us and global economic review & forecast 2010

TRANSCRIPT

Client-tailored solutions for what’s next

Economic Review and Forecast

Summary presentation of e-forecasting.com’s outlook for US

and global economic conditionsFriday, October 15th, 2010

Client-tailored solutions for what’s next 04/18/23

2

Presentation Agenda

Overview of recession/rebound

Snapshot of current economic climate: stagnation?

Future outlook

Q&A

Client-tailored solutions for what’s next 04/18/23

3

Client-tailored solutions for what’s next 04/18/23

4

Stagnation Nation?

European style high unemployment Where is US economic dynamism? Good, Bad & Ugly Policies? Major Risks

Client-tailored solutions for what’s next 04/18/23

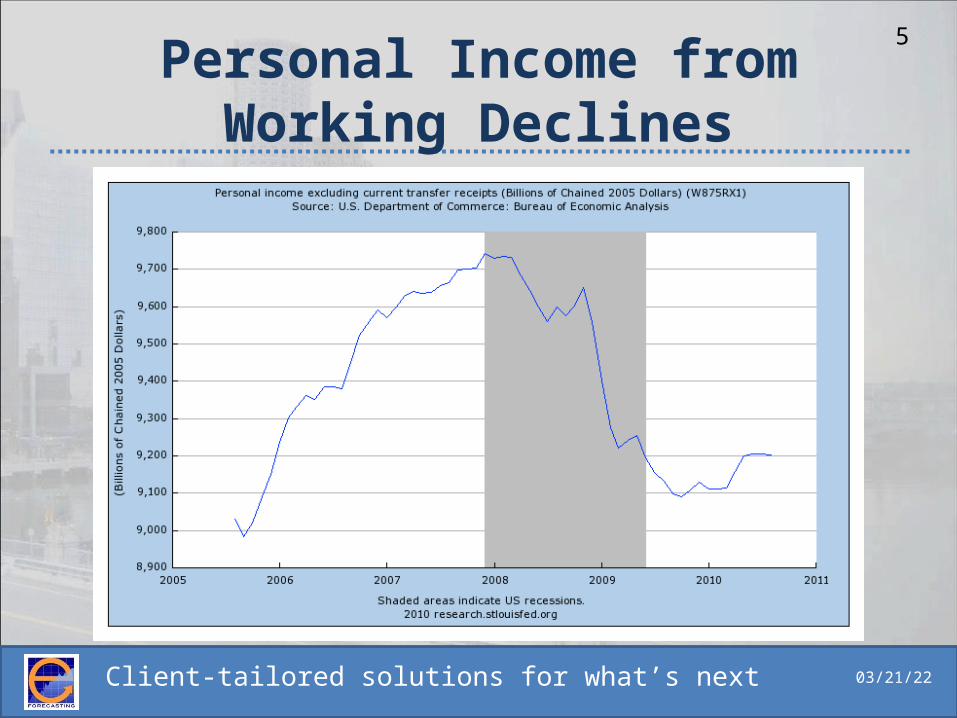

5Personal Income from

Working Declines

Client-tailored solutions for what’s next 04/18/23

6Policy-Makers, Advisers & the

Economy

The British Keynesian Recipes• Business is the problem, Government is the

solution

The American “School” (Monetarism)– Government is the problem, private sector is

inherently stable

Client-tailored solutions for what’s next 04/18/23

7Policy-Makers, Advisers & the

Economy

Effectiveness of Policies Peoples reaction & behavior Permanent Policies vs. Transitory (Las

Vegas style) policies Income or Wealth (assets) drives

behavior

Client-tailored solutions for what’s next 04/18/23

8

Current Risks

Ineffectiveness of low interest rates Deficits, Debts and Fear – The Greek

experience Running out of “others money” Free fall of the Dollar, panic, high

interest rates, a “real” depression Inflate the economy, fooling workers

and fixing the budget

Client-tailored solutions for what’s next 04/18/23

9

Client-tailored solutions for what’s next 04/18/23

10

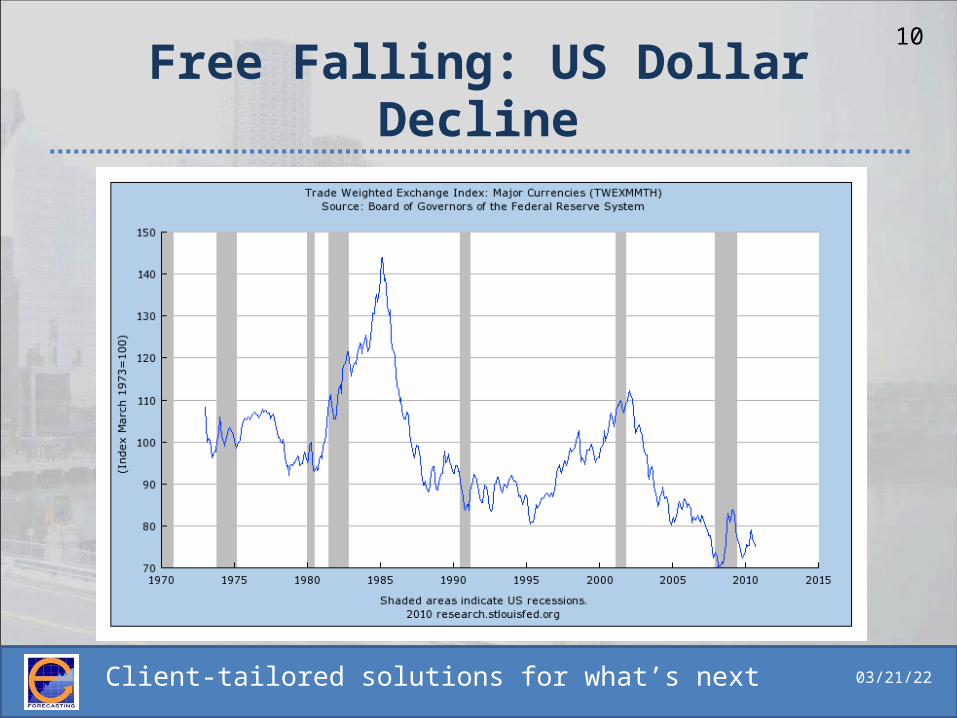

Free Falling: US Dollar Decline

Client-tailored solutions for what’s next 04/18/23

11

Fed in a printing mode again

Client-tailored solutions for what’s next 04/18/23

12

Real-Time Look @ Economy NOW

What is happening RIGHT now with the economy– US monthly GDP, current macro

components, policies, etc

Client-tailored solutions for what’s next 04/18/23

13

Real Time Monthly GDP

• e-forecasting estimates US monthly GDP increased 0.8% in September to $13,243B, after going up 2.4% in August

