understanding financial reports and the income statement chapter 2 robinson, munter, grant

TRANSCRIPT

Understanding Financial Reports and the Income Statement

Chapter 2

Robinson, Munter, Grant

Grant, Munter & Robinson

Chapter 2 2

Learning Objectives

• Securities regulations

• Required components of financial statements

• Income statements

• Operating and non-operating results

• Inventory, fixed assets and R&D

• Quality and conservatism of earnings

Grant, Munter & Robinson

Chapter 2 3

Securities Regulation Principal Objectives

• Protect investors.

• Ensure that market are fair, efficient, and transparent.

• Reduce systematic risk.

International Organization of Securities Commissions

Grant, Munter & Robinson

Chapter 2 4

Securities Regulation Issuers of Securities

• Full, accurate and timely disclosure of relevant information

• Treat securities holders in fair and equitable manner

• Accounting and auditing standards should be of high and internationally acceptable quality

International Organization of Securities Commissions

Grant, Munter & Robinson

Chapter 2 5

International Accounting Standards (IAS)

A complete set of financial statements includes:

• Balance sheet

• Income statement

• Statement of changes in equity

• Cash flow statement

• Explanatory notes

Grant, Munter & Robinson

Chapter 2 6

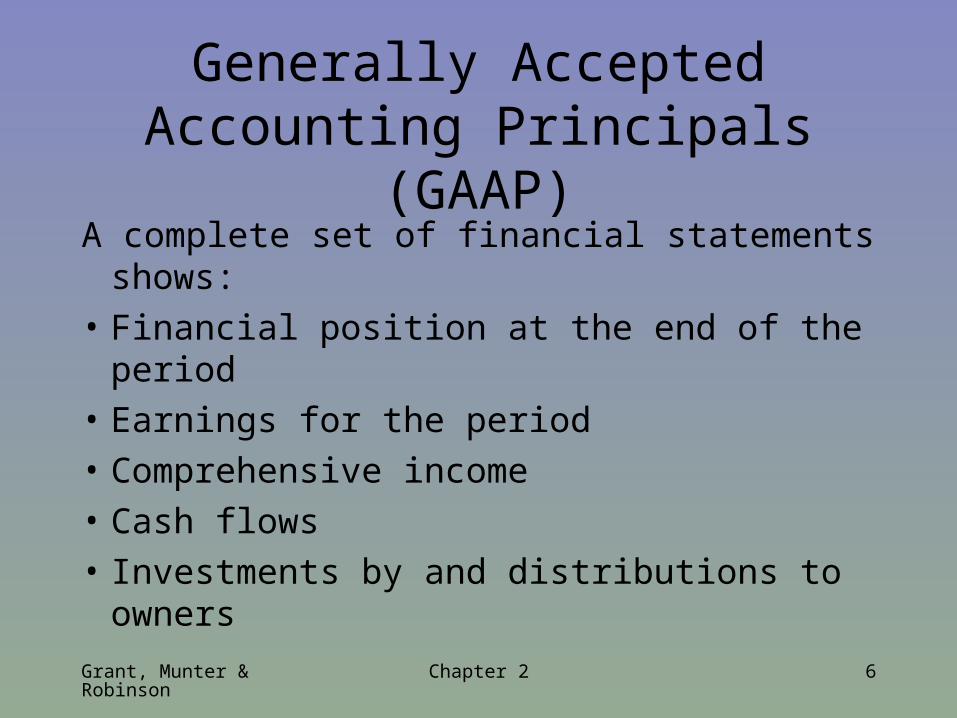

Generally Accepted Accounting Principals (GAAP)

A complete set of financial statements shows:

