trends in data center procurement and support · non-traditional data center environments are...

TRANSCRIPT

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

January 2016

Sponsored by

© 2016 Dimensional Research.All Rights Reserved. www.dimensionalresearch.com

IntroductionThe days of partnering with a single strategic vendor to deliver end-to-end data center equipment and services are over. Today’s IT decision makers are expected to make decisions that take into account capabilities and quality of technology as well as cost, all in the context of the business value delivered. To meet these goals, modern data centers are embracing a wide range of procurement and support alternatives that were almost unknown in the past, including third-party maintenance, pre-owned equipment, and multi-vendor environments. But how prevalent are these alternative approaches? What are the trends driving adoption? What roles are IT and procurement taking in influencing these changes?

The following report, sponsored by Curvature, is based on a global survey of 507 IT decision makers. All survey participants had managerial or hands-on responsibilities for data center purchasing and support. Questions were asked on a variety of topics related to experiences and attitudes towards purchasing equipment and services for data centers.

Key Findings• 2015 and 2016 strong growth years for pre-owned equipment and maintenance alternatives

- 92% use pre-owned equipment, third-party maintenance, or multi-vendor infrastructure in their data centers today including

◦ 53% purchase pre-owned equipment ◦ 60% use third-party maintenance ◦ 85% have multi-vendor environments

- 60% increased use of pre-owned equipment, third-party maintenance, or multi-vendor infrastructure alternatives in 2015 and 54% plan to increase in 2016

• “Perfect storm” driving increase in pre-owned equipment and maintenance alternatives - Growth is driven by a wide range of factors including new technologies that enable flexible architectures, need for negotiating power, and availability of better alternatives

• Equipmentbuyerswantflexibilityandchoice - 90% see benefits in third-party maintenance of data center equipment including lower costs, optimized spending, and retaining vendor flexibility

- 96% see advantages in multi-vendor data centers including optimized spending, reducing risk of vendor lock-in, and retaining vendor flexibility

- Making decisions based on process rather than IT need is common, including internal purchasing processes (56%), vendor requirements (55%) and internal policies (52%)

- 42% say procurement processes are getting better and only 14% think they are getting worse - IT executives value staff that makes changes that help both technology and financials

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

Dimensional Research | January 2016

Sponsored by

Dimensional Research | January 2016

www.dimensionalresearch.com © 2016 Dimensional Research.All Rights Reserved. Page 3

