trends in healthcare payments seventh annual report:...

TRANSCRIPT

Trends in Healthcare PaymentsSeventh Annual Report: 2016

Published: May 2017

2 © 2017 InstaMed. All rights reserved.

Consumer healthcare spending

is expected to grow to $608 billion

by 2019.1

of consumersare confused by their medical

bills and EOBs.

page 36

page 30

Source

1 Kalorama Foundation

rank direct-to-consumer solutions as their top priority in 2017.

of payers

of providers report it takes one month or

longer to collect from patients.

page 24

%73

%40

%74

© 2017 InstaMed. All rights reserved.3

All content, including text, graphics, logos, icons, images and the selection and arrangement thereof, is the exclusive property of InstaMed and is protected by U.S. and international copyright laws. No portion of this document may be reproduced, modified, distributed, transmitted, posted or disclosed in any form or by any means without the express written consent of InstaMed.

06

16

24

36

04

10

20

30

Consumers Are Demanding More From Healthcare

Paper Is Hurting All Healthcare Stakeholders

Omnichannel Payments Are Impacting Healthcare

Provider Sentiment

Consumer SentimentPayer Sentiment

Executive Summary

Healthcare Data Is Under Attack

Contents

44 Conclusions

4 © 2017 InstaMed. All rights reserved.

Healthcare in the Spotlight

Healthcare was front and center in the

news in 2016 as the country ramped

up to the November election. Each

candidate campaigned on the future

of healthcare in the United States. For

all the attention healthcare gathered,

there was no indication of a shift in

the trend towards consumerism or any

overwhelming sentiment within the

industry about the election’s impact. In

fact, when surveyed about the impact

of the 2016 election on healthcare, the

response from healthcare providers

was almost evenly split among positive,

neutral and negative.1 The data analyzed

in this report reveals that whether

the American Health Care Act (AHCA)

becomes the law of the land or the

Affordable Care Act (ACA) remains in

place, there are four key areas that

require the industry’s attention.

Consumers Are Demanding More From

Healthcare

The new reality in healthcare is that

consumers not only owe more – in

the form of deductibles, copayments,

coinsurance and health plan premiums

– but the amounts are higher than

they ever have been before. However,

many in the industry are slow to

recognize the new role of consumers

as an industry stakeholder. When

consumer demands are ignored, the

consequences are severe – irreparable

damage to an organization’s brand

resulting in lost patients and members,

and ultimately revenue.

Executive Summary

Sources

1 Provider Healthcare Payments Survey 2016

2016 Trends in Healthcare Payments

Omnichannel Payments Are Impacting

Healthcare

What exactly are consumers

demanding from healthcare payments?

The data reveals that common

assumptions are incorrect. First,

consumers do not view healthcare

as different from other industries.

Second, consumers want multiple

ways to pay all of their healthcare

bills and premiums just as they do

for their household bills – everything

from paying online to making payments

through their bank’s bill payment

site. Third, and most surprising,

consumers across all generations want

convenience through online payment

channels and electronic payment

methods when it comes to healthcare

payments.

When surveyed about

the impact of the 2016

election on healthcare,

the response from

healthcare providers was

almost evenly split among

positive, neutral

and negative.

© 2017 InstaMed. All rights reserved.5

The purpose of this report

is to objectively educate

the market and promote

awareness, change and

greater efficiency.

Paper Is Hurting All Healthcare

Stakeholders

Paper remains ubiquitous within the

healthcare industry. The true costs of

paper are hurting the entire industry,

which continues to be burdened by high

overhead and lack of resources. Forward-

thinking organizations are looking to

the untapped potential of electronic

transactions to streamline and simplify

healthcare payments, as well as satisfy

the consumer demand for convenience

in the industry. The industry needs to go

paperless now more than ever.

Healthcare Data Is Under Attack

Any healthcare organizations unsure

if their data is at risk should assume

the worst. Ransomware is a rapidly

growing threat that has proven to

have the capability to paralyze an

entire organization as seen in the

recent attacks of WannaCry. However,

ransomware is just one of many threats

to data in the industry. The threats will

only grow as the industry attempts to

keep up with the increases in demands

for a consumer-centric, electronic

healthcare payments experience.

Survey of Industry Drivers

The 2016 Trends in Healthcare

Payments Annual Report identifies the

healthcare payments industry shifts

that are business drivers for payers

and providers to make changes to

address consumerism, improve cash

flow, operate more efficiently and

enhance data security. The purpose

of this report is to objectively educate

the market and promote awareness,

change and greater efficiency. These

trends highlight quantitative data derived

from the InstaMed Network and feature

qualitative, proprietary, independently

gathered survey data from healthcare

providers, payers and consumers

nationwide.

Consumers across

all generations want

convenience when it

comes to healthcare

payments.

Any healthcare

organizations unsure if

their data is at risk should

assume the worst.

6 © 2017 InstaMed. All rights reserved.

As consumers owe more in healthcare,

payers and providers are challenged to

adapt to the consumer’s new role as an

industry stakeholder.

TRENDSin HEALTHCARE PAYMENTS

Consumer Healthcare Financial Realities

In 2016, healthcare spending grew

to $3.4 trillion and is expected to

reach $5.5 trillion by the year 2025.1

Much of this growth has been and

continues to be spurred by increasing

consumer payments for healthcare

services and health plan premiums.

Overall, consumer spending in the

healthcare industry is expected to

grow to $608 billion by 2019.2

When this report was first released

in 2010, 10 million consumers were

enrolled in high deductible health

plans (HDHPs),3 which require

consumers to pay a minimum

deductible amount before their health

plans cover any portion of the cost.

Less than a decade later, 75 million

consumers are enrolled in HDHPs, a

more than seven-fold increase.4

The average deductible for covered

workers with single coverage has

doubled from $735 in 2010 to

$1,478 in 2016.5

Consumers Are Demanding More From Healthcare

Sources

1 Centers for Medicare & Medicaid Services

2 Kalorama Foundation

3 AHIP 2010

4 CDC’s National Center for Health Statistics

5 Kaiser Family Foundation

6 U.S. Department of Health and Human Services

Data from the InstaMed Network

confirms this trend as the total volume

of consumer payments to providers on

the InstaMed Network has increased

by 58 percent from 2013 to 2016,

growing 16 percent on average each

year. (Figure 1.1)

Consumers are paying more to have

health plan coverage as well, with rates

for health plan premiums on the rise.

In fact, premiums for plans available to

consumers via HealthCare.gov increased

by an average of 22 percent in 2017.6

1.1

Increase in the Total Volume of Consumer Payments to ProvidersFrom 2013 to 2016, the total volume of consumer payments to providers on the InstaMed Network has increased by 58%, growing by 16% on average each year

2016

2013

© 2017 InstaMed. All rights reserved.7

What Does This Mean For Providers and

Payers?

The impacts of consumer payments

on the healthcare economy are felt by

both providers and payers alike.

As seen in recent years, the trend in

increasing consumer responsibility

requires that providers must collect

a larger portion of their revenue

directly from patients. This holds true

for 2016 as 72 percent of providers

reported an increase in patient

responsibility over 2015.7 Since

2013, the majority of providers have

consistently reported this increase in

patient responsibility.

Sources

7 Provider Healthcare Payments Survey 2016

8 Payer Healthcare Payments Survey 2016

9 Consumer Healthcare Payments Survey 2016

10 University of Connecticut’s Health Disparities Institute

11 UnitedHealthcare Consumer Sentiment Survey

The burden to collect from patients

has become a growing concern for

providers as the top three provider

revenue cycle concerns in 2016

were related to patient payments:

increases in patient responsibility for

payment, how to increase cash flow

and ways to reduce days in accounts

receivable. In particular, the last

concern is validated by the 73 percent

of providers who reported that it takes

one month or longer to collect from a

patient. (Figure 1.2)

In 2013, the ACA changed the

landscape of the healthcare economy

by greatly expanding the individual

market. As a result, millions of

consumers now buy health plans

directly from payers.

Payers must now interact with

consumers in ways that they rarely

did before, including collecting

monthly health plan premiums

directly from consumers instead of

working primarily with an insurance

broker or employer group. The

political landscape and questionable

future of the ACA has done little to

stymie payer concerns about their

relationship with consumers as 40

percent of payers rank offering direct-

to-consumer solutions as their top

priority in 2017.8

1.2

Significant Delays to Collect From Patients 73% of providers reported that it takes one month or longer to collect a patient payment

%73

When this report was

first released in 2010, 10

million consumers were

enrolled in HDHPs. Less

than a decade later, 75

million consumers are

enrolled in HDHPs.

Healthcare Is Wrought With Confusion

Despite these relationship shifts

driven by consumer payments, many

in the industry have been slow

to acknowledge or encourage the

consumer’s new role as an industry

stakeholder. Consider that 92 percent

of consumers reported that it was

important to know their payment

responsibility prior to a provider

visit.9 (Figure 1.3) Yet, only a third of

consumers understood their payment

responsibility when a deductible or

copay were part of their health plan.10

This gap is perpetuated by a general

lack of literacy on common terms in

the healthcare payments vernacular

– only seven percent of consumers

could successfully define terms

such as plan premium, deductible,

co-insurance and out-of-pocket

maximum.11

8 © 2017 InstaMed. All rights reserved.

Sources

12 Consumer Healthcare Payments Survey 2016

13 Consumer Healthcare Payments Survey 2016

14 2015 The Hospital Consumer Assessment of

Healthcare Providers and Systems (HCAHPS) Survey

15 Deloitte

16 Melior 2015 Consumer Survey

There are various contributing factors to

this confusion. One disconnect is that

consumers may not receive statements

for services until weeks or even months

have passed. Another cause can be

lack of billing consolidation between

different organizations under a single

business identity, which means that

a consumer could reasonably receive

multiple statements for what they

consider to be one visit.

Consumer Demands Have Real Impacts

The ability to ignore or deprioritize

consumer demands in healthcare

payments may no longer be an option in

the near future. The consequences of

inaction go beyond just longer days in

accounts receivable or bad debt.

The trends now delineate a clear

correlation between the payment

experience and a healthcare

organization’s brand. For example,

patients who are satisfied with billing

are five times more likely to recommend

the hospital.14

How a consumer views a healthcare

organization has direct ties to that

organization’s revenue. Between 2008

and 2014, hospitals with excellent

HCAHPS patient ratings had a net

margin of 4.7 percent compared to

just 1.8 percent for hospitals with low

ratings.15 Additionally, 75 percent of

consumers reported that they prefer

health plans with payment capability

when they were selecting a plan.16

1.4

Consumers Are Confused by Healthcare Bills 74% of consumers are confused by EOBs and medical bills

Typically, consumers are only

aware that they may have payment

responsibility after they seek

healthcare services when they are

sent an explanation of benefits

(EOB) by their health plan. Though

it discusses payment responsibility,

the EOB typically includes bold

language that it is not a bill and

should not be paid by the consumer.

This mixed messaging may be one

of the reasons that 74 percent of

consumers are confused by EOBs.12

Consumer confusion does not lessen

when the provider sends a statement

for payment responsibility as 74

percent of consumers were also

confused by their medical bills.13

(Figure 1.4)

Only 7 percent of

consumers can

successfully define terms

such as plan premium,

deductible, co-insurance

and out-of-pocket

maximum.

1.3

Consumers Want to Know Payment Responsibility Upfront92% of consumers reported that it was important to know payment responsibility prior to a provider visit

%92

© 2017 InstaMed. All rights reserved.9

Are Providers the Ultimate Lenders?

The Patient Financing Debate

As consumer responsibility soars,

providers are seeking ways to ensure they

get paid. This shift has created industry

buzz around patient financing.

Businesses often seek lending solutions

for their cash flow problems. Patient

financing offerings have been in the

market since the 1990s, and the market

for elective procedures is the strongest

and most mature. Alternatively, the

market for non-elective procedures

(procedures that are medically necessary

and/or essential) has been wrought with

challenges and churn of business models

and lending structures. In spite of the

challenges, the market for non-elective

procedures garners attention because

it is the largest slice of the $3 trillion

healthcare economy.

There are three models for non-elective

patient financing: self-funding, recourse

lending and non-recourse lending. Self-

funding is what providers do today when

they carry the account as a receivable

and attempt to collect the money directly

from the patient.

The recourse lending model requires the

provider pass the underwriting criteria

of the lender to launch the patient

financing program. As patients elect

to join the program, their receivable is

funded to the provider by the lender in

exchange for a one-time discount fee and

ongoing service fees from the provider.

Additionally, the lender has the right to

recover losses from the patient by way of

a pre-defined process of recovering the

loss from the provider.

The non-recourse lending model requires

the provider to agree to the terms and

fees of the lender to launch the patient

financing program. Then each patient is

required to pass the underwriting criteria

of the lender for funding to occur and any

losses are borne by the lender without

recourse to the provider. The lender has

the right to accept or deny each patient

based on its underwriting policies and

procedures before entering into the

lending agreement with the patient

and funding the provider. Non-recourse

lending may result in patients facing very

high interest rates and fees, as the lender

does not have any other option to offset

their losses.

