understanding your good faith estimate - discover - card ... · a good faith estimate (gfe) is...

TRANSCRIPT

A Good Faith Estimate (GFE) is exactly that... an estimate provided by a lender detailing the anticipated costs associated with any real estate transaction: buying, refinancing or taking out a home equity loan.

After you apply for a loan, your lender must mail a GFE to you within three business days of your application being accepted. If you apply with multiple lenders, each must provide you with a separate GFE. All lenders are required by law to prepare an identical form using the same method and terminology to present your prospective loan to you—so even though there are no fees or closing costs when you take out a Discover® Home Equity Loan, we must disclose the types and amounts of the fees we pay on your behalf.

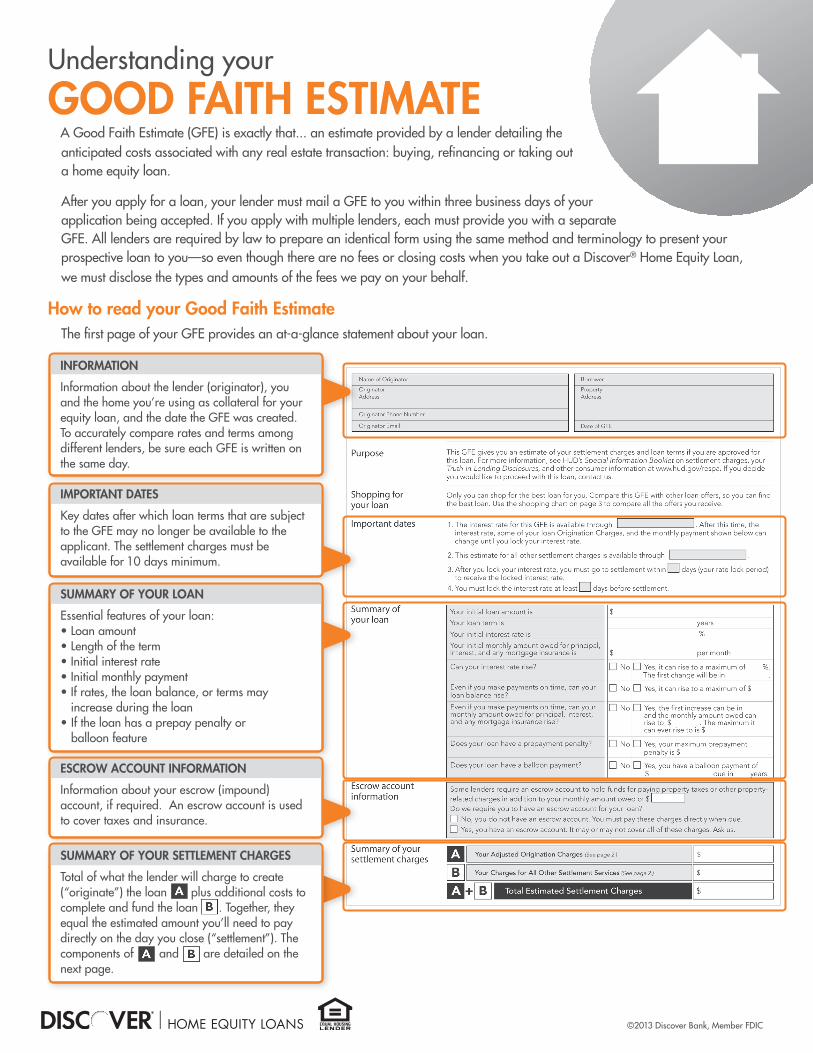

How to read your Good Faith EstimateThe first page of your GFE provides an at-a-glance statement about your loan.

SUMMARY OF YOUR LOAN

Essential features of your loan:• Loan amount• Length of the term• Initial interest rate• Initial monthly payment• If rates, the loan balance, or terms may

increase during the loan• If the loan has a prepay penalty or

balloon feature

Understanding your

GOOD FAITH ESTIMATE

INFORMATION

Information about the lender (originator), you and the home you’re using as collateral for your equity loan, and the date the GFE was created. To accurately compare rates and terms among different lenders, be sure each GFE is written on the same day.

