u.s.-mexico dual taxation: residency rules, filing...

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE PROGRAM

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext. 1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

U.S.-Mexico Dual Taxation: Residency Rules, Filing

Requirements, Planning OpportunitiesTHURSDAY, JULY 18, 2019, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality FOR LIVE PROGRAM ONLY

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

July 18, 2019

U.S.-Mexico Dual Taxation: Residency Rules, Filing Requirements, Planning Opportunities

Patrick J. McCormick, J.D., LL.M., Principal

Drucker & Scaccetti

David A. Matos, CPA, CISA, CRFAC, RFI, Partner

MATOS & JAWAD PLLC

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Patrick J. McCormick, JD, LLM

U.S.-Mexico Dual

Taxation: Rules,

Requirements, and

Planning Opportunities

© Copyright 2018 Drucker & Scaccetti

PATRICK J. MCCORMICK

• Patrick J. McCormick is a principal with Drucker & Scaccetti, P.C. He earned his J.D. from Vanderbilt University Law School in 2008, and his LL.M. from New York University School of Law in 2009.

• The exclusive focus of Patrick’s practice is international taxation; Patrick regularly publishes articles and gives presentations on all areas of international tax law, with a significant subset of his clients having Mexican assets and/or residency.

6

INTRODUCTION

• Mexican taxpayers – whether individual or corporate –

increasingly engage in United States business activities

• For individuals, United States investments can be

intertwined with exploration of United States residency

• Significant planning opportunities exist in the pre-U.S.

taxpayer period

• Mexican corporate entities with United States operations

are subject to tax on United States-sourced business profits

• United States taxpayers with Mexican operations are

also subject to special tax rules by both jurisdictions

• Cognizance of Mexican-specific factors – both from the tax

and business perspective – is critical when entering the

Mexican market

7

MEXICAN TAXPAYERS – UNITED STATES

INCOME TAX

• Under default U.S. rules, Mexican nonresident

aliens/corporate entities are subject to United States tax

on:

• (1) income effectively connected with a United States trade

or business, and

• (2) fixed or determinable annual or periodic income

• Non-U.S. taxpayers are subject to U.S. tax primarily

on income items sourced to the United States

• Detailed sourcing rules for income items exist; for example,

interest/dividend income is sourced to the payor’s location

• Rent/royalties sourced to the place of use of the asset

• Personal services sourced to where services performed

8

MEXICAN TAXPAYERS – EFFECTIVELY

CONNECTED INCOME

• Under default rules, income earned by individuals

effectively connected to a United States trade or

business is subject to tax

• “Trade or business” undefined in the Code/regulations – but

profit-oriented activities carried on in the United States

which are regular, substantial, and continuous are properly

classified as a trade or business for these purposes

• Effectively connected income includes performance of

U.S.-based personal services

• Macro-level – relatively light requirements to be

considered engaged in a U.S. trade or business

• Effectively connected income taxed by the United States at

graduated rates, with deductions/credits available

9

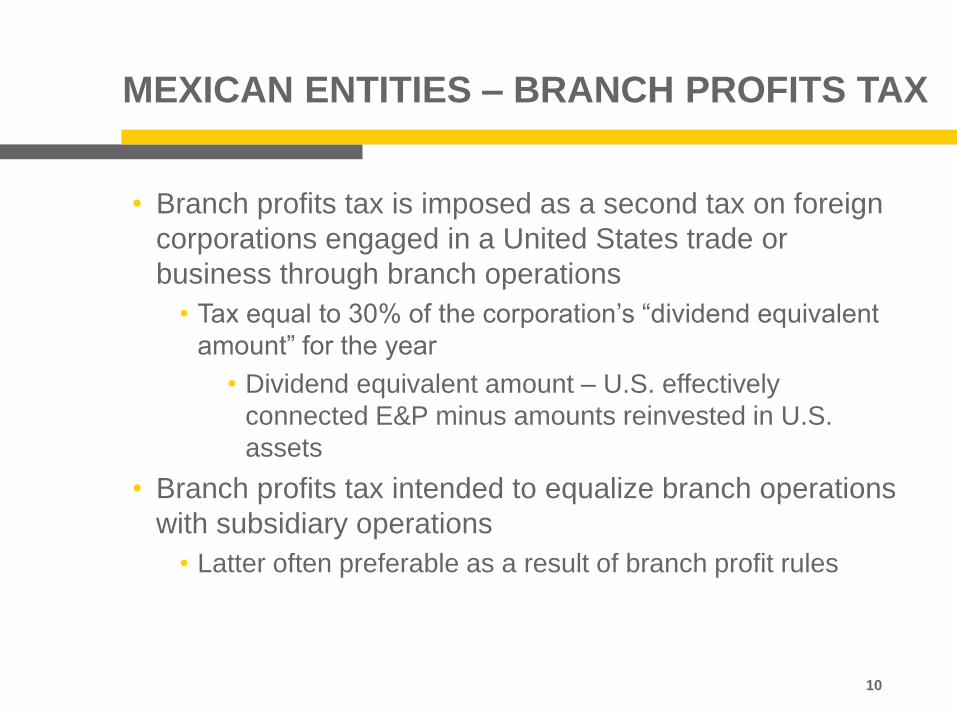

MEXICAN ENTITIES – BRANCH PROFITS TAX

• Branch profits tax is imposed as a second tax on foreign

corporations engaged in a United States trade or

business through branch operations

• Tax equal to 30% of the corporation’s “dividend equivalent

amount” for the year

• Dividend equivalent amount – U.S. effectively

connected E&P minus amounts reinvested in U.S.

