uruguay. presentation schedule country profile uruguayan free trade zones tax and corporate regimes

TRANSCRIPT

URUGUAYURUGUAY

Presentation SchedulePresentation Schedule

Country ProfileCountry Profile

Uruguayan Free Trade Zones Uruguayan Free Trade Zones

Tax and Corporate RegimesTax and Corporate Regimes

UruguayUruguayGeneral OverviewGeneral Overview Population – 3,314 millionPopulation – 3,314 million Area – 173.215 km2Area – 173.215 km2 GDP 2006 – US$ 18,590 millions GDP 2006 – US$ 18,590 millions GDP per capita 2006 – US$ 5,812 GDP per capita 2006 – US$ 5,812 Annual growth rate – 7,0%Annual growth rate – 7,0% Unemployment (Sept. 2007) – 8,5%Unemployment (Sept. 2007) – 8,5% Common external tariff – 0 to 20%Common external tariff – 0 to 20% Exports 2006 - US$ 3,985 millionsExports 2006 - US$ 3,985 millions Exports 2007 – US$ 4,496 millionsExports 2007 – US$ 4,496 millions Imports 2006 – US$ 4,775 millionsImports 2006 – US$ 4,775 millions Imports 2007 – US$ 5,588 millionsImports 2007 – US$ 5,588 millions

Uruguay = Switzerland of Uruguay = Switzerland of the Americas…the Americas…

Social and Political BackgroundSocial and Political Background Quality of LifeQuality of Life

Security Security Distances Distances Pollution Pollution Close contact among peopleClose contact among people

Social Characteristics of our CommunitySocial Characteristics of our Community Small sized and homogenous populationSmall sized and homogenous population Sophisticated, trained and qualified workforceSophisticated, trained and qualified workforce High literacy levelsHigh literacy levels One child, one PC One child, one PC

Political Reasons Political Reasons Tradition of democracyTradition of democracy StabilityStability

Economic Policy of the Economic Policy of the Uruguayan Governments Uruguayan Governments

over the Last Three over the Last Three DecadesDecades • Market economy Market economy

• Free inflow and outflow of foreign currency Free inflow and outflow of foreign currency • No exchange rate controlsNo exchange rate controls• Bank secrecy protectionBank secrecy protection

• No foreign investment registryNo foreign investment registry• Equal treatment to foreign Equal treatment to foreign

investors guaranteed by lawinvestors guaranteed by law

Legal PerspectiveLegal PerspectiveSophisticated legal systemIndependent judicial systemEnforceability of foreign rulings and

awardsEnforceability of contracts on foreign

currencyNo taxes on foreign sourced

incomeMERCOSURInvestment Promotion Act

Investment climateInvestment climate: B+ : B+ grade (Standard and grade (Standard and Poors - 3 March 2008)Poors - 3 March 2008)

Currently Growing Currently Growing SectorsSectors

Pulp projects (BOTNIA, ENCE)Pulp projects (BOTNIA, ENCE)ForestryForestry

Agribusiness (meat, wool and soybean) Agribusiness (meat, wool and soybean) Real EstateReal EstateCall CentersCall Centers

Transparency Transparency International 2006International 2006

Source: Source: www.transparency.orgwww.transparency.org

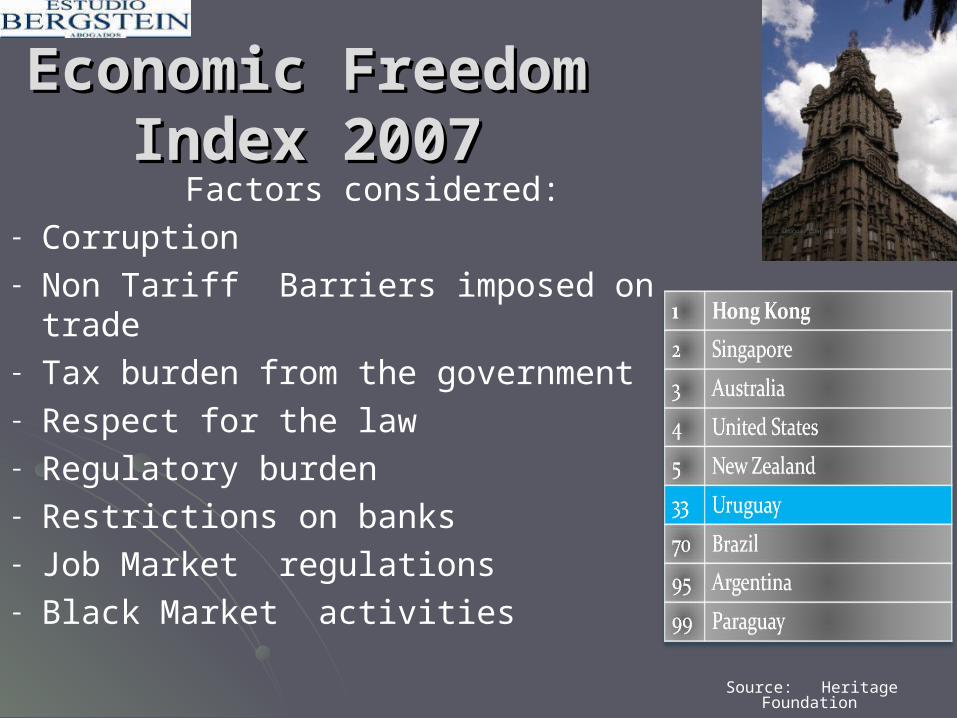

Economic FreedomEconomic FreedomIndex 2007Index 2007

Source: Heritage Foundation

Factors considered:- Corruption- Non Tariff Barriers imposed on trade- Tax burden from the government- Respect for the law- Regulatory burden- Restrictions on banks- Job Market regulations- Black Market activities

