us wireless market_q2_2015_update_aug_2015_chetan_sharma_consulting

TRANSCRIPT

US Wireless Market Update Q2 2015

Chetan Sharma Consultingchetansharma.com

Research. Technology. Strategy. Intellectual Property. Thought Leadership Summits.

Page Title Goes HereChetan Sharma Consulting

© Chetan Sharma Consulting, 2015. All Rights Reserved

• Product & Tech Strategy– Consumer & Enterprise

• Roadmap• Product/Technology Strategy• Technical Due-Diligence• R&D• Business Plan Development• Revenue Models

• Market Research– Research and Forecasting– Competitive Analysis– Market Sizing

• Intellectual Property– Strategy, Audit, & Policy– Patents, Infringement analysis– Patent Mining and Valuation– Litigation

• Mobile Thought-leadership Summits– Mobile Future Forward– Mobile Breakfast Series

www.chetansharma.com

14 yr young Management Consulting firm exclusively focused on Mobile

Advisor to major operators, OEMs, brands, startups, VCs, and Fortune 500 firms around the world

Strategy for each of the top 6 global mobile data operators, top OEMs and Internet players

Have a unique 360o view of the ecosystem

Page Title Goes HereUS Mobile Market Update Q2 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Summary

The US mobile data market grew by 3% QoQ and 14% YoY. The overall services revenue declined again by 1%. The device revenue increased by 21% which helped the overall revenue to grow by 3%.

