understanding bills receivable, factoring, and banker’s ... · cfra, an independent research...

TRANSCRIPT

© CFRA. All rights reserved.

Understanding Bills Receivable, Factoring, and Banker’s Acceptance Notes in China May 29, 2014

David Bassett Nigel Fletcher [email protected] [email protected] Jennifer Latz [email protected]

© CFRA. All rights reserved.

About CFRA CFRA, an independent research provider, is the global leader in

forensic accounting research, analytics and advisory services

Our mission is to uncover underappreciated differences between reported financial results and underlying economic reality to help our clients make sound investment and risk management decisions

CFRA has been in operation since 1994 and we are a privately-held firm with operations in New York, London, Hong Kong, and Rockville, MD

2

© CFRA. All rights reserved.

CFRA Presenters

Jennifer Latz, CPA Ms. Jennifer Latz is a senior analyst on the CFRA Asia research team. Prior to joining CFRA in 2011, Jennifer worked in the New York office of Ziff Brothers Investments for almost 5 years. Before ZBI, Latz performed financial due diligence for KPMG's Transaction Services Group. Jennifer holds a Masters in Professional Accounting from the University of Texas at Austin, and a B.A. from the University of Michigan.

© CFRA. All rights reserved.

CFRA Presenters

Nigel Fletcher Mr. Nigel Fletcher joined CFRA in February 2012 as an analyst within the Financials Team focusing on non-US banks and insurers. Prior to joining CFRA, Nigel was an analyst at Silkroute Financial in London covering emerging market banks in the Central/Eastern European region. Before this he was an associate at Keefe, Bruyette & Woods in London, a financial sector dedicated investment bank. Nigel holds an LLM in International Commercial Law from the University of Nottingham and an LLB (Hons) in Law with Economics from Durham University.

© CFRA. All rights reserved.

CFRA Presenters

David Bassett, CFA Mr. David Bassett is a forensic accounting analyst at CFRA. Before joining the CFRA Asia research team in 2011, he spent time covering the consumer and TMT space, as well as conducting Bespoke research, which is CFRA’s custom research offering. David joined CFRA in 2003. David's research has been cited in several leading business publications including BusinessWeek, Barron's and the Wall Street Journal. David earned his B.S. in Business Management with an emphasis in Finance from Brigham Young University.

© CFRA. All rights reserved. 6 www.cfraresearch.com

Asia Performance

© CFRA. All rights reserved. 7 www.cfraresearch.com

Questions can be submitted to: [email protected] or by using the submit questions functionality through the webinar tool. All questions will be answered anonymously at the end of the prepared discussion.

© CFRA. All rights reserved.

Part 1: Bankers’ Acceptance Notes

© CFRA. All rights reserved.

Understanding Banker’s Acceptance Notes at Chinese Banks: Background Short-term debt instrument with an unconditional

guarantee of a bank; Form is not unique, but use is: - accounting treatment; - re-discount and repo transactions; Concerns: - lower-quality deposits; - hides ‘lending’ off-balance sheet; - has become a “shadow currency”.

9 www.cfraresearch.com

© CFRA. All rights reserved.

Bankers Acceptance Notes

“The truth is, most BANs are not used to support real transactions,” says a grinning shadow banker in Shenzhen. His company is one of many Chinese conglomerates whose business tentacles seem to span every industry from mining to tourism. But nearly half of its transactions are unprofitable: they are formalities, conducted solely for the purpose of acquiring BANs. – From the Diplomat, December 12, 2013, article by

Matthew Lowenstein, “China’s Shadow Currency”

10 www.cfraresearch.com

© CFRA. All rights reserved.

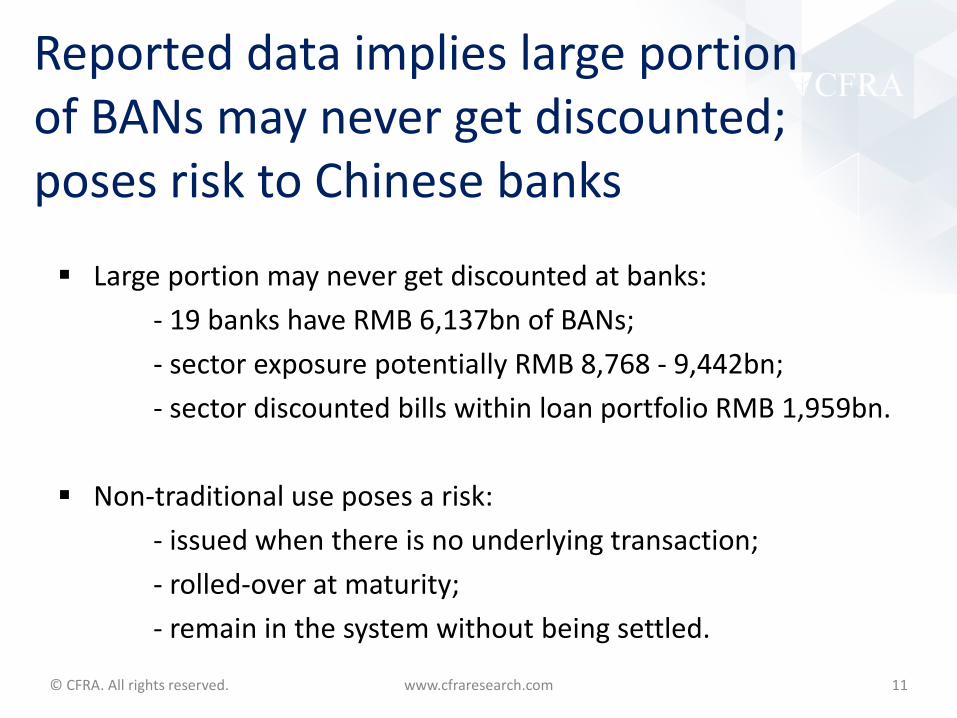

Reported data implies large portion of BANs may never get discounted; poses risk to Chinese banks

Large portion may never get discounted at banks: - 19 banks have RMB 6,137bn of BANs; - sector exposure potentially RMB 8,768 - 9,442bn; - sector discounted bills within loan portfolio RMB 1,959bn.

Non-traditional use poses a risk: - issued when there is no underlying transaction; - rolled-over at maturity; - remain in the system without being settled.

11 www.cfraresearch.com

© CFRA. All rights reserved.

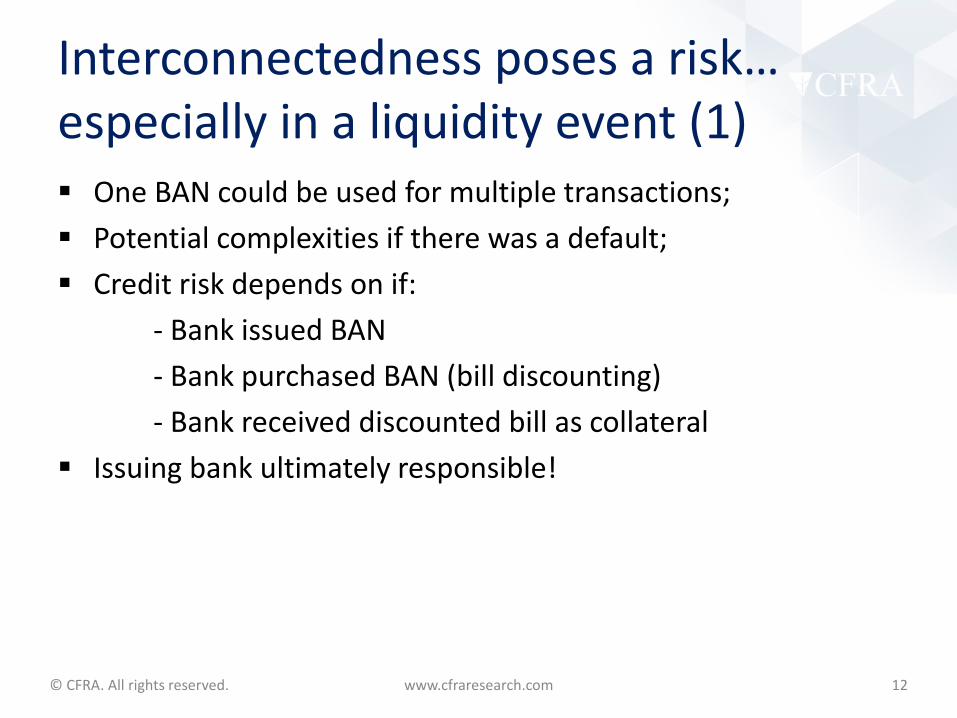

Interconnectedness poses a risk… especially in a liquidity event (1) One BAN could be used for multiple transactions; Potential complexities if there was a default; Credit risk depends on if: - Bank issued BAN - Bank purchased BAN (bill discounting) - Bank received discounted bill as collateral Issuing bank ultimately responsible!

