u.s. gdp growth - milken institute › assets › events › ... · 2014-08-20 · u.s. gdp growth...

TRANSCRIPT

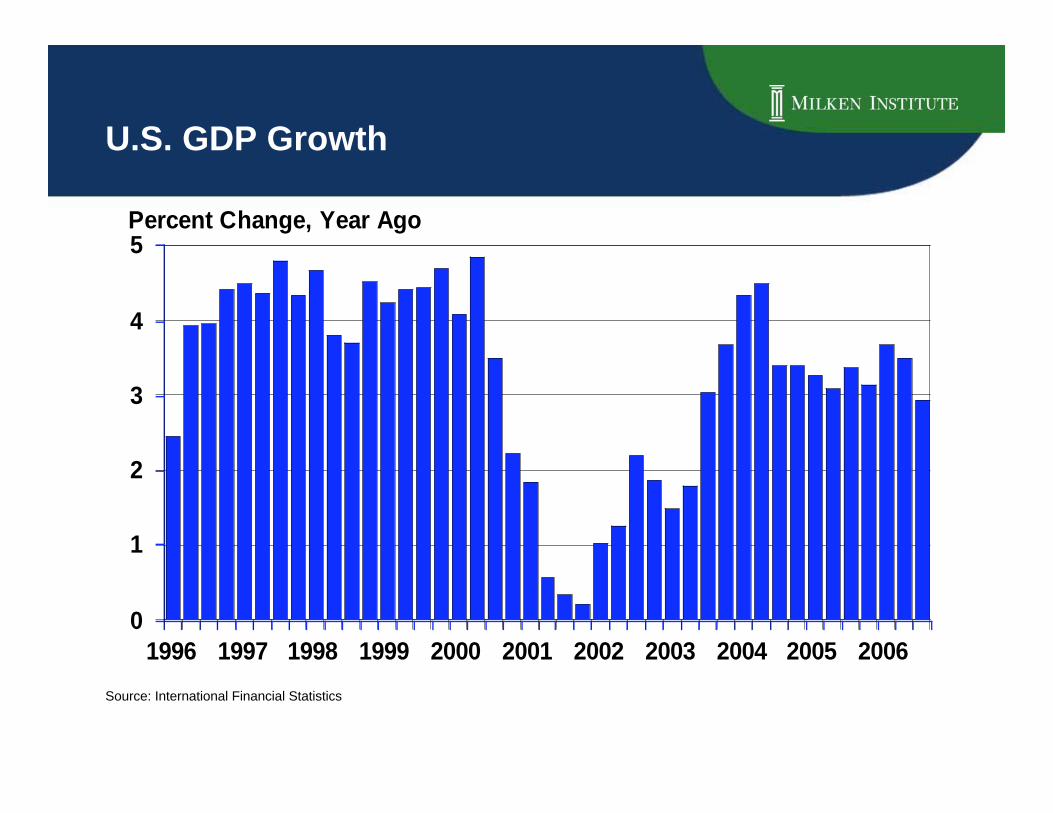

U.S. GDP Growth

Source: International Financial Statistics

0

1

2

3

4

5

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Percent Change, Year Ago

200620011996199119861981

4

2

0

-2

-4

-6

-8

% of GDP

A Brief Period of U.S. Budget Surplus

Surplus

Deficit

Source: U.S. Department of the Treasury, Bureau of the Public Debt

Where the U.S. Budget Money Goes Spending, 2008 Budget, % of Total

Total = $2.9 Trillion

Social

security

21%

Medicare and

Medicaid

20%

Other non-

discretionary

11%

Non-security

discretionary

16%Net interest

9%

Defense

17%Other

security

6%

Source: Office of Management and Budget

2006200420022000199819961994199219901988

450

400

350

300

250

200

10

8

6

4

2

U.S. Billions %

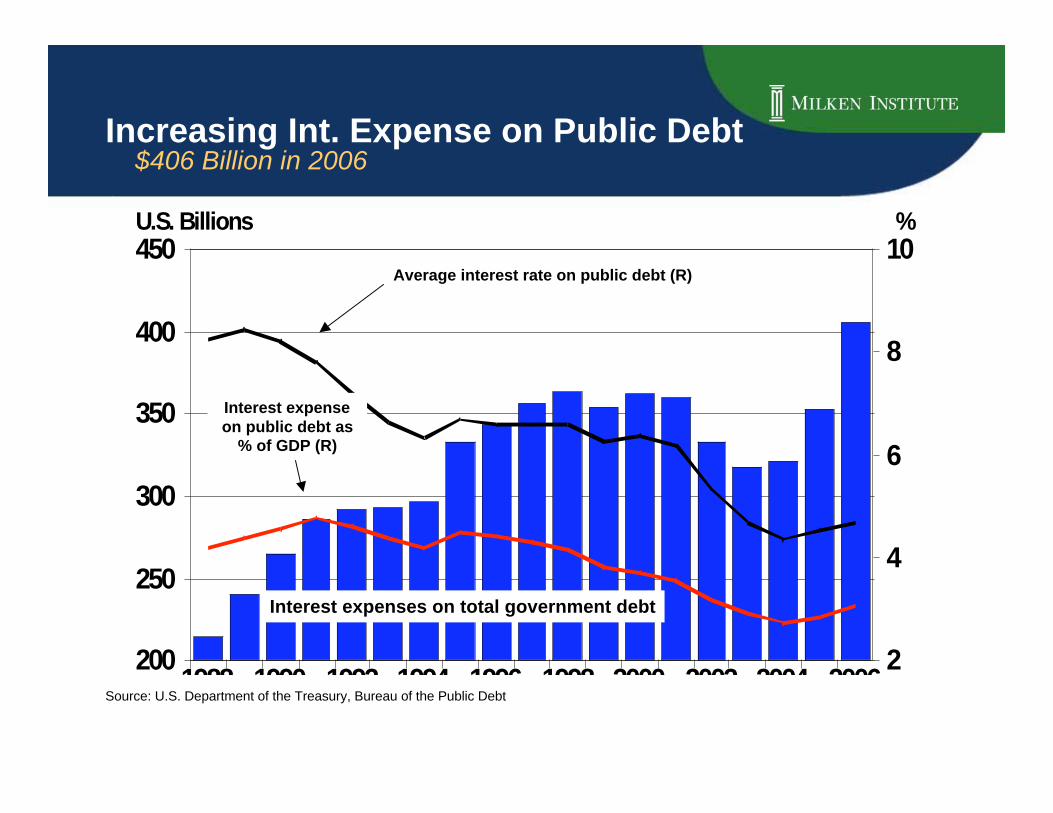

Increasing Int. Expense on Public Debt $406 Billion in 2006

Average interest rate on public debt (R)

Interest expenseon public debt as

% of GDP (R)

Interest expenses on total government debt

Source: U.S. Department of the Treasury, Bureau of the Public Debt

Declining U.S. Dollar Role Currency Denomination of International Debt Outstanding

U.S.

dollar

37%

Pound

sterling

8%

Euro

47%

Japanese

yen

3%

Other

5%

U.S.

dollar

47%

Other

6%

Pound

sterling

8%

Euro

29%

Japanese

yen

10%

1999US$ 4,999 Billions

2006Q3US$ 16,267 Billions

Decline of the Dollar

Yen (L)

Euro (R)

100

105

110

115

120

125

130

135

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

2001 2002 2003 2004 2005 2006

Yen/USD Euro/USD

Source: Bloomberg

0

50

100

150

200

250

300

80

90

100

110

120

130

140

January 2000 = 100 January 2000 = 100

2000 2001 2002 2003 2004 2005 2006

Lower Dollar, Higher Oil Price

Crude oil (L)

Trade-weighted dollar (R)

Source: Bloomberg, International Financial Statistics

12.0

12.5

13.0

13.5

14.0

14.5

15.0

2000 2001 2002 2003 2004 2005 2006

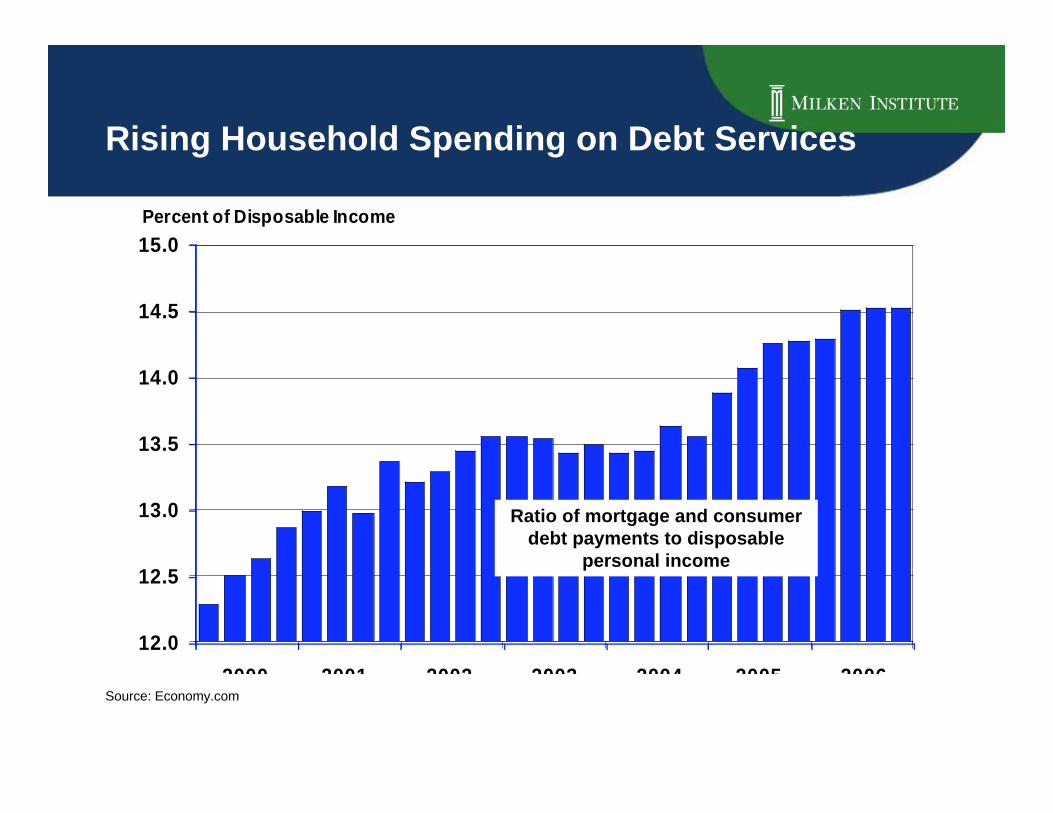

Percent of Disposable Income

Ratio of mortgage and consumerdebt payments to disposable

personal income

Source: Economy.com

Rising Household Spending on Debt Services

20062005200420032002200120001999199819971996

10

8

6

4

2

0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Percent Percent

ML Corp AAA 1-3 Yr (L)

ML Corp BBB 1-3 Yr (L)

Spread (R)

