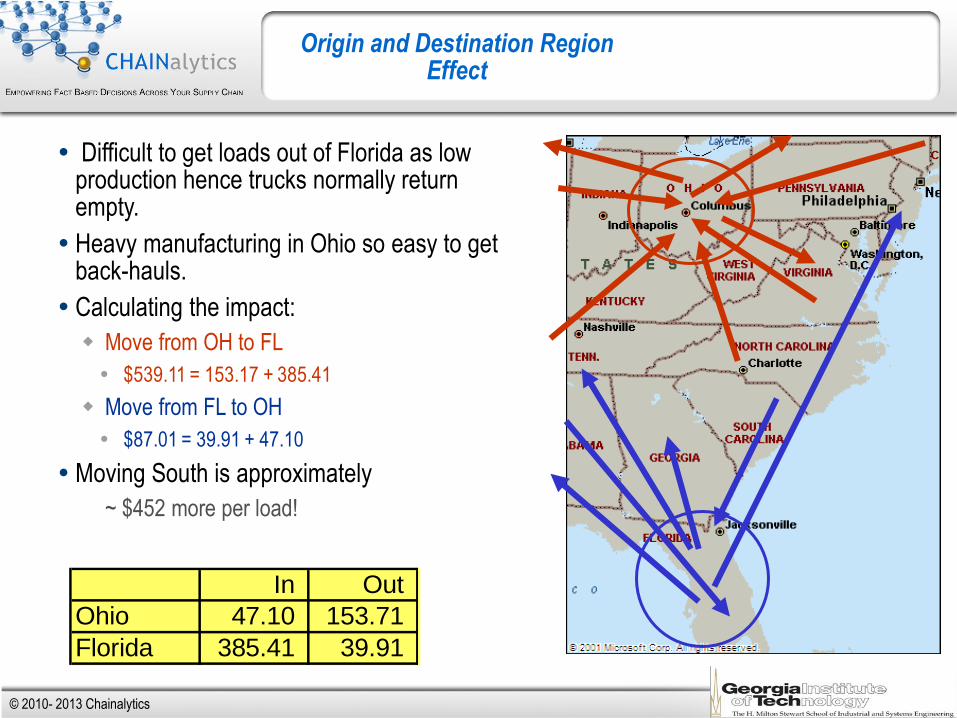

Origin and Destination Region Effect

Difficult to get loads out of Florida as low production hence trucks normally return empty.

Heavy manufacturing in Ohio so easy to get back-hauls.

Calculating the impact:

Move from OH to FL

$539.11 = 153.17 + 385.41

Move from FL to OH

$87.01 = 39.91 + 47.10

Moving South is approximately

~ $452 more per load!

In Out

Ohio 47.10 153.71

Florida 385.41 39.91

© 2010- 2013 Chainalytics

Confidential 16

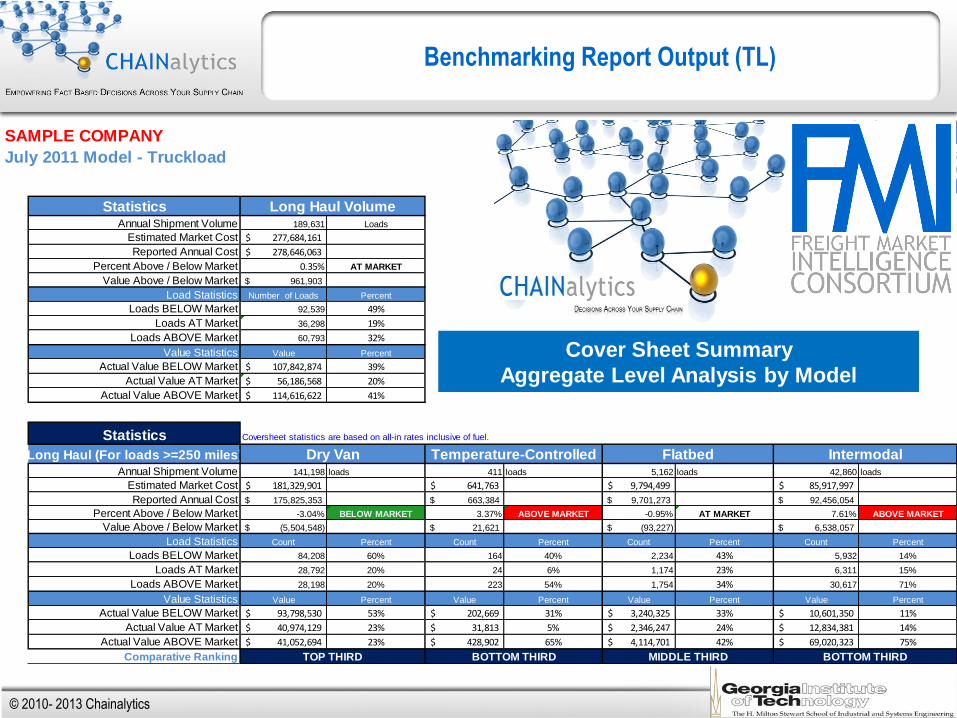

SAMPLE COMPANY

July 2011 Model - Truckload

Model-Based Benchmarking Consortium

StatisticsAnnual Shipment Volume 189,631 Loads

Estimated Market Cost 277,684,161$

Reported Annual Cost 278,646,063$

Percent Above / Below Market 0.35% AT MARKET

Value Above / Below Market 961,903$

Load Statistics Number of Loads Percent

Loads BELOW Market 92,539 49%

Loads AT Market 36,298 19%

Loads ABOVE Market 60,793 32%

Value Statistics Value Percent

Actual Value BELOW Market 107,842,874$ 39%

Actual Value AT Market 56,186,568$ 20%

Actual Value ABOVE Market 114,616,622$ 41%

Statistics Coversheet statistics are based on all-in rates inclusive of fuel.

