tt emba• - shodhganga.inflibnet.ac.inshodhganga.inflibnet.ac.in/bitstream/10603/14449/7/07_chapter...

TRANSCRIPT

• MD usa »BVaoPE1l co~tts ..... JMPBMTt.VJS Ol? V~B

a• <J.f t.be waJ<»: funotioftt:J. ot the »tP .tf#· to prov.l«e

fin~al as~1$Mnee to tte ~\'lttttl$$• tt ~y ~

··be· ttO:tU&tl that the l•s ~eloped 00\11ltt!• whteh a~r• poytngo

. to emba• <$ tile path <:;t ~~ deve1o~t. tryittg t()

~bJ.eve Enitlf••~Ua~• and .$el~suS'ttaln~ Qliowtb. need mre

fthlm~1e.1 a-.sit!tam;e t~ 4o tbo ~e~ =~r.tu q.f ~~·

~ toll$ ~ p#Ol>l• La ~l$t t.~e le- ~eloPfid ~td••

&J'~ ak~ ·lfm4• heavy de~ Whtle at the ~tame tim(!' i!bd)1

re.quiJi~t$ of ~s~ltt$1 flu~• ~~~ on the i~t'~ae.t

in fa~::~:t" Wbtat u ru•;~4-e-4 is t:h$t tho~ developino QOtmw£•

sh0ul4 i'ft'tl $Oft loQfJ tn'Yb).:;;.ttag easy~ and. eona!.~ns

a~cl st.l.Cb lO&N sbQ'u14 enable them. to acbie'fte .QCo~ •uto:nomv

~- ~ lfmt .t"Uft• If'Qw :£$,t JMr· ba& £ulfi.1led the as~tloM

of tl\ese 4we1opiltg co~.ltis ol t;btt tbl~ we>r14t llut., t.he

tel• o~ IMP a economic 4eve~ent of these ~ttrt• cannot

be etrakated unleaa we w<!ertft.and their :e)laracte!fLstf.(.ts, needs

of u~~ ~- and th•~ 1ocaUQn$.· ~ the ~t.t

of the wor16: ~ml'• 1'hetefotttt'* the .starting point has to

<:ondd..- 'Url4er~lopn$nt tn ~:r-~tLve.,.

-~~t_ID_!«SR!S$.&1rJi,

~hrougbout the U~t'Ure on •neve1opment EQ;)nom1«:13••

onG una. ~ ·.mul:tiplid.t? o.f J.nt.~ang-bl.e -te:ans ~ es ·tbe

65

·~ \fCI'ld~•, 'dev'eloPbio ·eonntr::wJ: "Ut~4'e~elo~

eol.llltd.e$•,.·~ •.1~•*' ~4E!lrel.Q~ C9Uf.lttt•'• <JJ:" the JS()uth',•

Although •1'$ .a~p.ri.~~eaeJ~$ o! .~ ~$\~S!Qn. ,ts ps~!~

able in i'ts own 1!igbt, ftle\re;ltt~ng *ZO~%'J.est ,I.e ~bab.ly t'he·

mot;~t·~nt•tious term• ltt impU~ all o~b·•g·ptoe~s of

devehl~l)t on tb$ part ()f the ~ottntneo eo-ncern~ implytnq

that t:MY ate ''eatehtn'Q' ~~· with ~ i~du$tr5,al.;L$ed co~ti®

. tcEttobJ.ng u.p ~.as Upol\ ~lat!ve ~wth ;t&.·~·~· A ~

may d$V'~11>P ~4 flt~.11 npt •catch ·~.,}. Thi9 t~ •·~ S utb' ~-.. ,....b it..~-~ ... ,.. 1t....__-... ,v.e .. 1'1lt !i'V'!iftit'tar """'·· ""--~ - .,ftA . Q' ' ... ,. ,,,~.:q~ ~~lil ~,a;.~,.;l.l(J·~ ~~4. I~· #c~.1"""'S~

.i:tl a ~·P'Oli~al c:ont~ ~~ td..ll ·be -~~ a~at.~ iio

isll 1A Une· w.tth WO.t'ld S$$3 and 'a<~opt. the t~ •·~& owe~~ ~~lee' (because the t:m:rn .. ~$$ D~$l.opE!do: tnd.f.~,

cates $ comparison Yltth.. developed ®t&n~d~s.) ,. The 'lfO::tld Banlt

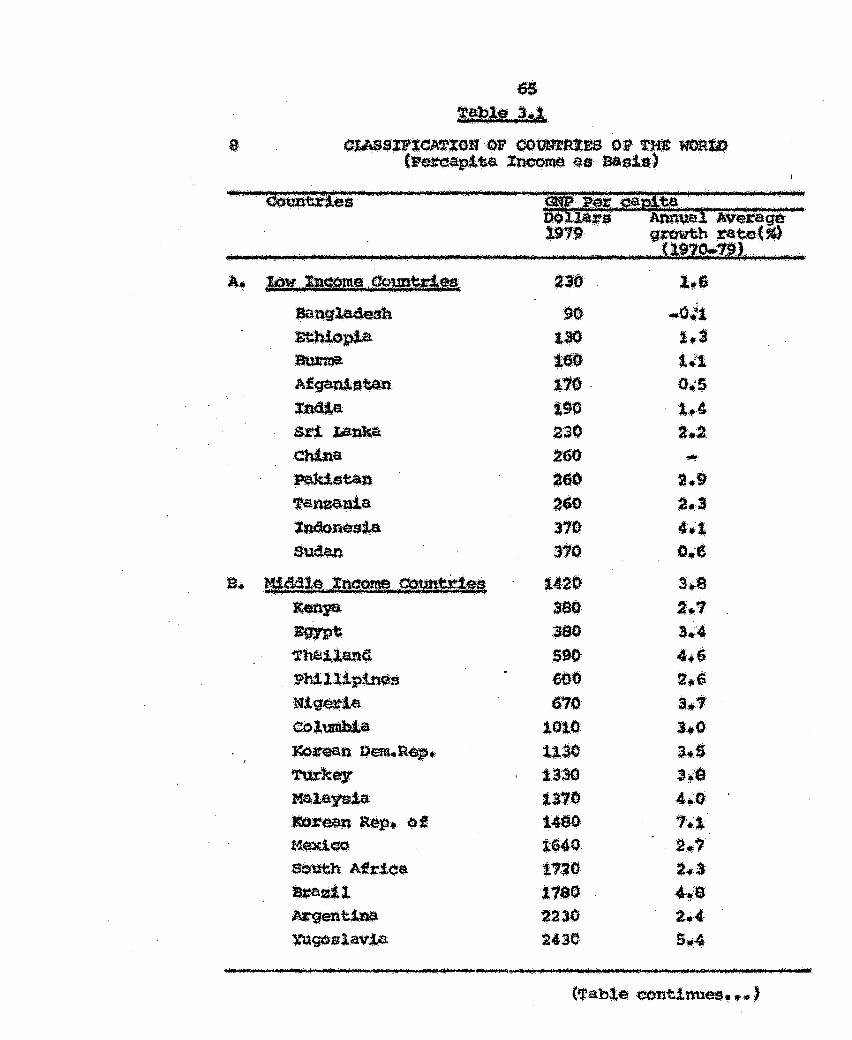

:t.tt. qleaJ:lY 4lstln.gulsb$$ ~ •tow In<:Ome CCuntties•

with ~ ¢apito income qf us. 0 31l1 o:t bEllow (lln the bs.s!$

of ,..919 date.) and •Middle ~me Cou'ntdes• w!tl~ pep· capita

iric:Q.mo aboV~ W .'$ Jto • t 4000 and. the .t:emalnmg <:O~t;t;ies.

atre •·High ~e CQun'tzrtea• .~· trhte .ts~ aboWll .tn '®~ 3•~··

rvt!- ' ·_._,., 1 '_f TrifJr 1 e: · •' ,. - -·~··· ·· ., ... ·1,.

l t1ntt:~a Natto;ns ~$'Wt'E'Mll fQr th~ ~toono~ oevel~· aent of ~aer4evelope<S a~~~,,. liEU., P•:S•

2 Worl.a n~ ... ¥.Srtfil:lm~Sf;l,.!2~.f· l.'9S1·

6$

!f$1! .3:'&. (UASSl?le14'XON' OF COtmTRI!S 01" t'Jm wt".mtl.t

· (P~ap:l~ lncome ao Da$1td ·

raa.-~m.~··_l·,.· · ~· es

. if . . . - ··-· . ,. . ' ...... ' _' ..

, i . 'if -. ' ij_' It _Jt nu· i? -•

A. JQ!t_~s j£BEta•, ~ftgl$4esh

m;b;f.op!a 8tU:1na

AfganA>o~

tfl4la &x-t Lanka

China PakiSt$.1$

'ranaanla Xndone·si&. aud.an

&enya Egypt>

"l'bai:la.,wt(i

. Phi1Upirle1i N!~J~ta

<»ltallbLat ~~n oem.·RG9•· 'rttr'k~ Me;l&ysla J.(Qttean a~ •. ot M~<:O

SOUtb Aft'iC&. kaal.l. i¢gentJ.na \'UgoslavJ.a

210

~0 ,., 1~ 170. Ito .23.0 260 260 260 370 :J10

14:20 380· 380 590 6&0 670

101(1

1130 1330 !3"10 1480 1640 t7#0 1180 2230 2430

16 " .-.0·4'1-:t.a 111 o.·s

. t,..4 'i.2

2.9 2.3 .. , o.;~

3.,S 2.1 3 •. :4 4.6 2~6

·'·' s.o· 3,~5

,~·e

4.:0

'·:1 . 2.?

2.3 •~s a~• S•:4

_____ Wti_>_M_f'M-[f?-~ ·-·-· ·-· --· -~ -----.· -1'·-··@·F-0.-f'i'f!i'lip~ R- ,' _IT t }ii? d ~ 'pi If 'W +'tjopf!lli111011MF'llll.ltliii '

()jl•- Oo I f i" • 0 ''·". 1 it."' -·· "1 J'f.l!t. 0

0 RJjii(

V~ueta

X$rae1 Spe.1ta

c ! . .....Arot~.·~ ... ·'.al ~.· ~.t.·· ~.·.~-.· • -='"~~~·.·c·•'-~-•Sl=~~-J~leJ'ld.

lt~y

~slana

u~x.:

l1tfella.na A\U\rt:.!:'~*'

Ca.tta$1.

F.-ame ••tn.-lands t:rnt~ states

' Ne$\tay

Belg:11ltR aermany F.a. -~k lwec:t~n .. SwJ. t~·erlsnd

D •. ~Ri~J, §!Utl:49R ()il !!Jert,ert Iraq $au41 A~7abJ.e;

~ Kuwait

•• N.2!'Cl~52S&t: ·&nt!l!staa+ .!sit·-. Bulg&i:i;l;.a

PO .lana. Hung~

tiSSR

)130 4.1$0

4380

9440 4210 52 SO 5930 63!0 8160 8$3Q H40· 9950

:tQJ$0

"S.0$30 to?OO 10920'

. 10730 11900 11930 11920 54?0 2410 1!80 9110

11100 4230 36~0

3810 lB$0 4110

a.11 4.to 1 .. 1

•• ,o a.a J•6

1•' 2~2 .. , i.tti

l•& ,,~o

3.4 2 .• 4 .~.s ,., l•3 a.A-·~~• .2.1 ,,.o 4;,.G

s,.·J S,.l

~t-·t

""' s • .s , .. 4,.a ... ,

e&eQhcud.ovaldJl 5~96 4 .. 1 $. ~. ISf ·.1 ~-~lla··!!R·•t. Jt ' 1 t.'J..· ..• !lfM'¥1.11( n ... 844:~·2.f.L. ~ ·-p )Ill. J.) ·:Til;t,flfH 11!1 Ald. ti_.

SO~et l'(tdd lE,t~ ,.Rtl!!~•· 'WOJ:ld eank.~ 19S1i

Xn sptt.e of the heterogeneity ~ch reflects relative

d~GM tn un<le~tdeveJ.O}lnent ·and~ geneJ:aU$at1ons ·dlff.tcult,

-the J.et~s 4welol:)ed COlmtd.es sh&J:$ a ·~ of tun~ta1

fGatUt$$ tv:hich c:J1ea~1y dtst1n~sb them fi.rom thE! e.avano.a

!ndustr~a11raed count;ries of ~be weflt•· The most eaUeni! of th~se

. f~t~s $re de.scJ!"ibed beclowl

(a') M.Q:St of the less tlwetoped dounn!es ere fo~~ co).Qnt~.

~his ,otn~ to the iaot that w~devt!!lopment . i:e1. !:11 .many ways, . . ~ I

a ,legaey of <:o.l.Qnialtsm· .find also ~l.alnG that links ol! ·

~nom.tc depsnetenqe .• est~.Ushed ~tween .eelO.td.e.s G.~d met~ ...

]l)Oles ~ hav(l sutv1Ved the tb~.l intJ:Od,ueUon of. polii!ical . J;n<lepen;dende end nattonal SCYtt•eignty .t.n tbes£l •~olonJ..et~~oto

' . 'rhet is1 thf;;l moV.rop-;>l~sat.elllt$ relat.tonships which ~·~·

C'l!bat"~~isti.:.l of colonialism have ~ur:vJ.•1.(;ld t:hs f{)~l ae.tn~.ee

ot;.' the ;J.at.ter.

-fb' In ell !nst&.ne•s• the d~gJ:"ee .of J.nd.usilr!aUe~tton (as " '

meaS"wred 'by t.h$ tJhare of manu~tliri.ng tnaust:t'i$• in ·~or:

by thea pC:Cettage of the lal:x>ur fotos ~loyed. in s~b lnd\lSt.

rtes) of lGSs tteveloped countt't.e,s t.s eona.f.der&bly lower that\ ~

t.hat of any ·&dvance4 CO\Ult.ry,~;,.. Tektng the SOuth as a 'tlh01e1

~ ....... +' ••.. ,~.:·:···1

,

69

lt, accounts for on1t 2.0 pei"'ent of t~ wo~1d's ~nutactU.tin,g

output.4 "able 3. '2· smws the ~upat£o11a1 ·<11$'6-~oll of

ti40dt!ng popu1atton in some of ~he comtr!ee~··

tt.tia1:!,,!•1 P~N!AG£ OF Ae'»XV'B l?O~XDN 'ENG\(lD) tN AGRXCUL~t$E ARP· htllfS'l'RJAL ()ltXQXN or ON» ~

SELltOTU> CO~ .til 1.978 .--·-,.. .. 11 d I·- ·-.ftxst~J.--1 :::::: _::x•~~g~¥.teh;::::: :::

AUSt#a.-. ~' . 1 • ' -~ • - • '

. -. . . ~- - "• ' .

qauaaa 1'#$.~

.Uap6ft

:t-ndf.a

6

6

' l-3

14

. A9t'1c;Ui.t=-e 11'1dUst.q ~tng

. lll I

' ,) • * --" 1-- .. f ··-:: ?. .I ., rre-

a !G 62

J $4 63

s )!. S!

4 31 65

s !1 59

5 40 JS

40 as 34

- •• -·_n'' lJ!L .. l .. :··r:J r·_,:··rt .·(T_.lTJi·l·,qttr ."f .• t -~J- ·.··~ -- ."._,:_iii:M'1 .. 1.11' a··_-.·-_-.···- ._._;-. f J_lf-·_p __ t_pjl',

(c) Gtven th• low· de-ee ()f ifKlusv.taUaa~n,, &gJ"l~t~

an<! prJ.m&J:iY --$'$cti:Ve 1ndu::.ttr1ett ~unt foJr tbe latrter $h$re

ot .enpl.o~~ a:nQ. in¢0rtle itt l$$$ develOl)ed <;O'Uti1Utles.:S

r r: ·- ,. ·i ,_ · t.J: · -_, _;.. __ ,_ ·_it<,_ --·~- ·: t-.- •- __

4 wor:l<~ lllarik, :n~2j 1te1~'

s ,~:'# 1.910,

6~

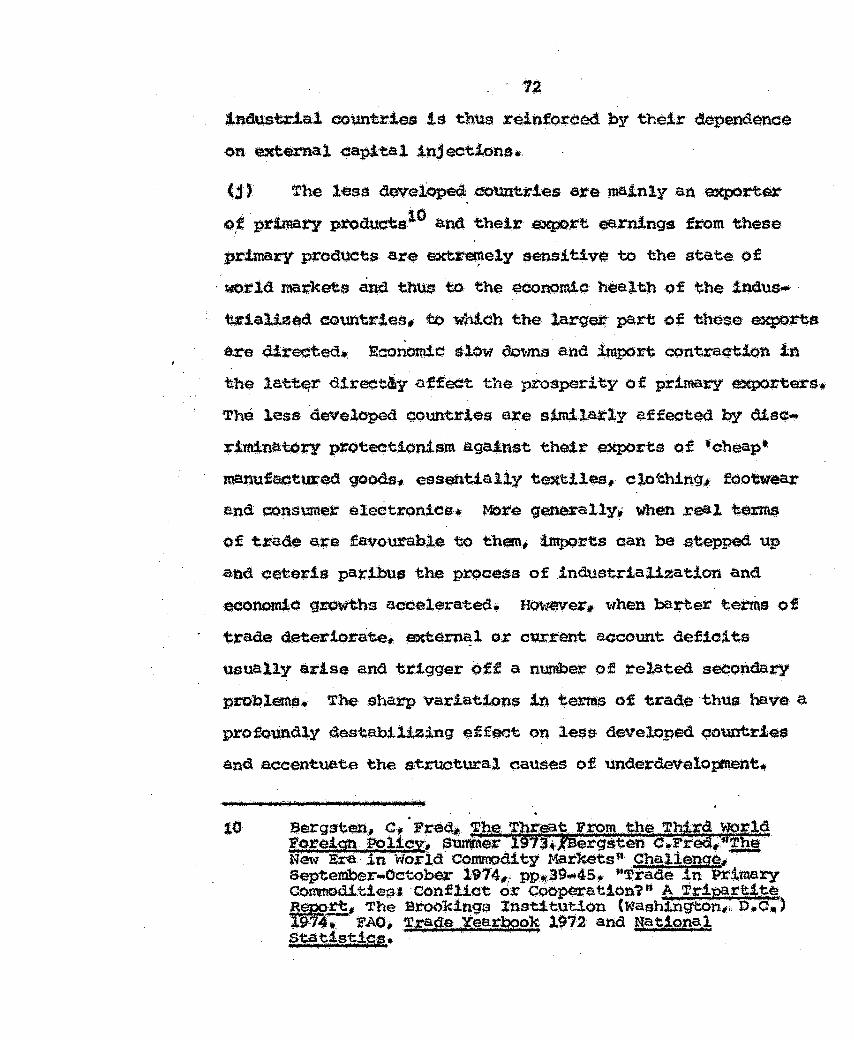

·( . .;t) t.ess ~veloped ceuntrtss are heavtly depGndent on

eJ!pbrts, pertic:ulatly of p~t!n1ary prod~ (ca$b ci:OpS and

mia~ral$)• 'fhese ~unt for some 6! pe.rcent of less d~eloped

eountry expotts.,~ in value terms. The. rrota~le fee.ture is that

even where the production of .. p~~ COttlnOdities is confu:'o.11ed

locally the ~cesainq and marketing of t.hlls·@! same eommoMt:t.s

is mostlY oontro1l$d by transnational corporations of tthe

a<tvancea west. lt. £sa situati-on oiLweak $$1lers and. pc>wet-fu1

bUyers.