12 www.cfraresearch.com

© CFRA. All rights reserved.

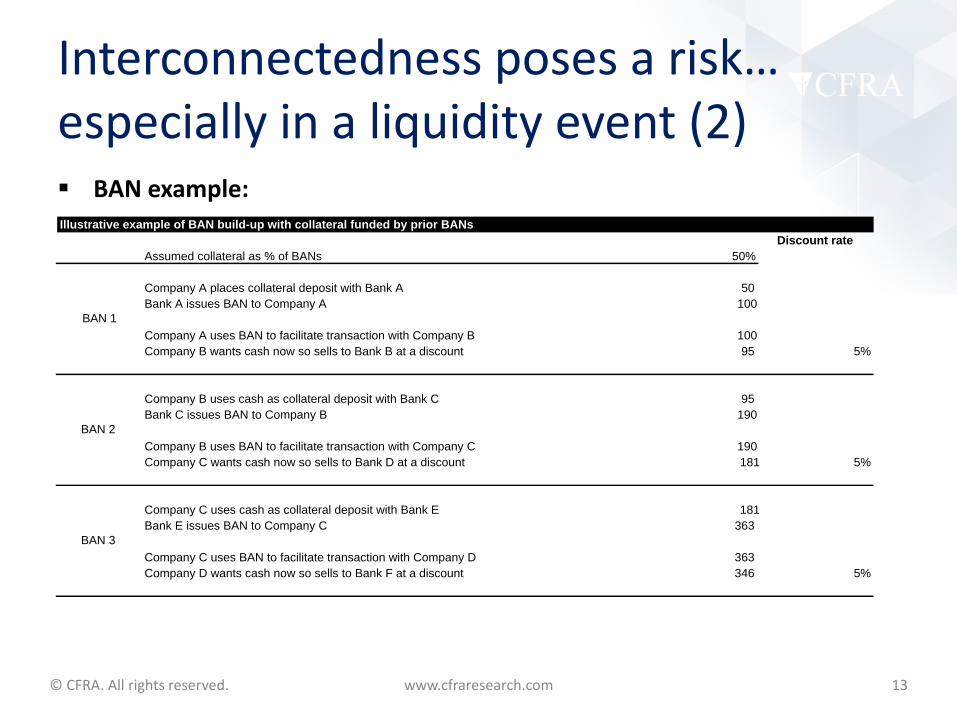

Interconnectedness poses a risk… especially in a liquidity event (2) BAN example:

13 www.cfraresearch.com

Discount rateAssumed collateral as % of BANs 50%

Company A places collateral deposit with Bank A 50Bank A issues BAN to Company A 100

Company A uses BAN to facilitate transaction with Company B 100Company B wants cash now so sells to Bank B at a discount 95 5%

Company B uses cash as collateral deposit with Bank C 95Bank C issues BAN to Company B 190

Company B uses BAN to facilitate transaction with Company C 190Company C wants cash now so sells to Bank D at a discount 181 5%

Company C uses cash as collateral deposit with Bank E 181Bank E issues BAN to Company C 363

Company C uses BAN to facilitate transaction with Company D 363Company D wants cash now so sells to Bank F at a discount 346 5%

BAN 1

BAN 2

BAN 3

Illustrative example of BAN build-up with collateral funded by prior BANs

© CFRA. All rights reserved.

Interconnectedness poses a risk… especially in a liquidity event (3) Discounted bill example:

14 www.cfraresearch.com

CollateralCollateral

Collateral

Sells bill

Cash

Funding

Funding

© CFRA. All rights reserved.

Interconnectedness poses a risk… especially in a liquidity event (4) If a negative event resulted in a loss in faith… …would there be enough funds to honor this commitment;

Exposure sizeable as % of liquid assets for small/mid banks; Other connected transactions also present a risk.

15 www.cfraresearch.com

57.1% 52.4% 48.1% 46.8% 45.6% 44.2% 43.8% 34.6% 31.5% 29.0% 27.1% 24.3%

19.4% 17.5% 11.2% 8.3% 8.1% 5.5% 2.5%

0.0%10.0%20.0%30.0%40.0%50.0%60.0%

CITI

C Ba

nk

Ever

brig

ht

Hua

Xia

Hui

shan

g

Ping

An

Bank

Cho

ngqi

ng

Min

shen

g

Shan

ghai

Pud

ong

Bcom

m

Nan

jing

Mer

chan

ts

Indu

stria

l

Beiji

ng

Nin

gbo

BoC

CCB

ABC

ICBC

CRCB

BANs / Cash (less reserves) + liquid investments

© CFRA. All rights reserved.

Incentives: BANs aid deposit collection Collateral must be pledged for BANs; Additional deposits: - improves the loan-to-deposit ratio; - more loans potentially originated; Aids compliance with regulatory loan-to-deposit ratio.

16 www.cfraresearch.com

RMB m Delta Delta Delta (1) (2)ytd chg ytd chg ytd chg as % of as % of

2012 2013 (1) 2012 2013 (2) 2012 2013 (3) (3) (3)ICBC N.D N.D N.A N.D N.D N.A 13,680,919 14,620,825 939,906 N.A N.AChina Construction Bank 124,367 129,392 5,025 393,698 419,974 26,276 11,444,302 12,223,037 778,735 1% 3%Agricultural Bank of China 70,409 89,842 19,433 216,879 247,656 30,777 10,862,935 11,811,411 948,476 2% 3%Bank of China N.D N.D N.A 373,305 438,174 64,869 9,009,978 9,941,288 931,310 N.A 7%Bank of Communications N.D N.D N.A 399,290 594,655 195,365 3,728,412 4,157,833 429,421 N.A 45%China Merchants Bank N.D N.D N.A N.D N.D N.A 2,532,444 2,775,276 242,832 N.A N.AIndustrial Bank N.D N.D N.A N.D N.D N.A 1,813,266 2,170,345 357,079 N.A N.AShanghai Pudong Development Bank N.D N.D N.A 345,805 350,781 4,976 2,134,365 2,419,696 285,331 N.A 2%CITIC Bank Corp 309,526 302,969 -6,557 410,391 443,134 32,743 2,266,734 2,664,396 397,662 -2% 8%China Minsheng Bank 279,918 268,516 -11,402 361,114 386,203 25,089 1,926,194 2,146,689 220,495 -5% 11%China Everbright Bank 184,085 207,803 23,718 221,962 252,330 30,368 1,426,941 1,605,278 178,337 13% 17%Ping An Bank N.D N.D N.A 205,573 242,338 36,765 1,021,108 1,217,002 195,894 N.A 19%Hua Xia Bank 141,806 137,135 -4,671 176,944 181,050 4,106 1,036,000 1,177,592 141,592 -3% 3%Bank of Beijing N.D N.D N.A 40,757 52,654 11,897 713,772 834,480 120,707 N.A 10%Chongqing Rural Commercial Bank 3,033 3,164 131 4,477 4,923 446 294,510 347,883 53,373 0% 1%Bank Ningbo N.D N.D N.A 19,453 21,031 1,578 207,577 255,278 47,701 N.A 3%Bank of Nanjing 22,018 28,195 6,177 29,829 33,856 4,028 213,656 260,149 46,494 13% 9%Huishang Bank N.D N.D N.A 26,579 32,355 5,776 239,543 272,798 33,255 N.A 17%Bank of Chongqing N.D N.D N.A 13,147 20,287 7,140 114,043 148,801 34,758 N.A 21%* Total pledged deposits include collateral for bank acceptances, letters of credit and guarantees and other pledged deposits.

deposits*Customerdeposits

Pledged deposits forbanker's acceptance

Total pledged

© CFRA. All rights reserved.