Long Haul (For loads >=250 miles)

Annual Shipment Volume 141,198 loads 411 loads 5,162 loads 42,860 loads

Estimated Market Cost 181,329,901$ 641,763$ 9,794,499$ 85,917,997$

Reported Annual Cost 175,825,353$ 663,384$ 9,701,273$ 92,456,054$

Percent Above / Below Market -3.04% BELOW MARKET 3.37% ABOVE MARKET -0.95% AT MARKET 7.61% ABOVE MARKET

Value Above / Below Market (5,504,548)$ 21,621$ (93,227)$ 6,538,057$

Load Statistics Count Percent Count Percent Count Percent Count Percent

Loads BELOW Market 84,208 60% 164 40% 2,234 43% 5,932 14%

Loads AT Market 28,792 20% 24 6% 1,174 23% 6,311 15%

Loads ABOVE Market 28,198 20% 223 54% 1,754 34% 30,617 71%

Value Statistics Value Percent Value Percent Value Percent Value Percent

Actual Value BELOW Market 93,798,530$ 53% 202,669$ 31% 3,240,325$ 33% 10,601,350$ 11%

Actual Value AT Market 40,974,129$ 23% 31,813$ 5% 2,346,247$ 24% 12,834,381$ 14%

Actual Value ABOVE Market 41,052,694$ 23% 428,902$ 65% 4,114,701$ 42% 69,020,323$ 75%

Comparative Ranking

Long Haul Volume

Dry Van Temperature-Controlled Flatbed Intermodal

TOP THIRD BOTTOM THIRD MIDDLE THIRD BOTTOM THIRD

Benchmarking Report Output (TL)

Cover Sheet Summary

Aggregate Level Analysis by Model

© 2010- 2013 Chainalytics

Confidential 17

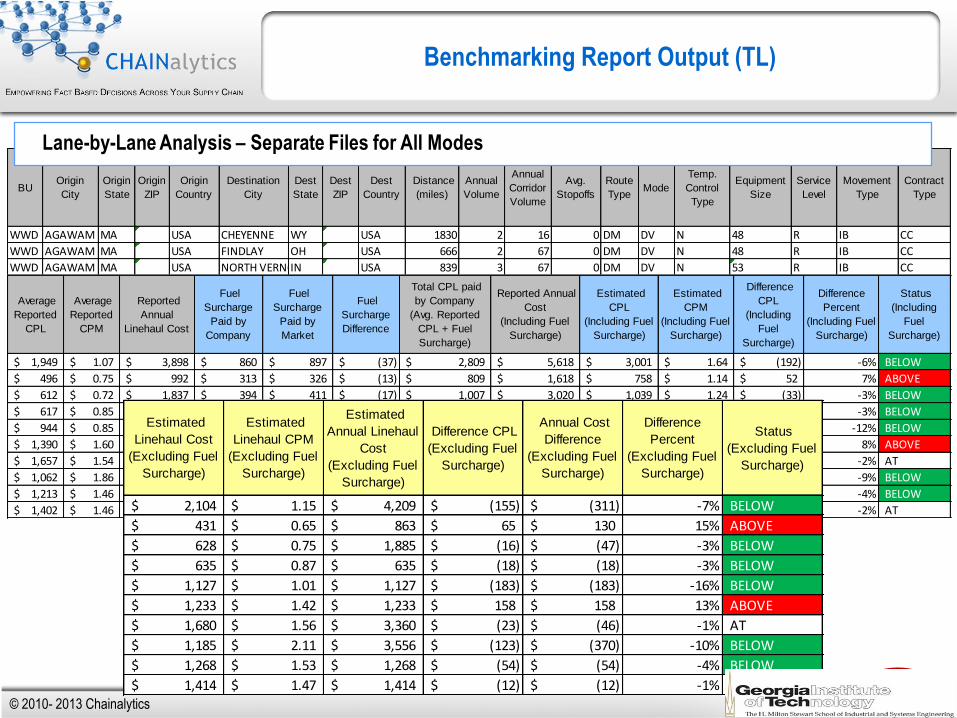

BUOrigin

City

Origin

State

Origin

ZIP

Origin

Country

Destination

City

Dest

State

Dest

ZIP

Dest

Country

Distance

(miles)

Annual

Volume

Annual

Corridor

Volume

Avg.

Stopoffs

Route

TypeMode

Temp.

Control

Type

Equipment

Size

Service

Level

Movement

Type

Contract

Type

WWD AGAWAM MA 01001 USA CHEYENNE WY 82007 USA 1830 2 16 0 DM DV N 48 R IB CC

WWD AGAWAM MA 01001 USA FINDLAY OH 45840 USA 666 2 67 0 DM DV N 48 R IB CC

WWD AGAWAM MA 01001 USA NORTH VERNONIN 47265 USA 839 3 67 0 DM DV N 53 R IB CC

WWD AGAWAM MA 01001 USA STATESVILLE NC 28625 USA 726 1 29 0 DM DV N 53 R IB CC

WWD AGAWAM MA 01001 USA VALDOSTA GA 31601 USA 1111 1 14 0 DM DV N 53 R IB CC

WWD AIRPORT TX 75261 USA CHEYENNE WY 82007 USA 869 1 1729 0 DM DV N 53 R IB CC

WWD ALEXANDRIAIN 46001 USA CHEYENNE WY 82007 USA 1076 2 149 0 DM DV N 53 R IB CC

WWD ALEXANDRIAIN 46001 USA MINERSVILLE PA 17954 USA 563 3 1059 0 DM DV N 53 R IB CC

WWD ALEXANDRIAIN 46001 USA MOUNT VERNONTX 75457 USA 831 1 470 1 MS DV N 53 R IB CC

WWD ALEXANDRIAIN 46001 USA MOUNT VERNONTX 75457 USA 960 1 470 1 MS DV N 53 R IB CC

Lane-by-Lane Analysis – Separate Files for All Modes

Benchmarking Report Output (TL)

