united tractors (untr id) relies on spare part sales and ... · pdf fileunited tractors (untr...

TRANSCRIPT

Page | 1 | PHILLIP SECURITIES INDONESIA

United Tractors (UNTR ID)

Relies on spare part sales and services

INDONESIA | HEAVY EQUIPMENT | INITIATION

13 July 2015

Coal remains depressed

Due to unfavorable condition coal miners cut their production, and even

stop producing altogether since with current coal price the margin is so thin. The national coal production target of 425 million tons will likely not

be achieved after several coal miners slashed their production.

Mining sector is still unfavorable for heavy equipment

Undeniably, heavy equipment business will be also affected by sluggish

coal industry. Until 5M15 sales to other sectors were also weak, with slow progress in the construction and agriculture industries. The plantation

business had expanded minimally so far this year. Production of heavy equipment is targeted at around 5,000-6,000 units this year

Revenue is expected to decline

We expect UNTR total revenue to decline 8.82% this year amid

unfavorable condition in mining sector which is a major contributor to the company’s revenue. On the other hand, we see potential 6.7% increase in

revenue from heavy equipment services as machinery maintenances are still in demand although periodically.

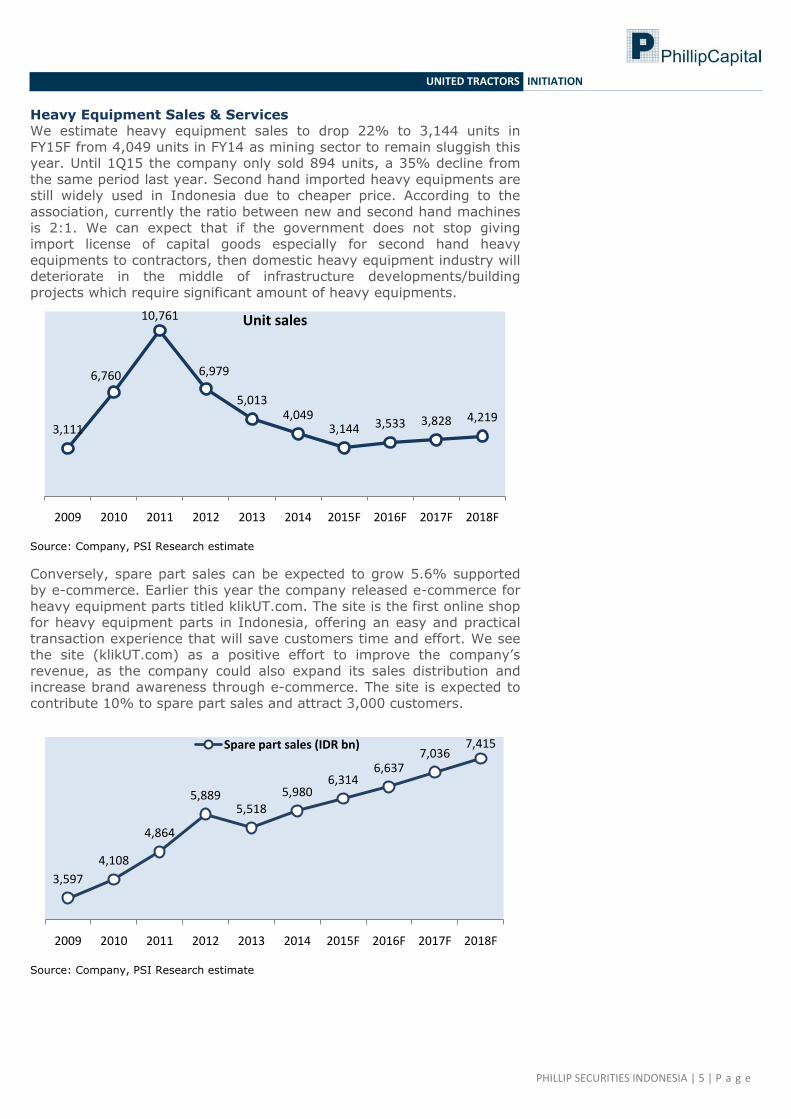

Heavy Equipment Sales & Services We estimate heavy equipment sales to drop 22% to 3,144 units in FY15F

from 4,049 units in FY14. Conversely, spare part sales can be expected to grow 5.6% supported by e-commerce (klikut.com). The site is expected to

contribute 10% to spare part sales. Heavy equipment services to increase 6.7% in FY15F backed by workshop service and non destructive test.

Coal production reduced to 3 million tons The company deliberately reduced coal production to control its

production cost as coal price will likely not going to improve in the near future. The coal production will concentrate on Asmin Bara Bronang which

has the largest production capacity of 7 million tons/year and has a variety of coal qualities from medium to high grade. The company also

buys coal from third parties in order to maintain sales.

Mining services to follow the decline

In FY15F we estimate revenue from mining services as major contributor to total revenue to decline 14.05% as weak coal prices will encourage

several coalminers to cut their production to minimum with the intention of maintaining their coal reserves and efficiency. A number of small coal

miners have stop their operations since the current coal price cannot offset their production costs. UNTR will likely to maintain strip ratio of

6.7x.

Construction services to contribute 5% to total revenue

We expect ACST revenue to increase 18.60% this year supported by several construction projects. With Astra group behind them it is easier for

ACST to expand its business as Astra has strong brand positions in Indonesia. ACST also can take benefit from Astra’s construction projects.

Astra group carries out construction works of around IDR 15 trillion per year and ACST will likely to secure at least 25% from these projects.

Accumulate CLOSING PRICE IDR 18,800

TARGET PRICE IDR 22,000

UPSIDE 17.04% COMPANY DATA

O/S SHARES (MN) : 3,730.14

MARKET CAP (IDR BN) : 70,872.56

MARKET CAP (USDBN) : 5.45

52 - WK HI/LO (IDR) : 25,350 / 16,425

AVG. VOLUME 3M (Share) : 29,516

PAR VALUE (IDR) : 250

TOP 5 SHARE HOLDER, %

ASTRA INTERNATIONAL Tbk : 59.50

LAZARD LTD:

MATTHEWS INTERNATIONAL CAPITAL:

FRANKLIN RESOURCES:

2.72

1.54

1.35

PUBLIC (<5%): 34.89

PRICE vs. JCI

Source: Phillip Securities Indonesia Research

KEY FINANCIALS

FY Dec FY14 FY15F FY16F

Revenue (IDR bn) 53,142 48,456 51,167

NI (IDR bn) 5,370 6,434 6,794

EPS, adj. (IDR) 1,440 1,725 1,821

P/E (X) 13.06 10.90 10.32

BV (IDR bn) 38,577 40,398 43,150

P/BV (X) 1.82 1.74 1.63

DPS (IDR) 535 551 691

EV/EBITDA 8.31 6.88 6.63

Debt/Equity 5.47% 5.83% 6.09%

ROE 8.91% 10.19% 10.10%

ROA 13.92% 15.93% 15.75%

Source: Phillip Securities Indonesia Research Est.