• Annual growth rate in the third quarter is estimated to be 1%

• Six-month growth rate, which signals confirmation of turning points, went up 1.8% in September, after going up 2.1% in August

$12,900

$13,000

$13,100

$13,200

$13,300

J F M Q1 A M J Q2 J A S Q3

Monthly GDP Up in September

BEA, Quarterly e-forecasting, Monthly

Client-tailored solutions for what’s next

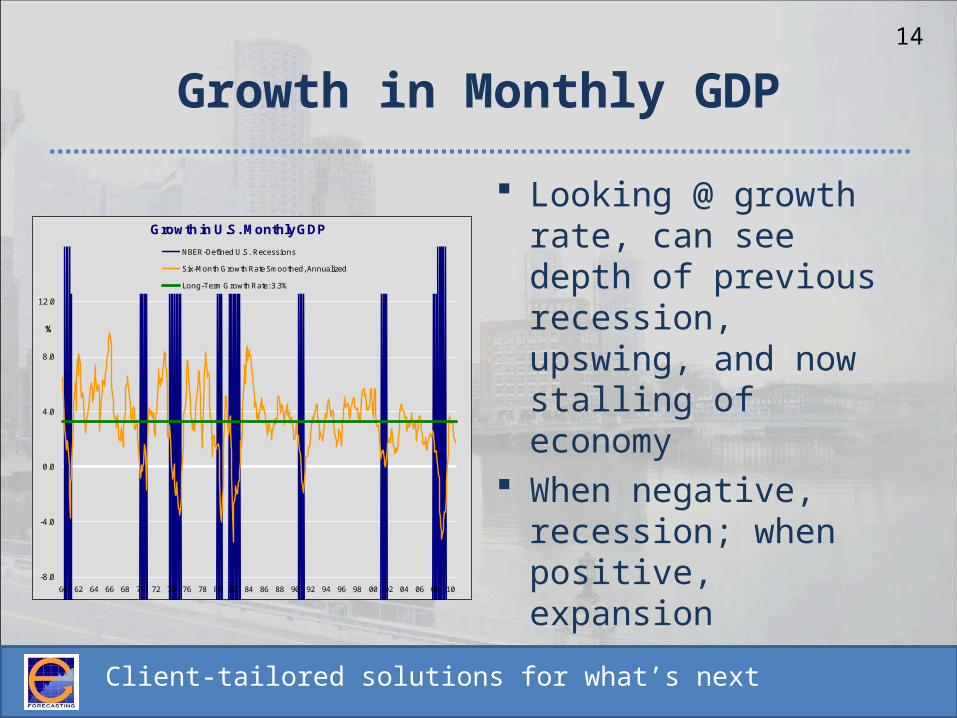

Growth in Monthly GDP

Looking @ growth rate, can see depth of previous recession, upswing, and now stalling of economy

When negative, recession; when positive, expansion

14

-8.0

-4.0

0.0

4.0

8.0

12.0

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

%

Growth in U.S. Monthly GDP

NBER-Defined U.S. Recessions

Six-Month Growth Rate Smoothed, Annualized

Long-Term Growth Rate: 3.3%

Client-tailored solutions for what’s next

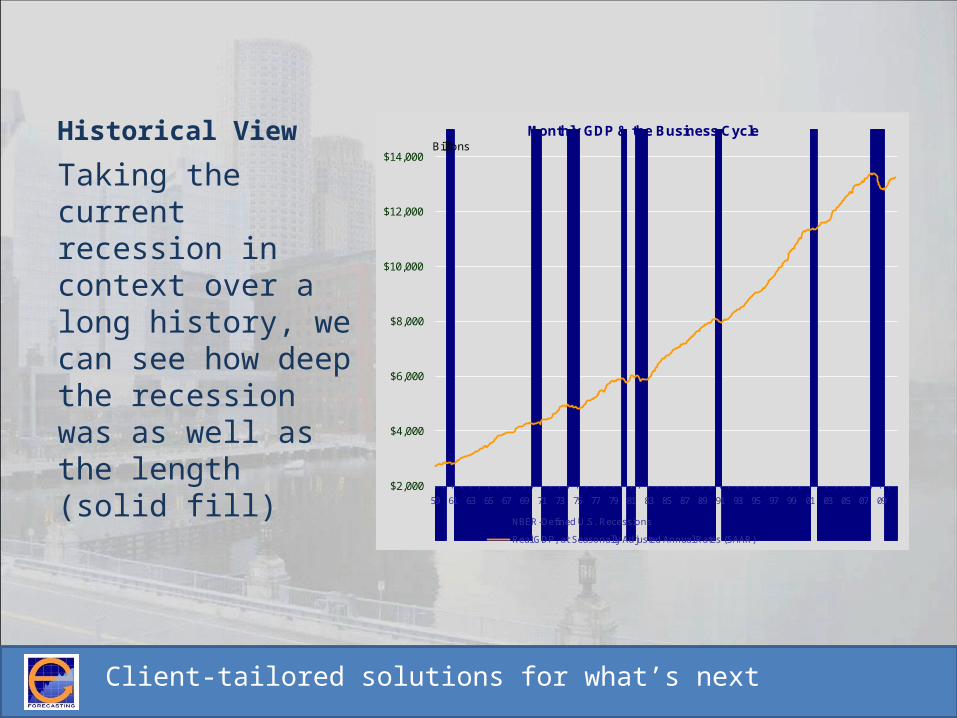

Historical View

Taking the current recession in context over a long history, we can see how deep the recession was as well as the length (solid fill)

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09

BillionsMonthly GDP & the Business Cycle

NBER-Defined U.S. Recessions

Real GDP, at Seasonally Adjusted Annual Rates (SAAR)