assets

• Branch profits tax intended to equalize branch operations

with subsidiary operations

• Latter often preferable as a result of branch profit rules

10

MEXICAN TAXPAYERS – FIRPTA

• Under the Foreign Investment in Real Property Tax Act of 1980, gain from disposition of United States real property interest by a foreign taxpayer is subject to tax

• Gains are automatically classified as ECI!

• United States real property interest: any interest in United States real property or an interest in a domestic corporation unless such corporation was not a United States real property holding corporation for the prior five years

• United States real property holding corporation: corporation where more than 50% of the corporation’s assets are United States real property interests

• Transferee must withhold on disposition at a rate of 15% of the amount realized

• Vitally, nonresident aliens generally not subject to capital gains tax on non-ECI U.S.-sourced gains

11

MEXICAN TAXPAYERS – FDAP INCOME

• Fixed or determinable annual or periodic income (“FDAP income”) also subject to tax by the United States (for income items sourced to the U.S.)

• FDAP income functions as a catch-all for U.S.-sourced income items (aside from capital gains) not otherwise subject to U.S. tax

• Includes interest (subject to expansive exceptions), dividends, rent, salaries, wages, premiums, annuities, compensation, remuneration, etc.

• Interplay exists between ECI and FDAP income

• US-sourced income is classified as effectively connected to a U.S. trade or business rather than FDAP if it satisfies an asset use test or a business activities test

• FDAP income generally subject to a flat 30% rate of tax (with tax collected through withholding by payors)

• Deductions not permitted for FDAP income

12

MEXICAN TAXPAYERS – U.S.-MEXICO INCOME

TAX TREATY

• The United States and Mexico maintain an income tax

treaty, which (upon election) can alter tax ramifications

for Mexican taxpayers with United States-sourced

income

• Under treaties, residents of a treaty country can be taxed at

a reduced rate, or even exempted from tax, on specified

items of income from the other country

• i.e. withholding taxes on United States-sourced income

• Savings clause prevents a United States

citizen/resident/entity from using a tax treaty to alter tax on

US-source income

• Treaty-based positions generally must be disclosed

• Subject to exemptions under the Regulations

13

MEXICAN TAXPAYERS – U.S.-MEXICO INCOME

TAX TREATY

• Residency takes on importance in this realm – generally foreign taxpayers are entitled to treaty benefits only when they are residents of a treaty party country

• Treaty definitions of residence normally include persons liable for tax to a country based on domicile, residence, citizenship, place of management, or place of incorporation

• Corporations are residents of countries for these purposes if liable for tax based on the country being its place of management

• Can have conflicts as to residence where place of management and place of incorporation differ

• Tiebreaker typically is the treaty between those two countries

• Rules exist to prevent “treaty shopping” – entity creation solely for purposes of treaty benefits

4-16

14

MEXICAN TAXPAYERS – U.S.-MEXICO INCOME

TAX TREATY

• Treaty modifications for business income – “effectively

connected to a United States trade or business” shifted to

business profits attributable to a permanent establishment

• Treaty Article 7(1)

• Heightened standard for U.S. taxation – though threshold still

low

• Dividends – if a U.S. company pays a dividend to a Mexican

shareholder, the U.S. tax rate is capped at 10% (and can be

reduced to 0 or 5% under specified circumstances)

• Treaty Article 10(2)

• Branch profits tax generally reduced so that tax ramifications of

U.S. branch operations match U.S. subsidiary ramifications

15

MEXICAN TAXPAYERS – U.S.-MEXICO INCOME

TAX TREATY

• Treaty modifications for independent (non-employee) personal services – income taxable if attributable to a regularly available fixed base or if nonresident spends >183 days in source country in a 12-month period

• Treaty Article 14(1)

• Treaty modifications for dependent (employee) personal services – income taxable by source country except if (1) employee present in source country for <184 days, (2) compensation paid by an employer not a resident of the source country, and (3) compensation not deducted by a permanent establishment or fixed base of the employer in the source country

• Treaty Article 15(1)