Incentives: Leverage can be increased without appearing at risk (outside of regulatory limits) All the credit risk of lending but off-balance sheet; Leverage of 19 bank shifts from 15.4x to 16.4x including BANs; Potential for lack of transparency as off-balance sheet

exposures; Allow to side step any regulatory limits (i.e. loan quotas).

17 www.cfraresearch.com

© CFRA. All rights reserved.

Incentives: Lower capital requirements Lower capital requirement than corporate loans; Benefits capital ratios; Effectively require half the risk-weight of corporate loans;

18 www.cfraresearch.com

RMBm

2012 2013 2012 2013 2012 2013ICBC 2,076,206 2,445,956 817,008 917,567 39.4% 37.5%CCB 2,016,299 2,310,227 908,026 899,272 45.0% 38.9%ABC 1,489,391 1,481,945 710,782 728,028 47.7% 49.1%BoC 2,317,505 2,499,810 754,824 981,223 32.6% 39.3%Bcomm 1,363,676 1,550,719 449,980 N.D 33.0% N.DMerchants 725,317 963,435 300,994 362,533 41.5% 37.6%Industrial 543,468 676,586 N.D N.D N.D N.DShanghai Pudong 792,451 842,398 N.D N.D N.D N.DCITIC Bank 1,117,527 1,243,204 414,221 428,172 37.1% 34.4%Minsheng 877,715 850,201 352,776 327,515 40.2% 38.5%Everbright 676,121 752,538 298,095 319,225 44.1% 42.4%Ping An 410,971 501,182 171,952 181,995 41.8% 36.3%HuaXia 373,869 387,967 N.D N.D N.D N.DBeijing 162,563 190,931 N.D N.D N.D N.DCRCB 6,920 8,287 1,547 2,939 22.4% 35.5%Ningbo 78,098 104,418 24,493 31,923 31.4% 30.6%Nanjing 79,291 98,951 N.D N.D N.D N.DHuishang 52,476 59,647 22,413 35,831 42.7% 60.1%Bank Chongqing 27,335 38,001 9,518 5,978 34.8% 15.7%

credit commitments credit commitments total off bal sheet)

Total off-balance Credit risk-weight Risk weightsheet contingent liab & amount of cont. liab & (credit risk-weight /

© CFRA. All rights reserved.

Who are the most exposed Chinese banks? (1) Everbright, CITIC Bank and Ping An have the largest exposure to BANs as a

percent of 2013 adjusted assets; CFRA analyzes the exposure of the Chinese banks to BANs by adjusting

assets to assume the exposure is on-balance sheet.

19 www.cfraresearch.com

RMB m

2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013ICBC 15.5 14.8 341,033 327,048 17,883,250 19,244,800 15.8 15.1 1.9% 1.7% 30.2% 25.6%China Construction Ban 14.7 14.3 344,848 360,499 14,317,676 15,723,709 15.1 14.6 2.4% 2.3% 36.3% 33.6%Agricultural Bank of Ch 17.6 17.2 397,311 404,852 13,641,653 14,966,954 18.2 17.7 2.9% 2.7% 52.9% 47.9%Bank of China 14.7 14.4 396,460 465,496 13,077,075 14,339,795 15.2 14.9 3.0% 3.2% 46.0% 48.4%Bank of Communication 13.8 14.1 517,946 612,830 5,791,325 6,573,767 15.2 15.6 8.9% 9.3% 135.8% 145.4%China Merchants Bank 17.0 15.1 301,399 354,816 3,709,498 4,371,215 18.5 16.4 8.1% 8.1% 150.4% 133.4%Industrial Bank 19.1 18.3 392,352 452,710 3,643,327 4,130,145 21.4 20.5 10.8% 11.0% 229.9% 225.0%Shanghai Pudong Deve 17.5 17.8 521,767 502,094 3,667,474 4,182,219 20.4 20.2 14.2% 12.0% 290.4% 242.3%CITIC Bank Corp 14.6 15.8 666,007 695,944 3,625,946 4,337,137 17.9 18.8 18.4% 16.0% 327.9% 301.6%China Minsheng Bank 19.1 15.8 586,654 522,849 3,798,655 3,749,059 22.5 18.4 15.4% 13.9% 348.1% 255.9%China Everbright Bank 19.9 15.8 407,585 469,996 2,686,880 2,885,082 23.5 18.9 15.2% 16.3% 356.5% 307.1%Ping An Bank 18.9 16.9 315,436 359,583 1,921,972 2,251,324 22.7 20.1 16.4% 16.0% 372.0% 320.8%Hua Xia Bank 19.9 19.4 296,998 286,995 1,785,858 1,959,442 23.9 22.8 16.6% 14.6% 397.5% 333.6%Bank of Beijing 15.6 17.1 81,945 117,579 1,201,914 1,454,343 16.8 18.6 6.8% 8.1% 114.3% 150.2%Chongqing Rural Comm 13.5 13.6 4,667 5,808 438,494 508,254 13.6 13.8 1.1% 1.1% 14.5% 15.7%Bank Ningbo 16.9 18.3 38,321 40,925 411,018 508,697 18.6 19.9 9.3% 8.0% 173.3% 160.4%Bank of Nanjing 13.9 16.2 57,348 68,408 401,140 502,465 16.2 18.7 14.3% 13.6% 231.1% 254.7%Huishang Bank 15.8 12.1 46,602 52,567 370,826 434,676 18.1 13.7 12.6% 12.1% 227.5% 166.0%Bank of Chongqing 18.9 15.3 26,461 36,329 182,625 243,116 22.1 18.0 14.5% 14.9% 320.4% 269.5%Total of sample 15.9 15.4 5,741,138 6,137,328 92,556,605 102,366,199 17.0 16.4 6.2% 6.0% 105.4% 98.1%* adjusted assets defined as total assets + bankers' acceptances

Asset / equity (x) bankers' acceptance total assets*Adjusted assets / Bankers' acceptance

as % of adj assetsBankers' acceptance

as % of equityequity (x)Off-balance sheet Adjusted

© CFRA. All rights reserved.

Who are the most exposed Chinese banks? (2) Hua Xia, Minsheng and Chongqing have the largest total

exposure as a percentage of 2013 adjusted assets; Total exposure = BANs + discounted bills + reverse repos

collateralized by discounted bills.

20 www.cfraresearch.com

RMB m

2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013ICBC 73,358 61,876 180,292 148,258 253,650 210,134 341,033 327,048 594,683 537,182 3.3% 2.8% 52.7% 42.0%China Construction Ban 94,612 19,876 137,558 116,962 232,170 136,838 344,848 360,499 577,018 497,337 4.0% 3.2% 60.8% 46.3%Agricultural Bank of Ch 307,047 332,921 112,706 97,993 419,753 430,914 397,311 404,852 817,064 835,766 6.0% 5.6% 108.7% 99.0%Bank of China 0 22,196 166,650 128,445 166,650 150,641 396,460 465,496 563,110 616,137 4.3% 4.3% 65.4% 64.1%Bank of Communication N/D N/D 64,769 60,443 517,946 612,830China Merchants Bank 935 43,696 64,842 71,035 65,777 114,731 301,399 354,816 367,176 469,547 9.9% 10.7% 183.2% 176.6%Industrial Bank 370,452 352,626 17,042 14,605 387,494 367,231 392,352 452,710 779,846 819,941 21.4% 19.9% 457.0% 407.6%Shanghai Pudong Deve 258,520 256,487 55,124 33,690 313,644 290,177 521,767 502,094 835,411 792,271 22.8% 18.9% 465.0% 382.3%CITIC Bank Corp N.D N.D 74,994 64,769 666,007 695,944China Minsheng Bank 616,805 383,494 15,764 33,364 632,569 416,858 586,654 522,849 1,219,223 939,707 32.1% 25.1% 723.4% 460.0%China Everbright Bank 184,001 119,638 12,643 13,464 196,644 133,102 407,585 469,996 604,229 603,098 22.5% 20.9% 528.5% 394.0%Ping An Bank 64,649 55,938 10,410 12,338 75,059 68,276 315,436 359,583 390,495 427,859 20.3% 19.0% 460.5% 381.7%Hua Xia Bank 237,109 117,022 2,605 5,268 239,714 122,290 296,998 286,995 536,712 409,285 30.1% 20.9% 718.3% 475.8%Bank of Beijing 79,226 114,328 10,224 6,290 89,450 120,619 81,945 117,579 171,395 238,198 14.3% 16.4% 239.1% 304.2%Chongqing Rural Comm 26,389 14,649 5,256 1,508 31,646 16,157 4,667 5,808 36,312 21,965 8.3% 4.3% 112.7% 59.5%Bank Ningbo 33,512 33,402 6,304 3,183 39,816 36,585 38,321 40,925 78,136 77,509 19.0% 15.2% 353.3% 303.7%Bank of Nanjing 40,144 37,164 3,995 3,672 44,139 40,836 57,348 68,408 101,487 109,244 25.3% 21.7% 409.0% 406.8%Huishang Bank 38,198 35,538 11,907 9,725 50,105 45,263 46,602 52,567 96,707 97,830 26.1% 22.5% 472.2% 308.9%Bank of Chongqing 16,150 18,396 6,458 5,245 22,608 23,642 26,461 36,329 49,069 59,971 26.9% 24.7% 594.2% 444.9%

