u.s. office market statistics (q4 2014) and 2015 outlook

TRANSCRIPT

Expansionary leasing activity

driving growth across markets

United States Office Review Q4 2014

The increase in corporate profitability and economic growth will continue to result in headcount increases and expansionary leasing activity across markets. As a result, the rate of absorption will likely reach 2.0 percent of total inventory in 2015, a 25 percent increase from 2014 levels.

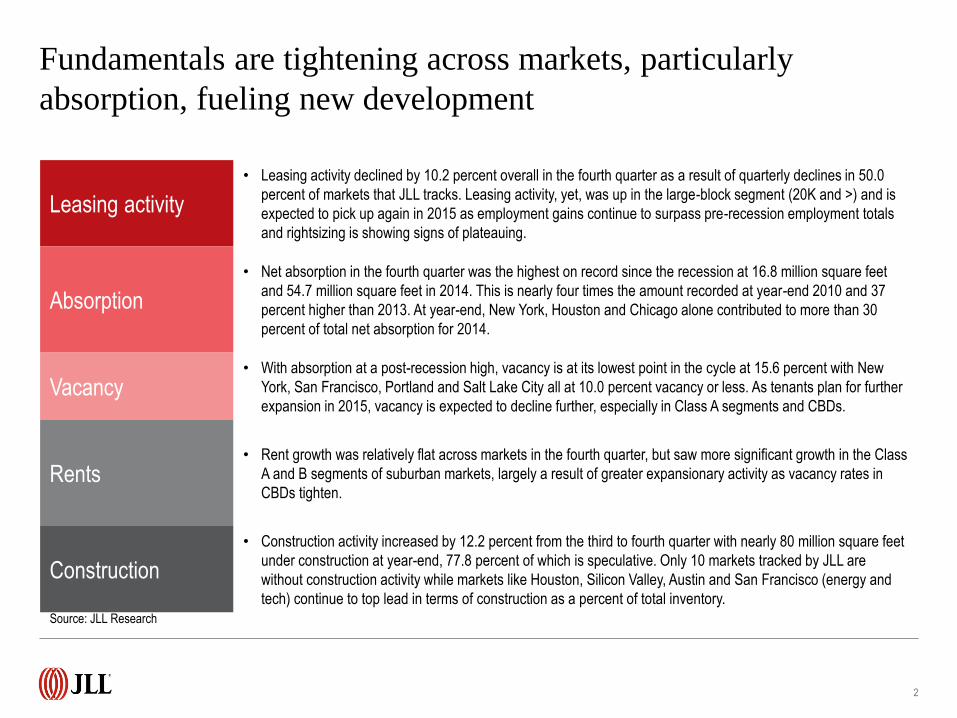

Fundamentals are tightening across markets, particularly

absorption, fueling new development

2

Source: JLL Research

Leasing activity

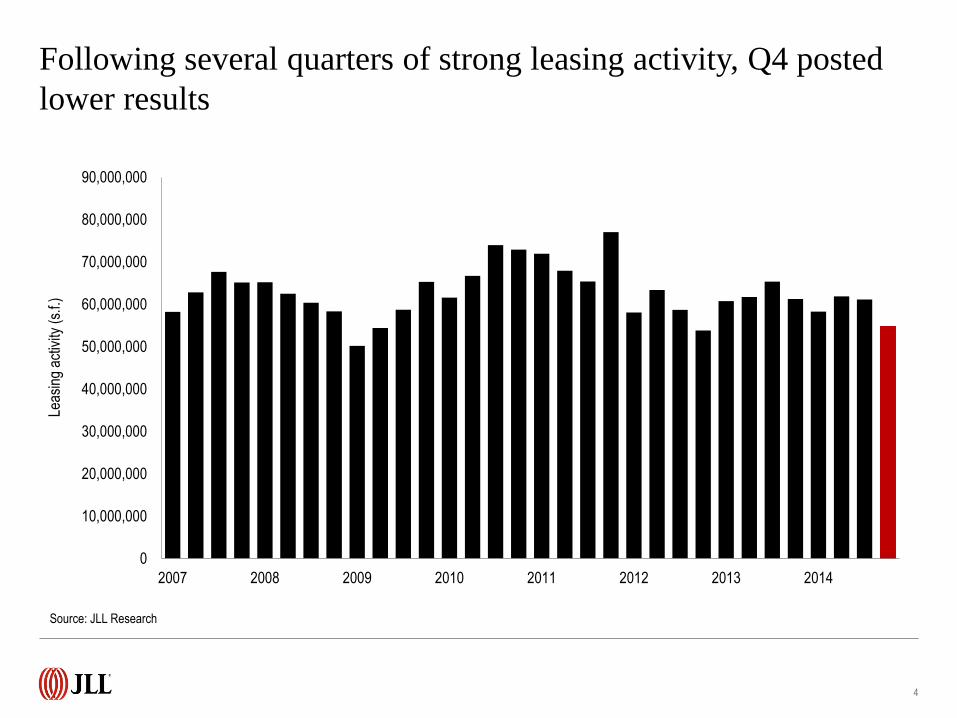

• Leasing activity declined by 10.2 percent overall in the fourth quarter as a result of quarterly declines in 50.0

percent of markets that JLL tracks. Leasing activity, yet, was up in the large-block segment (20K and >) and is

expected to pick up again in 2015 as employment gains continue to surpass pre-recession employment totals

and rightsizing is showing signs of plateauing.

Absorption

• Net absorption in the fourth quarter was the highest on record since the recession at 16.8 million square feet

and 54.7 million square feet in 2014. This is nearly four times the amount recorded at year-end 2010 and 37

percent higher than 2013. At year-end, New York, Houston and Chicago alone contributed to more than 30

percent of total net absorption for 2014.

Vacancy • With absorption at a post-recession high, vacancy is at its lowest point in the cycle at 15.6 percent with New

York, San Francisco, Portland and Salt Lake City all at 10.0 percent vacancy or less. As tenants plan for further

expansion in 2015, vacancy is expected to decline further, especially in Class A segments and CBDs.

Rents • Rent growth was relatively flat across markets in the fourth quarter, but saw more significant growth in the Class

A and B segments of suburban markets, largely a result of greater expansionary activity as vacancy rates in

CBDs tighten.

Construction

• Construction activity increased by 12.2 percent from the third to fourth quarter with nearly 80 million square feet

under construction at year-end, 77.8 percent of which is speculative. Only 10 markets tracked by JLL are

without construction activity while markets like Houston, Silicon Valley, Austin and San Francisco (energy and

tech) continue to top lead in terms of construction as a percent of total inventory.

Leasing activity

Following several quarters of strong leasing activity, Q4 posted

lower results

4

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

2007 2008 2009 2010 2011 2012 2013 2014

Leas

ing

activ

ity (

s.f.)

Source: JLL Research

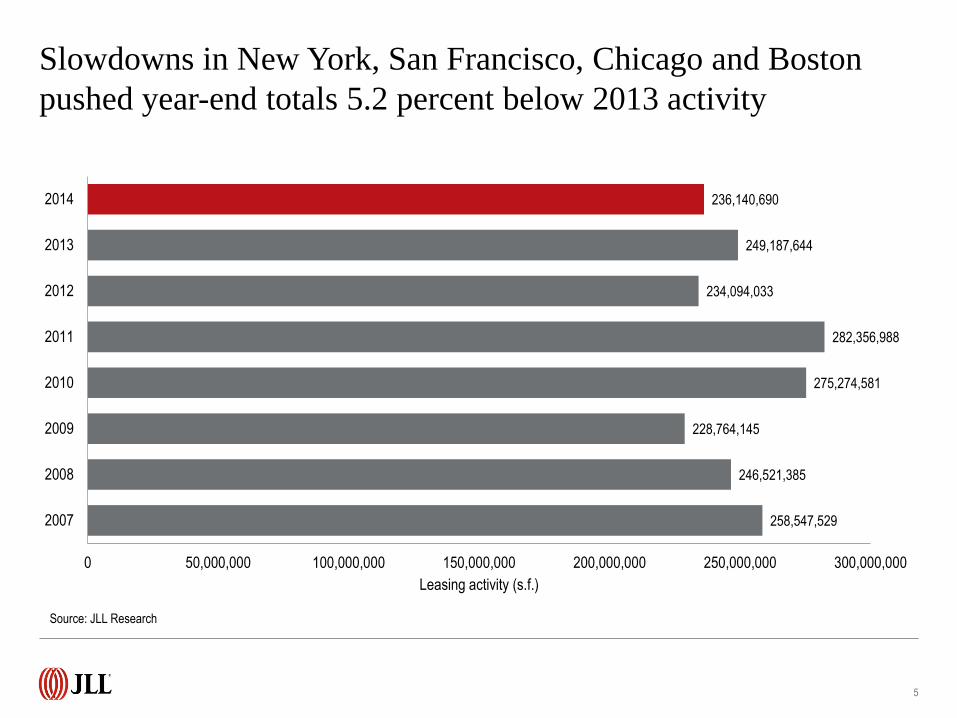

Slowdowns in New York, San Francisco, Chicago and Boston

pushed year-end totals 5.2 percent below 2013 activity

5

258,547,529

246,521,385

228,764,145

275,274,581

282,356,988

234,094,033

249,187,644

236,140,690

0 50,000,000 100,000,000 150,000,000 200,000,000 250,000,000 300,000,000

2007

2008

2009

2010

2011

2012

2013

2014

Leasing activity (s.f.)

Source: JLL Research

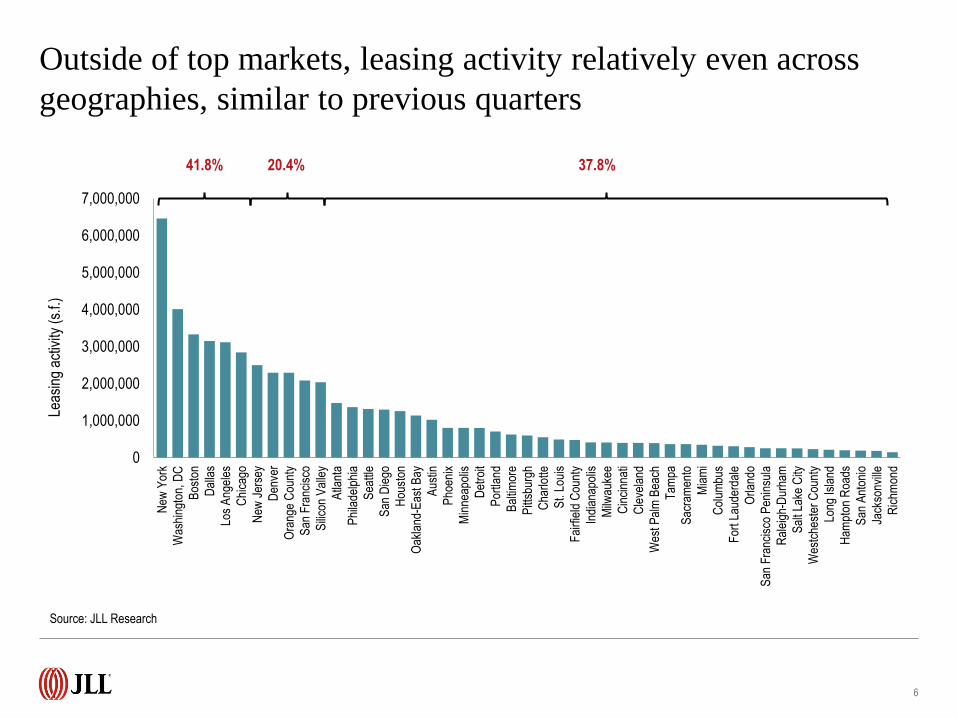

Outside of top markets, leasing activity relatively even across

geographies, similar to previous quarters

6

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

New

Yor

k

Was

hing

ton,

DC

Bos

ton

Dal

las

Los

Ang

eles

Chi

cago

New

Jer

sey

Den

ver

Ora

nge

Cou

nty

San

Fra

ncis

co

Sili

con

Val

ley

Atla

nta

Phi

lade

lphi

a

Sea

ttle

San

Die

go

Hou

ston

Oak

land

-Eas

t Bay

Aus

tin

Pho

enix

Min

neap

olis

Det

roit

Por

tland

Bal

timor

e

Pitt

sbur

gh

Cha

rlotte

St.

Loui

s

Fai

rfie

ld C

ount

y

Indi

anap

olis

Milw

auke

e

Cin

cinn

ati

Cle

vela

nd

Wes

t Pal

m B

each

Tam

pa

Sac

ram

ento

Mia

mi

Col

umbu

s

For

t Lau

derd

ale

Orla

ndo

San

Fra

ncis

co P

enin

sula

Ral

eigh

-Dur

ham

Sal

t Lak

e C

ity

Wes

tche

ster

Cou

nty

Long

Isla

nd

Ham

pton

Roa

ds

San

Ant

onio

Jack

sonv

ille

Ric

hmon

d

Leas

ing

activ

ity (

s.f.)

Source: JLL Research

41.8% 20.4% 37.8%

7

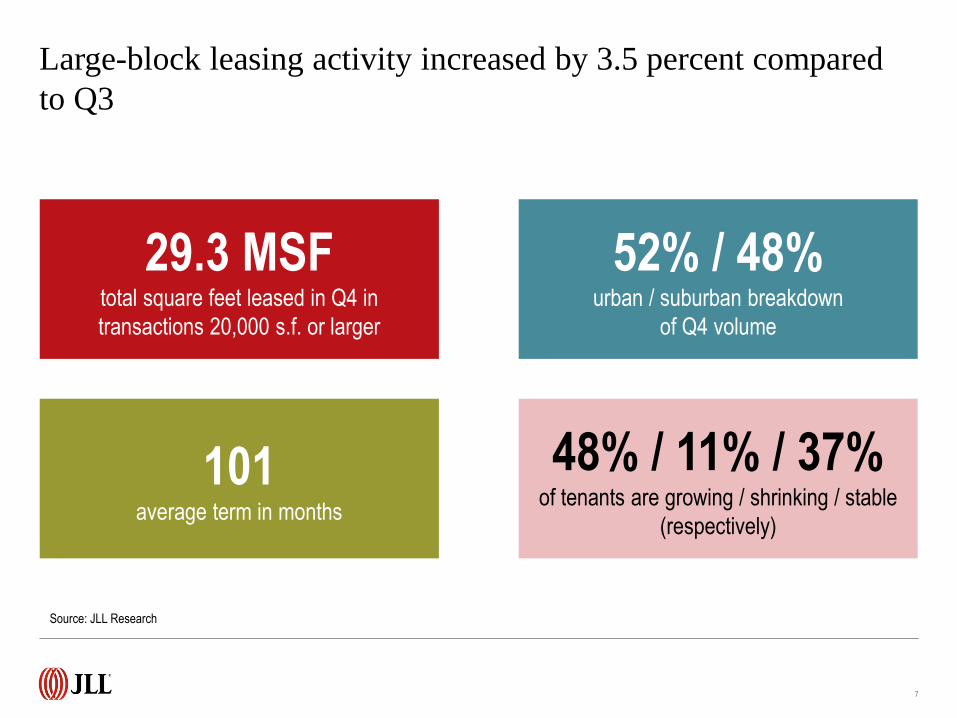

29.3 MSF total square feet leased in Q4 in

transactions 20,000 s.f. or larger

101 average term in months

48% / 11% / 37% of tenants are growing / shrinking / stable

(respectively)

52% / 48% urban / suburban breakdown

of Q4 volume

Large-block leasing activity increased by 3.5 percent compared

to Q3

Source: JLL Research

8

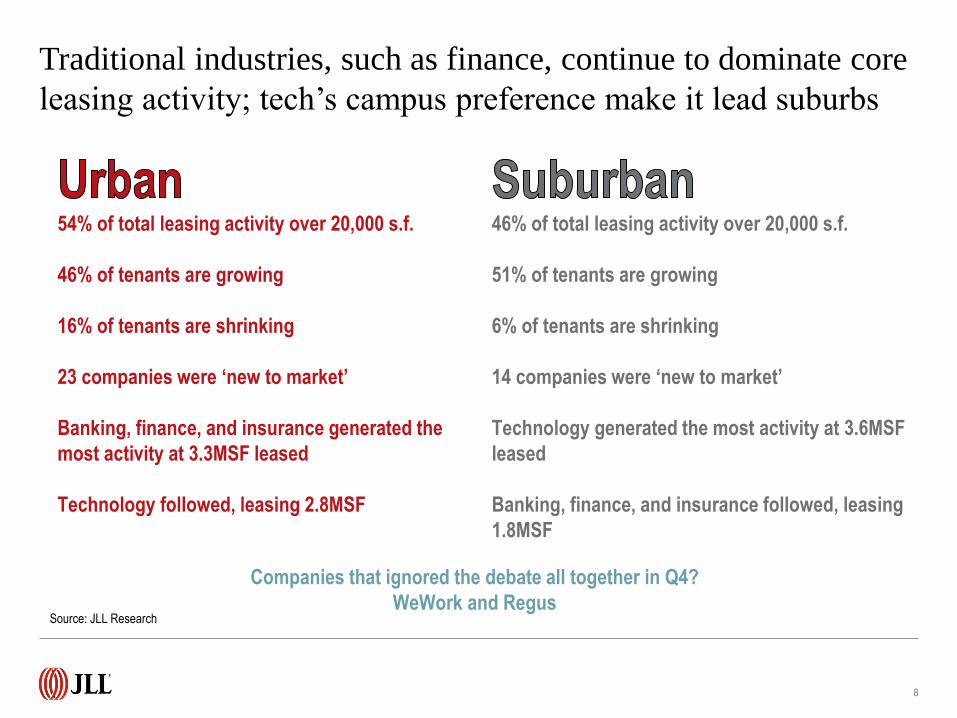

54% of total leasing activity over 20,000 s.f.

46% of tenants are growing

16% of tenants are shrinking

23 companies were ‘new to market’

Banking, finance, and insurance generated the

most activity at 3.3MSF leased

Technology followed, leasing 2.8MSF

46% of total leasing activity over 20,000 s.f.

51% of tenants are growing

6% of tenants are shrinking

14 companies were ‘new to market’

Technology generated the most activity at 3.6MSF

leased

Banking, finance, and insurance followed, leasing

1.8MSF

Companies that ignored the debate all together in Q4?

WeWork and Regus

Traditional industries, such as finance, continue to dominate core

leasing activity; tech’s campus preference make it lead suburbs

Source: JLL Research

9

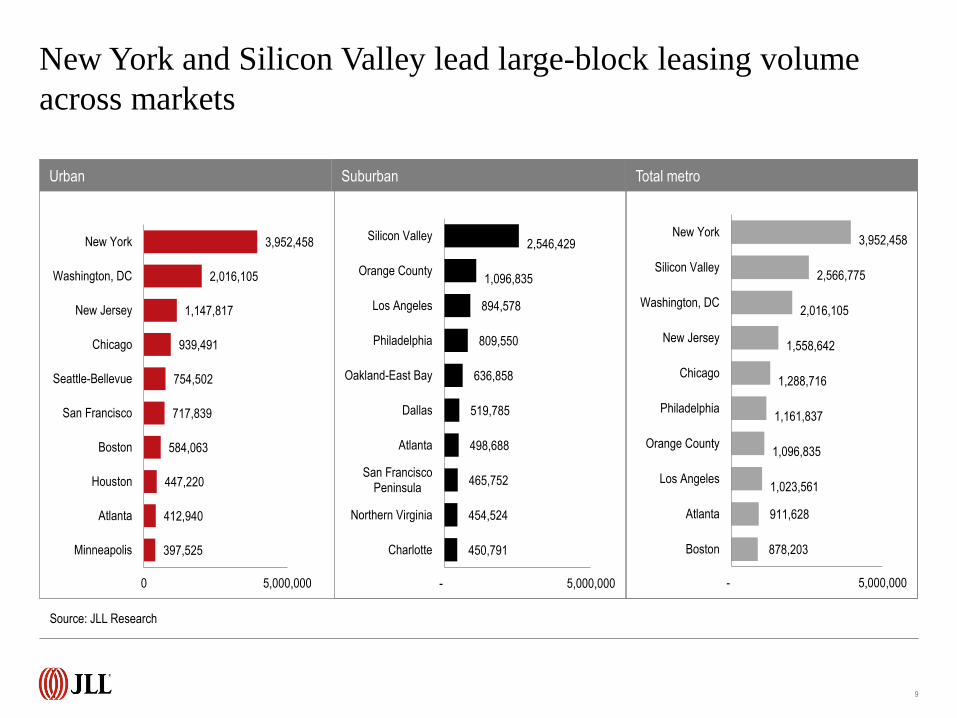

Urban Suburban Total metro

397,525

412,940

447,220

584,063

717,839

754,502

939,491

1,147,817

2,016,105

3,952,458

0 5,000,000

Minneapolis

Atlanta

Houston

Boston

San Francisco

Seattle-Bellevue

Chicago

New Jersey

Washington, DC

New York

450,791

454,524

465,752

498,688

519,785

636,858

809,550

894,578

1,096,835

2,546,429

- 5,000,000

Charlotte

Northern Virginia

San FranciscoPeninsula

Atlanta

Dallas

Oakland-East Bay

Philadelphia

Los Angeles

Orange County

Silicon Valley

878,203

911,628

1,023,561

1,096,835

1,161,837

1,288,716

1,558,642

2,016,105

2,566,775

3,952,458

- 5,000,000

Boston

Atlanta

Los Angeles

Orange County

Philadelphia

Chicago

New Jersey

Washington, DC

Silicon Valley

New York

New York and Silicon Valley lead large-block leasing volume

across markets

Source: JLL Research

10

However, large leasing is taking place throughout the United

States, with a focus on gateway markets

Seattle CBD Zillow: 155,000 s.f.

Pleasanton North (East Bay) Workday: 151,000 s.f.

Sunnyvale (Silicon Valley) Google: 946,000 s.f.

North County (Orange County) St. Joseph Heritage

Medical Group: 192,000 s.f.

Dallas CBD Crosstex Energy: 158,000 s.f.

Minneapolis CBD Seed Partners: 280,000 s.f.

West Loop (Chicago) Hyatt: 229,000 s.f.

Hudson Waterfront (NJ) ISO Insurance: 392,000 s.f.

