trendsalert -- workers' comp · csg is the nation’s only organization serving every elected...

TRANSCRIPT

Workers’ Comp

Workers’ Comp

Melissa Taylor Bell

Irakli Khodeli

February 2004

The Council of State Governments

2760 Research Park Dr.—P.O. Box 11910—Lexington, KY 40578-1910 Phone: (859) 244-8000—Fax: (859) 244-8001—www.csg.org

The Council of State Governments

CSG is the nation’s only organization serving every elected and appointed official in all three branches of each state and territorial government through its national office, as well as regional offices based in the East, Midwest, South and West. CSG champions excellence in state government by advocating multi-state shared problem solving and states’ rights; by tracking national conditions, trends and innovations; and through nonpartisan groundbreaking leadership training and support.

Council Officers President Gov. Mike Huckabee, Ark.

Chair Rep. Dan E. Bosley, Mass. President-Elect Gov. Frank Murkowski, Alaska

Chair-Elect Sen. John Hottinger, Minn. Vice President Gov. Ruth Ann Minner, Del.

Vice Chair Assemblyman Lynn Hettrick, Nev.

Headquarters Eastern Southern

Daniel M. Sprague Executive Director

Alan V. Sokolow Director

Colleen Cousineau Director

40 Broad Street, Suite 2050 P.O. Box 98129 Albert C. Harberson

Director of Policy New York, NY 10004-2317

Phone: (212) 482-2320 Atlanta, GA 30359

Phone: (404) 633-1866 Fax: (212) 482-2344 Fax: (404) 633-4896

Washington, D.C. Midwestern Western

Jim Brown Director

Michael H. McCabe Director

Kent Briggs Director

444 N. Capitol Street, Suite 401 614 E. Butterfield Road, Suite 401 1107 9th Street, Suite 650 Washington, D.C. 20001 Lombard, IL 60148 Sacramento, CA 95814 Phone: (202) 624-5460 Phone: (630) 810-0210 Phone: (916) 553-4423

Fax: (202) 624-5462 Fax: (630) 810-0145 Fax: (916) 446-5760

i

Table of Contents

Executive Summary 1

1. Current Trends in Workers’ Compensation 2

Medical Costs 2 Investment Income 2 Effects of Terrorism 3 Slow Economic Growth 3 Workforce Demographics 3 Insurance Fraud 3 Excessive Litigation 4

2. Overview of Workers’ Comp Insurance 4

Workers’ Comp Provision 4 Basics of Workers’ Comp 7 Interstate Differences 7 Intrastate Differences 9 Ups and Downs of Workers’ Comp 10 Workers’ Comp through the Years 10

3. Policy Options 11

Workplace Safety and Return-to-Work Programs 11 Workplace Safety Programs 11 Early Return-to-Work Programs 15

Medical Cost Containment Strategies 16

Provider Choice Laws 17 Health Care Provider Networks 19 Medical Provider Fee Schedules and Bill Review 21 Treatment Guidelines and Utilization Review 22 Case Management 23 Promotion of Generic Drugs 23

General Cost Containment Strategies 23

Deregulation and Competitive Premium Rates 25 Self-Insurance and Pooled Insurance Options 26 Advisory Councils 27 Technological Innovations 28 Streamlined Workers’ Compensation System for State Employees 29 Fraud Prevention 29 Litigation Controls 29

Conclusion 30 Glossary of Terms 31

1

Executive Summary Over the past decade, the number of workers’ comp compensation claims has been declining. That is the good news. The bad news is that workers’ comp costs and benefits paid out are still rising. In fact, workers’ comp costs are experiencing double-digit increases across the country. The average cost of workers’ compensation has risen 50 percent over the past three years.1 Increased costs are leading to higher premiums for employers, and this can affect business and economic development. In some states, it is not only a crisis of affordability but one of access as well. Faced with rising costs, some insurers have pulled out of the workers’ comp market or shut down shop altogether. A variety of factors are leading to a potential workers’ comp crisis. These cost drivers include:

• medical expenses increases; • investment income losses; • effects of terrorist acts; • slow economic growth; • increasing fraud in the system; • excessive litigation; and • workforce demographics.

States are subject to different cost drivers based on their specific circumstances and their reliance on certain economic sectors. A state with a large number of dangerous jobs, for instance, faces a different set of factors than a state with an economy dominated by low-risk industries. States that have had relatively stable costs over the years have several similar characteristics, but they differ in many ways as well. Therefore, it is virtually impossible to list the elements of the “perfect” workers’ comp system. Although there is no magic bullet, there are a number of policies that state officials can introduce to deal with workers’ comp problems. The policies outlined in this report focus on cost containment measures related to:

• enhancing workplace safety and decreasing the number of workers’ comp claims; • containing medical costs; and • dealing with a number of inefficiencies in the system.

Because states may be affected by different cost drivers and to different degrees, policy-makers should choose the combination of policy options that best address the needs of their particular state workers’ comp systems.

2

1. Current Trends in Workers’ Compensation

Claim frequency is beginning to level off, but costs are not.2 This situation is illustrated in Figures 1.1 and 1.2. Because of these increasing costs, insurers are raising their rates. Higher premiums are putting a burden on employers, who pay for workers’ comp insurance for their employees. Figure 1.1 Workplace Injury and Illness Incidence Rates, 1989-2001

Figure 1.2 Costs and Benefits Paid Out for Workers’ Comp (in billions), 1989-2001

0.02.04.06.08.0

10.0

1989

1991

1993

1995

1997

1999

2001

Year

Inci

denc

e ra

te p

er

100

full-

time

wor

kers

Total cases

Lost w orkday cases

Cases w ithout lost w orkdays

Data Source: National Academy of Social Insurance

0

10

20

30

40

50

60

70

1989

1991

1993

1995

1997

1999

2001

Costs Benefits

Data Source: U.S. Department of Labor

A variety of factors are leading to a potential workers’ comp crisis. These cost drivers include:

• medical expenses; • investment income losses; • effects of terrorist acts; • slow economic growth; and • workforce demographics (older and immigrant workers).

Medical Costs The annual average rate of increase in workers’ compensation medical care costs was 8.1 percent from 1996 to 2002, compared with an annual average rise of 3.8 percent for the medical consumer price index over the same period.3 Medical costs for workers’ comp have risen more than general medical inflation, leading some experts to surmise that workers are overusing workers’ comp and underutilizing their health insurance. In other words, as co-payments for health insurance rise, workers may be more prone to classify their injuries as work-related so that workers’ comp, without co-payments, will cover their medical expenses. In addition to overutilization, there are several other factors leading to this rise. For instance, “Some workers’ comp carriers have seen costs for some commonly prescribed drugs rise by more than 100 percent over the past few years.”4 There is also evidence of abuse and fraud, such as doctors billing for more serious ailments than the workers have and workers faking injury. One study by an insurance company suggests medical costs are rising because of a broader definition of workplace injuries, rising number of visits to medical providers and the use of more expensive medical treatments.5 Investment Income In the 1990s, insurers invested some of their premium income in stocks and bonds. During the economic boom of the 1990s, some made a hefty profit from this practice. With the current climate in the stock and bond markets, however, net investment income in the property/casualty insurance industry fell 7.1 percent in 2001 and an estimated 4.9 percent in 2002.6

3

Since market outcomes are out of their hands, insurers must focus on efficient pricing and cost-cutting in order to generate profits. Therefore, many insurers are raising their premiums and trying to limit the effects of current cost drivers. Effects of Terrorism Before September 11, 2001, the effects of terrorism were negligible in the workers’ comp industry. Workers’ comp claims stemming from the terrorist attacks on the World Trade Center in New York, however, are estimated at about $2 billion.7 This is obviously a big loss for the workers’ comp insurance industry. Workers’ comp insurers must provide terrorism insurance, but reinsurers are not required to do so. Therefore, workers’ comp insurers can’t distribute this risk in the reinsurance markets. Consequently, premiums have risen, and insurers are instituting strict underwriting reviews. Slow Economic Growth Workers’ comp insurers pay out $1.07 for every $1 they receive in premiums; this added up to about a $2 billion loss in 2002.8 Slow economic growth, which is interrelated with other cost drivers, contributes to this deficiency. In a sluggish economy, there is not a major increase in wages. During these times, workers’ comp benefit payouts rise more than wages. Because workers are generally compensated until they get a new job, this process can take longer in a slow economy. Also, in slow economic times, there is less business formation and job creation. Therefore, there are fewer employers to serve as customers for workers’ comp insurers. This leads to intense price competition among insurers, which can have damaging effects on the industry. Insurers may engage in a pricing war and actually sell premiums that don’t pay for insurance costs. Insurers can make up these losses with investment income from the stock and bond markets. When these markets take a dive, as noted above, this source of income also dries up. To make up for investment losses, insurers raise their prices, leading to problems with access and affordability. During a recession, average medical costs per claim grow faster than during economic growth. During times of high unemployment, unemployed workers may try to compensate lost income from other sources by over-utilizing workers’ compensation benefits. Also, when unemployment rises, businesses tend to lay off less experienced workers, who tend to be younger and less susceptible to serious injuries, while retaining more experienced workers, who tend to be older and prone to more serious injuries. Consequently, the average severity and the average costs of workers’ compensation claims increase during economic downturns.9 Workforce Demographics One set of cost drivers that some insurers are paying attention to deals with workforce demographics. The American workforce is becoming older and more diverse. This affects workers’ comp rates primarily in two ways. First, as noted above, older workers are more susceptible to injury and work-related illness, so the number and severity of claims may rise in the near future as the workforce ages. Second, due to influx of immigrant workers, insurers or employers may need to hire interpreters and translate workers’ comp materials into other languages; in addition, there are often few work alternatives for certain groups of unskilled immigrants. Interpreters and translation services can be expensive. Since workers’ comp pays until the injured employee finds another job, there are increased costs associated with low-skill workers who cannot easily find other employment. Insurance Fraud According to the National Insurance Crime Bureau, workers’ comp fraud costs the insurance industry approximately $5 billion each year and is partially responsible for a rising trend in insurance premiums for employers. 10

4

• Employee claim abuse is the most common type of fraud and occurs when an employee knowingly files a false claim about an injury that has not occurred or that did not occur at the workplace. This results in unnecessary expense for the insurance carrier and loss of workforce for the employer.