SUMMARY OF YOUR SETTLEMENT CHARGES

Total of what the lender will charge to create (“originate”) the loan plus additional costs to complete and fund the loan . Together, they equal the estimated amount you’ll need to pay directly on the day you close (“settlement”). The components of and are detailed on the next page.

©2013 Discover Bank, Member FDIC

IMPORTANT DATES

Key dates after which loan terms that are subject to the GFE may no longer be available to the applicant. The settlement charges must be available for 10 days minimum.

ESCROW ACCOUNT INFORMATION

Information about your escrow (impound) account, if required. An escrow account is used to cover taxes and insurance.

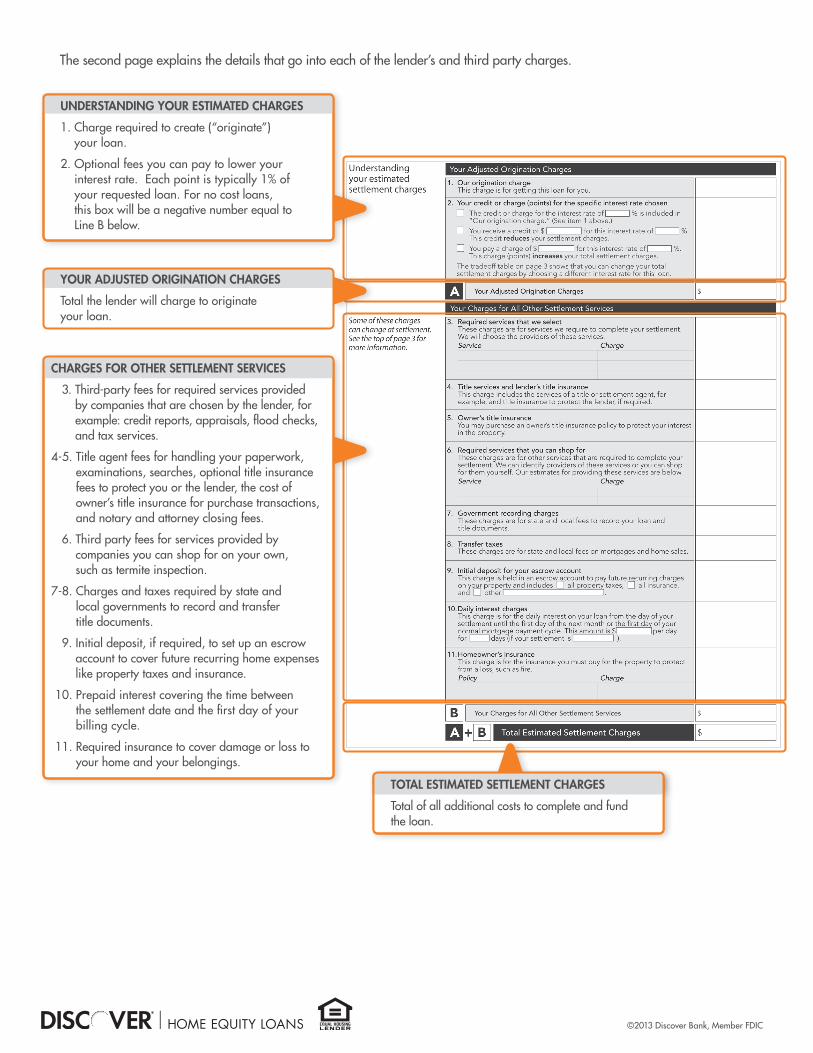

The second page explains the details that go into each of the lender’s and third party charges.

UNDERSTANDING YOUR ESTIMATED CHARGES

1. Charge required to create (“originate”) your loan.

2. Optional fees you can pay to lower your interest rate. Each point is typically 1% of your requested loan. For no cost loans, this box will be a negative number equal to Line B below.

CHARGES FOR OTHER SETTLEMENT SERVICES

3. Third-party fees for required services provided by companies that are chosen by the lender, for example: credit reports, appraisals, flood checks, and tax services.

4-5. Title agent fees for handling your paperwork, examinations, searches, optional title insurance fees to protect you or the lender, the cost of owner’s title insurance for purchase transactions, and notary and attorney closing fees.

6. Third party fees for services provided by companies you can shop for on your own, such as termite inspection.

7-8. Charges and taxes required by state and local governments to record and transfer title documents.