Penn Plaza/Garment (NYC) Amazon: 470,000 s.f.

Southwest (DC) U.S. Dep’t of Education: 314,000 s.f.

Source: JLL Research

Month 00, 2014 11

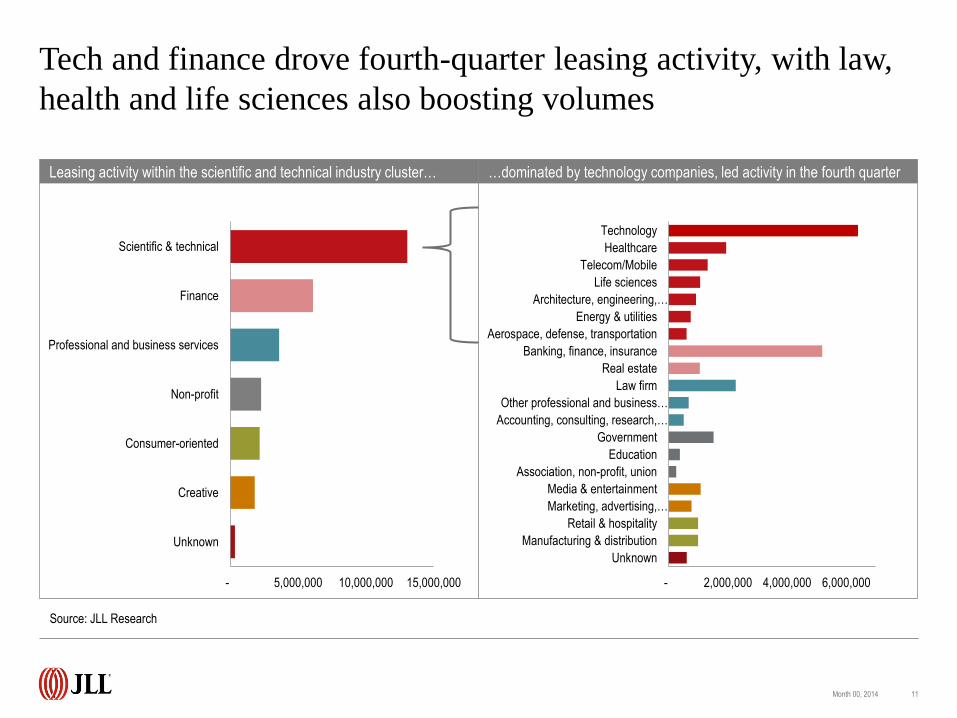

Unknown

Creative

Consumer-oriented

Non-profit

Professional and business services

Finance

Scientific & technical

- 5,000,000 10,000,000 15,000,000

Unknown

Manufacturing & distribution

Retail & hospitality

Marketing, advertising,…

Media & entertainment

Association, non-profit, union

Education

Government

Accounting, consulting, research,…

Other professional and business…

Law firm

Real estate

Banking, finance, insurance

Aerospace, defense, transportation

Energy & utilities

Architecture, engineering,…

Life sciences

Telecom/Mobile

Healthcare

Technology

- 2,000,000 4,000,000 6,000,000

Leasing activity within the scientific and technical industry cluster… …dominated by technology companies, led activity in the fourth quarter

Tech and finance drove fourth-quarter leasing activity, with law,

health and life sciences also boosting volumes

Source: JLL Research

Month 00, 2014 12

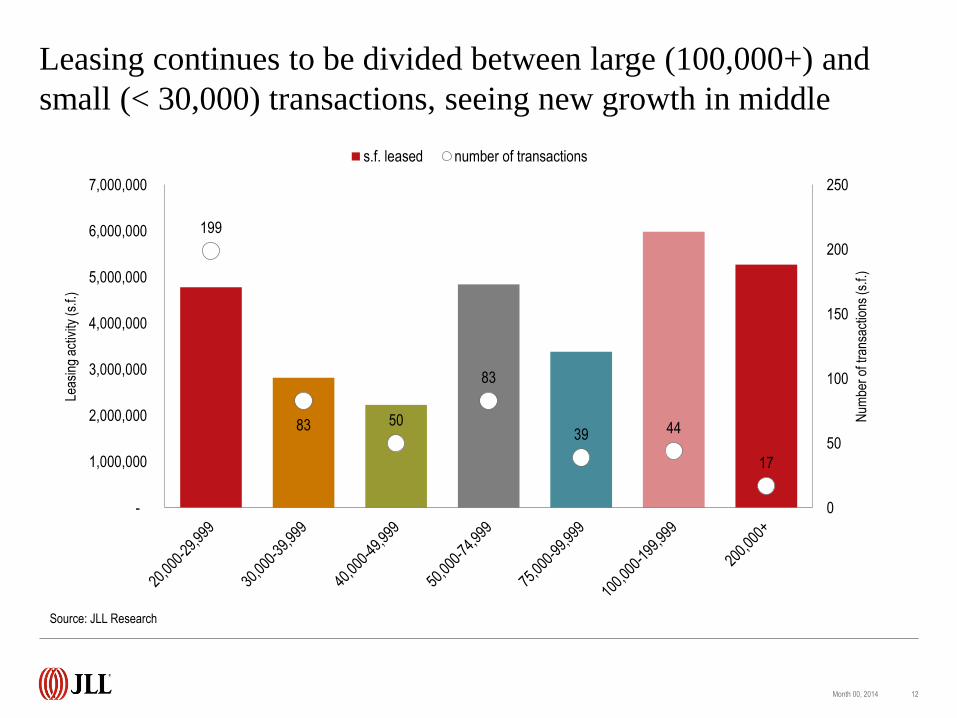

199

83 50

83

39 44

17

0

50

100

150

200

250

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

Num

ber

of tr

ansa

ctio

ns (s

.f.)

Leas

ing

activ

ity (

s.f.)

s.f. leased number of transactions

Leasing continues to be divided between large (100,000+) and

small (< 30,000) transactions, seeing new growth in middle

Source: JLL Research

13

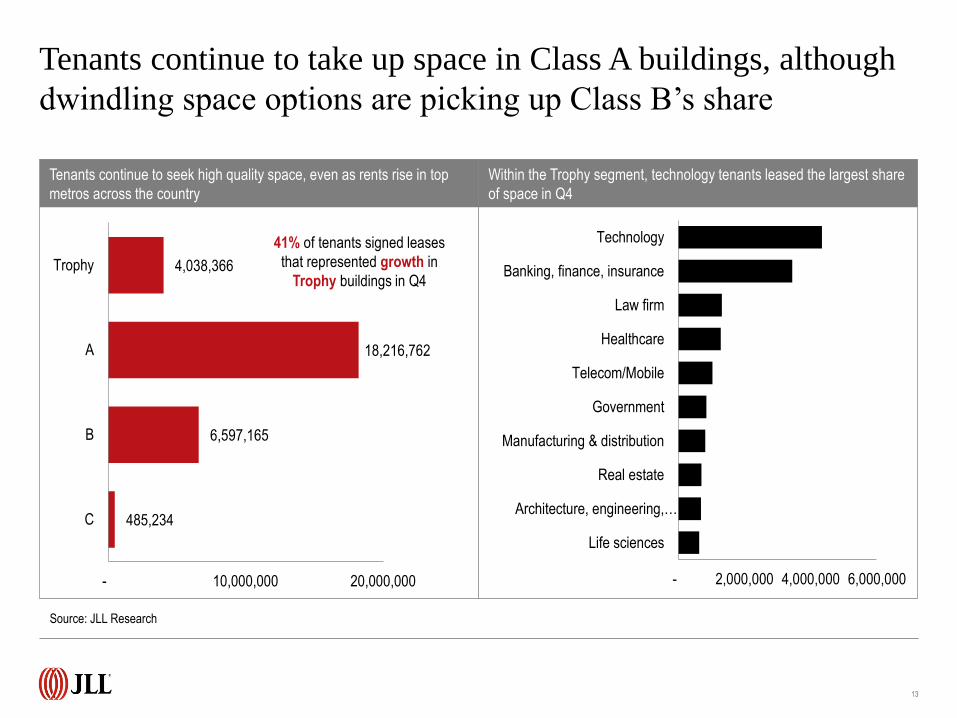

485,234

6,597,165

18,216,762

4,038,366

- 10,000,000 20,000,000

C

B

A

Trophy

41% of tenants signed leases

that represented growth in

Trophy buildings in Q4

Life sciences

Architecture, engineering,…

Real estate

Manufacturing & distribution

Government

Telecom/Mobile

Healthcare

Law firm

Banking, finance, insurance

Technology

- 2,000,000 4,000,000 6,000,000

Tenants continue to seek high quality space, even as rents rise in top

metros across the country

Within the Trophy segment, technology tenants leased the largest share

of space in Q4

Tenants continue to take up space in Class A buildings, although

dwindling space options are picking up Class B’s share

Source: JLL Research

14

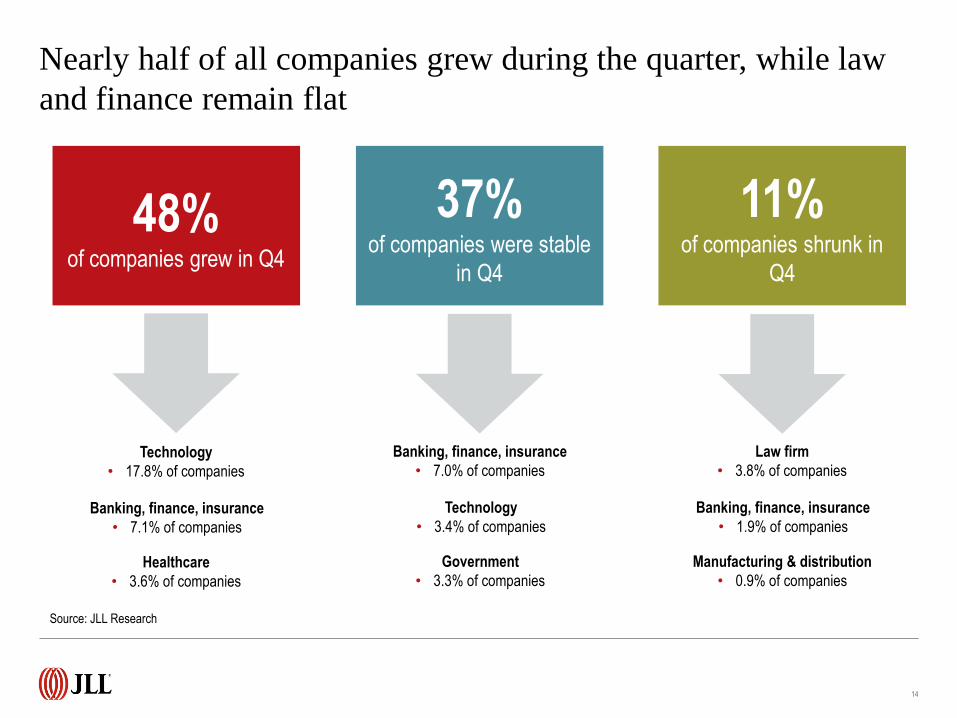

48% of companies grew in Q4

11% of companies shrunk in

Q4

37% of companies were stable

in Q4

Technology

• 17.8% of companies

Banking, finance, insurance

• 7.1% of companies

Healthcare

• 3.6% of companies

Banking, finance, insurance

• 7.0% of companies

Technology

• 3.4% of companies

Government

• 3.3% of companies

Law firm

• 3.8% of companies

Banking, finance, insurance

• 1.9% of companies

Manufacturing & distribution

• 0.9% of companies

Nearly half of all companies grew during the quarter, while law

and finance remain flat

Source: JLL Research

Absorption

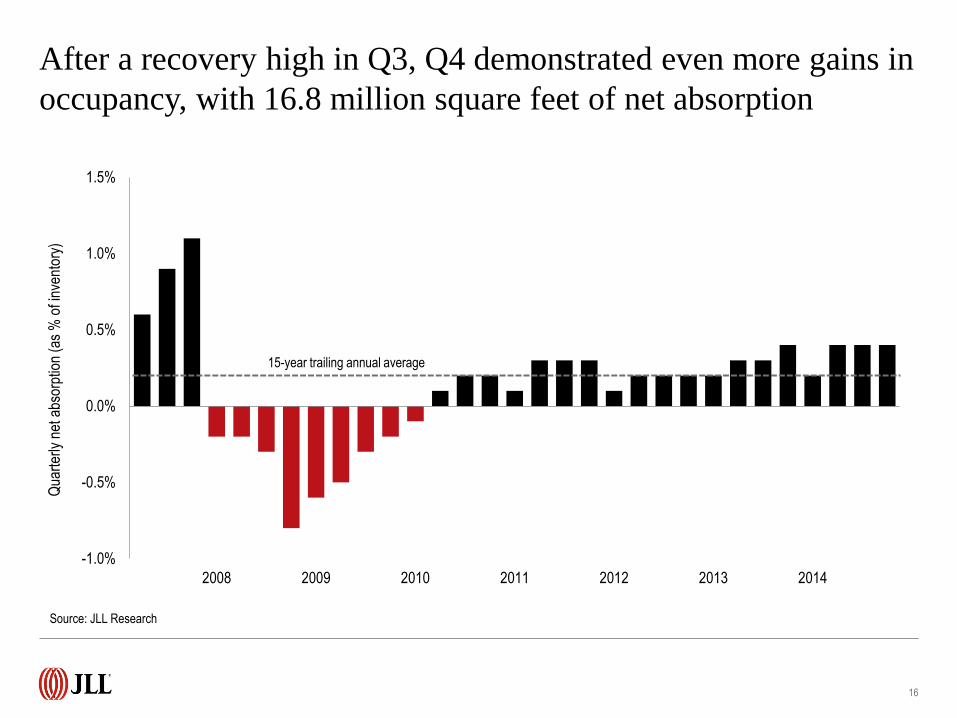

After a recovery high in Q3, Q4 demonstrated even more gains in

occupancy, with 16.8 million square feet of net absorption

16

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2008 2009 2010 2011 2012 2013 2014

Qua

rter

ly n

et a

bsor

ptio

n (a

s %

of i

nven

tory

)

Source: JLL Research

15-year trailing annual average

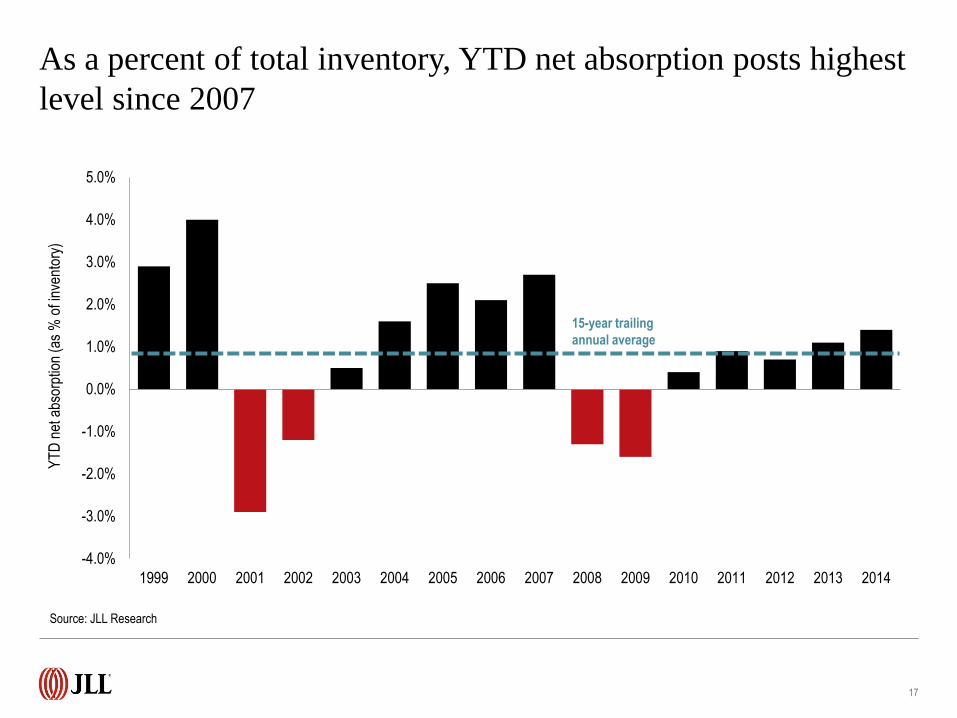

As a percent of total inventory, YTD net absorption posts highest

level since 2007

17

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

YT

D n

et a

bsor

ptio

n (a

s %

of i

nven

tory

)

Source: JLL Research

15-year trailing

annual average

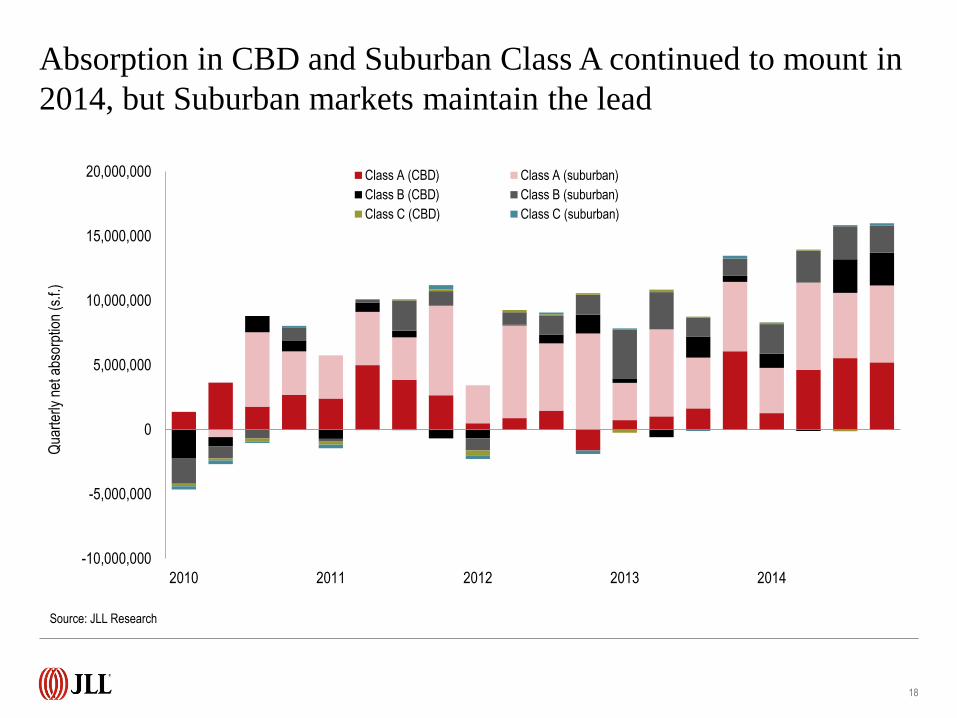

Absorption in CBD and Suburban Class A continued to mount in

2014, but Suburban markets maintain the lead

18

-10,000,000

-5,000,000

0

5,000,000

10,000,000

15,000,000

20,000,000

2010 2011 2012 2013 2014

Qua

rter

ly n

et a

bsor

ptio

n (s

.f.)

Class A (CBD) Class A (suburban)

Class B (CBD) Class B (suburban)

Class C (CBD) Class C (suburban)

Source: JLL Research

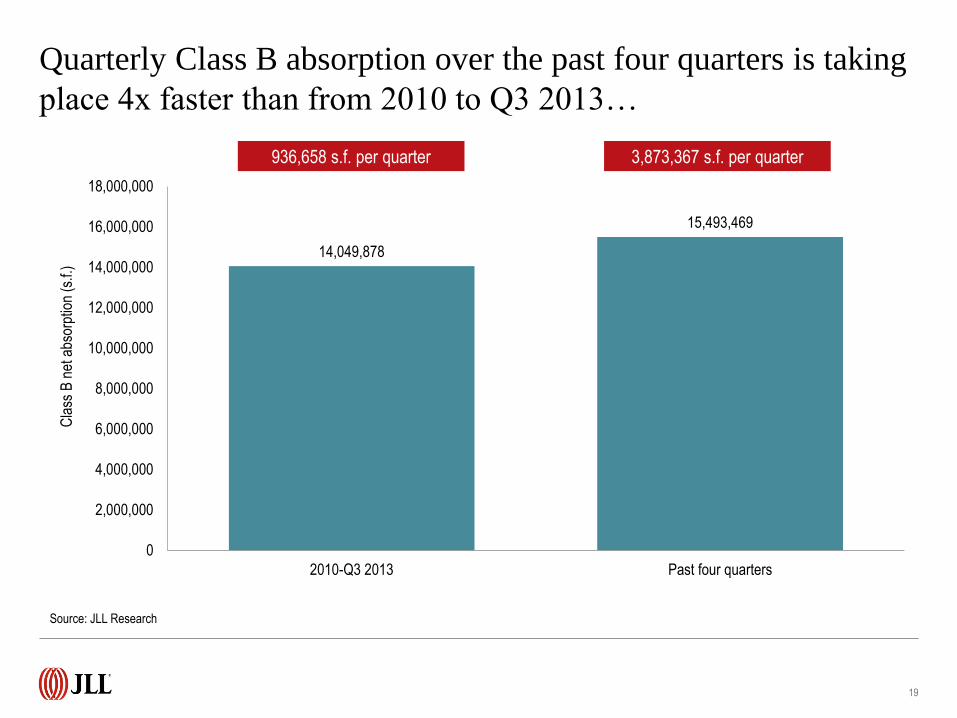

Quarterly Class B absorption over the past four quarters is taking

place 4x faster than from 2010 to Q3 2013…

19

Source: JLL Research

14,049,878

15,493,469

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

2010-Q3 2013 Past four quarters

Cla

ss B

net

abs

orpt

ion

(s.f.

