uk retail banking insights - pwc · pdf file*connectedthinking uk retail banking insights...

TRANSCRIPT

*connectedthinking

UK Retail Banking InsightsEvolving Industry Observations*

Banking & Capital Markets

November 2007

04 After the crunch: What next?

08 Sullen but not mutinous: Emotional engagement and bank switching amongst corporate SME customers

12 Unanswered questions threaten to weaken Basel II

16 The US sub-prime story: Contagion or distraction?

20 Customer profitability versus product profitability: The impact of economic regulation

Editor: Richard AdnettDirectorRetail and Mortgage Banking Group PricewaterhouseCoopers (UK)T: +44 (0)161 245 2773E: [email protected]

Distribution: If you would like to receivethis publication by email or you would liketo add your colleagues to the mailing list,please contact Carly Dyer [email protected]

3 PricewaterhouseCoopers UK Retail Banking Insights November 2007

Welcome to the latest edition of UK Retail Banking Insights, PricewaterhouseCoopers regularpublication which focuses on topical issues facing the retail banking sector.

In recent months we have seen a vivid reminder of the consequences of mismanagingrisk. In the increasingly complex and globalised world, risks may not be identified or maybe inappropriately measured. You therefore won’t be surprised to see that this editionfocuses on topical risks being faced by the retail banking sector.

Unsurprisingly, we have two articles relating to the credit crunch – one on the cause andthe other on the effect. In our lead article: ‘After the crunch: What next?’, Andrew Grayfocuses on how industry players can be better placed to deal with the effects of thenext financial shock. Robert Boulding, in his article, ‘The US sub-prime story: Contagionor distraction?’ focuses on the causes of the US sub-prime lending difficulties andwhether these could be replicated in the UK lending marketplace.

The risk theme continues with our article on whether firms are seeing businessbenefits arising from Basel II, penned by Richard Barfield. His paper is based on theoutcome of discussions he chaired at the PricewaterhouseCoopers1 June BaselExecutive Forum. Although these discussions took place before the credit crunch beganto bite, his article demonstrates that despite the huge amount of work that banks haveput into Basel II, there has been little impact to date on product pricing, and doubtsremain about whether Pillar 3 will really provide the marketplace with comparable data onrisk, which has clearly been lacking in recent months.

Our remaining two articles focus on the risk of Small and Medium Sized Enterprise (SME)customers switching to other banks and regulatory pricing risks.

Our paper on the SME business banking sector by David Wardrop-White argues thatbanks can differentiate themselves by focusing on the emotional aspect of their customerrelationship rather than just the more usual product, service and price aspects.

Tim Ogier’s article on economic regulation challenges whether industry players havesufficient focus on managing their relationships with the regulators and whether they aremoving fast enough towards a customer, rather than product, profitability mindset.

I hope you find this edition enjoyable and thought provoking. As ever, we welcome anyfeedback on topics you would like to see covered in future editions.

John HitchinsUK Banking LeaderPricewaterhouseCoopers (UK)T: +44 (0)20 7804 2497E: [email protected]

1 ‘PricewaterhouseCoopers’ refers to the networkof member firms of PricewaterhouseCoopersInternational Limited, each of which is a separateand independent legal entity.

4 PricewaterhouseCoopers UK Retail Banking Insights November 2007

After the crunch: What next?The full effects of the much-predicted credit crunch are probably still to be felt, but what is certainis that more challenges will come. As events unfold, it is becoming increasingly clear that theimpact on individual organisations is varying considerably. Businesses must take time now toprepare themselves for further shocks.

One question still to be answered in the wake of yet another ‘once in a lifetime’ financialcrisis is: how bad can it get? For some, the answer is ‘very’. Other businesses are morerobust, or have been able to take preventative action. The ripple effect of the credit crisison business (which, more accurately, is a shortage of liquidity and difficulties in pricingcredit risk) that began to unfold in August 2007 could have the potential to be deeplydamaging to the conduct of everyday business, to reputations and to attitudes to risk.And the full extent of the impact is still unfolding.

Yet this was a crisis long predicted, although the speed and severity caught almosteveryone out. The roots of it go deep – into the dot-com crash of 2000 – when, aroundthe world, the response was to keep interest rates as low as possible to encourage areturn to economic confidence. Money became cheap and plentiful, and as aconsequence, investors increasingly found themselves competing for assets, the pricingof risk became increasingly difficult as structures became more complex, and frequentlyinvestors underestimated the real risk. With low interest rates, benign inflation and risingasset prices, all was going well. As interest rates have risen over the past few years, thechickens have been coming home to roost. A combination of questionable lendingpractices of some US mortgage lenders, falling US property values and the consequentialdefaults by overborrowed mortgagees, has caused widespread credit losses onsub-prime mortgage portfolios.

This may have been a local difficulty for the US, except that many of these poor-qualityassets were, when originated, bundled into various types of investment securities,so-called ‘asset-backed securities’ or collateralised debt obligations (CDOs), and sold toinvestors and financial institutions around the world, many of them respected householdnames. The initial shocks were significant, but also resulted in contagion into othermarkets. The problem was that the downside risk was not fully reflected in the assetprices. Some are now questioning the assignment of credit ratings. Nobody really knowswho is left holding how many of these parcels of overvalued assets, hence the profoundreluctance of financial institutions to lend to each other for fear of throwing perfectly goodmoney after bad.

Contact us

Andrew GrayPartnerPerformance Improvement ConsultingPricewaterhouseCoopers (UK)T: +44 (0)20 7804 3431E: [email protected]

Further complications exist in thepricing of these assets for those that dohold them. In the absence of liquidity inthe market and price transparency, thecalculation of fair value of assets requiresa far greater degree of managementjudgement. This is compounded by thefact that there are examples of holders ofassets not having complete records of theactual assets backing the securities theyhave purchased.

Surprises are likely to continue for sometime, driven by the lack of transparencyof asset ownership, the complexity of theasset-backed structures, the differingdegrees to which conduit vehicles canlook to sponsors/managers for support,and the nature of risk transfer in today’scomplex financial world.

On the edge?

Market corrections can easily becomecrashes as confidence is lost. The threatgoes deeper than the possible extent ofcredit losses on complex asset andderivative products. This latest financialcrisis could seriously affect businessrevenues and costs more widely. However,the US Federal Reserve Bank has cut USrates, stock market values have remained

buoyant, and Bank of England auctions toprovide liquidity, albeit at a price, havegone unused.

All firms will have to factor in the likelyimpact of a weakening economy andhousing market on loan loss provisionsand recoveries. Concerns remain that theliquidity crisis in the debt markets couldspill over into the equity market and triggera steep fall in prices (a fear that wasunfounded at the time of writing this articleas the FTSE 100 stood at over 6500, only3% off the 12-month peak). For themoment, firms that hold good levels ofcash and employ a spread of short-,medium- and long-term funding methodsare largely unscathed by the credit crunch.In the short term there may be casualtiesacross all sectors among businesses thatare reliant on short-term funding from thedebt markets. But if rising mortgage ratesundermine High Street spending,businesses that depend on consumers’discretionary spending will be impacted.Ongoing evidence from the US points toproblems in the housing market, andelsewhere consumers appear to beshowing greater willingness to manage tolower personal debt levels.