Recourse models have high recourse

rates for consumers with weak credit

and poor ability to pay and therefore do

not add much value in exchange for the

discount fees and service fees charged.

Non-recourse models deny funding to

those with weak credit and naturally

select consumers that have good credit

and access to other credit facilities.

It is debatable whether a viable

financing market exists for non-elective

procedures. However, for providers

that are self-funding, it is essential for

those businesses to deploy the most

efficient and consumer-friendly collection

models. This is where payment plans

play a big role. Payment plans, deployed

with the proper collection methods,

policies, procedures, technical security

and compliance, can yield equally high

collection rates without the fees pursuant

to recourse and non-recourse lending. In

effect, the self-funding model powered

with payment plans replaces the lender

as an intermediary with technology and

improved business practices.

10 © 2017 InstaMed. All rights reserved.

Omnichannel Payments Are

Impacting Healthcare

Whether a baby boomer or millennial,

consumers want omnichannel options to

make their healthcare payments.

TRENDSin HEALTHCARE PAYMENTS

Sources

1 2015 McKinsey Consumer Health Insights Survey

This Isn’t About Millennials – Consumers

Across All Generations Want Payment

Convenience

Inaccurate generalizations on how

consumers want to pay their healthcare

payments persist within the industry

and indicate that consumers prefer one

channel for their healthcare payments.

For example, incorrect assumptions

are made when statements like “baby

boomers pay their bills by check” and

“only millennials are making payments

online” are used to make business

decisions for providers and payers

alike. The data tells a very different

story. Consumers want an omnichannel

payments experience regardless of their

demographic attributes, like age. An

omnichannel payment experience means

that consumers have multiple channels

to make payments with the freedom to

decide which channel they want to use.

What Are Consumers Demanding?

There is a new stakeholder in the

healthcare payments market –

consumers. As outlined in the previous

section, healthcare organizations

must find new ways to meet consumer

demands or face impacts to their

bottom line.

The first step to meeting consumer

demands is to understand consumer

expectations of the healthcare

payments process. On this point,

the data tells us that consumers do

not view healthcare payments as

different or distinct from payments

they make in other industries. When

surveyed, traits that consumers value

closely align between commercial

and healthcare industries. The traits

include giving great customer service,

delivering on expectations, making

life easier and offering great value.1

Put simply, consumers do not view

shopping online or using a ride-sharing

service as different from paying their

medical bill or health plan premium.

If consumers can have an up-to-the-

minute status on their pizza delivery,

they expect the same type of visibility

in healthcare.

Consumers do not view

healthcare payments as

different or distinct from

payments they make in

other industries.

© 2017 InstaMed. All rights reserved.11

Sources

2 Eighth Annual Billing Household Survey, Fiserv Inc., 2016

3 Consumer Healthcare Payments Survey 2016

4 Consumer Healthcare Payments Survey 2016

5 Consumer Healthcare Payments Survey 2016

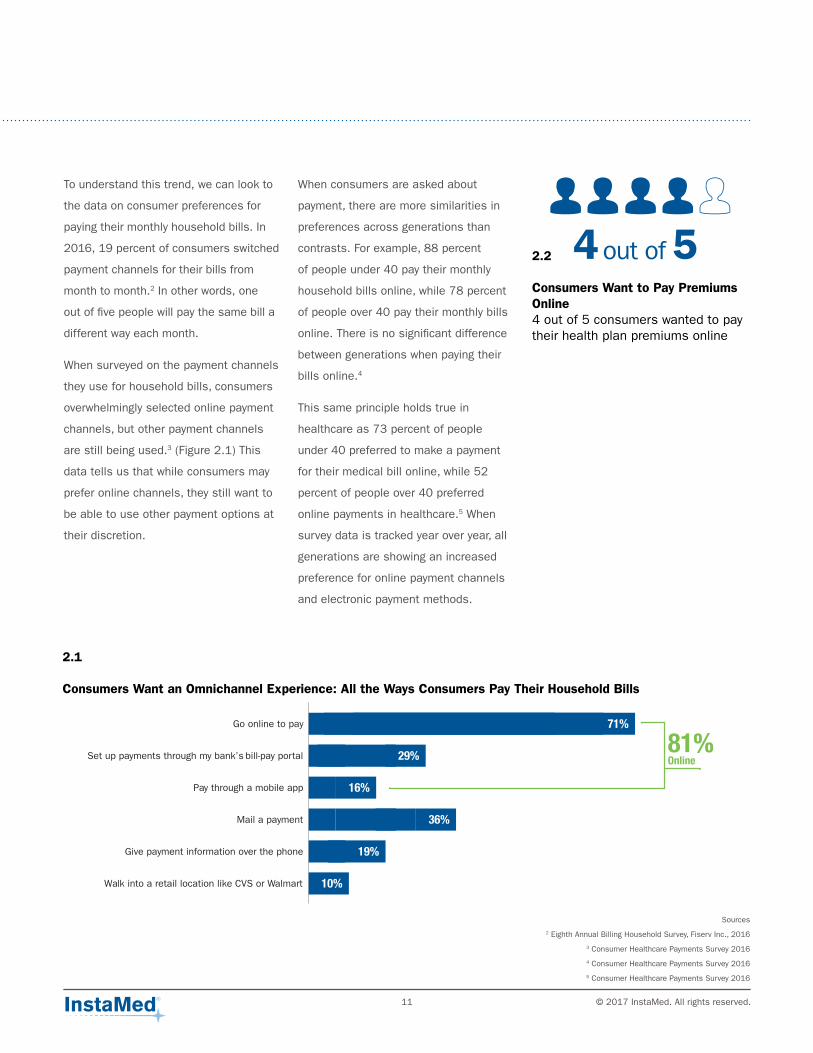

When consumers are asked about

payment, there are more similarities in

preferences across generations than

contrasts. For example, 88 percent

of people under 40 pay their monthly

household bills online, while 78 percent

of people over 40 pay their monthly bills

online. There is no significant difference

between generations when paying their

bills online.4

This same principle holds true in

healthcare as 73 percent of people

under 40 preferred to make a payment

for their medical bill online, while 52

percent of people over 40 preferred

online payments in healthcare.5 When

survey data is tracked year over year, all

generations are showing an increased

preference for online payment channels

and electronic payment methods.

Walk into a retail location like CVS or Walmart 10%

Give payment information over the phone 19%

Mail a payment 36%

Pay through a mobile app 16%

Set up payments through my bank’s bill-pay portal 29%

Go online to pay 71%

81%Online

2.2

Consumers Want to Pay Premiums Online 4 out of 5 consumers wanted to pay their health plan premiums online

2.1

Consumers Want an Omnichannel Experience: All the Ways Consumers Pay Their Household Bills

To understand this trend, we can look to

the data on consumer preferences for

paying their monthly household bills. In

2016, 19 percent of consumers switched

payment channels for their bills from

month to month.2 In other words, one

out of five people will pay the same bill a

different way each month.

When surveyed on the payment channels

they use for household bills, consumers

overwhelmingly selected online payment

channels, but other payment channels

are still being used.3 (Figure 2.1) This

data tells us that while consumers may

prefer online channels, they still want to

be able to use other payment options at

their discretion.

4 5

12 © 2017 InstaMed. All rights reserved.

Being Where Your Patients and

Members Are

The data for household bill payment

preferences demonstrates a need for a

comprehensive omnichannel approach.

However, there is a clear connection

between consumer preference and

payment channels that promote

convenience and simplicity. From 2010

to 2016, household bills paid by paper

check declined by 20 percent, while

electronic options increased. Bills paid

through online and automated options

increased by 10 percent, while card

payments doubled to 15 percent.6

The preference for online payment

channels holds true for healthcare

payments as well. More than half of

consumers prefer to pay their medical

bills through an online payment

channel, while almost 80 percent prefer

to pay their health plan premiums this

way.7 (Figure 2.2)

Online payments go beyond simply

collecting payments from a healthcare

organization’s website. There are

opportunities to accept payments

within online portals that consumers

already visit for payments or healthcare

information. In fact, 73 percent of

consumers want to pay all of their

healthcare bills in one place.8

Data from the InstaMed Network

confirms that consumers want to pay

from websites where they already go for

healthcare information as there was rapid

growth in those payment channels from

2013 to 2016: payments to providers

through a health plan’s website increased

527 percent or 84 percent year over year

(Figure 2.3), and payments from an online

patient portal increased 139 percent or

34 percent year over year. (Figure 2.4)

As consumers turn to their smartphones

for more of their daily activities,

healthcare payments must become an

integrated part of the mobile experience

as well. According to the Pew Research

Center, 77 percent of Americans own

smartphones up from just 35 percent

in Pew Research Center’s first survey

of smartphone ownership conducted in

2011.

When that data is broken out across

age ranges, smartphones are ubiquitous

as ownership is high across all age

brackets: 92 percent of consumers aged

18-29, 88 percent of consumers aged

30-49, 74 percent of consumers aged

50-64 and 42 percent of consumers

aged 65+. An “always connected” world

is no longer an idea – it’s here – and

healthcare needs to respond.

2.3

Consumers Want to Make Payments Through Health Plan Websites Payments to providers through a health plan’s website increased 527% or 84% year over year

2.4

Consumers Want Convenient Online Payment ChannelsPayments from an online patient portal increased 139% or 34% year over year

Health Plan Website

Online Patient Portal

2013 - 2016

527%increase

139%increase

Sources

6 Aite

7 Consumer Healthcare Payments Survey 2016

8 Consumer Healthcare Payments Survey 2016

© 2017 InstaMed. All rights reserved.13

According to research done by Google,

four in 10 smartphone owners turn to

their phones for finance activities. Data

from the InstaMed Network confirms

this shift to mobile as payments from

a mobile device have increased to 20

percent of all online payments in 2016,

which has doubled in three years. (Figure

2.5) In addition, 61 percent of consumers

reported having interest in using a new

mobile payment system such as Apple

Pay, Samsung Pay or Android Pay to make

a healthcare payment.9 (Figure 2.6)

2.5

Expanding Use of Mobile Payments in Healthcare Payments from a mobile device have increased to 20% of all online payments in 2016

%

2.6

Consumer Interest in Mobile Payment Systems for Healthcare Bills 61% of consumers reported having interest in using a new mobile payment system such as Apple Pay, Samsung Pay or Android Pay to make a healthcare payment

How Consumers Prefer to Pay –

Electronic Payment Methods

One common denominator for consumer

preference seems to be the preference

to leverage electronic payment methods.

When given the option of various payment

methods to pay healthcare bills in 2016,

68 percent of consumers indicated that

they preferred to pay with an electronic

payment method, including payment

cards, directly from a bank account

(ACH) and digital wallet.10 86 percent

of consumers prefer an electronic

payment method when making premium

payments to a health plan.11 Data from

the InstaMed Network confirms this as

payment card transactions increased 120

percent, or 30 percent year over year from

2013 to 2016.

61

18%

11%

9%

5%

20%2016

2015

2014

2013

2012

Sources

9 Consumer Healthcare Payments Survey 2016

10 Consumer Healthcare Payments Survey 2016

11 Consumer Healthcare Payments Survey 2016

77 percent of Americans

own smartphones up

from just 35 percent in

Pew Research Center’s

first survey of smartphone

ownership conducted

in 2011.

14 © 2017 InstaMed. All rights reserved.

How Consumers Prefer to Pay –

Automated Payment Channels

The ability to leverage electronic payment

methods in healthcare offers consumers

the convenience and accessibility that

they already find in other industries.

For healthcare organizations, electronic

payment methods streamline workflows

that may depend on paper and manual

processes. Yet, there is an added

benefit of electronic payment methods

that healthcare is just starting to realize

the rewards of – automated payment

channels.

2.8

Increase in Automated Payment PlansAutomated payment plans increased by 272%, growing by 55% on average each year

There are multiple benefits of paying

electronically for consumers. First is

the instant satisfaction of knowing

that the payment is complete and not

having to wait weeks to see an updated

balance as when mailing a paper check.

Secondly, electronic payments can

employ additional layers of security when

done correctly. Thirdly, consumers can

have the added convenience of saving

their electronic payment method on

file for future payments. The capability

of a digital wallet has gone from an

innovative ecommerce feature to a de

facto expectation very rapidly. Other

industries are increasingly offering digital

wallets to their customers as a quick way

to pay without having to enter payment

information for every transaction.

There are countless examples of digital

wallets in consumer-focused industries

– look at the ecommerce shopping

experience with any major retailer, and

there will be the ability to save payment

methods to create a digital wallet.

