uk construction plan

TRANSCRIPT

Table of Contents

1. Introducing the organisation

Balfour Beatty Company Profile

2. Environmental Analysis

UK Construction Industry Overview

Porter’s Five Forces Analysis

Competitive Rivalry

Threat of Entrants

Power of Suppliers

Bargaining Power of Buyers

Threat of Substitutes

Overall attractiveness of the Industry

SWOT Analysis

3. Results and Implications of the analysis

Executive Summary

In this report we have review the current position of Balfour Beatty

Construction Company and the overall UK Construction Industry. Balfour Beatty is

one of the leader companies in construction industry in UK. The construction industry

is a cyclical industry and its growth rate is steady. The five forces analysis of the

showed that the market is attractive and fairly competitive.

Internal analysis showed that Balfour Beatty competitiveness is at a high

level. Also, there are different major competitors that Balfour Beatty has to face like,

Taylor Woodrow, Carillion, Amec. Balfour Beatty should has as a primary focus the

maintenance of its leading position in the UK Industry and also its extension to new

markets. Since the market is at a growing stage, threats and opportunities were

various and Balfour Beatty should take them into great consideration.

Business plan objectives

The objectives of this business plan are the following:

To provide a review of the company’s present position

To describe the industry the company operates within

To analyse the competitiveness of the market

To make specific proposals

I. Introduction

Balfour Beatty Company overview

One of the UK's most infamous construction companies due to its wilful

involvement with projects such as the Ilisu dam in Turkey (www.ilisu.org.uk), it is

also the UK's largest and most profitable with a turnover in excess of £2.6 billion. In

2000, the company made £94m profit, £477, 233 of which went to its chief executive,

Michael Welton (www.socialistworker.co.uk). Balfour Beatty is the world's twentieth

largest construction company (see Appendix I, table1) and first in the UK

construction industry (see Appendix I, table2). Also, it is important to mention that in

2002, it had 5,449 new global contracts (ENR, 2002).

Balfour Beatty is a world-class engineering, construction, services and

investment group and it includes the following section (Annual review of Balfour

Beatty, 2007):

Building, Building Management and Services: Balfour Beatty is an

international specialist in the design, construction, equipping, maintenance and

management of buildings and selected aspects of their internal environment.

Rail Engineering and Services: Balfour Beatty is an international leader in

the design, construction, equipping, maintenance, management and renewal of rail

assets and systems.

Civil and Specialist engineering and Services: Balfour Beatty is a leading

international provider of civil and other specialist engineering, design and

management services, principally in transport, energy and water.

Investments: Balfour Beatty promotes, develops and invests in privately

funded infrastructure assets in selected sectors, on an international basis.

Balfour Beatty is the largest UK-listed construction group (by market

capitalization). It is seeking growth through investment in public-private partnerships

(PPP), as well as expansion of its core engineering and construction operations

overseas.

Mission: “To continue reliable, responsible growth in shareholder value over the long

term”.

Vision: “We aspire to being the pre-eminent infrastructure company in the world”.

Company’s Objectives:

There are four areas that they intended to further develop their business to ensure

that they will be able to maintain their target growth rates over the medium and long

term. These are:

UK regional contracting;

Professional and technical services;

Extension of their investment business into new markets;

Establishing strong domestic businesses in selected overseas markets based on

our UK model (Annual review of Balfour Beatty, 2007).

II. Environmental Analysis

UK Construction Industry Overview

The UK's construction industry has been enjoying a period of strong growth,

with the infrastructure and the commercial construction sectors at the forefront of this

trend (Construction Industry Market Review, 2003). The annual round of results

published by construction firms in March 2003 showed that the sector is shifting away

from one-off contracts carrying high risks and big returns toward lower risk long-term

deals that go beyond construction to designing, maintaining and operating buildings

(www.unison.org.uk )

The UK construction industry provides a tenth of the UK's gross domestic

product, employs 1.4 million people and is worth around £65 bn per annum

(www.dti.gov.uk) With an output of £81.9bn in 2002 (Construction Industry Market

Review 2003) the UK construction industry is ranked in the global top ten (Crowley,

