ukti market research report final - amazon s3€¦ · china lifesciences market research report...

TRANSCRIPT

China LifeSciences MarketResearch Report

October, 2009

2

Scope of the report

Pharma products

Pharma products refer to those used in the prevention, treatment and diagnosis of human diseases and/or intended for the regulation of the physiological functions of human beings. In this report, pharma products include active pharmaceutical ingredients (APIs), small molecule medicines, and traditional Chinese medicines (TCMs).

Biotech products

Biotech products refer to the medical products which are produced using biotechnology. In this report, biotech products include plasma derived products, vaccines, and other protein derived products such as antibodies, nucleic acids for therapeutic use.

Medical devices

Medical devices cover a wide range of health or medical instruments, apparatus, appliances, materials used in the treatment, mitigation, diagnosis or prevention of a disease or abnormal physical condition.

This report aims to provide an overview of the Chinese LifeSciences market from both the product and service perspectives. To remain consistent with the common terminology used by the UK Trade & Investment (UKTI), the product group is subcategorized by pharma, biotech products, and medical devices. In parallel, the service group is to focus on the private health insurance and private healthcare provision. The detailed definitions are illustrated as follows:

Please note, the exchange rate applied in this report is 1 British pounds (£) = 11 Chinese Yuan RMB

Structure of the report

► According to the UKTI LifeSciences definitions, the report is divided into Part A and Part B, as illustrated below.

Part BPart A

LifeSciences market in China

Services

Private healthcare provision

Private health insurance

Products

Pharma Biotech Medical devices

IVD Diagnostic imaging equipments

Dental products Others

3

Part A

Key competitor analysis for the UK LifeSciences marketing strategy in China

Table of contents

34III. UK’s position in China

36 – 42IV. Investment structures and tax considerationsA. Options of different investment structuresB. Tax consequences and entity functionsC. Business registration procedures

23 - 32II. Key competitor analysis

6 - 21I. Chinese LifeSciences market overview

Page No.Section

I. Chinese LifeSciences market overview

Chinese LifeSciences market size (£ billion), 2006-2010

Note: CAGR stands for “Compound Annual Growth Rate”; E stands for “Estimation”

► China is among the largest high growth LifeSciences markets in the world

Source: Espicom Business Intelligence reports, 2007-2009; Datamonitor, 2008; Ernst & Young analysis

9.9% CAGR

Market size (2006) £ 21.7 billion Market size (2010 E) £ 30.7 billion

Medical device 11%

Biotech 23%

Pharmaceuticals 66%

Medical device10%

Biotech27%

Pharmaceuticals63%

6

I. Chinese LifeSciences market overview

► China is forecast to become the world’s fifth largest pharmaceutical market by 2010

Source: Espicom Business Intelligence reports, 2009; Southern Medicine Economic Institute, 2008; China Medical Statistics data, 2008

Size2010 ESize2005Size2000Rank

9.2 Brazil6.0 Spain2.6 Spain109.8 Spain6.1 Canada2.8 Canada9

10.4 Canada6.1 Brazil3.7 Brazil814.1 Italy8.6 China4.2 China714.7 UK9.2 Italy6.7 Italy614.7 China9.8 UK6.7 UK517.2 France12.9 France10.4 France422.7 Germany14.7 Germany10.4 Germany349.7 Japan39.9 Japan35.6 Japan2

285.9 US160.7 US92.0 US1

Top 10 pharmaceutical market in the world (£ billion)

Note: E stands for “Estimation”

7

I. Chinese LifeSciences market overview

0

5

10

15

20

25

2006 2007 2008 2009 E 2010 E 2011 E

► The Chinese pharmaceutical market is one of the largest in the world with a high growth rate

Source: Espicom Business Intelligence reports, 2009; Southern Medicine Economic Institute (SMEI), 2008; China Medical Statistics data, 2008

► Features of the pharmaceutical market in China

► Generic products dominate the market, 97% of the total market value in 2008, i.e. £ 15 billion, are generic products

► Highly fragmented with large number of small size companies► 4,500 pharmaceutical manufacturers

► 70% of companies have annual revenues lower than £ 30 million (for comparison, GlaxoSmithKline’s annual revenue in 2008 is £ 24 billion)

► Domestic companies are growing rapidly in size

► Nine of the top 10 manufacturers are Chinese companies

► Multinational companies are operating at a higher profit margin (2008 data). In 2008, the revenue growth of multinational pharmaceutical companies is between 20% and 30%, higher than most domestic companies

CAGR=8.6 %

Pharmaceutical market size in China (£ billion) Pharmaceutical market by sub-sector (%)

Note: E stands for “Estimation”

Traditional Chinesemedicines

34%

Active pharmaceuticalingredients

29%

Small moleculepharmaceutical

products37%

8

I. Chinese LifeSciences market overview

► The biotech sector has embraced strong growth in China

Source: Espicom Business Intelligence reports, 2009; Ernst & Young analysis

0123456789

2006 2007 2008 2009 E 2010 E 2011 E

CAGR=13.7 %

Biotech market size in China (£ billion)

► The biotech sector has been identified as a strategic sector in theChinese government’s 11th Five-year Plan for 2006-2010

► Manufacturing and marketing of blood products are highly regulated

► Foreign investment in blood product manufacturing is restricted

► Licenses to manufacture blood products have been granted to 33 domestic companies

► Blood products are in short supply in China. Due to the short supply in plasma, prices for human albumin increased by 40% in 2007

► Blood products with an only exception of human albumin are prohibited from import

► China is the largest vaccine producer in the world

► 29 domestic companies can produce 49 types of vaccines for the prevention of 26 infectious diseases. The total annual output has exceeded one billion doses

► In September 2009, China approved the clinical use of the A/H1N1influenza vaccines produced by a domestic company Sinovac, making it the first company in the world to be granted with a production license

Note: E stands for “Estimation”

9

I. Chinese LifeSciences market overview

► Trade of LifeSciences products remains strong

Import and export (£ billion, 2006 – 2008)

► In 2008, China’s import and export of LifeSciences products are both increasing with a 26.14% annual growth rate to reach £ 29.9 billion by the year end

► Top three export markets: US, Japan and India

► Top three API exporters: Zhejiang Medicine Co., Ltd, Zhejiang New Harmony Unit Company Ltd, Weisheng Pharmaceutical Co., Ltd

► Top three formulation exporters: Pfizer (China), Jiangsu Jiangshan Pharma, North China Pharmaceutical Group

Source: China Chamber of Commerce for Import & Export of Medicines & Health Products (CCMHPIE) data, 2009

Export of LifeSciences products (£ billion, 2008)

Activepharmaceutical

ingredient55%Others

24%

Medical dressing10%

Diagnosticimaging products

11%

Import Export

CAGR = 23.4%

CAGR = 20.1%

0

5

10

15

20

25

2006 2007 2008 2006 2007 2008

BiopharmaceuticalproductsMedical device

Pharmaceuticalproducts

10

I. Chinese LifeSciences market overview

► To effectively enter the LifeSciences market in China, companies should think broadly about the customers and their needs

Source: Ministry of Health data, 2009; Morgan Stanley Research, 2008; Institute of Southern Medical Economy Research of SFDA data, 2008

► Population: 1.33 billion ► Population growth: 0.8% (1996-2006)► Life expectancy

► Male 72 years old► Female 75 years old

► Aging population: 9.4% population older than 65 years

► Top three chronic diseases (2008)► Hypertension (5.5%)► Gastroenteritis (1.1%)► Diabetes mellitus (1.1%)

► Top three malignant neoplasm (2004-2005, per 100,000 persons)► Lung cancer (30.6)► Liver cancer (26.1)► Stomach cancer (24.5)

► Top three diseases leading to hospitalization (2008)► Respiratory system diseases► Digestive system diseases► Injury, poisoning and external causes

Major customers for LifeSciences products:

Patients and general public

Important business partners:Distribution companies

Access to LifeSciences products:Hospitals and retail pharmacies

► Distributors► The annual sales of the distribution

industry is expected to be £ 63.2 billion in 2010, representing a two-year CAGR of 21.7%

► China has nearly 20,000 pharmaceutical distribution companies. The industry is undergoing consolidation, with top 20 distributors accounted for more than 40% (£ 18.4 billion) of the total sales in the market in 2008. The largest distributors are:Sinopharm, Shanghai Pharma, Jiuzhoutong, Guangzhou Pharma, Nanjing Pharma

