uk space agency - the space economy and role of the uk space agency

TRANSCRIPT

gov.uk/ukspaceagency

The space economy and the role of the UK Space Agency

Northern Space Consortium,Liverpool, 18 March 2016

Elizabeth SeamanUK Space Agency

What is the Space Economy?

OECD Handbook on Measuring the Space Economy, 2012

Space sector– Not one space activity but many across different fields of science

and technology, including astronomy (including astrophysics, space science), aerospace engineering, applied mechanics, atmospheric sciences.

Space economy– Wider than the space sector– Can be defined in many ways such as by products (e.g. satellites);

services (image delivery, broadcasting); programmatic objectives (human spaceflight, robotic exploration)…

– upstream space industry (infrastructure and technology),– downstream space industry (direct space services) – the wider space economy (space-enabled value-added

applications)

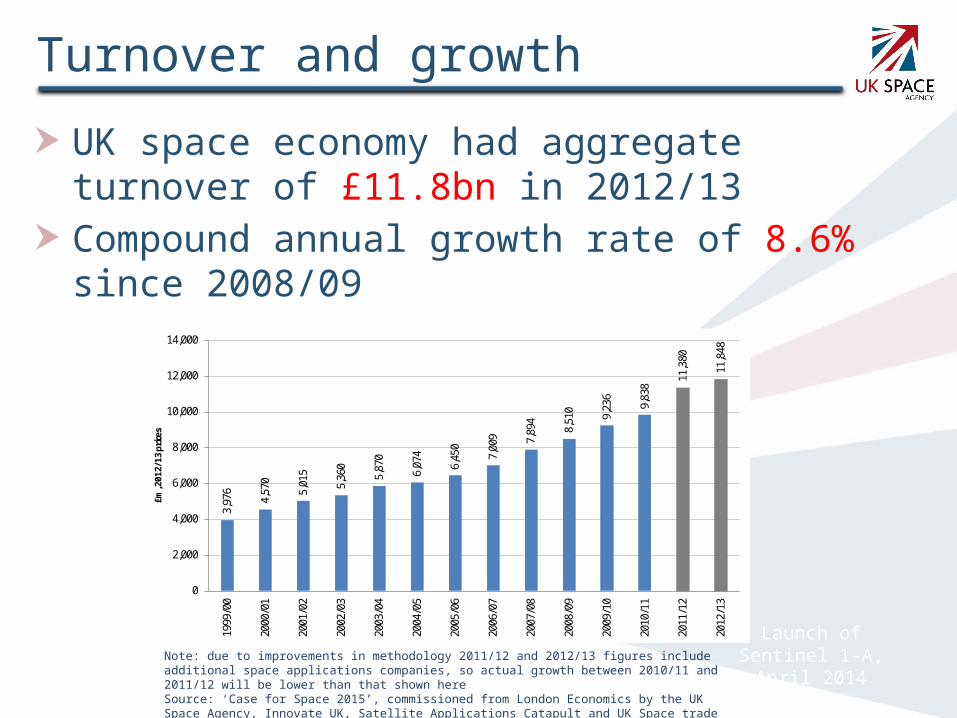

Turnover and growth

UK space economy had aggregate turnover of £11.8bn in 2012/13Compound annual growth rate of 8.6% since 2008/09

3,97

6

4,57

0

5,01

5

5,36

0

5,87

0

6,07

4

6,45

0

7,00

9 7,89

4

8,51

0 9,23

6

9,83

8

11,3

80

11,8

48

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

£m, 2

012/

13 p

rices

Note: due to improvements in methodology 2011/12 and 2012/13 figures include additional space applications companies, so actual growth between 2010/11 and 2011/12 will be lower than that shown hereSource: ‘Case for Space 2015’, commissioned from London Economics by the UK Space Agency, Innovate UK, Satellite Applications Catapult and UK Space trade association

Launch of Sentinel 1-A, April 2014

ExportsUK space exports in 2012/13 were estimated at £3.6bnSurvey data suggest 31% of turnover from the UK space economy is generated from exports, more than twice the export share of the UK as a whole (15%)When big broadcasters (BSkyB) are not counted, this rises to 66% UK-built telecommunication satellites account for 25% of the world marketThe UK has particular strengths in satellite communications, and in manufacturing small satellites