off & on-bal sheet off & on-bal sheetTotal exposure Total exposure

discounted bills customer loans on balance sheet as % of adj assets as % of equitycollateralized by within to discounted bills bankers' acceptance off & on-bal sheetReverse repos Discounted bills Total exposure Off-balance sheet Total exposure

© CFRA. All rights reserved.

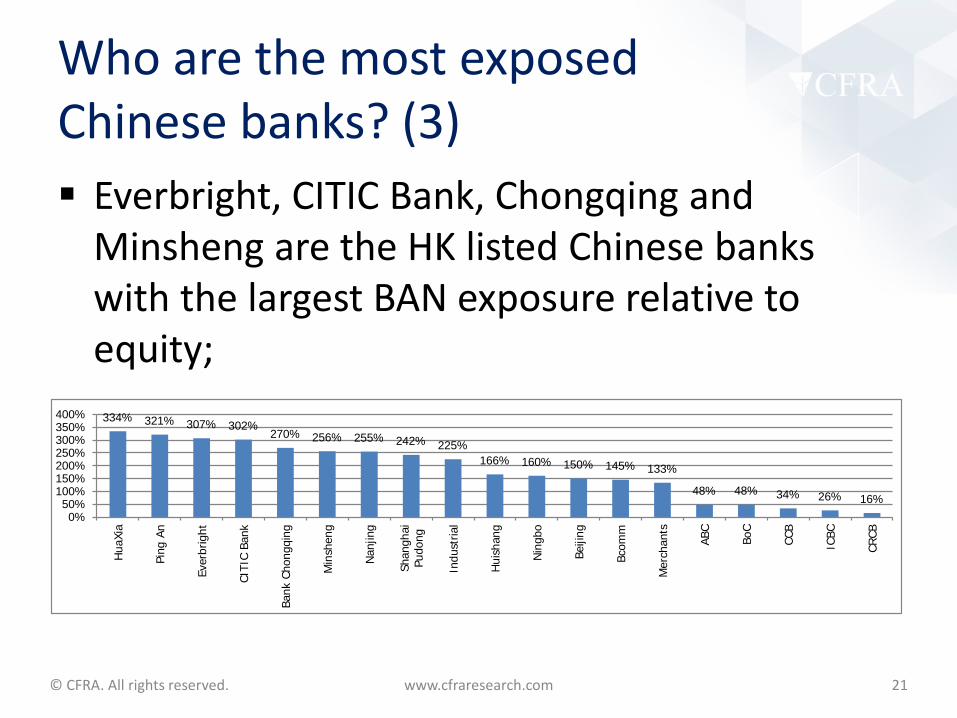

Who are the most exposed Chinese banks? (3) Everbright, CITIC Bank, Chongqing and

Minsheng are the HK listed Chinese banks with the largest BAN exposure relative to equity;

21 www.cfraresearch.com

334% 321% 307% 302%270% 256% 255% 242% 225%

166% 160% 150% 145% 133%

48% 48% 34% 26% 16%0%

50%100%150%200%250%300%350%400%

Hua

Xia

Ping

An

Ever

brig

ht

CITI

C Ba

nk

Bank

Cho

ngqi

ng

Min

shen

g

Nan

jing

Shan

ghai

Pudo

ng

Indu

stria

l

Hui

shan

g

Nin

gbo

Beiji

ng

Bcom

m

Mer

chan

ts

ABC

BoC

CCB

ICBC

CRCB

© CFRA. All rights reserved. 22 www.cfraresearch.com

Questions can be submitted to: [email protected] or by using the submit questions functionality through the webinar tool. All questions will be answered anonymously at the end of the prepared discussion.

© CFRA. All rights reserved.

Part 2: Bills Receivable

© CFRA. All rights reserved.

What are Bills Receivable?

We don’t commonly see them outside of Chinese companies.

“Official” accounting definitions are evasive. Common nomenclature includes: “Bills

Receivable” and “Notes Receivable” within annual / financial reports.

The corporate side of BANs. Hengan 2013 annual report: “Trade and bills

receivables are amounts due from customers for merchandise sold or services performed in the ordinary course of business.”

24 www.cfraresearch.com

© CFRA. All rights reserved.

What are Bills Receivable? (cont’d) Bills Receivable may be further disaggregated into

Commercial Acceptance Bills and Bank Acceptance Bills.

Commercial acceptance - similar to Commercial Paper. – Promissory note issued by corporates. No bank

guarantee. – Generally short-term; from a couple of days to not more

than a year. – Not secured by company assets; generally restricted to

higher quality-rated companies.

25 www.cfraresearch.com

© CFRA. All rights reserved.

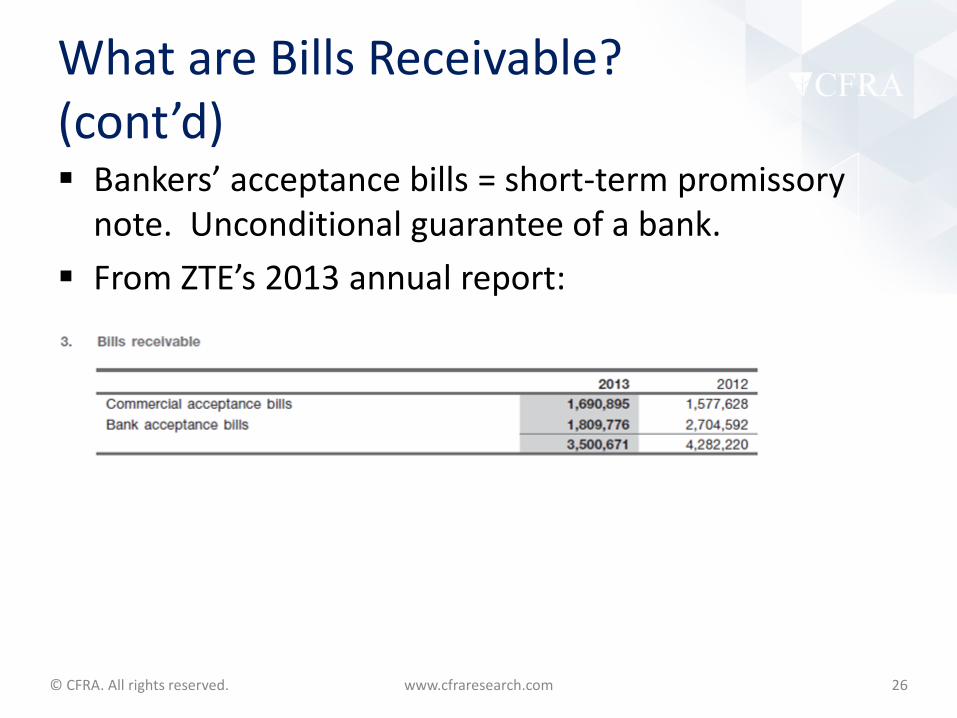

What are Bills Receivable? (cont’d) Bankers’ acceptance bills = short-term promissory

note. Unconditional guarantee of a bank. From ZTE’s 2013 annual report:

26 www.cfraresearch.com

© CFRA. All rights reserved.