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

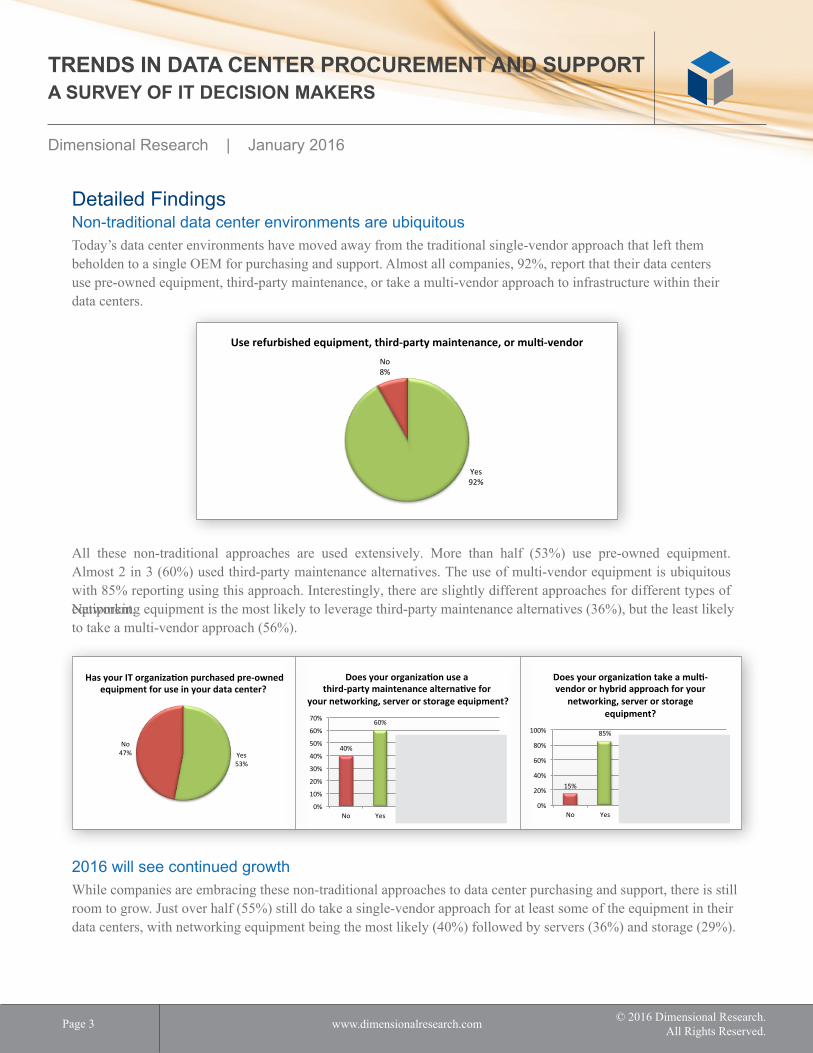

Detailed FindingsNon-traditional data center environments are ubiquitousToday’s data center environments have moved away from the traditional single-vendor approach that left them beholden to a single OEM for purchasing and support. Almost all companies, 92%, report that their data centers use pre-owned equipment, third-party maintenance, or take a multi-vendor approach to infrastructure within their data centers.

All these non-traditional approaches are used extensively. More than half (53%) use pre-owned equipment. Almost 2 in 3 (60%) used third-party maintenance alternatives. The use of multi-vendor equipment is ubiquitous with 85% reporting using this approach. Interestingly, there are slightly different approaches for different types of equipment. Networking equipment is the most likely to leverage third-party maintenance alternatives (36%), but the least likely to take a multi-vendor approach (56%).

2016 will see continued growth While companies are embracing these non-traditional approaches to data center purchasing and support, there is still room to grow. Just over half (55%) still do take a single-vendor approach for at least some of the equipment in their data centers, with networking equipment being the most likely (40%) followed by servers (36%) and storage (29%).

Yes 53%

No 47%

Has your IT organiza/on purchased pre-‐owned equipment for use in your data center?

15%

85%

56% 62% 63%

0%

20%

40%

60%

80%

100%

No Yes Networking Servers Storage

Does your organiza.on take a mul.-‐vendor or hybrid approach for your

networking, server or storage equipment?

Yes 92%

No 8%

Use refurbished equipment, third-‐party maintenance, or mul8-‐vendor

40%

60%

32% 35% 36%

0%

10%

20%

30%

40%

50%

60%

70%

No Yes Storage Servers Networking

Does your organiza.on use a third-‐party maintenance alterna.ve for

your networking, server or storage equipment?

Dimensional Research | January 2016

www.dimensionalresearch.com © 2016 Dimensional Research.All Rights Reserved. Page 4