(e) Even tn those 4Cttnt~if!s where indUat.Jrla1ieat1on .S.s mo~e

pronoimc.ed~ l.ocal ntanufaoew:-J.ng indUstries are mostly <=~ontl't01led.

1)r forej..gn mult1nationa1 C01rJ)O:tations an4 thus produCing goods·

f<:>r ~rt. ma.t::~t.s teHJ•'# ·cameras, calculators, etd. maete in

south East Asia) :. As a :t-etsult. the less developed cottntJ:'.ie$

depend on .i.mpo:;-ts fot' the prOVision of eons~ 4\ttables_,.

industrial tecl"tnology anu ~ requtremertts and thi.th· o:f

·course, .ts a part of satelll!fettioJ:l of let5s developed oountries

.referr~ to above~:

(f) The economtc atructure o! several les& developed oour.tt:.•

rtes reveals a duaU.~c tn the fot:m of the coedstetlCe of

teebnologpi.rl.t$tis£Ve J.nd\lst;:J.al SE!Qto~ ·On the one 'haft4, aQet $

bacltwa3;"4 tradlt.tona.l $Getot' ( e~ g.,, aUbstst.cmoe ~norrw ~:P4

\' ' ... •

10

ba~ar economy) ott the OthE!r .• 6 Although <J.ual.imn !s en 'Uftderd.•

abl~ feature of most of the ·eount.ries concerned. theories:

whtah attempt to ~1ain \U\<iardevelopment in tet:mS of tb&

retat'da.tive eff~t. o~ .baakwat-d sector$ on the economy as a ·whQl(!, •

are highly contztoversial. The etnetgence of modern en¢1av~a

with tecthnologtaallY .aavanQed industt"ies -- mostly controll.ad

by- for.eign J.nteres<ts . .-,. .ts, in fact,- 1mparttnq a n$1 tnt~•

t.tonal dtv1dt>n of labotu: and production• charaoter:tst~¢ of

the tnoreasing in'herne.tionali~at.ion of contanporasy cap!taUsm.

Whtle those enclaves undoUbtedly have a ·stimulat!ng impaot. on

the growth of GNP, they· e.z:e also a QOn~ibttttng factor U()

inet'&a$ed . st~uotuz:'al trnbalances. Pol: instance:~. by e.tt.:tactitlg

a le.rqe pa:rt of these countries·• reso\lr'Ces, the moa~m

enqlaves can cause a ClltttUlative retardation of the bacl<ward

seoto.ts•

(g) %t also follows that the low per capita GN; of ntOSt

less dev'$loped ooun~.ltas !s c:o~ut1ded by enormous dlspati.tles 1

1

71

in the d14tril:JUt.1on of ·ineortte and wealth~ On the one band,

there et.tEe' small1 wealthy. elites of burea~ats; land o~a l

and a :few .loc~l entr~pr~eurs while -ges in the •taoden1'

.s •. tor are gettE»:allY weU above the nattona.l ·wage. lt !$'

a«:l<:ompa:nted by la.rge scale Un~loyed ancl underemployed

J;iving und$r outright. pev$rty.

(b) Jdueat.!on of all but th~ ~11 privi:t.eged. ~Ute is

g.e~erally defieient.8 This ts .shown by the high lrtWe1~ of

i:lliter:aay and the underprovtoion. ?£ eetucational facilities

tn many l.ess· aeva:toped oountr1es and 'this' is excerbated by.a

b~ain drain of eduoated J.ndivtduals and skllled wor~er:J, to i:he

J,.n(iustrlal c.~nt.res o~ the vlest in the times of ~lU"onic st*"'~

tural unemployment- . This tendency is ptevalent even flrf\Qn-g

uaskilled WQt'kers p 'l'h1s large $<:ale nd.grat.J.on .ts ref1eeted

by the .ttnpQtrtance of ~t~iates remittances~ as a soUrti:e of

fox-e!gn .sxehang~ fot their Qountey of or!gin~ In some ¢ase:s,

net. :remtttanc4::ls ® exceed fox-Edgn earnings :front ~J:t$.·

U .. ) Since the lsvels o£ average dotrui!st1t!! income and savings

Of these QQtmtX'J.es at:e lOW (even if high .1h relatiVe ~$)I

they are 1nsuff1c:tent to ptov1de 'the basi8 for 1net19'er.tO\UI

cap.l tal. ~c~lation and indUst.rial deVelopment~ 9 The ~e¢hnoJ.Qgtoa1 end import dependence of less developed oount .. iea on

,,., q--··rr. ·-J ·•· _·-;·~· . ,~-· • a._. t · ·-·r_: .:.

a Un!t¢d Nations; ,s;tatist:iea:l. 7'~1tb?.slv 19'-~· worl~ . 13ank. TreJ1ds ,.tn qevelo:Q~.ng .count,rie~- l973t pp.t.tO •.

Uni t.e4 Nations. ,savJ.nns ~..nr ,Develo:mon+: (New York), . . u••- ~ _ . tlii ~ 9 ~. r L. _ . ~- · -

19Sl. pp~S..7t

12

indust.tJ.al eountr.ies is thus t'~nforc!Xi by their dependence

on external capital injectionth

tf) The less dweloped. cou.nt.ties a~~ mainly an exporter

o,f primary proauets10 ana. ·their .expot:t earn.f.ngs from thes~

prtmary products ax-~ extr~ely $ensitive to the state of

'world max'kets aoo thus to the economic health -of the inClus•'

'f»:'ia1ized ~unt~tef3* to wh!oh the larg&Jt part of those ~xts

are Q!~eeted.- l!!eoxlonp.e $lO\tt dot-ms and import eontrrca~tion in

the latt~r direetiy affect the prosperity of primary -a:r.:xn:te:!i's•

Too .less ·developed QQunt.tr1es are sitni.latly affeoted by disca•

rtminatol'n{ pr:oteot!on!sm against their eXpOrts of 'fcheap·•

ma.nuf~tux-ed goods; essentiallY textil~s;. clc.rt:hingli footwear

and consumer eleQtronics, MOire <Jenerally, when .real tenrl$

o:f tJfad.e are favourable to them# lntports oan be stepped up

and c~e~is par~bus the prQc¢ss ·Of .industrialization and

eeonOld;.c gl!owths accelerated• Hot;ever., \ithen barter terms ot

tJ:ad(;t deterio.trate• $Xtern~l o:r el.ll:ttent account defieits

usually a~ . .tse and t.t;1gger off a number o£ .related seeondary

problem$~ The sharp variations in terms of trade thus have a

pX"ofoUr1dl.y 9.est.ab1lizing ~ffact on les.s developed Qountr1es

and accentuate the structural causes of und.erde'\teloprnentll!

10

73

These ctreumstahee$ force these eountrl<:!s . to go for heavy

e)tt~rnal debts.

Xt follows from abQve that the less develo~ countries

a:re ehet'acterised by low <i~gree of dE;N'elcpment. aut at. the

same ttme thes$ countr'ies aspi+e to develOp fast. On~ ·of the

essential requirements of fast groW"~ of thes.e countr,ies !s high

rate of investment whie.h could make the de'Velot:rnental ptOjeo:t.$

fee,sib~e. But the high~~ of investment would be pOssible

'Only vihen higher ~tes by sO.ving$ a~e forthcotn:t.ng (l()mest!callY.t

The savings a~e a direct function of 1ncome1 a.ceording to Keybesi'

but the income levels of these less dev-eloped countries ar~ low . and. the.refo~~ higher domestic swing$ ar~ not possible over·

11 aome fundamental theax>otical fo:rrnulations of the fc.a:eigb ·exchange constraint.., two gap analysis., and foreign capital requir~t$ a:re presented :in the following · studies'· · · · · · · ·

Mckir\nont R. ; •Fo:t:"ei.gn EXchange Const;:aints in EOonotd.¢ pev~l.Opment•., Eco.c Jo,umaf June l964t Che~ry. Hard Adelman, a .• :J ~t'Ore!gn A1~ and Ee<:>nomie Development• The Case o£_ Gree<;:e8

, .. ~~w J)t· !eon,omia ~.tudies, Februa~.· . 1966: Mac EWart" A., nQp. ·. al pe,ttern ol Gl"'l>Ttll and Ald. .t The t:a.s.~ of p!ak,istan••·. F!.k1,st,a.n P,sxeloeent. Rsvtew, sunmer 1966; Chen~ H~ and Strout., A•, nFo:relgn Aasts .... t€inee and EconoW.c oeveloprnent" American ·sc no··«:! R · w., Stapteniber 1966,. Vanek., E •• :Est.imat!n 'F rei Reso ee N s ~r Eecmo · e .D · lo · nt. New York • .l 6 1 John

·ler ~ ed• ·. ·~·· _ca: ta .. MOvr:snents an4, Economic p,evelo::rtnent, (tendon), 196 : A+Sengupta, 'lJ?oreJ.gn capital R~ir~ements fot" Economic Development••, 0~., !-'larch 19691 Bruton# H•J'•• 11'.t'Wo Gap Approach to Aid anO. Developtnent • Cortment,#' • perfGaq. Economi,c, R$,_~~.. June !969; ;t,al1 Deepak1 *'The. Fore~gn EXchange BOttYenec:k Revisited". illC£• ,July 197.2.

74

a sho~ span of time. 'l'bts creates ld.nderan<;:es .in atbanoln9

economi.G 11evelo~nt ,of these C!Qtmtties.

ln an open eqQnomy, when dotnest1e savings prove to ·he·

tnadeqtlf.tte and insufficient tn rel~t,i'on to the targ-att$d ~ate

of gml(t!h.,. then• ~hese Ciomest.te savings: tean be supplem~tecft by

many ld.nds of e~etnal assist-ance.- Tha •:oual-Gap t«>Q.el~ basi~ ....

· · ally ~'¢Pl:&.ins the rale of foreign bo~wtng in the develoPll\en.t: . . . .

·xndotne (1')

then,

Qt'

'* Q +X + J:

e + M + s "

~bus in national incorne ac~~tLng an excess of !nveet.

ment over domestic savJ.ng is equivalent to a sut""plus ~! impc:u,~,;

,

·OVft: expc>rts. 1\n ~rt surplus financed by . for:eign bo~rotd.nq

o'h sUpplement: dt.ntt~tic · stav:tngs. directly .or ~ndit'ectlV by l / -

pr~ri~g for~ign GX¢hanqe to buy impOrts which .QO\lld be $ap1t.~tt-1

g~~$ .or s\lbstitutes fer domest.$.ca1ly produced cons~ good$. ' i'f· ' .

/ k lr· It rnay be noted that in aceounttn9 terms the amount o.~

fdjetgn. · · lX>rrow,in.· 9 requi. r.ed to . s .. upplem··· · ent. dom. est1o s. wings i.s r: same wh-ether the need .ts just for more resources fo~ capital

/formation or fort imports as well.. The .4-dent: ty between the

two ~ps, the savings ·• J.b,vesttnent (s;...t,) g-ap and the ·~~

import. (X..M) · gap. follows from the ver:y nature of the eccountir,t.g

/procedure~~. Xt 1$ a mattet' of ari thmatic 'tllat if a country

tlt.les to invest more than !t save$1 a balance of pa~nt~

deficit w!ll result; or an exeet:Js of imports aver ~rts

neoes$a~ily :lntpUes an · ~ess of resotUZ"Css us&d by an economy

over ~esources aUpplled by it, that .ts. an exc:ese of investment

over savirtqs. The twq. gap~ .need not be equal ex....a.J'i't!-$• 12

·~ understand the meanantes or th~ ''Dual Gap1 analysis;.

stan w1th a .p$.~t:ieule:r ta.:rg:et. x-at.e of growth and to aehieve

~his 'target 9l'Owth rate, the savings and investment gooc:!l

imports wtll .be ~equired.,.l3 JJ.':)oking ~n t..erms of famous Ha~d-,.

12

- • ·.!" .. i ~· •.

Zbi~ t p~293~

76

pomar ncdel o.f e¢a:notnie growth, the relatton bet.weert growth \

and savings .i!f $Xpres$ed 1n te.tms ot. 1;be investment ¢aplta1 ...

output ·;flO ratio (Q-)~ which is the J:"®iproaal of the produativit.y

of capital (P) t~e· 9 !:# -s/4 or g =t -~ t.zhere p = ~, -, g = growth

ra~~ o.f inaont~,. s t3 .saving ra.tto. SWlarly the t'elat!on

between growth and t.nves~t gooas. tmports is expr~ssed in

· te.tms Qf the 1neranental capital impo~ ratio· (~l) t.•$• q a tm•

t.f~i'e 1 ~S import Jt&.tio GiVen P and rn• ,, an increase in g teqtdr~ '/ ' . .

an increase !n s &ftd :t, •f target ~auo of gt'o'Wth is r• then ' .

the :t"equired saving ratio ~s•> to achieve that target. growth

t:ate J.s S* =t ~ and the :r$qU!red ln\pOrt ta~io i* J.s i* • !• ._ If (k)me$tto saving is calculated to be less than the level

necessary to aohteve the target. growth ra.te1 the:re is said to

m1n1nru.m .import requlrenents to e.ehiev~ the target. qrowth J:ate

-are oal-culated to be great~ tban the ntaximUll\ fetasible ·leVel

of export~, there is said to ~st an export-imp()it or ~:r:e.ign

"' exchange gap equal to A,~- 1. l-n the absence of foreign borrowing

~wth will proc$$d at the highest rate permitted. by tb'$ most

l.tmiUng factor:. tf the b!,gqest gap is th~ s .. :t gap, then.,:

growth ,is lJ.n1ited by the availability of domestic savings ana.

is scd;.d ·to be investment l!mitG~ lf the biggest gap illS t:he

foretgn.exohanqe gap# then. the QrOwth .is limited~ ava11~J.1lt;y

o-f fo:t$1gn exchange and. 1~ said to be 'trade limited.14

77 T.tadttional).y the role of foreign bort"Owittg ·wa$ to supplement

. deficient domest.ie savings. But the distindtive eontr.tbUt1on

that has b&en made by dual (rap model to the -development theoey

is that. !f mt-eign exchange is t.he dond;nant oonstta!rtt, J:t

peA.nts to the additional ro1e of-· £oretqn l»~.tnq in E.iUppletne~

i:!t\g fo~eign -~angej'-5 wi'thout Which$ ifractton of dontestie

1!1aVinQ$ mlght 90 u.nutillse(l b(;lcaus~ ac:t.ual growth would be

aonstraint!d ·by tbe tnab!11tt to hnpo.rt: neeessar:y .tnputts. T()

put tt. m:>re necisely.- .tf fQr~ign gap J..s the larqer, $0 that

(t~t.ii.iJ m1'> (S*--S) P, growth -cannot. prooeed et the .-at~ Sp

but mast p:-oceed at tba l0t1~ rate· .tm• • lf p ~s given.~ a

ftaetion of. s must go unus$4.; lt. may be further stras.s«i

that since growth .~s Umit.eQ: by the la~ger of the two gaps~

iol:"cl.gn borrow~g .:ls only t~red. to ~et the larger of .the

two gaps• lf the (x-M) gap is the larger, then foreign borro-viin9'

tQ Sill 1t will -also £111 the s-.t gap slnQe investment goodS

~em. ®Ine btom Gither here ot abroad. Xf th$·s-:t gap is the

larger for~i9l'l bo.t-rowing- t.o fill it will obviOU$ly cover tln~

smaller Jr•E gap, The t~$. gaps are not ad&tive,..

'rhus . th$ dUal gap analysJ;.s not on.ly empb<u~i~es the rol.a

of l.mpox-ts and fot:eign ~bange in the developnent prQdess but

78

also $Yl\t'hesises the .tradtttona:t and modern vi,et-ts coneet."ning

aid~ trade and dsvelo]illtent~ 'While on the one hand it ~e~s .~

the trad.Ltiona.1 V'!~ of foreign a.ssistanoo· .as merely a bo0$'tl.

to domestic saVings and at the same ttme it also $uppot'te: the

eonolusion that many goods neceseaty for growth cannot be

produeed by the developing eountr.tEts th.emael.ves and, must,

t.herefore, be imported w!th the a,id of for.eign assistance, Xf '

foreign e,xohange is truely the dond.natttt oonsttaint and c:onsist-

ently iu sbQrt supply setne would aay that dual gap analysi~J

al$0 px-es·ents a more rE3levant thoory of trade fort developing

countries whieh just:J.f1es prot.ect!on and import aubst!;tut~iort.

