understanding accruals accounts

TRANSCRIPT

1

Understanding accruals accounts

Chris Smith FCIE

2

Types of Charity Accounts

Receipts & payments – sometimes called cash accounts

Accrued accounts

Who Must Prepare Accrued Accounts

All Companies

Non Company charities with income of £250,000 or more

Non Company charities with income less than £250,000, but where

Constitution

Enactment

Decision of trustees

Requires accrued accounts

Accrued Accounts

. Accrued accounts set out the true contractual position of the

charity.

They account for resources moving into and out of the charity as the charity become’s legally entitled to those resources or obliged to pay them out,

This is not necessarily the date on which money is received or paid out from the bank.

Financial Statements

Statement of Financial Activities or SoFA– Financial performance for the period– Income, expenditure and surplus or deficit– Reconciled to the opening and closing funds

The Balance Sheet– Financial position at year end– Assets, liabilities and funds

Total Funds on SoFA and Balance Sheet always equal

Preparing Accrued Accounts

Start with R&P or cash account

Adjust for:

– True contractual position

– Non-monetary resources

Exercise 1

Starting from the cash position what types of transactions or adjustments need to be made in preparing accrued accounts?

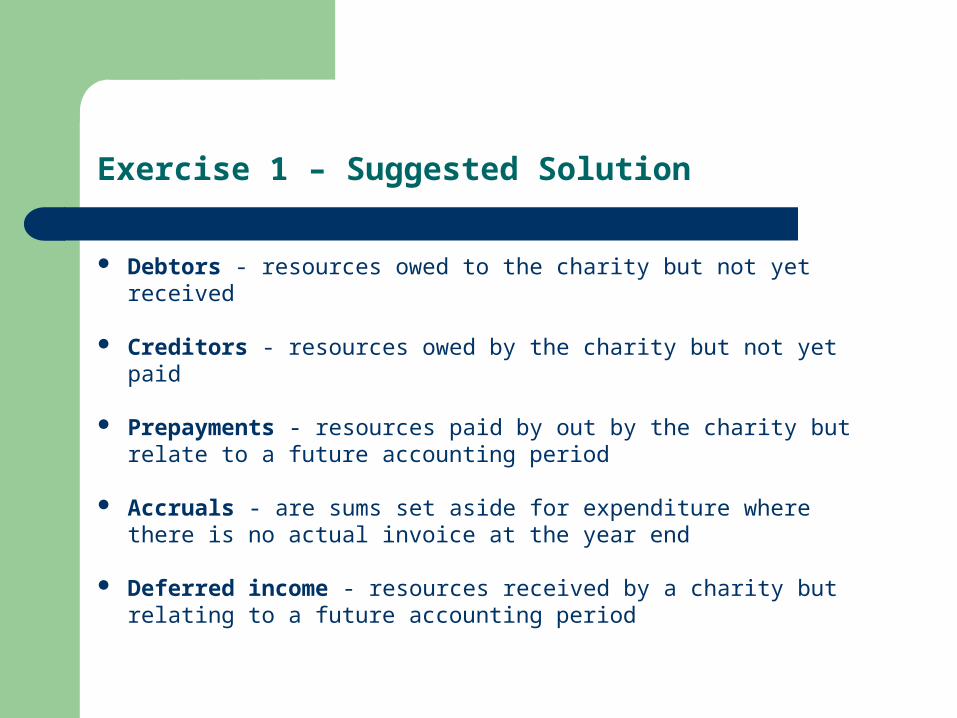

Exercise 1 – Suggested Solution

Debtors - resources owed to the charity but not yet received

Creditors - resources owed by the charity but not yet paid

Prepayments - resources paid by out by the charity but relate to a future accounting period

Accruals - are sums set aside for expenditure where there is no actual invoice at the year end

Deferred income - resources received by a charity but relating to a future accounting period