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

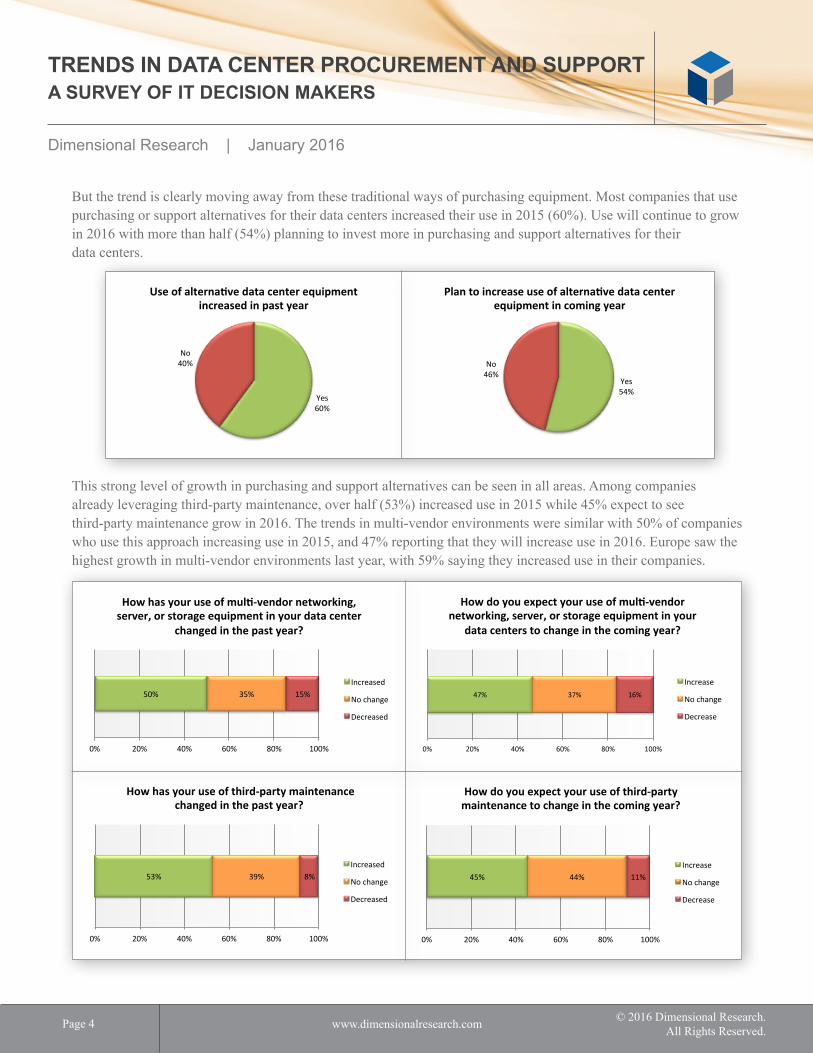

But the trend is clearly moving away from these traditional ways of purchasing equipment. Most companies that use purchasing or support alternatives for their data centers increased their use in 2015 (60%). Use will continue to grow in 2016 with more than half (54%) planning to invest more in purchasing and support alternatives for their data centers.

This strong level of growth in purchasing and support alternatives can be seen in all areas. Among companies already leveraging third-party maintenance, over half (53%) increased use in 2015 while 45% expect to see third-party maintenance grow in 2016. The trends in multi-vendor environments were similar with 50% of companies who use this approach increasing use in 2015, and 47% reporting that they will increase use in 2016. Europe saw the highest growth in multi-vendor environments last year, with 59% saying they increased use in their companies.

Yes 60%

No 40%

Use of alterna,ve data center equipment increased in past year

Yes 54%

No 46%

Plan to increase use of alterna/ve data center equipment in coming year

47% 37% 16%

0% 20% 40% 60% 80% 100%

How do you expect your use of mul2-‐vendor networking, server, or storage equipment in your

data centers to change in the coming year?

Increase

No change

Decrease

50% 35% 15%

0% 20% 40% 60% 80% 100%

How has your use of mul/-‐vendor networking, server, or storage equipment in your data center

changed in the past year?

Increased

No change

Decreased

53% 39% 8%

0% 20% 40% 60% 80% 100%

How has your use of third-‐party maintenance changed in the past year?

Increased

No change

Decreased

45% 44% 11%

0% 20% 40% 60% 80% 100%

How do you expect your use of third-‐party maintenance to change in the coming year?

Increase

No change

Decrease

Dimensional Research | January 2016

www.dimensionalresearch.com © 2016 Dimensional Research.All Rights Reserved. Page 5

