unit 9 cost accounting & decision making...

TRANSCRIPT

1

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

Technology Education Section, Curriculum Development InstituteEducation Bureau, HKSARG

August 2008

Unit 9 : Cost Accounting for Decision Making 2

Course 1 : Contemporary Perspectives on Accounting

22

Learning objectivesLearning objectives

On completion of this unit, you should be able to:On completion of this unit, you should be able to:

•• Identify the nature of various cost items and their Identify the nature of various cost items and their relevance to decision making.relevance to decision making.

•• Apply costing concepts and techniques in business Apply costing concepts and techniques in business decisions:decisions:–– hire, make or buy;hire, make or buy;–– accept or reject an order at a special price;accept or reject an order at a special price;–– retain or replace equipment; retain or replace equipment; –– sell or process further; andsell or process further; and–– eliminate or retain an unprofitable segment.eliminate or retain an unprofitable segment.

•• Explain the importance of qualitative factors. Explain the importance of qualitative factors.

33

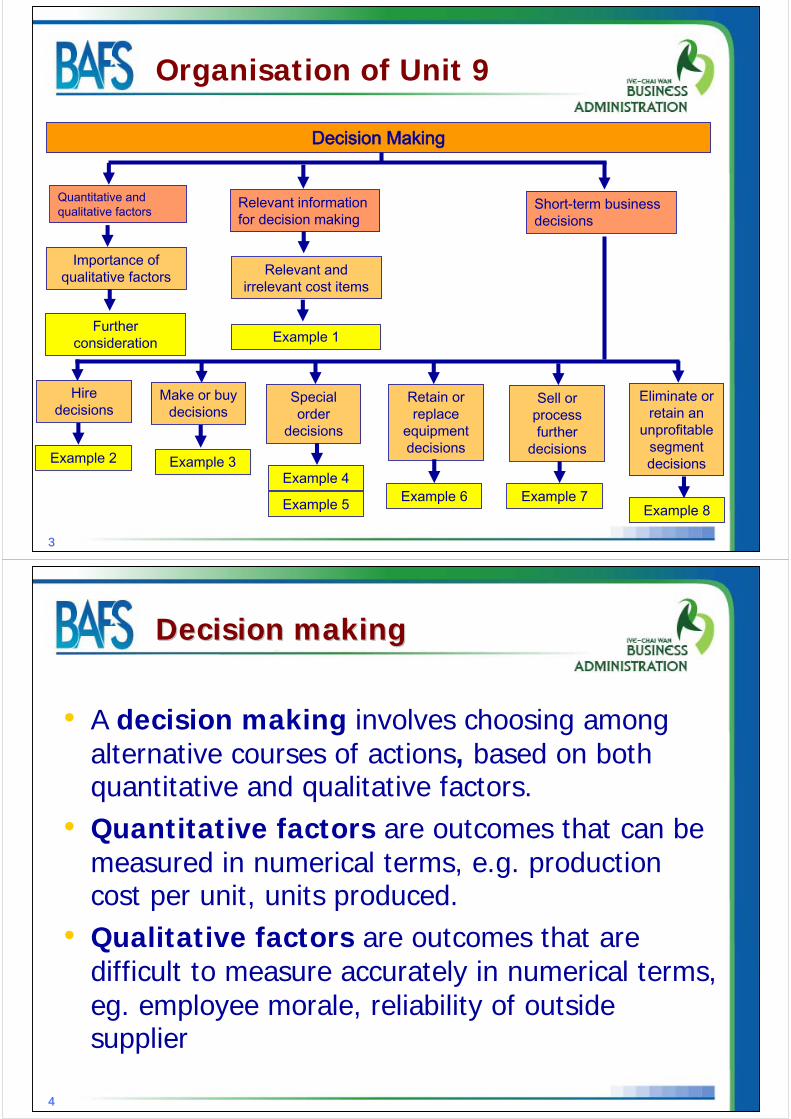

Organisation of Unit 9

Decision Making

Relevant information for decision making

Quantitative and qualitative factors

Importance of qualitative factors

Further consideration Example 1

Short-term business decisions

Relevant and irrelevant cost items

Hire decisions

Make or buy decisions

Special order

decisions

Retain or replace

equipment decisions

Sell or process further

decisions

Eliminate or retain an

unprofitable segment decisionsExample 2 Example 3

Example 4

Example 5 Example 6 Example 7Example 8

44

Decision making Decision making

• A decision making involves choosing among alternative courses of actions, based on both quantitative and qualitative factors.

• Quantitative factors are outcomes that can be measured in numerical terms, e.g. production cost per unit, units produced.

• Qualitative factors are outcomes that are difficult to measure accurately in numerical terms, eg. employee morale, reliability of outside supplier

55

Relevant information for decision Relevant information for decision making making

•• Relevant informationRelevant information relates to the future and relates to the future and varies among alternative courses of action. varies among alternative courses of action.

