trident debt solutions stephen t. craig bankruptcy attorney professional debt negotiator...

TRANSCRIPT

TRIDENT DEBT SOLUTIONS

DEBT HAPPENS:

how to get out of debt, live debt-free, and never look back

Stephen T. CraigBankruptcy AttorneyProfessional Debt Negotiator

303-520-3414www.boulderbankruptcy.comwww.tridentdebtsolutions.com

Copyright © 2012 Trident Debt Solutions, Inc. All rights reserved.

TRIDENT DEBT SOLUTIONS2

Introduction

My law practice has been limited to debt counseling and debt relief since 1994.

I have represented more than 3,000 individuals and small businesses in the U.S. Bankruptcy Court.

I founded Trident Debt Solutions, Inc., in 2000 in order to help individuals achieve debt relief through non-bankruptcy means.

TRIDENT DEBT SOLUTIONS3

Overview

The goals of this class are to:

Explain all of the different options for getting out of debt and the pros and cons of each option

Discuss the most common money mistakes people make — and how to avoid them

Teach you how to turn the tables and go from debt to prosperity

In addition, you can also sign up for a free consultation on how to create your personal strategy for becoming debt-free.

TRIDENT DEBT SOLUTIONS4

Definitions

Unsecured Debt: Debt that has no collateral associated with it. Examples include credit card debt, medical bills, and bounced checks.

Secured Debt: Debt that is secured by collateral. Examples include mortgages, home equity loans, and car loans.

TRIDENT DEBT SOLUTIONS5

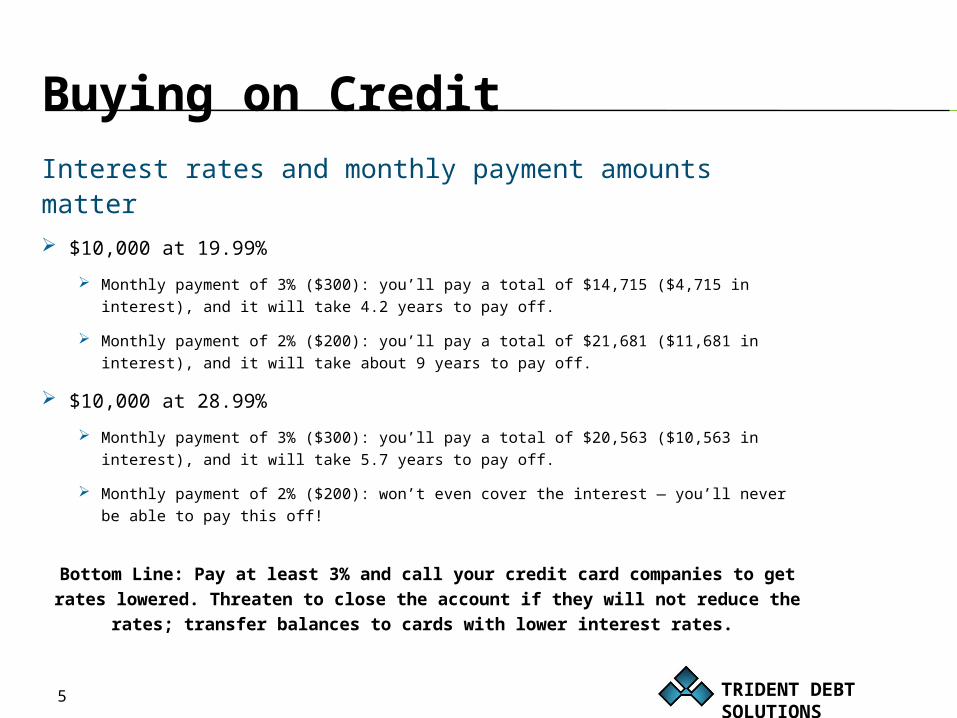

Buying on Credit

Interest rates and monthly payment amounts matter $10,000 at 19.99%

Monthly payment of 3% ($300): you’ll pay a total of $14,715 ($4,715 in interest), and it will take 4.2 years to pay off.

Monthly payment of 2% ($200): you’ll pay a total of $21,681 ($11,681 in interest), and it will take about 9 years to pay off.

$10,000 at 28.99%

Monthly payment of 3% ($300): you’ll pay a total of $20,563 ($10,563 in interest), and it will take 5.7 years to pay off.

Monthly payment of 2% ($200): won’t even cover the interest — you’ll never be able to pay this off!

Bottom Line: Pay at least 3% and call your credit card companies to get rates lowered. Threaten to close the account if they will not

reduce the rates; transfer balances to cards with lower interest rates.

TRIDENT DEBT SOLUTIONS6

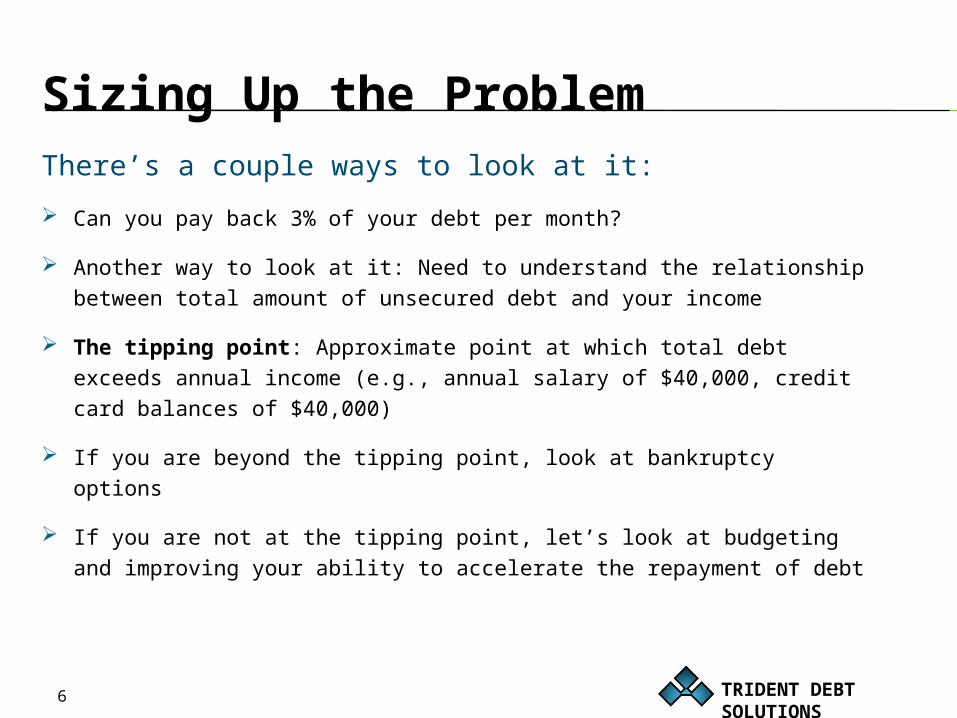

Sizing Up the ProblemThere’s a couple ways to look at it:

Can you pay back 3% of your debt per month?

