uncorrelated return

TRANSCRIPT

PRESENTED BY

)

U N -C O R R E L A T E D

R E T U R N

PRESENTED TO

Asst. Prof.Department of

Business Administration

INTRODUCTION

Return is the primary motivating force that drives

investment.

It represents the reward for undertaking

investment.

The return of an investment consists of two

components-----

1. Current return: It is the periodic income.

2. Capital return: It is simply the price

appreciation

PORTFOLIO RETURN & RISK

Investors generally hold a portfolio of securities.

What matters finally is the return & risk of the

portfolio

PORTFOLIO EXPECTED RETURN: is simply the

weighted average of the expected returns on

the individual securities in the portfolio.

E(Rp )= )(1

RiEWin

i

PORTFOLIO RISK

The risk of a portfolio too is measured by the

variance (or standard deviation).

UN-CORRELATED RETURN::

When the co-rrelation between two or more

securities return is Zero(0), it is called Un-

correlated return

M E A S U R E M E N T O F C O M O V E M E N T S I N

S E C U R I T Y R E T U R N S

Comovements between the returns of securities

are measured by Covariance & Coefficient of

Co-rrelation

Covariance essentially tells us whether or not two

securities returns are correlated.

Covariance is standardized by dividing with the

product of the standard deviation of two

individual securities, called as Correlation

Coefficient.

Cor(Ri, Rj)=rij= ji

RjRiCov

.

),(

The correlation coefficient can vary between -1

&+1

A correlation of +1 means that the returns of the

two securities always move in the same

direction

A correlation of -1 means that the returns of the

two securities move in opposite direction.

A correlation of Zero(0) means the two securities

are Uncorrelated and have no relationship to

each other.

