ultimate four - zacks investment research · pdf filewelcome to your quarterly ultimate four...

TRANSCRIPT

ULTIMATE FOURFebruary 2016

Ultimate Four 1

Welcome to your quarterly Ultimate Four report!Included in this report are the four stocks our experts believe have the greatest upside potential over the next quarter. It is just one of your ben-efits as a member of our Zacks Ultimate program.

It features the single favorite pick for the quarter ahead by four Zacks experts. This edition features selections from:

< Kevin Cook, Editor of Follow The Money Trader and Tactical Trader

< Eric Dutram, Editor of ETF Investor and Surprise Trader

< Brian Bolan, Editor of Stocks Under $10 and Game Changers

< Neena Mishra, CFA, FRM, Editor of Income Investor

Simply read on to learn our Ultimate Four stocks for the coming quarter.

Ultimate Four 2

Kevin CookNXP Semiconductors (NXPI) NXP Semiconductors (NXPI) is a $21 billion Netherlands-based semicon-ductor company in a prime position to capitalize on trends in “smart cars” after the 2015 acquisition of Freescale Semi. Building on its expertise in high-performance mixed-signal electronics, NXP is also driving innova-tion in the areas of cyber security, portables & wearables, and the Internet of Things, as well as the connected car. NXP has operations in more than 25 countries, and posted trailing 12-month revenues of just over $6 billion as of September 30, 2015.

Zacks Ultimate members will know that I have been talking about NXP for some time, though we have never traded it. Instead we focused on other excellent semi companies, like Avago Technologies (AVGO) and Skyworks (SWKS). I think NXP is a company to pay increasing attention to as the stock becomes a better value during the stock market correction because NXP’s growth niches will make it one of the few chip companies to buy between 10 and 15 times forward EPS projections. The Freescale acquisi-tion, which closed in Q4 2015, will not only be accretive to earnings, it will boost 2016 revenues to nearly $10 billion.

A Long Track Record

NXP was spun off from Philips Electronics in 2006 and completed its IPO in August 2010. With over 55 years of experience in semiconductors, of-fering high performance mixed signal and standard product solutions, its products serve a broad range of applications including automotive, com-puting, security, wireless infrastructure, lighting, industrial, mobile devices and consumer electronics. Key to the company’s technology platform is its ability to design high-performance, low power semiconductors by using proprietary hardware and customized software capabilities. The company is targeting key trends in the electronics industry, offering dif-

Ultimate Four 3

ferentiated products in the areas of energy efficiency, connected devices, security and health.

The Growth Trajectory

As I write this before the company’s early February earnings report, NXP is expected to bounce back from flat revenue growth in Q3. Continued strong adoption of tablets and smartphones, automotive electronics and the emergence of the new category of wearables boosted the demand for processing and sensing devices that run them.