Source: Bloomberg

Corporate Bond Credit Spread Yield to Maturity

Step by Step 17 Fed Fund Rate Hikes Since 2004

200620052004

6

5

4

3

2

1

0

Percent

Source: Federal Reserve

Mortgage Rates United States

Sources: Freddie Mac, Economy.com

3

4

5

6

7

8

930-Year Fixed

15-Year Fixed

1-Year ARM

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Percent

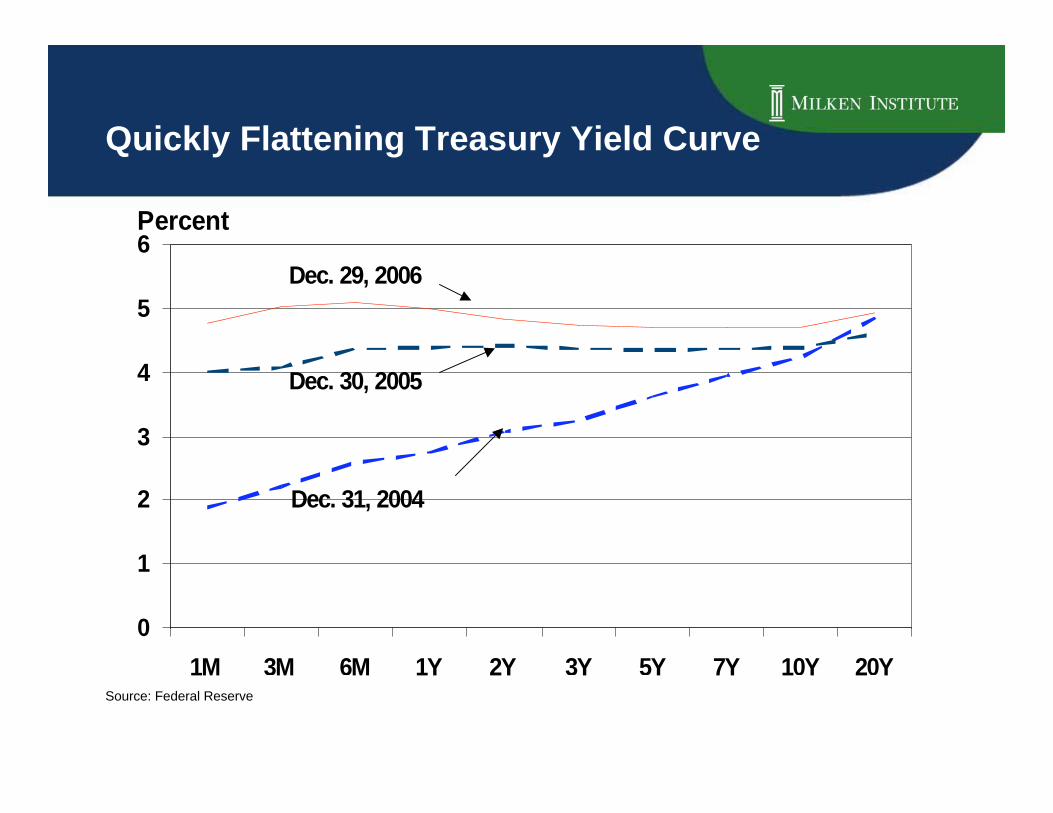

Dec. 31, 2004

Dec. 30, 2005

Dec. 29, 2006

0

1

2

3

4

5

6

1M 3M 6M 1Y 2Y 3Y 5Y 7Y 10Y 20Y

Percent

Quickly Flattening Treasury Yield Curve

Source: Federal Reserve

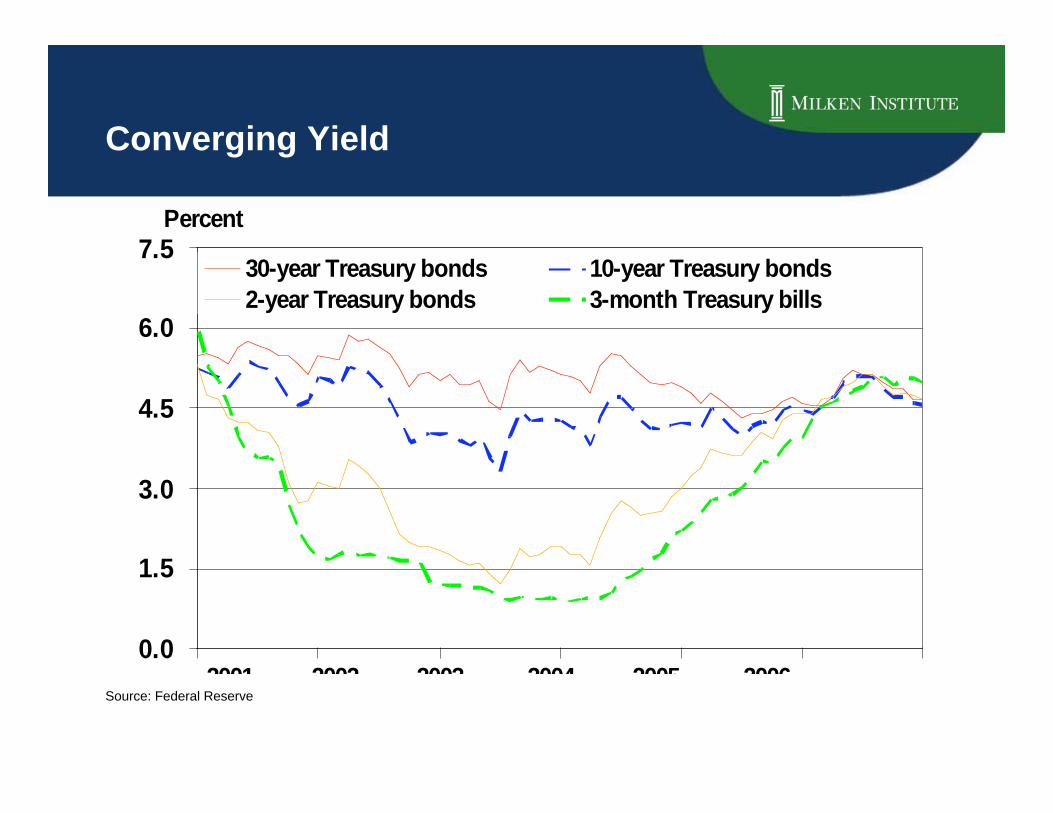

Converging Yield

0.0

1.5

3.0

4.5

6.0

7.530-year Treasury bonds 10-year Treasury bonds

2-year Treasury bonds 3-month Treasury bills

Percent

2001 2002 2003 2004 2005 2006Source: Federal Reserve

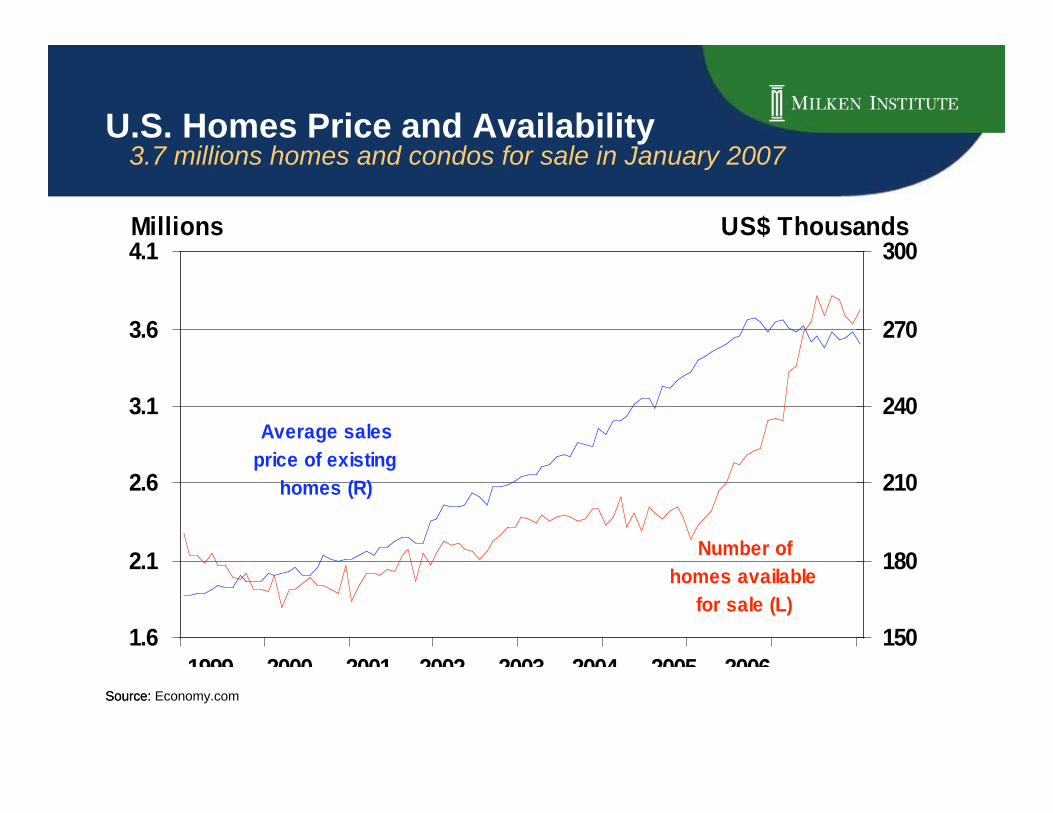

U.S. Homes Price and Availability3.7 millions homes and condos for sale in January 2007

Source:Source: Economy.com

Number of

homes available

for sale (L)

Average sales

price of existing

homes (R)

1.6

2.1

2.6

3.1

3.6

4.1

150

180

210

240

270

300Millions US$ Thousands

1999 2000 2001 2002 2003 2004 2005 2006

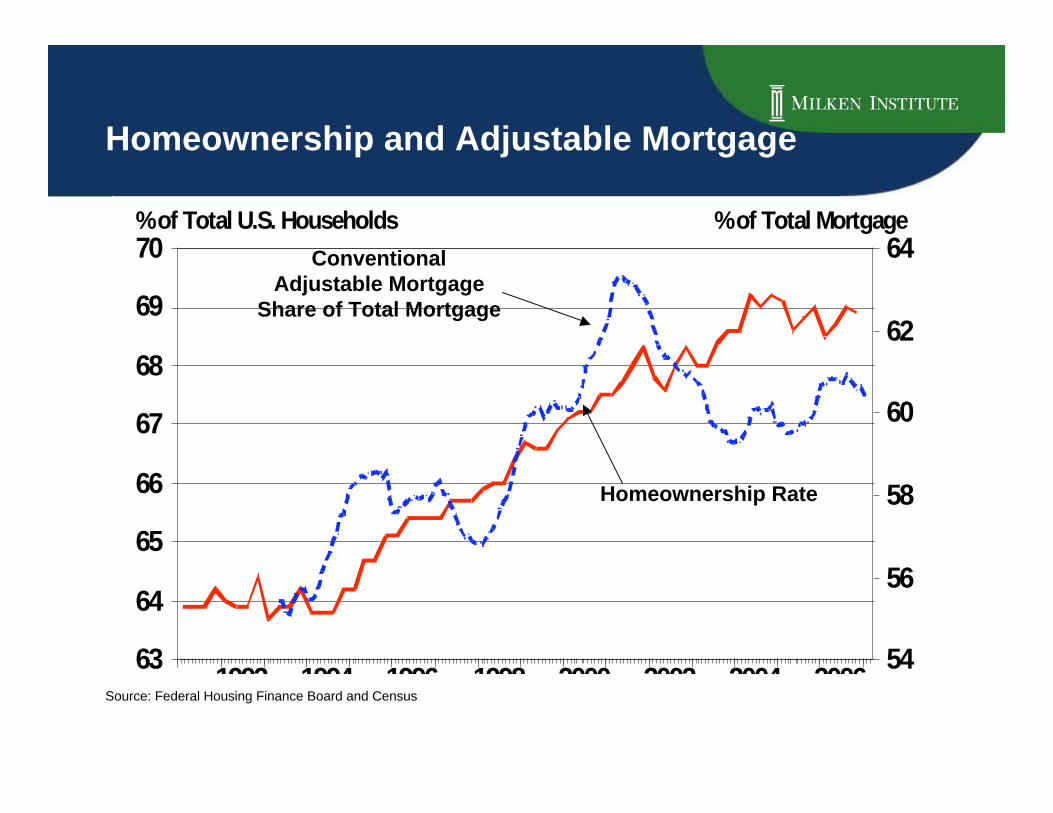

Homeownership and Adjustable Mortgage

20062004200220001998199619941992

70

69

68

67

66

65

64

63

64

62

60

58

56

54

% of Total U.S. Households % of Total Mortgage

Source: Federal Housing Finance Board and Census

ConventionalAdjustable Mortgage

Share of Total Mortgage

Homeownership Rate

0605040302010099989796

14

12

10

8

6

4

9

8

7

6

5

4

US$ Billions Percent

Mortgage Rate and Mortgages Outstanding

$13.3 trilliontotal mortgages

outstanding

30-years fixedmortgage rate

Source: Economy.com

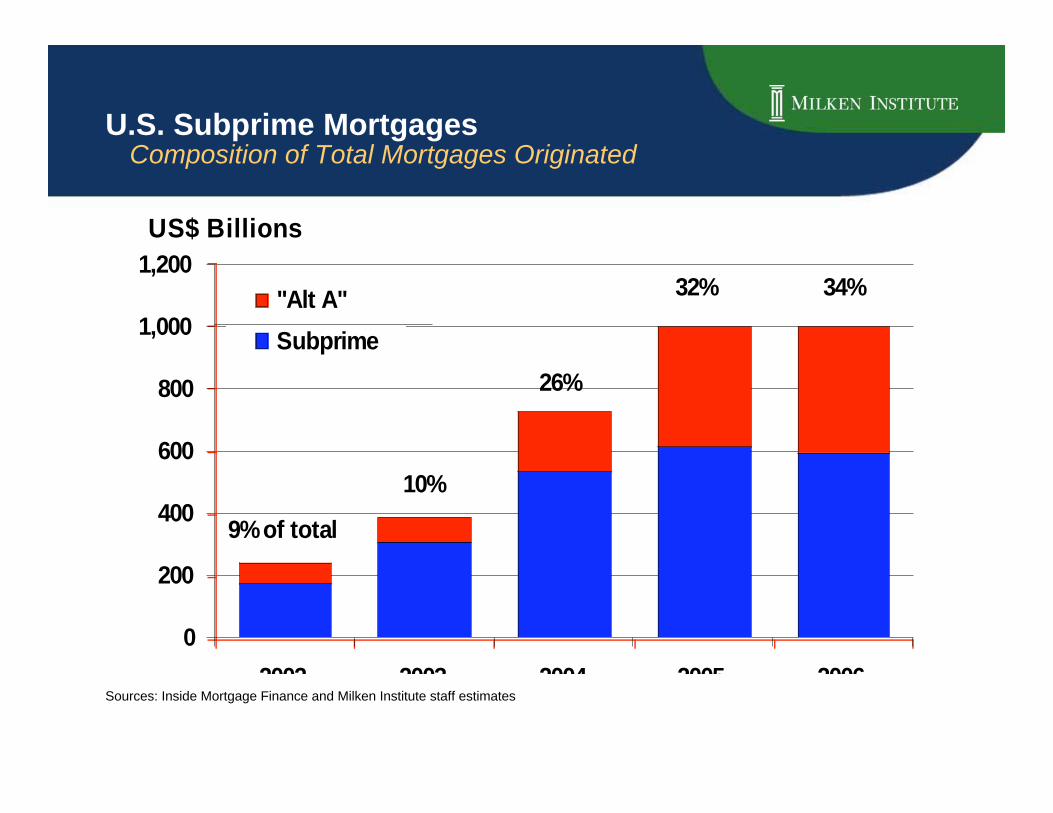

U.S. Subprime Mortgages Composition of Total Mortgages Originated

Sources: Inside Mortgage Finance and Milken Institute staff estimates

0

200

400

600

800

1,000

1,200

2002 2003 2004 2005 2006

"Alt A"

Subprime

9% of total

10%

26%

32% 34%

US$ Billions

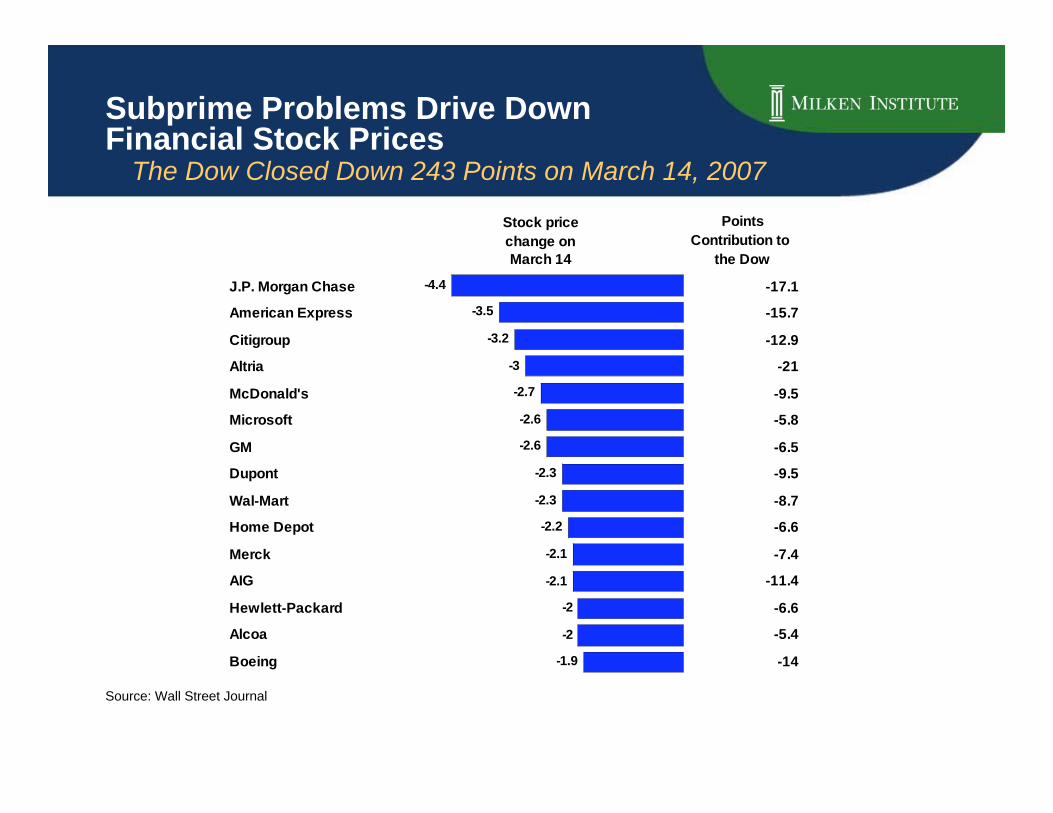

Subprime Problems Drive DownFinancial Stock Prices The Dow Closed Down 243 Points on March 14, 2007

Points

Contribution to

the Dow

J.P. Morgan Chase -17.1

American Express -15.7

Citigroup -12.9

Altria -21

McDonald's -9.5

Microsoft -5.8

GM -6.5

Dupont -9.5

Wal-Mart -8.7

Home Depot -6.6

Merck -7.4

AIG -11.4

Hewlett-Packard -6.6

Alcoa -5.4

Boeing -14

Stock price

change on

March 14

-4.4

-3.5

-3.2

-3

-2.7

-2.6

-2.6

-2.3

-2.3

-2.2

-2.1

-2.1

-2

-2

-1.9

Source: Wall Street Journal

Riskier in Mortgage? By Type of Mortgage Loan

58

34

8.4

98

2

0.4

0

20

40

60

80

100

2001 2005

Negative

Amortization

Normal (positive)

Amortization

Interest Only (zero)

Amortization

Percent

U.S. Energy Supply and Consumption Quadrillion BTU, 2005

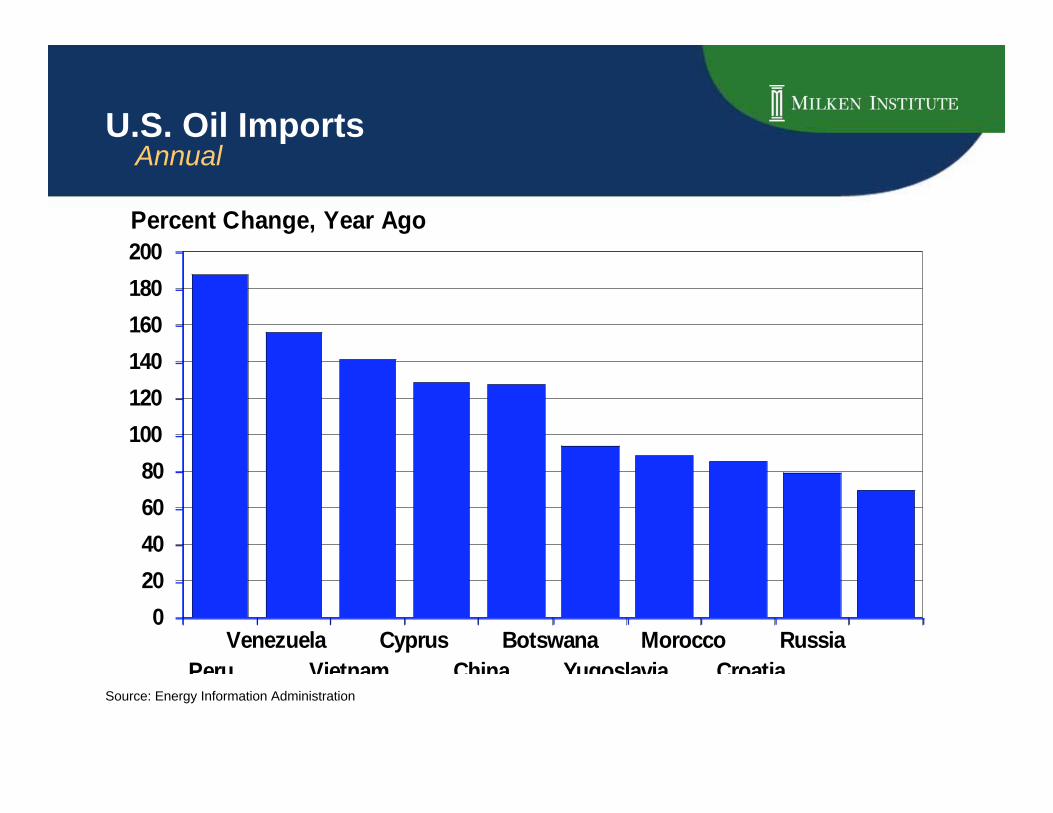

U.S. Oil ImportsAnnual

Source: Energy Information Administration

0

20

40

60

80

100

120

140

160

180

200

Percent Change, Year Ago

Venezuela Cyprus Botswana Morocco Russia

Peru Vietnam China Yugoslavia Croatia

Foreign Holdings of U.S. Securities

S. Korea

2%

Taiwan

2%

Singapore

2%

Russia

1%

HK

1%Australia

1%

Switzerland

3%

Canada

5%

Middle East

3%

Others

11%

U.K.