► Hospitals► China has 19,712 hospitals, including

► General hospitals 13,119► Traditional Chinese Medicine

hospitals 2,688► Specialized hosptials 3,437► Others 468

► China has 1.71 million registered doctors, 1.65 million registered nurses, 0.3 million pharmacists, and 0.2 million laboratory technicians

► The total hospital sales of LifeSciences products was £ 27.5 billion in 2008

► Retail pharmacies► China has about 365,000 retail

pharmacies and 35.4% of the retail pharmacies are chain stores

► The total sales of LifeSciences products in retail pharmacy was £ 11.8 billion in 2008

11

I. Chinese LifeSciences market overview

► As the end-customer, the needs of patients and general public play the most important roles in determining drug sales growth

4,848.9 3,886.9 2,989.8 2,663.7 Total

639.1 506.7 394.1 340.9 Others

410.5 315.2 214.6 183.0 Nervous system drug

527.1 446.9 372.8 320.5 Hematological system drugs

610.0 490.8 377.4 332.3 Digestive and metabolic drugs

648.5 519.5 411.7 435.4 Cardiovascular drugs

824.2 648.0 494.9 368.1 Anti-tumor immune adjusting reagents

1189.5 959.8 724.3 683.5 Anti-infection drugs

2008200720062005

Source: Institute of Southern Medical Economy Research of SFDA data, 2008

Hospital sales of pharmaceutical products

(£ million, 2005 – 2008)► Anti-infection drugs remain the most needed

in hospitals► The percentage of anti-tumor drugs and

cardiovascular drugs are increasing in recent years due to the increase of related diseases

Hospital sales of pharmaceutical products in 2008 (%)

Anti-infection drugs25%

Anti-tumor immuneadjusting reagents

17%

Cardiovascular drugs13%

Digestive and metabolicdrugs13%

Hematological systemdrugs11%

Nervous system drugs8%

Others13%

12

I. Chinese LifeSciences market overview

Timeline

—— 2003

—— 1998

—— 1997

—— 1994

—— 1992

—— 1985

—— Post 1949

► China launched the rural cooperative medical care program in 2003, under which rural residents and governments jointly contributed to a cooperative fund. Participants could reclaim some of the costs of hospital care. The rate of reimbursement varied according to the ailment and the actual cost of medical expenses incurred

► China began to establish a medical insurance system. The basic insurance system aimed to cover all employers and employees in urban areas, including employees and retirees of all government agencies, public institutions, enterprises, mass organizations and private non-enterprise units

► The State Council defined medicine as a public welfare sector, changing the previous concept that it was a commercial product

► The State Council launched a pilot scheme in two cities to establish medical insurance systems covering urban employees

► Special medical services, including better nursing and more comfortable wards, emerged as market forces increasing demand

► China launched market-oriented reforms. Public hospitals were encouraged to increase their own income with the aim of mobilizing medical workers and improving hospital efficiency. Public organizations were also encouraged to run medical institutions in order to make services more accessible. Government investment in public hospitals gradually fell

► After the founding of the People's Republic of China in 1949, government covered more than 90 percent of medical expenses for urban residents. Meanwhile, rural people had access to subsidized health clinics run by barefoot doctors. The primitive services, essentially free, played a role in doubling the country's average life expectancy from 35 years in 1949 to 68 years in 1978

Milestone

Source: People's daily website data

► The development and reform of the healthcare system in China is a gradual process

13

I. Chinese LifeSciences market overview

Timeline

► A report by the Development Research Centre under the State Council harshly criticized health sector reforms and concluded that reforms over the past decade had been basically unsuccessful. Statistics showed that only 20 percent of medical fees were covered by the patients themselves in 1978. The percentage rose to 52 percent in 2005

—— 2005

—— August 2009

—— July 2009

—— April 2009

—— October 2008

—— February 2008

—— 2007

—— 2006

► The Ministry of Health and other eight government agencies released Opinions on the establishment of the national essential drug system, officially launched the structure of the national essential drug system

► The General Office of the State Council released Work Plan for 2009 on five key aspects of healthcare reform, in which 10 tasks were proposed to propel the reform from five key aspects in three years

► The reform plan was officially published for implementation

► The reform plan was released for public debate. More than 27,000 comments and suggestions were offered in the month-long debate

► Initial draft of the reform plan was developed

► China introduced a comprehensive medical insurance program that would cover all urban citizens, including children and the unemployed. The medical insurance system for urban employees covered 180 million Chinese people by 2007

► The State Council set up a joint working team consisting of experts from 16 departments to draft a new health reform plan

Milestone

Source: People's daily website data

► The development and reform of the healthcare system in China is a gradual process (cont’d)

14

15

I. Chinese LifeSciences market overview

► On June 11 2009, the China Insurance Regulatory Commission (CIRC) issued a document promoting the role of insurance companies in China's health care reform:► Insurance companies are encouraged to develop a greater variety of health

insurance products in disease insurance, disability income insurance, long-term care insurance and medical liability insurance

► Closer cooperation between insurance companies and hospitals areencouraged to help insurance companies develop better health insurance products

► Insurance companies should help the government in the implementation of the basic medical insurance program, which will help the government reduce administrative costs and limit unreasonable medical expenses

► The Chinese private health insurance market will continue to grow, providing opportunities for foreign insurance companies

► The Chinese private health insurance market has been growing at an annual rate of nearly 30% since 2002. Nearly 100 insurance companies across China currently provide some forms of private medical insurance products

► The Chinese private health insurance coverage has a very low penetration rate and only accounts for 2% of total health expenditure compared with 20% globally

► The Chinese private health insurance market is dominated by domestic insurance companies, with Ping An and China Life take up 45% and 31% market share, respectively

► American International Group’s (AIG) is the largest foreign provider of private health insurance services with a 3% market share as of 2005

► Foreign insurance companies are only allowed to enter the market through joint venture, subject to a cap of no more than 50% equity capital, posing challenges of partnering with less experienced domestic partners

► The number of foreign insurance companies is expected to increase to 60, taking up around 8% of the whole market by 2012

Private health insurance market overview

Source: Ministry of Health data, 2009; China Insurance Regulatory Commission (CIRC) data, 2009; ISI Emerging Markets data, 2009

117 million815 million200 million

Covered population as of 2008

► Voluntary medical insurance scheme for urban residents other than employees

► Voluntary medical insurance scheme for rural residents

► Mandatory medical insurance scheme for employees

Features200720031998Effective year

Basic Medical Insurance Scheme for Urban Residents

New Rural Cooperative

Medical Insurance Scheme

Basic Medical Insurance Scheme

for Urban Employees

Basic medical insurance system in China

I. Chinese LifeSciences market overview

► The Chinese medical service sector is in an transitional stage, developing from a system primarily based on public hospital treatments into a comprehensive healthcare system, including private sector players. Healthcare provisions other than public or state-owned are collectively coined Private Healthcare Provisions

136,934

129,544

304

3,1981

3,887

Private owned

64,11768,064Total

44,57210,957Others

92038,636Health centres

12,4648,598Community health service centres11396Sanatorium

6,0489,777Hospitals

Society funded

Government fundedInstitutions

Number of medical institutions in 2008

Source: Ministry of Health data, 2008; Ernst & Young analysis

► Increasing number of patients are treated in private hospitals► 2.85 million patients in 2007 vs. 1.5 million in 2003

► The majority of Private healthcare provision are small in size► Only 7% of the Private healthcare provision have assets higher than £ 2.7 million

► China will encourage the development of private hospitals, as indicated in its healthcare reform plan

16

I. Chinese LifeSciences market overview

► China is among the most attractive destinations for outsourcing research services

Source: EMIS data, 2008

► In 2009, PPD company in America announced to expand its global central laboratory to China

► In 2008, Quintiles Transnational Corp announced to move and expand its global central laboratory in Beijing

► In 2007, MDS Pharma Services moved its central laboratory to Beijing

► In 2007, Covance completed its central laboratory in Shanghai

Representative CRO companies

Representative Chinese companies► WuXi AppTec► Excel► Venture Pharm CRO

► Contract Research Organization Service Alliance (CROSA)

► Alliance of Bio-Box Outsourcing (ABO)► Zhongguancun CRO Alliance► Northern Antibody Alliance

CRO Alliances

Chinese CRO companies

Chinese Contract Research Organization

(CRO) Market (£ million) ► The growth rate of the Chinese CRO market was 52% in 2006 and 38% in 2007, respectively