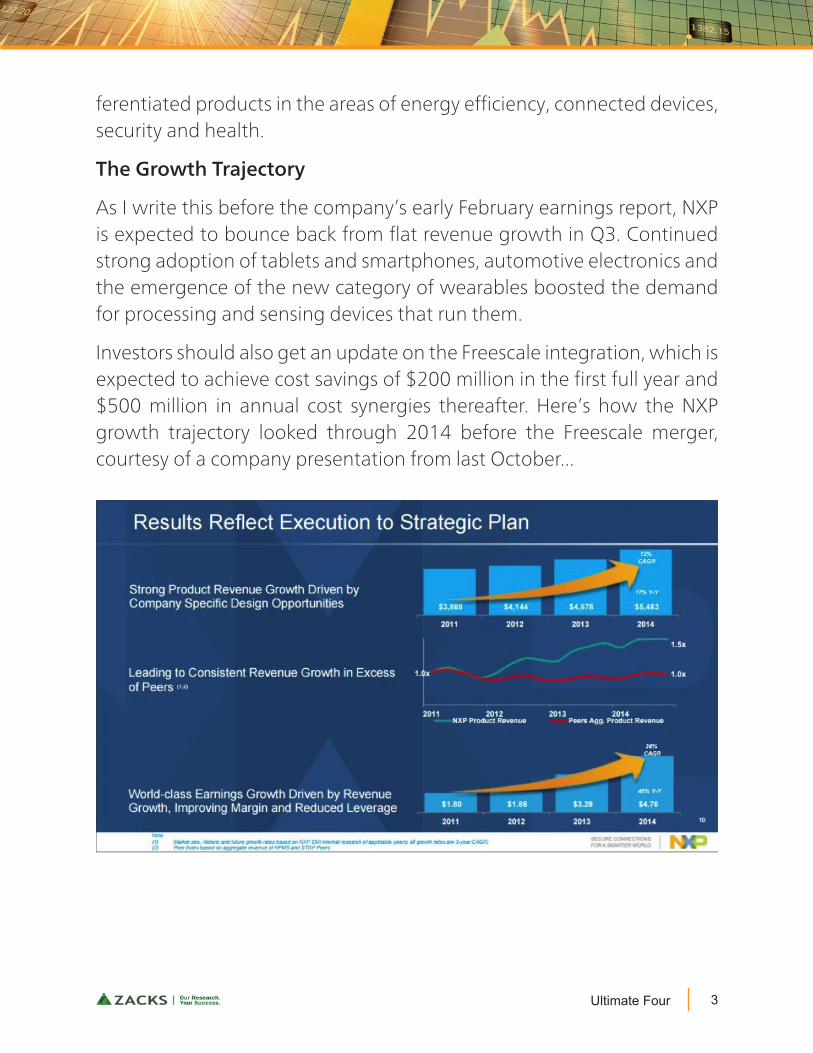

Investors should also get an update on the Freescale integration, which is expected to achieve cost savings of $200 million in the first full year and $500 million in annual cost synergies thereafter. Here’s how the NXP growth trajectory looked through 2014 before the Freescale merger, courtesy of a company presentation from last October...