%£ 9'l!Ol-lth is constrain$<1 by alack or foreign ~han.ge, free

trade eannot guarantee s;tmul.taneous. internal and ~ernPl equi.•

11btiun. and the gains ftom trade may be offset by W'lderuttlJ. ...

sation :of dom~stic resouroes~,1S

The d.ual ~P itndel no doUbt explains the t-ationale of

tmr1t1ng foreign asslstan(!e to develop1ti9' countries. ho,w$Vet'~

the nn,del. itt npt. free f£Pm o·dticr!,.smet• - :Wirst of a11,- it assumes

the lack of substit.utabilit.y,_ between imports and dom.estlc

resources,, but. in prac:t1c:e thi,s lack of stib.stitutability is

quest.ione.bl·e~ Second question relates to the ass.t»n,Pti¢ns of

!6 Thi.rlwal* n.12. pp.2!J.t.95~ .,.

11 Oheneey1 H and Bruno. M., ttl)evelopment Alternati\fes ill .an Open :Economy .t The Case o~ zsra~l "• ~donoroAp, Jo~~.l, March 196.2 ~, ·

19

~~~ .propQttion$,,19 an inflexible compt)~!tions o£ .impo!'ts

· .. ·~t.~~ qonsurnpt.ton and investment goods~ and rigid rela·tionf'~ t·- . ., . . . ~~/ sr;t~b betlteen impOrts and 1nvest.n'letlt a.nd J.rnport$ and output

. at'eA,l~tnewha.t strong• lf there is a complE!ta Sub$tit1,ltab11ity

~.en .imports at1d. dotnes~ie res .. ource&~ theo~~i~. ally. # 121. e~ J .one gap - ~ante end export. Then; the factor ,propo.ttions

/may be slow· ·to adjust, and substitution between foreign $Xld I - ,

I . . / d.Qmestl.c resota:ces rnar be a long drawn out prodess_. 'which makes

1.-t not ~•sonable,. to · ~dertake empi.rieal analysil! of shortagee

<>.~ foJre19n exchange ana domestic savings a-t part!oula.r points

in ttmo1 e:nd over time es \otell... Xt may further be pointed out ' .

that stnee the t'WO gaps are not additive~, the crit!e!sms of

dt.tel•Q'ap ana*y$is" &>not se~iously af!ec;:t ealcrulations o£ inte~

nat:Lon$1 a$s:ls~~u ne<;essary fo~ .gra,fth targets to be a<:h!evad,,

· except whete- tb.~ FE .gap s't!bstantially excee!ds .the savings- gap

and !lO al.lo-nee has been ro.ade tor the pOssibility o£ substitu-

1d.n~ domest~ Jt¢SOut:'Oes for imports. Xt is unlikely in developtn9

countries that Qna 9SP n11l predomtna.te as the major coP..atraint•

~ht,rdly. 1 t has also been a'.ttgued thet in the context of d~elo~ " .

I

ment! of a less develop$! co.untry. why only talk of two gaps#

namely. fO.re.t.gn eXchang-e and s-x gaps. '·Wlty not to talk of

multiple gaps e.9~· seotora.l gaps ei:e;j, By confining to two gaps

alone, we are not able to take into account ~he othet constraints

in the economy. while 1;hose constraints ~Y be qui t:.e important.

'.~:'here e.re other models that explatn how growth rat~ of

U>Cs can be 1nct:"-eaS~tt One such model rel.at~s capital imports

' lS · Chenery Qnd st.r:eut; n.~11.

eo and growth x-ate tn less developed -countxJ.e-.,,.19 This tnOde-1

tesu1t.s fr:Qm the outcome of a debate between. Ball a11,d Masaell

em: the t.-elatj.onsldp between capi ~1 !rnpc~s and eeonond.<: growths.

· ;t. u -.h.own by this model tbat.J

(~) '.rhe rat.e of ~'Wth of output \11.11 be fas:t~r with .eapit:al

.in:tpoJ:ts provided new inflowll of for~ign capital exceed the l()S$

of <lQmestte sa.vtng to ~Y zl.nt•est.. %£, noweve:t.; 1ntertest

ehq-gQs arC~! me1t by new bolrl:~wlr!<J, <C~ap.ttel iJ\pQrts tm.tst have a

.tavo'Ul'able effeqt on the growth rate o:e out.._putJ and

. -~Q.uoti:vit.y o .• <:$:p1tal ~.ltt$ e>tQ~~da th~ rate of 111te!:'est.

(1)

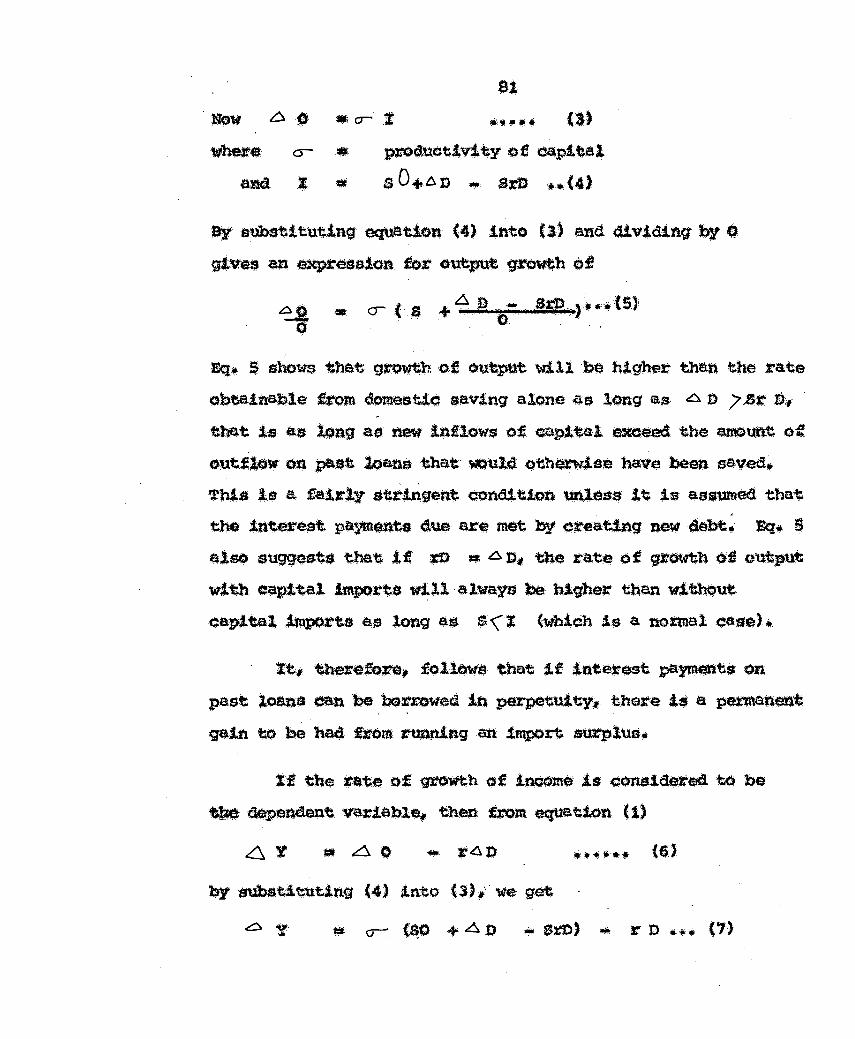

whex>:e :t =. '0\ttpu.t:

20

Y ·• Income t: • Interest· .rate, an4 D a Debt

_The d$.ffetenee .hM!ween ®mest1e output and national . • +

(2)

":he mo4e1 r~su1t.s from the outcome of a debate b~een Bail and Ma$seli-.: See R-J tall, •aapi.tal zmport.s ant! Eeonomtc nevelopmemt •I ParadOxy or O:tthodo~ "~· .~:rl$Aos no.l. 1962 and :S.F.Massell1 "EXpOrts capJ.ta.1 Imports and Economi.c Growths"~ K:z14os. no.4._ ig64.

'rldrl.walt n~.12, pp-,_29~300 .•

where cs- •

ad I = p;r;roductlv£ty of ·Qapl tal

sO+~D ... srn ~-(4)

·tiy substituting equation (4) into ($) and d!vidtnq by 0

gtves an exprcesaion for outp'* growth of

Bqjl $ snows that gt:Owth ·off outpUt will ·be higher; than the .rate

obtainable i1:otn 4omestie saving alone as long as a o 7 1St"· n.t that is as l.Qng ~a new inflows of ~pltal. mcceed th$ amount oe

outJ:low c>n ,paa:t lqa.n,;; that. wuld qtherwJ.s:a haY~e been s~ved•

'lbl.s ls .a fa.ir1y ete-t,n.gen.t;. condi t.ion unlt.ut~ it. is assumed tha-t '

the J.nt:er•su paym.m.te 4ue ar~ met by .c.-~at1ng new d®t. Eq~ S

also suggests that if .xn ~. ~ n, the rat.~ of gt'OWth oil output.

with Qap'ital imports will always. ba bighe~ then without

capt tal $.tnport.s .es long a$ s (J (whieh .is a nottnal e$se) •.

tt~ therefo~~ follows that lf ittt.er(!!st paymQl'ltl on past lo&na $Jl ·be ~rrcwed ill perpetuity~ thGre !'$ a ~nen't

qa.tn to be had from r~g .au !tnpO.tt surplus;!

Xf the rate of 9t'<)wth of !r'lCQme is 40lUJ1d~l'Eid to be

~ C~ependent variable, then from equation (1)

S.i:nce Y ca o .,. rD. therefore_, eque.tion (1) ecu:l also be

. wttitbell S.SI

if (!c,t;' (8) l~ divlded ·by "! through out., .t .. t results in the %'lita

of growth ot' J.noome ·Of

and .equation (t) abows that the growth rate of .lncome w.ltb

capital tnlpQrts will be higller than that obtaine¢1 froln dbmestlc

sa.ving -alone as long as the prodtnt!vlty Qf cap!:ta1 .tmpo.J."t$

( o- ) .exceeds the tate of .f.ntet-est on fcu::eign bOrrowing b:) ,.

wtcb is a $'tandard result that t.be .:J.nvestment. is pro:fJ.table

e.s l()ng la.$ the r~te of return .egc~ the re:te of interest.

t<so dOubt impo~ sw:plUSEJS haVe a ~-t. potential fo.t:'

a.ev-Ulpment-prooess, there are two <tanger$ in this .Lmpl!eat.S.on

of the (DI)del, J?irstly,. the ~::r:t su::pluses &anQed by foreign

captta1 lnfl.ow:s .increas$ t1n~ cap.ttal~ut.put ratio and tthereby

disoou:-ages the <.iomestJ.e $aV.ltlg. And secondly#' a fl'aetton of

cap.f.tal inflow .is. consumed x:ather ·than invested• Both thsse

faiClt.ors may redUCe ttbe gr(')Wth rate o~ may result. in .no ext.tG

9t0'Wtb .$t a11. ":hi$ argument was put fo~rd by S:r!_ff.ln~~1

21

$! s•s14••• tl\f). emp.t:,-i~al $t.U4.te$ a.lso sugg$st $ negative

. . . . . ;l~ ' #e.la.tf.on. ~Et&A 4tlpc;;res .aaa ~est14 #tt.Vift9• aut etu.m. tb!.s

baa tO- 1wJ consid•ed ln tbe Ug-ht of bo'W eavttifs a," a-fined

l.n a t~evel~ng \e~~ lii •ewing$ $Jte defin~d as $ ;o l j(jj>- •

<Whez:e F • VQ~gn. eapLi.tel) and 1f F ti~;,-ea.. ~d I r.ts&• -

.l(t$$ than ~. s ·mtlSt fal~ to· bttng about the equa1~'toy and itbu

t't '"'aDt'lOt; haVe e W$Gke~g $itt~ on ~elot>lnefit ~c~s::~. %1.'4

may .aA.mply sref1•t t.h$t ;a ~n <lf eapttal. i~ns l.s ~~

J'oa:tun$te1~ bo empirical studies baY$ suggostGd e. neoattve

rel~ne between ~p.ttal #.fnpo~t$ ana: tbe.in.vesttn~ tatto~

GJ'iifiJl. 4\l$0 al"gtte' tha~ 'th~ f0ftl9Fl <:mpital LnflOWiJ

also lt~ t.b& ~tvttv Q.f.capltal aft4 -t;e ~bs <=ap1"1

O'tt~put .-e."• 'b•$U,$G the .. rtted capi.•J. .14 u•.a i:n $0•al

i>Vubea4 ~aplUel. and tn_..tt.>Ut.ltwre ~~~s,.. • Thl$ e.~t G~tt'l be nsolvd ':by ®n.s4,d(llr!n-g t:.he dtffe~~o~ between the

eapt,-~~~:PUt J!a't£& of ~se pr~J•• an4 ;(lapltal output Dt:.Lo

of ·ttl~- ettD~Y fill a whole, ~t LSJ Sntpt>~ is tb& 1s:tt:ea:r •

• l-ong ·th~.t oapit::al o~tr • ~tit\ for the . «:onomy a.s a whole

is l'lOt t_,~•J..tlg, t:t ®es n.Qt ~· a ~~O$ c:f wo.t'ry.,

b£!1SJ!. J121!2il.11.s! ... S§ D~Stn~o!QI J;i~N.a~~--23

~h$ anal~l$ given a~$ no· ~t ~stabl~.shtas then~

ftlt -rtd.gn ~ng fQJ:· <ieveloptng oountr!~& in ·o.:Jtd.• t.o

.~· 'it_'l'L . . '· . . PKM.: 1"l!Jli_J;,tlt_'_$Ji@·

22 3l

at ~ ia\EJir dw~. eftons •.. b\tt. $.t may be ~~tid

tha-t· the assiotanc:e. tbat a tlevaloptng ®tm'tl:Y ~t'..tJ# ....

foteign ®unbrlea u not withoUt. tear:a!!l xn fact lt ~•et

a lot ~f 4ebt::w.~n £n the subs~ ~s.. !ftte uwes• . ~ 'arnort1zeticm pa~ts on th$ loafta an -ll.ed. ·~ •

a~tdug ~· aa'6 such ~ •ro• p-ov14e Q atratn on f\ltUt~ :t.taJ.ance of pa~ts be,cauoe t~ pa~ntsCln paflt. Mbt..-

'\ . . ___.

also absOI'b ·a ·hlQb proportJ.on-:" ,of: f6re19fl ~· e&rain91 .

. ~ ~ts, ~rdlng to an <~ts·tf.mate24 l.r. 1911 ·the cu.t"ren~ wt.ua of! ovtJ~rt;antU:.ng debt waa $ SO blllton and ae~

J;*j'mtmta ..,Ubt~ to nea#'lY $ 7 bilUOn, tbe't is, tapp~tdf 40 ~at. o£ nev oapit:al. tnflottth• Xt ~~~ ~lso ~timate<l ttJat)

i£ -~s 8:salsteMe tenaf.ned tltlebangetl ur.tt111917~ ~e..,tc<t

pa~u as e pete~e of gross &.lill1#ttil1Qe ift 1$71 ·W(1U14

/ oxceed. 100 ~ent. :;t J.s, ot •we•"' no~ poasiblt! to ·UK a

11mlt to ·it¥ <J.®t-~ic~ ot. fol'elgn ~mre teeld.pt4t J:G~

thai! sbtml:CI no-t be ~~. · The bade quutlOft ie can a ~

bc>now es rn\JI:b li$ it ~· $'# it -that af-tc a paint, ev'efl

'though a 4~1optag =~., stlU. Jrequiar• l!!fJ!SO~ ~ ft'btoaa.

~ d£$a~ntages oft 1\#the' bo.l"l:Cld."9 ontwoigb tho adV~qesJ