Another way to look at it: Need to understand the relationship between total amount of unsecured debt and your income

The tipping point: Approximate point at which total debt exceeds annual income (e.g., annual salary of $40,000, credit card balances of $40,000)

If you are beyond the tipping point, look at bankruptcy options

If you are not at the tipping point, let’s look at budgeting and improving your ability to accelerate the repayment of debt

TRIDENT DEBT SOLUTIONS7

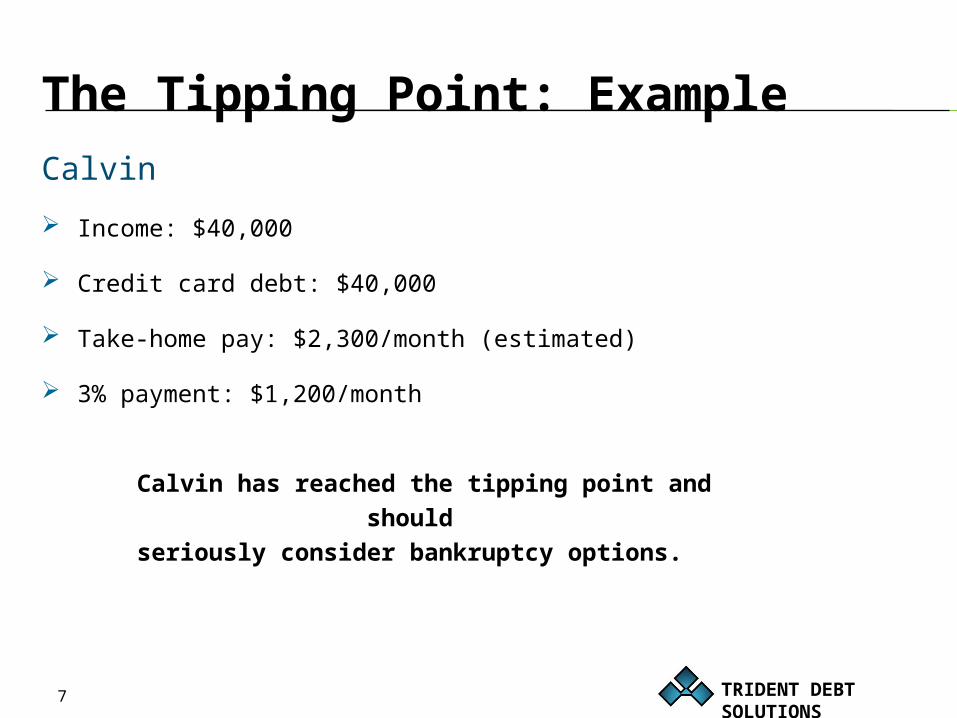

The Tipping Point: Example Calvin

Income: $40,000

Credit card debt: $40,000

Take-home pay: $2,300/month (estimated)

3% payment: $1,200/month

Calvin has reached the tipping point and should seriously consider bankruptcy options.

TRIDENT DEBT SOLUTIONS8

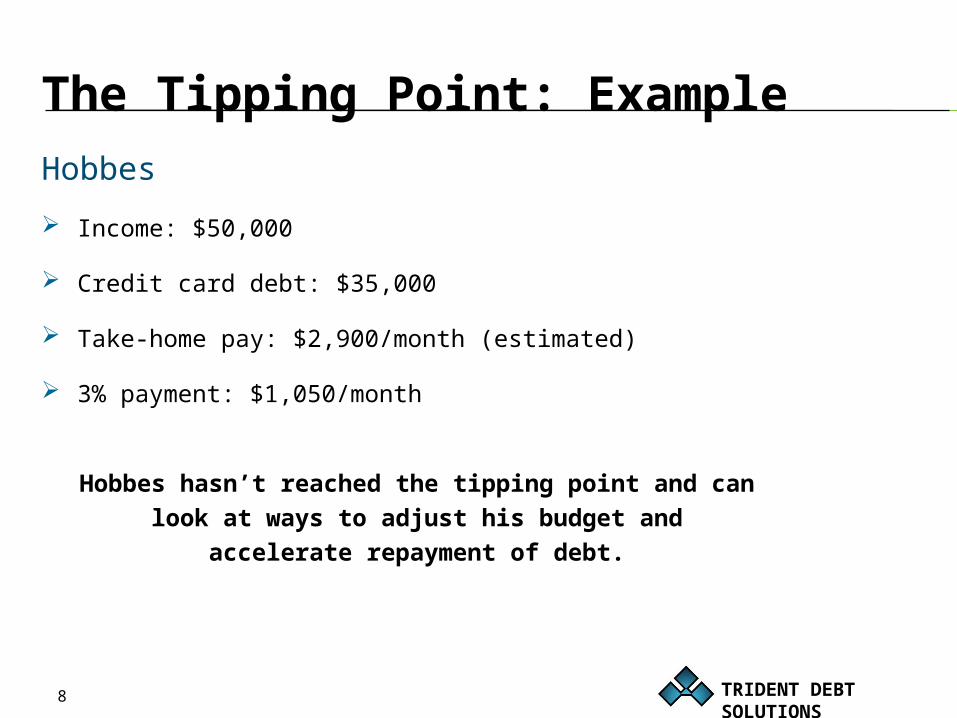

The Tipping Point: Example Hobbes

Income: $50,000

Credit card debt: $35,000

Take-home pay: $2,900/month (estimated)

3% payment: $1,050/month

Hobbes hasn’t reached the tipping point and can look at ways to adjust his budget and accelerate

repayment of debt.

TRIDENT DEBT SOLUTIONS9

Knowledge Is PowerWhere Does the Money Go?

You have no control over your finances until you know where your money goes

Keep track of every dollar spent for two months — cash, checks, online bill-pay, debit cards — everything!

Don’t leave anything out, no matter how small

Rule of thumb: Combined cost of mortgage/rent and car payment should not exceed 40% of net monthly income

Nothing happens without a plan

TRIDENT DEBT SOLUTIONS10

Knowledge Is Power

Finding the “Latte Factor”

Coffee shop/snacks Eating out Magazines Gifts Lottery tickets Parking Cash-register impulse buys ATM fees Bank fees/late charges Bottled water Cigarettes

What seems like “just a couple bucks”

here and there can add up to more than you

think!

TRIDENT DEBT SOLUTIONS11 11

Little Things Mean a Lot

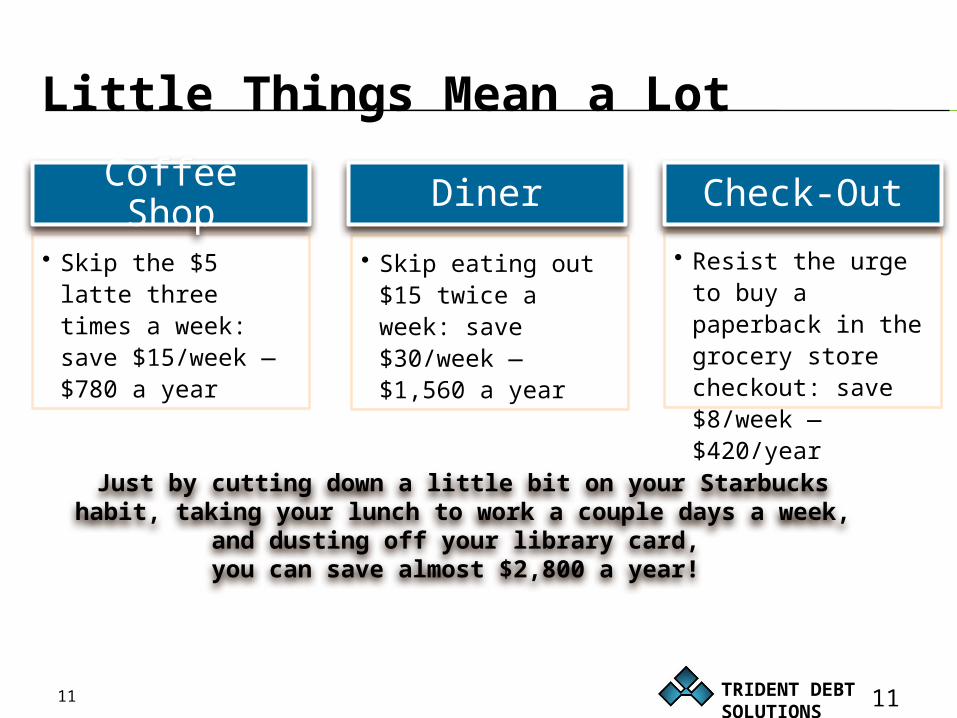

• Skip the $5 latte three times a week: save $15/week — $780 a year

Coffee Shop

• Skip eating out $15 twice a week: save $30/week — $1,560 a year

Diner

• Resist the urge to buy a paperback in the grocery store checkout: save $8/week — $420/year

Check-Out

Just by cutting down a little bit on your Starbucks habit, taking your lunch to work a couple days a week, and

dusting off your library card, you can save almost $2,800 a year!