Client-tailored solutions for what’s next

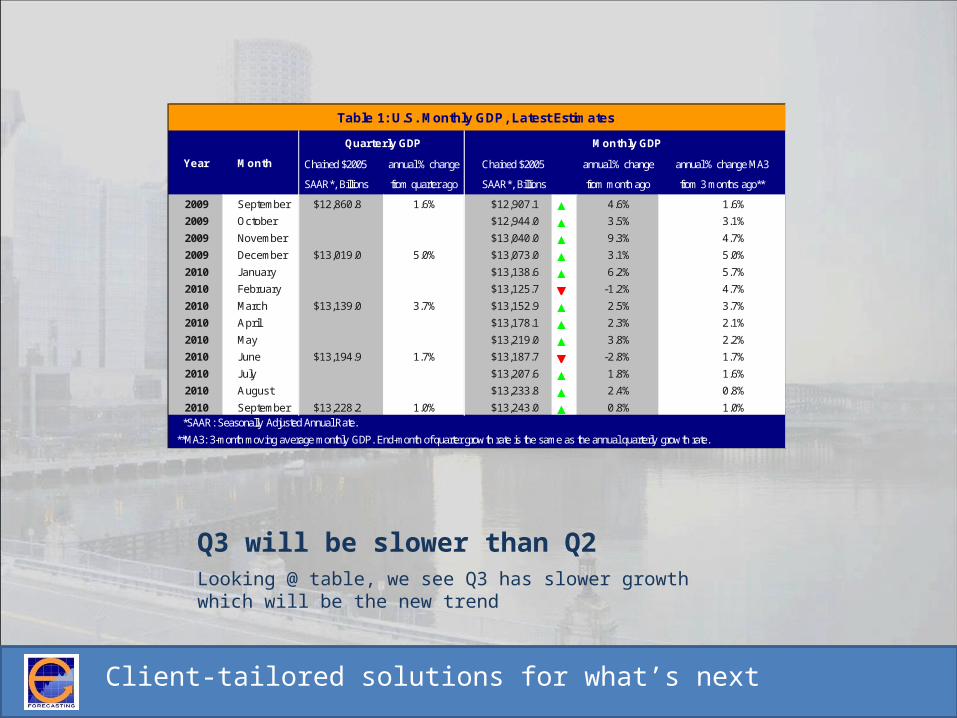

Q3 will be slower than Q2Looking @ table, we see Q3 has slower growth which will be the new trend

Chained $2005 annual % change annual % change annual % change MA3

SAAR*, Billions from quarter ago from month ago from 3 months ago**

2009 September $12,860.8 1.6% $12,907.1 ▲ 4.6% 1.6%

2009 October $12,944.0 ▲ 3.5% 3.1%

2009 November $13,040.0 ▲ 9.3% 4.7%

2009 December $13,019.0 5.0% $13,073.0 ▲ 3.1% 5.0%

2010 January $13,138.6 ▲ 6.2% 5.7%

2010 February $13,125.7 ▼ -1.2% 4.7%

2010 March $13,139.0 3.7% $13,152.9 ▲ 2.5% 3.7%

2010 April $13,178.1 ▲ 2.3% 2.1%

2010 May $13,219.0 ▲ 3.8% 2.2%

2010 June $13,194.9 1.7% $13,187.7 ▼ -2.8% 1.7%

2010 July $13,207.6 ▲ 1.8% 1.6%

2010 August $13,233.8 ▲ 2.4% 0.8%

2010 September $13,228.2 1.0% $13,243.0 ▲ 0.8% 1.0% *SAAR: Seasonally Adjusted Annual Rate.

Year

Quarterly GDP

Table 1: U.S. Monthly GDP, Latest Estimates

**MA3: 3-month mov ing av erage monthly GDP. End-month of quarter grow th rate is the same as the annual quarterly grow th rate.

Monthly GDP

Chained $2005

SAAR*, Billions

Month

Client-tailored solutions for what’s next 04/18/23

17

What’s Ahead?

Focus on manufacturing, inflation, other major factors

Global overview Exports/imports outlook

Client-tailored solutions for what’s next 04/18/23

18

Short-Term Outlook: US Lead

Using leading indicator helps with short-term forecast and turning point identification