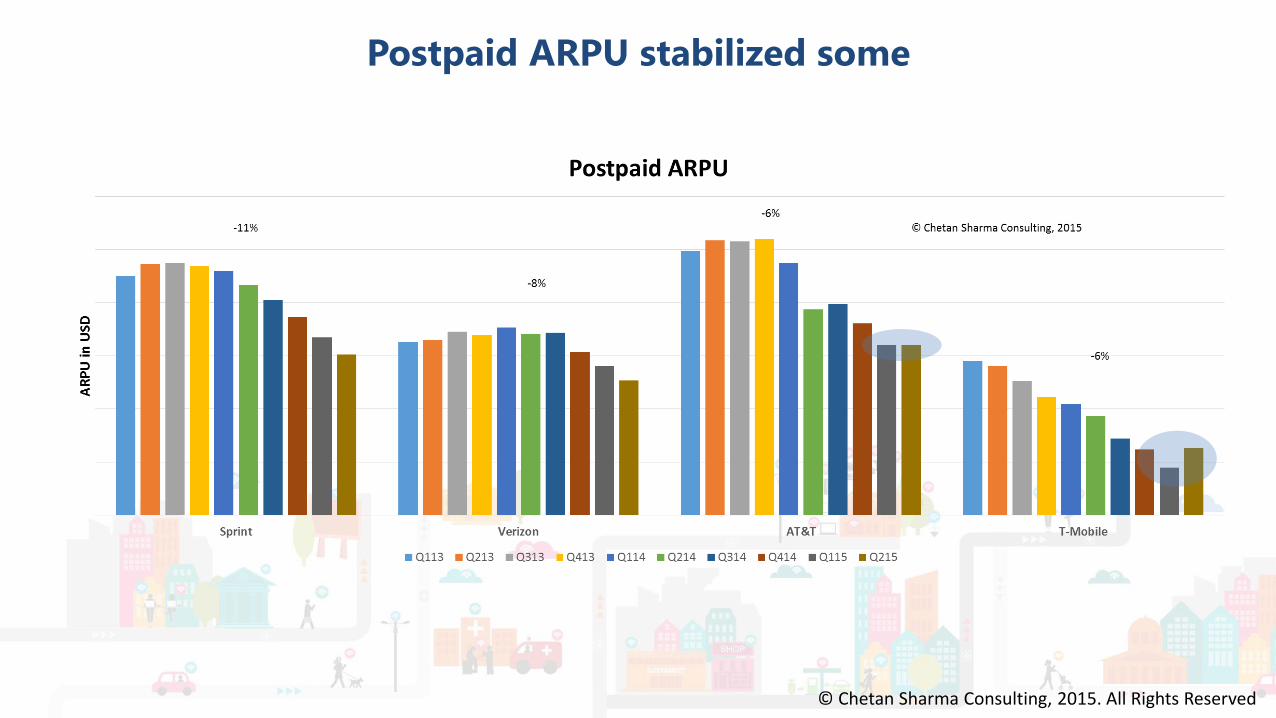

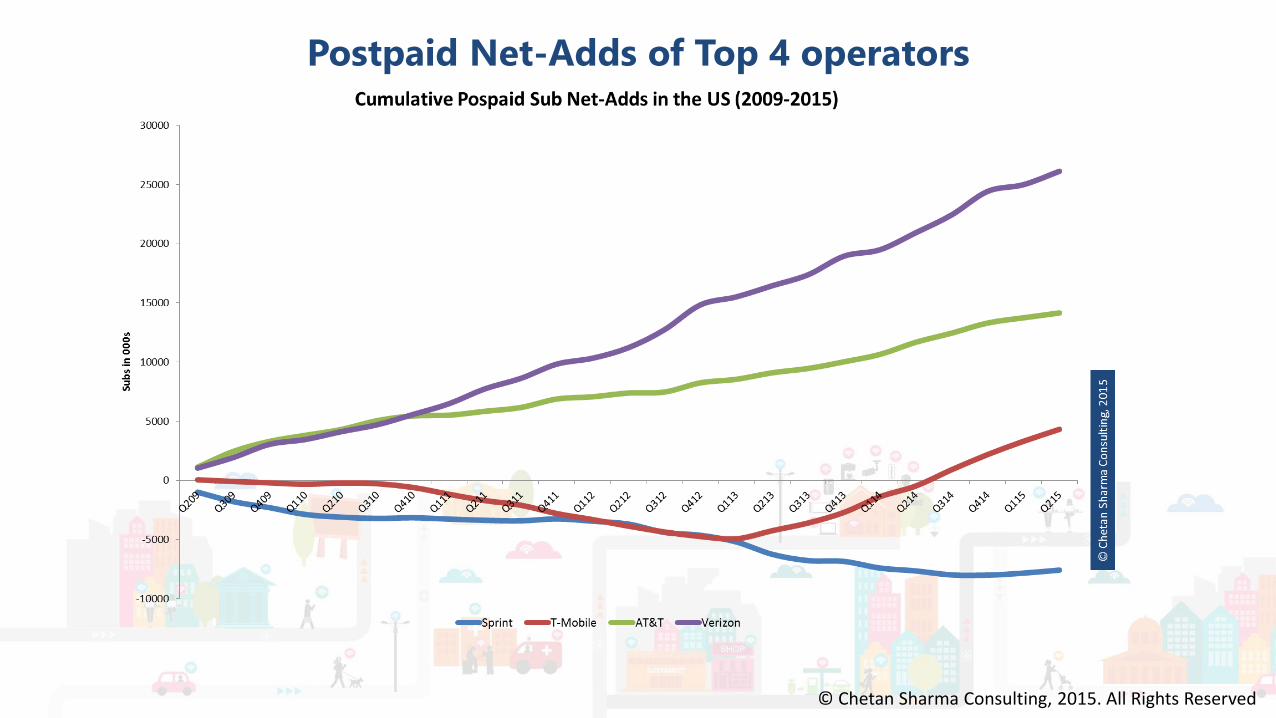

The biggest news of the quarter was as we had suggested last year - T-Mobile finally going past Sprint to become #3 for the first time. TMO continues to add the bulk of postpaid phone subs and it helped the company reverse the declining postpaid ARPU trend that had been so prevalent for the last three years. AT&T’s postpaid ARPU also stabilized

All four operators delivered historic low churn rates and are running much tighter operations. Net income improved 11% YoY.

After seeing steep declines in 2014, the mobile data pricing has started to inch up in 1H 2015. The emphasis of unlimited is paving way for shared data plans and the data buckets per account keep on inching up. In fact, many low-to-mid tiers have seen a price increase. Some of the upper enterprise tiers have seen the prices double. This bodes well for the margins and revenue in 2H 2015.

Smartphone penetration increased to 78% and roughly 95% of the devices sold now are smartphones. The smartphone penetration amongst postpaid users is now 84%.

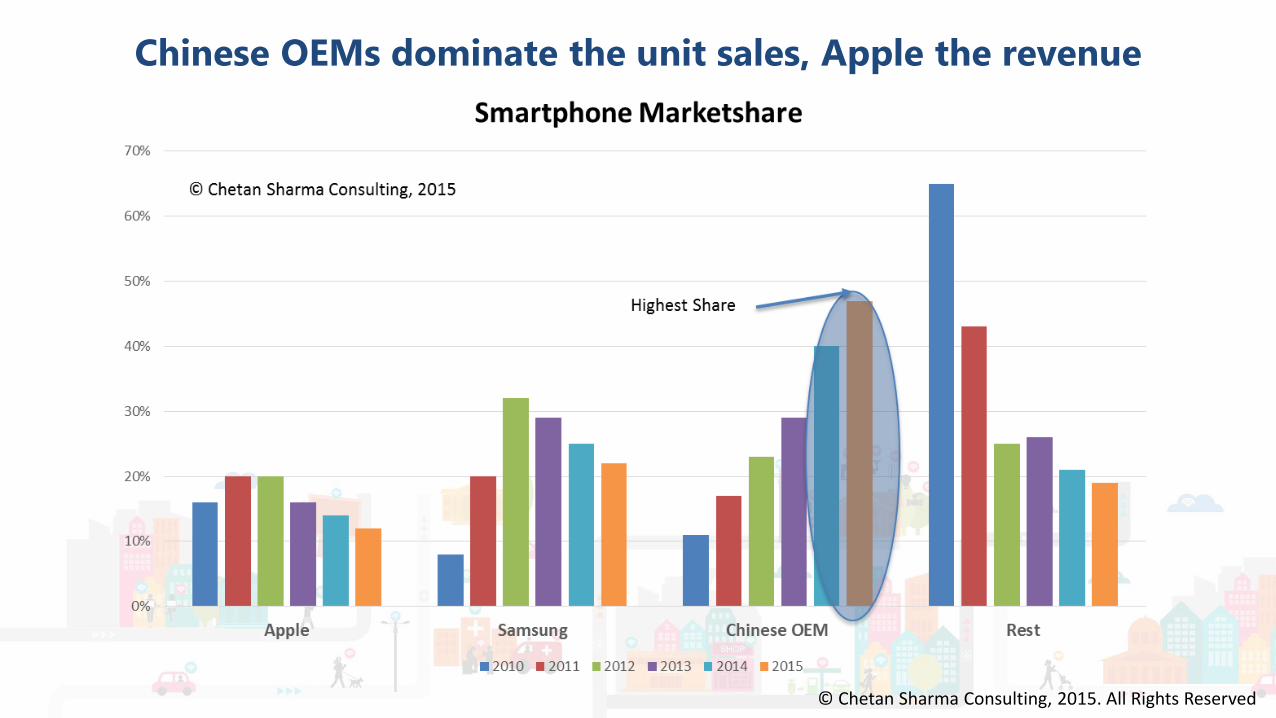

The iPhone again dominated with 75% of the smartphone profits. While the Android profits improved 41% QoQ, the smartphone business remains a challenge for a number of Android OEMs.