Data from the InstaMed Network

confirms that consumers want digital

wallets for healthcare payments too as

the total number of cards saved on file

from 2013 to 2016 increased by 217

percent or an average growth of 47

percent year over year. (Figure 2.7)

2016

2013

2.7

Shift to Digital WalletsThe total number of cards saved on file increased by 217% or an average growth of 47% year over year

Automated payment channels leverage

electronic payment methods saved on

file to automatically collect a payment.

For example, if a consumer wants to

pay down a larger medical bill over time,

the provider can set up an automated

payment plan to collect in regular

intervals, such as $100 a month to pay a

$1,000 balance over 10 months.

The capability of a digital

wallet has gone from an

innovative ecommerce

feature to a de facto

expectation very rapidly.

217%

© 2017 InstaMed. All rights reserved.15

Automatic payments guarantee revenue

that might otherwise go uncollected

for healthcare organizations. Payers

are uniquely positioned to leverage

automated payments to collect

health plan premiums directly from

their members, which reduce plan

terminations due to missing payments.

Consumers indicated that they want to

pay this way as 58 percent preferred

the option to schedule an automatic

deduction to pay their premiums.12 (Figure

2.9)

Data from the InstaMed Network shows

that consumers are increasingly adopting

the option to leverage automated

payments in healthcare as the total

number of automated payments on the

InstaMed Network is growing at a rate of

111 percent per year. (Figure 2.10)

2.9

Consumers Want Automated Payments for Premiums 58% of consumers preferred the option to schedule an automatic deduction to pay their premiums

Data from the InstaMed Network shows

that payment plans are a growing

consumer payment channel as the total

number of automated payment plans

on the InstaMed Network from 2013 to

2016 increased by 272 percent, growing

by 55 percent on average each year.

(Figure 2.8)

Beyond payment plans, healthcare

organizations can leverage automated

payments for smaller balances by saving

a card on file to automatically collect as

soon as a balance is due. Consumers

are accustomed to payment experiences

like this outside of healthcare. For

example, consumers know that they will

have to present a payment method upon

checking into a hotel, and that they will

be charged upon checkout. Healthcare

can look to these best practices to avoid

poor accounts receivable metrics that

often result in financial losses.

%582.10

Automated Payments Are Rapidly Increasing The total number of automated payments is growing at a rate of 111% year over year

%111

Sources

12 Consumer Healthcare Payments Survey 2016

Automatic payments

guarantee revenue that

might otherwise go

uncollected for healthcare

organizations.

16 © 2017 InstaMed. All rights reserved.

The True Costs of Paper in Healthcare

Healthcare is one of the last industries

where the majority of information

is primarily transmitted via paper,

including the information associated

with the payment process: EOPs,

EOBs, mailed paper statements, paper

check payments, etc.

Overall, the ability to support these

paper-based transactions requires

manual processes that cost the

industry significant resources

– consider that 16 percent of

total healthcare spending is on

administrative costs.1

The costs are not just monetary either

as 21 percent of physicians’ time

is spent on non-clinical paperwork.2

Additionally, 87 percent of physicians

say paperwork and administration are

a key source of staff burnout.3

However, providers alone do not suffer

the burdens of paper clogging up their

time and resources. These costs are

felt across all healthcare constituents.

Paper Is Hurting All Healthcare

StakeholdersProviders, payers and consumers are all

experiencing the costly inefficiency of paper in

healthcare payments.

TRENDSin HEALTHCARE PAYMENTS

Sources

1 McKinsey

2 2016 Biennal Physicians Survey

3 Medscape

3.1

Almost All Providers Are Receiving Paper Payments From Payers 88% of providers reported that they received paper checks and EOPs from one or more of their payers

88

Healthcare is one of the

last industries where the

majority of information is

transmitted via paper.

© 2017 InstaMed. All rights reserved.17

The Payer and Provider Paper

Disconnect

Every year, three billion transactions

take place via paper-based and manual

processes between providers and

payers.4 In fact, 88 percent of providers

reported that they received paper checks

and EOPs from one or more of their

payers. (Figure 3.1) With that same group

of providers, 85 percent said that they

preferred to receive payer payments via

3.2

Providers Prefer ERA/EFT Significantly Over Paper Payments 85% said that they preferred to receive payer payments via ERA/EFT

85%

13%

2%

Sources

4 2016 CAQH Index Report

5 Provider Healthcare Payments Survey 2016

6 Provider Healthcare Payments Survey 2016

7 2016 CAQH Index Report

8 Provider Healthcare Payments Survey 2016

electronic remittance advice (ERA) and

electronic funds transfer (EFT).5 Yet, only

13 percent of providers said they prefer

payments in the form of paper checks

and two percent preferred virtual card

payments from payers.6 (Figure 3.2)

Providers are required to navigate

paper processes with both payers and

consumers to get paid. Therefore, the

costs and time to process a paper claim,

paper check or paper statement directly

impact their bottom line. The average

time spent on processing a manual

paper-based transaction is eight minutes,

but can be as long as 30 minutes and

costs three dollars more when compared

to electronic transactions.7

This may be why so many providers

reported that they prefer electronic

transactions over paper. In addition to

the 85 percent of providers who prefer

EFT payments from payers, 58 percent

of the providers surveyed preferred

an electronic payment method from

consumers.8

The average time spent

on processing a manual

paper-based transaction

is eight minutes, but can

be as long as 30 minutes

and costs three dollars

more when compared to

electronic transactions.

18 © 2017 InstaMed. All rights reserved.

Untapped Potential of Electronic

Transactions

If electronic transactions were to become

the norm in the industry over today’s

paper processes, the potential annual

savings would be $9.4 billion in overall

administrative costs.9

Put simply, electronic options for

payments require much fewer resources

to complete a transaction when

compared to paper transactions. For

example, an automated email notification

can be sent to a consumer with a link

to pay online. If the consumer makes

a payment that way, there is no staff

intervention needed to collect the

payment.

The industry could further lower

administrative costs by $24 billion to

$48 billion annually from productivity

gains made through increased

automation and self-service.10

The Healthcare Industry Is Prime to

Go Paperless

It appears that many in the industry are

ready for the change from a paper-heavy

payment market to realize the potential

of electronic transactions – such as the

27 percent of payers who said that cost

reduction strategies were their top priority

for 2017.11

Sources

9 2016 CAQH Index Report

10 McKinsey

11 Payer Healthcare Payments Survey 2016

12 Consumer Healthcare Payments Survey 2016

Some forward-thinking payers are working

to close this disconnect between how

providers want to get paid and how they

actually get paid by payers. Data from

the InstaMed Network confirms this

trend as ERA/EFT payments increased

106 percent from 2013 to 2016, with a

27 percent annual growth rate each year.

(Figure 3.3)

If electronic transactions

were to become the norm

in the industry over today’s

paper processes, the

potential savings would be

$9.4 billion.

3.3

ERA/EFT Payment Growth on the InstaMed Network ERA/EFT payments increased 106% with a 27% annual growth rate each year

2013 2016106%

increase

As the role of consumers continues

to grow in the industry, payers and

providers will need to meet their

expectations of an electronic payment

experience. Right now, consumers

expect Amazon-like experiences, but

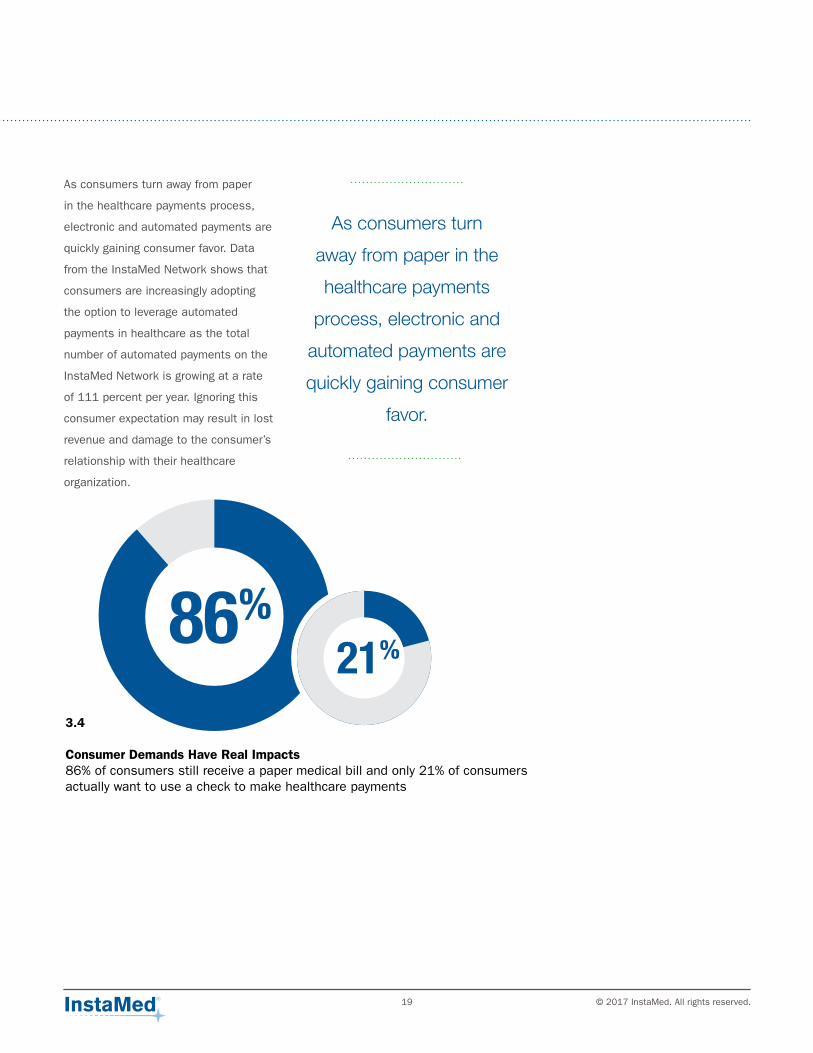

86 percent of consumers still receive

a paper medical bill. Within that same

group of consumers, only 21 percent of

consumers actually want to use checks

to make healthcare payments.12 (Figure

3.4)

© 2017 InstaMed. All rights reserved.19

3.4

Consumer Demands Have Real Impacts 86% of consumers still receive a paper medical bill and only 21% of consumers actually want to use a check to make healthcare payments

86%21%

As consumers turn away from paper

in the healthcare payments process,

electronic and automated payments are

quickly gaining consumer favor. Data

from the InstaMed Network shows that

consumers are increasingly adopting

the option to leverage automated

payments in healthcare as the total

number of automated payments on the

InstaMed Network is growing at a rate

of 111 percent per year. Ignoring this

consumer expectation may result in lost

revenue and damage to the consumer’s

relationship with their healthcare

organization.

As consumers turn

away from paper in the

healthcare payments

process, electronic and

automated payments are

quickly gaining consumer

favor.

20 © 2017 InstaMed. All rights reserved.

Healthcare is a prime target for data breaches.

TRENDSin HEALTHCARE PAYMENTS

Healthcare Data Is a Target

The healthcare payments market

handles a massive amount of

information on a daily basis that

includes such highly sensitive items

as social security numbers and

payment data. Many healthcare

organizations rely on paper-based

processes or legacy technology

systems to transmit this data, which

can easily be intercepted by or

exposed to hackers and thieves.

Any organizations unsure if their

data is at risk should assume the

worst. 2016 saw more healthcare

data breaches than any other year on

record.1 In fact in 2016, there was

roughly one health data breach per

day, affecting more than 27 million

total patient records.2

The risk is not limited to data

breaches or stolen information.

Ransomware is a growing threat in

the healthcare industry that cannot be

ignored as it increased in healthcare

by 36 percent in 2016.3 Ransomware

refers to when a type of malware

freezes an organization’s entire

system until a ransom is paid to the

Healthcare Data Is Under Attack

Sources

1 Symantec

2 Protenus

3 Symantec

4 Symantec

2016 saw more healthcare

data breaches than any

other year on record.

hackers. The threat will continue

to grow in the coming years as the

ransom amounts climb – the average

ransom rose 266 percent in 2016

with the average ransom amount

at $1,077 per victim, from $294 in

2015.4

True Costs of Unsecure Data

Once a healthcare organization’s

data is exposed, a figurative dam has

been broken and the data is available

to any hacker or thief to put on the

black market for sale to the highest

bidder. At present time, there is no

way to make exposed data secure

again or to take it off of the black

market.

© 2017 InstaMed. All rights reserved.21

Financially, data breaches are estimated

to cost the healthcare industry $6.2

billion annually.5 However, the unseen

costs of an exposure reverberate

through the industry at an alarming

rate as headlines quickly announce the

breach and consumers panic over the

status of their personal information

– damaging the organization’s brand

and losing the trust of their patients or

members.