US leading indicator has been slowing down last few months

Six month growth rate was negative for first time since May 09 in last report

0

20

40

60

80

100

120

59 63 67 71 75 79 83 87 91 95 99 03 07

© 2010 e-forecasting.com

e-forecasting Leading Economic Index

U.S. Recessions* eLEI, 2000=100

Client-tailored solutions for what’s next 04/18/23

19

Short-Term Outlook: US Lead

Six month growth rate was negative for first time since May 09 in last report

-20

-10

0

10

20

59 63 67 71 75 79 83 87 91 95 99 03 07

Expansion and Recession Signals from Growth in eLEI

Six-Month Growth Rate Smoothed, Annualized, in eLEI

U.S. Long-Term Growth Rate: 3.3%

Client-tailored solutions for what’s next 04/18/23

20US Leading indicator shows

double dip probabilities

4%

3%

3%

1%

19%

2%

1%

3%

32%

61%

52%

44%

0% 25% 50% 75% 100%

Oct-09

Nov-09

Dec-09

Jan-10

Feb-10

Mar-10

Apr-10

May-10

Jun-10Jul-10

Aug-10

Sep-10

Recession Probabilities

Client-tailored solutions for what’s next 04/18/23

21

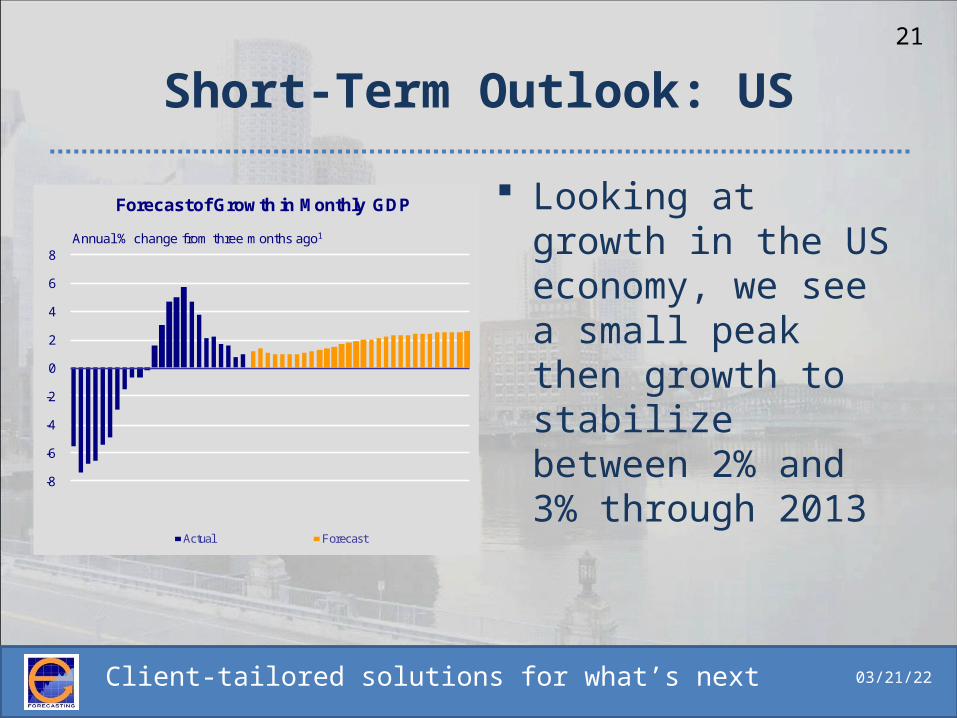

Short-Term Outlook: US

Looking at growth in the US economy, we see a small peak then growth to stabilize between 2% and 3% through 2013

-8

-6

-4

-2

0

2

4

6

8Annual % change from three months ago1

Forecast of Growth in Monthly GDP

Actual Forecast

Client-tailored solutions for what’s next 04/18/23

22

US Manufacturing

Manufacturing recovery will slow then continue, yet not reach peak of 06

80

85

90

95

100

105

00:Sep 02:Sep 04:Sep 06:Sep 08:Sep 10:Sep 12:Sep

Index, 2007=100

Manufacturing Production

Client-tailored solutions for what’s next 04/18/23

23

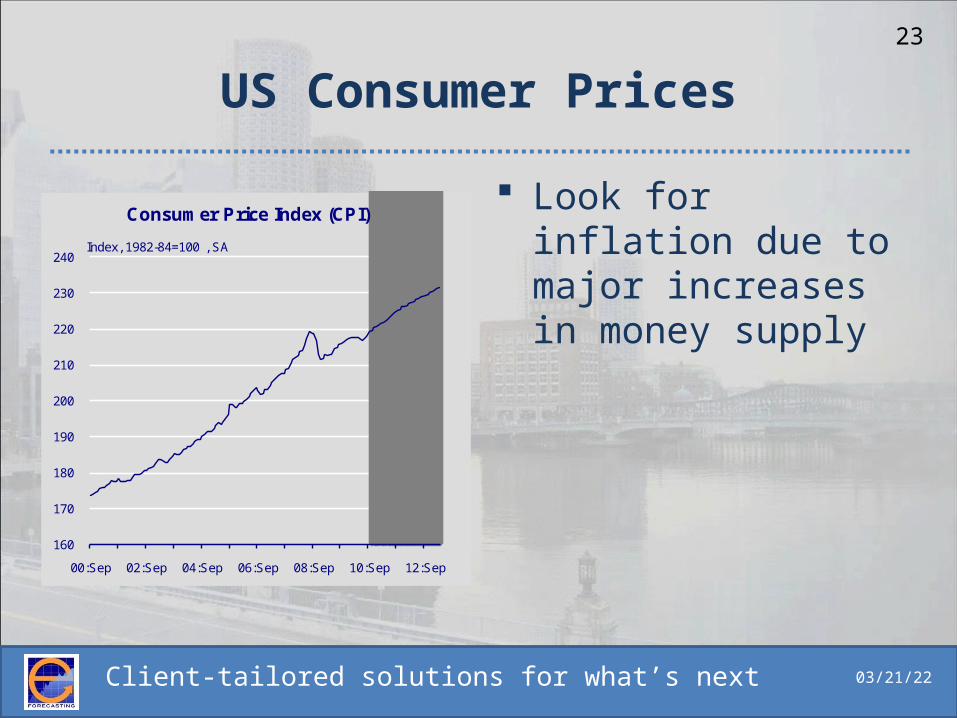

US Consumer Prices

Look for inflation due to major increases in money supply

160

170

180

190

200

210

220

230

240

00:Sep 02:Sep 04:Sep 06:Sep 08:Sep 10:Sep 12:Sep

Index, 1982-84=100 , SA

Consumer Price Index (CPI)

Client-tailored solutions for what’s next 04/18/23

24

US Durable Goods

Consumer expenditures on durable goods will continue to recover nearing $1,300 trillion at 2005 constant prices