–– Relevant revenuesRelevant revenues are expected future are expected future revenues.revenues.

–– Relevant costs Relevant costs are expected future costs.are expected future costs.

66

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (1)(1)

•• Fixed costs Fixed costs are costs that will remain are costs that will remain unchanged irrespective of the changes in the unchanged irrespective of the changes in the level of activity (e.g. production volume) within a level of activity (e.g. production volume) within a relevant range. relevant range.

•• Unit fixed costs increases as the level of activity Unit fixed costs increases as the level of activity decreases, and vice versa. decreases, and vice versa.

77

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (2)(2)

Production Volume

Cost $

Fixed costs

88

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (3)(3)

•• Examples of fixed costs are rent, wages for Examples of fixed costs are rent, wages for production supervisors and depreciation of fixed production supervisors and depreciation of fixed assets calculated on straight line or reducing assets calculated on straight line or reducing balance method. balance method.

•• Fixed costs are usually irrelevant costs, unless Fixed costs are usually irrelevant costs, unless they are avoidable fixed costs.they are avoidable fixed costs.

99

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (4)(4)

•• Variable costs Variable costs are costs that will change in are costs that will change in direct proportion to the changes in the level of direct proportion to the changes in the level of activity (e.g. production volume). activity (e.g. production volume).

•• Unit variable costs will remain unchanged Unit variable costs will remain unchanged irrespective of the change in level of activity. irrespective of the change in level of activity.

1010

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (5)(5)

Production Volume

Cost $

Variable costs

1111

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (6)(6)

•• Examples of variable costs are raw materials, Examples of variable costs are raw materials, direct direct labourlabour and distribution costs calculated on and distribution costs calculated on the basis of units sold. the basis of units sold.

•• Variable costs are usually relevant costs, because Variable costs are usually relevant costs, because they vary among the possible courses of action. they vary among the possible courses of action.

1212

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (7)(7)

•• Avoidable costs Avoidable costs are costs that can be eliminated by are costs that can be eliminated by choosing one alternative over another, e.g. the wages of choosing one alternative over another, e.g. the wages of the foreman for a product line that can be saved when the foreman for a product line that can be saved when that product line is discontinued.that product line is discontinued.

•• Avoidable costs are relevant costs.Avoidable costs are relevant costs.

•• Unavoidable costs Unavoidable costs are costs that do not differ between are costs that do not differ between the alternatives, e.g. the rental costs of a factory having the alternatives, e.g. the rental costs of a factory having numerous product lines that would not be reduced even numerous product lines that would not be reduced even though one of its product lines is discontinued.though one of its product lines is discontinued.

•• Unavoidable costs are irrelevant for decision making.Unavoidable costs are irrelevant for decision making.

1313

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (8)(8)

•• Past costsPast costs, also known as , also known as sunk costssunk costs, are , are those costs that have either been charged as those costs that have either been charged as expenses in prior accounting period or will be expenses in prior accounting period or will be charged as expenses in a future accounting charged as expenses in a future accounting period, e.g. the depreciation of a machine that period, e.g. the depreciation of a machine that has been bought. has been bought.

•• Past costs are also irrelevant for decision making Past costs are also irrelevant for decision making because they cannot be changed, regardless of because they cannot be changed, regardless of whether the decision is made. whether the decision is made.

1414

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (9)(9)

•• Historical costsHistorical costs are the amount of cash or the are the amount of cash or the fair value of consideration given to acquire the fair value of consideration given to acquire the assets and expenses at the time of their assets and expenses at the time of their acquisition, e.g. the purchase costs of a motor acquisition, e.g. the purchase costs of a motor vehicle. vehicle.

•• Historical costs are past costs.Historical costs are past costs.

1515

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (10)(10)

•• Opportunity costOpportunity cost is the cost of an action in is the cost of an action in terms of the value of the best alternative terms of the value of the best alternative opportunity foregone. opportunity foregone.

•• For example, a scarce material can be used to For example, a scarce material can be used to produce product X, Y or Z which yields profits of produce product X, Y or Z which yields profits of $40, $60 and $70 respectively. The opportunity $40, $60 and $70 respectively. The opportunity cost of using the scarce material in producing cost of using the scarce material in producing product Z (the best action) is $60 (the best product Z (the best action) is $60 (the best alternative forgone). alternative forgone).

1616

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (11)(11)

•• Incremental cost Incremental cost is the additional total cost is the additional total cost incurred for an activity, e.g. the additional cost incurred for an activity, e.g. the additional cost incurred for hiring 3 technicians instead of 2 incurred for hiring 3 technicians instead of 2 technicians in the repair and maintenance technicians in the repair and maintenance department.department.

•• Differential cost Differential cost is the difference in total cost is the difference in total cost between two alternatives, e.g. the difference in between two alternatives, e.g. the difference in total cost between the maketotal cost between the make--parts and buyparts and buy--parts parts of a product. of a product.