► The growth will continue at CAGR of 33% (estimated) over the next five years to reach £ 485 million in 2012

► By 2012, Chinese CROs will account for an estimated 2.3% of the global CRO market

0

50

100

150

200

250

300

2006 2007 2008 2009 E 2010 ENote: E stands for “Estimation”

17

I. Chinese LifeSciences market overview

► A network of industrial parks have been established to provide a supportive environment of the LifeSciences industry. Parks with strong focus on the LifeSciences companies include:

► Beijing – Beijing Zhongguancun LifeSciences Park; Beijing Economic Technological Development Area► Shanghai – State Biotech & Pharmaceutical Industrial Base (Shanghai)

► Xi’an – State High & New Technological Development Area (Xi’an)

► Changsha- Changsha High & New Technological Development Area

► Taizhou – China Medical City

► The industrial parks provide preferential policies to Chinese and foreign small and medium sized companies. The representative policies include

► Providing funding support (up to 30% subsidies) to high-tech start-ups which own intellectual property rights

► Providing preferential Customs policy. For instance, tariffs and import-related Value-Added-Tax (VAT) can be exempted for some companies which have to import equipments, accessories, and spare parts as these items can not be obtained in China

► Providing preferential tax policy. For instance, the 15% corporate income tax can be exempted from local income tax for the first 5 years

► Some parks provide office facilities free of charge or with discounted rental fees for defined period of time

18

I. Chinese LifeSciences market overview

► The Chinese government is strengthening the protection of Intellectual Property (IP) rights, aiming to encourage innovation and long term development of the LifeSciences industry

► China’s patent law has been updated three times since it was issued in 1984

► The IP rights protection is available through patents and various regulatory mechanisms

► Invention patents are the most relevant to pharmaceutical and biotechnology industries. An application for aninvention patent is examined for subject matter, novelty, inventiveness, sufficiency of disclosure, and practical applicability

► Administrative Protection of Pharmaceuticals gives protection to pharmaceutical products that were excluded from patent protection before 1993

► Some foreign IP owners prefer the administrative enforcement to the legal proceedings. However, the legal proceeding is highly recommended by the government because it is the legitimate proceeding

► To avoid IP disputes in China, foreign companies should► Understand the Chinese patent laws & regulations and pay special attention to the differences in regulatory

requirements

► Understand the local patent regulations & requirements of the invested locations/cities

► Understand the regulations of the specific area like science and technology parks, if deciding to do business in such areas

► Foreign investors should understand and work with the evolving pharmaceutical regulatory framework in China

Source: Interview with Huake Pharmaceutical Intellectual Property Consultative Centre; Ernst & Young analysis19

I. Chinese LifeSciences market overview

► The early registration of Trade Marks and patents is critical in China. The registration process should be in place even before an actual product is introduced to the market

► A successful protection strategy should take a multidisciplinary approach and cover four perspectives:► Trade Mark protection

► Patent protection

► Customs protection

► Administrative protection► Trade Mark registration is essential. As under Chinese law, any pharmaceutical product intended for human

consumption should bear a Trade Mark

► Trade Marks protection is an important approach for foreign LifeSciences companies

► An effective IP protection strategy includes:

► File Trade Marks immediately, “intent to use” is a sufficient ground for registration

► File patents promptly, so infringement can be prevented

► Register copyright, as this provides proof of creation

► The following precautions should be taken from the time of market entry:

► Closely monitor business partners, subcontractors, and licenses

► Conduct due diligence & exercise audit rights

► Sign non-disclosure and confidentiality agreements with employees

Source: Ernst & Young analysis 20

I. Chinese LifeSciences market overview

Source: http://www.ipo.gov.uk; http://www.cipa.org.uk

► UK companies can approach the Intellectual Property Office (IPO) for IP related questions and services. IPO is the UK official government body responsible for IP rights. It provides patent database search and IP dispute mediator services to UK companies upon request.

► The IPO signed two IP agreements with China’s State Intellectual Property Office in February 2009. The agreements which cover patents and trade marks aimed to enhance bilateral cooperation and improve commercial trade of both countries through exchange of information and shared capacity building activities relating to IP and trade marks.

► A Intellectual Property Right (IPR) China Helpdesk was launched in May 2008. The helpdesk answers China IPR questions from across Europe, produces businesses tools for developing IPR value and managing risk in China, delivers workshops to small and medium sized enterprises on the China IPR issues

► The IPO released a China-An Enforcement Roadmap in April 2007. The booklet, compiled for companies currently or intending to operation in China, was written to provide guidance on the Chinese Intellectual Property protection and enforcement system.

► A patent attorney obtains and enforces intellectual property rights on behalf of either individual inventors or organizations

► The Chartered Institute of Patent Attorneys (CIPA) is the professional and examining body for patent attorneys (also known as patent agents) in the UK.

► CIPA was founded in 1882 and was incorporated by Royal Charter in 1891.

► It represents virtually all the 1,750 registered patent attorneys in the UK whether they practise in industry or in private practice. Total membership is over 3,000 and includes trainee patent attorneys and other professionals with an interest in intellectual property (patents, trade marks, designs and copyright).

21

Table of contents

34III. UK’s position in China

36 – 42IV. Investment structures and tax considerationsA. Options of different investment structuresB. Tax consequences and entity functionsC. Business registration procedures

23 - 32II. Key competitor analysis

6 - 21I. Chinese LifeSciences market overview

Page No.Section

II. Key competitor analysis - United States

► The US has a good environment for entrepreneurial activities andhas comparative advantages in services, intellectual property and “creative” industries, with significant centres of technological innovation (for example, the biomedical cluster in Silicon Valley takes a leading position in LifeSciences manufacturing and research)

Business environment

► Pharmaceutical market is the largest in the world, worth £ 192.4 billion in 2008

► The world’s largest market for LifeSciences products, including pharmaceuticals, Biotech and Medical device

► Headquarters of the world’s largest pharmaceutical (Pfizer), biotechnology (Amgen) and Medical devices companies (GE)

► One of the major exporters of Medical device as well as medicines

Market size

► Worker productivity in the US is higher than in most of other developed states, according to the International Labor Organization. This is primarily because US workers work longer hours than their counterparts in other developed countries

► With a vey high literacy rate (at 98%), the US has a fairly goodeducation system with several top international universities

► According to US Department of Labor, in 2008, the productivity per person employed (GDP per person employed ) in US is £ 59,571, ranked the first among France, Switzerland, UK and Germany

Talent pipeline

► The US has often been the origin of new drivers of economic growth booms, it is the world's largest economy with a high research and development spend

Finance

► United States’ key strengths in the LifeSciences industry

23

II. Key competitor analysis - United States

► www.export.gov/china/policyadd/jcct.asp?dName=policyadd

► The 19th U.S. – China Joint Commission on Commerce and Trade (JCCT) was held on September 16, 2008 to discuss important issues on intellectual property (IP) rights, pharmaceuticals and Medical device and trade relationship improvement

Department of Commercewww.commerce.gov

► www.nist.gov/tip/► Technology Innovation Program (TIP): the goal of the TIP is to benefit the U.S. economy by cost-sharing research with industry to foster new, innovative technologies, and LifeSciences is among TIP’s major focuses

National Institute of Standards and Technology, U.S. Department of Commerce www.nist.gov

► nccam.nih.gov/► NIH is active in conducting traditional Chinese medicine research through its National Centre for Complementary and Alternative Medicine (NCCAM), which collaborated with China closely

National Institutes of Health (NIH)www.nih.gov/

Related marketing collateralsDevelopment/marketing strategies or activitiesGovernment agencies and organizations

► www.ita.doc.gov/td/health/► OMMEI is dedicated to enhancing the global competitiveness of the U.S. health industry, expanding its market access, and increasing exports

► Participating in several initiatives such as JCCT, and the most updated information about LifeSciences industry on JCCT can be found at www.ita.doc.gov/td/health/

Office of Microelectronics, Medical Equipment & Instrumentation (OMMEI) Medical Equipment, International Trade Administration, Department of Commercewww.ita.doc.gov/mdequip

Supporting government agencies

► United States’ LifeSciences development/marketing strategies in China

24

II. Key competitor analysis - United States

► www.chinaids.org.cn/n1971/index.html

► globalhealth.gov/news/agreements/ia121107a.html

► Since 2002, HHS’ Centres for Disease Control and Prevention (CDC) has maintained a Global AIDS Program (GAP) China Office to assist the Government of China by strengthening strategic information efforts, including surveillance, and building laboratory capacity. HHS/CDC also supports voluntary counseling and testing (VCT), behavior change, and care and treatment activities and programs