Valuation Method: Discounted Cash Flow

Destya Faishal (+6221 57900800) [email protected]

60

70

80

90

100

110

120

Jun-14 Sep-14 Dec-14 Mar-15 Jun-15UNTR IJ JCI Rebased

PHILLIP SECURITIES INDONESIA | 2 | P a g e

UNITED TRACTORS INITIATION

Business diversification to offset depressed mining sector We think the decision to acquire ACST is correct. Through establishing

construction services segment, the company could partake in Indonesia’s plan to add more infrastructure and facilities construction

projects in order to cut high logistic cost and improve its economy. Acquisition on ACST also becomes another realization of the company’s

plan to diversify its business to reduce its dependency on coal industry.

Other than construction sector, UNTR also diversifies its business to gold mining by acquiring Sumbawa Juturaya through Pamapersada. However,

the gold mine is still in exploration stage to determine gold reserve and we assume it will take 3-5 years to start production.

Investment Action

We initiate UNTR IJ with “Accumulate” recommendation and 52-weeks price target of IDR 22,000 per share with potential upside of 17.04%

based on DCF valuation with long term growth of 3%. Our price target implies P/E of 10.32x compared to current P/E of 10.9x. PBV of 1.63x

VS 1.73 x currently. FY15F EPS of IDR 1,725 and FY16F EPS of 1,821 backed by increase of spare part sales and heavy equipment services

with assumption that the company’s customers especially miners will

only maintain existing machines instead of buying new units as they reduce the amount of work that requires the use and purchase of heavy

equipments due to lowered production targets and even postponed expansion plans.

Major Assumption

FY14 FY15F FY16F FY17F

Heavy equipment sales (unit) 4,049 3,144 3,533 3,828 Coal mining (mn tons) 5.9 3.7 4.1 4.6 Coal delivery (mn tons) 119.4 104.5 112.3 120.6 Overburden removal (mn bcm) 806.4 706.3 726.2 747.8

Source: Company, PSI Research estimate

PHILLIP SECURITIES INDONESIA | 3 | P a g e

UNITED TRACTORS INITIATION

Coal remains depressed

As we know the overall mining sector especially coal mining is still under pressure due to oversupply, as demand from China- the biggest coal

importer continues to decline due to economic slowdown and air pollution issue. On the other hand, domestic demand from Indonesia

does not improve to absorb coal stockpile as majority of industries and power plants still use liquid fuel as primary source of energy. Due to

these unfavorable conditions, coal miners cut their production to reduce losses. Undoubtedly, heavy equipment business will continue to be

affected.

The government’s plan to develop 35,000 megawatt (MW) power plants

will increase domestic coal consumption to around 200 million tons per year, which currently stands at around 90 million tons per year.

However, the government’s plan also raised questions among environmental activists, who fear that the government might prioritize

building cheap, environmentally unsustainable power plants to support economic growth and meet the country’s growing electricity needs. It is

no secret that, among all energy sources available in the world, coal

remains the dirtiest. The government had no cheaper economic alternative than to build coal fired power plants as coal is an abundant

energy source available in Indonesia and it is still relatively cheap. Miners will have to abide by existing regulations and pay close attention

to environmental health. There also will be production controls, not in terms of figures but in terms of quality. Such production restrictions

would result in better environmental health and maintain the national coal supply therefore coal price could improve. Moreover, India’s coal

consumption will likely to pick up following growth in steel consumption.

Although India's steel sector is not yet a dominant force, it is clearly starting to show strength in supporting demand in oversupplied global

market. India’s coal import from Indonesia was the highest of 188.4 million tons in 2014.

But we consider that achievement is the peak and will start to decline as

India plans to stop their coal import in 2017 and will be more dependent on domestic output. Due to this event we estimate coal export to India

to reach around 120 million tons in 2015 or 36% lower from export in

2014 as India will begin to reduce their imports. For the long term we expect coal price to remain low at around below USD 60/metric tons.

The national coal production target of 425 million tons will likely not be

achieved as 1Q15 coal production dropped 21% to 97 million tons from the same period last year of 124 million tons after several coal miners

slashed their productions even stop producing due to narrow margin.

Mining sector is still unfavorable for heavy equipment

Heavy Equipment Manufacturer Association of Indonesia estimates that

mini to middle size heavy equipments (10-30 tons) will dominate the production in the year ahead to support infrastructure development

which has been planned by the government. Besides construction and

infrastructure, there is still hope to improve heavy equipment sales from other sector/industries, such as agriculture and forestry. However, until

5M15 sales to other sectors have also been weak, amid slow progress in the construction and agriculture industries. The plantation business had

expanded minimally so far this year due to CPO oversupply. The association estimates heavy equipment sales in 2015 will stagnate and

sets production target of 5,000-6,000 units this year.

PHILLIP SECURITIES INDONESIA | 4 | P a g e

UNITED TRACTORS INITIATION

Heavy equipment industry in Indonesia has installed capacity of 10,000 units per year. However, utilization rate is estimated at only 50% due to

increasing imported heavy equipments and slow realization of infrastructure projects, which will only likely to speed up in 2016.

Revenue is expected to decline

United Tractors is the leading and the largest distributor of heavy

equipments, providing product brands such as Komatsu, UD truck, Scania, Bomag, and Tadano. The company also provides heavy

equipment rentals such as forklift and excavator. United Tractor as market leader with market share of 37% (May 2015) sets heavy

equipment sales target of 3,000 units in 2015. This target was revised from previous target of 4,000 units. Heavy equipment sales are the

second major contributor to total revenue (25%) after mining services (63%).

We expect revenue from all segments except construction and heavy equipment services to decline this year amid unfavorable condition in

mining sector which is a major contributor to the company’s revenue. On the other hand, we expect heavy equipment services to increase as

machinery maintenances are still in demand although periodically. Revenue estimates

Total Revenue -8.82%

Sales: Heavy

equipment -0.28%

Slightly declining. 6% increase in spare

parts sales will buffer overall sales.

Sales: coal mining -35.81% Coal production target has been slashed to

3 million tons in 2015.

Services: Heavy

equipment +6.70% Supported by workshop service

Services: mining

contracting -14.05%

Several coalminers cut their production

targets amid unfavorable condition

Services: construction

contracting +18.60%

We expect to contribute 5% to total revenue

backed by the government’s commitment to

improve infrastructure.

