united arab market overview emirates -...

TRANSCRIPT

RCSC – Study tour – February 2013 1 AE – United Arab Emirates – Market overview

Market overview

UNITED ARAB

EMIRATES

Guide 24 – 28 February 2013

RCSC Study Tour Dubai & Abu Dhabi

RCSC – Study tour – February 2013 2 AE – United Arab Emirates – Market overview

AE – UNITED ARAB EMIRATES – market overview From: HKo Date: February 2013 Introduction

• The United Arab Emirates is the trend setting market in the Gulf region, and of the main destinations for international retail formats.

• Dubai is together with London and New York among the most internationalized retail markets in the world, while Abu Dhabi is rapidly catching up.

• Dubai transformed itself from an oil based economy into the main hub in the Middle East for financial services, trade and tourism.

• Both Dubai and Abu Dhabi grew from small towns several decades ago into large international hubs nowadays.

• This report presents some back ground on the United Arab Emirates, as well as the retail markets and main shopping centers in Dubai and Abu Dhabi.

Content United Arab Emirates 2

• General, economy, state structure, retail, property market Dubai 10

• Overview, retail market, retail property market, shopping centers Abu Dhabi 32

• Overview, retail market, retail property market, shopping centers UNITED ARAB EMIRATES General

• Trucial States of the Persian Gulf coast granted the UK control of their defense and foreign affairs in 19th century treaties.

• In 1971, six of these states - Abu Dhabi, 'Ajman, Al Fujayrah, Sharjah, Dubai, and Umm al Quwayn - merged to form the United Arab Emirates (UAE). They were joined in 1972 by Ras al Khaymah.

• The UAE's per capita GDP is on par with those of leading West European nations. Its high oil revenues and its moderate foreign policy stance have

• allowed the UAE to play a vital role in the affairs of the region. For more than three decades, oil and global finance drove the UAE's economy.

• However, in 2008-09, the confluence of falling oil prices, collapsing real estate prices, and the international banking crisis hit the UAE especially hard.

• The UAE has essentially avoided the "Arab Spring" unrest seen elsewhere in the Middle East, though in March 2011, political activists and intellectuals signed a

RCSC – Study tour – February 2013 3 AE – United Arab Emirates – Market overview

petition calling for greater public participation in governance that was widely circulated on the Internet. In an effort to stem potential further unrest, the government announced a multi-year, $1.6-billion infrastructure investment plan for the poorer northern Emirates.

• The UAE is one of the most liberal countries in the Gulf but still does not have formally elected bodies.

Geography & climate

• Location: Middle East, bordering the Gulf of Oman and the Persian Gulf, between Oman and Saudi Arabia

• Area: 83,600 km2 • Climate: desert; cooler in eastern mountains • Terrain: flat, barren coastal plain merging into rolling sand dunes of vast desert

wasteland; mountains in east. Population

• Population: 5.3 million (July 2012) o note: only approximately 20% are UAE citizens

• Ethnic groups: Emirati 19%, other Arab and Iranian 23%, South Asian 50%, other expatriates (includes Westerners and East Asians) 8% (1982)

• Languages: Arabic (official), Persian, English, Hindi, Urdu • Urban population: 84% of total population • Average life expectancy: 77 years

Source: CIA World Factbook

RCSC – Study tour – February 2013 4 AE – United Arab Emirates – Market overview

Economy • The UAE has an open economy with a high per capita income and a sizable

annual trade surplus. Successful efforts at economic diversification have reduced the portion of GDP based on oil and gas output to 25%.

• Since the discovery of oil in the UAE more than 30 years ago, the country has undergone a profound transformation from an impoverished region of small desert principalities to a modern state with a high standard of living.

• The government has increased spending on job creation and infrastructure expansion and is opening up utilities to greater private sector involvement. In April 2004, the UAE signed a Trade and Investment Framework Agreement with Washington and in November 2004 agreed to undertake negotiations toward a Free Trade Agreement with the US; however, those talks have not moved forward.

• The country's Free Trade Zones - offering 100% foreign ownership and zero taxes - are helping to attract foreign investors.

• The global financial crisis, tight international credit, and deflated asset prices constricted the economy in 2009. UAE authorities tried to blunt the crisis by increasing spending and boosting liquidity in the banking sector. The crisis hit Dubai hardest, as it was heavily exposed to depressed real estate prices. Dubai lacked sufficient cash to meet its debt obligations, prompting global concern about its solvency. The UAE Central Bank and Abu Dhabi-based banks bought the largest shares. In December 2009 Dubai received an additional $10 billion loan from the emirate of Abu Dhabi.

• Dependence on oil, a large expatriate workforce, and growing inflation pressures are significant long-term challenges. The UAE's strategic plan for the next few years focuses on diversification and creating more opportunities for nationals through improved education and increased private sector employment.

• As a member of the Gulf Cooperation Council (GCC), the UAE participates in the wide range of activities that focus on economic issues, including development of common policies covering trade, investment, banking and finance, transportation, telecommunications, and other areas. Having implemented a customs union in January 2003, the GCC is taking further steps to integrate economic systems, including a proposed move to a single currency, but the UAE opted out of this in May 2009. The AED has been pegged to the US$ at close to AED3.67 since 1980.

Key ratings United Arab Emirates Rating Foreign currency Local currency

Fitch AA (Stable) AA (Stable)

Moody's Aa2 (Stable) Aa2 (Stable)

S&P AA (Stable) AA (Stable)

Source: Oxford Economics

RCSC – Study tour – February 2013 5 AE – United Arab Emirates – Market overview

Corruption perceptions index Area Score

Developed economies average 74,8

Emerging economies average 38

United Arab Emirates 68

Middle East 41,3

Source: Transparency International • 100 = highly clean, 0 = highly corrupt

Economic outlook

• GDP growth outlook positive, to pickup to 3.7% in 2013 from an estimated 3.3% in 2012.

• Growth drivers: o improvement in domestic activity o benefit from faster growth in emerging markets o supportive fiscal policy in Dubai and Abu Dhabi.

• New mortgage regulations were announced at the end of last year, setting caps on lending to property buyers. Such prudential measures should benefit the sector in the long term by checking some of the speculative short-term buying that preceded the bursting of the property bubble in 2008/09. However, in the short run these regulations are also likely to limit the pace of a still-tentative property market recovery.

o The loan-tovalue limit is to be set at 50% for expatriates and 70% for Emiratis buying their first property.

• Growth outlook for Dubai will be strong as its property and construction sectors continue to recover and its trade, tourism and logistics sectors remain strong.

• Growth in Abu Dhabi will remain healthy, but will be checked by the modest fall in oil prices that is anticipated.

Economic outlook United Arab Emirates

2011 2012-E 2013-F 2014-F 2015-F

GDP 4,2% 3,3% 3,7% 3,9% 4,1%

CPI inflation 0,9% 0,7% 2,0% 2,7% 3,0%

Current account 9,1% 10,5% 6,3% 4,7% 4,2%

Government balance 6,2% 8,5% 5,9% 5,7% 6,2%

Exports of goods (%) 30,7% 38,8% 23,9% 19,2% 18,4%

Imports of goods (%) 22,8% 14,9% 13,0% 10,0% 9,0%

Source: Oxford Economics

• Main risk for the UAE involves the stability of its financial system, as the UAE cannot be said to have fully resolved its debt problems. In December 2012, Moody’s downgraded three Dubai banks – including the largest, Emirates NBD – and placed all on negative watch. This decision was connected to:

o Elevated problem loan (NPL) levels in the 15% to 17% range”, well above the regional GCC average of 6.1%.

