udn vision studio_t_hu_presentation_2015 (final)

TRANSCRIPT

Bag of Tricks & Shots You Must Miss

Career of Investing & Investing in Your Career

Thomas Hu 胡一天

1

April 2015

Table of Contents

n Career of Investing & Investing in Your Career n How to Build Your Bag of Tricks

n How to Take the Shots You Must Miss

n Questions & Answers

n Appendix: Financial Technology for the Greater Good

2

Career of Investing & Investing in Your Career

“Income is a series of events.” The Theory of Interest ~ , Irvin Fisher

3

Speaker Profile

4 4

創勢模楷 – 創辦人簡歷

n 胡一天 Thomas Hu

Ø 中華開發資本國際(香港)副總裁暨亞太區高收益槓桿收購融資團隊共同創辦人

- 經手融資項目總額:逾四億美元

Ø 紐約Epoch Investment Partners副總裁暨亞太區股權投資分析師

- 經手投資項目總額:逾二億五千萬美元 - 投資經驗:電信、媒體,科技,互聯網,金融服務,

化工,航太,零售,能源,醫藥,旅遊,教育,民生消費品,大宗原物料,物流運輸,商用不動產,連鎖餐飲

Ø 紐約哥倫比亞大學金融工程碩士畢業 - 研究領域:計量交易策略,信貸衍生品,價值投資

Ø 紐約哥倫比亞大學電機工程博士肆業

Ø 台灣大學電機工程/財經法學双學士

Ø 專欄作家

Selected Investment/Deal Experiences:

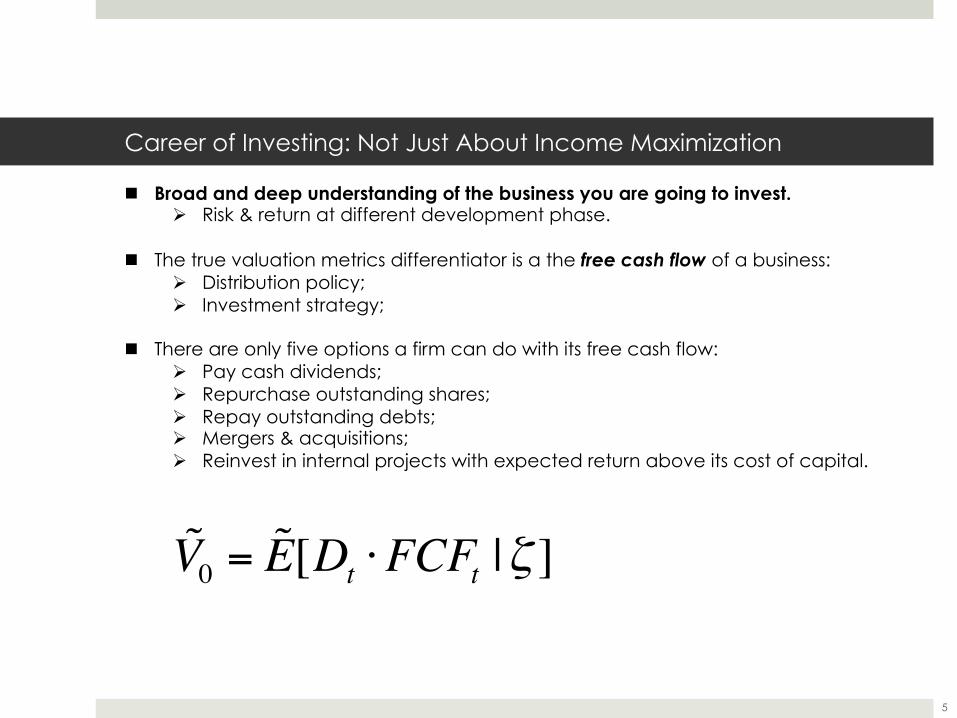

n Broad and deep understanding of the business you are going to invest. Ø Risk & return at different development phase.

n The true valuation metrics differentiator is a the free cash flow of a business: Ø Distribution policy; Ø Investment strategy;

n There are only five options a firm can do with its free cash flow: Ø Pay cash dividends; Ø Repurchase outstanding shares; Ø Repay outstanding debts; Ø Mergers & acquisitions; Ø Reinvest in internal projects with expected return above its cost of capital.