4-16

16

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

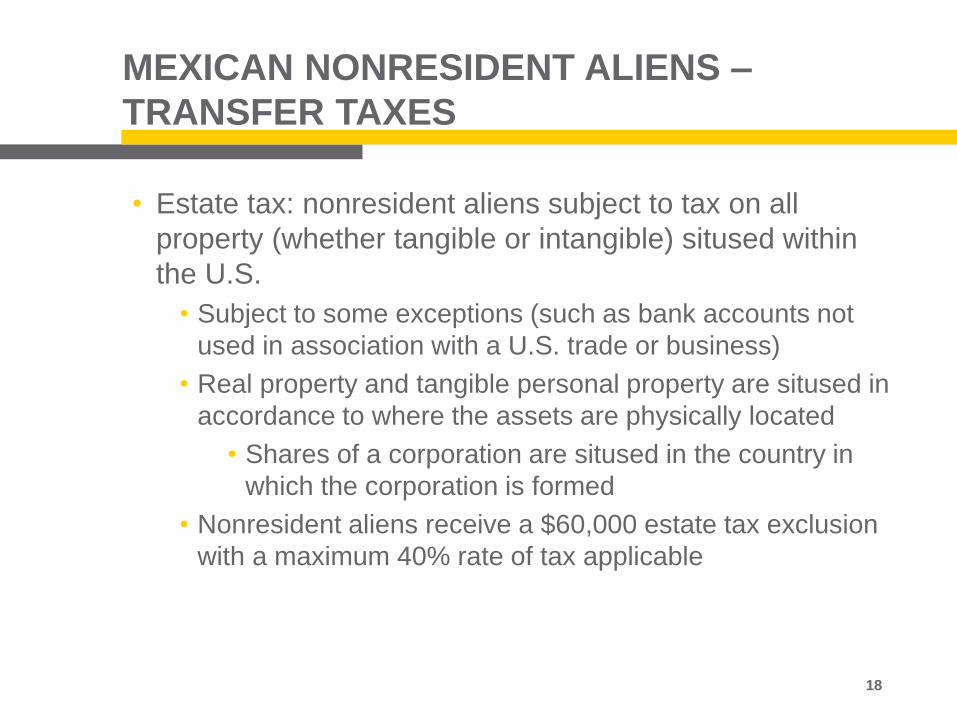

• Estate tax: nonresident aliens subject to tax on all

property (whether tangible or intangible) sitused within

the U.S.

• Subject to some exceptions (such as bank accounts not

used in association with a U.S. trade or business)

• Real property and tangible personal property are sitused in

accordance to where the assets are physically located

• Shares of a corporation are sitused in the country in

which the corporation is formed

• Nonresident aliens receive a $60,000 estate tax exclusion

with a maximum 40% rate of tax applicable

18

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

• Gift tax: nonresident aliens normally are subject to gift

tax on lifetime gratuitous transfers of tangible property

within the United States

• Generally comprising real property situated within the

country and tangible personal property within the U.S. at

the time of the gift, including hard currency or cash situated

within the U.S.

• Intangible property (i.e. shares of a corporation) is not

subject to gift tax for nonresident alien donors

• No specific gift tax exclusion for nonresident aliens,

though the $15,000 per donee annual exclusion is

available

19

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

• What isn’t subject to transfer tax?

• Non-U.S. sitused assets are not subject to U.S. transfer tax

when donor is a NRA

• Foreign property, foreign holdings are not subject to

U.S. transfer taxes

• Intangible assets are not subject to gift tax for NRA donor

regardless of situs

• i.e. stock in a U.S. corporation generally will not be

subject to gift tax

• Reliance on ability to gift asset pre-death to remove

from taxable estate an option, but carries risk (i.e.

sudden death)

20

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

• How should Mexican nonresident alien investments into

the United States be structured?

• Nonresident alien investors typically focus on three United

States tax factors: (1) income tax consequences, (2)

estate/gift tax consequences, (3) anonymity; and (4)

simplicity of structure/minimization of filing requirements

• Anonymity – nondisclosure of identity to the United

States government

• Foreign corporations do not face estate/gift tax exposure,

but are subject to branch profits tax

• Branch profits tax avoidance available by having

foreign corporation own a separate U.S. corporation

21

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

• Common ownership structures

• Individual ownership of a U.S.-sitused income generating

asset (or ownership through a DRE)

• Benefits: exemption from capital gains tax (if gain from

asset sale not classified as ECI – real estate gains not

exempt), long-term assets which are ECI subject to

capital gains rates on disposition (though can be

subject to FIRPTA withholding)

• Detriments – estate/gift tax exposure, need to file

individual U.S. tax returns if ECI generated

22

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

• Common ownership structures

• Ownership of a U.S.-sitused income generating asset

through a foreign corporation

• Benefits: same exemption from capital gains tax as for

NRA ownership; protection from estate/gift tax

exposure (as NRA owns a foreign corporation – non-

U.S. sitused asset); subject to corporate tax rates on

income

• Detriments – exposure to branch profits tax on earned

income; Form 1120-F can require disclosure of

underlying ownership; no differentiated tax rate for

LTCG

23

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

• Common ownership structures

• Ownership of a U.S.-sitused income generating asset

through a foreign corporation owned by a domestic

corporation

• Benefits: protection from estate/gift tax exposure; no

branch profits tax; no disclosure of ownership required

(as Form 1120 filed showing foreign corporation as

owner); subject to corporate tax rates on income

• Detriments – no differentiation for LTCG; no exemption

for non-ECI capital gains (as asset owned by domestic

corporation)

24

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

• Common ownership structures

• Ownership of a U.S.-sitused income generating asset

through a foreign nongrantor trust

• Benefits: protection from estate/gift tax exposure; no

branch profits tax; subject to LTCG rates

• Detriments – potential ramifications for U.S.

beneficiaries of trust; need disclosure of identity on tax

return; subject to individual tax rates on ordinary

income

25

MEXICAN NONRESIDENT ALIENS –

TRANSFER TAXES

• Critically, proper structure will hinge on the specific

investment – and investor - involved

• Multitude of questions needs to be asked in order to

properly structure the investment’s ownership

• Questions will typically focus on the types of

income/gains anticipated from an investment, the type

of taxpayer making the investment, treaty application,

etc.