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

00:Sep 02:Sep 04:Sep 06:Sep 08:Sep 10:Sep 12:Sep

In Billions, SAAR

Consumer Expenditures on Durables

Client-tailored solutions for what’s next 04/18/23

25

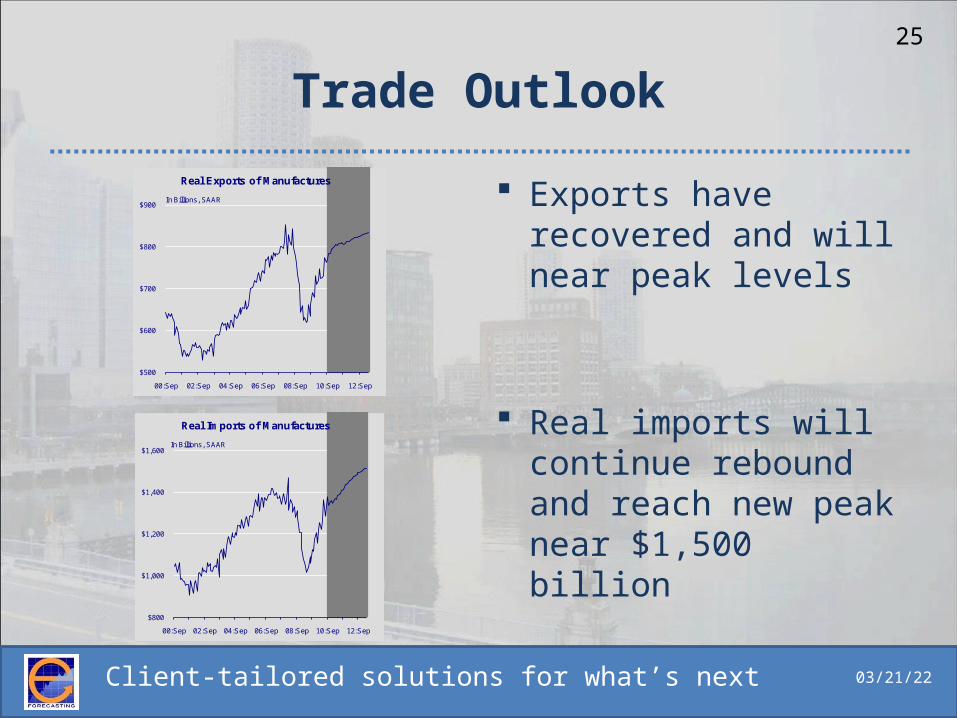

Trade Outlook

Exports have recovered and will near peak levels

Real imports will continue rebound and reach new peak near $1,500 billion

$500

$600

$700

$800

$900

00:Sep 02:Sep 04:Sep 06:Sep 08:Sep 10:Sep 12:Sep

In Billions, SAAR

Real Exports of Manufactures

$800

$1,000

$1,200

$1,400

$1,600

00:Sep 02:Sep 04:Sep 06:Sep 08:Sep 10:Sep 12:Sep

In Billions, SAAR

Real Imports of Manufactures

Client-tailored solutions for what’s next 04/18/23

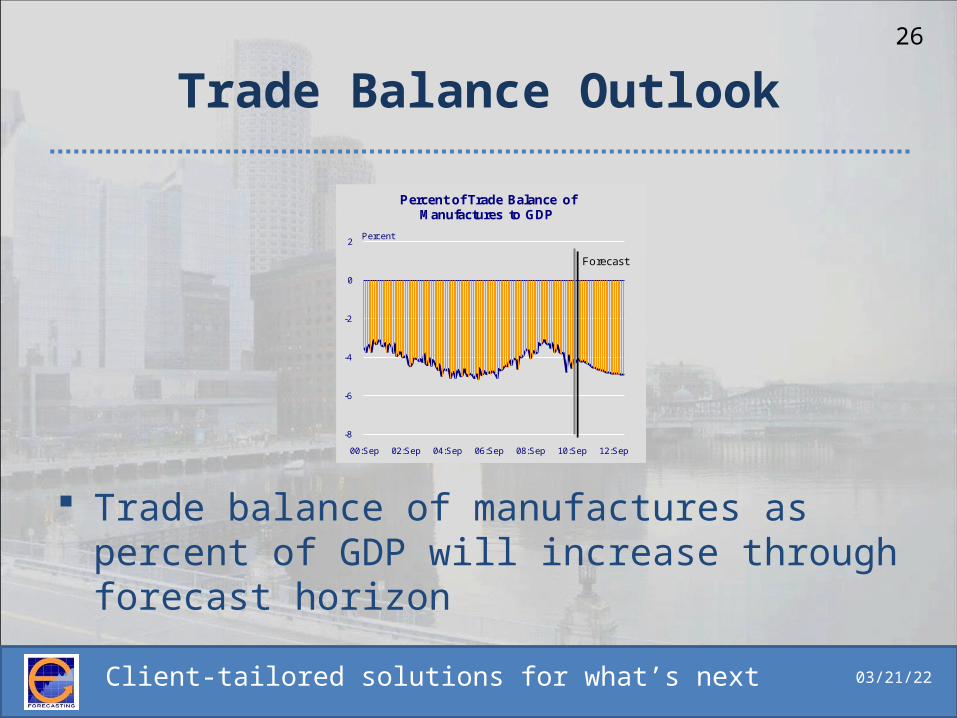

26

Trade Balance Outlook

Trade balance of manufactures as percent of GDP will increase through forecast horizon

-8

-6

-4

-2

0

2

00:Sep 02:Sep 04:Sep 06:Sep 08:Sep 10:Sep 12:Sep

Forecast

Percent

Percent of Trade Balance of Manufactures to GDP

Client-tailored solutions for what’s next 04/18/23

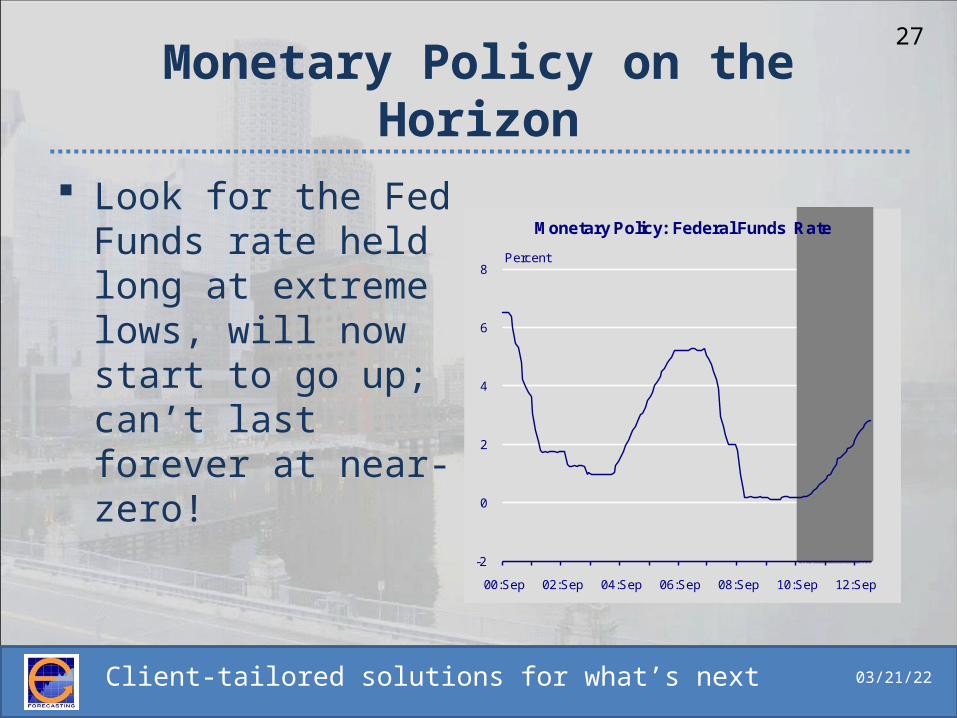

27Monetary Policy on the

Horizon Look for the Fed

Funds rate held long at extreme lows, will now start to go up; can’t last forever at near-zero!