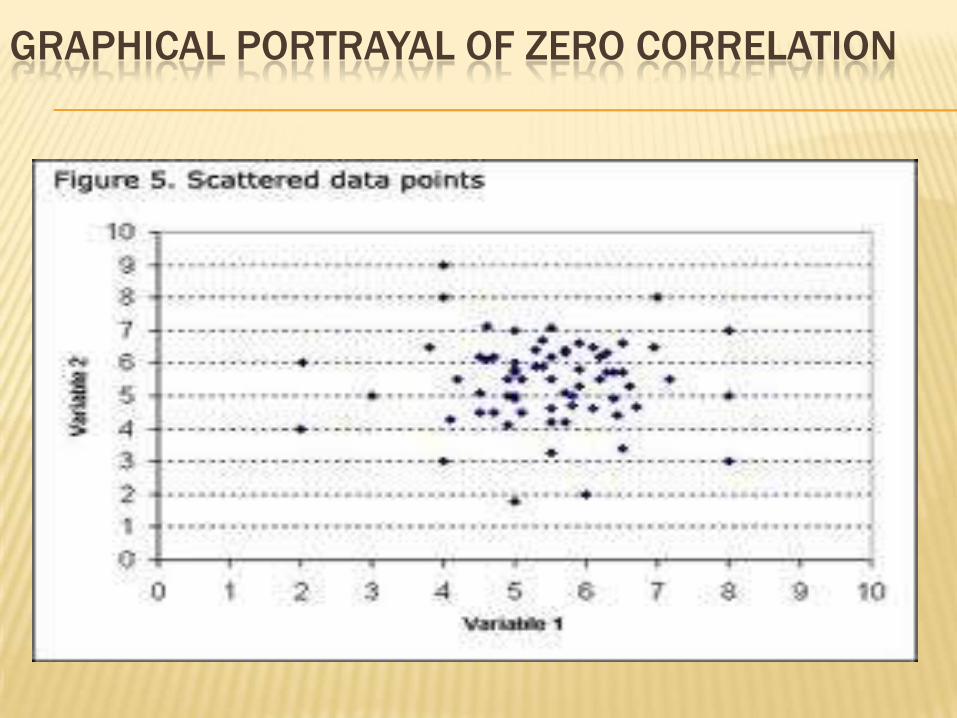

GRAPHICAL PORTRAYAL OF ZERO CORRELATION

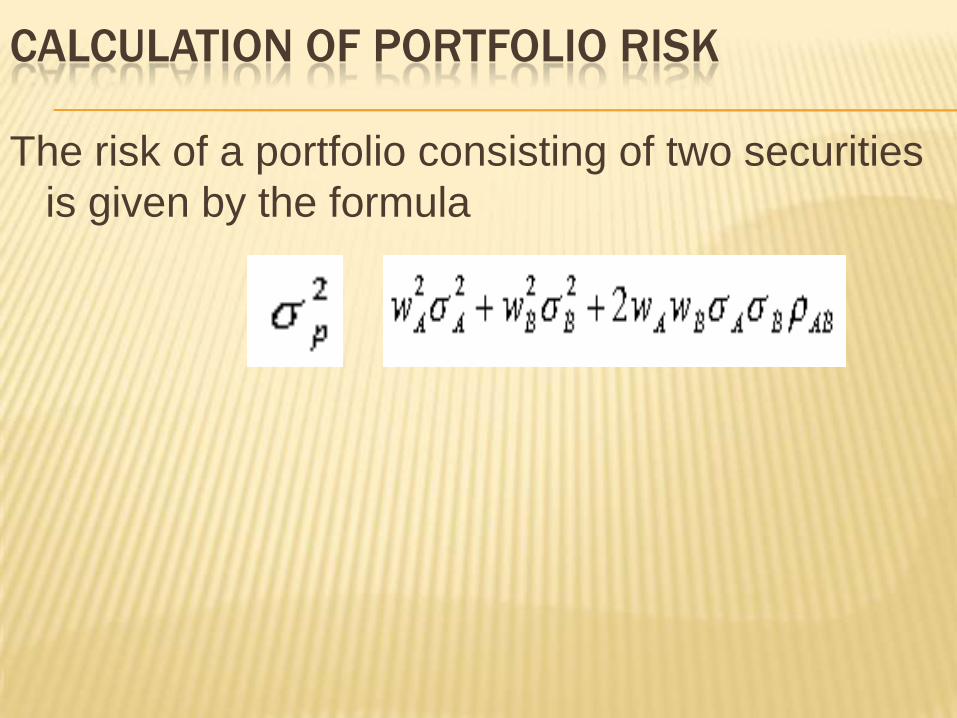

CALCULATION OF PORTFOLIO RISK

The risk of a portfolio consisting of two securities

is given by the formula

=

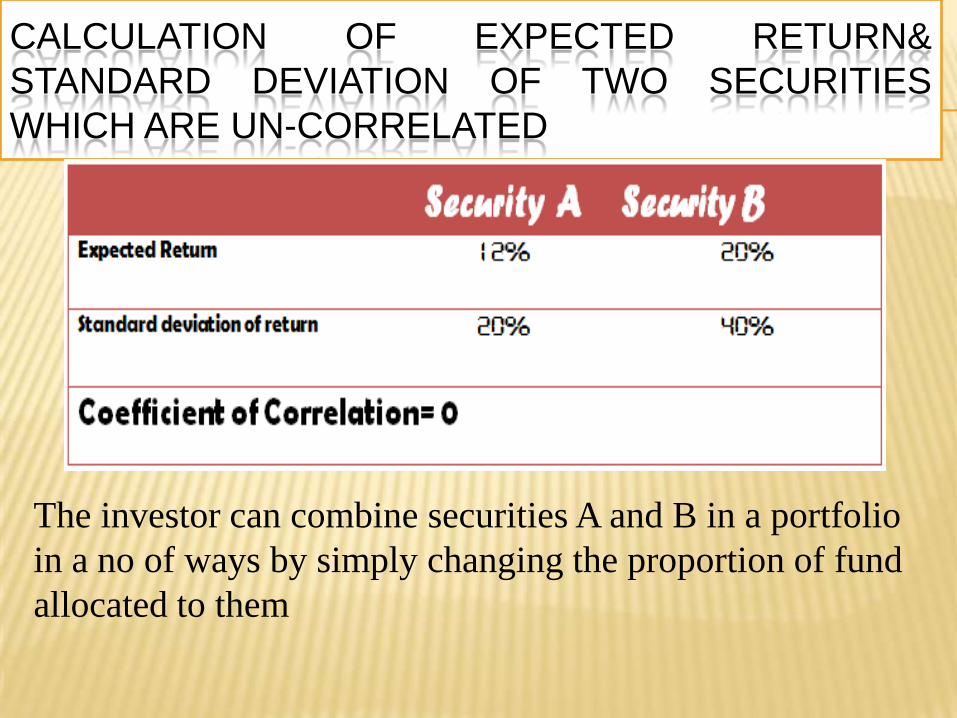

CALCULATION OF EXPECTED RETURN&