1717

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (12)(12)

•• Joint costs Joint costs are the cost incurred for a single are the cost incurred for a single process that produces two or more products at process that produces two or more products at the same time, e.g. the cost of distillation of coal the same time, e.g. the cost of distillation of coal which yields coke, natural gas and other products. which yields coke, natural gas and other products.

•• Joint costs are irrelevant for sell or process Joint costs are irrelevant for sell or process further decisions.further decisions.

1818

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (13)(13)

•• Net Net realisablerealisable value (NRV) value (NRV) is the estimated is the estimated selling price in the ordinary course of business selling price in the ordinary course of business less estimated costs of completion and estimated less estimated costs of completion and estimated costs necessary to make the sale, e.g. the costs necessary to make the sale, e.g. the estimated selling price of a second hand motor estimated selling price of a second hand motor vehicle net of the commission paid for the agent vehicle net of the commission paid for the agent to sell it. to sell it.

•• NRV is considered as the relevant cost of NRV is considered as the relevant cost of materials already bought with no other usage but materials already bought with no other usage but to sell them.to sell them.

1919

Relevant and irrelevant cost itemsRelevant and irrelevant cost items (14)(14)

•• Committed cost Committed cost is a future cash outflow that is a future cash outflow that will be incurred no matter what decision is taken will be incurred no matter what decision is taken now about alternative courses of action, e.g. now about alternative courses of action, e.g. rent expenses under an unexpired tenancy.rent expenses under an unexpired tenancy.

•• Replacement cost Replacement cost is the amount of cash or the is the amount of cash or the fair value of consideration given to acquire the fair value of consideration given to acquire the assets and expenses now, e.g. the purchase cost assets and expenses now, e.g. the purchase cost for acquiring a material now. for acquiring a material now.

•• Replacement cost may be relevant or irrelevant Replacement cost may be relevant or irrelevant depends on the circumstances.depends on the circumstances.

2020

Example 1 Example 1 (1)(1)

Chai Wan Limited is a Hong Kong based company engaging in the production and supply of a vast variety of durable products and consumer products. 200 kg of material A at a cost of $8,000 are in stock as a result of previous over-buying and they have restricted use. It can be converted for sales at a cost of $2,000. The sales proceeds after the conversion will be $12,000. Material A can now be bought at a cost of $35 per kg. A recent job would require the whole lot of 200 kg of material A. Required:Calculate and explain the relevant cost of using 200 kg of material A for the job.

2121

Example 1 Example 1 (2)(2)

Solution:Solution:

Historical cost Historical cost of $8,000 is a sunk cost and is of $8,000 is a sunk cost and is irrelevant.irrelevant.

Replacement costReplacement cost of $7,000 ($35 x 200) is also of $7,000 ($35 x 200) is also irrelevant here as the company has already had irrelevant here as the company has already had the required quantity. If the job would require, the required quantity. If the job would require, say 250 kg of material A, then replacement cost say 250 kg of material A, then replacement cost is relevant for the additional 50 kg of material A is relevant for the additional 50 kg of material A that need to be bought for the job. that need to be bought for the job.

The The relevant costrelevant cost of using 200 kg of material A of using 200 kg of material A for the job is the for the job is the net net realisablerealisable valuevalue of of $10,000 ($12,000 $10,000 ($12,000 -- $2,000).$2,000).

2222

ShortShort--term business decisions term business decisions

There are a wide variety of short-term business decisions that can show how costing techniques can be used. They include:–– Hire, make or buy decisionsHire, make or buy decisions–– Special order decisionsSpecial order decisions–– Retain or replace equipment decisionsRetain or replace equipment decisions–– Sell or process further decisionsSell or process further decisions

–– Eliminate or retain an unprofitable segment Eliminate or retain an unprofitable segment decisionsdecisions

2323

Hire decisions Hire decisions (1)(1)

Hire decision concerns whether to hire an asset Hire decision concerns whether to hire an asset or not. Basically, the benefits generated from the or not. Basically, the benefits generated from the use of the asset must exceed the cost of having use of the asset must exceed the cost of having the right to use the asset.the right to use the asset.

2424

Example 2 Example 2 (1)(1)

Following a policy in adopting the advanced Following a policy in adopting the advanced manufacturing technology, the management of manufacturing technology, the management of ChaiChai Wan Limited is considering hiring an Wan Limited is considering hiring an automating machine in its automating machine in its DongguanDongguan factory at factory at an annual rent of $230,000 in order to save an annual rent of $230,000 in order to save labourlabour costs and to increase the outputs. costs and to increase the outputs.

Data about the companyData about the company’’s annual sales and costs s annual sales and costs without the machine are:without the machine are:

2525

Example 2 Example 2 (2)(2)

60,000Net profit

190,000Fixed selling overheads

Less: Fixed costs:

250,000Contribution

750,000

150,000Variable overheads

500,000 Direct labour

100,000 Direct materials

Less: Variable costs:

1,000,000Sales

$ Operating statement:Operating statement:

2626

Example 2 Example 2 (3)(3)

With the new machine, it is estimated that annual labour costs will be reduced to $350,000 and the production and sales volume will be increased by 20%. Unit selling price will remain unchanged while other variable costs will be changed in direct proportion to the change in production volume.