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

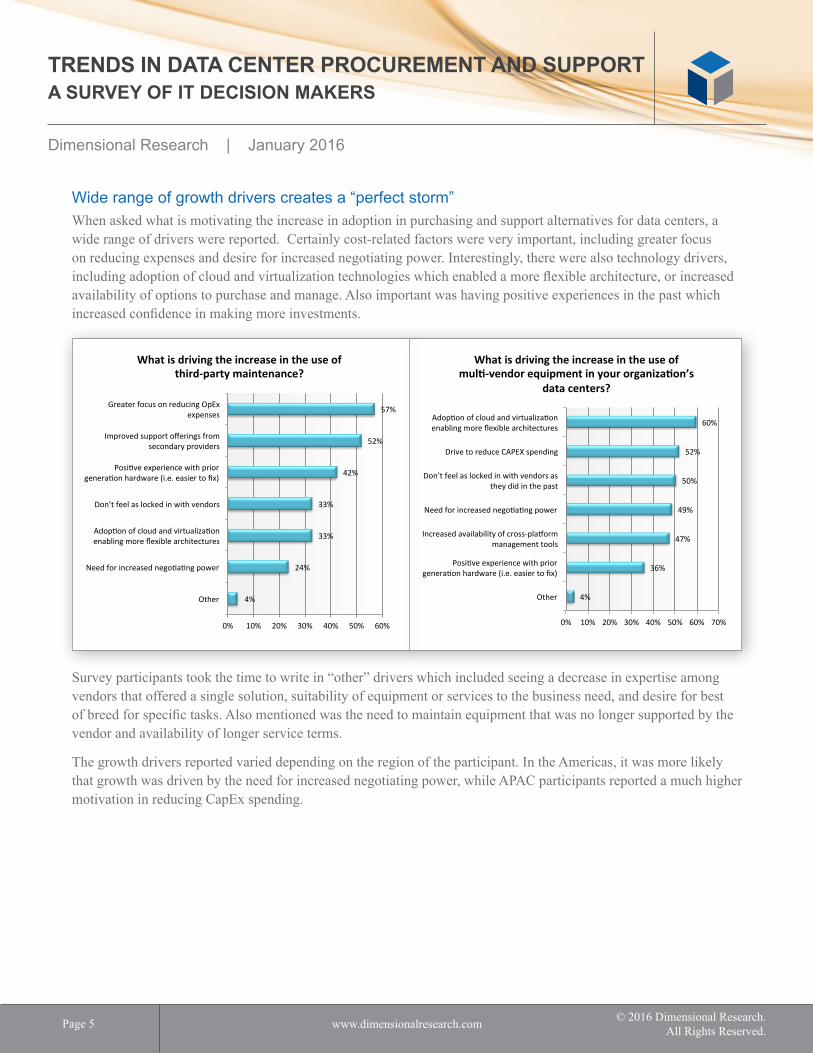

Wide range of growth drivers creates a “perfect storm” When asked what is motivating the increase in adoption in purchasing and support alternatives for data centers, a wide range of drivers were reported. Certainly cost-related factors were very important, including greater focus on reducing expenses and desire for increased negotiating power. Interestingly, there were also technology drivers, including adoption of cloud and virtualization technologies which enabled a more flexible architecture, or increased availability of options to purchase and manage. Also important was having positive experiences in the past which increased confidence in making more investments.

Survey participants took the time to write in “other” drivers which included seeing a decrease in expertise among vendors that offered a single solution, suitability of equipment or services to the business need, and desire for best of breed for specific tasks. Also mentioned was the need to maintain equipment that was no longer supported by the vendor and availability of longer service terms.

The growth drivers reported varied depending on the region of the participant. In the Americas, it was more likely that growth was driven by the need for increased negotiating power, while APAC participants reported a much higher motivation in reducing CapEx spending.

4%

24%

33%

33%

42%

52%

57%

0% 10% 20% 30% 40% 50% 60%

Other

Need for increased nego:a:ng power

Adop:on of cloud and virtualiza:on enabling more flexible architectures

Don’t feel as locked in with vendors

Posi:ve experience with prior genera:on hardware (i.e. easier to fix)

Improved support offerings from secondary providers

Greater focus on reducing OpEx expenses

What is driving the increase in the use of third-‐party maintenance?

4%

36%

47%

49%

50%

52%

60%

0% 10% 20% 30% 40% 50% 60% 70%

Other

Posi5ve experience with prior genera5on hardware (i.e. easier to fix)

Increased availability of cross-‐plaIorm management tools

Need for increased nego5a5ng power

Don’t feel as locked in with vendors as they did in the past

Drive to reduce CAPEX spending

Adop5on of cloud and virtualiza5on enabling more flexible architectures

What is driving the increase in the use of mul4-‐vendor equipment in your organiza4on’s

data centers?