• Employer fraud occurs when an employer intentionally provides inaccurate information about business operations and workforce composition to reduce workers’ comp costs. Also called premium fraud, it is a growing concern for many states because it escalates insurance rates and hurts other businesses that are less able to compete with companies defrauding the system.

• Medical provider fraud results when doctors perform unnecessary tests and procedures on patients, lie about procedures and state of patient’s injuries to share a percentage of employee’s compensation, or otherwise abuse professional discretion to maximize gains from the system.

• Insurance carrier fraud occurs when an insurance provider overcharges on premiums or makes false or misleading claims about coverage.

Organized fraud involving doctors and lawyers have been an ongoing problem, especially in southern California. Fraud rings recruit people to file fraudulent work injury claims and to seek help from medical clinics or legal centers commonly known as “claim mills.” Claim mills, in turn, refer workers to doctors or lawyers who participate in the scheme. Excessive Litigation Excessive litigation and attorney involvement in workers’ compensation claims process can contribute to high costs and system inefficiency. Litigiousness of the system may raise concerns in the states because the very purpose of the workers’ compensation is to create a “no-fault” system that delivers benefits for work injuries in a timely and non-litigious manner.11 Attorneys are now involved in 5 to 10 percent of all worker’s compensation claims, and nearly one-third of all claims for injuries that are serious enough to result in loss-time payments.12 Although claim costs for cases in which attorneys get involved increase by 12 to 15 percent, after paying attorney fees the injured workers enjoys no gains on the actual net benefits received.13 2. Overview of Workers’ Comp Insurance Workers’ comp is a no-fault system. As such, employers pay medical costs and lost wages for injured employees, and employees cannot sue their employers. Workers’ comp is a mandatory program in every state except Texas. According to the Insurance Information Institute, almost nine out of 10 workers are covered by workers’ comp insurance14 even though small businesses with fewer than three to five employees are exempt in 16 states.15 Workers’ Comp Provision As illustrated in Table 1.1, there are basically three ways for employers to get workers’ comp insurance:

• private insurance; • self insurance; or • state-provided insurance.

Table 1.1 Workers’ Comp Insurance Provision, 2003

Insurance Provided By: Self-Insurance Provided By:

State Type of Law State Fund Private Carrier Individual Employer

Group of Employers

Alabama Compulsory No Yes Yes Yes Alaska Compulsory No Yes Yes No Arizona Compulsory Competitive Yes Yes Yes Arkansas Compulsory No Yes Yes Yes

5

Table 1.1 Workers’ Comp Insurance Provision, 2003 (cont.)

California Compulsory Competitive Yes Yes Yes Colorado Compulsory Competitive Yes Yes Yes Connecticut Compulsory No Yes Yes Yes Delaware Compulsory No Yes Yes No Florida Compulsory No Yes Yes Yes Georgia Compulsory No Yes Yes Yes Guam Compulsory No Yes Yes Yes Hawaii Compulsory Competitive Yes Yes Yes Idaho Compulsory Competitive Yes Yes No Illinois Compulsory No Yes Yes Yes Indiana Compulsory No Yes Yes No Iowa Compulsory No Yes Yes Yes Kansas Compulsory No Yes Yes Yes Kentucky Compulsory Competitive Yes Yes Yes Louisiana Compulsory Competitive Yes Yes Yes Maine Compulsory Competitive Yes Yes Yes Maryland Compulsory Competitive Yes Yes Yes Massachusetts Compulsory No Yes Yes Yes Michigan Compulsory No Yes Yes Yes Minnesota Compulsory Competitive Yes Yes Yes Mississippi Compulsory No Yes Yes Yes Missouri Compulsory No Yes Yes Yes Montana Compulsory Competitive Yes Yes Yes Nebraska Compulsory No Yes Yes No Nevada Compulsory No Yes Yes Yes New Hampshire Compulsory No Yes Yes Yes New Jersey Elective1 No Yes Yes No New Mexico Compulsory Competitive Yes Yes Yes New York Compulsory Competitive Yes Yes Yes North Carolina Compulsory No Yes Yes Yes North Dakota Compulsory Exclusive No No No Ohio Compulsory Exclusive No Yes No Oklahoma Compulsory Competitive Yes Yes Yes Oregon Compulsory Competitive Yes Yes Yes Pennsylvania Compulsory Competitive Yes Yes Yes Puerto Rico Compulsory Exclusive No No No Rhode Island Compulsory2 Competitive Yes Yes Yes South Carolina Compulsory No Yes Yes Yes South Dakota Compulsory No Yes Yes Yes Tennessee Compulsory No Yes Yes Yes Texas Elective Competitive Yes Yes No Utah Compulsory Competitive Yes Yes No Vermont Compulsory No Yes Yes No Virginia Compulsory No Yes Yes Yes Virgin Islands Compulsory Exclusive No No No Washington Compulsory Exclusive No Yes Yes West Virginia Compulsory Exclusive No Yes No Wisconsin Compulsory No Yes Yes No Wyoming Compulsory3 Exclusive No No No

1 New Jersey: Technically coverage is elective, but practically compulsory. 2 Rhode Island: Employees are allowed to claim common law rights and opt out of the workers’ compensation system. 3 Wyoming: The law is compulsory for all employers engaged in extra-hazardous occupations and elective for all other occupations. Source: U.S. Department of Labor

