trc q2 2016 earnings slides final

TRANSCRIPT

www.trcsolutions.com

Q2 Fiscal 2016 Investor Review

February 4, 2016Chris Vincze Tom BennetChairman & CEO Chief Financial Officer

T R R

Safe Harbor Statement

2

Certain statements in this presentation may be forward-looking statements within the meaning of Section 27A of the Securities Act of

1933 and Section 21E of the Securities Exchange Act of 1934. You can identify these statements by forward-looking words such as

"may," "expects," "plans," "anticipates," "believes," "estimates," or other words of similar import. You should consider statements that

contain these words carefully because they discuss TRC’s future expectations, contain projections of the Company’s future results of

operations or of its financial condition, or state other "forward-looking" information. TRC believes that it is important to communicate

its future expectations to its investors. However, there may be events in the future that the Company is not able to accurately predict

or control and that may cause its actual results to differ materially from the expectations described in its forward-looking statements.

Investors are cautioned that all forward-looking statements involve risks and uncertainties, and actual results may differ materially

from those discussed as a result of various factors, including, but not limited to, the uncertainty of TRC’s operational and growth

strategies; circumstances which could create large cash outflows, such as contract losses, litigation, uncollectible receivables and

income tax assessments; regulatory uncertainty; the availability of funding for government projects; the level of demand for TRC’s

services; product acceptance; industry-wide competitive factors; the ability to continue to attract and retain highly skilled and qualified

personnel; the availability and adequacy of insurance; and general political or economic conditions. Furthermore, market trends are

subject to changes which could adversely affect future results. See the risk factors and additional discussion in TRC’s Annual Report on

Form 10-K for the fiscal year ended June 30, 2015, Quarterly Reports on Form 10-Q, and other factors detailed from time to time in the

Company’s other filings with the Securities and Exchange Commission.

These slides are intended as a visual aid to TRC’s commentary on the Second Quarter Fiscal Year 2016 Financial Results Conference

Call. As such they should be considered in the full context of that commentary, the transcript of that conference call and TRC’s second

quarter Form 10-Q and Financial Results Press Release. Also, this presentation contains references to non-GAAP metrics such as

EBITDA, gross margin and free cash flow. A reconciliation of GAAP to non-GAAP metrics can be found on slides 22-27.

Q2 Fiscal 2016 Overview

3

NSR1 increased 12% YOY to $111.4MEnergy +11%, Environmental -2%, Infrastructure +26%Growth: 49.5% Organic, 50.5% from Acquisitions

Adjusted Operating income2 grew 16% YOY to $7.9M

Organic NSR backlog increased 23% YOY to $313MEnergy +4%, Environmental -1%, Infrastructure +133%

(1) TRC believes net service revenue (gross revenue less subcontractor costs and other direct reimbursable charges) best reflects the value of services provided to its customers and is the most meaningful indicator of its revenue performance.

(2) Excludes $1.2 million of acquisition and integration expenses during the second quarter of fiscal 2016.

Adjusted EBITDA2 grew 13% YOY to $10.7M

Adjusted Net income2 increased 18% YOY to $4.7M

Envi

ronm

enta

l Seg

men

t

4

$52.6 $51.4

Q2 2015 Q2 2016

Net Service Revenue (in millions)

$10.2 $9.5

Q2 2015 Q2 2016

Segment Profit (in millions)

-2% -6%

Q2 Fiscal 2016 Results

NSR -2% YOY

Segment profit -6% YOY, but overall margins remain strong

Segment NSR backlog -1% YOY

Midstream activity and major capital projects constrained in near term

Real estate, construction and remediation markets remain solid

Ener

gy S

egm

ent

5

$35.8 $39.8

Q2 2015 Q2 2016

Net Service Revenue (in millions)

$8.1

$9.5

Q2 2015 Q2 2016

Segment Profit (in millions)

+17%+11%

Q2 Fiscal 2016 Results

NSR +11% YOY

Segment profit +17% YOY

NSR backlog +4% YOY

Growing interest in energy efficiency programs and projects

Increased utility investment in electric transmission and distribution infrastructure

