update on vermont health care reform implementation sci winter meeting february 7-8, 2008 nashville,...

TRANSCRIPT

Update on Vermont Health Care Update on Vermont Health Care Reform ImplementationReform Implementation

SCI Winter Meeting

February 7-8, 2008Nashville, TN

Susan W. Besio, Ph.D.

Director of Health Care Reform

Vermont Agency of Administration

22

Vermont Data 2005 – The UninsuredVermont Data 2005 – The Uninsured10% of Vermonters, 5% of Vermont children10% of Vermonters, 5% of Vermont children

An 1.4% increase in the rate of uninsured since 2000

51% are eligible for Medicaid-related programs but not enrolled

Traditional Medicaid – up to 100% FPL

Dr. Dynasaur – Children in households up to 300% FPL

Vermont Health Access Plan (VHAP) – Adults up to 150% FPL and caretakers of dependent children up to 185% FPL

27% have household income between 150-185% and 300% FPL and are not eligible for a Medicaid program but cannot afford private insurance

69% have been without insurance for more than a year

33

Vermont Data 2005 – The UninsuredVermont Data 2005 – The Uninsured10% of Vermonters, 5% of Vermont children10% of Vermonters, 5% of Vermont children

77% reported cost as the main reason for being uninsured

30% of uninsured children and 40% of uninsured adults did not see a health care professional in past year

45% of uninsured children did not see a physician for routine care (compared to 7% of insured children) Much more likely to go to ER or urgent care (8.6% vs .7%)

25% of uninsured adults reported not seeking needed medical care due to cost

44

Assumptions of Effects of Uninsured Assumptions of Effects of Uninsured Vermonters on Health, Quality and CostVermonters on Health, Quality and Cost Un-reimbursed care increases private insurance

premiums via cost-shift- Makes insurance less affordable for Individuals, businesses

Fewer people are covered Benefits are decreased and/or employers / people choose

non-comprehensive plans to make plans affordable

People with comprehensive insurance coverage are more likely to participate in preventive care- Increases quality of life- Decreases cost of health care overall

55

Political Context for ReformPolitical Context for Reform

Governor (R) and Legislature (D) Shared Goals: Decrease the uninsured Control health care costs Focus on quality and prevention

Governor’s Parameters:• No increase on state’s tax burden as reform funding source• Public Program Cost Containment (no state-run single-payer; promoted

HSA/High Deductible Plan as new offering)• Support for Existing Employer-based Insurance System• Focus on Prevention via public health programs

Legislature’s Desires:• Government-run new coverage program as step towards single payer• Possible Individual Mandate• Comprehensive, affordable coverage to get at prevention

66

Political Context for ReformPolitical Context for Reform Final Compromises in Acts 191, 191

• Legislature compromised on:Private Insurance plan with state subsidies caveat of reviewing

viability in 2009 to trigger state-risk productDelayed Individual Mandate (if uninsured rate < 96% by 2010) Support of Employer-based system via ESI Premium Assistance

• Governor compromised on:Support of comprehensive, low cost-sharing coverage as new planEmployer Assessment and Tobacco taxes as reform funding

sources

• Both Supported:Blueprint for Health for Prevention and Chronic Care ManagementHealth ITAdministrative Simplification

77

Health Care Reform GoalsHealth Care Reform Goals

Increase Access Improve Quality

Contain Costs

35+ Initiatives in initial reform

legislation (2006)

88

Vermont’s New Coverage PlansVermont’s New Coverage Plans((in bluein blue))

Medicaid VHAP Catamount

Dr. Dynasaur

Catamount or ESI Premium Assistance

or ESI Premium

Assistance

150%-185%100% + other criteria

150- 185% 300%

Health

Income Eligibility: Federal Poverty Level

99

New Catamount HealthNew Catamount Health PlansPlans A non-group insurance product for uninsured Vermont

residents

Offered as a preferred provider organization plan by BCBS-VT and MVP, beginning October 1, 2007

Is required to be a comprehensive insurance package covering:

• Primary care• Preventative care• Acute episodic care• Chronic care• Hospital services • Pharmaceutical coverage

Individuals may choose which insurer they would like to use.