RCSC – Study tour – February 2013 6 AE – United Arab Emirates – Market overview

o Low coverage ratios compared to the global median of similarly rated peers leaves UAE banks exposed to further increases in NPLs.

• Thus, three years on from the financial crisis, asset quality problems persist and present a downside risk to the stability of the UAE’s financial system.

State structure

• Federation with specified powers delegated to the UAE federal government and other powers reserved to member emirates.

• Capital city: Abu Dhabi • Federation of 7 emirates (imarat, singular - imarah): Abu Dhabi, 'Ajman, Al

Fujayrah, Sharjah, Dubai, Ras al Khaymah, Umm al Quwain. • Executive branch:

o Chief of state: President Khalifa bin Zayid Al-Nuhayyan (since 3 November 2004), ruler of Abu Dhabi (since 4 November 2004);

o Vice President and Prime Minister Muhammad bin Rashid Al-Maktum (since 5 January 2006)

o Federal Supreme Council (FSC), composed of the seven emirate rulers, is the highest constitutional authority in the UAE; establishes general policies and sanctions federal legislation; meets four times a year. Abu Dhabi and Dubai rulers have effective veto power

• Legislative branch: o Unicameral Federal National Council (FNC), o 40 seats; 20 members, appointed by the rulers of the constituent states,

20 members elected to serve four-year terms o Election results: elected seats by emirate - Abu Dhabi 4, Dubai 4, Sharjah

3, Ras al-Khaimah 3, Ajman 2, Fujairah 2, Umm al-Quwain 2. Number of appointed seats for each emirate are same as elected seats;

• Judicial branch: o Union Supreme Court (judges are appointed by the president)

• Political parties and leaders: o Not allowed

Retail market

• The UAE has an open economy with a high per capita income and a sizable annual trade surplus. Successful efforts at economic diversification have reduced the portion of GDP based on oil and gas output to 25%.

• Mm • Growth drivers:

o Growing GDP, substantial government spending, low fuel prices, and low or no tax incidence ease substantial portions of individuals’ income to spend on food and non-food items.

o The GCC hospitality industry is being developed as an all-round tourist attraction. In line with the continued uptrend in tourist traffic, all the GCC countries have embarked upon ambitious plans to improve and expand their existing airport and airline infrastructure. An expanding tourism sector coupled with the establishment of the necessary infrastructure to

RCSC – Study tour – February 2013 7 AE – United Arab Emirates – Market overview

handle this growth bodes well for the region’s retail industry, due to the close inter-relationships between the industries.

o Growth in the online retail segment is supported by a growing number of internet users in the GCC. Proliferation of e-commerce websites has opened up a new avenue of growth for the retail industry.

o Other key driving factors include strong pipeline of new malls assuring an uninterrupted supply of high-quality store locations for retailers, availability of strong and experienced franchise partners, strong consumer confidence, and proactive measures taken by the governments to pre-empt any form of social unrest

• Key challenges: o Recent events show that certain parts of the GCC are vulnerable to

incidences such as the socio-political unrest and the global financial crisis.

o Fast-paced real estate development has led to increasing congestion of retail infrastructure in the Gulf’s current shopping hotspots. With competition stepping-up among rival firms, retailers have to continuously reinvent themselves.

o High attrition rates amongst the large expatriate workforce and high unemployment rates amongst locals add to retailers’ human resources challenges.

o Retails rentals have started to move up in top-tier malls in the GCC. As the global economic uncertainty gradually recedes, rental expenses are expected to increase further and squeeze margins of retailers. Containing inflation also remains one of the biggest fiscal challenges in the Gulf.

o A parallel market for counterfeit products, high bank fees on e-commerce transactions, severe price competition in the online segment, and high dependence on food imports are other challenges facing the retail sector.

• Market trends o Large supermarkets/hypermarkets in the GCC are gradually making in-

roads into private label retailing as they focus on profit growth. Currently, sales from private labels account for around 10% of overall retail sales, compared to just 3% three years back.

o Group-buying is becoming increasingly popular in the GCC, and is a major force behind the growth of online retail sales in the region.

o Economic slowdown and increasing personal debt have led to average consumers becoming more value-conscious. Buyers in the MENA give equal consideration to product quality and price, and are willing to delay their purchases to bag best deals.

o Conventional franchising is evolving further to develop a new model called sub-franchising. Though still nascent in the Gulf, the sub-franchise model may gain prominence as all concerned parties realize its benefits.

RCSC – Study tour – February 2013 8 AE – United Arab Emirates – Market overview

Global ranking of attractiveness of markets for international retailers Rank 2012 2011

UAE 7 9

Kuwait 12 5

Oman 8 -

Saudi Arabia 14 7

Source: AtKearny

UAE retail sales * bn US$ Retail sales as % UAE GDP Property market

• The UAE has an open economy with a high per capita income and a sizable annual trade surplus. Successful efforts at economic diversification have reduced the portion of GDP based on oil and gas output to 25%.

Shopping center stock existing and planned (*1,000 m2 gla) in GCC countries

Source: Alpen Capital (2012)

RCSC – Study tour – February 2013 9 AE – United Arab Emirates – Market overview

New m2 gla retail space added – Source: JLL

• In terms of players – developers and investors alike – the difference between Dubai and Abu Dhabi is striking. While Dubai counts several strong real estate conglomerates with international operations, players in Abu Dhabi tend to be smaller and some even semi-public.

• Main players in Dubai: o Emaar o Majid al Futtaim o Nakheel

•

RCSC – Study tour – February 2013 10 AE – United Arab Emirates – Market overview

DUBAI Overview

• Dubai is a city-state in the United Arab Emirates, located within the emirate of the same name.

• The emirate of Dubai is located southeast of the Persian Gulf on the Arabian Peninsula and is one of the seven emirates that make up the country.

• It has the largest population in the UAE (2,104,895) and the second-largest land territory by area (4,114 km2) after Abu Dhabi..

• Dubai and Abu Dhabi, the national capital, are the only two emirates to have veto • power over critical matters of national importance in the country's legislature. • The city of Dubai is located on the emirate's northern coastline and heads up the

Dubai-Sharjah-Ajman metropolitan area. History

• The earliest mention of Dubai is in 1095 AD, and the earliest recorded settlement in the region dates from 1799.

• The Sheikhdom of Dubai was formally established in 1833 by Sheikh Maktoum bin Butti Al-Maktoum when he persuaded around 800 members of his tribe of the Beni Yas, living in what is then the Second Saudi State and now part of Saudi Arabia, to follow him to the Dubai Creek by the Abu Falasa clan of the Beni Yas.

• It remained under the tribe's control when the United Kingdom assumed protection of the Sheikhdom in 1892[7] and joined the nascent United Arab Emirates upon independence in 1971 as the country's second emirate.

• Its strategic geographic location made the town an important trading hub and by the beginning of the 20th century, Dubai was already an important regional port.

• Today, Dubai has emerged as a cosmopolitan metropolis that has grown steadily to become a global city and a business and cultural hub of the Middle East and the Persian Gulf region.

• Although Dubai's economy was historically built on the oil industry, the emirate's Western-style model of business drives its economy with the main revenues now coming from tourism, real estate, and financial services.