Average

Reported

CPL

Average

Reported

CPM

Reported

Annual

Linehaul Cost

Fuel

Surcharge

Paid by

Company

Fuel

Surcharge

Paid by

Market

Fuel

Surcharge

Difference

Total CPL paid

by Company

(Avg. Reported

CPL + Fuel

Surcharge)

Reported Annual

Cost

(Including Fuel

Surcharge)

Estimated

CPL

(Including Fuel

Surcharge)

Estimated

CPM

(Including Fuel

Surcharge)

Difference

CPL

(Including

Fuel

Surcharge)

Difference

Percent

(Including Fuel

Surcharge)

Status

(Including

Fuel

Surcharge)

1,949$ 1.07$ 3,898$ 860$ 897$ (37)$ 2,809$ 5,618$ 3,001$ 1.64$ (192)$ -6% BELOW

496$ 0.75$ 992$ 313$ 326$ (13)$ 809$ 1,618$ 758$ 1.14$ 52$ 7% ABOVE

612$ 0.72$ 1,837$ 394$ 411$ (17)$ 1,007$ 3,020$ 1,039$ 1.24$ (33)$ -3% BELOW

617$ 0.85$ 617$ 341$ 356$ (15)$ 958$ 958$ 991$ 1.36$ (32)$ -3% BELOW

944$ 0.85$ 944$ 522$ 544$ (22)$ 1,467$ 1,467$ 1,672$ 1.50$ (205)$ -12% BELOW

1,390$ 1.60$ 1,390$ 408$ 426$ (17)$ 1,799$ 1,799$ 1,658$ 1.91$ 140$ 8% ABOVE

1,657$ 1.54$ 3,314$ 506$ 527$ (22)$ 2,163$ 4,326$ 2,207$ 2.05$ (44)$ -2% AT

1,062$ 1.86$ 3,187$ 265$ 276$ (11)$ 1,327$ 3,980$ 1,461$ 2.60$ (135)$ -9% BELOW

1,213$ 1.46$ 1,213$ 391$ 407$ (17)$ 1,604$ 1,604$ 1,675$ 2.02$ (71)$ -4% BELOW

1,402$ 1.46$ 1,402$ 451$ 470$ (19)$ 1,853$ 1,853$ 1,884$ 1.96$ (31)$ -2% AT

Estimated

Linehaul Cost

(Excluding Fuel

Surcharge)

Estimated

Linehaul CPM

(Excluding Fuel

Surcharge)

Estimated

Annual Linehaul

Cost

(Excluding Fuel

Surcharge)

Difference CPL

(Excluding Fuel

Surcharge)

Annual Cost

Difference

(Excluding Fuel

Surcharge)

Difference

Percent

(Excluding Fuel

Surcharge)

Status

(Excluding Fuel

Surcharge)

2,104$ 1.15$ 4,209$ (155)$ (311)$ -7% BELOW

431$ 0.65$ 863$ 65$ 130$ 15% ABOVE

628$ 0.75$ 1,885$ (16)$ (47)$ -3% BELOW

635$ 0.87$ 635$ (18)$ (18)$ -3% BELOW

1,127$ 1.01$ 1,127$ (183)$ (183)$ -16% BELOW

1,233$ 1.42$ 1,233$ 158$ 158$ 13% ABOVE

1,680$ 1.56$ 3,360$ (23)$ (46)$ -1% AT

1,185$ 2.11$ 3,556$ (123)$ (370)$ -10% BELOW

1,268$ 1.53$ 1,268$ (54)$ (54)$ -4% BELOW

1,414$ 1.47$ 1,414$ (12)$ (12)$ -1% AT

© 2010- 2013 Chainalytics

Confidential 18

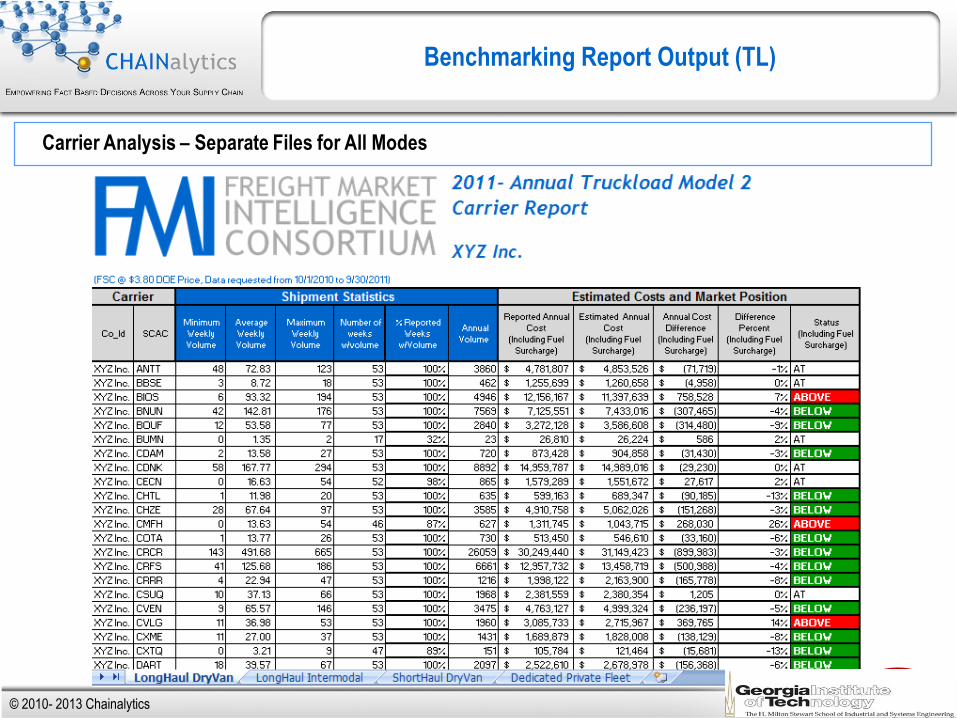

Benchmarking Report Output (TL)

