university-income generated through waqfconference.kuis.edu.my/ifid/docs/ifid2016-speaker5.pdf ·...

TRANSCRIPT

UNIVERSITY-INCOME GENERATED THROUGH WAQF

Dato’ Prof Dr Noor Inayah Yaakub

NOVOTEL MELAKA KUIS

2 BANK NEGARA MALAYSIA CENTRAL BANK OF MALAYSIA

Takaful

Takaful in Malaysia developed as component of

comprehensive Islamic financial system operating in

parallel with conventional financial system

Dual

syst

em

Islamic

financial system

Conventional

financial system

Islamic

banking

Islamic

capital

market

Islamic

money

market

Four

main

pillars

The mandate for developing dual

financial system explicitly

codified in Central Bank of

Malaysia Act 2009

Dual Financial

System

Ensure sustained industry

viability via optimised

synergies from interlinkages

Underpinned by :

Strong & diversified

players

Wide range of products &

vibrant financial market

Comprehensive Islamic

Financial System

3 BANK NEGARA MALAYSIA CENTRAL BANK OF MALAYSIA

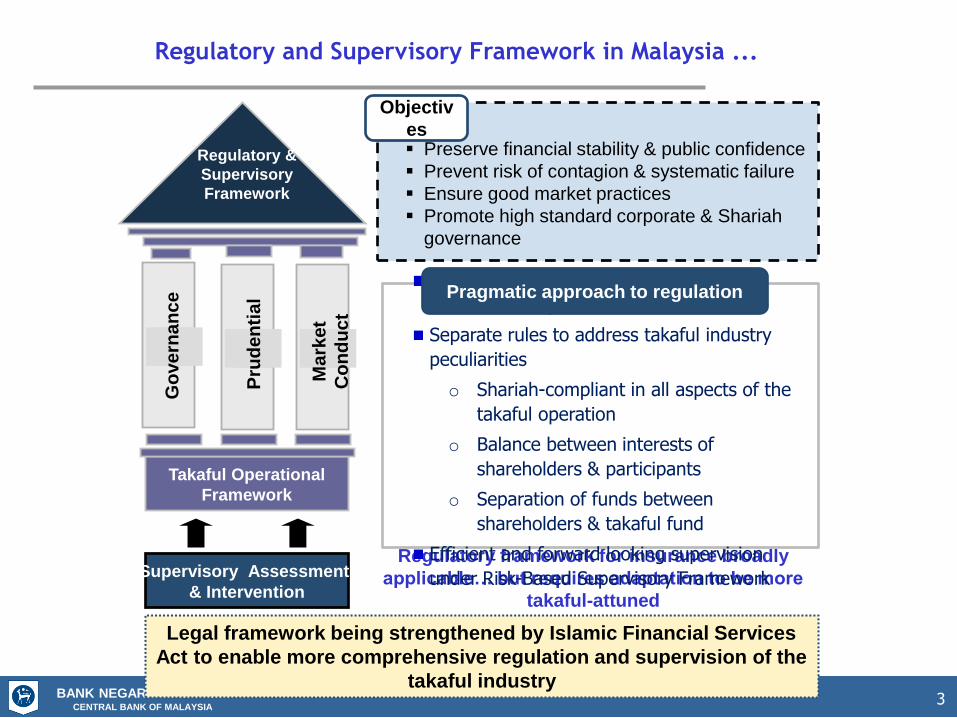

Regulatory framework for insurance broadly

applicable… but requires adaptation to be more

takaful-attuned

Regulatory and Supervisory Framework in Malaysia ...

Preserve financial stability & public confidence

Prevent risk of contagion & systematic failure

Ensure good market practices

Promote high standard corporate & Shariah

governance

Objectiv

es

Leveraging on established field of

conventional system

Separate rules to address takaful industry

peculiarities

o Shariah-compliant in all aspects of the

takaful operation

o Balance between interests of

shareholders & participants

o Separation of funds between

shareholders & takaful fund

Efficient and forward looking supervision

under Risk-Based Supervisory Framework

Pragmatic approach to regulation

Supervisory Assessment

& Intervention

Go

ve

rna

nc

e

Pru

de

nti

al

Ma

rket

Co

nd

uc

t

Takaful Operational

Framework

Regulatory &

Supervisory

Framework

Legal framework being strengthened by Islamic Financial Services

Act to enable more comprehensive regulation and supervision of the

takaful industry

4 BANK NEGARA MALAYSIA CENTRAL BANK OF MALAYSIA

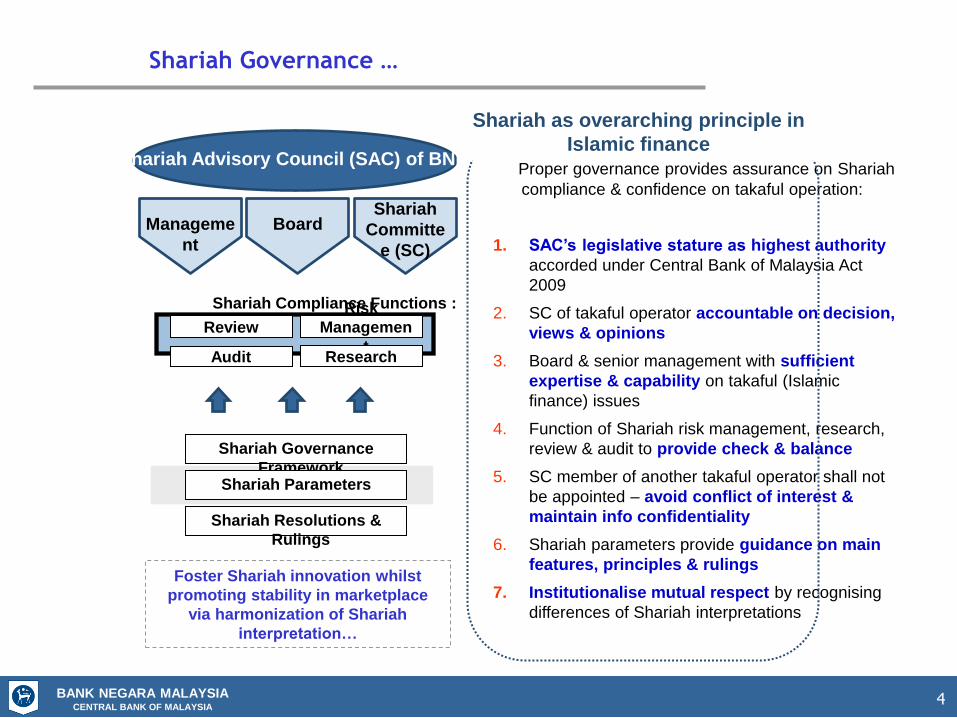

Shariah Governance …

Foster Shariah innovation whilst

promoting stability in marketplace

via harmonization of Shariah

interpretation…

Proper governance provides assurance on Shariah

compliance & confidence on takaful operation:

1. SAC’s legislative stature as highest authority

accorded under Central Bank of Malaysia Act

2009

2. SC of takaful operator accountable on decision,

views & opinions

3. Board & senior management with sufficient

expertise & capability on takaful (Islamic

finance) issues

4. Function of Shariah risk management, research,

review & audit to provide check & balance

5. SC member of another takaful operator shall not

be appointed – avoid conflict of interest &

maintain info confidentiality

6. Shariah parameters provide guidance on main

features, principles & rulings

7. Institutionalise mutual respect by recognising

differences of Shariah interpretations

Shariah as overarching principle in

Islamic finance Shariah Advisory Council (SAC) of BNM

Shariah Compliance Functions :

Review

Audit

Shariah Governance

Framework Shariah Parameters

Shariah Resolutions &

Rulings

Manageme

nt

Board Shariah

Committe

e (SC)

Risk

Managemen

t Research

* 1963-1983

Establishment of Lembaga Tabung Haji Branding of Islamisation in the context of Transaction, Bank Islam, IIUM, Takaful Act

1998 Hong Kong Univ: House of Lords in England in Union Eagle case : 5 minutes late to complete the purchasing price was considered detrimental to the seller (Lord Lytton): Compared with Islamic Law of transaction

2000 Legal Education Association of England & Wales: Web-based learning for Islamic law Subjects as a core subjects for legal education in commonwealth countries

2004 Islamic Bank of Britain was set up

2002-2005

Research 400 decided court cases in England on disputes between H & W in banking Guarantee transactions where a husband is assumed to have exercised some “undue influence” over the wife.

2006 Prime Minister Depart on the prospects of Malaysia as the Hub for Global Islamic Finance with multi-racial populations

2008 Kyoto Univ, Japan offered a research grant on Comparative studies of the remedies offered by Islamic Banking to customers of non Muslims in Japan

( A 50 years Journey…) Global demands in Islamic

Finance Related-Impacts on Malaysia

NOVOTEL MELAKA KUIS

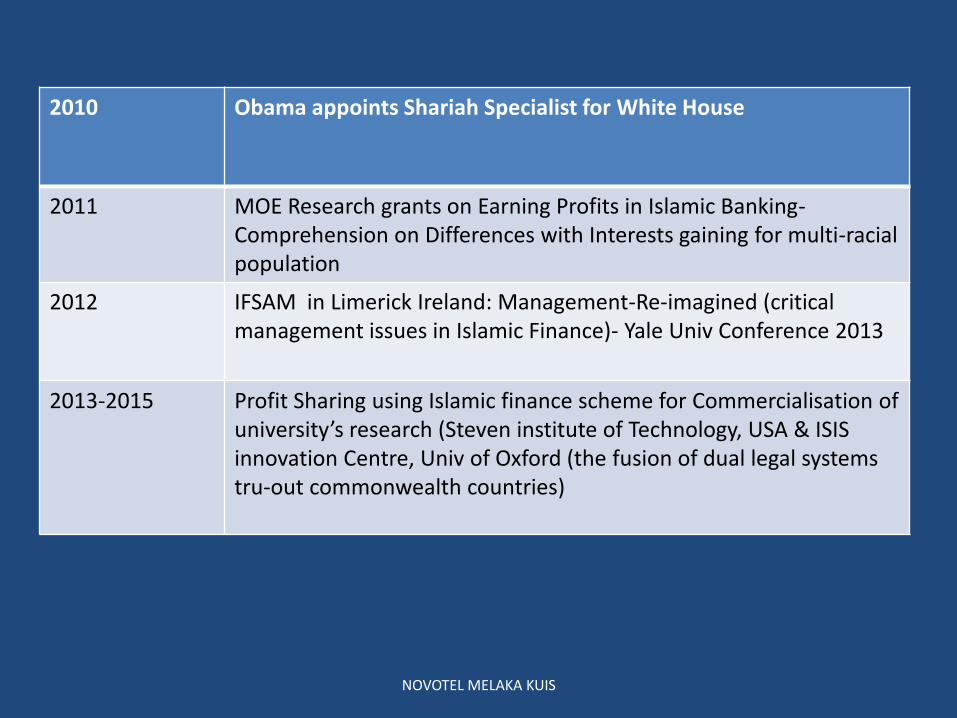

2010 Obama appoints Shariah Specialist for White House

2011 MOE Research grants on Earning Profits in Islamic Banking- Comprehension on Differences with Interests gaining for multi-racial population

2012 IFSAM in Limerick Ireland: Management-Re-imagined (critical management issues in Islamic Finance)- Yale Univ Conference 2013

2013-2015 Profit Sharing using Islamic finance scheme for Commercialisation of university’s research (Steven institute of Technology, USA & ISIS innovation Centre, Univ of Oxford (the fusion of dual legal systems tru-out commonwealth countries)

NOVOTEL MELAKA KUIS

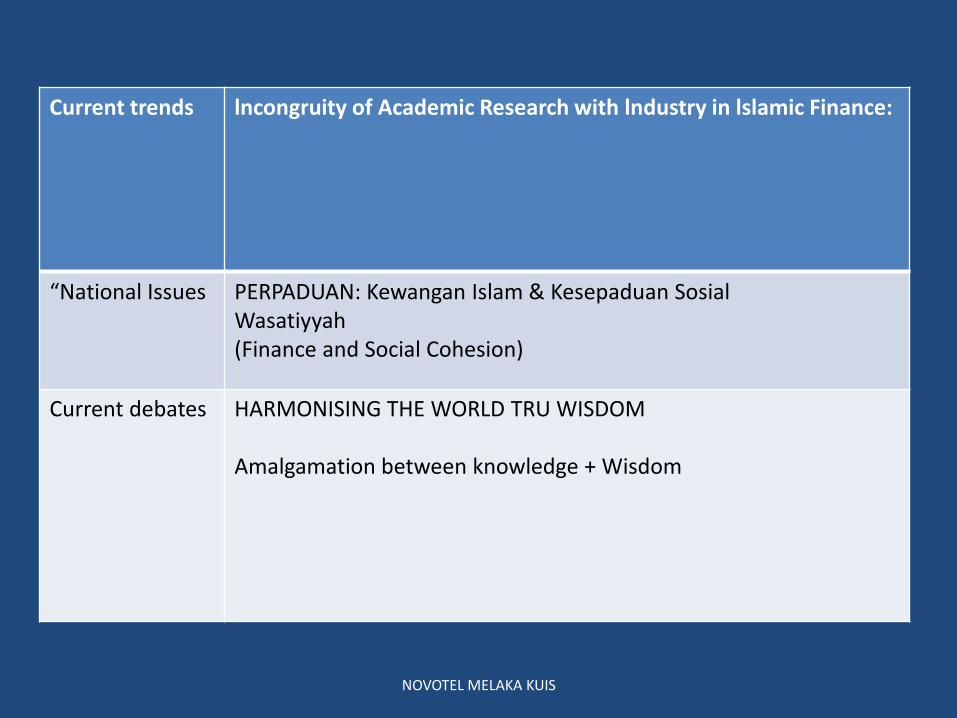

Current trends lncongruity of Academic Research with lndustry in lslamic Finance:

“National Issues PERPADUAN: Kewangan Islam & Kesepaduan Sosial Wasatiyyah (Finance and Social Cohesion)

Current debates HARMONISING THE WORLD TRU WISDOM Amalgamation between knowledge + Wisdom

NOVOTEL MELAKA KUIS

“The Global University in Islamic Finance”

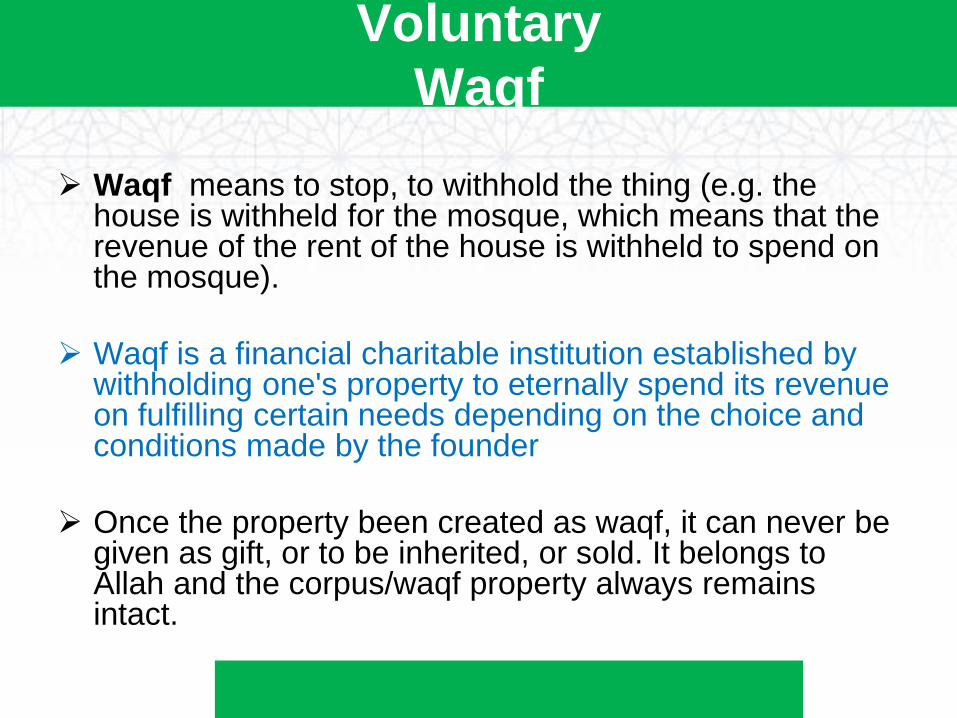

Voluntary

Waqf

Waqf means to stop, to withhold the thing (e.g. the house is withheld for the mosque, which means that the revenue of the rent of the house is withheld to spend on the mosque).

Waqf is a financial charitable institution established by withholding one's property to eternally spend its revenue on fulfilling certain needs depending on the choice and conditions made by the founder

Once the property been created as waqf, it can never be given as gift, or to be inherited, or sold. It belongs to Allah and the corpus/waqf property always remains intact.

“The Global University in Islamic Finance”

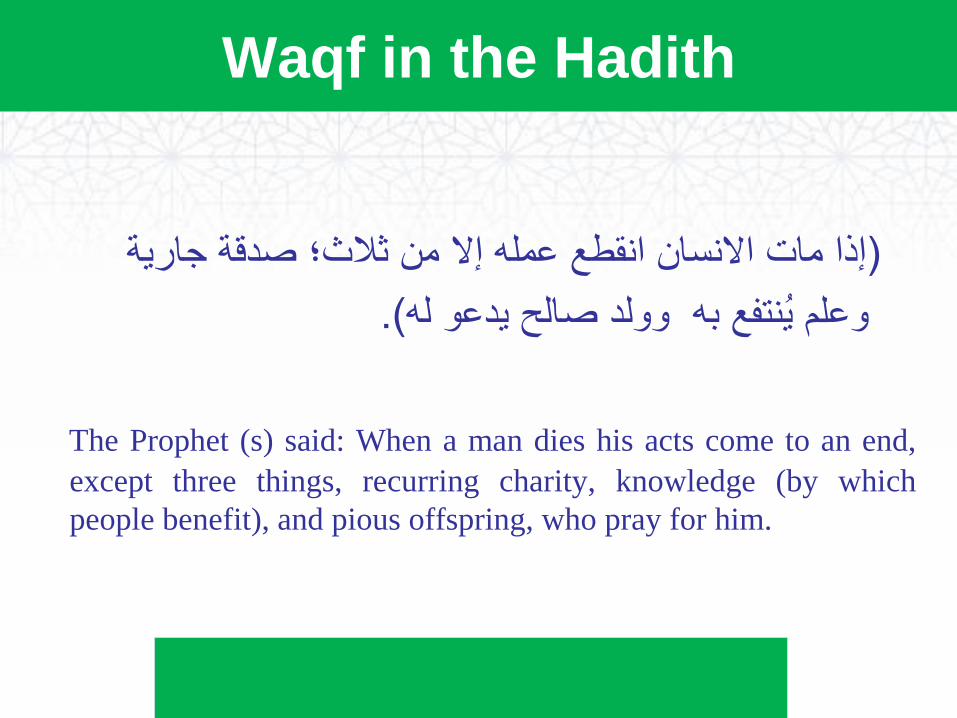

Waqf in the Hadith

إذا مات االنسان انقطع عمله إال من ثالث؛ صدقة جارية )

(.وعلم ُينتفع به وولد صالح يدعو له

The Prophet (s) said: When a man dies his acts come to an end,

except three things, recurring charity, knowledge (by which

people benefit), and pious offspring, who pray for him.