UK economy average Space economy Space economy (excluding BSkyB)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Export Intensity - % of turnover from

exports

Source: ONS input-output tables; ‘Case for Space 2015’

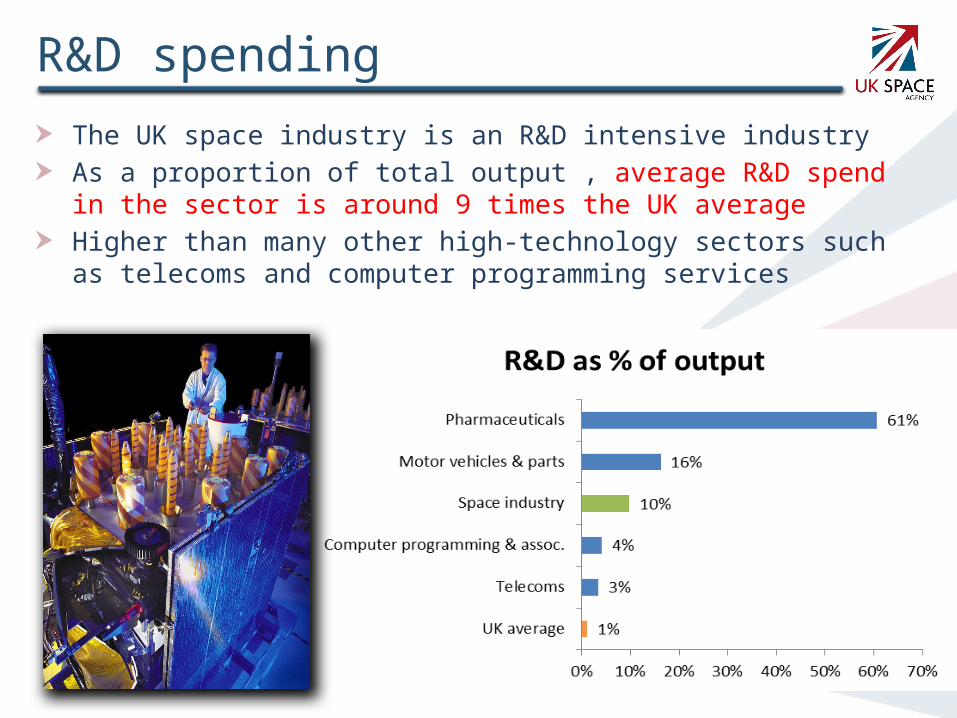

R&D spendingThe UK space industry is an R&D intensive industryAs a proportion of total output , average R&D spend in the sector is around 9 times the UK averageHigher than many other high-technology sectors such as telecoms and computer programming services