Dimensional Research | January 2016

www.dimensionalresearch.com © 2016 Dimensional Research.All Rights Reserved. Page 6

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

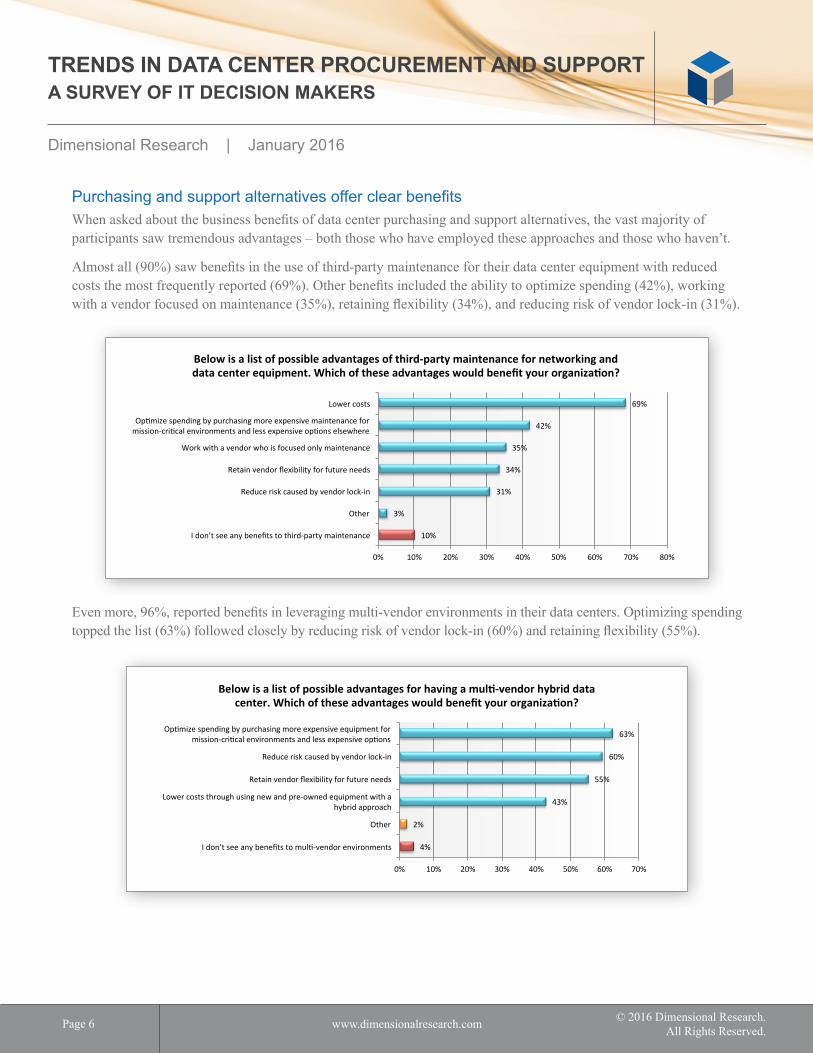

Purchasing and support alternatives offer clear benefitsWhen asked about the business benefits of data center purchasing and support alternatives, the vast majority of participants saw tremendous advantages – both those who have employed these approaches and those who haven’t.

Almost all (90%) saw benefits in the use of third-party maintenance for their data center equipment with reduced costs the most frequently reported (69%). Other benefits included the ability to optimize spending (42%), working with a vendor focused on maintenance (35%), retaining flexibility (34%), and reducing risk of vendor lock-in (31%).

Even more, 96%, reported benefits in leveraging multi-vendor environments in their data centers. Optimizing spending topped the list (63%) followed closely by reducing risk of vendor lock-in (60%) and retaining flexibility (55%).

10%

3%

31%

34%

35%

42%

69%

0% 10% 20% 30% 40% 50% 60% 70% 80%

I don’t see any benefits to third-‐party maintenance

Other

Reduce risk caused by vendor lock-‐in

Retain vendor flexibility for future needs

Work with a vendor who is focused only maintenance

OpKmize spending by purchasing more expensive maintenance for mission-‐criKcal environments and less expensive opKons elsewhere

Lower costs

Below is a list of possible advantages of third-‐party maintenance for networking and data center equipment. Which of these advantages would benefit your organiza?on?

4%

2%

43%

55%

60%

63%

0% 10% 20% 30% 40% 50% 60% 70%

I don’t see any benefits to mul:-‐vendor environments

Other

Lower costs through using new and pre-‐owned equipment with a hybrid approach

Retain vendor flexibility for future needs

Reduce risk caused by vendor lock-‐in

Op:mize spending by purchasing more expensive equipment for mission-‐cri:cal environments and less expensive op:ons

Below is a list of possible advantages for having a mul6-‐vendor hybrid data center. Which of these advantages would benefit your organiza6on?