9. Initial deposit, if required, to set up an escrow account to cover future recurring home expenses like property taxes and insurance.

10. Prepaid interest covering the time between the settlement date and the first day of your billing cycle.

11. Required insurance to cover damage or loss to your home and your belongings.

YOUR ADJUSTED ORIGINATION CHARGES

Total the lender will charge to originate your loan.

TOTAL ESTIMATED SETTLEMENT CHARGES

Total of all additional costs to complete and fund the loan.

©2013 Discover Bank, Member FDIC

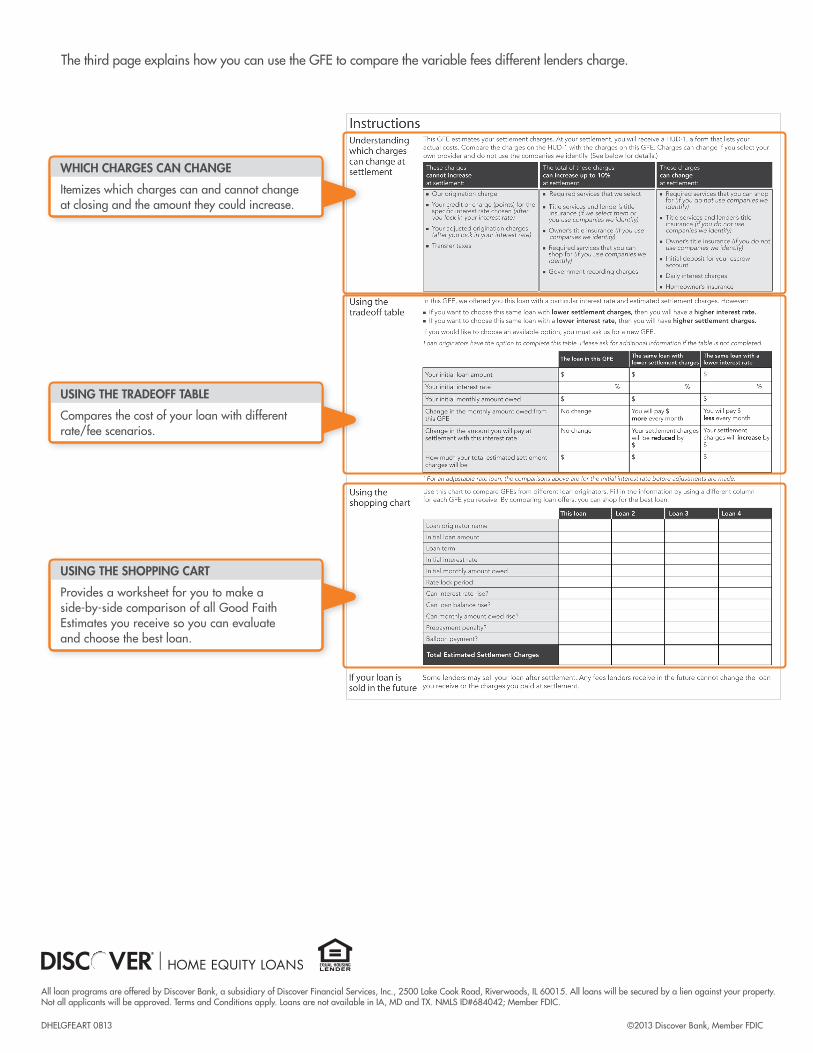

The third page explains how you can use the GFE to compare the variable fees different lenders charge.

WHICH CHARGES CAN CHANGE

Itemizes which charges can and cannot change at closing and the amount they could increase.

USING THE TRADEOFF TABLE

Compares the cost of your loan with different rate/fee scenarios.

USING THE SHOPPING CART

Provides a worksheet for you to make a side-by-side comparison of all Good Faith Estimates you receive so you can evaluate and choose the best loan.

DHELGFEART 0813

All loan programs are offered by Discover Bank, a subsidiary of Discover Financial Services, Inc., 2500 Lake Cook Road, Riverwoods, IL 60015. All loans will be secured by a lien against your property. Not all applicants will be approved. Terms and Conditions apply. Loans are not available in IA, MD and TX. NMLS ID#684042; Member FDIC.

©2013 Discover Bank, Member FDIC