6

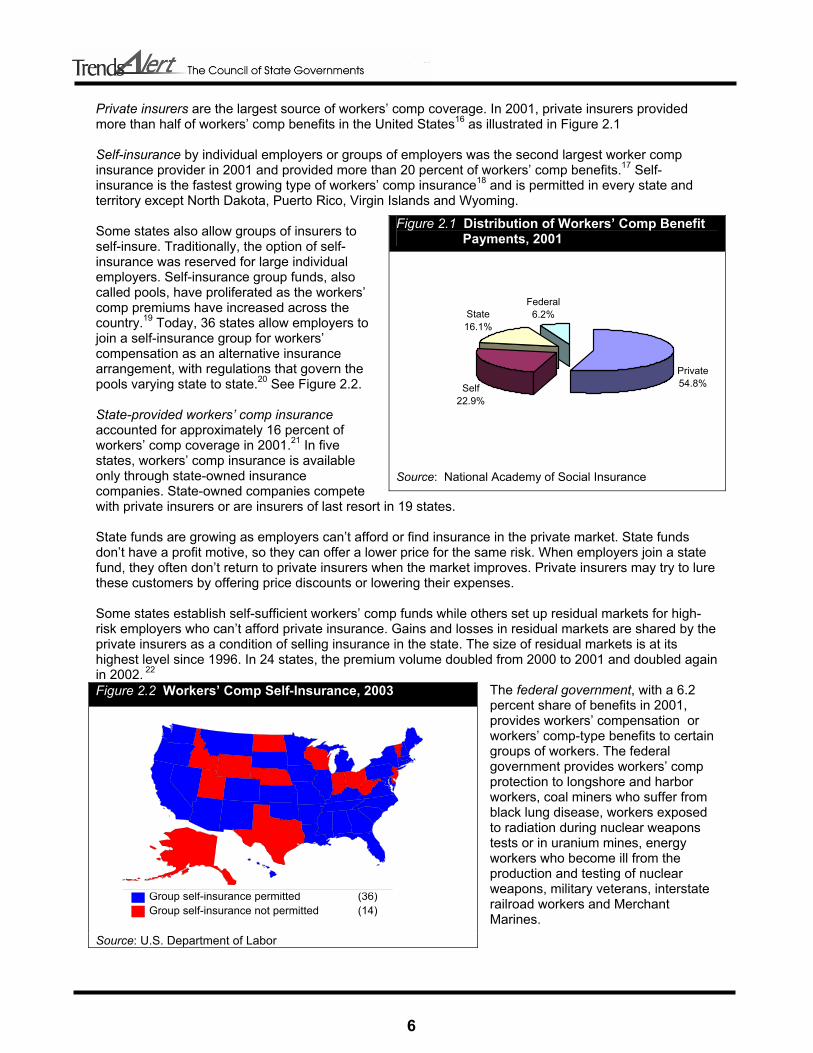

Private insurers are the largest source of workers’ comp coverage. In 2001, private insurers provided more than half of workers’ comp benefits in the United States16 as illustrated in Figure 2.1 Self-insurance by individual employers or groups of employers was the second largest worker comp insurance provider in 2001 and provided more than 20 percent of workers’ comp benefits.17 Self-insurance is the fastest growing type of workers’ comp insurance18 and is permitted in every state and territory except North Dakota, Puerto Rico, Virgin Islands and Wyoming. Some states also allow groups of insurers to self-insure. Traditionally, the option of self-insurance was reserved for large individual employers. Self-insurance group funds, also called pools, have proliferated as the workers’ comp premiums have increased across the country.19 Today, 36 states allow employers to join a self-insurance group for workers’ compensation as an alternative insurance arrangement, with regulations that govern the pools varying state to state.20 See Figure 2.2. State-provided workers’ comp insurance accounted for approximately 16 percent of workers’ comp coverage in 2001.21 In five states, workers’ comp insurance is available only through state-owned insurance companies. State-owned companies compete with private insurers or are insurers of last resort in 19 states. State funds are growing as employers can’t afford or find insurance in the private market. State funds don’t have a profit motive, so they can offer a lower price for the same risk. When employers join a state fund, they often don’t return to private insurers when the market improves. Private insurers may try to lure these customers by offering price discounts or lowering their expenses. Some states establish self-sufficient workers’ comp funds while others set up residual markets for high-risk employers who can’t afford private insurance. Gains and losses in residual markets are shared by the private insurers as a condition of selling insurance in the state. The size of residual markets is at its highest level since 1996. In 24 states, the premium volume doubled from 2000 to 2001 and doubled again in 2002. 22

The federal government, with a 6.2 percent share of benefits in 2001, provides workers’ compensation or workers’ comp-type benefits to certain groups of workers. The federal government provides workers’ comp protection to longshore and harbor workers, coal miners who suffer from black lung disease, workers exposed to radiation during nuclear weapons tests or in uranium mines, energy workers who become ill from the production and testing of nuclear weapons, military veterans, interstate railroad workers and Merchant Marines.

Figure 2.1 Distribution of Workers’ Comp Benefit Payments, 2001

Private54.8%

Federal6.2%State

16.1%

Self22.9%

Source: National Academy of Social Insurance

Figure 2.2 Workers’ Comp Self-Insurance, 2003

Source: U.S. Department of Labor

Group self-insurance permitted (36)Group self-insurance not permitted (14)

7

Basics of Workers’ Comp Premiums are based on industry classification of the employers and occupational classifications of individual workers. Employers in high-risk industries, such as construction, pay higher premiums than lower-risk desk jobs. The vast majority of workers’ comp cases are medical only; that is, most cases do not involve lost work time. While medical-only cases account for almost 80 percent of cases, they account for only 6 percent of benefits paid.23 In contrast, cases involving lost wages account for about 20 percent of workers’ comp cases but 94 percent of all benefits paid.24 There are four types of workers’ compensation benefits for lost wages:

• If a worker returns to work with reduced responsibilities and a lower wage before reaching maximum medical improvement, the injured worker can receive temporary partial disability benefits.

• If a worker is hurt and must miss work for more than the state-mandated waiting period, in most states, temporary total disability benefits generally pay for two-thirds of a worker’s pre-injury wage.

• If an injured worker is able to work at reduced efficiency but is disabled for life, the worker is eligible for permanent partial disability benefits. This category of benefits accounts for 31 percent of workers’ comp cash payments and 63 percent of all workers’ comp spending.25

• If an injured worker is permanently disabled and is unable to work at all, the worker is eligible for permanent total disability. These cases are uncommon.

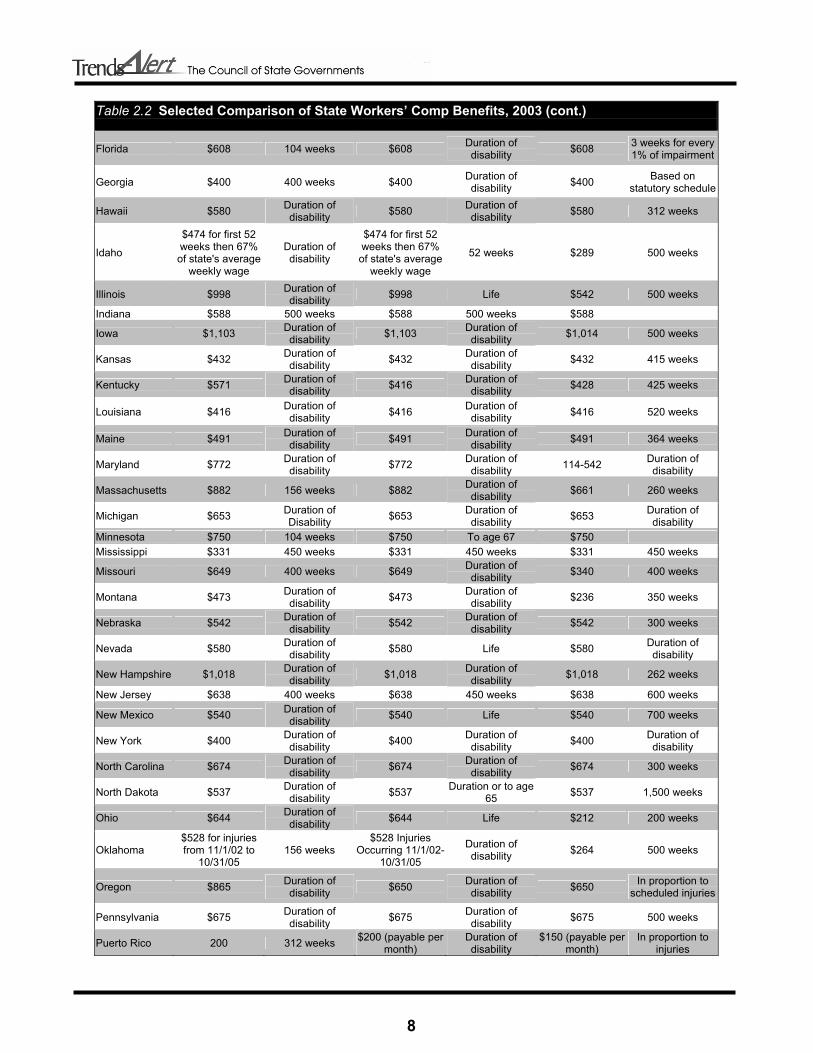

Most workers’ comp cases that involve cash benefits for lost wages are temporary – either temporary partial or temporary total. Interstate Differences States vary in terms of benefit levels and what is compensable. Table 2.2 provides a glimpse of variations in state workers’ comp benefits. Table 2.2 Selected Comparison of State Workers’ Comp Benefits, 2003

Temporary Total Disability Permanent Total Disability Permanent Partial Disability State

Maximum Weekly Benefit

Benefit Duration Limit

Maximum Weekly Benefit

Benefit Duration Limit

Maximum Weekly Benefit

Benefit Duration Limit

Alabama $569 Duration of disability $569 Duration of

disability $220 300 weeks

Alaska $814 Duration of disability $814 Duration of

disability

Based on impairment;

payable in lump sum

Arizona $374 Duration of disability $374 Duration of

disability $374 Duration of disability

Arkansas $440 450 weeks $440 Duration of disability $330 450 weeks

California $602 Duration of disability $602 Life $230 619 weeks

Colorado $659 Duration of disability $645 Life $354 Duration of

disability

Connecticut $909 Duration of disability $909 Duration of

Disability $687 520 weeks

Delaware $491 Duration of disability $491 Duration of

disability $491 300 weeks

8

Table 2.2 Selected Comparison of State Workers’ Comp Benefits, 2003 (cont.)