Financial services companies will strugglewith portfolio risk and complexity, thedifficulty of fair valuing assets and theneed to rapidly rethink strategy in the lightof radically changed conditions. Banksand fund managers, in particular, face arocky time working through therepercussions of investors’ failure to fullyunderstand the risks they were taking on.Far fewer are now prepared to buysecurities such as the commercial paperand certificates of deposit issued by banksand building societies to raise short-termmoney. And more institutions are reluctantto undermine their own strength by lendingto others. The most popular home for cashis overnight deposits held by banks withthe strongest credit ratings and where thefunds can be called at any time. Themarket has already begun to differentiatemuch more sharply between issuers, tothe benefit of those with the strongestbalance sheets.

Other difficulties include a reduction insecuritisation and conduit administrationfees, and underwriting fees for mortgagepackaging. Some hedge funds could goout of business and lead to cuts in primebrokerage fees. Credit rating agencies arecoming under significant scrutiny, and may

6 PricewaterhouseCoopers UK Retail Banking Insights November 2007

well adopt a more cautious approach inthe future. As a consequence, creditratings may be affected, raising fundingcosts and regulatory capital relatedcharges. The sheer volume of marketactivity still continues; some marketsreported record volumes in August 2007.This will put companies under operationalpressures too, such as in deal processingand settlement and account reconciliation.Not only might operational costs rise, butthere could also be lapses of controlleading to operational losses.

Opportunities

Potentially the most serious loss of allcould be loss of reputation. Manyconsumers are already highly sceptical ofthe financial services industry and therecent events are another blow toreputations. There is also a danger ofoverreaction and some good assets maybe marked down with the bad ones.

However, it’s not all bad news. The fact isthat corporate UK is still relatively lowlygeared and companies are holding a fairamount of cash. This could be themoment to do deals. There is a backlogof deals to be done, as well as a greatdeal of money available to invest, with

Asian growth and Middle Eastern oildollars adding to the funds needing to finda home. Alongside the threats to business,there are opportunities, and money is stillavailable for good quality propositions.In the financial services sector, the short-term funding famine could accelerate therate of consolidation. Certainly, from along-term perspective, current marketprices for bank stocks look low. And oneconsequence of the impact on the privateequity sector of the credit markets turmoilis that backers of M&A deals are likely tobe sitting on their hands. This gives strongtrade buyers a chance to make strategicacquisitions without seeing prices drivenup by private equity backers. Companiesthat have accumulated a war chest offunds for just such an eventuality will nowbe well placed.

What are the next steps?

Organisations can, and will, continue tomake money where they manage riskeffectively. Those that do well will beincreasingly sophisticated, as discussedbelow. However, of critical importanceis ensuring that there is adequategovernance over the steps taken.

Alongside the threats to business, thereare opportunities, and money is stillavailable for good quality propositions.In the financial services sector, theshort-term funding famine could acceleratethe rate of consolidation.

Stress testing

Whilst the wider economic picture remainsunclear, the best advice for many firmsacross all sectors may be to take a wait-and-see approach – and a careful look attheir businesses, stress testing them forboth economic slowdown and full-blownrecession. And it would be useful to factorin the wider commercial and operationalimpacts through combined risk, valuation,economics, operations and HR teams.

There are practical ways of approachingthe problems. Certainly, for financialservices firms, some crisis managementmay still be necessary in the form of assetand portfolio revaluation on a mark-to-model basis for both management andstatutory accounting purposes – and thismay need some independent validation.

Financial forecasting and strategy mayneed careful reappraisal. Manyassumptions underpinning strategies,plans, budgets and transactions could wellneed revision and material change mightalso have to be disclosed under regulatory,statutory or stock exchange obligations.

In the medium term, detailed contingencyplans for disaster recovery and businesscontinuity need to be prepared to achievea clear understanding of what to do in thecase of a sharp market deterioration. A lotof work may need to be undertaken toimplement changes to models, policies,processes and operations in response tolessons learned. Firms need to be wellprepared for the next ‘once in a lifetime’financial shock.

Reviews required

In the meantime, the crunch could wellshake out further changes in regulation,or prompt further demands for changefrom stakeholders. Various reviews maybe required and a simple checklist mightlook like this:

Reviewing risk model adequacy:

• Transparency of exposures;

• Back-testing of model assumptions,particularly on:

1. Asset volatility;

2. Asset liquidity; and

3. Asset correlation.

Reviewing valuation/reporting systemadequacy, concentrating on:

• Transparency, validity and robustness ofvaluation models;

• Accuracy and quality of underlyingreference data;

• Adequacy of controls on model useand maintenance;

• Consistency in the bases andassumptions of risk and valuationmodels (particularly as assumptions maynot reflect recent experience); and

• Effectiveness of risk escalationprocedures in the event of seriousmarket volatility or disruption.

Reviewing organisational capacity:

• Check policies, procedures andavailability of skilled people to respondquickly and effectively to serious marketvolatility or disruption to stem losses(or even make profits).

Also review the adequacy of:

• Limit framework;

• Reporting framework;

• Stress-testing procedures;

• Review operational capability to handlethe situation, with particular focus on:

1. Process effectiveness;

2. Infrastructure effectiveness;

3. Functional capacity (front, middle,back office);

4. Straight Through Process/workflowevaluation.

For the moment, the market appearsto be safe from multiple bank and buildingsociety collapses. Sooner or later, thescale and depth of the sub-prime crisiswill be measured and liquidity will returnto the short-term debt markets.

There is now a deeper, broader distresseddebt and impaired asset market than everbefore. Hedge funds, brokers, vulturefunds and activist investors can price justabout anything that smells like a deal,and there is more data on downside risksas well as upside. Certainly, there will besome ongoing discomfort, and somebanks, funds and other investors mayhave to ride out the storm, but wenow have markets that are morecapable of trading their way out of justabout anything.