“The Global University in Islamic Finance”

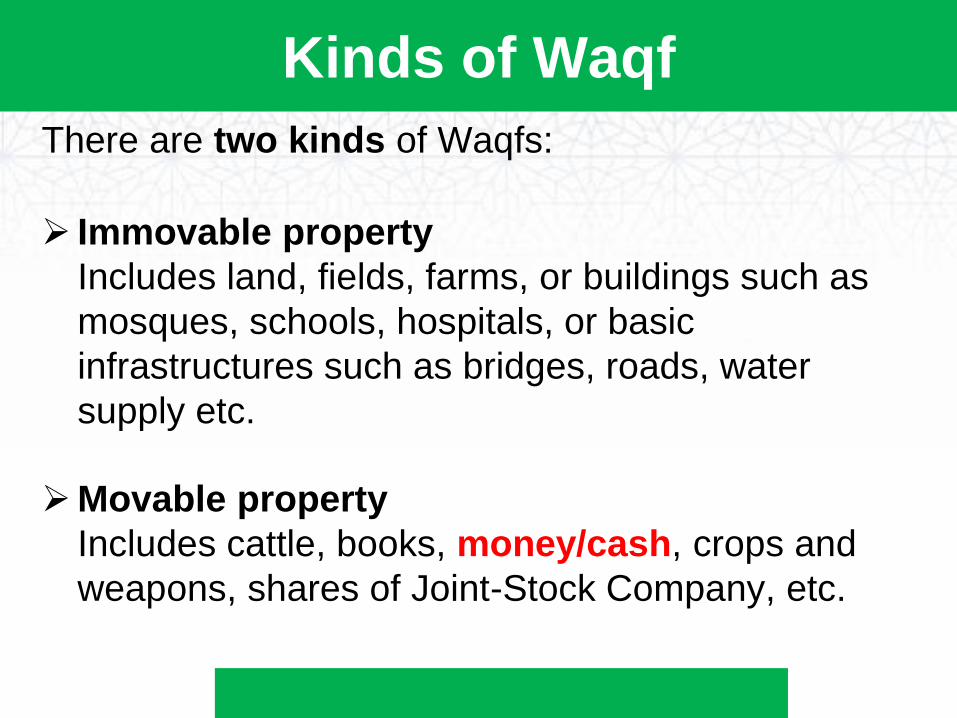

Kinds of Waqf

There are two kinds of Waqfs:

Immovable property

Includes land, fields, farms, or buildings such as

mosques, schools, hospitals, or basic

infrastructures such as bridges, roads, water

supply etc.

Movable property

Includes cattle, books, money/cash, crops and

weapons, shares of Joint-Stock Company, etc.

“The Global University in Islamic Finance”

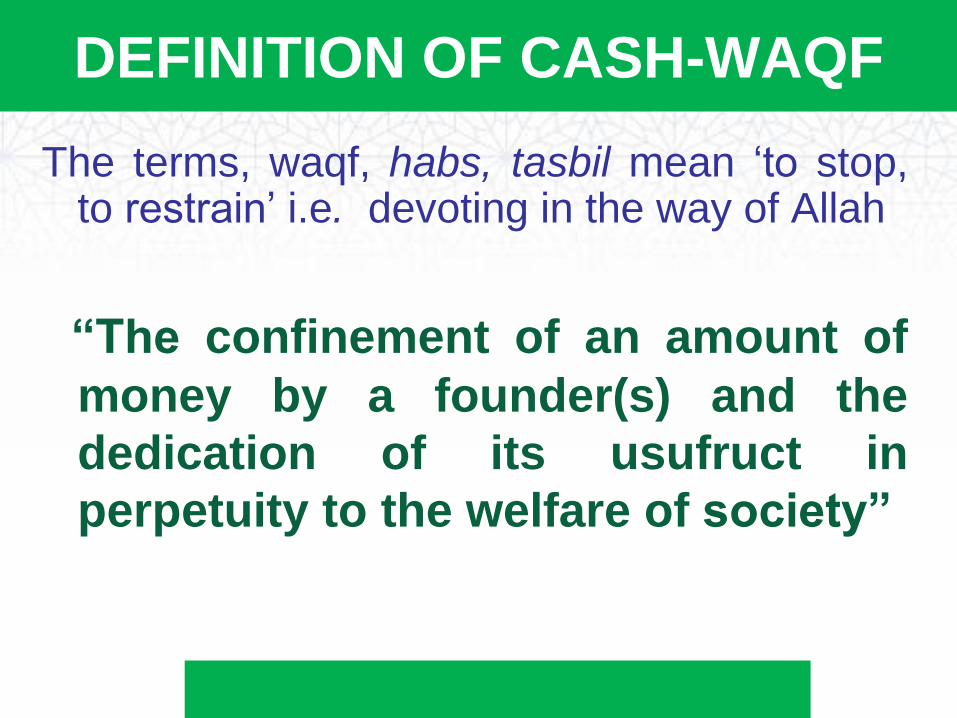

The terms, waqf, habs, tasbil mean „to stop, to restrain‟ i.e. devoting in the way of Allah

“The confinement of an amount of

money by a founder(s) and the

dedication of its usufruct in

perpetuity to the welfare of society”

DEFINITION OF CASH-WAQF

“The Global University in Islamic Finance”