8%

China

9%

Offshore

Financial

Centers

11%

Japan

15%

Euro Area

26%

$15.5 Trillion, June 2006

Source: U.S. Treasury

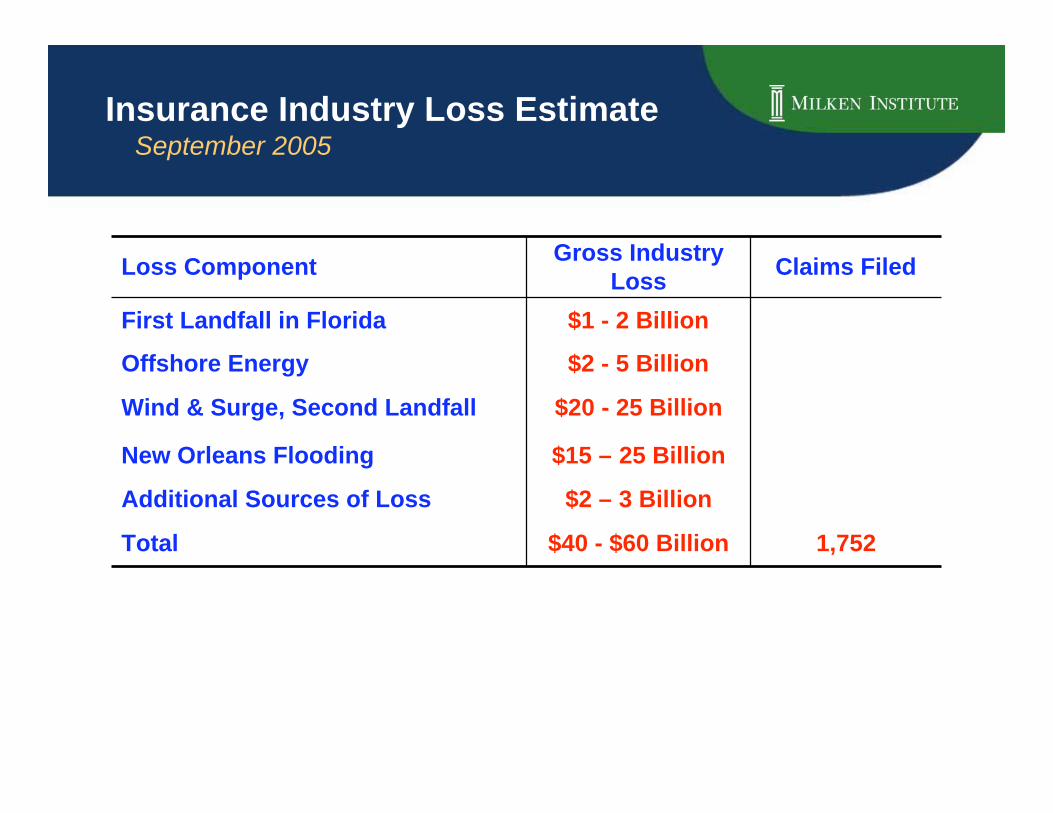

Most Costly Disaster in US History

TOTAL ECONOMIC IMPACT ~ APPROX. $200B USD

Drasticallyreduced tax

revenue base,unemployment,displacement,

bankruptcy

Loss ofapproximately

$500,000 in taxrevenue for each

day riverboatcasinos were

closed

Loss of timberproducts

estimated at $1.3billion; USDAdeclared 31agricultural

disaster areas

Interrupted oilproduction,

importation, andrefining in the Gulfarea had a major

effect on fuelprices

$40 - $60 Billion

$2 – 3 Billion

$15 – 25 Billion

$20 - 25 Billion

$2 - 5 Billion

$1 - 2 Billion

Gross IndustryLoss

1,752

Claims Filed

Additional Sources of Loss

Total

Wind & Surge, Second Landfall

New Orleans Flooding

First Landfall in Florida

Offshore Energy

Loss Component

Insurance Industry Loss Estimate September 2005

104

44

18 16

0

20

40

60

80

100

120

Hurricane Katrina

(2005)

Sept. 11 Attacks

(2001)

Hurricane Andrew

(1992)

Hurricanes

Charley, Frances,

Ivan & Jeanne

(2004)

Billions USD

Within 3 weeks of Katrina’s landfall, thefederal govn’t authorized $75B in aid --more than all the federal aid for 9/11,

2004’s hurricanes and Hurricane Andrewcombined

Government Aid After Disasters 2005 Billion USD

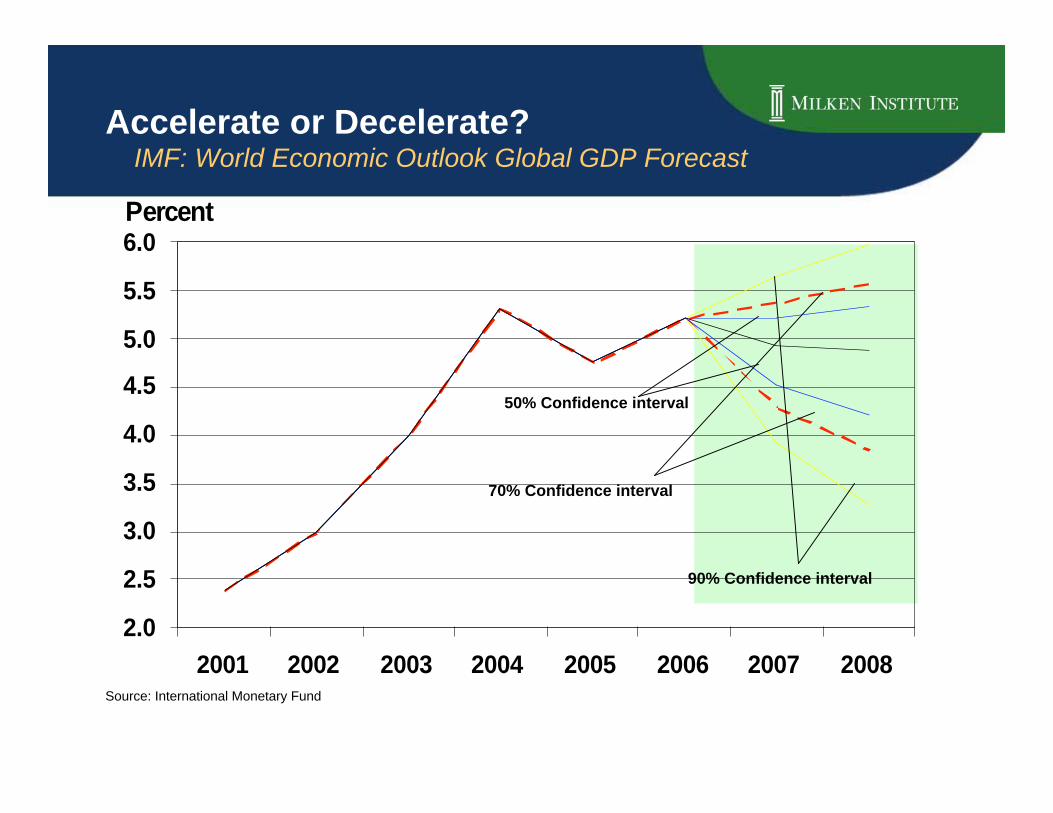

Accelerate or Decelerate? IMF: World Economic Outlook Global GDP Forecast

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

2001 2002 2003 2004 2005 2006 2007 2008

Percent

Source: International Monetary Fund

90% Confidence interval

50% Confidence interval

70% Confidence interval

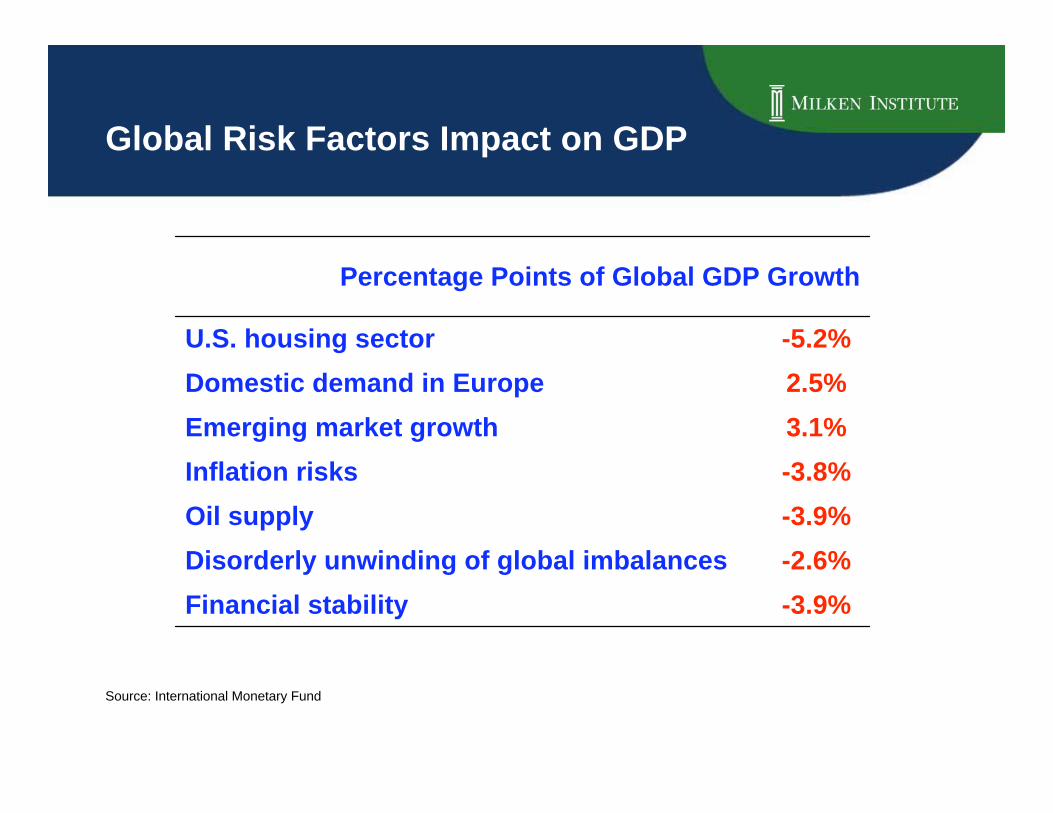

Global Risk Factors Impact on GDP

-3.9%Financial stability

-2.6%Disorderly unwinding of global imbalances

-3.9%Oil supply

-3.8%Inflation risks

3.1%Emerging market growth

2.5%Domestic demand in Europe

-5.2%U.S. housing sector

Percentage Points of Global GDP Growth

Source: International Monetary Fund

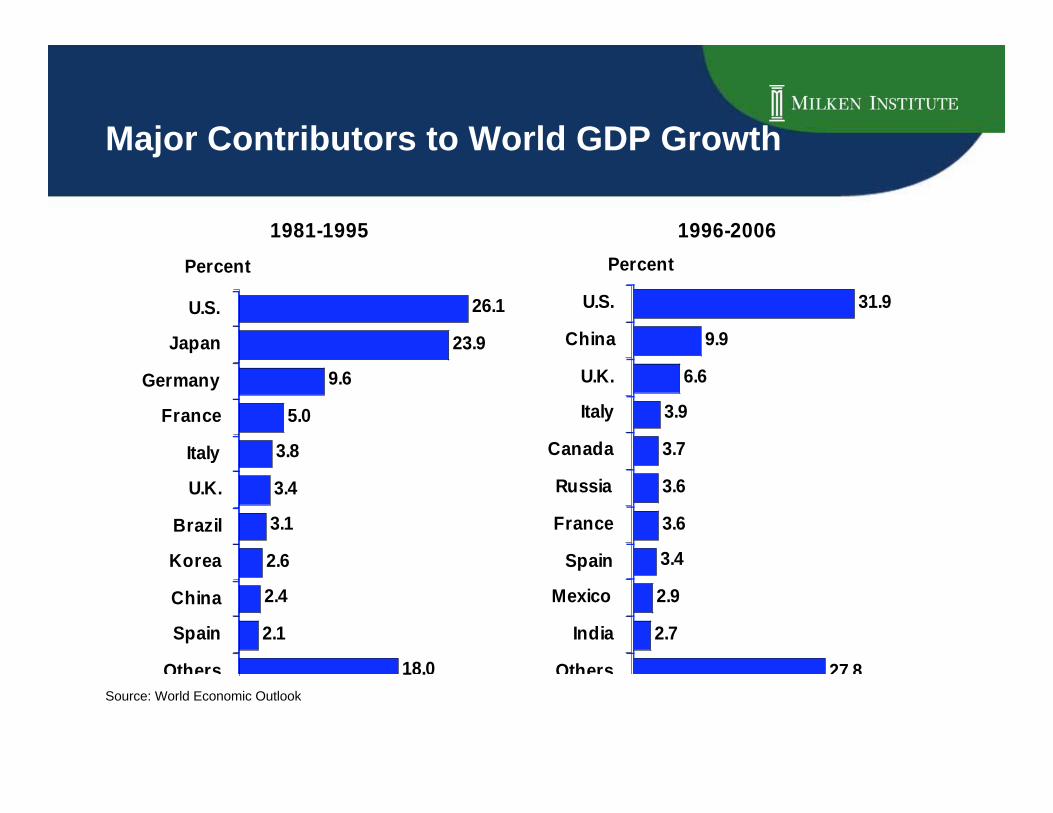

Major Contributors to World GDP Growth

1981-1995

26.1

23.9

9.6

5.0

3.8

3.4

3.1

2.6

2.4

2.1

18.0

U.S.

Japan

Germany

France

Italy

U.K.

Brazil

Korea

China

Spain

Others

Percent

1996-2006

31.9

9.9

6.6

3.9

3.7

3.6

3.6

3.4

2.9

2.7

27.8

U.S.

China

U.K.

Italy

Canada

Russia

France

Spain

Mexico

India

Others

Percent

Source: World Economic Outlook

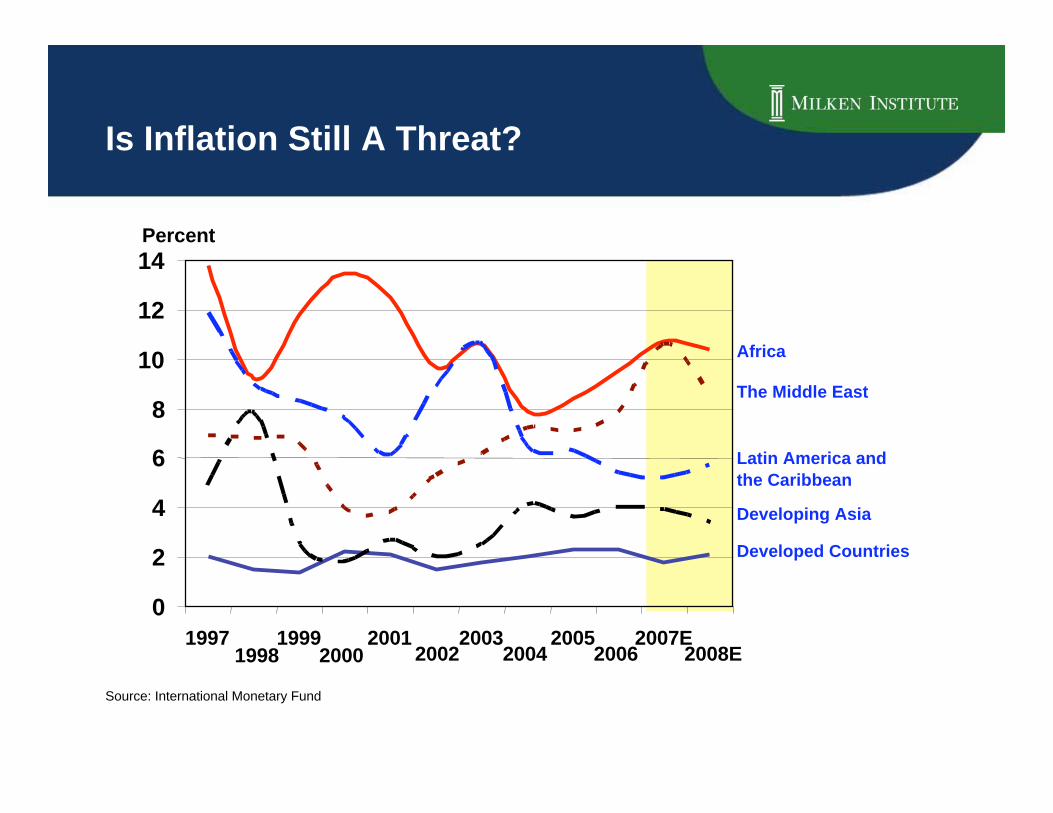

Is Inflation Still A Threat?

0

2

4

6

8

10

12

14

1997 1999 2001 2003 2005 2007E

Developed Countries

Developing Asia

Latin America and

the Caribbean

The Middle East

Africa

Percent

2008E20062004200220001998

Source: International Monetary Fund

GDP Growth: Is Europe Left Behind?