► HHS and China signed several Memoranda of Understandings in recent years, covering a wide range of health issues such as improving the safety of drugs and Medical device and establishing a collaborative program to combat infectious diseases in China

U.S. Department of Health & Human Services (HHS)www.hhs.gov

Related marketing collateralsDevelopment/marketing strategies or activitiesGovernment agencies and organizations

Supporting government agencies

► United States’ LifeSciences development/marketing strategies in China (cont’d)

25

II. Key competitor analysis - Germany

► There are 19 “bioregions” throughout the whole Germany. These regions provide platforms for LifeSciences development and facilitate the interaction between corporate and institutional resources

Business environment

► The largest European single market for pharmaceuticals and the third largest market for pharmaceuticals behind the USA and Japan

► The largest single market for Biotech within the European Union and the second worldwide behind the USA

► The largest European single market for Medical device and the third largest in the world

Market size

► Germany has 343 universities and over 330 research institutes who cooperate with companies to discover and bring new LifeSciences products to market

► Germany’s globally leading position in international research is traditionally ensured by independent research organizations like the well-known Max-Planck, Fraunhofer and Leibniz-Societies

Talent pipeline

► Government support ranges from cash incentives for the reimbursement of direct investment costs to incentives for labor and R&D

► The government has developed the "High-Tech Strategy" and provides a funding of £ 1.18 billion to support innovation in biotechnology, pharmaceuticals, and Medical device sectors

► Biotech industry attracted the highest value of venture capital investments in Europe in 2007

Finance

► Germany’s key strengths in the LifeSciences industry

Source: Federal Ministry of Education and Research (BMBF) website data; Ernst & Young analysis26

II. Key competitor analysis - Germany

► SPECTARIS website► SPECTARIS is the German industry association for the high-tech medium-sized business sector and representative body in the areas of medical technology, optical technologies and analytical, biological, laboratory, and ophthalmic devices

► Organizes trade fairs and projects on medical technologies between China and Germany periodically (detailed information can be found at www.spectaris.de/english/index.htm)

SPECTARIS - German Industry Association for Optical, Medical, and MechatronicalTechnologies www.spectaris.de/english/index.htm

Related marketing collateralsDevelopment/marketing strategies or activitiesGovernment agencies and organizations

► Bio Deutschland website► BIO Deutschland acts as the single voice of the German biotechnology industry in society and politics

► Organizes trade delegations, working groups, bi-lateral meetings on biotechnology with Chinese counterparties

BIO Deutschlandwww.biodeutschland.de

► www.hightech-strategie.de/en/682.php

► High-Tech Strategy for Germany: the strategy has placed a great emphasis on health research and biotechnology as Germany’s lead industries in the future

► Strategy for the Internationalization of Science, Research and Development: improve Germany's role as a centre of science and innovation with the help of cross-border cooperation

► Scientific and technological cooperation (STC) between Germany and China: emphasize on project/institutional cooperation. The Joint STC Commission is also active in biotechnology

Federal Ministry of Education and Research (BMBF)www.bmbf.de

Supporting government agencies

► Germany’s LifeSciences development/marketing strategies in China

27

II. Key competitor analysis - Germany

www.achemasia.de/►The 8th International Exhibition-Congress on Chemical Engineering and Biotechnology will be held in China in 2010

DECHEMA (Society for Chemical Engineering and Biotechnology) www.dechema.de

Related marketing collateralsDevelopment/marketing strategies or activitiesGovernment agencies and organizations

China portal : www.china.mpg.de/english/index.html

► Has a long established relationship with the Chinese Academy of Sciences

► Has set up a China portal website at www.china.mpg.de/english/index.html

Max Planck Societywww.mpg.de/english/portal/index.html

Chinese-German Centre:

www.sinogermanscience.org.cn

►The DFG and its partner, the National Natural Science Foundation of China (NSFC), opened a Chinese-German Centre for Science Promotion in Beijing in October 2000

►Chinese-German Centre is active in funding research projects and facilitating cooperation among researchers between Germany and China. LifeSciences project is one of the Centre’s key emphases

German Research Foundation (DFG)www.dfg.de

Beijing office: www.helmholtz.cn/►Germany’s largest scientific organization, with 28,000 employees in 16 research centres and an annual budget of approximately £ 2.46 billion

►The Association has set up a Beijing office in China in 2004 to expand strategic and long-term scientific cooperation with China in six key research fields, including LifeSciences

The Helmholtz Association www.helmholtz.de/en

►R&D Associations

► Germany’s LifeSciences development/marketing strategies in China (cont’d)

28

II. Key competitor analysis - France

► A research tax credit is available to help companies launch research and development projects in France. The credit is capped at £ 14 million per company per year, and is calculated on research expenditures posted by a company in a calendar year. It’s one of the most advantageous tax credit in the Europe Union (EU), which will be further improved.

Business environment

► France has one of the world’s highest level of per capita drug expenditure, which is estimated to have reached £ 481 in 2008

► Globally, France ranks the fifth-largest Medical device market, behind the US, Japan, Germany and the UK. In 2008, the value of the market was estimated at between £ 4.9 and £ 5.5 billion

► France has the largest hospital network in Europe

Market size

► The pharmaceutical industry in France employs more than 100,000 people, including 22,000 focusing on R&D

► The French academic sector is involved in the training of talents, with 1,000 doctors in LifeSciences s every year, along with some 2,000 engineers in biosciences, 1,000 masters degrees and 8,600 pharmacists, veterinaries and physicians

► Some of the most reputable LifeSciences research centres in the world are located in France, such as INSERM (national institute for medical research), the research foundations Institute Pasteur (microbiology and vaccines) and Institute Curie (cancer)

Talent pipeline

► Among France’s high-tech clusters, there are eight zones dedicated specifically to pharmaceutical and biopharmaceutical. The Frenchgovernment planed to invest £ 1.3 billion from 2006 to 2008 into its 71 designated clusters, including eight pharmaceutical clusters.

Finance

► France’s key strengths in the LifeSciences industry

29

II. Key competitor analysis - France

• www.ambafrance-cn.org/第三轮-法国医学日-巡回活动.html?lang=zh

► The French Embassy in China has launched a “French medical science day”, which aims at promoting the recent development of medical sciences in France as well as strengthening the medical cooperation between China and France

► In April 2009, the third round of itineration was held in Shanghai, Wuhan and Guangzhou with broad support from local governments in thesecities

The French embassy in Chinawww.ambafrance-cn.org

► Programme Sino-Français de Recherches Avancées (PRA) is a bilateral cooperation plan between Ministry of Science and Technology of China and France, which aims to strengthen and promote Sino-France cooperation in basic research and hi-technology. LifeSciences is also a major focus of PRA

► “Sino-France LifeSciences and genome research centre” was established in April 2002. The centre was located in Ruijin Hospital, Shanghai and aimed to promote the cooperation in LifeSciences research between China and France

► Chinese and French governments collaborated to set up several Sino-France joint laboratories in China to promote and deepen the research cooperation between the two countries, especially in the LifeSciences sector

• www.sante-sports.gouv.fr/

► China’s Ministry of Health and French Ministry of Health, Youth and Sport signed a letter of intent on Sino-France healthcare cooperation in August 2008

► A Sino-France healthcare training centre was set up in Beijing on July 2009 to promote and facilitate Sino-France healthcare cooperation in the future

French Ministry of Health, Youth and Sport www.sante-sports.gouv.fr/

Related marketing collaterals

Development/marketing strategies or activitiesGovernment agencies and organizations

Supporting government agencies

► France’s LifeSciences development/marketing strategies in China

30

II. Key competitor analysis - Switzerland

► Switzerland has a long track record of democratic stability, coupled with neutrality in international affairs

► Switzerland has a favorable corporate tax environment, compared with other European countries. In 2007, the average tax rate as a percentage of corporate income in Switzerland is about 21.3%, the lowest among US, UK, France, and Germany

► It takes about six months to register a new pharmaceutical product in Switzerland, one of the fastest in the world

Business environment

► One of the most sophisticated and well funded pharmaceutical andhealthcare markets in Europe, worth around £ 3.3 billion in 2008 and a per capita expenditure of £ 431.3