• Financial position at the end of the period

• Earnings for the period

• Comprehensive income

• Cash flows

• Investments by and distributions to owners

Grant, Munter & Robinson

Chapter 2 7

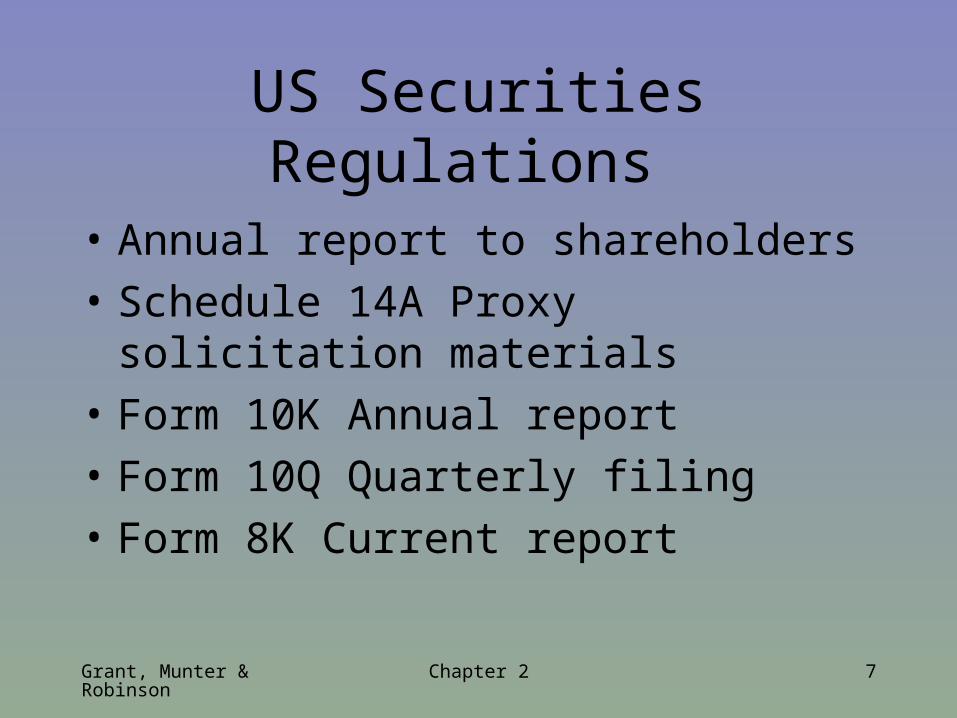

US Securities Regulations

• Annual report to shareholders

• Schedule 14A Proxy solicitation materials

• Form 10K Annual report

• Form 10Q Quarterly filing

• Form 8K Current report

Grant, Munter & Robinson

Chapter 2 8

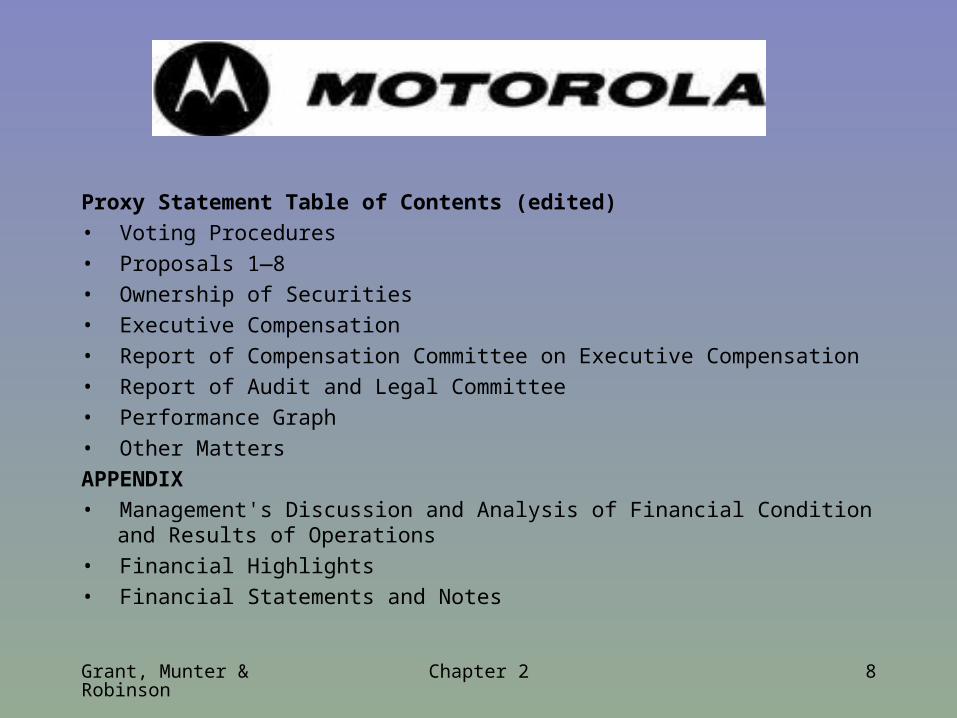

Proxy Statement Table of Contents (edited) • Voting Procedures• Proposals 1—8• Ownership of Securities• Executive Compensation• Report of Compensation Committee on Executive Compensation• Report of Audit and Legal Committee• Performance Graph• Other MattersAPPENDIX• Management's Discussion and Analysis of Financial Condition and