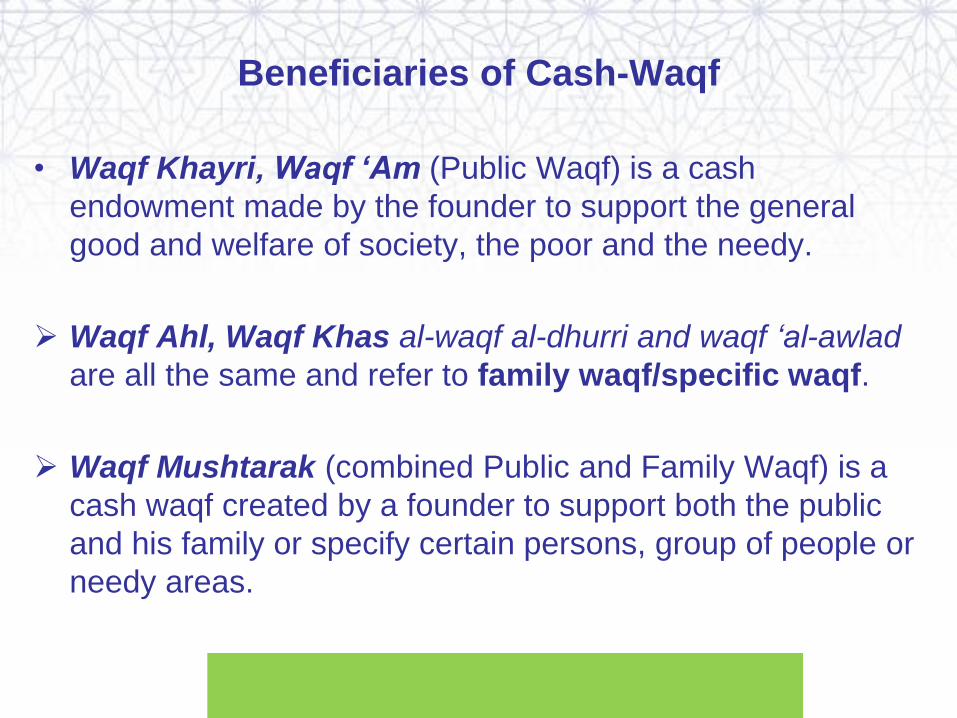

Beneficiaries of Cash-Waqf

• Waqf Khayri, Waqf ‘Am (Public Waqf) is a cash

endowment made by the founder to support the general

good and welfare of society, the poor and the needy.

Waqf Ahl, Waqf Khas al-waqf al-dhurri and waqf ‘al-awlad

are all the same and refer to family waqf/specific waqf.

Waqf Mushtarak (combined Public and Family Waqf) is a

cash waqf created by a founder to support both the public

and his family or specify certain persons, group of people or

needy areas.

“The Global University in Islamic Finance”

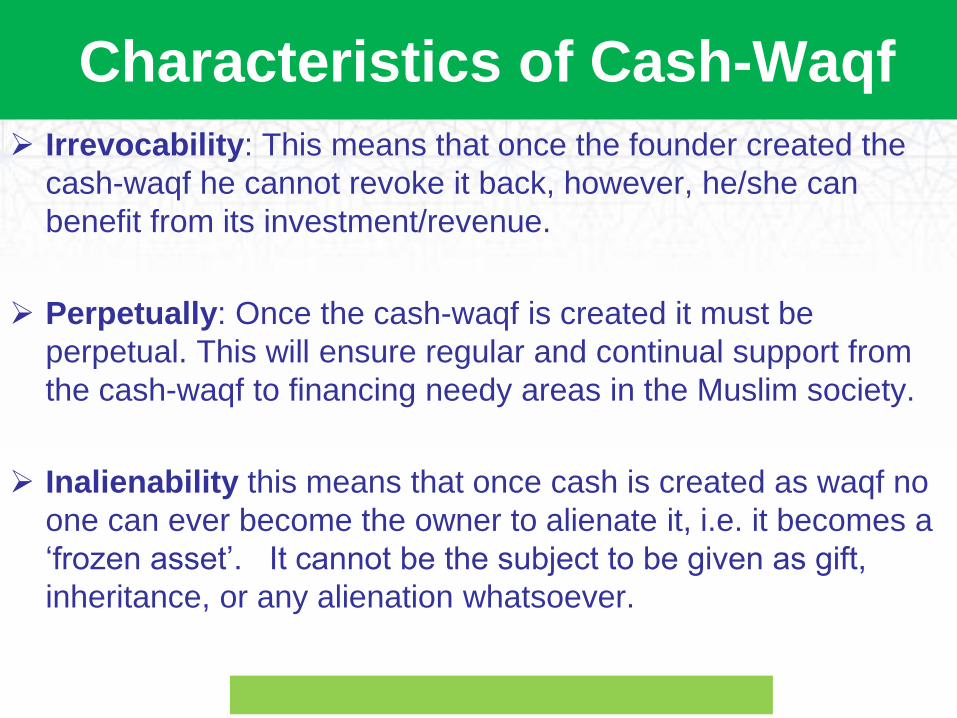

Characteristics of Cash-Waqf

Irrevocability: This means that once the founder created the

cash-waqf he cannot revoke it back, however, he/she can

benefit from its investment/revenue.

Perpetually: Once the cash-waqf is created it must be

perpetual. This will ensure regular and continual support from

the cash-waqf to financing needy areas in the Muslim society.

Inalienability this means that once cash is created as waqf no

one can ever become the owner to alienate it, i.e. it becomes a

„frozen asset‟. It cannot be the subject to be given as gift,

inheritance, or any alienation whatsoever.

“The Global University in Islamic Finance”

Investment of Cash-Waqf

• Mudarabah (partnership) has been

recommended by earlier Muslim jurists.

• The latest fatwa issued by Fiqh Academy

Islam, agreed that cash waqf can be

invested in any shari‟ah compliant mode of

investment, such as Mudharabah,

Murabaha, BBA, Musharakah, Istisna, etc.

“The Global University in Islamic Finance”

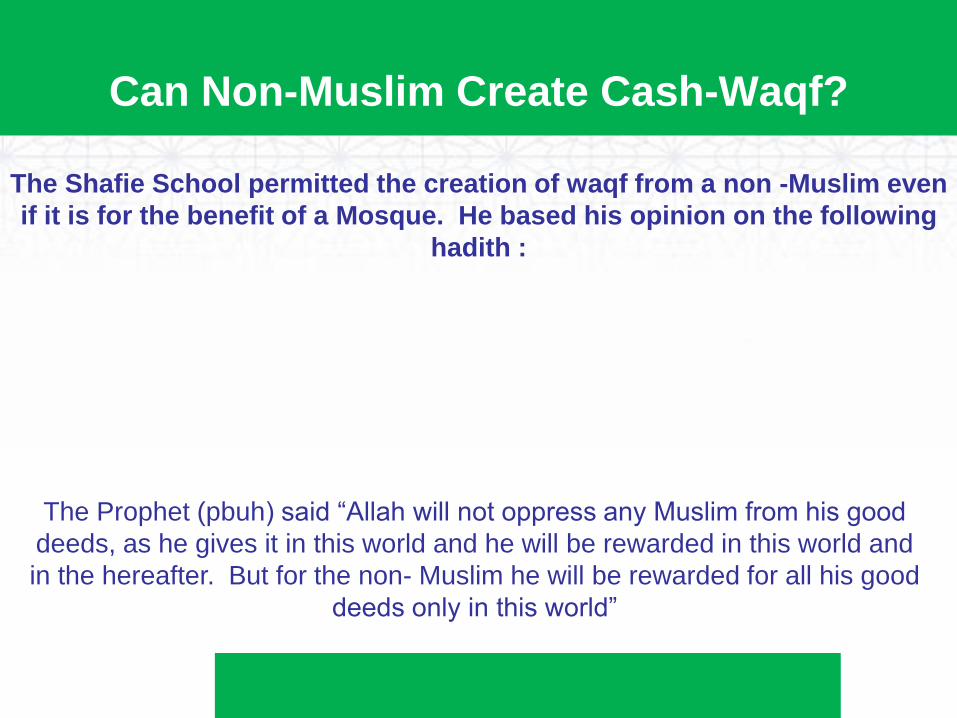

Can Non-Muslim Create Cash-Waqf?

