ubs swiss small & mid cap summit th august 2009 … · panalpina –a leading asset-light...

TRANSCRIPT

Panalpina – a leading asset-light forwarding and logistics provider

Zurich, 27th August 2009UBS Swiss Small & Mid Cap Summit

UBS Swiss Small & Mid Cap Summit

27th August 2009 2

Comprehensive global network

� Worldwide no. 3 in Air freight, no. 4 in Ocean freight

� Among top 15 in Supply Chain Management

� 500 own offices in over 80 countries

� > 13’000 employees

Financial highlights (2008)

� Net forwarding revenue: CHF 8.9 billion (€ 5.6 billion)

� Gross profit: CHF 1.7 billion (€ 1.1 billion)

� EBITDA: CHF 241 million (€ 152 million)

� Net earnings: CHF 114 million (€ 72 million)

Panalpina at a glance

Air Freight

Three business segments

Six industry verticals

AutomotiveHealthcare &

ChemicalsRetail & Fashion Hi-Tech Telecom Oil & Gas

Ocean Freight Supply Chain Management

UBS Swiss Small & Mid Cap Summit

27th August 2009 3

Air freight Ocean freight Non-containerized*

1.35 million tons (2008)

*non-containerized break bulk cargo from Oil & Gas and Special Project forwarding

791 000

2005

1 233 000

2007

923 000

2005

947 000

2007

901 000 tons (2008)

874 000

2006

1 278 000 TEU (2008)