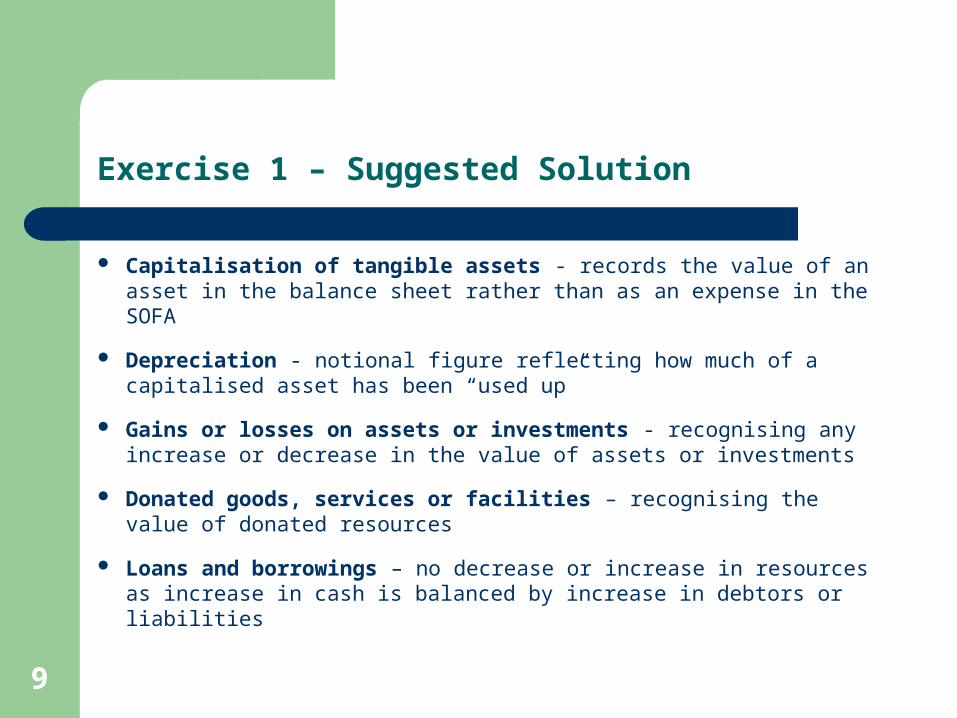

Exercise 1 – Suggested Solution

Capitalisation of tangible assets - records the value of an asset in the balance sheet rather than as an expense in the SOFA

Depreciation - notional figure reflecting how much of a capitalised asset has been “used up”

Gains or losses on assets or investments - recognising any increase or decrease in the value of assets or investments

Donated goods, services or facilities – recognising the value of donated resources

Loans and borrowings – no decrease or increase in resources as increase in cash is balanced by increase in debtors or liabilities

9

10

Main Differences Between Receipts & Payments and Accrued Accounts

Receipts and Payments AccruedIncome and expenditure accounted for when credited or debited from bank account or cash box.

The timing of income and expenditure adjusted to be accounted for during the period of the activity to which they relate or when a contractual obligation arises.

The purchase or sale of assets for cash included in statement of receipts and payments.

The purchase or sale of capitalised assets are not included in the SOFA. They do not represent resources moving into or out of the charity.

Assets listed as a note on the statement of assets and liabilities

Value of assets shown in balance sheet

Changes in value of assets are not included. Therefore depreciation also not included.

Changes in value of assets are included in the balance sheet. Depreciation included in SOFA

Debtors and creditors are not included in financial statements. They are listed as a note on the statement of assets and liabilities

Debtors and creditors are included in the balance sheet.

11

Any Questions on Accruals?

12

Charity Accounting - Funds

FUNDS

Restricted Unrestricted

Endowment Income

Permanent Expendable

Designated General

13

The Charities SORP (Statement of Recommended Practice)

Charities SORP 2005 - For accounting periods starting before 1 January 2015

Charities SORP (FRSSE) – For accounting periods starting in 2015. Only available to “smaller entities”

Charities SORP (FRS 102) – For accounting periods starting on or after 1 January 2015