Results of Operations• Financial Highlights• Financial Statements and Notes

Grant, Munter & Robinson

Chapter 2 9

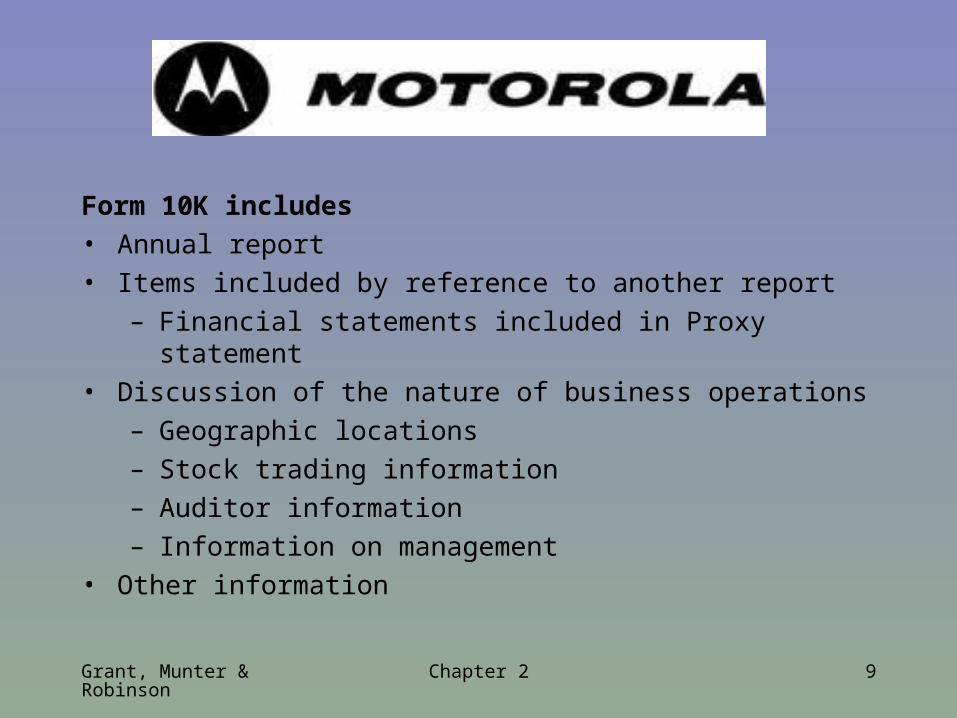

Form 10K includes• Annual report• Items included by reference to another report

– Financial statements included in Proxy statement• Discussion of the nature of business operations

– Geographic locations– Stock trading information– Auditor information– Information on management