7 PricewaterhouseCoopers UK Retail Banking Insights November 2007

8 PricewaterhouseCoopers UK Retail Banking Insights November 2007

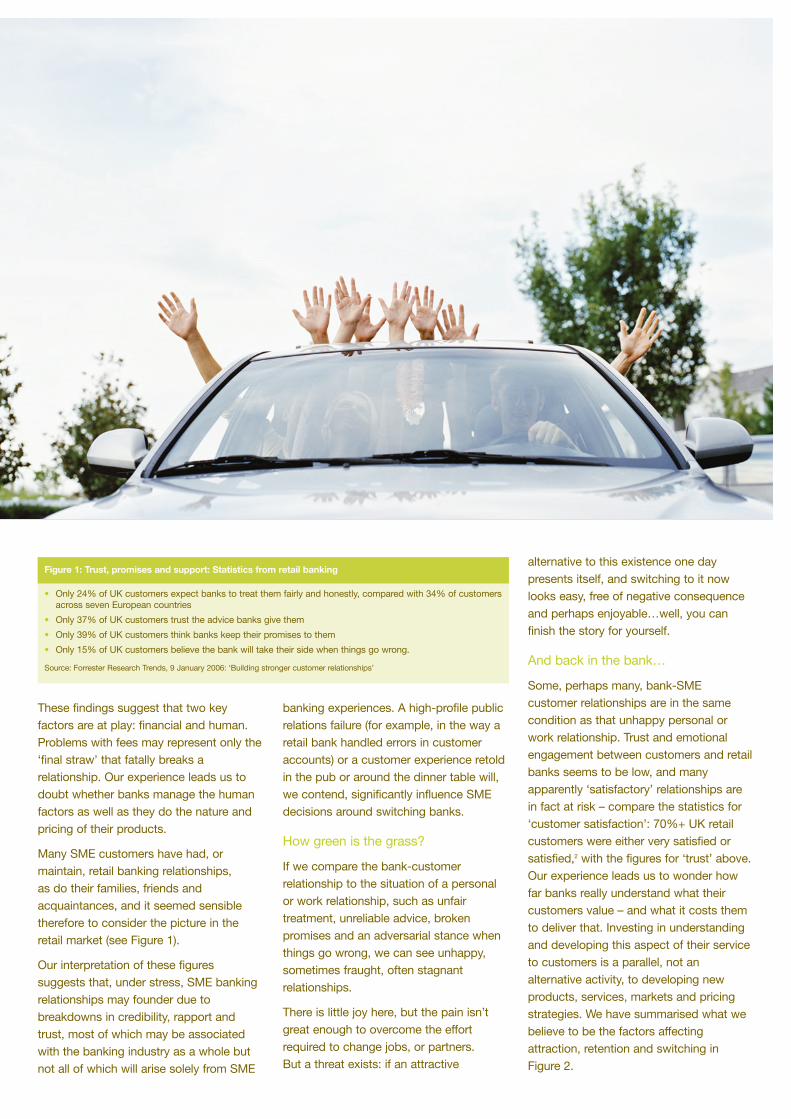

Sullen but not mutinous:Emotional engagement andbank switching amongstcorporate SME customersBusiness Banking – or Small and Medium Sized Enterprise (SME) – customers are an importantsegment of the customer base for many retail banks, and indeed the nature of these customersmeans that the key challenges in meeting their needs are very similar to those presented by personalcustomers. As such, the emotional and psychological aspects of the relationships between banks andtheir SME customers are coming under further investigation as banks work to maximise their abilityto retain and attract customers.

A number of UK banks are seeking to grow their share of the SME market. It is likely thatthe majority of this growth will come from customers who switch their business from acompetitor. This market already faces two challenges: buyers who are less sophisticatedthan their counterparts in the major corporate banking environment; and limitedresources with which banks can build relationships and tailor their products. This has ledto the search for mass customisation at low cost.

Human factors

Around 15% of UK ‘small businesses’ switched banks in the period 2002-2003. ‘Humanfactors’ are significant in decisions about switching banks, as highlighted in the researchcommissioned in 2004 by the Federation of Small Businesses.1 It identified the top sixreasons for switching banks as:

• Avoid/reduce bank charges

• Poor quality of service received

• Search for better terms

• Poor quality of advice received

• Earn a higher rate of interest

• Change of bank personnel

The same research identified the six main reasons for not switching as:

• Happy with the services provided

• No real difference between banks

• Competence of bank staff I deal with

• Convenience of the bank’s location

• Reliability of bank in meeting the financial needs of the business

• The bank understands my business

Contact us

David Wardrop-WhiteDirectorPerformance Improvement ConsultingPricewaterhouseCoopers (UK)T: +44 (0)131 524 2236E: [email protected]

1 Federation of Small Businesses ‘Lifting the barriersto growth in UK small businesses’, 2004

2 Forrester Research Trends, 9 January 2006:‘Building stronger customer relationships’

These findings suggest that two keyfactors are at play: financial and human.Problems with fees may represent only the‘final straw’ that fatally breaks arelationship. Our experience leads us todoubt whether banks manage the humanfactors as well as they do the nature andpricing of their products.

Many SME customers have had, ormaintain, retail banking relationships,as do their families, friends andacquaintances, and it seemed sensibletherefore to consider the picture in theretail market (see Figure 1).

Our interpretation of these figuressuggests that, under stress, SME bankingrelationships may founder due tobreakdowns in credibility, rapport andtrust, most of which may be associatedwith the banking industry as a whole butnot all of which will arise solely from SME

banking experiences. A high-profile publicrelations failure (for example, in the way aretail bank handled errors in customeraccounts) or a customer experience retoldin the pub or around the dinner table will,we contend, significantly influence SMEdecisions around switching banks.

How green is the grass?

If we compare the bank-customerrelationship to the situation of a personalor work relationship, such as unfairtreatment, unreliable advice, brokenpromises and an adversarial stance whenthings go wrong, we can see unhappy,sometimes fraught, often stagnantrelationships.

There is little joy here, but the pain isn’tgreat enough to overcome the effortrequired to change jobs, or partners.But a threat exists: if an attractive

alternative to this existence one daypresents itself, and switching to it nowlooks easy, free of negative consequenceand perhaps enjoyable…well, you canfinish the story for yourself.