-2

0

2

4

6

8

00:Sep 02:Sep 04:Sep 06:Sep 08:Sep 10:Sep 12:Sep

Percent

Monetary Policy: Federal Funds Rate

Client-tailored solutions for what’s next 04/18/23

28

Global Future Outlook

Looking @ major economic blocs and their leading indicators helps give an idea of turning points, which areas suffered more than others and which will come out of recession faster and stronger…

Client-tailored solutions for what’s next 04/18/23

29

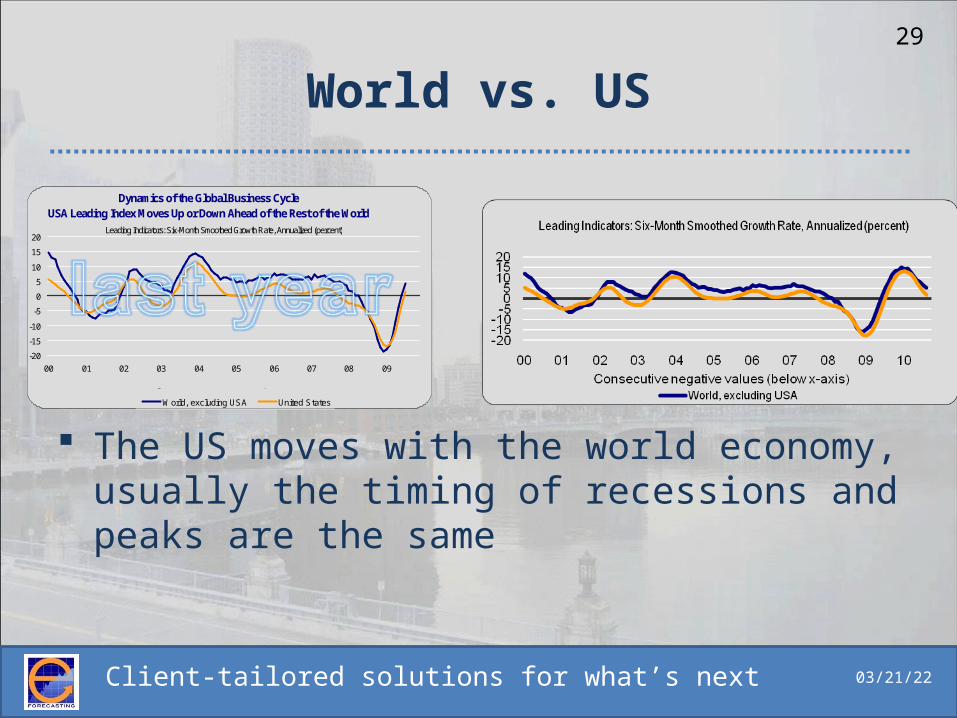

World vs. US

The US moves with the world economy, usually the timing of recessions and peaks are the same

Dynamics of the Global Business Cycle USA Leading Index Moves Up or Down Ahead of the Rest of the World

-20

-15

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

World, excluding USA United States

Consecutive negative values (below x-axis) predict recessions

Client-tailored solutions for what’s next 04/18/23

30

BRIC Attack

BRIC HAD been continually outperforming the world and USED TO move out of recession much faster

BRIC is now slowing down at same time and pace as the rest of the world

Early Warning Signals for Booms and Busts in BRIC Area

-20

-15

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

World BRIC Area

Consecutive negative values (below x-axis) predict recessions

Client-tailored solutions for what’s next 04/18/23

31

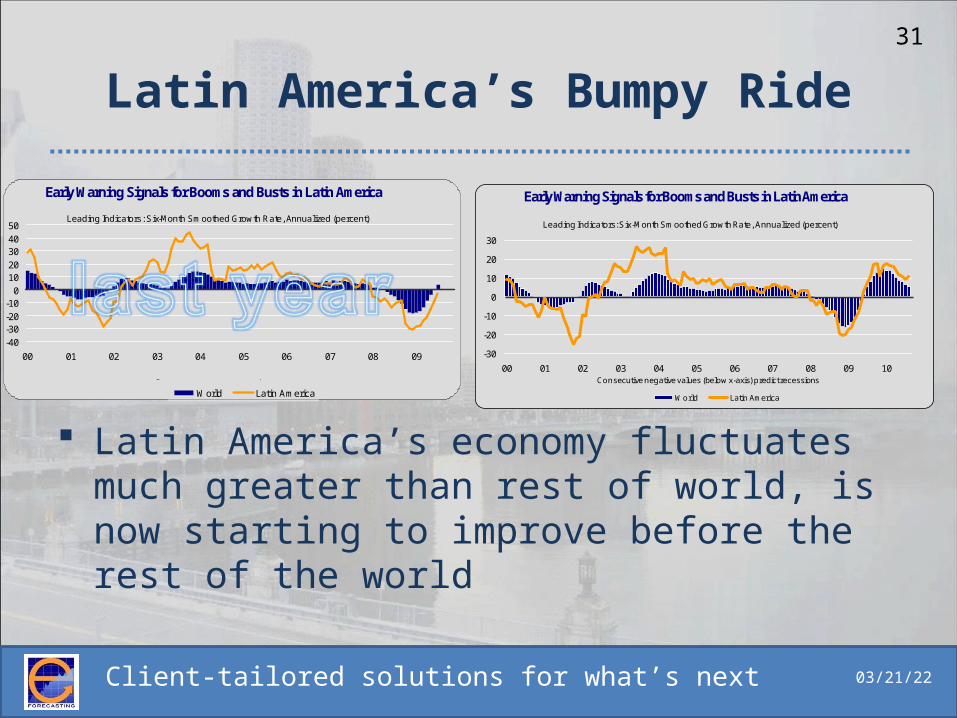

Latin America’s Bumpy Ride

Latin America’s economy fluctuates much greater than rest of world, is now starting to improve before the rest of the world