• Other information

Grant, Munter & Robinson

Chapter 2 10

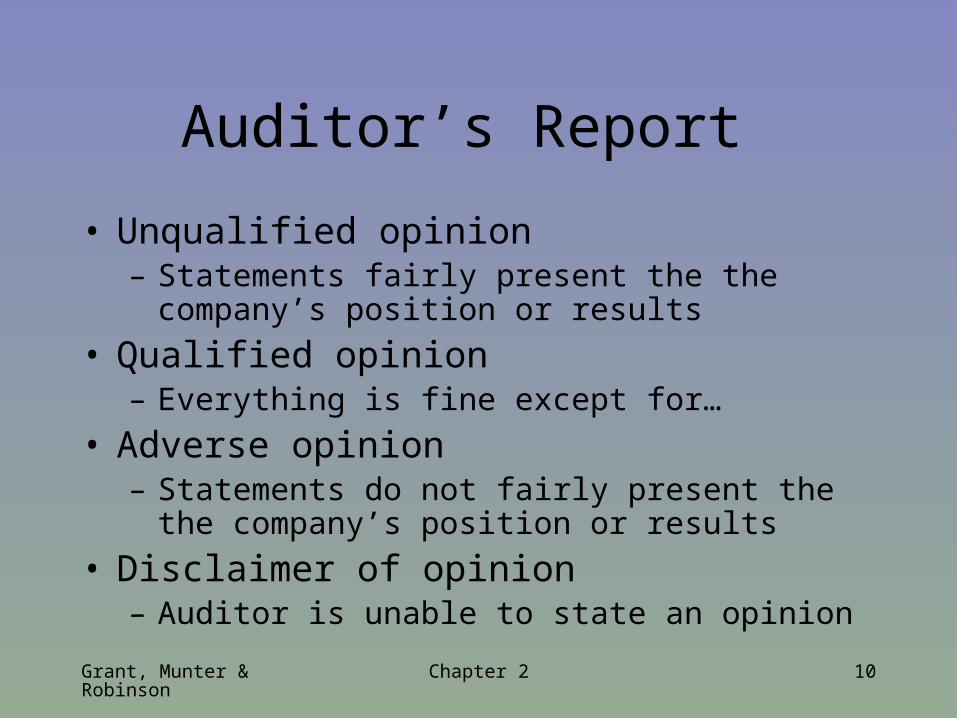

Auditor’s Report

• Unqualified opinion– Statements fairly present the the company’s position or

results

• Qualified opinion– Everything is fine except for…

• Adverse opinion– Statements do not fairly present the the company’s

position or results

• Disclaimer of opinion– Auditor is unable to state an opinion

Grant, Munter & Robinson

Chapter 2 11

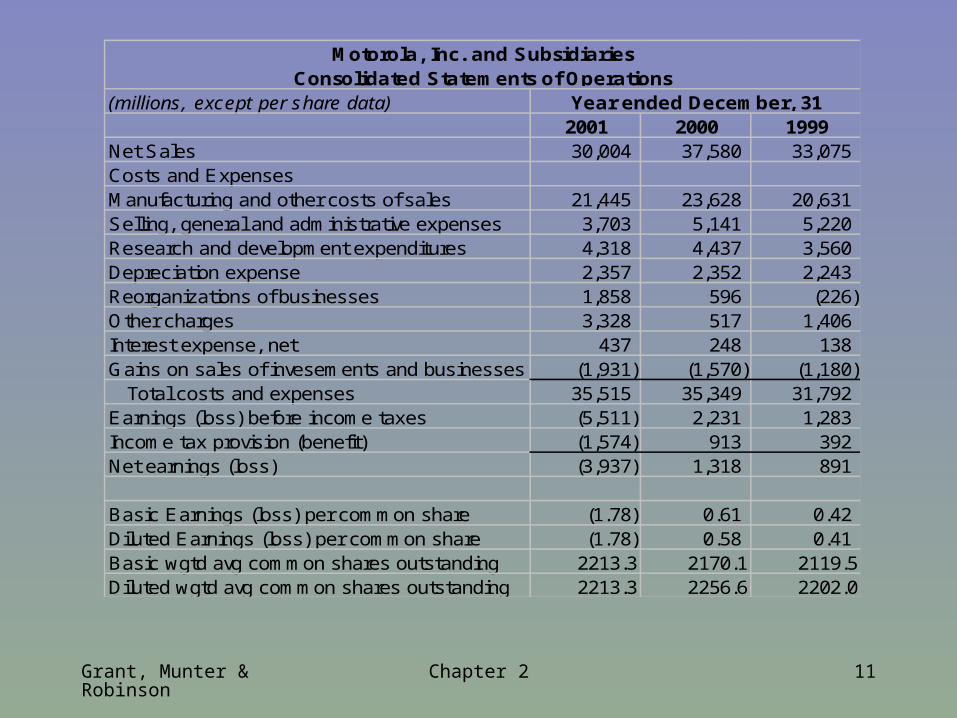

(millions, except per share data)2001 2000 1999

Net Sales 30,004 37,580 33,075 Costs and ExpensesManufacturing and other costs of sales 21,445 23,628 20,631 Selling, general and administrative expenses 3,703 5,141 5,220 Research and development expenditures 4,318 4,437 3,560 Depreciation expense 2,357 2,352 2,243 Reorganizations of businesses 1,858 596 (226) Other charges 3,328 517 1,406 Interest expense, net 437 248 138 Gains on sales of invesements and businesses (1,931) (1,570) (1,180)

Total costs and expenses 35,515 35,349 31,792 Earnings (loss) before income taxes (5,511) 2,231 1,283 Income tax provision (benefit) (1,574) 913 392 Net earnings (loss) (3,937) 1,318 891

Basic Earnings (loss) per common share (1.78) 0.61 0.42 Diluted Earnings (loss) per common share (1.78) 0.58 0.41 Basic wgtd avg common shares outstanding 2213.3 2170.1 2119.5Diluted wgtd avg common shares outstanding 2213.3 2256.6 2202.0

Year ended December, 31

Motorola, Inc. and SubsidiariesConsolidated Statements of Operations

Grant, Munter & Robinson

Chapter 2 12

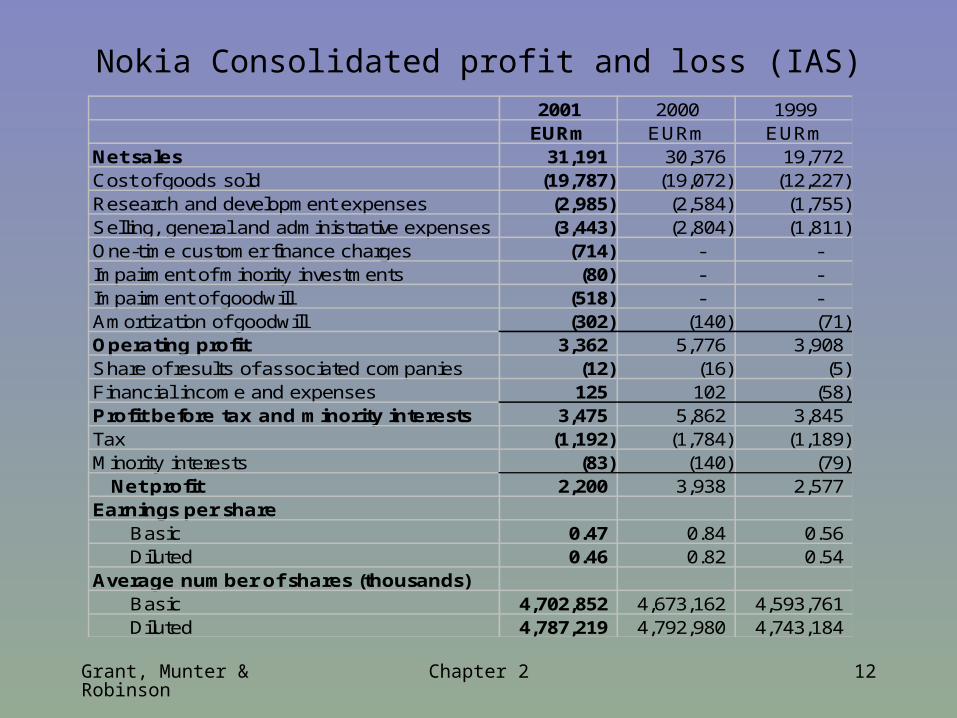

Nokia Consolidated profit and loss (IAS)2001 2000 1999

EURm EURm EURmNet sales 31,191 30,376 19,772 Cost of goods sold (19,787) (19,072) (12,227) Research and development expenses (2,985) (2,584) (1,755) Selling, general and administrative expenses (3,443) (2,804) (1,811) One-time customer finance charges (714) - - Impairment of minority investments (80) - - Impairment of goodwill (518) - - Amortization of goodwill (302) (140) (71) Operating profit 3,362 5,776 3,908 Share of results of associated companies (12) (16) (5) Financial income and expenses 125 102 (58) Profit before tax and minority interests 3,475 5,862 3,845 Tax (1,192) (1,784) (1,189) Minority interests (83) (140) (79)