)

936,658 s.f. per quarter 3,873,367 s.f. per quarter

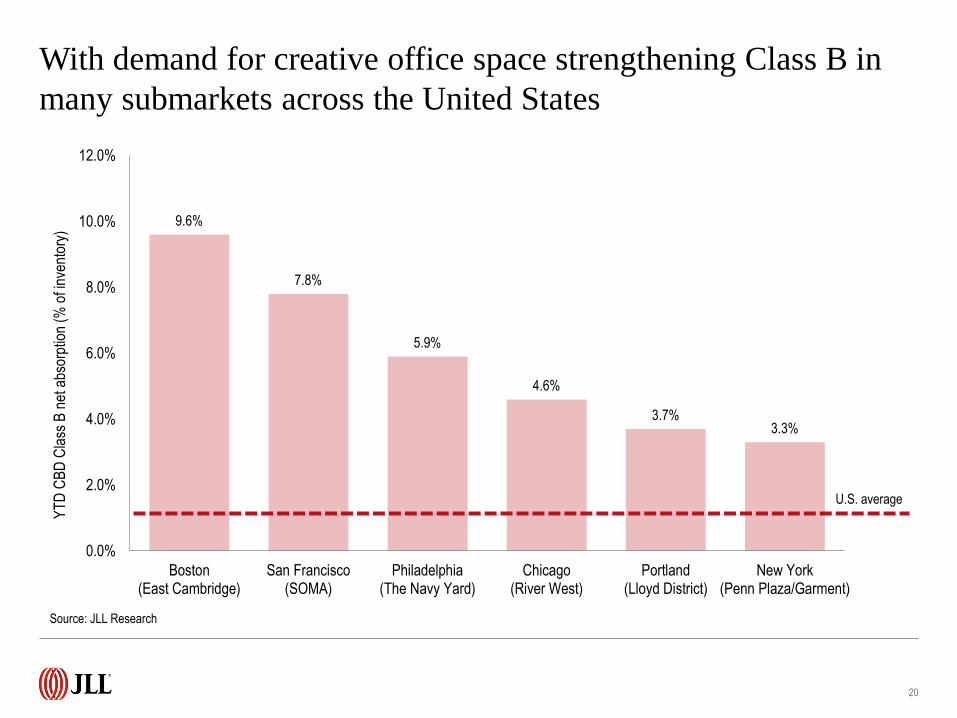

With demand for creative office space strengthening Class B in

many submarkets across the United States

20

9.6%

7.8%

5.9%

4.6%

3.7% 3.3%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Boston(East Cambridge)

San Francisco(SOMA)

Philadelphia(The Navy Yard)

Chicago(River West)

Portland(Lloyd District)

New York(Penn Plaza/Garment)

YT

D C

BD

Cla

ss B

net

abs

orpt

ion

(% o

f inv

ento

ry)

Source: JLL Research

U.S. average

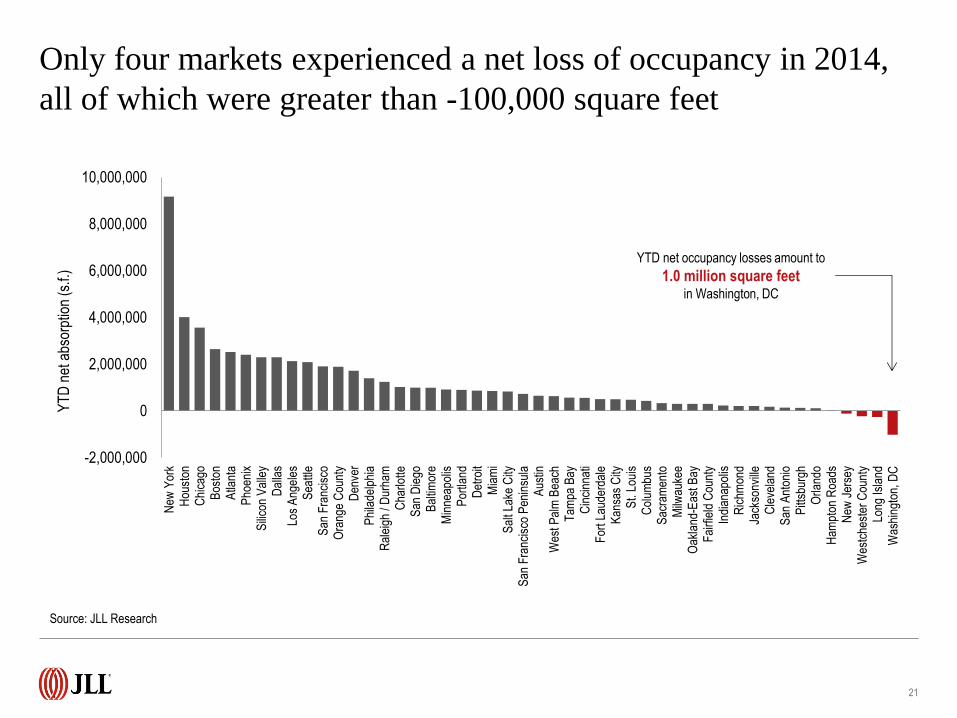

Only four markets experienced a net loss of occupancy in 2014,

all of which were greater than -100,000 square feet

21

-2,000,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000N

ew Y

ork

Hou

ston

Chi

cago

Bos

ton

Atla

nta

Pho

enix

Sili

con

Val

ley

Dal

las

Los

Ang

eles

Sea

ttle

San

Fra

ncis

coO

rang

e C

ount

yD

enve

rP

hila

delp

hia

Ral

eigh

/ D

urha

mC

harlo

tteS

an D

iego

Bal

timor

eM

inne

apol

isP

ortla

ndD

etro

itM

iam

iS

alt L

ake

City

San

Fra

ncis

co P

enin

sula

Aus

tinW

est P

alm

Bea

chT

ampa

Bay

Cin

cinn

ati

For

t Lau

derd

ale

Kan

sas

City

St.

Loui

sC

olum

bus

Sac

ram

ento

Milw

auke

eO

akla

nd-E

ast B

ayF

airf

ield

Cou

nty

Indi

anap

olis

Ric

hmon

dJa

ckso

nvill

eC

leve

land

San

Ant

onio

Pitt

sbur

ghO

rland

oH

ampt

on R

oads

New

Jer

sey

Wes

tche

ster

Cou

nty

Long

Isla

ndW

ashi

ngto

n, D

C

YT

D n

et a

bsor

ptio

n (s

.f.)

Source: JLL Research

YTD net occupancy losses amount to

1.0 million square feet in Washington, DC

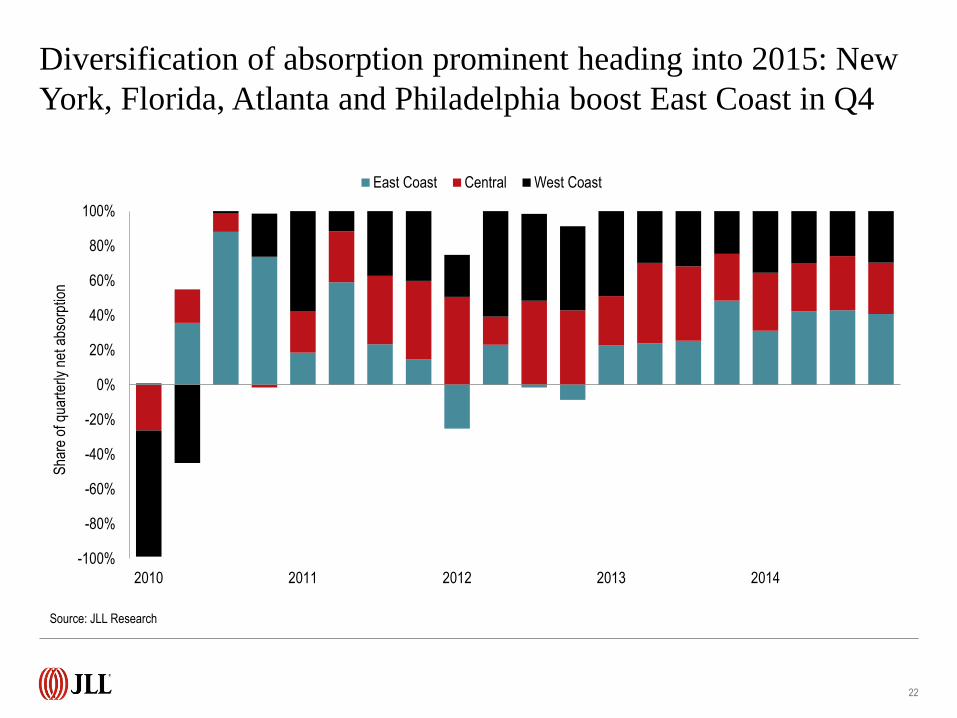

Diversification of absorption prominent heading into 2015: New

York, Florida, Atlanta and Philadelphia boost East Coast in Q4

22

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014

Sha

re o

f qua

rter

ly n

et a

bsor

ptio

n

East Coast Central West Coast

Source: JLL Research

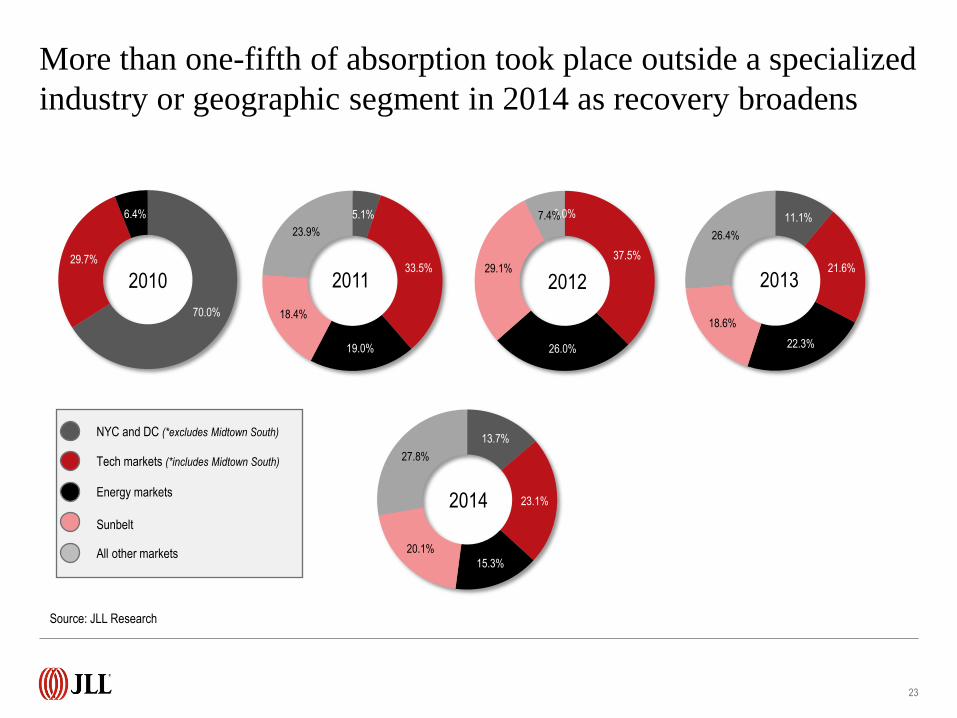

More than one-fifth of absorption took place outside a specialized

industry or geographic segment in 2014 as recovery broadens

23

Source: JLL Research

NYC and DC (*excludes Midtown South)

Tech markets (*includes Midtown South)

Energy markets

Sunbelt

All other markets

70.0%

29.7%

6.4%

2010

5.1%

33.5%

19.0%

18.4%

23.9%

2011

0.0%

37.5%

26.0%

29.1%

7.4%

2012

11.1%

21.6%

22.3%

18.6%

26.4%

2013

13.7%

23.1%

15.3%

20.1%

27.8%

2014

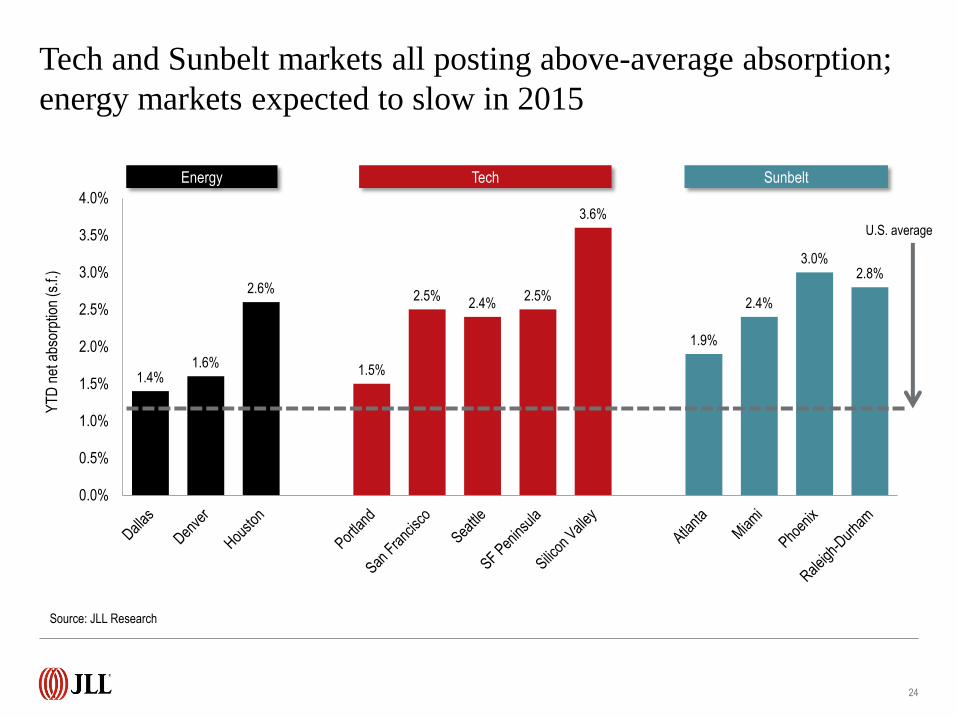

Tech and Sunbelt markets all posting above-average absorption;

energy markets expected to slow in 2015

24

1.4% 1.6%

2.6%

1.5%

2.5% 2.4%

2.5%

3.6%

1.9%

2.4%

3.0% 2.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

YT

D n

et a

bsor

ptio

n (s

.f.)

Source: JLL Research

Energy Tech Sunbelt

U.S. average

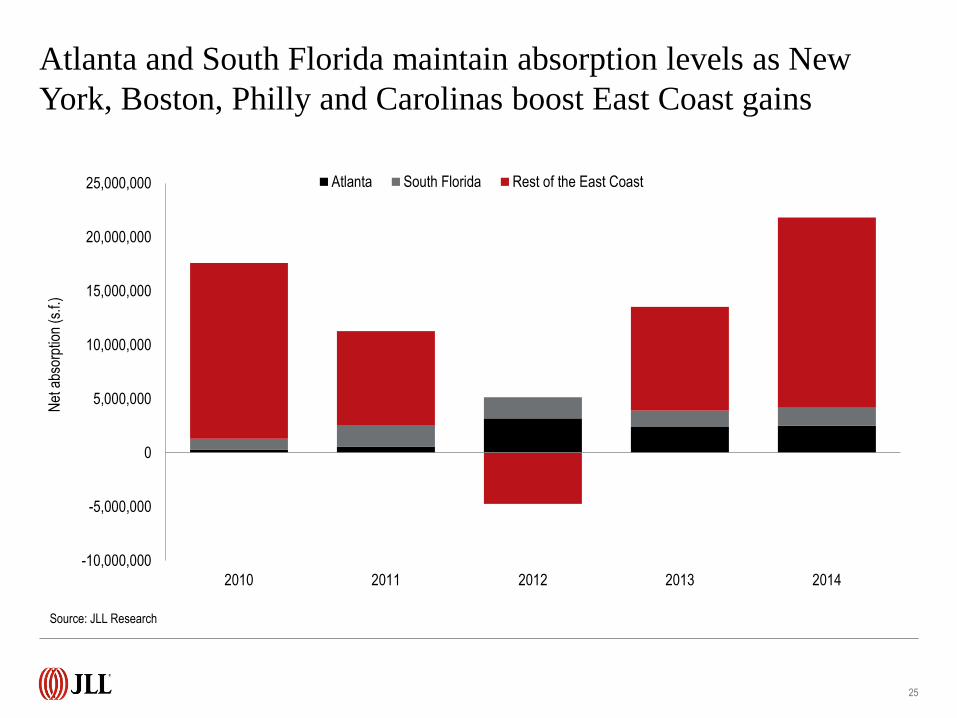

Atlanta and South Florida maintain absorption levels as New

York, Boston, Philly and Carolinas boost East Coast gains

25

Source: JLL Research

-10,000,000

-5,000,000

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

2010 2011 2012 2013 2014

Net

abs

orpt

ion

(s.f.

)

Atlanta South Florida Rest of the East Coast

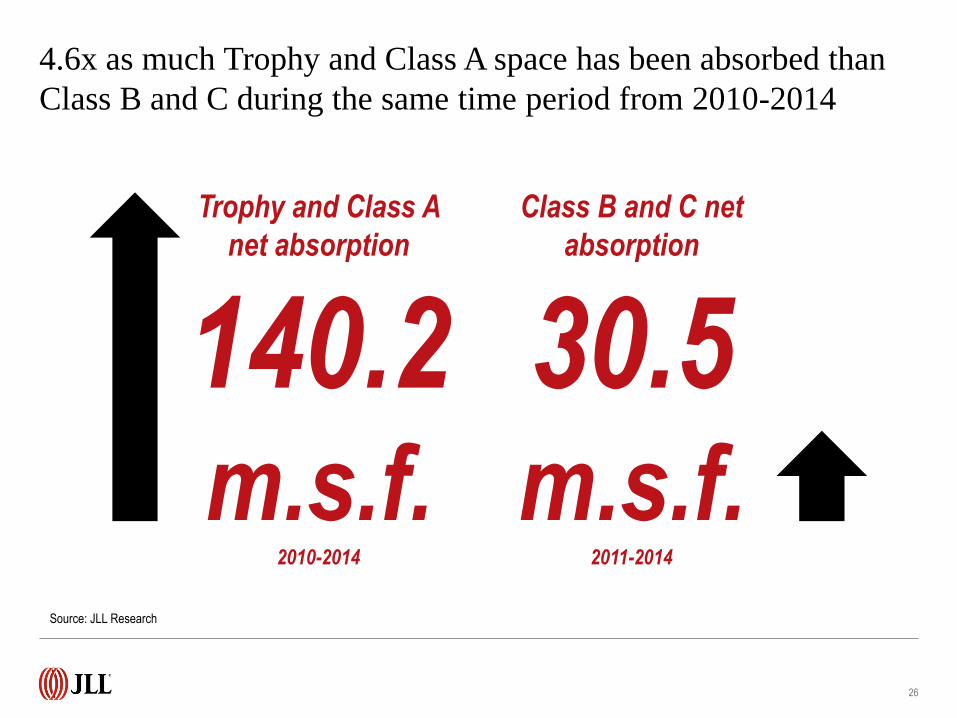

4.6x as much Trophy and Class A space has been absorbed than

Class B and C during the same time period from 2010-2014

26

Source: JLL Research

Trophy and Class A

net absorption

140.2 m.s.f.

2010-2014

Class B and C net

absorption

30.5 m.s.f.

2011-2014

-4,000,000

-3,000,000

-2,000,000

-1,000,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

2010 2011 2012 2013 2014

Net

abs

orpt

ion

(s.f.

)

Atlanta Chicago Los Angeles Miami Philadelphia Phoenix

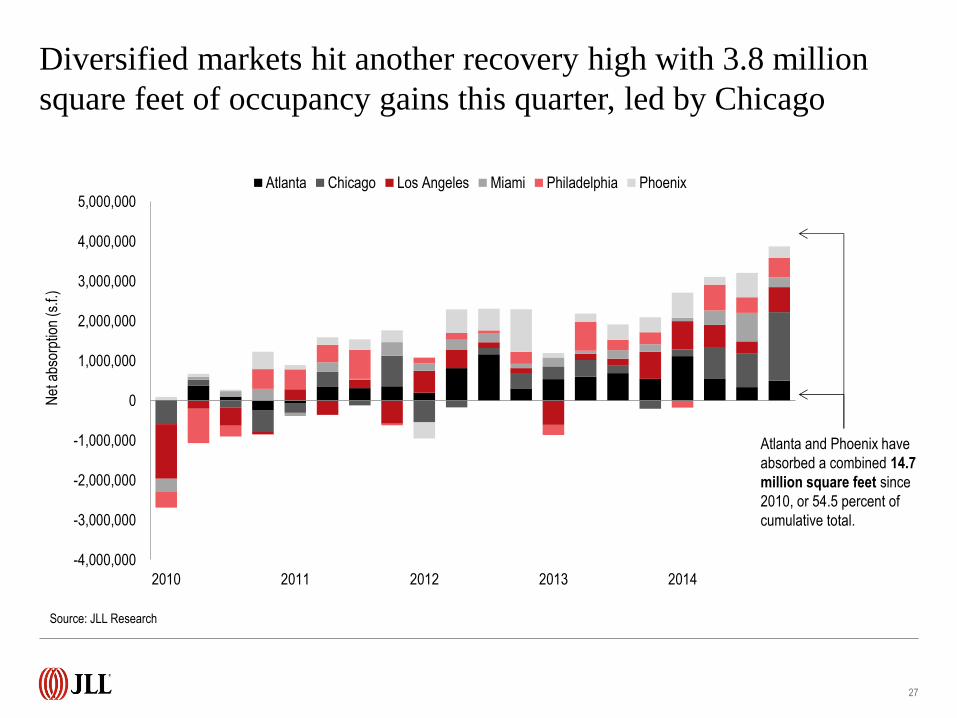

Diversified markets hit another recovery high with 3.8 million

square feet of occupancy gains this quarter, led by Chicago

27

Source: JLL Research

Atlanta and Phoenix have

absorbed a combined 14.7

million square feet since

2010, or 54.5 percent of

cumulative total.

