turkish economy in 2010 and beyond murat ucer global source partners all information copyright of...

TRANSCRIPT

Turkish Economy in 2010 and Beyond

Murat UcerGlobal Source Partners

All information copyright of GlobalSource and/or Murat Ucer. All rights reserved. No reproduction by any form or by any means without the express consent of GlobalSource and Murat Ucer.

December 14, 2009

2

Outline

• Understanding the Past(or, why a lot of what I said last time did not happen …)

• Looking to the Future(or, why I will insist on saying them again!)

3

A year ago, the outlook was very gloomy…

• Globally, we were busy with 1930 comparisons; we had seen unprecedented collapses in global trade and output in Q4…

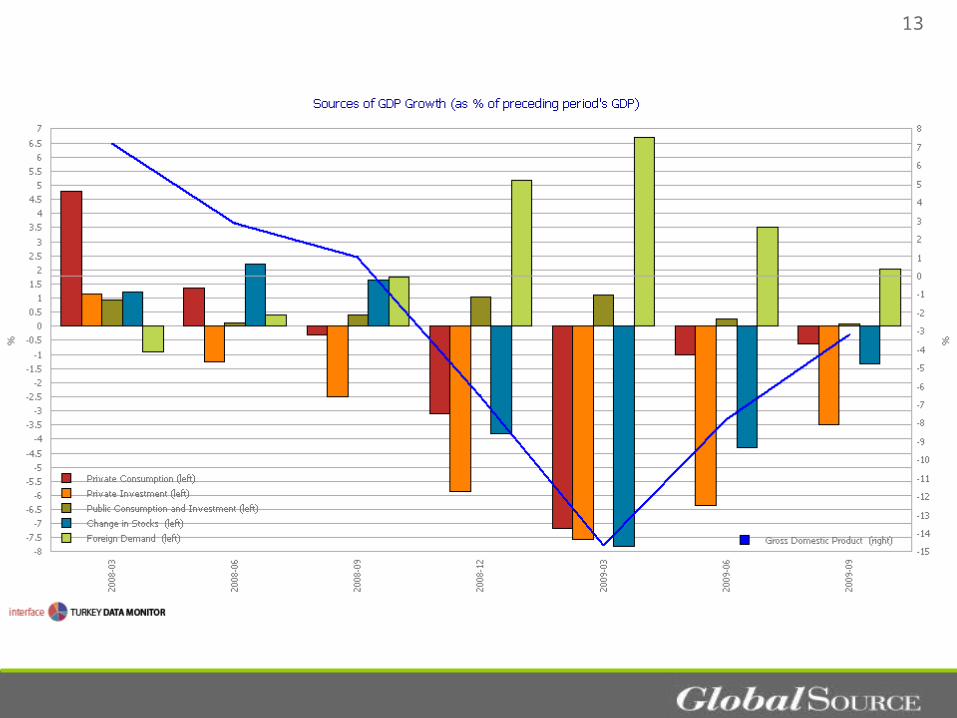

• Turkey was also sinking, and had a significant external financing gap on the order of $15-$30 billion…

• Fiscal situation was deteriorating very rapidly…

• We did not look too eager to sign up an IMF program…

• Without IMF, most forecasts speculated, lira/$ could hit 1.9, interest rates would stay elevated, etc…

• But now instead, the 1930s parallel is long forgotten; on the external financing side, things “added up somehow”; inflation has declined to 5%-5.5% range, and lira/$ is at 1.5/bonds at below 10%...

4

Why? What happened?

• First deflation fears (because of the deep recession that was coming) and then recovery hopes dominated the global markets. “Decoupling” (of emerging markets from advanced countries) came back with a vengeance…

• IMF championed fiscal stimulus globally, promoted new lending arrangements; G-20 raised hopes as a new cooperation platform

• With global economy in major recession, central banks continued to ease monetary policy, so did our MPC, taking the O/N rate to 6.5% presently, from 15% in early 2009

• Turkey received over $12 billion (cumulative) in “unidentified inflows” during Q408-Q109

• True, Turkish growth collapsed because of domestic demand contraction and inventory drawdown, and we shall experience one of the highest contractions in the world this year…

• Yet, Turkey reacted to the crisis as a relatively “mature” economy overall, largely because the crisis did not originate from here and the financial sector did not blow up

5

6

7

8

9

10

11

12

13

14

Where do we go from here?

• Globally, we are hardly out of the woods. As the recent corporate/sovereign troubles remind us, the road ahead may be rocky. The world economy needs “rebalancing” at two levels, domestic and international, but it is not so clear whether this can happen smoothly.

• “G” will have to be replaced by “C” as we “exit” expansionary policies, but the U.S. consumer will likely remain weak

• China, on the other hand, has to be a great contributor to this “rebalancing” act, but it doesn’t look willing to let the currency appreciate, nor is the sustainability of the recovery there, is a forgone conclusion.

• Domestically, our fiscal and external financing situations (“twin gaps”) both look challenging.

• The Treasury will work with some 100% domestic debt rollover this year, and because of a relatively tight external financing situation, monetary growth will be limited.

• This makes crowding out (of the private sector) a very likely outcome, and robust growth its main casualty -- 3%-3.5% growth is possible next year, but that should be considered a “bounce-back”, not solid, sustainable recovery.

15

Nispetiye Cad. Tepecik Yolu No:1/18 Etiler / İstanbul - + 90 212 352 12 70