Net profit 2,200 3,938 2,577 Earnings per share

Basic 0.47 0.84 0.56 Diluted 0.46 0.82 0.54

Average number of shares (thousands) Basic 4,702,852 4,673,162 4,593,761 Diluted 4,787,219 4,792,980 4,743,184

Grant, Munter & Robinson

Chapter 2 13

Sales revenue• Proceeds from customers in exchange for the

delivery of goods or services for the use of assets• Also use the terms revenue and turnover (U.K.)• Generally recognized when earned and realized or

realizable– When goods/services are exchanged for cash or claims

to cash

– Substantially accomplished what must be done

• Service revenue is recognized with reference to the percentage of completion

Grant, Munter & Robinson

Chapter 2 14

Net sales

• Sales revenue less returns and allowances

• Returns: – Customer returns goods for a refund

• Allowance: – Customer retains goods but receive a partial

refund if unhappy with quality of merchandise

Grant, Munter & Robinson

Chapter 2 15

Cost of Sales and Gross Profit

• Net sales – Cost of sales = Gross profit• Cost of sales

– Direct cost of purchasing or producing the goods or services to be delivered to customers

– Also Cost of good sold or Cost of services provided– Retail: purchase cost of goods sold to customers– Manufacturing: material, labor and overhead used in

the production of goods– Service: cost required to provide service (labor and

supplies)

Grant, Munter & Robinson

Chapter 2 16

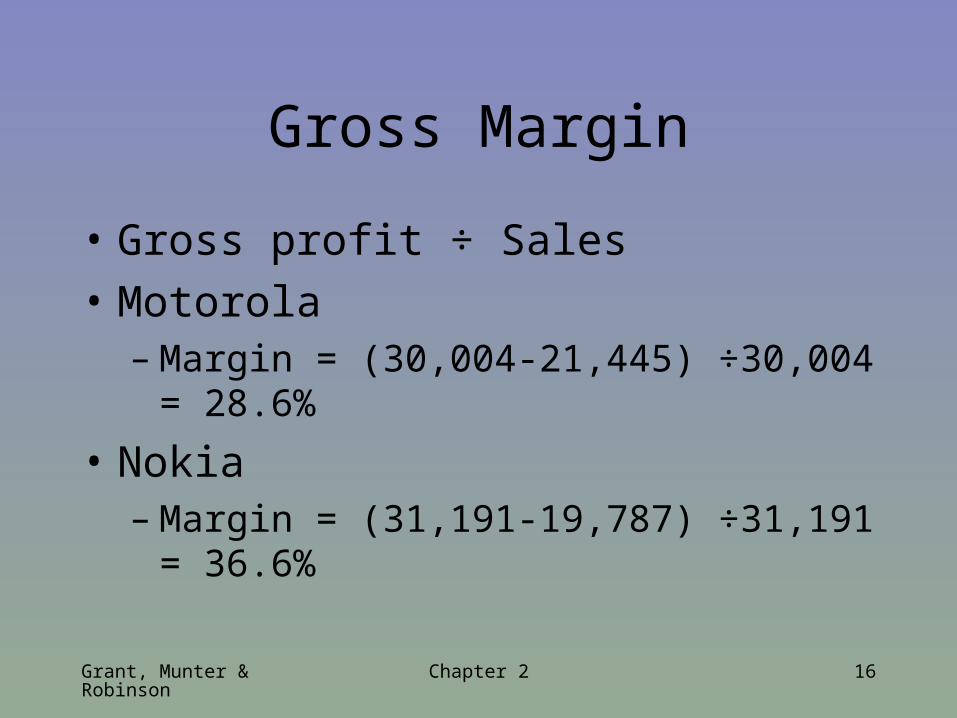

Gross Margin

• Gross profit ÷ Sales

• Motorola– Margin = (30,004-21,445) ÷30,004 = 28.6%

• Nokia– Margin = (31,191-19,787) ÷31,191 = 36.6%

Grant, Munter & Robinson

Chapter 2 17

Selling, General and Administrative (SG&A) Expenses

• Operating expenses including• Salaries• Pension costs• Marketing costs• Insurance• Rent• Depreciation• Other• Generally reported as a single line item