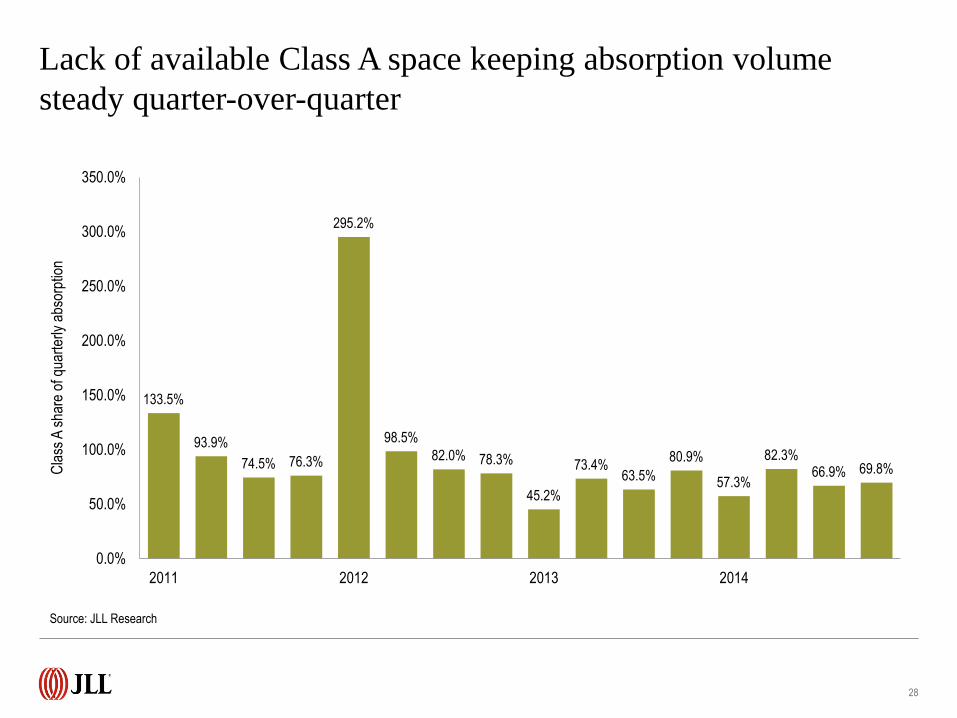

Lack of available Class A space keeping absorption volume

steady quarter-over-quarter

28

133.5%

93.9%

74.5% 76.3%

295.2%

98.5%

82.0% 78.3%

45.2%

73.4% 63.5%

80.9%

57.3%

82.3% 66.9% 69.8%

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

350.0%

2011 2012 2013 2014

Cla

ss A

sha

re o

f qua

rter

ly a

bsor

ptio

n

Source: JLL Research

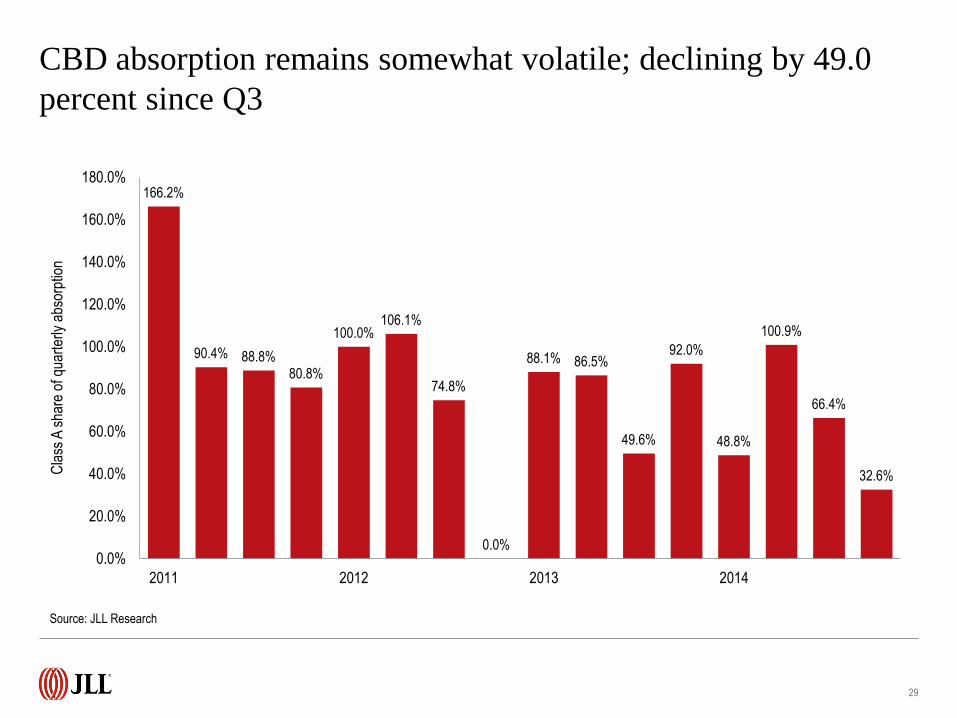

CBD absorption remains somewhat volatile; declining by 49.0

percent since Q3

29

166.2%

90.4% 88.8% 80.8%

100.0% 106.1%

74.8%

0.0%

88.1% 86.5%

49.6%

92.0%

48.8%

100.9%

66.4%

32.6%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

2011 2012 2013 2014

Cla

ss A

sha

re o

f qua

rter

ly a

bsor

ptio

n

Source: JLL Research

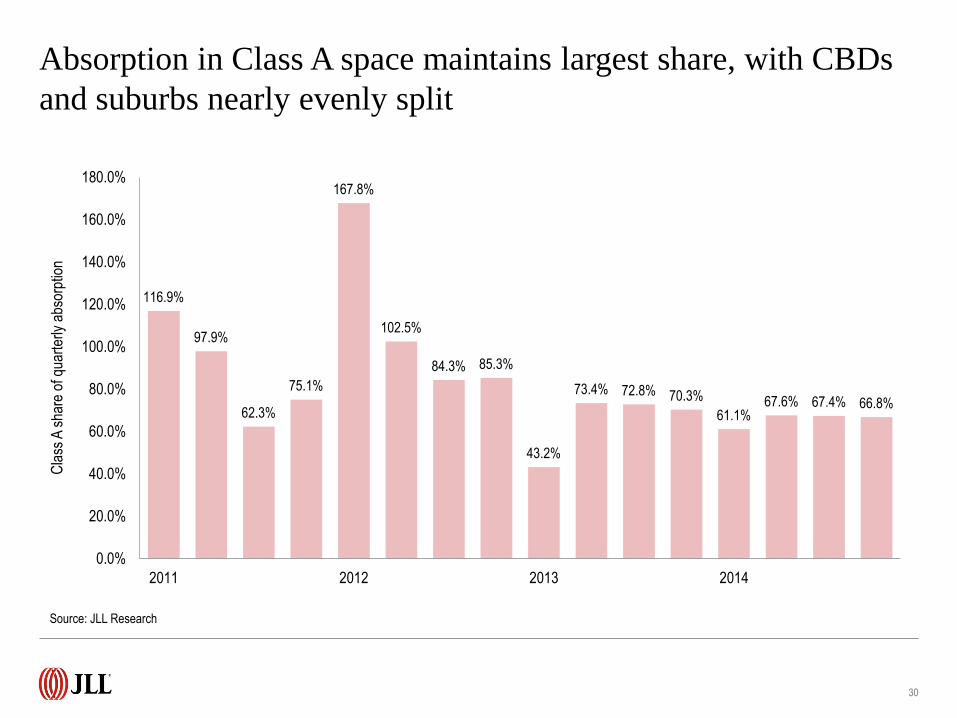

Absorption in Class A space maintains largest share, with CBDs

and suburbs nearly evenly split

30

116.9%

97.9%

62.3%

75.1%

167.8%

102.5%

84.3% 85.3%

43.2%

73.4% 72.8% 70.3%

61.1% 67.6% 67.4% 66.8%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

2011 2012 2013 2014

Cla

ss A

sha

re o

f qua

rter

ly a

bsor

ptio

n

Source: JLL Research

But demand for creative office space is strengthening Class B in

many submarkets across the United States

31

7.3%

5.9% 5.6%

4.7%

3.3%

2.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

San Francisco(SOMA)

Philadelphia(The Navy Yard)

Boston(East Cambridge)

Chicago(River West)

Portland(Lloyd District)

New York(Penn Plaza/Garment)

YT

D C

BD

Cla

ss B

net

abs

orpt

ion

(% o

f inv

ento

ry)

Source: JLL Research

U.S. average

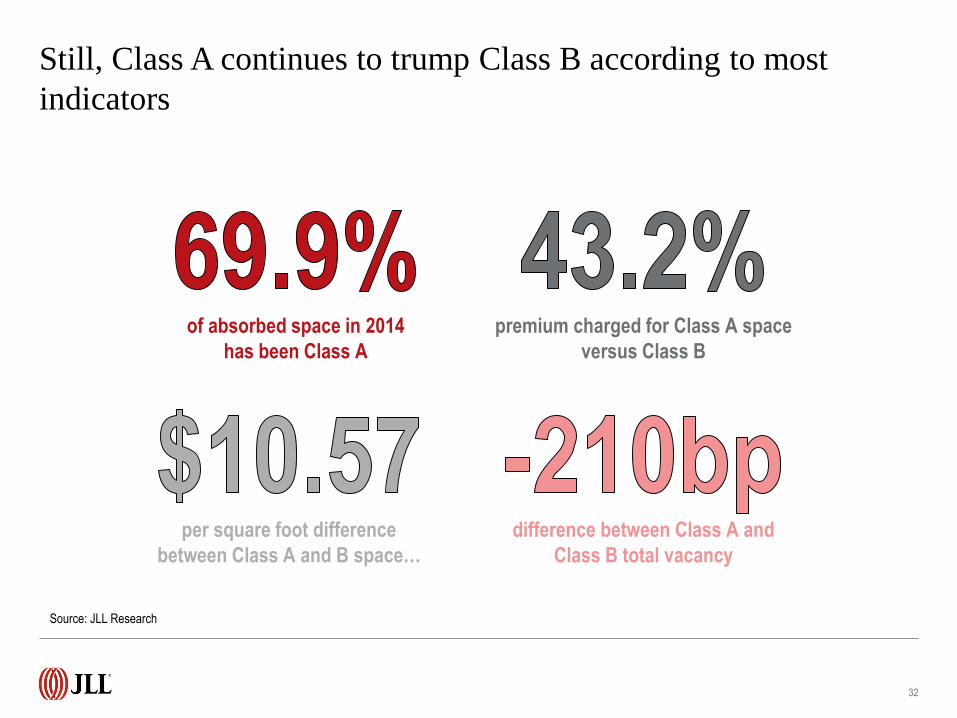

Still, Class A continues to trump Class B according to most

indicators

32

Source: JLL Research

of absorbed space in 2014

has been Class A

per square foot difference

between Class A and B space…

premium charged for Class A space

versus Class B

difference between Class A and

Class B total vacancy

Vacancy

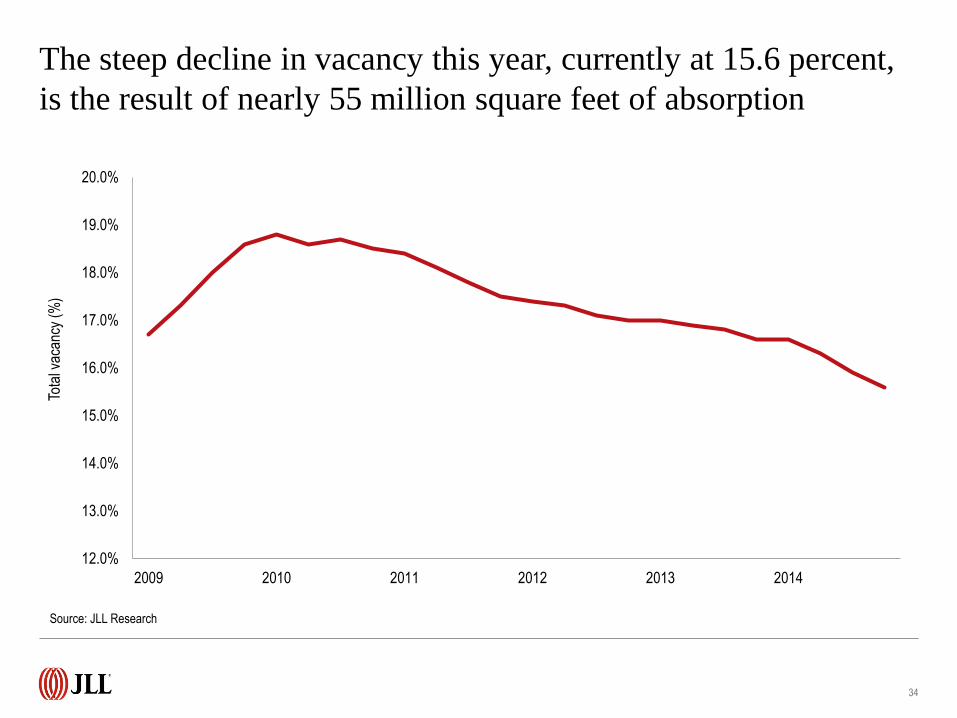

The steep decline in vacancy this year, currently at 15.6 percent,

is the result of nearly 55 million square feet of absorption

34

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

2009 2010 2011 2012 2013 2014

Tota

l vac

ancy

(%

)

Source: JLL Research

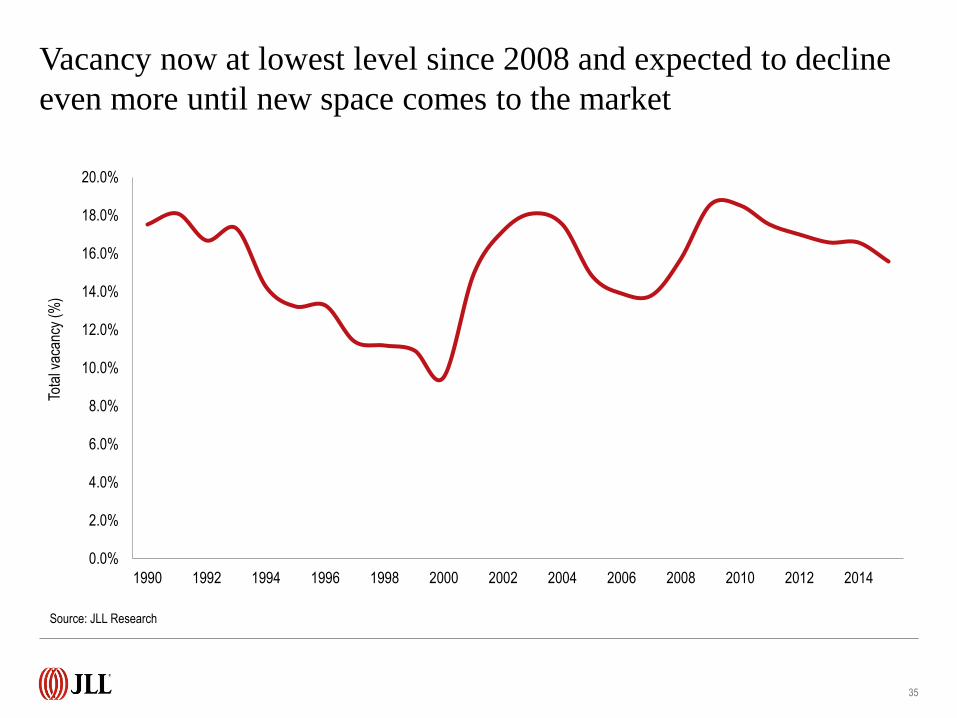

Vacancy now at lowest level since 2008 and expected to decline

even more until new space comes to the market

35

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Tota

l vac

ancy

(%

)

Source: JLL Research

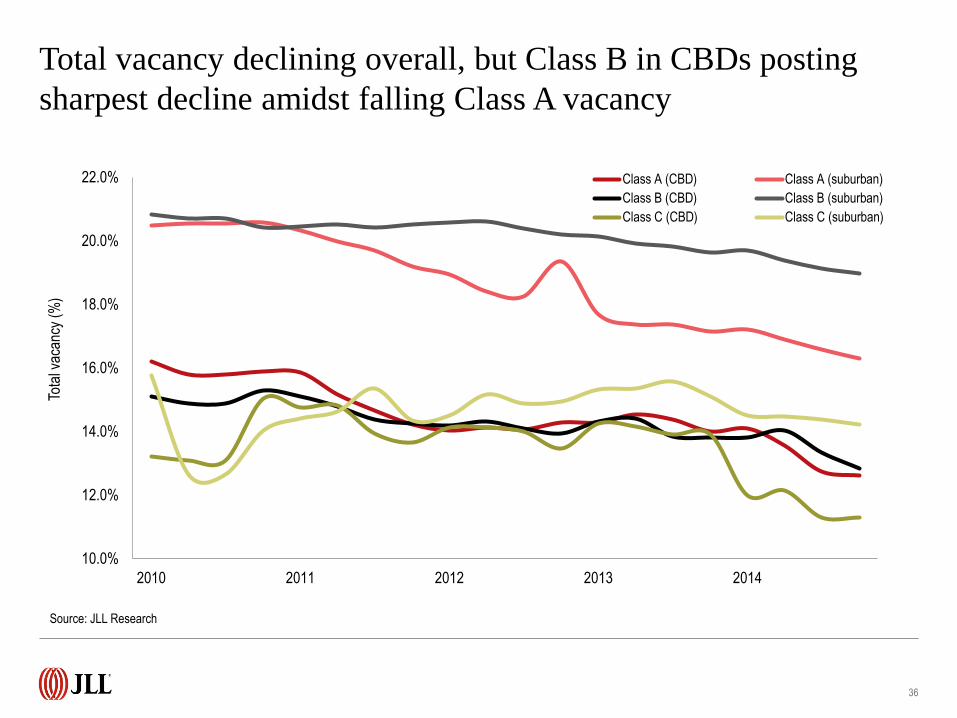

Total vacancy declining overall, but Class B in CBDs posting

sharpest decline amidst falling Class A vacancy

36

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

2010 2011 2012 2013 2014

Tota

l vac

ancy

(%

)

Class A (CBD) Class A (suburban)

Class B (CBD) Class B (suburban)

Class C (CBD) Class C (suburban)

Source: JLL Research

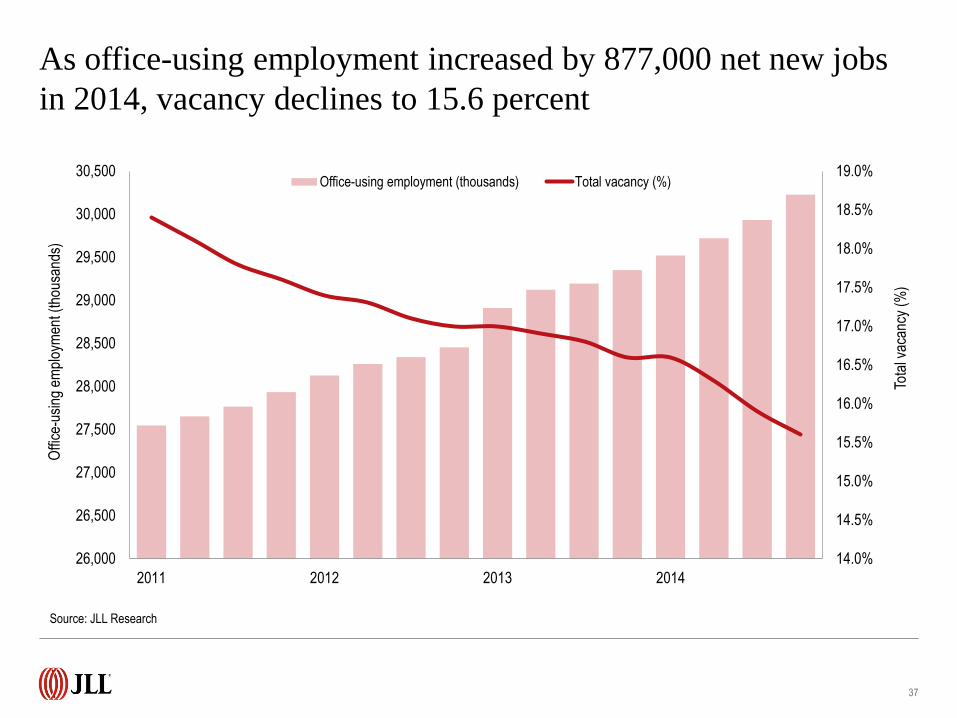

As office-using employment increased by 877,000 net new jobs

in 2014, vacancy declines to 15.6 percent

37

14.0%

14.5%

15.0%

15.5%

16.0%

16.5%

17.0%

17.5%

18.0%

18.5%

19.0%

26,000

26,500

27,000

27,500

28,000

28,500

29,000

29,500

30,000

30,500

2011 2012 2013 2014

Tota

l vac

ancy

(%

)

Offi

ce-u

sing

em

ploy

men

t (th

ousa

nds)

Office-using employment (thousands) Total vacancy (%)

Source: JLL Research

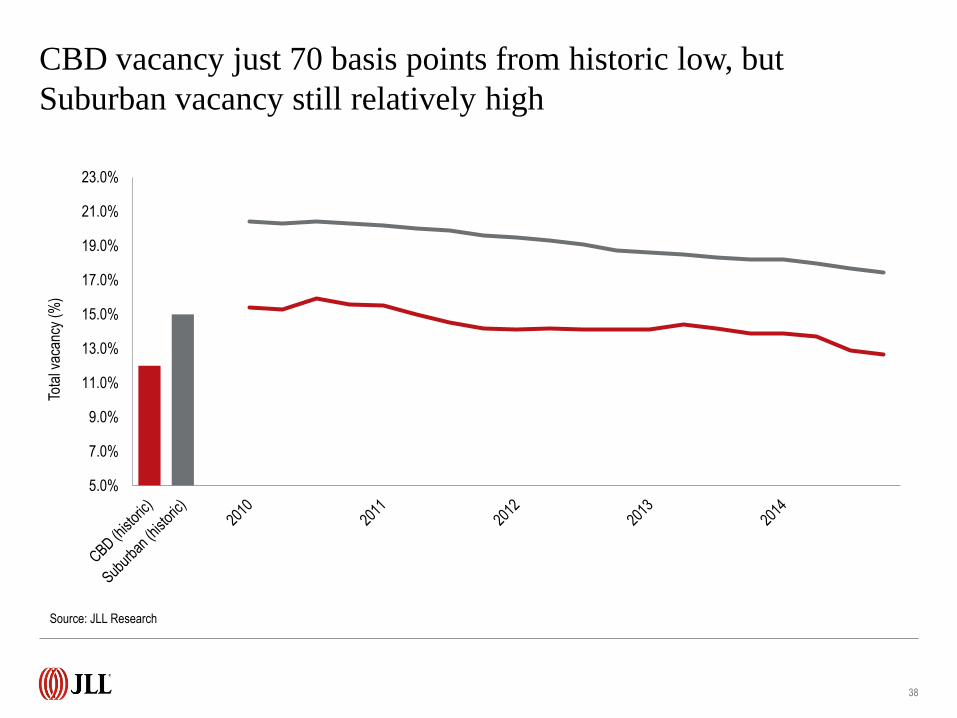

CBD vacancy just 70 basis points from historic low, but

Suburban vacancy still relatively high

38

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

23.0%

Tota

l vac

ancy

(%

)

Source: JLL Research

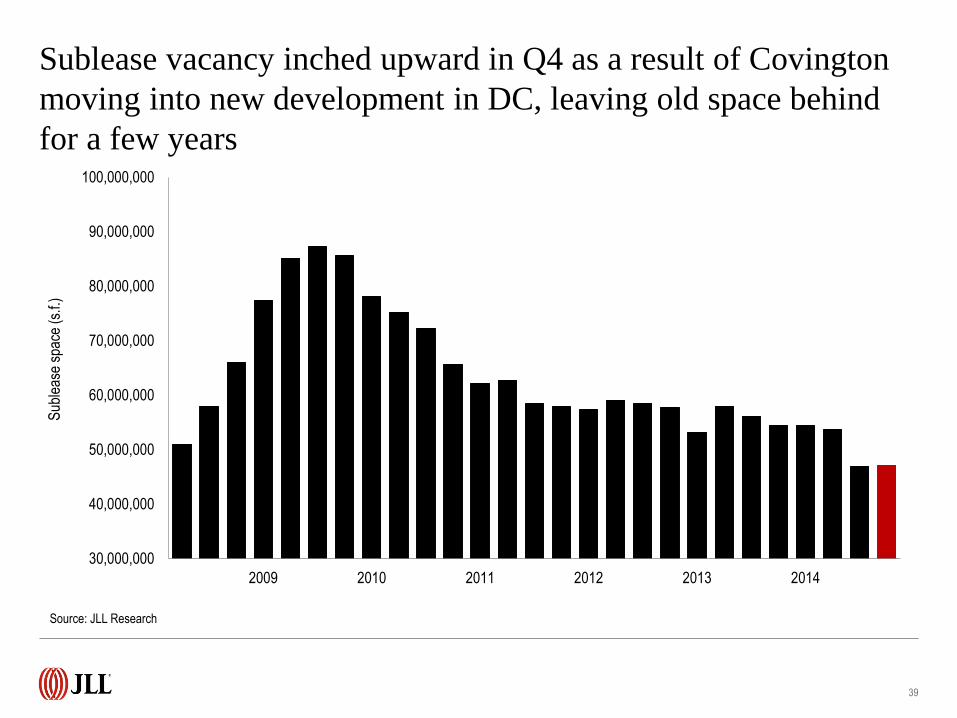

Sublease vacancy inched upward in Q4 as a result of Covington

moving into new development in DC, leaving old space behind

for a few years

39

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

100,000,000

2009 2010 2011 2012 2013 2014

Sub

leas

e sp

ace

(s.f.