2727

Example 2 Example 2 (4)(4)

Required:Required:a.Advise the management, based on financial

consideration alone, whether the new automating machine should be hired or not. Show your calculations.

b.Apart from financial consideration, discuss the other factors that the management needs to consider before coming to a decision.

2828

Example 2 Example 2 (5)(5)

Solution:a.

70,000130,00060,000Net profit

420,000190,000

(230,000)230,000-Rental of the machine

190,000190,000Fixed selling overheads

Less: Fixed costs:

550,000250,000Contribution

650,000750,000

(30,000)180,000150,000Variable overheads

150,000350,000500,000Direct labour

(20,000)120,000100,000Direct materials

Less: Variable costs:

200,000$1,200,000$1,000,000Sales

$$$

Differential benefits/(costs)

Situation with the new machine

Existing situation

Based on financial consideration alone, it is advisable to hire the new machine so as to increase its profit by $70,000.

2929

Example 2 Example 2 (6)(6)

b.Before making the final decision for the hire of the machine, Chai Wan also needs to consider the qualitative factors such as the decline in employee morale and the possible objection from the trade union. Moreover, the accuracy and reliability of the estimates should be ascertained. For example, if the company needs to lay off workers due to the hiring of machine, they may have to pay the redundancy costs.

3030

Make or buy decisions Make or buy decisions (1)(1)

Make or buy decision refers to the situation where a product could be made internally or bought externally. Cost will be of over-riding importance and marginal costing is proved useful in providing a comparison between the cost of buying the product and the marginal cost of production.

Fixed costs are excluded from the analysis, as they would be incurred in any case and so irrelevant for the decision. However, should the fixed costs be increased as a result of the decision, they would be included in determining profit.

3131

Make or buy decisions Make or buy decisions (2)(2)

The decision rule for make or buy decision is The decision rule for make or buy decision is that the company shall take the option with that the company shall take the option with the lowest relevant costs so as to earn the the lowest relevant costs so as to earn the highest profit.highest profit.

Apart from the financial consideration, the Apart from the financial consideration, the company should take into account a variety of company should take into account a variety of qualitative factors in reaching the decision. qualitative factors in reaching the decision.

3232

Make or buy decisions Make or buy decisions (3)(3)

Qualitative factors that may influence the make Qualitative factors that may influence the make or buy decisions include the following:or buy decisions include the following:

a.a. The reliability of the outside supplier with The reliability of the outside supplier with delivery time and quality of the products or delivery time and quality of the products or services provided. services provided.

b.b. Redundancies and decline in employee morale Redundancies and decline in employee morale may result if the components are bought from may result if the components are bought from outside suppliers.outside suppliers.

3333

Make or buy decisions Make or buy decisions (4)(4)

•• The possible uses of the spare capacity upon The possible uses of the spare capacity upon the discontinuance of the production of the the discontinuance of the production of the component.component.

•• The possible future increase in price offered by The possible future increase in price offered by outside suppliers and the possible increase or outside suppliers and the possible increase or decrease in future production costs.decrease in future production costs.