Florida $608 104 weeks $608 Duration of disability $608 3 weeks for every

1% of impairment

Georgia $400 400 weeks $400 Duration of disability $400 Based on

statutory schedule

Hawaii $580 Duration of disability $580 Duration of

disability $580 312 weeks

Idaho

$474 for first 52 weeks then 67% of state's average

weekly wage

Duration of disability

$474 for first 52 weeks then 67% of state's average

weekly wage

52 weeks $289 500 weeks

Illinois $998 Duration of disability $998 Life $542 500 weeks

Indiana $588 500 weeks $588 500 weeks $588

Iowa $1,103 Duration of disability $1,103 Duration of

disability $1,014 500 weeks

Kansas $432 Duration of disability $432 Duration of

disability $432 415 weeks

Kentucky $571 Duration of disability $416 Duration of

disability $428 425 weeks

Louisiana $416 Duration of disability $416 Duration of

disability $416 520 weeks

Maine $491 Duration of disability $491 Duration of

disability $491 364 weeks

Maryland $772 Duration of disability $772 Duration of

disability 114-542 Duration of disability

Massachusetts $882 156 weeks $882 Duration of disability $661 260 weeks

Michigan $653 Duration of Disability $653 Duration of

disability $653 Duration of disability

Minnesota $750 104 weeks $750 To age 67 $750 Mississippi $331 450 weeks $331 450 weeks $331 450 weeks

Missouri $649 400 weeks $649 Duration of disability $340 400 weeks

Montana $473 Duration of disability $473 Duration of

disability $236 350 weeks

Nebraska $542 Duration of disability $542 Duration of

disability $542 300 weeks

Nevada $580 Duration of disability $580 Life $580 Duration of

disability

New Hampshire $1,018 Duration of disability $1,018 Duration of

disability $1,018 262 weeks

New Jersey $638 400 weeks $638 450 weeks $638 600 weeks

New Mexico $540 Duration of disability $540 Life $540 700 weeks

New York $400 Duration of disability $400 Duration of

disability $400 Duration of disability

North Carolina $674 Duration of disability $674 Duration of

disability $674 300 weeks

North Dakota $537 Duration of disability $537 Duration or to age

65 $537 1,500 weeks

Ohio $644 Duration of disability $644 Life $212 200 weeks

Oklahoma $528 for injuries from 11/1/02 to

10/31/05 156 weeks

$528 Injuries Occurring 11/1/02-

10/31/05

Duration of disability $264 500 weeks

Oregon $865 Duration of disability $650 Duration of

disability $650 In proportion to scheduled injuries

Pennsylvania $675 Duration of disability $675 Duration of

disability $675 500 weeks

Puerto Rico 200 312 weeks $200 (payable per month)

Duration of disability

$150 (payable per month)

In proportion to injuries

9

Table 2.2 Selected Comparison of State Workers’ Comp Benefits, 2003 (cont.)

Rhode Island $702 Duration of disability $702 Duration of

disability $702 Duration of disability

South Carolina $563 500 weeks $563 500 weeks $563 340 weeks

South Dakota $482 Duration of disability $482 Duration of

disability $482 Duration of disability

Tennessee $599 400 weeks $599 Until retirement age $599 400 weeks

Texas $537 104 weeks $537 401 weeks or life

for injuries listed in statute

$373 401 weeks

Utah $562 312 weeks $478 312 weeks or life if

can't be rehabilitated

$375 312 weeks

Vermont $865 Maximum medical improvement $865 Duration of

Disability $865

Virginia $681 500 weeks $681 Duration of disability $681 500 weeks

Virgin Islands $385 Duration of disability $385 Duration of

disability $385 200 weeks

Washington $868 Duration of temporary disability

$868 Life

Based on % of permanent

physical impairment

West Virginia $526 208 weeks $526 Duration or to age 65 $526

Wisconsin $669 Duration of disability $647 Life $222 1,000 weeks

Wyoming $527 Duration of disability $527 350 weeks $364

Source: U.S. Department of Labor Numerous economic, financial, administrative and political factors have contributed to the rising costs of state workers’ comp systems. For instance, a report on workers’ comp for agricultural workers in Minnesota lists the following factors that are influencing the workers’ comp system in the state, some of which correspond with national trends and some of which run counter to these trends:26

• increasing number of claims; • longer periods of disability; • rising medical costs; • increasing number of pre-existing risk factors, such as obesity, diabetes and an aging

workforce; • more social complications, such as chemical dependency; • more benefits extending past retirement age; • more permanent total disability claims; • rising cultural and language barriers; • lower investment income; • higher reinsurance costs with less coverage; and • low pricing in the past decade which can no longer be sustained.

While the number of claims has been declining nationwide, Minnesota’s agricultural sector is experiencing an increase in claims. This divergence highlights how States are subject to different cost drivers based on their specific circumstances and their reliance on certain economic sectors. Intrastate Differences Benefit levels can vary within states across time. There are several possible reasons for these intrastate differences from year to year, 27 including changes in:

10

• mandated coverage; • administrative procedures or court rulings; • industry or occupational mix in the state; • unemployment level (more workers means more risk); • wages (benefits are linked to wages); • health care practices; • claims frequency and severity; and • reporting procedures.

Because of these factors, it is sometimes difficult to analyze workers’ comp data in a single state and to make interstate comparisons. Ups and Downs of Workers’ Comp The workers’ comp system goes through a regular cycle of rising and falling premiums. The causes behind the insurance cycle are not precisely identified, but three different economic trends are known to contribute to the cycle: the employment/unemployment cycle, the investment cycle and the underwriting cycle. First, workers’ comp claims ebb and flow somewhat with changes in unemployment. When unemployment rises, previously injured workers are more likely to file a claim, especially if they have already been laid off. Additionally, workers receiving workers’ comp have an incentive to wait out the unemployment cycle, which increases costs. Second, premiums tend to rise and fall in tandem with changes in the stock and bond markets. When stocks are doing well and interest rates are high, insurers tend to compete with lower premiums to attract more customers. When stock and bond markets aren’t doing as well, insurers tend to increase premiums. Third, during a soft market when insurance is relatively available and affordable, insurers tend to practice aggressive pricing in order to increase market share. Eventually, they realize that the premiums collected fall short of covering the claims costs. They then start to tighten underwriting by setting strict rules regarding who can purchase policies and increasing premium prices, thereby limiting the supply of insurance on the market. This leads to a hard market, meaning that insurance is less available and affordable.28 Workers’ Comp through the Years The workers’ comp system has experienced problems before. Workers’ comp benefits grew by double digits in the late 1980s. There is some evidence that there was a higher tendency to report workers’ comp claims during the late 1980s. 29 However, the primary reason for the crisis, it has been argued, was that premiums did not increase enough to cover the costs of the workers’ comp system. 30 At the time, many states regulated premium increases. Sometimes premiums were not allowed to rise enough to cover the increase in costs. Consequently, some insurers chose not to sell premiums. During the late 1980s and early 1990s, some states set premiums in the residual market that did not take the inherently higher costs of the residual market into account. This contributed to insurance losses. To deal with the losses, some states assessed fees on private sector insurers. This added cost increased the need for private insurers to raise rates. In response to the situation, many states stopped regulating rates in the late 1980s and early 1990s. In addition, many states emphasized worker safety and return-to-work programs. For example, some states started to allow employer deductibles, which provided an incentive for employers to promote worker safety. To deal with rising medical costs, several states began to allow managed care options. Medical costs did not rise very much in the early 1990s, partly because of one-time cost savings from implementation of managed care. By the end of the decade, however, these one-time savings were exhausted but many insurers did not raise their premiums accordingly.

11

Worker injury rates and workers’ comp claims declined in the 1990s. The 1990s also saw lower benefits and costs for other reasons, including rate deregulation. High profits ensued as the economy and the stock market were strong. This, however, led to price undercutting as insurers competed for business by pricing premiums below cost. (This situation is very similar to that of the medical malpractice insurance market. For more information on the medical malpractice crisis, go to www.csg.org; keyword: medical malpractice). 3. Policy Options Several states are experiencing or have experienced problems with workers’ comp pricing and access in the last few years. Recent efforts by policy-makers to control the rapidly rising workers’ comp costs while maintaining access to benefits for injured workers have produced a high degree of experimentation and a rapidly changing legislative and regulatory environment. This TrendsAlert outlines policy and program options that address some of the major cost drivers in the workers’ comp system. This section focuses on cost containment strategies that address:

• worker safety issues; • medical costs; and • system inefficiencies, such as economic inefficiencies, administrative inefficiencies, fraud and

excessive litigation. In addition to changing benefit levels, which is not the focus of this section, states can choose a range of cost containment strategies to address the rising costs of workers’ comp insurance. There is no magic bullet. States that have had relatively stable costs over the years have several similar characteristics, but they differ in many ways as well. Therefore, it is virtually impossible to list the elements of the “perfect” workers’ comp system. Workplace Safety and Return-to-Work Programs Put simply, fewer accidents mean fewer chances of lost workdays. Since the vast majority of workers’ comp costs are related to indemnity or reimbursement for lost wages, workplace safety is a key element in reducing the number of accidents and achieving lower workers’ compensation insurance costs.31 In addition, states can also implement return-to-work programs that lead to lower workers’ comp costs. Workplace Safety Programs During the 1990s, states implemented four types of workplace safety regulations that are more stringent than traditional federal OSHA standards:

• Employer safety committee laws are mandated by general state statutes or workers’ compensation regulations. The purpose of safety committees is to involve employees in achieving and maintaining a safe workplace. Their roles include involvement in workplace inspections and accident investigations.