14

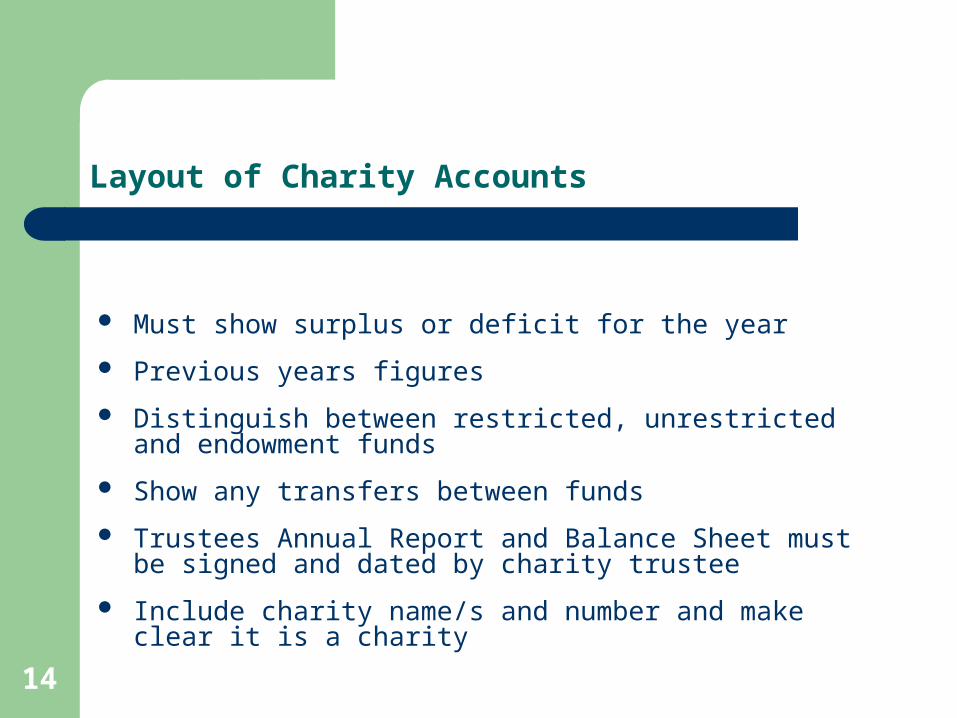

Layout of Charity Accounts

Must show surplus or deficit for the year Previous years figures Distinguish between restricted, unrestricted and endowment

funds Show any transfers between funds Trustees Annual Report and Balance Sheet must be signed

and dated by charity trustee Include charity name/s and number and make clear it is a

charity

15

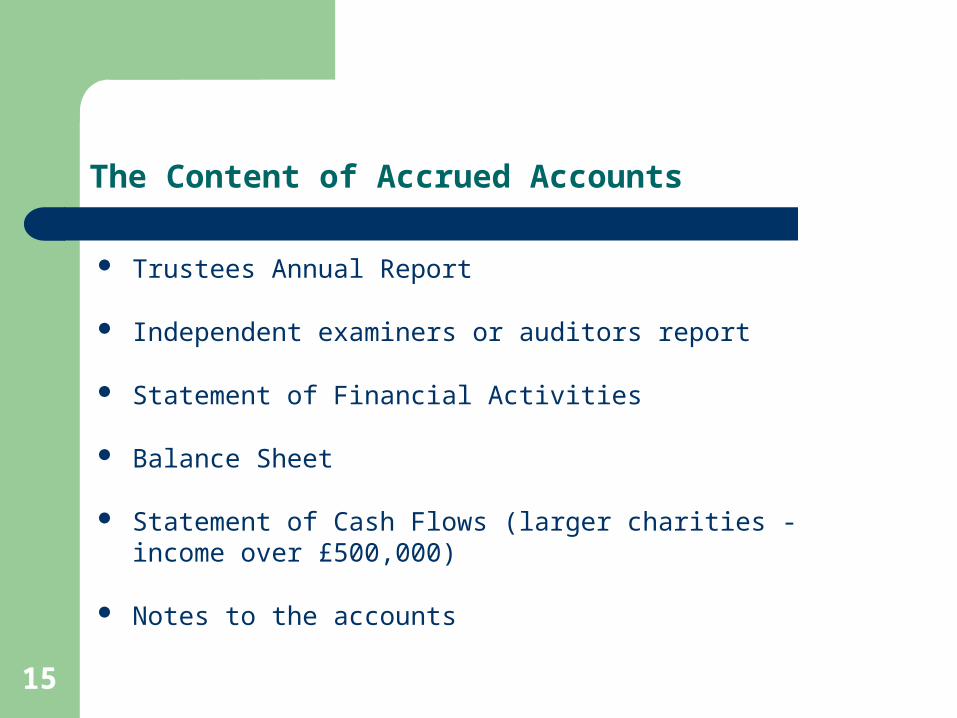

Trustees Annual Report

Independent examiners or auditors report

Statement of Financial Activities

Balance Sheet

Statement of Cash Flows (larger charities - income over £500,000)

Notes to the accounts

The Content of Accrued Accounts

Trustees Annual Report (TAR)

Objectives and activities

Achievements and performance

Financial review

Reference and administrative details

Structure governance and management

Statement on public benefit

Funds held on behalf of others as a custodian trustee or agent

Additional reporting by larger charities (para 1.35 – 1.54)

