unit v export incentives

TRANSCRIPT

UNIT V

Export IncEntIvEs

Dear MIBians • Lets discuss the aim and objectives of

export incentives ? • What are all the different type of schemes

are available ? • CASE STUDY OF INDIA

The 1992 -97 Mantra in India

• India’s external Trade policy [laid down the foundation of globalization of Indian economy].• Initiating liberalization and making

Indian industries to face competition from foreign MNCs

Just EXPLORE

•IMPORT is a source to encourage EXPORT•How to document the statement

Support which Indian exporters GET • JUST see your FTP [2009-14]

EPCG[ Export Promotion Capital Goods Scheme]

Introduced in 1992-97 EXIM policy.

To enable exporter to import capital goods.

Export obligation !! i.e EXPORTER required to guarantee exports of certain minimum value, which is multiple of the value of capital goods imported.

Advance Authorizations Scheme • Allow duty free imports of inputs,

which are physically incorporated in exports.[ in addition fuel, oil, energy, catalysts, which are used to discover export products. • Up to 10% of CIF value of authorization

are allowed under this scheme.

Duty free import authorization[DFIA]

• DFIA is issued to allow duty free imports of inputs, fuel, oil, energy sources, catalyst which are required in export production.• This is given based on the SION

-Standard INPUT OUTPUT norms]

DUTY remission Schemes • Duty Entitlement Passbook [ BEPB] : is to

neutralize the incidence of customs duty on import contents of export product.

• Here Exporter may apply for credit as a specified percentage of FOB value of exports.

• Such credit may be utilized for payment of customs duty on freely importable items/ or restricted items and also on imports under EPCG Scheme.

What is this ? Export promotion capital goods (EPCG) scheme of

Government of India allows import of capital goods at concessional duty. In return company should export some quantity of its production. Indian company Nippon Dendro Ispat Ltd. Imported capital goods from Taiwan. Taiwan Company supplied the machine which reached Mumbai without any damage. But from Mumbai to Pune transit, the machinery vehicle met an accident to cost to damage to machinery. The company could not use the machinery and could not fulfill the export order. Therefore company will have to increase export marketing to compensate the loss.

DBK[ Duty Drawback Scheme] • Administered by the Directorate of Drawback,

Dept. of Revenue, Ministry of Finance, Govt. of India, Jeevan Deep, Parliament Street, New Delhi - 110 001.

• Under this scheme: Exporters are entitled to claim: 1. Customs duty paid on the import of raw materials, components, and consumables.

• 2. Central excise duty paid on indigenous raw materials, components and consumables utilized in the manufacture if exportable goods.

Classification of DBK • All Industry rates: • Brand rates • Special brand rates [ Performa

I,II and III] • ElGILIBILITY :

Claiming DBK • CLAIMING advance : read

directorate manual • Execution of BOND:• Green shipping BILL: TRIPLICATE

COPY accompanied by L/C, PACKING LIST/ ARE-1 /insurance cert/special brand rate.

Excise duty refund • Excise duty is a tax by Central government on good mfd

in India. This duty is collected at source, ie. Removal of goods from factory premises.

• Though exports goods are exempted /// • But for necessary clearance the following methods are

used:

1. export under rebate

2.Export under bond

Rebate/ bond Procedure for Excise Clearance under Bond / Letter Undertaking// The procedure

under this rule is similar to the one under claim for rebate. This is governed under Rule 13.

Under this rule, there is no PLA(personal Ledger Account) as no duty is paid. Instead of payment of duty, the manufacturer exporter executes bond/letter of undertaking to the amount equivalent to the excise duty. Bond can be executed with surety or without surety. Such a bond is to be supported by the bank guarantee to protect financial interests of excise department. Exporters of the following categories are allowed to execute bond with surety and do not have to furnish any bank guarantee or cash security.