Est. Est.Source: World Economic Outlook

-3

0

3

6

9

12

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

WorldEuro area

Newly Industrialized AsiaUnited States

Percent

Europe’s Energy Reliance on FormerSoviet Union Countries Percent of Total Oil Imports, 2005

Source: BP

Former Soviet

Union

45%

Middle East

24%

Unidentified*

5%

North America

3%

South & Central

America

2%

Sub-Saharan

Africa

5%

North Africa

15%

Asia

1%

* Includes changes in the quantity of oil in transit,movements not otherwise shown, unidentifiedmilitary use etc.

World’s Equity Market Share December 1950 vs. December 2006

Market Capitalization

1950

Other

6%

Europe

26%

U.S.

59%Japan

9%

Market Capitalization

2006

Other

23%

Europe

26%

U.S.

39%

Japan

9%

Source: World Exchanges Federation

World’s Equity Market Share December 1988 vs. December 2006

Market Capitalization

1988

Other

14%

Europe

26%

U.S.

29%

Japan

Market Capitalization

2006

Other

23%

Europe

26%

U.S.

39%

Japan

9%Source: World Exchanges Federation

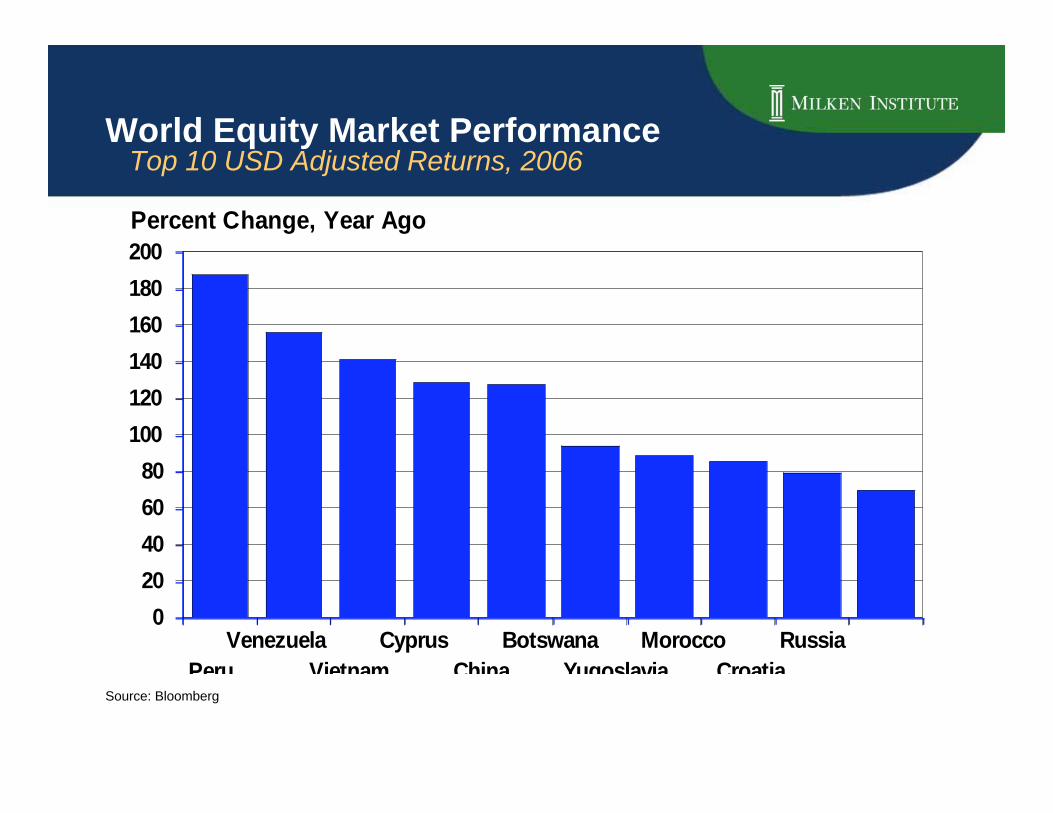

World Equity Market PerformanceTop 10 USD Adjusted Returns, 2006

Source: Bloomberg

0

20

40

60

80

100

120

140

160

180

200

Percent Change, Year Ago

Venezuela Cyprus Botswana Morocco Russia

Peru Vietnam China Yugoslavia Croatia

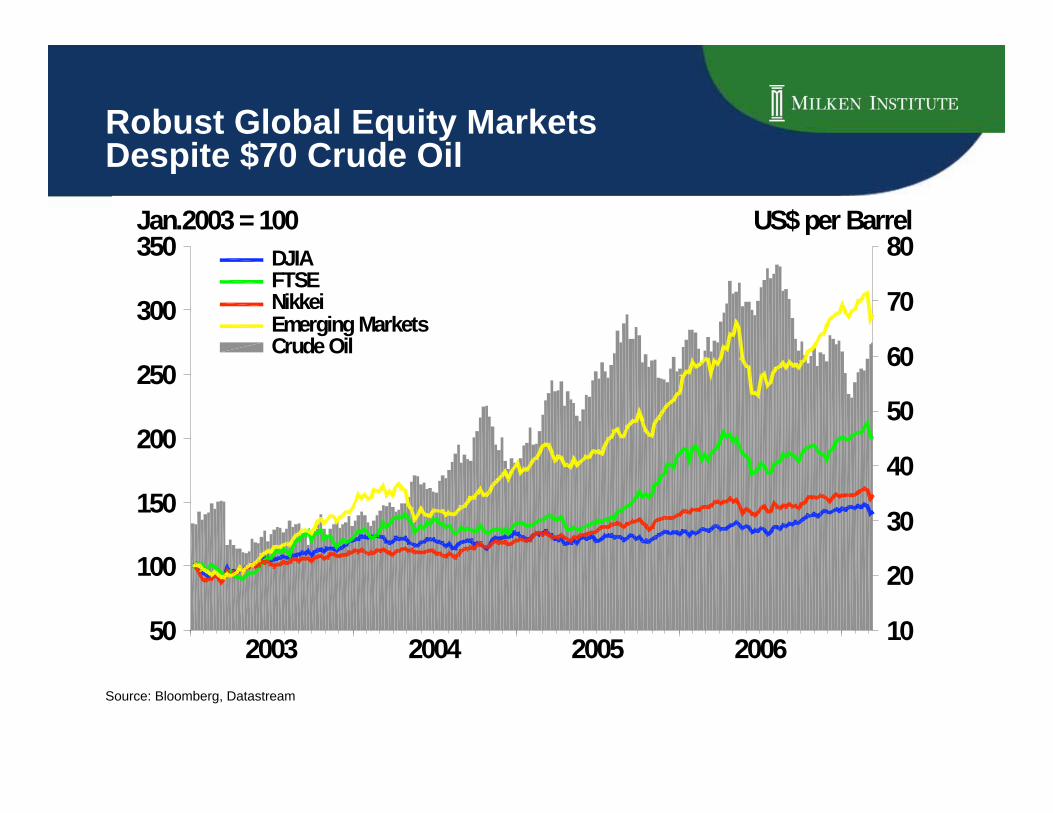

Robust Global Equity MarketsDespite $70 Crude Oil

2006200520042003

350

300

250

200

150

100

50

80

70

60

50

40

30

20

10

Jan.2003 = 100 US$ per Barrel

DJIAFTSENikkeiEmerging MarketsCrude Oil

Source: Bloomberg, Datastream

Countries That Export Capital 2006

China

13.5%

Japan

12.2%

Germany

8.8%

Russia

8.8%Saudi ArabiaNorwaySwitzerland

3 7%

Netherlands

3.7%

Kuwait

3.6%

Singapore

2.8%

Other countries

22.2%

U.A.E.

2.7%

Algeria

2.3%

Venezuela

2.1%

Source: IMF

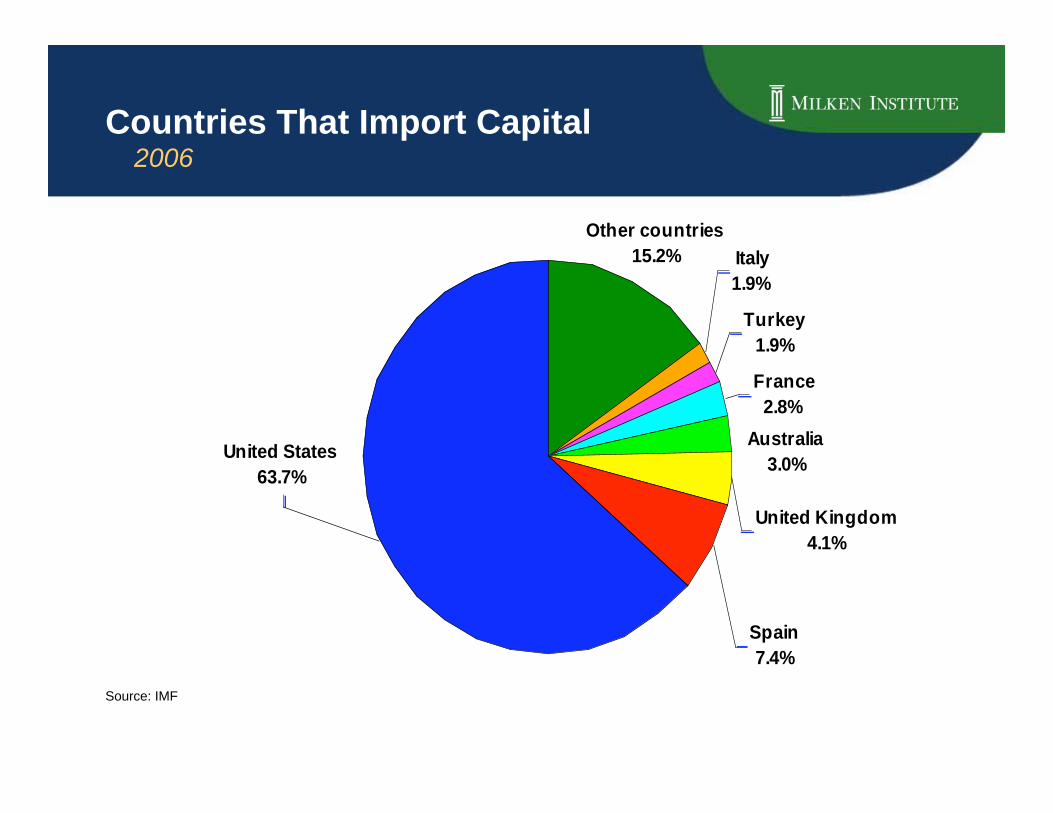

Countries That Import Capital 2006

Italy

1.9%

Turkey

1.9%

France

2.8%

Other countries

15.2%

Australia

3.0%United States

63.7%

Spain

7.4%

United Kingdom

4.1%

Source: IMF

Net Direct InvestmentDeveloping Countries, 1997-2006

Source: World Economic Outlook

0

20

40

60

80

100

120

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Africa Developing AsiaMiddle East Western Hemisphere

US$ Billions

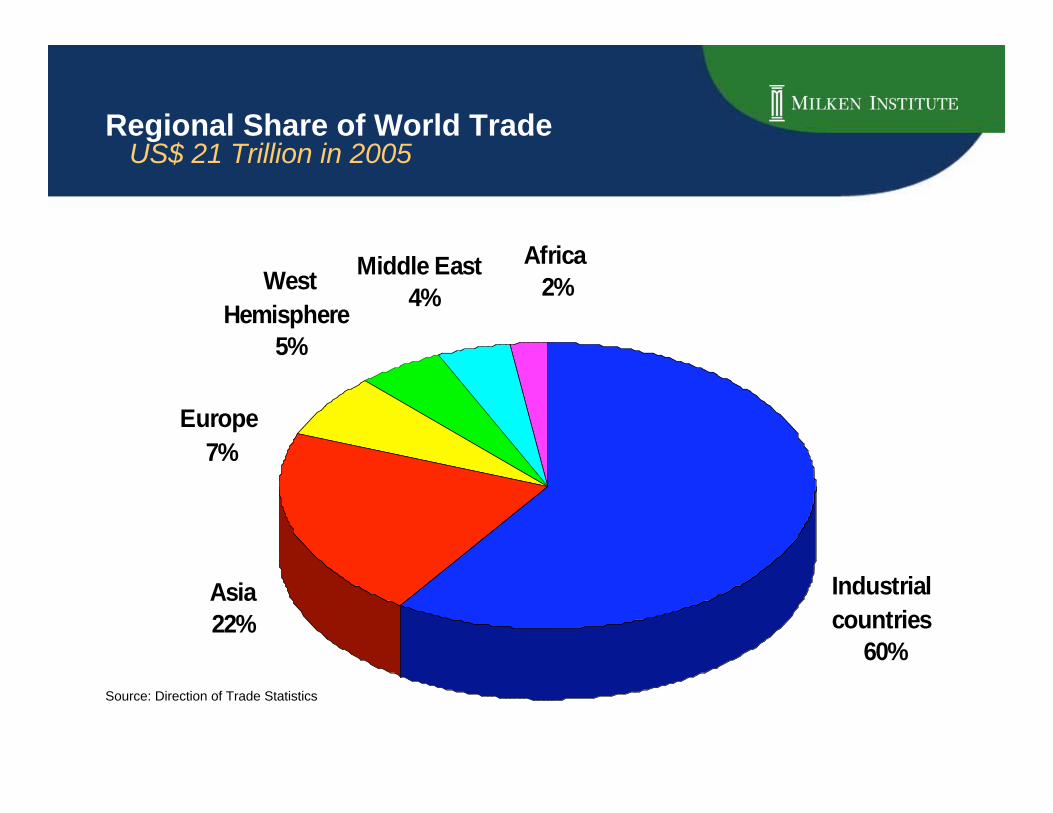

Regional Share of World TradeUS$ 21 Trillion in 2005

Asia

22%

West

Hemisphere

5%

Industrial

countries

60%

Middle East

4%

Africa

2%

Europe

7%

Source: Direction of Trade Statistics

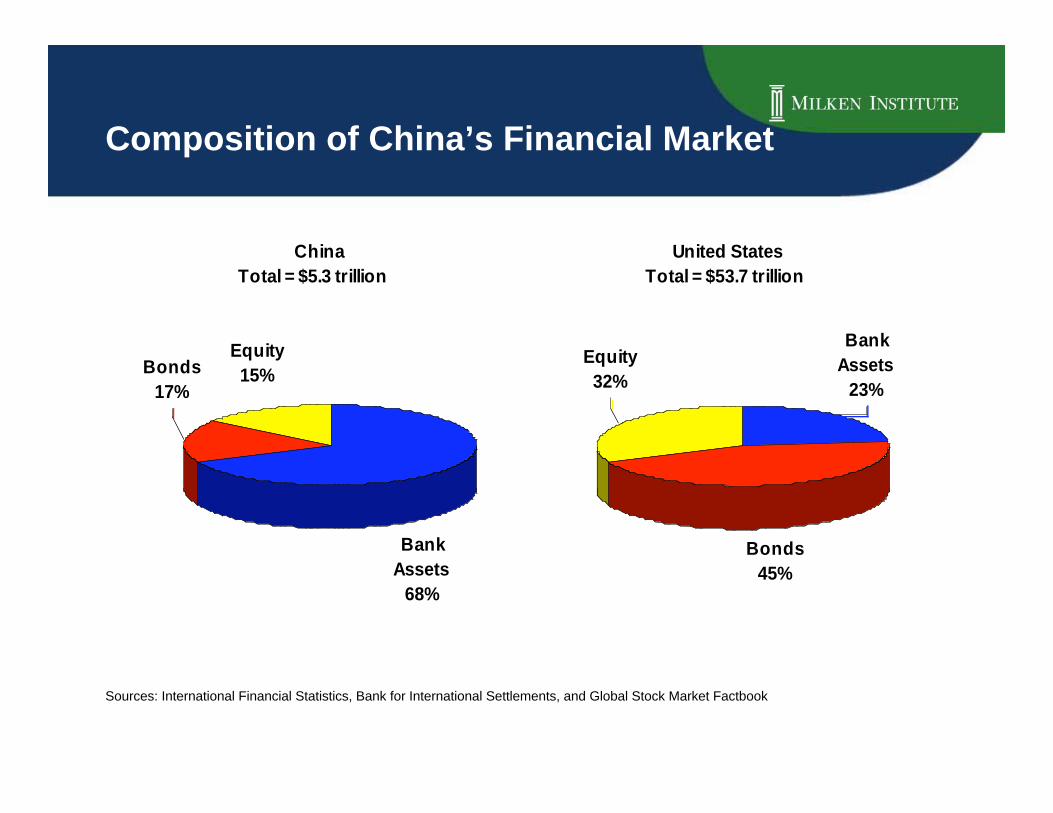

Composition of China’s Financial Market

China

Total = $5.3 trillion

Bank

Assets

68%

Bonds

17%

Equity

15%

United States

Total = $53.7 trillion

Equity

32%

Bonds

45%

Bank

Assets

23%

Sources: International Financial Statistics, Bank for International Settlements, and Global Stock Market Factbook

Fixed Investments ContributeMore than 40% to China’s GDP Growth

Sources: International Financial Statistics and Bureau of Statistics (China)