Career of Investing: Not Just About Income Maximization

5

V0 = E[Dt ⋅FCFt |ζ ]

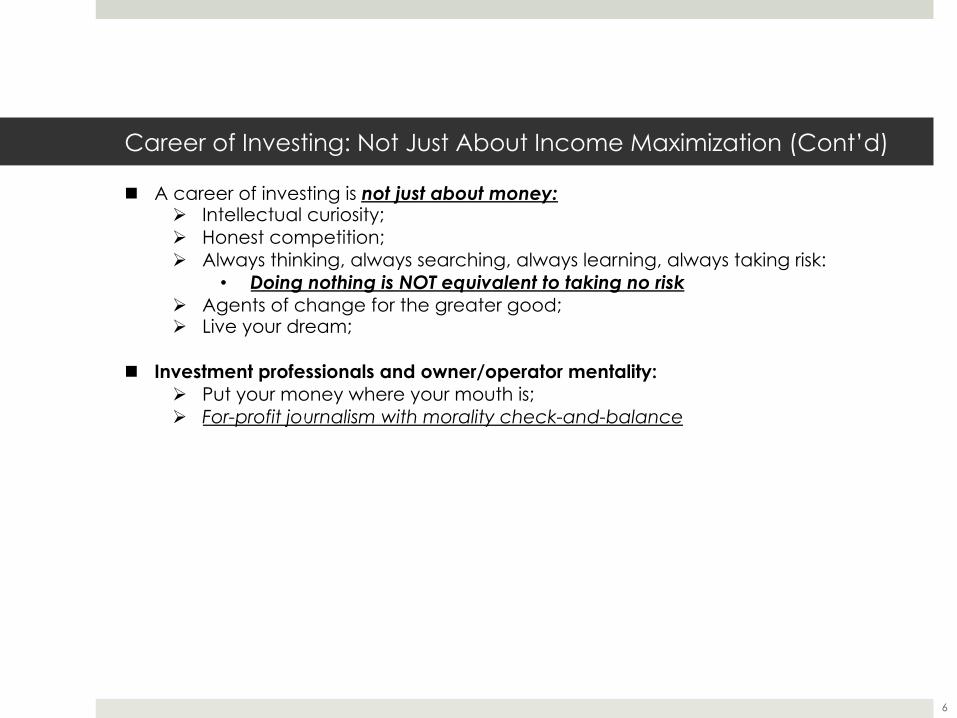

n A career of investing is not just about money: Ø Intellectual curiosity; Ø Honest competition; Ø Always thinking, always searching, always learning, always taking risk:

• Doing nothing is NOT equivalent to taking no risk Ø Agents of change for the greater good; Ø Live your dream;

n Investment professionals and owner/operator mentality: Ø Put your money where your mouth is; Ø For-profit journalism with morality check-and-balance

Career of Investing: Not Just About Income Maximization (Cont’d)

6

Investing in Your Career: Maximizing Exposure to Favorable Events

n Income is a series of events, so is your career. Ø It’s a dynamic, evolutionary process, with inherent uncertainty.

n Short-term Greed vs. Long-term Greed.

Ø Co-exist with volatility; entropy always increases in life.

n Proactive management of convexity and optionality.

7

Probability Distribution of x Probability Distribution of fHxL

There are infinite numbers of functions F depending on a unique variable X.

All utilities need to be embedded in F.

Limitations of knowledge. What is crucial, our limitations of knowledge apply to X not necessarily to F(X). We have no control over X, somecontrol over F(X). In some cases a very, very large control over F(X).This seems naive, but people do, as something is lost in the translation.

† The danger with the treatment of the Black Swan problem is as follows: people focus on X (“predicting X”). My point is that, although we do not understand X, we can deal with it by working on F which we can understand, while others work on predicting X which we can’t because small probabilities are incomputable, particularly in “fat tailed” domains. F(X) is how the end result affects you.

† The probability distribution of F(X) is markedly different from that of X, particularly when F(X) is nonlinear. We need a nonlinear transformation of the distribution of X to get F(X). We had to wait until 1964 to get a paper on “convex transformations of random variables”, Van Zwet (1964).

Bad news: F is almost always nonlinear, often “S curved”, that is convex-concave (for an increasing function).