As we have suggested for the last couple of years, Microsoft finally got rid of Nokia and is focusing its energy on software and services.

4th wave services continue to grow at a very past face around the globe. IoT as a category is also making steady progress with a number of players reporting multi-million dollar revenue quarters most notably Intel with over a billion dollars in revenue in the first six months. Fitbit reported $736M in 1H with a whopping 49% margin.

T-Mobile Ascension to #3 – a historical perspective

One year ago, we suggested that T-Mobile is likely to become the #3 operator in early 2015. Given the current trends, the T-Mobile’s ascension to the #3 spot was rather anticlimactic.

In the service provider land, switching rank based on organic growth is rare. Most of the times, the rank switches because of M&A. This has been true for most part for US mobile operators over the last 30+ years. The top two positions in the last 20 years have been held by AT&T and Verizon who have taken turns to hold the #1 spot. The #3 and #4 rankings haven’t changed since 2004. In fact, when Sprint acquired Nextel, T-Mobile had less than half the customers of Sprint Nextel. However, aided by the Metro PCS acquisition, while Sprint added only 13M subs in 11 years, T-Mobile added more than 3x – 37M. Nextel proved to be a really bad operator acquisition – the company is still reeling from that decision.

At the time of the Nextel acquisition, T-Mobile’s share of the market was roughly 10%. By the end of 2015, T-Mobile’s share will increase to almost 17%. During the same 10 year period, Sprint’s share has declined from 23% to 16%. Verizon and AT&T controlled 51% of the market in 2005. Now that share stands at 68%. Rest of the market has virtually dissipated in light of the fierce competition.

Page Title Goes HereUS Mobile Market Update Q2 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