Super Star Trading House/Star Trading House /Trading House/Export House/ Registered Exporters (Registered with relevant Export Promotion Council)

Application for refund claim• Triplicate copy of the Bill of Entry / Post parcel wrapper / shipping bill / baggage

receipt / purchase invoice (as the case may be).• 2. Letter from the importer / buyer / exporter (in case the applicant is an agent)• 3. Duty Challan / other document as evidence of duty payment.• 4. Signed working sheet for the amount of refund claimed.• 5. Customs attested invoice and packing list.• 6. Bill of Lading / Airway Bill.• 7. Documents for establishing the applicant’s eligibility to receive the refund amount

in terms of the proviso to sub-section (2) of Section 27 of the Act (for e.g. CA certificate), including documents for the purposes of section 28C and 28D of the Act. (wherever applicable).

• 8. Contract and Purchase Order.• 9. Order-in-Original / in revision / in appeal / any other order. (wherever applicable).• 10. Short delivery certificate from custodian.• 11. Short shipment certificate from supplier.• 12. Survey report. (wherever applicable).

• 13. Insurance claim settlement certificate. (wherever applicable).• 14. Catalogue / technical write up / literature. (wherever

applicable).• 15. Bills for freight / insurance/other charges. (wherever

applicable).• 16. Certificate of Origin. (wherever applicable).• 17. Inventory list (for e.g. in case of refund of duty on bunkers on

reversion of a vessel to foreign-run).• 18. Modvat / Cenvat credit certificate from Central Excise

authorities (for e.g. in case of refund on account of export duty).• 19. Any other document considered necessary in support of the

claim

Central Tax Exemption • Sce.5 of CST act,1956: “ Any

dealer who is registered with sales tax authority can claim exemption in terms of sales made by him outside India// for H

What are those forms F,C ,H and all?• "C" Form is issued by buyer who is registered dealer. If the buyer

issues "C" form, he can purchase goods at concessional rates in the inter-state sale. C Form can be issued only by a registered dealer to another registered dealer. It can be issued, generally, only in respect of raw materials, packing materials goods covered by the certificate of registration of the issuing dealer.

• "F" form is evidence to provide that goods are sent in stock transfer basis and not on sale. The consignment agent/ branch receiving is required to issue "F" form to the selling dealer.

• "H" Form is issued when the buyer buys the goods for export. If buyer issue "H" form, the selling dealer is not required to charge or pay any CST on the transaction

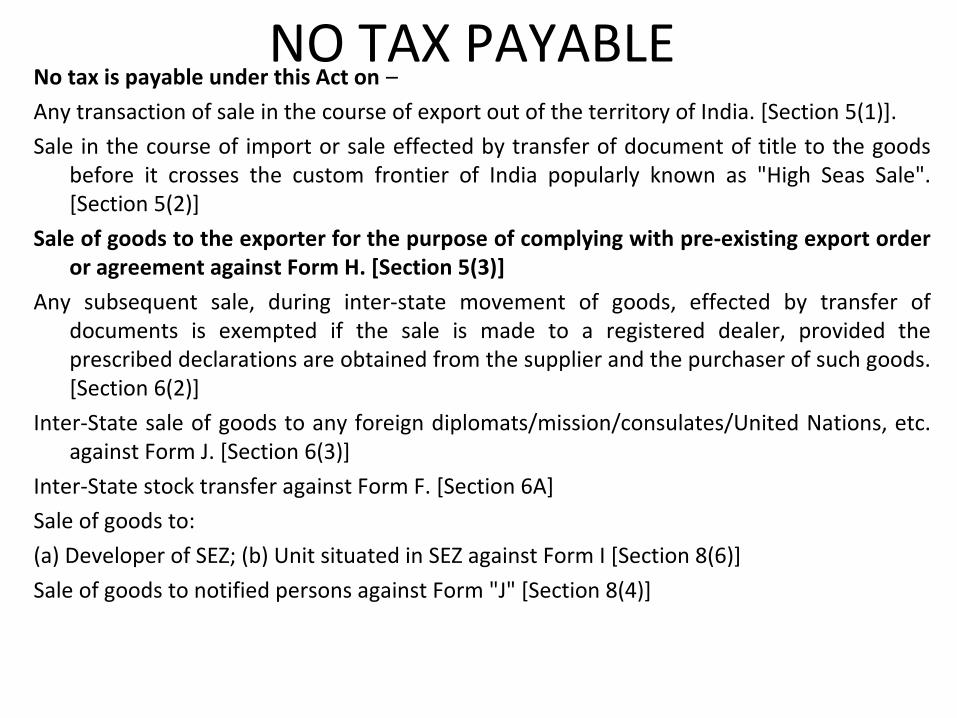

NO TAX PAYABLE No tax is payable under this Act on –

Any transaction of sale in the course of export out of the territory of India. [Section 5(1)].