~here ts t1D «:dtenon. available on the bGQ..s of whlch o J~

meat ® the quost&on can be ~J-but th$ tbx'ee ~ra wou14

-~~t consi4et'ation~2' , 1.1 _ * It wM: .l .tr,. t -, - n ·• ·• 1 ·- M •. " _ a t.lt r · ' -

24 ':thl•lwal# a.12. PP• 302.03~

28 M$l'JL'ea, 8.23"

85

•$,) There is a question whether tnc:J:fjases. in the 1nteJ"et:lt

btttden ~eed the in~eases 1n national :f.neome which will

de~ne whether or not domestic Ga'Ving eont.inUe$ to inort!Rse

as a tesult of fOr~gn bo%.'t:'Qwin9• Do•stte saving will

continue to inCJ:ease as long as income !Mrsaseli a~d income

will .inQ.r-se es long as tbe .rate of intet"est on fotetgn lJon ....

owing t• 1f1ss than the P#Otluetivi"t;y of capital.

(2) tther(J is also the question o.f wheth~ Cl(!bt a:.; a prop0r....

t!on of national inc:ome is .~tsing or falling. 'rbls depends

not. only $$ !merest ~:ate on loana but a.lsc· on the re'i!la'tion

bet~ t.he aveaqe and marginal savings 5tio. Q):neid~ t.wo ~erne sltuattorUh At ·one <mtrane sav.tngs equal ~~

inve~t so that 'the ~ebt increases at a .:t:'Ste equal to the

rstle of interest. and if the .rate of :inter~st exq~ the ¥:ate

o:! qtowth o·f tttcome debt· aa a proportion of .inc:orne will .rise ..

At .. the other ~eme savings :exe·eed investMent by Just. anougb

tO A\Elet .int..-est payments on past tlabts so i:'hat thfitre ia no

iMJ"S~ast\l ln net indebtedness~ Be:tween these two attrem~.,

q1ven tb~ s:iSS$ of the debt ~ela1:1~ to nattonal. income (lnd a

·marginal eav.tnqs ;tate m:eat~r . than the investment tat!on, there

will .~ some rate of inte~$t such that d®t will increase

et the $&me ~ate as national income. Assuming no debt at the

begtnning ot the periocl the ~itioal interest rate oan be showrt

to be a. function of' !nttta1 and marginal (}avinqs ratio,. the

capt tal--output. eat:J.o. and the destted growth· te.tef in th~ formufB •

Wh.$r~ 1: a 4~s!red grQwth rate.

so "'* Wtt.al sav.t11gs #&tto.

c • captte1/out;put .raet.o. s a :marginal savJ.nga J:at1o jli

Xf ~be initial a;-at.e of .interest is exceeded, th$ debt ~uld

,~.11 l:J-roQine unmanageable~' in the ~~'Eli o£ being 'WlCO~et.va.ble . by furth~x bOn-.)wing+ Fore£911 eap1ta1 may .<ky til)· and t:r~.,

tor$ may be :fon:e-t to ~::opr.tate assets.

(3) 'l'h..U:e !s also the cons14eratton of x-at.io of d~

sen:icet payments to ~tt earn1n9s as a me&SUJt'f! o£ c:ountl:y•s,

pronen"Os.e tc (laf&.ult whtQh <;»uld be.ve tmpUoattqns ~· fut:ure

bcrltewing eapaoity~21 D~t-servf.ce payments are g.:m-.rally

t-equi:::-ed .tn e()nve;tible cu~ren<:.tes and these twacome e. fii3~

charge ,on export. earn!ngs • BUt $l!tp0l:t el:'l'ltngs haV~ a tEm&m

ey to flu.otuate. KenQe t.he higher the t:at$.0 of ~t-service

payments to ~1!'1: es.mtngsf the greater the likelihood of

def~ult for aay give flt14tuat.tor. in SK.POrt. J:•eipts. At the

s~e tlme.,, a coun.t.ey nteY &1$0 w!$h tQ. aonsteleat the t-atio of·

loan rrepaymen1:a to new .c;::aptta1 tnflowEJ:.,: LOan npay,i't'tents will

exc~ nw t:nflows .tf the rate o:f intettest exceedS the rate ·~ -, - - - '

of growth of J.nvesi:m(:jnt ana the o•put will eu:tul1lly fall

.11! new <:apt tal inflow tall short· of the los$ of $8vilig

. arising-~ .dQbt tepayntent.s•~.

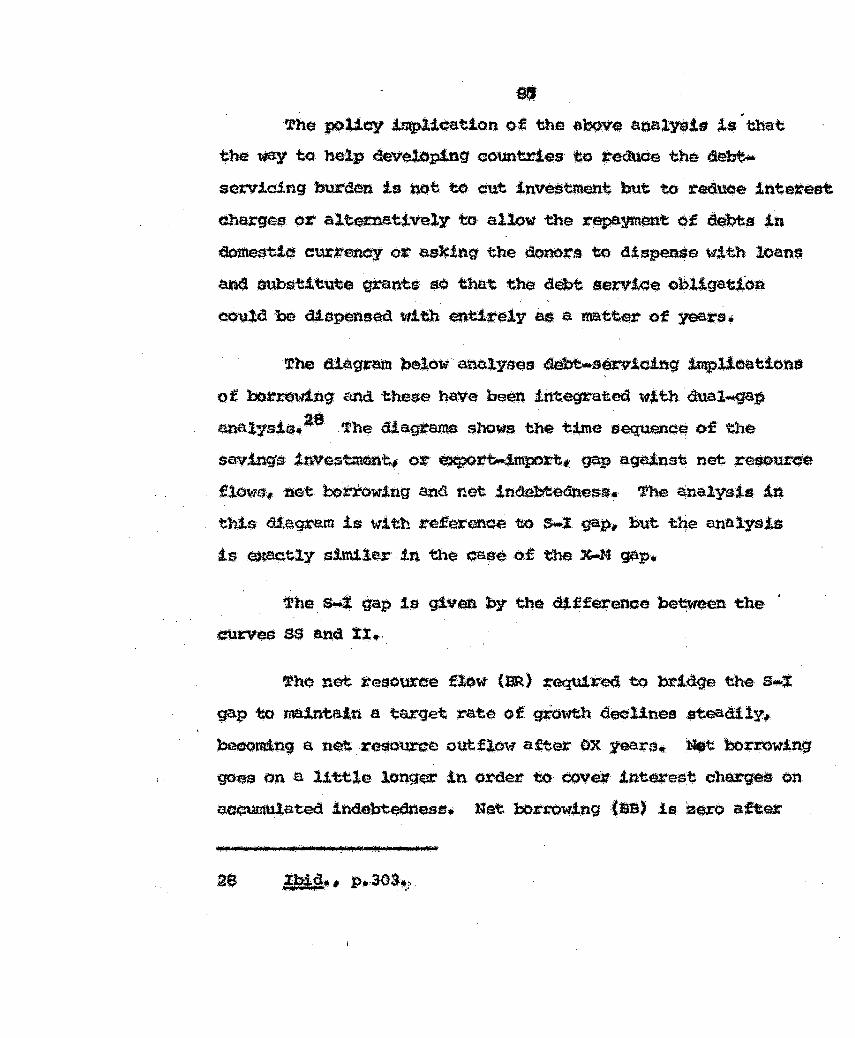

.. ?!he poltey lmpUcatton of 'tme al:;O:ve a.nalys'!s is· that

the way to help dettelt;ptng countries to J:eduae the de~

servioing burden is not t.o out inveStment but to reduce interest

charge$ or a1te=attve1y to allow the repayment c>f debts tn

domestic ew:.r~ney ott esk.f.ng t~ dono:r:s to dispense wtth loaru~

an<! $Ubs.~t.ut;e grants E~O tba1: the debt servi® obllgatt.on

could ·be dts~nsed ttith ent!re1y .as a matte:- Qf years.

The diagJtam b$lov analyses ~$~J.ol.nq .trnplleni:iona

of bOt.rQ\d.ng and these have been integrated wtth ch.tal.....g&l)

a:nalysta.t ae . The d!,agt~ shows the t;tme sequene~ of the

$~U9'~ inves~t,, oJt ~;tt;...J.mport« ~~ aqe.tnst net %"e$our¢e

flows,. r.tGt b:u:t'owing and net indebted:nes$. 'l'he analysi$ in

this d1.e9%!'atn is with refer~ 1t0 S.% gap, but the analysis

,ts ~<ltly stmtlar· in the cmee o£ the X..M gap.

The s-i gap is gi-ven by the <Uf,ference 'bertlween the

dU!:'V$$ sa ana. xx •.

'tho net teaouree flow (BR) requil:'~ to bridge the s...,t

gap to ~intaLn a target rat~ of giowt.h declines $'tead11y.

~omln9 .a n~ .. r~e outflow after ox years. J.tiet borrowing

go~ on a little longer tn order to C.OV$# intt:trest chugee on

aa¢'Umtt1ated indebte&less• Net borrowJ.ng (SB) is zero after

-~--- ---:·-------- ------

I 1- I. c" ··v't4~ •IA"-.hA..( \ t)

, -"1'P~'\(\ '1/) ( $)

1'--l -Q)- t\A::> i14/VtP,

. ~0W (ISR-)

j:Lv-~ oYntt~ l~f-0 )

' ' ' '

' I \f)

f

$9

OY reers and at thls pOillt net ii'l&!bteQbe$fl (ID) startG' ~

®elin~, l>ebt .r;epa~Mt.t:J•- in th«!!li'Yt tak$' p1ac:e by conv~g

the coefJS of savin-gs over ,tnvest.rnent i11to a balanee o~ papents

eurp#.W:1 ®til all tndebtecl.ru.l$$ iS~ ~d by the ~t' s. $£tu

whte:h tl$ e<>Ul'lt#r becom~ a net crea.ttor.

This moCllitl sequen<.'e of ~ants..,_, l$s be$tt ap~mated

to by mal'l¥ of the new- ~~;loped ctO'Untt:£~8-. Xn the case cit manJ'

developing qo\lt"itdes toda-y~ ho'tte'ler, tbe;:e ts lit.t;l-e evtaence \'\~V(Z...

that they t.iie $b!llty 1:0 pay of:B their J*.st J.ndebt;.e~ess an<t

cut aown on 11et. J:e®Wf:Ei .U!flows. The n$$.\ foJr J'G$O'turcea iii

as aoute &$ f!Na1t tand t.bek lndeb-te4n•f:i• is _,untlbg ·b$eause &:tt.

~rt-~t:t ga~- hGJ& replaced th$ a..: gap~a• "r~-~ c:ountt!es

_ t:.tnd tt di.fU<::nilt to tx"anslate dQme$tiQ saVings Lnto aet!vlttes

·whtoh -$e tbe shortage of ~re;tgn -exchan-ge l>eca•e ~~-

are p.d.Ce and income inclas~Lc and tmport.s are '*come elas-tlo-..

'fhat b whY the fanpus t~lO;an •'l'rade uot. Aid' ie (l plea for

more lJ.b.ef:a~ t.t:"ad!nq poU.oies to solVe a~ one and the S$M

tim$ t.hl;! folt.'tiign $l(ehange gap end the 4ebi$-~erv.lctn9 p~Oblem

and the 4ebt..$e:tVJ.ng pl'!Ob).«n a~;isin9 ~ m.ountlng :7$$0UtCe

flows tnay well ~me ~a{loabl.e &n not too dtstartb lutut~•,SO

l:tt.•.--.··.:tltle, x~ an. d .cu.· f ..• ~G. - t'. dt a •.• lt:!t;!ft!S&onnl .!U. Allen .. Mit unwtn (LQndort1 1965.- p.:1 ·· •· : · ·

30 .a!d~.,, :p~ 145~

to

t.l'bl\l analys.lJJ gtv~ a:bove exple.in$ the theo~al t'ela'""

t.to.nsl.Up 'between •avtng• .- Xmtestlil$n\; and ~~il¥\pott .giip!l and

a.lfiO bow these t'W Qe ret~~pt>nsJ.ble to~ tthtl debt·,.'b~n oi the

. dWE.liOpl.ng OOUt!tX"lG$~ wow it w.tll. be 1n~erest:lng to e~e the

.aeituaa ~nence oi! thiit developing oount.Ji$-ee in ~'O~a.tion to.

•avtngs• .snve•tlt'tent, l'3nla~£:~ o~ paymEmtst ana debt OW:®~ • .-

~eal capt'tl,ll fol:mat.ton from dom$stic ·,:eso~ea requi~~s

investment. e.n4 a. eottmenaurt.\t;e J.~~~$.~ ln · tbe VOl\1;\e of teal

se.v!ng. ln tlte iibael'lde of .tnteJ:national ttade and. foretQI) " < ' :

bortowt.ng• cap!:t.al fonnatton 1.& only possible thro~gh. abstin~ce

~tom pt.esen'l:, ®MUl'l'lptl.on ana when so¢Lety· 'PtQd04ea. a stl)tl)lus

tlf consun@ good$ .su~·ac1Gtrt: to meet the neec.is of labow:: engag~

1n pl"Q~1n9 capital, xn a subsistence economy saving and inv~

stJnent. are slttttd.~$!:>1J$ act$ wbU.e in a ltlOtt&y exchange eeonomy

savtnS'$ aDd inv'"t.lnt:mt may be 'un~aken by dif!er~t gr¢1.1P$«

ana ~~ proo~s of cap~~l fo.~Uon ts Ukely to ~~re a<>me

fo%1n of fin~nce and cred.lt ·meehan1$m to .r~d1$tribute l!'eS()~es

trom s&.Vfl:t'S to i'tl"''estc>rs. ~n t.he early st.a.qes of <Jevel0pm$.l'li:;.

main ~1e~ to capital fc:urmat.tol:'l &:Jes mt dQne fl!"9tn ahottagEt

of s"ings but. \lD.WilUngness to J.nv.._t an4 1nab11J.'t:.y to tnvest

in Jrtsky' vent~G$* one way -to overcome this ptob1em is through

!nt~tnat.tonal taeade and foreign bQ~g31 and it ~.e for thi.s

91

~te&son that. ~M ~P ls Uke.1y to ex¢ee.d t.he s-s gap in the

:eaJ:l.Y stages of &;ave2.0,pn&nt•

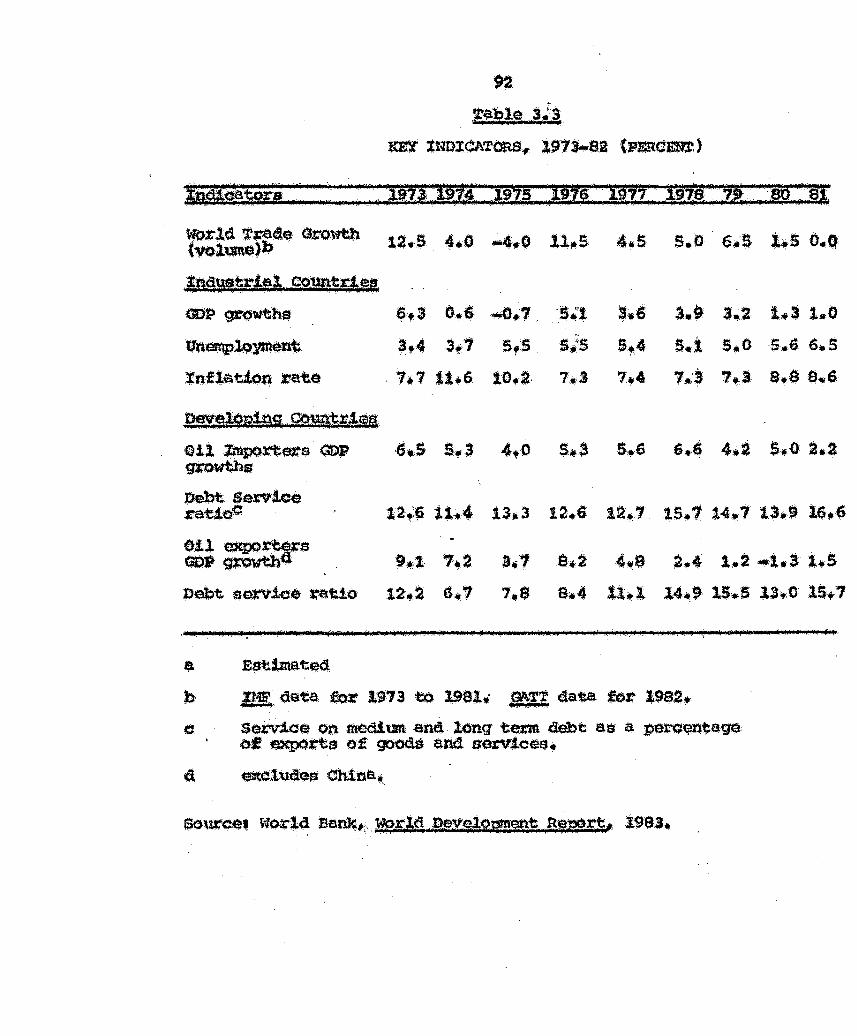

While loold.ng at the ~er1enae of the ~~1«>pU;tq o0Utlt:.

t'i&.s, our: ~g pcint WQu1d be to look at the key- indica-eon

of ileVf)iopment and how they nave behnveti Ln the r:eo«nt pase.~

The teport32 pctnts out that the· ~ession that nea$ afflic~ t.he world GQO~my $~e .19&0 ~s to -~ Qa$itl)J., i But tme

eco~a eondtU.Ons .tn Utatt:Y de_v$l{)ptng ·aountir!Et$ ~V'e worsened~

Me.l\.Y middl~inoome countltle$ have fac(1Q a .1iqu1<i1ty cri.sis

than W£l$. ~ec:tedf b...···c-.n:r.qht Qn by high .int~rest i:att~Js a~ reduc:!ed

il«n$l'ld for ~ns. tow ineome countries dependent· on the

expott:, Q-f raw •t.e;tal$ nave wfi!Ued ~m b1s~~oal1Y !.ow · ocnmodtty ~l<#ea 1n rea-l -t~. ·

trbe d-ev~1opj.ng ®uni!rieS' pt'esent dif f!cu1ti.tas a~e ube

culrntnet.t.on o£ f3Vents -&1 ting ba~k a decade ·Ot mo~e. 3-3 They aJ:>e

~ eon~end$ ~ll' of eonditLons in the tndustnal market