And back in the bank…

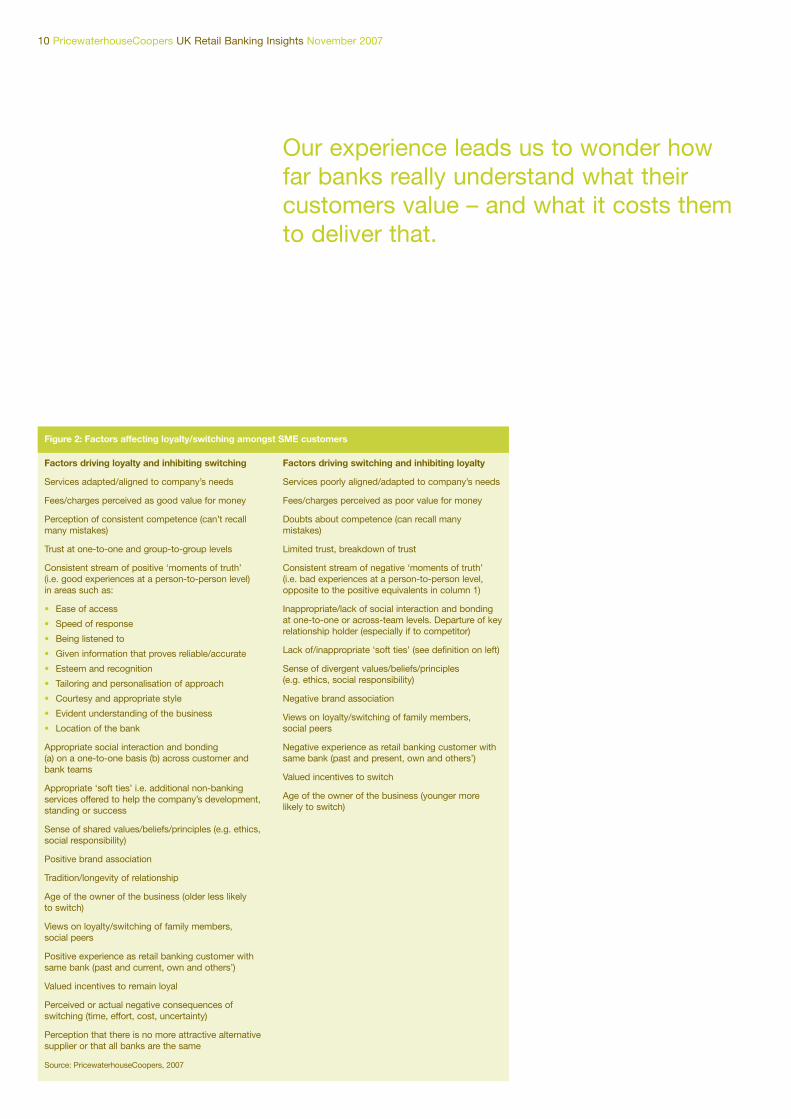

Some, perhaps many, bank-SMEcustomer relationships are in the samecondition as that unhappy personal orwork relationship. Trust and emotionalengagement between customers and retailbanks seems to be low, and manyapparently ‘satisfactory’ relationships arein fact at risk – compare the statistics for‘customer satisfaction’: 70%+ UK retailcustomers were either very satisfied orsatisfied,2 with the figures for ‘trust’ above.Our experience leads us to wonder howfar banks really understand what theircustomers value – and what it costs themto deliver that. Investing in understandingand developing this aspect of their serviceto customers is a parallel, not analternative activity, to developing newproducts, services, markets and pricingstrategies. We have summarised what webelieve to be the factors affectingattraction, retention and switching inFigure 2.

• Only 24% of UK customers expect banks to treat them fairly and honestly, compared with 34% of customersacross seven European countries

• Only 37% of UK customers trust the advice banks give them

• Only 39% of UK customers think banks keep their promises to them

• Only 15% of UK customers believe the bank will take their side when things go wrong.

Source: Forrester Research Trends, 9 January 2006: ‘Building stronger customer relationships’

Figure 1: Trust, promises and support: Statistics from retail banking

10 PricewaterhouseCoopers UK Retail Banking Insights November 2007

Our experience leads us to wonder howfar banks really understand what theircustomers value – and what it costs themto deliver that.

Factors driving loyalty and inhibiting switching

Services adapted/aligned to company’s needs

Fees/charges perceived as good value for money

Perception of consistent competence (can’t recallmany mistakes)

Trust at one-to-one and group-to-group levels

Consistent stream of positive ‘moments of truth’(i.e. good experiences at a person-to-person level)in areas such as:

• Ease of access

• Speed of response

• Being listened to

• Given information that proves reliable/accurate

• Esteem and recognition

• Tailoring and personalisation of approach

• Courtesy and appropriate style

• Evident understanding of the business

• Location of the bank

Appropriate social interaction and bonding(a) on a one-to-one basis (b) across customer andbank teams

Appropriate ‘soft ties’ i.e. additional non-bankingservices offered to help the company’s development,standing or success

Sense of shared values/beliefs/principles (e.g. ethics,social responsibility)

Positive brand association

Tradition/longevity of relationship

Age of the owner of the business (older less likelyto switch)

Views on loyalty/switching of family members,social peers

Positive experience as retail banking customer withsame bank (past and current, own and others’)

Valued incentives to remain loyal

Perceived or actual negative consequences ofswitching (time, effort, cost, uncertainty)

Perception that there is no more attractive alternativesupplier or that all banks are the same

Source: PricewaterhouseCoopers, 2007

Factors driving switching and inhibiting loyalty

Services poorly aligned/adapted to company’s needs

Fees/charges perceived as poor value for money

Doubts about competence (can recall manymistakes)

Limited trust, breakdown of trust

Consistent stream of negative ‘moments of truth’(i.e. bad experiences at a person-to-person level,opposite to the positive equivalents in column 1)

Inappropriate/lack of social interaction and bondingat one-to-one or across-team levels. Departure of keyrelationship holder (especially if to competitor)

Lack of/inappropriate ‘soft ties’ (see definition on left)

Sense of divergent values/beliefs/principles(e.g. ethics, social responsibility)

Negative brand association

Views on loyalty/switching of family members,social peers

Negative experience as retail banking customer withsame bank (past and present, own and others’)

Valued incentives to switch

Age of the owner of the business (younger morelikely to switch)

Figure 2: Factors affecting loyalty/switching amongst SME customers

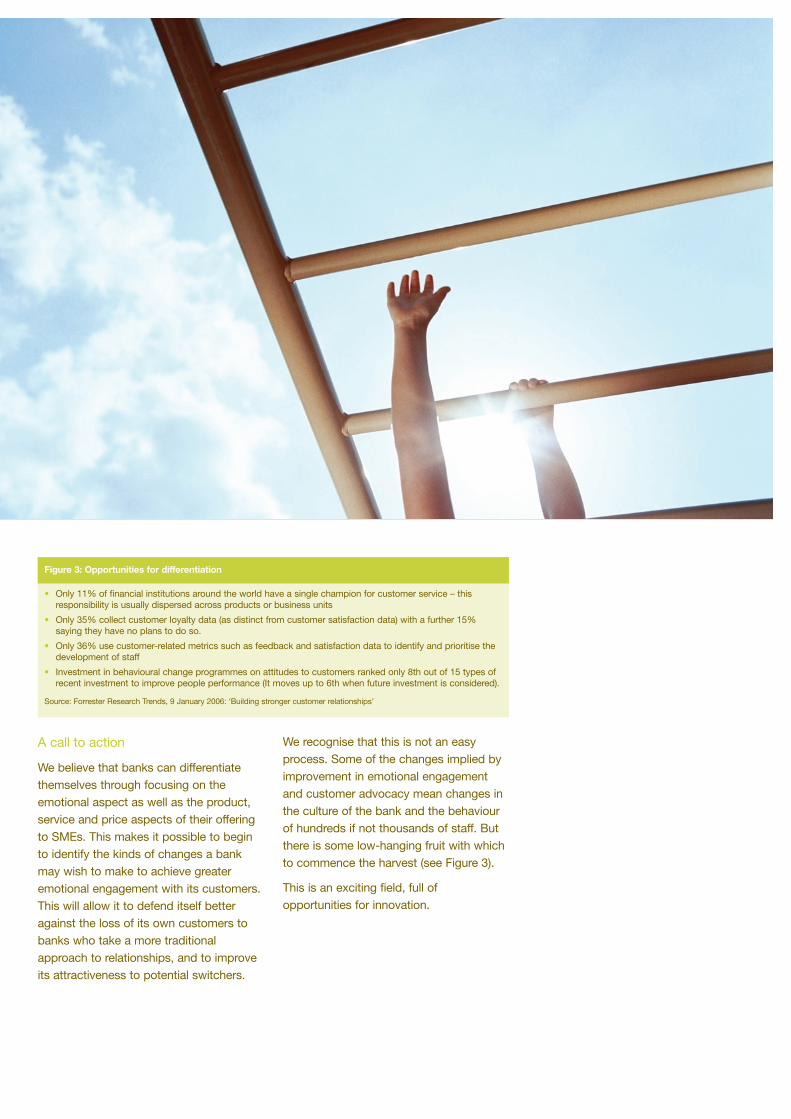

A call to action

We believe that banks can differentiatethemselves through focusing on theemotional aspect as well as the product,service and price aspects of their offeringto SMEs. This makes it possible to beginto identify the kinds of changes a bankmay wish to make to achieve greateremotional engagement with its customers.This will allow it to defend itself betteragainst the loss of its own customers tobanks who take a more traditionalapproach to relationships, and to improveits attractiveness to potential switchers.