17

Statement of Financial Activities (SOFA)

Analysis of income and expenditure, reconciling surplus or deficit to opening & closing fund balances

Analysis by activity or nature (if under audit threshold)

Distinguish between different funds and show transfers

Same format as previous year with corresponding figures

Can omit lines with nothing in current and previous year

Income & expenditure recognised when probable, measurable and legally entitled to income or obligation to make payment

Format set out in Charities SORP (FRS102) – Table 2

Balance Sheet

Adopt the same format as for previous period

Signed and dated by a trustee

Provide additional information in other headings or sub headings if necessary to give a true and fair view

Provide a corresponding amount for the previous period,

Can omit lines with nothing in current and previous year

Value assets and liabilities at “fair value”

Recognition at “Present value” for assets and liabilities receivable or payable over several years

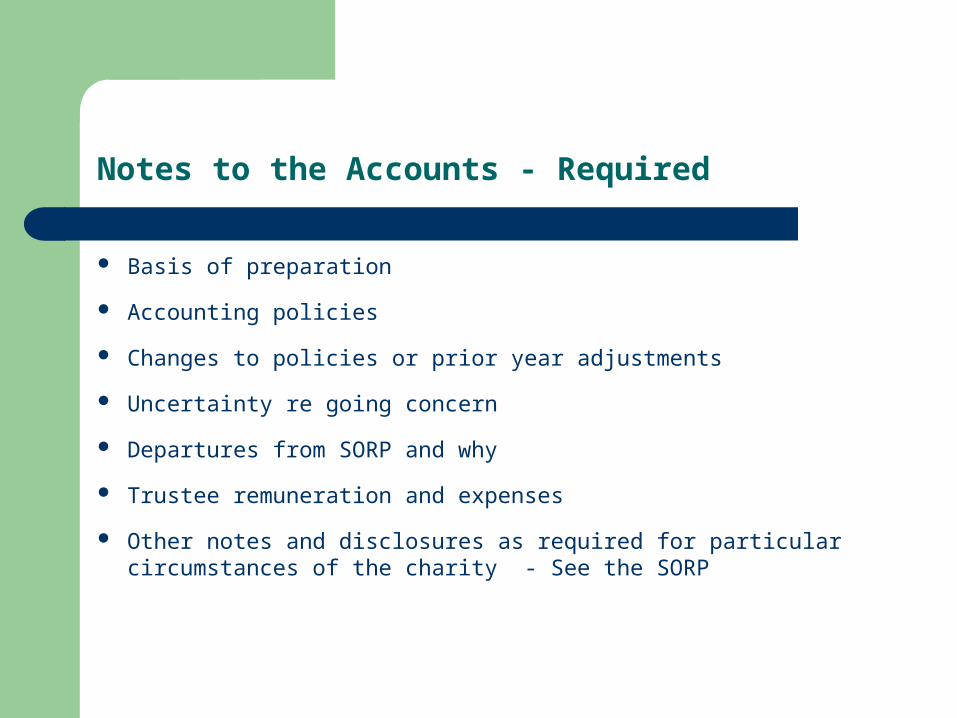

Notes to the Accounts - Required

Basis of preparation

Accounting policies

Changes to policies or prior year adjustments

Uncertainty re going concern

Departures from SORP and why

Trustee remuneration and expenses

Other notes and disclosures as required for particular circumstances of the charity - See the SORP

Exercise 2

Review the report and accounts for ACIE.

Is there anything you do not understand or want clarified?

20

21

Help and Support

Guidance from CCNI– ARR01 Charity reporting and accounting overall summary– ARR02 Charity reporting and accounting the essentials guidance– ARR04 Accruals accounts guidance– ARR07 Guidance for independent examiners– Template examiners reports - supporting document for independent

examiners Join Association of Charity Independent Examiners

– Training– Regular information mailings & newsletters– Helpline– www.acie.org.uk

22

ACIE - Membership

Affiliate

Associate - R&P to £100,00- R&P to £250,000- R&P to £250,000 and accruals to £100,000- All accounts to £100,000- All accounts to £250,000

Fellow - All accounts to the legal limit for IE

23

ACIE – Applying for full membership

Join as an affiliate Review your knowledge and experience against ACIE checklist Prepare two sets of accounts appropriate to the category of

membership you wish to apply for If not able to carry out IE get someone else to do the IE Complete application form with questions on theory and

practice of IE

24

Any questions?