Security Concerns in the Industry

The impact of unsecure data to

an organization’s reputation and

bottom line have not gone unnoticed

in the industry. In fact, 90 percent

of providers reported that payment

security is very important when

collecting patient payments.6

(Figure 4.1) These growing concerns

regarding payment security will only

be compounded as organizations

attempt to keep up with the demands

of consumers by adding new payment

options such as automated payments

and online payment portals.

As discussed in the previous

sections of this report, the ability to

meet the demands of consumers will

be critical to the future of healthcare

payments. However, the ability to

make those payments secure must

be equally as important as making

the experience more consumer-

friendly. More than half of consumers

surveyed reported having significant

concerns regarding the security of

making online payments for both

their medical bills and health plan

premiums.7 (Figure 4.2)

4.1

Payment Security Is on the Minds of Providers 90% of providers reported that payment security is very important when collecting patient payments

%90

Sources

5 Ponemon

6 Provider Healthcare Payments Survey 2016

7 Consumer Healthcare Payments Survey 2016

4.2

Payment Security Is on the Minds of Consumers More than half of consumers reported that having significant concerns regarding the security of making online payments for medical bills and health plan premiums

%59

22 © 2017 InstaMed. All rights reserved.

Source

8 Accenture

9 Accenture

10 Harvard Business Review

11 Protenus

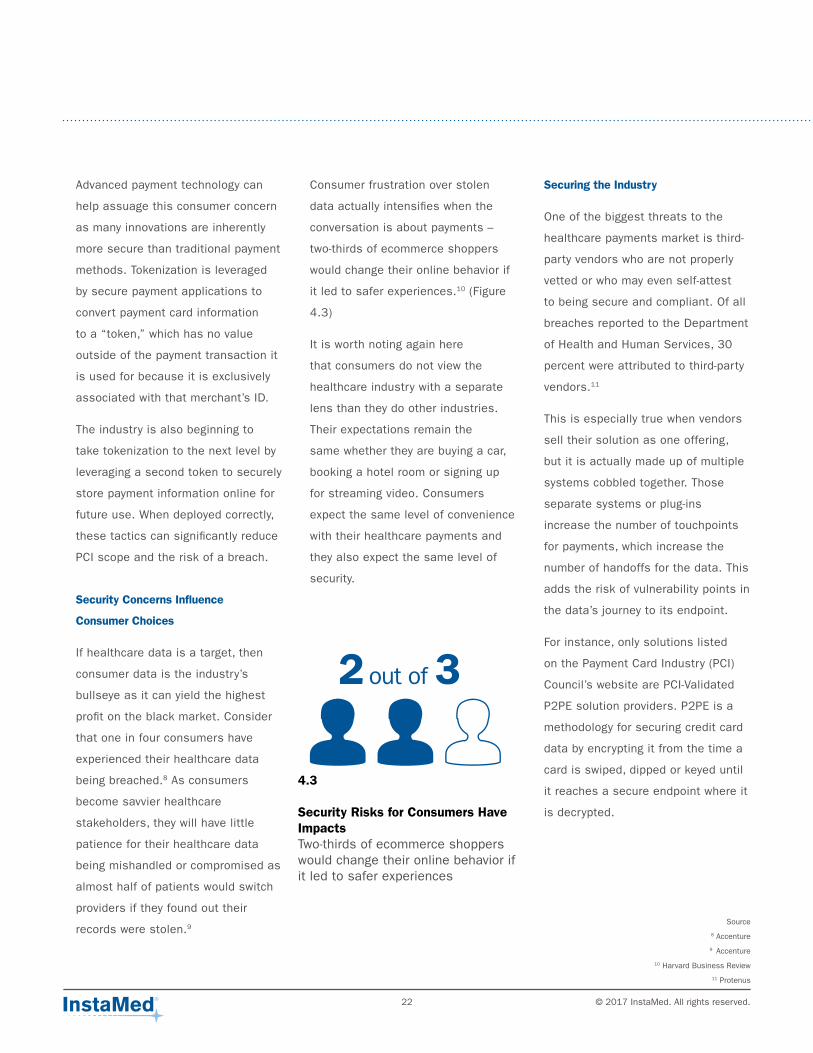

Consumer frustration over stolen

data actually intensifies when the

conversation is about payments –

two-thirds of ecommerce shoppers

would change their online behavior if

it led to safer experiences.10 (Figure

4.3)

It is worth noting again here

that consumers do not view the

healthcare industry with a separate

lens than they do other industries.

Their expectations remain the

same whether they are buying a car,

booking a hotel room or signing up

for streaming video. Consumers

expect the same level of convenience

with their healthcare payments and

they also expect the same level of

security.

Advanced payment technology can

help assuage this consumer concern

as many innovations are inherently

more secure than traditional payment

methods. Tokenization is leveraged

by secure payment applications to

convert payment card information

to a “token,” which has no value

outside of the payment transaction it

is used for because it is exclusively

associated with that merchant’s ID.

The industry is also beginning to

take tokenization to the next level by

leveraging a second token to securely

store payment information online for

future use. When deployed correctly,

these tactics can significantly reduce

PCI scope and the risk of a breach.

Security Concerns Influence

Consumer Choices

If healthcare data is a target, then

consumer data is the industry’s

bullseye as it can yield the highest

profit on the black market. Consider

that one in four consumers have

experienced their healthcare data

being breached.8 As consumers

become savvier healthcare

stakeholders, they will have little

patience for their healthcare data

being mishandled or compromised as

almost half of patients would switch

providers if they found out their

records were stolen.9

4.3

Security Risks for Consumers Have ImpactsTwo-thirds of ecommerce shoppers would change their online behavior if it led to safer experiences

Securing the Industry

One of the biggest threats to the

healthcare payments market is third-

party vendors who are not properly

vetted or who may even self-attest

to being secure and compliant. Of all

breaches reported to the Department

of Health and Human Services, 30

percent were attributed to third-party

vendors.11

This is especially true when vendors

sell their solution as one offering,

but it is actually made up of multiple

systems cobbled together. Those

separate systems or plug-ins

increase the number of touchpoints

for payments, which increase the

number of handoffs for the data. This

adds the risk of vulnerability points in

the data’s journey to its endpoint.

For instance, only solutions listed

on the Payment Card Industry (PCI)

Council’s website are PCI-Validated

P2PE solution providers. P2PE is a

methodology for securing credit card

data by encrypting it from the time a

card is swiped, dipped or keyed until

it reaches a secure endpoint where it

is decrypted.

© 2017 InstaMed. All rights reserved.23

These compliance requirements need

to be taken seriously by healthcare

organizations and the third-party

organizations to which they entrust

their payment data. By meeting these

standards, organizations will ensure

that their data is secure and reduce

the risk of a breach.

By meeting industry

standards, organizations

will ensure that their data

is secure and reduce the

risk of a breach.

To be a PCI-Validated P2PE Solution

Provider, a vendor must complete

the detailed security requirements

and testing procedures outlined

by the PCI Council to ensure that

their solutions meet the necessary

requirements to protect payment card

data.

EMV, or Europay, MasterCard and

Visa, is another area where third-

party certification is key. EMV is

the global standard for chip-based

debit and credit card transactions.

In October 2015, the major

processing banks implemented a

shift that transferred fraud liability to

merchants who process fraudulent

chip card transactions, unless they

use EMV-capable point of sale (POS).

However, for EMV to work, payment

vendors also have to be certified with

all major card brands for EMV.

This is an expensive yet necessary

process that many vendors claim they

can do, but cannot due to the many

hurdles to complete certification with

processors, card brands and payment

card devices. In order to avoid fraud

liability, merchants across the U.S.

must upgrade their point-of-sale

devices to accept EMV transactions.

24 © 2017 InstaMed. All rights reserved.

The 2016 industry trends have had a significant impact on healthcare providers.

To better understand the experiences of providers, InstaMed commissioned the

Provider Healthcare Payments Survey 2016, conducted by LHK Partners. The

nationwide survey participants ranged from solo practitioners to large health

systems. The following are the key data points from the survey:

ProviderSentiment

Summary

of providersreport it takes one month or longer to

collect from patients.

%73

© 2017 InstaMed. All rights reserved.25

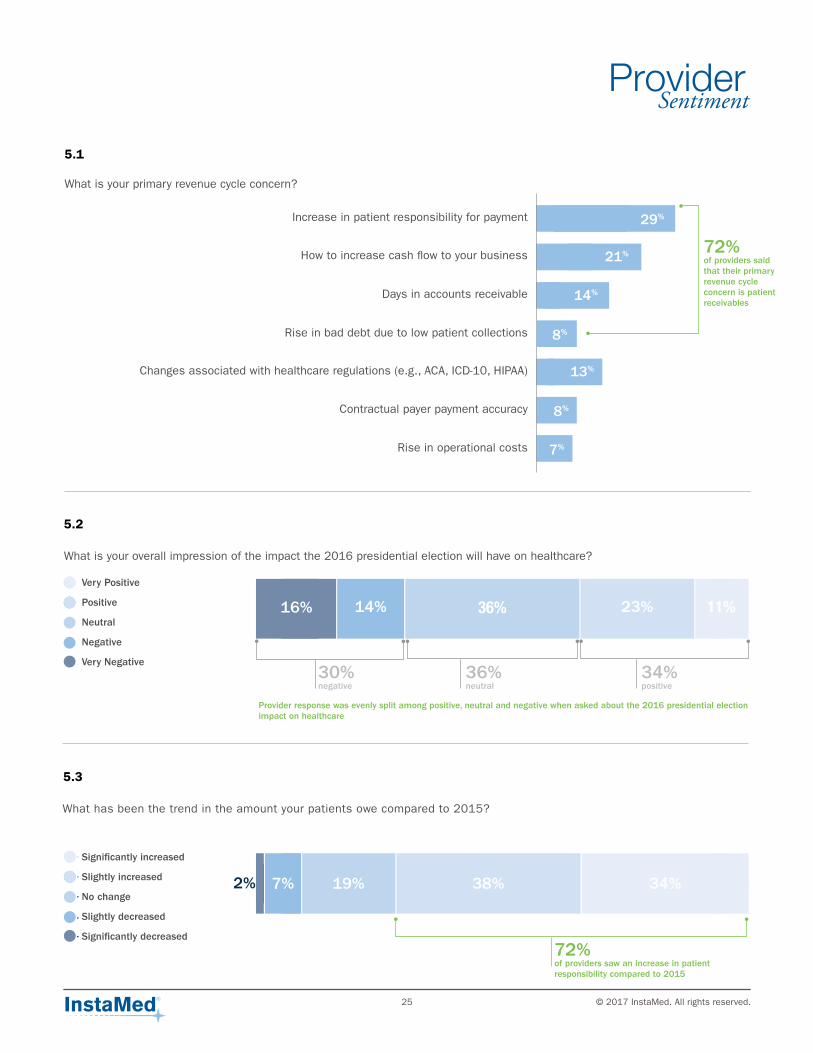

What is your primary revenue cycle concern?

What is your overall impression of the impact the 2016 presidential election will have on healthcare?

What has been the trend in the amount your patients owe compared to 2015?

5.1

5.2

5.3

ProviderSentiment

29%

21%

14%

13%

8%

7%

Increase in patient responsibility for payment

How to increase cash flow to your business

Days in accounts receivable

Changes associated with healthcare regulations (e.g., ACA, ICD-10, HIPAA)

Contractual payer payment accuracy

Rise in operational costs

19% 38% 34%

72% of providers saw an increase in patient responsibility compared to 2015

2% 7%

Significantly increased

Slightly increased

No change

Slightly decreased

Significantly decreased

Provider response was evenly split among positive, neutral and negative when asked about the 2016 presidential election impact on healthcare

Very Positive

Positive

Neutral

Negative

Very Negative

14% 36% 23%

30% negative

16% 11%

34% positive

36% neutral

8%Rise in bad debt due to low patient collections

72% of providers said that their primary revenue cycle concern is patient receivables

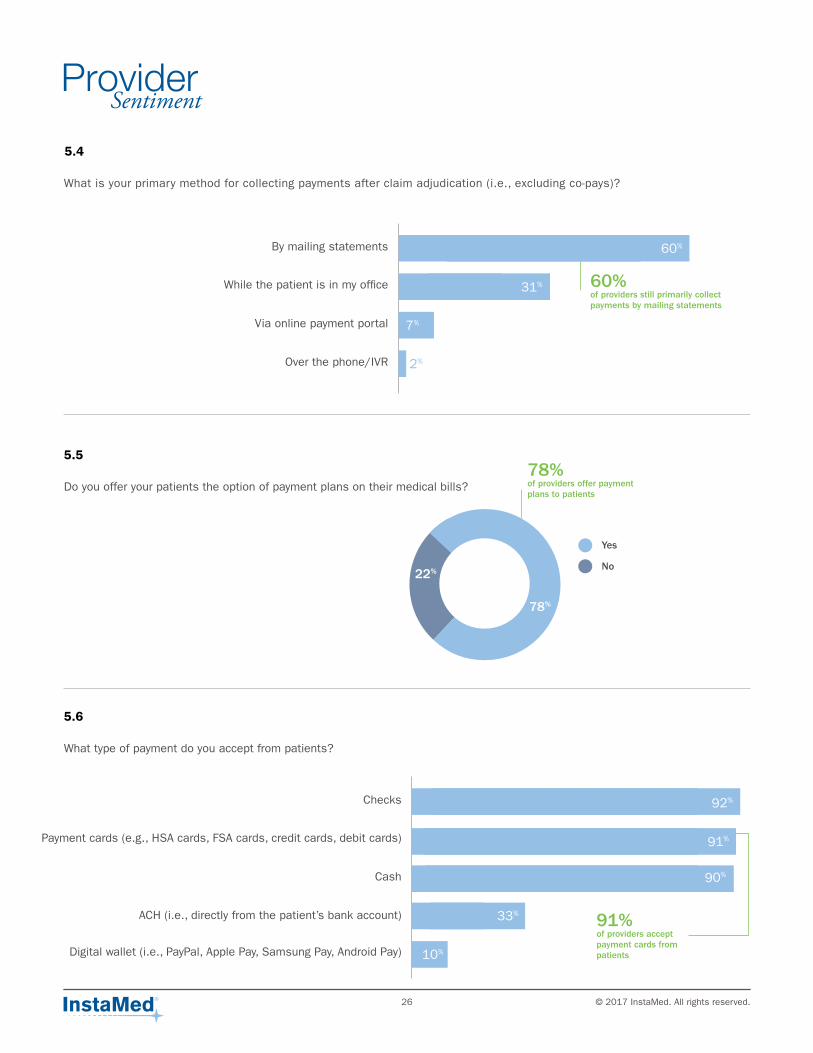

26 © 2017 InstaMed. All rights reserved.