What are Bills Receivable? (cont’d) Anecdotally, bills receivable typically have longer

terms than accounts receivable. Bills receivable terms are generally 3-6 months as a loose guide.

From the Nine Dragons Paper (Holdings) Limited 2013 annual report:

“The Group’s credit sales to corporate customers are entered into on credit terms of 30 to 60 days….Bills receivables from third parties are normally with maturity period of 90 to 180 days...”

27 www.cfraresearch.com

© CFRA. All rights reserved.

What are Bills Receivable? (cont’d) Another example from the CNBM (3323.HK)

2013 annual report: “The Group normally allowed an average of

credit period of 60-180 days to its trade customers….The bills receivable is aged within six months.”

28 www.cfraresearch.com

© CFRA. All rights reserved.

How Should We Analyze Bills Receivable? CFRA treats bills receivable as trade

receivables for various ratio analysis. For example, in calculating how long it takes

for companies to collect receivables (Days Sales Outstanding or “DSO”), CFRA includes bills receivable as part of trade receivables.

29 www.cfraresearch.com

© CFRA. All rights reserved.

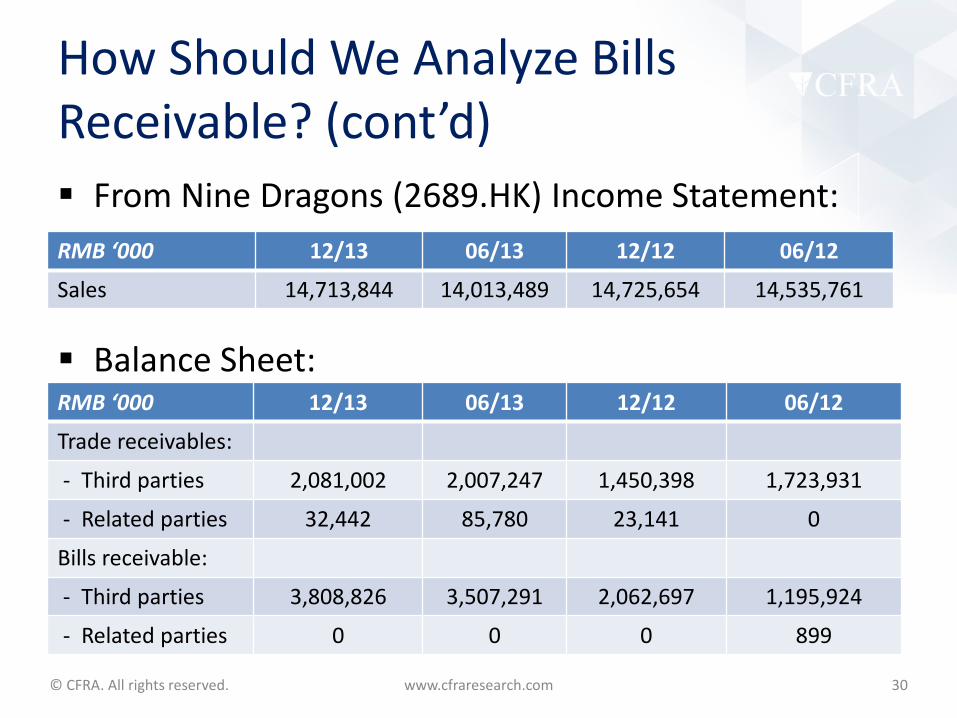

How Should We Analyze Bills Receivable? (cont’d) From Nine Dragons (2689.HK) Income Statement:

Balance Sheet:

30 www.cfraresearch.com

RMB ‘000 12/13 06/13 12/12 06/12

Sales 14,713,844 14,013,489 14,725,654 14,535,761

RMB ‘000 12/13 06/13 12/12 06/12

Trade receivables:

- Third parties 2,081,002 2,007,247 1,450,398 1,723,931

- Related parties 32,442 85,780 23,141 0

Bills receivable:

- Third parties 3,808,826 3,507,291 2,062,697 1,195,924

- Related parties 0 0 0 899

© CFRA. All rights reserved.

How Should We Analyze Bills Receivable? (cont’d)

31 www.cfraresearch.com

RMB ‘000 12/13 06/13 12/12

Management DSO termed as “turnover days of trade receivables”*

26 27 18

CFRA calculated DSO^ 73 73 44

There is a difference of 47 days in H1/14 between CFRA-calculated DSO, which includes bills receivable, versus Management-calculated DSO, which excludes bills receivable

*Calculated as: 182.5 days / (Half-year sales / Trade Receivables) ^Calculated as: 182.5 days / (Half-year sales / ((Trade Receivables + Bills Receivables)))

© CFRA. All rights reserved.

How Should We Analyze Bills Receivable? (cont’d) In Nine Dragons case, Management changed its definition of

turnover calculation. It went from “turnover days for debtors” to “turnover days of trade receivables” – Consciously excluding bills receivable as they rose

32 www.cfraresearch.com

RMB ‘000 12/13 06/13 12/12 06/12

Management DSO 26 27 18 39

CFRA calculated DSO^ 73 73 44 37

“turnover days for debtors”

*Calculated as: 182.5 days / (Half-year sales / Trade Receivables) ^Calculated as: 182.5 days / (Half-year sales / ((Trade Receivables + Bills Receivables)))

“turnover days of trade receivables” (e.g. Mgmt. excluding bills receivable

© CFRA. All rights reserved.

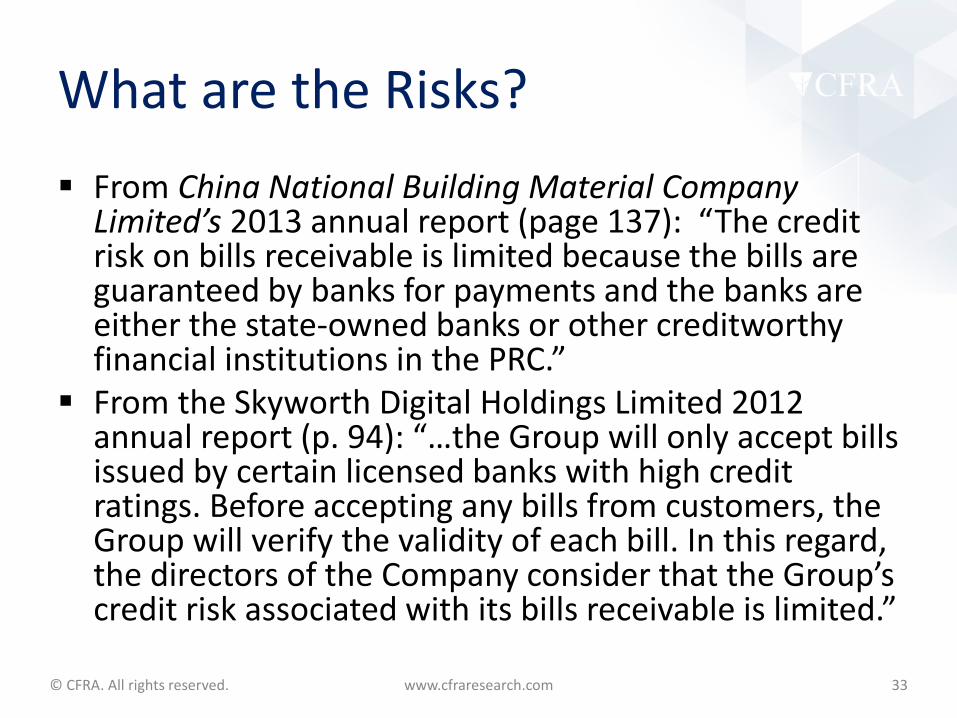

What are the Risks? From China National Building Material Company

Limited’s 2013 annual report (page 137): “The credit risk on bills receivable is limited because the bills are guaranteed by banks for payments and the banks are either the state-owned banks or other creditworthy financial institutions in the PRC.”