Dimensional Research | January 2016

www.dimensionalresearch.com © 2016 Dimensional Research.All Rights Reserved. Page 7

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

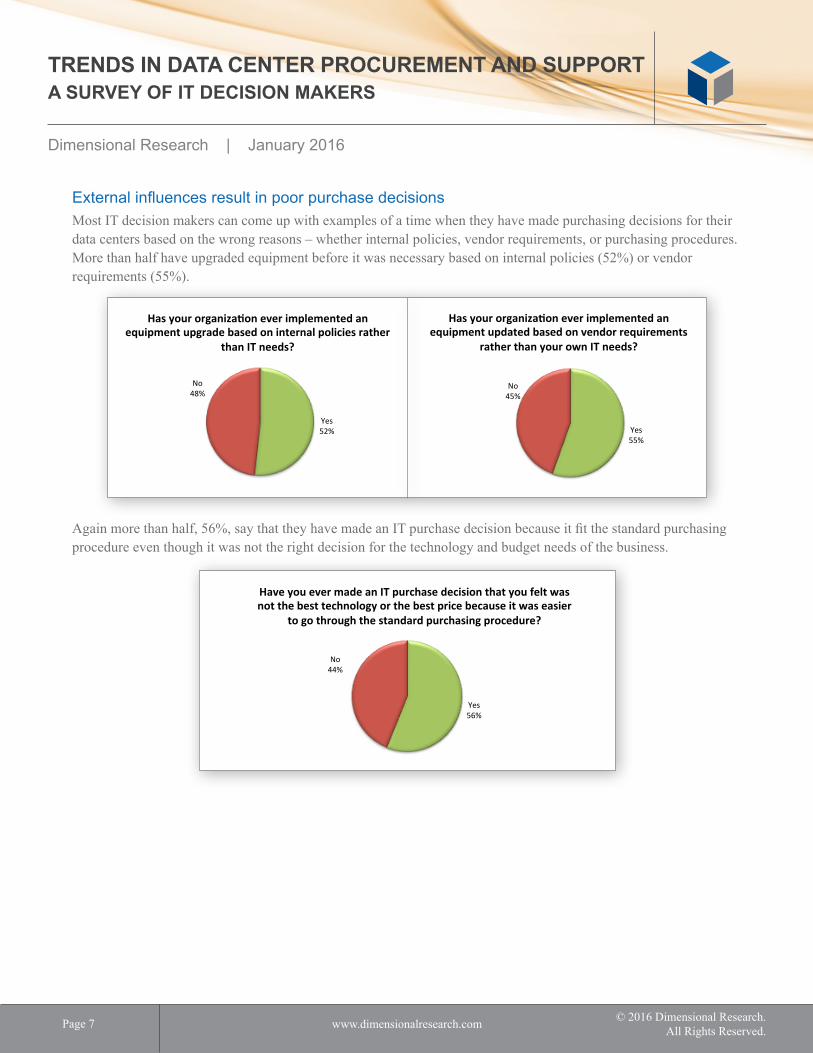

External influences result in poor purchase decisionsMost IT decision makers can come up with examples of a time when they have made purchasing decisions for their data centers based on the wrong reasons – whether internal policies, vendor requirements, or purchasing procedures. More than half have upgraded equipment before it was necessary based on internal policies (52%) or vendor requirements (55%).

Again more than half, 56%, say that they have made an IT purchase decision because it fit the standard purchasing procedure even though it was not the right decision for the technology and budget needs of the business.

Yes 52%

No 48%

Has your organiza-on ever implemented an equipment upgrade based on internal policies rather

than IT needs?

Yes 55%

No 45%

Has your organiza-on ever implemented an equipment updated based on vendor requirements

rather than your own IT needs?

Yes 56%

No 44%

Have you ever made an IT purchase decision that you felt was not the best technology or the best price because it was easier

to go through the standard purchasing procedure?