The Shafie School permitted the creation of waqf from a non -Muslim even

if it is for the benefit of a Mosque. He based his opinion on the following

hadith :

The Prophet (pbuh( said “Allah will not oppress any Muslim from his good

deeds, as he gives it in this world and he will be rewarded in this world and

in the hereafter. But for the non- Muslim he will be rewarded for all his good

deeds only in this world”

Waqf for Education

UNIVERSITI OXFORD, UK

UNIVERSITI AL- AZHAR, MESIR

UNIVERSITI Cambridge, UK

UNIVERSITI Harvard, USA

NOVOTEL MELAKA KUIS

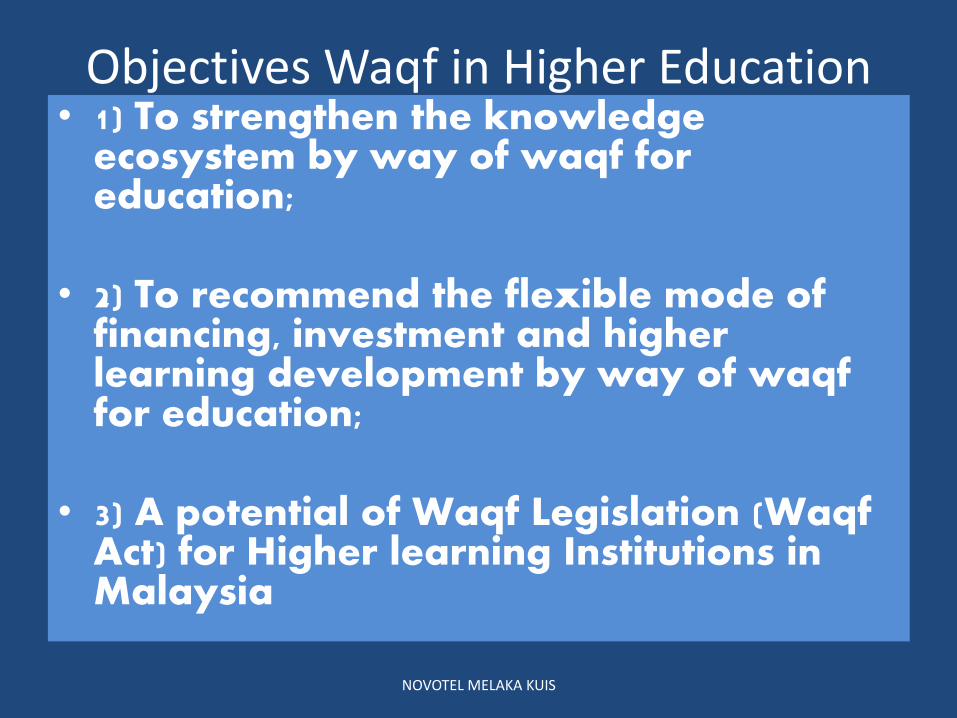

Objectives Waqf in Higher Education • 1) To strengthen the knowledge

ecosystem by way of waqf for education;

• 2) To recommend the flexible mode of financing, investment and higher learning development by way of waqf for education;

• 3) A potential of Waqf Legislation (Waqf Act) for Higher learning Institutions in Malaysia NOVOTEL MELAKA KUIS

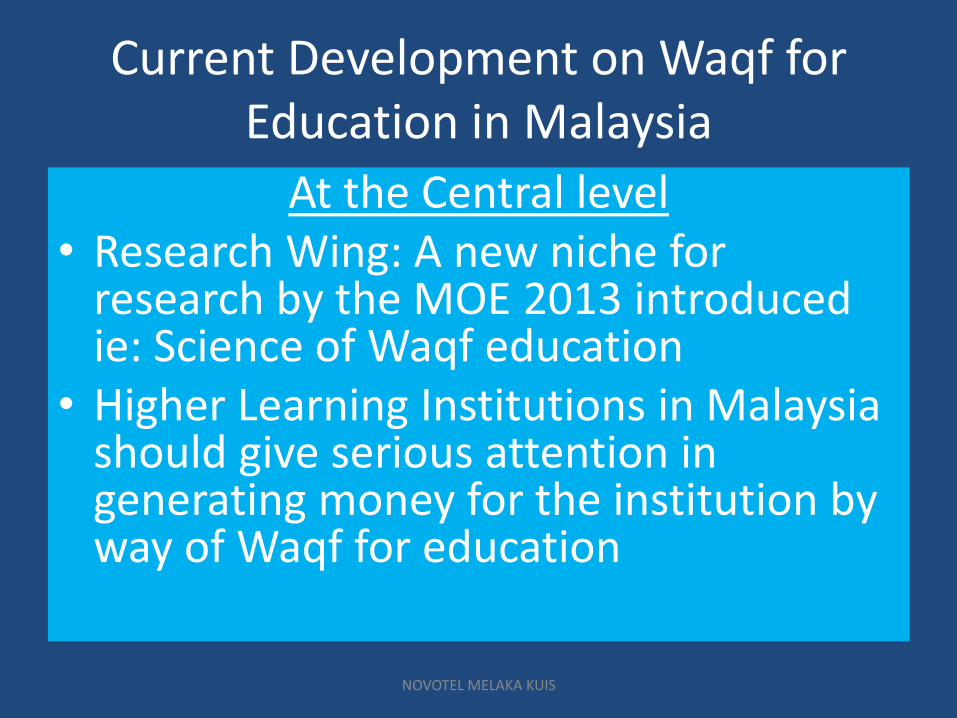

Current Development on Waqf for Education in Malaysia

At the Central level • Research Wing: A new niche for

research by the MOE 2013 introduced ie: Science of Waqf education

• Higher Learning Institutions in Malaysia should give serious attention in generating money for the institution by way of Waqf for education