1010

Catamount Health: Catamount Health: Low Cost - SharingLow Cost - Sharing

LEGISLATIVELY-MANDATED COST-SHARING

Deductibles: In-Network: Out-of-Network: $250/individual $500/individual

$500/family $1,000/family

Co-Payment: $10/office visit

Prescription Drugs: No deductible Co‑payments: $10 generic drugs

$30 drugs on preferred drug list $50 non-preferred drugs

Preventive Care & Chronic Care*: $0 Not subject to deductible, co-insurance, co-

payments

Out-of-Pocket Maximum: In-Network: Out-of-Network: (excluding Premium) $800/individual $1,500/individual

$1,600/family $3,000/family

* For people enrolled in Chronic Care Management Program

1111

Catamount Health EligibilityCatamount Health Eligibility You can purchase Catamount Health if you are an uninsured Vermont

resident, are 18+, and are not eligible for an Employer-Sponsored Insurance (ESI) plan *

Uninsured means:• You have not had private insurance for the past 12 months

• You had VHAP or Medicaid but became ineligible for those programs

• You had private insurance but lost it because you: Lost your job Got divorced Had insurance through someone else who died Are no longer a dependent on your parent’s insurance Graduated, took a leave of absence, or finished college or

university and got your insurance through school No longer have COBRA coverage

* You can purchase Catamount Health even if you are eligible for an ESI plan IF you have an income under 300% FPL

1212

Premium AssistancePremium Assistance Catamount Health

• For people with income less than or equal to 300% Federal Poverty Level (FPL) - $31,350 for one person

Employer-Sponsored Insurance (ESI)• For people with income less than or equal to 300% FPL who are

eligible for Catamount Health or VHAPMust be more cost effective for the state

• ESI plans must be comprehensive and affordable Affordable = maximum individual in-network deductible of $500Comprehensive = covers physician, inpatient care, outpatient,

prescription drugs, emergency room, ambulance, mental health, substance abuse, medical equipment/supplies, and maternity care

Employers do not have to contribute to the plan for it to qualify

1313

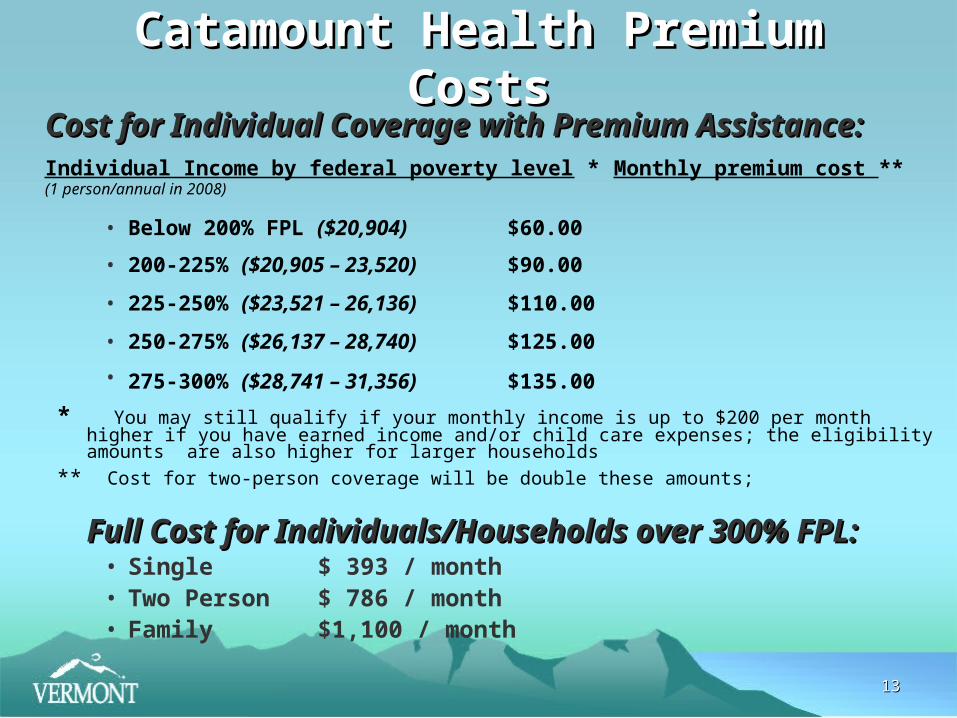

Catamount Health Premium CostsCatamount Health Premium CostsCost for Individual Coverage with Premium Cost for Individual Coverage with Premium