~nomtLe!l ·Slld pax-tly of theit ~ pOlicies., :tt i~· quite ¢1ea~.t

.from· the ~@le J.-~ that the reo~ei.On ·Of. the paet t.m:~e ~rs

~s no simple _.epetit.ton of t.be midi!!!il.t70s"~ following i:'he

hike in oil pt:J.-ces in i973t GOP gJ;"Owth rates £n indust,;ial '

~notd.es fa11 sha.J!ply for tWQ years and then l'e¢W~e4 t:a.p1dq

l:n 1$)7"' al.tho:UOh l.n th~ ttu:e~ sub$equertt. vear• -wth --•

... . t···x

~a

33

worla: ~ •. n~ 21. 1993t »~>•1·6~.

;tb:t(t., •. pp·· •lw.2 .. . ;:;, ' ~

92

~abl""" 3·· '3 f_ ., .. ~I;!;

ltSY 1NDXCATORS, l91S..Si (PE.RCEN:r.)

'fO:t'.ld 1'#ti4Cii Grolitb 12•$ 4.0 .;..4,.0 11-.S (vol\llQe)b

.~~t£!!1. ,P.~!!Qt:r4e1t

anp -cwths

unernplo~tlt

lnfl$-tion ,;ate

D~UQ~s. ,POtL.lt:Sltl

•O.tl ;mportets G'D, ~wths

Pebt Servlce rattce

a Est.trnate(l

&,3 () .• &. ....o.-1. !-.4 3i1 s,s

. 1,. 1 11•6 to .. ~.

o •. l "7-2 ~ ., 3"1

12 •. 2 G.,? 1-.e

·s ~~ ~-

s~~s

1.3

a. a 84 ...

~·6 39 • S"4 s.t 7.4 7 •. ·3

4 .. s 2!!'4

11.1 14.$j

Jl· ltlDr,. QSta for 1973 to l981>i . ~TT data fOX' l;9S},.

3.2

s,o 7 • .3

1.2

1S.JS

e S(;trvJ.ca on aod!un end.J.onq tem debt as a ~~nta-ge. o£ ~.tts of goods and $~ieea. ·

4 ~lude$ Chitta•

1.3 1.0

·.$.6 6.5

e. a a. a

·1·' 1·5

13.0 15.-1

93

still we'll below the . averaqe for the 1960.s. The. s~~nd

roos$sion was $hallower than the fhst. l::>ut tt bas last(!d .longer

since industr1aU.Ze4 ooun~tes ti9ht~ned monetary coptt-ols to

brinq down inflation but the unemplOl'frtent he$ picked \l.Pto· e% from 'that of 5%<.

Developing ®1.11\tl:ies ere directlY a.ffeoted. by fluct-uations

in the .indUstrial world.M The.!r overall #'owth rates have

been higher, but even tb.o$4a that have grow fastest J'tave not . . .

b~on able t.Q avoid the eyeUdal 1.nf1ueno~ of industrf[al c:Otlntries.

'l'h.ey bav<~ also bean af~t~ tr.f high 1n:te)re$t rate$ as a result,

many dwe,1()p1ng- eountJ:i~s hav~ been sque~ed beet.:~ stagnating

fOreign exehangt;;! ·e€1nlil19S and soaring .irtterest pa~s on their

debt.

Df;!V'elop!ng CO\li'it.r1es ·have :r~c:rtt.ed to t-hesE! p.Jtes:sures in

4ifferent ways .. 35 Those middle ineome <:Ountries ., l'QP.inly in

~st. As.ta - have manaq~ t¢· ma!ntaln the momentum. of ~rt

~n$!on and avo~d serious n~ tiebt pi'Oblems,.. aut some eQunt

~i(Js, . ineluatng several in Latin. Amertoa that bat$. bo~etl

heavily and adjus;te(l less (o-r inapproprtat&ly) durtng the 1970$

bava been hit by the high interest rat$$ and )'la.ve ha~ to deflate

~n .response .to a llqtd.~ty cr~sts. In Latin .America as a whol.$;

aceorrdinq to prelJ,.tninary estiJnateg, ®l' fell by 3•6 ~roent

bet.t-1~. 19so.e2. 36

34 !bid.~ 1993. p.2.

35 :~~tlfi ~·Ilk~· n-,.21. p .• 2.i,

36 Ibid, ...

94

9ut. xnata .an(! Chtna bav$ shOwn enC:O'U.I:f1Qing reststant:e

in ov-ercrOllltng current x-eee&slort. 31 ~hey were not s¢ heavilY

·dependent on fot'eign trado•, ha4 llt.tle <:rommercial debt" and,

ao were not mucb effect~ by ·htgh interest rauea ana have

mad~ impl:'GSsiV'e progJr•sa in egr!oultwre~t India's iow GnP

growth ln 1992 was largely due t.o the f!e.Llur-e of t)le monsoon.. 3'

:But. tbe Aflr:iean countries h&.Vl3 suffer~ badly, their per

qaptta tncorne has continued to fall and is ~ed to !all

furth~ and .t ts prevention will requi~ international aid. to

the$e eountrtes .• Sf

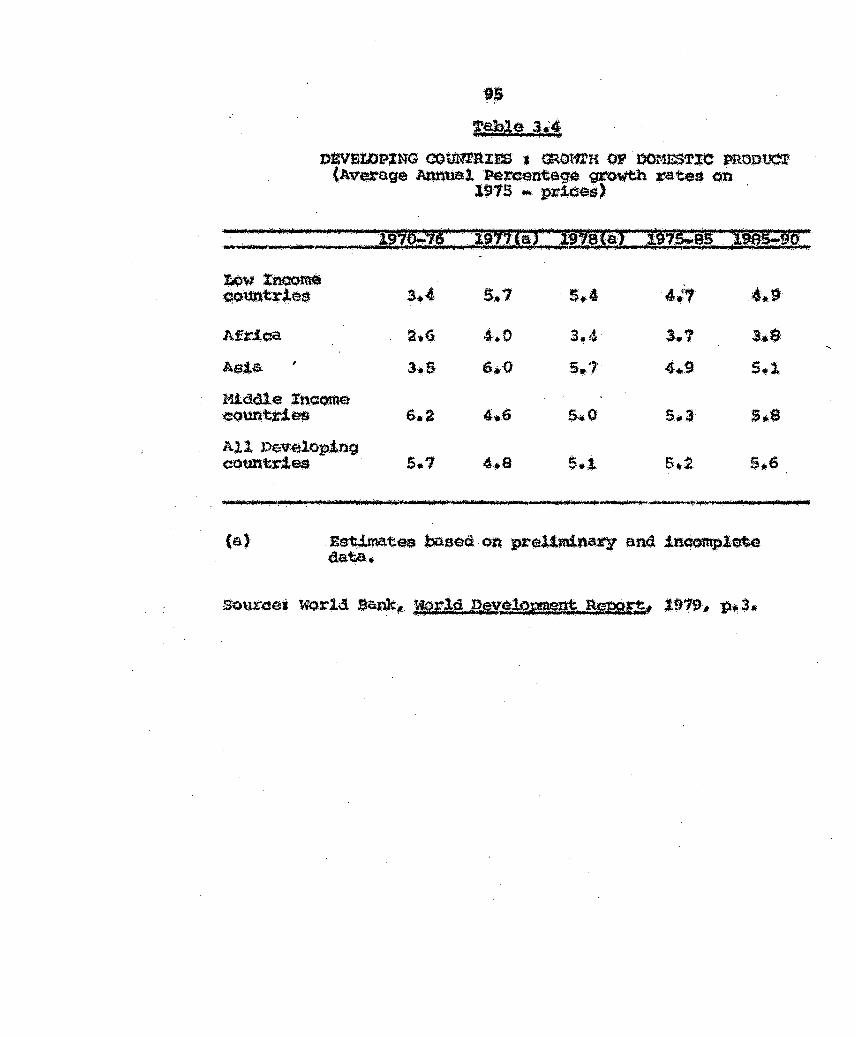

vJh!le aomt.aring the growth of Ql!'O$S domestic pro(luet o,f'

1970 with that of 1990 for d~eloptnq oountriss,.. (.of courseJ

the f$..gures i!o~ 1990 have ~ pi.'Qjaat$d.) as listed in Table 3.4.

tile qcnQJ.us1Qll Seetna to GmelNJ'Q ·~ ttl.o. tJ!l'III\Q:fl\Uf.Jtl."))l ~ te

~-that ~~the ~!od 197S...S5 th~ main che.*ges that a££ect

the d~e1oping CO\m'b:i~~ ax-e alightly sl<.>~:er grOwth !n indus•

t.riali~•a cotmtries~ world. tta(l(l) and external conc..e!!t~d.onal

assistance; e.."\d a diff«E:n't trajectoJ:Y of privat~ commercial

lenainq~ 40 'rhe ove:rall e:ffeq~t is to :reduce the proj eqted

annual growth of ~o~s domestiC product in. the developing

oountrlet;~. in 1915-95 from 5,7 perl:lsnt to s~ 2 pe;:cent.

sa 39

40

world,. nwel-ot:MJlt Remx:1i; o. 2~ t>~ 2. •.

world ·sank:~. ·tr,e,r.id oovtl2ta.en1:. B!WG~. lt?a, p.i~

~~

t~hJ<t ,3~-·'

DWtn.OPlNG COtJN"llRIES 1 ~OtfrH OF . DOrm.sTIO PROOte.r (Average Annual 'J?ercentage growth ~ate$ on

· 1~75 - price•>

Afr1aa

A$,I.S.

Middle tncom.E~t eountriet~

All Pe:velo~tng count:r:1es

a.f

a.G 3•5

6-.2

5.1

5.1

4.0 ,_.o 4-.6

4 .• s

s.4

3 .. 4

s~.7-

s.o

5.1

4:?'

3.1

4 •. 9

5~3

5.2

s.a 5~1

· ·.::i:d:(.--u · -·-·-·-··ar" nsr,·s ··· --iauc'f,. ,._, .-.,.·-, __ .,._.,..._. •• .,.:-t,..w.-r•• •·'*'f!~'*-· .. t .. -, ·i_·_.-

(a) . ~~tee baaed on prel.Ud.natry and indom:Plete data.

96

-the largest . .:~uetion is seen in· the Mtdd1e Xnoome

countries ..,. fJ:'Oln ~h 9 perce-nt to s~ 3 percent a year • A $.1aeabl$

r:e<luct1¢n ts also !nd;lcated ln XDw x:naorne Aftlc:an CO:U11tr$es.4l

in the light:. of the infc>~tion r~g the m:owth

oi oott lor the •eloping countries gtven ab()ve. we can s-ee

tbe s.x- and JC-M. gap. Table 3"5 .stunmau:·!ze$ the ea:v·ings an<ii

btves.t~mmti e.e a perae11ta·ge of oross dbmesti¢ practuc~ at. 1~15

p,t.J.cea. The ~rison .$.8 rmde between t.he actual ,esUma'te foi!>

the year 1916 with that of; -the p;t:ojected ftoures of 1•90.

Th~ table snovs that the aav.tngs anet investment as a ratio of

GOP an ~~er! to ri$e :&om 1976 ~ U'O seen either in.(l!v.s....

<lually for Aflrica., Asta. FA!Jt Asia an<! Pact.flc. Mitt<Ue -.t and

ltolitb Atrica.; or for th~ gt:Ouji$ as a 'WbQle for Iow ~~:orne

<:ountrt.e.~J, M!ddl~ Xneom:e coupt.ttes Q-X' the Dew~loping e~ie§

~s a wb()le. What is more .f.mport~ant to note ie the gap betveen ' '

tbe ;t;J.avtngs and the invee~nt #at.!o. For .tndividu~l. centr-e-s/

groups the . .tn-vestment. r~tLo ts ,l~Y to-~ the· $&.vings

r;a~to ~ tb~ the s.;..x gap is Uk~ly to temain~ 11le teason$ fat

this wsp may be quite obvious nami!itly, high population qrowth,

1Qw pJ:Openst.ty t.~ .Jave,. inor$aatng m¢te.tn.a1 capt tal flows (But

t.he net :flat~ of ~ernal. assi.stanoe tc> •tess oevelo~ countrie.s*

~- a wbQle ts ~- to decline as a % o~ GDP) and the aeetl

far increasing £w:theJ:> the devel-opment ~ffort whi<lh t~auld requA.n

httqe investment ;-es~ts~·

~able ,lt:!i XNVFSl'MENr AND SAVINGS RATXOS, D'EVEtt)PlJtG COU!ft'RXU* . ,tg.1'6· and 1990

, . • .. ;(P:~o~aae ·~~ ,;rsss dgmes;x-;a, :emd:gct. at 197J · pr&ces~) . , .·•·· Gm'ss nomest· <Cinv.eatmsnt Gross: Domest.tc Net flow of external

· · savings ass.tstance. · n #.' 1

p, 1976 0 , I 199~ 0 1 .'0 j 19:16i! 0 II 1:~90 *!76 I 0 199p

Low Ineome co~EJ

Africa

I?. a 16•0

18~0

Middle lneom:e counU1es U-•1.

East Asia. and t.be Pacific 21 ... 0

Latin America end t:h~ Antill~$ 2'3 .• 7

Middle East and North Afriea 31.4

Africa South O•f' Sahara 2?~1>:

southern Eutope atS .. a Developing· c:omt.r.i.es ea a whOle 24.8

25 .• :0 15.1

22.'1. e.s 25.3 16 .. 1

24.:0 al~t

30.t as.s .

2o.·o 22.3

a!l •. 1 29.0

24.4 25.1

al.a. 19.-0

as.a 21.9

. 2l\.t2 2.t 3~&

..

'11 "~4. .... ' 7~2·. 10~~1

22·· 1.3 3.:0 .

23.9 3.0 2.'1

J:l.~ 1.$ -0..'2:

'2:4 •. 8, 1.4 1.'2

!2.·() 2 .• 4. s~1

21.6 .l;; •. S} 3.;4

.21 .• 1 1.2 2,.:7

23 •. 5 2· •. 9 2-.3

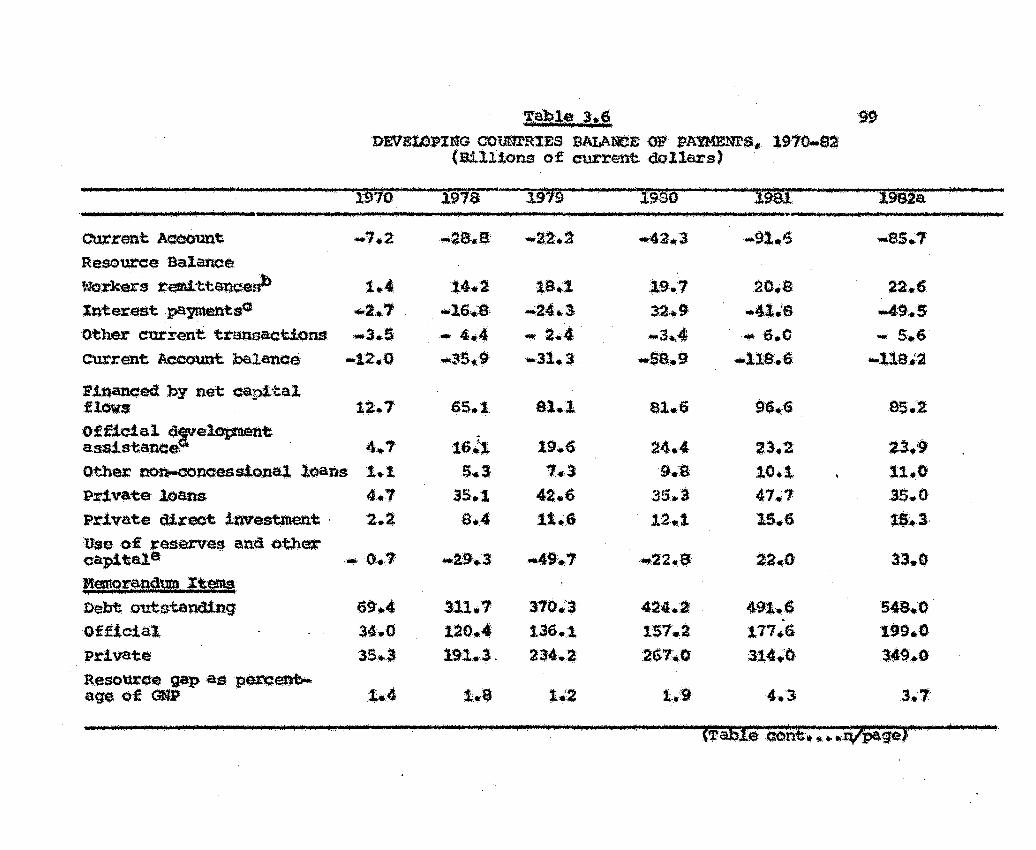

This gap between savings at'ld i,onveatrnent will Qbr/iottsly

be met l>:r fore,tgn bortowinglll This \dll invo,lve an .analysis o£

1.mpq~tt., •)(pe)~, balance ot payment, the qUanttum of fOreign

assiatanc.e and th~ c:Qru)eqnent debt ratio in &:ivelopl.ng <I!O~tries. ' . . . ,.

Jn the ea•ly 15)80s tnaQY c.ountr!es Jtan into sedo.us /

L-.al,anc$ oi p&YJftG.J""lt$ problems"'42 ReQessio:n 4-n. the ind\letrial

countries reduced the export ·~ngs <>f aev~lopinq c-ounU".ies,

wblle. 'high real interest t:ates tnex-ea:sed t.h~t' debt serv.ice

obl!gatJ..ons.43 some lenders ccncerned. about the ability of

.,indiVidual borrowers to surmount thes& Q!ffieul;ties and unoe.r:-•

· tatn about t.o.?'(Utld edonem1e prospects, b~ame l(!$s wil3J.tlg 'than e.

they have been to ~ettse theiz: l~nqs. '!'he outcome for (~~~ . . " . a::u. deVeloping in ·1992 on Table 3~-6 i11~at.es tb~ ~ent of

tleterl.orettoncff For t:nst.e.nc:Qi

(1) The C\Jt1:'ent a~eount. <iefi~t. was $ 1!9 billie~ th$

same · a• on. 1991 end mt>re than twice that in l'eo. tt wasequ1val~nt .to .5% of (tip anca_asn of_ exports o:; good$ and non

£a<;ttor ael!Vt<:Jes~ By oontrast. in 1~75 (the preVio\l!il peak

deUcit year) def$..eJ;es We.t'e 3.3% Q# GNP and 17-.-S% <'f ~s.

(2} .rt ~ming$ fell for second ~ons~t:tve year, to a level '"below that of .1980 .... the· resul.t <;)f declining

4o11ar pJ;"ices of e;cpo~s end stagnant volume.~

42 .Korld Bank# n.2. ·pp~3-Si

43 ·~s.~: ~ pp./3··~·