Grant, Munter & Robinson

Chapter 2 18

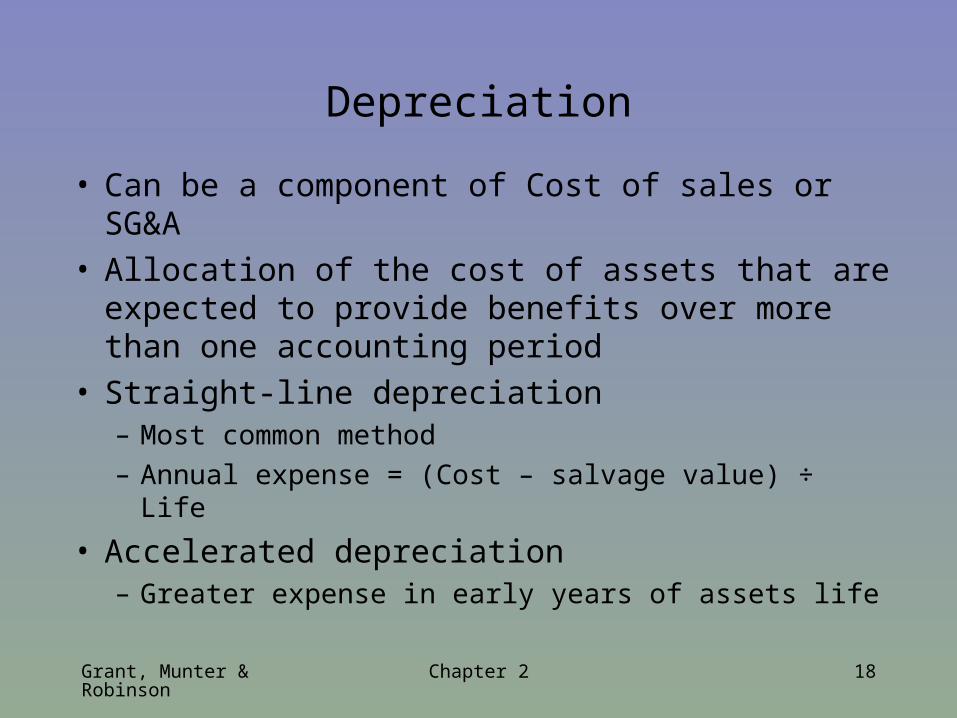

Depreciation

• Can be a component of Cost of sales or SG&A• Allocation of the cost of assets that are expected to

provide benefits over more than one accounting period

• Straight-line depreciation– Most common method

– Annual expense = (Cost – salvage value) ÷ Life

• Accelerated depreciation– Greater expense in early years of assets life

Grant, Munter & Robinson

Chapter 2 19

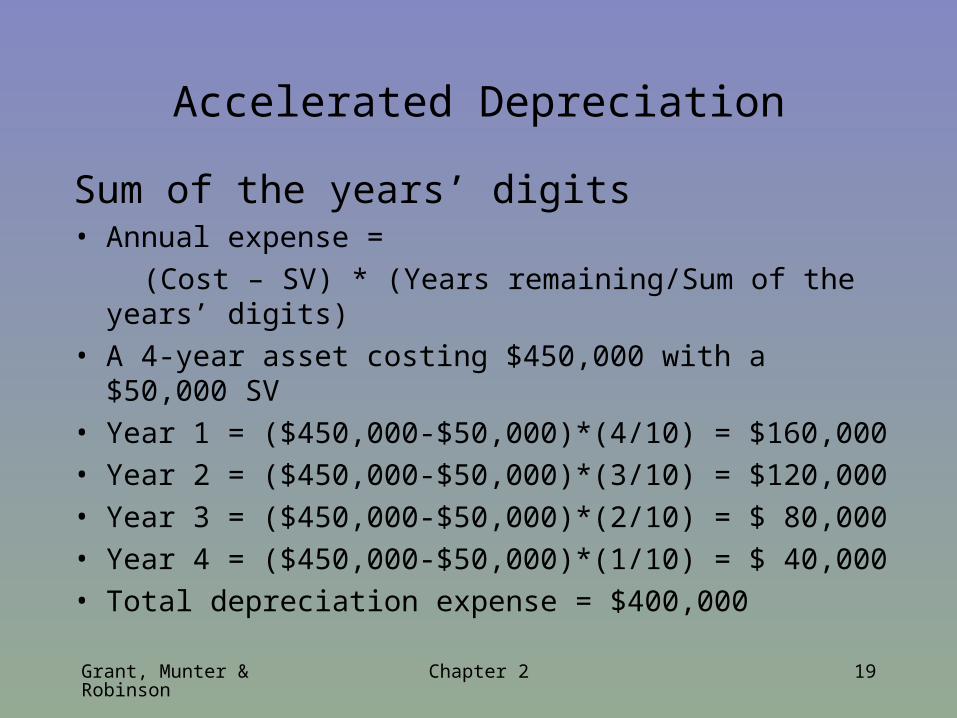

Accelerated Depreciation

Sum of the years’ digits• Annual expense =

(Cost – SV) * (Years remaining/Sum of the years’ digits)