Infr

astr

uctu

re S

egm

ent

6

$10.9

$13.7

Q2 2015 Q2 2016

Net Service Revenue (in millions)

$1.3

$2.6

Q2 2015 Q2 2016

Segment Profit (in millions)

+26%

+96%

Q2 Fiscal 2016 Results

NSR +26% YOY

Segment profit +96% YOY

NSR backlog +133% YOY

Successful growth plans and initiatives with geographic expansion and P3 projects

Increased transportation investments throughout the country

$43$91 $100

$85

$98 $88

$126

$130 $125

Q2 2015 Q1 2016 Q2 2016

Organic Segment NSR Backlog

$313

NSR Backlog & New Project Wins

7

(in millions)

$254

$319

Energy• Applied Energy Group (NJ) – $21 million to

manage NJ Clean Energy Program• Sempra (San Diego) – $20 million for design

and modeling of fire risk mitigation program

Environmental• 100MW Wind Turbine Project (NY) – $1.1

million• PG&E – Environmental MSA -- $20 million

Infrastructure• Louisiana DOT – $1.3 million for statewide

PPP strategic advisory services• City of San Francisco – $3.4 million for

rehabilitation of historic Third Street Bridge

Pipeline Services• Pipeline Project (Gulf Coast) – $5.7 million• Multiple Compression Station Feed Study –

$0.5 million

Recent Project Awards

8

Willbros Integration – Operations Update

All Pipeline Services active projects are able to bill time and report financials on TRC’s Deltek enterprise system

Pipeline Services migrated onto TRC’s IT networks and operating platforms

Pipeline Services employees integrated into payroll and benefits plan

Billing now conducted on TRC systems

Pipeline Services now incorporated into TRC’s weekly and monthly internal reporting, including company-wide management meetings

Identified and pursuing cost synergies

Management retention and incentive programs in place

Pipeline Services has been functionally integrated within two months of closing

9

Willbros Integration – Market Update

Oil and gas market constraining new capital projects

Midstream segment less impacted than Upstream / Downstream markets

Full TRC rebranding of Pipeline Services offices and marketing now complete

Launched integrated client strategy pursuits with TRC verticals and operations

Multiple opportunities with integrated services in pursuit and awarded

Identifying key market players in support of our organic profitable growth strategy

On track to be accretive to net income in FY 2017

10

Growth Strategy

0%

4%

8%

12%

16%

20%

24%

Q3 2015 Q4 2015 Q1 2016 Q2 2016

Total

Organic

Total & Organic NSR Growth Recent Acquisitions

Willbros Professional Services (November 2015)

X-Line (April 2015)

Investing in our vertical business development / marketing strategy

Increase volume of program management and EPC projects

Pursuing strategic acquisitions to expand our platform in key North American markets

Key Initiatives

11

Invest in organic growth opportunities

Increase focus on strategic markets:

Oil & Gas – Changing market plus enhanced regulatory attention resulting in increased investment in existing assets

Utility/Power – Continued investment to modernize gas & electric systems, including energy efficiency programs; regulatory drivers for significant renewable generation investment

Transportation – $305 billion five-year surface transportation reauthorization package supports capital expansion and P3 projects

Pursue strategic acquisitions that provide geographic expansion and enhanced technical capabilities

Capture scale-based synergies and continue to emphasize cost efficiency

$9.5 $9.5

Q2 2015 Q2 2016

EBITDA (in millions)

Quarterly Financial Results Overview

12

$6.9 $6.7

Q2 2015 Q2 2016

Operating Income (in millions)

-2%

$99.8 $111.4

Q2 2015 Q2 2016

Net Service Revenue (in millions)

+12% 0%

$9.5 $10.7

Q2 2015 Q2 2016

Adjusted EBITDA* (in millions)

*Excludes $1.2 million of acquisition and integration expense during the second quarter of fiscal 2016.