3434

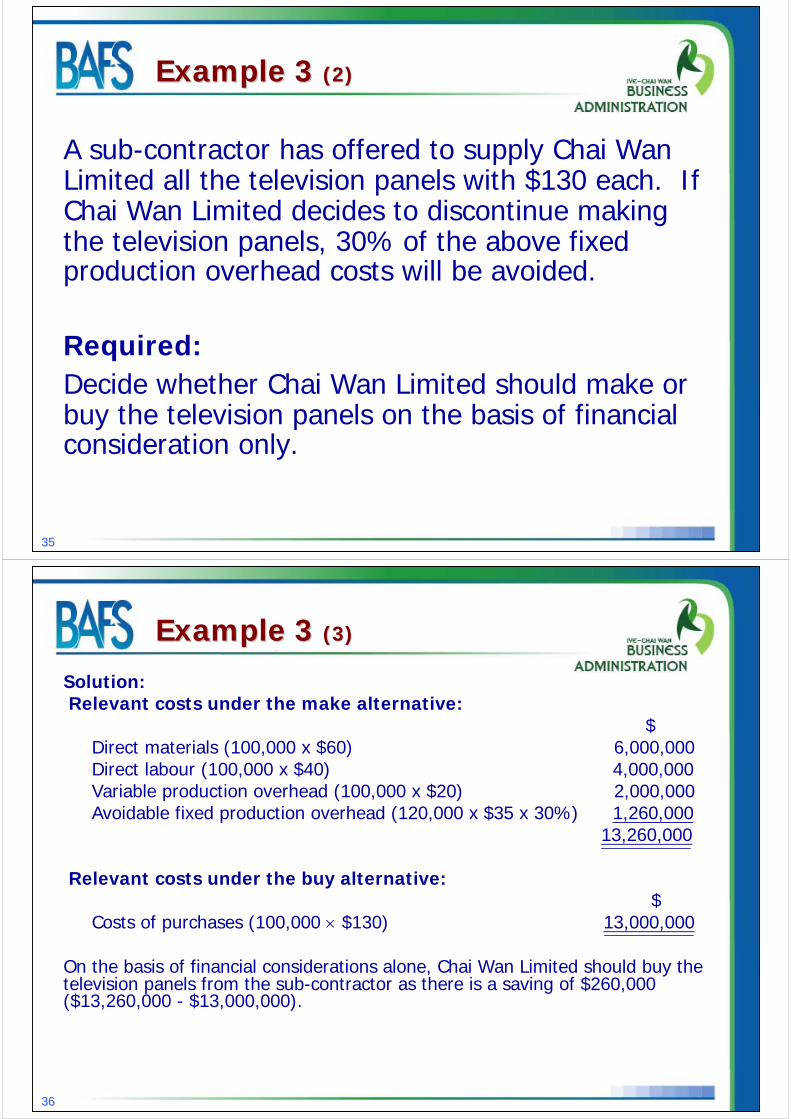

Example 3 Example 3 (1)(1)

Chai Wan Limited makes 100,000 units 20” LCD televisions per year. Currently, it produces the television panels itself. The following data relate to the unit production cost of the television panels at a full capacity of 120,000 units.

Unit production costs:Direct material $60Direct labour $40Variable production overhead $20Fixed production overhead $35

3535

Example 3 Example 3 (2)(2)

A sub-contractor has offered to supply Chai Wan Limited all the television panels with $130 each. If Chai Wan Limited decides to discontinue making the television panels, 30% of the above fixed production overhead costs will be avoided.

Required:Decide whether Chai Wan Limited should make or buy the television panels on the basis of financial consideration only.

3636

Example 3 Example 3 (3)(3)

Solution:Relevant costs under the make alternative:

$Direct materials (100,000 x $60) 6,000,000Direct labour (100,000 x $40) 4,000,000Variable production overhead (100,000 x $20) 2,000,000Avoidable fixed production overhead (120,000 x $35 x 30%) 1,260,000

13,260,000

Relevant costs under the buy alternative:$

Costs of purchases (100,000 × $130) 13,000,000

On the basis of financial considerations alone, Chai Wan Limited should buy the television panels from the sub-contractor as there is a saving of $260,000 ($13,260,000 - $13,000,000).

3737

Special order decisions Special order decisions (1)(1)

This type of decision refers to the situation where normal production would remain unaffected and spare capacity exists so as to facilitate a one-off special order, usually at a lower than normal price, without causing disruption to the regular production.

In a special order decision when there is spare production capacity, relevant revenues and relevant costs are compared in order to determine whether it is worthwhile or not.

3838

Special order decisions Special order decisions (2)(2)

The decision rule is that the special order should be:

(a) accepted, if it generates additional contribution; and

(b) rejected, if it does not generate positive contribution.