1 084 000

2006

901 000

2008

1 278 000

2008 20082007

1.20

1.35

20062005

0.70

0.95

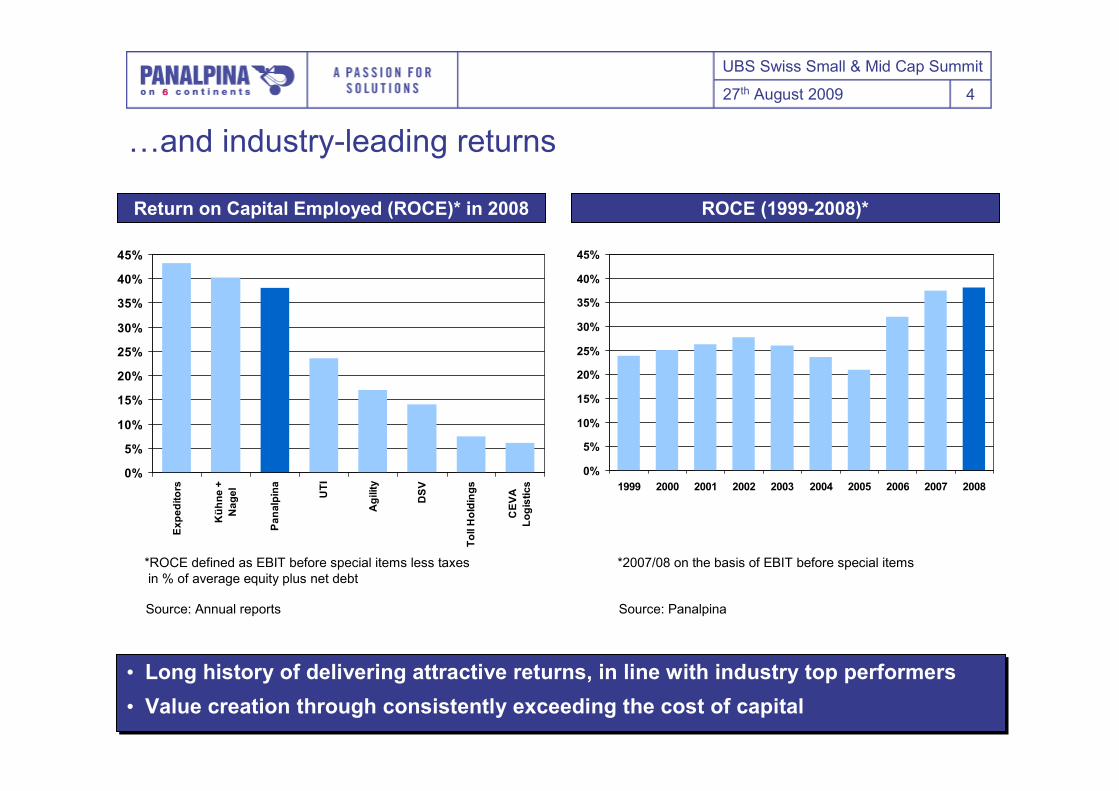

Many years with above-market growth…

UBS Swiss Small & Mid Cap Summit

27th August 2009 4

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

ROCE (1999-2008)*

Source: Panalpina

• Long history of delivering attractive returns, in line with industry top performers

• Value creation through consistently exceeding the cost of capital

• Long history of delivering attractive returns, in line with industry top performers

• Value creation through consistently exceeding the cost of capital

…and industry-leading returns

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Expeditors

Kühne +

Nagel

Panalpina

UTI

Agility

DSV

Toll Holdings

CEVA

Logistics

Return on Capital Employed (ROCE)* in 2008

Source: Annual reports

*ROCE defined as EBIT before special items less taxesin % of average equity plus net debt

*2007/08 on the basis of EBIT before special items

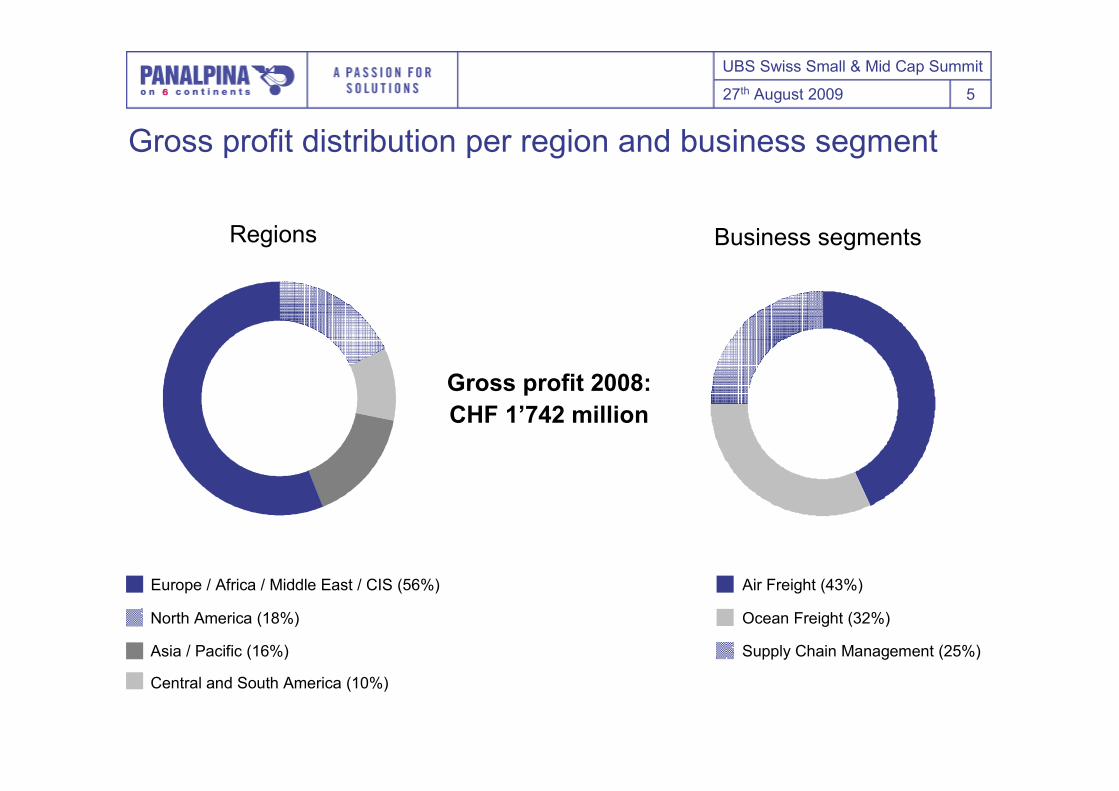

UBS Swiss Small & Mid Cap Summit

27th August 2009 5

Regions

Central and South America (10%)