We recognise that this is not an easyprocess. Some of the changes implied byimprovement in emotional engagementand customer advocacy mean changes inthe culture of the bank and the behaviourof hundreds if not thousands of staff. Butthere is some low-hanging fruit with whichto commence the harvest (see Figure 3).

This is an exciting field, full ofopportunities for innovation.

• Only 11% of financial institutions around the world have a single champion for customer service – thisresponsibility is usually dispersed across products or business units

• Only 35% collect customer loyalty data (as distinct from customer satisfaction data) with a further 15%saying they have no plans to do so.

• Only 36% use customer-related metrics such as feedback and satisfaction data to identify and prioritise thedevelopment of staff

• Investment in behavioural change programmes on attitudes to customers ranked only 8th out of 15 types ofrecent investment to improve people performance (It moves up to 6th when future investment is considered).

Source: Forrester Research Trends, 9 January 2006: ‘Building stronger customer relationships’

Figure 3: Opportunities for differentiation

12 PricewaterhouseCoopers UK Retail Banking Insights November 2007

Unanswered questions threatento weaken Basel IIAs world financial markets grapple with the fall out from the unravelling of US sub-prime loans, itseems that the need for Basel II is vindicated. But many in the banking industry still believe that somefundamental questions remain unresolved as they work to embed Basel II in their businesses.

Many firms say they are finding it hard to see the value of Basel II. Despite signs thatmany businesses, particularly in the retail sector, are gaining from the support to theirdecision-making that stress testing and better risk information is giving them, others areyet to be convinced.

In June, PricewaterhouseCoopers held a special forum in London on Basel II to whichsenior banking executives of UK-based domestic and international banks were invited.During round table discussions, it emerged that a wide cross-section of participantscould see little advantage to their business from this body of regulation.

For a wide cross-section of banks, the answer to the question, ‘What’s in it for me?’,critical to embedding any major change in a business, remains largely unansweredoutside the risk management community. Admittedly, that was before the latest bout offinancial instability hit the headlines, but in one of the world’s most dynamic andinnovative businesses, cultural attitudes may be slow to change.

There is a marked difference in approach between retail and investment banks.Risk managers in trading firms reported that they find it difficult to demonstrate anythingother than compliance benefits from a Basel II programme. Trading businesses alsoquestion the value of calculating operational risk and credit risk capital.

Limited effect on pricing

Yet the answer to this all-important question of buy-in seems straightforward enoughfor a mortgage lending bank, in that it attracts a lower regulatory capital charge. And incontrast to trading businesses, risk managers in retail banking are becoming involved inthe business planning process at an earlier stage as stress testing becomes arequirement for budgeting and long-term planning.

There is limited evidence across the sector that pricing is being affected by Basel II.The risk-based price is seen as a reference point for the commercial price, which relieson competitive considerations rather than regulatory capital being the key driver. Firmsworry that the reduction of capital requirements to support certain portfolios might lead to

Contact us

Richard BarfieldDirectorAdvisoryPricewaterhouseCoopers (UK)T: +44 (0)20 7804 6658E: [email protected]

more aggressive underwriting practicesto grow market share and thereby depressmargins, especially in secured lending.But pricing strategy is complex. Banks areunlikely to take a mechanistic approach toprice-setting, based on the required returnon risk-based capital. So far, no forumparticipants present have changed theirpricing policies fundamentally as a resultof Basel II. However they do expect itto have an impact in due course.

Opportunity cost

The potentially high opportunity cost ofBasel compliance is a major concern.Basel II projects, say some forumparticipants, are being funded at the costof projects that would be more beneficialto the firm’s risk management.

And Basel’s Pillar 3 throws up somefundamental problems that couldseriously weaken its impact as a sourceof market discipline:

• External reporting disclosures areunlikely to be comparable. Marketdiscipline depends on comparability ofdata, but firms are likely to interpret thedisclosure requirements differently andalso choose differently between

accounting and risk sources for thequantitative data.

• A major issue is the lack of precisionof some of the requirements and hencedoubt over interpretation. This is onereason that firms have to makechoices in many elements of thequantitative disclosures.

• A common view is that Pillar 3 is moreabout demonstrating that a firm hasenough available capital relative to Pillar1 requirements, rather than providingmeaningful risk data.

Firms recognise the need to explain clearlythe basis for disclosures, but thereappears to be little appetite for disclosingeconomic capital data alongside Pillar 1data and analysing the differences. At aminimum though, qualitative explanation ofthe differences between economic andregulatory capital will be needed.

FSA too flexible?

That the FSA is seen as relatively flexiblein its approach to Pillar 3 compared toother more prescriptive regulators is seenby some as a drawback; while othersremain content. To date, the FSA has notprovided any guidance or clarification on

definitions or interpretations of therequirements. Many firms worry that theFSA shows insufficient appreciation of thehuge data and management reportingimplications of making late changes tothe FSA’s Integrated Regulatory Reportingrequirements. Currently, the FSA expectsfirms to make Pillar 3 disclosures duringthe calendar year 2008 (or during 2007for the firms who adopt the Basel II rulesin 2007).

Pillar 3 projects are typically resourcedfrom risk, finance and investor relationsfunctions, but many firms have yet todecide who, ultimately, owns the data andtakes responsibility for it. But as with Pillar2, Pillar 3 seems to be breaking down thebarriers between risk and finance.

No ‘feel’ for the numbers

The main focus is on sourcing thequantitative data needed to comply, sincethere are substantial lead times involved.In contrast, qualitative disclosures areseen as comparatively quick to source.Yet there are major risks in disclosing datathat senior management does notunderstand. A significant proportion ofPillar 3 disclosures are not used internallyfor risk management, so management has

14 PricewaterhouseCoopers UK Retail Banking Insights November 2007

yet to develop a ‘feel’ for the numbers.For most firms there is also a mismatchbetween the Pillar 1 risk profile and theinternally determined risk profile due todifferences between regulatory andinternal methods.

The problem is exacerbated by uncertaintyover what is actually required to bedisclosed. And disclosures may well giverise to unexpected or difficult questionsfrom analysts or others, either about afirm’s own disclosure or in comparisonwith peers.

According to our information, firmsworry that:

• Complexity and comparabilityproblems in Pillar 3 disclosures willconfuse analysts.

• There is also a real risk to share prices ifthe data is not well understood.