+13%

$6.9 $7.9

Q2 2015 Q2 2016

Adjusted Operating Income* (in millions)

16%

$4.0 $4.7

Q2 2015 Q2 2016

Adjusted Net Income* (in millions)

Quarterly Financial Results Overview

13

$0.13 $0.13

Q2 2015 Q2 2016

Diluted EPS

0%

$4.0 $3.9

Q2 2015 Q2 2016

Net Income (in millions)

-2% +18%

*Excludes $1.2 million of acquisition and integration expense during the second quarter of fiscal 2016.

$0.13 $0.15

Q2 2015 Q2 2016

Adjusted Diluted EPS*

+15%

Q2 2015

$99.8

$82.6

17.3%

$8.4

8.4%

--

$6.9

$6.9

$9.5

9.5%

$9.5

9.5%

$4.0

$4.0

$0.13

$0.13

Q2 2016

$111.4

$93.7

15.9%

$8.0

7.2%

$1.2

$6.7

7.9

$9.5

8.5%

$10.7

9.6%

$3.9

$4.7

$0.13

$0.15

14

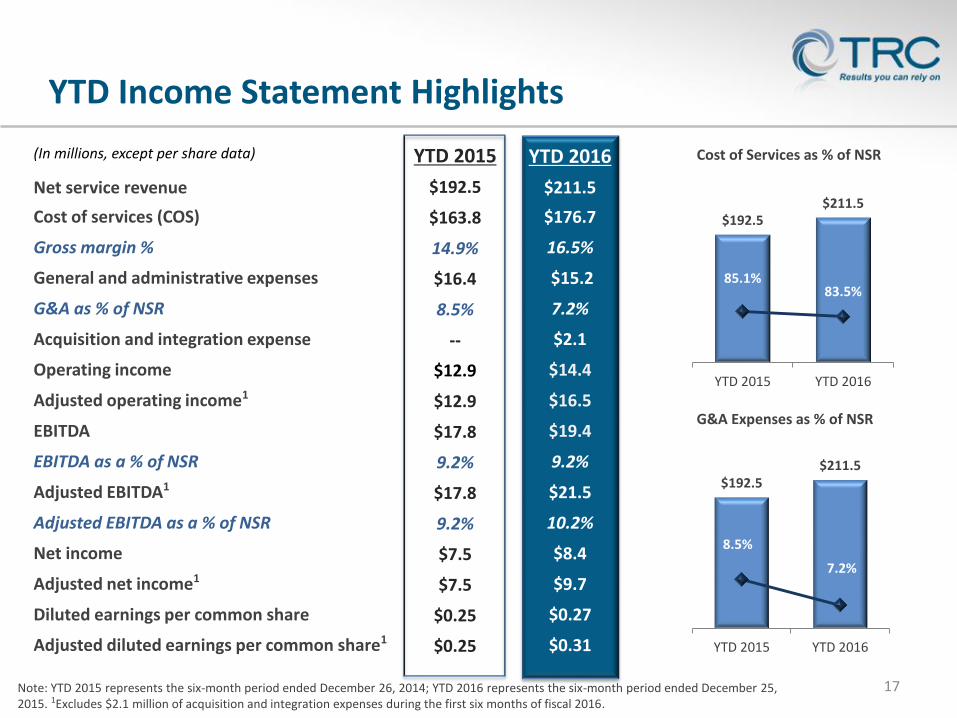

(In millions, except per share data)

Quarterly Income Statement Highlights

$99.8

$111.4

82.7% 84.1%

Q2 2015 Q2 2016

Cost of Services as % of NSR

$99.8

$111.4

8.4%

7.2%

Q2 2015 Q2 2016

G&A Expenses as % of NSR

Net service revenue

Cost of services (COS)

Gross margin %

General and administrative expenses

G&A as % of NSR

Acquisition and integration expenses

Operating income

Adjusted operating income1

EBITDA

EBITDA as a % of NSR

Adjusted EBITDA1

Adjusted EBITDA as a % of NSR

Net income

Adjusted net income1

Diluted earnings per common share

Adjusted diluted earnings per common share1

(1) Excludes $1.2 million of acquisition and integration expenses during the second quarter of fiscal 2016.