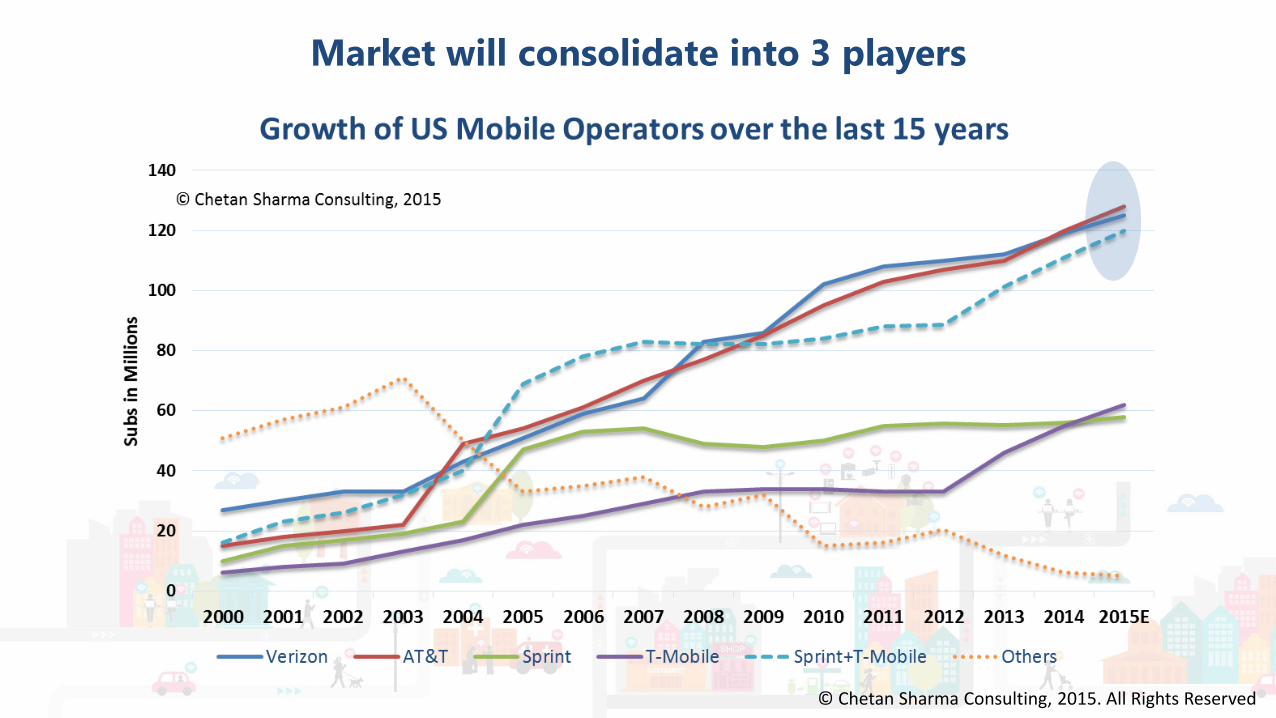

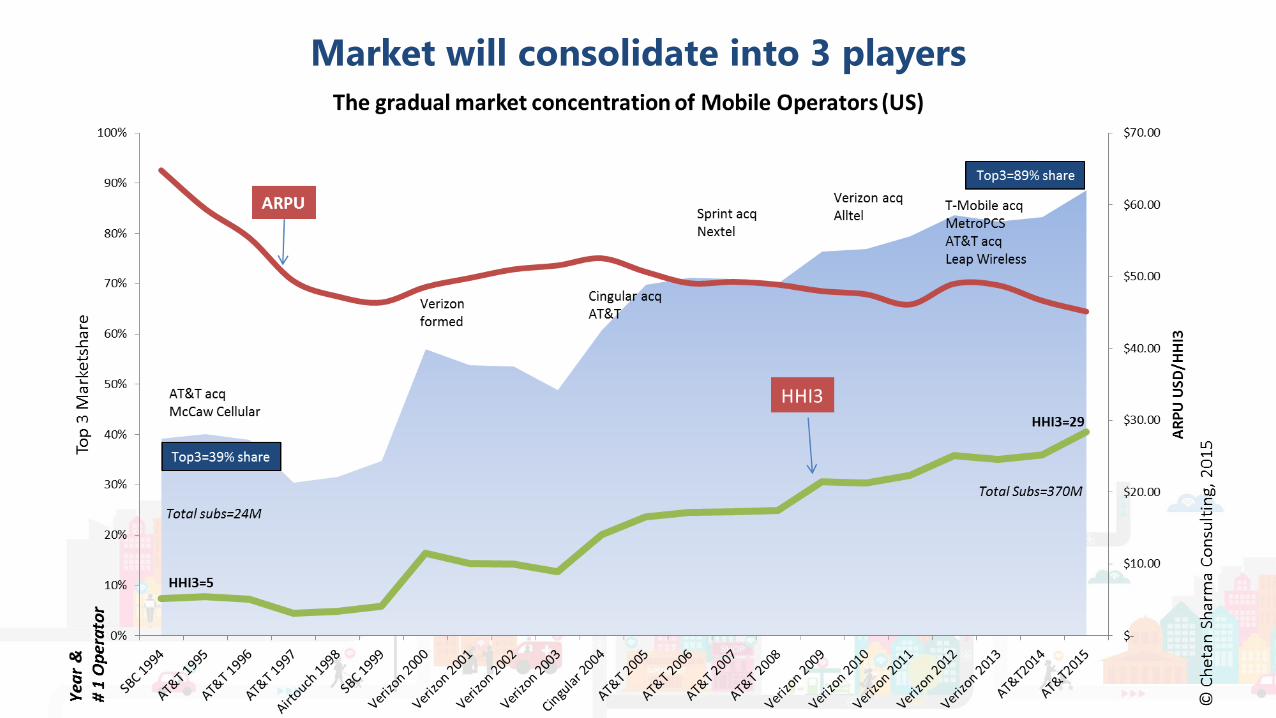

US mobile operator consolidation – what’s next?

Like any other market and like what you would expect in a maturing industry, the US mobile operator segment has consolidated in predictable ways. 20 years ago, AT&T fresh from its McCaw Cellular acquisition led the market with 3.95M subs at 14.5% share. Today, it still leads the market with 124M subs at 34% share. In the last 20 years, the market has whittled down to four national players. As we discussed back in our 2011 paper, in every market, the competitive and regulatory forces narrows down the field to 3 players. The top 3 players controlled 40% of the market in 1995. With T-Mobile ascending to #3, by the end of 2015, the top 3 will have almost 90% of the market. This is no different than other major mobile markets. Barring India (which will follow this trend soon as well), each market either by design or by market forces has consolidated to three major players.

The US regulators have resisted the trend and it has worked out better for the consumers as competition has led to better deals and non-stop new offers. However, as we suggested in our paper, market forces are often more powerful than the regulatory ideology. In the last two years, since the Softbank acquisition, T-Mobile’s marketcap has doubled while Sprint’s has been cut down into half. T-Mobile is only slighty ahead in the subscriber count but in terms of marketcap, it is 2.5x more valuable than Sprint. Instead of being the hunted, it has become the hunter. On the other hand, without a substantial infusion of external investment, it will be a challenging few quarters for Sprint.

Given that there are only a few legit big suitors left for T-Mobile or Sprint, the market is waiting for a major acquisition to happen in the next 12-18 months.

US Service Revenues: Turnaround?

In 2014, data pricing came down by 77% to historic lows. However, in the first half of 2015, price/GB hasn’t really come down any further than the lowest levels seen in 2014. In fact, some categories even saw a jump as some of the promotions went away. It is also notable that both T-Mobile and Sprint are de-emphasizing (though the plans are still available) unlimited data plans and instead they are promoting their shared bucket data plans. This is good for profitability.

Though Sprint saw its position slip, the churn number looked much better than past quarters. AT&T and Verizon have managed their respective companies to historic low churn numbers. T-Mobile has literally cut down its churn rate by 50% over the last three years.

The fierce competition has put pressure on the service revenues which declined (YoY) for the first time in the history of the industry in Q1 2015 by 2%. In Q2 2015, the service revenues still declined by 1% but there are some early signs of stabilization.

T-Mobile’s postpaid ARPU which has been in decline for three years increased QoQ (YoY it still declined). For AT&T, the postpaid ARPU stayed flat. For Verizon and Sprint, the postpaid ARPU declined but by less amount than it did in Q1.

The industry also delivered better EBITDA and Net Income numbers which shows the operators are running a tighter operation compared to last year.

One data point doesn’t make a trend and we need to study the numbers of the next two quarters, if the industry has stemmed the decline or it was just a blip.

Page Title Goes HereUS Mobile Market Update Q2 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Microsoft’s turbulent history with mobile

In 2001, of all the major computing brands, Microsoft probably had the clearest view of the things to come in mobile. It was working with several leading players in Japan where imode was taking the country (and the world) by storm. It did make incremental progress with Windows CE but never really embraced mobile as a strategic pillar of growth until Satya became the CEO. However, his first task was to undo the mistakes of the previous administration and he had no choice but to untangle Microsoft from the Nokia deal. It has just taken this amount of time to write-off one of the biggest corporate mistakes in the industry.

As we have been saying for the last couple of years, Microsoft should abandon the strategy to fight Apple on Apple’s turf and instead focus on services and the cloud where it has historically been more agile. However, ceding the platform has its repercussions and it is not clear how far the current strategy will take the company. Microsoft is focusing early on IoT so as to not miss the next big wave but it seems like the strategic architecture to attack the market remains old school.