• A 4-year asset costing $450,000 with a $50,000 SV

• Year 1 = ($450,000-$50,000)*(4/10) = $160,000

• Year 2 = ($450,000-$50,000)*(3/10) = $120,000

• Year 3 = ($450,000-$50,000)*(2/10) = $ 80,000

• Year 4 = ($450,000-$50,000)*(1/10) = $ 40,000

• Total depreciation expense = $400,000

Grant, Munter & Robinson

Chapter 2 20

Accelerated Depreciation

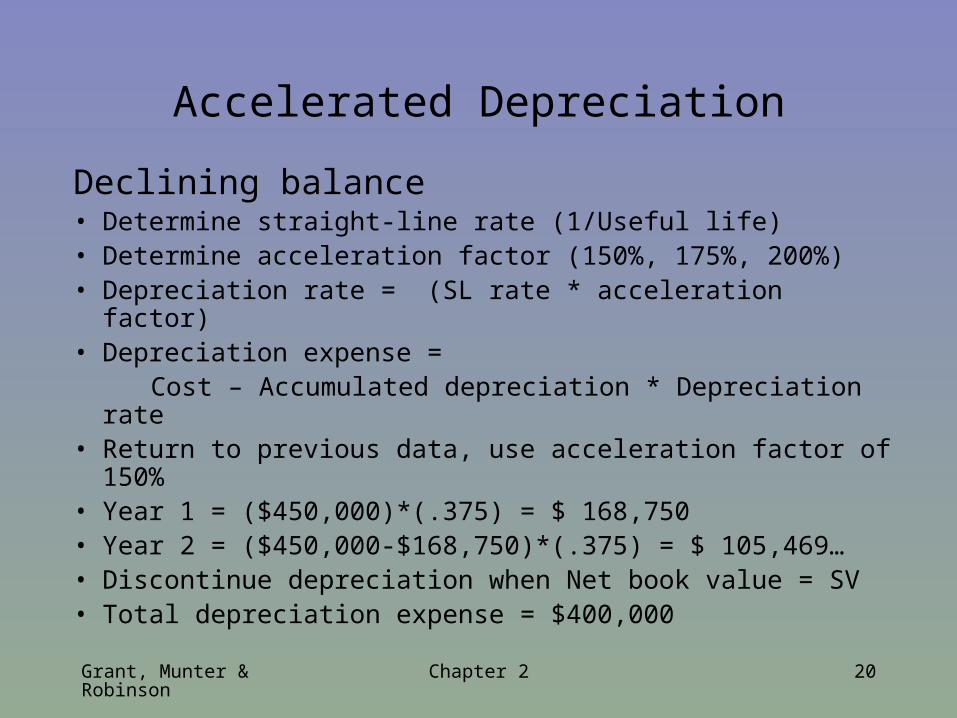

Declining balance• Determine straight-line rate (1/Useful life)• Determine acceleration factor (150%, 175%, 200%)• Depreciation rate = (SL rate * acceleration factor)• Depreciation expense = Cost – Accumulated depreciation * Depreciation rate• Return to previous data, use acceleration factor of 150%• Year 1 = ($450,000)*(.375) = $ 168,750• Year 2 = ($450,000-$168,750)*(.375) = $ 105,469…• Discontinue depreciation when Net book value = SV• Total depreciation expense = $400,000

Grant, Munter & Robinson

Chapter 2 21

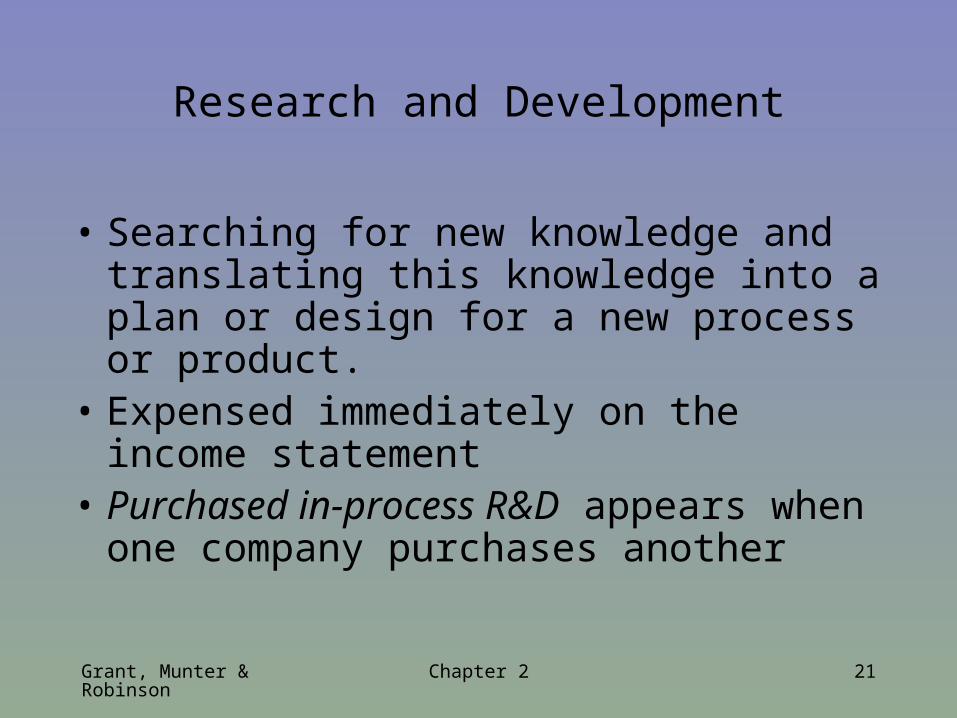

Research and Development

• Searching for new knowledge and translating this knowledge into a plan or design for a new process or product.