• Dubai has attracted world attention through many innovative large construction projects and sports events. The city has become symbolic for its skyscrapers and high-rise buildings, such as the world's tallest Burj Khalifa, in addition to ambitious development projects including man-made islands, hotels, and some of the largest shopping malls in the region and the world.

• Dubai's property market experienced a major deterioration in 2008–2009 as a result of the worldwide economic downturn following the financial crisis of 2007-2008. However, Dubai has made a steady and gradual recovery with help coming from neighboring emirates.

• As of 2012, Dubai is the 22nd most expensive city in the world, surpassing London (25th). Dubai has also been rated as one of the best places to live in the Middle East.

• Most formats through franchise: sub-franchisee agreements with master franchises in Russia, Turkey, or UAE.

• In 2011, Inditex bought back franchise from Fawaz Alhokair, which was seen as sign of trust in the market.

RCSC – Study tour – February 2013 11 AE – United Arab Emirates – Market overview

Population Dubai city - Source: Wikipedia – various sources

• Dubai invests heavily on infrastructure, including upgrading of the road system and a public transport system.

• As part of it, an extensive metro system is being built, of which the first two lines have been opened in 2009 and 2011.

• One line runs more or less parallel to the coast and the main road artery, while the second one goes around Dubai city center.

• An express line connecting the Dubai international airport with the new Al makthoum airport under construction, is also under construction.

• A monorail has been built to connect the Palm to the mainland. However, as the connection to the nearest metro transfer station is still missing, the monorail is hearly being used.

RCSC – Study tour – February 2013 12 AE – United Arab Emirates – Market overview

Shopping center market

• Dubai: o Increased competition as market reaches saturation o Polarisation of market into winners and losers o Under performing centres to be repositioned, redevelopment or

conversion to non-retail uses o Limited opportunities for new developments:

� Small convenience centre’s on infill sites within established areas. � F&B / tourist related projects – in very select locations. � Big box / retail warehousing

RCSC – Study tour – February 2013 13 AE – United Arab Emirates – Market overview

Property clock Dubai - Source: JLL

Dubai: evolution shopping center supply (*1,000 m2 gla) Source: JLL

RCSC – Study tour – February 2013 14 AE – United Arab Emirates – Market overview

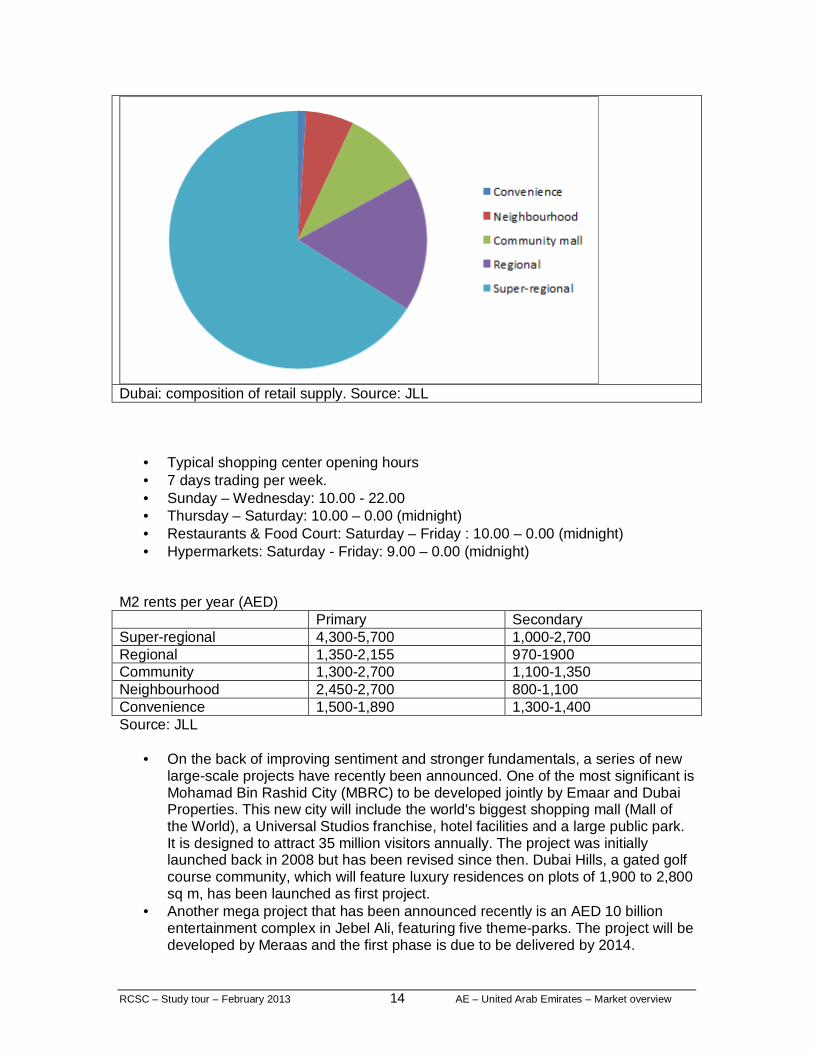

Dubai: composition of retail supply. Source: JLL

• Typical shopping center opening hours • 7 days trading per week. • Sunday – Wednesday: 10.00 - 22.00 • Thursday – Saturday: 10.00 – 0.00 (midnight) • Restaurants & Food Court: Saturday – Friday : 10.00 – 0.00 (midnight) • Hypermarkets: Saturday - Friday: 9.00 – 0.00 (midnight)

M2 rents per year (AED) Primary Secondary Super-regional 4,300-5,700 1,000-2,700 Regional 1,350-2,155 970-1900 Community 1,300-2,700 1,100-1,350 Neighbourhood 2,450-2,700 800-1,100 Convenience 1,500-1,890 1,300-1,400 Source: JLL

• On the back of improving sentiment and stronger fundamentals, a series of new large-scale projects have recently been announced. One of the most significant is Mohamad Bin Rashid City (MBRC) to be developed jointly by Emaar and Dubai Properties. This new city will include the world's biggest shopping mall (Mall of the World), a Universal Studios franchise, hotel facilities and a large public park. It is designed to attract 35 million visitors annually. The project was initially launched back in 2008 but has been revised since then. Dubai Hills, a gated golf course community, which will feature luxury residences on plots of 1,900 to 2,800 sq m, has been launched as first project.

• Another mega project that has been announced recently is an AED 10 billion entertainment complex in Jebel Ali, featuring five theme-parks. The project will be developed by Meraas and the first phase is due to be delivered by 2014.

RCSC – Study tour – February 2013 15 AE – United Arab Emirates – Market overview

• The world’s tallest hotel, JW Marriott Marquis, has opened its first phase, which consists of 804 rooms out of the total of 1,608 to be delivered. The hotel has a height of 355 meters, a total of 82 storeys and includes the largest celebration hall in the Middle East. The second phase of the hotel is currently under construction and is due for completion in 2014.

• The fourth phase of Madinat Jumeirah has been approved and is anticipated to be completed by 2015. The AED2.5 billion project will include a five-star hotel, a villas complex, restaurants, retail stores and a pedestrian precinct.

• Construction work on the USD408 million Business Bay Canal project is expected to start in early 2013. The project, which consists of a 2.8km canal extending Business Bay to the Arabian Gulf, is expected to be completed in two years.