)

Source: JLL Research

Rents

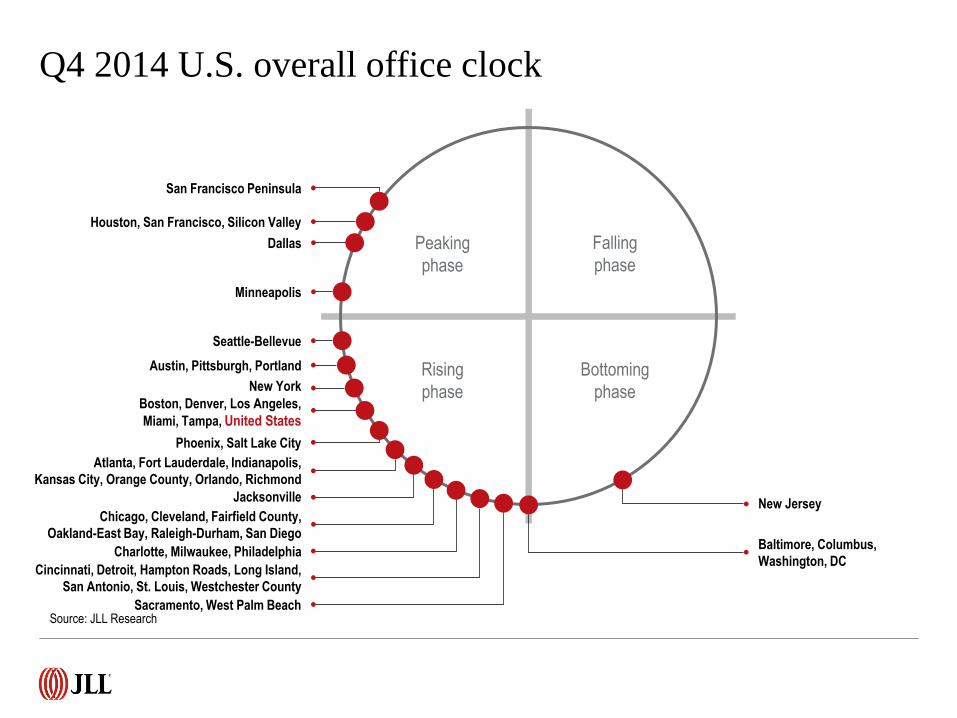

Q4 2014 U.S. overall office clock

Peaking

phase

Falling

phase

Rising

phase

Bottoming

phase

Houston, San Francisco, Silicon Valley

Boston, Denver, Los Angeles,

Miami, Tampa, United States

Cincinnati, Detroit, Hampton Roads, Long Island,

San Antonio, St. Louis, Westchester County

Phoenix, Salt Lake City

Atlanta, Fort Lauderdale, Indianapolis,

Kansas City, Orange County, Orlando, Richmond

Sacramento, West Palm Beach

Baltimore, Columbus,

Washington, DC

Dallas

Austin, Pittsburgh, Portland

San Francisco Peninsula

Jacksonville New Jersey

Chicago, Cleveland, Fairfield County,

Oakland-East Bay, Raleigh-Durham, San Diego

New York

Charlotte, Milwaukee, Philadelphia

Seattle-Bellevue

Minneapolis

Source: JLL Research

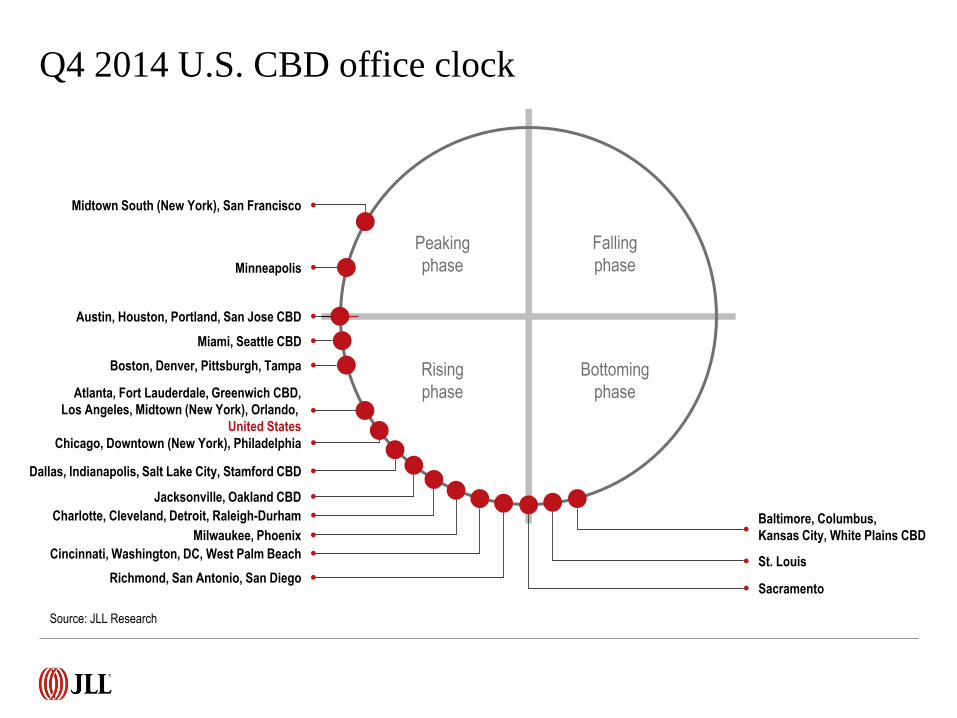

Q4 2014 U.S. CBD office clock

Peaking

phase

Falling

phase

Rising

phase

Bottoming

phase

Austin, Houston, Portland, San Jose CBD

Miami, Seattle CBD

Dallas, Indianapolis, Salt Lake City, Stamford CBD

Atlanta, Fort Lauderdale, Greenwich CBD,

Los Angeles, Midtown (New York), Orlando,

United States

Cincinnati, Washington, DC, West Palm Beach

Boston, Denver, Pittsburgh, Tampa

Richmond, San Antonio, San Diego

Baltimore, Columbus,

Kansas City, White Plains CBD

Jacksonville, Oakland CBD

Midtown South (New York), San Francisco

Chicago, Downtown (New York), Philadelphia

Charlotte, Cleveland, Detroit, Raleigh-Durham

St. Louis

Milwaukee, Phoenix

Sacramento

Minneapolis

Source: JLL Research

Peaking

phase

Falling

phase

Rising

phase

Bottoming

phase

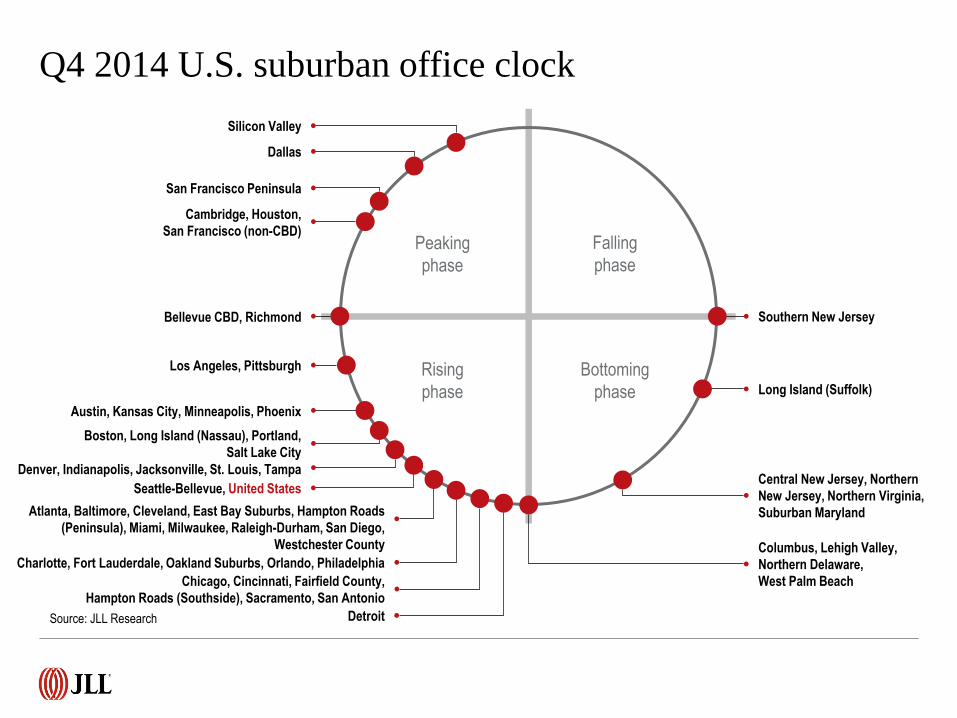

Q4 2014 U.S. suburban office clock

Atlanta, Baltimore, Cleveland, East Bay Suburbs, Hampton Roads

(Peninsula), Miami, Milwaukee, Raleigh-Durham, San Diego,

Westchester County

Boston, Long Island (Nassau), Portland,

Salt Lake City

Long Island (Suffolk)

Charlotte, Fort Lauderdale, Oakland Suburbs, Orlando, Philadelphia Columbus, Lehigh Valley,

Northern Delaware,

West Palm Beach

Central New Jersey, Northern

New Jersey, Northern Virginia,

Suburban Maryland

Dallas

Denver, Indianapolis, Jacksonville, St. Louis, Tampa

Chicago, Cincinnati, Fairfield County,

Hampton Roads (Southside), Sacramento, San Antonio

Bellevue CBD, Richmond

Austin, Kansas City, Minneapolis, Phoenix

Cambridge, Houston,

San Francisco (non-CBD)

San Francisco Peninsula

Silicon Valley

Southern New Jersey

Los Angeles, Pittsburgh

Seattle-Bellevue, United States

Detroit Source: JLL Research

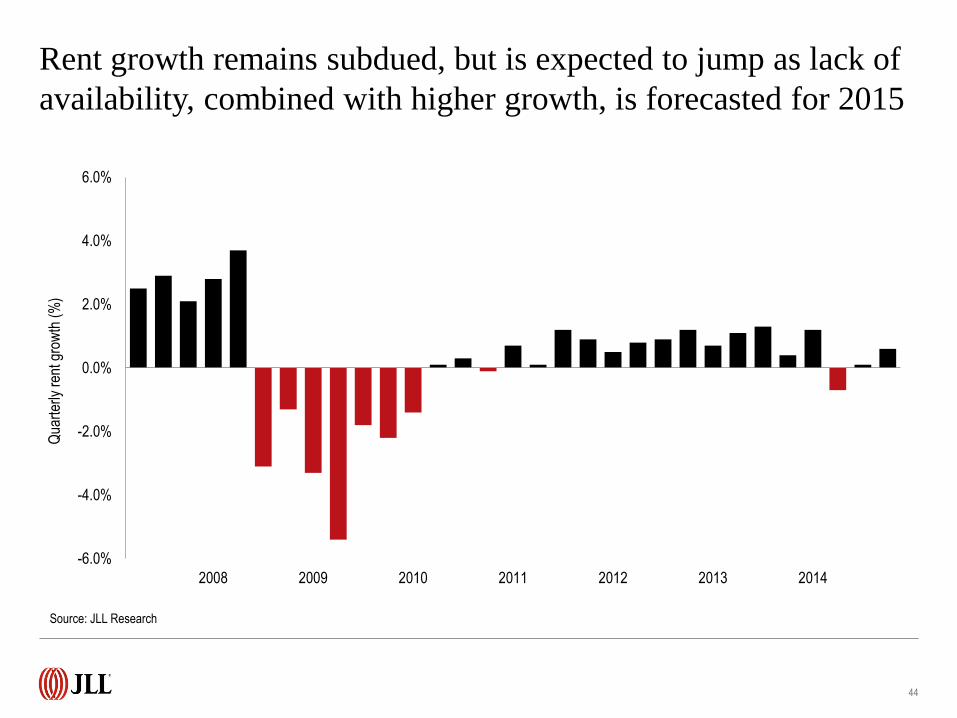

Rent growth remains subdued, but is expected to jump as lack of

availability, combined with higher growth, is forecasted for 2015

44

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2008 2009 2010 2011 2012 2013 2014

Qua

rter

ly r

ent g

row

th (

%)

Source: JLL Research

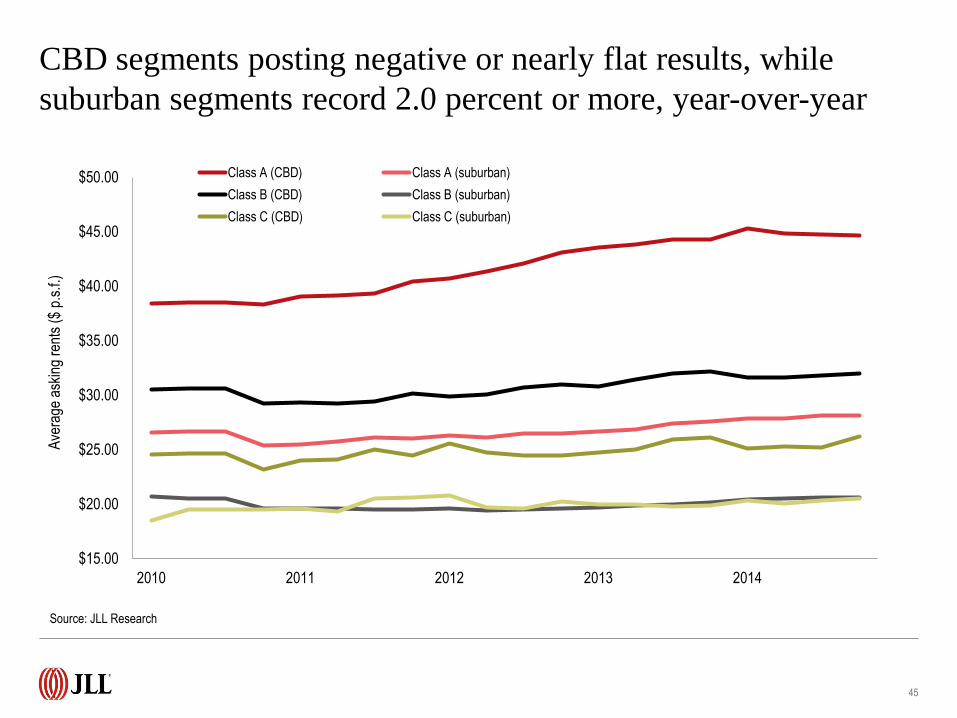

CBD segments posting negative or nearly flat results, while

suburban segments record 2.0 percent or more, year-over-year

45

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

2010 2011 2012 2013 2014

Ave

rage

ask

ing

rent

s ($

p.s

.f.)

Class A (CBD) Class A (suburban)

Class B (CBD) Class B (suburban)

Class C (CBD) Class C (suburban)

Source: JLL Research

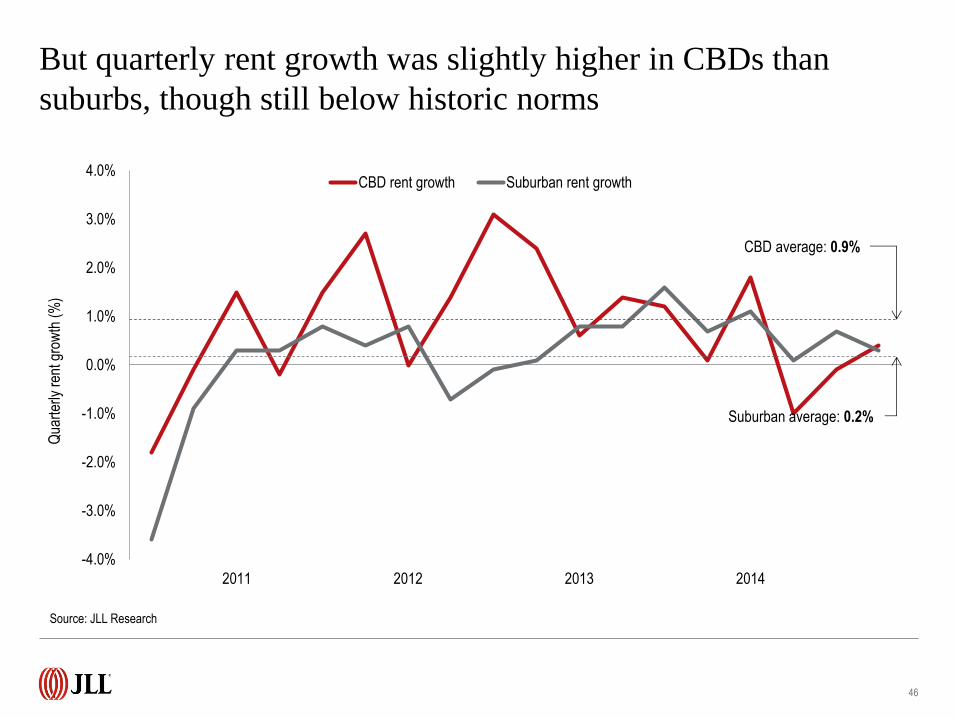

But quarterly rent growth was slightly higher in CBDs than

suburbs, though still below historic norms

46

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2011 2012 2013 2014

Qua

rter

ly r

ent g

row

th (

%)

CBD rent growth Suburban rent growth

Source: JLL Research

CBD average: 0.9%

Suburban average: 0.2%

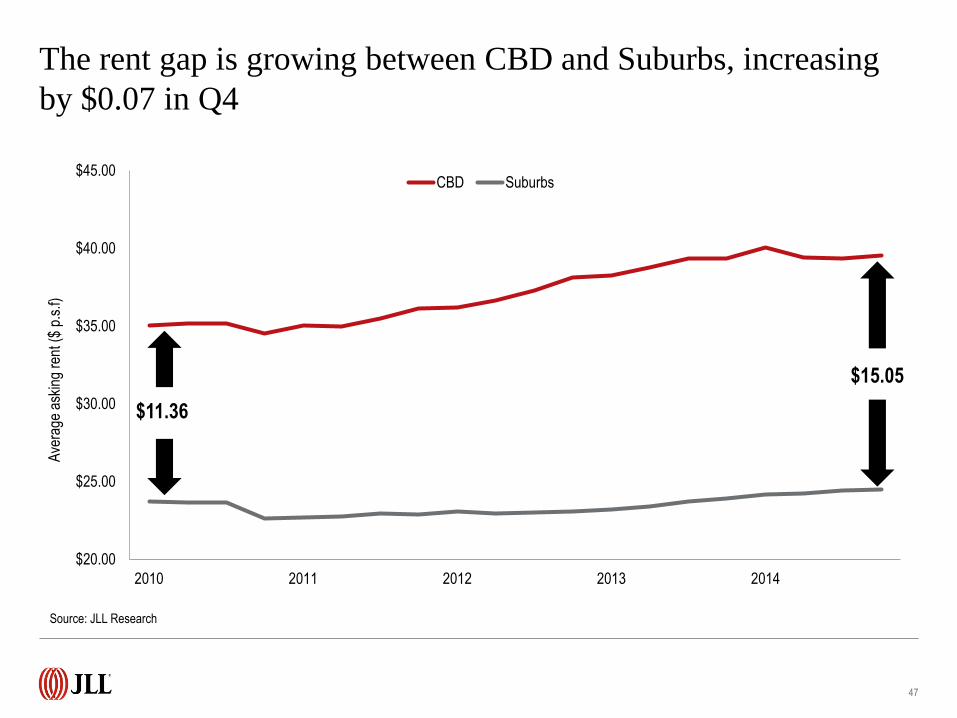

The rent gap is growing between CBD and Suburbs, increasing

by $0.07 in Q4

47

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

2010 2011 2012 2013 2014

Ave

rage

ask

ing

rent

($

p.s.

f)

CBD Suburbs

Source: JLL Research

$11.36

$15.05

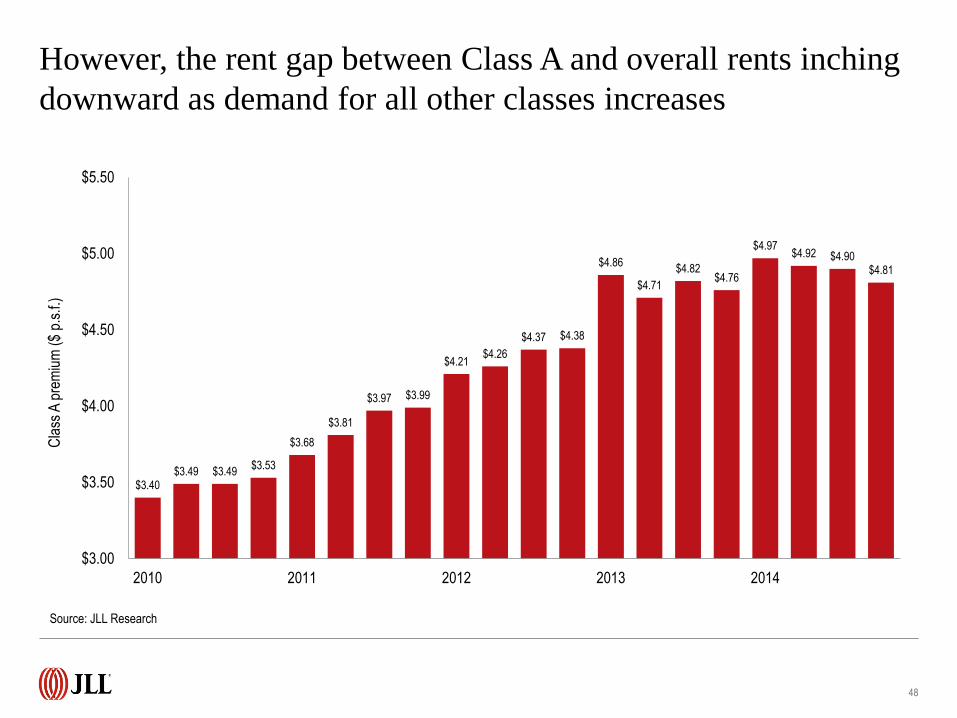

However, the rent gap between Class A and overall rents inching

downward as demand for all other classes increases

48

$3.40 $3.49 $3.49

$3.53

$3.68

$3.81

$3.97 $3.99

$4.21 $4.26

$4.37 $4.38

$4.86

$4.71

$4.82 $4.76

$4.97 $4.92 $4.90

$4.81

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

2010 2011 2012 2013 2014

Cla

ss A

pre

miu

m (

$ p.

s.f.)