44 Worl.d.Sank~.n.2# p.19•

.tr~ble l.,f>. 99' - I - . -

DEVELOPXNG OOUNl'RXES BALANCl:: "'. PAYMEN.rs.. l97~S2. (atl11ons of current dollars)

,. .-,

current Account •7.2: Resource Balane&

Workers temi.ttar.u:eab 1.4 Xnterest .paymentsO ._.2 •. 1 Other current transactions •3.5 current Aecount balance -12.0

F.inanced by net capital flows 12: .• 7 Official &:!Nelopnent asaistanc:e4 4 .. 1 Other non-eonc:essioneJ. loans 1.1. Private J.()ans 4.7 Private direct. irwestmellt · 2.2 :u$e of resatvE:fs and Othet' c:ap1t:ale ·

~emor9l'l5lutn Its Debt outstanaing of£1e1al llr!vat• R.esource gap as perc~ age ·Of GNP

6,., l4.,0

3·5-.)

rw;s .. · .. "f9'79 ·• · ·

14.2 •lo,.::S-

- 4-.4 ·35.,.9'

65-.1

16 .• ~ !l.3

35·.1 .a.4

~11/1

120.4 191.!.

;os·ft. ..,. """":.c.: • .a

1S.:t . .a:2;.4.3 -: 2.4.

-31.3

81.1

19.6 1 •. 3

42 6 ... 11.6

310 .. '3

136.1 23'4 •. 2

. Sf-

t<'isao li'l- l -

·42.,.3 -91.?

,).,9.7 2:o .• a 32.9 •41.'B .3 ... 4 ... ·6.0

-se.9 •llS.6

&1 •. 6 96.16

24 •. 4 23.2 9.::$ 10.1

35.3 47.;'7 .12.115.1 15.6

·•'22 .. $ 22,.0

·424.2 491.6 . 157.2 177.6 267-..0 :3:14:.'0

1.'9 4.3

-as.?

22.6 ·49-.5

·-· 5.6 -11S . .t2

as.·!

23.9 11.0 s:s_.o 1&.3

33.0

S~Ui •. O

199.0 349.0

3.7·

.• j

CW:x.-mt A.oeotmt deficit~.percentage .of GNP·

llebt' service a$ ~entag:e of GNP

Debt service as· peraeni:age of ·EtXpeft&

l'ntq.l:a.st pa:ymen.ts S$. pf!rt.lell-· · tnge o£ ··GNP

Deflatex-f

a Es~at.U

il ~.

2 •. 5

ll.:S

o.;s

38.:4

b Rat~ oil red. ttanoe peytneuts.

!.:2 1.:6

4.-0 4.,3

tS.4 15-,0

s·o . .,· s.s S3:.o· '91 . .;?

c Xn~est. paymen:ts on medtum atld long ~ loans

.2.7 s.:s s.o

3.1 4.5 a.. a

1:3, •. & 16.-3 :!0.7

s.:SJ 2.;0 2.1

100 99.3 98 •. 4

d Bet . o.ffie.la.l develoi;.inent cls:ststClnee:.. def.ined as not disbt.U."senent$ of· eoncess!or.tal official loans plus net official. tran.sf~s.

' . . e Other eapital .f.ncl:udes .. net· short t.etm borl!QW'inq, eapj.tal not els·ewhare indicated;

no •roro ·and.. «td.sslonu. · t us doll~ GlP defla~r fo.r .tnQusttial eot.ttt~t$$ ..

SOm:ctl~. worl4 Bank,. li'lg.t:,ld .RUII9Pment, .~..!W~" 1993 . .- p.J.l .•. . - . . - . . . ' - .

101

(3) Xnter•st payments on medium and long term debt rose

tO neatly $ 5~ o billion SD% above their 1900 leVel. The

r.t>ndon Interbank Offtar Raue (X13M) fo~ six month dollar

d,epos.tt• averaged 16~6% in 1991 and 13.5% 1ll 19e!_.

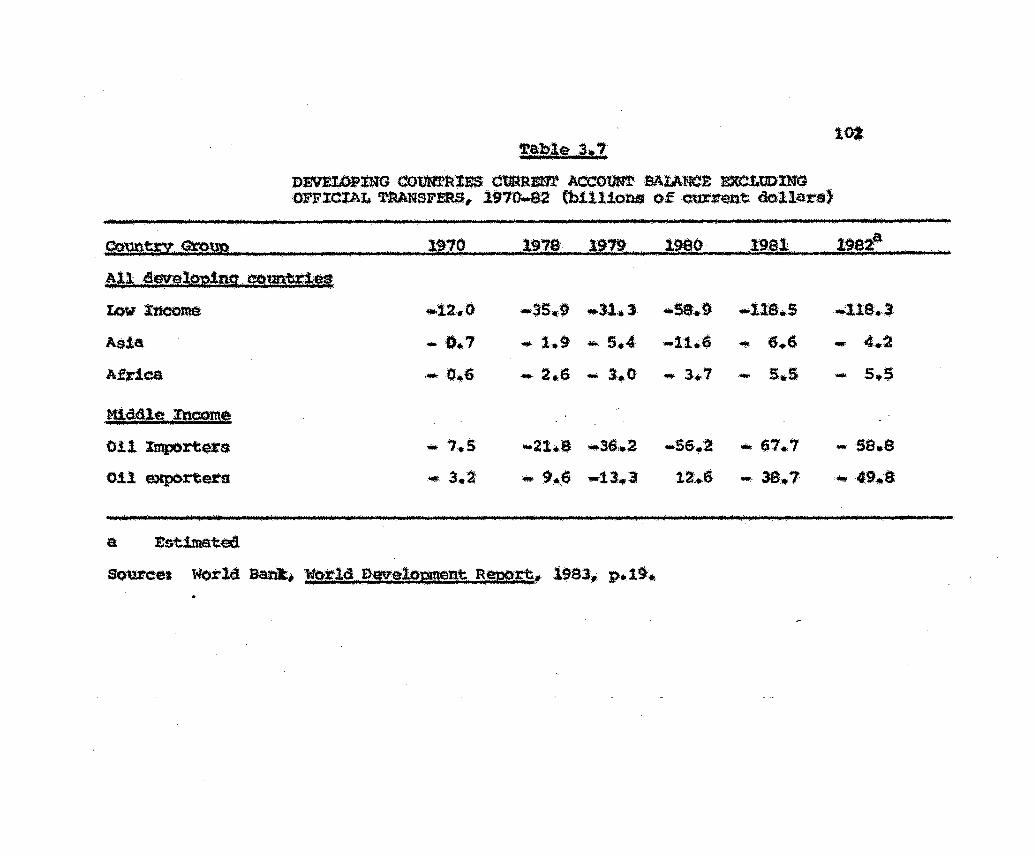

The external det$t"i.otation a£f-e¢!ted dif~etlt group$

of developing ,countries J.n different ways •s ~hoWn. in Table

3.745 Fo~ oil import~rs the high tntete$t tates a~d dep~ess.,Ci cap,J.tal markets of 1990..82 came on top of the 1979-SO

,rf.af.! £n 'tJil. price$ to whieb most eountrtes bad btlt'ely sttilrte.d

to aciju.:rt,.- Between 1978 and 1990 their current account.

def4.<t!t lt'Qse !rom $ 21.6 ~1llton to $ 56•2 billion, Well

though they reduced the rate o~ growth tn the VQlume of t:h&ir

:.i.mports fJ:Om an averag$ 1 ~ent a yee,~ tiC 191$..7g to only

4 percent in 19-SO• In l991 theY held ·the volume of thelr

. imports constant, bllt! this <ltd not $top the defteit ftO'm

Jtistnq to a new peak of a,lmost $ 61.? bill:i()n. E:,q,ort.:-J wer~

fal:ttnq ;:apidly while interest payment.s sttll ro,.e. Xn 1982

expo~t eamings fell agalnt stnae. <::at?i i1al importing count.rJ.q

were unable eo inereasG their l»rrow1n.g,t. they had to cut

back the!~ merchandise imports.

The oil exporting deVeloping (.Wuntr:t.es initially

benefitted from the l91J-aO t~ss in qil p.r:lees• However~ aa

the tnoment'Um of expanding imports ran J.nto pt'Ogressively

J)!.VE!.DPlNG CO'liNTli1!1$ ctJ:Rnmr ACCOtm BAlANCE EXCLUDXN'O OFFICIAL lf'MNSFERS" 197D-&2 (billioNJ of eux'~ent dollars)

. ~U develQllins. em~

Low rnccme

Asia

Africa

f!lgdlg. Jpeontt

Oil !inportel'S

011. exporters

. -1!7.q '"'

.;ta .• o

- 0.7 ...... o.s

-7.5

""" 3.~

191& 1979 ' .

-35 .• :9 ... 31.3

.... 1.9 - 5.4

• 2.6 -3~.0

•21.8 ·36.2

.... 9.,6 -tl.l

... sa.9 . . ·• •11S.,S

-11•·' - 6.6

.... 3-.7 .... s .• s

-56.2 ..,., 67.7

12.6 .... , 38.1

.-na •. J

.. 4.2 .. s.,s

- sa.e

• 49.,9

103

_Weakening 4emand .fer otl ana tbll.$ their surplus of 1980 ·

swung .iflto deftc:U: tn both USl and l.992• ~hetr $.mpt>rtt:J

rose by$ 4S billtc>n .ln ew:rent pr!o$$ durtnq 1980..82 while

expurta fe.ll by $ i3 bl.llton .. 46

In ·the 1970$ medium. and lOng tetnt borrowing exceeded

otwren~ payments needS and re$ult.ed In a sttb8tant!al build

Up of fO;:etgn ex~hange resotll'ees~47 -t'he $ eo biilton ~s!on of the combined current account def!C!its of: dENeloping

countries between 191S.S2 waG accompanied by notable sbi~s

t.n ftnaneing pat:eerrm,. MQ.<U.um and; long tE»..rm finfl.noa I:"'Sfl by

30 ~cE!nt over thts period but this inezrease met only 1/3r4

of the rJ.se tn ~be current aeE:otUlt deficit.. Within thi.&

total.,. 1ol'lg.terrn private 1em9!ng, which ha4 expanded to $ · 48

billion in 1991,·£~11 back in 1992 to close to the level. !n

197a.. Net receipts of ODA expanded by 50 pereen-tr between

··l97S and 1980, but. have !'fubseq;Uently stagnated" plnoing

sGVete st,:ains on low 1ne<m\$ cotmt.ries t.hat cannot borrow ·

pdvately. 4S Net private dh"ectl .investment wh!cb began to

accel~ate ln the ·late 1910s also stalled. as growth in dEJVel*'

oping and. lndustr.tal count~:1~s dealined..49 MOst of the eat:ra

46 !fo,r,ld nwelg:e!!!!V}t . Repol£S:;. u~ 32~ P• 20.

47 !W-et•·*' p.2o.

49 !fO.rld 1Jank,":n~32,. p.20.r 49 !1?.\d~:-\ p.20.

104

S.nan¢ing needs sine$ 19SO have 'f:.berefore been met by both

resot.1rces l'flGVettenta al:td short-term bo~ing~t 50

Now J..t has been established both theor~tid~l.ly and

.-npiric:ally that domestic def!ci ts continue to persist an(l

rather tn 11'tcrsasinq amo.unt over the yearet· tberE!fox-t:t.. 'the

importta.nctt~~ of the inflow of G(ter~t&l. capital fOJ: 1fbe develop.

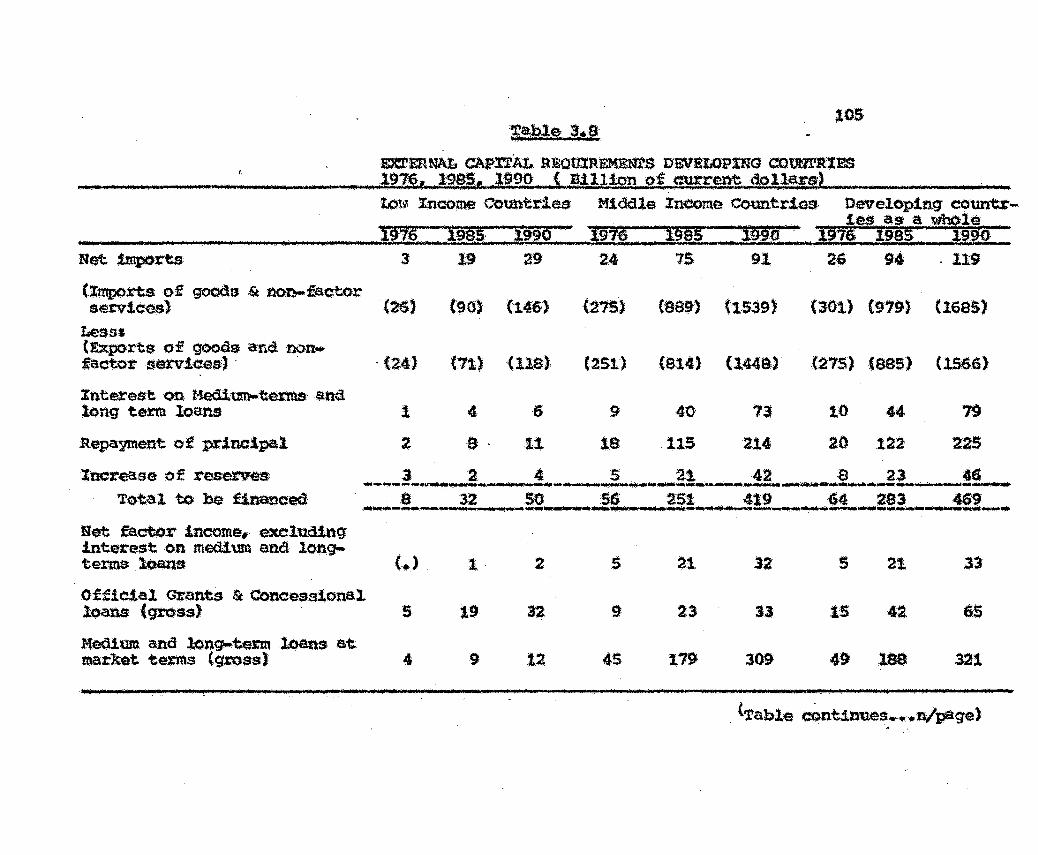

ing aountrtes <:!&Mot be ruled. out,. !n faet~ lt aequlrea a11

the more .important r:ole as they ~bance theitt d~elopmant..

efforts~ An. estttnat.e as w~U as the f.utur.a projections about

t.hQ eaptt.tll requ;trcnetlt$ ~.e given in t'he i!able below. The

tnvest.ments of e. :Qountry are equal to its domosti¢ savtngs1

subj taCt: to one varieblo,. the $;!fiei t in tb$ C1irrent balance

Of payments~ This dcflett pOsition,. elthOu~ no:t un~m in

eettain ~el~ countr'iea is pert1.cularly widespread in

the· c:tevelop1ng c:ountrles- This deficit can be f!tnanced in

.different \i'S.'YS.t net private transfes:s.~ e~ternal i.naOmet foreign

.tnvesttnentt but aJJove all tlu;'ough government grants anct. loans, ' ~~ . . .

at Sub$¥ed or market interest ratet~,o; Table 3·•S shows the

gro:w1ng neet\ fol:' fin≠lng haa two main ortgins. The first is

the repaj7rr.an1: o£ prev!out!! debts and the second the defioii:

in tba balanee of trade and 'dt.h .internal pl:'i<;:es rising faster

then the extatmal pric~s. the real debt will grow heavier"

while ~~s will be more difficult and .t.mporta will b~

dearer a11d thus the defieit. vi11 tend to inar~se and th~e

J . I i8:a iiW ·-- -

105 ·t,a,ble l•'f:l

UllttUU\L C-t'Wl'l'AL lUliOUIRIMENlS OEVILOPING COtltlrRJES t ) . ,-_ . ·~ 19_76,.. 19~c .• l99t;. ( ~illion pf e~ros~t dollartd ...

.... ; l .. 7 l

(Imports O·f goods & non-factor serv1ces)

Lesss (Exports of goo.as arvi ll01'1o1ir f'aetoJt services:)·

l'nterest on 11editn'llo*tent\S long term lOans

Repayment of. principal

zncrease of resewa Total to be financed

and

Ret factor 1neolne., excluding interest on medbun and longterms ~s

Offietal Grants & Concesaional loans (g.t'()ss) ·

Medium and lon~term loans at xnarket tems (gmss)

l:otf Xncome Countries: Middle Inccnne count.rie~ llevelop1nq c::ounu-.. 1e!J a-st a whOle

(25) {90) (146) (21S) (aSP) {·1$39) (301) ('979) (1685)

·(24) (:71) (llS)· (i51J ($.14) (1448.)' (275) (SBS) (1566)

1 4 6 9 4tl "13 10 44 79

2 a 11 18 115 214 20 122 225

{.) '1. 2 21 32 '$ 21 .33

5 1~ 9 23 33 15 4:2: &$

4 9 12 45 1'19 309 49 188 321

<.,;ablf! centinues .•. ..,.n/paga) '

. LQw-fncome CO~tr!es Middle Income Countries" '"nc:WelOpfng-eountrJ..e

. . .lfti.f : :it~.Ja:: : l!!t[ , Hil : ::: ~~~~::: : l~2o: :: =tiita::'::~l:: :. :-.J~9Q: · I . J «

Direct lnvestment and other cap.t.tel (net}

Ne-t private 'transfers

TOtal f.tnanci:ng· ·or ~pi tal :reeeived

At. 1975 price~;~

,-1

(.l

a

2 3 .. s

l 1 2

so 56

17

23 '36 .,0 25 41

s e .3 1 g

251 64 283 469 -

147 133 -165

--------------~------------------------------------------------------------~ Total• may not adii due to rounding. The assumed ·average annual rate of tnfla:t!on bet-ween 1975-90 i-s 7.2%

/

107

J.s a danger that inflation could be one of the factors eausing