• Al Maktoum International Airport will start business aviation operations in early 2013 while the commercial passenger facility is scheduled to open later in the year. The airport, located at Dubai World Central (DWC), has a capacity for 160 million passengers and 12 million tonnes of cargo. It is anticipated to be the largest airport in the world once completed.

• Dubai International Airport is projected to reach a new record by handling more than 57 million passengers in 2012. The worlds fourth busiest international airport handled over 50 million passengers in 2011. This growth reflects the robust tourism sector and the continued expansion of local airlines.

• According to figures from the Dubai Statistics Center, Jebel Ali Free Zone (JAFZA) is the Middle East’s largest free zone, accounting for around 20% of Dubai’s economy and almost 13% of its labor force. JAFZA houses around 6,700 companies and 170,000 employees.

• On December 31st the UAE Central Bank announced new limits on loan to value

ratios for all mortgages of 50% for expatriates and 70% for Emiratis. This new measure aims to control rising prices and prevent another property bubble in Dubai, similar to that which occured in 2007/8. The new guidelines are likely to reduce demand in the residential sector and slow the recovery of prices in 2013.The top open market net rent for a notional standard shop in prime super regional centres has increased slightly in Q4 2012 as demand remains strong. Rents in secondary and old malls have either remained flat or dropped marginally, widening the differential between primary and secondary centres.

• •The Dubai Mall and Mall of the Emirates continue to outperform the industry in terms of record footfalls, sales volumes and occupancy. Emaar has announced a 93,000 sq m expansion plan for the Dubai Mall.

• •Despite the large number of retail centres in Dubai, several new projects are likely to perform well. “The Beach” project by Meraas on JBR, is expected to benefit from the strong population density in Dubai Marina, the inflow of tourists as well as the upcoming tram project in the area.

• Demand remains strong from international franchises and a number of flagship stores, ranging from luxury to medium and value brands, are entering the market. The Food & Beverage sector is reported to be doing particularly well and a number of new to the market F&B brands, such as The Cheesecake Factory, have opened very successfully.

• As the resident population is growing, retail sales in community malls are increasing year-on-year. However, these sales increases have not yet translated into high rental levels.

RCSC – Study tour – February 2013 16 AE – United Arab Emirates – Market overview

• Overall, the retail market in Dubai continues to perform well, especially in the large best quality centres, supported by a strong tourism industry and the perception of Dubai as a “safe haven”. Secondary malls are seeing weakened demand and have been reviewing their tenant mix and offering leasing incentives to improve their positioning.

• Dubai remains the most transparent real estate market in the MENA region • The UAE has reinforced its position as the most transparent real estate market in

the region with progress being recorded in both Dubai and Abu Dhabi. This reflects the UAE's status as one of the most stable and secure real estate markets in a still volatile region heavily affected by the social unrest and political turmoil resulting from the Arab Spring of 2011.

• Dubai is MENA's most developed real estate market and remains the regional benchmark for transparency. While there have been no major new initiatives, modest gains in the areas of transactions process and property management have resulted in Dubai registering an improvement since 2010. Dubai's Real Estate Regulatory Authority (RERA) is widely recognised as the region's leading real estate regulator and several other countries have sought to emulate RERA through similar initiatives. RERA's initiatives have resulted in Dubai achieving the strongest legal and regulatory framework in MENA.

• Dubai also scores well on the Listed Vehicles Sub-Index where it is ranked 23rd globally, the highest position of any MENA market on any of the five transparency sub-indices. A number of listed property trusts or REITs have been launched or proposed over the past two years and the region's preferred exchange is the Dubai International Financial Centre (DIFC), which provides investors with a new means of exposure to the real estate investment market.

• The Dubai market continues to lag on the Market Fundamentals (53rd globally) and Performance Measurement (41th globally). Outside of the residential sector there are no investment performance indices available to potential investors and the quality of market data remains poor. Improvements in these areas are required if Dubai is to be promoted from the 'Semi-Transparent' category.

• Abu Dhabi records modest improvement • While Abu Dhabi is one to two years behind Dubai in its property development

cycle, it has seen a similar improvement in transparency to Dubai since 2010. The quality of market data is better in Abu Dhabi than Dubai in some sectors and the planning system is more regulated (through the Urban Planning Council); advances in these areas have reinforced Abu Dhabi's position as the second most transparent market in the MENA region. m

RCSC – Study tour – February 2013 17 AE – United Arab Emirates – Market overview

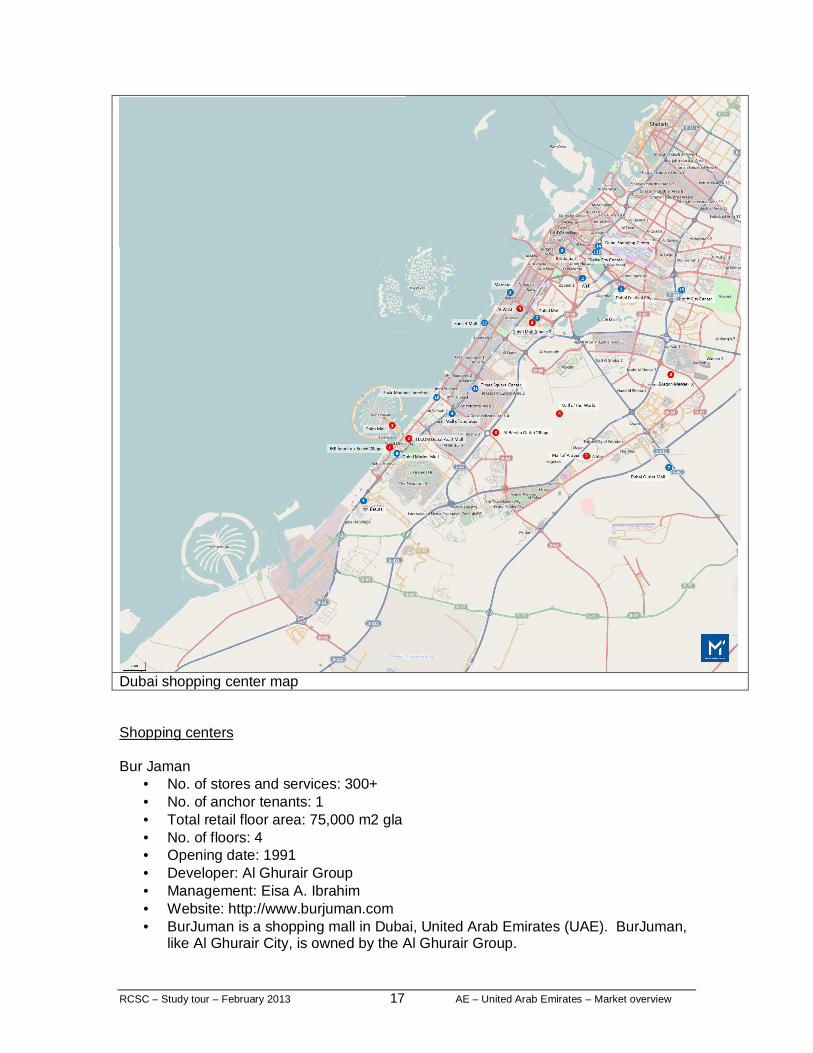

Dubai shopping center map Shopping centers Bur Jaman

• No. of stores and services: 300+ • No. of anchor tenants: 1 • Total retail floor area: 75,000 m2 gla • No. of floors: 4 • Opening date: 1991 • Developer: Al Ghurair Group • Management: Eisa A. Ibrahim • Website: http://www.burjuman.com • BurJuman is a shopping mall in Dubai, United Arab Emirates (UAE). BurJuman,

like Al Ghurair City, is owned by the Al Ghurair Group.