Sale in the course of import or sale effected by transfer of document of title to the goods before it crosses the custom frontier of India popularly known as "High Seas Sale". [Section 5(2)]

Sale of goods to the exporter for the purpose of complying with pre-existing export order or agreement against Form H. [Section 5(3)]

Any subsequent sale, during inter-state movement of goods, effected by transfer of documents is exempted if the sale is made to a registered dealer, provided the prescribed declarations are obtained from the supplier and the purchaser of such goods. [Section 6(2)]

Inter-State sale of goods to any foreign diplomats/mission/consulates/United Nations, etc. against Form J. [Section 6(3)]

Inter-State stock transfer against Form F. [Section 6A]

Sale of goods to:

(a) Developer of SEZ; (b) Unit situated in SEZ against Form I [Section 8(6)]

Sale of goods to notified persons against Form "J" [Section 8(4)]

Exemption from service tax • Levi able only on taxable services

supplied within India except Jammu and Kashmir / read Export service rules 2005::: all those services exported outside the territory of India are exempted from service tax

Octroi Exemption EXEMPTION FROM OCTROI [EXPORT ROMOTION] RULES 1976.

Every claim for exemption from Octroi under these Rules must be supported by an application for exemption in triplicate in form 'EP, ' annexed to these Rules and duly filled in and signed by a Registered Exporter or by a Custom House Agent who may be Authorised to sign such 'EP' From under the condition of the Bond or by a person holding power of attorney from under the condition of the Bond or by a person holding power of attorney from a registered exporter, and no such application shall be entertained unless it fulfills the following conditions.

Forms to be used by tax-payers.FormRemarksADeclaration-cum-application to pay Octroi, to be filled in by the importer

at the time of import. ( Rules 4, 6, 8 & 12 of Levy of Octroi Rules. )BImport Octroi Bill - Receipt showing

Octroi Collected. ( Rules 4, 6, 8 &12 of Levy of Octroi Rules. )C (Front)

C (Back)Octroi Export Note for use in case of export by Sea. (Rule 4, Refund of Octroi Rules). Also in case of export by Air.CCOctroi Export Note

for use in case of export by Road. ( Rule, 29(g), Refund of Octroi Rules. )D (Front)

D (Back)Application for refund on account of export.

( Rule, II (a) Refund of Octroi Rules.)ERefund Receipt. [ Rule, 11 ( c ), Refund of Octroi Rules. ]EP (Front)EP (back)Application for exemption in respect of

articles imported for export to Foreign Countries. (Rule, 5-A, Export Promotion Rules. )

FISCAL INCENTIVES A) Exemption from Income Tax : to promote

export –just dilute IT act, 1961.

Ten Year Tax holiday to newly established industrial undertakings in FTZs, Electronic hardware , Techno parks, software techno9logy parks (Sec.10 A)

15 years Tax holiday for SEZ ( Sec.10AA)

10 YEARS for 100% EOUs

Wood based handicrafts ( sec. 10 B)

Marketing Assistance • MDA- Market development Assistance [ EPCs,

commodity boards, FIEO• MAI- market Access initiative [ survey/ field

study]

Supply of Raw Materials: Indian Raw material assistance centre

Back to back inland L/C

Marketing Development Assistance (MDA)

The Ministry of Commerce and Industry has a scheme of MDA, which was launched in 1963 with a view to stimulate and diversify the export trade, along with the development of marketing of Indian products and commodities abroad. The MDA is utilized for: Market research, commodity research, area survey and research; Participation in trade fairs and exhibitions;

MDI………..Export publicity and dissemination of

information; Trade delegation and study teams; Establishment of offices and branches in abroad; Grant-in-aid to Export Promotion Councils and other approved organizations for the development of exports and the promotion of foreign trade; and any other scheme which is generally aimed at promoting the development of markets for Indian products and commodities abroad.