The central point about what to understand: When F(X) is convex, say as in trial and error, or with an option, we do not need to understand Xas much as our exposure to H. Simply the statistical properties of X are swamped by those of H. That's the point of Antifragility in whichexposure is more important than the naive notion of "knowledge", that is, understanding X.Fragility and Antifragility:

† When F(X) is concave (fragile), errors about X can translate into extreme negative values for F. When F(X) is convex, one is immune from negative variations.

† The more nonlinear F the less the probabilities of X matter in the probability distribution of the final package F.† Most people confuse the probabilites of X with those of F. I am serious: the entire literature reposes largely on this mistake.

So, for now ignore discussions of X that do not have F. And, for Baal’s sake, focus on F, not X.

10.2. Transformations of Probability DistributionsSay x follows a distribution p(x) and z= f(x) follows a distribution g(z). Assume g(z) continuous, increasing, and differentiable for now.

The density p at point r is defined by use of the integral

DHrL ª ‡-¶

rp HxL „ x

hence

‡-¶

rpHxL „ x = ‡

-¶

f HrLgHzL „ z

In differential form

gHzL „ z = pHxL „ x

since x = f H-1LHzL, we get

gHzL „ z = pI f H-1LHzLM „ f H-1LHzL

Now, the derivative of an inverse function f H-1LHzL = 1f £I f -1HzLM

, which obtains the useful transformation heuristic:

72 | Risk and (Anti)fragility - N N Taleb

Probability Distribution of x Probability Distribution of fHxL

There are infinite numbers of functions F depending on a unique variable X.

All utilities need to be embedded in F.

Limitations of knowledge. What is crucial, our limitations of knowledge apply to X not necessarily to F(X). We have no control over X, somecontrol over F(X). In some cases a very, very large control over F(X).This seems naive, but people do, as something is lost in the translation.

† The danger with the treatment of the Black Swan problem is as follows: people focus on X (“predicting X”). My point is that, although we do not understand X, we can deal with it by working on F which we can understand, while others work on predicting X which we can’t because small probabilities are incomputable, particularly in “fat tailed” domains. F(X) is how the end result affects you.

† The probability distribution of F(X) is markedly different from that of X, particularly when F(X) is nonlinear. We need a nonlinear transformation of the distribution of X to get F(X). We had to wait until 1964 to get a paper on “convex transformations of random variables”, Van Zwet (1964).

Bad news: F is almost always nonlinear, often “S curved”, that is convex-concave (for an increasing function).

The central point about what to understand: When F(X) is convex, say as in trial and error, or with an option, we do not need to understand Xas much as our exposure to H. Simply the statistical properties of X are swamped by those of H. That's the point of Antifragility in whichexposure is more important than the naive notion of "knowledge", that is, understanding X.Fragility and Antifragility:

† When F(X) is concave (fragile), errors about X can translate into extreme negative values for F. When F(X) is convex, one is immune from negative variations.

† The more nonlinear F the less the probabilities of X matter in the probability distribution of the final package F.† Most people confuse the probabilites of X with those of F. I am serious: the entire literature reposes largely on this mistake.

So, for now ignore discussions of X that do not have F. And, for Baal’s sake, focus on F, not X.

10.2. Transformations of Probability DistributionsSay x follows a distribution p(x) and z= f(x) follows a distribution g(z). Assume g(z) continuous, increasing, and differentiable for now.

The density p at point r is defined by use of the integral

DHrL ª ‡-¶

rp HxL „ x

hence

‡-¶

rpHxL „ x = ‡

-¶

f HrLgHzL „ z

In differential form

gHzL „ z = pHxL „ x

since x = f H-1LHzL, we get

gHzL „ z = pI f H-1LHzLM „ f H-1LHzL

Now, the derivative of an inverse function f H-1LHzL = 1f £I f -1HzLM

, which obtains the useful transformation heuristic:

72 | Risk and (Anti)fragility - N N Taleb

Jensen’s Inequality: φ(E[X]) <= E[φ(X)]

How To Build Your Bag of Tricks

“I am a traveler of both time and space, to be where I have been.” Kashmir, Physical Graffiti ~ Led Zeppelin

8

Important Tricks You Should Have in Your Bag

n See the big picture & let your imagination run; n Identify pattern anomaly & act timely;

n Select industry wisely & refine your taste;

n Pay attention to deal structure;

n Have a sense of history;

9

See the Big Picture & Let Your Imagination Run

10

Source: 風傳媒

n Thesis: Form a world view from a higher vintage point and dare to think.

n When sovereign breakdown is topic for coffee break, nothing is impossible. Ø Extreme actions beget extreme reactions.

n No one can predict the future, but anyone who dares to think can prepare for the unknowns. Ø Financial markets are anticipatory.