► There are five high technology clusters in LifeSciences s in Switzerland, namely, BioAlps, BioValley, Medizinal-Cluster Bern, Zurich Mednet, Biopolo Ticino, all of which have a high concentration of LifeSciences companies and intensive links between firms and research institutions

Market size

► The domestic manufacturing sector is led by Switzerland’s two major multinationals, Novartis and Roche, which accounted for 60% of domestic production and represent the country’s traditional strengths in innovative pharmaceutical development

► Switzerland is a country with intensive research activities. It spends almost 3% of its GDP on research and development

Talent pipeline

► Switzerland is well-placed to further develop its role as an international financial centre and to take advantage of the globalization of financial and banking services

► Switzerland has low interest rates, which in turn reduces overall financial costs. In recent years, the average spread in the money market and capital market interest rates in Swiss Francs and Euros ranged between 1.5 to 2 percent

Finance

Source: Great Zurich Area website data, 2009

► Switzerland’s key strengths in the LifeSciences industry

31

II. Key competitor analysis - Switzerland

► www.global.ethz.ch/stc/china

► www.swissnexshanghai.org

Bilateral Science and Technology program:► The Federal Council Dispatch on the Promotion of

Education, Research and Innovation for 2008-2011 mentions China as a potential partner with whom Switzerland would like to establish broader and deeper bilateral research cooperation ties

► The Sino-Swiss Science and Technology Cooperation (SSSTC) program was established in 2003, after the signing of a memorandum of understanding (MOU) between the Swiss State Secretariat for Education and Research (SER) and the Chinese Ministry of Science and Technology (MOST). One of SSSTC’s major focus is LifeSciences s and biotechnology

► The new phase of the SSSTC (2008-2011) intends to reach beyond the MOST and to include the Ministry of Education (MOE) and Chinese Academy of Science (CAS) in the program as well

► Swissnex Shanghai:► Swissnex Shanghai is an initiative of the Swiss State

Secretariat for Education and Research of the Ministry of Home Affairs and the Swiss Ministry of Foreign Affairs. The goal is to fully exploit the potential of cooperation between Switzerland and China in the fields of higher education, research, technology, innovation and culture and to promote Switzerland as one of the leading countries in those domains. LifeSciences is among the top agenda of Swissnex Shanghai

State Secretariat for Education and Research SER, Federal Department of Home Affairs FDHAwww.sbf.admin.ch/htm/sbf/sbf_en.html

Related marketing collateralsDevelopment/marketing strategies or activitiesGovernment agencies and organizations

Supporting government agencies

► Switzerland’s LifeSciences development/marketing strategies in China

32

Table of contents

34III. UK’s position in China

36 – 42IV. Investment structures and tax considerationsA. Options of different investment structuresB. Tax consequences and entity functionsC. Business registration procedures

23 - 32II. Key competitor analysis

6 - 21I. Chinese LifeSciences market overview

Page No.Section

III. UK’s position in China

Source: Interviewee’s opinion on UK’s LifeSciences in China

► A number of interviews were conducted to understand UK’s position in China

► Strengths ► High quality products & strong brand► Strong R&D capacity► UK government’s support to companies► Friendly diplomatic relationship between UK and the Chinese government

► Opportunities ► The Chinese healthcare reform spurs the growth of the LifeSciences market► China is a high growth emerging market for LifeSciences products and services► China provides a comparatively low cost talent pool► Various level of governments provide support in science and technology parks

► Challenges ► Some UK companies are less aggressive in the Chinese market comparing to the US and

German companies► Some companies lack understanding of the Chinese culture and business handlings► Some companies are overly conservative in exploring business opportunities in China

34

Table of contents

34III. UK’s position in China

36 – 42IV. Investment structures and tax considerationsA. Options of different investment structuresB. Tax consequences and entity functionsC. Business registration procedures

23 - 32II. Key competitor analysis

6 - 21I. Chinese LifeSciences market overview

Page No.Section

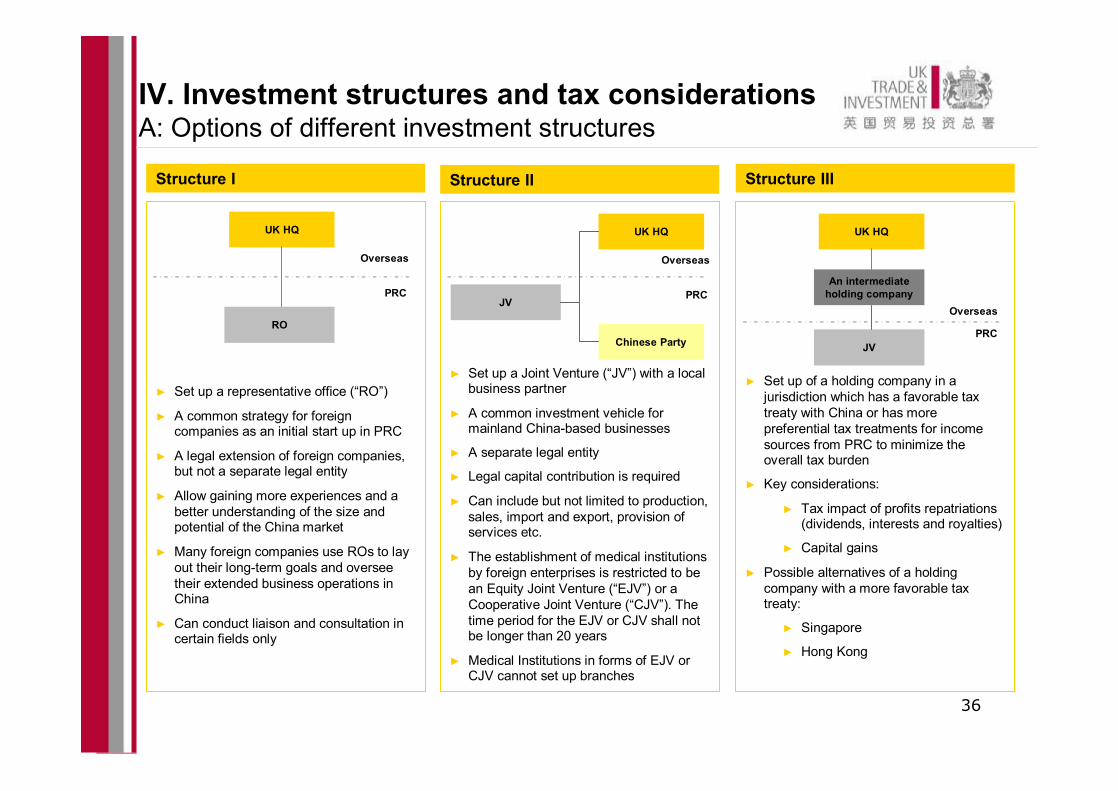

IV. Investment structures and tax considerationsA: Options of different investment structures

Structure I Structure II Structure III

UK HQ

RO

Overseas

PRC

UK HQ

JV

Overseas

PRC

UK HQ

An intermediate holding company

JV

Overseas

PRC

► Set up a representative office (“RO”)

► A common strategy for foreign companies as an initial start up in PRC

► A legal extension of foreign companies, but not a separate legal entity

► Allow gaining more experiences and a better understanding of the size and potential of the China market

► Many foreign companies use ROs to lay out their long-term goals and oversee their extended business operations in China

► Can conduct liaison and consultation in certain fields only

► Set up a Joint Venture (“JV”) with a local business partner

► A common investment vehicle for mainland China-based businesses

► A separate legal entity

► Legal capital contribution is required

► Can include but not limited to production, sales, import and export, provision of services etc.

► The establishment of medical institutions by foreign enterprises is restricted to be an Equity Joint Venture (“EJV”) or a Cooperative Joint Venture (“CJV”). The time period for the EJV or CJV shall not be longer than 20 years

► Medical Institutions in forms of EJV or CJV cannot set up branches

► Set up of a holding company in a jurisdiction which has a favorable tax treaty with China or has more preferential tax treatments for income sources from PRC to minimize the overall tax burden

► Key considerations:

► Tax impact of profits repatriations (dividends, interests and royalties)

► Capital gains

► Possible alternatives of a holding company with a more favorable tax treaty:

► Singapore

► Hong Kong

Chinese Party

36

► Prohibited:►The employee of the RO should not make

independent saledecisions – must be clear in the employment contract

►Sales contracts of the head office should not be signed in the name of, or by, the RO

►Any press announcement of documentation must not indicate or imply the presence of the RO

►Advertisements must indicate that it is a liaison office only if the address of the RO is included

► The holding company holds shares of the EJV or CJV

► Establishment of the holding company is to find a company in a jurisdiction that has a favorable tax treaty with China or has more preferential tax treatments for income sourced from PRC, in order to minimize the overall tax burden

► A shell Corporation► The EJV or CJV in China

underneath the holding company can include but not limited to:

► Medical services► Sales of medicine► Medical equipment importation, etc.