• Additional layer of questions – what are the Mexican tax

implications?

26

U.S. TAXPAYERS – INCOME TAXES

• United States citizens and residents are taxable on their

worldwide income

• Sourcing determinations less relevant – taxable on all

income, whether domestic or foreign-sourced

• Foreign tax credits alleviate burdens of double taxation

for U.S. taxpayers with Mexican-sourced income

• Generally, citizens/residents utilize FTC rather than income

tax treaties

• Tax treaties contain “saving” clause, exempting

citizens/residents from most treaty benefits

• United States taxpayers subject to capital gains on

worldwide asset dispositions

27

U.S. TAXPAYERS – INCOME TAXES

• Which individuals are U.S. taxpayers?

• Citizenship – persons born in the United States, naturalized in the United States, or (under specified circumstances) where parents were United States citizens at the time of their birth

• Classified as a “resident” for United States income tax purposes under default rules if:

• Lawfully admitted for permanent residence (green card holder); or

• Meet substantial presence requirements

• Substantial presence – 31 days in the current year in the United States and the sum of days in the last three years (after applicable multipliers) exceeds 183

28

U.S. TAXPAYERS – INCOME TAXES

• Which individuals are U.S. taxpayers?

• Special rules exist which can reclassify individuals who meet U.S. tax residency requirements as nonresident aliens

• “Closer connection exception” can reclassify substantial presence residents as NRAs

• U.S.-Mexico Treaty Art. 4(2) – if an individual is treated as a resident of both the U.S. and Mexico under default rules, tiebreaker provisions reclassify them as a resident of only one

• Applies to substantial presence residents and green card holders!

• Both closer connection/treaty tiebreaker rules inapplicable to citizens

29

U.S. TAXPAYERS – INCOME TAXES

• Pre-immigration transfer tax planning options where a Mexican nonresident alien seeks become a resident/citizen (i.e. investor looking for residency options)?

• Income tax: goal is to achieve basis step-ups (on non-U.S. assets) and income recognition (on non-U.S. income) prior to U.S. taxpayer status

• Transfer tax: want to transfer non-United States assets prior to residency/citizenship if potentially be subject to domestic transfer taxes (and can live without the assets to be transferred)

• Whether an individual will face transfer tax exposure depends on a multitude of variables – length of anticipated stay, age/asset growth potential, potential for reduction in citizen/resident exemption amounts

30

U.S. TAXPAYERS – INTERESTS IN MEXICAN

ENTITIES

• Special tax rules come into play for U.S. taxpayers with interests in foreign corporations

• Technically, the foreign corporation is respected as a separate taxpayer; however, current inclusion (irrespective of corporate distributions) can be required for U.S. shareholders

• Subpart F/GILTI regimes create current inclusion for significant income amounts if ownership thresholds met

• Passive foreign investment company (“PFIC”) rules do not require ownership thresholds, and carry potential for punitive tax ramifications on dispositions/excess distributions

• Special anti-deferral rules inapplicable to flow-through entities – because no deferral occurs!

• Threshold question: How is a Mexican entity classified for U.S. tax purposes?

31

U.S. TAXPAYERS – INTERESTS IN MEXICAN

ENTITIES

• Foreign-domiciled business entities generally are able to elect their entity classification for United States tax purposes

• EXCEPTION: Per-se corporations (as listed in the Regulations)

• Mexican Sociedad Anonima automatically classified as a corporation under U.S. rules

• Default rules for classification exist, which hinge on the limited liability of owners/members

• If limited liability for owner/owners – association taxable as a corporation

• If no limited liability for at least one owner – partnership if multiple members, disregarded entity if one

• Elections out of default rules are available - can elect to be a partnership, corporation, or disregarded entity

• Election made on Form 8832 – initial election required within 75 days of entity becoming “relevant”

32

U.S. TAXPAYERS – INTERESTS IN MEXICAN

ENTITIES

• Subpart F imposes a direct tax on a U.S. shareholder of a controlled foreign corporation (“CFC”) as to the CFC’s Subpart F income

• Tax imposed directly on U.S. shareholder, regardless of whether distributions of income are made to the shareholder

• Provides a method for the United States to disincentivize transactions improperly sourcing income to foreign jurisdictions

• Threshold requirements must be met for Subpart F regime to apply

• Requirements: look to (1) whether a U.S. shareholder exists, (2) whether there is a CFC, and (3) whether the CFC has Subpart F income

• U.S. shareholder – United States person owning at least 10% of the foreign corporation’s voting stock or value

• Controlled foreign corporation exists if on any day during a given year U.S. shareholders own more than 50% of the stock of the foreign corporation

33

U.S. TAXPAYERS – INTERESTS IN MEXICAN

ENTITIES

Subpart F income is primarily comprised of “movable income” –income that can be shifted to foreign jurisdictions more easily

• Foreign base company income is typically the largest component of Subpart F income

• Includes foreign personal holding company income, foreign base company sales income, foreign base company services income, etc.