However, revenue for FY16F can be expected to improve as the

government’s infrastructure project will likely to commence in 2016 and certainly the government will need significant amount of heavy

equipments.

Source: Company, PSI Research estimate

Machinery sales, 25%

coal mining, 9%

Machinery services, 4%

Mining services, 63%

Revenue FY14

Machinery sales, 26%

coal mining, 6%

Machinery services, 4%

Mining services, 61%

Construction services, 5% Revenue FY15F

PHILLIP SECURITIES INDONESIA | 5 | P a g e

UNITED TRACTORS INITIATION

Heavy Equipment Sales & Services We estimate heavy equipment sales to drop 22% to 3,144 units in

FY15F from 4,049 units in FY14 as mining sector to remain sluggish this year. Until 1Q15 the company only sold 894 units, a 35% decline from

the same period last year. Second hand imported heavy equipments are still widely used in Indonesia due to cheaper price. According to the

association, currently the ratio between new and second hand machines

is 2:1. We can expect that if the government does not stop giving import license of capital goods especially for second hand heavy

equipments to contractors, then domestic heavy equipment industry will deteriorate in the middle of infrastructure developments/building

projects which require significant amount of heavy equipments.

Source: Company, PSI Research estimate

Conversely, spare part sales can be expected to grow 5.6% supported

by e-commerce. Earlier this year the company released e-commerce for

heavy equipment parts titled klikUT.com. The site is the first online shop for heavy equipment parts in Indonesia, offering an easy and practical

transaction experience that will save customers time and effort. We see the site (klikUT.com) as a positive effort to improve the company’s

revenue, as the company could also expand its sales distribution and increase brand awareness through e-commerce. The site is expected to

contribute 10% to spare part sales and attract 3,000 customers.

Source: Company, PSI Research estimate

3,111

6,760

10,761

6,979

5,013 4,049

3,144 3,533 3,828 4,219

2009 2010 2011 2012 2013 2014 2015F 2016F 2017F 2018F

Unit sales

3,597

4,108

4,864

5,889 5,518

5,980 6,314

6,637 7,036

7,415

2009 2010 2011 2012 2013 2014 2015F 2016F 2017F 2018F

Spare part sales (IDR bn)

PHILLIP SECURITIES INDONESIA | 6 | P a g e

UNITED TRACTORS INITIATION

Source: Company, PSI Research estimate

Heavy equipment services to increase 6.7% in FY15F backed by

workshop service and non destructive test, with the objective of this program is to restore heavy equipment to its peak condition and also to

reduce owner's undercarriage maintenance costs. Undercarriage is one of the most important parts of the heavy equipment that consumes up

to 40% of the total maintenance cost. We assume that the company’s

customers especially miners will only conduct full maintenance to heavy equipments their already owned instead of buying new ones as they

reduce the amount of work that need the use and purchase of heavy equipment since they slashed their target production and even

postponed their expansion plan. Some components such as undercarriage can be rebuilt and it can reduce cost of up to 60%

compared to the cost to buy new components.

In the midst of depressed mining sector, we consider heavy equipment

companies will make efforts to improve their sales by increasing the production of mini heavy equipments with operating weight of less than

6 tons such as mini excavator, wheel loader, backhoe, and dump truck which is generally used for construction, plantation, highways, and

drainage maintenance tool.

Komatsu Heavy Equipment Sales Contribution per Sector

Source: Company, PSI Research estimate

United Tractors has a strategy to strengthen its brand by deepening the relationship with its customers. This strategy is also a value added in

heavy equipment services compared to its competitors that could gain

0 0

1,271 1,525 1,623

1,883 2,009

2,168 2,309

2,478

2009 2010 2011 2012 2013 2014 2015F 2016F 2017F 2018F

Heavy equipment services (IDR bn)

24% 20% 17% 24% 30% 24% 24%

16%11% 10%

16%

25%28% 32%

9%6%

6%

8% 14%15%

60% 61% 67%54%

37% 35% 29%

2009 2010 2011 2012 2013 2014 2015F

Agriculture Construction Forestry Mining

PHILLIP SECURITIES INDONESIA | 7 | P a g e

UNITED TRACTORS INITIATION

customers confidence through trainings the company provided to its clients about maintenance and operation of heavy equipments that they

bought. With these trainings the clients can perform light maintenance on their own without depending on United Tractors. In addition, the

company also routinely held customer gatherings in order to get customers feedbacks for improvement. The company also has parts

financing program cooperating with banking institutions, where the

company provides loan facility for its customers to purchase parts and service. Through this program, business partners have benefits such as

credit limit of up to IDR 3 billion, no collateral, and free of administration costs. With end to end service and a wide range of products, the

company could maintain its market shares above 35%.

From product view there is no question about Caterpillar (CAT) for its superiority and reputation. However, Komatsu offers almost similar

value with less cost and more eco-friendly compared to CAT. According

to heavy equipment operators they prefer Komatsu because it is more comfortable to use since Komatsu has better suspension system thus

reduce vibration compare to CAT. In term of power, CAT has the upper hand but Komatsu is not too far behind. Stronger USD also gave

advantage to Komatsu sales. Even though both companies have factories in Indonesia, import costs for components are relatively

cheaper in JPY rather than USD, allowing lower production cost to generate more competitive selling price.

Coal production reduced to 3 million tons For coal mining segment, further decline in coal prices due to

unfavorable coal market conditions force the company to mine at minimum production level in order to maintain its financial performance.

The company sets target production of 3 million tons this year or 50% lower from realized production of 6 million tons in FY14. In order to

maintain coal sales, the company will buy coal from third parties. We assume coal sales to reach above the production target as the

company’s sales has reached 2.3 million tons in 5M15. We forecast coal

sales to reach 3.71 million tons in FY15F or decreased 37.5% from 2014.