Early Warning Signals for Booms and Busts in Latin America

-40-30-20-10

01020304050

00 01 02 03 04 05 06 07 08 09

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

World Latin America

Consecutive negative values (below x-axis) predict recessions

-30

-20

-10

0

10

20

30

00 01 02 03 04 05 06 07 08 09 10

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

Early Warning Signals for Booms and Busts in Latin America

World Latin America

Consecutive negative values (below x-axis) predict recessions

Client-tailored solutions for what’s next 04/18/23

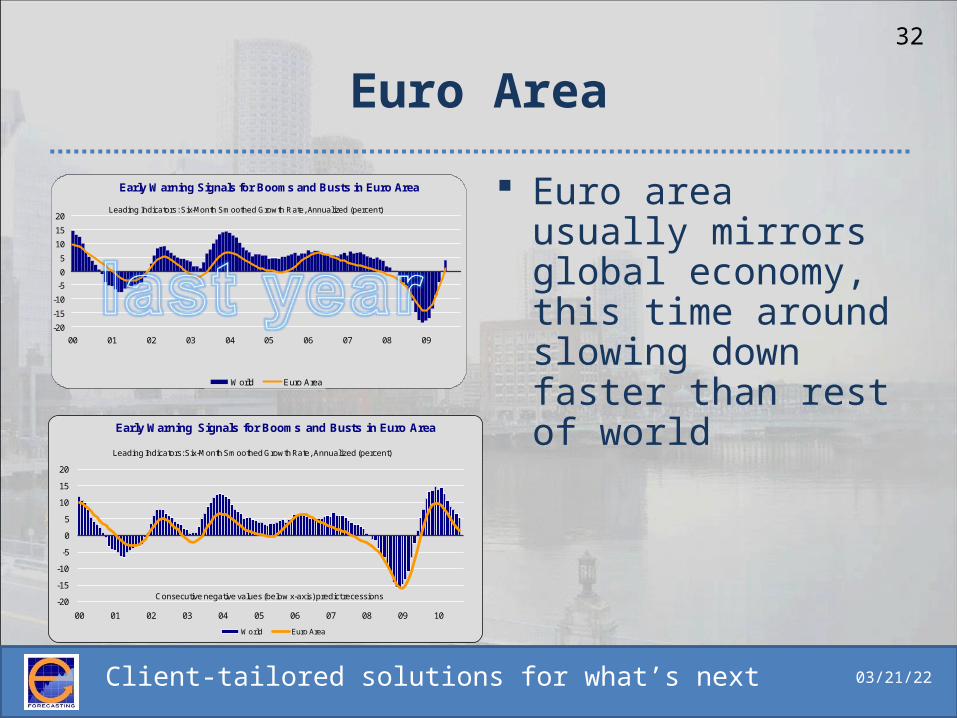

32

Euro Area

Early Warning Signals for Booms and Busts in Euro Area

-20

-15

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

World Euro Area

Consecutive negative values (below x-axis) predict recessions

Euro area usually mirrors global economy, this time around slowing down faster than rest of world

-20

-15

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09 10

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

Early Warning Signals for Booms and Busts in Euro Area

World Euro Area

Consecutive negative values (below x-axis) predict recessions

Client-tailored solutions for what’s next 04/18/23

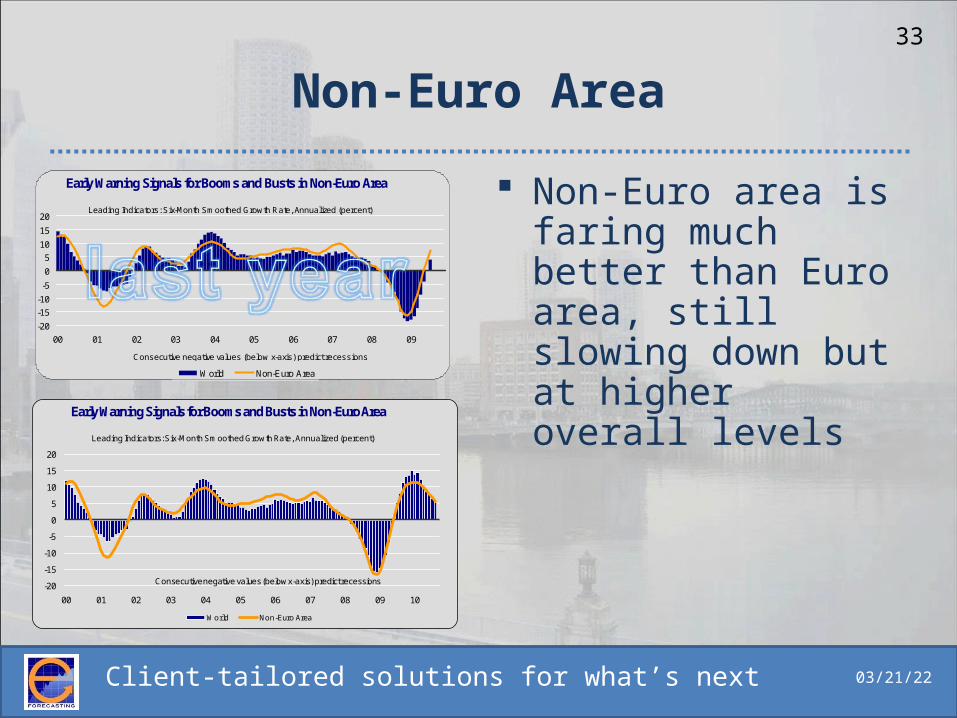

33

Non-Euro Area

Non-Euro area is faring much better than Euro area, still slowing down but at higher overall levels