• Some buy-side analysts are said torelish the prospect of more useful creditrisk disclosure. This means that Pillar 3disclosures will require carefulpresentation with a corresponding need‘to tell a coherent story’.

Understanding risk appetite

For most firms greater senior managementinvolvement in the Internal CapitalAdequacy Assessment Process (ICAAP)is a top priority. A firm’s score from theARROW process on Governance andOversight will be a key consideration forthe FSA in arriving at Individual CapitalGuidance that follows the SupervisoryReview and Evaluation Process (SREP).As part of meeting the use test, firmspresent identified a need to focus onplausible but severe stress events toengage senior management effectively.

There is broad agreement that riskappetite is an area of challenge.Executives outside the risk discipline needto understand the concept of risk appetite,specifically the totality of the firm’s riskuniverse, agreed limits and paths ofescalation. But as Pillar 2 is principles-based the FSA does not (nor is it likely to)give specific guidance on risk appetite nordetailed expectations to firms. It isparticularly important for management todemonstrate its ability to manage thebusiness under testing circumstances,particularly in managing reputation risk.

A firm’s score from the ARROW processon Governance and Oversight will be a keyconsideration for the FSA in arriving atIndividual Capital Guidance that followsthe Supervisory Review and EvaluationProcess (SREP).

A commonly held view among theforum participants is that the FSA’sdistinction between Pillar 1 and Pillar 2for stress testing remains unclear, as doits intentions for holistic stress testing.This is clearly an area where moredialogue would be beneficial.

Positive effects

Yet despite all the doubt and difficulty,Basel II is having positive effects.Enhanced stress testing is improvingdiscussion with and engagement of, seniormanagement and the business on riskissues. And it could be that the businesswill be less reluctant to embedstrengthened risk management if, as nowseems highly likely, external influences,such as investor requirements for moreinformation on risk, have an impact andanalysts latch on to the importance ofstrong risk management.

Basel II has forced banks to invest in abetter data environment and strengtheneddecision-making processes on risk.The result should be a better-controlled

operating environment, in turn favourablyinfluencing ARROW assessments. And, asPillar 3 encourages more visibility of risk,more organisations could come underpressure to explain how they manage it toinvestors, rating agencies and the media:no bad thing in the present circumstances.

PricewaterhouseCoopers hosts an annualBasel Executive Forum in the City for clients whoengage in roundtable discussions. The forum waschaired by Richard Barfield. The full report fromthe 2007 forum, ‘Getting the most out of your BaselII efforts’, is available at www.pwc.com/basel.

16 PricewaterhouseCoopers UK Retail Banking Insights November 2007

The US sub-prime story:Contagion or distraction?

What has been happening in the US mortgage space?

The state of the US consumer lending market is changing day by day. Driven primarilyby aggressive lending to sub-prime mortgage borrowers and investor demand formortgage-related debt, the US mortgage market is now undergoing a significantcorrection which has impacted investor appetite for all forms of debt. We consider belowwhether the US story could have a contagion effect for the UK with specific reference tounsecured lending.

As of writing, US delinquencies have continued to rise across US prime and non-primemortgage products, but are particularly pronounced in sub-prime. Delinquency rates onresidential lending are at their highest levels since 2001. In addition there is a significantamount of uncertainty driving capital markets perceptions and appetite for consumer-related debt. There are concerns about house price depreciation, the estimated $1trillionof Adjustable Rate Mortgages (ARM) resets coming over the next year and poor housingmarket statistics. Given that most forms of consumer lending in the US are fundedthrough the capital markets rather than by the balance sheets of the issuing bank orfinancial institution, this has resulted in both contraction and higher prices for almost allconsumer debt in the US today, including credit cards, auto loans and student lending.

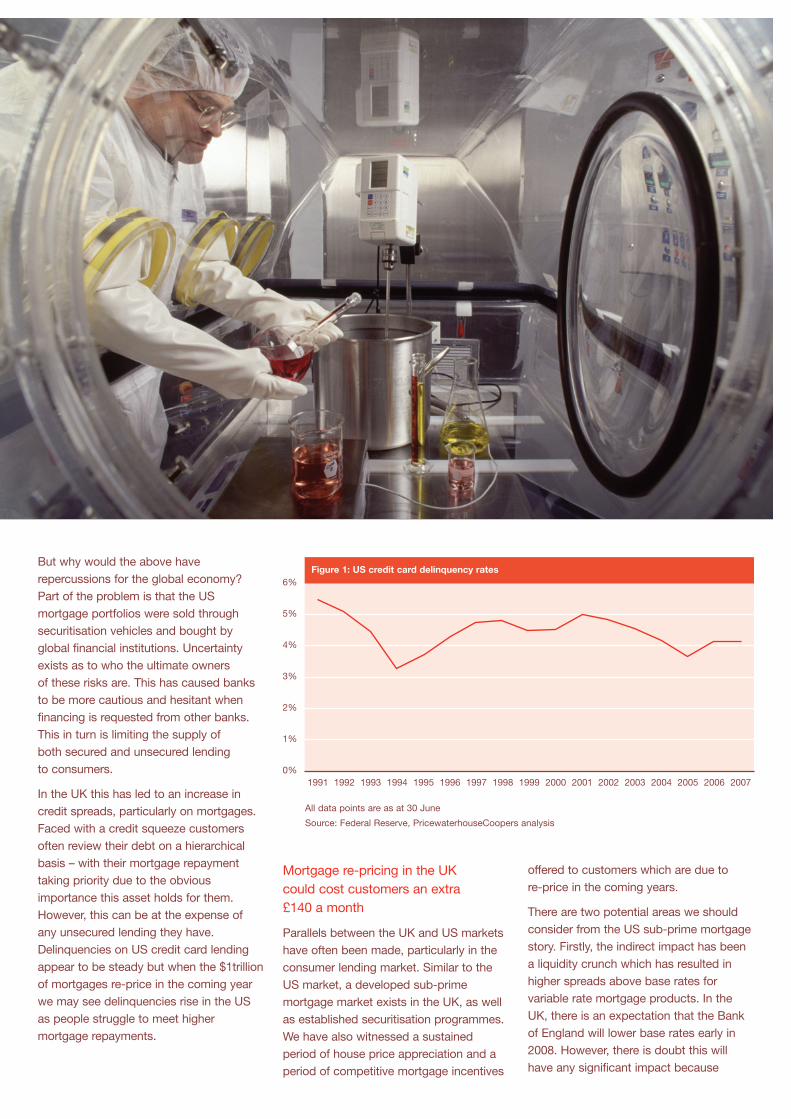

These concerns fuel speculation that consumer spending patterns are shifting enough toaffect the issuers of unsecured debt and also drive a broader downturn in the economy.Data from Q2 2007 indicates, however, that debt-servicing problems were mostlyconfined to mortgage-related products for the first half of the year. Credit carddelinquencies are still below levels witnessed during the early nineties, as highlighted bythe graph (see Figure 1), and in more recent times have been steadily falling between2001 and 2005. However, credit card delinquencies stopped falling in 2005 and betweenJune 2006 and June 2007 they have remained steady. As a result, US companies thatparticipate in the consumer lending market are on the one hand dealing with the fallouton their first and second mortgage portfolios and on the other reassessing theirunsecured products in terms of risk profile, pricing and profitability.