Source: Company, PSI Research estimate

Given the Japan 2030 energy mix plan that allows little room for any generation from fossil fuel and focuses on renewable and nuclear energy

generation, Japan’s coal import will likely to decrease in years ahead. This situation will affect the company’s coal production and sales as the

company has been exporting to Japan, South Korea, and Taiwan. In the

2.40 3.05

4.49

5.57

4.18

5.94

3.71 4.09

4.63

5.17

2009 2010 2011 2012 2013 2014 2015F 2016F 2017F 2018F

Coal mining (million tons)

PHILLIP SECURITIES INDONESIA | 8 | P a g e

UNITED TRACTORS INITIATION

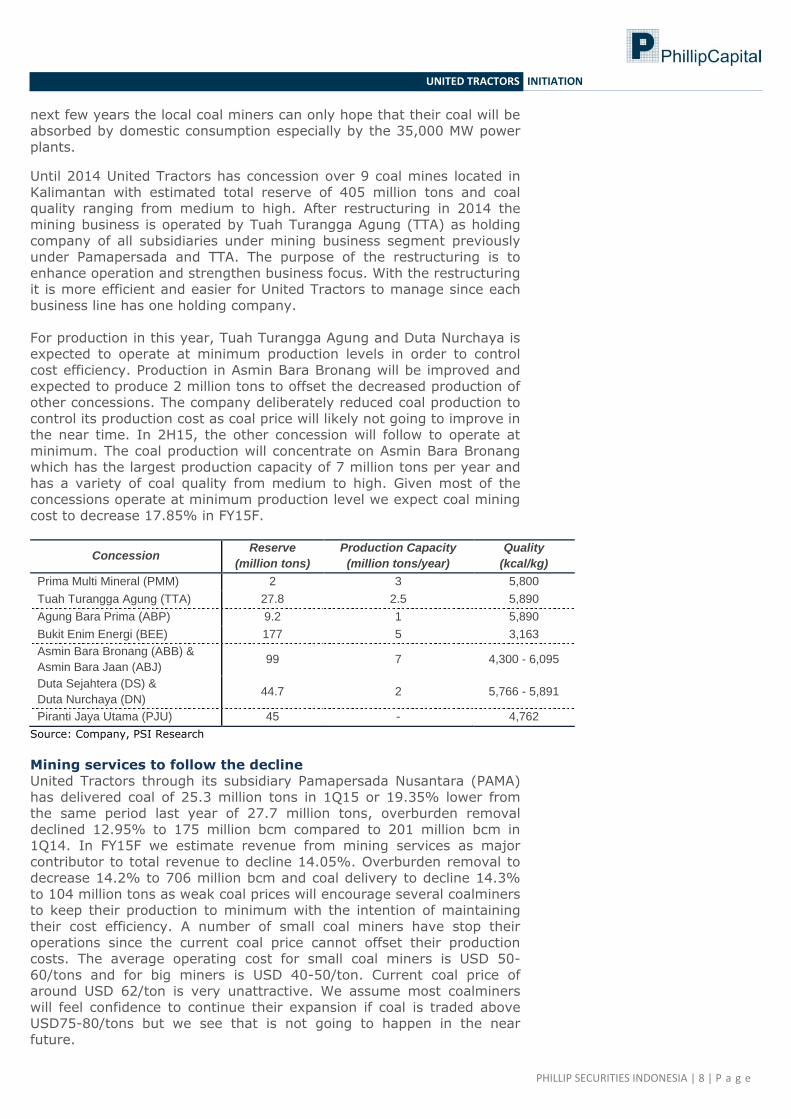

next few years the local coal miners can only hope that their coal will be absorbed by domestic consumption especially by the 35,000 MW power

plants.

Until 2014 United Tractors has concession over 9 coal mines located in

Kalimantan with estimated total reserve of 405 million tons and coal quality ranging from medium to high. After restructuring in 2014 the

mining business is operated by Tuah Turangga Agung (TTA) as holding

company of all subsidiaries under mining business segment previously under Pamapersada and TTA. The purpose of the restructuring is to

enhance operation and strengthen business focus. With the restructuring it is more efficient and easier for United Tractors to manage since each

business line has one holding company.

For production in this year, Tuah Turangga Agung and Duta Nurchaya is expected to operate at minimum production levels in order to control

cost efficiency. Production in Asmin Bara Bronang will be improved and

expected to produce 2 million tons to offset the decreased production of other concessions. The company deliberately reduced coal production to

control its production cost as coal price will likely not going to improve in the near time. In 2H15, the other concession will follow to operate at

minimum. The coal production will concentrate on Asmin Bara Bronang which has the largest production capacity of 7 million tons per year and

has a variety of coal quality from medium to high. Given most of the concessions operate at minimum production level we expect coal mining

cost to decrease 17.85% in FY15F.

Concession Reserve

(million tons)

Production Capacity

(million tons/year)

Quality

(kcal/kg)

Prima Multi Mineral (PMM) 2 3 5,800

Tuah Turangga Agung (TTA) 27.8 2.5 5,890

Agung Bara Prima (ABP) 9.2 1 5,890

Bukit Enim Energi (BEE) 177 5 3,163

Asmin Bara Bronang (ABB) &

Asmin Bara Jaan (ABJ) 99 7 4,300 - 6,095

Duta Sejahtera (DS) &

Duta Nurchaya (DN) 44.7 2 5,766 - 5,891

Piranti Jaya Utama (PJU) 45 - 4,762

Source: Company, PSI Research

Mining services to follow the decline

United Tractors through its subsidiary Pamapersada Nusantara (PAMA)

has delivered coal of 25.3 million tons in 1Q15 or 19.35% lower from the same period last year of 27.7 million tons, overburden removal

declined 12.95% to 175 million bcm compared to 201 million bcm in 1Q14. In FY15F we estimate revenue from mining services as major

contributor to total revenue to decline 14.05%. Overburden removal to decrease 14.2% to 706 million bcm and coal delivery to decline 14.3%

to 104 million tons as weak coal prices will encourage several coalminers to keep their production to minimum with the intention of maintaining

their cost efficiency. A number of small coal miners have stop their

operations since the current coal price cannot offset their production costs. The average operating cost for small coal miners is USD 50-

60/tons and for big miners is USD 40-50/ton. Current coal price of around USD 62/ton is very unattractive. We assume most coalminers

will feel confidence to continue their expansion if coal is traded above USD75-80/tons but we see that is not going to happen in the near

future.

PHILLIP SECURITIES INDONESIA | 9 | P a g e

UNITED TRACTORS INITIATION

Source: Company, PSI Research estimate

PAMA is the market leader in mining contracting with market share of around 30% and entrusted to continue to manage 14 mining contracting

projects with major clients including Adaro Energy (ADRO IJ), Tambang Batubara Bukit Asam (PTBA IJ), and Indo Tambangraya Megah (ITMG

IJ). Most of them want to keep production at the same level as last

year. To meet the clients’ demand, UNTR will likely to continue its “Cost Down Program”. The idea is to reduce cost while maintaining production

level. After successfully lowering strip ratio in FY14 to 6.75x from 8.04x in FY13, for this year the company will likely to maintain strip ratio of

6.7x.

As we know demand from the biggest coal importer China decreases every year due to economic slowdown and the government’s policy to

protect local coal miners. Moreover, demand from Indonesia domestic

market is not improving given the slow realization of power plant construction which the government plans to build with total capacity of

35,000 MW in the next 5 years. Until this report is written the construction has not been commence. Land acquisition in Batang,

Central Java faces rejection from local residents backed by environmental society, and it seems the construction will not start by

this year. Given the condition, domestic coal demands will likely not going to improve until the project is finished.