Carrier Analysis – Separate Files for All Modes

© 2010- 2013 Chainalytics

Confidential 19

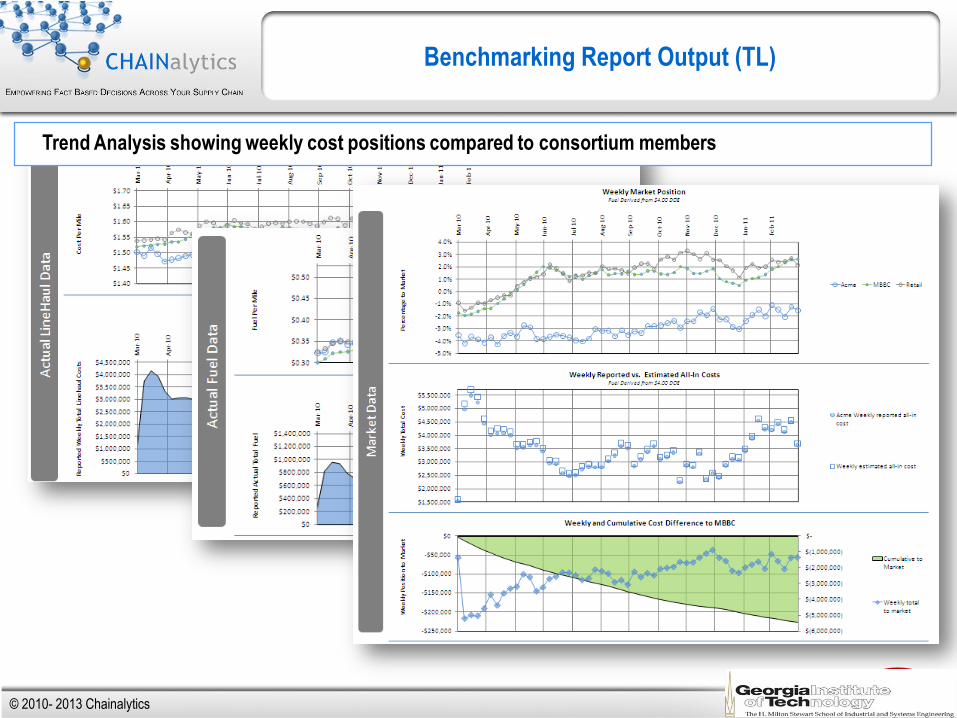

Benchmarking Report Output (TL)

Trend Analysis showing weekly cost positions compared to consortium members

© 2010- 2013 Chainalytics

Confidential 20

Agenda

CHAINalytics Overview

Transportation Benchmarking

Transportation Modes in the Supply Chain

Transportation Modeling/Planning

Lane Matching

Opportunities at Chainalytics

© 2010- 2013 Chainalytics

Confidential 21

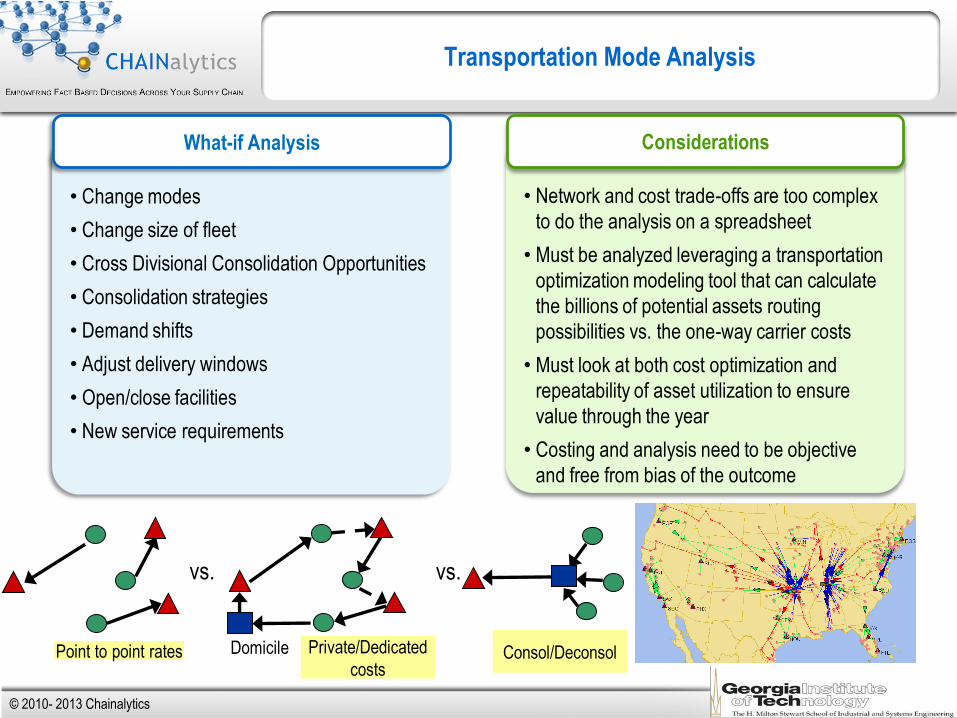

Transportation Mode Analysis

Private/Dedicated

costs

Domicile

vs.

Point to point rates

vs.