Contact us

Richard Thompson PartnerMarket & Value AdvisoryPricewaterhouseCoopers (UK)T: +44 (0)20 7213 1442E: [email protected]

Steve DaviesPartnerAssurancePricewaterhouseCoopers (US)T: +1 646 471 4185E: [email protected]

Robert BouldingAssistant DirectorMarket & Value AdvisoryPricewaterhouseCoopers (UK)T: +44 (0)20 7804 5236E: [email protected]

But why would the above haverepercussions for the global economy?Part of the problem is that the USmortgage portfolios were sold throughsecuritisation vehicles and bought byglobal financial institutions. Uncertaintyexists as to who the ultimate ownersof these risks are. This has caused banksto be more cautious and hesitant whenfinancing is requested from other banks.This in turn is limiting the supply ofboth secured and unsecured lendingto consumers.

In the UK this has led to an increase incredit spreads, particularly on mortgages.Faced with a credit squeeze customersoften review their debt on a hierarchicalbasis – with their mortgage repaymenttaking priority due to the obviousimportance this asset holds for them.However, this can be at the expense ofany unsecured lending they have.Delinquencies on US credit card lendingappear to be steady but when the $1trillionof mortgages re-price in the coming yearwe may see delinquencies rise in the USas people struggle to meet highermortgage repayments.

Mortgage re-pricing in the UKcould cost customers an extra£140 a month

Parallels between the UK and US marketshave often been made, particularly in theconsumer lending market. Similar to theUS market, a developed sub-primemortgage market exists in the UK, as wellas established securitisation programmes.We have also witnessed a sustainedperiod of house price appreciation and aperiod of competitive mortgage incentives

offered to customers which are due tore-price in the coming years.

There are two potential areas we shouldconsider from the US sub-prime mortgagestory. Firstly, the indirect impact has beena liquidity crunch which has resulted inhigher spreads above base rates forvariable rate mortgage products. In theUK, there is an expectation that the Bankof England will lower base rates early in2008. However, there is doubt this willhave any significant impact because

6%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

All data points are as at 30 June

Source: Federal Reserve, PricewaterhouseCoopers analysis

5%

4%

3%

2%

1%

0%

Figure 1: US credit card delinquency rates

18 PricewaterhouseCoopers UK Retail Banking Insights November 2007

variable rate margins above base rate haveincreased significantly in response to thecredit crisis. What is certain is that withconsumers facing likely increasedmortgage costs in the UK, there will beincreased pressure on their ability toservice unsecured lending repayments.In addition, from a lender’s perspectivethere may be mounting pressure to offloadconsumer finance portfolios if willingbuyers can be found. On first reflectionone may think that in this contextconsumer lending would be subduedfurther, however there are indicationsthat the opposite is true in the US.According to data published by theFederal Reserve, revolving credit usageincreased post the sub-prime crisis aspeople borrowed more to fund normalliving expenses, an unsustainable situationfor both consumer and lender. It is tooearly to tell whether we will witness thesame trend in the UK market but it clearlyhighlights some of the dilemmas facedby lenders in today’s market.

The second lesson we can learn from theUS market is in relation to the $1trillionof ARM mortgages (discounted) set tore-price in the coming year and the impact

on delinquencies. In Figure 2 we draw aparallel with the UK market and estimatethe potential impact on those customerscoming to the end of their discount orfixed rate period. The average mortgageloan over the last 18 months to June 2007has been around £120k.1 Fixed mortgagesoffered 18 months ago were on average138 basis points below the average June2007 Standard Variable Rate (SVR).For discounted mortgages the marginbetween the discount offer rate and theSVR rate in 2006 is less significant ataround 60 basis points. Whilst somepeople will re-mortgage and others mayhave made capital payments against theirmortgage, what the analysis shows is thatmortgage customers are likely to face asignificant increase in their monthlymortgage repayments (up to £140 on fixedrate mortgages taken out in January 2006).Over 1.4m fixed rate mortgages werecompleted in 2006 alone and a further276,000 of discounted mortgages. Whenthese re-price an individual’s ongoingcommitment to service mortgagerepayments may result in unsecuredlending arrears increasing or the use ofunsecured facilities to fund the additionalmortgage cost. It is not clear how

7%

Fixed Discount

Average rate January 2006 Re-priced average rate at June 2007

Note: Fixed rate re-pricing based on difference between average fixed rate January 2006 and SVR rate June2007; discount rate re-pricing based on average discount margin compared to SVR for every month in 2006

Source: Federal Reserve, PricewaterhouseCoopers analysis

6%

5%

4%

3%

2%

1%

0%

1 Council of Mortgage Lenders Banksearch RegulatedMortgage Survey – 04.09.07

£140 monthlyrepaymentimpact £60 monthly

repaymentimpact

Figure 2: Estimated impact of mortgage incentive products after re-pricing

significant this will be compared to theUS. However, when the $1trillion of ARMmortgages re-price over the next year inthe US, UK lenders should watch with acareful eye (see Figure 2).

Other contagion effects facedby lenders

Queues of people outside every NorthernRock branch in the UK highlights animportant behavioural impact – the impactof consumer confidence and adversepublicity. Consumer confidence has beenhit by market turbulence in the UKeconomy. This fear could result in lowerspending on the high street and increasedsavings. Faced with the Northern Rockexample, banks will look to close theirfunding dependency on the credit marketsand this could result in higher savingsrates offered to customers and furthersubdue consumer spending.

We are now in a period of economicuncertainty and the degree to which thiswill hit retail banks and their customers issubject to debate. Keeping a watchful eyeon the US mortgage market and its impacton unsecured delinquency performancecould become increasingly important inpredicting and being prepared for whatcould happen in the UK market.

This article has been re-produced from‘Precious Plastic 2008’, PricewaterhouseCoopers.For more information visitwww.pwc.com/uk/preciousplastic

20 PricewaterhouseCoopers UK Retail Banking Insights November 2007

Customer profitability versusproduct profitability: The impactof economic regulation

What is happening?

In recent years the banking sector has seen increasing scrutiny from competitionauthorities assessing the reasonableness of prices and practices. This has been underboth consumer and competition law and at the national and EC level. It is fair to say thatbanking is well and truly in the ‘cross-hairs’ of the competition authorities.

The UK has been at the forefront of this trend. The first foray by the UK competitionauthorities into this sector in 20021 led to the imposition of an onerous price controlremedy. Since then, the UK authorities have challenged credit card interchange fees,credit card default fees, store cards, unauthorised overdraft charges (UOCs), home credit,payment protection insurance (PPI) and the general state of competition in both currentaccounts and credit cards.