Do you offer your patients the option of payment plans on their medical bills?

What is your primary method for collecting payments after claim adjudication (i.e., excluding co-pays)?

ProviderSentiment

5.4

5.5

What type of payment do you accept from patients?

5.6

60%

31%

7%

2%

By mailing statements

While the patient is in my office

Via online payment portal

Over the phone/IVR

78%

22%

Yes

No

Checks

Payment cards (e.g., HSA cards, FSA cards, credit cards, debit cards)

Cash

ACH (i.e., directly from the patient’s bank account)

Digital wallet (i.e., PayPal, Apple Pay, Samsung Pay, Android Pay)

33%

10%

90%

92%

91%

60% of providers still primarily collect payments by mailing statements

78% of providers offer payment plans to patients

91% of providers accept payment cards from patients

© 2017 InstaMed. All rights reserved.27

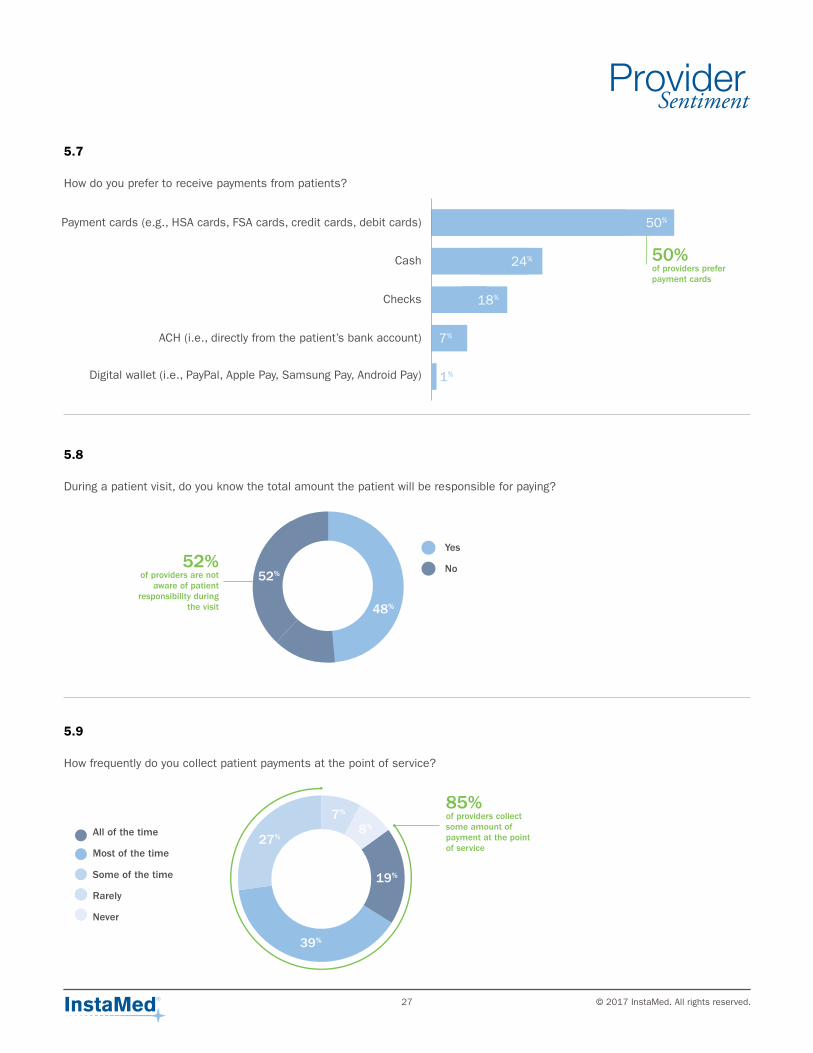

How do you prefer to receive payments from patients?

ProviderSentiment

5.7

How frequently do you collect patient payments at the point of service?

5.9

24%

18%

7%

1%

Payment cards (e.g., HSA cards, FSA cards, credit cards, debit cards)

Cash

Checks

ACH (i.e., directly from the patient’s bank account)

50%

Digital wallet (i.e., PayPal, Apple Pay, Samsung Pay, Android Pay)

During a patient visit, do you know the total amount the patient will be responsible for paying?

5.8

27%

39%

7%

8%

19%

All of the time

Most of the time

Some of the time

Rarely

Never

50% of providers prefer payment cards

52% of providers are not

aware of patient responsibility during

the visit 48%

52%

Yes

No

85% of providers collect some amount of payment at the point of service

28 © 2017 InstaMed. All rights reserved.

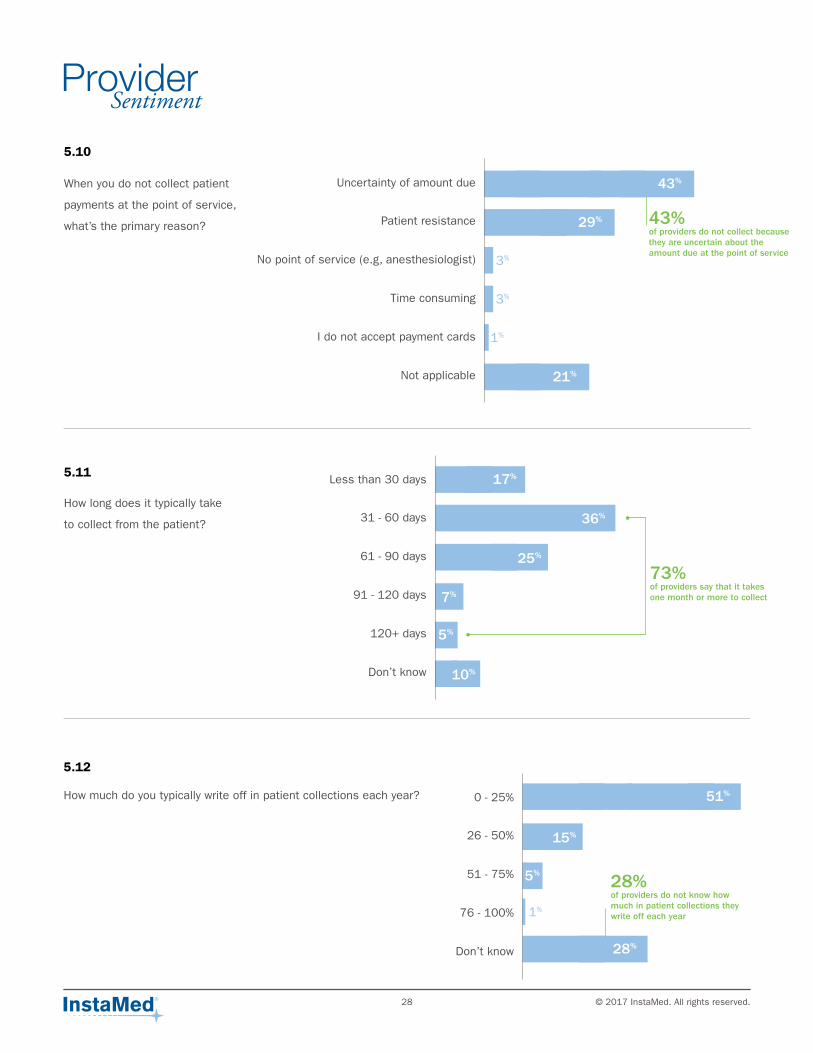

When you do not collect patient

payments at the point of service,

what’s the primary reason?

How long does it typically take

to collect from the patient?

ProviderSentiment

5.10

5.11

29%

Uncertainty of amount due

Patient resistance

No point of service (e.g, anesthesiologist)

Time consuming

I do not accept payment cards

Not applicable

43%

21%

1%

3%

3%

25%

Less than 30 days

31 - 60 days

61 - 90 days

91 - 120 days

120+ days

Don’t know

28%

0 - 25%

26 - 50%

51 - 75%

76 - 100%

Don’t know

1%

How much do you typically write off in patient collections each year?

5.12

17%

36%

7%

5%

10%

51%

15%

5%

43% of providers do not collect because they are uncertain about the amount due at the point of service

73% of providers say that it takes one month or more to collect

28% of providers do not know how much in patient collections they write off each year

© 2017 InstaMed. All rights reserved.29

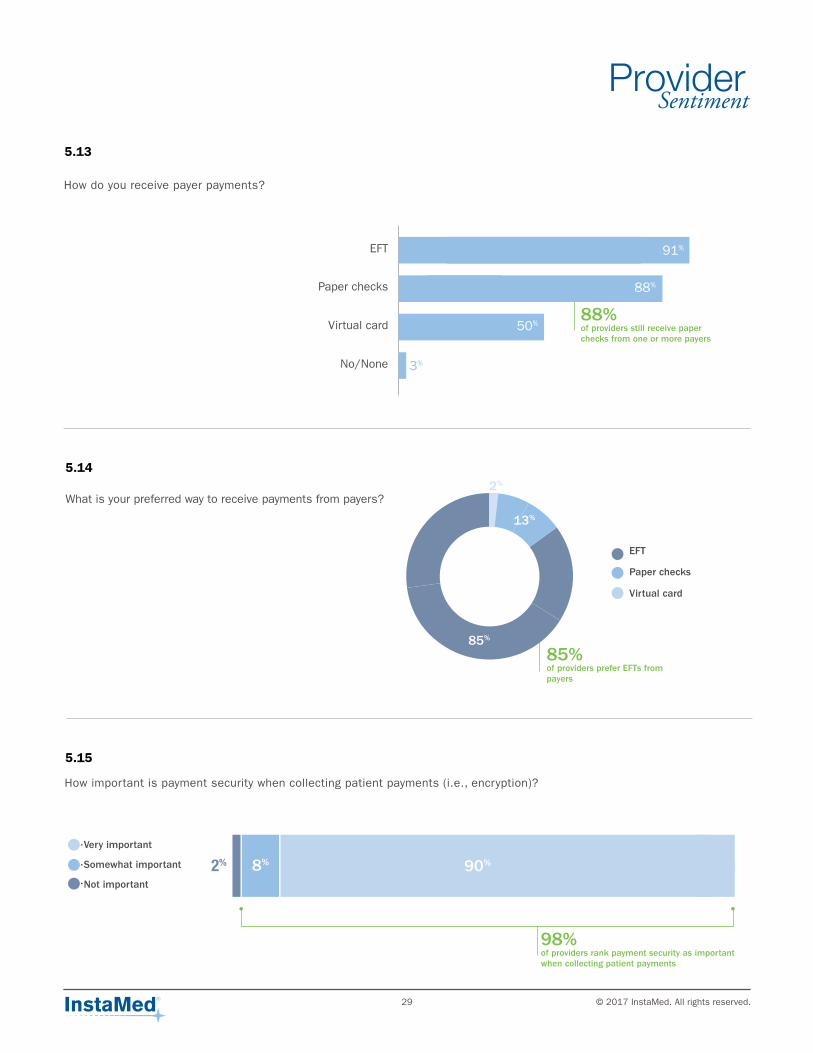

5.13

What is your preferred way to receive payments from payers?

5.14

How important is payment security when collecting patient payments (i.e., encryption)?