3939

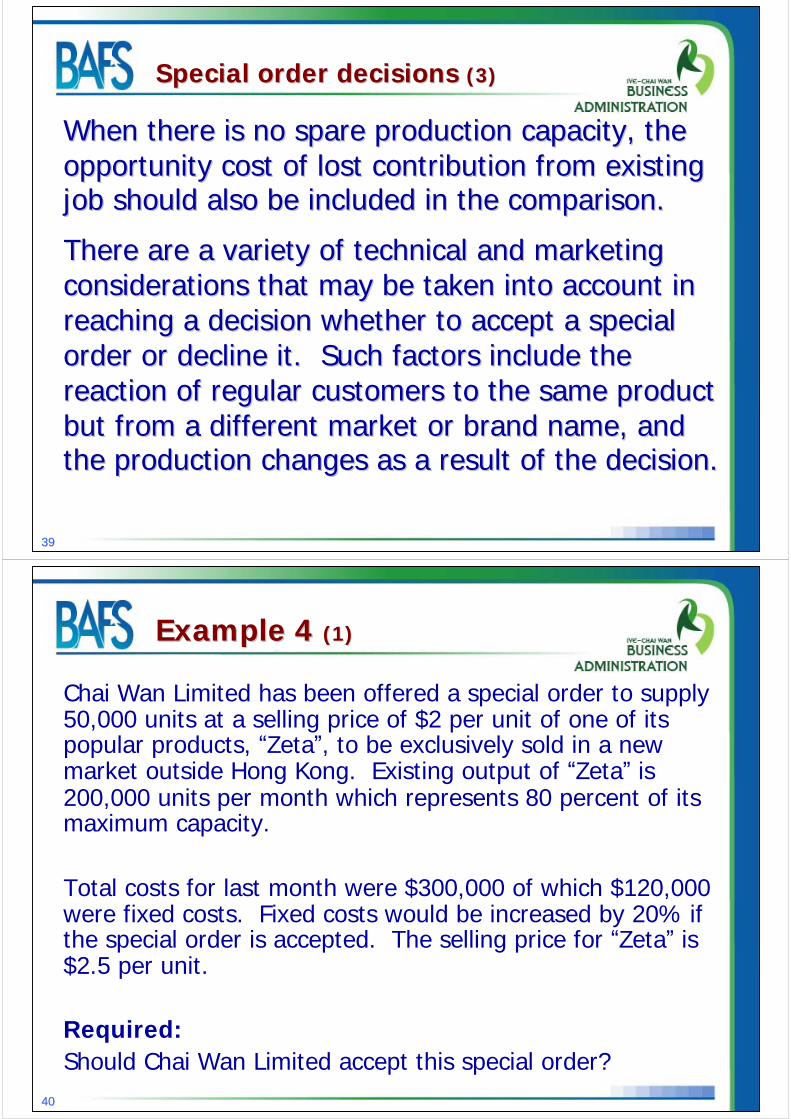

Special order decisions Special order decisions (3)(3)

When there is no spare production capacity, the When there is no spare production capacity, the opportunity cost of lost contribution from existing opportunity cost of lost contribution from existing job should also be included in the comparison.job should also be included in the comparison.

There are a variety of technical and marketing There are a variety of technical and marketing considerations that may be taken into account in considerations that may be taken into account in reaching a decision whether to accept a special reaching a decision whether to accept a special order or decline it. Such factors include the order or decline it. Such factors include the reaction of regular customers to the same product reaction of regular customers to the same product but from a different market or brand name, and but from a different market or brand name, and the production changes as a result of the decision.the production changes as a result of the decision.

4040

Example 4 Example 4 (1)(1)

Chai Wan Limited has been offered a special order to supply 50,000 units at a selling price of $2 per unit of one of its popular products, “Zeta”, to be exclusively sold in a new market outside Hong Kong. Existing output of “Zeta” is 200,000 units per month which represents 80 percent of its maximum capacity.

Total costs for last month were $300,000 of which $120,000 were fixed costs. Fixed costs would be increased by 20% if the special order is accepted. The selling price for “Zeta” is $2.5 per unit.

Required:Should Chai Wan Limited accept this special order?

4141

Solution:

Spare capacity: 200,000 units ÷ 80% x 20% = 50,000 units

Chai Wan Limited has spare capacity to make the required 50,000 units for the special order.

Unit variable cost of “Zeta”: = ($300,000 - $120,000) ÷ 200,000 = $0.9

Example 4 Example 4 (2)(2)

4242

Solution:

Operating statement for the one-off contract:

Since there is additional profit of $31,000 from the special order, ChaiWan Limited should accept the offer.

Example 4 Example 4 (3)(3)

31,000Profit

69,00024,000Incremental fixed costs ($120,000 x 20%)

45,000Less: Variable costs ($0.9 x 50,000)

100,000Sales ($2 x 50,000)

$$

4343

Example 5 Example 5 (1)(1)

Chai Wan Limited has been asked to quote a price for a special order. This order requires 4,000 kg of material X, which is used regularly by the company in other production. The company has 10,000 kg of material X in stock which had been purchased last month for total costs of $200,000. Since then the price per kg has been increased by 10%. 800 labour hours have to be diverted from existing production of product “Vera” and $30,000 variable overheads to be incurred.

Details of product “Vera” are as follows:$ per unit $ per unit

Selling price 500Less: Direct material 80

Direct labour (2 hours at $50 per hour) 100 Variable overheads 20 200

300

4444

Example 5 Example 5 (2)(2)

Required:

What is the minimum selling price Chai Wan Limited should quote for the special order?

4545

Example 5 Example 5 (3)(3)

Solution:

Relevant cost for the special order:$

Direct material X ($200,000 ÷ 10,000 x 110% x 4,000 kg) 88,000Direct labour ($50 x 800 hours) 40,000Variable overheads 30,000Contribution loss from product “Vera” ($300 ÷ 2 hours x 800 hours) 120,000

278,000

The minimum selling price for the special order is $278,000.

4646

Retain or replace equipment Retain or replace equipment decisionsdecisions (1)(1)

When equipment has almost reached the end of its estimated useful life or there is a newer or more efficient model, the company will consider replacing the existing equipment. For this type of decision, the cost, accumulated depreciation and book value of existing equipment are past costs and are thus irrelevant.

4747

Retain or replace equipment Retain or replace equipment decisionsdecisions (2)(2)

The relevant cost is the cost of the new equipment because it is an expected future cost that will only occur if the equipment is purchased. In addition, the possible savings in operating costs are relevant in making retain or replace equipment decisions.

The general decision rule is to select the alternative that will generate the highest profit.