Early Warning Signals for Booms and Busts in Non-Euro Area

-20

-15

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

World Non-Euro Area

Consecutive negative values (below x-axis) predict recessions

-20

-15

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09 10

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

Early Warning Signals for Booms and Busts in Non-Euro Area

World Non-Euro Area

Consecutive negative values (below x-axis) predict recessions

Client-tailored solutions for what’s next 04/18/23

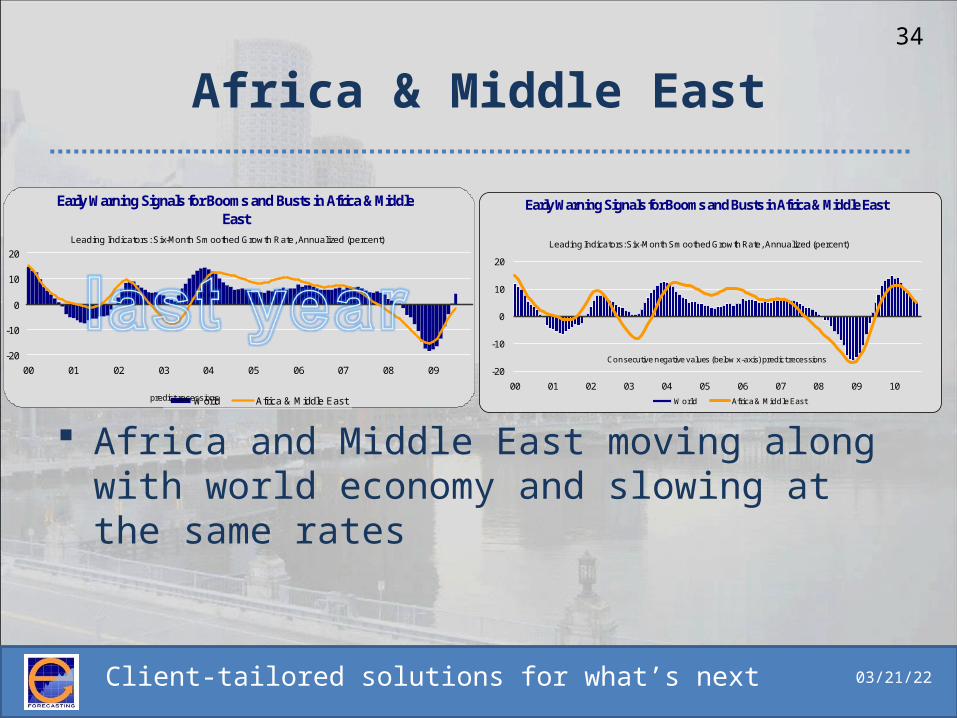

34

Africa & Middle East

Africa and Middle East moving along with world economy and slowing at the same rates

Early Warning Signals for Booms and Busts in Africa & Middle East

-20

-10

0

10

20

00 01 02 03 04 05 06 07 08 09

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

World Africa & Middle East

Consecutive negative values (below x-axis) predict recessions

-20

-10

0

10

20

00 01 02 03 04 05 06 07 08 09 10

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

Early Warning Signals for Booms and Busts in Africa & Middle East

World Africa & Middle East

Consecutive negative values (below x-axis) predict recessions

Client-tailored solutions for what’s next 04/18/23

35

Asia Pacific

Asia Pacific showed a lot of strength coming out of recession but is also victim to the recent and upcoming slowdown

Early Warning Signals for Booms and Busts in Asia & Pacific Area

-24

-18

-12

-6

0

6

12

18

24

00 01 02 03 04 05 06 07 08 09

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

World Asia & Pacific Area

Consecutive negative values (below x-axis) predict recessions-20

-10

0

10

20

30

00 01 02 03 04 05 06 07 08 09 10

Leading Indicators: Six-Month Smoothed Growth Rate, Annualized (percent)

Early Warning Signals for Booms and Busts in Asia & Pacific Area

World Asia & Pacific Area

Consecutive negative values (below x-axis) predict recessions

Client-tailored solutions for what’s next 04/18/23

36Emerging Asia will carry global

economy

2009 2010 2011 2012 2009 2010 2011 2012

-0.97 0.27 0.36 0.44 -129.7 7.1 10.2 11.3

-0.68 0.17 0.20 0.24 -90.9 4.5 5.8 6.3

-0.29 0.10 0.15 0.19 -38.7 2.6 4.3 5.0

-0.43 0.21 0.22 0.21 -57.2 5.6 6.3 5.6

-0.79 0.48 0.36 0.49 -104.8 12.6 10.1 12.7

-0.58 0.33 0.22 0.34 -77.4 8.6 6.2 8.9

-0.01 0.35 0.25 0.24 -1.6 9.0 7.1 6.2

-0.32 0.35 0.26 0.26 -42.9 9.2 7.3 6.9

1.54 1.96 1.87 1.99 205.5 51.2 53.4 51.8

1.50 1.60 1.57 1.67 199.9 41.7 44.8 43.4

0.05 0.14 0.14 0.16 6.1 3.6 3.9 4.1

-0.7 3.8 3.5 3.8 100.0 100.0 100.0 100.0

ASIA & PACIFIC INDUSTRIAL

EMERGING ASIA

China & India

MIDDLE EAST & AFRICA

WORLD GROWTH1

1Sum of Regional Contributions Source: www.e-forecasting.com

Euro Area (euro16)

Non-Euro Members (11)

OTHER EUROPE

NORTH AMERICA

United States

SOUTH AMERICA

TABLE 2

CONTRIBUTION OF REGIONS TO GLOBAL GROWTH

REGIONPercentage Points Contribution Relative Contribution, Percent

EUROPEAN UNION (EU27)

Client-tailored solutions for what’s next 04/18/23

37

Market size

Client-tailored solutions for what’s next 04/18/23

38

Client-tailored solutions for what’s next 04/18/23

39

Long term global forecast

Client-tailored solutions for what’s next 04/18/23

40

Wrap Up

Find us on the web: http://www.e-forecasting.com

Fan us on Facebook:http://www.facebook.com/eforecasting

Follow CEO Maria on twitter: http://www.twitter.com/mesimos

Information taken from our forecast and reports, for subscription queries, please contact:

Maria [email protected] you!