Although coal will remain as important energy fuel in the next decade, coal consumption begins to decrease as many developed countries in

the world are concerned about pollution, prompting them to switch to green or renewable energy. On the other hand a large section of the

population in the developing nations of Asia and Africa are yet to have access to electricity. For most of these developing nations, thermal coal

is the preferred choice of electricity generation as coal price is relatively cheap compared to other sources of energy. So we assume next

destination for coal is Africa and developing nation of Asia.

598652

792856 845

806

706 726748 769

6878

8794

105

119104

112121 122

0

20

40

60

80

100

120

140

0

100

200

300

400

500

600

700

800

900

2009 2010 2011 2012 2013 2014 2015F 2016F 2017F 2018F

Overburden removal (mn bcm) Coal delivery (mn ton)

PHILLIP SECURITIES INDONESIA | 10 | P a g e

UNITED TRACTORS INITIATION

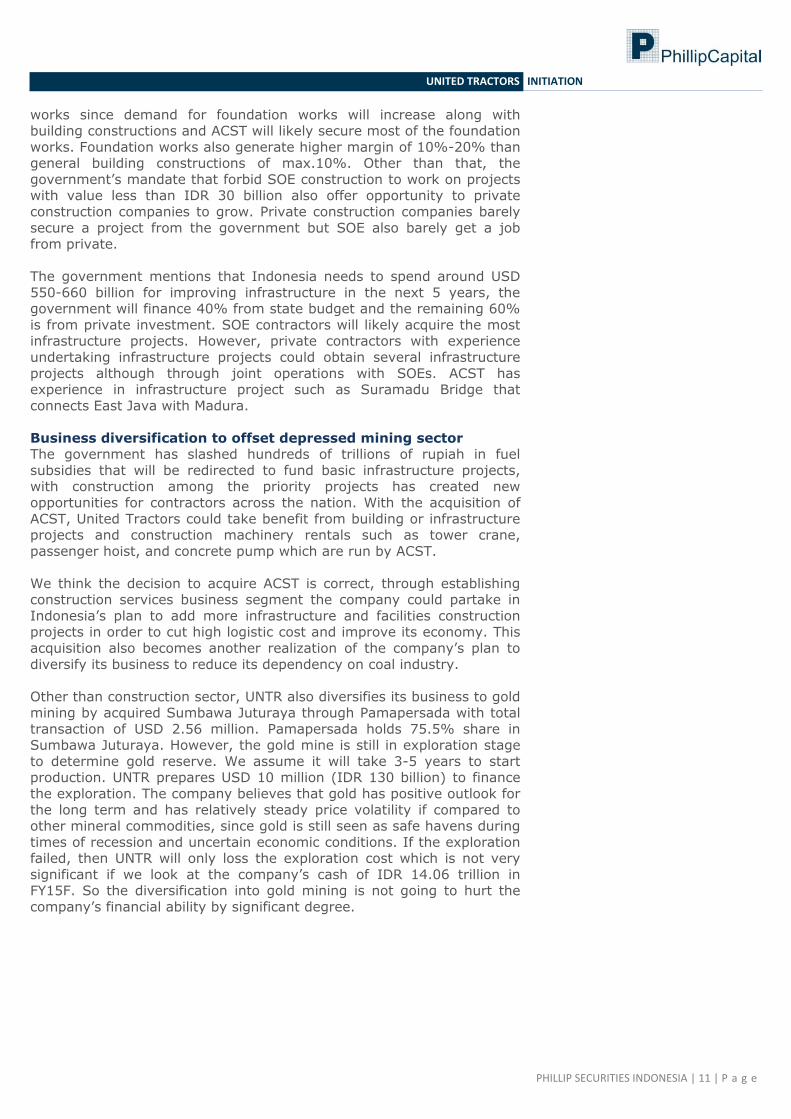

Construction services to contribute 5% to total revenue In late 2014, United Tractors through its subsidiary Karya Supra Perkasa

acquired Acset Indonusa (ACST IJ), a construction company, to diversify its business to offset the declining coal mining sector. ACST works on

projects that include foundations, civil works, detail designs, mechanical & electrical, plumbing, and finishing, making ACST a construction

company with the ability to provide end to end construction services.

Through ACST, United tractors wish to participate in the government’s plan to improve infrastructure in order to support economic growth. The

company believes that through participation in infrastructure project it could increase revenue also strengthen business portfolio to provide end

to end services to its customers.

In 1Q15 ACST posted revenue of IDR 313.35 billion, increased 19.8% from IDR 261.64 in 1Q14. ACST also secured new contract of IDR 1.36

trillion or 68% of new contract target of IDR 2 trillion. We expect ACST

revenue to increase 18.60% in this year supported by several construction projects such as Harris Hotel, Yellow Hotel, Gayanti City,

TCC Batavia Tower, Taman Anggrek Residence, and Thamrin Nine phase 2. The company does not have big expectation that construction sector

will soar in this year due to pending realization of massive infrastructure projects in the country.

Source: Company, PSI Research estimate

With Astra group behind them, it is easier for ACST to expand its

business as Astra has strong brand positioning in Indonesia. Also, ACST

can take benefit from Astra if they need funding from financial institutions to finance its projects since Astra certainly has cheaper

credit facility. ACST can also take benefit from Astra’s construction projects. Astra group carries out construction work of around IDR 15

trillion per year and ACST will likely to secure at least 25% from the projects.

Construction business in Indonesia remains attractive since Indonesia is

the biggest construction market and contributes more than 65% to

construction business in ASEAN. However, domestic construction business is dominated by state owned general constructions as SOE

always secure contracts to work on government projects. SOEs also have larger order book, working cap, market cap, etc. This fact makes it

harder for private construction companies with smaller size to compete with SOEs to secure large projects that require high working capital. But

that matter is relatively not a significant threat for specialist construction companies such as ACST which specializes in foundation

669.91

1,014.50

1,350.91

1,601.78

1,898.49

2,249.98

2,666.51

2012 2013 2014 2015F 2016F 2017F 2018F

Construction services revenue (IDR billion)

PHILLIP SECURITIES INDONESIA | 11 | P a g e

UNITED TRACTORS INITIATION

works since demand for foundation works will increase along with building constructions and ACST will likely secure most of the foundation

works. Foundation works also generate higher margin of 10%-20% than general building constructions of max.10%. Other than that, the

government’s mandate that forbid SOE construction to work on projects with value less than IDR 30 billion also offer opportunity to private

construction companies to grow. Private construction companies barely

secure a project from the government but SOE also barely get a job from private.