RCSC – Study tour – February 2013 18 AE – United Arab Emirates – Market overview

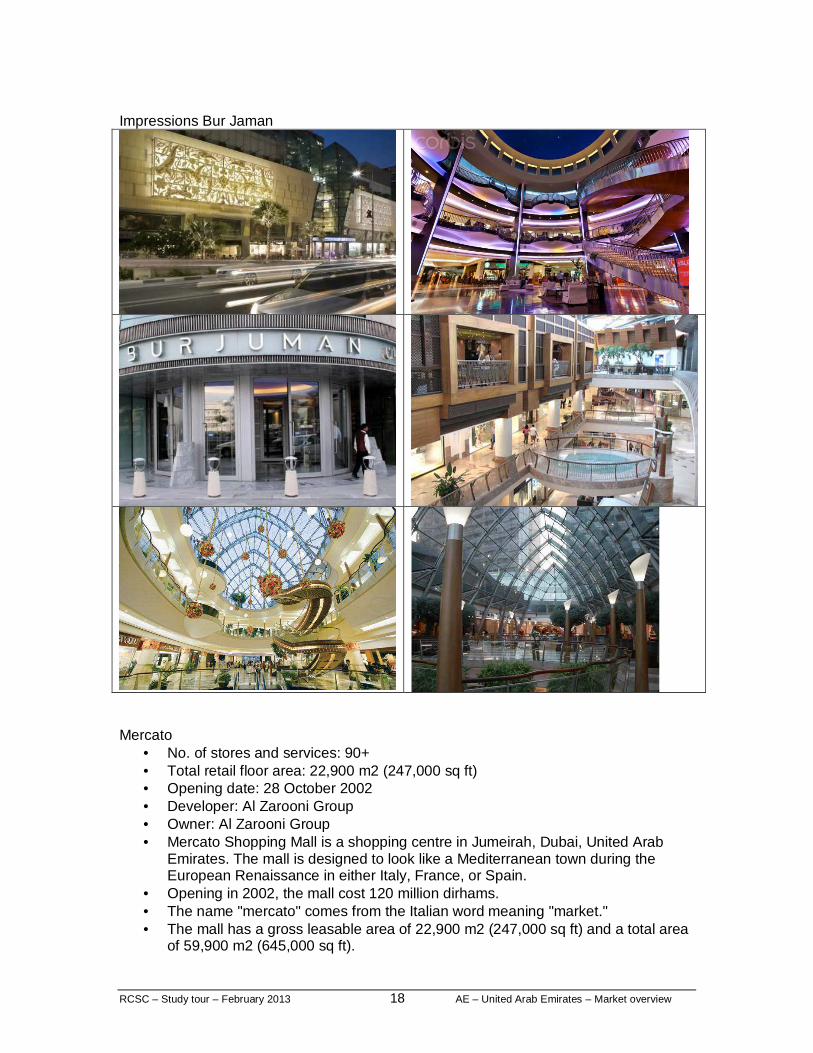

Impressions Bur Jaman

Mercato

• No. of stores and services: 90+ • Total retail floor area: 22,900 m2 (247,000 sq ft) • Opening date: 28 October 2002 • Developer: Al Zarooni Group • Owner: Al Zarooni Group • Mercato Shopping Mall is a shopping centre in Jumeirah, Dubai, United Arab

Emirates. The mall is designed to look like a Mediterranean town during the European Renaissance in either Italy, France, or Spain.

• Opening in 2002, the mall cost 120 million dirhams. • The name "mercato" comes from the Italian word meaning "market." • The mall has a gross leasable area of 22,900 m2 (247,000 sq ft) and a total area

of 59,900 m2 (645,000 sq ft).

RCSC – Study tour – February 2013 19 AE – United Arab Emirates – Market overview

Impressions Mercato

Wafi City

• No. of stores and services: 275 • 50 gastronomy units, including restaurants, bistro’s, café’s • Total retail floor area: 80,000 m2 (861,000 sq ft) • Opening date: 2001 • The walls have Ancient Egyptian designs on them • Wafi City is a mixed-use development in Dubai, United Arab Emirates. The

complex includes a mall, hotel, restaurants, residences, and a nightclub. • The project is themed and styled after Ancient Egypt. This themed environment

includes columns reminiscent of Karnak, small pyramids, and images of

RCSC – Study tour – February 2013 20 AE – United Arab Emirates – Market overview

pharaohs. All the walls are the color of the light brown stone that can be found on all structures in Ancient Egypt.

• The main feature of Wafi City is the mall, called Wafi Mall. • In November 2007, Raffles opened its first property in the Middle East. Raffles

Dubai is a 5-star hotel in a pyramidal shape that contains 248 rooms on 18 floors.

Ibn Batuta Mall

• No. of stores and services: • Total retail floor area: m2 ( sq ft) • Opening date:

RCSC – Study tour – February 2013 21 AE – United Arab Emirates – Market overview

• Owner-developer: Nakheel • One level center: 1.3 km length. • Themed after discovery travels of Ibn Batuta: 6 themed courts: China, India,

Persia, Egypt, Tunisia and Andalusia.

RCSC – Study tour – February 2013 22 AE – United Arab Emirates – Market overview

Mall of Emirates

• No. of stores and services: • Total retail floor area:220,000 m2 ( 2,400,000 sq ft) • Opening date: September 2005 • Ownership: Majd al Futtaim • Design: F+A Architects (USA) • 2010: 31 million visitors • 2nd largest mall in Dubai.

Ground floor plan Mall of Emirates

RCSC – Study tour – February 2013 23 AE – United Arab Emirates – Market overview

Dubai Mall

• 1,200 of stores and services: • Total retail floor area: 340,000 m2 (3,700,000 sq ft) • Opening date: November 2008 • Developed and owned by Emaar. • Largest mall in Dubai. • Part of the 20-billion-dollar Burj Khalifa complex. • 2011 visitors: 54 million (said to be busiest mall in the world).

RCSC – Study tour – February 2013 24 AE – United Arab Emirates – Market overview

Ground floor plan Dubai Mall

RCSC – Study tour – February 2013 25 AE – United Arab Emirates – Market overview

RCSC – Study tour – February 2013 26 AE – United Arab Emirates – Market overview

Dubai Festival City

• 370 stores and services, including 25 anchor stores. • 90 restaurants, cafes, bistro’s • Leisure: entertainment center, bowling, 12 screen multiplex • Total retail floor area: 180,000 m2 ( 2,000,000 sq ft) • Parking areas: 7,000 parking lots • Opening date: 2005 • Developed and owned by: Majid al Futtaim • Rising along the banks of the historic Dubai Creek, Festival City Mall is Dubai’s

unrivalled waterfront destination for style and sophistication, showcasing an exciting selection of prestigious retailers, international food and beverage outlets and a world-class entertainment retreat.

• Dubai festival Mall is located at the heart of Dubai Festival City.