STANDARD DEVIATION OF TWO SECURITIES

WHICH ARE UN-CORRELATED

The investor can combine securities A and B in a portfolio

in a no of ways by simply changing the proportion of fund

allocated to them

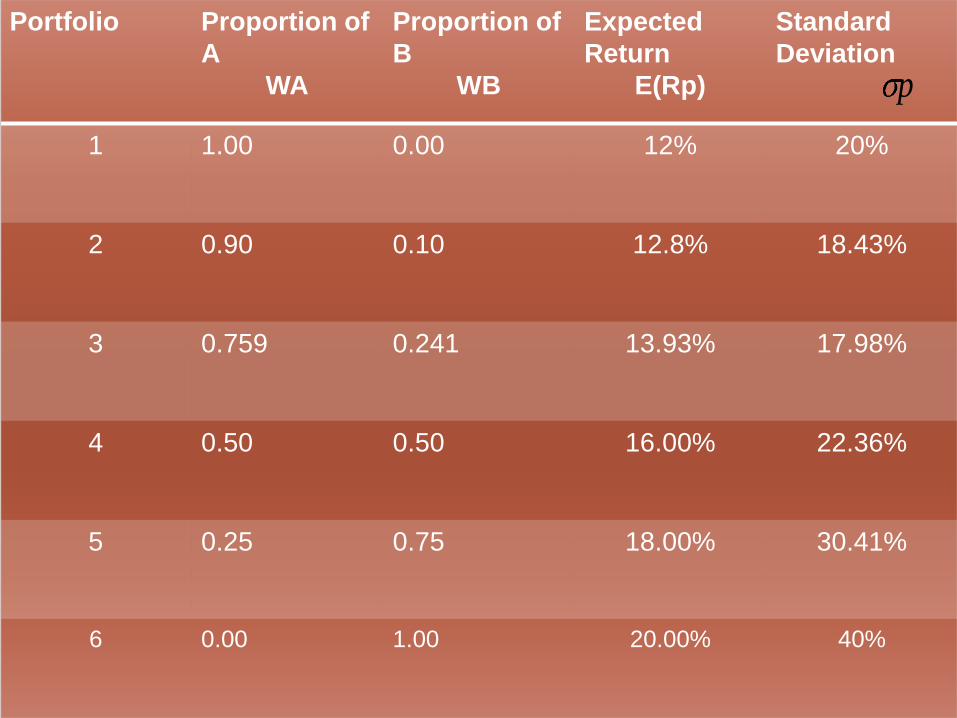

Portfolio Proportion of

A

WA

Proportion of

B

WB

Expected

Return

E(Rp)