TRIDENT DEBT SOLUTIONS12

Reducing Your Monthly Overhead Keep monthly recurring expenses as low as possible

Insurance

Rent

Premium cable

Phone bills

Car payment and related auto insurance

Taxes: increase your exemptions if you usually get a refund — get more cash on your paycheck

Don’t be “house poor” — reduce these payments if you can

TRIDENT DEBT SOLUTIONS13

Becoming Debt-Free

YOU HAVE OPTIONS!

TRIDENT DEBT SOLUTIONS14 14

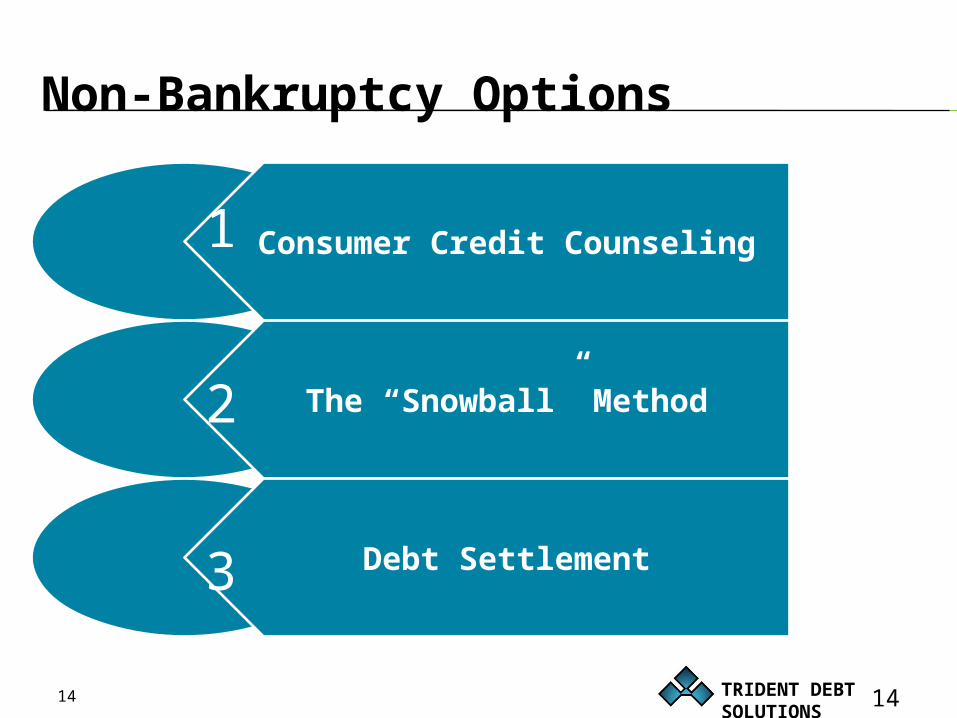

Non-Bankruptcy Options

Consumer Credit Counseling

The “Snowball” Method

Debt Settlement

1

2

3

TRIDENT DEBT SOLUTIONS15

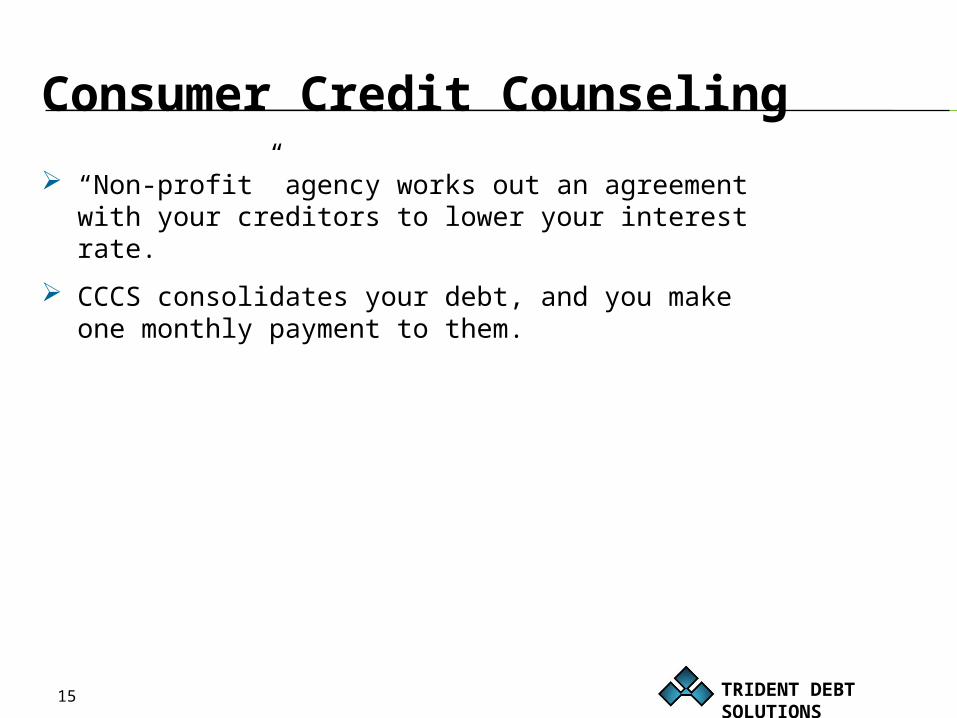

Consumer Credit Counseling

“Non-profit” agency works out an agreement with your creditors to lower your interest rate.

CCCS consolidates your debt, and you make one monthly payment to them.

TRIDENT DEBT SOLUTIONS16

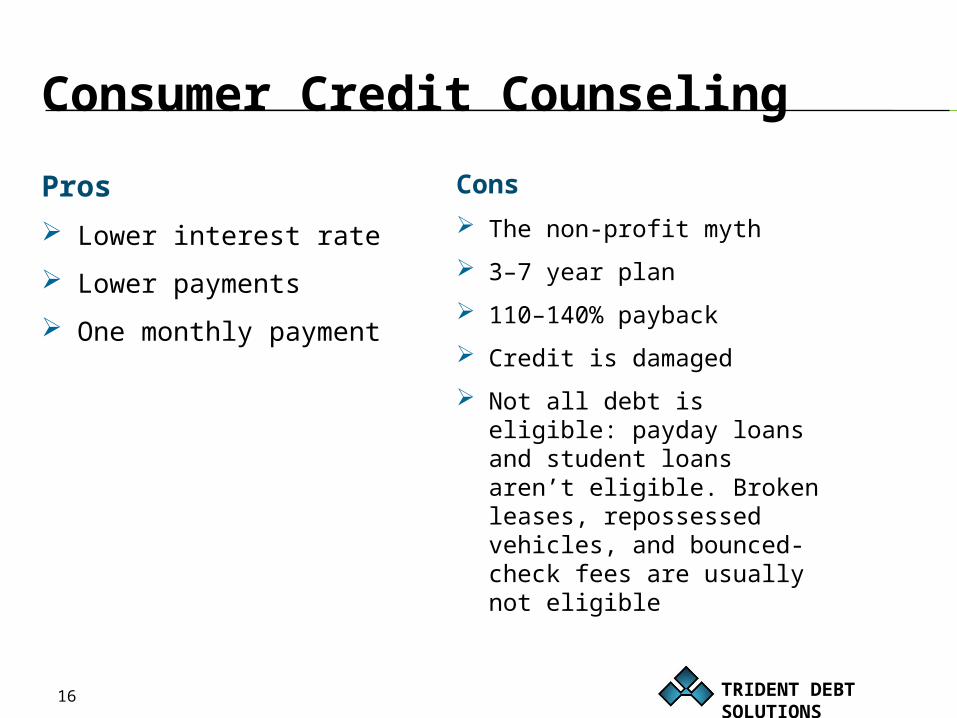

Consumer Credit Counseling

Pros

Lower interest rate

Lower payments

One monthly payment

Cons

The non-profit myth

3–7 year plan

110–140% payback

Credit is damaged

Not all debt is eligible: payday loans and student loans aren’t eligible. Broken leases, repossessed vehicles, and bounced-check fees are usually not eligible