Dimensional Research | January 2016

www.dimensionalresearch.com © 2016 Dimensional Research.All Rights Reserved. Page 8

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

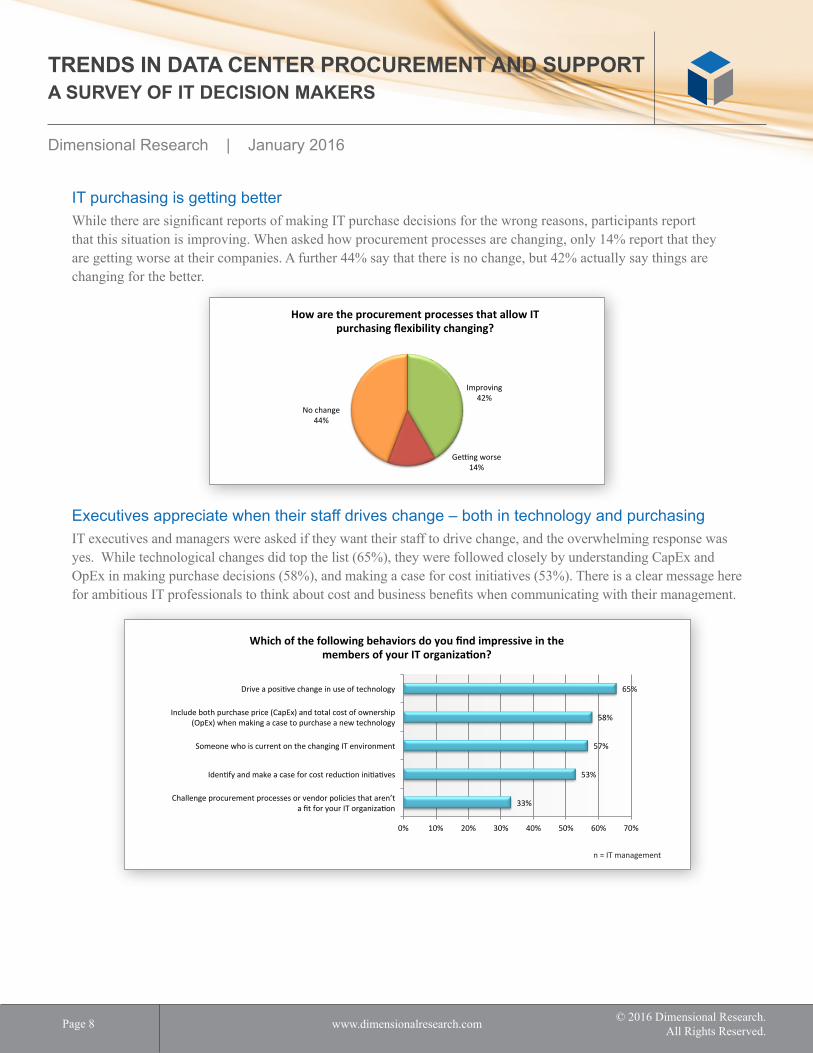

IT purchasing is getting betterWhile there are significant reports of making IT purchase decisions for the wrong reasons, participants report that this situation is improving. When asked how procurement processes are changing, only 14% report that they are getting worse at their companies. A further 44% say that there is no change, but 42% actually say things are changing for the better.

Executives appreciate when their staff drives change – both in technology and purchasingIT executives and managers were asked if they want their staff to drive change, and the overwhelming response was yes. While technological changes did top the list (65%), they were followed closely by understanding CapEx and OpEx in making purchase decisions (58%), and making a case for cost initiatives (53%). There is a clear message here for ambitious IT professionals to think about cost and business benefits when communicating with their management.

n = IT management

33%

53%

57%

58%

65%

0% 10% 20% 30% 40% 50% 60% 70%

Challenge procurement processes or vendor policies that aren’t a fit for your IT organizaEon

IdenEfy and make a case for cost reducEon iniEaEves

Someone who is current on the changing IT environment

Include both purchase price (CapEx) and total cost of ownership (OpEx) when making a case to purchase a new technology

Drive a posiEve change in use of technology

Which of the following behaviors do you find impressive in the members of your IT organiza<on?

Improving 42%

Ge0ng worse 14%

No change 44%

How are the procurement processes that allow IT purchasing flexibility changing?