4848

Example 6 Example 6 (1)(1)

Chai Wan Limited is considering replacing a printing machine with a new model, which is more efficient than the existing one for itsmagazine publishing business. Data for the existing (old) machine and the replacement (new) machine are as follows:

Required:Advise Chai Wan Limited whether to retain or replace the old machine.

$550,000$1,000,000Annual operating costs

$0$10,000Terminal disposal value (3 years later)

N/A$60,000Current disposal value

N/A$1,200,000Carrying amount

N/A$800,000Accumulated depreciation

3 years3 yearsRemaining useful life

0 years2 yearsCurrent age

3 years5 yearsEstimated useful life

$1,200,000$2,000,000Purchased cost

New machineOld machine

4949

Example 6 Example 6 (2)(2)

Solution:

Chai Wan Limited should replace the old machine with the new machine since there is a lower relevant cost and thus will bring in an additional benefit of $200,000 in total in the next three years.

200,0002,790,0002,990,000Total relevant costs(1,200,000)1,200,000

New machine, written off periodically as depreciation (W2)

(10,000)-(10,000)Terminal disposal value of old machine

60,000(60,000)-Current disposal value of old machine

1,350,0001,650,0003,000,000Cash operating costs (W1)$$$

DifferenceReplaceRetainThree years together

5050

Example 6 Example 6 (3)(3)

Working:

(W1) Cash operating costs for retaining the old machine: $1,000,000 x 3 = $3,000,000Cash operating costs for replacing the old machine with the new machine: $550,000 x 3= $1,650,000

(W2) The cost of old machine is sunk cost and is thus excluded.

5151

Sell or process further decisions Sell or process further decisions (1)(1)

In continuous production industries such as oil refining, soap manufacturing, food processing and paper making, etc, they will adopt the process costing system. When two or more products are separated from a joint processing operation, that joint processing operation is known as separation point or split-off point. Joint costs incurred in the joint processing operation have to be allocated among the joint products.

5252

Sell or process further decisions Sell or process further decisions (2)(2)

There are three common methods to allocate the joint costs to the joint products. They are:

(a) Physical measurement basis;(b) Sales value at split-off point basis; and(c) Net realisable value (sales value of the end

product less further processing costs beyond split-off point) basis.

5353

Sell or process further decisions Sell or process further decisions (3)(3)

After the split-off point joint products may be ready to sell or they can undergo further processing by incurring further processing costs to secure a higher sale value. For example, in petroleum refining industry, crude oil and natural gas are joint products from the initial process. They can be sold separately after the split-off point. Crude oil can further refined to produce enhanced joint products such as petrol which can be sold at a much higher price.

5454

Sell or process further decisions Sell or process further decisions (4)(4)

The sell or process further decisions should be based the difference between the incremental revenue attainable and the further processing costs incurred beyond the split-off point. How the joint costs will be allocated to the joint products is irrelevant to the sell or process further decisions.

The decision rule is that the product should be processed further if the enhanced product generates additional contribution; and the product should be sold immediately after the split-off point if the enhanced product does not generate additional contribution.

5555

Example 7Example 7 (1)(1)

Chai Wan Limited has a farm in Shenzhen which grows and processes chicken. Each chicken is disassembled into three main parts: breasts, wing and thigh. Every month it produces 50,000 pounds of breasts, 20,000 pounds of wings and 30,000 pounds of thighs at joint costs of $150,000. The company currently allocates the joint costs based on the physical measurement basis.

5656

Example 7Example 7 (2)(2)

The company is considering whether to further process the joint products by taking a frying process to sell fried chicken breasts, wings and thighs.

The following information is also provided.

5757

Example 7Example 7 (3)(3)

$13$4$10Thighs

$15$3$8Wings

$23$5$15Breasts

Selling price per pound of

the fried products

Further processing costs per pound

Selling price per pound at split-off point

Parts

5858

Example 7Example 7 (4)(4)

Required:

Should the chicken breasts, wings and thighs be further processed?

5959

Example 7Example 7 (5)(5)

Solution:

The joint costs to be allocated based on the physical measurement are irrelevant.

We have to compare the incremental revenues and the incremental process costs of the three products separately to decide which product(s) is/are worth to further process.

6060

Example 7Example 7 (6)(6)

Solution:

Further processing chicken breasts into fried chicken breasts:$

Incremental revenues $(23 – 15) x 50,000 pounds 400,000

Less: Incremental process costs $5 x 50,000 pounds 250,000

Increase in profit from fried chicken breasts 150,000

6161

Example 7Example 7 (7)(7)

Solution:Solution:

Further processing chicken wings into fried chicken wings:$

Incremental revenues $(15 – 8) x 20,000 pounds 140,000

Less: Incremental process costs $3 x 20,000 pounds 60,000

Increase in profit from fried chicken wings 80,000

6262

Example 7Example 7 (8)(8)

Solution:Solution:

Further processing chicken thighs into fried chicken thighs:$

Incremental revenues $(13 – 10) x 30,000 pounds 90,000

Less: Incremental process costs $4 x 30,000 120,000

Decrease in profit from fried chicken breasts (30,000)

6363

Example 7 Example 7 (9)(9)

Solution:

Chai Wan Limited should further process chicken breasts and chicken wings into fried chicken breasts and chicken wings, and sell chicken thighs in its raw form.