TRIDENT DEBT SOLUTIONS17

Optimal Candidate for CCC

Almost no one, but it can be okay for someone who…

Makes an average income

Has credit card or medical debt of less than $20,000

TRIDENT DEBT SOLUTIONS18

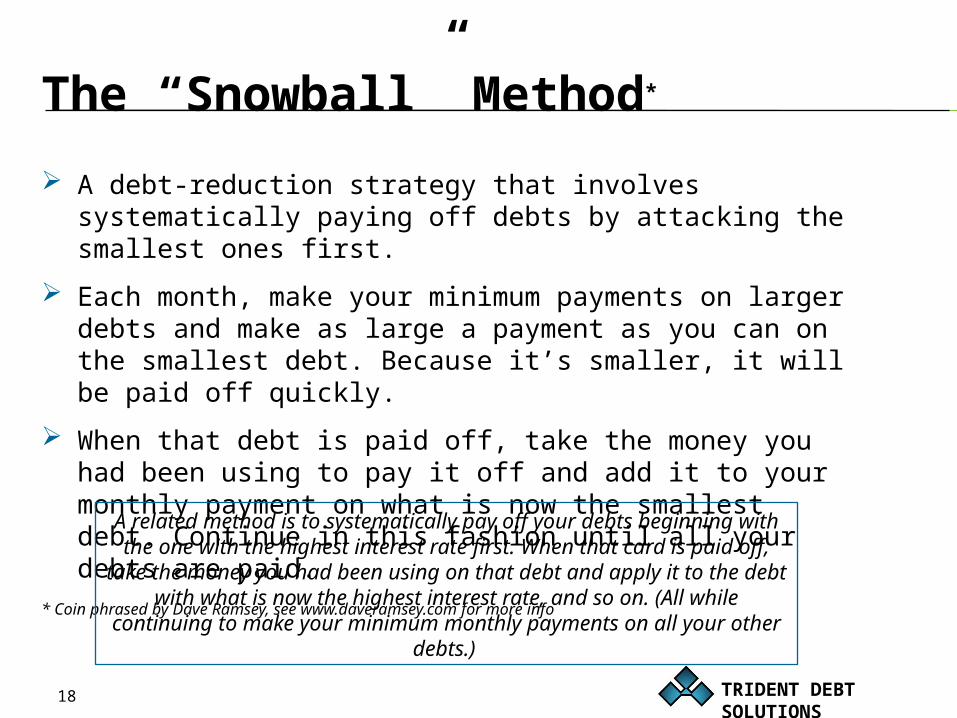

The “Snowball” Method*

A debt-reduction strategy that involves systematically paying off debts by attacking the smallest ones first.

Each month, make your minimum payments on larger debts and make as large a payment as you can on the smallest debt. Because it’s smaller, it will be paid off quickly.

When that debt is paid off, take the money you had been using to pay it off and add it to your monthly payment on what is now the smallest debt. Continue in this fashion until all your debts are paid.

* Coin phrased by Dave Ramsey, see www.daveramsey.com for more infoA related method is to systematically pay off your debts

beginning with the one with the highest interest rate first. When that card is paid off, take the money you had been using

on that debt and apply it to the debt with what is now the highest interest rate, and so on. (All while continuing to make your minimum monthly payments on all your other debts.)

TRIDENT DEBT SOLUTIONS19

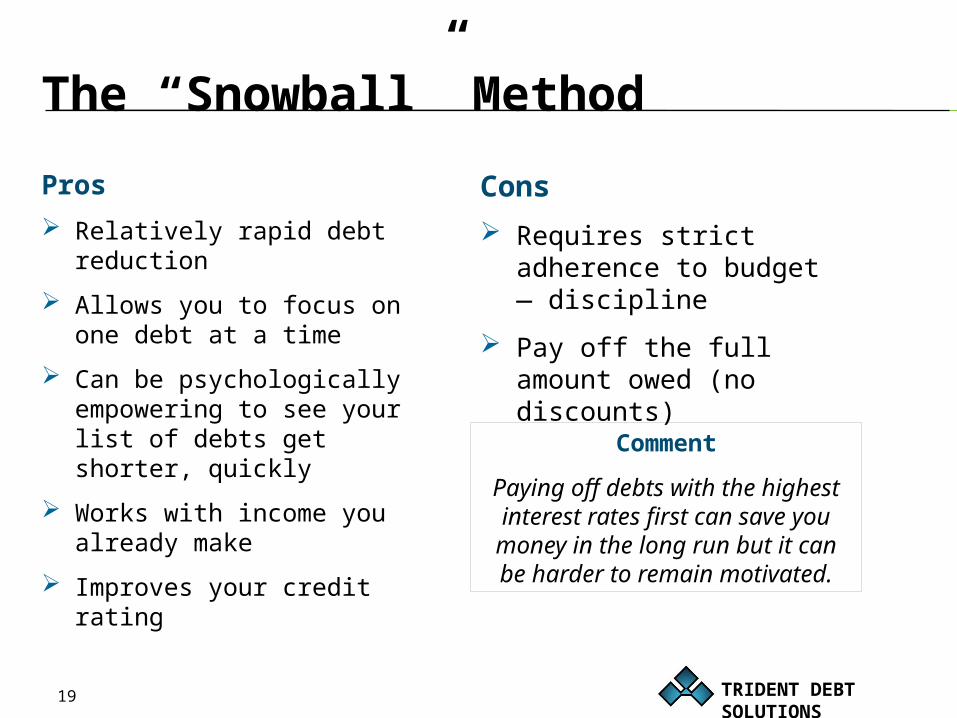

The “Snowball” Method

Pros

Relatively rapid debt reduction

Allows you to focus on one debt at a time

Can be psychologically empowering to see your list of debts get shorter, quickly

Works with income you already make

Improves your credit rating

Cons

Requires strict adherence to budget — discipline

Pay off the full amount owed (no discounts)

Comment

Paying off debts with the highest interest rates first can save you money in the long run but it can be harder to

remain motivated.