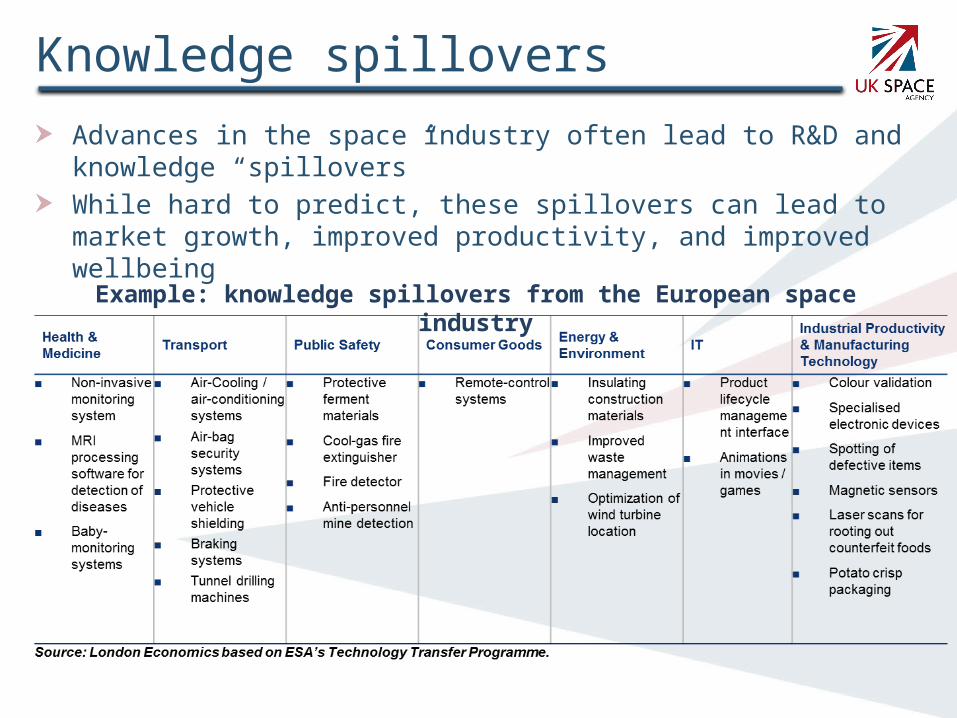

Knowledge spilloversAdvances in the space industry often lead to R&D and knowledge “spillovers”While hard to predict, these spillovers can lead to market growth, improved productivity, and improved wellbeing

Example: knowledge spillovers from the European space industry

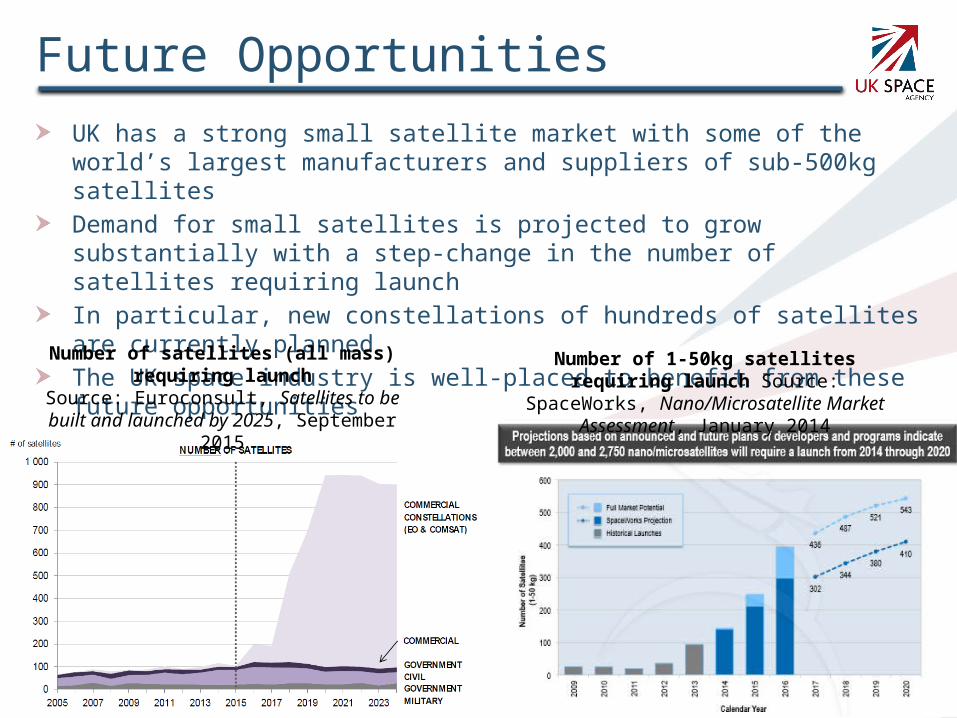

Future OpportunitiesUK has a strong small satellite market with some of the world’s largest manufacturers and suppliers of sub-500kg satellitesDemand for small satellites is projected to grow substantially with a step-change in the number of satellites requiring launchIn particular, new constellations of hundreds of satellites are currently plannedThe UK space industry is well-placed to benefit from these future opportunities

Number of satellites (all mass) requiring launchSource: Euroconsult, Satellites to be built and

launched by 2025, September 2015

Number of 1-50kg satellites requiring launch Source: SpaceWorks, Nano/Microsatellite Market

Assessment, January 2014

The UK Space Agency leads the civil space programme– Policy advice to Ministers– Regulation– Investment – ~80 staff (Swindon, London and UK Space Gateway)

Is an executive agency sponsored by Department for Business, Innovation & Skills (BIS) and was established in 2011Responsible for:– all strategic decisions on the UK civil space programme – provision of a clear, single voice for UK space ambitions