$192.5 $211.5

YTD 2015 YTD 2016

Net Service Revenue (in millions)

YTD Financial Results Overview

15

$17.8 $19.4

YTD 2015 YTD 2016

EBITDA (in millions)

$12.9 $14.4

YTD 2015 YTD 2016

Operating Income (in millions)

+10%

+12%

+9%

Note: YTD 2015 represents the six-month period ended December 26, 2014; YTD 2016 represents the six-month period ended December 25, 2015.*Excludes $2.1 million of acquisition and integration expenses during the first six months of fiscal 2016.

$17.8

$21.5

YTD 2015 YTD 2016

Adjusted EBITDA* (in millions)

+21%

$12.9

$16.5

YTD 2015 YTD 2016

Adjusted Operating Income* (in millions)

+28%

$0.25 $0.27

YTD 2015 YTD 2016

Diluted EPS

YTD Financial Results Overview

16

+8%

$0.25

$0.31

YTD 2015 YTD 2016

Adjusted Diluted EPS*

+24%

Note: YTD 2015 represents the six-month period ended December 26, 2014; YTD 2016 represents the six-month period ended December 25, 2015.*Excludes $2.1 million of acquisition and integration expenses during the first six months of fiscal 2016.

$7.5

$9.7

YTD 2015 YTD 2016

Adjusted Net Income* (in millions)

$7.5 $8.4

YTD 2015 YTD 2016

Net Income (in millions)

+12% +30%

YTD 2015

$192.5

$163.8

14.9%

$16.4

8.5%

--

$12.9

$12.9

$17.8

9.2%

$17.8

9.2%

$7.5

$7.5

$0.25

$0.25

YTD 2015

$192.5

$5.5

$163.8

14.9%

$16.4

$12.9

$17.8

9.2%

$7.5

$0.25

17

(In millions, except per share data)

YTD Income Statement Highlights

$192.5 $211.5

85.1%83.5%

YTD 2015 YTD 2016

Cost of Services as % of NSR

$192.5 $211.5

8.5%

7.2%

YTD 2015 YTD 2016

G&A Expenses as % of NSR

Note: YTD 2015 represents the six-month period ended December 26, 2014; YTD 2016 represents the six-month period ended December 25, 2015. 1Excludes $2.1 million of acquisition and integration expenses during the first six months of fiscal 2016.

Net service revenue

Cost of services (COS)

Gross margin %

General and administrative expenses

G&A as % of NSR

Acquisition and integration expense

Operating income

Adjusted operating income1

EBITDA

EBITDA as a % of NSR

Adjusted EBITDA1

Adjusted EBITDA as a % of NSR

Net income

Adjusted net income1

Diluted earnings per common share

Adjusted diluted earnings per common share1

YTD 2016

$211.5

$176.7

16.5%

$15.2

7.2%

$2.1

$14.4

$16.5

$19.4

9.2%

$21.5

10.2%

$8.4

$9.7

$0.27

$0.31

18

TRC Historical and WPS Reclassified Results(12 months ended June 30, 2015)

Reclassified

WPS

$154.4

--

$120.0

$33.5

21.7%

$0.8

$(0.0)

TRC

$408.0

$6.6

$337.3

$37.0

9.1%

$9.3

$30.7

(In millions, except per share data)

Net service revenue

Exit strategy and other income

Cost of services (COS)

General and administrative expenses

G&A as a % of NSR

Depreciation and amortization

Operating income (loss)

Note: Reclassified WPS represents the unaudited historical operating income results for Willbros Professional Services, including reclassification of certain operating costs to subcontract and direct reimbursable charges but prior to pro-forma adjustments as depicted in exhibit 99.3 of the 8K/A filed on February 2, 2016

WPS G&A includes cost allocations from the parent that will not be incurred by TRC

19

(In millions)

Acquisition Closing Cash Outflow Reconciliation

Estimated purchase price $130.0 Sources of cash at closing

Less: Initial working capital adjustment, net of cash acquired (2.5) Balance sheet cash $22.5