Dimensional Research | January 2016

www.dimensionalresearch.com © 2016 Dimensional Research.All Rights Reserved. Page 9

TRENDS IN DATA CENTER PROCUREMENT AND SUPPORTA SURVEY OF IT DECISION MAKERS

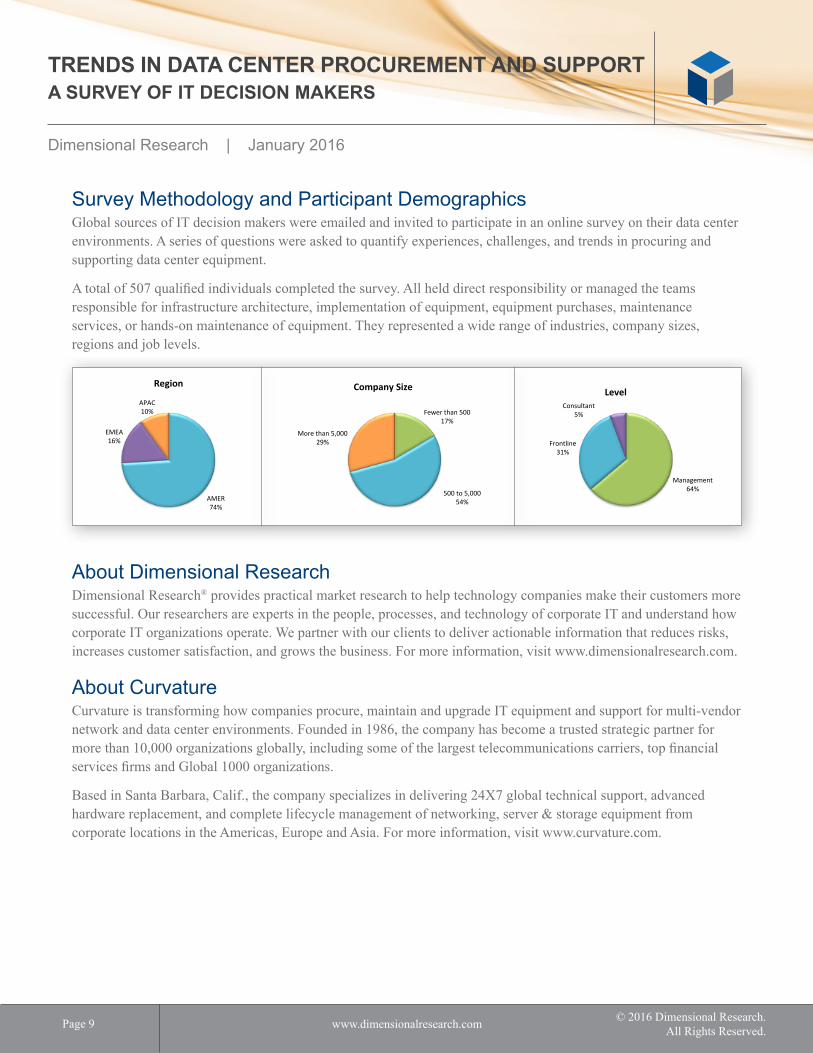

Survey Methodology and Participant DemographicsGlobal sources of IT decision makers were emailed and invited to participate in an online survey on their data center environments. A series of questions were asked to quantify experiences, challenges, and trends in procuring and supporting data center equipment.

A total of 507 qualified individuals completed the survey. All held direct responsibility or managed the teams responsible for infrastructure architecture, implementation of equipment, equipment purchases, maintenance services, or hands-on maintenance of equipment. They represented a wide range of industries, company sizes, regions and job levels.

About Dimensional ResearchDimensional Research® provides practical market research to help technology companies make their customers more successful. Our researchers are experts in the people, processes, and technology of corporate IT and understand how corporate IT organizations operate. We partner with our clients to deliver actionable information that reduces risks, increases customer satisfaction, and grows the business. For more information, visit www.dimensionalresearch.com.

About CurvatureCurvature is transforming how companies procure, maintain and upgrade IT equipment and support for multi-vendor network and data center environments. Founded in 1986, the company has become a trusted strategic partner for more than 10,000 organizations globally, including some of the largest telecommunications carriers, top financial services firms and Global 1000 organizations.

Based in Santa Barbara, Calif., the company specializes in delivering 24X7 global technical support, advanced hardware replacement, and complete lifecycle management of networking, server & storage equipment from corporate locations in the Americas, Europe and Asia. For more information, visit www.curvature.com.

AMER 74%

EMEA 16%

APAC 10%

Region

Fewer than 500 17%

500 to 5,000 54%

More than 5,000 29%

Company Size

Management 64%

Frontline 31%

Consultant 5%

Level