Role of the UK Space Agency

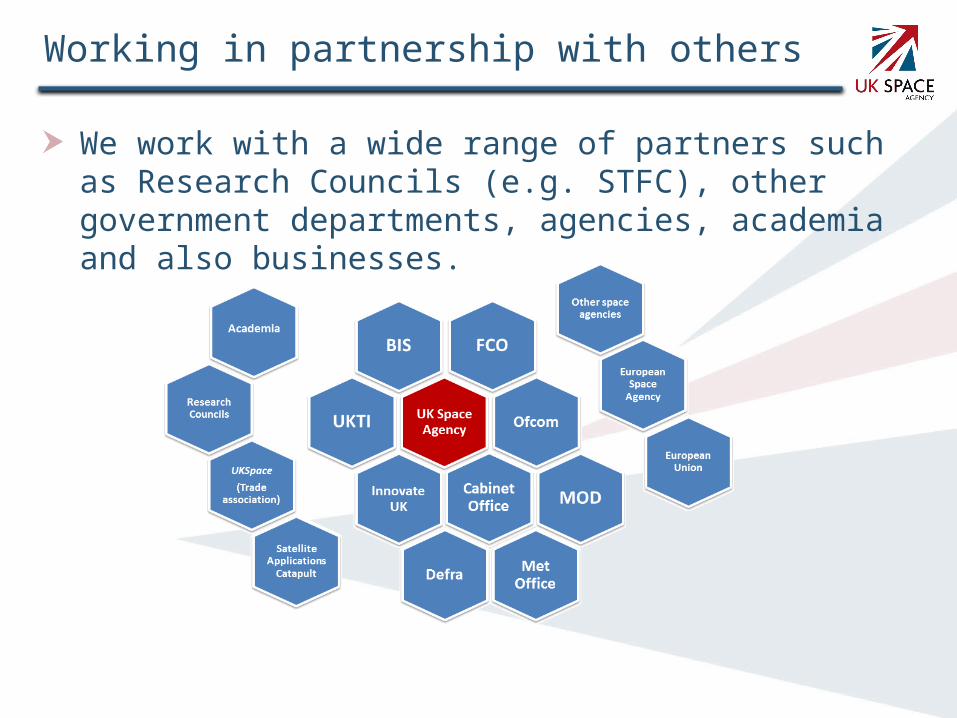

Working in partnership with others

We work with a wide range of partners such as Research Councils (e.g. STFC), other government departments, agencies, academia and also businesses.

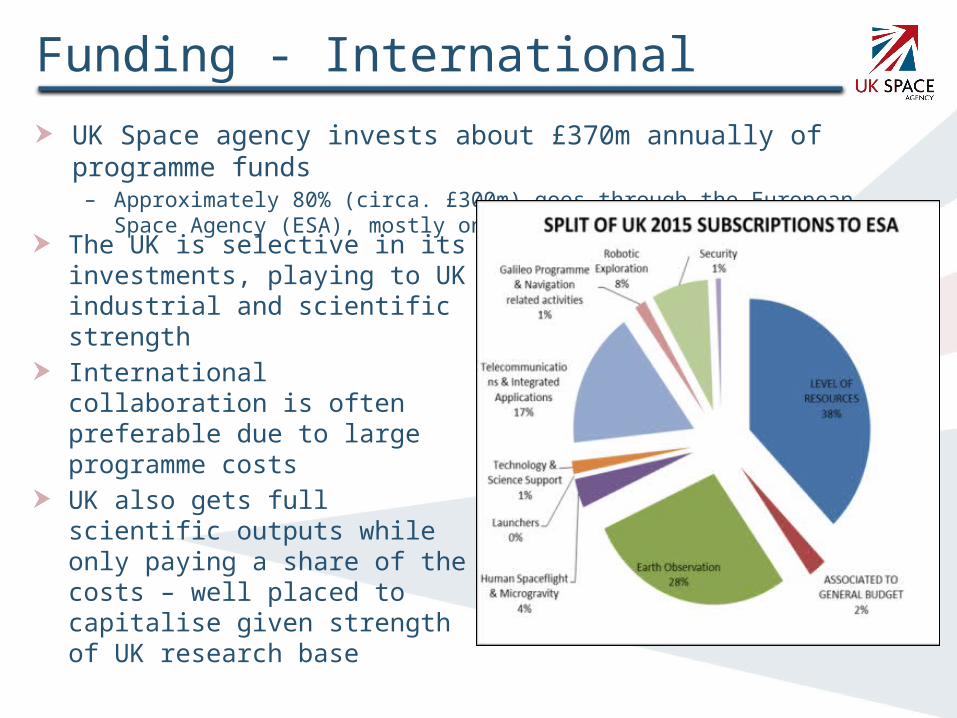

Funding - InternationalUK Space agency invests about £370m annually of programme funds