• Employer safety and health programs are required by general state statutes or regulations. 33 Typical components of such programs include hazard identification and control, as well as safety and health training. While

Figure 3.1 Merits and Drawbacks of Safety and Early Return-to-Work Programs

Workplace Safety Programs Pros

• Reduces number of accidents and therefore decreases costs

Cons • State efforts to mandate workplace safety without

federally approved OSHA plans may be challenged in courts32

Early Return-to-Work Programs Pros

• Offers a “win-win” strategy for both employers and employees

• Helps employer save indemnity costs while allowing employee to resume source of income

Cons • Some injuries may be too serious for early return • Permanent total disability claimants will not be able

to resume work

12

some states make workplace health and safety programs mandatory for either all employers or the ones with high injury rates, other states have encouraged voluntary programs through statutory language.34

• Insurance carrier loss control services employ a strategy of curbing costs through mandating that insurance carriers assist policyholders with drafting and implementing health and safety programs.35

• An increasingly popular approach of targeted initiatives involves imposing mandatory safety requirements on employers with above-average injury or workers’ compensation loss rates.

The statutory initiatives to control workers’ compensation costs through improvements in workplace health and safety are found in two places: state workers’ compensation authority and the state OSHA agency (if the state has an approved OSHA plan). Although currently 24 states operate safety programs that are approved by OSHA, most of them have adopted standards identical to federal ones, and do not include comprehensive safety and health program requirements. With the exception of California, Minnesota and North Carolina, mandatory safety and health programs are found either under a state’s occupational safety and health program or its workers’ compensation program, but not both.36 Some states, such as Oregon, have placed their OSHA and workers’ compensation agencies under the same department to achieve efficiency and increase coordination.37 Refer to Table 3.1 for more information on state worker safety programs. States have also promoted safe workplace environments through financial incentives. In some states that partially regulate worker’s comp insurance rates, a rate credit or discount system rewards employers with superior workplace safety programs.38 Also, in a majority of states, optional medical deductibles are included in workers’ comp insurance policies.39 Legislative changes have raised the allowable deductible limits, encouraging better safety records among employers that have to pay these deductibles.40 Labor safety data indicate that similar legislative reforms in the early 1990s significantly improved workplace safety and contributed to the decline of occupational injury and illness rates. The Insurance Information Institute reported that, between 1980 and 1990, claim costs increased an average of 11 percent.41 Between 1991 and 1995, however, they increased by only 2 percent. The institute identified successful accident prevention regulations enacted in the states in early 1990s as a reason for the decline.42 According to Tony Skiff, director of workers’ education for the Connecticut Compensation Commission, “safety is the most direct, effective method of reducing workers’ compensation caseloads and costs.”43 Workplace safety initiatives, in combination with rate deregulation which is discussed below, have synergistic effects. Deregulation enhances safety initiatives because firms can evaluate individual firm records and reward good prevention practices by lower insurance rates.

Table 3.1 Workplace Safety Programs In the States

State

State OSHA Approved Program

Safety Initiatives to Limit Workers’ Compensation Costs Initiative Description

Alabama

Alaska All employers

Arizona All employers

Insurance Carrier Loss Control Regulations Carriers’ loss control plans reviewed by state Arkansas

Targeting Initiatives Hazardous employer program under WC

13

Table 3.1 Workplace Safety Programs In the States (cont.)

Safety and Health Program Laws All employers

Insurance Carrier Loss Control Regulations Loss certification program (carriers reviewed by state) California All employers

Targeting Initiatives Targeted inspection and consultation programs

Colorado

Safety Committee Laws Employers with 25 or more employees Connecticut Public sector

only Targeting Initiatives Safety committee required if employer has above average rates

Delaware

Safety Committee Laws Employers with 20 or more employees

Insurance Carrier Loss Control Regulations Various requirements affecting carrier loss control services Florida

Targeting Initiatives Employers with above average SIC injury rate plus three or more lost-time injuries within three years must implement a safety and health program

Georgia

Hawaii All employers Safety and Health Program Laws Employers with 25 or more employees

Idaho

Illinois

Indiana All employers

Iowa All employers

Kansas Insurance Carrier Loss Control Regulations Carriers must help policyholders establish a safety and health program

Kentucky All employers

Safety and Health Program Laws Employers with 15 or more employees Louisiana

Targeting Initiatives Hazardous employer law

Insurance Carrier Loss Control Regulations Various requirements affecting carrier loss control services

Maine Targeting Initiatives Employers with WC experience rating of 2 or more

must submit safety plan to state Maryland All employers

Massachusetts

Michigan All employers

Safety Committee Laws Employers with 25 or more employees

Safety and Health Program Laws All employers in certain SIC codes Minnesota All employers

Targeting Initiatives Safety committees required for certain employers who meet WC loss or injury rate criteria; also state targeted inspection program through state OSHA

Mississippi

Insurance Carrier Loss Control Regulations

Carriers must help policyholders establish a safety and health program

Missouri Insurance Carrier Loss Control Regulations Carriers must have safety engineering and management plan approved by state

Safety Committee Laws Employers with 5 or more employees Montana

Safety and Health Program Laws All employers

14

Table 3.1 Workplace Safety Programs In the States (cont.)

Safety Committee Laws All employers

Safety and Health Program Laws All employers Nebraska

Targeting Initiatives Targeted consultation program for certain employers with high injury rates

Safety Committee Laws

Employers with 25 or more employees

Safety and Health Program Laws

Employers with 11 or more employees Nevada All employers

Targeting Initiatives

Safety program required if employer meets experience rating criteria

Safety Committee Laws Employers with 10 or more employees New Hampshire

Safety and Health Program Laws Employers with 5 or more employees

New Jersey Public sector only

Insurance Carrier Loss Control Regulations Carriers must help policyholders establish a safety and health program; annual inspection required New Mexico All employers

Targeting Initiatives Hazardous employer law

New York Public sector only Targeting Initiatives

Certain employers who meet payroll requirements and experience rating criteria must establish safety and loss prevention plan

North Carolina All employers Safety program required if WC experience modification of 1.5 times the average

North Dakota

Ohio

Insurance Carrier Loss Control Regulations Carriers must help policyholders establish a safety and health program Oklahoma

Targeting Initiatives Employers targeted for safety programs if injury/illness rate is 1.25 times the average

Safety Committee Laws Employers with 11 or more employees

Insurance Carrier Loss Control Regulations Insurer loss prevention plan required (state oversight) Oregon All employers

Targeting Initiatives Safety committee required for employers with 10 or fewer employees and if lost-workday incident rate in top 10 percent

Pennsylvania

Rhode Island

South Carolina All employers

South Dakota

Tennessee All employers Targeting Initiatives Safety committees required for certain employers who meet WC experience modification criteria

Insurance Carrier Loss Control Regulations Various requirements affecting carrier loss control services Texas

Targeting Initiatives Hazardous employer law

Utah All employers Targeting Initiatives Employers with above average rates must implement a safety program

Vermont All employers

Virginia All employers

15

Table 3.1 Workplace Safety Programs In the States (cont.)

Safety Committee Laws Employers with 11 or more employees Washington All employers

Safety and Health Program Laws All employers

West Virginia Targeting Initiatives Employers with above average rates or experience modification factor must implement various requirements

Wisconsin

Wyoming All employers

Source: Matt W. Smitha, Kent R. Oestenstad and Kathleen C. Brown, “State Workers’ Compensation Reform and Workplace Safety Regulations,” Professional Safety, 46, no. 12 (Dec. 2001); U.S. Department of Labor, Occupational Safety and Health Administration, <http://www.osha.gov/fso/osp/index.html> (Jan. 13, 2004).

Early Return-to-Work Programs A timely return of an injured worker to productive employment is one of the primary functions of the workers’ compensation system.48 A successful return-to-work program incorporates three specific practices. First, an early intervention after a potential workplace injury promotes and facilitates an early return to work. Second, identifying and providing necessary return-to-work assistance, together with closely managing each worker’s case is essential for achieving return-to-work goals. Third, properly structuring cash and health benefits provides incentive for injured workers to resume employment.49 Although return-to-work programs are not mandatory for employers in most states, some states provide incentives to employers for finding ways to return injured workers to alternative work duties before their total recovery.50 Some state laws encourage injured workers to re-enter workforce by allowing insurance providers to reduce or discontinue time loss benefits if the worker refuses modified work. An employee can also risk termination for refusing to accept alternative work duty that is approved by a doctor as suitable for his or her injury.51 According to employer surveys, return-to-work programs are among the most effective cost containment strategies and are increasingly utilized by public and private entities.52 The economic opportunity in return-to-work programs is immense: many employers that have successfully established such programs have reduced the costs of lost days and indemnity/time loss payments by 25 to 50

Example 3.1 Oregon’s Workplace Injury Prevention and Early Return-to-Work Programs

In 1990, Oregon initiated joint labor-management safety committees, stiff fines for OSHA safety violations and a comprehensive public program of voluntary consultation by safety and prevention experts at individual workplaces. Despite significant benefit increases in the state, Oregon has realized workers’ comp rate reductions each year since 1991.44

Oregon encourages early return through the Employer-at-Injury Program that defrays an employer’s early return-to-work costs and reduces claim costs. The program reimburses employers for 50 percent of the early return-to-work gross wages for a maximum of three consecutive months; provides maximum of $2,500 to modify the worksite to suit the early returnee’s job duties; financially assists the employer with early return-to-work purchases such as tools, equipment and clothing required for the light-duty job; and reimburses the employer for tuition, books and fees for courses needed to update existing skills for a light-duty job.