NOVOTEL MELAKA KUIS

Transformation of the Role of Waqf in Higher Learning Institutions in

Malaysia “the inter agencies codification system for waqf in Malaysia

The accommodation for students of Higher learning inst by way of waqf

The need of waqf corporate to

strengthen the ecosystem of

knowledge Strategic Planning and entrepreneurship invites the waqf for education

Holistic model for financing and investment for Universities trough Waqf concept

Waqf concept redefined

NOVOTEL MELAKA KUIS

Rooms for Collaborations with Financial

Institutions

Waqf concept

redefined to

include waqf

for

education

Corporate

waqf and HEis

Investments FOR

Students

Entrep/SHIP

Financing &

Investments

Accomodation

Financing For

Students

A CODIFIED

SYSTEM FOR

DATA on WAQF

FOR MOE

2

1

3 5

6

4 NOVOTEL MELAKA KUIS

Future Collaborations between Higher Learning Institutions and Islamic Financial

Institutions on WAQF FOR EDUCATION

FINANCING AND INVESTING CONCEPT ON WAQF FOR THE DEVELOPMENT OF HIGHER LEARNING INSTITUTIONS

Islamic Financial

Institutions –

Mudharabah and

Musyarakah on the Endowment

fund for eg

The rules and procedures of

Shariah for the Waqf

instruments in the context of

education

NOVOTEL MELAKA KUIS

NOVOTEL MELAKA KUIS

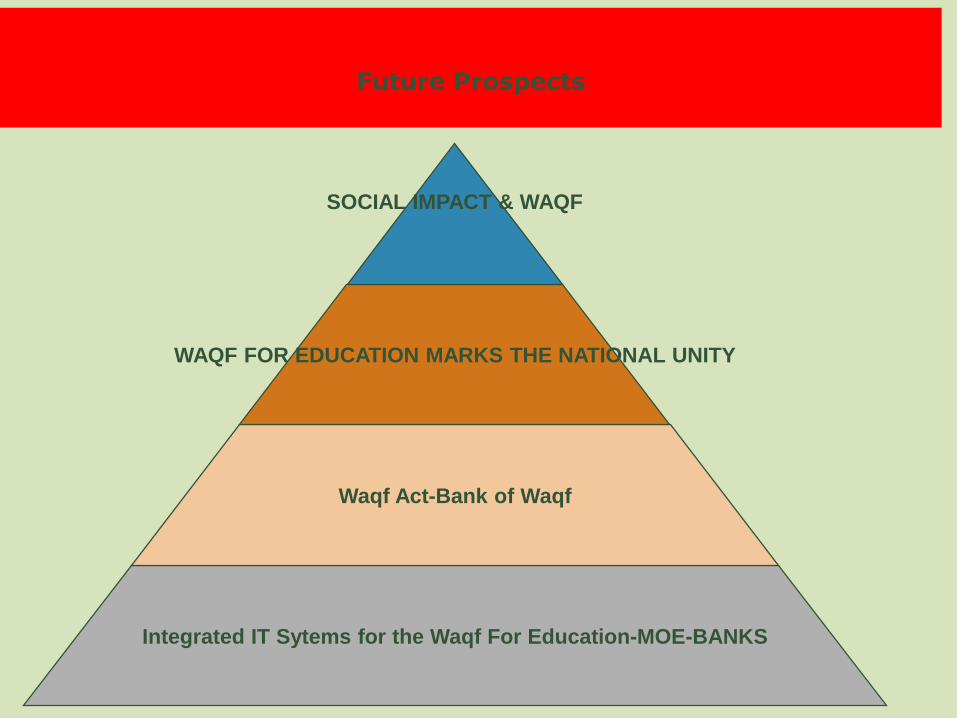

Future Prospects

Integrated IT Sytems for the Waqf For Education-MOE-BANKS

Waqf Act-Bank of Waqf

WAQF FOR EDUCATION MARKS THE NATIONAL UNITY

SOCIAL IMPACT & WAQF

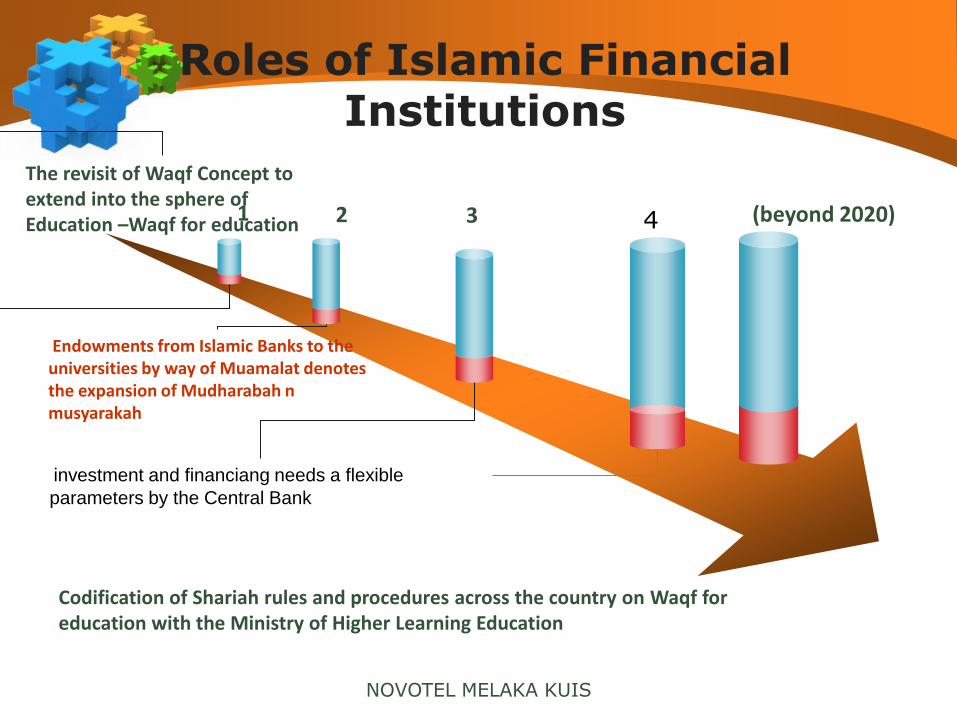

Roles of Islamic Financial Institutions

1 2 3 (beyond 2020)

The revisit of Waqf Concept to extend into the sphere of Education –Waqf for education

Endowments from Islamic Banks to the universities by way of Muamalat denotes the expansion of Mudharabah n musyarakah

investment and financiang needs a flexible

parameters by the Central Bank

Codification of Shariah rules and procedures across the country on Waqf for education with the Ministry of Higher Learning Education

4

NOVOTEL MELAKA KUIS

The issues are: 1. The clarification on how to develop the waqf according to the Islamic scholar's opinion (Shariah issues); 2. Legislation obstacles (Legal issues); and 3. The problem of Baitul Mal's administration that is inefficient and unsystematic (human resources and management issues).