• Foreign personal holding company income: dividends, interest, rents, royalties, annuities

• Also includes certain net gains from sale of property which generates passive income

• Foreign base company sales/services income –look to activities outside the corporation’s country of domicile and the transactions with related persons

34

U.S. TAXPAYERS – INTERESTS IN MEXICAN

ENTITIES

• What if Subpart F application requirements are not met?• No mechanism for immediate tax is implemented; however,

prospective distributions by the foreign corporation (or dispositions of the shares of the foreign corporation) potentially subject to PFIC regime

• PFIC – punitive ramifications for shareholders of foreign corporations with significant passive income

• Income automatically classified as ordinary (taxable at highest rates), with an interest charge applicable based on the holding period for the interest

• Sec. 1297(d) – if a shareholder’s interest in a foreign corporation meets both Subpart F and PFIC requirements, only Subpart F applies

• Often preferable to apply Subpart F – tax accelerated, but punitive PFIC ramifications avoided

35

U.S. TAXPAYERS – INTERESTS IN MEXICAN

ENTITIES

• Under Sec. 951A, U.S shareholders of a controlled foreign corporation must include their share of global intangible low-taxed income in US tax

• GILTI: Excess of the shareholder’s net CFC tested income over the shareholder’s net deemed tangible income return

• U.S. shareholder and controlled foreign corporation concepts mirror Subpart F

• GILTI inclusion treated similarly to Subpart F in many ways, but not technically a component of Subpart F

• 50% deduction available for GILTI, but ONLY for C-Corporations!

• Makes the effective tax rate for corporate shareholders 10.5%

• For non-corporate U.S. shareholders, rate can be 37%

36

U.S. TAXPAYERS – INTERESTS IN MEXICAN

ENTITIES

• GILTI Application

• Functionally, GILTI essentially is tax imposed on U.S.

shareholders of a CFC on the excess of an assumed 10%

rate of return on tangible business assets of the CFC

• GILTI imposes a minimum tax on foreign earnings that

exceed a standard rate of return amount

• No direct reference to intangibles is made in Sec. 951A

• Aim may have been intangible income, but application

will be significantly more far-reaching, and not limited to

one type of income (i.e. movable income)

37

U.S. TAXPAYERS – DIRECT MEXICAN

ACTIVITIES

Foreign-Derived Intangible Income (“FDII”)

• A deduction is allowed to domestic corporations in an amount equal to 37.5% of the FDII of the domestic corporation for the tax year

• Deduction ONLY available to C-corporations!

• FDII equals deemed intangible income multiplied by a fraction: foreign-derived deduction eligible income over deduction eligible income.

• FDII is the portion of intangible income derived from serving foreign markets; like GILTI, it assumes a 10% rate of return on tangible assets

• FDII concept offers a special reduced effective tax rate on income from US-held intangibles; concept does not explicitly look at intangibles but assumes a fixed rate of return on business assets with the balance of income being from intangibles

38

U.S. TAXPAYERS – TRANSFER TAXES

• United States citizens/domiciliaries taxable on transfers

of worldwide assets, whether during life or at death

• However, given a lifetime exclusion of roughly $11.4 million

(as per TCJA increases)

• Treated as a domiciliary for estate/gift tax purposes when

maintaining a United States domicile – person is a United

States resident with no present intention of leaving

• Facts and circumstances determination – look to length

of stay, ties to U.S. versus other countries, etc.

• Imposes an elevated standard for presence-based tax

as compared to income tax requirements!

• No U.S.-Mexico estate/gift tax treaty!

39

U.S. TAXPAYERS – TRANSFER TAXES

• Special rules can apply to interests in/transfers to

Mexican trusts

• United States beneficiaries of foreign nongrantor trust are

subject to tax via the “throwback” rule on accumulated

distributions

• Replicates PFIC tax – creates punitive tax ramifications

• For foreign trusts created by a nonresident alien who

becomes a United States citizen or resident within five

years of transfers to the trust, the trust is treated as a

grantor trust if it has any United States beneficiaries

• Importantly, this rule applies for income tax purposes –

but NOT transfer tax purposes

40

41

U.S.-MEXICO: TAX

COMPLIANCE

David A. Matos, CPA, CISA, CRFAC, RFI

INTRODUCTION

David A. Matos

• Matos & Jawad PLLC – Partner

• Matos CPA LLC - Owner

• Pride International, Inc. - Country

Controller – Mexico

• Nabors, Inc. - Finance Director –

Mexico

• Weatherford, Inc. – Corp.

Accounting Systems Manager

• Continental Airlines – Sr.