Asia / Pacific (16%)

Europe / Africa / Middle East / CIS (56%)

North America (18%)

Gross profit 2008:

CHF 1’742 million

Business segments

Supply Chain Management (25%)

Air Freight (43%)

Ocean Freight (32%)

Gross profit distribution per region and business segment

UBS Swiss Small & Mid Cap Summit

27th August 2009 6

Panalpina stands for global presence and complex supply chain solutions – with ambitions to grow further

DBSchenkerAGLT

CEVA

EXPD

UTIW

CHRW

KWE

TOLL

PWTN2015

KNINDHL GF

Global network

Complexity of service offering

Bubble size refers to turnover (in $bn) in 2008.

PWTN2008

DSV

UBS Swiss Small & Mid Cap Summit

27th August 2009 7

Source: IMF, World Bank, U.S. Census Bureau (August 2009)

Precedent years

• High GDP growth, driven by emerging markets

• Trade growing at a 1.5 multiple of GDP

• Sales growing faster than inventories

Present

• Trade forecasted to shrink much more than GDP in 2009

• Investments into emerging markets decreasing

• Inventories falling, but due to collapse of demand 50% of U.S. shippers do not expect restocking to occur before 2010.*

Future

• Is a major short-term boost from restocking activity on the horizon?

• Will we get back to the growth figures seen in recent years?

• Will trade still outpace GDP growth as a rule?

Currently, trade is being hit much harder than production…

World trade and GDP growth forecasts (%)

Forecast

Total U.S. business inventories/sales ratio

*Source: Wolfe Research Shipper Survey, August 2009

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009E

2010E

YoY change in %

Global real GDP growth World trade growth

UBS Swiss Small & Mid Cap Summit

27th August 2009 8

…as a result, 2009 volumes are tracking far below 2008…

Panalpina air freight volumes(absolute and % y/y)

Panalpina ocean freight volumes(absolute and % y/y)

• Volumes double-digit below prior year in all months for both air and ocean

• Visibility of business environment remains low, although there are recent signs of improvement.

• Volumes double-digit below prior year in all months for both air and ocean

• Visibility of business environment remains low, although there are recent signs of improvement.

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Tons 2009 y/y in %

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

TEUs 2009 y/y in %

UBS Swiss Small & Mid Cap Summit

27th August 2009 9

…partially compensated by GP margins at record levels…

10%

15%

20%

25%

30%

35%

40%

45%

Q1 2007 Q2 2007 Q3 2007 Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Air Ocean SCM

Gross profit margins business segments

GP margins have reached historically high levels as a result of:

•Declining freight rates to record low levels

•Falling oil prices, resulting in lower fuel surcharges

•Focus on profitable business, resulting in high GP per cargo unit

GP margins have reached historically high levels as a result of:

•Declining freight rates to record low levels

•Falling oil prices, resulting in lower fuel surcharges

•Focus on profitable business, resulting in high GP per cargo unit

UBS Swiss Small & Mid Cap Summit

27th August 2009 10

…and productivity improvements through FTE reduction

Development of FTE’s and FTE productivity (shipments handled per FTE)

• Productivity declined sharply as a result of strongly falling volumes towards year-end 2008

• FTE reduction initiated in March 2009 helped to improve productivity

• Positive recent trend reinforced through customers’ tendency to opt for smaller shipment sizes

• Productivity declined sharply as a result of strongly falling volumes towards year-end 2008

• FTE reduction initiated in March 2009 helped to improve productivity

• Positive recent trend reinforced through customers’ tendency to opt for smaller shipment sizes

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

FTE SHI/FTE

UBS Swiss Small & Mid Cap Summit

27th August 2009 11

The fundamental growth drivers are intact…

• Shippers will continue to expand their reliance on

leading logistics partners as SCM complexity and cost

pressure continue to challenge int’l freight movements.