The government mentions that Indonesia needs to spend around USD

550-660 billion for improving infrastructure in the next 5 years, the government will finance 40% from state budget and the remaining 60%

is from private investment. SOE contractors will likely acquire the most infrastructure projects. However, private contractors with experience

undertaking infrastructure projects could obtain several infrastructure

projects although through joint operations with SOEs. ACST has experience in infrastructure project such as Suramadu Bridge that

connects East Java with Madura.

Business diversification to offset depressed mining sector The government has slashed hundreds of trillions of rupiah in fuel

subsidies that will be redirected to fund basic infrastructure projects, with construction among the priority projects has created new

opportunities for contractors across the nation. With the acquisition of

ACST, United Tractors could take benefit from building or infrastructure projects and construction machinery rentals such as tower crane,

passenger hoist, and concrete pump which are run by ACST.

We think the decision to acquire ACST is correct, through establishing construction services business segment the company could partake in

Indonesia’s plan to add more infrastructure and facilities construction projects in order to cut high logistic cost and improve its economy. This

acquisition also becomes another realization of the company’s plan to

diversify its business to reduce its dependency on coal industry.

Other than construction sector, UNTR also diversifies its business to gold mining by acquired Sumbawa Juturaya through Pamapersada with total

transaction of USD 2.56 million. Pamapersada holds 75.5% share in Sumbawa Juturaya. However, the gold mine is still in exploration stage

to determine gold reserve. We assume it will take 3-5 years to start production. UNTR prepares USD 10 million (IDR 130 billion) to finance

the exploration. The company believes that gold has positive outlook for

the long term and has relatively steady price volatility if compared to other mineral commodities, since gold is still seen as safe havens during

times of recession and uncertain economic conditions. If the exploration failed, then UNTR will only loss the exploration cost which is not very

significant if we look at the company’s cash of IDR 14.06 trillion in FY15F. So the diversification into gold mining is not going to hurt the

company’s financial ability by significant degree.

PHILLIP SECURITIES INDONESIA | 12 | P a g e

UNITED TRACTORS INITIATION

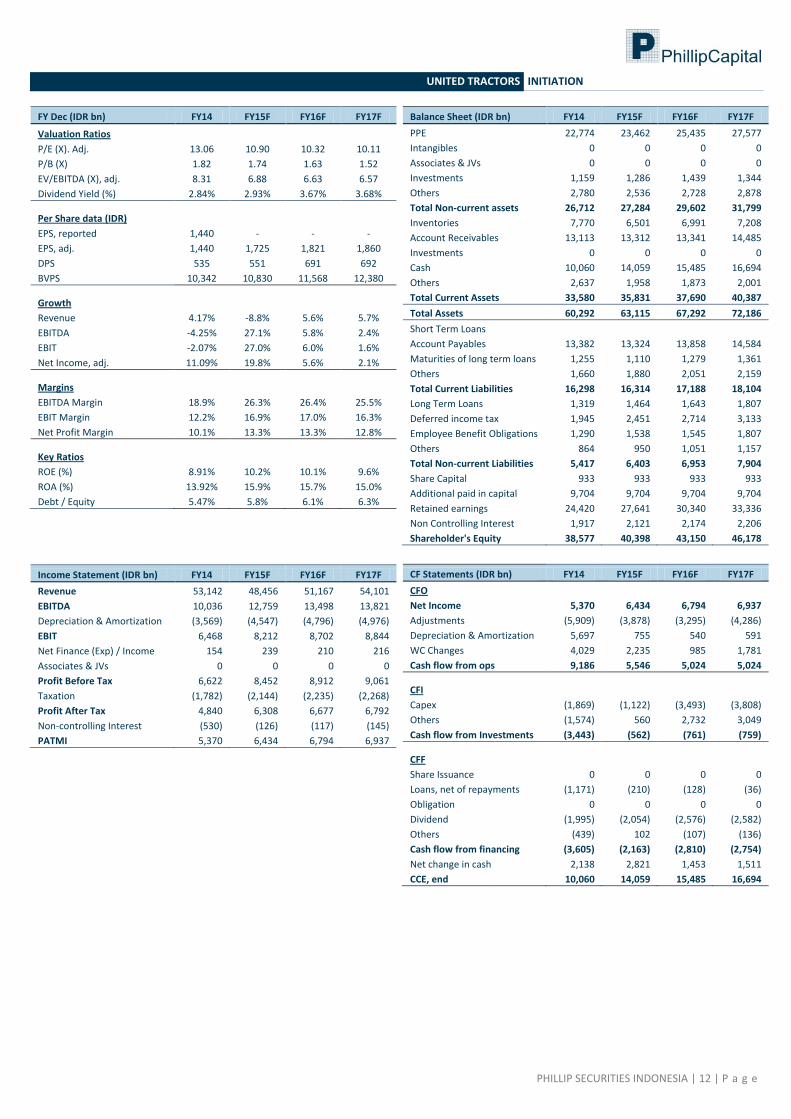

FY Dec (IDR bn) FY14 FY15F FY16F FY17F

Valuation Ratios

P/E (X). Adj. 13.06 10.90 10.32 10.11

P/B (X) 1.82 1.74 1.63 1.52

EV/EBITDA (X), adj. 8.31 6.88 6.63 6.57

Dividend Yield (%) 2.84% 2.93% 3.67% 3.68%

Per Share data (IDR)

EPS, reported 1,440 - - -

EPS, adj. 1,440 1,725 1,821 1,860

DPS 535 551 691 692

BVPS 10,342 10,830 11,568 12,380

Growth

Revenue 4.17% -8.8% 5.6% 5.7%

EBITDA -4.25% 27.1% 5.8% 2.4%

EBIT -2.07% 27.0% 6.0% 1.6%

Net Income, adj. 11.09% 19.8% 5.6% 2.1%

Margins

EBITDA Margin 18.9% 26.3% 26.4% 25.5%

EBIT Margin 12.2% 16.9% 17.0% 16.3%

Net Profit Margin 10.1% 13.3% 13.3% 12.8%

Key Ratios

ROE (%) 8.91% 10.2% 10.1% 9.6%

ROA (%) 13.92% 15.9% 15.7% 15.0%

Debt / Equity 5.47% 5.8% 6.1% 6.3%

Income Statement (IDR bn) FY14 FY15F FY16F FY17F

Revenue 53,142 48,456 51,167 54,101

EBITDA 10,036 12,759 13,498 13,821

Depreciation & Amortization (3,569) (4,547) (4,796) (4,976)