– Approximately 80% (circa. £300m) goes through the European Space Agency (ESA), mostly on science programmes

The UK is selective in its investments, playing to UK industrial and scientific strengthInternational collaboration is often preferable due to large programme costsUK also gets full scientific outputs while only paying a share of the costs – well placed to capitalise given strength of UK research base

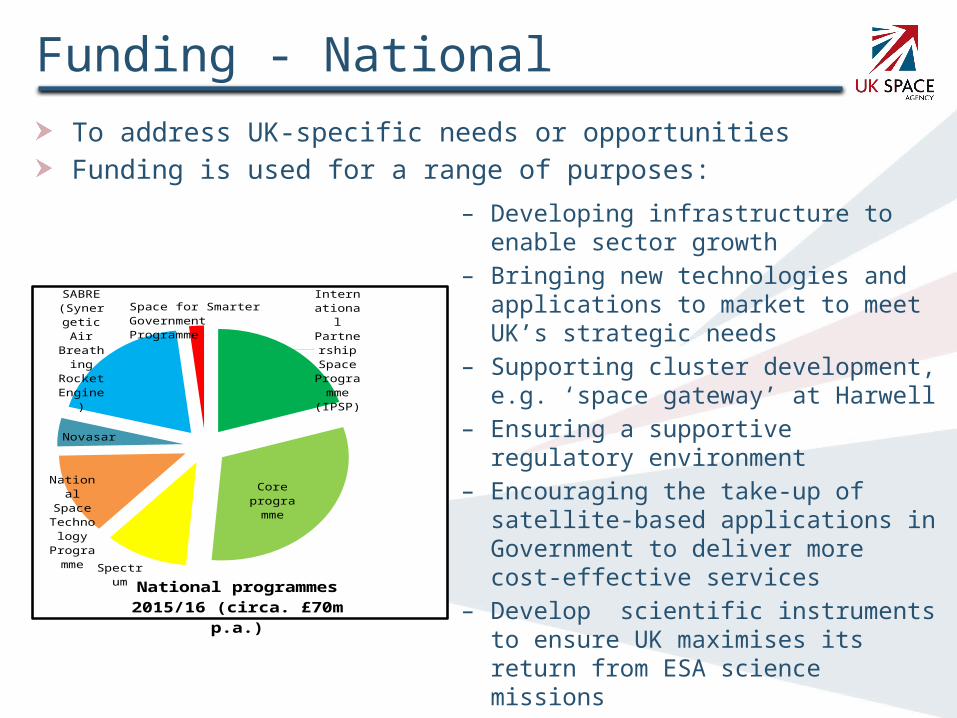

Funding - NationalTo address UK-specific needs or opportunities Funding is used for a range of purposes:

Inter-national

Part-nership Space Pro-

gramme (IPSP)

Core pro-

gramme

Spectrum

National Space Tech-

nology Pro-

gramme

Novasar

SABRE (Syner-getic Air

Breathing Rocket Engine)

Space for Smarter Govern-ment Programme

National programmes 2015/16 (circa. £70m p.a.)