6464

Eliminate or retain an unprofitable Eliminate or retain an unprofitable segment decisions segment decisions (1)(1)

It is quite common for companies to prepare divisional operating statements to assess the relative effectiveness and profitability of each segment.

Management may investigate into those unprofitable segments identified from segment operating statements and have to decide whether to keep it or not.

6565

Eliminate or retain an unprofitable Eliminate or retain an unprofitable segment decisions segment decisions (2)(2)

The decision rule for retaining or eliminating by selling or shutting down an unprofitable segment, is to select the course of action that adds profit to the company.

6666

Example 8 Example 8 (1)(1)

The following data relates to three products of Chai Wan Limited:

It has been suggested to sell the unprofitable product, Rose. $100,000 of the fixed costs of Rose are direct fixed costs which will be saved if its production ceases. All other fixed costs would remain the same.Required:Should product Rose be retained or eliminated?

140140(150)(150)170170120120Profit/(loss)Profit/(loss)

2,2602,2601,1501,150630630480480

1,2501,250550550400400300300Fixed costsFixed costs

1,0101,010600600230230180180Less: Variable costsLess: Variable costs

2,4002,4001,0001,000800800600600SalesSales

$$’’000000$$’’000000$$’’000000$$’’000000

TotalTotalRoseRosePeonyPeonyLilyLilyProductProduct

6767

Example 8 Example 8 (2)(2)

Solution:To discontinue production of Rose, the operating results will be:

$Loss of contribution ($1,000,000 - $600,000) (400,000)Savings in attributable fixed costs 100,000Incremental loss (300,000)

Chai Wan Limited should not discontinue the production of product Rose as it will cause a drop in profit of $300,000. Instead, the company may consider the possibility of switching the resources from producing Rose to other more profitable products.

6868

Importance of qualitative factorsImportance of qualitative factors (1)(1)

Many examples above on business decision making are not based on financial consideration only but also involve consideration of qualitative factors.

In most situations, it is difficult to quantity in monetary terms all relevant factors in making a decision. These qualitative factors should be considered by the management during the evaluation process in order to make a wise decision.

6969

Importance of qualitative factorsImportance of qualitative factors (2)(2)

For example, the cost of buying components from an outside supplier may be cheaper than producing internally. However, if such decision results in the closure of a segment for producing the components, this will likely lead to redundancies and create bad effect on employee morale, which can affect future productivity.

The decline in employee morale may not easily be quantified in monetary terms, but management has to think about its possible impact on the company’s future profitability.

7070

Further considerationFurther consideration

In this unit, we ignore the time value of money in our analysis in situations that have cash inflows or outflows for more than one year. Take for example, in Example 8, if the time value of money is taken into account, the relevant cost items will be discounted at an appropriate discount rate (cost of capital) before the differential costs are computed.

For further information concerning the time value of money, please refer to Unit 10 “Capital Investment Appraisal”.

7171

Further readingsFurther readings (1)(1)

•• Horngren et al, (2006), Horngren et al, (2006), Cost Accounting , A Cost Accounting , A Managerial EmphasisManagerial Emphasis, Pearson, 12th Edition, , Pearson, 12th Edition, Chapter 11.Chapter 11.

•• Drury, C. (2004), Drury, C. (2004), Management and Cost Management and Cost AccountingAccounting, London, Thomson, 6th Edition, , London, Thomson, 6th Edition, Chapter 9.Chapter 9.

•• Garrison et al, (2006), Garrison et al, (2006), Managerial AccountingManagerial Accounting, , McGrawMcGraw--Hill, 11th Edition, Chapter 13.Hill, 11th Edition, Chapter 13.

•• Li, T. M. and Ng, P. H. (2007), Li, T. M. and Ng, P. H. (2007), HKAL HKAL –– Principles Principles of Accounts (Volume 2)of Accounts (Volume 2), Pilot Publishing Company , Pilot Publishing Company Ltd, 2nd Edition, Chapter 24. Ltd, 2nd Edition, Chapter 24.

7272

Further readingsFurther readings (2)(2)

•• 王怡心王怡心 ((二二0000二年二年)),,管理會計管理會計,台北,台北::三民書局,三民書局,修訂二版,第十章修訂二版,第十章 。

7373

End of the Unit End of the Unit

This is the end of Unit 9. This is the end of Unit 9. Please go to the Unit Please go to the Unit Assessment before Assessment before attempting the next unit.attempting the next unit.

EndEnd--ofof--unit Assessmentunit Assessment