► The establishment of medical institutions by foreign enterprises is restricted according to the Guidance Catalogue of Industries for Foreign Investment. Its structure must be an EJV or a CJV.

► In addition, both the Chinese and foreign parties shall meet one of the following requirements:

► ⑴ Able to provide advanced managerial experience in managing medical institutions and service modes

► ⑵ Able to provide international advanced level of medical technologies and equipment; and

► ⑶ Able to make up for the inadequacy of local medical capacity, medical treatment technologies, fund and medical facilities

► Allowed:► Provide liaison services to the head office► Collect market information for the head office► Deal with relevant government departments► Products promotion► Make travel arrangements for personnel of the head office► Technological exchange

Structure III – with a Holding CompanyStructure II – JVStructure I - RO

Business Scope

37

IV. Investment structures and tax considerationsA: Options of different investment structures

► The same as structure II► Allowed by submitting application to the China tax bureau

► Not allowed

►The same as structure II►Being able to hire employees in the name of the JV with discretion

►No restriction on hiring non-PRC nationals (Chief representative / representative)

►PRC nationals can only be hired under the officially approved HR consulting companies, e.g. the Foreign Enterprises Services Corporation (“FESCO”), China International Enterprises Cooperative Corporation (“CIECCO”), China Star Corporation for International Economic & Technical Corporation (“China Star”), China International Intellectech Corporation (“CIIC”) and China International Talent Development Center (“CITDC”)

►Must appoint a “Chief Representative”

► The same as structure II► No less than £ 1,818,182 (£909,091 for Hong Kong and Macau EJV or CJV) for joint venture medical institutions. The equity proportion of the Chinese party shall be no less than 30% (No restriction for HK and Macau investors in Guangdong Province) in particular

► No Capital Requirement

Structure III – with a Holding CompanyStructure II – JVStructure I - RO

Registered Capital

Issuance ofInvoices

38

Staffing

IV. Investment structures and tax considerationsB: Tax consequences and entity functions

Structure III – with a Holding CompanyStructure II – JVStructure I - RO

► The same as structure II

► For reference, the tax preferential treatment for certain items in Hong Kong-PRC DTA and in Singapore-PRC DTA are listed as the following

► CIT (25%)► BT (3% ~ 20%, mainly 5%)► IIT (nine level progressive tax

rates ranging from 5% to 45%)

► SD► VVT► Value Added Tax (3% / 17%)► Customs Duty (“CD”)► Withholding Tax (“WHT”)► Real Estate Tax (“RET”), etc.

► Taxable income is calculated on an accrual basis. As a company incorporated in the PRC, the JV would be treated as a PRC tax resident. Resident enterprises shall pay CIT on earnings sourced from both inside and outside China:

► Corporate Income Tax (“CIT”) ( tax rate: 25%)► Business Tax (“BT”) (5%)► Individual Income Tax (“IIT”) (nine level

progressive tax rates ranging from 5% to 45%)► Stamp Duty (“SD”)► Vehicle and Vessel Tax (“VVT”), etc.

► The RO is a non-resident company in the PRCand shall file CIT and BT based on the tax filing method assessment

► Category One – Actual revenue / actual profit basis

► A RO that is engaged in business advisory, law, tax advisory, accounting, auditing or other types of consulting services, shall be taxed on an actual revenue and actual profit basis. It must maintain complete accounting records and properly calculate revenues and taxable income

Tax

Applicable

39

Tax

Implications

IV. Investment structures and tax considerationsB: Tax consequences and entity functions

► CIT payable = taxable income x applicable tax rate – reduced or waived tax – tax credits

► BT payable = taxable turnover x applicable BT rate

► Small-scale VAT-payer (3%): Input VAT is not creditable

► VAT payable = Sales x 3%► General VAT-payer (17%): Input

VAT is creditable► VAT payable = (Sales –

purchase) x 17%► Capital gain shall be subject to

withholding income tax at 10% under the CIT law

► According to the Double Tax Treaty (“DTA”) between UK and China:

►Dividend: 10%►Interest: 10%►Royalties: 7% (applies to

copyright royalties) or 10%

► Category Two – Cost-plus / deemed profit basis

► If a head office is engaged in trading (including self-trading and agency trading), advertising and travel business, its RO should be taxed on a “cost-plus basis.” Under the cost-plus method, the RO is required to keep accounts on all the costs and expenses incurred. Such records are subject to an annual audit conducted by a Certified Public Accountant firm

► Category Three – Actual revenue / deemed profit basis

► A RO that has not been described as fitting into one of the above methods, and is engaged in taxable activities, should report to the local tax authorities and compute BT based on the actual revenue generated from their activities. The tax authorities will collect the CIT on a deemed profit basis. If no revenue is generated during the year, the RO should submit an Annual Activity Report within one month of the year-end. Revenue must be reported include those that are not directly received by the RO, but attributable to the activities of the RO and collected by the headoffice

Structure III – with a Holding CompanyStructure II – EJV or CJVStructure I - RO

Taxable in the PRC (if capital participation ≥ 25% in the past 12 months)

Taxable in the PRC (≥ 25%PRC shares)

10%7%

7% (for banks)10% (for otherenterprises)

7%

5% (≥25%shares)10% (< 25%shares)

5% (≥ 25%shares)10% (< 25%shares)

Dividend

Interest

Royalty

Capital Gains

Hong Kong Singapore

40

Tax

Implications

(cont’d)

IV. Investment structures and tax considerationsB: Tax consequences and entity functions

► The procedures for setting up a holding company may varydepending on the countries or areas where the companywould be established. Nevertheless, the basic process may include:

► Step 1: Choose and check to avoid duplicate an intended company name

► Step 2: Submit required documents for the company registration

►The memorandum of association of the intended company

►The articles of association►Other documents upon

requirement► Step 3: Payment of the

company registration fees to the Companies Registry

► Step 4: Collect the certificate of incorporation

► Other steps upon requirements in applicable countries and areas

► Step 1: Pre-approval for establishment of EJV or CJV medical institutions from the Ministry of Healthy (Application shall be submitted to the administrative department of health at the municipal level)

►The following documents are generally required: Application report; feasibility report; business registrations of both parties; assets verification report, etc.

► Step 2: Pre-approval of company name from the Beijing Administration of Industry and Commerce (“BAIC”)

► Step 3: Approval from the Ministry of Commerce (“MOC”)

►During this step, there are many documents to be submitted, e.g. articles of association, resumes and passports or identity cards of all members of the Board

► Step 1: Pre-approval from appropriate authorities if applicable

► Approval from Ministry of Commerce► ⑴Foreign non-enterprise organization

to set up ROs in PRC► ⑵Taiwan non-enterprise organization

to set up ROs in PRC► ⑶Enterprise to set up ROs in PRC from

countries which do not build diplomatic relationship with PRC

► Approval from specific industries► ⑴Foreign transportation enterprise to

set up RO need to obtain pre-approval from the Transportation Department

► ⑵Foreign aviation enterprises to set up RO need to obtain pre-approval from theGeneral Admission of Civil Aviation of China

► ⑶Foreign law firms to set up RO need to obtain pre-approval from the Ministry of Justice PRC

► ⑷Foreign financial institutions to set up RO need to obtain pre-approval from the People’s Bank of China

► ⑸Others

► Slightly more time-consuming than directly setting up an EJV or a CJV

► Generally, 6 – 12 months or more upon all documents are provided by the applicant

► Generally, 2 – 5 months or more upon all documents are provided by the applicant

Structure III – with a Holding CompanyStructure II – EJV or CJVStructure I - RO

Time Required

in Application

Establishment Steps

41

IV. Investment structures and tax considerationsC: Business registration procedures

► After establishment of the holding company, the holding company can set up a JV in the PRC.