2003)

Sectors

Housebuilding accounted for 38.6% of the construction industry's output in

2000 (UK Construction Industry Market Review, 2001) The amount spent on public

housing has never exceeded £2bn whereas the figure for private housing has

consistently been double or triple that amount (Construction Statistics Annual, 2003)

Infrastructure accounted for 9.2% of all construction work in 2000 - a

slightly lower figure than for the previous 4 years - and was worth £6.43bn. Road

building is the main source of infrastructure work (UK Construction Industry Market

Review, 2001) The National Audit Office revealed that more than £434m worth of

road-construction contracts - 51% of those awarded - were won by five firms, Balfour

Beatty, Budge, Fairclough, Alfred McAlpine and Tarmac (www.geocities.com).

Industrial construction is the smallest of the basic sectors of the whole

construction industry. In 2000, the output of private construction work was £3.7bn, or

5.3% of the total construction sector (UK Construction Industry Market Review,

2001)

Commercial construction output, which includes a wide variety of

commercial work, accounted for just over 18% of all construction work in 2000 (UK

Construction Industry Market Review, 2001).

Building materials embrace a wide range of materials and components such

as bricks, tiles, cement and timber. The UK construction materials sector is

undergoing a period of rationalisation, with many UK companies now forming part of

international companies. The UK building materials market is forecast to increase by

13.7% at current prices between 2001 and 2005 (UK Construction Industry Market

Review, 2001).

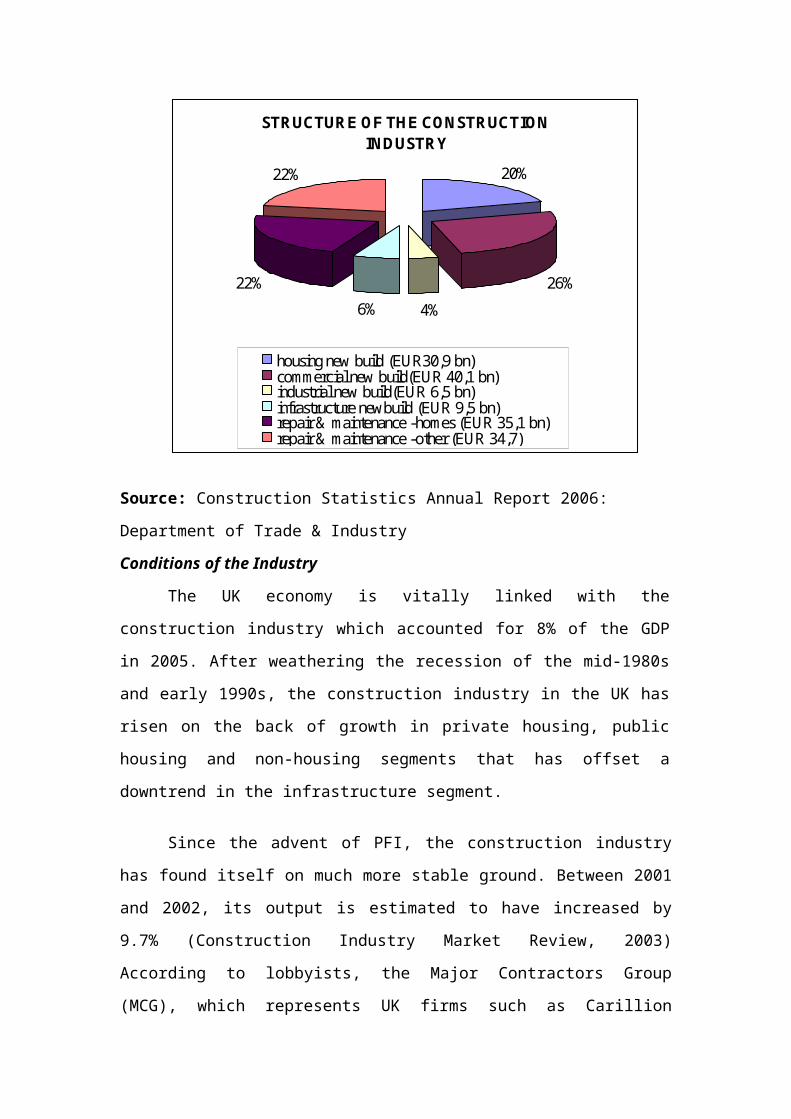

The total value of UK construction output in 2005 was EUR 157.11 billion.