• Further consolidation of the market is likely, given the

high fragmentation, financial constraints of smaller

competitors and the importance of economies of scale.

• Forwarding and logistics companies continue to grow

their share of the market pie as asset owners

concentrate on their core competences.

• Economic growth will come back at some point and –

coupled with the ongoing globalization process – will

spur international trade.

UBS Swiss Small & Mid Cap Summit

27th August 2009 12

…however a U-shaped scenario is assessed by Panalpina to be the most probable one

• Optimistic scenario• Economy close to hit bottom• Fiscal stimulus leading to rebound already before 2010• Quick recovery, similar speed as decline

• Base scenario: long U-shape• Bottom to be reached towards year end• Recession lasting well into 2010• Gradual recovery of markets and turnaround during 2nd

half of 2010 with reviving trade flows and globalization

• Air volumes back at 07 levels in 2013 and ocean in 2012

• Worst case: L-shaped, similar to “lost decade” in Japan• Still long way until bottom is reached• Depression to last 3-5 years or longer• Downward spiral resulting from mass layoffs, collapse of consumer spending, protectionism and reversed globalization

2010

today

UBS Swiss Small & Mid Cap Summit

27th August 2009 13

Sales and earnings growth peer group Profit margins (conversion ratio) peer group

Median for Panalpina, Kühne & Nagel, Expeditors, UTiWorldwide, CH Robinson, DSV

Median for Panalpina, Kühne & Nagel, Expeditors, UTiWorldwide, CH Robinson, DSV

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009E 2010E

YoY change

Net forwarding revenue Gross profit EBITDA

?-5%

0%

5%

10%

15%

20%

25%

30%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009E 2010E

Conversion ratio in %

EBITDA/GP margin EBIT/GP margin

?

Forwarding proved to be resilient to margin pressure during past down cycles

UBS Swiss Small & Mid Cap Summit

27th August 2009 14

The company is well positioned to weather the storm…

Panalpina is well positioned:

• People business: motivated staff, ‘can do’ attitude

• Global network

• Diversified across industries and trade lanes

• Asset-light (most asset-light of any publicly listed logistics companies)

• Strong balance sheet

Key success factors in freight forwarding:

• Be globally present

• Be responsive to customer needs

• Deliver constantly high quality

• Be able to provide complex logistics solutions beyond transportation

• Manage subcontractors

• Continued focus on expense control

• Be able to work in a network and exploit synergies

• Have an impeccable image and compliant underlying procedures

• Be innovative

• Have sufficient financial strength

• Have an integrated IT

UBS Swiss Small & Mid Cap Summit

27th August 2009 15

…and is on track to achieve its short- and mid-term targets

2009 financial targets

� Downsize global FTEs by ~1‘500 (10% of workforce)

� Reduce operating expenses by CHF 130 million (seebelow for details)

� Adapt cost structure in line with volume development

� Preserve cash (tight NWC management, low capex, travel ban, no share buybacks)

Status quo

� Number of FTE‘s reduced by >1‘700 as per 30 June

� Full financial benefits (‚run rate‘) from personnel costsavings will be visible in second half of 2009

� Contingency plans in place in case that volumedevelopment in second half-year deviates materiallyfrom internal assumptions

40 Net organic savings

50 Organic savings (resulting from FTE reduction and other implemented cost measures)

-10 Severance provisions (booked in 1Q09 due to FTE reduction)