5.15

Very important

Somewhat important

Not important

EFT

Paper checks

Virtual card

85%

2%

13%

90%2% 8%

98% of providers rank payment security as important when collecting patient payments

How do you receive payer payments?

91%

88%

50%

3%

EFT

Paper checks

Virtual card

No/None

88% of providers still receive paper checks from one or more payers

85% of providers prefer EFTs from payers

ProviderSentiment

30 © 2017 InstaMed. All rights reserved.

PayerSentiment

Healthcare payers were also greatly impacted by the healthcare payment trends

in 2016. To better understand the experiences of payers, InstaMed commissioned

the Payer Healthcare Payments Survey 2016, conducted by LHK Partners. The

nationwide survey participants included national and regional payers, third-party

administrators (TPA) and Blues plans. The following are the key data points from the

survey:

Summary

of payers

%40rank direct-to-consumer solutions as their

top priority in 2017.

© 2017 InstaMed. All rights reserved.31

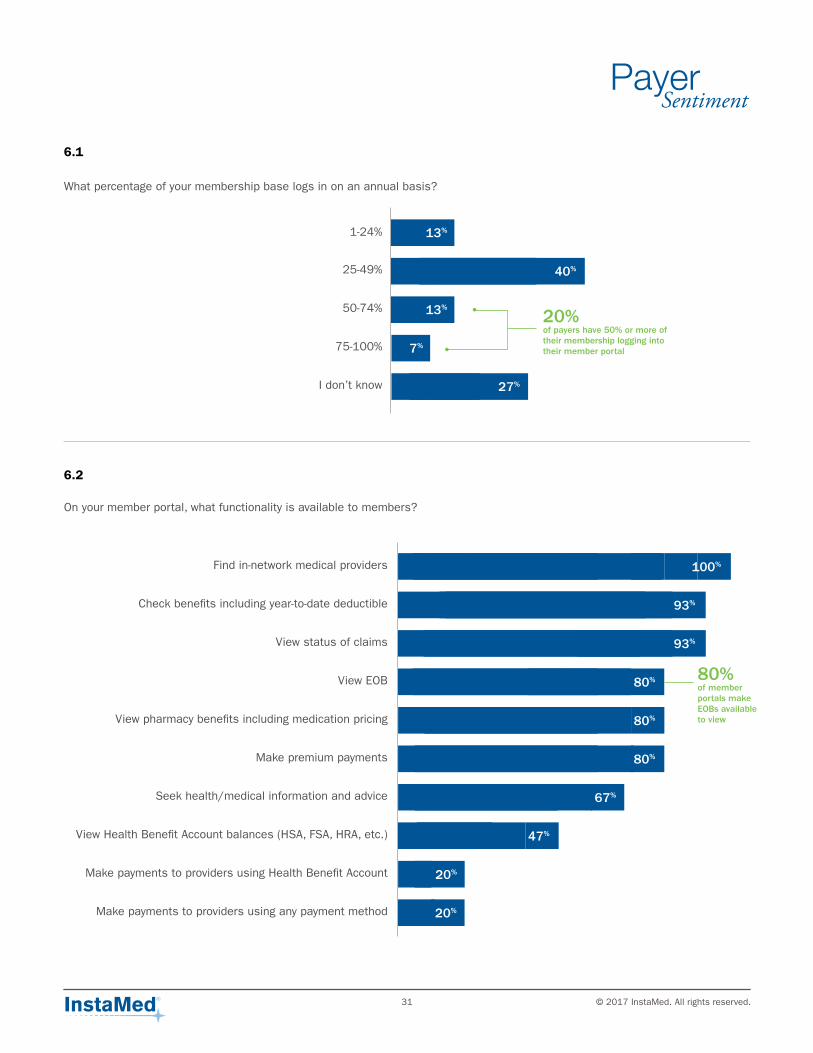

On your member portal, what functionality is available to members?

6.1

6.2

What percentage of your membership base logs in on an annual basis?

13%1-24%

40%

13%

7%

27%

25-49%

50-74%

75-100%

I don’t know

Seek health/medical information and advice

100%

93%

93%

80%

80%

80%

67%

47%

20%

20%

View Health Benefit Account balances (HSA, FSA, HRA, etc.)

Make payments to providers using Health Benefit Account

Make payments to providers using any payment method

View status of claims

View EOB

View pharmacy benefits including medication pricing

Make premium payments

Find in-network medical providers

Check benefits including year-to-date deductible

20% of payers have 50% or more of their membership logging into their member portal

80% of member portals make EOBs available to view

PayerSentiment

32 © 2017 InstaMed. All rights reserved.

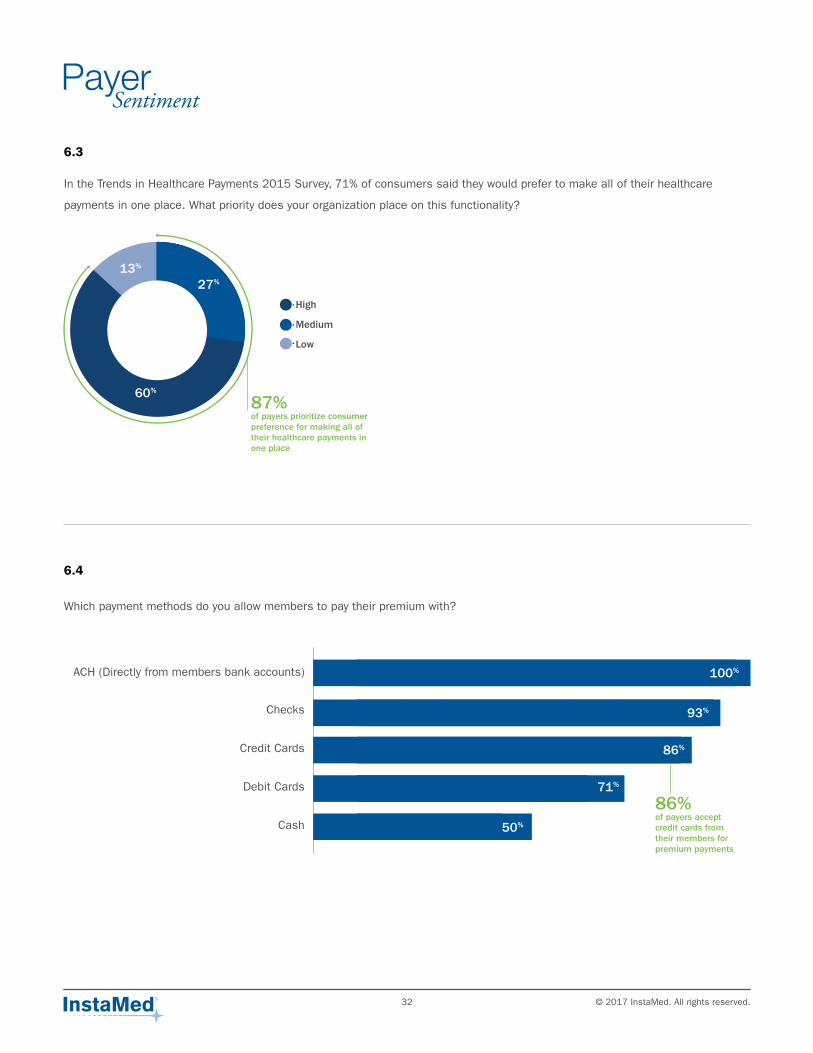

In the Trends in Healthcare Payments 2015 Survey, 71% of consumers said they would prefer to make all of their healthcare

payments in one place. What priority does your organization place on this functionality?

Which payment methods do you allow members to pay their premium with?

6.3

6.4

High

Medium

Low

60%

13%

27%

87% of payers prioritize consumer preference for making all of their healthcare payments in one place

ACH (Directly from members bank accounts)

Checks

Credit Cards

Debit Cards

Cash 50%

86%

71%

93%

100%

86% of payers accept credit cards from their members for premium payments

PayerSentiment

© 2017 InstaMed. All rights reserved.33

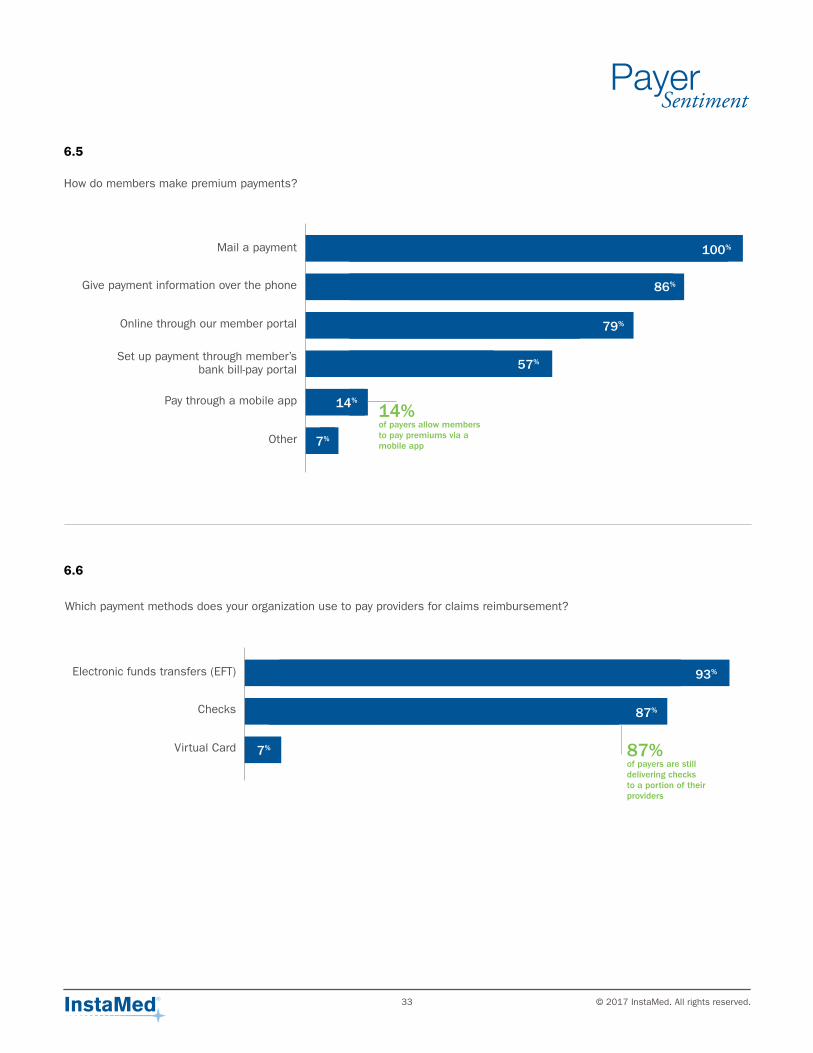

How do members make premium payments?

Which payment methods does your organization use to pay providers for claims reimbursement?

PayerSentiment

6.5

6.6

Mail a payment

Give payment information over the phone

Online through our member portal

Set up payment through member’s bank bill-pay portal

Pay through a mobile app

57%

86%

79%

100%

Other

14%

7%

14% of payers allow members to pay premiums via a mobile app

Electronic funds transfers (EFT)

Checks

Virtual Card

87%

7%

93%

87% of payers are still delivering checks to a portion of their providers

34 © 2017 InstaMed. All rights reserved.

PayerSentiment

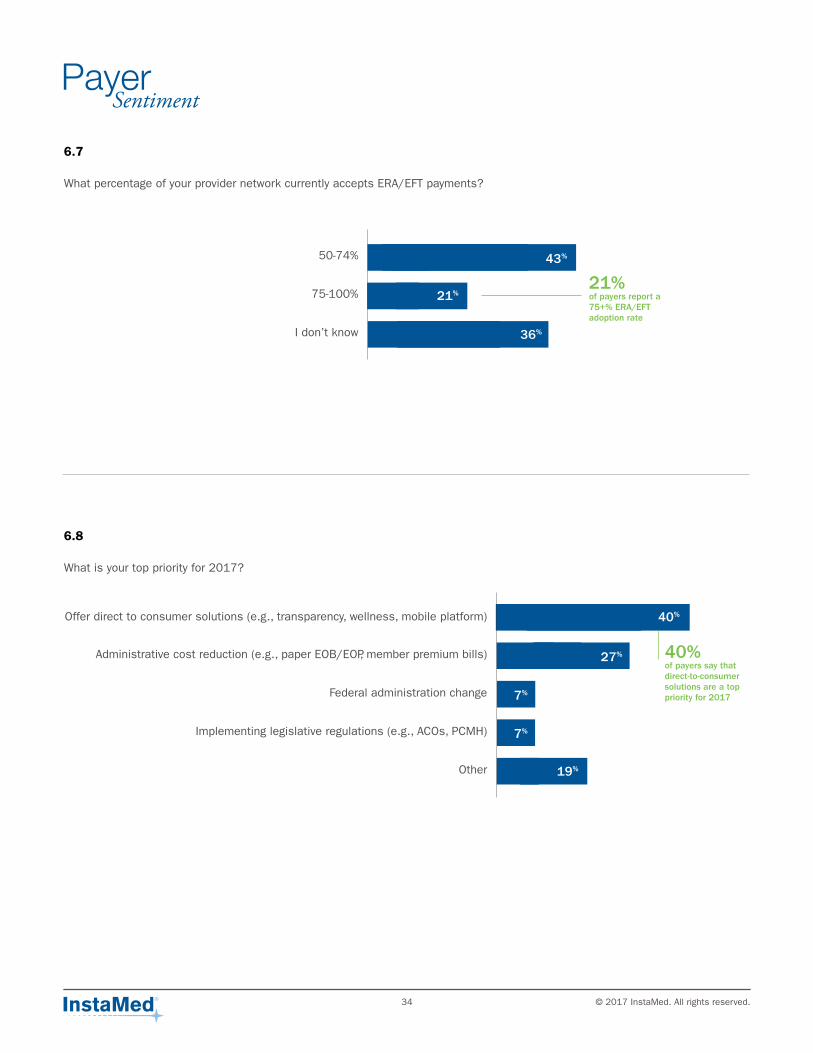

What percentage of your provider network currently accepts ERA/EFT payments?