Nokia – final nail in the coffin and quickest destruction of a loved consumer brand

Nokia’s decision to pursue Windows OS will go down in the industry history as the biggest blunder of all times. By putting all eggs in one broken immature basket, Nokia’s fate was sealed from day one. Barring any strategic brilliant maneuvers from Microsoft, the seeds of demise of a fabled brand were sown, the writing was on the wall. The company’s board had made poor decision to let things go out of control. In its heydays, Nokia’s marketcap was almost $250 billion - many times that of Apple. With the launch of the history-shattering device in 2007, Apple laid the foundations of irrational behavior amongst its competitors. Nokia’s board did an extremely poor job of navigating the company out of turbulent waters. There was no strategy, no plan, just a misguided Hail Mary pass. More than the burning platform, the decision to switch to windows set forth in motion an inextricable trajectory into an inferno. Will the phoenix rise from the ashes in 2016 remains to be seen.

The verdict on Apple Watch

Quarterly sales of 2.5M units with almost a billion dollars on debut would have been hailed by the press and critics alike. But given that it was Apple’s name behind the watch, expectations were lofty and it led many to prejudge the platform and its future. People often forget what the first version of iPhone or even iPad felt like. While there are a number of issues with the Apple watch, it is just too soon to have a final say on the platform. While the potential marketsize is every wrist on the planet, the overall size just by definition will be smaller than the smartphone base. As developers learn to understand how to use the dual screens of watch and phone, as they master the different language of vibrations, taps, heartbeats, and notifications, as they connect the signals of health to the dots of care, we will see if the platform can deliver on its promise.

Page Title Goes HereUS Mobile Market Update Q2 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Android vs. iOS: The fight for profit continues

HTC’s losses from Android operation were really bad. LG barely eked out a profit from its quarter. Apple accounted for 75% of the industry profits in Q2 2015 down from Q1 but up 13% YoY. Samsung better than last quarter but is nowhere near the peak it hit two years ago. Overall, the revenue for the Android ecosystem declined 5% QoQ while the profits increased 41%.

4th Wave/IoT Revenues

Qualcomm reported $1B in IoT revenues (chips used in city infrastructure projects, home appliances, cars, and wearables) in 2014. Intel is on track to exceed $2B in IoT revenue this year. Fitbit is likely to eclipse $1.5B in revenue with an astonishing 48-50% margin. AT&T’s IoT business is over a billion dollars. Verizon’s annual run rate is over $650M now. Google is approaching half a billion in IoT revenues. There are numerous other players who are doing sizable IoT revenues. We haven’t even gotten to the Industrial part yet where the savings and earnings are into billions (we will cover them in a future paper).

In other 4th wave segments, the number of players making $250M/quarter on mobile continues to increase rapidly and these aren’t your traditional wireless players. For example, Mobile is now contributing 76% (up from 30% in Q1 2013) to Facebook’s quarterly revenues. Latest addition to the club is Twitter which is now doing 88% in mobile (of the total advertising revenue) up from 60% in 2013.

Alphabetizing Corporations

In the late breaking news, Google restructured the businesses under Alphabet. I have been thinking about this from the 4th wave point of view. Various business are quasi-conglomerates of many multi-million and even multi-billion dollar businesses. In fact, we wrote about it in May – Unicorns at incumbents. Mobile operators should think their various businesses as building blocks that can be under a holding company. For example, at some point access can be a separate company just focused on operating the pipes while the content company is focused on creating the best content for various distribution channels. Connected car is easily a separate business, so is Industrial IoT which can be further broken by verticals etc. This might give a better yield and return to the shareholder rather than holding them under the core entity.