From the Skyworth Digital Holdings Limited 2012 annual report (p. 94): “…the Group will only accept bills issued by certain licensed banks with high credit ratings. Before accepting any bills from customers, the Group will verify the validity of each bill. In this regard, the directors of the Company consider that the Group’s credit risk associated with its bills receivable is limited.”

33 www.cfraresearch.com

© CFRA. All rights reserved.

What are the Risks? (cont’d) Should we treat bills receivable as cash? We don’t typically see the language from CNBM and

Skyworth on the previous slide. Some things to consider with respect to bills receivable

risks: – What CNBM considers as a “creditworthy financial

institutions in the PRC” may be highly subjective – It is not clear the extent to which bills receivable are

regulated. Are Chinese trust companies, which are much less regulated than Chinese banks, also issuing bankers’ acceptances?

34 www.cfraresearch.com

© CFRA. All rights reserved.

What are the Risks? (cont’d)

Some things to consider with respect to bills receivable risks (cont’d): – Are bills receivable easily counterfeited? – What happens to companies holding a large amount

of bills receivable if liquidity tightens in China? – How much do bank customers need to put down as a

deposit, if any, to receive a banker’s acceptance note? Are the credit checks robust?

– How many hands has the bills receivable passed through before getting to the Company you are analyzing?

35 www.cfraresearch.com

© CFRA. All rights reserved.

Big Picture Summary

Include Bills Receivable in DSO calculation – Be aware of companies with a big discrepancy in your

DSO versus Mgmt.'s due to exclusion of Bills Receivable

How safe are Bills Receivable – ask the Company which banks are guaranteeing them.

Some companies / industries may be more at risk if there is liquidity volatility in China due to heavy / disproportionate use or acceptance of Bills Receivable

36 www.cfraresearch.com

© CFRA. All rights reserved. 37 www.cfraresearch.com

Questions can be submitted to: [email protected] or by using the submit questions functionality through the webinar tool. All questions will be answered anonymously at the end of the prepared discussion.

© CFRA. All rights reserved.

Part 3: Receivables Factoring

38 www.cfraresearch.com

© CFRA. All rights reserved.

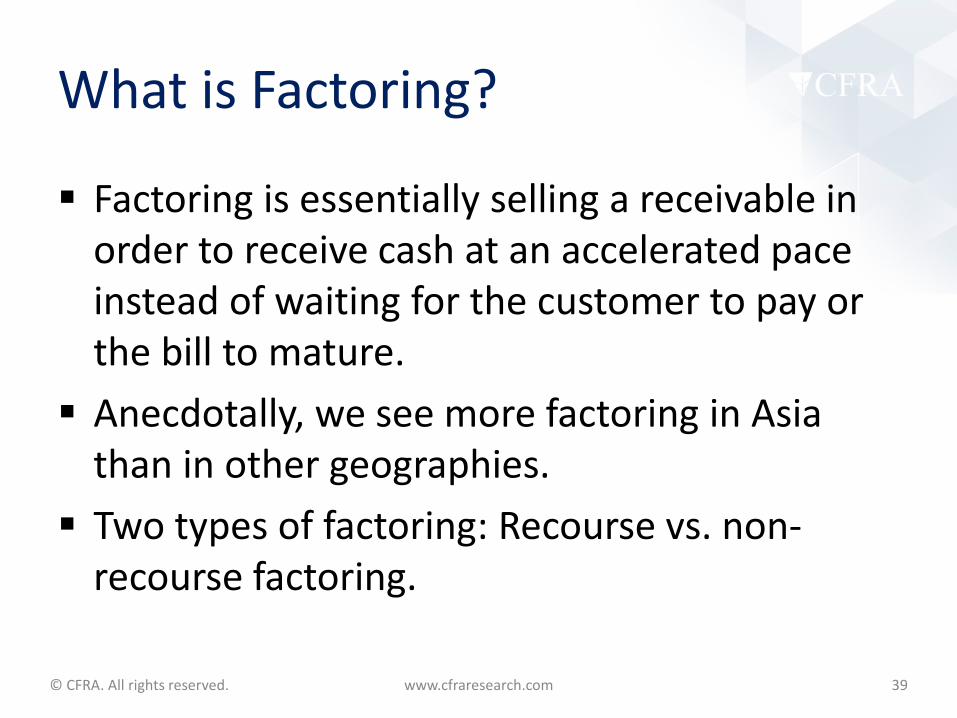

What is Factoring?

Factoring is essentially selling a receivable in order to receive cash at an accelerated pace instead of waiting for the customer to pay or the bill to mature. Anecdotally, we see more factoring in Asia

than in other geographies. Two types of factoring: Recourse vs. non-

recourse factoring.

39 www.cfraresearch.com

© CFRA. All rights reserved.

Factoring with Recourse Company retains risks and rewards of ownership. Cash inflow is considered a borrowing, in the financing section of the cash

flow statement. Receivables remain on balance sheet, offset by a liability for the borrowing.

ZTE’s Balance Sheet Receivables and cash flow from operations (CFFO) are unaffected. Thus, we

are less interested in factoring arrangements with recourse.

40 www.cfraresearch.com

© CFRA. All rights reserved.

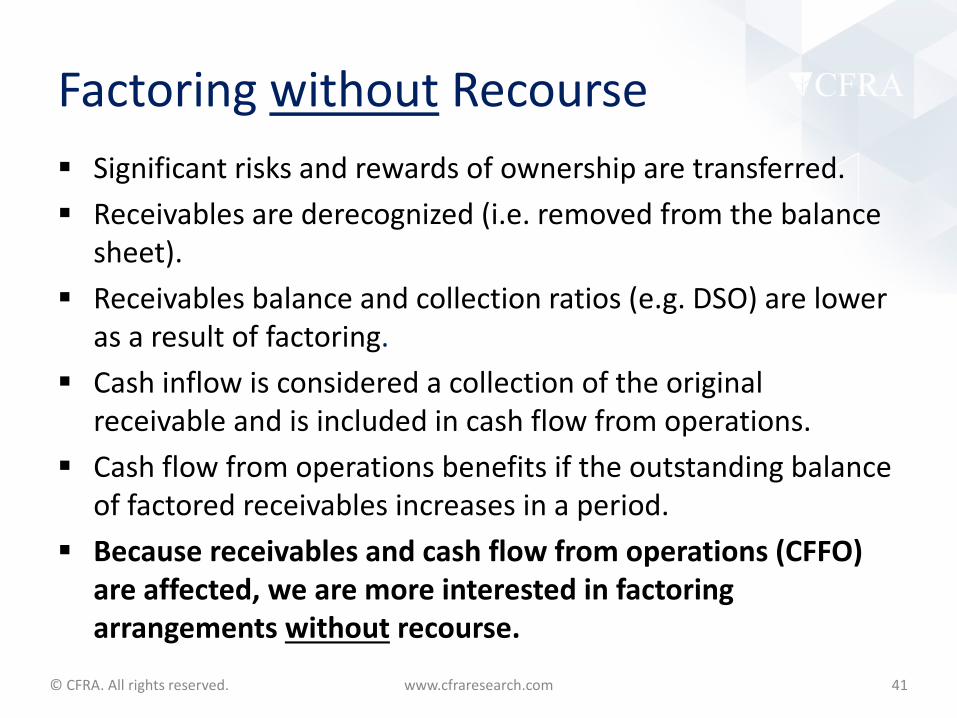

Factoring without Recourse Significant risks and rewards of ownership are transferred. Receivables are derecognized (i.e. removed from the balance

sheet). Receivables balance and collection ratios (e.g. DSO) are lower

as a result of factoring. Cash inflow is considered a collection of the original

receivable and is included in cash flow from operations. Cash flow from operations benefits if the outstanding balance

of factored receivables increases in a period. Because receivables and cash flow from operations (CFFO)

are affected, we are more interested in factoring arrangements without recourse.

41 www.cfraresearch.com

© CFRA. All rights reserved.

Effect of Factoring on the Cash Flow Statement Factoring without recourse

– Accelerates the collection of cash inflows in the operating section. – Since factoring affects only the timing of the collections, in the long

run, cumulative CFFO is unchanged. Factoring with recourse

– Cash received is considered a borrowing and included in the financing section, until the receivable is collected from the customer (and included in the operating section). ZTE’s annual report:

42 www.cfraresearch.com

© CFRA. All rights reserved.