Purchase price $127.5

Less: Holdback amount (7.5) Credit facility:

Purchase price outflow at closing $120.0 Term loan 75.0

Employee benefits advance payment 1.5 Revolving credit line 27.0

Financing related fees 3.0

Total cash outflow at closing $124.5 Total sources of cash $124.5

20

(In millions)

Financing and Leverage Update

Borrowing Source $ Capacity Uses on Acquisition Closing Date $ Drawn

Revolving Credit Line $ 100 Acquisition Funding $ 27

Term loan (amortizing) 75 Acquisition Funding 75

Total Credit Facility Capacity

$ 175 Total Credit Facility Usage for Financial Closing (11/30/2015)

$ 102

Borrowing rates: 1-6 mo. LIBOR + 200bps; current borrowing rate of 2.4%

Operating cash flow used to reduce revolver balance during Q2 by $18 million

Outstanding credit facility balance as of end of Q2 on 12/25/2015: of $84 million (excluding letters of credit)

21

Balance Sheet Highlights

Cash and cash equivalents

Days sales outstanding (DSO)

Cash Flow Highlights

Cash flow from operations

Capital expenditures

Free cash flow

Q2 2015

$(1.3)

$(2.5)

$(3.8)

Q2 2016

$(1.0)

$(2.0)

$(3.0)

(In millions)

Balance Sheet and Cash Flow Highlights

YTD 2015

$13.3

85 days

$1.2

$(4.0)

$(2.8)

YTD 2016

$9.5

78 days

$13.4

$(4.0)

$9.4

Note: YTD 2015 represents the six-month period ended December 26, 2014; YTD 2016 represents the six-month period ended December 25, 2015.

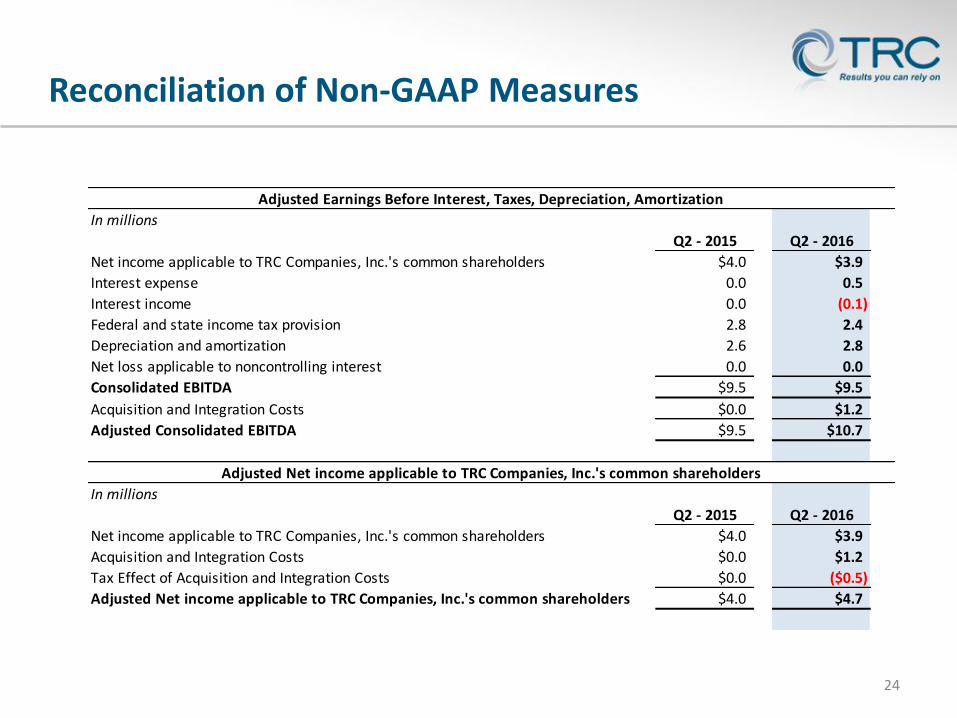

Reconciliation of Non-GAAP Measures

22

In millions

Q2 - 2015 Q2 - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders $4.0 $3.9