0

5

10

15

20

25

30

35

40

45

50

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Percent of GDP Growth

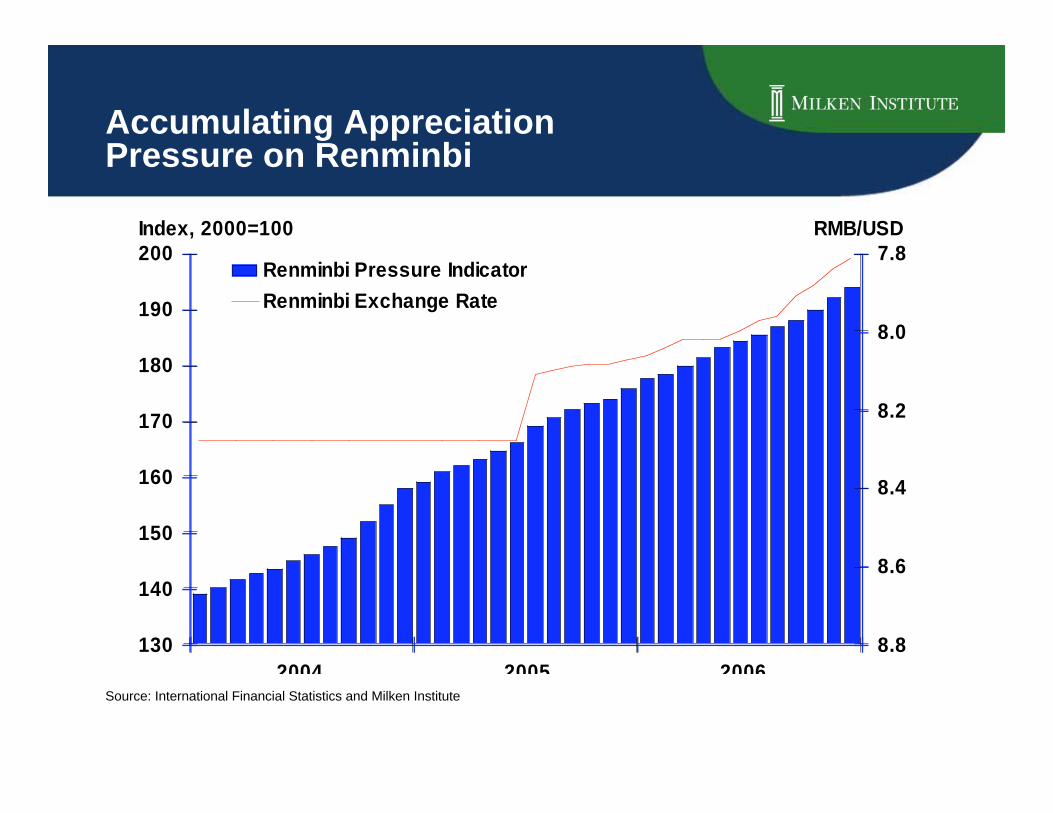

Accumulating AppreciationPressure on Renminbi

130

140

150

160

170

180

190

200 7.8

8.0

8.2

8.4

8.6

8.8

Renminbi Pressure Indicator

Renminbi Exchange Rate

2004 2005 2006

Index, 2000=100 RMB/USD

Source: International Financial Statistics and Milken Institute

100 Most Underfunded S&P 500Defined-Benefit Plans

$26

-$141

-$114

-$137 -$138

-$94

-160

-140

-120

-100

-80

-60

-40

-20

0

20

40

2001 2002 2003 2004 2005 2006

US$ Billions

Source: Bloomberg

2054204620382030202220142006

4000

3000

2000

1000

0

-1000

-2000

Percent

Payments from G-10 Government Bonds OutstandingProjected Payments Out of G-10 Pension Fund LiabilitiesCash Flows

Cash Flows from G-10 GovernmentBonds and Projected Pension Payments

Assumption: 75 percent oftotal pension fund assetsare allocated to bonds

Source: OECD, Global Pension Statistics, Insurance Statistics and other administrative sources.

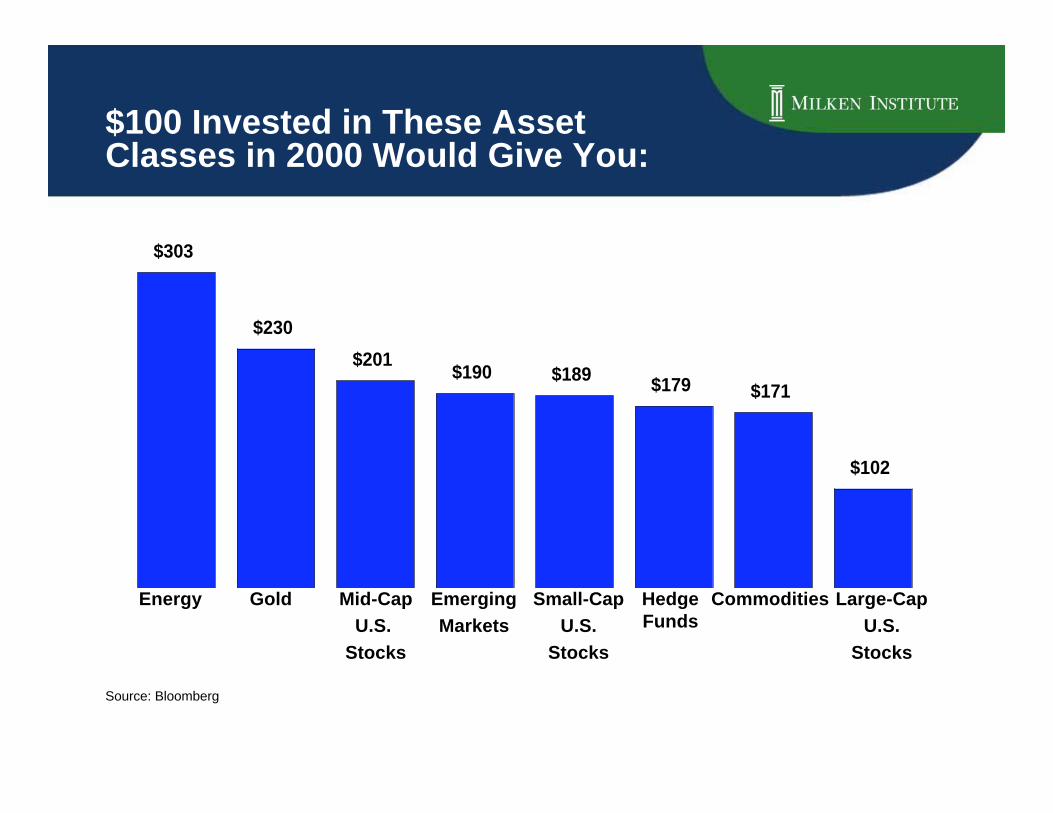

$100 Invested in These AssetClasses in 2000 Would Give You:

Large-Cap

U.S.

Stocks

CommoditiesHedgeFunds

Small-Cap

U.S.

Stocks

Emerging

Markets

Mid-Cap

U.S.

Stocks

GoldEnergy

$303

$230

$201$190 $189

$179 $171

$102

Source: Bloomberg

The Dow dropped 241points in 3 minutes

Source: Bloomberg

U.S. Stock Market Plummeted onFebruary 27, 2007:A Market Correction “Made in China”

12,050

12,100

12,150

12,200

12,250

12,300

12,350

12,400

12,450

11:00 11:15 11:30 11:45 12:00 12:15 12:30 12:45 13:00

Dow Jones Index

Higher Degree of IntegrationBetween NYSE and Shanghai Stock Exchange

Correlation = 0.8773

January 2006 – March 2007

Source: Bloomberg

Dow Jones

Industrial

Average (L)

Shanghai

Stock

Exchange

Composite ®

90

95

100

105

110

115

120

0

50

100

150

200

250

300

2006Q1 2006Q2 2006Q3 2006Q4 2007Q1

Index, Jan. 2006 = 100

(R)

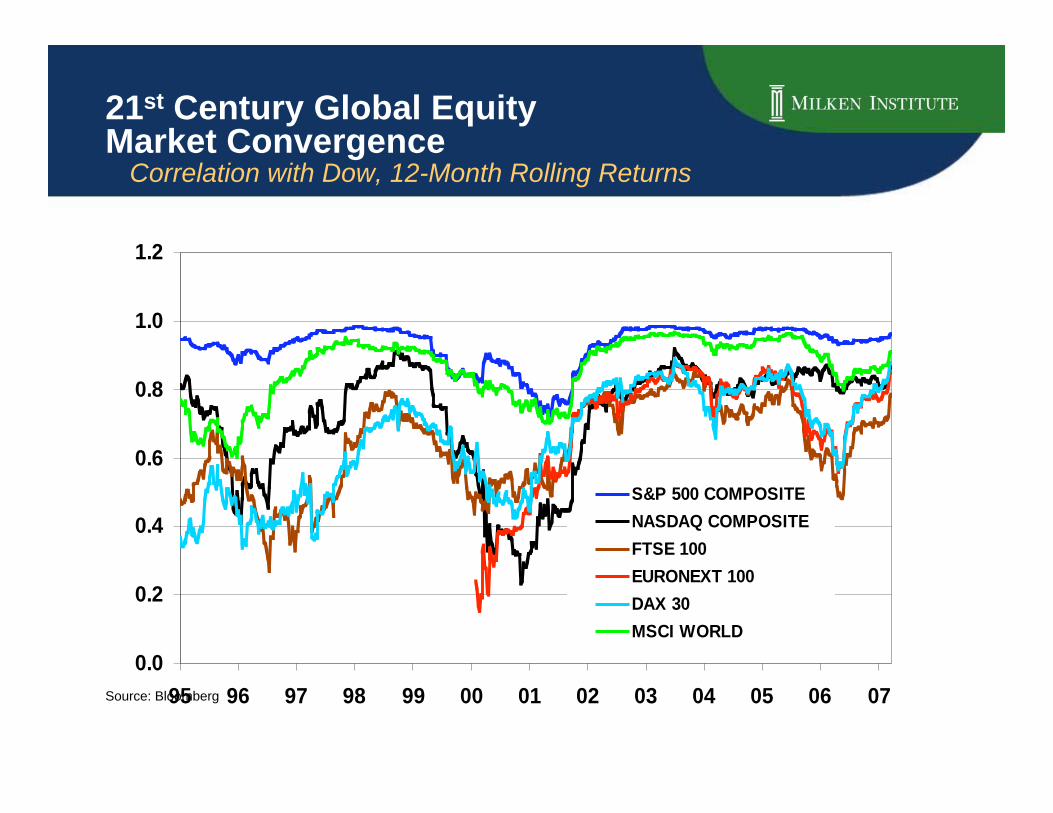

21st Century Global EquityMarket Convergence Correlation with Dow, 12-Month Rolling Returns

0.0

0.2

0.4

0.6

0.8

1.0

1.2

95 96 97 98 99 00 01 02 03 04 05 06 07

S&P 500 COMPOSITE

NASDAQ COMPOSITE

FTSE 100

EURONEXT 100

DAX 30

MSCI WORLD

Source: Bloomberg

20062005200420032002200120001999

16

14

12

10

8

6

4

2

Percent

Converging Yield to Maturity

Source: Merrill Lynch

Emerging Markets Sovereign Plus Index

U.S. Government Index

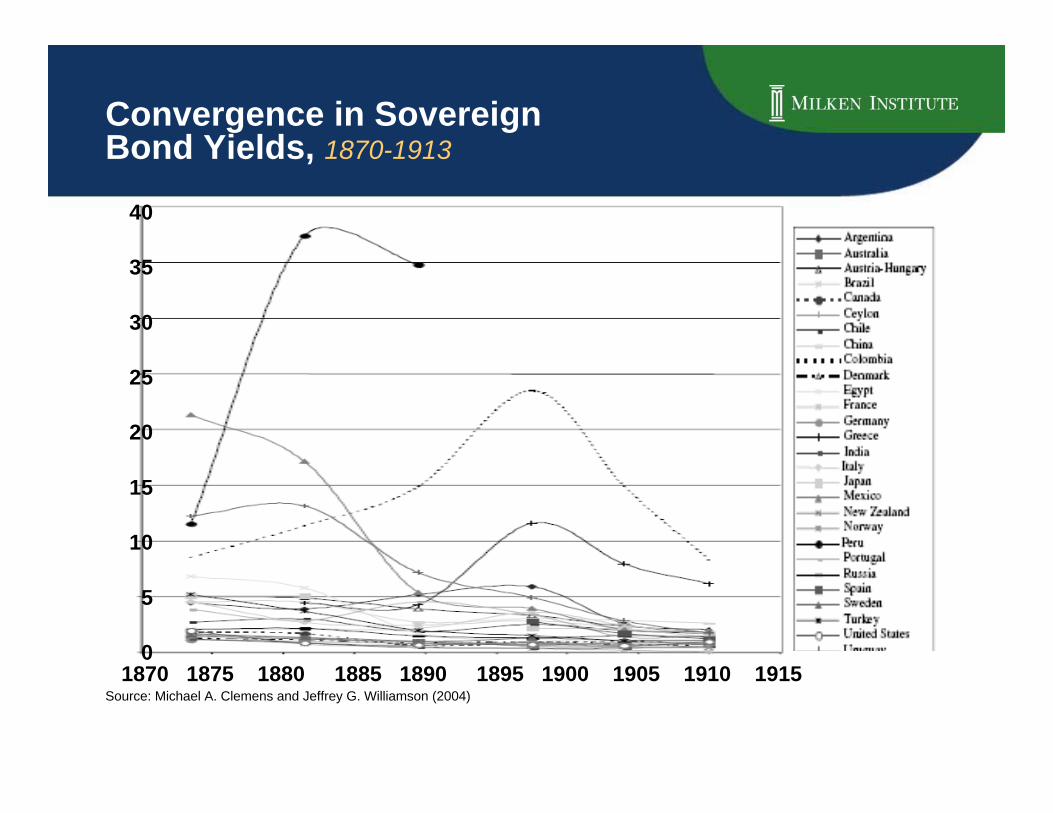

Convergence in SovereignBond Yields, 1870-1913

40

35

30

25

20

15

10

5

01870 1875 1880 1885 1890 1895 1900 1905 1910 1915

Source: Michael A. Clemens and Jeffrey G. Williamson (2004)

Narrowing Spread Between Hedge FundReturn and One-Year Treasury Yield

0

2

4

6

8

10

12

14

16

1981 1986 1991 1996 2001 2006

Percent

Spread between averagehedge funds return and1-year Treasury yield

Sources: Hedgefund.net, Bloomberg and MI staff

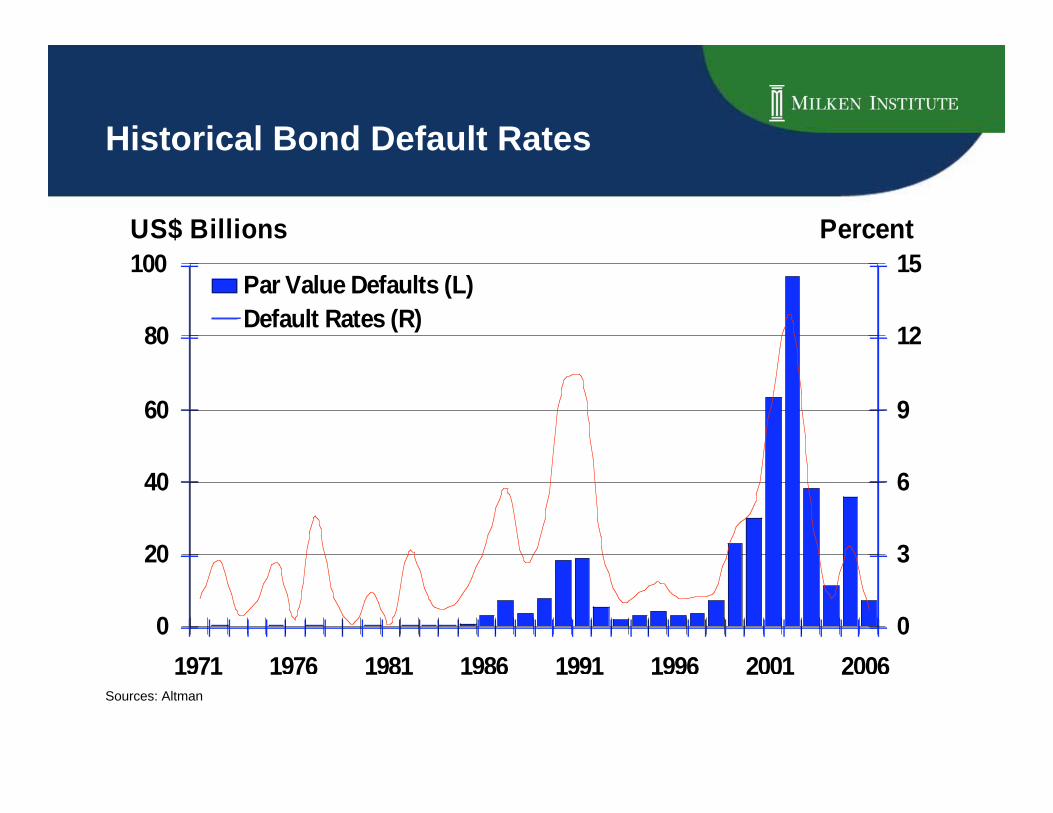

Historical Bond Default Rates

0

20

40

60

80

100

1971 1976 1981 1986 1991 1996 2001 2006

0

3

6

9

12

15Par Value Defaults (L)