There is a clear domino effect going on: in 2005 the Office of Fair Trading (OFT) wieldedthe Unfair Terms in Consumer Contracts Act in anger at credit card default fees, resultingin these fees being cut in half.2 The OFT has since looked to ‘cut and paste’ thisapproach to regulate unauthorised overdraft charges: but mindful of potential knock-oneffects, in particular the risk of ending ‘free banking’, it has widened this inquiry to look atcompetition in current accounts (an area already criticised by the CompetitionCommission (CC) in respect of Northern Ireland).3 The fairness of UOCs is now also beingthrashed out in court. Meanwhile, the increase in APRs following the cut in credit carddefault fees has led to a further complaint to the OFT by Which?, bemoaning a generallack of competition in the provision of credit cards.4

Why is this happening?

There is undoubtedly a range of factors contributing to this trend. What is clear is thatthe consumer bodies (Which? and Citizens Advice) are increasingly influential in shapingthe debate and the OFT in the UK is pursuing an increasingly consumerist agenda.This has been encouraged by the Enterprise Act. For some commentators, banks enjoya quasi-utility status (everyone has to have a bank account), enjoy low switching inproducts like current accounts, and serve consumers who are not altogether savvy whenit comes to financial products.

Contact us

Tim OgierPartnerMarket & Value AdvisoryPricewaterhouseCoopers (UK)T: +44 (0)20 7804 5207E: [email protected]

Liam ColleyDirectorMarket & Value AdvisoryPricewaterhouseCoopers (UK)T: +44 (0)20 7804 5316E: [email protected]

1 ‘The supply of banking services by clearing banks tosmall and medium-sized enterprises’, CompetitionCommission – 14.03.02.

2 ‘Calculating fair default charges in credit cardcontracts, a statement of the OFT’s position’, OFT842 – 05.04.06.

3 ‘Personal current account banking services inNorthern Ireland market investigation’, CompetitionCommission – 15.07.07.

4 ‘Which? ICM Supercomplaint’, Which? – 30.03.07.

The apparent high profits of UK banks inrecent years are also a factor. However,the true profitability of banking products isvery difficult to identify due to theprevalence of intangible assets andsignificant common costs in retail banking.Often the authorities have taken an overlysuperficial approach – for example theOFT recently sought to infer PPIprofitability using comparisons of claimsratios with products like pet insurance.5

More fundamentally, the banking businessmodel is complex and interrelated, anddoes not lend itself easily to scrutiny ofa single price. For example, some mayregard UOCs as ‘poor value’ but lowerUOCs would surely lead to increased baddebts, a cost that all non-defaultingcustomers must ultimately cover, andlower average deposits, the source ofcheap finance which makes the banks’loan products so competitive.

The banks have not always explained thiskind of thing very forcefully or in aconsistent manner. In fairness, the bankscould be forgiven for not always knowingwhat to aim at, as often the authorities’position has been quite muddled. Therecent review of SME terms concluded

that price regulation was no longerrequired as competition had improved, butin truth price regulation would havehampered this process. The likely increasein APRs following the cut in credit carddefault fees was welcomed by the OFT as‘providing greater transparency’ but hasbeen criticised by the consumer bodiesand led to further complaints.6

What impact is this having and whatshould the banks be doing?

Assessing the impact of these trends isalso difficult. Perhaps the most damagingaspect of these inquiries relates to the badpress that they generate; for example takeup rates on PPI have fallen dramaticallysince the launch of the Citizens Advicecomplaint, yet the CC has only really justbegun its review and the banks have onlynow started to engage properly in thedebate. More proactive engagement earlieron could have helped address thiscustomer holdback. The reality is that thebanks’ engagement strategies have variedwidely and often been fragmented alongproduct lines, reflecting perhaps thehitherto piecemeal nature of the regulatorycreep the sector has witnessed and afeeling that there may be bigger threats to

manage (e.g. the ‘back book’ risk).7

Going forward, the banks may do well tolearn from other sectors that experienceregular interaction with economicregulators, such as telecoms, whereregulatory strategy has greater priority,is more centrally co-ordinated and hashigh board-level sponsorship.

The financial impact of interventions willvary considerably according to the natureof the product and depending on thecommercial position of individual players.Some interventions may allow banks totweak other aspects of their products.For certain we have seen evidence of a‘waterbed’ effect, where direct interventionin one area of pricing has led to othersgoing up. For example, cuts in interchangefees and credit card default fees have ledto significant changes in APRs, especiallyfor cash withdrawals. This reflects the factthat if price cuts reduce the value ofcustomers, firms will compete for them

5 ‘Payment protection insurance: Report on themarket study and proposed decision to make amarket investigation reference’, OFT869,(paragraph 6.49 et seq) – 19.10.06.

6 See footnote 4. 7 i.e. the risk of having to reimburse customers for

historic transactions.

22 PricewaterhouseCoopers UK Retail Banking Insights November 2007

less aggressively. However, as interventionthreatens more core areas of bank activity,such as current accounts and personallending, damage limitation strategiesmay be harder to achieve. Figure 1 showsthe implications if reduced profits onPPI were to be fully recovered throughloan APRs (assuming no effect onloan take-up).

What is clear is that an across-the-board,rebalancing would not be achievable formaterial cuts in PPI profits. To minimisethe impact of further interventions, thebanks will need to target any rebalancing,whilst being mindful of how individualcustomer groups might respond andbased on an understanding of whichcustomers they really need to keep andwhich ones they can afford to lose. Thefocus therefore will be more on customerprofitability as opposed to productprofitability. This will require a move totracking customer profitability more closelyand developing more sophisticatedsystems to allow more complex chargingstructures to reduce the impact ontotal profits.

A similar story is likely to emerge withrespect to any interventions on UOCs.The banks could not afford to imposeannual fees on all accounts as noteveryone would follow, exposing thebanks to churn risk for their bestcustomers. Rather, the banks needto assess quickly the underlyingprofitability of different customer groupsin a reduced UOC world to understandwhich customers they must keep andthose they can risk losing. This wouldimply developing a range of currentaccount products as a coherentcompetitive response to intervention.

The challenge, therefore, is that inaddition to managing the regulatoryprocess better, the banks need tounderstand, and respond to, the changingeconomics of their customers in a moresophisticated manner.

16%

0% 20% 40% 60%

Erosion of PPI Income

Average

Source: PricewaterhouseCoopers analysis, 2007

AP

R

80% 100%

14%

12%

10%

8%

6%

Figure 1: ‘Waterbed’ effect APR range

The member firms of the PricewaterhouseCoopers network provide industry-focused assurance, tax and advisory services to build public trust and enhance value for its clients and their stakeholders.More than 146,000 people in 150 countries across our network share their thinking, experience and solutions to develop fresh perspectives and practical advice.

This report is produced by experts in their particular field at PricewaterhouseCoopers, to review important issues affecting the financial services industry. It has been prepared for general guidance onmatters of interest only, and is not intended to provide specific advice on any matter, nor is it intended to be comprehensive. No representation or warranty (express or implied) is given as to the accuracyor completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers firms do not accept or assume any liability, responsibility or duty of care forany consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

If specific advice is required, or if you wish to receive further information on any matters referred to in this paper, please speak with your usual contact at PricewaterhouseCoopers or those listed inthis publication.

www.pwc.com© 2007 PricewaterhouseCoopers. All rights reserved. ‘PricewaterhouseCoopers’ refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate andindependent legal entity.