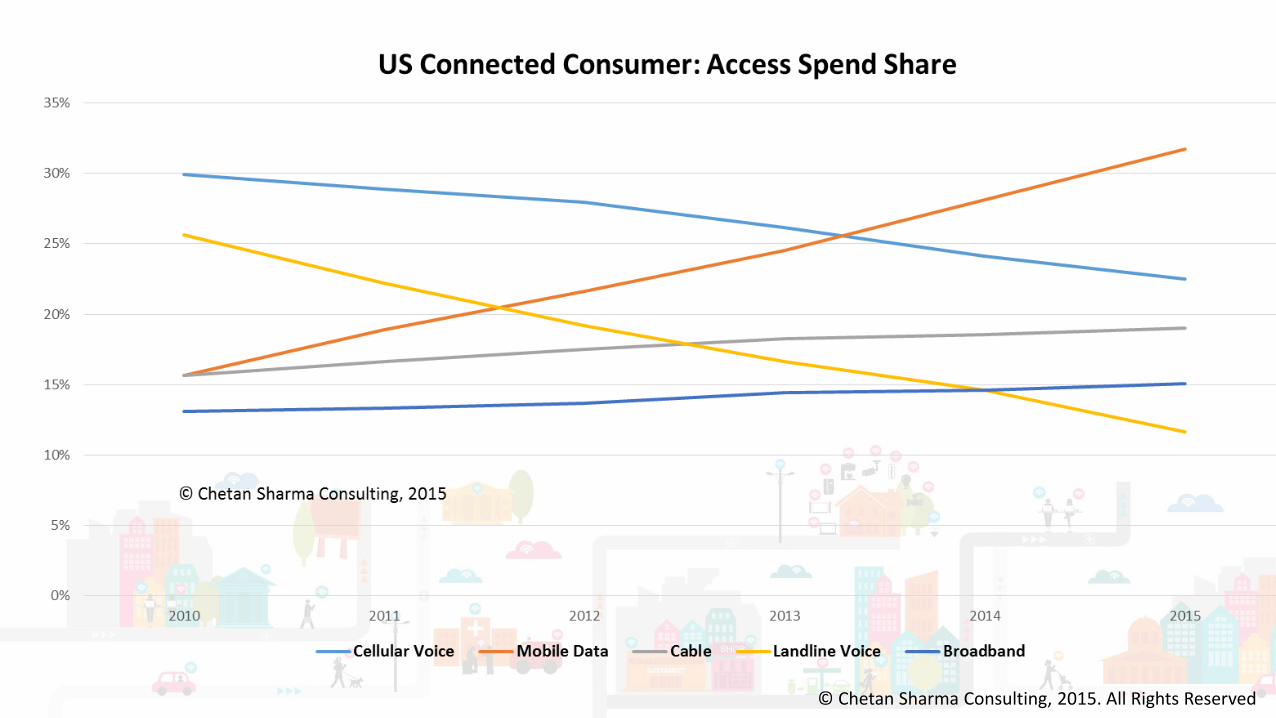

Connected Consumer

• On average, each US household will spend approximately $3800 on access and devices in 2015.

• Roughly 80% or $3000 of the US household spend will go to access of services such as cellular voice, mobile data, cable, landline voice, and broadband internet.

• Roughly 20% or $800 of the US household spend will go to devices such as computers, smartphones, feature phones, wearables, tablets, e-readers, connected cars, drones, robots, connected home, and other connected devices.

• 41% of the household access spend will go to cellular phones (for voice and data services).

• As a standalone category, mobile data is the biggest category approaching $1000 in yearly household spend.

• In the last 5 years, mobile data spend has risen the most and landline voice has declined the most. Cellular voice spend has also gone down while cable and broadband spend have seen relatively modest uptick.

Page Title Goes HereUS Mobile Market Update Q2 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

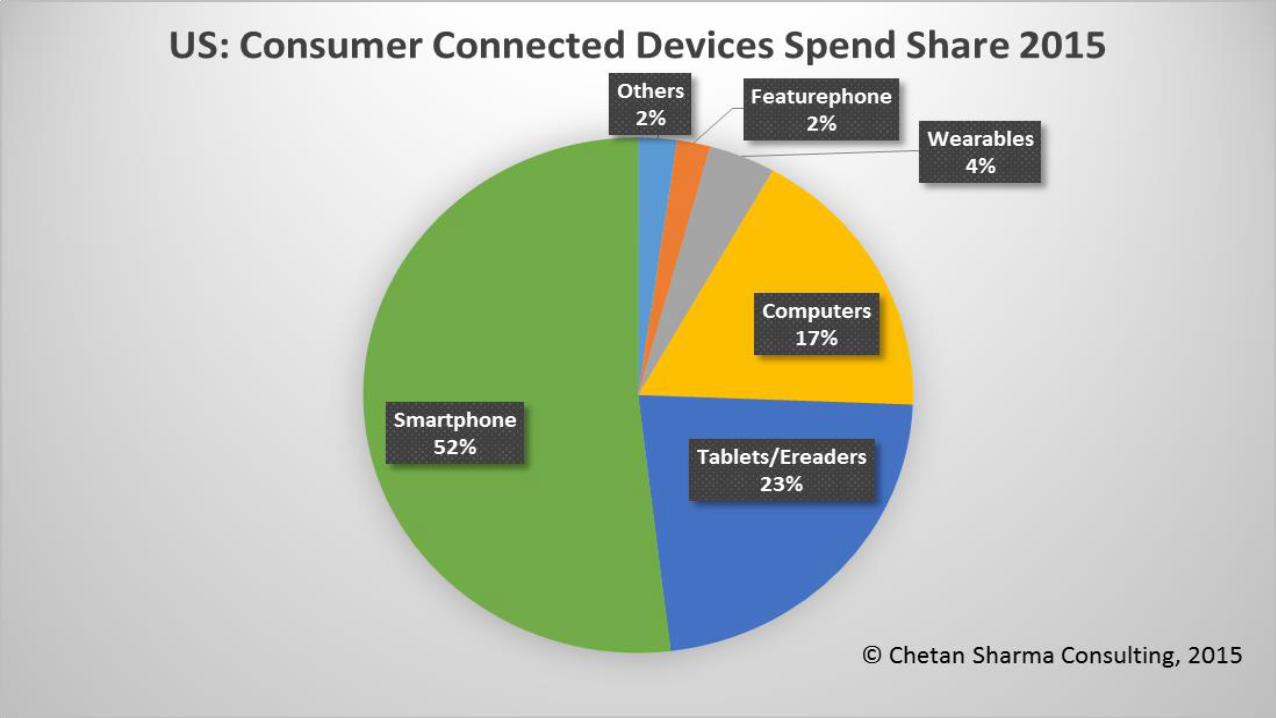

• In devices, smartphones is by far the biggest spend category. Consumers spend almost 3x on smartphones than they spend on personal computers. Smartphones will account for more than 50% of the US household connected spend in 2015.

• New categories such as wearables, connected cars, drones/robotics, and connected homes have started to make a tangible impact on consumer spend.

• US consumers will spend more on wearables than feature phones in 2015.

• Chetan Sharma Consulting conducted its annual Connected Consumer survey of 1000 US households. The results confirmed the ongoing increase in the number of connected devices/household.

• The number of connected devices per US household is now 5.3 with over 37% of the households in the 4-8 range.

• Almost 6% of the households have 15 or more connected devices.

• More details are available at: http://chetansharma.com/connectedconsumer15.htm

Quad Moves

AT&T closed its DirectTV acquisition. Verizon acquired AOL. Similar moves are afoot in Europe and other regions. Regular readers won’t be surprised. Video is a key offering for many service providers and by bundling quad plays, operators can further lower the churn. Content will continue to play a big role in how various offerings get bundled. The traditional cable bundle is being pulled apart in favor of more al carte OTT offerings. Media companies will have to figure out how they play in the new converged world. The ones that have been sitting on the sidelines will have to make some moves in the wireless ecosystem to stay relevant in the long-term.