Default Rates (R)

US$ Billions Percent

Sources: Altman

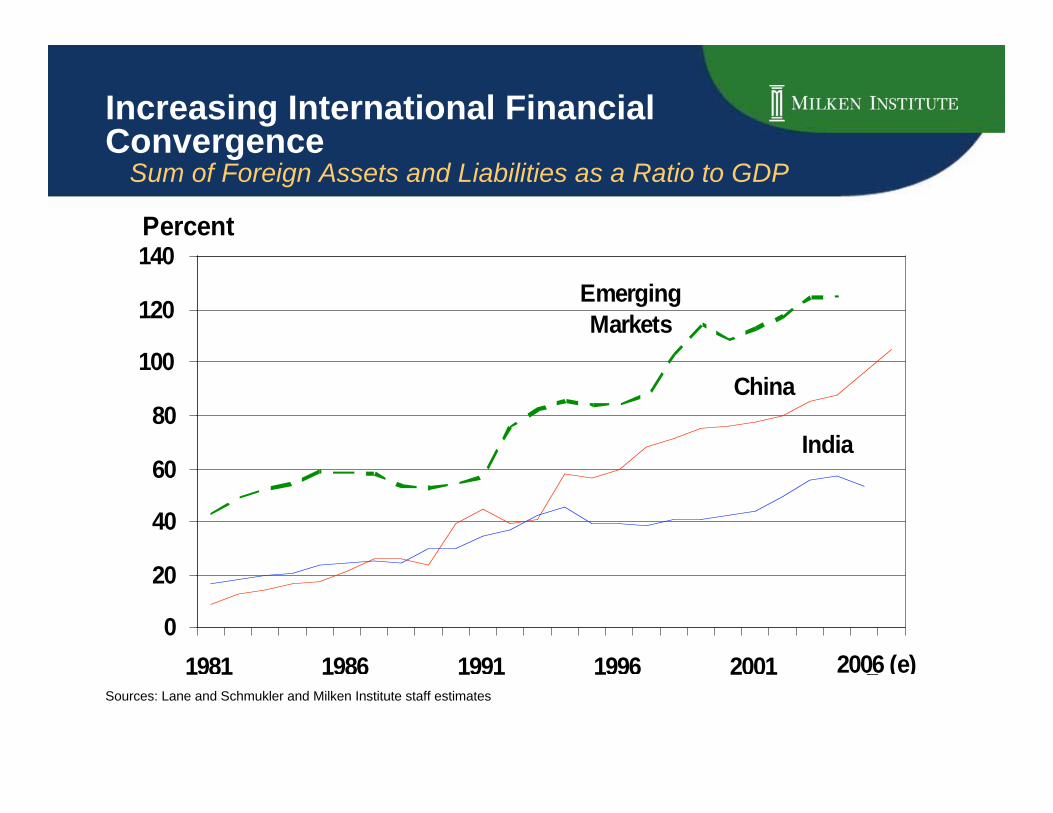

Increasing International FinancialConvergence Sum of Foreign Assets and Liabilities as a Ratio to GDP

Sources: Lane and Schmukler and Milken Institute staff estimates

China

India

Emerging

Markets

0

20

40

60

80

100

120

140

1981 1986 1991 1996 2001 2006

Percent

2006 (e)

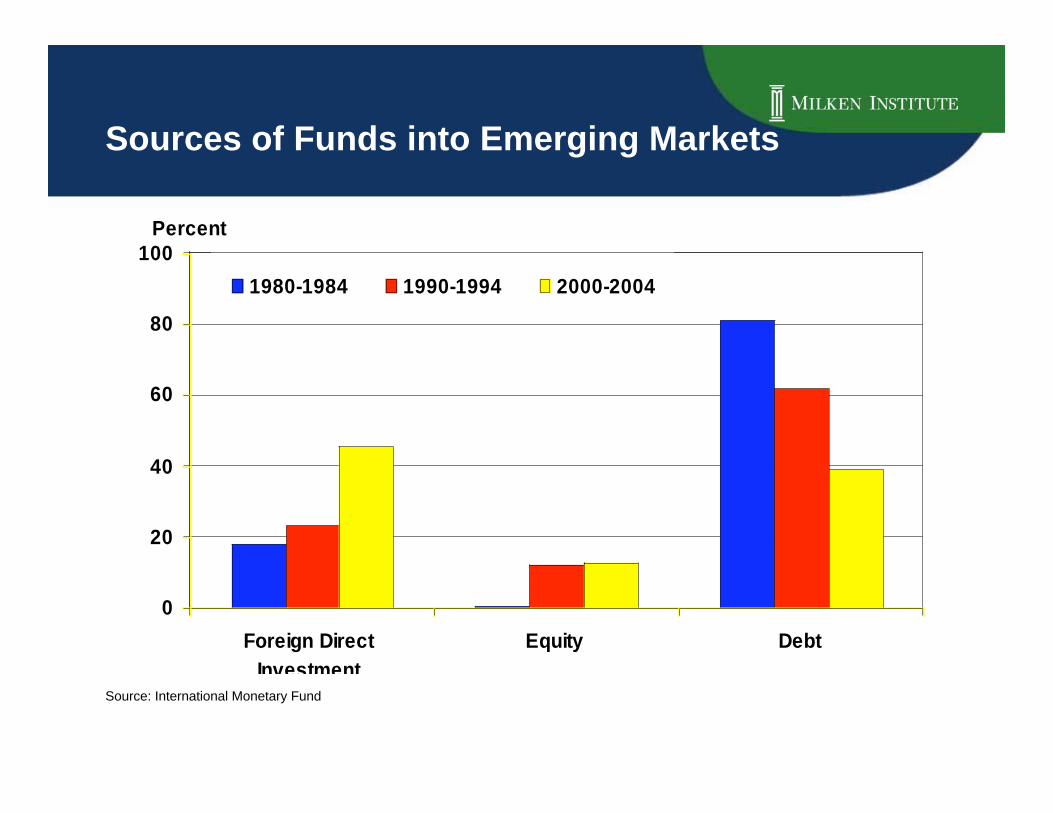

Sources of Funds into Emerging Markets

Source: International Monetary Fund

0

20

40

60

80

100

Foreign Direct

Investment

Equity Debt

1980-1984 1990-1994 2000-2004

Percent

Global Futures Market Notional Amounts

Source: Bank for International Settlements

Currency (R)

Equity index

(R)

Interest rate

(L)

0.0

0.3

0.5

0.8

1.0

1.3

1.5

0

5

10

15

20

25

30US$ Trillions

94 95 96 97 98 99 00 01 02 03 04 05 06

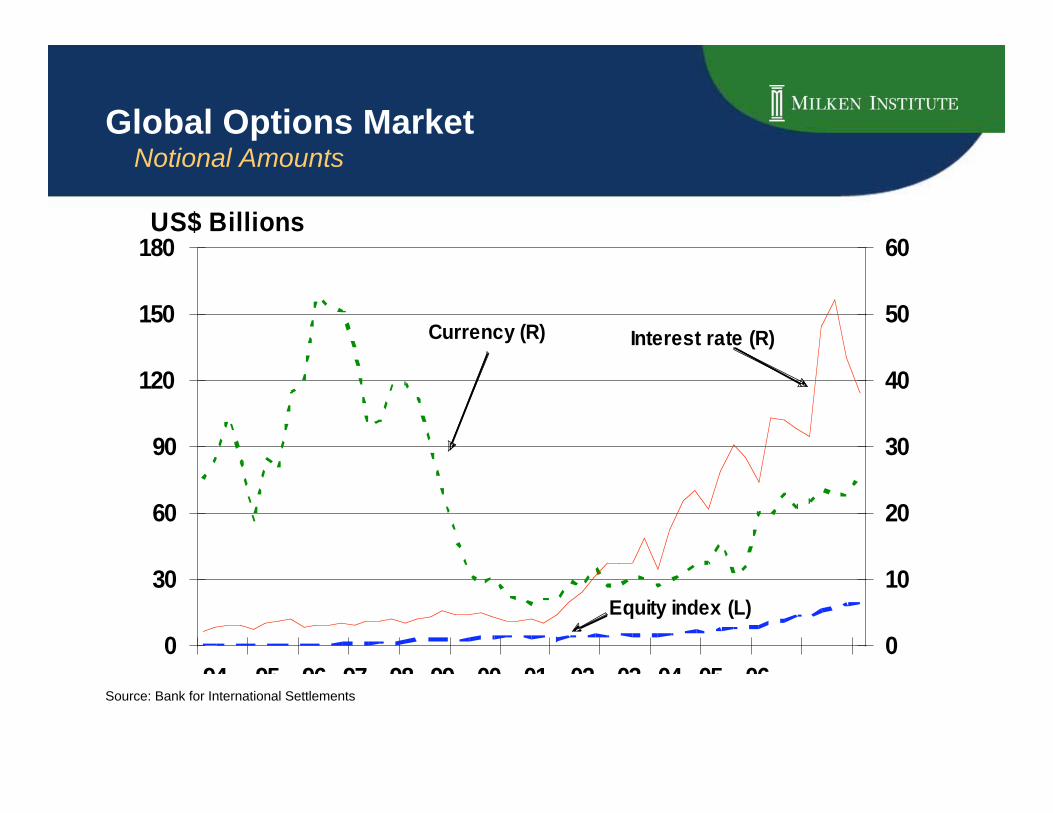

Global Options Market Notional Amounts

Source: Bank for International Settlements

Currency (R) Interest rate (R)

Equity index (L)

0

30

60

90

120

150

180

0

10

20

30

40

50

60US$ Billions

94 95 96 97 98 99 00 01 02 03 04 05 06

Global Credit Derivatives Market

0.2 0.3 0.4 0.6 0.9 1.2 2.03.5

5.0

20.2

33.1

0

5

10

15

20

25

30

35

1996 1997 1998 1999 2000 2001 2002 2003 2004 2006 2008

(est.)

US$ Trillions

Source: British Bankers’ Association

Global Derivative Markets:Rating of Underlying Assets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

99-00 01-02 03-04 05-06 07-08 (Est.)

Below B BB B A BBB AAA AASource: British Bankers’ Association

Banking Crises Since Late 1970s 168 Crises in 138 Countries

117 Systemic in 93 Countries

51 Nonsystemic in 45 Countries

Information not AvailableSource:Caprio, Gerard and Daniela Klingebiel (2003)

Argentina (1980-1982)Indonesia (1997-ongoing)

Chile (1981-1983)Thailand (1997-ongoing)

Uruguay (1981-1984)South Korea (1997-ongoing)

Côte d'Ivoire (1988-1991)Venezuela (1994-1997)

Japan (1992-ongoing)Mexico (1994-ongoing)

Malaysia (1997-ongoing)Slovenia (1992-1994)

Brazil (1994-1996)Philippines (1983-1987)Bulgaria (1996-1997)Ecuador (1996-ongoing)

Czech Republic (1991-present)Finland (1991-1994)

Hungary (1991-1995)Senegal (1988-1991)

Norway (1987-1993)Spain (1977-1985)

Paraguay (1995-ongoing)Colombia (1982-1987)Sri Lanka (1989-1993)

Malaysia (1985-1988)Sweden (1991-1994)Indonesia (1992-1994)

Poland (1992-1995)United States (1984-1991)Ghana (1982-1989)

Turkey (1982-1985)Thailand (1983-1987)Australia (1989-1992)

Turkey (1994)New Zealand (1987-1990)

France (1994-1995)Argentina (1995)Egypt (1991-1995)Philippines (1998-ongoing)

0 10 20 30 40 50 60

Percent of GDP

Indonesia50%

Thailand33%

S. Korea27%

UnitedStates

3%

Cost of Resolving Bank Problems

Share of World Oil Production 2005

Total: 81.1 million Barrels per Day

Rest of World

31%

Nigeria

3%

U.A.E.

3%

Kuwait

3%

Norway

4%Venezuela

4%

Saudi Arabia

14%

Iran

5%

Russia

12%

United States

8%

Mexico

5%

Canada

4%China

4%Source: BP

Share of World Oil Consumption 2005

Total: 82.5 million Barrels per Day

Rest of World

45%

Canada

3%

United States

25%

Russia

3%

China

8%

Japan

7%

Germany

3%

South Korea

3%

India

3%Source: BP

Oil Reserves Concentrated inUnstable Regions

Sources: Energy Information Administration

Middle East

60%

Africa

10%

Venezuela

6%

Russia

5%

Other

3%

Canada

14%

United States

2%

Global Demand for Oil ExceedsRefinery Capacity

Source: EIA

50

60

70

80

90

1980 1985 1990 1995 2000 2005

Oil Demand

Refinery Capacity

Thousand Barrels per Day

Rising Global Prices of Oil, Gold and Food

Source: Bloomberg, Datastream

Crude Oil

Food

Gold

50

100

150

200

250

300

350

400

January 2002 = 100

2002 2003 2004 2005 2006

World Gas Prices November 2006

Source:GTZ

0

1

2

3

4

5

6

7

Venezuela Libya Nigeria China S Africa Japan France Italy

$ Per Gallon

Iran S. Arabia U.S. Mexico India Brazil Germany U.K.