TRIDENT DEBT SOLUTIONS20

The “Snowball” Method

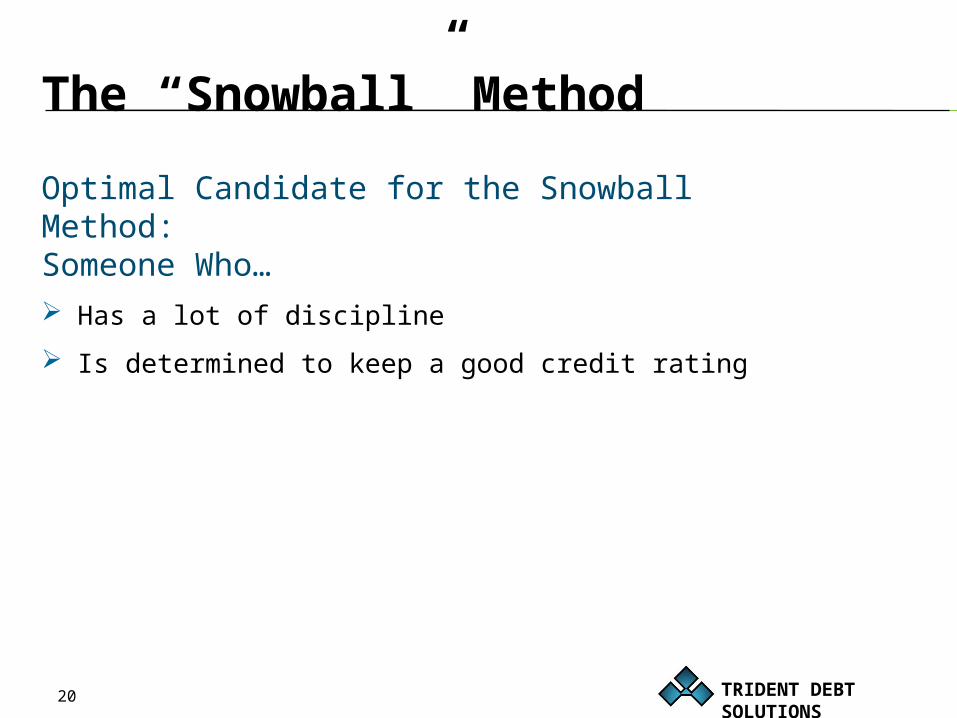

Optimal Candidate for the Snowball Method: Someone Who… Has a lot of discipline

Is determined to keep a good credit rating

TRIDENT DEBT SOLUTIONS21

Debt Settlement

Also referred to as debt negotiation, debt settlement is the art of negotiating with your creditors so they will accept less than the full amount of the debt owed to them, generally 50–65 cents on the dollar, in full satisfaction of the debt.

TRIDENT DEBT SOLUTIONS22

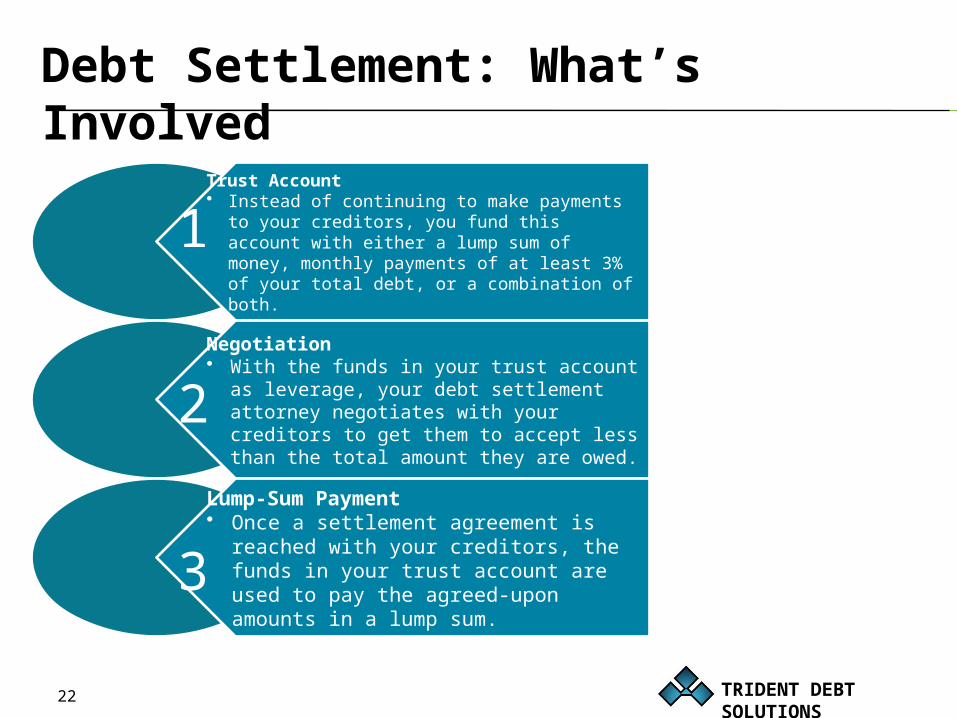

Debt Settlement: What’s Involved

Trust Account• Instead of continuing to make payments

to your creditors, you fund this account with either a lump sum of money, monthly payments of at least 3% of your total debt, or a combination of both.

Negotiation• With the funds in your trust account as

leverage, your debt settlement attorney negotiates with your creditors to get them to accept less than the total amount they are owed.

Lump-Sum Payment• Once a settlement agreement is

reached with your creditors, the funds in your trust account are used to pay the agreed-upon amounts in a lump sum.

1

2

3

TRIDENT DEBT SOLUTIONS23

Debt Settlement

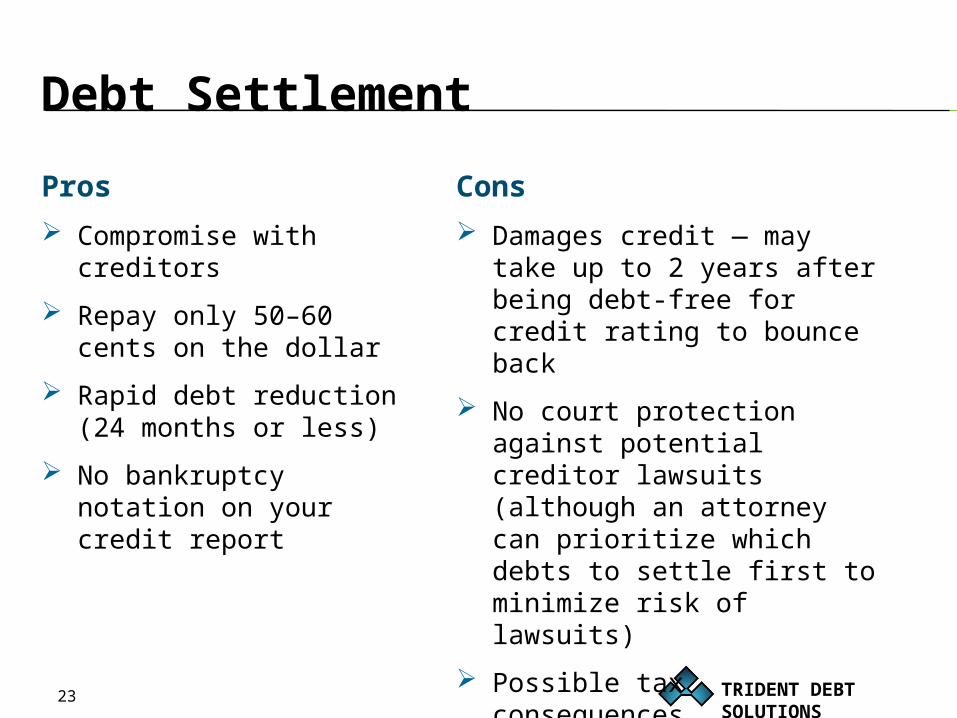

Pros

Compromise with creditors

Repay only 50–60 cents on the dollar

Rapid debt reduction (24 months or less)

No bankruptcy notation on your credit report

Cons

Damages credit — may take up to 2 years after being debt-free for credit rating to bounce back

No court protection against potential creditor lawsuits (although an attorney can prioritize which debts to settle first to minimize risk of lawsuits)