Source: JLL Research

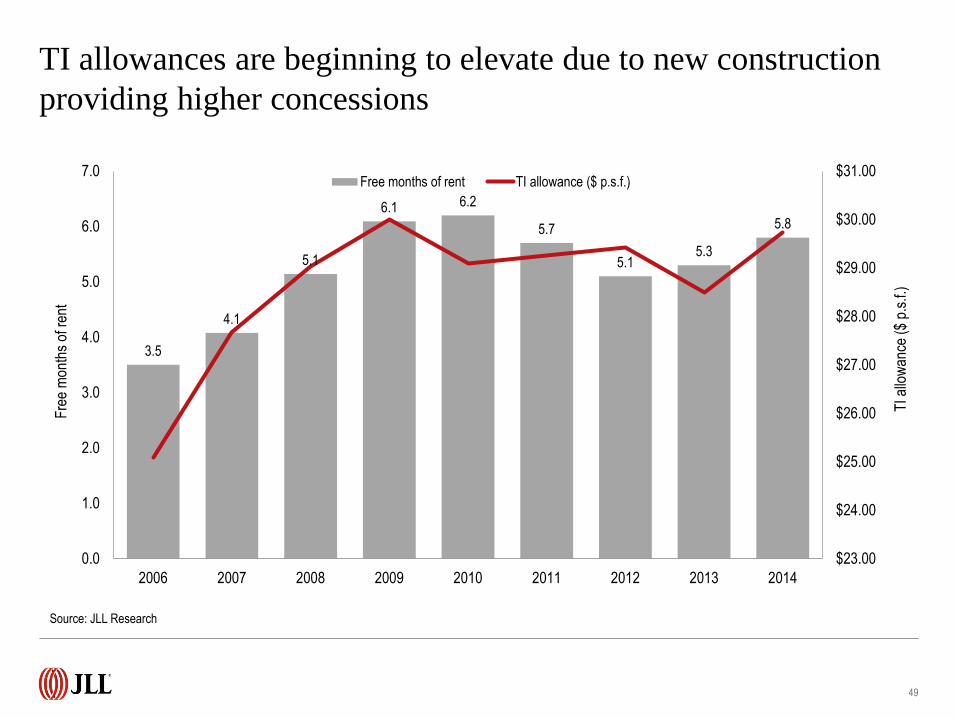

TI allowances are beginning to elevate due to new construction

providing higher concessions

49

3.5

4.1

5.1

6.1 6.2

5.7

5.1 5.3

5.8

$23.00

$24.00

$25.00

$26.00

$27.00

$28.00

$29.00

$30.00

$31.00

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2006 2007 2008 2009 2010 2011 2012 2013 2014

TI a

llow

ance

($

p.s.

f.)

Fre

e m

onth

s of

ren

t

Free months of rent TI allowance ($ p.s.f.)

Source: JLL Research

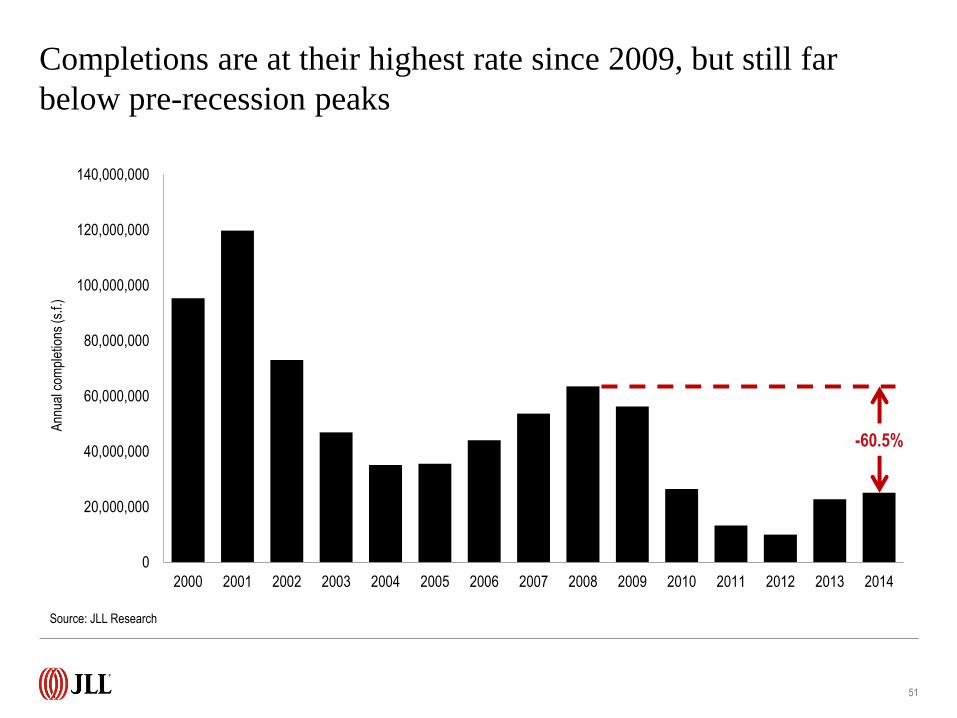

Construction

Completions are at their highest rate since 2009, but still far

below pre-recession peaks

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Ann

ual c

ompl

etio

ns (s

.f.)

51

Source: JLL Research

-60.5%

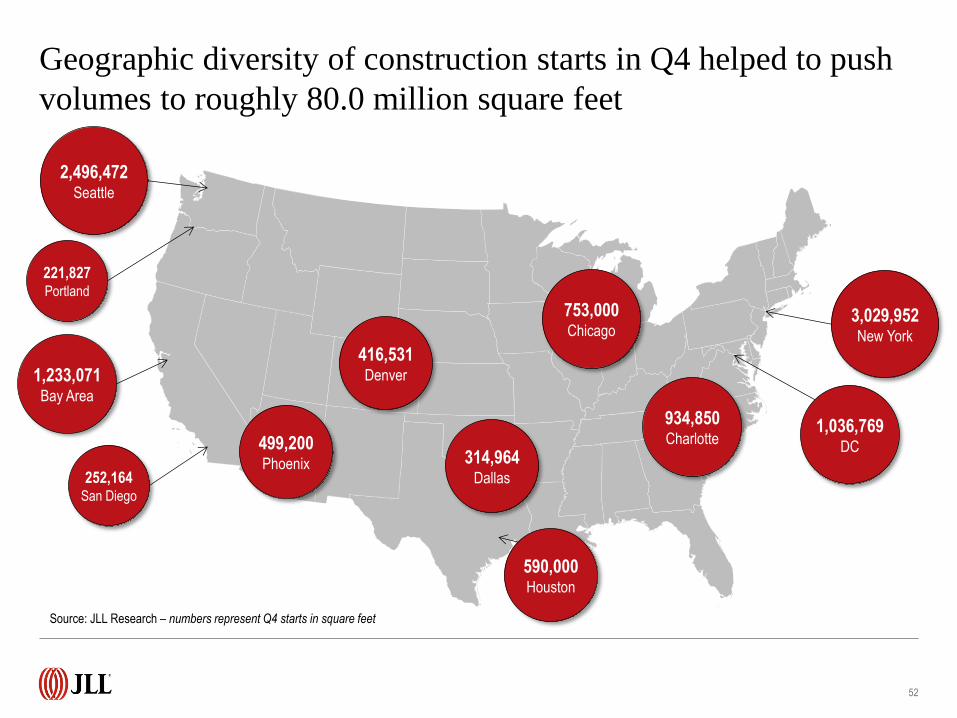

Geographic diversity of construction starts in Q4 helped to push

volumes to roughly 80.0 million square feet

52

Source: JLL Research – numbers represent Q4 starts in square feet

2,496,472 Seattle

221,827 Portland

1,233,071 Bay Area

252,164 San Diego

499,200 Phoenix

416,531 Denver

590,000 Houston

314,964 Dallas

1,036,769 DC

3,029,952 New York

934,850 Charlotte

753,000 Chicago

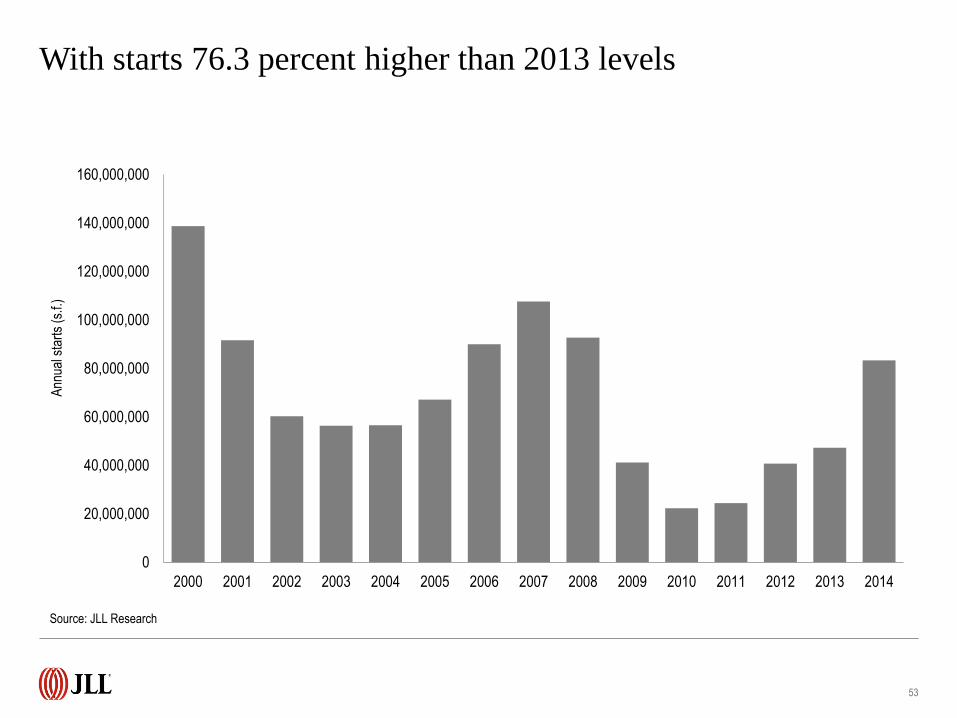

With starts 76.3 percent higher than 2013 levels

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Ann

ual s

tart

s (s

.f.)

53

Source: JLL Research

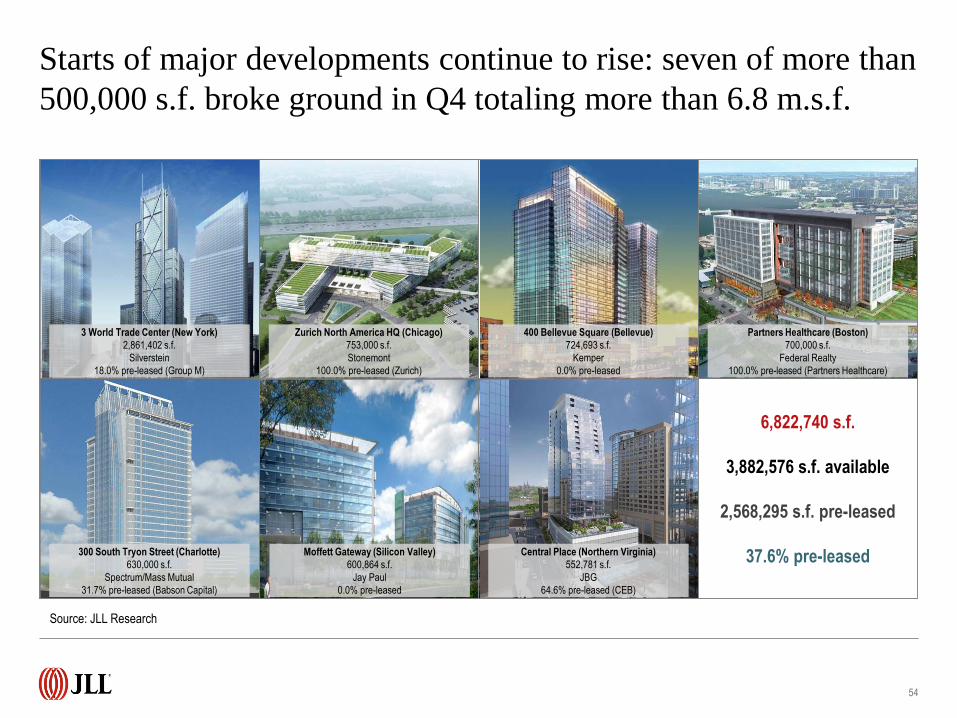

Starts of major developments continue to rise: seven of more than

500,000 s.f. broke ground in Q4 totaling more than 6.8 m.s.f.

54

Source: JLL Research

3 World Trade Center (New York)

2,861,402 s.f.

Silverstein

18.0% pre-leased (Group M)

Central Place (Northern Virginia)

552,781 s.f.

JBG

64.6% pre-leased (CEB)

Zurich North America HQ (Chicago)

753,000 s.f.

Stonemont

100.0% pre-leased (Zurich)

400 Bellevue Square (Bellevue)

724,693 s.f.

Kemper

0.0% pre-leased

Partners Healthcare (Boston)

700,000 s.f.

Federal Realty

100.0% pre-leased (Partners Healthcare)

300 South Tryon Street (Charlotte)

630,000 s.f.

Spectrum/Mass Mutual

31.7% pre-leased (Babson Capital)

Moffett Gateway (Silicon Valley)

600,864 s.f.

Jay Paul

0.0% pre-leased

6,822,740 s.f.

3,882,576 s.f. available

2,568,295 s.f. pre-leased

37.6% pre-leased

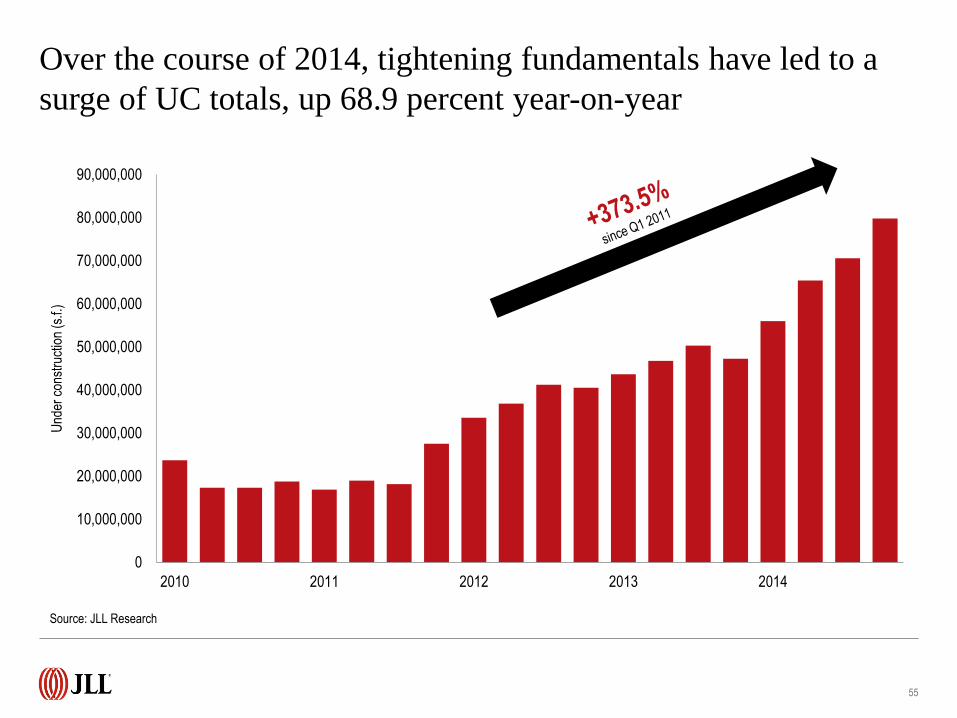

Over the course of 2014, tightening fundamentals have led to a

surge of UC totals, up 68.9 percent year-on-year

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

2010 2011 2012 2013 2014

Und

er c

onst

ruct

ion

(s.f.

)

55

Source: JLL Research

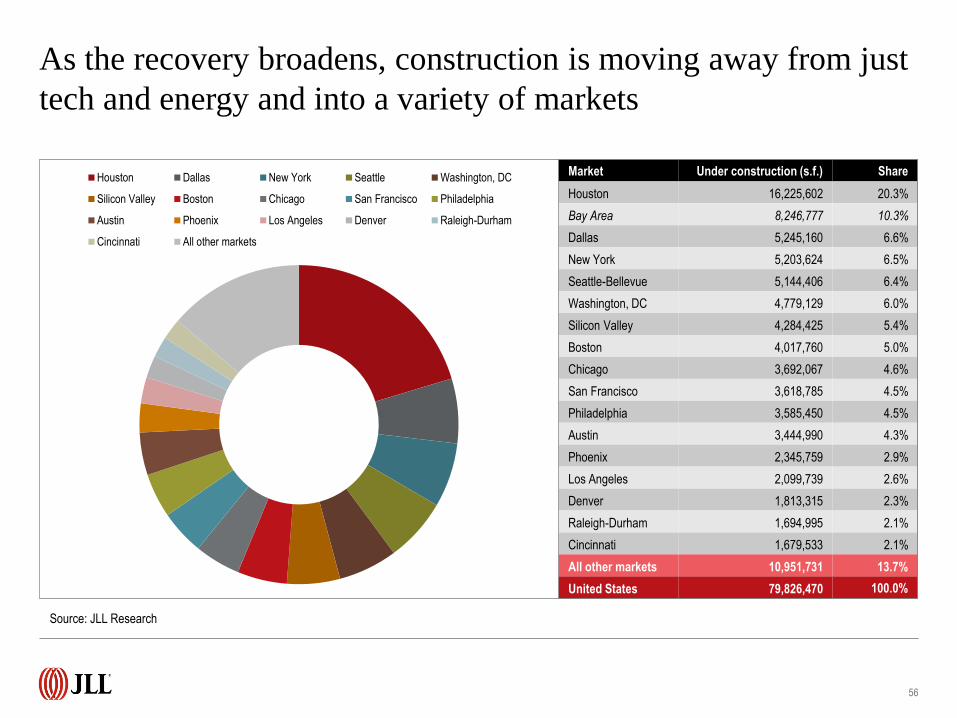

Market Under construction (s.f.) Share

Houston 16,225,602 20.3%

Bay Area 8,246,777 10.3%

Dallas 5,245,160 6.6%

New York 5,203,624 6.5%

Seattle-Bellevue 5,144,406 6.4%

Washington, DC 4,779,129 6.0%

Silicon Valley 4,284,425 5.4%

Boston 4,017,760 5.0%

Chicago 3,692,067 4.6%

San Francisco 3,618,785 4.5%

Philadelphia 3,585,450 4.5%

Austin 3,444,990 4.3%

Phoenix 2,345,759 2.9%

Los Angeles 2,099,739 2.6%

Denver 1,813,315 2.3%

Raleigh-Durham 1,694,995 2.1%

Cincinnati 1,679,533 2.1%

All other markets 10,951,731 13.7%

United States 79,826,470 100.0%

As the recovery broadens, construction is moving away from just

tech and energy and into a variety of markets

Houston Dallas New York Seattle Washington, DC

Silicon Valley Boston Chicago San Francisco Philadelphia

Austin Phoenix Los Angeles Denver Raleigh-Durham

Cincinnati All other markets

56

Source: JLL Research

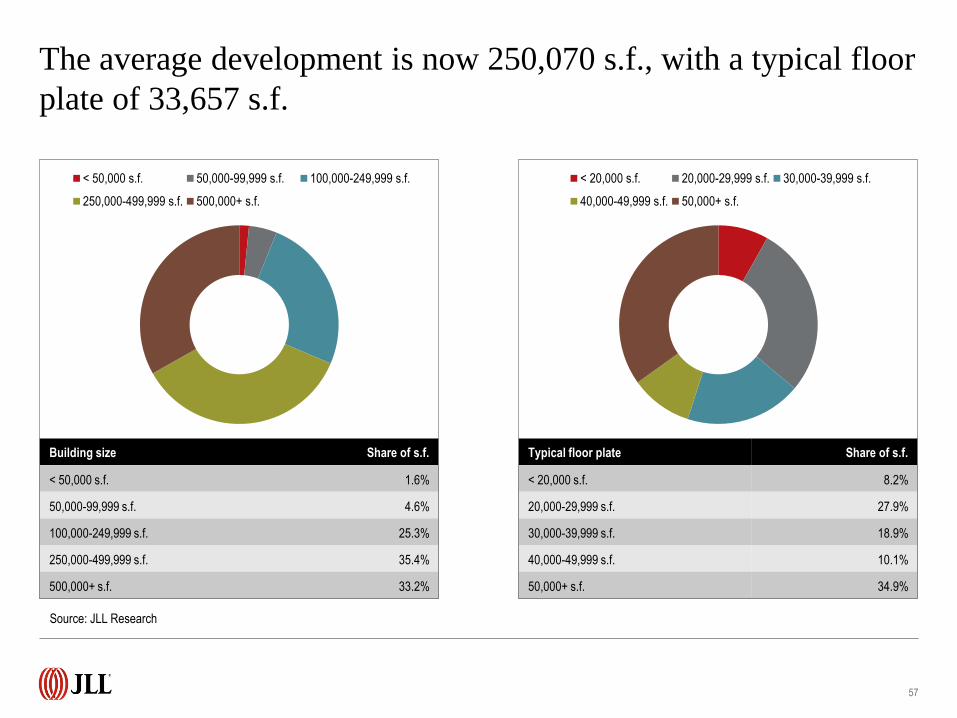

Typical floor plate Share of s.f.