Interest expense 0.0 0.5

Interest income 0.0 (0.1)

Federal and state income tax provision 2.8 2.4

Depreciation and amortization 2.6 2.8

Net loss applicable to noncontrolling interest 0.0 0.0

Consolidated EBITDA $9.5 $9.5

In millions

Q2 - 2015 Q2 - 2016

Net service revenue $99.8 $111.4

Cost of services 82.6 93.7

Gross Margin $17.2 $17.7

Gross Margin % 17.3% 15.9%

In millions

Q2 - 2015 Q2 - 2016

Cash flow from operations $(1.3) $(1.0)

Additions to property and equipment (2.5) (2.0)

Free Cash Flow $(3.8) $(3.0)

Earnings Before Interest, Taxes, Depreciation, Amortization

Gross Margin and Gross Margin %

Free Cash Flow

Reconciliation of Non-GAAP Measures

23

In millions

YTD - 2015 YTD - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders $7.5 $8.4

Interest expense 0.1 0.5

Interest income 0.0 (0.1)

Federal and state income tax provision 5.3 5.6

Depreciation and amortization 4.9 5.0

Net loss applicable to noncontrolling interest 0.0 0.0

Consolidated EBITDA $17.8 $19.4

In millions

YTD - 2015 YTD - 2016

Net service revenue $192.5 $211.5

Cost of services 163.8 176.7

Gross Margin $28.7 $34.9

Gross Margin % 14.9% 16.5%

In millions

YTD - 2015 YTD - 2016

Cash flow from operations $1.2 $13.4

Additions to property and equipment (4.0) (4.0)

Free Cash Flow $(2.8) $9.4.

Earnings Before Interest, Taxes, Depreciation, Amortization

Gross Margin and Gross Margin %

Free Cash Flow

Reconciliation of Non-GAAP Measures

24

In millions

Q2 - 2015 Q2 - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders $4.0 $3.9

Interest expense 0.0 0.5

Interest income 0.0 (0.1)

Federal and state income tax provision 2.8 2.4

Depreciation and amortization 2.6 2.8

Net loss applicable to noncontrolling interest 0.0 0.0

Consolidated EBITDA $9.5 $9.5

Acquisition and Integration Costs $0.0 $1.2

Adjusted Consolidated EBITDA $9.5 $10.7

In millions

Q2 - 2015 Q2 - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders $4.0 $3.9

Acquisition and Integration Costs $0.0 $1.2

Tax Effect of Acquisition and Integration Costs $0.0 ($0.5)

Adjusted Net income applicable to TRC Companies, Inc.'s common shareholders $4.0 $4.7

Adjusted Earnings Before Interest, Taxes, Depreciation, Amortization

Adjusted Net income applicable to TRC Companies, Inc.'s common shareholders

Reconciliation of Non-GAAP Measures

25

In millions

YTD - 2015 YTD - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders $7.5 $8.4

Interest expense 0.1 0.5

Interest income 0.0 (0.1)

Federal and state income tax provision 5.3 5.6

Depreciation and amortization 4.9 5.0

Net loss applicable to noncontrolling interest 0.0 0.0

Consolidated EBITDA $17.8 $19.4

Acquisition and Integration Costs $0.0 $2.1

Adjusted Consolidated EBITDA $17.8 $21.5

In millions

YTD - 2015 YTD - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders $7.5 $8.4

Acquisition and Integration Costs $0.0 $2.1

Tax Effect of Acquisition and Integration Costs $0.0 ($0.8)

Adjusted Net income applicable to TRC Companies, Inc.'s common shareholders $7.5 $9.7