Discounting and Endorsing of Bills Receivable When bills receivable are sold, the term is usually

‘discounting’ as bills are transferred to banks at a discount. Same recourse vs. non-recourse framework. Bills receivable in China may be ‘endorsed’ to suppliers to pay

off accounts payable.

43 www.cfraresearch.com As disclosed in GCL-Poly Energy’s 2013 report.

© CFRA. All rights reserved.

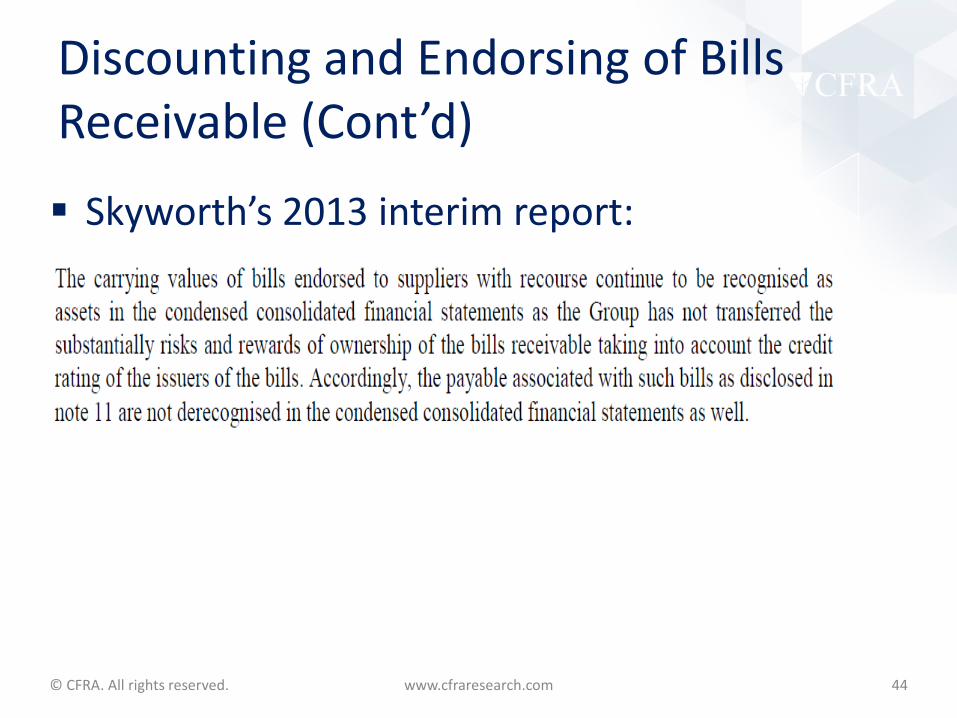

Discounting and Endorsing of Bills Receivable (Cont’d)

Skyworth’s 2013 interim report:

44 www.cfraresearch.com

© CFRA. All rights reserved.

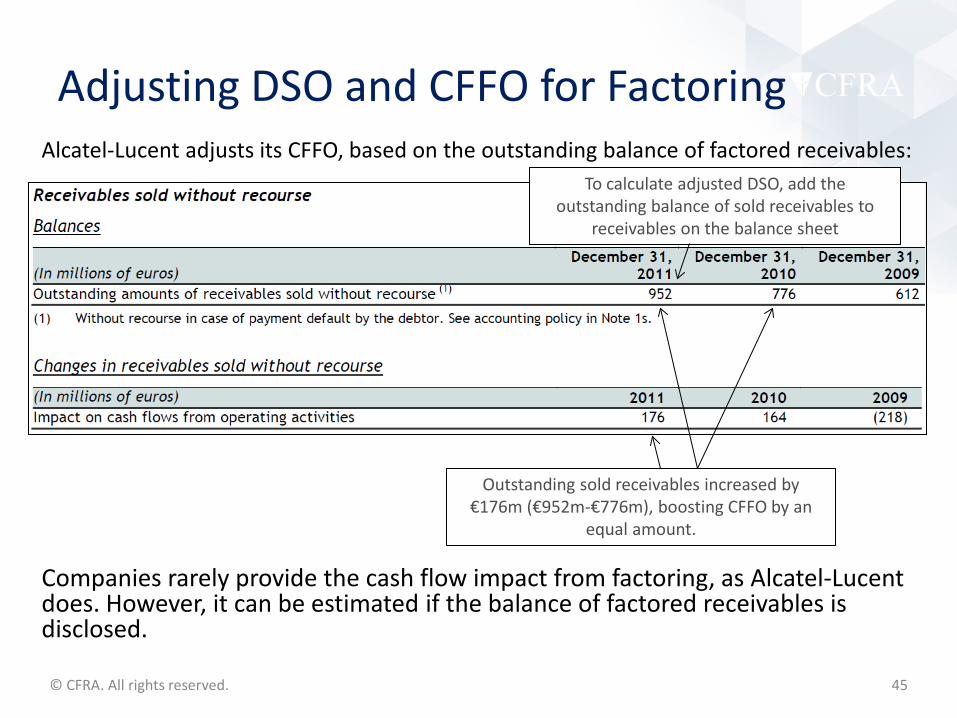

Adjusting DSO and CFFO for Factoring Alcatel-Lucent adjusts its CFFO, based on the outstanding balance of factored receivables:

Companies rarely provide the cash flow impact from factoring, as Alcatel-Lucent does. However, it can be estimated if the balance of factored receivables is disclosed.

To calculate adjusted DSO, add the outstanding balance of sold receivables to

receivables on the balance sheet

Outstanding sold receivables increased by €176m (€952m-€776m), boosting CFFO by an

equal amount.

45

© CFRA. All rights reserved.

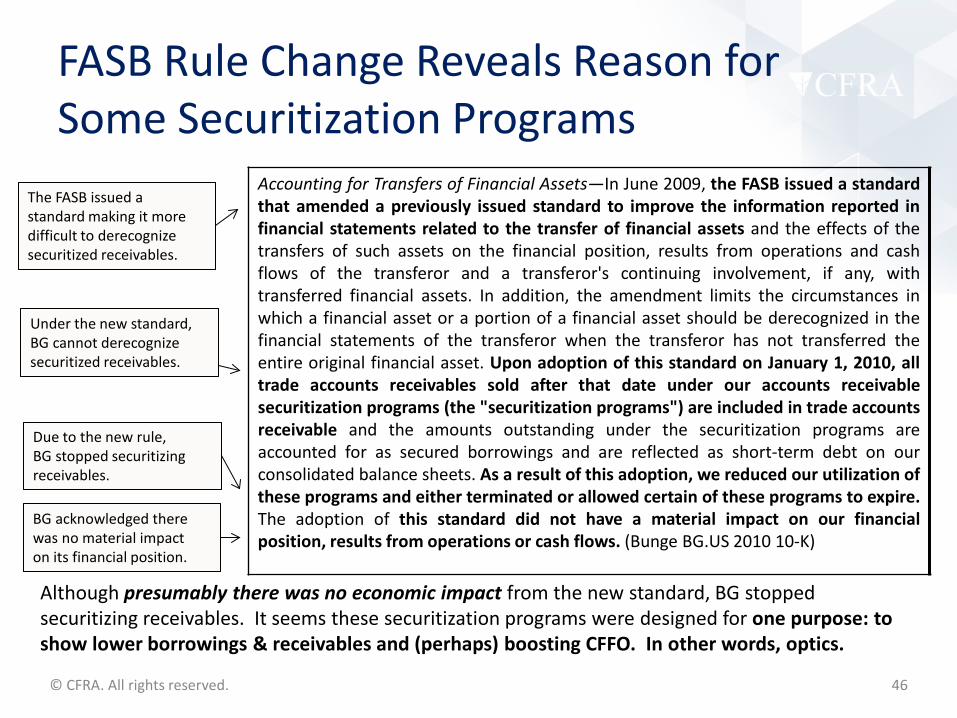

FASB Rule Change Reveals Reason for Some Securitization Programs

Accounting for Transfers of Financial Assets—In June 2009, the FASB issued a standard that amended a previously issued standard to improve the information reported in financial statements related to the transfer of financial assets and the effects of the transfers of such assets on the financial position, results from operations and cash flows of the transferor and a transferor's continuing involvement, if any, with transferred financial assets. In addition, the amendment limits the circumstances in which a financial asset or a portion of a financial asset should be derecognized in the financial statements of the transferor when the transferor has not transferred the entire original financial asset. Upon adoption of this standard on January 1, 2010, all trade accounts receivables sold after that date under our accounts receivable securitization programs (the "securitization programs") are included in trade accounts receivable and the amounts outstanding under the securitization programs are accounted for as secured borrowings and are reflected as short-term debt on our consolidated balance sheets. As a result of this adoption, we reduced our utilization of these programs and either terminated or allowed certain of these programs to expire. The adoption of this standard did not have a material impact on our financial position, results from operations or cash flows. (Bunge BG.US 2010 10-K)

Although presumably there was no economic impact from the new standard, BG stopped securitizing receivables. It seems these securitization programs were designed for one purpose: to show lower borrowings & receivables and (perhaps) boosting CFFO. In other words, optics.