Ultimate Four 4

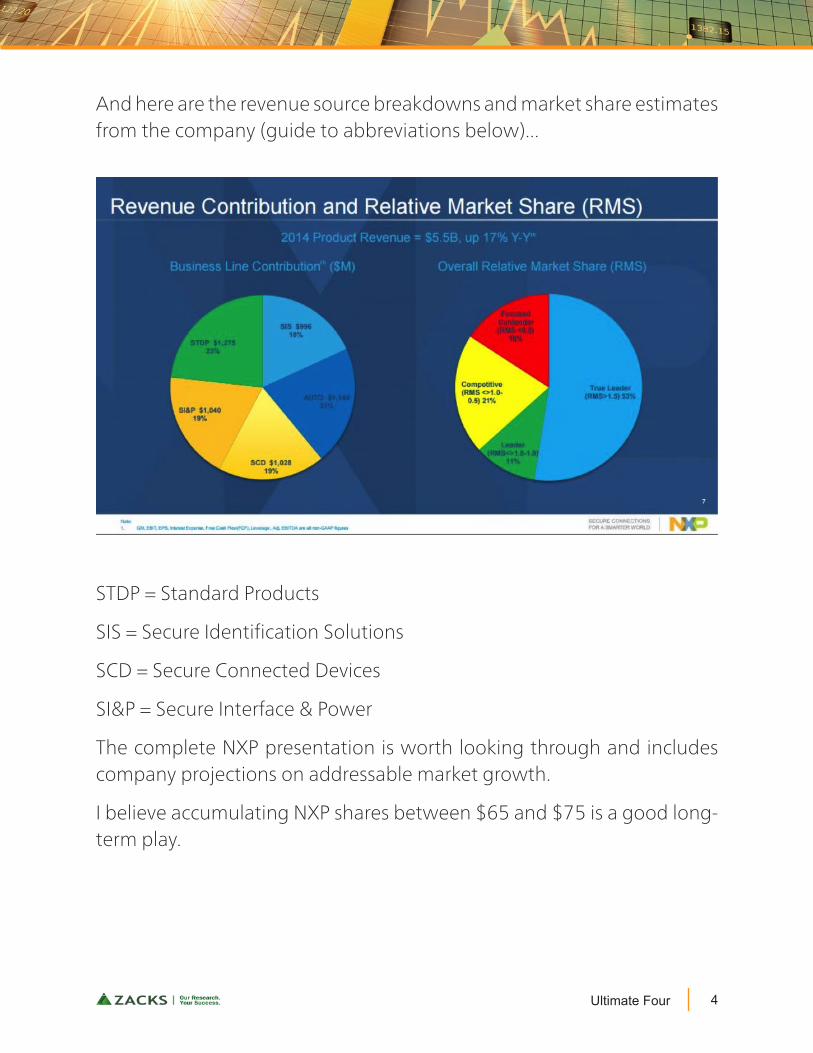

And here are the revenue source breakdowns and market share estimates from the company (guide to abbreviations below)...

STDP = Standard Products

STDP = Standard Products

SIS = Secure Identification Solutions

SCD = Secure Connected Devices

SI&P = Secure Interface & Power

The complete NXP presentation is worth looking through and includes company projections on addressable market growth.

I believe accumulating NXP shares between $65 and $75 is a good long-term play.

Ultimate Four 5

Eric DutramMid-America Apartment Communities (MAA) 2016 isn’t off to a great start for markets as major indexes have had one of their worst starts of all time. And with oil in a deep slump and China on the brink, there are few reasons to expect a banner year from markets.

In this type of environment, it may be a better idea to look to safer stocks that have survived the turmoil and thus could be great picks if more trouble is on the horizon. In particular, companies in the REIT space could be excellent choices for many investors these days.

Why REITs?

REITs, or Real Estate Investment Trusts, were in-focus thanks to the Fed’s rate hike. It was thought that a Fed hike would result in higher Treasury yields and push investors out of higher yielding equity instruments like utilities or REITs as Treasury bond payouts become more attractive.

The problem is especially acute for REITs since they must pay out at least 90% of their income to unit holders in order to avoid certain taxes and they are among the most popular choices for dividend-focused investors. However, thanks to market turmoil, the chances of another Fed rate hike have plunged, putting REITs and other dividend securities back in the spotlight.

With this new reality, it could be time to look at REIT investments once more, and fortunately there are plenty that have strong industry ranks right now. One area to watch is the residential side of the REIT market as it isn’t as impacted by commercial woes (as consumers shop increasingly online) making this the perfect area to find solid securities to profit from this turbulent market. And while there are several great choices here, I think many would be well-served by looking towards Mid-America Apartment Communities (MAA).

Ultimate Four 6

MAA in Focus

MAA is a well-diversified owner and operator of apartment buildings across the country, but with a focus on the Southeast and Southwest markets. The company has over 80,000 units and it is very well spread out with no single market accounting for more than 10% of total net operat-ing income.

This insures that a single downturn in an industry or a city won’t ad-versely impact their portfolio too much, as holdings in places like Houston or Dallas are well-balanced with areas such as Nashville or Charlotte.

But this diversification isn’t the only reason to like MAA as analysts have slowly been increasing their earnings estimates for this stock as well, po-tentially making MAA a great pick.

Rising Estimates

For both the current year and next year periods, analysts seem to agree that MAA’s prospects are looking better. That is why estimates continue to rise and EPS growth looks to stay above 7% for both time frames.

Clearly, analysts have been steadily increasing their estimates enough to boost the consensus estimate to new heights. And as we can see in the chart on the next page, the company is on the right track in terms of in-creasing expectations year-after-year, giving earnings-focused investors plenty to like right now.

Ultimate Four 7

But for those investors worried about MAA living up to the hype at earn-ings season, note that the company has a pretty stellar track record. The company has actually missed less than four times since the start of 2012, making it a likely candidate to keep the great earnings season perfor-mance alive well into the future, and particularly if rates stay low and in-terest remains high in REIT securities.