48 One-time costs incurred in 2008 (risk provisions, liquidation Nigerian subsidiary)

37 Reduced cost base as a result of discontinued business as of 1 Oct 2008

5 Reduction in anticipated legal fees in 2009 vs. 2008

130 Cost reduction target in 2009

Other targets

� Continue to gain market share

� Implementation of various long-term efficiencyimprovement initiatives

� Resolve pending investigations

Recap of 2009 cost reduction target (vs. 2008, figures in CHF million):

Status quo

� Large number of new business wins in recent weeks

� Automation and consolidation of variousadministrative processes in progress

� FCPA: completion of investigations in Q4 remainstarget; Anti-trust: likely to stretch into 2010

UBS Swiss Small & Mid Cap Summit

27th August 2009 16

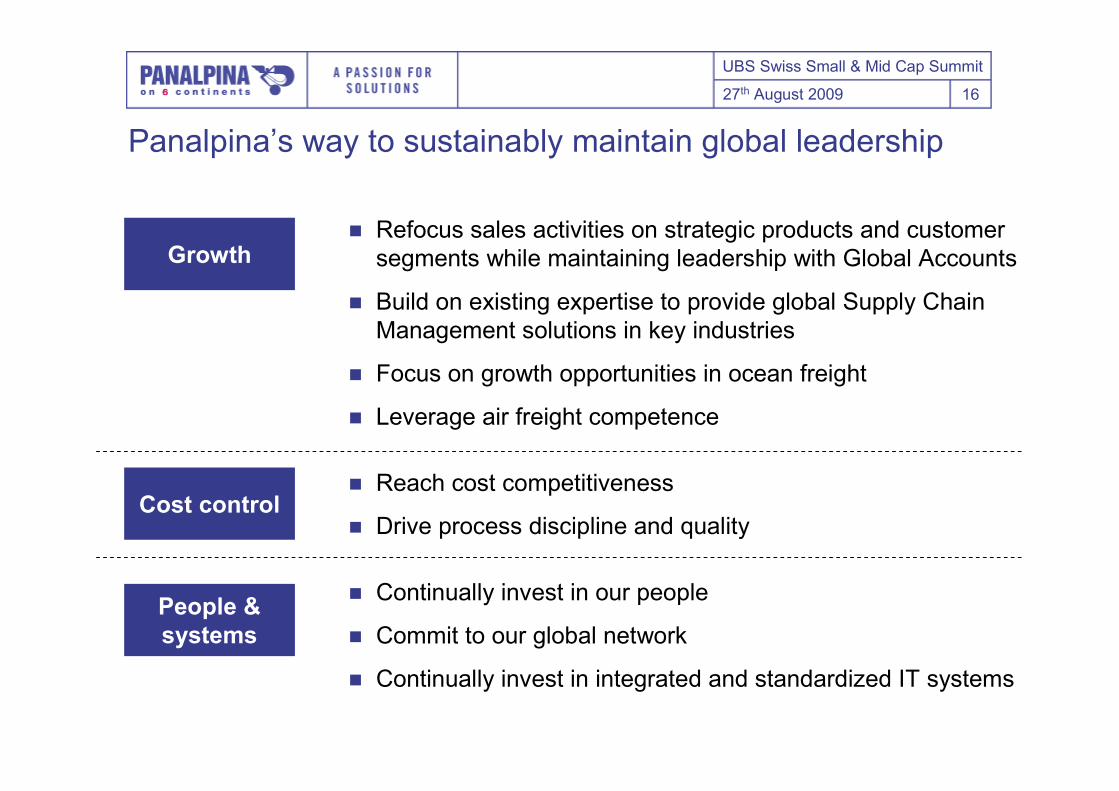

Panalpina’s way to sustainably maintain global leadership

� Refocus sales activities on strategic products and customer segments while maintaining leadership with Global Accounts

� Build on existing expertise to provide global Supply Chain Management solutions in key industries