– Developing infrastructure to enable sector growth

– Bringing new technologies and applications to market to meet UK’s strategic needs

– Supporting cluster development, e.g. ‘space gateway’ at Harwell

– Ensuring a supportive regulatory environment

– Encouraging the take-up of satellite-based applications in Government to deliver more cost-effective services

– Develop scientific instruments to ensure UK maximises its return from ESA science missions

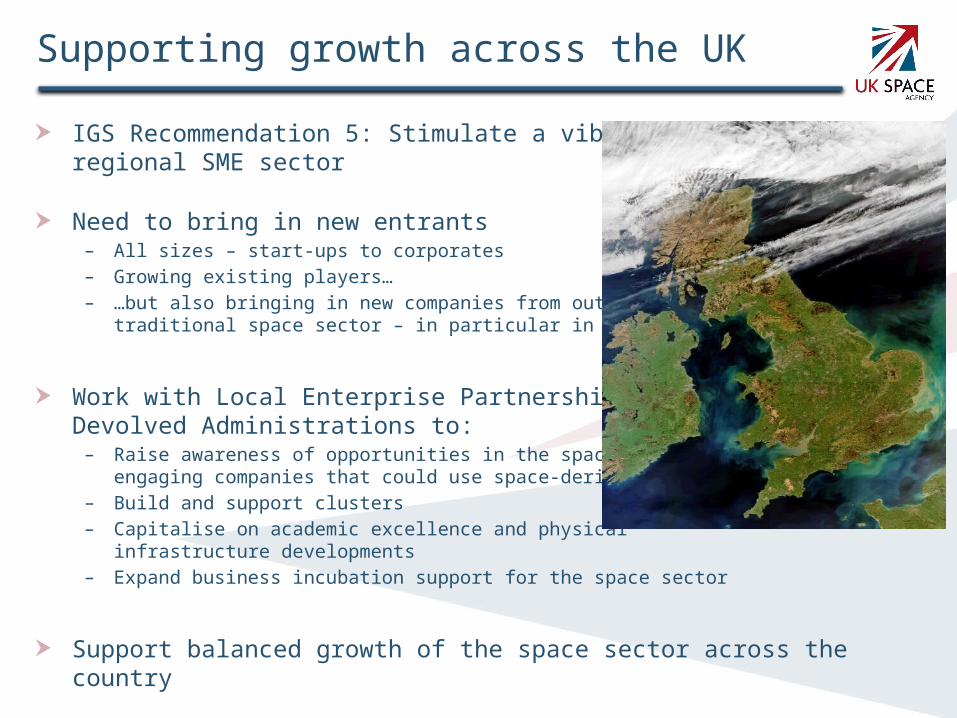

IGS Recommendation 5: Stimulate a vibrantregional SME sector

Need to bring in new entrants – All sizes – start-ups to corporates– Growing existing players…– …but also bringing in new companies from outside the

traditional space sector – in particular in the downstream

Work with Local Enterprise Partnerships and Devolved Administrations to:

– Raise awareness of opportunities in the space sector – engaging companies that could use space-derived data

– Build and support clusters– Capitalise on academic excellence and physical

infrastructure developments– Expand business incubation support for the space sector

Support balanced growth of the space sector across the country

Supporting growth across the UK

The Vision: UK Space Gateway at Harwell

Harwell is critical for the UK’s space sector….

Direct employment: – ~200 space-sector workers in 2010– ~600 in 2016– Targeting 1000+ by 2020, 5000+ by 2030 (plus a further

5000 in Oxfordshire)

A vibrant international community– Expertise and national facilities– Collaborative working: industry, academia and public sector– From start-ups to corporate HQs