Assistance:Assistance:Individual Income by federal poverty level * Monthly premium cost **

(1 person/annual in 2008)

• Below 200% FPL ($20,904) $60.00

• 200-225% ($20,905 – 23,520) $90.00

• 225-250% ($23,521 – 26,136) $110.00

• 250-275% ($26,137 – 28,740) $125.00

• 275-300% ($28,741 – 31,356) $135.00

* You may still qualify if your monthly income is up to $200 per month higher if you have earned income and/or child care expenses; the eligibility amounts are also higher for larger households

** Cost for two-person coverage will be double these amounts;

Full Cost for Individuals/Households over 300% FPL:Full Cost for Individuals/Households over 300% FPL:• Single $ 393 / month• Two Person $ 786 / month• Family $1,100 / month

1414

Outreach and EnrollmentOutreach and Enrollment Integrated Medicaid, Catamount Outreach and Enrollment

Strategies• Aggressive Marketing and Education Campaign in Fall 2007

• 1-800 number

• New web-site

• Using state and local staff, partners and volunteers

• Delayed Hard Launch (1 month) to identify and resolve implementation issues

New Over-arching Brand:

Green Mountain Care – a healthier state of living

Re-tooling of Existing Application and Enrollment Processes

Phased-in New IT systems

1515

1616

1717

1818

1919

Marketing ResultsMarketing ResultsWeb Hits and Number of Visits

Web Hits/Number of

Visits

Dates Total Increa

se

Percentage Increase

3 weeks prior to launch (Oct. 11-31)

3 weeks post launch (Nov. 1-21)

Web Hits 69,039 348,117279,07

8404%

Number of Visits 1,747 8,005 6,258 358%

Comparison of Calls to Hotline Pre- and Post-Launch

DatesTotal

IncreasePercentage

Increase

Week prior to launch (Oct. 25-31)

6,528

Week of launch (Nov. 1–7)9,834

3,306 51%

2 weeks prior to launch (Oct. 18-31)13,729

2 weeks post launch (Nov. 1-14)

18,8015,072 37%

3 weeks prior to launch (Oct. 11-31)20, 783

3 weeks post launch (Nov. 1-21)

26,8066,023 29%

2020

Enrollment Results in First 3 MonthsEnrollment Results in First 3 Months

Comparisons to Estimates - FY08

Estimated Total Approved

Approved % of

Estimate

Enrolled as of

01/28/08

Enrolled % of

Estimate

Catamount Full Cost 1,447 220 11% 165 15%

CHAP 2,798 3,319 119% 1,818 65%

ESIA 656 907 138% 402 61%

2121

Financing of ReformsFinancing of Reforms Based on the principle that everybody is covered and

everybody pays:• Catamount Health Plan: individuals pay sliding scale

premiums based on income

• Employers pay an assessment based on number of uncovered employees

• Increases in tobacco taxes

• VHAP savings due to Employer-Sponsored Insurance (ESI) enrollment

• Matching federal dollars via Global Commitment 1115 waiverRequested CMS approval to 300% FPLReceived CMS approval to 200% FPLGovernor and Legislature agreed to contribute GF to bridge the