The chart below shows how this output was divided between the different

construction sectors:

STRUCTURE OF THE CONSTRUCTION INDUSTRY

20%

26%

4%6%

22%

22%

housing new build (EUR30,9 bn)commercial new build(EUR 40,1 bn)industrial new build(EUR 6,5 bn)infrastructure newbuild (EUR 9,5 bn)repair & maintenance -homes (EUR 35,1 bn)repair & maintenance -other (EUR 34,7)

Source: Construction Statistics Annual Report 2006: Department of Trade & Industry

Conditions of the Industry

The UK economy is vitally linked with the construction industry which

accounted for 8% of the GDP in 2005. After weathering the recession of the mid-

1980s and early 1990s, the construction industry in the UK has risen on the back of

growth in private housing, public housing and non-housing segments that has offset a

downtrend in the infrastructure segment.

Since the advent of PFI, the construction industry has found itself on much

more stable ground. Between 2001 and 2002, its output is estimated to have increased

by 9.7% (Construction Industry Market Review, 2003) According to lobbyists, the

Major Contractors Group (MCG), which represents UK firms such as Carillion

(formerly part of Tarmac), Costain and Amec, construction companies engaged in the

private finance initiative expect to make between three and ten times as much money

as they do on traditional contracts. This strategy is reinforced by figures from the

European Construction Industry Federation (ECIF), which show that the UK

construction sector grew by over 8% last year while its counterpart in Germany and

France slumped by 2.5% and 0.7% respectively (Macalister,2003).

The UK government defends PFI by its use of something called the 'public

sector comparator'. This shows whether or not privately financed schemes offer better

value for money than conventional funding. The main problem with this is that the

government has provided an accounting device called 'risk costing' which has meant

that private firms generally emerge as winners. When a consortium of private

companies agrees to build something for a public body, it acquires the risk that the

project might fail. This risk is 'costed' and becomes a key component of the value-for-

money calculations.

Furthermore, the UK construction industry is extremely diverse, and is

dominated by SMEs; approx. 270,000 contractors and builders contributed 67% of the

total construction output in 2005. There has been a marked shift among UK

contractors and consultants towards Public-Private Partnership (PPP) and Private

Finance Initiative (PFI) Also, the surge in the Chinese construction demand is

expected to increase input prices globally, including those for domestic UK

construction companies. Growth strategies adopted by the key players include

expansion into overseas markets, diversification through acquisitions, exiting low-

value businesses in the construction sector and leveraging PFI projects for long-term

growth in revenues and profitability.

Main Competitors

There are several competitors threatening Balfour Beatty but its major ones

are the following:

Carillion, is likely to become Balfour Beatty's strongest competitor, as it has

refocused on the lower-risk segments in construction services and towards support

services and PPP (www.unison.org.uk).

AMEC, one of the leading construction services companies in the UK, has a

highly leveraged balance sheet and volatile cash flow. Therefore, it is unlikely to pose

a threat to Balfour (AMEC Annual Report and Accounts, 2007).

Alfred McAlpine, though small in terms of scale of operations, is well-

positioned in high-growth markets (www.mcalpineplc.com).

Taylor Woodrow, its house building sector is the fourth largest in the UK

following the £480m acquisition of rival Wilson Connolly in 2003 and £556m

acquisition of Bryant Homes (Wilson Connolly Company profile, 2008).