Standard

Deviation

1 1.00 0.00 12% 20%

2 0.90 0.10 12.8% 18.43%

3 0.759 0.241 13.93% 17.98%

4 0.50 0.50 16.00% 22.36%

5 0.25 0.75 18.00% 30.41%

6 0.00 1.00 20.00% 40%

p

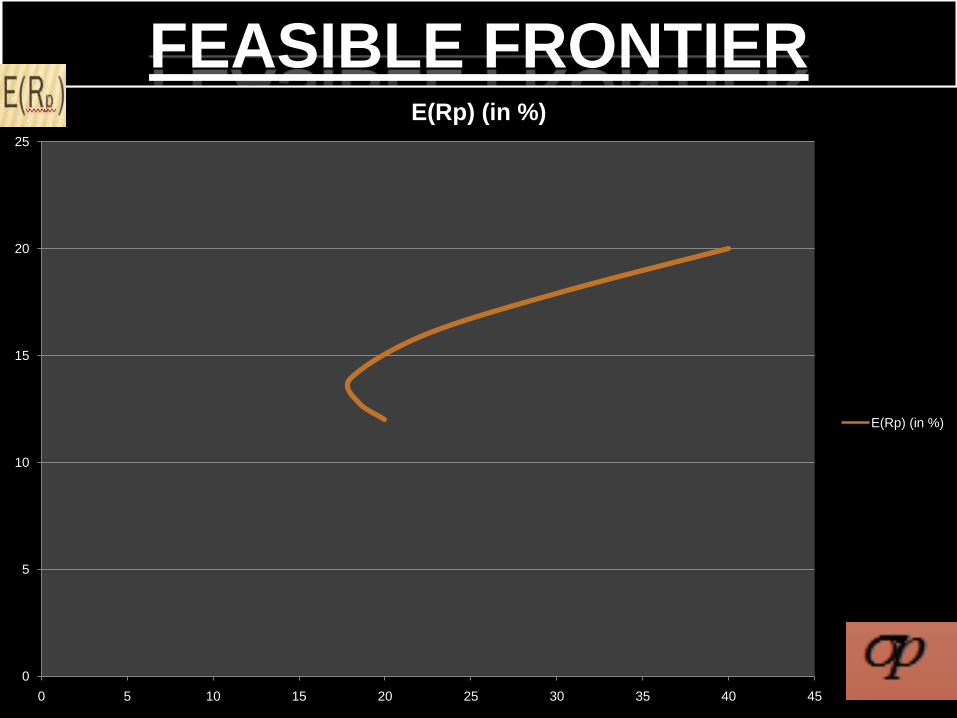

FEASIBLE FRONTIER

0

5

10

15

20

25

0 5 10 15 20 25 30 35 40 45

E(Rp) (in %)

E(Rp) (in %)

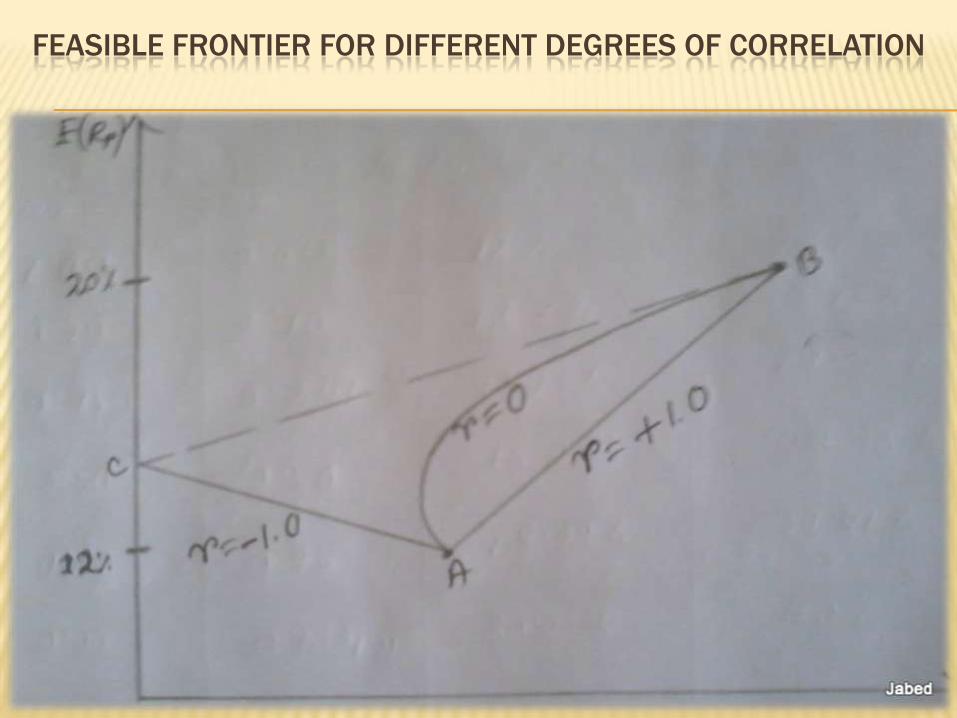

FEASIBLE FRONTIER FOR DIFFERENT DEGREES OF CORRELATION

For r=+1, diversification does not reduce risk.

For r=-1, diversification leads to reduction of risk

For r=0, i.e., when securities are un-

correlated, it indicates that they have no

measurable correlation in their price

movements.

C O N C L U S I O N

In practice, since no company is perfectly

isolated and independent from the global

economy, most companies stock prices are

some what correlated with the general

movement of the market