� Focus on growth opportunities in ocean freight

� Leverage air freight competence

� Reach cost competitiveness

� Drive process discipline and quality

� Continually invest in our people

� Commit to our global network

� Continually invest in integrated and standardized IT systems

Growth

Cost control

People &

systems

UBS Swiss Small & Mid Cap Summit

27th August 2009 17

Market leadership in

freight forwarding

and supply chain

solutionsLimited cyclicality

and high returns on

capital due to asset-

light business model

Long-term industry

growth prospects

with goal to gain

market shareDifferentiation

through customer-

focused approach

and specialist

industry expertise

Strong net cash

position and

potential to improve

profitability

Leading global

network and

leverage through

size and scale of

operations

Recap of investment highlights

UBS Swiss Small & Mid Cap Summit

27th August 2009 18

Appendix

UBS Swiss Small & Mid Cap Summit

27th August 2009 19

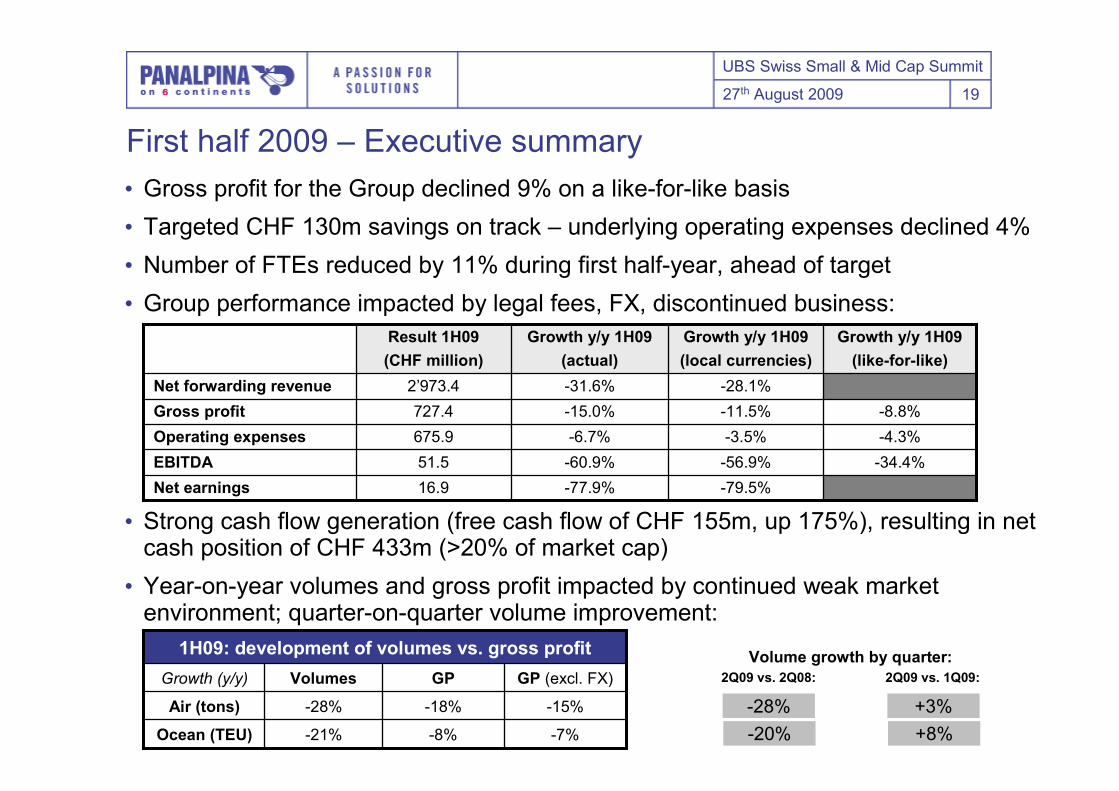

First half 2009 – Executive summary

-21%

-28%

Volumes

Ocean (TEU)