This voluntary program, financed through the worker’s compensation tax, does not increase costs for insurers or employers.45 Insurers assist employers with identifying transitional (light-duty or modified) work, obtaining a temporary release for work from the injured worker’s medical provider and in placing the injured worker in a suitable job.

The program saves employers money on workers’ comp premiums.46 Estimates indicate that while the program used about $7.3 million in wage subsidies, it saved $10.8 million on time loss for claims closed in 2000.47

16

percent.53 Mid-sized employers (between 1,000 and 1,500 employees) have realized annual savings up to $300,000-$500,000 after implementing return-to-work programs.54 For every $1 invested in implementing a successful program an organization saves $9.55 Return-to-work programs benefit employees as well as employers. When return to work is delayed, employees risk more than their earnings. Special skills may deteriorate; the vacancy might be filled with someone else, and the long absence from work can become an obstacle in seeking future employment. In fact, workers who remain off work for six months or longer have an unemployment rate of 14 percent or more one year later.56 Timely return to work also has health benefits. Evidence suggests that engaging in limited physical activity after low-back injuries can help the employee function and reduce the possibility of long-term injury.57 Medical Cost Containment Strategies For $1 spent on workers’ compensation, about 40 cents is spent on medical care, and the rest is spent on reimbursement for lost wages.58 For a typical claim involving more than seven days of lost work, medical expenses total approximately $4,753.59 Physicians account for 33 percent of the average workers’ compensation medical payment, hospitals for 34 percent, physical and occupational therapists for 11 percent, chiropractors for 4 percent, and other medical providers, including unclassified providers, for 18 percent.60 In addition to comprising 40 percent of all workers’ compensation costs, medical costs are increasing at a very rapid rate. The policy and program options outlined below focus on helping state officials deal with these medical cost drivers. Options include:

• state provider choice laws; • health care provider networks; • fee schedules; • treatment guidelines and utilization review; • case management; and • use of generic drugs.

State lawmakers should note, however, that past successes in curbing the medical costs growth rate in group health plans have been relatively short-lived. Medical cost containment in the future will be more difficult to realize because “much of the low lying cost containment fruit was harvested in the cost containment activities of the 1990s.”61 But there are still cost savings to be captured. The central concept in health care cost containment efforts of the 1990s is the managed care arrangement. Managed care is an umbrella term that describes a wide range of systems and techniques that are used to control the utilization and costs of health care services. The core principle of managed care in workers’ compensation is the existence of special network of health care providers that contract insurers to treat the injured workers covered by the policy. In order to control health care costs, these managed care organizations perform utilization reviews, institute medical fee schedules and offer case-to-case management of claims. Managed care organizations involved in workers’ compensation have also responded to market demands by offering additional services not mandated by state regulations, such as medical bill auditing, counseling and educating businesses about workers’ comp system, and promoting early return-to-work initiatives.62 Since the proliferation of these cost-saving measures in 1990s, numerous studies have assessed their benefit for the workers’ compensation systems in the states. These studies point to a great potential of managed care techniques to curb the growth of health care costs. For example, a Washington state workers’ comp managed care pilot evaluation found that the use of managed care techniques for workers’

17

comp claims lowered costs per injury by an average of 21.5 percent, mainly due to reduction in outpatient services such as X-rays and physical therapy. 63On the downside, studies have also found lower patient satisfaction with the quality of treatment through managed care arrangements.

Provider Choice Laws States regulate injured workers’ ability to choose or change medical providers to different degrees. Twenty-four states mandate some form of restriction on employee’s choice of medical provider for a workers’ compensation claim. New York, for example, mandates selection from a list prepared by state agency. Georgia, Tennessee and Virginia mandate selection from lists maintained by employers. Ten states give the employer sole responsibility for selecting a physician to handle workers’ compensation claims. In seven states, employers make the initial selection, but after specified periods stated in the law, employees have free choice. In Arkansas, Colorado and Idaho, the initial physician selection by employer may be changed by the state agency.64 Changing a state’s law from “employee choice” to “employer choice” results in roughly 7 to 10 percent reduction in medical costs.65 The cost reduction is related to employers’ tendency to participate in health provider networks.66 Employer control over physician choice raises network involvement by 15 to 20 percent for treatment given four to nine months after an injury and by 25 to 30 percent after 10 months of treatment.67 In other words, employers are more likely to choose networks, and the cost savings come from health care

network participation, which is discussed below.

Figure 3.2 Merits and Drawbacks of Medical Cost Cutting Measures

Employer Choice of Physician Laws Pros

• Promotes the use of special provider networks • Discourages over-utilization of a medical service

Cons • Restricts employees’ flexibility and choice of physician • Can adversely affect the quality of workers’ compensation

benefits received Health Care Provider Networks

Pros • Provides medical expertise in occupational medicine • Better coordinates and integrates care for injured workers • Offers discounted prices and standardized services that

significantly reduce medical care costs Cons

• Possibility of lower patient satisfaction with delivered care because of fewer medical services offered within a network

Medical Fee Schedules Pros

• Controls medical costs by increasing the efficiency of delivering the required medical care

• Makes resolution of disputed over excessive charges easier

• Increases the consistency of procedure definitions and admissible charges

Cons • May cause medical treatment utilization to increase to

compensate for financial losses to providers

Treatment Guidelines and Utilization Reviews Pros

• Ensures that injured workers receive the right treatment at the right time

• Deters over- and under-utilization of physician services and other professional medical services and products

Cons • Limits the utility of the latest medical innovations and

discoveries • Stifles the development of more effective treatments for

injuries sustained in a constantly changing workplace environment

Promotion of Generic Drugs Pros

• Addresses the most rapidly rising group of medical costs Cons

• May not offer a generic alternative for some medications

18

Table 3.2 Medical Cost Containment Measures in the States (As of May 2001)

State Provider Fee Schedule

Mandated Bill Review

Treatment Guidelines

Mandated Utilization Review

Case Management1

Promotion of Generic Drugs2

Alabama Yes No No No No No Alaska Yes No Yes* No No No Arizona Yes No No No No No Arkansas Yes Yes Yes No Yes Yes California Yes No Yes Yes* No No Colorado Yes Yes Yes Yes Yes Yes Connecticut Yes No Yes No No No Delaware No No No No No No Florida Yes Yes Yes Yes Yes Yes Georgia Yes No No No Yes No Hawaii Yes No Yes* No No Yes Idaho Yes No No No No No Illinois No No No No No No Indiana No No No No No No Iowa No No No No No No Kansas Yes No No No No No Kentucky Yes Yes Yes Yes Yes Yes Louisiana Yes Yes No Yes No No Maine Yes No Yes Yes No Yes Maryland Yes No No No No No Massachusetts Yes No Yes Yes No No Michigan Yes Yes No Yes No Yes Minnesota Yes No Yes No Yes Yes Mississippi Yes Yes No Yes No Yes Missouri No No No No No No Montana Yes No No No Yes Yes Nebraska Yes No No No Yes No Nevada Yes Yes Yes No No Yes New Hampshire No No No No No No New Jersey No No No No Yes No New Mexico Yes No No Yes No No New York Yes No No No No No North Carolina Yes Yes Yes* No No No North Dakota Yes Yes No Yes Yes Yes Ohio Yes Yes No Yes Yes Yes Oklahoma Yes No Yes No Yes Yes Oregon Yes Yes No No Yes No Pennsylvania Yes No No No Yes No Rhode Island Yes No Yes Yes* No No South Carolina Yes Yes No No No No South Dakota Yes No Yes* No Yes No Tennessee No No No Yes Yes No Texas Yes Yes Yes Yes No Yes

19

Table 3.2 Medical Cost Containment Measures in the States (cont.)

Utah Yes No Yes Yes No No Vermont Yes No No No No Yes Virginia No No No No No No Washington Yes Yes Yes Yes No Yes West Virginia Yes Yes Yes Yes Yes Yes Wisconsin Yes No No No No No Wyoming Yes Yes Yes Yes No Yes TOTALS 41 17 21 19 17 19 1 Except Colorado and Tennessee, states do not mandate the use of medical case management outside the provider networks. Instead, managed care organizations must offer case management to be certified to handle workers’ comp cases. In Colorado, employers that opt out of a managed care arrangement must choose medical case management. In Tennessee, claims that meet certain treatment or financial criteria necessitate case management. 2 Promotion of generic drugs means that the state’s workers’ comp regulations require that a generic drug is dispensed when available unless the doctors specifies to “dispense as written.” Alaska: Treatment guidelines limit the physical therapy and chiropractic treatment utilization. California: Utilization review is required for health care organizations. If insurers or self insured employers choose to implement utilization reviews, they must follow the state standards. Colorado: In several designated counties managed care through designated organizations is mandatory. Case management is allowed in lieu of managed care organizations. If service or procedure is not specified under treatment guidelines or fee schedule, prior authorization is required. Hawaii: Guidelines set the maximum utilization level. New Hampshire: Managed care is mandated for residual markets North Carolina: Treatment guidelines limit the utilization of rehabilitation, chiropractic and physical therapy visits. North Dakota: Managed care is required only for employers with agency-approved risk management plan. Mandatory managed care includes case management, bill review, and utilization review. The exclusive state fund might contract a third party to provide these services. Rhode Island: Utilization review is required only for surgical procedures. South Dakota: Employees may obtain treatment with non-network providers only if these providers agree to abide by the terms of the agreement. Treatment guidelines stipulate duration limits and return-to-work programs. Source: Ramona P. Tanabe and Susan M. Murray, Managed Care and Medical Cost Containment in Workers’ Compensation: A National Inventory, 2001-2002. Workers Compensation Research Institute, Cambridge, Massachusetts, 2001.