Ultimate Four 8

Rock of Stability… and Outperformance

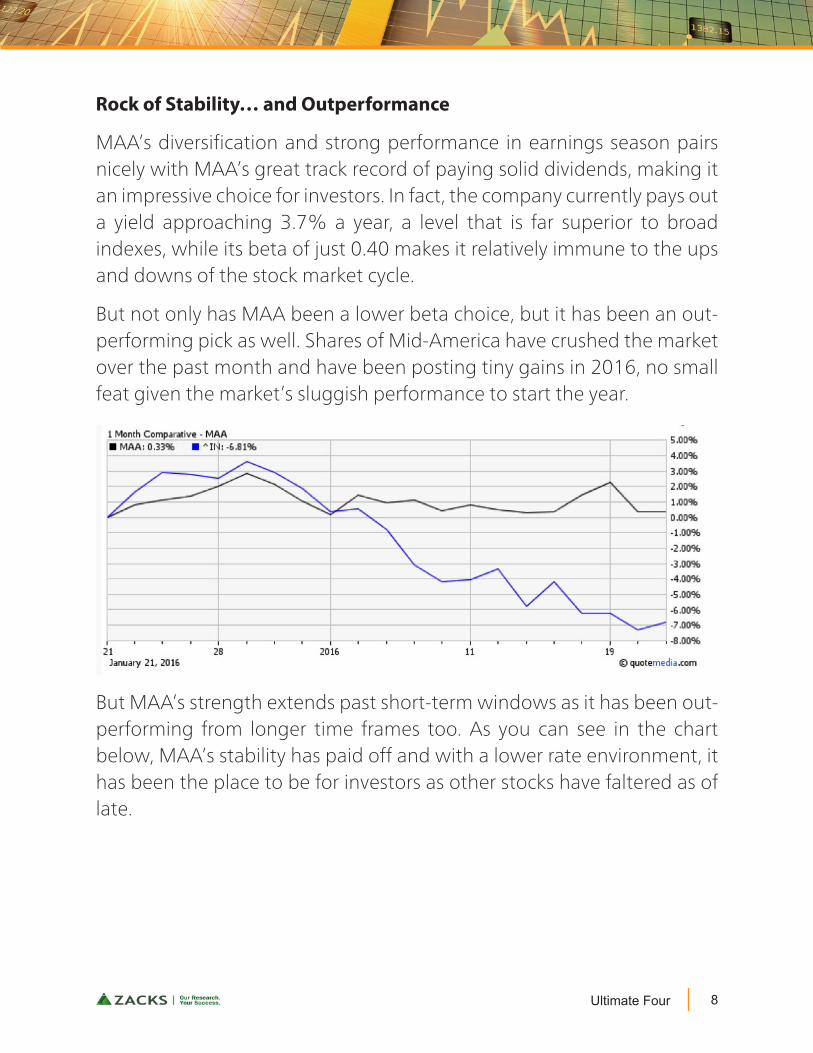

MAA’s diversification and strong performance in earnings season pairs nicely with MAA’s great track record of paying solid dividends, making it an impressive choice for investors. In fact, the company currently pays out a yield approaching 3.7% a year, a level that is far superior to broad indexes, while its beta of just 0.40 makes it relatively immune to the ups and downs of the stock market cycle.

But not only has MAA been a lower beta choice, but it has been an out-performing pick as well. Shares of Mid-America have crushed the market over the past month and have been posting tiny gains in 2016, no small feat given the market’s sluggish performance to start the year.