Information Systems Auditor

• Deloitte & Touché - Systems

Auditor44

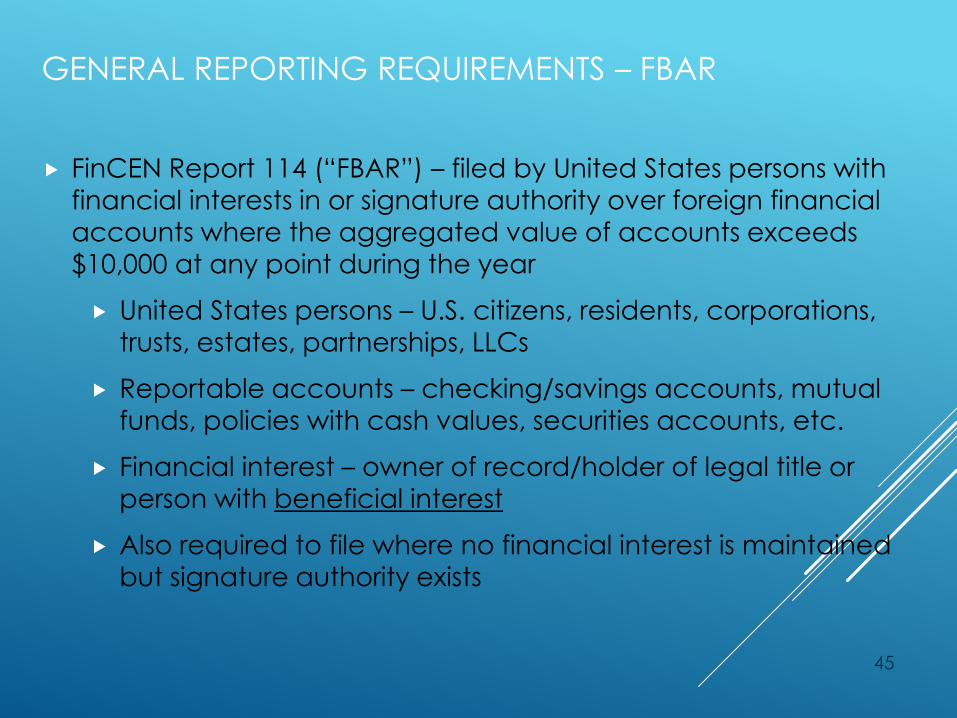

GENERAL REPORTING REQUIREMENTS – FBAR

FinCEN Report 114 (“FBAR”) – filed by United States persons with

financial interests in or signature authority over foreign financial

accounts where the aggregated value of accounts exceeds

$10,000 at any point during the year

United States persons – U.S. citizens, residents, corporations,

trusts, estates, partnerships, LLCs

Reportable accounts – checking/savings accounts, mutual

funds, policies with cash values, securities accounts, etc.

Financial interest – owner of record/holder of legal title or

person with beneficial interest

Also required to file where no financial interest is maintained but signature authority exists

45

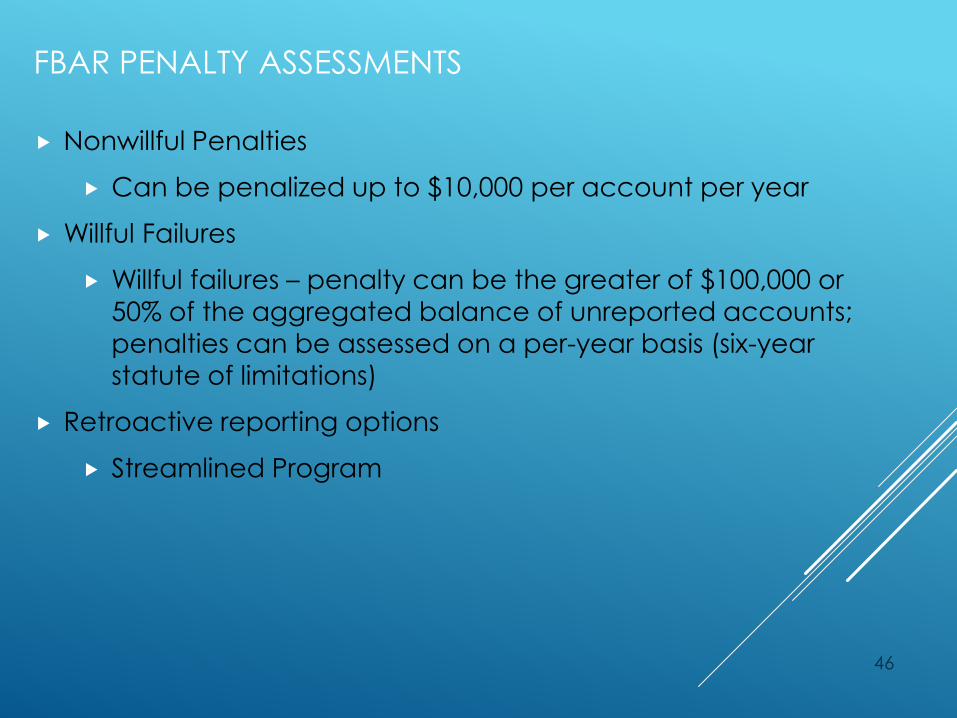

FBAR PENALTY ASSESSMENTS

Nonwillful Penalties

Can be penalized up to $10,000 per account per year

Willful Failures

Willful failures – penalty can be the greater of $100,000 or 50% of the aggregated balance of unreported accounts;

penalties can be assessed on a per-year basis (six-year

statute of limitations)