NOVOTEL MELAKA KUIS

Methods of Development

: 1. Credit based finance; 2. Joint venture or equity and income sharing; and 3. Self-financing.

NOVOTEL MELAKA KUIS

Waqf & Islamic Finance

NOVOTEL MELAKA KUIS

•Integrating Waqf with the Financial Sector

•While there are different issues related to

development of waqf, here we examine how it

can benefit by integrating with the financial

sector

Waqf and the financial sector

•Demand side (input to waqf)

•Supply side (output from waqf)

Waqf and Demand for Services from the Financial

Sector

NOVOTEL MELAKA KUIS

•

Inputs for development of waqf institutions

•Financing

•Financing from financial institutions (FIs)

•Financing from raising funds from the market

•Management Services

•Issues in financing

•The benefit from waqf asset should continue

•Cannot use waqf asset as collateral

•Cannot sell waqf asset

Financing from FIs

NOVOTEL MELAKA KUIS

•

Like any other enterprise, waqf assets can be

developed by investments

•Example Awqaf Properties Investment Fund

•An entity financing the development of awqaf

properties worldwide

•Came up with innovative financing mechanism

(Built-Operate-Transfer)

Waqf Financing Through Sukuk

NOVOTEL MELAKA KUIS

•Cannot sell waqf assetcannot issue ijarah

sukuk

•Sukuk al IntifaaZamzam Towers in Makkah

•Waqf land leased land to Binladin Group for 28

years to build complex (4 towers, mall

hotel)

•Bin laden leased the project to Munshaat Real

Estate Projects for 28 years

•Manshaat raised 390 million issuing sukuk al

intifaa (time-share bond) for 24 years by selling

usufruct rights

Waqf Financing Through Sukuk (2)

NOVOTEL MELAKA KUIS

•SingaporeMusharakah sukuk used to raise

60

million to develop 2 projects

•Waqf provided the land, the investors (sukuk

holders) provided the funds for investment,

and Warees managed the project.

•In one case, a new mosque was built with

attached commercial property earning 200,000

annually

Services Provided by Waqf

Management Organization

NOVOTEL MELAKA KUIS

1.Services of Mutawalli

2.Custody Services

3.Estate Management Services

4.Investment Management

Services

5.Advisory Services

NOVOTEL MELAKA KUIS

NOVOTEL MELAKA KUIS

MANAGEMENT OF WAQF FUND

CASH WAQF DONATION FROM PUBLIC/INDIVIDUAL/COOPERATIVE/COMPANY

(All cash Waqf to Selangor Waqf Corporation are entitle tax relief under sub-section 44(6) of Income Tax ACT 1967.Allowable deductions from Income

Aggregates for Individual/ Cooperative (7%) and Company(10%). However Cooperative also entitle tax relief by paying dividend under section 65A &

65B.Original official MAIS receipt must be submitted for tax declaration).

AIR RITHS WAQF AIRLINE’S FUND

MANAGED

BY

PWS

70%

DIRECT COST FOR AIRLINE

OPERATION

MAINTENANCE LEASING OF AIRCRAFT

TAX FUEL

30%

OPERATION COST & OTHERS

HUMAN CAPITAL OFFICE RENTAL

OTHERS

34 AN INNITIATIVE BY SELANGOR WAQF CORPORATION / PERBADANAN WAKAF SELANGOR

THE FIRST AIRLINE OF WAQF CONCEPT

This fund is managed through joint management committee (JMC) comprised of Selangor Wakaf

corporation reps & Air Rith‟s Rep

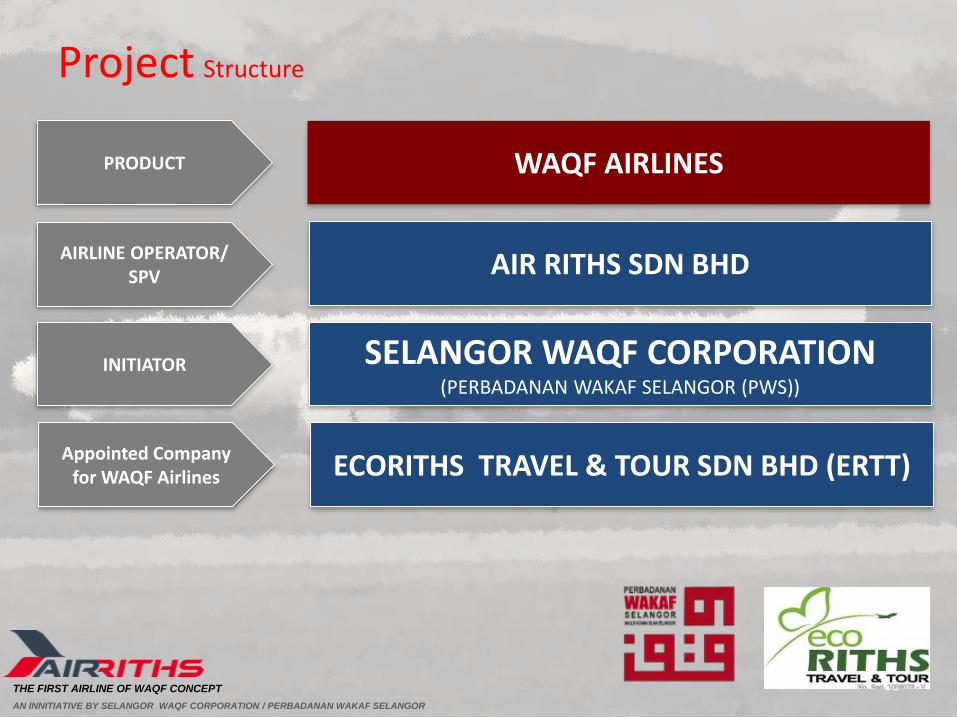

WAQF AIRLINES

AIR RITHS SDN BHD

SELANGOR WAQF CORPORATION (PERBADANAN WAKAF SELANGOR (PWS))

PRODUCT

AIRLINE OPERATOR/ SPV

INITIATOR

ECORITHS TRAVEL & TOUR SDN BHD (ERTT) Appointed Company

for WAQF Airlines

Project Structure

35 AN INNITIATIVE BY SELANGOR WAQF CORPORATION / PERBADANAN WAKAF SELANGOR

THE FIRST AIRLINE OF WAQF CONCEPT

THANK YOU

NOVOTEL MELAKA KUIS