Market Access Initiative (MAI)The Ministry of Commerce and Industry has introduced

the MAI in April 2001 with the idea that the Government shall assist the industry in R&D, market research, specific market and product studies, warehousing and retail marketing infrastructure in select countries and direct market promotion activities through media advertising and buyer-seller meets. Financial assistance shall be available under the scheme to EPCs, industry and trade associations and other eligible activities, as may be notified from time to time. A small allocation of Rs 42 crore has been made for 2002-03.

Central Assistance to StatesThe State Governments shall be encouraged to fully

participate in encouraging exports from their respective States. For this purpose, a new scheme “Assistance to States for Infrastructural Development for Exports” (ASIDE) has been initiated which would provide funds to the States based on the twin criteria or gross exports and the rate of growth of exports from different States. Eighty per cent of the total funds would be allotted to the States based on the above criteria and remaining 20 per cent will be utilized by the Centre for various infrastructure activities that cut across State boundaries, etc. A sum of Rs 49.5 crore has already been sanctioned for 2001-02 and further a sum of Rs 330 crore has also been approved for 2002-03. The State shall utilize this amount for developing complementary and critical infrastructure.

Towns of Export Excellence• A number of towns in specific geographical locations have

emerged as dynamic industrial locations and handsomely contributing to India’s exports. These industrial cluster-towns have been recognized with a view to maximiing their export profiles and help in upgrading them to move up the higher value markets. A beginning is being made to consider industrial cluster towns such as Tirupur for Hosiery, Panipat for Woollen Blankets and Ludhiana for Woollen knitwear. Common service providers in these areas shall be entitled for EPCG Scheme, funds under the MAI scheme for creating focused technological services, priority assistance for identified critical infrastructural gaps from the Scheme on Central Assistance to States. Units in these notified areas would be eligible for availing all the Exim Policy Scheme.

Special Economic Zones (SEZ)• The Government of India had announced an SEZ

scheme in April 2000 to promote India’s exports. Four Export Processing Zones (EPZ), namely Noida (UP), Falta (West Bengal), Chennai (Tamilnadu), and Viskhapatnam (Andhra Pradesh) have been converted into SEZs from 1 January 2003. There are seven EPZs in the country. In addition, three formal approvals and 14 in-principle approvals have been granted for the establishment of SEZs in private, state, and joint sectors. Policy initiatives taken to promote SEZs include duty-free import/domestic procurement of goods for development…………

….operation and maintenance of SEZs and SEZ units, external commercial borrowing up to $500 million in a year without any maturity restriction through recognized banking channels and a facility to set up overseas banking units in SEZs. The SEZ units have also been getting exemption from central sales tax on sales made from the domestic tariff area to SEZ units and exemption from service tax to SEZ units and developers.

Duty Drawback on Goods ExportedUnder this Duty Drawback scheme export products

get relief of incidence of customs and excise duties paid on raw materials and components used at various stages of production. It is defined as “rebate of duty chargeable on any imported or excisable material used in the manufacture of goods exported from India. Duty Drawback is admissible for exports irrespective of mode of export, i.e. whether despatched by Sea, Air, Land Customs or by Post.

WOW… institutions • IIFT • EPCs• EICs • Indian Council of Arbitration • FIEO • EXIM • What not

WHY DON’T you present ??

• Is there any special documentation for DEEMED EXPORTS

DFIA [ duty free import authorization] • EOUs• Software Techno Parks • Electronic Hardware TECHNO parks[ EHTPS] • Bio- Tech parks • Supply of goods • Supply of Infrastructure • Supply of projects • What not ??

Hey! Deemed exporter • You enjoy

Advance authorization – duty free authorization

Deemed export drawback

Exemption from Terminal excise duty where – you deal international competitive bidding

TOWN of export Excellence

•Why don’t you remember some right now •Why are the called as Town of export excellence