The FASB issued a standard making it more difficult to derecognize securitized receivables.

Under the new standard, BG cannot derecognize securitized receivables.

Due to the new rule, BG stopped securitizing receivables.

BG acknowledged there was no material impact on its financial position.

46

© CFRA. All rights reserved.

Varying Disclosures on Factoring: Almost Nothing Li & Fung’s annual report had only one boilerplate sentence on factoring.

When CFRA asked Li & Fung if factoring led to the decline in receivables, the Company responded:

“Major causes for the fluctuation in DSO include: (i) Trade receivables factored to external financial institutions without recourse would be regarded as true sales and being derecognized. It is true that derecognition of trade receivable factored without recourse would shorten the DSO. The Group had no public disclosure on the amount of receivable factored without recourse. We are not allowed to make selective dissemination of such financial information to you..”

47 www.cfraresearch.com

© CFRA. All rights reserved.

Varying Disclosures on Factoring: Factoring Cost Lenovo discloses its factoring cost as a component of finance costs.

Tracking this cost can provide a directional sense of a company’s factoring activities.

48 www.cfraresearch.com

© CFRA. All rights reserved.

Varying Disclosures on Factoring: Amount Factored During the Period Zoomlion discloses the amount factored during the period:

“During the year ended 31 December 2012, trade receivables of RMB4,830 million (2011: RMB1,000 million) were factored to banks and other financial institutions without recourse, and were therefore derecognised.”

While this disclosure is useful, it does not allow for a precise estimate of DSO and CFFO, as there is no way to know how much would have been collected by period end.

49 www.cfraresearch.com

© CFRA. All rights reserved.

Varying Disclosures on Factoring: Amount Outstanding at Period End Sinopharm discloses the factored amount outstanding at period-end:

“As at 31 December 2013, outstanding accounts receivable of RMB3,989,172 thousands (2012: RMB2,620,273 thousands) were derecognized under the accounts receivable factoring programs without recourse.”

An increase in the outstanding balance implies that the amount factoring during the period exceeded collections.

This is the most helpful disclosure as it allows adjustment of DSO and CFFO (as discussed with Alcatel-Lucent).

50 www.cfraresearch.com

© CFRA. All rights reserved.

Continuing Involvement In some arrangements, companies do not retain or transfer all the risks and rewards of ownership of the factored receivables. In such cases, a company may derecognize the receivables but retain a continuing involvement on the balance sheet. ZTE’s 2012 annual report:

If there is default in the payment, the Company would bear the first 20% of default losses on the factored amount unless the Company breaches the Agreements or the factoring conditions are not satisfied. As at 31 December 2012, under the above arrangements, accounts receivable due from the customer amounted to RMB7,745,078,000 (2011: RMB7,643,736,000) among which RMB6,196,062,000 (2011: RMB6,114,989,000) has been derecognised from the consolidated statement of financial position as these receivables have fulfilled the derecognition conditions as stipulated in HKAS 39. An associated liability of RMB1,549,016,000 (2011: RMB1,528,747,000) has been recognized in the consolidated statement of financial position to the extent of the Company’s continuing involvement.

51 www.cfraresearch.com

The continuing involvement of

RMB1,549m amounted to 20% of the factored amount (RMB7,745m),

representing the company’s remaining

exposure. The difference (RMB6,196m)

was derecognized.

© CFRA. All rights reserved.

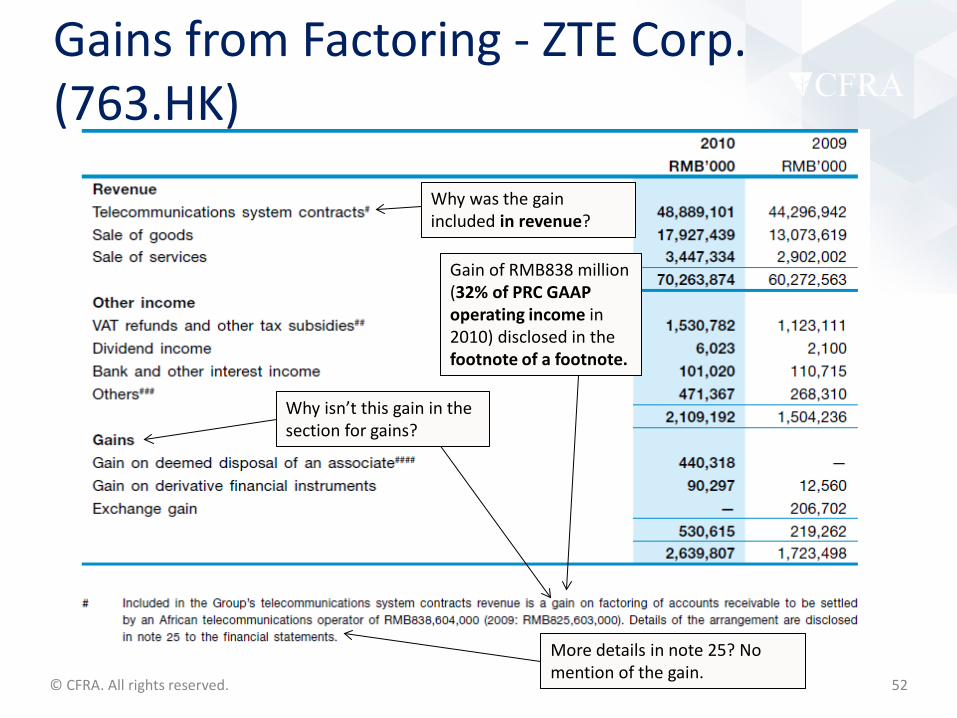

Gains from Factoring - ZTE Corp. (763.HK)

Why was the gain included in revenue?

Gain of RMB838 million (32% of PRC GAAP operating income in 2010) disclosed in the footnote of a footnote.

Why isn’t this gain in the section for gains?

More details in note 25? No mention of the gain.

52

© CFRA. All rights reserved. 53 www.cfraresearch.com

Questions can be submitted to: [email protected] or by using the submit questions functionality through the webinar tool. All questions will be answered anonymously at the end of the prepared discussion.

© CFRA. All rights reserved.

The content of this report and the opinions expressed within are those of CFRA. This analysis has not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. While CFRA exercised due care in compiling this analysis, CFRA AND ALL RELATED ENTITIES SPECIFICALLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, regarding the accuracy, completeness or usefulness of this information. and assumes no liability with respect to the consequences of relying on this information for investment or other purposes. In particular, the research provided is not intended to constitute an offer, solicitation or advice to buy or sell securities. CFRA’s financial data provider for financial companies is SNL FINANCIAL LC. CONTAINS COPYRIGHTED AND TRADE SECRET MATERIAL DISTRIBUTED UNDER LICENSE FROM SNL. FOR RECIPIENT’S INTERNAL USE ONLY CFRA, CFRA Accounting Lens, CFRA Legal Edge, CFRA Score, and all other CFRA product names are the trademarks, registered trademarks, or service marks of CFRA or its affiliates in the United States and other jurisdictions. CFRA Score may be protected by U.S. Patent No. 7,974,894 and/or other patents. If you have any comments or questions, please contact [email protected].

Client Services: Email: + 1 (212) 981-1062 [email protected]