The Upcoming 5G wars?

I started my career when 1G was all the rage. My first 4G project was back in 2002. By some measures, we are already behind on the 5G discussions. In general, it takes 7-10 years before the standards are finalized and then the network technology lasts for approximately 20 years before a market moves onto the next generation of technology. US led in the growth of 1G (AMPS, TACS) followed by Europe on 2G (GSM, CDMA). Japan took the leadership role with 3G (WCDMA, EVDO) and US wrestled it back on 4G (LTE). Japan and EU are determined to lead on 5G and have been making very public statements and R&D investments about their ambitions on 5G. Japan of course has a very clear goal of having 5G by Tokyo Olympics in 2020. Am sure some operator(s) somewhere will jump the gun and start calling LTE-A+ as 5G around 2017-18 or sooner. You can expect a lot of activities both in public and private on 5G as companies and governments try to figure out a way to claim the 5G leadership mantle.

Our paper on 5G covers the past, present, and future of the network evolution.

Page Title Goes HereUS Mobile Market Update Q2 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

What to expect in the coming months?

• 1H 2015 was a tremendous year for the mobile as it becomes omnipresence in every industry. We saw some massive moves, astounding acquisitions, and interesting strategic endeavors. 2H promises to be an exciting for the industry as well.

• As usual, we will be keeping a very close eye on the micro- and macro-trends and reporting on the market on a regular basis in various private and public settings.

• Against this backdrop, the analysis of the Q2 2015 US wireless market is:

Service Revenues

• The US mobile data services revenues in Q2 2015 increased 3% QoQ and 16% YoY.

• After crossing the $100B in data revenues last year, the US market is set for explosive growth and is likely to cross $130B in data revenues in 2015.

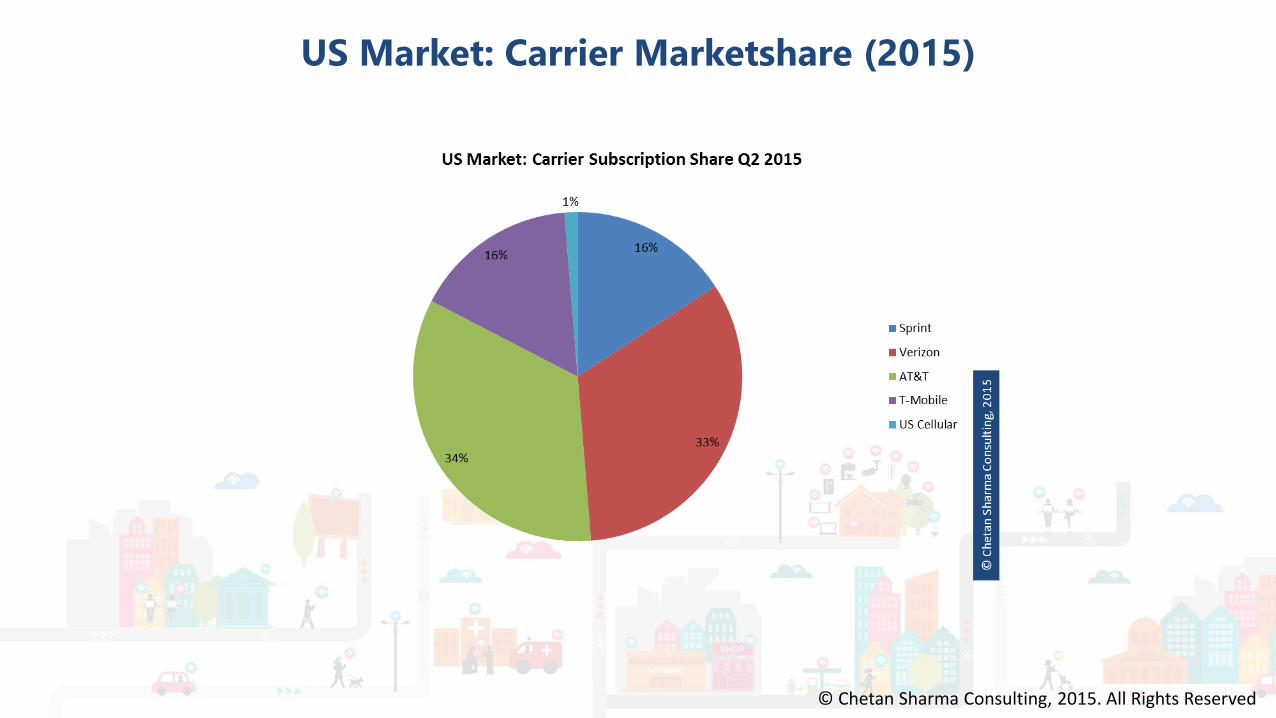

• Verizon and AT&T dominated the quarter accounting for 70% of the mobile data services revenue and had 67% of the subscription base.

• Verizon and AT&T are at #2 & #3 global mobile data revenue ranking respectively in Q2 2015. Sprint and T-Mobile also maintained their rankings in the top 10 global mobile data operators.

ARPU

• The Overall ARPU fell by 1%.