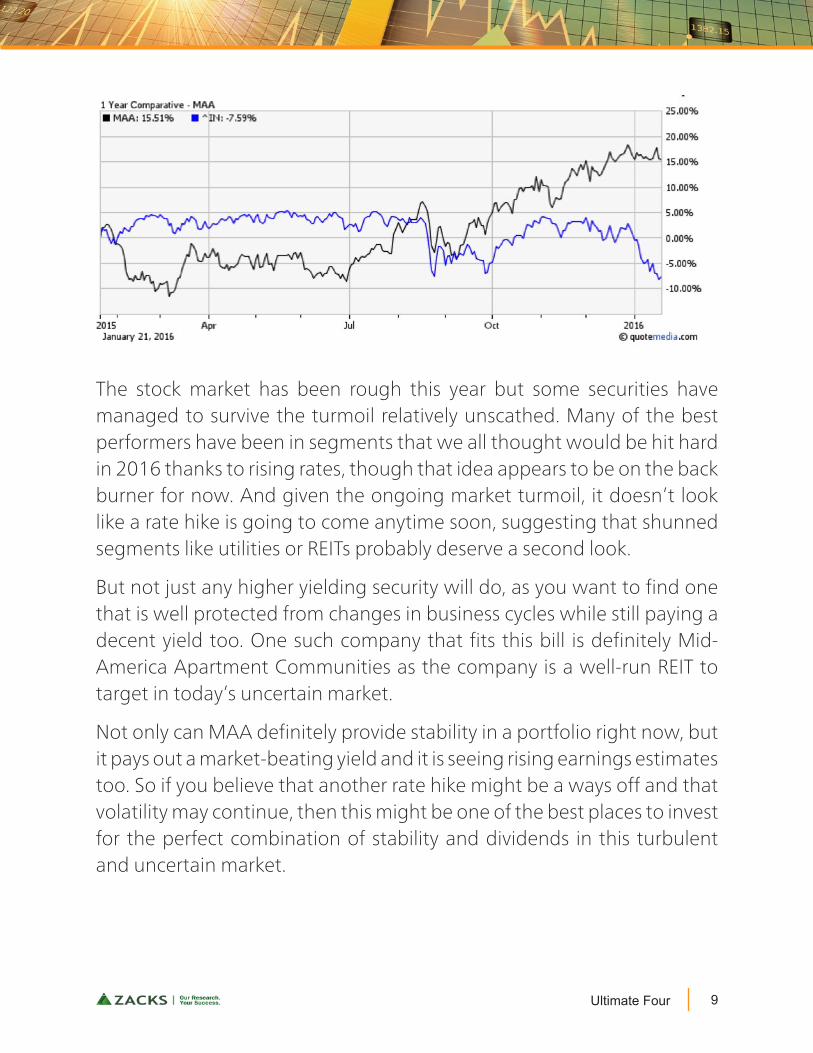

But MAA’s strength extends past short-term windows as it has been out-performing from longer time frames too. As you can see in the chart below, MAA’s stability has paid off and with a lower rate environment, it has been the place to be for investors as other stocks have faltered as of late.

Ultimate Four 9

The stock market has been rough this year but some securities have managed to survive the turmoil relatively unscathed. Many of the best performers have been in segments that we all thought would be hit hard in 2016 thanks to rising rates, though that idea appears to be on the back burner for now. And given the ongoing market turmoil, it doesn’t look like a rate hike is going to come anytime soon, suggesting that shunned segments like utilities or REITs probably deserve a second look.

But not just any higher yielding security will do, as you want to find one that is well protected from changes in business cycles while still paying a decent yield too. One such company that fits this bill is definitely Mid-America Apartment Communities as the company is a well-run REIT to target in today’s uncertain market.

Not only can MAA definitely provide stability in a portfolio right now, but it pays out a market-beating yield and it is seeing rising earnings estimates too. So if you believe that another rate hike might be a ways off and that volatility may continue, then this might be one of the best places to invest for the perfect combination of stability and dividends in this turbulent and uncertain market.

Ultimate Four 10

Brian BolanFacebook (FB) Facebook (FB) recently reported a blowout fourth quarter. Earnings, revenue and usage metrics were all ahead of expectations. Analysts loved the quarter and moved price targets up in a meaningful way. Let’s take a look at the quarter, what the analysts said and why I think this will be a safe stock even if the market moves lower.

The Headline

The first thing that investors gravitate to is the bottom line. The company beat the Zacks Consensus Estimate by $0.09, and in an absolute basis, that was the largest beat in company history. The previous largest beat was $0.07 which was posted in the March 2014 quarter.