< 20,000 s.f. 8.2%

20,000-29,999 s.f. 27.9%

30,000-39,999 s.f. 18.9%

40,000-49,999 s.f. 10.1%

50,000+ s.f. 34.9%

< 50,000 s.f. 50,000-99,999 s.f. 100,000-249,999 s.f.

250,000-499,999 s.f. 500,000+ s.f.

Building size Share of s.f.

< 50,000 s.f. 1.6%

50,000-99,999 s.f. 4.6%

100,000-249,999 s.f. 25.3%

250,000-499,999 s.f. 35.4%

500,000+ s.f. 33.2%

The average development is now 250,070 s.f., with a typical floor

plate of 33,657 s.f.

57

< 20,000 s.f. 20,000-29,999 s.f. 30,000-39,999 s.f.

40,000-49,999 s.f. 50,000+ s.f.

Source: JLL Research

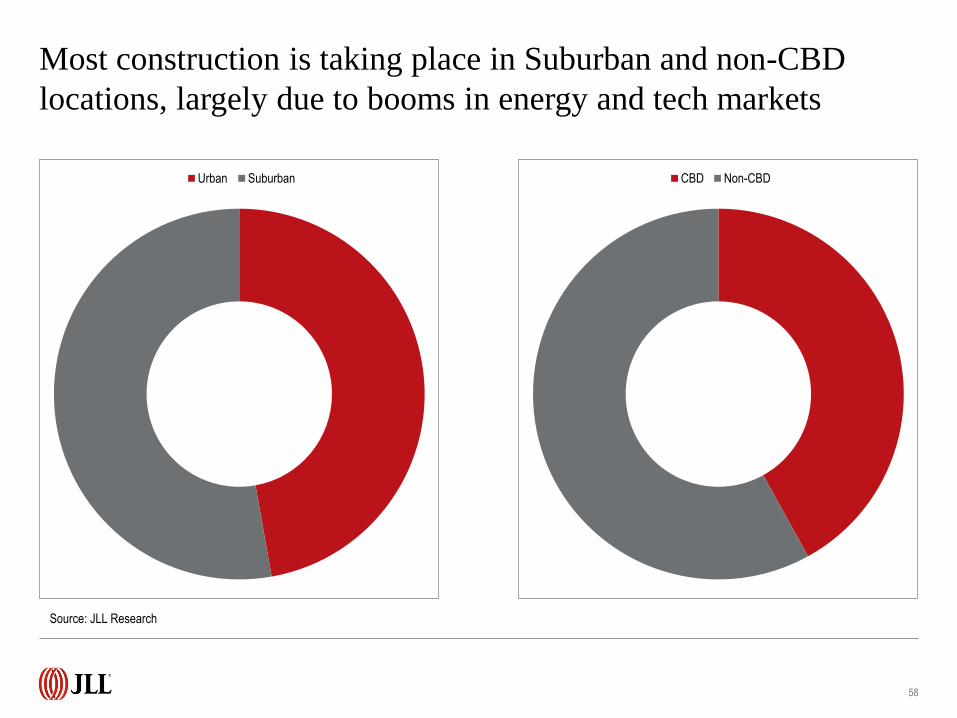

Urban Suburban

Most construction is taking place in Suburban and non-CBD

locations, largely due to booms in energy and tech markets

58

CBD Non-CBD

Source: JLL Research

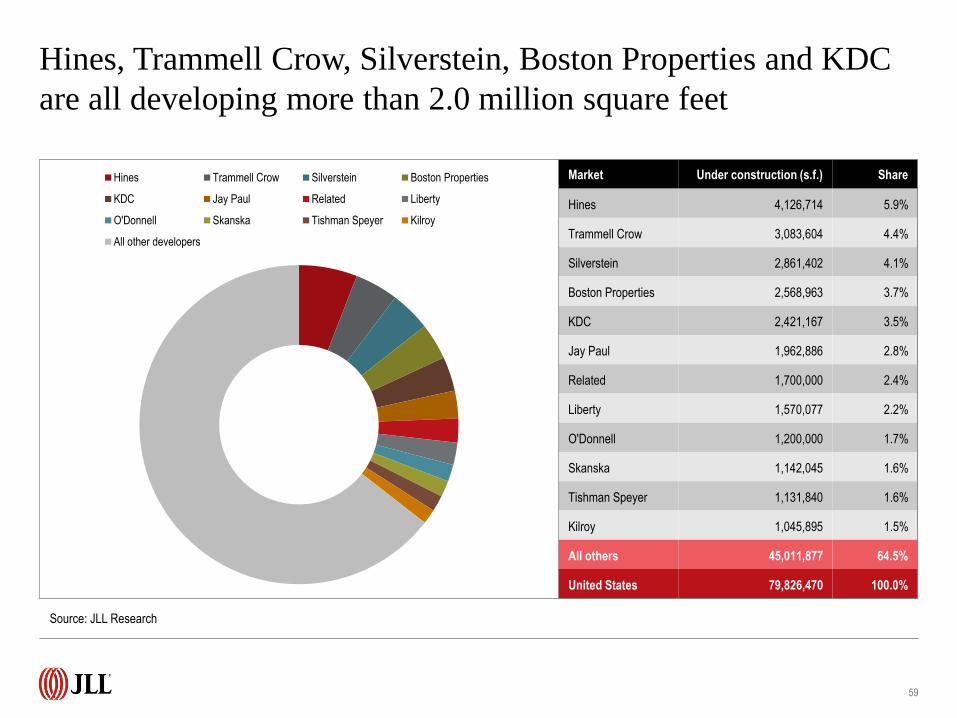

Market Under construction (s.f.) Share

Hines 4,126,714 5.9%

Trammell Crow 3,083,604 4.4%

Silverstein 2,861,402 4.1%

Boston Properties 2,568,963 3.7%

KDC 2,421,167 3.5%

Jay Paul 1,962,886 2.8%

Related 1,700,000 2.4%

Liberty 1,570,077 2.2%

O'Donnell 1,200,000 1.7%

Skanska 1,142,045 1.6%

Tishman Speyer 1,131,840 1.6%

Kilroy 1,045,895 1.5%

All others 45,011,877 64.5%

United States 79,826,470 100.0%

Hines, Trammell Crow, Silverstein, Boston Properties and KDC

are all developing more than 2.0 million square feet

Hines Trammell Crow Silverstein Boston Properties

KDC Jay Paul Related Liberty

O'Donnell Skanska Tishman Speyer Kilroy

All other developers

59

Source: JLL Research

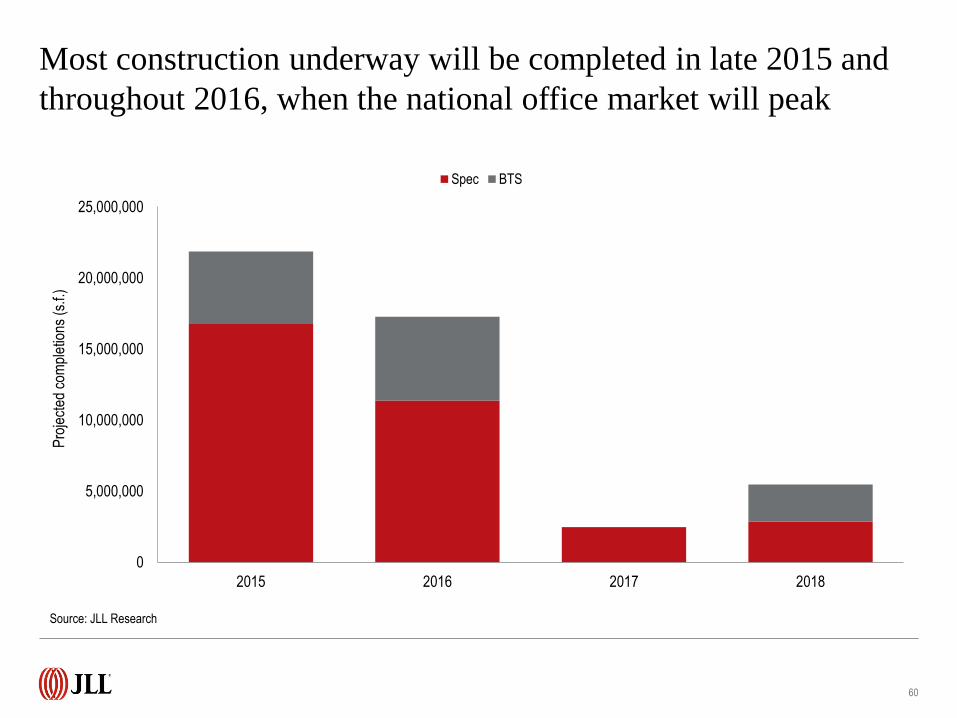

Most construction underway will be completed in late 2015 and

throughout 2016, when the national office market will peak

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

2015 2016 2017 2018

Pro

ject

ed c

ompl

etio

ns (

s.f.)

Spec BTS

60

Source: JLL Research

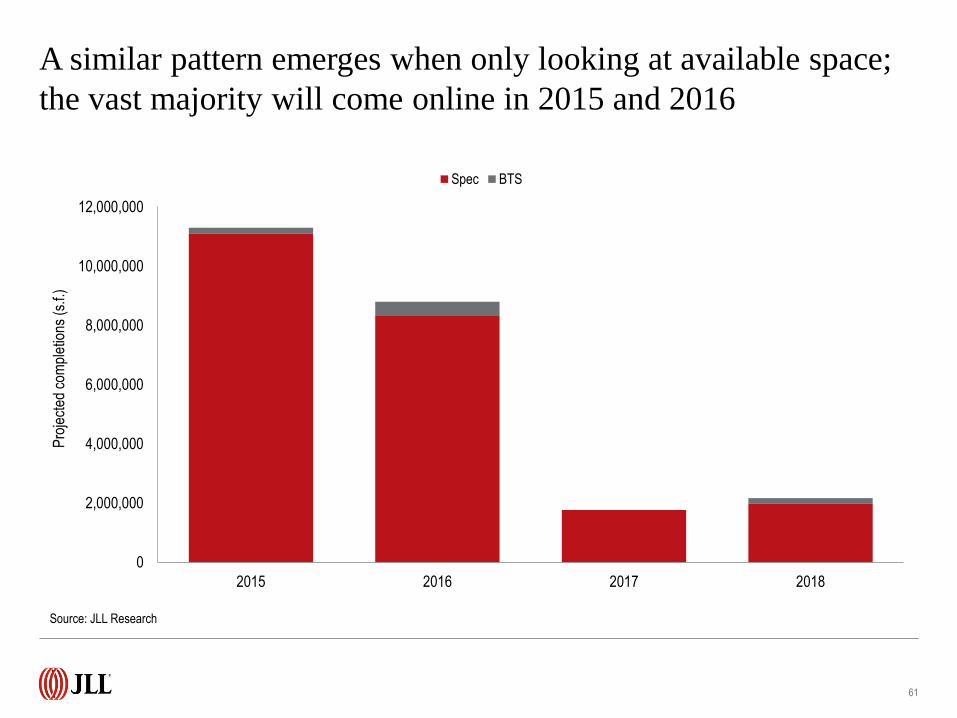

A similar pattern emerges when only looking at available space;

the vast majority will come online in 2015 and 2016

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

2015 2016 2017 2018

Pro

ject

ed c

ompl

etio

ns (

s.f.)

Spec BTS

61

Source: JLL Research

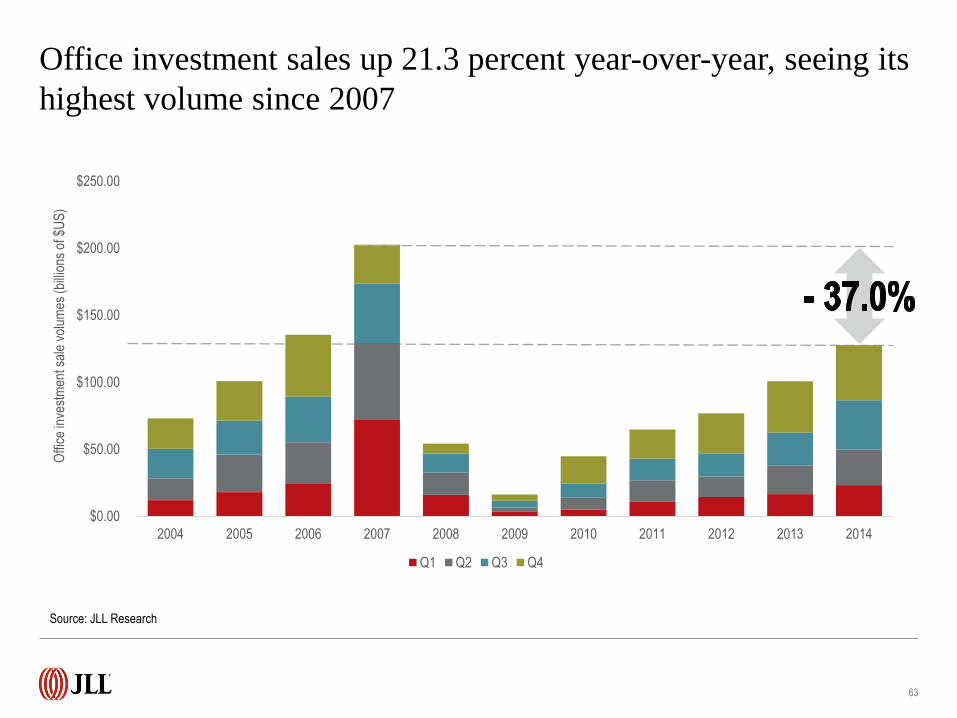

Investment sales

Office investment sales up 21.3 percent year-over-year, seeing its

highest volume since 2007

63

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Offi

ce in

vest

men

t sal

e vo

lum

es (b

illio

ns o

f $U

S)

Q1 Q2 Q3 Q4

Source: JLL Research

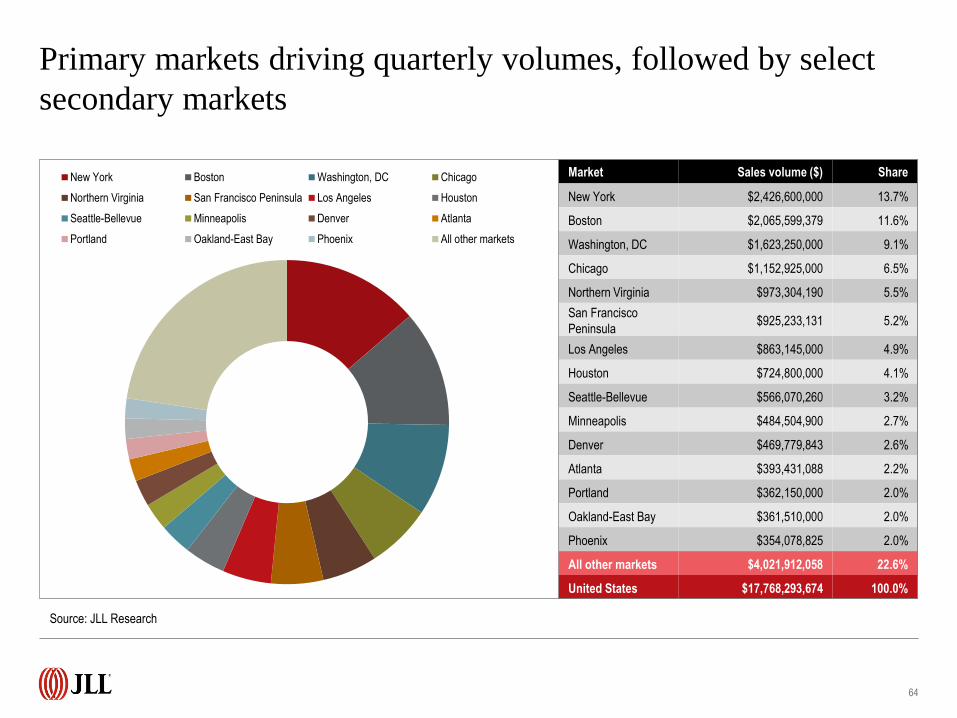

Market Sales volume ($) Share

New York $2,426,600,000 13.7%

Boston $2,065,599,379 11.6%

Washington, DC $1,623,250,000 9.1%

Chicago $1,152,925,000 6.5%

Northern Virginia $973,304,190 5.5%

San Francisco

Peninsula $925,233,131 5.2%

Los Angeles $863,145,000 4.9%

Houston $724,800,000 4.1%

Seattle-Bellevue $566,070,260 3.2%

Minneapolis $484,504,900 2.7%

Denver $469,779,843 2.6%

Atlanta $393,431,088 2.2%

Portland $362,150,000 2.0%

Oakland-East Bay $361,510,000 2.0%

Phoenix $354,078,825 2.0%

All other markets $4,021,912,058 22.6%

United States $17,768,293,674 100.0%

Primary markets driving quarterly volumes, followed by select

secondary markets

New York Boston Washington, DC Chicago

Northern Virginia San Francisco Peninsula Los Angeles Houston

Seattle-Bellevue Minneapolis Denver Atlanta

Portland Oakland-East Bay Phoenix All other markets

64

Source: JLL Research

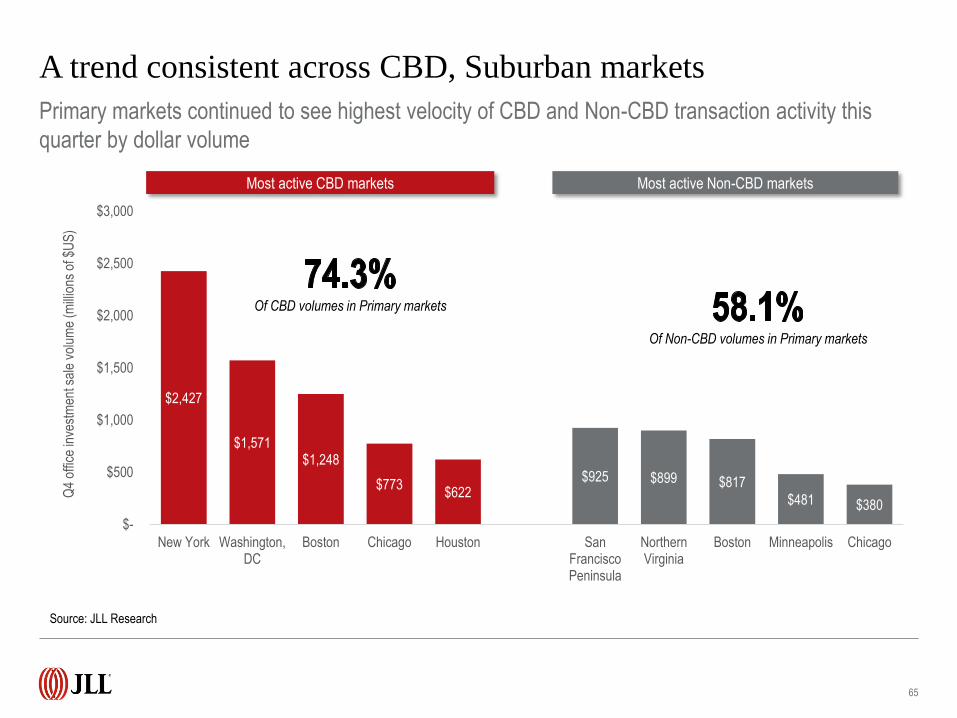

A trend consistent across CBD, Suburban markets

Primary markets continued to see highest velocity of CBD and Non-CBD transaction activity this

quarter by dollar volume

65

$2,427

$1,571 $1,248

$773 $622

$925 $899 $817

$481 $380

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

New York Washington,DC

Boston Chicago Houston SanFranciscoPeninsula

NorthernVirginia

Boston Minneapolis Chicago

Q4

offic

e in

vest

men

t sal

e vo

lum

e (m

illio

ns o

f $U

S)