Air (tons)

Growth (y/y)

-7%-8%

-15%-18%

GP (excl. FX)GP

1H09: development of volumes vs. gross profit

• Gross profit for the Group declined 9% on a like-for-like basis

• Targeted CHF 130m savings on track – underlying operating expenses declined 4%

• Number of FTEs reduced by 11% during first half-year, ahead of target

• Group performance impacted by legal fees, FX, discontinued business:

• Strong cash flow generation (free cash flow of CHF 155m, up 175%), resulting in net cash position of CHF 433m (>20% of market cap)

• Year-on-year volumes and gross profit impacted by continued weak market environment; quarter-on-quarter volume improvement:

-4.3%-3.5%-6.7%675.9Operating expenses

16.9

51.5

727.4

2’973.4

Result 1H09

(CHF million)

-79.5%-77.9%Net earnings

-56.9%

-11.5%

-28.1%

Growth y/y 1H09

(local currencies)

-8.8%-15.0%Gross profit

-34.4%-60.9%EBITDA

-31.6%Net forwarding revenue

Growth y/y 1H09

(like-for-like)

Growth y/y 1H09

(actual)

+3%

+8%

Volume growth by quarter:

2Q09 vs. 2Q08: 2Q09 vs. 1Q09:

-28%

-20%

UBS Swiss Small & Mid Cap Summit

27th August 2009 20

1H08 1H09

Gross profit declined 9% on a like-for-like basis

831

30

757

727

856

-25

1H08 restated discontinued

business*

1H08 actual 1H09 actual FX effect 1Q09 adjusted

-9%

* Adjustment for discontinued business for which GP was still recorded during 2008 (refer to Appendix for details)

(Figures in CHF million)

-15%

Reported

growth:

Like-for-like

growth:

UBS Swiss Small & Mid Cap Summit

27th August 2009 21

Total expense overview reveals cost base on track to achieve targeted CHF 130m savings in 2009*

-11%-1’74015’27013’530FTE

% ∆∆31 Dec 0830 Jun 09

(CHF million)

•Reduction of more than 1’700 FTEs over the last six months, ahead of target

•Resulting cost savings started at the end of Q1 – major effect expected in second half-year

•Strict cost control to continue – cost structure / FTEs adapted in line with volume declines

•Reduction of more than 1’700 FTEs over the last six months, ahead of target

•Resulting cost savings started at the end of Q1 – major effect expected in second half-year

•Strict cost control to continue – cost structure / FTEs adapted in line with volume declines

359

381

396

361

315

351

333

301

365

342338

346

280

300

320

340

360

380

400

420

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09

Opex reported Opex adjusted

* based on originally guided CHF 40m legal fees

UBS Swiss Small & Mid Cap Summit

27th August 2009 22

Outlook for current business year – review of Guidance

StatusGuidance 2009 Assessment

•Reduction of 1’400 – 1’600 FTEs

•Substantially lower volumes with larger customers, especially in Automotive / Hi-Tech. Recent business wins should have positive impact in 2nd half-year.

•Reduce operating expenses by CHF 130m*

•Full financial benefits (‘run rate’) from personnel cost savings will be visible in second half of 2009

•Market share gains

•Ahead of target – continue to adapt cost structure in line with volume development.

•CHF 40m legal fees related to pending investigations

•Likely to exceed guided amount – fees can be influenced by the Group only to a limited extent

•Tax rate 26 – 27% •On track

YoY volume declines should lessen in H2, however no substantial short-term recovery expected:

•Strict cost control and tight cash management continue and remain a high priority

•Focus on growth opportunities and continually invest in people & systems

YoY volume declines should lessen in H2, however no substantial short-term recovery expected:

•Strict cost control and tight cash management continue and remain a high priority

•Focus on growth opportunities and continually invest in people & systems

* based on originally guided CHF 40m legal fees