Health Care Provider Networks The emergence of workers’ comp health care networks in the past decade has altered the way the workers’ comp claimants receive health care. These networks consist of health care providers that organize to contract with workers’ compensation insurance carriers to provide health care for injured workers, often at discounted prices. The use of networks for workers’ comp claims has a number of benefits. Networks often include occupational medicine specialists with competencies in recognizing and treating work-related illnesses, injuries and disabilities.68 The specialized knowledge of injury prevention, workplace hazards and the workers’ compensation system allows the specialized network physicians to better coordinate and integrate care for injured workers.69 As mentioned above, mandating employer’s choice of medical provider is one way to promote the use of preferred provider networks. Another way is to require insurance carriers to disburse payments for treating workers’ comp patients only to providers with certain occupational medicine credentials or who have participated in state-mandated workers’ compensation training.

20

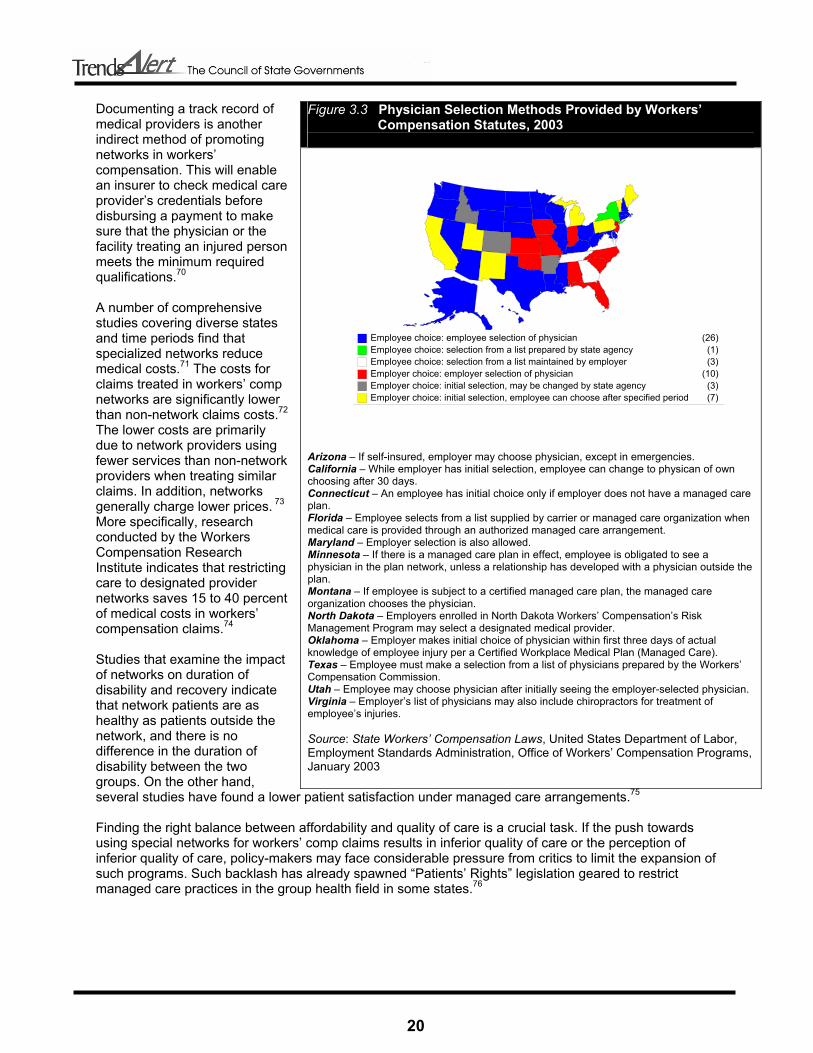

Documenting a track record of medical providers is another indirect method of promoting networks in workers’ compensation. This will enable an insurer to check medical care provider’s credentials before disbursing a payment to make sure that the physician or the facility treating an injured person meets the minimum required qualifications.70 A number of comprehensive studies covering diverse states and time periods find that specialized networks reduce medical costs.71 The costs for claims treated in workers’ comp networks are significantly lower than non-network claims costs.72 The lower costs are primarily due to network providers using fewer services than non-network providers when treating similar claims. In addition, networks generally charge lower prices. 73 More specifically, research conducted by the Workers Compensation Research Institute indicates that restricting care to designated provider networks saves 15 to 40 percent of medical costs in workers’ compensation claims.74 Studies that examine the impact of networks on duration of disability and recovery indicate that network patients are as healthy as patients outside the network, and there is no difference in the duration of disability between the two groups. On the other hand, several studies have found a lower patient satisfaction under managed care arrangements.75 Finding the right balance between affordability and quality of care is a crucial task. If the push towards using special networks for workers’ comp claims results in inferior quality of care or the perception of inferior quality of care, policy-makers may face considerable pressure from critics to limit the expansion of such programs. Such backlash has already spawned “Patients’ Rights” legislation geared to restrict managed care practices in the group health field in some states.76

Figure 3.3 Physician Selection Methods Provided by Workers’ Compensation Statutes, 2003

Arizona – If self-insured, employer may choose physician, except in emergencies. California – While employer has initial selection, employee can change to physican of own choosing after 30 days. Connecticut – An employee has initial choice only if employer does not have a managed care plan. Florida – Employee selects from a list supplied by carrier or managed care organization when medical care is provided through an authorized managed care arrangement. Maryland – Employer selection is also allowed. Minnesota – If there is a managed care plan in effect, employee is obligated to see a physician in the plan network, unless a relationship has developed with a physician outside the plan. Montana – If employee is subject to a certified managed care plan, the managed care organization chooses the physician. North Dakota – Employers enrolled in North Dakota Workers’ Compensation’s Risk Management Program may select a designated medical provider. Oklahoma – Employer makes initial choice of physician within first three days of actual knowledge of employee injury per a Certified Workplace Medical Plan (Managed Care). Texas – Employee must make a selection from a list of physicians prepared by the Workers’ Compensation Commission. Utah – Employee may choose physician after initially seeing the employer-selected physician. Virginia – Employer’s list of physicians may also include chiropractors for treatment of employee’s injuries. Source: State Workers’ Compensation Laws, United States Department of Labor, Employment Standards Administration, Office of Workers’ Compensation Programs, January 2003

Employee choice: employee selection of physician (26)Employee choice: selection from a list prepared by state agency (1)Employee choice: selection from a list maintained by employer (3)Employer choice: employer selection of physician (10)Employer choice: initial selection, may be changed by state agency (3)Employer choice: initial selection, employee can choose after specified period (7)