Adjusted Earnings Before Interest, Taxes, Depreciation, Amortization

Adjusted Net income applicable to TRC Companies, Inc.'s common shareholders

Reconciliation of Non-GAAP Measures

26

In millions

Q2 2015 Q2 2016

Operating income $6.9 $6.7

Acquisition and Integration Costs $0.0 $1.2

Adjusted Operating Income $6.9 $7.9

In millions

Q2 2015 Q2 2016

Net income applicable to TRC Companies, Inc.'s common shareholders $4.0 $3.9

Acquisition and Integration Costs $0.0 $1.2

Tax Effect of Acquisition and Integration Costs $0.0 ($0.5)

Adjusted Net income applicable to TRC Companies, Inc.'s common shareholders $4.0 $4.7

Diluted Shares Outstanding 30.5 31.4

Adjusted diluted earnings per common share $0.13 $0.15

Adjusted Diluted Earnings per Common Share

Adjusted Operating Income

Reconciliation of Non-GAAP Measures

27

In millions

YTD 2015 YTD 2016

Operating income $12.9 $14.4

Acquisition and Integration Costs $0.0 $2.1

Adjusted Operating Income $12.9 $16.5

In millions

YTD 2015 YTD 2016

Net income applicable to TRC Companies, Inc.'s common shareholders $7.5 $8.4

Acquisition and Integration Costs $0.0 $2.1

Tax Effect of Acquisition and Integration Costs $0.0 ($0.8)

Adjusted Net income applicable to TRC Companies, Inc.'s common shareholders $7.5 $9.7

Diluted Shares Outstanding 30.46 31.3

Adjusted diluted earnings per common share $0.25 $0.31

Adjusted Diluted Earnings per Common Share

Adjusted Operating Income

Definitions for Non-GAAP Measures

28

Earnings Before Interest, Taxes, Depreciation, Amortization (EBITDA)The Company presents EBITDA because it believes that it is a useful tool for the Company, its lenders and its investors to measure the Company’s ability to meet debt service, capital expenditure and working capital requirements. As used in the presentation, EBITDA is operating income plus depreciation and amortization.

Adjusted Earnings Before Interest, Taxes, Depreciation, Amortization (Adjusted EBITDA)The Company presents Adjusted EBITDA because it believes that it is a useful tool for the Company, its lenders and its investors to measure the Company’s ability to meet debt service, capital expenditure and working capital requirements to measure the Company’s underlying performance. As used in the presentation, Adjusted EBITDA is defined as operating income plus depreciation and amortization plus acquisition and integration expenses.

Gross Margin and Gross Margin %The Company presents Gross Margin and Gross Margin % to allow investors to better evaluate short-term and long-term profitability trends. The definition of Gross Margin is equal to Net Service Revenue less Cost of Services. Gross Margin % is equal to Gross Margin Divided by Net Service Revenue.

Free Cash FlowThe Company presents free cash flow, and ratios based on it, to conduct and evaluate its business because, although it is similar to cash flow from operations, the Company believes it is a useful measure of cash flows since purchases of fixed assets are a necessary component of ongoing operations. The definition of Free Cash Flow is equal to net cash provided by (used in) operating activities plus additions to property and equipment.

Definitions for Non-GAAP Measures

29

Adjusted Operating IncomeThe Company presents Adjusted Operating Income because it believes that it is a useful tool for the Company, its lenders and its investors to measure the Company’s underlying operating performance. As used in the presentation, Adjusted Operating Income is defined as operating income plus acquisition and integration expenses.

Adjusted Net IncomeThe Company presents Adjusted Net Income because it believes that it is a useful tool for the Company, its lenders and its investors to measure the Company’s financial performance. As used in the presentation, Adjusted Net Income is defined as net income applicable to TRC Companies, Inc. plus the tax effected acquisition and integration expenses. The Company utilizes its effective tax rate for the period in calculating the tax effect.

Adjusted Diluted Earnings Per Share (Adjusted Diluted EPS)The Company presents Adjusted Diluted EPS because it believes that it is a useful tool for the Company, its lenders and its investors to measure the Company’s financial performance. As used in the presentation, Adjusted Diluted EPS is defined as Adjusted Net Income divided by diluted weighted average shares outstanding.