increasing financial requirements which wiU be met by external

loans. 51

'The main forM$ of international resottt'C!·a flows to

dcwelop1ng countries consist of pt!V'ate :foreign 1nve!}tm~nt,

bilateral grants~ loans and teehn1eal a.ssist:~nce and multJ.la

'teral a•stste.nce of various qpes channelled through intetnat•

iona1 inst$o.tutione such as eba united Nations, the wcrld Bank

and its aff!l!at!on1 the Intetnat.tonalt>evelopment Assoete.tion

(XDA) and the lntet'l'~St!onel Finanee co~ration (l~C) + The

'q,rant olement • o:r • aid eomponent. 1 occUpies a place of $1g:ni f

tcanee,- in ·the total assistance, reee1ved by developing

countries from donors, The grant element or bene~1t of $1d is

mea.sur:eti as a 41 ffet:ent!al (as in cost benefi~ .analysts) beween

return to internat.!o.na.l assistance (whieh is the dif.fer«lt'!e

between the nominal value of assistance and the r.epaymQnts

discounted by t!be produetiv.ity of assistance in the ree1p1ent

country} end the benefi.t of assistanee (W'hieb is the difference

betwe$n the l'iOtninal value of assistance and repayments diaeount.cad

by the rate of interest at which the ~untry would have had ttl

borrow 1n the oapita..l market, ).52 O~iously if ~he x-ate at

which the country borrows ~m the dono.r is as high as it oould

' . 51.

. -

have borrowed i·n the free market,- t!.here is no ~ant element.

attaab$4 to the capital transfer.. The bene£,1.t of <as:s;tstanoe

may dlff~r !tom .t ts, however:; if the east stance i$ tied to

thE purchases of dono:rs• 9oods which diff~ in prtee from the

world ma.1.'."ket prtof!ht .!f tb~ was no concessionatY J.neer(irst

rut.a attaehEK! to the qap3. tal flow and t.he prices of dOnortr'

goods were higher than the world tnai'ket prices, the value of

thd. aid would ·be negat:tve.53

The developing eo\ll'ltries ha1te redeived ¢apital flowe

from e!thelt' pri~ate sources~ namely dir~ invest::ment. pOt:~

fo.lio investtnC9nt and the provision of export credits ·o~ offiCial

sourQeS which comp"'J.tie of five prin.clpal. forms e,.g,. grants

tt.neluding tecbniea1 assi!Jtan<:e) conc:essionaJrY loans (.J"epa.y-. . . I

able J.n bor.l"()\fe):s' ot lenders • currency) .; eontrtbutions in

kind~ supplie!rS credi.i!s and the repara t~on paym~ts:.

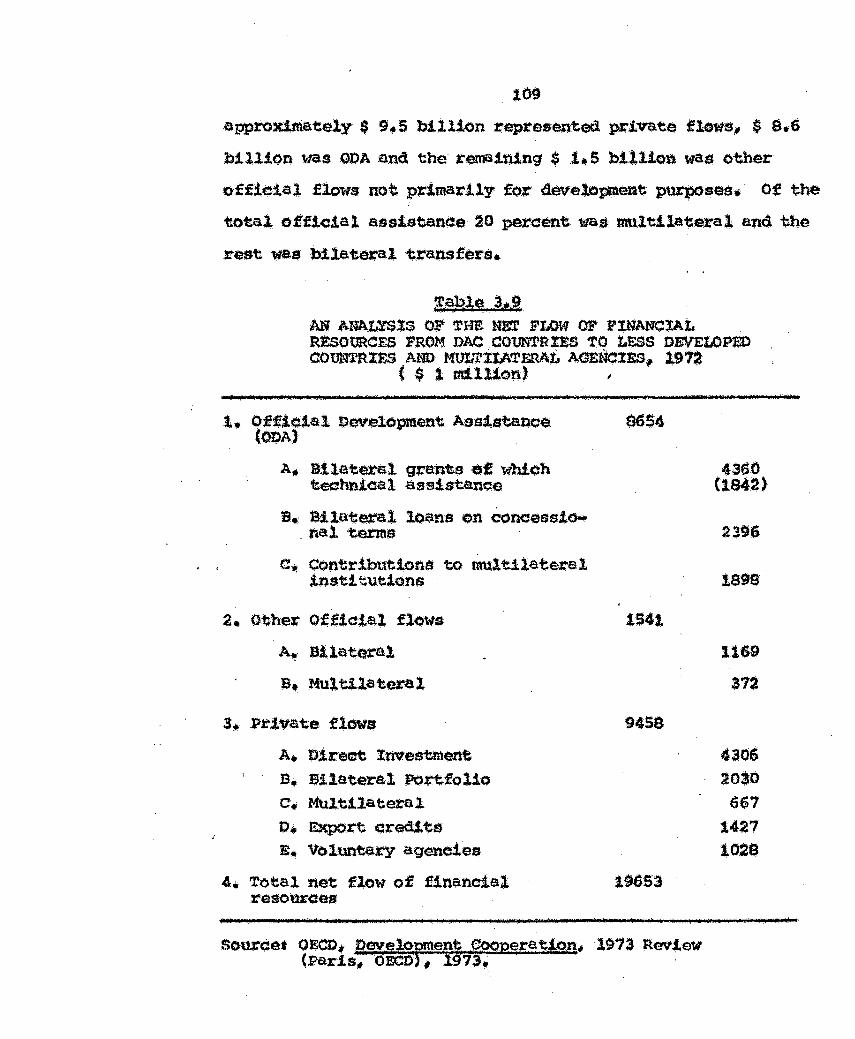

J!'CG$ ftom D~A•C• countries ~ the develOping Cduntrtes and

multilateral development agencies 11 S:hown in 'l'tiblo 3.9 .•

The total. of private flows, off;lc;.ta1 devetopmetli: a$s1st.e.nQe ·

and other official flows* n¢ .Qf emoJ."tigatton (but not of

interes~ &J1d prQfit.s)., is call~ the net flow of financial

)1!'esourc~. Of the $ 19'..iG billion total net· £lOY of f1nanoia1

reaourees from developed. to developi~g eountJ,".ies in 1972•

109

approldmately $ 9.5 billion represented private flows, $ e.G billion was ODA a.nd the remaining $ t., 5 billion was other

official flovs not primarilY for dev.elopMent purposes. Of the

tot.al oifl<U.al ass:tstanf::e 20 percent. was mul:t11ateral and the

rost was bilateral transfers.

~.able . 3.e! AN ANA%3SIS OF THE N&T FLOtf OF FINANCIAL RESOORCS:S FROM DAC .COUNTRlES TO t.tsS Ol\.1/ELOP.ED COt~N'11tXF.S ANt> Mut:r:ILATERAL AGENciES~ 197~

( $ 1 million) ,

A• Bilateral g1:ants e£ which teeind.cal assistanee

e. Bilateral loans ·on concessio. nal terms

c.., contribut1ona to multilat&ral .tnstitu~cns

2. Other Official flows

~· Bilateral

a. Mu1t11ateral.

a. Private flows

A., Direct:. Investment B. Bilateral POrtfolio c. Multilateral D. ~rt credits E• Voluntary agenoies

'• Total net flow of financial tesources

S654

9459

source• OECDt Develor;ent Cooperation,. 1913 Review (Paris, OEX:m 1 1973•

4360 (1842)

1S99

1169

372

4306 2030

6·67 1427 1028

110

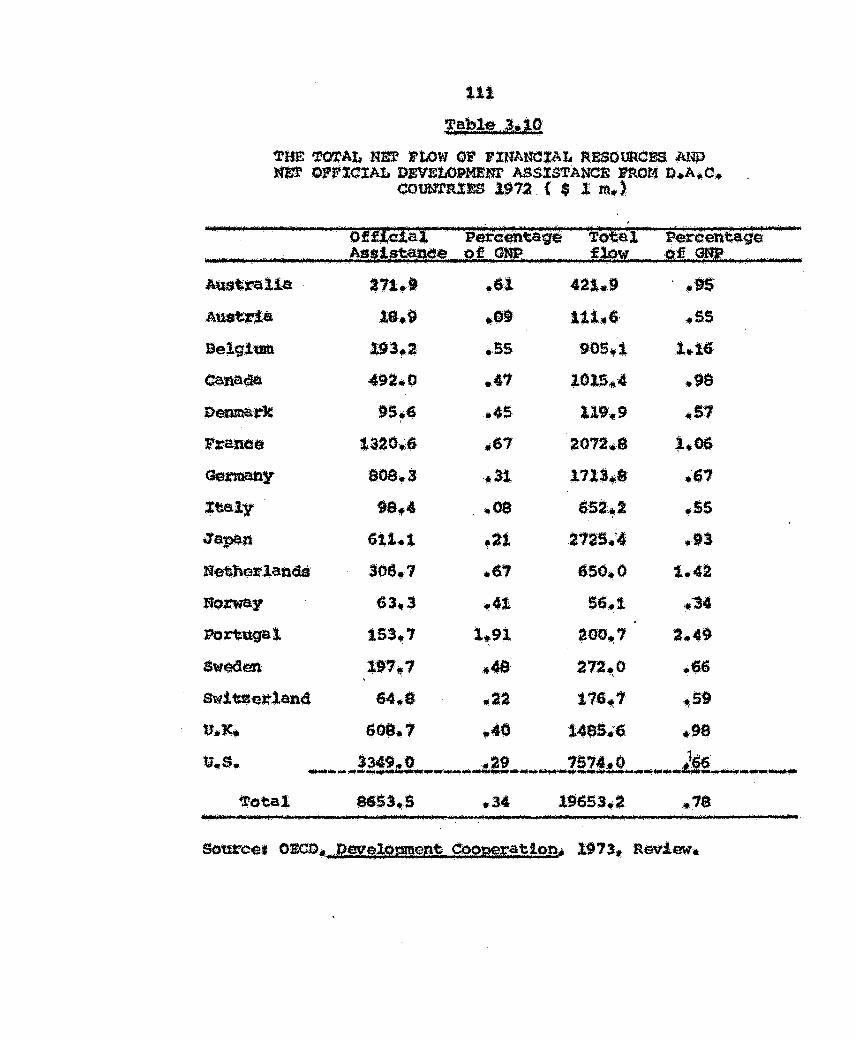

The aid targets set for the developed countries 0~

1 pereent of their national incomes re.fer to the tt)tal net

flow of financial r:esout"ces. · The t$rget: $:>r offi~ial de\felo~

ment assistance alone is 0,.7 percent of donor•s national

1naome. In if$b14 l.to it .is quite <:lsar that us acaountts

ns<.lr.1y ·Is of th$ total n~t; flow Qf financial resour~es, the

flow ft'om Japan is also high but p~:edom.tnantly private inVest ....

ment., The outflow from us l:'epr.esent o,.ue o£ its GlSIP.._ Ortly £oux aountl:ies of D,.A.c. t~c:hed th4 target of t percent tn

1g12, The av~aqe percentage of the total flOw to total

national inoomt:~s Of the D,.A.c. countries amounted t:o 0<~~'78 tn

1912. The us is also the major provoid.eJ: of otftetal developmetlt

assistanoe; followed by France, Japan,, U.K. Only France~ the

Nethe:-lands and Portugal~ how<Wer• provide official' development

assistance olose to or in ~xcess of the te.rg-et of 0~7 percent

of natt.ona:l lncomt)~: '!'he pereentage contribution of the t1S and

3apan are among the lowest of all count~,tes~

The major sourees of mult1lateral assis~OO$ ares. tbe

world· Bank and its tlfo affiliates., the International Developmen.t

Assoeiat.t.on and the Internetdonal J!inance Corporation' tm

Institution the European Development Pundt anc;i the nevelopment

Sanks for Latin America,. Asia, and Africa • Disbursements from

World Dank in fiscal year 1974 totall$d $ 1S33 m11Lf.on- end

from IDA .$ 711 million.;,_ The d1sbur.$ements by multilateral ag(:!neiec~~

to developing: countries consist not. only of the contribution

of developed eountr.f.es but also of funds $'ai$Gd on the capital

111

Tabl-e 3.10

'THE '.t'O'.t'AL NEr :&'LOW OF ttNANCXAL RESOURCES. 1\NP m:t OFFXCIAL PEVELOPME:tll' ASSlSTAt~E l1ROt4 +l•Ac;~C•

COUN'tRXl:S 1972 . ( $ 1 rn,. )

· r . · - 11··· 11.

Australia

Au$t:rta

Selg.tum

canada

Pe=ark

France

OeJ.'matly

:Italy .

.:tapan

Neth~:ttlandS

Noway

Portu.qa!.

sweaen

$w1~eJr.l&n4

21.1.,1

.19.9

193.2

492.0

95.6 i

1.120.6

aoe.s 99.4

611.1

30fJ.7

6.3.3

153.7

197··1 . '.!If

"·' 608.'7

.6,1

,09

•. ss .41

~45

.67

.31

.os

.21

.61

.4:t

1.91

.• 48

.22

,.40

.34

'{ •. c "i . To>al flow

'- [ i! -·

421.9

111 6 ... 905~1

1015~4

119-f9

2072,.8

1713,:8

652.2

2725 '4 ' ' ·: ... · :

650.0

56 .• 1

200~7

2'12ct.o

i7G •. 7

14S5i6

Percentage ' £ l"n.'ft'l ·a- ·~- ::r+!£ -, -- - ·1···· }~ •

• 95

~ss

1.16

.98

~s1

~.06

.. ,,

.93

1.42

,.'34

2 .. 4t

•'66

~59

.ta

1.12 trtark$ts a.r.<t J:$p&y.rnt3n.ts of previous l.Oans~54 1'ha Wbrl4 Dank

is eesent!e.lly a QOmmercial institution anci raises large

sum.s of mon~Y on the world• s <:apital m~.n:kets.- 1.'he :r,.o.A.

!s the soft loan affiliation of the \-toJtl<.i bal'lk whi~h dispenses

loans att low intet-est :t:.ates with long repayment periods.

'rbe x.F.c.,, the other main atfiliat~ of the world .Bank_,

concentrat$S an encouraotng .p;rtvate ent~rp,rise in c;twe1oping

~oun~t"ies by mald.ng ~ty inve:Stment$~t ·Wh!le $ 20000 m!lllon

1$ 'QndQtlbtetUy a s:ubatan:tisl sum absolutely, lt is 'tirl'ivtal

d0mpare4 to ·the development ner!ds o:f the countries to whtch

ttt flew$ and l.ook$ _.,en more de~so~ when divideca ey· the

population of the 4fNelopS.ng eo~tr1es.55 In 1972 the average

net: ·flow o:e total asetst.enQe per head of population of develop.

int countries was approXimately $ g.·e per annun.

The .s,lgnt.£J.c:tSJt't ~~ is that &Qm 1970 onwatds. t:h&,We

has peen & gradual shift: in the so~e~ of development. fbanoe,

from opA to aon-conoe$sJ.onal mar'ket of bot't'Cwings. $$ Por

!nst~nce~ b~ween 1970.11. and 1975..76 ilhel:'$ he$ been a thirtzeeu

fol4 . .t~reas~ tn the flow-, of QQ!'l'lm&lZ'e!al ·bank loans to tDC:s

tthil' over ~he same, per!oet1 t.he reiative share of OVA ~ell

by 20 ~c~. on the whole. private flows (tnolttd!nq ~ft

credits b:om,the We$t:) haV4i! ac<:ounted for·near:ly n4nety ~Mt;

54 'l'hirlwal,, n.12~ PP• :U.2•14. 55 ~.!d.~ pp~312-..t4.

56. pF ,sME:tez.# l!lf, June 19?7• PP•;l6S.1o.

113

of international capital flows to developing ¢0unt:ries

between 1970..75.57

'!'able 3~11 shows tha progres~iJ.ve increase in the

relative sher:e of pr!v.ate commi:t:ment;s (exclUding supplier

oredits) from 21 perdent .of the total in 1970 to 41 percent

in 1915 and during 1972-.75 funds committed were doubled.

1'a~l!! ,3•·11

LOAN CoMMITMEN'fS TO 84 :DEVELOPING COUNTRZE$

' ' p • ' ~ ' ~ n ;~ • • '(M£eeut,asm! ' ' ' ~ ' ~ ~ '

.Ss;t!¥'Qe, . , 1~?0 ,1211 ,19,7;2, ,19'73 J974 ... 1~7!3

%nterna.Uonal Orga.n.taatton a,s 3,1 3.7 6.1 4.9 7,8

r

GOvernment loans 4.9 3.2 '

1.3 8.'6 11,7 .1o,e

Supplier credits 2.9 2.,3 2 •. 1 21!3 s.n thO

Ftna·ncial markets 2"'8 ..... 5.7 10.6 14.2 16 .• 4

T-atal

P4l anal.ysj.s of emot.mts Outstanding U .• e. $tOek$-

as OppOsed to flows and crOtl'lni t.tnents) is equally ~svaal!ng

'rbese data are shown .in. Table 3.12. As these amounts &r$