► The same as structure II – EJV or CJV

► Step 4: Approval from BAIC►This step must be performed

within 30 days after the Approval Certificate is issued by the MOC

► Step 5: Application for practice registration at the administrative department of health designated by the administrative department of health at the provincial level to obtain the Practice Permit for Medical Institutions

► Step 6: Registration with the appropriate Public Security Bureau

►This step should be performedwithin 10 days after the business license is issued

► Step 7: Registration with the Technology Supervision Bureau

►A Unified Organization Certificate should be applied with the Technology Supervision Bureau within 15 days after the business license is issued

► Step 8: Registration with the Beijing Tax Bureau

►Tax Registration is required within 30 days after the business license is issued

► According to Beijing Enterprises Registration Pre-approval Catalogue, ROs set up by foreign medical companies do not need to obtain any pre-approvals.

► Step 2: Registration with the Beijing Administration of Industry and Commerce (“BAIC”)

► After receiving the pre-approval from appropriate authorities, the company should apply to BAIC for Business License and Chief Representative’s Working Card. The step will take around 7 working days

► Step 3: Registration with the Beijing Public Security Bureau

► After obtaining a business license, the RO should register with Public Security Bureau and apply for the chop engrave. The process will last about 2 ~ 5 working days

► Step 4: Registration with the Beijing Technology Supervision Bureau

► After the chop is engraved, the RO could apply for an Organization Code Certificate which will take 7 ~ 10 working days

► Step 5: Registration with the State Administration of Foreign Exchange (“SAFE”)

► To apply for the Foreign Exchange Registration will take 2 ~ 5 working days. The Business License and the Organization Code Certificate are required to be submitted

Structure III – with a Holding CompanyStructure II – EJV or CJVStructure I - RO

42

Establishment Steps

(cont’d)

IV. Investment structures and tax considerationsC: Business registration procedures

► The same as structure II –EJV or CJV

► Step 9: Registration with State Administration of Foreign Exchange (“SAFE”)

► Step 10: Opening Bank Accounts► Step 11: Report at the District Branch

of BAIC► Step 12: Registration with the Financial

Bureau► Step 13: Registration with the Beijing

Customs►Registration with the Beijing

Customs should be applied within 30 days after the business license is issued

► Step 14: Registration with Beijing Statistics Bureau (“BSB”)

►Registration with the BSB should be applied within 30 days after the business license is issued

► Step 15: Registration with the Beijing Labor Bureau (“BLB”)

►Social security registrations for the company and local employees shall be applied within 30 days after the business license is issued. Working permits and working cards should be applied for expatriates

► Step 6: Registration with the Beijing State Tax Bureau

►To register with the State Tax Bureau will take 15 ~ 20 working days. Tax Registration Form and Tax Filing Assessment Form are required to be submitted

► Step 7: Registration with the Beijing Local Tax Bureau

►To register with the Local Tax Bureau will last 15 ~ 20 working days. The Tax Registration Certificate will then be issued

► Step 8: Opening Bank Accounts►To open bank accounts, the Application

Letter, the Business License and other applicable documents are required. It normally takes 10 working days

► Step 9: Registration with the Beijing Statistics Bureau (“BSB”)

►To obtain a Statistics Registration Certificate will take around 2 ~ 5 working days

► Step 10: Registration with the Beijing Customs► To register with the Beijing Customs will

need 2 ~ 5 working days

Structure III – Holding CompanyStructure II – EJV or CJVStructure I - RO

43

Establishment Steps

(cont’d)

IV. Investment structures and tax considerationsC: Business registration procedures

Part B

Mapping and targeting of Chinese healthcare procurement: selling medical devices into the

Chinese market

66 - 67IV. Doing business in China

60 - 64III. Medical devices distribution channel analysis

55 - 58II. Regulatory environment of the Chinese Medical devices market

46 - 53I. Chinese medical devices market overview

Page No.Section

Table of contents

► China accounted for 5% of the global Medical devices market in 2008 and is estimated to reach 25% of the global market by 2050

► In 2007, the Medical devices market accounted for 12% of the total Chinese healthcare market capital, while US Medical devices market accounted for 35% of the total healthcare market capital

► Hospitals, Centres for Disease Control, and urban and rural health centres are the major buyers for Medical device in China. China has 19,700 hospitals, 3,500 Centres for Disease Control, and 63,000 urban and rural health centres

Note: E stands for “Estimation”

Medical devices market size (£ million)

CAGR 9.9%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2005 2006 2007 2008 2009 E 2010 E 2011 E

I. Chinese medical devices market overview

► The medical devices market in China is highly attractive due to its sheer size and the high growth potential

Source: Espicom Business Intelligence Reports, 2008

46

I. Chinese medical devices market overview

► Approximately 11,100 domestic Medical devices manufacturers compete with 33 multinational Medical devices companies in the market

► About 43% of total Medical devices sales were contributed by small companies (2006 data)► The government’s initiative in elevating quality standards in the Medical devices industry is leading to a clear trend in industry consolidation

► In the top 10 companies, only 1/3 were Chinese companies and others were joint ventures and foreign invested companies (2006 data)

► The Chinese Medical devices market is largely supplied by imported products or products locally made by joint ventures and/or foreign companies, especially for higher end products

Top 10 Medical devices companies in China (2006 sales £ million)

67.3KoreaCeragem866.4GermanySiemens (Suzhou) Hearing Instruments9

141.8ChinaWeigao Holding3136.4ChinaMindray Medical International4100.9JapanOMRON (Dalian)585.5USAKnowles Electronics (Suzhou)668.2ChinaXinxiang Piaoan Sanitary Material Group7

65.5Sino-GermanySiemens Shanghai Medical Equipment10

152.7ChinaShandong Zibo Shanchuan Medical Instrument2

172.7Sino-USGE Hangwei Medical Systems1Sales OwnershipCompany name

► The Chinese medical devices market is highly fragmented

Source: Morgan Stanley Research, 2008

47

I. Chinese medical devices market overview

► The total export value is increasing more rapidly than import

► Quick development of the Chinese Medical devices companies to the international standards enables these companies to export to the global market

► Increase in healthcare needs has resulted in a large demand of imported Medical device

Medical devices import and export in China (£ million)

CAGR 19.4%

CAGR 26.9%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006 2007 2008 2006 2007 2008

Import Export

► Both the import and export of medical device have been growing at the double digit rate in the past three years, reflecting the quick expansion of the market

Source: Chinese Chamber of Commerce for Import & Export of Medicines & Health Products data

48

I. Chinese medical devices market overview

Top three countries for imported devices in 2008

17.3%522.1Japan3

18.3%

28.8%

% of total Medical device imported

585.9Germany2

920.2United States1

Import value(£ million)

Country

3

2

1

Diagnostic imaging products

Consumables

Orthopaedics products

Category

14.5%

24.9%

29.6%

CAGR(2002 –

2006)

13.3%

15.2%

48.4%

% of total Medical device

imported

247.9Consumables3

282.8Orthopaedics products2

901.1Diagnostic imaging products1

Import value(£ million)

Category

A: by import valueTop three categories for imported products (2006)

► The United States, Germany and Japan remain China’s largest trading countries for imported medical device

Source: Espicom Business Intelligence Reports, 2008

49

B: by growth rate

I. Chinese medical devices market overview

Consumables

2006 (£ million)

Orthopaedics products

2006 (£ million)

Diagnostic imaging products

2006 (£ million)

20%

24%

10%

14%

14%

6%4%

8%

15%

15%

6%10%

11%

43%7%

9%5%

9%

9%

8%41%

12%

Medical X-ray apparatusUltrasonic scanning apparatusParts & accessories for radiation apparatusComputed tomography apparatusMagnetic resonance imaging apparatusOther electrodiagnostic apparatusX-ray tubesOthers

Other orthopaedic appliancesOther artificial body partsHearing aids, except parts & accessoriesOther orthopaedic or fracture appliancesArtificial jointsPacemakers, except parts & accessories

► Sub-categories and the import value of the top three imported product categories in 2006

Other needles, catheters, cannulae etc.Syringes (with/without needles)Medical X-ray film (rolled)Opacifying preparationsTubular metal needles/needles for suturesSutures, sterile, surgical & dental goodsMedical X-ray film (flat)Others

Source: Espicom Business Intelligence Reports, 2008

50

I. Chinese medical devices market overview

Top three countries for export devices in 2008

3

2

1

Health rehabilitation products

Diagnostic and treatment apparatus

Dental products

Category

30.4%

31.0%

49.1%

CAGR(2006-2008)

20.6%

28.1%

32.7%

% of total Medical device

exported

1,398.8Health rehabilitation products

3

1,908.0Medical dressing2

2,220.9Diagnostic and treatment apparatus

1

Export value(£ million)