6.7

What is your top priority for 2017?

6.8

Offer direct to consumer solutions (e.g., transparency, wellness, mobile platform)

Administrative cost reduction (e.g., paper EOB/EOP, member premium bills)

Federal administration change

Implementing legislative regulations (e.g., ACOs, PCMH)

Other 19%

7%

7%

27%

40%

50-74%

75-100%

I don’t know 36%

21%

43%

21% of payers report a 75+% ERA/EFT adoption rate

40% of payers say that direct-to-consumer solutions are a top priority for 2017

© 2017 InstaMed. All rights reserved.35

36 © 2017 InstaMed. All rights reserved.

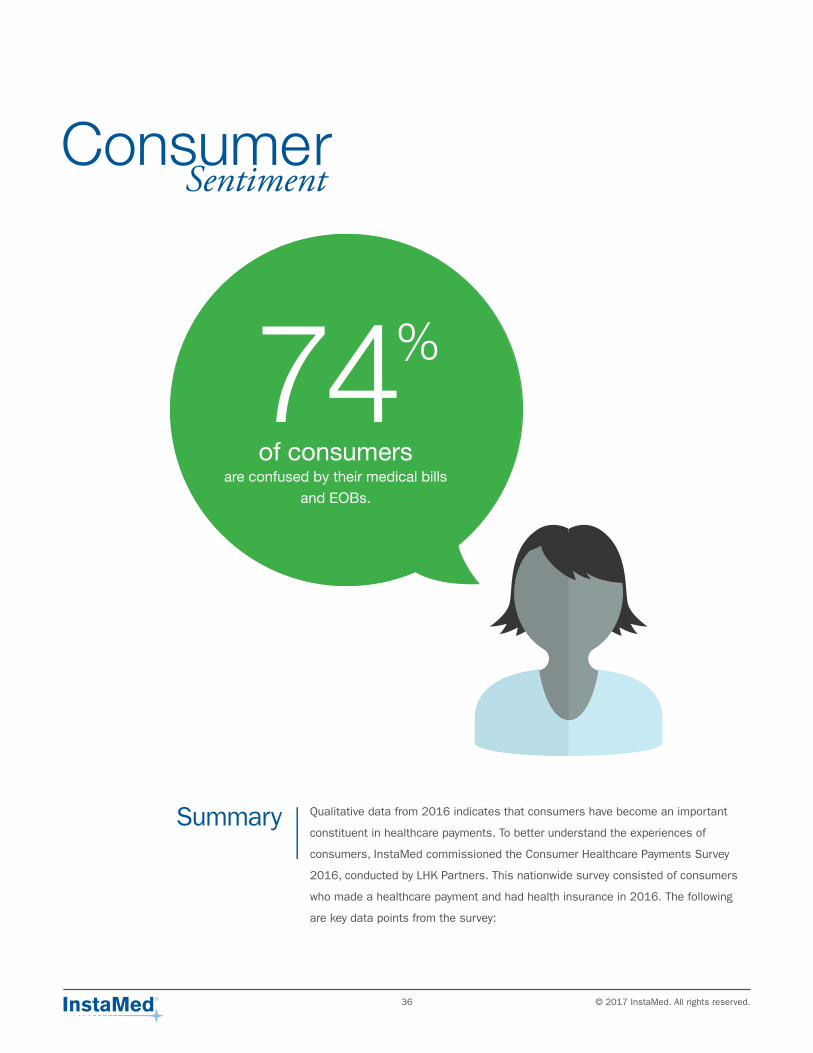

Qualitative data from 2016 indicates that consumers have become an important

constituent in healthcare payments. To better understand the experiences of

consumers, InstaMed commissioned the Consumer Healthcare Payments Survey

2016, conducted by LHK Partners. This nationwide survey consisted of consumers

who made a healthcare payment and had health insurance in 2016. The following

are key data points from the survey:

ConsumerSentiment

Summary

of consumersare confused by their medical bills

and EOBs.

%74

© 2017 InstaMed. All rights reserved.37

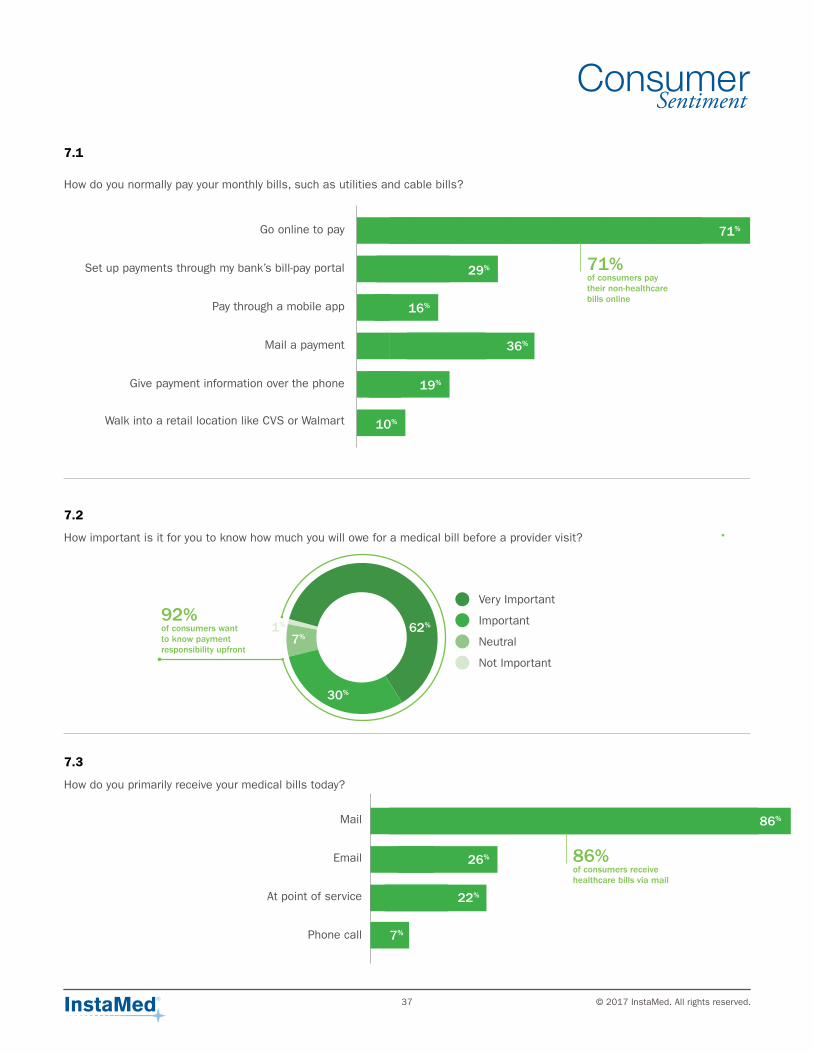

How do you normally pay your monthly bills, such as utilities and cable bills?

How important is it for you to know how much you will owe for a medical bill before a provider visit?

ConsumerSentiment

7.1

7.2

How do you primarily receive your medical bills today?

7.3

71%

29%

16%

36%

19%

10%

Pay through a mobile app

Mail a payment

Give payment information over the phone

Go online to pay

Set up payments through my bank’s bill-pay portal

Walk into a retail location like CVS or Walmart

62%

30%

7%1%

Very Important

Important

Neutral

Not Important

At point of service

Phone call

86%

26%

7%

22%

92% of consumers want to know payment responsibility upfront

71% of consumers pay their non-healthcare bills online

86% of consumers receive healthcare bills via mail

38 © 2017 InstaMed. All rights reserved.

Are you confused by your medical bills from doctors, hospitals and other medical providers?

How do you prefer to make a payment for medical bills?

7.4

7.5

All of the time

Some of the time

Never26% 57% 17%

29%

14%

9%

6%

21%

16%

5%

Pay through a mobile app

Mail a payment

At the provider’s office

Online through a health plan website

Set up payments through my bank’s bill-pay portal

Give payment information over the phone

Online through a doctor or hospital website

74% of consumers are confused by medical bills

58% of consumers prefer online payment channels to pay medical bills

ConsumerSentiment

© 2017 InstaMed. All rights reserved.39

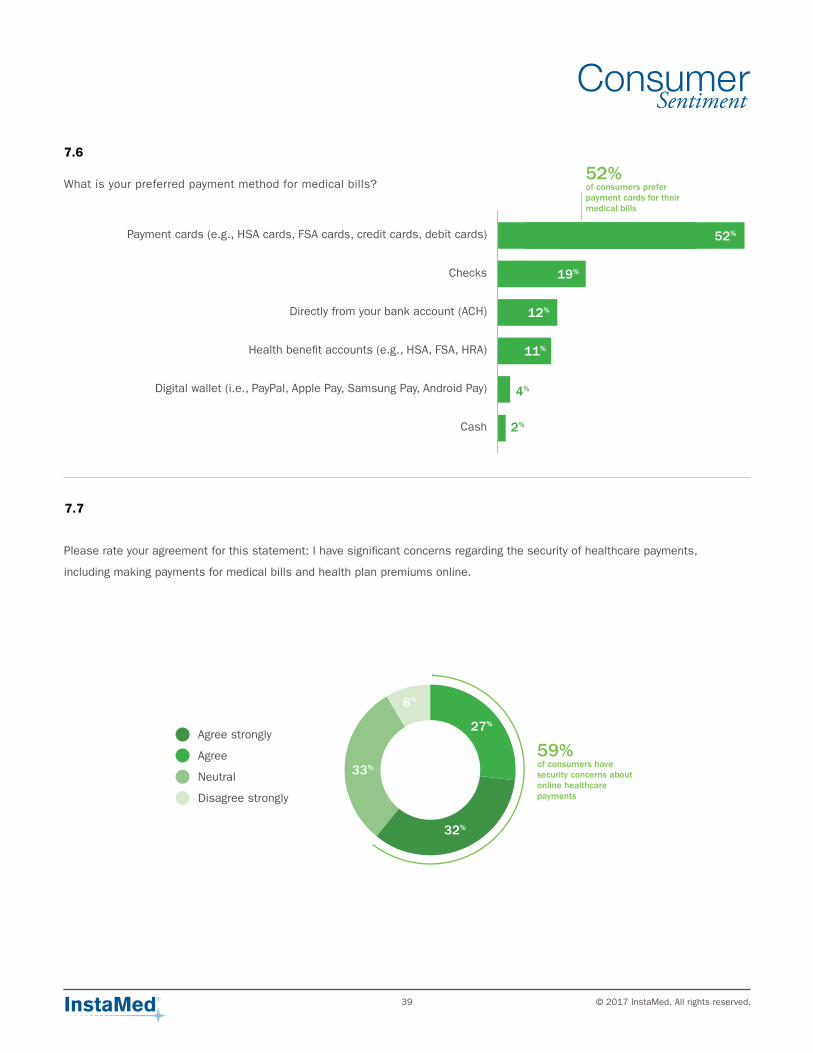

What is your preferred payment method for medical bills?

Please rate your agreement for this statement: I have significant concerns regarding the security of healthcare payments,

including making payments for medical bills and health plan premiums online.

7.6

7.7

Health benefit accounts (e.g., HSA, FSA, HRA)

Digital wallet (i.e., PayPal, Apple Pay, Samsung Pay, Android Pay)

Cash

Checks

Directly from your bank account (ACH)

Payment cards (e.g., HSA cards, FSA cards, credit cards, debit cards) 52%

19%

12%

11%

4%

2%

Agree strongly

Agree

Neutral

Disagree strongly

32%

33%

8%

27%

52% of consumers preferpayment cards for their medical bills

59% of consumers have security concerns about online healthcare payments

ConsumerSentiment

40 © 2017 InstaMed. All rights reserved.