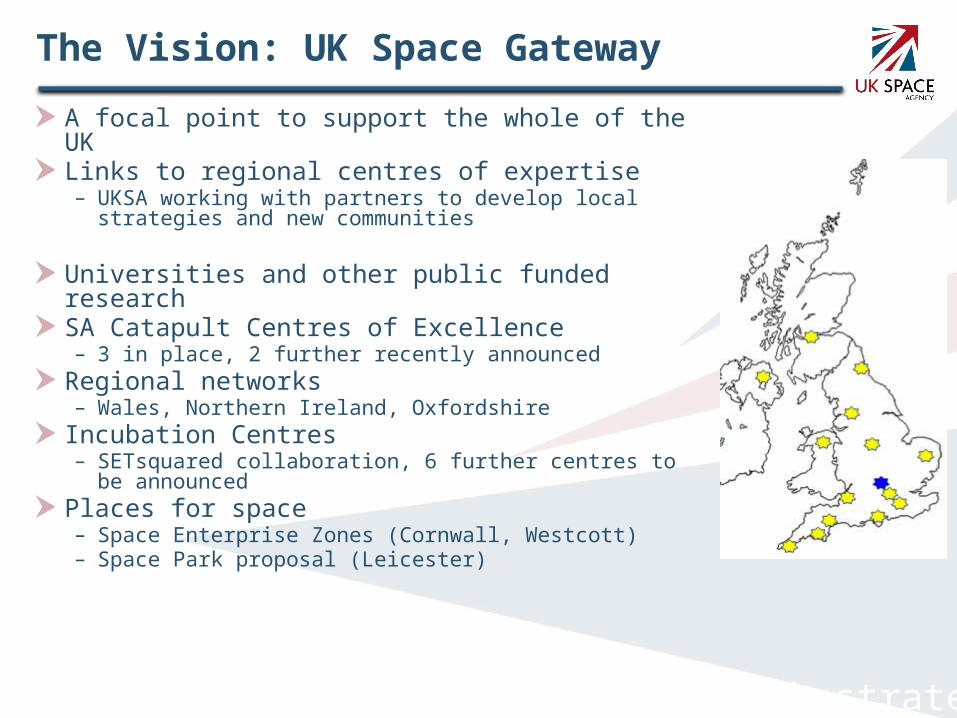

The Vision: UK Space Gateway

A focal point to support the whole of the UKLinks to regional centres of expertise– UKSA working with partners to develop local strategies

and new communities

Universities and other public funded researchSA Catapult Centres of Excellence– 3 in place, 2 further recently announced

Regional networks– Wales, Northern Ireland, Oxfordshire

Incubation Centres– SETsquared collaboration, 6 further centres to be

announcedPlaces for space– Space Enterprise Zones (Cornwall, Westcott)– Space Park proposal (Leicester)

A key vehicle to deliver the UK’s growth strategy

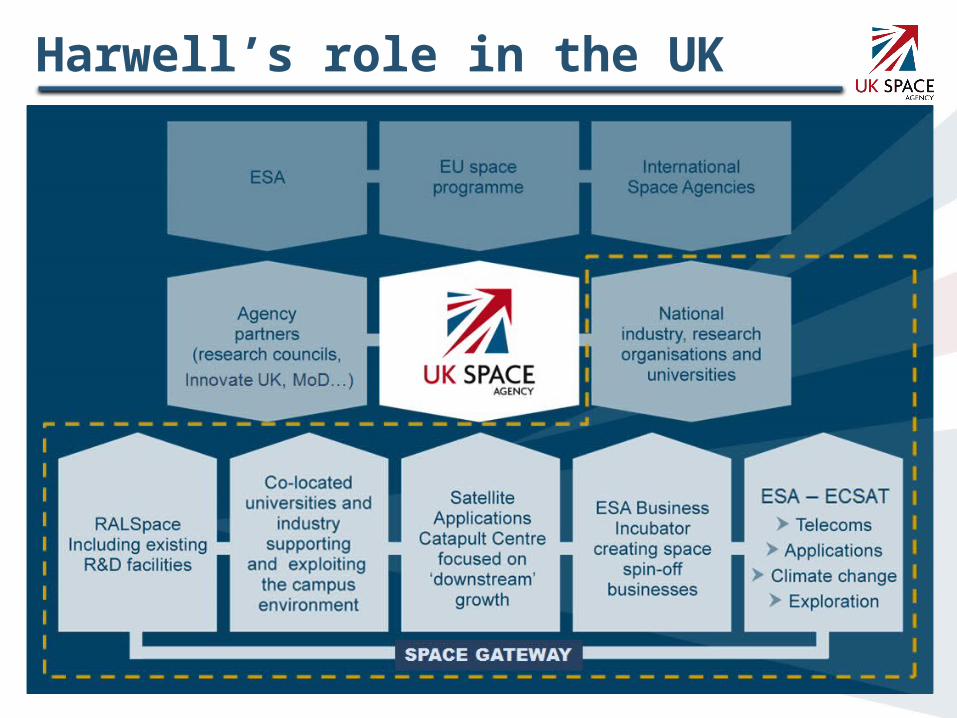

Harwell’s role in the UK

More information

UK Space Agency web site: https://www.gov.uk/government/organisations/uk-space-agency

UK Space Agency blog: https://space.blog.gov.uk/

@spacegovuk on TwitterSpacegovuk on YouTubeSpacegovuk on Flickr