Most active CBD markets Most active Non-CBD markets

Of CBD volumes in Primary markets

Of Non-CBD volumes in Primary markets

Source: JLL Research

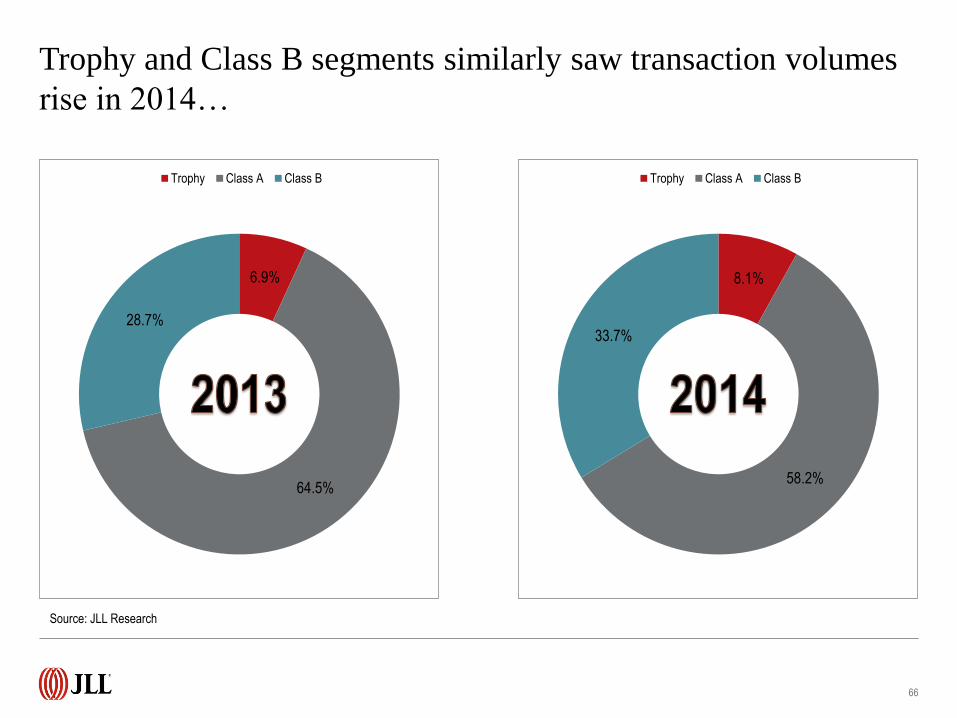

6.9%

64.5%

28.7%

Trophy Class A Class B

Trophy and Class B segments similarly saw transaction volumes

rise in 2014…

66

8.1%

58.2%

33.7%

Trophy Class A Class B

Source: JLL Research

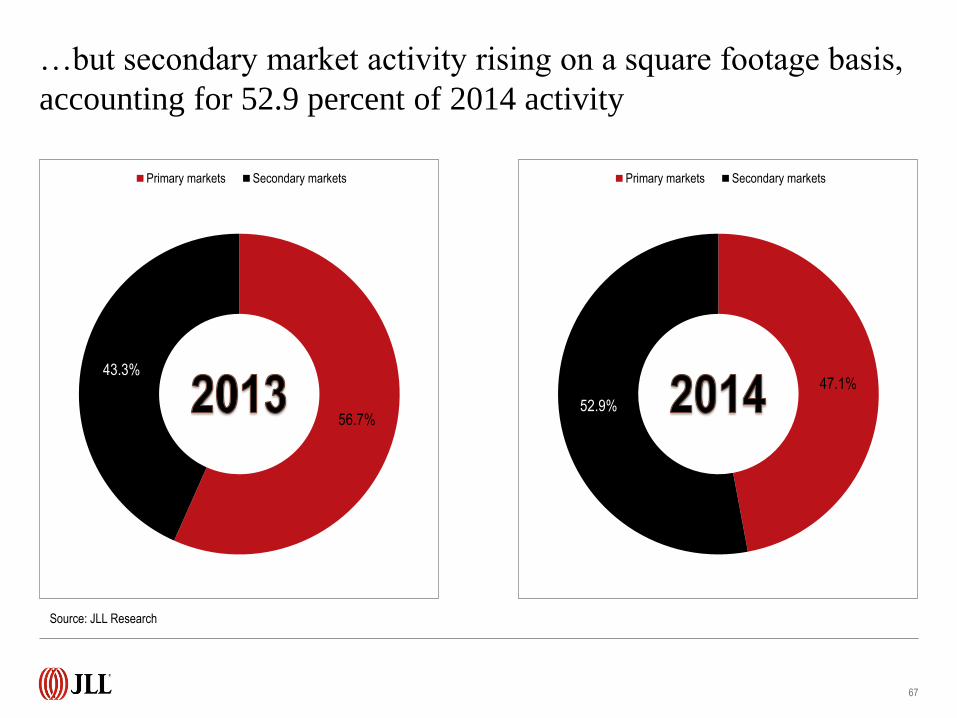

56.7%

43.3%

Primary markets Secondary markets

…but secondary market activity rising on a square footage basis,

accounting for 52.9 percent of 2014 activity

67

47.1%

52.9%

Primary markets Secondary markets

Source: JLL Research

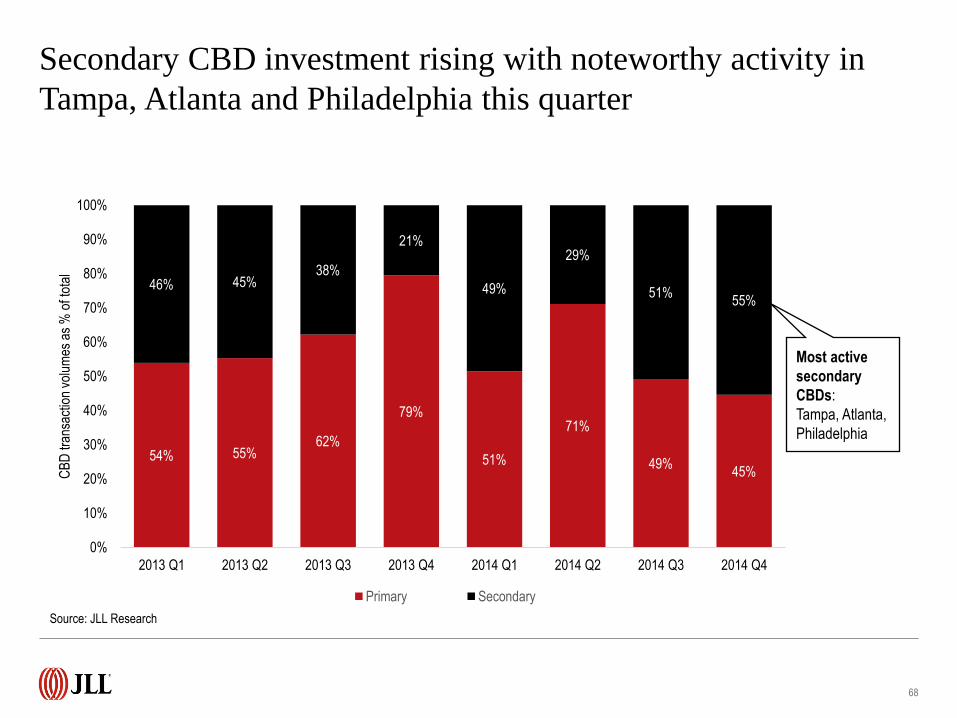

Secondary CBD investment rising with noteworthy activity in

Tampa, Atlanta and Philadelphia this quarter

68

54% 55% 62%

79%

51%

71%

49% 45%

46% 45% 38%

21%

49%

29%

51% 55%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 Q1 2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

CB

D tr

ansa

ctio

n vo

lum

es a

s %

of t

otal

Primary Secondary

Most active

secondary

CBDs:

Tampa, Atlanta,

Philadelphia

Source: JLL Research

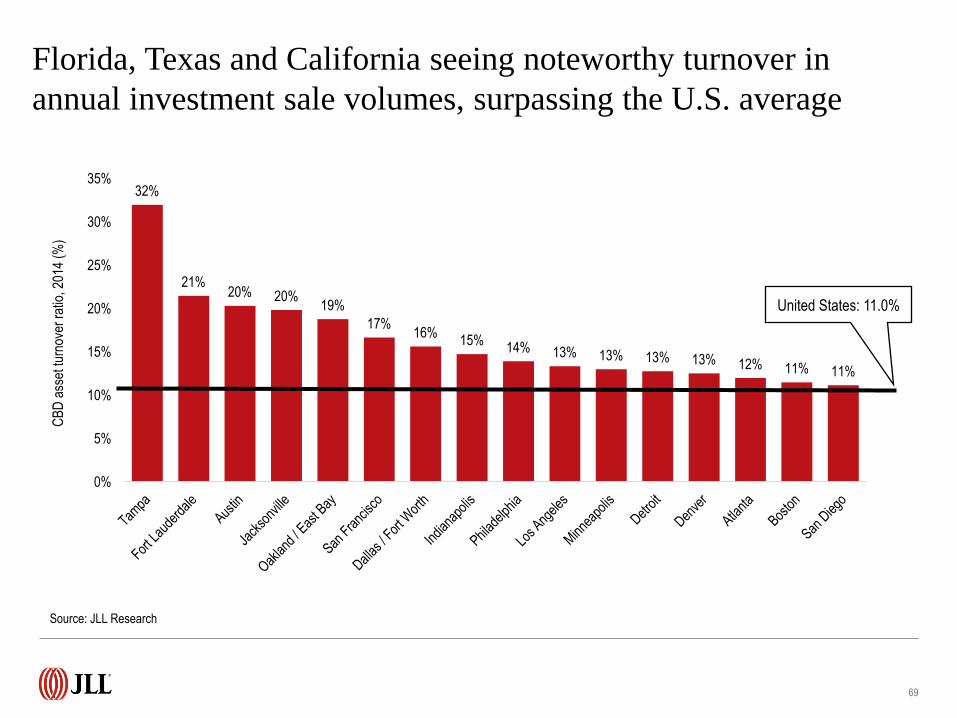

Florida, Texas and California seeing noteworthy turnover in

annual investment sale volumes, surpassing the U.S. average

69

32%

21% 20% 20%

19%

17% 16%

15% 14% 13% 13% 13% 13% 12% 11% 11%

0%

5%

10%

15%

20%

25%

30%

35%

CB

D a

sset

turn

over

rat

io, 2

014

(%)

United States: 11.0%

Source: JLL Research

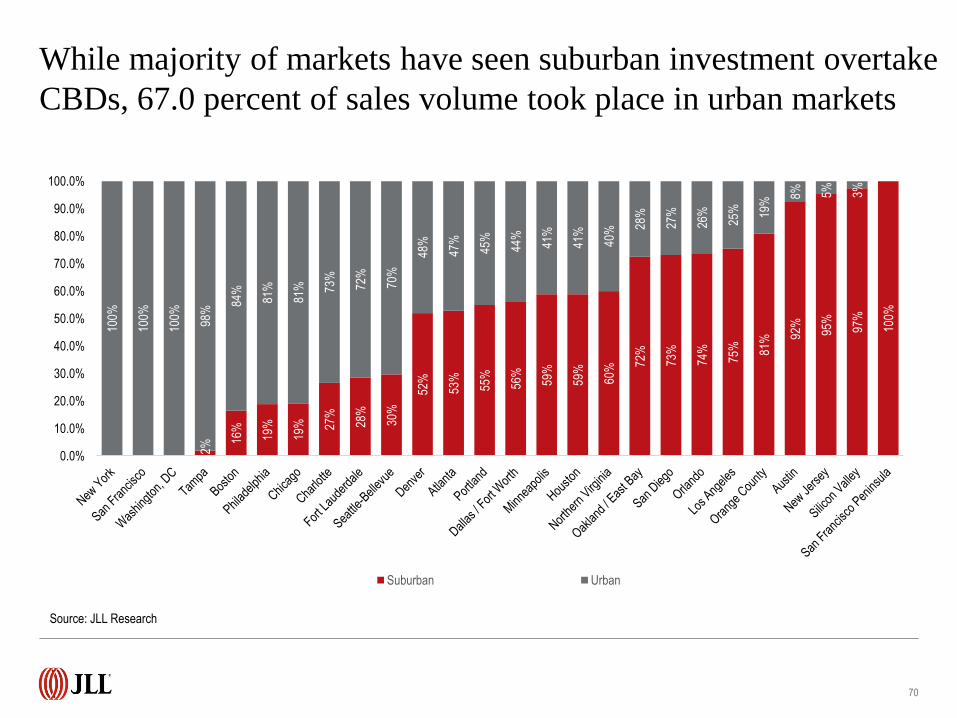

While majority of markets have seen suburban investment overtake

CBDs, 67.0 percent of sales volume took place in urban markets

70

2% 16

%

19%

19%

27%

28%

30%

52%

53%

55%

56%

59%

59%

60%

72%

73%

74%

75%

81%

92%

95%

97%

100%

100%

100%

100%

98%

84%

81%

81%

73%

72%

70%

48%

47%

45%

44%

41%

41%

40%

28%

27%

26%

25%

19%

8%

5%

3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Suburban Urban

Source: JLL Research

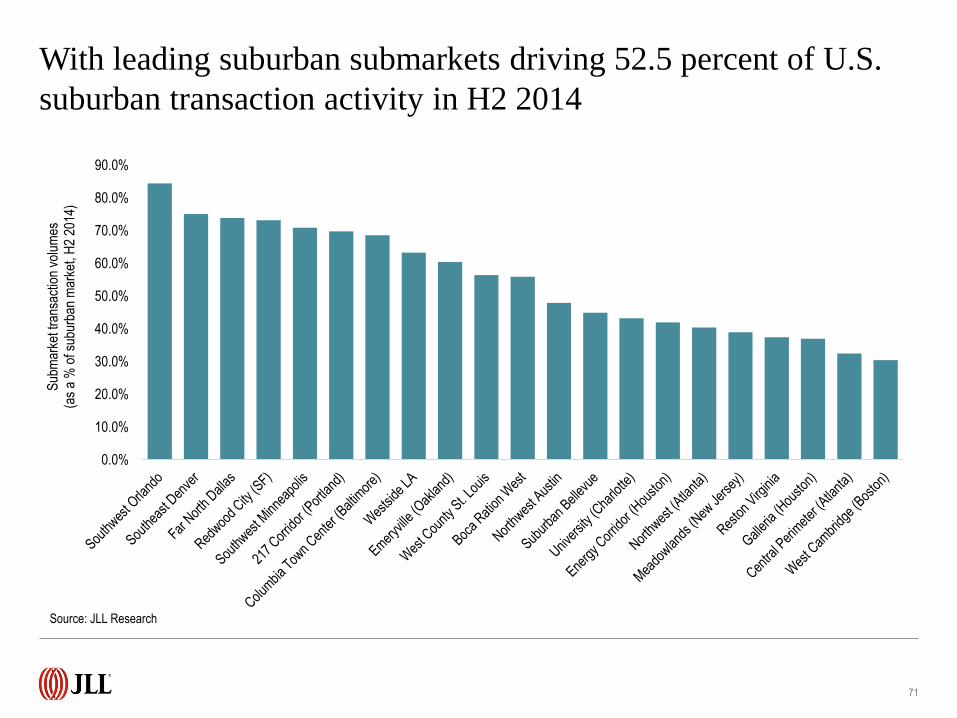

With leading suburban submarkets driving 52.5 percent of U.S.

suburban transaction activity in H2 2014

71

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Sub

mar

ket t

rans

actio

n vo

lum

es

(as

a %

of s

ubur

ban

mar

ket,

H2

2014

)

Source: JLL Research

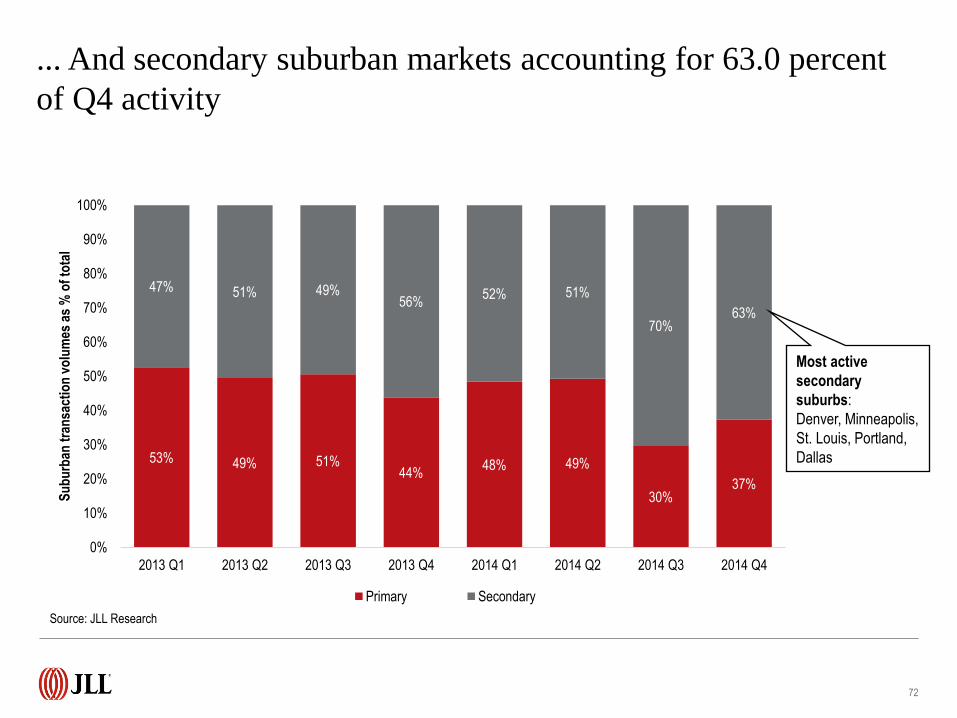

... And secondary suburban markets accounting for 63.0 percent

of Q4 activity

72

53% 49% 51% 44%

48% 49%

30% 37%

47% 51% 49% 56%

52% 51%

70% 63%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 Q1 2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

Su

bu

rban

tra

nsa

ctio

n v

olu

mes

as

% o

f to

tal

Primary Secondary

Most active

secondary

suburbs:

Denver, Minneapolis,

St. Louis, Portland,

Dallas

Source: JLL Research

Outlook

74

Source: JLL Research

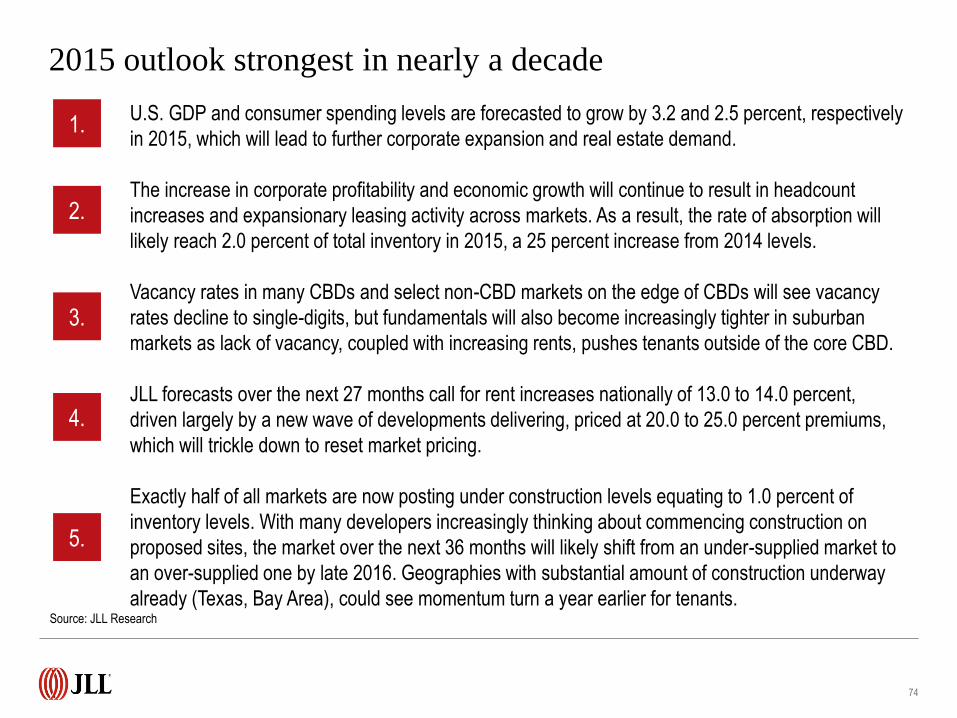

2015 outlook strongest in nearly a decade

U.S. GDP and consumer spending levels are forecasted to grow by 3.2 and 2.5 percent, respectively

in 2015, which will lead to further corporate expansion and real estate demand.

The increase in corporate profitability and economic growth will continue to result in headcount

increases and expansionary leasing activity across markets. As a result, the rate of absorption will

likely reach 2.0 percent of total inventory in 2015, a 25 percent increase from 2014 levels.

Vacancy rates in many CBDs and select non-CBD markets on the edge of CBDs will see vacancy

rates decline to single-digits, but fundamentals will also become increasingly tighter in suburban

markets as lack of vacancy, coupled with increasing rents, pushes tenants outside of the core CBD.

JLL forecasts over the next 27 months call for rent increases nationally of 13.0 to 14.0 percent,

driven largely by a new wave of developments delivering, priced at 20.0 to 25.0 percent premiums,

which will trickle down to reset market pricing.

Exactly half of all markets are now posting under construction levels equating to 1.0 percent of

inventory levels. With many developers increasingly thinking about commencing construction on

proposed sites, the market over the next 36 months will likely shift from an under-supplied market to

an over-supplied one by late 2016. Geographies with substantial amount of construction underway

already (Texas, Bay Area), could see momentum turn a year earlier for tenants.

1.

2.

3.

4.

5.

The slowdown in the energy industry, as a result of the decline in oil prices in recent weeks, will yield a slower demand environment in energy hotbeds such as Houston over the short to mid-term. Likewise, absorption in high-priced tech markets like San Francisco and Silicon Valley could also slow as rental rates reach peak levels amidst declining vacancy.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2015

John Sikaitis Managing Director – Office and Local Markets Research

+1 202 719 5839

Julia Georgules Associate Director – Office Research

+1 415 354 6908

Sean Coghlan Manager – Capital Markets Research

+1 215 988 5556

Phil Ryan Research Analyst – Office and Economy Research

+1 202 719 6295

>> Click to learn more, and see

market-by-market data