RCSC – Study tour – February 2013 27 AE – United Arab Emirates – Market overview

Deira City Center • No. of stores and services: • Total retail floor area: 110,000 m2 ( 1,290,000 sq ft) • Opening date: 1995 • Owned by: Majid Al Futtaim • •

Times Square

• No. of stores and services:

RCSC – Study tour – February 2013 28 AE – United Arab Emirates – Market overview

• Total retail floor area: m2 ( sq ft) • Opening date: • Owned by: Al Maskan Real Estate • •

RCSC – Study tour – February 2013 29 AE – United Arab Emirates – Market overview

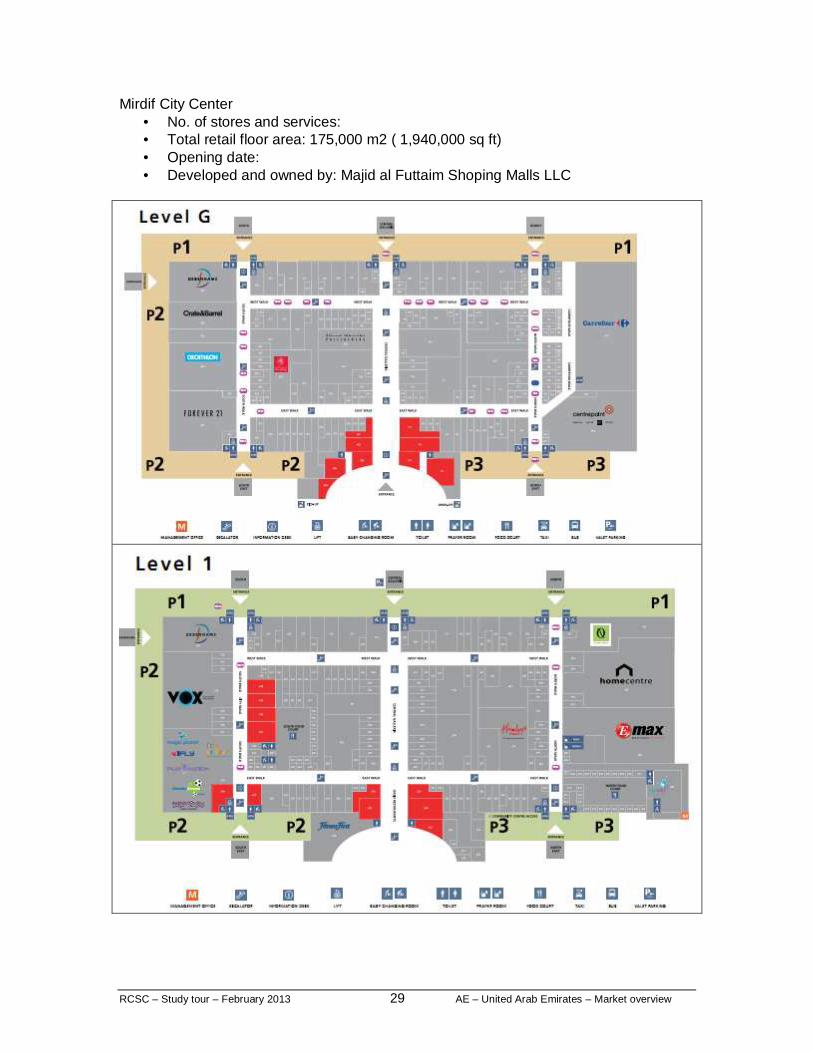

Mirdif City Center • No. of stores and services: • Total retail floor area: 175,000 m2 ( 1,940,000 sq ft) • Opening date: • Developed and owned by: Majid al Futtaim Shoping Malls LLC

RCSC – Study tour – February 2013 30 AE – United Arab Emirates – Market overview

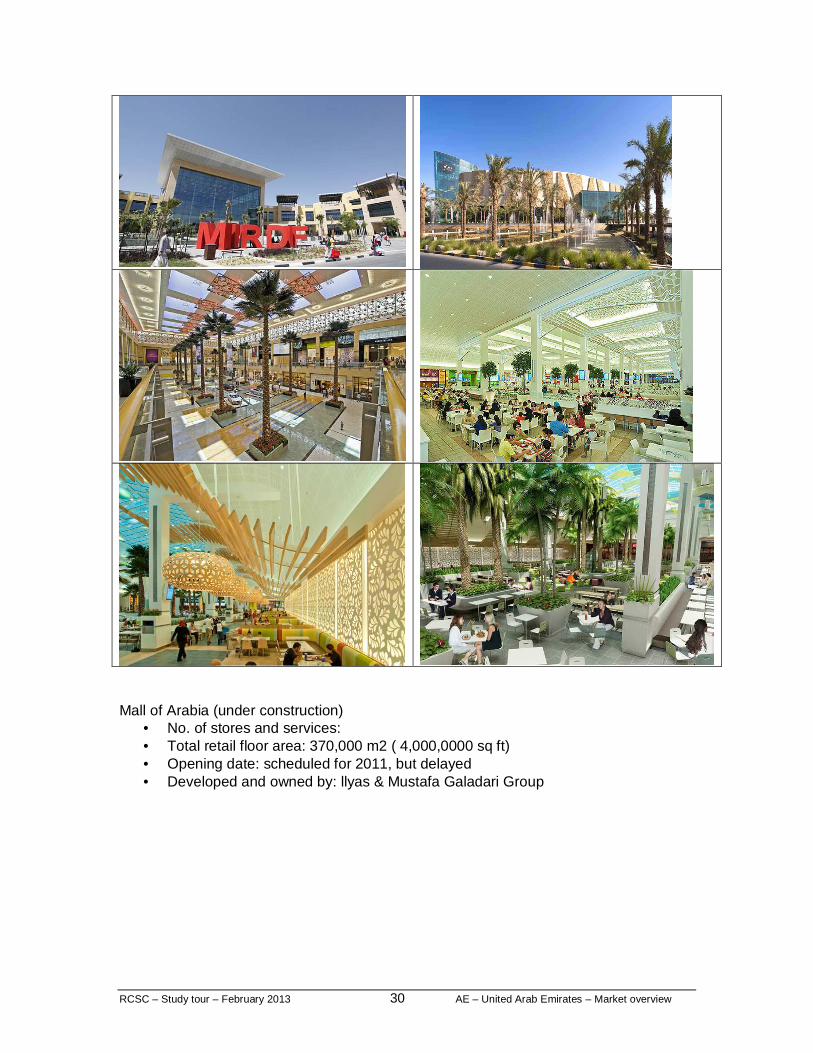

Mall of Arabia (under construction)

• No. of stores and services: • Total retail floor area: 370,000 m2 ( 4,000,0000 sq ft) • Opening date: scheduled for 2011, but delayed • Developed and owned by: llyas & Mustafa Galadari Group