Retroactive reporting options

Streamlined Program

46

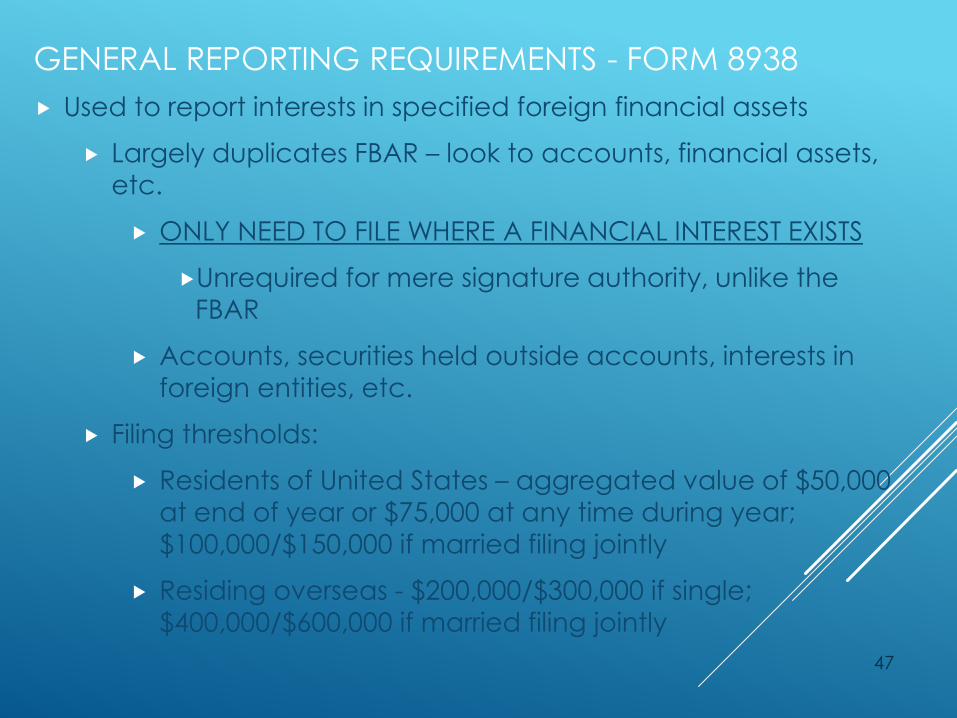

GENERAL REPORTING REQUIREMENTS - FORM 8938

Used to report interests in specified foreign financial assets

Largely duplicates FBAR – look to accounts, financial assets,

etc.

ONLY NEED TO FILE WHERE A FINANCIAL INTEREST EXISTS

Unrequired for mere signature authority, unlike the

FBAR

Accounts, securities held outside accounts, interests in foreign entities, etc.

Filing thresholds:

Residents of United States – aggregated value of $50,000

at end of year or $75,000 at any time during year;

$100,000/$150,000 if married filing jointly

Residing overseas - $200,000/$300,000 if single;

$400,000/$600,000 if married filing jointly

47

FORM 8938 PENALTY ASSESSMENTS

$10,000 penalty assessable for failure to file (with additional

penalties up to $50,000)

Treasury notifies of failure to file; after 90 days, if still not filed,

$10,000 penalties are assessed up to $50,000

Failure to file when required can cause statute of limitations for

entire tax return to stay open until three (3) years after the form is

filed

Reasonable cause exception exists

Form first required in 2011

48

GENERAL REPORTING REQUIREMENTS – FORMS 5471

FORM 5471 is used to report specified interests of United States

persons in foreign corporations

Required for U.S. person who is an officer or director in a

foreign corporation in which a U.S. person has acquired a 10%

interest

Required for U.S. person who acquires 10% interest in a foreign

corporation or who disposes of sufficient stock to reduce his/her interest below 10%

Required for U.S. person who had control of a foreign

corporation for an uninterrupted period of at least 30 days

during the annual accounting period of the foreign

corporation

Required for U.S. shareholder who owns stock in a foreign

corporation which is a CFC for an uninterrupted period of 30

days or more49

FORM 5471 PENALTY ASSESSMENTS

A $10,000 penalty is imposed for each annual accounting period

of each foreign corporation for failure to furnish the information

required by section 6038(a) within the time prescribed. If the

information is not filed within 90 days after the IRS has mailed a notice of the failure to the U.S. person, an additional $10,000

penalty (per foreign corporation) is charged for each 30-day

period, or fraction thereof, during which the failure continues after

the 90-day period has expired. The additional penalty is limited to

a maximum of $50,000 for each failure.