II. Porter’s Five Forces Analysis

The state of competition in an industry depends on five basic forces, the

strength of which determines the ultimate profit potential of the industry (Porter,

1985). Five forces analysis of the constructing sector is analyzed in the following

section (See also Appendix II)

Rivalry among Competitors

Balfour Beatty is the largest UK-listed construction group (by market

capitalization) and has to face with four major competitors within the UK Industry:

Carillion, AMEC, Alfred McAlpine and Taylor Woodrow. Each of these companies

targets the same clients and each has a fine reputation for customer satisfaction. New

homes are currently exempt from the Sale of Goods Act. Each year there are 150,000

homes purchased throughout the UK. With an average value of £100,000 per property

this means that an industry worth in excess of £1.5bn per year is unregulated by the

government and exempt from usual trading standards, leaving owners of new homes

with little or no protection for the most expensive purchase they will ever make.

(www.wimpeyrawdeal.co.uk) As a result, there is a high price competition within the

companies in the industry.

The industry is at a growing stage and with the 2012 London Olympics is

expected to further propel growth in the UK construction industry by boosting

investments in South-East London. Economic stability and low interest rates are also

likely to drive homebuilding demand. The highly fragmented nature of the UK

construction industry implies intense price competition and falling margins for a bulk

of the players. Also, because of the large amount of initial capital required for

constructions and the high prices leaves the entire industry to large companies that

have sufficient capital. Another factor is that the surge in the Chinese construction

demand is expected to increase input prices globally, including those for domestic

UK construction companies. As a consequence, competitive rivalry will be high but

also it will deteriorate entrance of small companies.

Threat of Entrants

It is important to identify the possibility and probability of new entrants in an

industry because they can intrude on market share and profitability of existing

competitors. Economies of scale, product differentiation, capital requirements,

switching costs and government policy affect UK construction industry.

The construction skills network report 'Blueprint for UK construction 2006-

2010' forecasts that UK construction output is set to average 3% growth annually

between 2006 and 2010. At the end of 2006 just over 2.5 million people are expected

to be employed in construction across all occupations. It predicts that in order to

deliver this growth, the amount of workers needed is likely to increase by

approximately 245,000 throughout the UK. This will mean that an average of 88,000

new recruits will be required each year (www.constructionskills.net).

The construction industry is heavily dependent on the adequate supply of a

skilled labour force, and as a result the skilled labour shortage in the UK has received

considerable attention in recent years. With the current economic recovery the

industry is expected to experience considerable skills shortages in both traditional and

new skills areas (MacKenzie et al, 2000). Unlike subcontractors, skilled construction

workers have supplier power. The construction industry has issues with worker

shortages (Scripps Howard New Service study, 2005). In addition, contractors’

associations say “it’s particularly crucial during times like now when commercial and

residential construction is in high demand” and this strong supplier power of

construction workers leads to high costs of labour (Scripps Howard New Service

study, 2005).

Power of Suppliers

The UK market is very competitive, with not only a large number of UK

suppliers active, but many overseas suppliers already established in the market.

Suppliers in this industry are not concentrated and they act as separate groups

competing for the same project through the bid system. Volume is a significant

concern to these homebuilders, thus, on one hand, require a specific amount of steel,

concrete and wood for the homes and on the other hand, the subcontractors must build

these variable costs into their homebuilding bids. As a consequence, large contractors

are not affected in terms of supply volume giving suppliers any leverage.

There are over 100 trade associations representing suppliers of various

construction products and materials. In addition to UK producers there are a large

number of overseas companies strongly active in the UK market and represented by

their own UK subsidiaries or distribution partners (http://www.constprod.org.uk).

Every contractor requires a large number of inputs except from land including

wood, concrete, plastic, gravel, oil, gasoline, steel and other raw materials. Prices for

some of these materials are non-negotiable, for instance, the price of gasoline and oil,

which affect all companies equally and do not lead to a strategic advantage for

suppliers. Still, the fragmented nature of the supplier market in all other construction

supplies to homebuilding companies severely limits supplier power.

In the house building sector there is a continued shortage of housing, and in

particular cheaper housing suitable for key workers in the South East of the country.

The government plans for the provision of 1 million new homes by 2016. House

builders are being encouraged to supply affordable housing as well as housing that

complies with new more stringent regulations on environmental performance.

Bargaining Power of Buyers

There are some large customers who repeatedly tender for business and are

well informed and experienced buyers. However none of these customers are large

enough to constitute a significant part of the procurement of building services. As

such there is little prospect of them being able to exercise any buyer power (OFT,

2003).