EBIT 6,468 8,212 8,702 8,844

Net Finance (Exp) / Income 154 239 210 216

Associates & JVs 0 0 0 0

Profit Before Tax 6,622 8,452 8,912 9,061

Taxation (1,782) (2,144) (2,235) (2,268)

Profit After Tax 4,840 6,308 6,677 6,792

Non-controlling Interest (530) (126) (117) (145)

PATMI 5,370 6,434 6,794 6,937

Balance Sheet (IDR bn) FY14 FY15F FY16F FY17F

PPE 22,774 23,462 25,435 27,577

Intangibles 0 0 0 0

Associates & JVs 0 0 0 0

Investments 1,159 1,286 1,439 1,344

Others 2,780 2,536 2,728 2,878

Total Non-current assets 26,712 27,284 29,602 31,799

Inventories 7,770 6,501 6,991 7,208

Account Receivables 13,113 13,312 13,341 14,485

Investments 0 0 0 0

Cash 10,060 14,059 15,485 16,694

Others 2,637 1,958 1,873 2,001

Total Current Assets 33,580 35,831 37,690 40,387

Total Assets 60,292 63,115 67,292 72,186

Short Term Loans

Account Payables 13,382 13,324 13,858 14,584

Maturities of long term loans 1,255 1,110 1,279 1,361

Others 1,660 1,880 2,051 2,159

Total Current Liabilities 16,298 16,314 17,188 18,104

Long Term Loans 1,319 1,464 1,643 1,807

Deferred income tax 1,945 2,451 2,714 3,133

Employee Benefit Obligations 1,290 1,538 1,545 1,807

Others 864 950 1,051 1,157

Total Non-current Liabilities 5,417 6,403 6,953 7,904

Share Capital 933 933 933 933

Additional paid in capital 9,704 9,704 9,704 9,704

Retained earnings 24,420 27,641 30,340 33,336

Non Controlling Interest 1,917 2,121 2,174 2,206

Shareholder's Equity 38,577 40,398 43,150 46,178

CF Statements (IDR bn) FY14 FY15F FY16F FY17F

CFO

Net Income 5,370 6,434 6,794 6,937

Adjustments (5,909) (3,878) (3,295) (4,286)

Depreciation & Amortization 5,697 755 540 591

WC Changes 4,029 2,235 985 1,781

Cash flow from ops 9,186 5,546 5,024 5,024

CFI

Capex (1,869) (1,122) (3,493) (3,808)

Others (1,574) 560 2,732 3,049

Cash flow from Investments (3,443) (562) (761) (759)

CFF

Share Issuance 0 0 0 0

Loans, net of repayments (1,171) (210) (128) (36)

Obligation 0 0 0 0

Dividend (1,995) (2,054) (2,576) (2,582)

Others (439) 102 (107) (136)

Cash flow from financing (3,605) (2,163) (2,810) (2,754)

Net change in cash 2,138 2,821 1,453 1,511

CCE, end 10,060 14,059 15,485 16,694

PHILLIP SECURITIES INDONESIA | 13 | P a g e

UNITED TRACTORS INITIATION

Important Information

Rating for Sectors: Overweight : We expect the industry to perform better than the primary market index (JCI) over the next 12 months. Neutral : We expect the industry to perform in line with the primary market index (JCI) over the next 12 months. Underweight : We expect the industry to under-perform the primary market index (JCI) over the next 12 months. Rating for Stocks: Buy : The stock is expected to give total return (price appreciation + dividend yield) of > +20% over the next 12 months. Accumulate : The stock is expected to give total return (price appreciation + dividend yield) of +5% to +20% over the next 12 months. Neutral : The stock is expected to give total return of between -5% and +5% over the next 12 months. Reduce : The stock is expected to give total return of between -5% and -20% over the next 12 months. Sell : The stock is expected to give total return of -20% or lower over the next 12 months. Outperform : The stock is expected to do slightly better than the market return. Equal to “accumulate” or “moderate buy” Underperform : The stock is expected to do slightly worse than the market return. Equal to “weak hold” or “moderate sell” Analyst Certification The research analyst(s) primarily responsible for the preparation of this research report hereby certify that all of the views expressed in this research report accurately reflect their personal views about any and all of the subject securities or issuers. The research analyst(s) also certify that no part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this research report. Disclaimers This document has been prepared for general circulation based on information obtained from sources believed to be reliable. But we do not make any representations as to its accuracy or completeness. Phillip Securities Indonesia (PSI) accept no liability whatsoever for any direct or consequential loss arising from any use of this document or any solicitations of an offer to buy or sell any securities. PSI and its directors, officials and/or employees may have positions in, and may affect transactions in securities mentioned herein from time to time in the open market or otherwise, and may receive brokerage fees or act as principal or agent in dealing with respect to these companies. PSI may also seek investment banking business with companies covered in its research reports. As a result investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Contact Information (Indonesia Research Team)

PHILLIP SECURITIES INDONESIA | 14 | P a g e

UNITED TRACTORS INITIATION

Management

Gunawan Sutanto (Head, Research - Equities)

+62 21 57 900 800 [email protected]

Fardini rahma Dewi (Research Assistant)

+62 21 57 900 800 [email protected]

Automotive | Strategy Cement | Construction | Property | Toll Road Banking | Telecommunication Gunawan Sutanto +62 21 57 900 800 Martha Christina +62 21 57 900 800 Milka Mutiara +62 21 57 900 800 [email protected] [email protected] [email protected] Agriculture | Consumer Goods Retail Trade | Poultry Gas | Mining | Heavy Equipment Edward Lowis +62 21 57 900 800 Muhamad Farhan +62 21 57 900 800 Destya Faishal +62 21 57 900 800 [email protected] [email protected] [email protected]

Contact Information (Regional Member Companies)

SINGAPORE

Phillip Securities Pte Ltd Raffles City Tower

250, North Bridge Road #06-00 Singapore 179101 Tel +65 6533 6001 Fax +65 6535 6631