Speaking of the biggest beat in company history, the revenue number was also the largest beat ever. Coming in a full $485M over the Zacks Consensus Estimate, FB had a positive revenue surprise of 9%. Only the December 2013 quarter (9.7%) and the June 2013 quarter (12.5%) were bigger on a percentage terms.

The Usage

Last quarter was the first time that daily active users clocked in at more than 1B. This quarter the number grew 3% sequentially and 17% year over year. The company is now closing in on the 1B number on daily mobile users, coming in at 934M this quarter. Mobile DAU increased 4.5% sequentially and 25% on an annual basis.

The monthly usage numbers were strong too, but the real eye-popping number was the growth in ad revenue. Roughly 57% growth on an annual basis is huge, but there was an even more impressive number. The sequential growth of ad revenue was 31%, up from 12% in the prior quarter.

Ultimate Four 11

That is the number to really hang your hat on. Yes the growth in the user base is there, but there is that much more growth from the advertising base that wants to be in front of those users. To me, this is the breakaway figure where growth could actually see a hockey stick style move up.

Analysts

The Zacks Rank is all about the revisions to earnings estimates, but retail investors tend to key in on price targets. When you have estimates moving higher, you generally see price targets move higher. Thing is, the price targets moved much higher than the estimates, which suggests the ana-lysts believe that multiple expansion is well deserved.

I see some small moves in price targets, but the upper end is really some-thing to see. Piper Jaffray moved their target from $155 to $170 and they hold the position of most bullish on the street. RBC Capital Markets moved their target from $130 to $160 and Jefferies took a more cautious stance with a move from $135 to $145. The rest of the cent price targets are more subdued in the $130 range.

Safety Stock

Along with retail investors, professionals are going to be owning a lot more FB in the near future. This is a stock that is providing relative safety amid a flurry of selling as 2016 gets started.

Most professional investors, especially fund managers, are mandated to stay long. Those that want to outperform the market are going to focus as much of their time on not losing money as they are making it. FB will be seen as the spot that can really do both.

This concentration of assets and long tail buying in the name should keep the stock price at much higher levels than other stocks in the market. For this reason, we call it a safety stock and I expect tech focused funds to load up on the name.