There is a weak demand-side in terms of the proportion by number of clients

who have access to innovative or improved techniques. The clients say that they want

to focus on value – this makes good business sense to them – and whilst cost is one of

the primary criteria it is not the only one, speed or quality being potentially as

important. In the supply chain cost seems to be the only criteria, an attitude of giving

the least and trying to claw back the most prevailing (Morledge, 2002).

Threat of Substitutes

There the threat of two substitutes: Prefabrication and Timber Frame.

Prefabrication, for a long time was a “dirty” word in the UK, but now is seen as one

of the ways the industry can achieve higher output and reduce build time and costs.

Prefabricated panels and components are being used in commercial, industrial and

housing projects. The organisers of the 2012 London Olympics are especially keen to

use prefabrication in the specification of stadiums and the Games infrastructure

(Olympic Delivery Authority).

While the cost of bricks and blocks used in most new home construction will

continue to rise disproportionately due to skyrocketing gas prices, the introduction of

tough new building regulations will also encourage more house builders and housing

associations to try timber frame construction – and the tangible business benefits of

this way of building will keep the construction industry coming back for more 2006

will be "the year of timber frame", predicts the UK Timber Frame Association

(UKTFA) (www.timber-frame.org). According to NAO report (2006), there are no

high risks associated with open panel timber frame, compared to traditional

construction which is perceived to be at high risk of price fluctuations, delays due to

bad weather, lack of key trade skills, service installation faults, health and safety

hazards, construction errors and other defects at handover.

Overall Attractiveness of the Industry

Regarding the future, PFI work will continue to be important, much of it for a

total-package approach to construction, with private companies being involved in

finance, operation and maintenance, as well as in the design and construction

processes. The continuing skills shortage will continue in the short term, or until

initiatives such as training take effect to give a longer-term solution. To help increase

the proportion of affordable housing, developments will continue through the use of

new materials and prefabricated construction through the use of structural insulated

panels, for example. The new Trustmark scheme should help homeowners to avoid

`cowboy' builders and, in the medium term, the 2012 Olympic Games in London

should provide a variety of opportunities for the construction industry.

SWOT Analysis

(see Appendix III for Balfour Beatty SWOT Analysis)

III. Results and Implications of the analysis

As a whole, the construction industry faces important challenges. The

sustainability of resources, energy, water and supplies to provide socially acceptable

and environmentally compatible building is a major theme, particularly to achieve

these aims at an agreeable price. The built environment makes a significant

contribution to the UK's greenhouse-gas emissions and the Government is seeking

ways in which these can be reduced. Planning consent for construction work is often

a major problem, largely as a result of difficulties in satisfying government planning

regulations.

In addition, the construction industry is the subject of increasing legislation

across a broad spectrum of topics relating to employees, customers, energy and

natural resources. Economically, some sectors of the construction industry have not

grown as rapidly as they might, owing to delays in government programmes. The

shortage of skilled labour continues to be a problem. Moreover, in the house building

sector, there is a shortage of housing, and this is unlikely to ease in the short term,

unless planning regulations are relaxed and a substantial affordable-housing

programme makes an impact: high house prices exclude many prospective first-time

buyers from the housing market. The infrastructure sub sectors have experienced a

decline in work, much of which is due to delayed programmes in.

In the building materials sub sector, there are challenges relating to rising

energy costs and environmental issues, such as sustainable material sources, disposal

of waste and recycling. New materials are being investigated to accommodate

improved environmental features; for example, reducing heat loss and simplifying

construction methods.

However, the competitive rivalry, on a national scale, is likely to increase

highly in the future. As both firms continue to grow, the number of geographic

regions that they find themselves in direct competition with each other broadens

market commonality and creates multi-market competition.

Factors, such as the UK government’s commitment to PFI projects, an

upswing in the demand for housing and outsourcing of facilities management, have

been driving the business of the construction companies in the UK. Balfour Beatty’s

growth has been driven by its success in the UK PFI market, a strong balance sheet

and record order books.