50

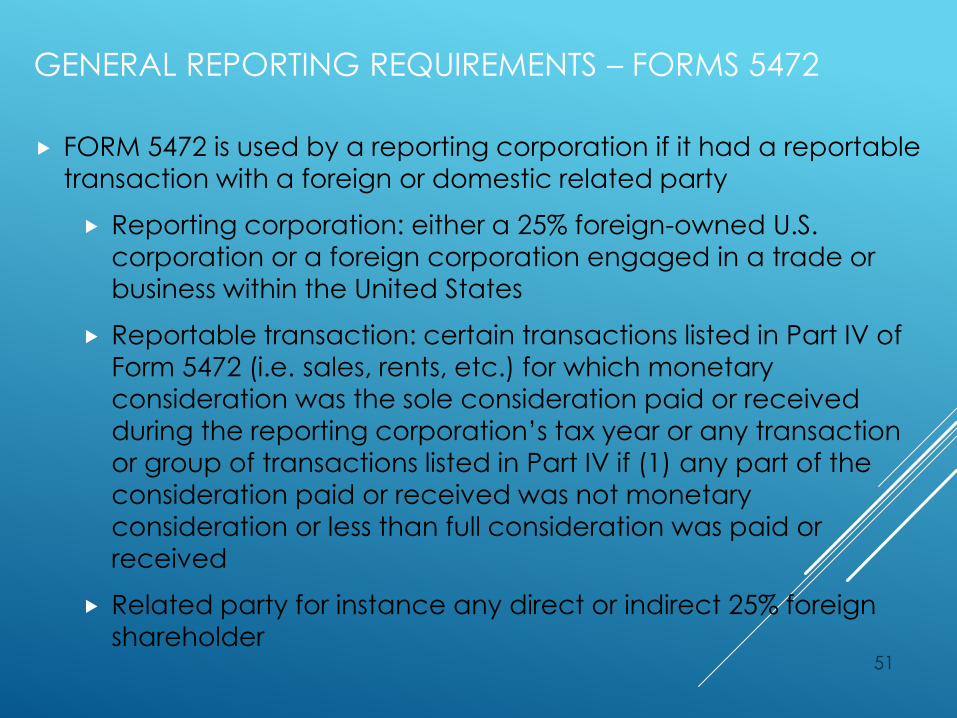

GENERAL REPORTING REQUIREMENTS – FORMS 5472

FORM 5472 is used by a reporting corporation if it had a reportable

transaction with a foreign or domestic related party

Reporting corporation: either a 25% foreign-owned U.S.

corporation or a foreign corporation engaged in a trade or

business within the United States

Reportable transaction: certain transactions listed in Part IV of

Form 5472 (i.e. sales, rents, etc.) for which monetary

consideration was the sole consideration paid or received

during the reporting corporation’s tax year or any transaction

or group of transactions listed in Part IV if (1) any part of the

consideration paid or received was not monetary

consideration or less than full consideration was paid or

received

Related party for instance any direct or indirect 25% foreign

shareholder51

FORM 5472 PENALTY ASSESSMENTS

A penalty of $25,000 will be assessed on any reporting corporation

that fails to file the form when due and in the manner prescribed.

The penalty also applies for failure to maintain records as required

by Regulations section 1.6038A-3. Filing a substantially incomplete

Form 5472 constitutes a failure to file Form 5472. Each member of

a group of corporations filing a consolidated information return is a separate reporting corporation subject to a separate $25,000

penalty and each member is jointly and severally liable. If the

failure continues for more than 90 days after notification by the

IRS, an additional penalty of $25,000 will apply. This penalty

applies with respect to each related party for which a failure

occurs for each 30-day period (or part of a 30-day period) during which the failure continues after the 90-day period ends.

52

GENERAL REPORTING REQUIREMENTS - NONRESIDENT

ALIENS

A non-U.S. citizen who does not pass the green card test or the

substantial presence test is considered a “non-resident alien.”

If a non-citizen currently has a green card they would pass the

green card test and would be classified as a US resident alien.

If the individual has resided in the U.S. for more than 31 days in

the current year and has resided in the U.S. for more than 183

days over a three-year period, including the current year, they

would pass the substantial presence test and also be classified as

a US resident alien.

Nonresident aliens with U.S.-source reportable income use Form 1040-NR

53

FORM 8833 - TREATY-BASED RETURN POSITION DISCLOSURE

Used by taxpayers to make treaty-based return position

disclosures required for many treaty benefits

Taxpayer takes a treaty-based return position by maintaining

that a treaty of the United States overrules or modifies a

provision of the Internal Revenue Code and thereby causes

(or potentially causes) a reduction of tax on the taxpayer’s tax

return

54

FORMS W-8BEN - W-8BEN-E - W-8ECI

Form W-8BEN - Used to provided to withholding agents or payers

by nonresident aliens who are the beneficial owners of an

amount subject to withholding

Form W-8BEN-E - Used by foreign entities

Form W-8ECI - Supplied by foreign persons to prevent withholding

on United States-sourced income which is effectively connected

with the conduct of a United States trade or business

55

David A. Matos, CPA, CISA, CRFAC, RFI

PartnerMATOS & JAWAD PLLC

250 Ed English Drive Building 3 Unit C

Shenandoah, TX 77385

Cell: (713) 245-6274

Fax: (713) 999-4929

www.matosjawad.com

56