Which of the following do you personally have access to in your home?

7.9

How interested are you in using mobile payment systems such as Apple Pay, Samsung Pay or Android Pay?

7.8

Very interested

Somewhat interested

Not very interested

Not interested at all

18%

34%

21%

27%

Tablet

None of the above

Laptop computer

Desktop computer

Smartphone 82%

81%

65%

63%

0.3%

61% of consumers are interested in mobile payment systems

ConsumerSentiment

© 2017 InstaMed. All rights reserved.41

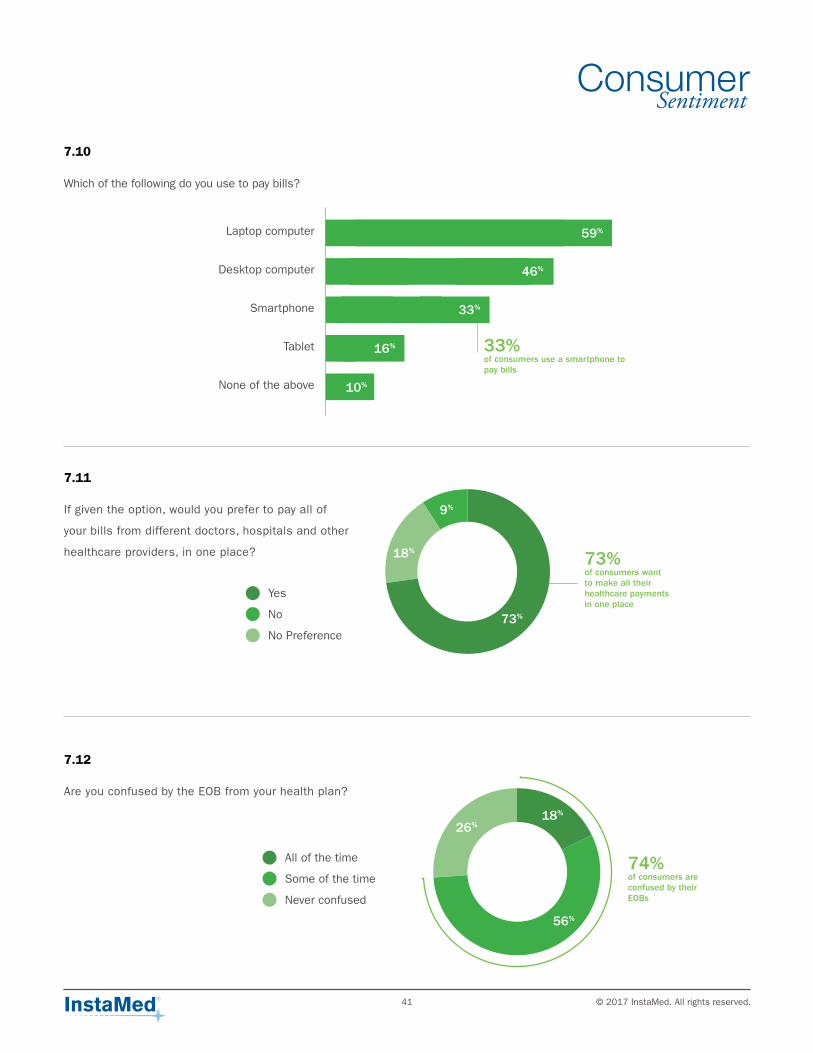

Which of the following do you use to pay bills?

7.10

If given the option, would you prefer to pay all of

your bills from different doctors, hospitals and other

healthcare providers, in one place?

7.11

Are you confused by the EOB from your health plan?

7.12

Tablet

None of the above

Desktop computer

Smartphone

Laptop computer 59%

46%

33%

16%

10%

Yes

No

No Preference73%

18%

9%

All of the time

Some of the time

Never confused

56%

26%18%

33% of consumers use a smartphone to pay bills

73% of consumers want to make all their healthcare payments in one place

74% of consumers are confused by their EOBs

ConsumerSentiment

42 © 2017 InstaMed. All rights reserved.

What is your preferred payment method to pay your premiums?

7.14

How do you prefer to pay your health plan premium?

7.13

Digital wallet (i.e., PayPal, Apple Pay, Samsung Pay, Android Pay)

Cash

Directly from your bank account (ACH)

Checks

Payment cards (e.g., credit cards, debit cards)

Mail a payment

Give payment information over the phone

Set up payments through my bank’s bill-pay portal

Pay through a mobile app

Go online to pay 47%

24%

9%

16%

4%

1%

50%

30%

13%

6%

80% of consumers prefer online payment channels to pay their health plan premiums

50% of consumers want to use payment cards to pay their premiums

ConsumerSentiment

© 2017 InstaMed. All rights reserved.43

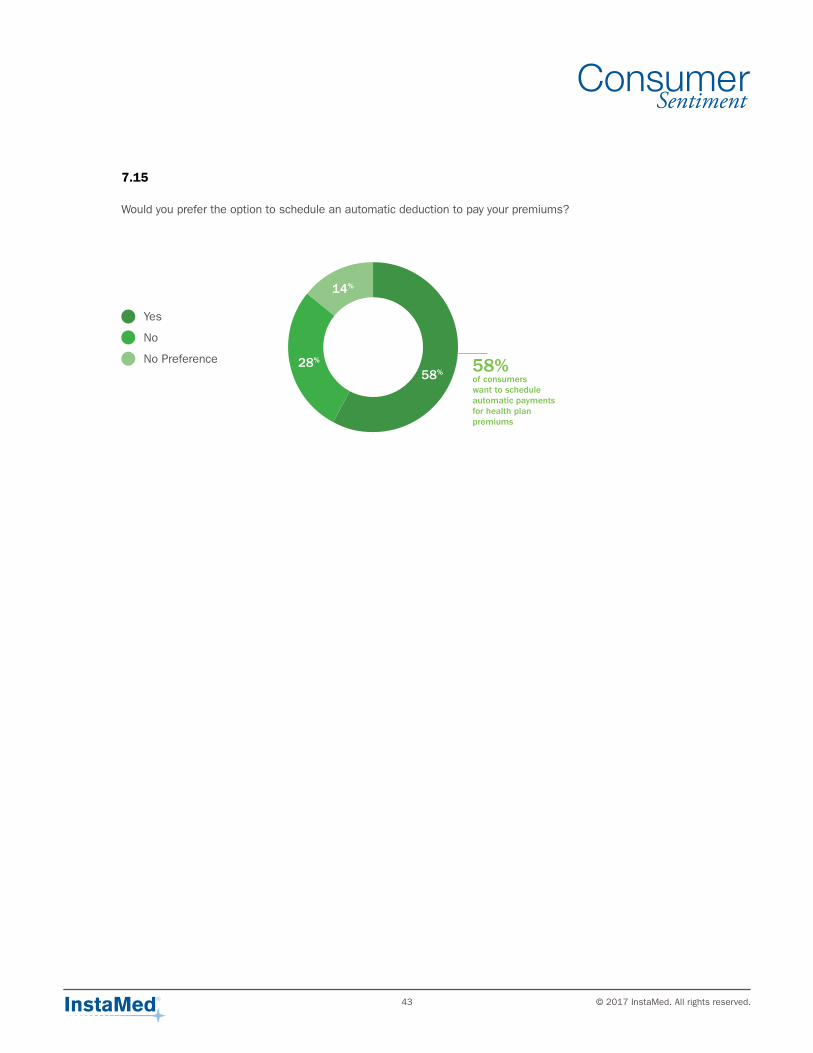

Would you prefer the option to schedule an automatic deduction to pay your premiums?

7.15

Yes

No

No Preference58%

28%

14%

58% of consumers want to schedule automatic payments for health plan premiums

ConsumerSentiment

44 © 2017 InstaMed. All rights reserved.

Now in its seventh year, the Trends in Healthcare Payments Annual Report is distributed

free of charge with the intention of starting a conversation about the current state

of the industry and to promote change. From analyzing the trends in this report, the

following conclusions have been made:

Consumer Demands Are the New Normal

Consumers are disrupting “business as usual” in the industry. This new reality is

spurred on by increases in financial responsibilities for consumers, which are primarily

in the form of health plan premiums, deductibles, copayments, coinsurance, etc. As

their payment responsibility continues to increase, consumer demands will become

the biggest drivers of change for providers and payers. Providers must collect larger

amounts from most or all of their patients, while payers must interact with members in

new ways including collecting health plan premiums.

Despite these relationship shifts, many in the industry have been slow to acknowledge

or encourage the new role of consumers as an industry stakeholder. Consumers often

do not know how much they will owe until they get a paper statement from a provider

or EOB from a payer, which often lead to high levels of confusion and frustration. If

consumer needs are not met, there are real impacts to an organization’s revenue and

brand trust.

Omnichannel Payments Answer Consumer Demands

Consumers bring their expectations and experiences from other industries to

healthcare payments. It isn’t just about millennials either. The demand for an

omnichannel payment experience is true across all generations, including baby

boomers. Omnichannel payments offer consumers the ability to pay how they want at

their discretion. There is a clear connection between consumer preference and payment

channels that promote convenience and simplicity. Electronic and automated payment

channels will become the norm in healthcare payments, as they already are in other

industries. Providers and payers who offer an omnichannel approach to payments will

be rewarded with consumer loyalty, brand trust and revenue to sustain the future of

their organizations.

Conclusions

Conclusions

© 2017 InstaMed. All rights reserved.45

Conclusions

The Industry Is Prime to Go Paperless

The healthcare industry is one of the last places where transactions are primarily done

on paper. The burden of paper is a drag on the entire industry causing wasted time and

money, even causing physician burnout. There is a growing consensus among providers

and consumers that eliminating paper in favor of electronic payments is the preferred way

to get paid. There are significant opportunities to reduce the waste of paper by harnessing

the potential of electronic transactions, especially when leveraged with automation. The

potential cost savings and lower overall administrative resources could save the industry

billions of dollars.

Security and Compliance Must Be a Priority

Any organizations unsure if their data is at risk should assume the worst. Ransomware,

data breaches and stolen information make data in the healthcare industry a constant

target to hackers and thieves – all of which cost the industry billions of dollars. The

impact of unsecure data has not gone unnoticed as consumers and providers reported

payment security is very important. Consequences of unsecure data and noncompliant

processes and systems will continue to cost the industry billions of dollars. Organizations

can ensure that their data is secure and reduce the risk of a breach by meeting industry

standards, and obtaining audits and certifications from respected industry groups.

46 © 2017 InstaMed. All rights reserved.

Conclusions

The 2016 Trends in Healthcare Payments Annual Report includes quantitative data

from over $239 billion in healthcare payments volume on the InstaMed Network,

which connects over two-thirds of the healthcare market. The data represented was

processed between 2013 and 2016.

The report includes qualitative market data based on an analysis of three InstaMed-

commissioned online surveys conducted by LHK Partners Incorporated, an independent

marketing research company, to better understand the experiences of the key

stakeholders in the healthcare payments process.

The data compiled by LHK Partners for the Provider Healthcare Payments Survey 2016

comes from respondents representing over 100,000 healthcare providers nationwide.

The group of respondents is comprised of 74 percent medical practices or clinics;

13 percent hospital, health system or integrated delivery network; 8 percent billing

services; 4 percent durable, medical equipment or home medical equipment and 1

percent lab.

The data compiled by LHK Partners for the Payer Healthcare Payments Survey 2016

comes from respondents representing over 3,000 payers nationwide. The group of

survey respondents is comprised of 47 percent regional payers; 27 percent Blues

plans; 13 percent national payers and 13 percent other types of payers, including state

Medicaid payers and PPOs.

The data compiled by LHK Partners for the Consumer Healthcare Payments Survey

2016 comes from respondents representing 2,730 consumers nationwide who paid a

medical bill and had health insurance in 2016.

Methodology

© 2017 InstaMed. All rights reserved.47

Conclusions

About InstaMed InstaMed is healthcare’s most trusted payments network, connecting providers,

payers and consumers on one platform. The InstaMed Network connects over

two-thirds of the market and processes tens of billions of dollars in healthcare

payments annually. InstaMed reduces the risks, costs and complexities of working

with multiple payment vendors by delivering one platform for all forms of payment

in healthcare, designed and developed on one code base and supported by one

onshore team of experts in healthcare payments. InstaMed enables providers to

collect more money from patients and payers while reducing the cost and time to

collect. InstaMed allows payers to cut settlement and disbursement costs with

electronic payments and facilitate consumerism for their members.

Visit InstaMed on the web at www.instamed.com or contact [email protected] for

more information.

3300 Irvine Avenue, Suite 305Newport Beach, CA 92660

1880 JFK Boulevard, 12th FloorPhiladelphia, PA 19103

www.instamed.com [email protected]