Consol/Deconsol

• Change modes

• Change size of fleet

• Cross Divisional Consolidation Opportunities

• Consolidation strategies

• Demand shifts

• Adjust delivery windows

• Open/close facilities

• New service requirements

What-if Analysis

• Network and cost trade-offs are too complex

to do the analysis on a spreadsheet

• Must be analyzed leveraging a transportation

optimization modeling tool that can calculate

the billions of potential assets routing

possibilities vs. the one-way carrier costs

• Must look at both cost optimization and

repeatability of asset utilization to ensure

value through the year

• Costing and analysis need to be objective

and free from bias of the outcome

Considerations

© 2010- 2013 Chainalytics

Confidential

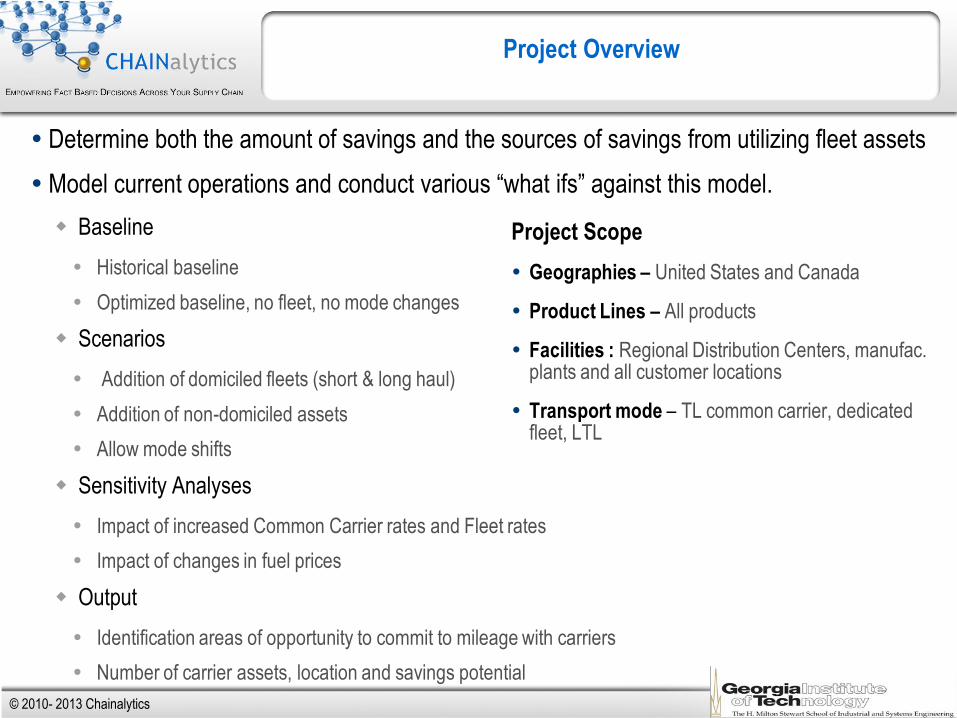

Determine both the amount of savings and the sources of savings from utilizing fleet assets

Model current operations and conduct various “what ifs” against this model.

Baseline

Historical baseline

Optimized baseline, no fleet, no mode changes

Scenarios

Addition of domiciled fleets (short & long haul)

Addition of non-domiciled assets

Allow mode shifts

Sensitivity Analyses

Impact of increased Common Carrier rates and Fleet rates

Impact of changes in fuel prices

Output

Identification areas of opportunity to commit to mileage with carriers

Number of carrier assets, location and savings potential

Project Overview

Project Scope

Geographies – United States and Canada

Product Lines – All products

Facilities : Regional Distribution Centers, manufac. plants and all customer locations

Transport mode – TL common carrier, dedicated fleet, LTL

© 2010- 2013 Chainalytics

Confidential 23

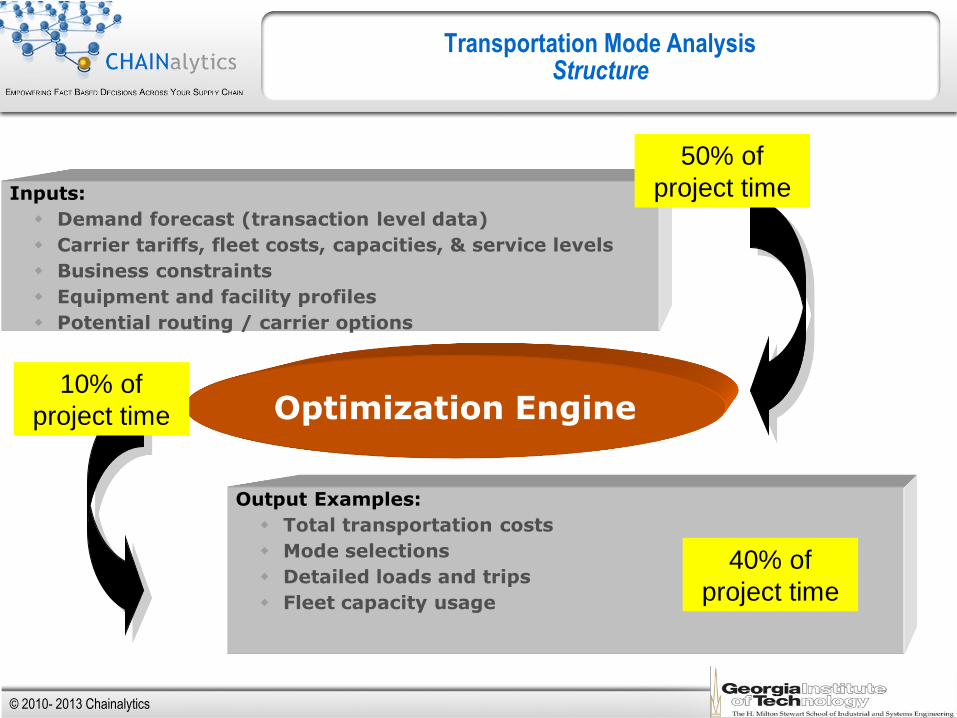

Transportation Mode Analysis Structure

Inputs:

Demand forecast (transaction level data)

Carrier tariffs, fleet costs, capacities, & service levels

Business constraints

Equipment and facility profiles

Potential routing / carrier options

Output Examples:

Total transportation costs

Mode selections

Detailed loads and trips

Fleet capacity usage

Optimization Engine

50% of

project time

10% of

project time

40% of

project time

© 2010- 2013 Chainalytics

Confidential

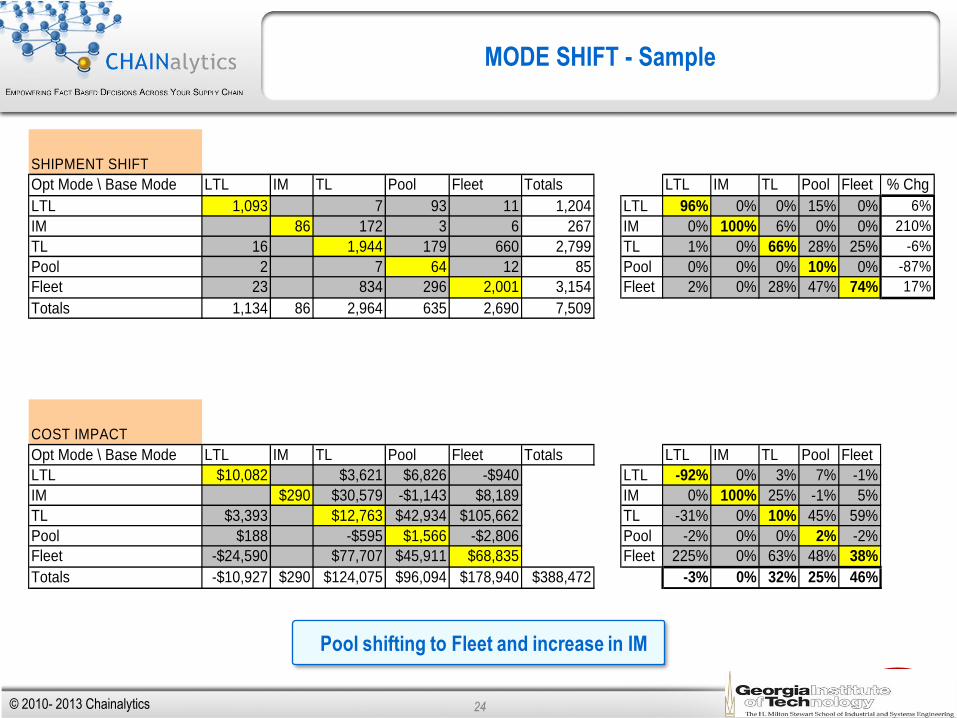

MODE SHIFT - Sample

SHIPMENT SHIFT

Opt Mode \ Base Mode LTL IM TL Pool Fleet Totals LTL IM TL Pool Fleet % Chg

LTL 1,093 7 93 11 1,204 LTL 96% 0% 0% 15% 0% 6%

IM 86 172 3 6 267 IM 0% 100% 6% 0% 0% 210%

TL 16 1,944 179 660 2,799 TL 1% 0% 66% 28% 25% -6%

Pool 2 7 64 12 85 Pool 0% 0% 0% 10% 0% -87%

Fleet 23 834 296 2,001 3,154 Fleet 2% 0% 28% 47% 74% 17%

Totals 1,134 86 2,964 635 2,690 7,509

COST IMPACT

Opt Mode \ Base Mode LTL IM TL Pool Fleet Totals LTL IM TL Pool Fleet

LTL $10,082 $3,621 $6,826 -$940 LTL -92% 0% 3% 7% -1%

IM $290 $30,579 -$1,143 $8,189 IM 0% 100% 25% -1% 5%

TL $3,393 $12,763 $42,934 $105,662 TL -31% 0% 10% 45% 59%

Pool $188 -$595 $1,566 -$2,806 Pool -2% 0% 0% 2% -2%

Fleet -$24,590 $77,707 $45,911 $68,835 Fleet 225% 0% 63% 48% 38%

Totals -$10,927 $290 $124,075 $96,094 $178,940 $388,472 -3% 0% 32% 25% 46%

24

Pool shifting to Fleet and increase in IM

© 2010- 2013 Chainalytics

Confidential 25

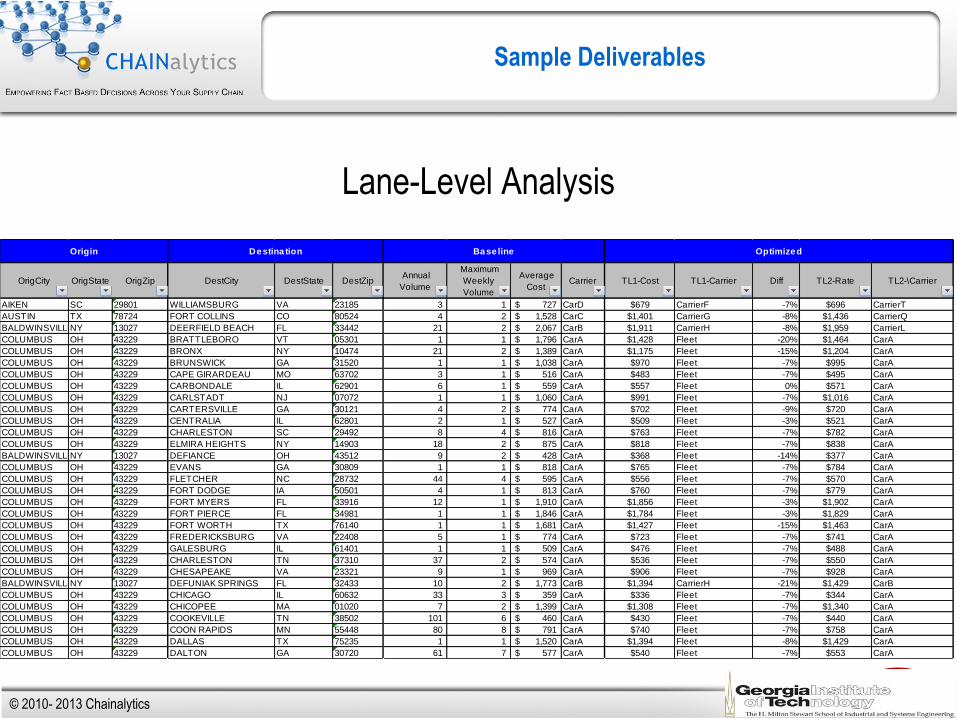

Sample Deliverables

Lane-Level Analysis

OrigCity OrigState OrigZip DestCity DestState DestZip Annual

Volume

Maximum

Weekly

Volume

Average

Cost Carrier TL1-Cost TL1-Carrier Diff TL2-Rate TL2-\Carrier

AIKEN SC 29801 WILLIAMSBURG VA 23185 3 1 727$ CarD $679 CarrierF -7% $696 CarrierT