RCSC – Study tour – February 2013 31 AE – United Arab Emirates – Market overview

RCSC – Study tour – February 2013 32 AE – United Arab Emirates – Market overview

ABU DHABI Overview

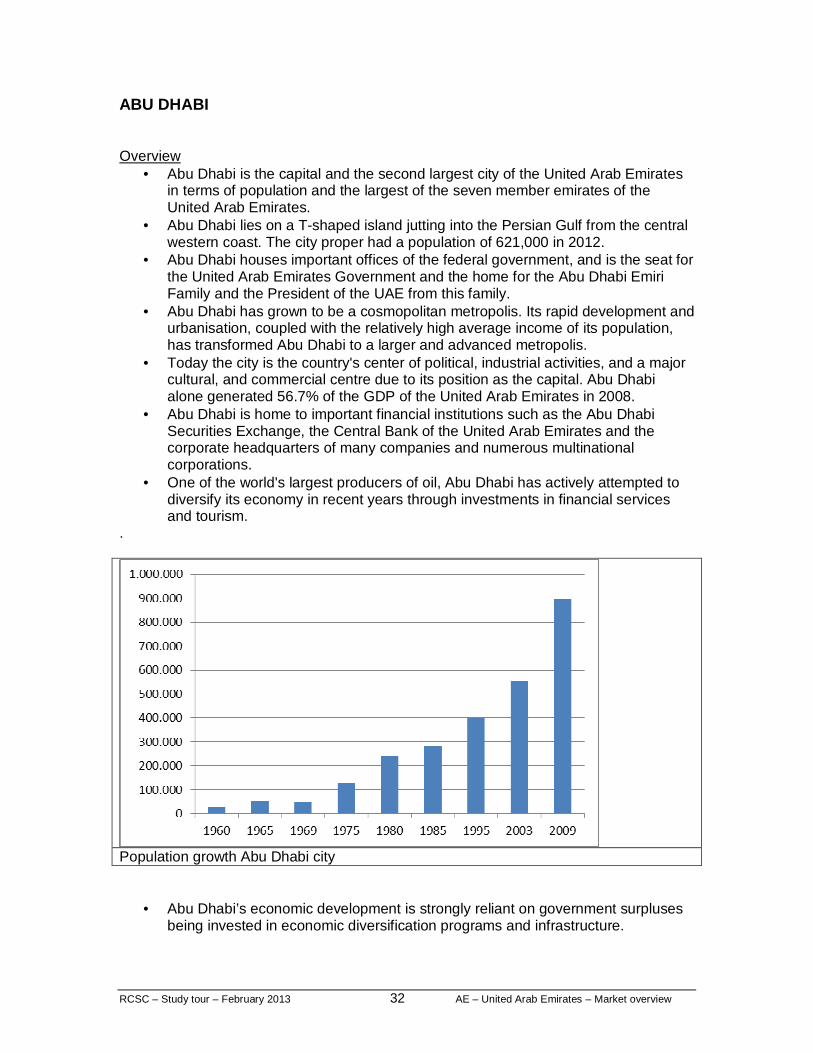

• Abu Dhabi is the capital and the second largest city of the United Arab Emirates in terms of population and the largest of the seven member emirates of the United Arab Emirates.

• Abu Dhabi lies on a T-shaped island jutting into the Persian Gulf from the central western coast. The city proper had a population of 621,000 in 2012.

• Abu Dhabi houses important offices of the federal government, and is the seat for the United Arab Emirates Government and the home for the Abu Dhabi Emiri Family and the President of the UAE from this family.

• Abu Dhabi has grown to be a cosmopolitan metropolis. Its rapid development and urbanisation, coupled with the relatively high average income of its population, has transformed Abu Dhabi to a larger and advanced metropolis.

• Today the city is the country's center of political, industrial activities, and a major cultural, and commercial centre due to its position as the capital. Abu Dhabi alone generated 56.7% of the GDP of the United Arab Emirates in 2008.

• Abu Dhabi is home to important financial institutions such as the Abu Dhabi Securities Exchange, the Central Bank of the United Arab Emirates and the corporate headquarters of many companies and numerous multinational corporations.

• One of the world's largest producers of oil, Abu Dhabi has actively attempted to diversify its economy in recent years through investments in financial services and tourism.

.

Population growth Abu Dhabi city

• Abu Dhabi’s economic development is strongly reliant on government surpluses being invested in economic diversification programs and infrastructure.

RCSC – Study tour – February 2013 33 AE – United Arab Emirates – Market overview

• With the market down in 2011, Abu Dhabi reduced its investments downward significantly, delaying many infrastructure and tourism projects, as the spending patterns were being reviewed.

• In 2012, the Abu Dhabi Executive Council decided on priorities. Those public investments which offer higher returns are regarded as priority. Priority areas are the following:

o Economic diversification o Infrastructure upgrade o Tourism related projects o Social infrastructure projects.

• Economic diversification and major infrastructure projects: o Upgrade road system o KIZAD, port, and related industrial areas o Etihad railway

• Tourism projects o Development of three main museums (Zajed National, Louvre,

Guggenheim) o Yas Island as main tourism destination (Yas Marina World, Ferrari World,

Yas Water Park) o Accommodate major sports and cultural events, festival. o Coordination between Tourism Board and Etihad to reinforce hub function

Abu Dhabi. • Social infrastructure:

o National housing program. Emirati housing communities. o Construction of additional hospitals and schools.

• Some of these projects are already underway, others still to be commenced.

. Shopping center market

• Abu Dhabi: o Shortage of quality stock now being addressed o Greater competition will require malls to become more focussed o Increased attention to management and promotions o Continued move to mall based retailing

Shopping center stock: 1.73 mn m2 gla in 2012 Q4 (JLL) • About 54,000 m2 gla added to the market mainly because of extension Al

Wahda. • Rents in prime shopping centers on Abu Dhabi Island unchanged in 2012. • 2013-2014 pipeline is dominated by development of regional malls, though

several mixed use projects will move ahead, including The Collection on Saadiyat Island and Galleria on Sowrah Square.

• Main regional malls to be delivered in coming years o Deerfields Town Square in Bahia o Emporium Mall at Central Market o Capital Mall in Building Materials City

• Because of new food and hygienic regulations, many small scale traditional food stores were forced to close.

•

RCSC – Study tour – February 2013 34 AE – United Arab Emirates – Market overview

Abu Dhabi – property clock. Source: JLL

Abu Dhabi: evolution shopping center supply (*1,000 m2 gla) Source: JLL

RCSC – Study tour – February 2013 35 AE – United Arab Emirates – Market overview

Abu Dhabi: composition of retail supply. Source: JLL Area type AED/m2/year (2012-Q4) Anchor (AED/m2) 500-1,500 Inline shop 1,500-3,000 Gastronomy 2,000-3,000 (casual dining)

2,500-4,500 (food court) Kiosks 60,000-180,000 Source: JLL

• Abu Dhabi records modest improvement • While Abu Dhabi is one to two years behind Dubai in its property development

cycle, it has seen a similar improvement in transparency to Dubai since 2010. The quality of market data is better in Abu Dhabi than Dubai in some sectors and the planning system is more regulated (through the Urban Planning Council); advances in these areas have reinforced Abu Dhabi's position as the second most transparent market in the MENA region. m

RCSC – Study tour – February 2013 36 AE – United Arab Emirates – Market overview

Abu Dhabi shopping center map Abu Dhabi shopping centers Dalma Mall

• No. of stores and services: • Total retail floor area: 220,000 m2 ( sq ft) • Opening date: 2001 • Owned by: H.H. Sheikh Suroor Bin Mohammed Al Nahyan