Category

A: by export value

Top three categories for export product (2008)

B: by growth rate

Japan3

Germany2

United States1

Country

► UK was among the top five export trading partners of China in 2008

► The export value with top five export trading partners (US, Germany, Japan, Hong Kong and UK) accounted for 53.6% of the total export value in 2008

► The United States, Germany and Japan remain China’s largest trading countries for exporting medical device

Source: Espicom Business Intelligence Reports, 2008

51

I. Chinese medical devices market overview

Medical dressingHealth rehabilitation products Diagnostic and treatment apparatus

Major exporters for the top three export product categories

► Main exporters of medical dressing and health rehabilitation products are domestic companies, while main exporters of diagnostic and treatment apparatus include domestic, foreign, and joint venture companies

Source: Chinese Chamber of Commerce for Import & Export of Medicines & Health Products data

52

I. Chinese medical devices market overview

► From 2006 to 2008, only the diagnostic and treatment apparatus sector showed trade deficits but the extent is decreasing at 16.2% year-on-year

► From 2006 to 2008, the proportion of the export diagnostic and treatment apparatus has increased among the total export medical device

Diagnostic and treatment apparatus import and export (£ million)

Import CAGR: 11.96% Export CAGR: 30.98%

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

2006 2007 2008

ExportImportBalance

► Chinese companies are becoming more competitive in the diagnostic and treatment apparatus sector

Source: Chinese Chamber of Commerce for Import & Export of Medicines & Health Products data

53

I. Chinese medical devices market overview

Source: company news, EY analysis

54

► British devices companies are accelerating their business expansions in China

►Smiths Medical, a leading supplier of specialist medical devices and equipment► Announced the establishment of a new headquarters for Greater China in Beijing. The new office will

consolidate the company’s operations in Taiwan, Hong Kong and China, and signals a major new investment in and commitment to the region [Oct 2009]

► Acquired Zhejiang Zheda Medical Instrument (ZDMI), a Chinese syringe pumps and enteral feeding devices manufacturer primarily for the Chinese market

► Has established distribution partnership with multiple distributors: Beijing Longer Medical Appliances Co Ltd, Cemma Enterprise Co., Ltd, Gold Pacific Enterprises, Goodman Medical Supplies Ltd., Goodwin Health Care Holdings Ltd, Goodwin Healthcare Ltd, SASN Medical Supplies Co., Ltd., SuntimeTechnology, Zhuhai Hualin Medical Devices Co Ltd

►Smith & Nephew, the largest medtech company in the UK, has begun more focused on the China market

► Announced that it would move its production facility for high tech wound care products from the USA to Suzhou, China. The plant in Suzhou is scheduled for completion in 2009 [Oct 2007]

► Announced that it will begin production of parts for artificial joints in a new 100,000 square foot manufacturing facility in Bejing [Aug 2008]

► However, the company remains wary of China counterfeiters, therefore, claims it will not build its latest, most high-tech devices in China

66 - 67IV. Doing business in China

60 - 64III. Medical devices distribution channel analysis

55 - 58II. Regulatory environment of the Chinese medical devices market

46 - 53I. Chinese medical devices market overview

Page No.Section

Table of contents

II. Regulatory environment of the Chinese medical devices market► The medical devices market is regulated by the Chinese State Food and Drug

Administration (SFDA) at the national, provincial, and municipal levels

► In charge of the inspection, approval and granting with a registration certificate for Class II domestic Medical device

► responsible for the inspection and approval of the clinical trial or verification of Class II domestic Medical device

Food and Drug Administration of provinces, autonomous regions and municipalities

► In charge of the inspection, approval and granting with a registration certificate for Class I domestic Medical device

Food and Drug Administration of Municipal level

► In charge of the inspection, approval and issuing the registration certificate for imported Medical device and Class III domestic Medical device

► responsible for the inspection and approval of the clinical trial or verification of Class III domestic Medical device

State Food and Drug Administration

►Most consumables, i.e., medical dressings, surgical gloves

► Medical device for which safety and effectiveness can be ensuredthrough routine administrationClass I

►X-ray tubes, dental drill engines► Medical device for which further control is required to ensure their safety and effectiveness Class II

►Magnetic resonance imaging apparatus, dental cements & other fillings, medical X-ray apparatus

► Medical device which are implanted into the human body, or used for life support or sustenance, or can pose potential risks to the human body and thus must be strictly controlled

Class III

ExamplesDefinition Category

Key regulators Key responsibilities

Source: SFDA data

56

II. Regulatory environment of the Chinese medical devices market► All imported Medical device must be registered with the Chinese SFDA to receive the

Import Medical Devices Registration Certificate. The certificate must be renewed every 4 years

5 working days 10 working days30 working days60 working daysStart

The applicant submits written

application and other required documents

The SFDA accepts the application

The SFDA requires

supplementary documents

Re-apply

The SFDA initiates technology evaluation

The SFDA makes a written decision

of approval

The SFDA issues Medical device

registration certificate

The SFDA makes a written rejection

of registration

The SFDA rejects the registration

Source: SFDA data

57

II. Regulatory environment of the Chinese medical devices market► The regulatory environment of the Chinese medical devices market is becoming more

and more rigorous

2009► SFDA issued State Key Supervised Medical device Lists2007► SFDA completed the draft version of the Revised Regulations for the Supervision and Administration of

Medical device► China launched a five-year plan to improve standards controlling the safety of Medical device ► 180 drugs and Medical device were banned because of illegal advertising

Major regulatory initiatives in recent years

Released new provisions

2007► SFDA shut down 300 drug & Medical devices manufacturers for inferior quality products► Guangdong Provincial FDA revoked the licenses of 67 Medical devices manufacturers and nearly 300

distributors for producing and selling sub-standard goods

Tightened quality control

2008► SFDA standardized management of labels and packaging marks of overseas Medical device► SFDA announced relevant issues concerning market access of some imported Medical device

Strengthened control of imported products

Key trends

Strengthened price control

2007► National Development and Reform Commission (NDRC) carried out a nation wide medicine price inspection,

including the price of Medical devices2006► NDRC solicited opinions on the provision for strengthening supervision and inspection of the implanted

Medical devices priceSource: SFDA data

58

II. Regulatory environment of the Chinese medical devices market► Chinese healthcare reform will increase the demand for medical device

► The demand for basic medical equipment will increase ► China's emphasis in health care will switch from being treatment-oriented to prevention-oriented

► A total of 39,441 township clinics need to be equipped with basic Medical device in the rural areas

► A total of 5,151 “Grade Two” hospitals and 2,738 “Grade One” hospitals in the urban areas need to upgrade the Medical device

► A total of 5,774 community health centres will receive government subsidies to purchase equipment and provide a variety of basic health care services

ReasonsPotential impact

► The demand for high-end diagnostic and treatment equipment will also increase

► A total of 1,045 “Grade Three” hospitals in China will be required to focus on major and severe disease treatment

► The willingness to pay for health care services is likely to increase as a result of increasing social insurance reimbursement rate

► The demand for digital-based medical device will increase

► Improving information technology in the healthcare industry will increase the use of digital equipment

Six categories of medical device may have the greatest growth potential:► In-vitro diagnostics► Low-end medical imaging equipment including corpuscle counter and portable ultrasound systems► Medical information technology (IT) solutions including computer-aided diagnostic systems and long-distance medical treatment systems► Minimally-invasive and non-invasive devices including stents, capsule endoscopes and insulin pumps► Medical consumables including disposable surgery instruments as well as home-use Medical device including blood glucose monitors► Sphygmomanometers

59

66 - 67IV. Doing business in China

60 - 64III. Medical devices distribution channel analysis

55 - 58II. Regulatory environment of the Chinese medical devices market

46 - 53I. Chinese medical devices market overview

Page No.Section

Table of contents

III. Medical devices distribution channel analysis

► The Chinese government is taking actions to streamline the medical devices distribution channel and reduce distribution costs

Complex distribution network► Most companies still rely on third-

party distributors to sell their products to hospitals and clinics

► The lack of transparency as to where products go or distribution inefficiencies may slow sales growth

To strengthen hospital procurement controls► The government is introducing measures, e.g. government-organized direct procurement, to

combat the growing problem of expensive and unnecessary high-end medical equipment procurements in China, because there have been worries that expensive equipment was being purchased by hospitals but that not in keeping with patients’ actual needs