cumulative,, t.he sh1ft: in the relative irrtportance of private

j I :~ .. s,gur· G ' ·C

Off.leial

Pr.tvate

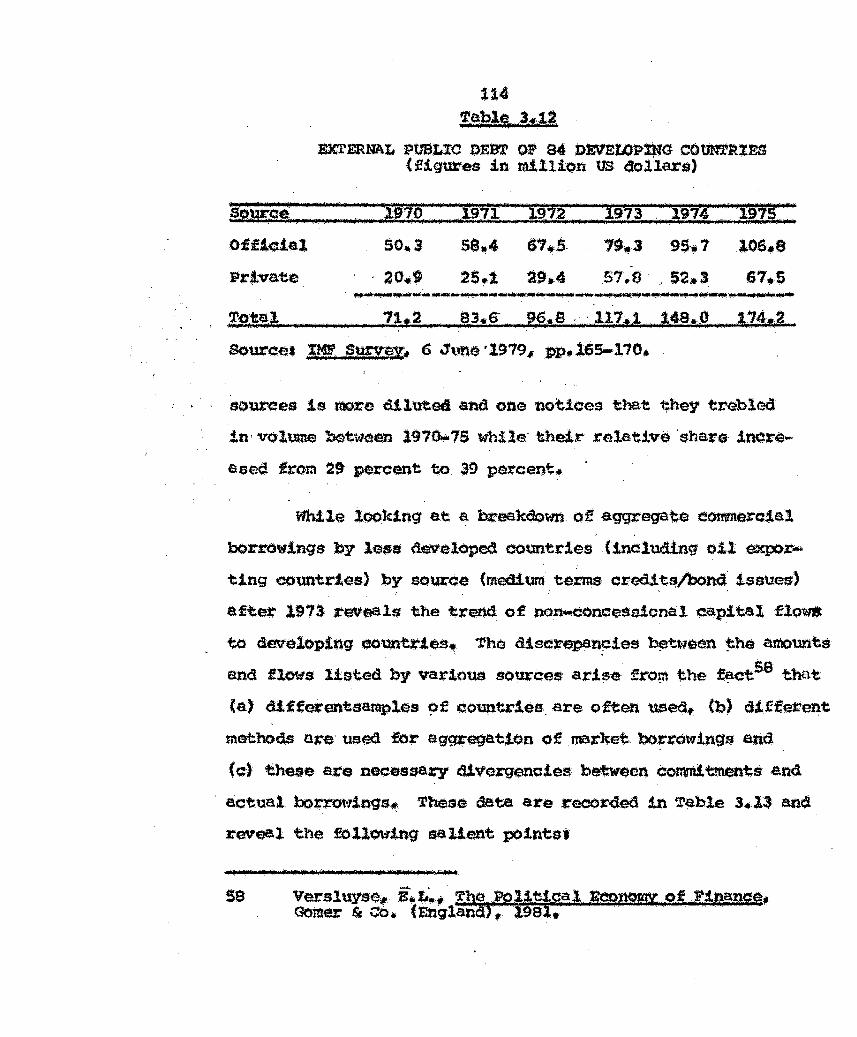

114 'l',a~lg, 34 .1i

EXI'ERNAL PUBLIC J)13:BT OF 84 l>EV'ELOPlNG COtiN".rR!ES ( figtU:•s tn million us doa.'lars)

i

. : .'197,0 ... l97J. 1272 '!9'73 •• '. . Ill i . 1'§;! .. '·• 1974 • r . 11 iMI • p- "J I .. ""•"tl_p_......,

so.s, 58.4 ''~!;. 79~3 9$~1 106.8

' 20 .• 9 25.1 29.4 57.8 52.3 67:.5 "

. 1 . 11.2 sJfs-- 7 . _ 1 ·- ' M ll"h I

so~es ie more diluted and ·one notices that they trebled.

in· volume betw<!en 1970.75 whilEr 1their relative shar,e incre

esea from 29 percant to 39 percent~

While looking at a brea.l«lown of aqgrsqate eommaJ:c:ial

bOr!:'Owings by less develQped countries (including oil expor•

ting oountries) by so~e (medium terms cred! ~/bond. issues) '

after 1973 .reveals the trend of non-concessional <:il.pital flows

td dE!V'e1op1ttq co'Untties,. Tho &scr.epe.n~!es b~tl<~~en ~he amounts

and flows Ust.ed by various sources ari.t:h! from the ~et56 t~'lt

(a) d.tffQX"entsamples ~f eountries. are often used, (b) different

methods are· used for ag~egat!on of market. bol:'rowings and

(c) these are nee.,ssary diverge.ncies be'tween eontnl~s and

· actual borrotdngs~, These data are recorded in T~ble J.l~ and

rev~l the follwtng salient pointer

59

115

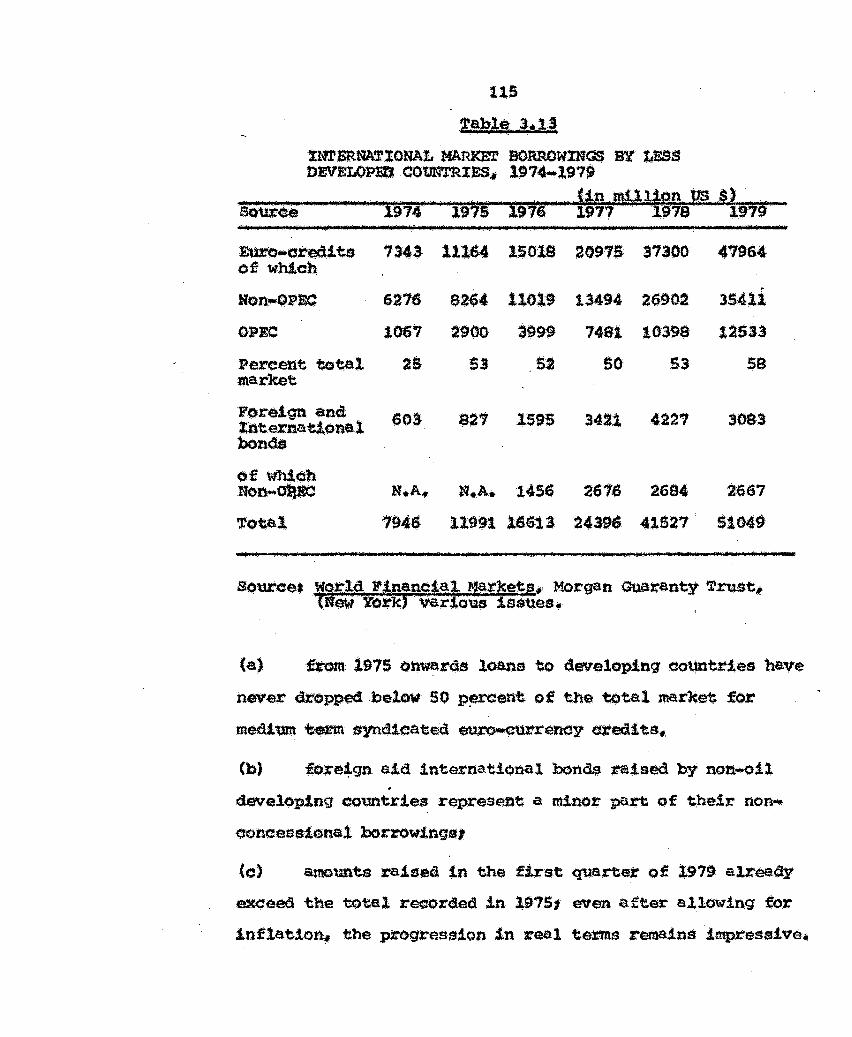

Tab&$ 31 1;-3

tNTSRNATlONAL MAR!OlT BORROWXNGS BY LESS DEVELOPl!U CO'fJ'NTRXES., 1974-197~

soui~-· '''1974"" I 1975 I976 ... l ~~Q,5'*!S7eys 1lt79

~are4its 734~ 111t$4 1$018 20975 37300 47964 of whtch . .Non-OPEC 6276 6264 11019 13494 26902 35411

OPEC 1067 :2900 3999 7481 10399 125i3

Percent total 2~ 53 52 so S3 sa market

Fore19t't and 603 $21 1595 3421 4227 3083 l:bternatione.l bond$

o:f wb!<::h Non-oP.J'd. N.A., N.A. '1456 2616 2694 i667

'ro~l 1946 11991 166'13 24.i9S 41527 51040

(a.) ·b'Qm 1975 onwards loans to developing countries have

never dropped below so p~raent of the total mar net for

mediunt +Iem syndicated euro-c:urrency ored:S. ta •.

(b) tore~gn aid inte;national bond$ :taised by non-oil . develop!nq countries represe-nt: a minor patt of their non-.

concesf!tona1 borrowingst

(c) amounts x-aised tn the first quarter of 1979 already

ex<:eed the total re¢rorded .t.n 197St even after allotd.ng for

inflation, the progression in real terms remaitu:J impressive.

.116

td) Fol.lowJ.ng tb~ sharp increase in market bortowings1

th& annual debt service payment of the S4 countri.es i:n

Table 3+14 inereasect from US $ 5.a billion 11'11970 to $ 14.3

billion in .1975 and this increase of 220 pere~nt eo!ne:idad

w.lth the very sharp deterioration of the borrowers export

perfQ~noe'o! fot the 96 dt.Wf!loptng c:ountri~s 1nelu<ied tn world I

Bank• s sample, the total projec:tecl debt sel!Vice to ~996• for:

the ~ernal debt outstand.inq at 31 Decembex' 1976# amounted

to us $ 213 billlon of this $ 15.4 billion ( 35%) was owed

to bt\nks.

(e) Tbe debt set:Vic:~ figures When taken in the form of

·d.ebt-serv!ee ratio (i., e., annual ·debt service paym~nts as a

· propc:u;t~on of foreign exchan.qe income over the same p~iod) .,

S.t is noUceable that these ;oatios in e3tQess. of 20 percent.

are f!atrly. comt!Dn plae~ among developing countr.!e$ as shown

in debt analysis above. Evidently these ratio'S db not reflect.

the impact of loans oontraQted in 19781 19·79• etc• A more

recent picture h$6 been presented ill Table 3.15. Thi.$ suggests

_that while the developing countr.tes medium and lohq term

debt increased by 20 pt'!X'cent a year in 1970s~ the, resources

needed tC) service the debt \Jter:e also growing rapidly· and

therefore, the debt service ration in 1990 was no hiqher as

compared to 197o,.Ji9 But after·l9SO the position ohsng:ea,.

although the rate of growt;h of debt valued to an estimate!d 1!

percent in l9S2. the slow down in ~rt ea:t-n!ng!l ·was sbQ:rper

.ua 1.eb1!i) 3• .. 11.

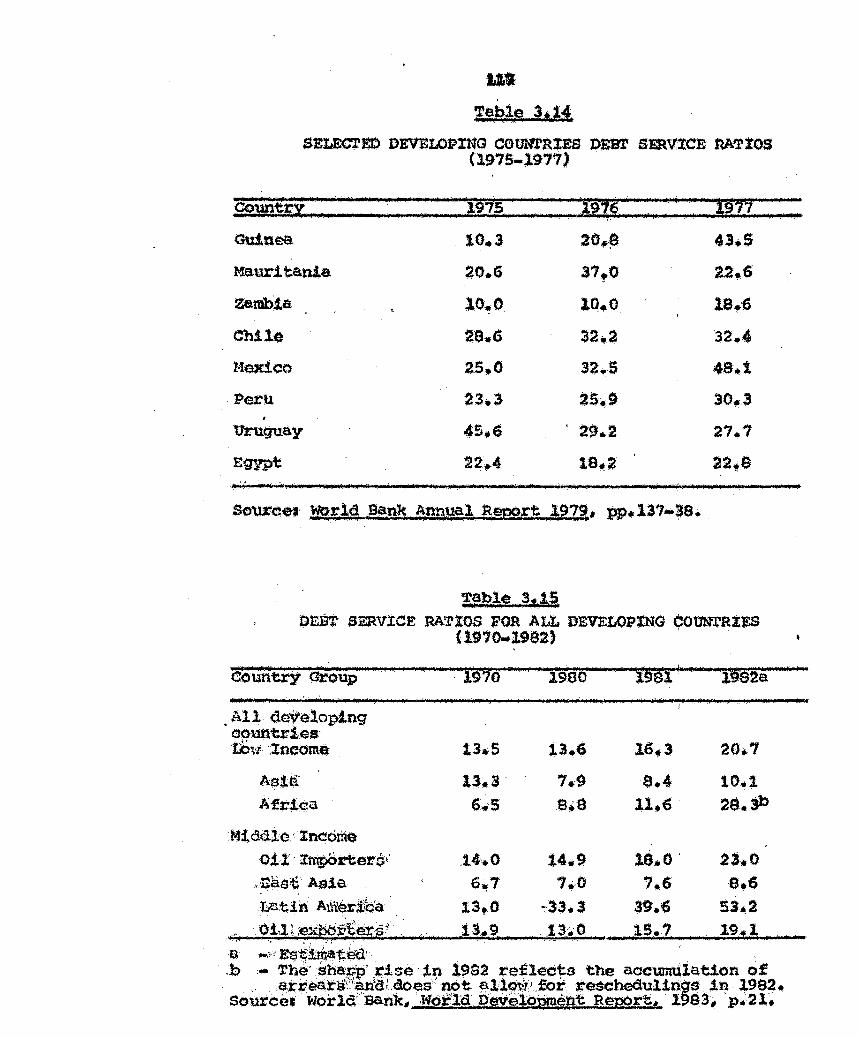

SELEC'.I'ED DEVI!;LOPING COUN:rRIES DEBT SERVICE RAT:tOS (1975-1977)

qom{{fi : :: : :< )27s.: :: : ''1276: :.:." • ::l9~i GUinea 10.3 20,~- 43,.5

Mauritania 20.6 31 0 ! 22 6 .... zamhta 1o.o 10~0 18.6

Chile 2S.G 32.2 '32 ·4 .. r.texic:o as.o 32.5 48.1

Peru 23.3 25.9 30,3 . Uruguay 45.6 . 29.2 27 1 • Egypt 22·4 • 19.2 22.a

~able.3f15. . -· -

l)EBT SERVXCE RATIOS FOR ALL DEVELOPING COUNTRXES (1970.1992) '

_··:~_-.,- '" p?

country CJroup

. All developing oo\'llltr.tes· tbt1· ·.Income

Ast4i\· AftiG;a

Midaie·:rneome Oi 1· Imp(:)rters:

.• J~~a.~ A$ie.

~.tin A1\1~ri\::a F • or,t; ~xpg~~tff · . . .

. i970

tJ •. s 13.3' 6.5

6~7

13t0 13.9 ..

l9"eo

13.6

7.9 a~ a

14.9 7~0

':'·33.3 . 13•0

DS% 1 n f • l'§saa

16,3 20~7

s.,4 10 .. 1 ll,.t) 2e.Jb

16.0 .23,0

.15.7. 19.1 a ~: ... Es~~at~a> .b ... The· sha;p· :~i:;~e it:t i9S2 reflecr;a the ao:c'UlnUiation .of

.· l?:X'.r'~lf:artCiidoes · not allcn1 ·.£or J:esehedulings in 1992. souree• · worla··aank, ·.wor'ld i>evalopn;tent Reyrt, l9s3, ·p.2l.

:::

119

and consequently the tate of debt to exports ros~ · from 16"

to 104 percent during 198M2 and wi ~h the inclusion o~ '

$h0rt-tem ~t this ratio EOC¢e~ 150 perc"nt. stnee a

large_ part of d6tleloping country debt is· denotnJ,nat:ed in

dol.lsre# the appr:ectation of dollar tn foreign exchange

msr'kets has added to their debt-.bur4en•60

' > •

:Dutting 1975-80 the medium and long tt'41!i debt of 4eve-

lopift9 economies. gt'ew by ~n artnu:al average of 2.1 percetit!•

· tt reached an estimated figute of $ 426 bil.lion in .1980, ·a

yE'Jar earliEtt J.t had been $ 7S b. 61 The Table 3,.15 shOt-rs ~·

~treordinary pace at t-.rhieh the total debt and the short . . •"

an.d medi\ln\ period debt has increased ove~t the decade 1971-so. · . ~ ,·

(1) There ba$ been enormous increase in the extemal debt.

of i:he deYt!lopinq count;"ios .in the l97l...SO decade and that

within th• total debt,., pubUc debt f.J:om private sow:'dtla ha$

grown disproponionately high .during this period. Thus- out

standing debt of third world countJ:"ies incteased from$ 18

billion (1911) to $ 426 billion in l9SO ~;tnd ~ut of this:# ' "

,

share of pr.tvat:e lenders was $ 269 (6)?4) as ~ed to $ as,, (46") tn 1911* PUblic ban!Owars tn • the developing cotU't'Ct'ies

LJl¢~;$8S<ld thelr debt to fi·ttanc.te.l markets at an average of

34 percent. a year durtnq .. 1971-eo,

60 ,J.bip,,.. p,.21.

61 ~os:;ld Devel9pment Repgr.e,, n,4o. p.21.,

!t9

(2) Mainly due to prJ.'V'Ste souree of financing~ the terms

on wbleh devE!!1op1ng countries borrowed hardened steadily

durinq the 1910s, share of offi~lal ~~nd!n9 deel!ned~ average

interest rates en cot'lt1'01tntent.s J:Ose, maturities and gr:aee

periodtJ shortced. Besides while in 1977# muoh of the

bor:toW!ng was on filled interest ratetJ but in 19tl0 1 t. was ' .

on variable ititerest rates ·and fw:thet' t:hat the interest -··- - - • - . - -- 1- -- •.•

payment rose sharply by an ·annual average of over· .40 percent

during 197S..SO, compcared to annual average rate of only 6%

during 197]...:77• The first oil crisis mark$d the begintd.ng

of the present debt problem and that o£ 1979 and 90 accentu

ated it further and bro\lght. it to a flash point artd the

.resuli! was that . the dtsbw:'sed and outstand!nq lobq and. meditun

t$:tms debt rose by 14 p~ent in l97l..SO. ay 19S2, the

interest. rates bad r:L.sen further and .fresh lending. which

further ·det~io~ated ~he eituat1on~6~

,Less DE:~Velo:gecll. count::r~es P,nd the XM;l? • 63

What emerges from the preceding analysis .ts that fot'eign

62 _ :S••• x. !;10nthiy Rem~~ pp.,230•J2.

63 Some of the important studies. on relationship bet:weat 1es& developed countries and the IMF are fOllowing& Bird, o •• "'!'he 1'nfcrmal Link between SDR AllOQation and Aid", A Note, '!'he. Jow;n~l of ~evel~t st;uales, .. no.,12 {J)" 1976• pp,268•73. Bird a., The ~~t@mat;I,oq£\1 .Mo;uaiiaa s:l!(tems and the Les:s Develo,2ed.cguntrles. Macmillan, ~Londo'ii). I978r' 'cliv·e,. w.R., xg~ernatigna,l,. ~netaEZ Rsfo,rm and the ,D,ev-alo-eing Countries, · Brooktrigs Xnstltute, hvasblngton o.c.,, 1976t Ghatak, s •• Pevelo2!!f.!nt J£eono;mi;es, Longman (London), _1978. Hellelnert G.t<:._. 'rhe Less Develop$d. Countries and the International MOnetary System•, T)le JottrnaJ.n .. of.: ~elOJ)1.l!!!n1;,,,Stud!f.ts, vo1.10(3), 1974, pp.l47-71.

: ::: : . ·: . ' :: . : : : '

Total Public & Pr.lvat.e

Official sources

120:

. DEDr OUl'STANDINQ~. COMM~S., DISSt:IRSEM.Em'S~: SERV:XCE PA'!ll-~NTS AND NET CAPITAL ltiOVEMEN'l'S OF DEVELOPING . COUN'l'Rl:F.S J t.fEDIUM AND

LOUG TERl"t. DEB!' 1977-80 ( In US 1Jollara 'billion) .

77: .. :9' 111'~1 174.~1. 212.0 ~ ~,;~

262~7 327.4 372.~& 426 .. 1

4a.o 55.7 75.2 M •• 104.,1 124.,0 1,37.1 1S6.7