AUSTIN TX 78724 FORT COLLINS CO 80524 4 2 1,528$ CarC $1,401 CarrierG -8% $1,436 CarrierQ

BALDWINSVILLENY 13027 DEERFIELD BEACH FL 33442 21 2 2,067$ CarB $1,911 CarrierH -8% $1,959 CarrierL

COLUMBUS OH 43229 BRATTLEBORO VT 05301 1 1 1,796$ CarA $1,428 Fleet -20% $1,464 CarA

COLUMBUS OH 43229 BRONX NY 10474 21 2 1,389$ CarA $1,175 Fleet -15% $1,204 CarA

COLUMBUS OH 43229 BRUNSWICK GA 31520 1 1 1,038$ CarA $970 Fleet -7% $995 CarA

COLUMBUS OH 43229 CAPE GIRARDEAU MO 63702 3 1 516$ CarA $483 Fleet -7% $495 CarA

COLUMBUS OH 43229 CARBONDALE IL 62901 6 1 559$ CarA $557 Fleet 0% $571 CarA

COLUMBUS OH 43229 CARLSTADT NJ 07072 1 1 1,060$ CarA $991 Fleet -7% $1,016 CarA

COLUMBUS OH 43229 CARTERSVILLE GA 30121 4 2 774$ CarA $702 Fleet -9% $720 CarA

COLUMBUS OH 43229 CENTRALIA IL 62801 2 1 527$ CarA $509 Fleet -3% $521 CarA

COLUMBUS OH 43229 CHARLESTON SC 29492 8 4 816$ CarA $763 Fleet -7% $782 CarA

COLUMBUS OH 43229 ELMIRA HEIGHTS NY 14903 18 2 875$ CarA $818 Fleet -7% $838 CarA

BALDWINSVILLENY 13027 DEFIANCE OH 43512 9 2 428$ CarA $368 Fleet -14% $377 CarA

COLUMBUS OH 43229 EVANS GA 30809 1 1 818$ CarA $765 Fleet -7% $784 CarA

COLUMBUS OH 43229 FLETCHER NC 28732 44 4 595$ CarA $556 Fleet -7% $570 CarA

COLUMBUS OH 43229 FORT DODGE IA 50501 4 1 813$ CarA $760 Fleet -7% $779 CarA

COLUMBUS OH 43229 FORT MYERS FL 33916 12 1 1,910$ CarA $1,856 Fleet -3% $1,902 CarA

COLUMBUS OH 43229 FORT PIERCE FL 34981 1 1 1,846$ CarA $1,784 Fleet -3% $1,829 CarA

COLUMBUS OH 43229 FORT WORTH TX 76140 1 1 1,681$ CarA $1,427 Fleet -15% $1,463 CarA

COLUMBUS OH 43229 FREDERICKSBURG VA 22408 5 1 774$ CarA $723 Fleet -7% $741 CarA

COLUMBUS OH 43229 GALESBURG IL 61401 1 1 509$ CarA $476 Fleet -7% $488 CarA

COLUMBUS OH 43229 CHARLESTON TN 37310 37 2 574$ CarA $536 Fleet -7% $550 CarA

COLUMBUS OH 43229 CHESAPEAKE VA 23321 9 1 969$ CarA $906 Fleet -7% $928 CarA

BALDWINSVILLENY 13027 DEFUNIAK SPRINGS FL 32433 10 2 1,773$ CarB $1,394 CarrierH -21% $1,429 CarB