21

Medical Provider Fee Schedules and Bill Review Forty-one states have implemented fee schedules to set the maximum reimbursement levels for workers’ compensation claims.77 Medical fee schedules are generally determined by state workers’ compensation agencies and represent a list of predetermined payments for medical services for injured workers. Fee schedules are instrumental in restricting providers’ fees and in increasing the consistency of procedure definitions and admissible charges. Also, fee schedules make the resolution of disputes over excessive charges easier. The services covered and the methodologies for developing reimbursement levels vary widely from state to state. Medicare’s resource-based relative value scale (RBRVS) has emerged as one of the leading methods for designing fee schedules.78 In the RBRVS system, the costs of resources needed to provide services determine the payments. Three components make up the cost of providing each service: physician work, practice expense and professional liability insurance. A physician’s work accounts for, on average, 55 percent of the total relative value for each service. Physician work is determined by using such factors as the time required to perform the service; the technical skill and physical effort; the mental effort and judgment; and stress due to the potential risk to the patient. The practice expense component of the RBRVS describes the usual supplies, equipment, overhead, staff and general expenses required to perform the procedure, and accounts for an average of 42 percent of the total relative value for each service. The professional liability insurance component reflects the potential malpractice implications of the procedure and accounts for 3 percent of the total relative value.79 Bill review is the most common procedure of enforcing medical fee schedules. As a rule, bill review programs evaluate patients’ bills to make sure that charges coincide with a fee schedule, no duplicate bills are submitted and the indicated services were in fact performed. Most states rely on private insurance providers for conducting their own bill reviews and require state agencies to review bills only when a dispute develops. Seventeen states mandate regular bill review by a state workers’ compensation agency, by the insurance company paying the bill or by both. In five states, exclusive state workers’ comp funds conduct bill reviews.80 Medical fee schedules can generate a number of concerns regarding access to care, quality of care and efficiency. If health care providers are forced to turn away workers’ comp patients because the medical fee schedule doesn’t cover the cost of the care provided, an injured worker’s access to quality care is eroded. In Hawaii, for example, private health insurance pays average fees that are comparable to 135 percent of the Medicare-RBRVS, while payments to injured workers are capped at 110 percent.81 Health care providers in the state claim the disparity in payments for similar treatments is driving health care providers away from accepting workers’ compensation patients and away from the state as well.82 The quality of care for injured workers is likely to suffer if fewer health care providers are available to treat injured workers. Policy-makers should be aware that when cost containment measures such as fee schedules lower the price of medical care, providers may have an incentive to increase the number of visits and the amount of services provided to injured workers unless the number of visits is restricted. For example, although California caps the chiropractor visit fee, it places no limit on the number of visits. As a result, the average number of visits to a chiropractor on a workers’ comp claim in the state is 34, compared to 14 nationwide.83 For this reason, fee schedules will be most effective in conjunction with other measures that also limit utilization, such as utilization reviews and treatment guidelines. States should also be careful not to compromise efficiency by instituting fee schedules. Massachusetts, for example, has long had a surgical fee schedule well below the prevailing group health plan rates. As a result, few surgeons accept the formal fees and negotiations frequently precede surgeries.84 Such inefficient regulatory feature prolongs injured workers’ disability, raises surgical fees and increases payments to replace lost wages.85

22

The key to addressing these concerns is a regular revision of the workers’ compensation medical fee schedule that reflects current conditions and criteria as they apply to the injured workers’ care and treatment in the state. Medicare applies a dollar conversion factor to the relative value for a given service to convert it into a payment amount. A multiplier can be applied to the Medicare conversion factor to establish a payment level that is adequate to provide access to high quality care for injured workers. Setting the rate too low may create access problems while setting the rate too high may encourage unnecessary utilization and result in excessive program expenditures.86 To set effective rates, states can establish advisory boards that include representatives from health care providers, the insurance industry, the business community, state labor agencies and unions. The board’s duties may include monitoring updates and adjustments to the Medicare schedule and deciding whether to accept or modify similar adjustments to medical fee schedules for workers’ compensation.87

Treatment Guidelines and Utilization Review The development and use of treatment guidelines is a new but rapidly growing area in workers’ comp cost containment.88 The number of states using the treatment guidelines grew from 12 in 1996 to 20 in 2002.89 Considerable variation in treatment of similar occupational injuries, poor quality of delivered health care, evidence of inappropriate utilization of certain medical procedures and rapidly rising health care costs fueled strong interest in treatment guidelines in the 1990s.90 Guidelines provide standards for the treatment reasonably required to relieve the effects of workers’ injuries and are presumed correct unless medical opinion establishes the need for a departure from those guidelines. Such measures can ensure that injured workers receive the right treatment at the right time, control medical costs and increase the efficiency of delivering the required medical care. States can also adopt a standardized set of treatment utilization guidelines based on clinical evidence. Such guidelines will deter over- and under-utilization of physician services and other professional medical services and products.91 State workers’ comp agencies, or medical entities within the agencies, are usually responsible for developing treatment guidelines. The drafts of such guidelines may be based either on input from a special medical advisory panel or published literature and scientific studies. Because panels often include political appointees and lobbyists, a concern exists that special-interest groups might influence guidelines to promote particular agenda at the expense of efficiency and cost-effectiveness. On the other hand, guidelines based solely on scientific studies may leave out important input from individual physicians with first-hand knowledge of occupational injuries and their treatment.92 Traditionally, the drafters of workers’ compensation treatment guidelines have given more weight to the consensus of expert panels over scientific studies.93 To ensure patients’ rights, a denial of significant treatment should not be based solely on treatment guidelines. Instead, consideration of individual patient circumstances by a physician, as well as certain appeal procedures, should be a part of the workers’ compensation system.94 States that implement treatment guides may update them with adequate frequency to reflect such changes as technological innovations and medical treatment advancements. Most states with treatment guidelines have no statutory requirements for reviewing treatment guidelines and instead respond to complaints to identify outdated areas and implement changes on an “as needed” basis. Five states – Colorado, Florida, Kentucky, Massachusetts and Texas – require that guidelines be reviewed regularly. Three states – Minnesota, Nevada and North Carolina – mandate reviews but have no specific schedules.95 Also, states may want to devise means for educating medical providers about the guidelines and their updates to ensure compliance. Only South Dakota mandates informing providers about the changes in the guidelines, while most states distribute information to providers upon request.96 Utilization review is one way to make sure that guidelines are being followed. Utilization review is used by insurers to review, approve, modify or deny physicians’ requests for treating patients based on clinically accepted medical guidelines and often outside the managed care programs. Utilization review may include a case-by-case analysis of the necessity of admission and appropriate lengths of hospital stays

23

for injured workers. In some states, utilization review is produced by a peer review group, while in others by a public agency, such as a workers’ compensation commission. The number of states that mandate utilization reviews increased from nine in 1990 to 19 by 2002.97 Twelve states mandate utilization review programs for private insurers only, seven states require state agency or exclusive state fund to perform the review, and two states mandate both private insurers and state entities to carry out utilization review. Fifteen states require preauthorization for certain procedures or preadmission requirements for non-emergency hospitalization, or both. 98 As with the treatment guidelines, the states should balance the need for using utilization review against the need for easy and expedient patient access to the required health care for occupational injuries.99 Case Management Case management for workers’ compensation claims is a proactive approach that assigns a manager (usually a nurse) to an injured worker to craft individualized treatment and care plans. Although case management is usually a component of a managed care organization, insurers also employ it to improve claims-handling. The goal of case management is to ensure a comprehensive treatment plan tailored for particular health care needs of every injured worker. This plan is coordinated between the worker, the employer, the insurance carrier and the health care provider to facilitate the expedient recovery and early return to productive employment. Typically, a case manager is assigned to a patient to oversee every step of his or her treatment and recovery, including referrals to qualified specialists, expedited office visits and avoidance of treatment delays. A case manager also acts as a liaison between the patient and all the other parties involved in the claim.100 Only two states mandate case management for workers’ compensation claims; in Colorado, case management is required for employers that do not participate in managed care organizations and in Tennessee claims that meet certain treatment and/or financial criteria necessitate case management. In 18 additional states, managed care organizations are required to provide case management in order to obtain state certification for covering workers’ compensation claims.101

Promotion of Generic Drugs Drug costs have been rising faster than physician or hospital costs for workers’ comp programs.102 Most of the proven techniques of controlling costs in traditional health care programs, however, are not permitted in workers’ comp programs. Since workers’ compensation laws require that the injured employees pay nothing for their treatment, employers cannot use the financial incentives such as co-payments or deductibles to control medication utilization or costs.103 Instead, state officials can cut costs by promoting the use of less expensive generic drugs over costly brand-name alternatives for workers’ compensation programs. As of 2003, 19 states have enacted laws that require pharmacies to dispense a generic drug for workers’ comp cases but only if one exists for a given prescription and physician does not prescribe a specific non-generic drug.104 Also, the insurance industry can limit how long individuals can take certain drugs with a high potential for abuse, such as painkillers, without physician’s approval. In a related effort, Washington state is in the process of adopting drug schedules for workers’ compensation patients similar to preferred drug lists for Medicaid that promote medications deemed as effective as costlier alternatives.105 General Cost Containment Strategies Besides policy reforms targeted at stabilizing workers’ compensation costs through preventing injuries, decreasing medical costs and expeditiously returning workers to productive employment, states can consider various experience-based measures that boost system efficiency. These measures involve:

• deregulation and competitive premium rates; • alternative insurance options such as self-insurance and pooled insurance; • advisory councils; • technological innovations;

24

• streamlined workers’ compensation systems for state employees; • fraud prevention; and • curbing litigation in the state workers’ compensation systems.

Figure 3.4 Merits and Drawbacks of General Cost Cutting Measures

Deregulation and Competitive Premium Rates

Pros • Avoids extreme distortions in the market • Increases number of carriers in the market, which improves employers’ choice and may decrease

premiums • Responds to changes in costs more quickly than administered pricing • Allows market-based incentives to prevent injuries

Cons

• Can lead to excessive price-cutting and contribute to the volatility of the system

Individual and Group (Pooled) Self-Insurance Pros

• Allows employers to retain insurance investment earnings, control claims costs and improve employee relations by speeding payouts

• Provides better safety and loss control, more stable rate fluctuations and pride of ownership • No tax liability on premiums

Cons • Members share in costs when losses exceed underwriting expectations • Unpredictability of claims costs • Poor underwriting and pricing can lead to dissolution

Advisory Councils Pros