Possible tax consequences

TRIDENT DEBT SOLUTIONS24

Debt Settlement

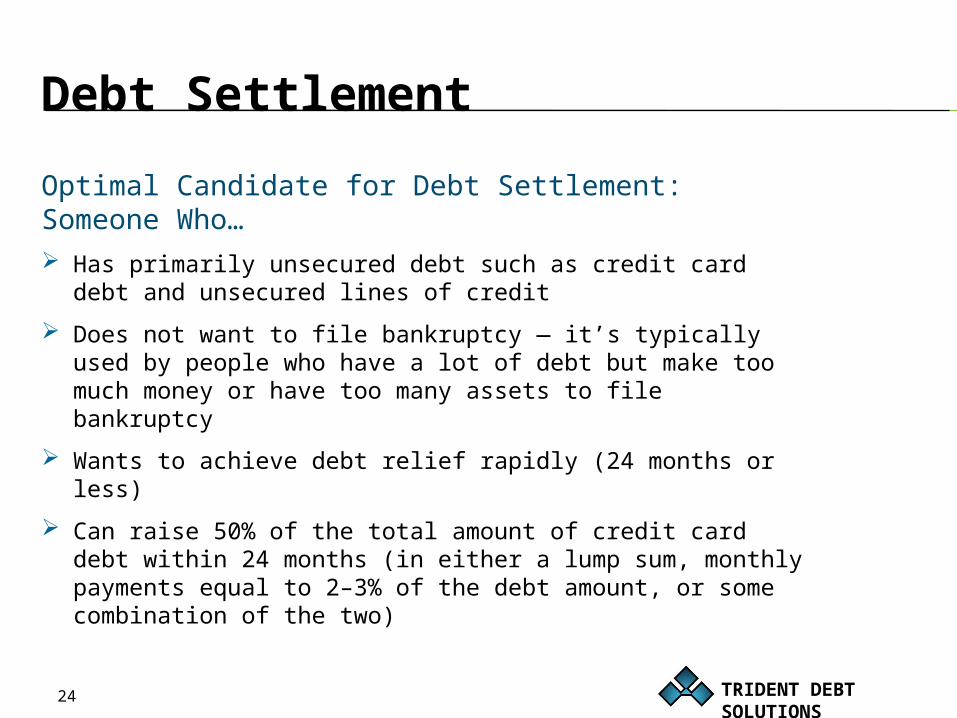

Optimal Candidate for Debt Settlement: Someone Who… Has primarily unsecured debt such as credit card debt

and unsecured lines of credit

Does not want to file bankruptcy — it’s typically used by people who have a lot of debt but make too much money or have too many assets to file bankruptcy

Wants to achieve debt relief rapidly (24 months or less)

Can raise 50% of the total amount of credit card debt within 24 months (in either a lump sum, monthly payments equal to 2–3% of the debt amount, or some combination of the two)

TRIDENT DEBT SOLUTIONS25

Debt Settlement Example

Hobbes Hobbes has $40,000 of credit card debt.

He has a lump sum of money available and gives $24,000 to his attorney to deposit in his trust account.

Within six months, his attorney has completed negotiations with all of Hobbes’ creditors, settling the debts for $22,500 — a savings of nearly 44%!

Hobbes is now out of debt and receives a refund of $1,500 from his attorney.

TRIDENT DEBT SOLUTIONS26

Debt Settlement Example

Calvin Calvin has $80,000 of debt consisting of credit cards

and unsecured lines of credit.

He does not have a lump sum of money available but can put $2,000/month in his trust account if he stops making his regular credit card payments.

Calvin makes 23 monthly payments and is out of debt for $46,000.

TRIDENT DEBT SOLUTIONS27

What If You Do Nothing?

Understanding the Collection Process Consider the stress of hiding from creditors

May be advisable if the statute of limitations on the debt is nearly up (varies by state: in Colorado, it’s 6 years)

Can use Cease Communications letter to stop creditor calls (doesn’t stop collection process)

Wage garnishment in Colorado: 25% of net income

Social Security income cannot be garnished

No one can garnish your wages without a court order

If court issues a judgment against you, creditor can garnish not only your wages but also your bank account, and can put a lien on any real estate you own

TRIDENT DEBT SOLUTIONS28

Bankruptcy Options

Chapter 7 Bankruptcy

Chapter 13 Bankruptcy

1

2

TRIDENT DEBT SOLUTIONS29

Chapter 7 Bankruptcy: Overview

Also referred to as a “liquidation” bankruptcy, Chapter 7 bankruptcy involves filing a petition asking the court to discharge your unsecured debts.

Chapter 7 bankruptcy is usually a good option for people who have high debt and limited income or assets.

It is intended to give individuals a fresh start.

“Exempt assets” — you can keep limited assets when their value falls below pre-established thresholds.*

“Non-exempt assets” — assets that exceed the allowed values — are sold, and the proceeds are distributed to creditors.

Any debts that remain after the assets are liquidated and creditors paid are then discharged by the court.

IRAs are exempt and cannot be attached by creditors.

* http://www.thebankruptcysite.org/exemptions/colorado.html

TRIDENT DEBT SOLUTIONS30

Chapter 7 Bankruptcy: Process

After meeting with your attorney, you stop making your unsecured payments.

You attorney gives you a packet to fill out, which will detail your income, expenses, assets, and liabilities.

From this packet, a Voluntary Petition is filed with the U.S. Bankruptcy Court.

6 weeks later you have a short hearing with the court-appointed Bankruptcy Trustee.

60 days later you receive a discharge order relieving you of your unsecured debts.

TRIDENT DEBT SOLUTIONS31

Chapter 7 Bankruptcy

Pros

Receive a “fresh start”

All unsecured debt is wiped out completely

Emotional weight is lifted quickly

Immediately stops all collection activity against you

Can usually keep home, car and other assets

Cons

Will remain on your credit for 10 years, but the practical effect is more like 3 years

You surrender non-exempt assets, if any

You must come to grips with it emotionally

Student loans, most taxes are non-dischargeable

TRIDENT DEBT SOLUTIONS32

Chapter 7 Bankruptcy

Optimal Candidate for Chapter 7 Bankruptcy: Someone Who… Has below-median income (varies by state*).

(Gross monthly income is calculated by taking your income for the six months prior to filing, doubling it, and dividing by 12)

Has a high amount of debt (more than $20,000) and no reasonable expectation of ability to pay