difference

2222

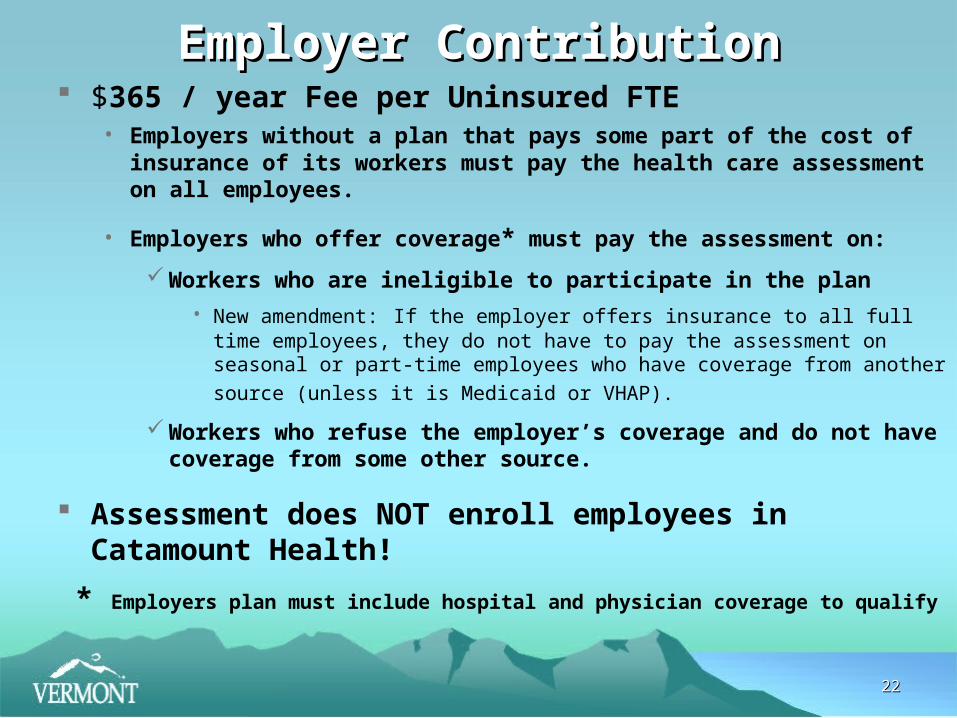

Employer ContributionEmployer Contribution $365 / year Fee per Uninsured FTE

• Employers without a plan that pays some part of the cost of insurance of its workers must pay the health care assessment on all employees.

• Employers who offer coverage* must pay the assessment on:

Workers who are ineligible to participate in the plan

• New amendment: If the employer offers insurance to all full time employees, they do not have to pay the assessment on seasonal or part-time employees

who have coverage from another source (unless it is Medicaid or VHAP).

Workers who refuse the employer’s coverage and do not have coverage from some other source.

Assessment does NOT enroll employees in Catamount Health!

* Employers plan must include hospital and physician coverage to qualify

2323

Challenges / Lessons LearnedChallenges / Lessons Learned Managing Expectations Estimates ≠ Reality, no matter

how many times you revise them • Estimating costs for new coverage plans• Estimating eligibles, take-up rates• Estimating revenues (ERISA limitations)

Where are the Feds? • Getting CMS approval for expansions• Recent CMS decision re: SCHIP, etc.

Managing Priorities, but which one?• Goal: 96% insured vs. available state funds for Medicaid programs

(50% of uninsured eligible for existing Medicaid programs)• Catamount Fund (new revenue sources, sacred) vs. Medicaid

programs (state funds dependent)

2424

Challenges / Lessons LearnedChallenges / Lessons Learned Managing Expectations Part 2 What is Catamount

Health? • Market Product vs. Entitlement Program vs. Public Policy vs. Cost

Control?• Example: Pre-existing Conditions (pregnancy, HIV-Aids, Cancer, etc.)

Competing issues: Adverse Selection, Increased Premiums, Promoting Early Care to avert later high costs overall

Managing Priorities Part 2 What about Everyone Else?• Catamount Health Changes introduced in legislation

Reduce or Eliminate12 Month Waiting PeriodExpand Categories of 12 month exemptions

– All people who expend more than 10% of income on health care – All Agricultural workers !

• Affordability of Non-Group & Small Group / Association MarketsNew Product or Reform to Existing Market?

2525

Challenges / Lessons LearnedChallenges / Lessons Learned Legislation (It and They Never Stop!)

• 2006 Health Care Affordability Acts (Acts 190, 191)Common Sense Initiatives (Appropriations Bill)Safe Staffing and Quality Patient Care (Act 153)

• 2007Corrections and Clarifications to the Health Care Affordability Acts of

2006 (Act 70)An Act relating to Ensuring Success in Health Care Reform (Act 71)

• 2008 Focus Eligibility Expansions for Catamount HealthNew Programs for the Underinsured, Small BusinessesIndividual, Small Group / Association Market ReformsFocus on Obesity and Public Health Prevention

2626

For more information

Vermont Health Care Reform Web-site:

www.hcr.vermont.gov

Health Care Coverage Information:

www.GreenMountainCare.org

1-800-250-8427