Democracy IndexDemocracy Index

Source: The EconomistSource: The Economist

The Economist – “The World in 2007”

Survey on Democracy around the world

Fu

ll D

em

ocra

cies

Fla

wed

D

em

ocra

cies

5 Categories:1. Electoral

process and pluralism

2. Functioning of government

3. Political participation

4. Political culture

5. Civil liberties

HighlightsHighlights – Major Business – Major Business OpportunitiesOpportunities

Distribution and logistics center for the regionDistribution and logistics center for the regionMERCOSUR: HeadquartersMERCOSUR: HeadquartersMultiple tax incentives:Multiple tax incentives:

- Free ports- Free ports

- Industrial parks- Industrial parks

- Software - Software

- Free trade zones- Free trade zones

URUGUAYAN FREE URUGUAYAN FREE TRADE ZONES (FZ)TRADE ZONES (FZ)

Uruguayan Free ZonesUruguayan Free Zones

I. ConceptI. Concept

Areas excluded of customs territoryAreas excluded of customs territory

Uruguayan Free ZonesUruguayan Free Zones

II. LocationII. LocationRIVERARIVERA

MONTEVIDEOMONTEVIDEO

RIO NEGRORIO NEGRO

NUEVA NUEVA HELVECIAHELVECIA

COLONIACOLONIA

Uruguayan Free ZonesUruguayan Free Zones

III. Pulp ProjectsIII. Pulp Projects

BOTNIA and ENCE are FZBOTNIA and ENCE are FZ

Uruguayan Free ZonesUruguayan Free Zones

IV. ActivitiesIV. ActivitiesTrading hub in the region:Trading hub in the region:

- Financial servicesFinancial services- Bank Rep. OfficesBank Rep. Offices- Logistic providersLogistic providers- Trading operatorsTrading operators

- Call centersCall centers- Software development industriesSoftware development industries

Uruguayan Free ZonesUruguayan Free Zones

V. FZ UsersV. FZ UsersConceptConceptSpecial bylaws Special bylaws Agreement with a FZ operator Agreement with a FZ operator Filing with FZ BureauFiling with FZ BureauCustomer practice: acquisition of a shelf Customer practice: acquisition of a shelf

corporation corporation

Uruguayan Free ZonesUruguayan Free Zones

VI. Tax TreatmentVI. Tax TreatmentEntrance and exit of goods abroad are tax Entrance and exit of goods abroad are tax

exempted. exempted. Circulation of goods and services within the Circulation of goods and services within the

FZ is exempted from sales taxes. FZ is exempted from sales taxes. Sale of products into Uruguayan territory = Sale of products into Uruguayan territory =

import transaction. import transaction.

Uruguayan Free ZonesUruguayan Free Zones

VI. Tax TreatmentVI. Tax TreatmentRemittance of dividends abroad (by Users) is Remittance of dividends abroad (by Users) is

untaxed (as opposed to companies who are not untaxed (as opposed to companies who are not FZ operators).FZ operators).

Payment of technical assistance fee exempted.Payment of technical assistance fee exempted.Payment of interests to foreign entities Payment of interests to foreign entities

exempted.exempted.Payment of royalties abroad exempted.Payment of royalties abroad exempted.

Uruguayan Free ZonesUruguayan Free Zones

VII. RequirementVII. Requirement

At least 75% of the personnel employed by At least 75% of the personnel employed by the FZ Users must be native or legal the FZ Users must be native or legal

Uruguayan citizenUruguayan citizen

TAX AND CORPORATE TAX AND CORPORATE REGIMESREGIMES

Tax and Corporate Regimes Tax and Corporate Regimes

I. Tax AspectsI. Tax Aspects• Only locally sourced income is taxed.Only locally sourced income is taxed.• Corporations with no activity and assets in Corporations with no activity and assets in

Uruguay are subject to no taxation in Uruguay Uruguay are subject to no taxation in Uruguay except for an annual fixed duty of US$ 400 per except for an annual fixed duty of US$ 400 per year.year.

• Remittance of dividends abroad is exempted when Remittance of dividends abroad is exempted when the local company has no locally sourced income.the local company has no locally sourced income.

• Transfer of shares of an Uruguayan bearer share Transfer of shares of an Uruguayan bearer share corporation is exempted from non residents corporation is exempted from non residents income tax.income tax.

Tax and Corporate Regimes Tax and Corporate Regimes

II. Corporate AspectsII. Corporate Aspects

• Bearer shares corporations admitted. Bearer shares corporations admitted. • Single shareholder admitted. Single shareholder admitted. • Shareholders may be all foreign non residents, Shareholders may be all foreign non residents,

individuals or legal entities.individuals or legal entities.• Directors may be nationals or foreigners, Directors may be nationals or foreigners,

individuals or legal entities. One is sufficient.individuals or legal entities. One is sufficient.

Other Tax Structures Other Tax Structures

II. Corporate AspectsII. Corporate Aspects

• Transfer of the stock is effected by means of the Transfer of the stock is effected by means of the physical delivery of the stock certificate.physical delivery of the stock certificate.

• Shareholders Meetings may be gathered per Shareholders Meetings may be gathered per proxy.proxy.

• Re-domiciliation is possible (into Uruguay or Re-domiciliation is possible (into Uruguay or abroad).abroad).

• Holding companies expressly contemplated under Holding companies expressly contemplated under local legislation.local legislation.

Thank youThank you

ESTUDIO BERGSTEINESTUDIO BERGSTEIN