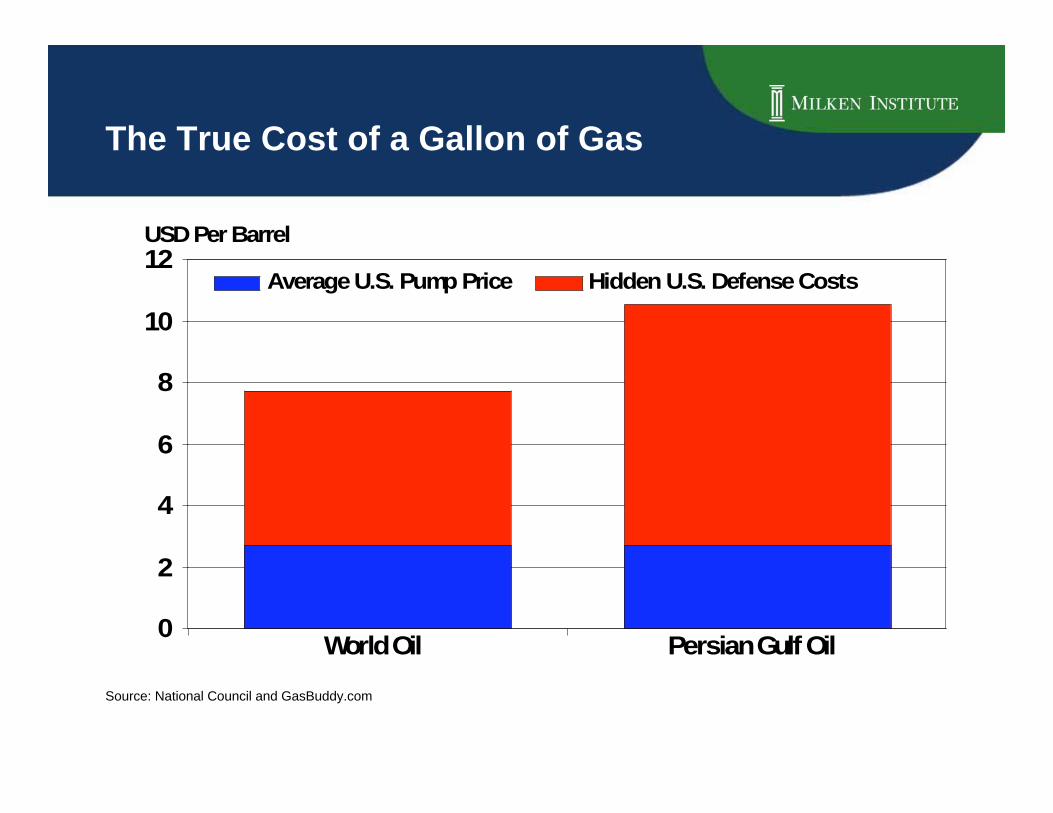

The True Cost of a Gallon of Gas

Persian Gulf OilWorld Oil

12

10

8

6

4

2

0

USD Per Barrel

Average U.S. Pump Price Hidden U.S. Defense Costs

Source: National Council and GasBuddy.com

Energy Prices and TaxesUS Dollars Per Gallon, 2006

0 1 2 3 4 5 6 7

TurkeyNorway

United KingdomGermany

ItalyFranceKorea

PolandJapan

FinlandLithuaniaAustralia

IndiaEcuador

BrazilCanada

South AfricaUnited States

GhanaJamaicaMexico

ArgentinaGuatemala

ChinaRussia

Saudi ArabiaIndonesia

Venezeula

Price Before Tax

Tax

Source: World Economic Outlook, 2006

China and India’s Energy Efficiency Energy Consumed per $ 1,000 GDP

Sources: BP, World Economic Outlook

0.0

0.4

0.8

1.2

1.6

2.0

1980 1985 1990 1995 2000 2005

China

India

United States

Tonnes Oil Equivalent Per US$ 1,000 GDP

Volatile Oil and Natural Gas Prices

Sources: Energy Information Administration

0500959085

$80

$70

$60

$50

$40

$30

$20

$10

$12

$10

$8

$6

$4

$2

$0

US dollars per barrel US dollars per Thousand Cubic

WTI Crude Oil PriceNatural Gas Price

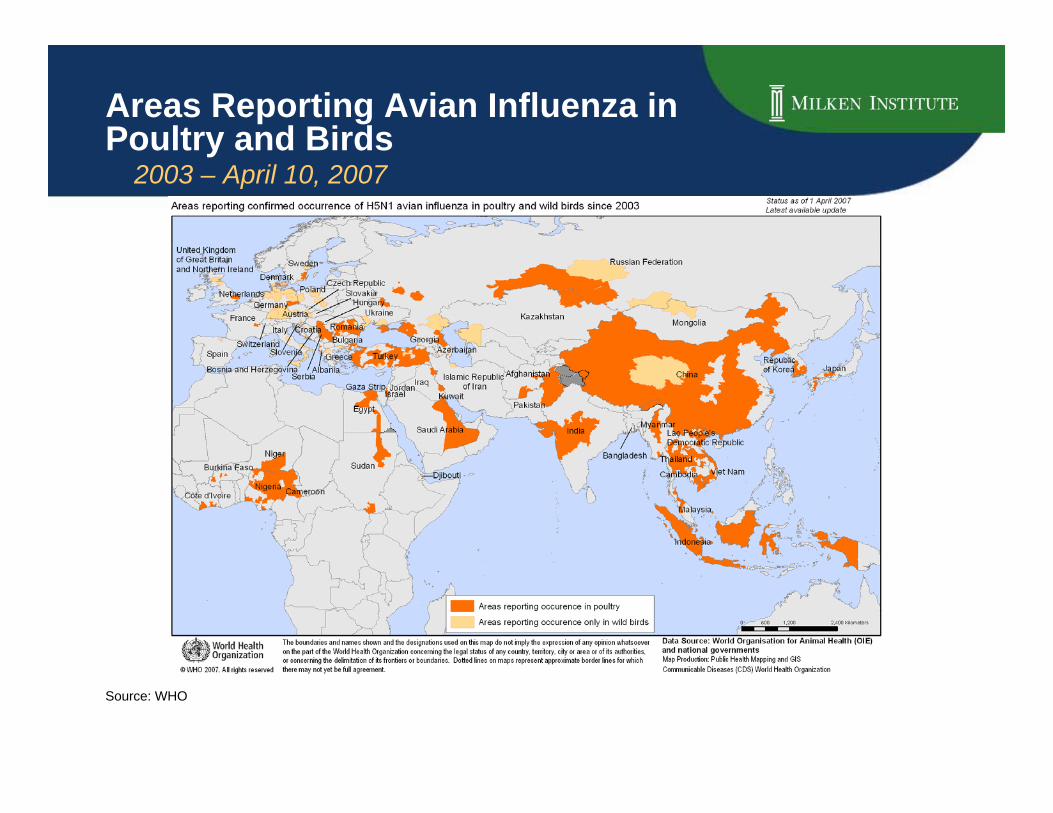

Areas Reporting Avian Influenza inPoultry and Birds 2003 – April 10, 2007

Source: WHO

Malaria Distribution Where Malaria is Endemic

Source: Malaria-vaccines.org

Tuberculosis Distribution 100 or More Cases Per 100,000 People

Source: University of South Carolina

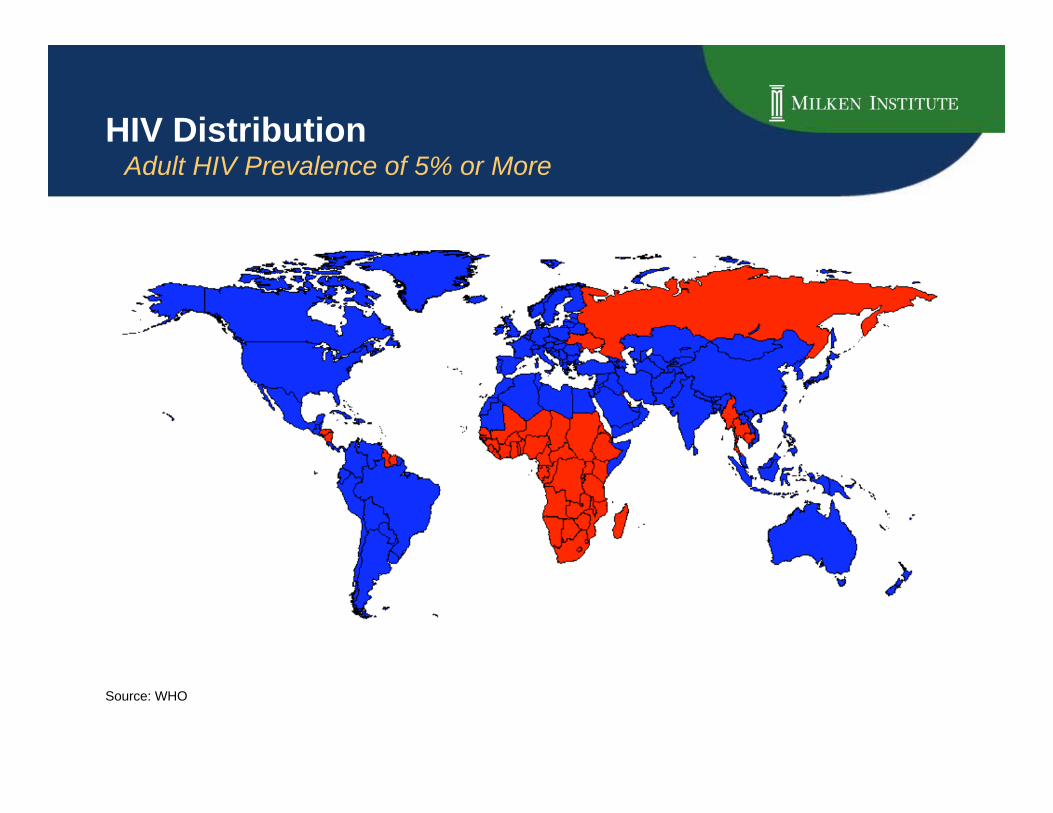

HIV Distribution Adult HIV Prevalence of 5% or More

Source: WHO

Hepatitis B Distribution Prevalence of 7% or More

Source: CIA

Water ShortagesHigh Vulnerability to Water Scarcity

Source: World Resources Institute

World Hunger 20% or More Undernourished

Source: World Resources Institute

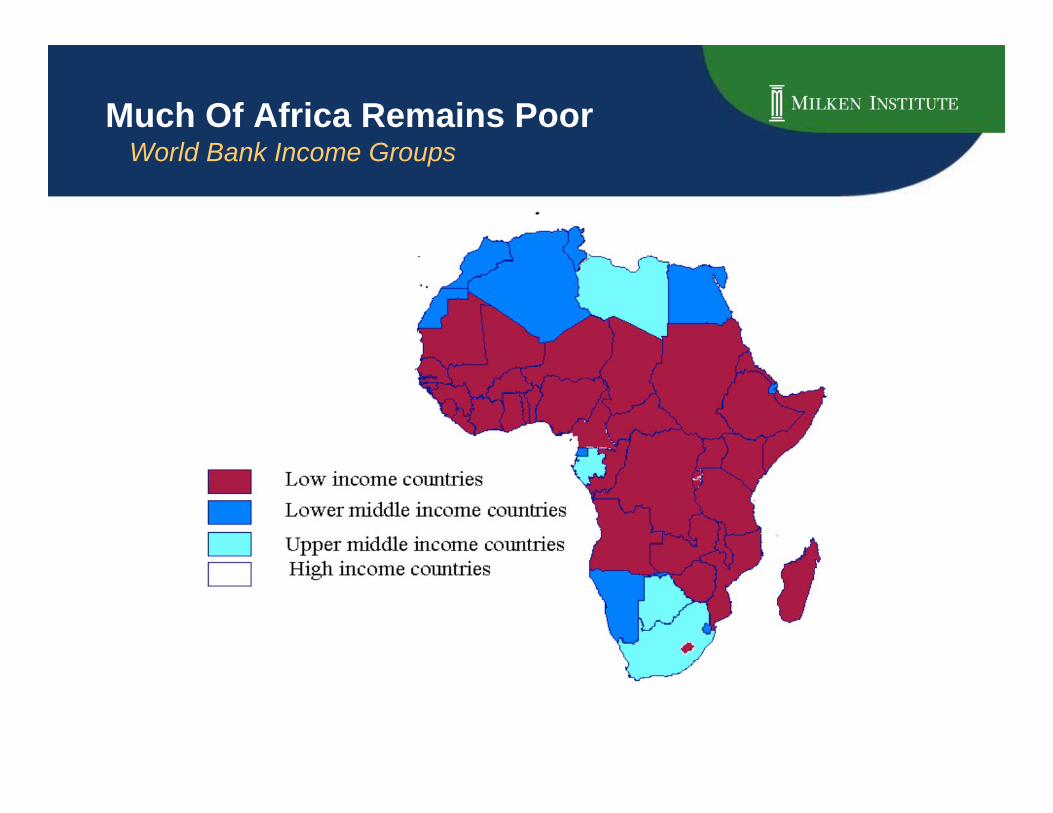

Much Of Africa Remains PoorWorld Bank Income Groups

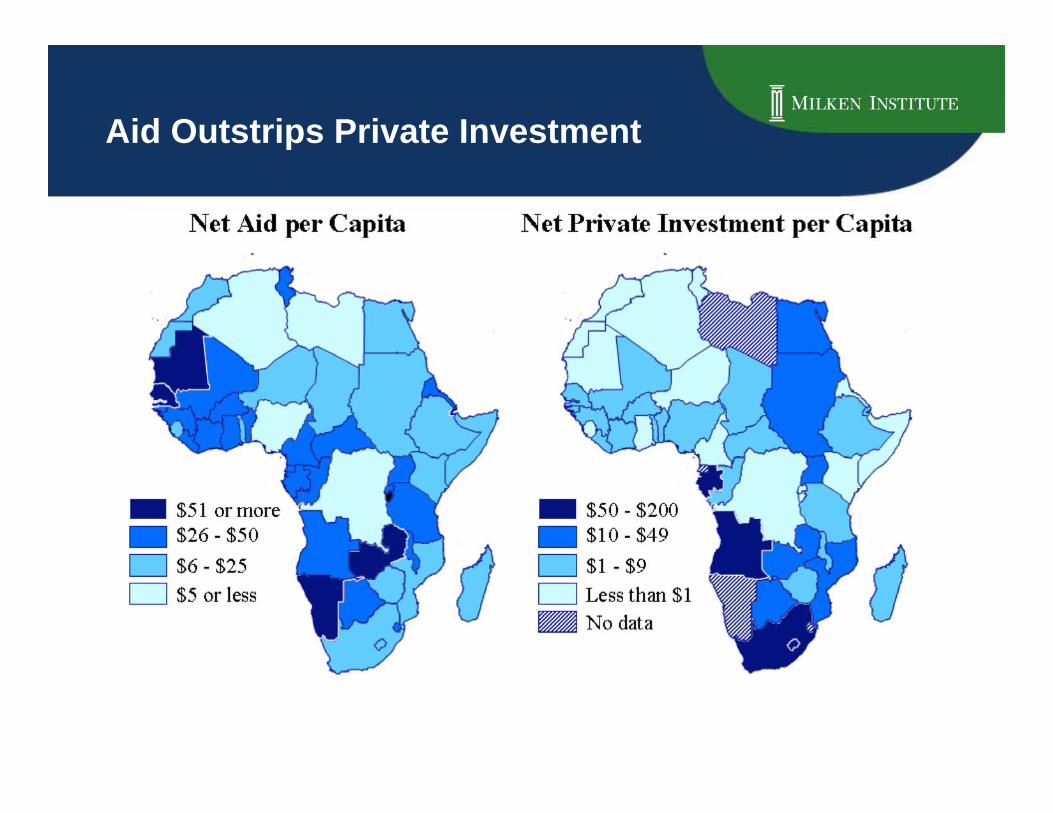

Aid Outstrips Private Investment

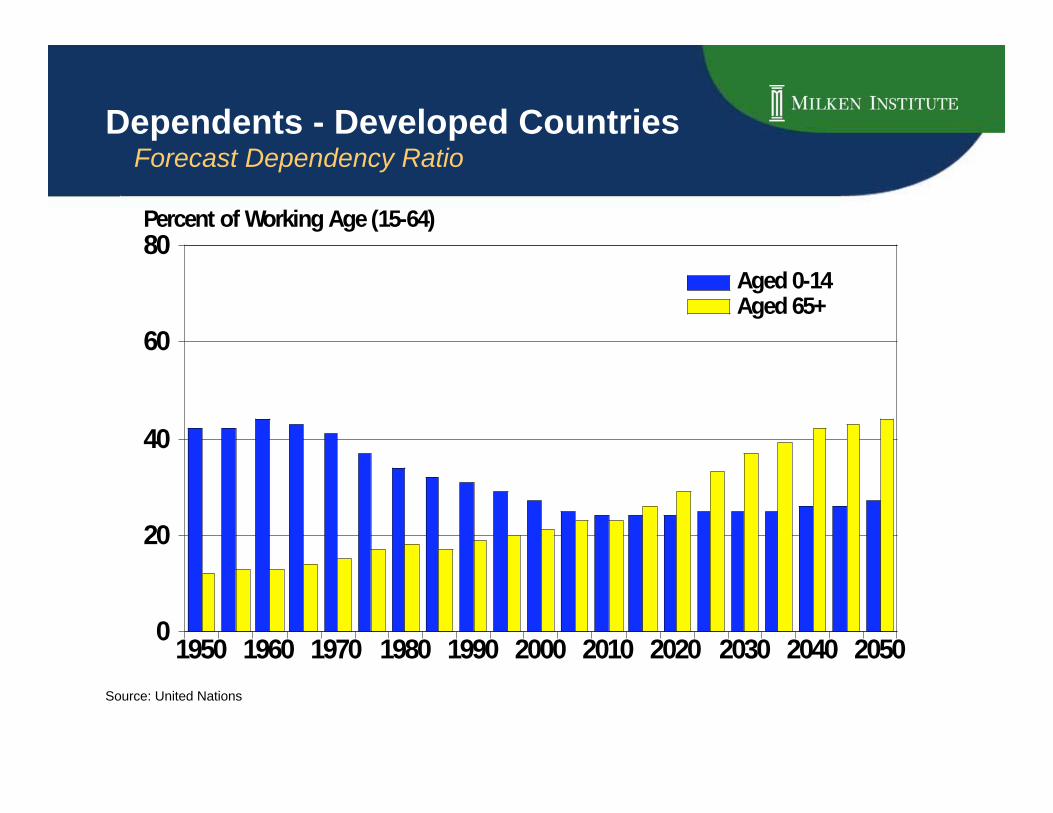

Dependents - Developed Countries Forecast Dependency Ratio

20502040203020202010200019901980197019601950

80

60

40

20

0

Percent of Working Age (15-64)

Aged 0-14Aged 65+

Source: United Nations

20502040203020202010200019901980197019601950

80

60

40

20

0

Percent of Working Age (15-64)