Ultimate Four 12

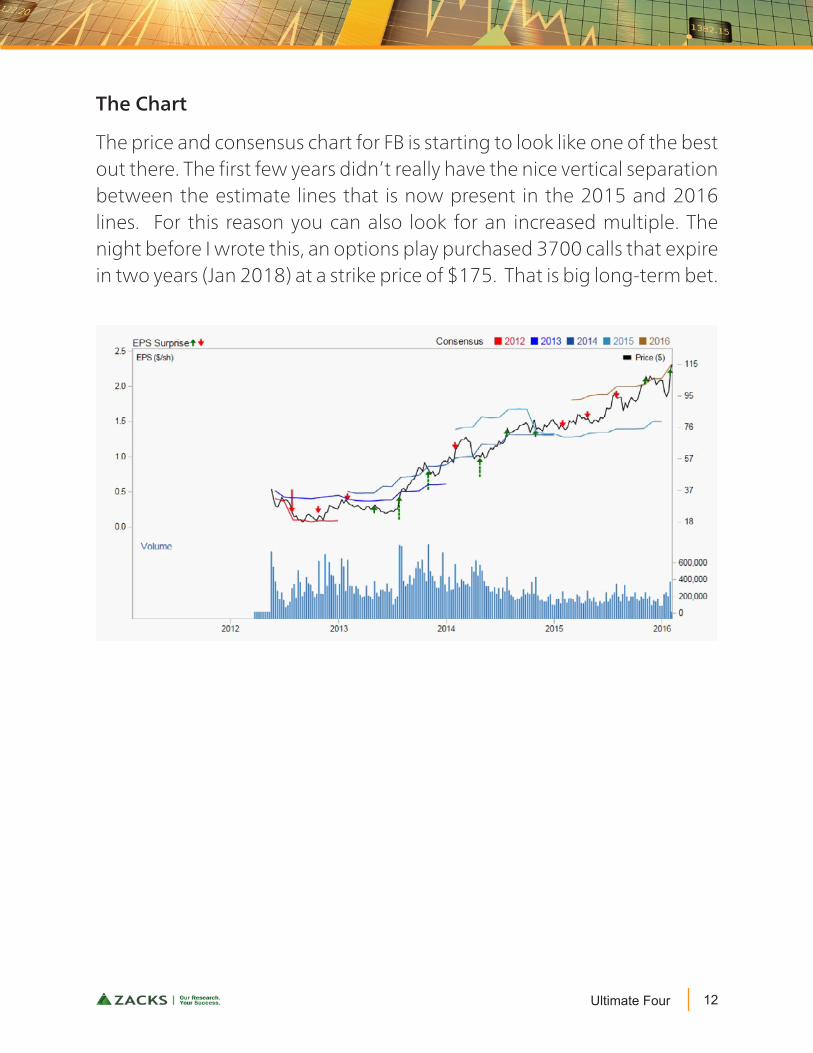

The Chart

The price and consensus chart for FB is starting to look like one of the best out there. The first few years didn’t really have the nice vertical separation between the estimate lines that is now present in the 2015 and 2016 lines. For this reason you can also look for an increased multiple. The night before I wrote this, an options play purchased 3700 calls that expire in two years (Jan 2018) at a strike price of $175. That is big long-term bet.

Ultimate Four 13

Neena MishraSouthwest Airlines (LUV) Low fuel prices continue to lift airlines’ earnings but their shares had taken a beating last year in the wake of global growth worries. Paris terror attacks also negatively impacted these stocks. Now may be a good time a take a look at airlines as many of them delivered solid Q4 results, thanks mainly to low oil prices, which are expected to stay lower for longer.

About the Company

Dallas-based Southwest Airlines (LUV) is the nation’s largest carrier in terms of originating domestic passengers boarded. They serve 77 of the top 100 domestic airports, focusing primarily on short-haul, high fre-quency, point-to-point and low-fare services.

Modern Fleet of Aircraft

At the end of last year, the airline had 704 aircraft in its fleet. They operate the largest fleet of Boeing aircraft in the world, most of which are equipped with satellite-based Wi-Fi providing gate-to-gate connectivity. They con-tinue to plan for modest year-over-year fleet growth through 2018.

Ultimate Four 14

Southwest recently ordered 33 new 737-800s from Boeing, in order to accelerate the replacement of their classic fleet with next generation air-planes.

Solid Fourth Quarter Results

The company reported record fourth quarter net income of $0.90 per share, from $0.59 per share in the same quarter a year ago, thanks to 29% lower jet fuel prices and fleet modernization. The airline estimates fuel costs in the current quarter to be about $1.70 a gallon, down from $2 a gallon a year ago and full year 2016 fuel price per gallon to be in the $1.70 to $1.75 range.

Total operating revenues were a record $5 billion, up 7.5% year-over-year on a capacity increase of 8.4%. This was the company’s best year of earnings, including a record return on invested capital of 32.7%.