COLUMBUS OH 43229 CHICAGO IL 60632 33 3 359$ CarA $336 Fleet -7% $344 CarA

COLUMBUS OH 43229 CHICOPEE MA 01020 7 2 1,399$ CarA $1,308 Fleet -7% $1,340 CarA

COLUMBUS OH 43229 COOKEVILLE TN 38502 101 6 460$ CarA $430 Fleet -7% $440 CarA

COLUMBUS OH 43229 COON RAPIDS MN 55448 80 8 791$ CarA $740 Fleet -7% $758 CarA

COLUMBUS OH 43229 DALLAS TX 75235 1 1 1,520$ CarA $1,394 Fleet -8% $1,429 CarA

COLUMBUS OH 43229 DALTON GA 30720 61 7 577$ CarA $540 Fleet -7% $553 CarA

Origin Destina tion Base line Optimized

© 2010- 2013 Chainalytics

Confidential 26

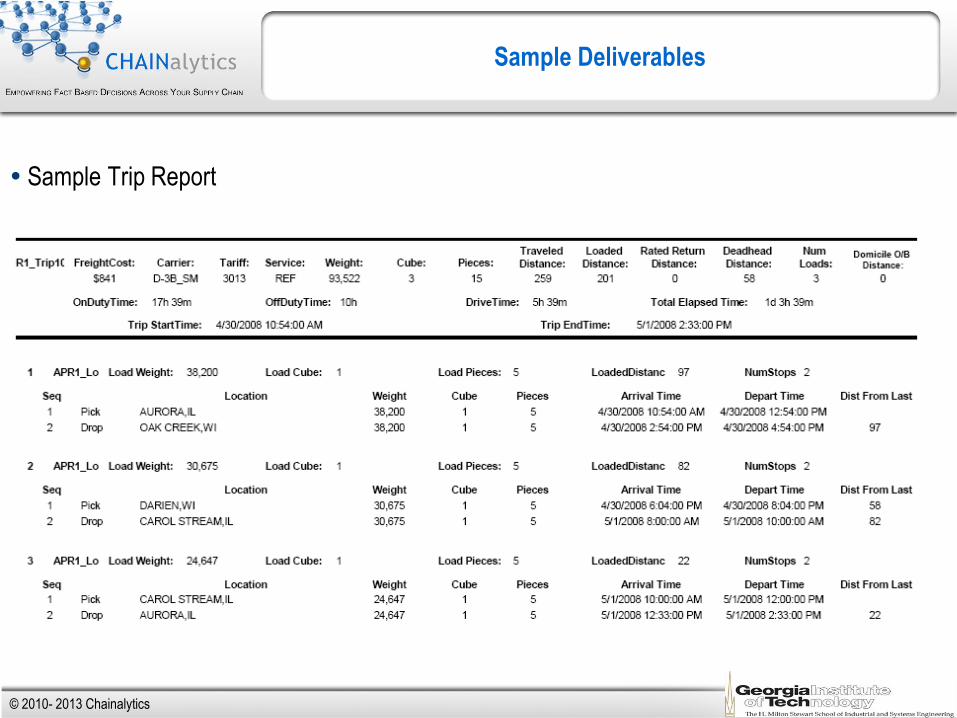

Sample Deliverables

Sample Trip Report

© 2010- 2013 Chainalytics

Confidential

Getting accurate historical shipment level data; location codes dates, costs, weights

Getting accurate shipment origin/destination location data

Building accurate potential transportation rates

This is where Chainalytics’ MBBC is very valuable

Implementation capabilities

Transportation Management System Capabilities

Truckload procurement capabilities

Project Key Success Factors and Risks

© 2010- 2013 Chainalytics

Confidential 28

Agenda

CHAINalytics Overview

Transportation Benchmarking

Transportation Modes in the Supply Chain

Lane Matching

Transportation Modeling/Planning

Opportunities at Chainalytics

© 2010- 2013 Chainalytics

Confidential 29

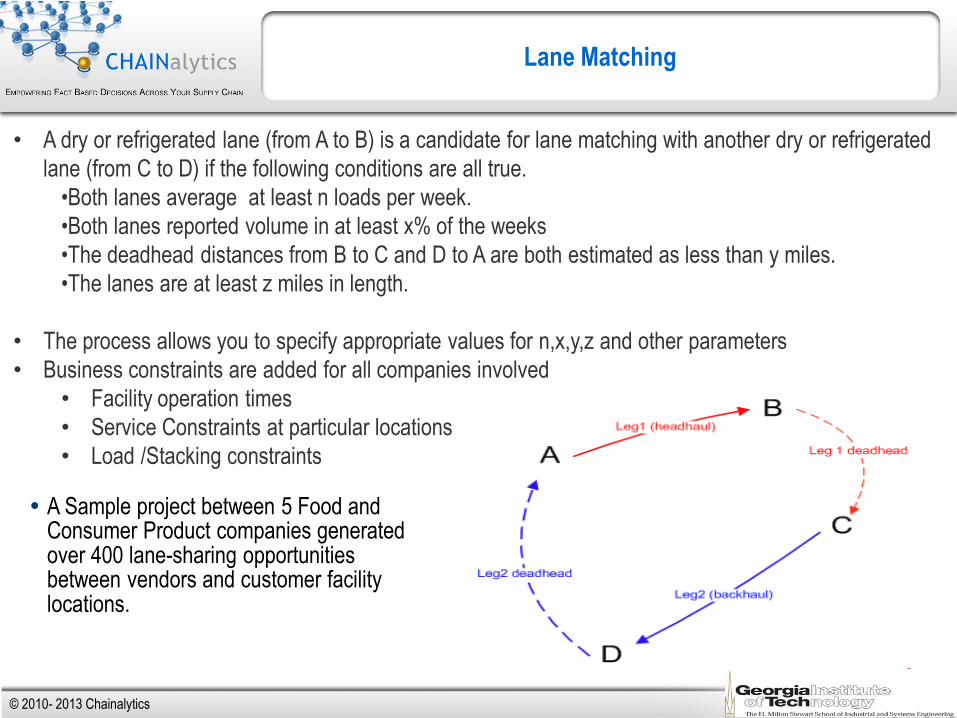

Lane Matching

• A dry or refrigerated lane (from A to B) is a candidate for lane matching with another dry or refrigerated

lane (from C to D) if the following conditions are all true.

•Both lanes average at least n loads per week.

•Both lanes reported volume in at least x% of the weeks

•The deadhead distances from B to C and D to A are both estimated as less than y miles.

•The lanes are at least z miles in length.

• The process allows you to specify appropriate values for n,x,y,z and other parameters

• Business constraints are added for all companies involved

• Facility operation times

• Service Constraints at particular locations

• Load /Stacking constraints

A Sample project between 5 Food and Consumer Product companies generated over 400 lane-sharing opportunities between vendors and customer facility locations.

© 2010- 2013 Chainalytics

Confidential 30

Agenda

CHAINalytics Overview

Transportation Benchmarking

Transportation Modes in the Supply Chain

Lane Matching

Transportation Modeling/Planning

Opportunities at Chainalytics

© 2010- 2013 Chainalytics

Confidential 31

Opportunities at Chainalytics

Active Positions looking to be filled in

Transportation Intern in the Summer/Fall semester 2013

Transportation Consultant – Junior or Senior based on level of experience.

Work in the US for 1-2 years before moving to India

Supply Chain and Network Design Consultants based on need

Other floating positions based on growth over next 6-12 months

Supply Chain Operations group seeking consultant candidates. (Involves travel)

Warehouse, distribution logistics, reverse logistics and client operation strategy

In addition to having great communication skills and analytical skills, a big plus would be to have good software skills with Access/SQL

Candidates can send their resume and a brief cover explaining which position would suit them and why, to Nishant Jain (me) [email protected] and to Mr. Tim Clement (HR head) [email protected]

© 2010- 2013 Chainalytics

Confidential 32

Thank You

© 2010- 2013 Chainalytics