Aged 0-14Aged 65+

Source: United Nations

Dependents - Developing Countries Forecast Dependency Ratio

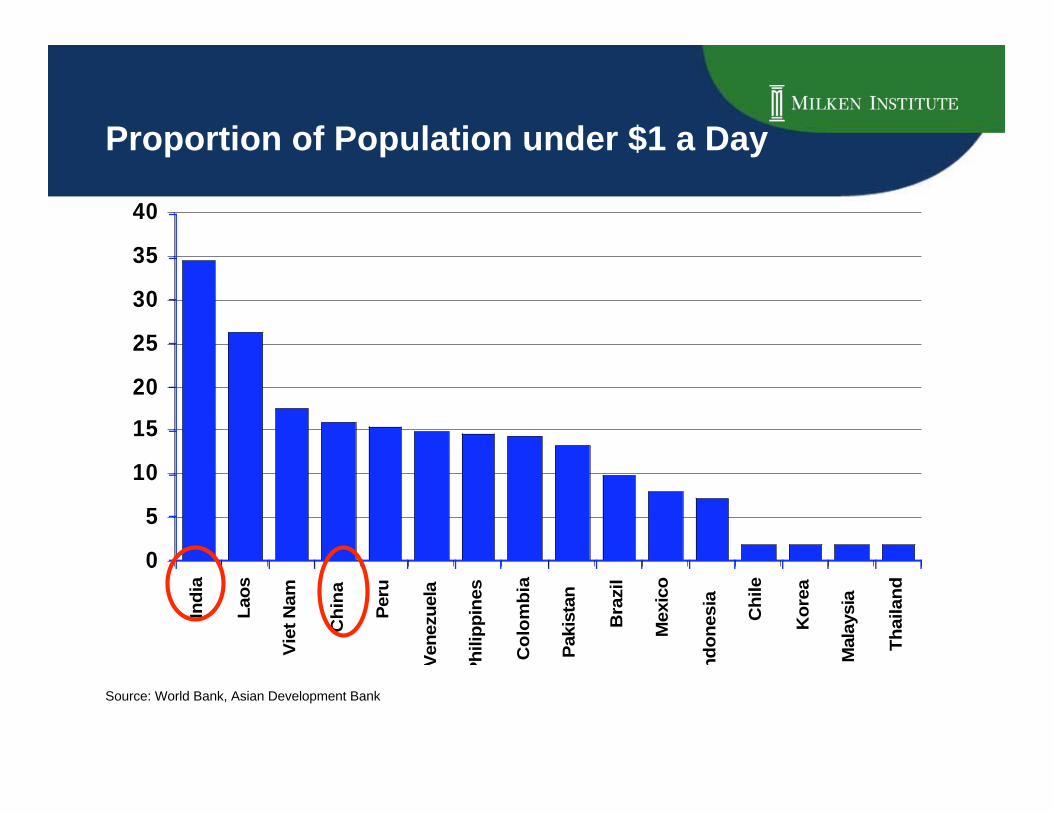

0

5

10

15

20

25

30

35

40In

dia

Lao

s

Vie

t N

am

Ch

ina

Peru

Ven

ezu

ela

Ph

ilip

pin

es

Co

lom

bia

Pakis

tan

Bra

zil

Mexic

o

nd

on

esia

Ch

ile

Ko

rea

Mala

ysia

Th

ailan

d

Source: World Bank, Asian Development Bank

Proportion of Population under $1 a Day

Catastrophic Risk on the Rise Global Number of Catastrophic Events, 1979 – 2004

Sources: Allstate Insurance Company

0

50

100

150

200

250

1979 1984 1989 1994 1999 2004

Natural Catastrophes

Man-Made Disasters

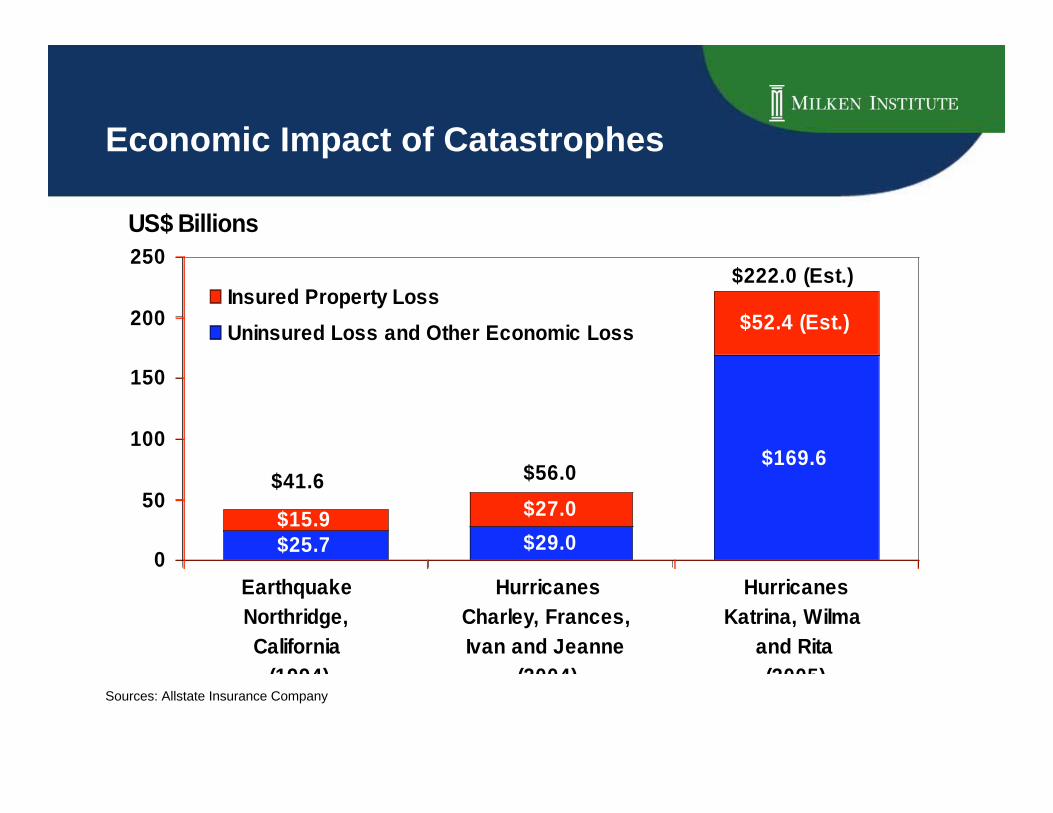

Economic Impact of Catastrophes

Sources: Allstate Insurance Company

$25.7 $29.0

$169.6

$15.9$27.0

$52.4 (Est.)

0

50

100

150

200

250

1 2 3

Insured Property Loss

Uninsured Loss and Other Economic Loss

Earthquake

Northridge,

California

(1994)

Hurricanes

Charley, Frances,

Ivan and Jeanne

(2004)

Hurricanes

Katrina, Wilma

and Rita

(2005)

US$ Billions

$41.6 $56.0

$222.0 (Est.)

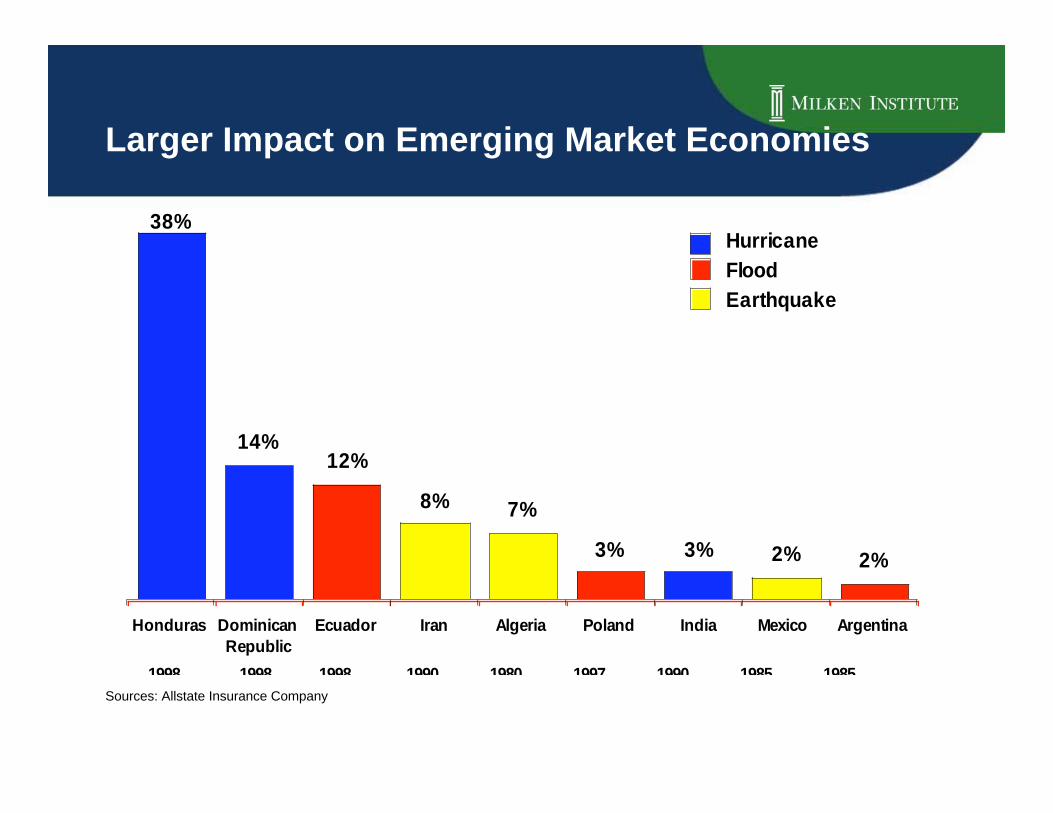

Larger Impact on Emerging Market Economies

Sources: Allstate Insurance Company

38%

14%12%

8% 7%

3% 3% 2% 2%

Honduras Dominican

Republic

Ecuador Iran Algeria Poland India Mexico Argentina

Hurricane

Flood

Earthquake

1998 1998 1998 1990 1980 1997 1990 1985 1985

Top 10 Military Spending Countries 2006

31.3Saudi Arabia

21.3India

32.1Italy

32.4Russia

44.9China

46.0Japan

57.5Germany

60.0France

66.2United Kingdom

532.8United States

Billion $MilitarySpending

Source: The World Factbook, CIA

4 0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0Max = 10

U.S.

Hong Kong

China

Russia

Brazil

India

United Kingdom

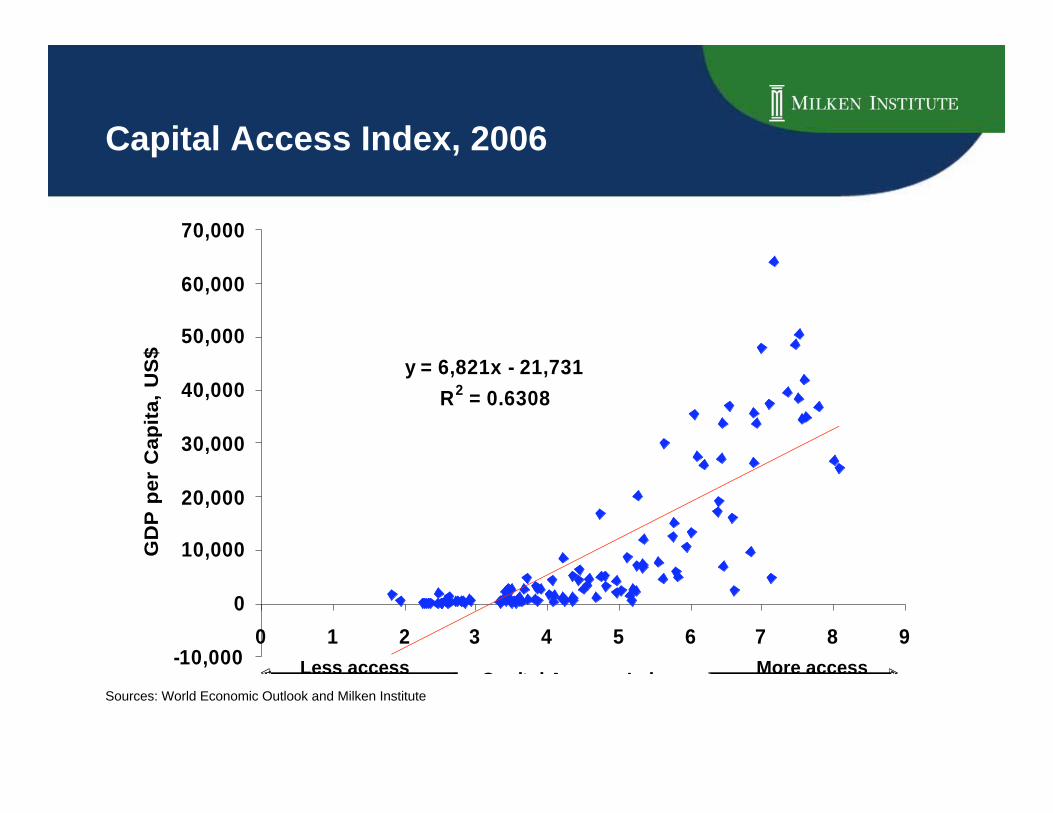

Capital Access Index 2006 Gauging Entrepreneurial Access to Capital

Source: Milken Institute

Capital Access Index, 2006

Less access More access

Sources: World Economic Outlook and Milken Institute

y = 6,821x - 21,731

R2 = 0.6308

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0 1 2 3 4 5 6 7 8 9

C it l A I d

GD

P p

er

Ca

pit

a,

US

$

Improved Capital Access CanAdd Billions to Emerging Economies

1.71.7India

2.41.7Pakistan

4.52.0Argentina

5.72.5Russia

15.72.6Mexico

Forgone GDP

US$ Billions

Forgone GDPGrowth %

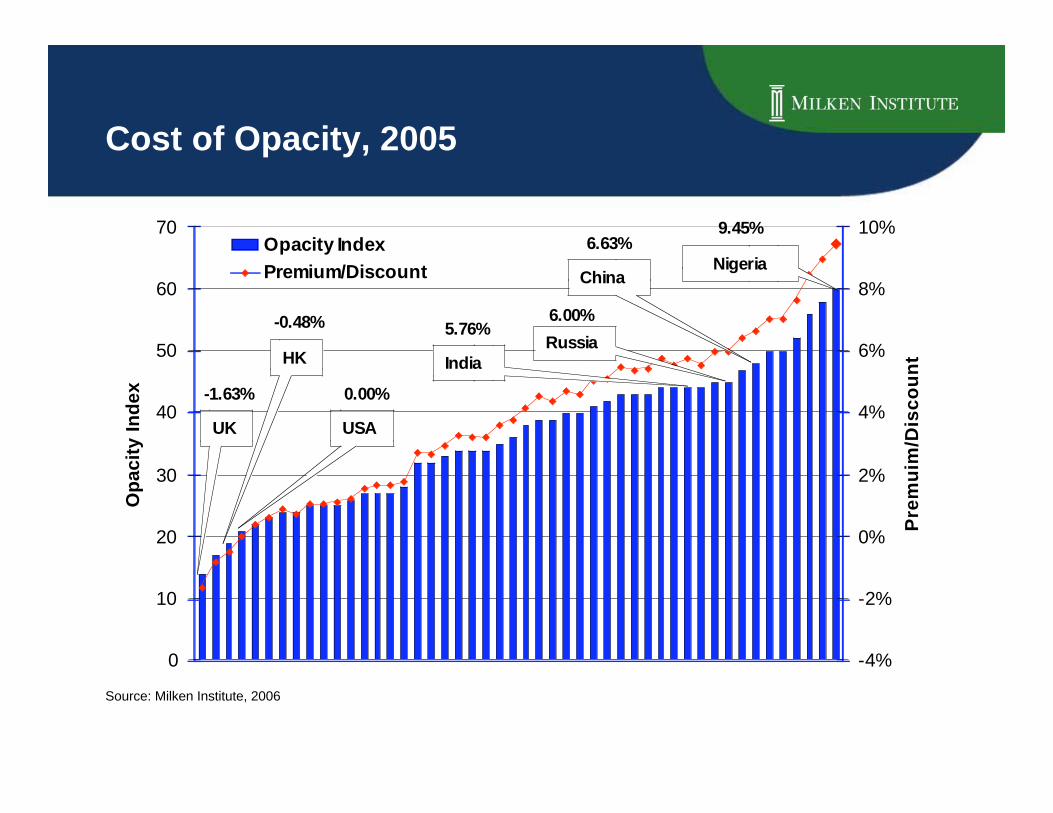

Cost of Opacity, 2005

Source: Milken Institute, 2006

6.00%

9.45%

-1.63%

-0.48%

0.00%

6.63%

5.76%

0

10

20

30

40

50

60

70

Op

ac

ity

In

de

x

-4%

-2%

0%

2%

4%

6%

8%

10%

Pre

mu

im/D

isc

ou

nt

Opacity Index

Premium/Discount Nigeria

UK

HK

USA

China

India

Russia

0

500

1000

1500

2000

2500

1968 1973 1978 1983 1988 1993 1998 2003

Nu

mb

er

of

Incid

en

ts

0

2000

4000

6000

8000

10000

12000

14000

Nu

mb

er

of

Fata

liti

es a

nd

In

juri

es

Incidents

Fatalities and Injuries

Oct. 23, 1983, Lebanon

June 25, 1985,

Canada

Dec. 21, 1988,

U.K.

Airline

Mar. 12, 1993, India

Jan. 11, 1998,

Algeria

Business

Aug. 7, 1998, Kenya

Diplom atic

Aug. 11, 2001,

Angola

Transportation

Sept. 11, 2001,

U.S.

Business

Feb. 21, 2004, Uganda,

Private

Sept. 1, 2004,

Russia

Educational

Apr. 1988,

Pakistan

Military

Feb. 26, 1993,

U.S.

Business

May 20, 1995,

Japan

Transportation

Jan. 31, 1996, Sri

Lanka

Business

Oct. 22, 2002,

Russia

Private

Mar. 11, 2004,

Spain,

Transportation

Sources: MIPT and Milken Institute staff calculation

Terrorist Attacks Are BecomingMore Frequent and More Intensive

0

5

10

15

20

25

30

2005 2002 1990

Percent

Corporate Crisis by Category

White Collar CrimeMismanagementClass Action Law SuitsLabor DisputesCatastrophesCasualty AccidentsDefects/RecallsConsumer Activism

DiscriminationFinancial DamagesWorkplace ViolenceEnvironmentExecutive DismissalSexual HarassmentHostile TakeoverWhistle Blowers

Sources: Institute for Crisis Management, 2007

Percent of Total Crisis