Website: www.poems.com.sg

MALAYSIA Phillip Capital Management Sdn Bhd

B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450

Kuala Lumpur Tel +603 2162 8841 Fax +603 2166 5099

Website: www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd

11/F United Centre 95 Queensway Hong Kong

Tel +852 2277 6600 Fax +852 2868 5307

Websites: www.phillip.com.hk

JAPAN

Phillip Securities Japan, Ltd. 4-2 Nihonbashi Kabuto-cho Chuo-ku,

Tokyo 103-0026 Tel +81-3 3666 2101 Fax +81-3 3666 6090

Website:www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia

ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia

Tel +62-21 5790 0800 Fax +62-21 5790 0809

Website: www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co Ltd

No 550 Yan An East Road, Ocean Tower Unit 2318,

Postal code 200001 Tel +86-21 5169 9200 Fax +86-21 6351 2940

Website: www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd

15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak,

Bangkok 10500 Thailand Tel +66-2 6351700 / 22680999

Fax +66-2 22680921 Website www.phillip.co.th

FRANCE King & Shaxson Capital Limited

3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France

Tel +33-1 45633100 Fax +33-1 45636017

Website: www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Capital Limited

6th Floor, Candlewick House, 120 Cannon Street, London, EC4N 6AS

Tel +44-20 7426 5950 Fax +44-20 7626 1757

Website: www.kingandshaxson.com

UNITED STATES Phillip Futures Inc

141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building

Chicago, IL 60604 USA Tel +1-312 356 9000 Fax +1-312 356 9005

AUSTRALIA PhillipCapital

Level 12, 15 William Street, Melbourne, Victoria 3000, Australia

Tel +61-03 9629 8288 Fax +61-03 9629 8882

Website: www.phillipcapital.com.au

SRI LANKA Asha Phillip Securities Limited

No 10, Prince Alfred Tower, Alfred House Gardens, Colombo 3, Sri Lanka

Tel: (94) 11 2429 100 Fax: (94) 11 2429 199 Website: www.ashaphillip.net/home.htm

INDIA

PhillipCapital (India) Private Limited No. 1, C‐Block, 2nd Floor, Modern Center , Jacob

Circle, K. K. Marg, Mahalaxmi Mumbai 400011 Tel: (9122) 2300 2999 Fax: (9122) 6667 9955

Website: www.phillipcapital.in

PHILLIP SECURITIES INDONESIA | 15 | P a g e

UNITED TRACTORS INITIATION

ANZ Tower Level 23B, Jl. Jendral Sudirman Kav 33A, Jakarta, 10220 - Indonesia

Telp. (62-21) 57 900 800, Fax. (62-21) 57 900 809, Email : [email protected]

Website: www.phillip.co.id | www.poems.co.id | www.poems.web.id

Jakarta

Komp. Ruko Mega Grosir Cempaka Mas Jl. Let. Jend. Soeprapto

Blok D No. 7 Jakarta, 10640 Telp. (62-21) 4288 5051 / 52; Fax. (62-21) 4288 5049

E-Mail: [email protected]

Mangga Dua Ruko Bahan Bangunan Mangga Dua Blok F1/8

Jl. Mangga Dua Selatan Jakarta 10730 Telp. (62-21) 6220 3589; Fax. (62-21) 6220 3602

E-Mail: [email protected]

Rukan Sentra Latumenten Jl.Prof.Dr Latumenten no.50

Blk AA 12 Jakarta, 11460 Telp. (62-21) 5694 1781; Fax. (62-21) 5694 1791

E-Mail: [email protected]

Roxy Pusat Niaga Roxy Mas Blok B2/2

Jl. KH. Hasyim Ashari - Jakarta Barat Telp. (62-21) 6386 8308; Fax. (62-21) 6333 420

E-Mail: [email protected]

Pantai Indah Kapuk Jl. Pantai Indah Barat Rukan Ekslusif BGM Blok B-6

Telp. (62-21) 5694 5791/92/93; Fax. (62-21) 56945790 E-Mail: [email protected]

Taman Palem Rukan Malibu Blok H No. 23 Cengkareng, Jakbar 11730

Telp. (62-21) 5694 5055 / 5077; Fax. (62-21) 5694 5013; E-Mail: [email protected]

Tanah Abang

Pusat Grosir Metro Tanah Abang (PGMTA) Lantai 6, Jl.Fachrudin Tanah Abang - Jakarta Pusat 10250

Telp : (021) 3003 6745 / 3003 6746; Fax : (021) 3003 6748 E-Mail: [email protected]

Kelapa Gading Jl. Boulevard Raya Blok WB2/27 Kelapa Gading Jakarta Utara

Telp. (62-21) 7070 0050/4587/9264; Fax. (62-21) 453 2939; E-Mail: [email protected]

Citra Garden 2

Komp. Citra Niaga Blok A No.18 Citra Garden 2 - Kalideres, JakBar

Telp. (62-21) 5436 0175; Fax. (62-21) 5436 0174 E-mail: [email protected]

Alam Sutera Ruko Prominence Blok 38 - G No. 18

Jl. Sutra Barat Boulevard Alam Sutra 15143, Tangerang No. Telp : (021) 50314300

Jawa Tengah Purwokerto

Jln. Perintis Kemerdekaan No. 38 Purwokerto - Jawa Tengah, 53110

Telp. (62-281) 626 899; Fax. (62-281) 891 150 E-Mail: [email protected]

Yogyakarta Kantor Perwakilan (KP) BEI Yogyakarta

Jl. Mangkubumi No. 111 Yogyakarta Telp. (0274) 557367

E-mail: [email protected]

Semarang Jl. Karang Wulan Timur No. 2 - 4 Semarang

Indonesia Telp. (62-24) 355 5959; Fax. (62-24) 351 3194

E-Mail: [email protected]

Tegal Kompleks Nirmala Square Blok C no.7

Jl. Yos Sudarso - Tegal 52121 Telp. (62-283) 340773; Fax. (62-283) 340774

E-mail: [email protected]

Jawa Barat Batam

Komp.Paskal Hypersquare Blok C-21 Jl Pasirkaliki 25-27 Bandung

Telp. (62-22) 8606 0690; Fax. (62-22) 8606 0765 E-Mail: [email protected]

Kompleks Mahkota Raya Blok A no. 10 Batam Centre, Kota Batam 29456, Kepri

Telp. (62-778) 748 3337/3030/3131; Fax. (62-778) 748 3117; E-Mail: [email protected]

Jawa Timur Kalimantan Barat

Jln. Flores No. 11 Surabaya, 60281 Telp. (62-31) 501 5777; Fax. (62-31) 501 0567

E-Mail: [email protected]

Jl. Teuku Umar Komplek Pontianak Mal C 23-24 Pontianak, Kalimantan Barat

Telp. (62-561) 777 887; Fax. (62-561) 745 103 E-Mail: [email protected]

Jambi Denpasar

Jln. GR. Djamin Datuk Bagindo No. 56A Jambi, 36142

Telp. (0741) 707 8260, 7555 699 E-Mail: [email protected]

Kantor Perwakilan (KP) BEI Denpasar Jl. P.B. Sudirman 10 X Kav. 2

Denpasar - Bali (0361) 255 900

Lampung

Jl. Ikan Tongkol No. 33 Blok 7-8 Teluk Betung - Bandar Lampung, 35223

Telp. (62-721) 474 234; Fax. (62-721) 474 108 E-Mail: [email protected]