• Expensed immediately on the income statement

• Purchased in-process R&D appears when one company purchases another

Grant, Munter & Robinson

Chapter 2 22

Restructuring and Other Charges

• Appears when a business reorganizes

• Includes charges associated with asset write downs and employee separations

• Consider whether these charges will continue

Grant, Munter & Robinson

Chapter 2 23

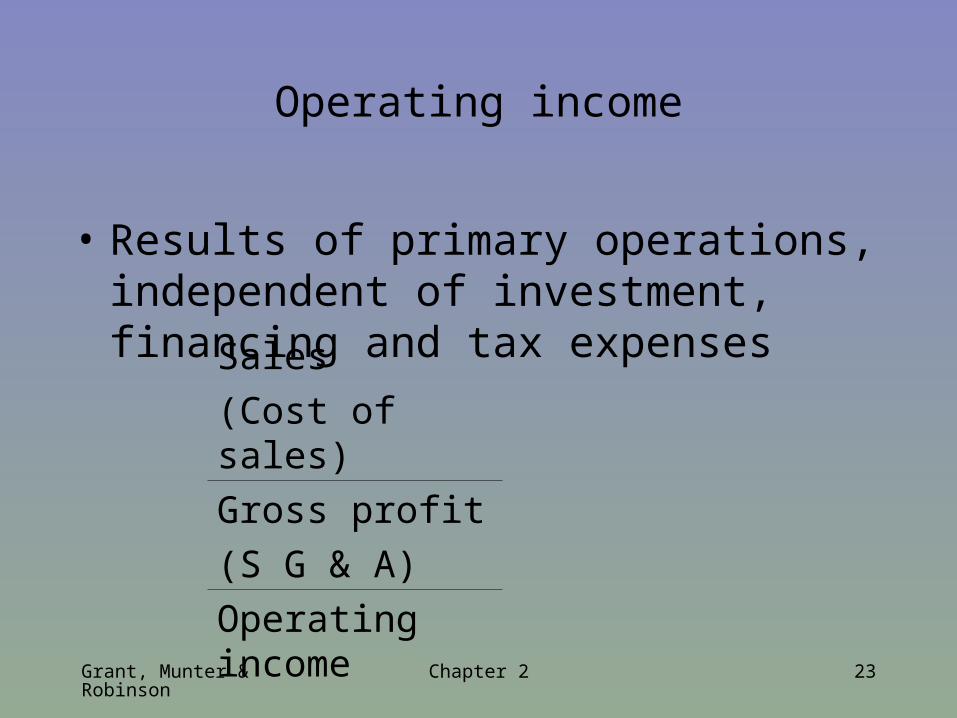

Operating income

• Results of primary operations, independent of investment, financing and tax expenses

Sales

(Cost of sales)

Gross profit

(S G & A)

Operating income

Grant, Munter & Robinson

Chapter 2 24

Income statement, continued

• Nonoperating income– Peripheral activities: interest income/expense, dividend

income, gain/losses on asset sales

• Income before income taxes• Provision for income taxes

– Expected amount of taxes to be paid

• Net income or loss

Grant, Munter & Robinson

Chapter 2 25

Income statement - Special items

• Minority share of income– Subsidiaries owned less than 100%

• Discontinued operations– Disposition (actual or planned) of a large component of

business

• Extraordinary items– Unusual and infrequent

• Cumulative effect of change in accounting principles

Grant, Munter & Robinson

Chapter 2 26

Earnings per share

• Basic– Net income/Weighted average number of shares outstanding

• Diluted– EPS equation includes securities that can be converted

into common stock (options)

– As if dilutive securities were exercised

• Discontinued operations, extraordinary items and changes in accounting principles are shown in total and on a per share basis

Grant, Munter & Robinson

Chapter 2 27

Special revenue recognition methods

• Long-term contract– Completed contract– Percentage of completion

• Warranty contracts

• Installment sales

• Commodities

Grant, Munter & Robinson

Chapter 2 28

Comprehensive income

• All income statement items

• Other comprehensive income– Change in the value of some securities held for

investment– Gain/losses on foreign currency translation

Grant, Munter & Robinson

Chapter 2 29

Quality of income

Consider– Conservatism– Accounting method (depreciation, inventory

valuation, revenue recognition)– Assumptions regarding retirement benefits– Reserves (sales returns, bad debts)– Deferral or unusual expenses

Grant, Munter & Robinson

Chapter 2 30

Summary

• Securities filings

• Auditor’s reports

• The income statement– Depreciation

• Quality of income