RCSC – Study tour – February 2013 37 AE – United Arab Emirates – Market overview

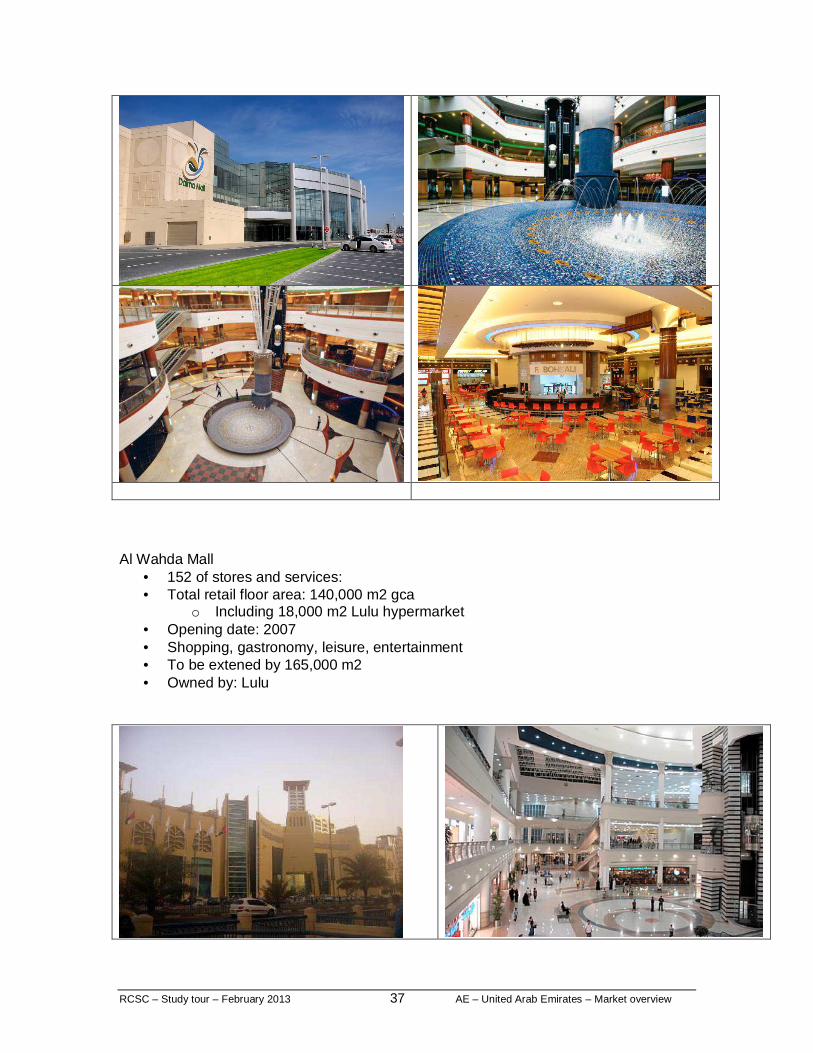

Al Wahda Mall

• 152 of stores and services: • Total retail floor area: 140,000 m2 gca

o Including 18,000 m2 Lulu hypermarket • Opening date: 2007 • Shopping, gastronomy, leisure, entertainment • To be extened by 165,000 m2 • Owned by: Lulu

RCSC – Study tour – February 2013 38 AE – United Arab Emirates – Market overview

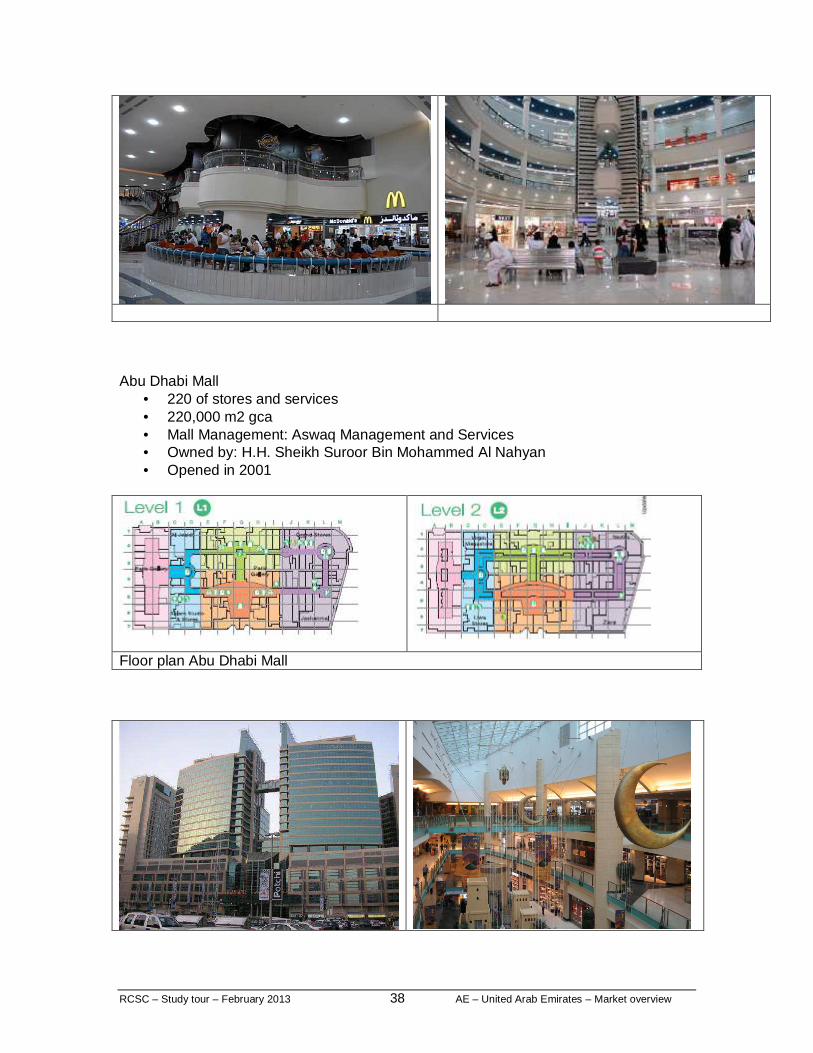

Abu Dhabi Mall

• 220 of stores and services • 220,000 m2 gca • Mall Management: Aswaq Management and Services • Owned by: H.H. Sheikh Suroor Bin Mohammed Al Nahyan • Opened in 2001

Floor plan Abu Dhabi Mall

RCSC – Study tour – February 2013 39 AE – United Arab Emirates – Market overview

Marina Mall

• Marina Mall is owned by National Investment Corporation • Total size of Marina Mall is 235,000 sq meters • Total gross leasable area (GLA) is 122,000 sq meters • 4,000 car parking space • 5 levels ( lower basement, basement, ground floor, first floor, second floor) • Anchor stores include; Carrefour, Marks & Spencer, Paris Gallery, VOX

Cinemas, Plugins, 2XL,Emirates Bowling Village and a Mercedes-Benz Showroom

• 400 stores • 48 restaurants, cafes, and other food and beverage shops

RCSC – Study tour – February 2013 40 AE – United Arab Emirates – Market overview

Khalidiya Mall

• 160 stores and services, including Lulu hypermarket. • Total retail floor area: 80,000 m2 • Opening date: 2007 • Three retail levels • Parking: 2,500 cars • Management: EMKE

RCSC – Study tour – February 2013 41 AE – United Arab Emirates – Market overview

Madinat Zayed Shopping Center • 70 stores and services: • Total retail floor area: 38,000 m2 ( 430,000 sq ft) • Opening date: 1999 • Developed and owned by: Abu Dhabi Municipality • With more than 70 jewelry stores that offer traditional and contemporary gold,

diamond and pearl jewelry from across the globe, the Madinat Zayed Shopping Centre is a true jewel in the cityscape.