Has no significant assets other than those allowed by state exemptions

* http://www.justice.gov/ust/eo/bapcpa/20111101/bci_data/median_income_table.htm

TRIDENT DEBT SOLUTIONS33

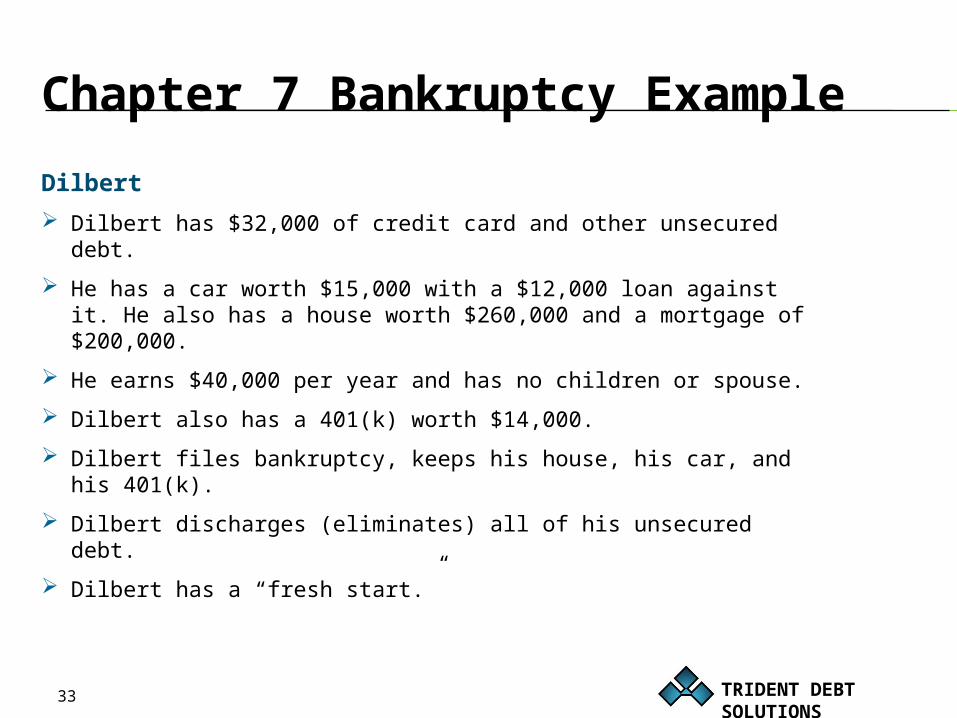

Chapter 7 Bankruptcy Example

Dilbert

Dilbert has $32,000 of credit card and other unsecured debt.

He has a car worth $15,000 with a $12,000 loan against it. He also has a house worth $260,000 and a mortgage of $200,000.

He earns $40,000 per year and has no children or spouse.

Dilbert also has a 401(k) worth $14,000.

Dilbert files bankruptcy, keeps his house, his car, and his 401(k).

Dilbert discharges (eliminates) all of his unsecured debt.

Dilbert has a “fresh start.”

TRIDENT DEBT SOLUTIONS34

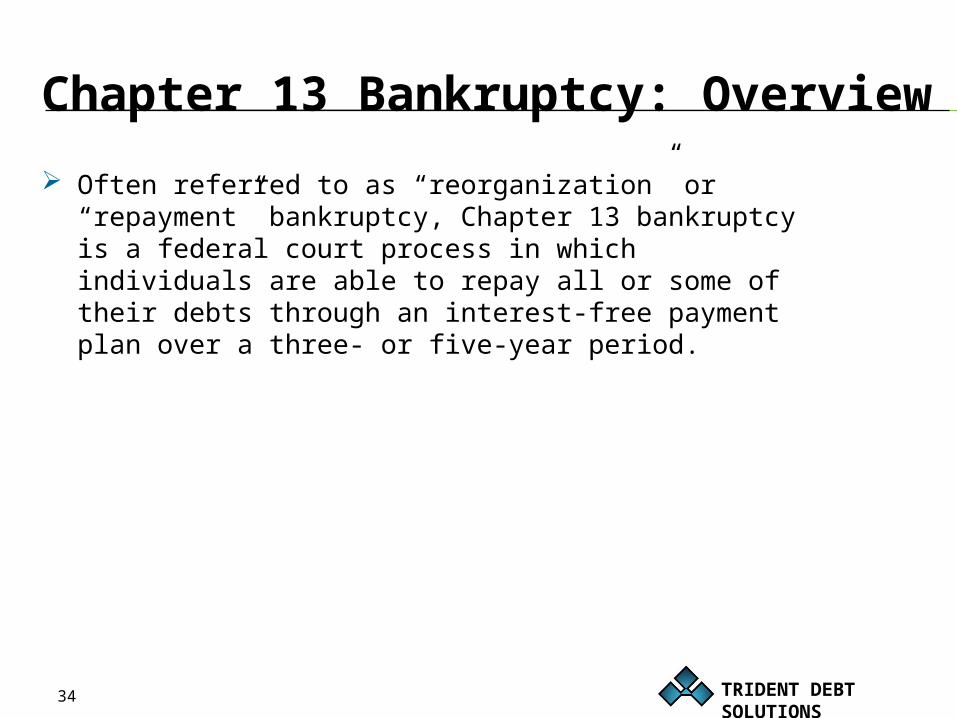

Chapter 13 Bankruptcy: Overview Often referred to as “reorganization” or “repayment”

bankruptcy, Chapter 13 bankruptcy is a federal court process in which individuals are able to repay all or some of their debts through an interest-free payment plan over a three- or five-year period.

TRIDENT DEBT SOLUTIONS35

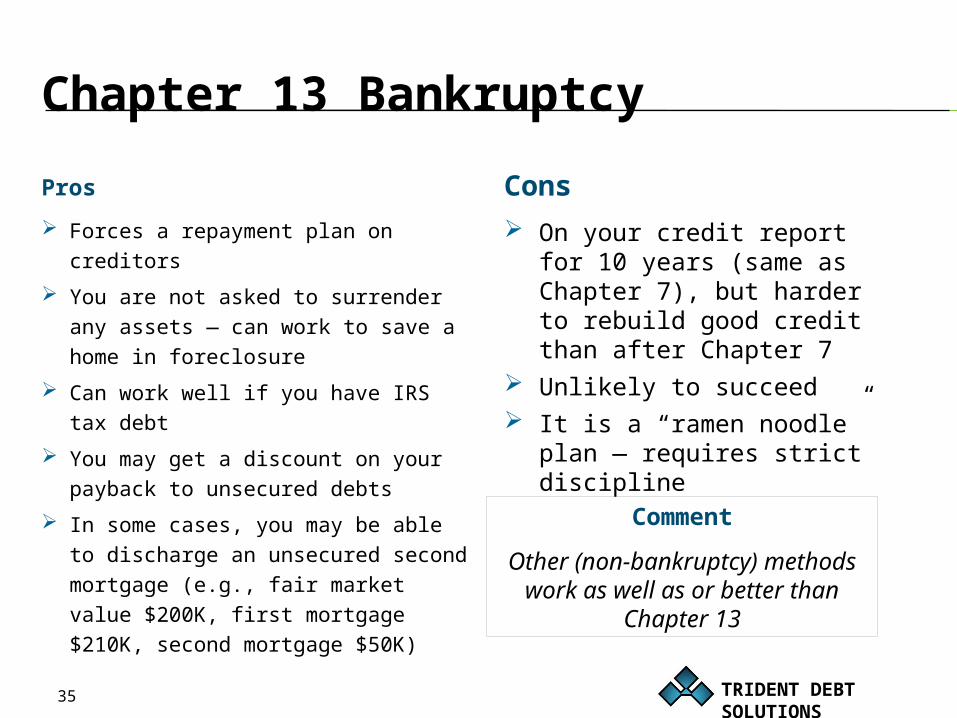

Chapter 13 Bankruptcy

Pros

Forces a repayment plan on creditors

You are not asked to surrender any assets — can work to save a home in foreclosure

Can work well if you have IRS tax debt

You may get a discount on your payback to unsecured debts

In some cases, you may be able to discharge an unsecured second mortgage (e.g., fair market value $200K, first mortgage $210K, second mortgage $50K)

Cons

On your credit report for 10 years (same as Chapter 7), but harder to rebuild good credit than after Chapter 7