Identify Pattern Anomaly & Act Timely

11

Source: 風傳媒

n Thesis: How can there a $100 dollar bill laying on the Fifth Avenue in New York for over 5 minutes?

n Every narrative must be dictated by logic and verified by observable facts. Ø If some action should have happened but it didn’t, either:

v The logic is wrong; v No one is paying enough attention; v No one believes in the story; v Someone is messing with the market; v Arbitrage!

n Timing is absolutely critical to every sound investment decision. Ø Better be approximately right vs. precisely wrong.

Select Industry Wisely & Refine Your Taste

12

Source: 風傳媒

n Thesis: Wrong people in the right industry might be a wrong bet.

n An industry is an ecosystem with many organisms that thrive in cycles. Ø Right industry vs. wrong cycle; Ø Right cycle vs. wrong people; Ø Right people vs. wrong industry;

n Financial promoters always have ulterior motives. Ø Did they put their money where their mouths are? Ø Are they making the right choice? Ø Is their choice suitable to your taste?

Pay Attention to Deal Structure

13

Source: 風傳媒

n Thesis: Getting properly compensated for the risk you take.

n Investment structures (“deals”) are designed to: Ø provide incentives; Ø encourage cooperation; Ø resolve difference in opinions about a business;

• Applicable to almost every aspect of life.

n Bargain Hunting vs. Growth at a Fabulous Price? Ø A good deal never lasts forever.

Have A Sense of History

14

n Thesis: Humanity evolves much slower than we think.

n Complex systems tend to make the same mistake over and over again. Ø Greed and fear are biological phenomena; Ø Cross-cultural understanding are critical for seizing opportunities;

“Hegel remarks somewhere that all great world-historic facts and personages appear, so to speak, twice. He forgot to add: the first time as tragedy, the second time as farce.”

~ The Eighteenth Brumaire of Louis Bonaparte, Karl Max (1852)

Source: 風傳媒

How to Take the Shots You Must Miss

“I can accept failure, but I can’t accept not trying.” ~ Michael Jordan

15

Sometime We Don’t Know What We Don’t Know

16

“I’ve always viewed investing as a complex game. It is like American football: those people on the street, they are on the one-yard line; we professional money managers are the two-yard line; the Sage of Omaha is on the three-yard line. Even if Mr. Buffett is three times smarter than common people, there are still ninety-seven yards ahead of him before touchdown.” “What we don’t know about the future is enormous. Sometimes we don’t know what don’t know because the unknown is simply unknowable. You do all the work, hoping to right and beat the market, and still you are going to be wrong a lot. That’s just life. All you need is to be right 60% of the time.”

~ Bill Priest

Source: Epoch

Accept Failure and Keep Trying

17

“I’ve missed more than 9,000 shots in my career. I’ve lost almost 300 games. 26 times I’ve been trusted to take the game-winning shot and missed.” “I’ve failed over and over and over again in my life. That is why I succeed.”

~ Michael Jordan

Source: Youtube

Questions & Answers

“To be, or not to be, that is the question.” ~ Hamlet, William Shakespeare

18

Follow Me

19

n Twitter:

Appendix: Financial Technology for the Greater Good

“Finance is the science of goal architecture.” ~ Finance and the Good Society, Robert Schiller

20

Financial Technology Provides Tools for the Greater Good

n Modern financial system is a complex web of contracts: Ø Asymmetric information & expected cash profit maximization.

n SoLoMo technology has greatly reduced the cost of democratizing, humanizing and expanding the reach of financial capitalism on a global scale. Ø Example: Blockchain/Bitcoin, LendingClub.

n Financial technologies facilitate the goal of individuals, companies and societies. Ø It is a means to an end, not the other way around. (the Latin root for finance

is finis, i.e., end)

n Finance is amoral. Ø Guns don’t kill; People kill.

n The fundamental innovation of financial system since the dawn of human

civilization is the monetization of memory in various forms of transferrable credit. Ø Memory is the source of credit which facilitates resource transfer across time

and space.

n We need a new definition of generalized investment yield. Ø Capital allocation model in broader social context.

21