Rising Estimates

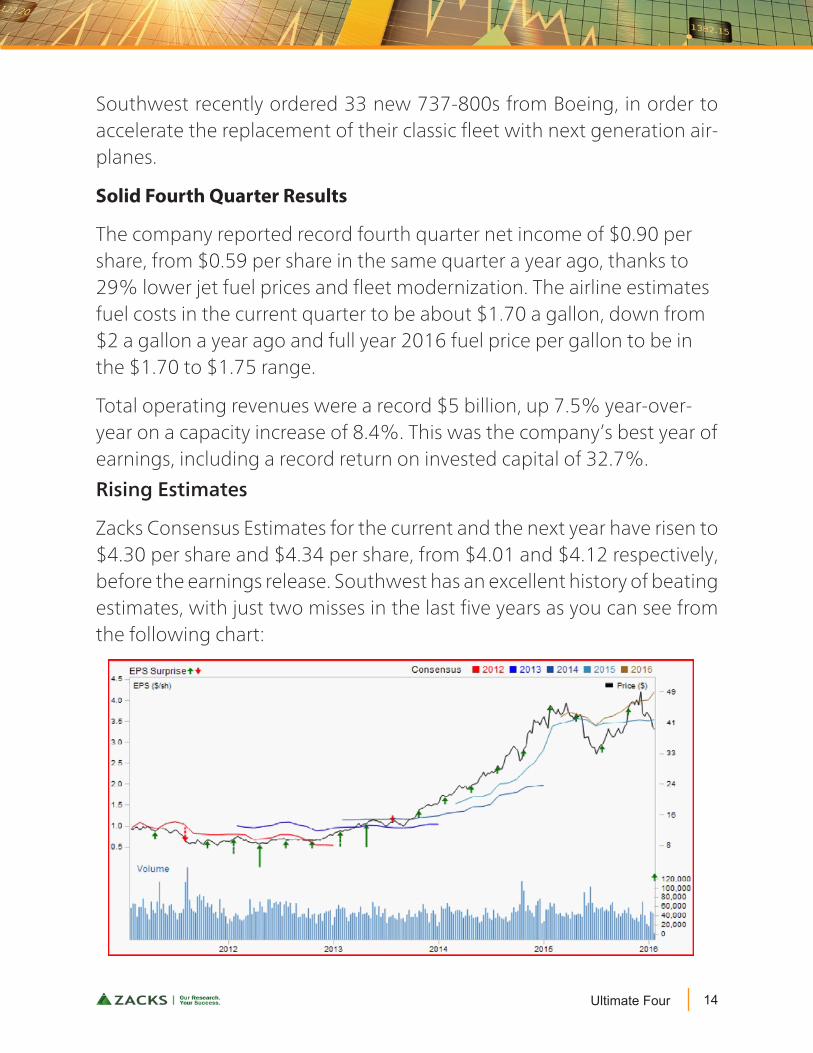

Zacks Consensus Estimates for the current and the next year have risen to $4.30 per share and $4.34 per share, from $4.01 and $4.12 respectively, before the earnings release. Southwest has an excellent history of beating estimates, with just two misses in the last five years as you can see from the following chart:

Ultimate Four 15

Returning Cash to Shareholders

During 2015, Southwest returned $1.4 billion to shareholders through share repurchases and dividends. They plan to buy back an additional $500 million starting in the current quarter.

Ranked #4 in 2015 Airline Scorecard

Southwest scored an overall rank of 4 in the annual ranking of major air-lines in operational areas by Middle Seat Scorecard.

Excellent Growth Potential with Attractive Valuation

In addition to a top Zacks rank, the stock has a Style Score of “A” for Mo-mentum and “B” for Value. It is currently trading at an attractive multiple of 9.7 times forward earnings.

Additionally the Airline industry is currently ranked 16 out of 265 Zacks industries (top 6%), reflecting solid fundamentals for the industry.

Should You be Concerned About Zika Virus?

Zika virus has been in news of late and many investors are concerned about the impact on airlines’ earnings since the CDC issued an alert about risks of traveling to countries affected by this virus.

Zika virus is mosquito-borne and causes mild symptoms in most cases. However the virus poses risks to pregnant women, as infection could result in birth defects. Thus CDC’s alert focused on pregnant women and women planning to become pregnant.

There should be minimal impact on airlines even though some reports are suggesting that the virus is spreading explosively. Just consider, how many pregnant women you see on a flight.

Ultimate Four 16

The Bottom Line

With 43 consecutive years of profitability, Southwest is one of the best managed airlines in the world. It will continue to benefit from the improv-ing U.S. economy and growing demand for air travel, in addition to tail-winds from low fuel prices.

Low fuel prices do put pressure on pricing, particularly due to heavy dis-counting by low-cost carriers, but with the depth and the breadth of the service, I believe this airline can continue to compete on cost and on price, maintaining its low fare leadership position in the country. Further, with their domestic focus, they are rather immune to currency headwinds that have been hurting some of their larger peers with more international presence.