Unlikely to succeed It is a “ramen noodle”

plan — requires strict discipline

Comment

Other (non-bankruptcy) methods work as well as or

better than Chapter 13

TRIDENT DEBT SOLUTIONS36

Chapter 13 Bankruptcy

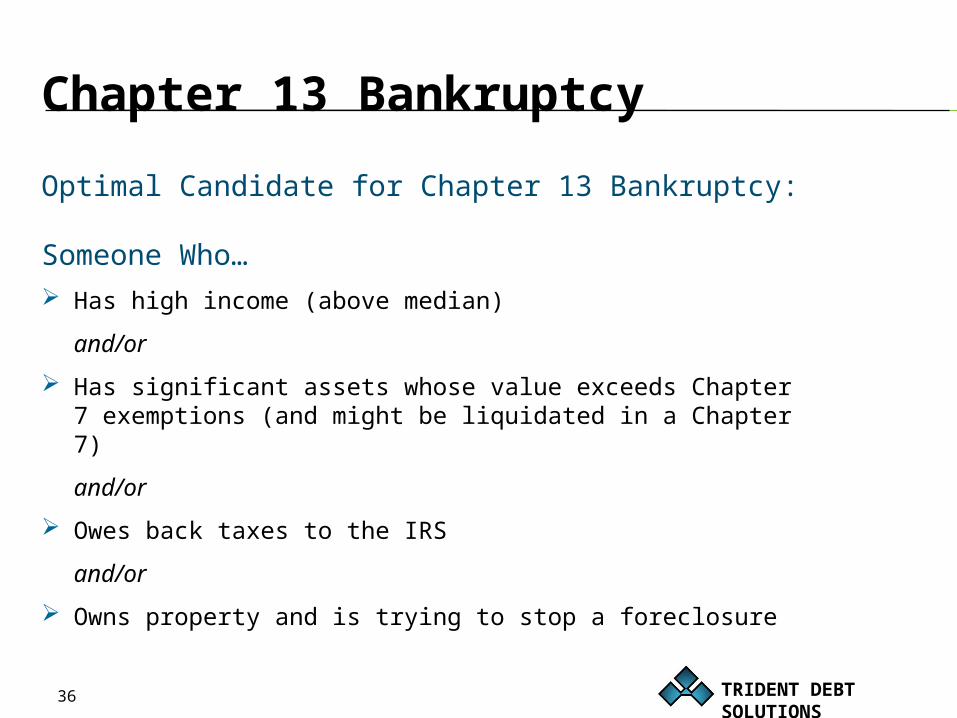

Optimal Candidate for Chapter 13 Bankruptcy: Someone Who… Has high income (above median)

and/or

Has significant assets whose value exceeds Chapter 7 exemptions (and might be liquidated in a Chapter 7)

and/or

Owes back taxes to the IRS

and/or

Owns property and is trying to stop a foreclosure

TRIDENT DEBT SOLUTIONS37

Life After Debt

Doing It Differently:

The Debt-Free Mindset

TRIDENT DEBT SOLUTIONS38

Debt: Avoid It Like the Plague

This should be your mantra

Live simply and your wealth will grow

If you can’t pay for it in cash don’t buy it

Don’t borrow to look rich

Example: $2,000 TV – financed at 29.9% interest at $60/month — really costs you $4,300

Compare that to a craigslist purchase

Use student loans with caution

TRIDENT DEBT SOLUTIONS39

Psychology of Spending

Thinking it through: avoid the “sugar high” of impulse purchases 24-hour rule: If you see something you want to buy,

wait 24 hours. If you still feel a need for the item, then buy it.

Don’t use credit to buy something you won’t have when you get the bill (e.g., eating out, movies, concert tickets)

Reduce trips to places like the mall, Costco, Target, etc. (where you go in for one thing and come out with five)

Resist the urge to buy something you see at the check-out stand — point-of-purchase impulse buying

TRIDENT DEBT SOLUTIONS40

Psychology of Spending

Intention — Ask yourself these questions: Do I need this? Or do I want this?

Who am I trying to impress? (“keeping up with Joneses”)

Will this purchase improve the quality of my life?

Can I buy this used for half-price?

Am I paying for form over function?

Develop a “frugal is good” mindset versus need for instant gratification —

be “value conscious”!

TRIDENT DEBT SOLUTIONS41

Marginal Utility Theory

The most important rule of spending! It’s about the amount of benefit or value derived from

consuming one additional unit of a product or service – in other words, whether the relative benefit or value of spending more for something is proportionate to the increased cost

Illustration: Is a $20,000 car twice as useful as a $10,000 car? Is an $80,000 car four times as useful?

Illustration: Does music sound three times better out of $900 speakers than out of $300 speakers? Will you get three times as much enjoyment from the $900 speakers?

This bears repeating: Be “value conscious”!

TRIDENT DEBT SOLUTIONS42

Pay For Cars With Cash

Don’t be “car poor” Using cash to buy cars is a common denominator

among wealthy people Having a high car payment is a common denominator

among people filing for bankruptcy Depreciating assets (cars, mobile/motor homes, boats,

ATVs, etc.) are not “investments”: by the time they are paid off, they have lost a large portion of their original value

TRIDENT DEBT SOLUTIONS43

Using Credit: Basics

If you must have a credit card, never have more than three

Avoid approaching the credit limit on your credit card or line of credit

Pay the full balance every month

Dispute any item you do not agree with

Must dispute with all three credit-reporting bureaus

Experian

TransUnion

Equifax

Focusing on FICO score: the old way of thinking

TRIDENT DEBT SOLUTIONS44

Money Mistakes to Avoid

Refinancing your home to pull out cash

Asking someone to co-sign a loan; being a co-signor on a loan

Getting friends involved in your finances (borrowing money from them, loaning money to them)

Cashing-out your IRA — consult an attorney and/or CPA first

Taking advice from a commissioned sales person

“Investing” in depreciating assets such as mobile homes and cars

Owing the IRS

Taking out a “payday loan”

Assuming spouse debt

Maintaining an “overdraft” line of credit

Having more than three credit cards

TRIDENT DEBT SOLUTIONS45

Life After Debt

Achieving Financial Prosperity

TRIDENT DEBT SOLUTIONS46

Pay Yourself First

Developing a Savings Plan Save 10% of everything you earn

Make savings automatic

Squirrel money away where you can’t get to it easily

Annually compounded interest dramatically increases the value of your savings.

Example: $10/day for 20 years, 10% return = $227,881!

Rule of 72 (72 divided by rate of return = # of years it will take to double money)

TRIDENT DEBT SOLUTIONS47

IRAs and 401(k)

Invest the maximum amount allowed by law, every year

Employer-matched 401(k): it’s a “no-brainer”

Do not cash them in to pay off credit cards

Tax consequences of early withdrawals

The amazing one-person 401(k) for self-employed

Don’t put more than 20% of your 401(k) in your employer’s company stock

TRIDENT DEBT SOLUTIONS48

Understanding Mortgages

Good strategies Fixed-rate mortgages

Short-term mortgages

Income tax deductions

Paying extra on your mortgage

Bi-weekly payment plan

Paying your mortgage off

Not-so-good strategies Variable-rate mortgages

Long-term (40- or 50-year) mortgages

Interest-only mortgages

Mortgage insurance

TRIDENT DEBT SOLUTIONS49

Habits of Financially Savvy People Pay for cars with cash Pay yourself first Have two to three sources of income (look for “passive”

income) Make additional payments on mortgage principal Invest in education, other ways to increase earning

capacity Reinvest profits Get paid for results not by the hour Think long-term rather than short-term Keep monthly overhead low — watch small expenses Avoid debt like the plague!

TRIDENT DEBT SOLUTIONS50

A Word on Greed

Revisiting the theory of marginal utility Money has its own diminishing returns

More is not necessarily better

Strive for simplicity

Frugal is good

Be value-conscious

TRIDENT DEBT SOLUTIONS

Thank You!

Stephen T. CraigBankruptcy AttorneyProfessional Debt Negotiator

303-520-3414www.boulderbankruptcy.comwww.tridentdebtsolutions.com

Don’t forget to sign up with Steve for your free consultation.

Copyright © 2012 Trident Debt Solutions, Inc. All rights reserved.