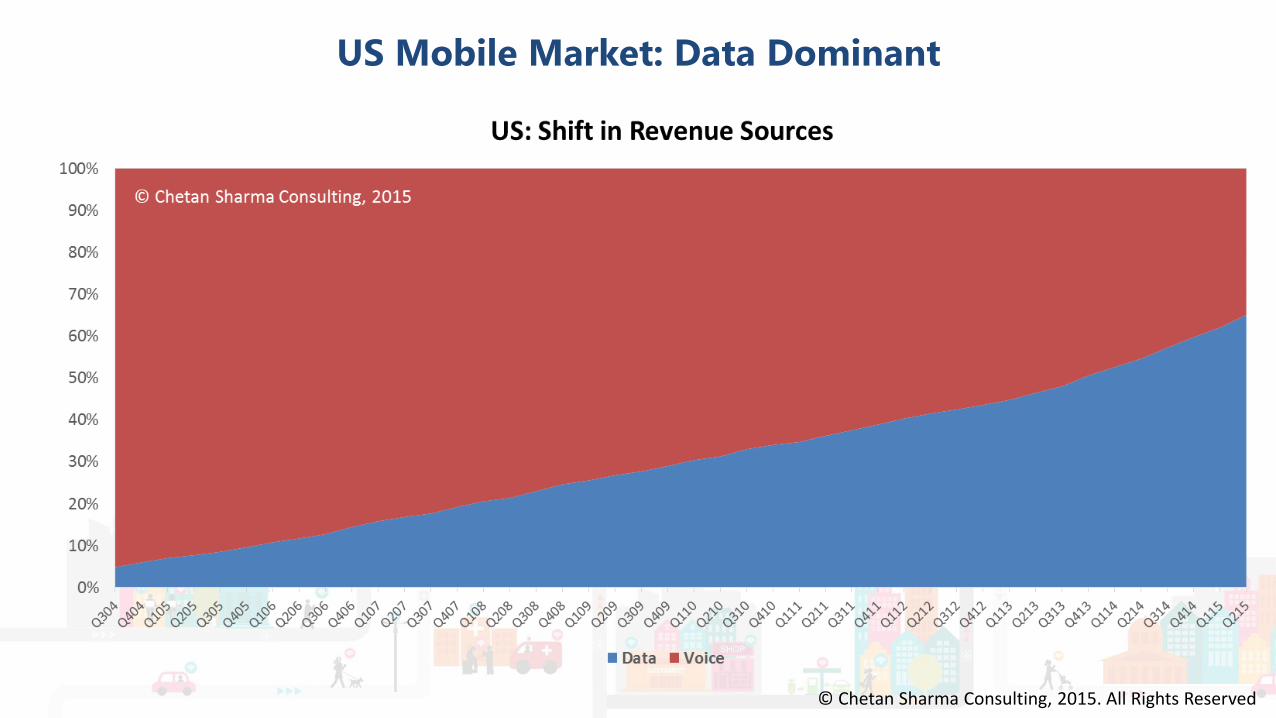

• Data contribution to the overall revenues is now at 65%.

• The postpaid ARPU increased for T-Mobile for the first time in 3 years. AT&T’s stemmed the decline of the last two quarters while others continued to see the pressure on postpaid ARPU.

Subscribers

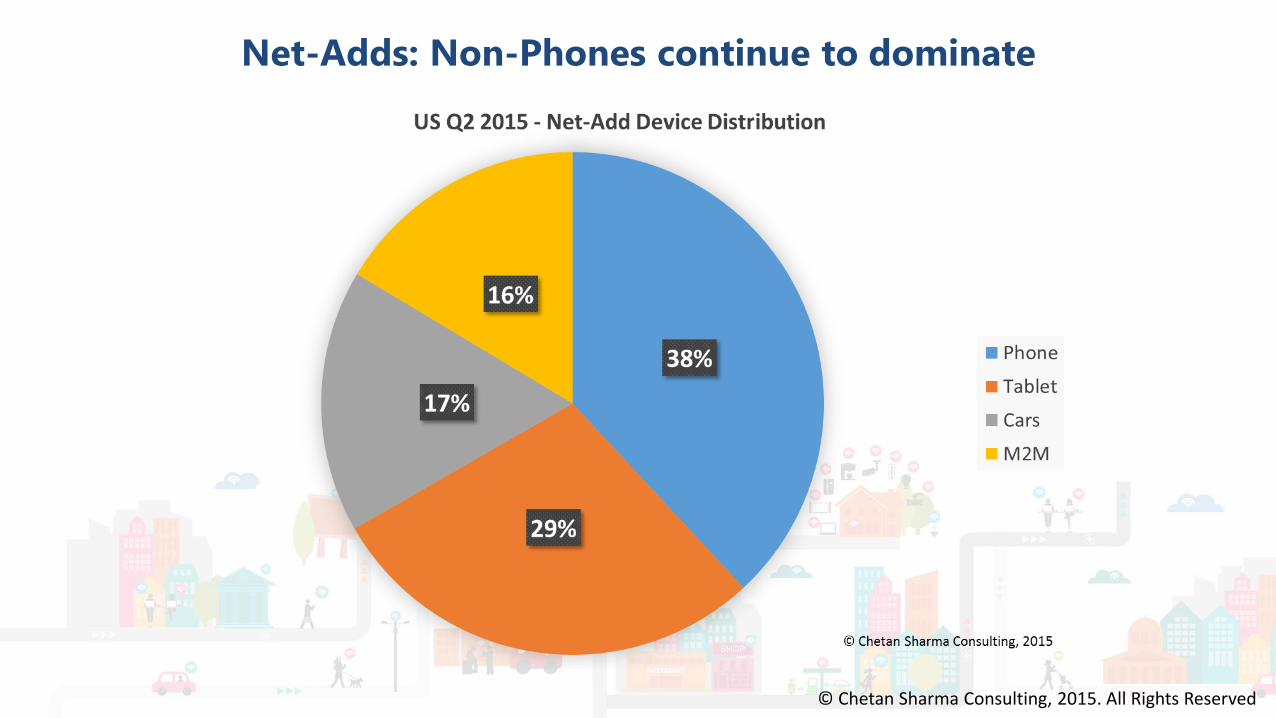

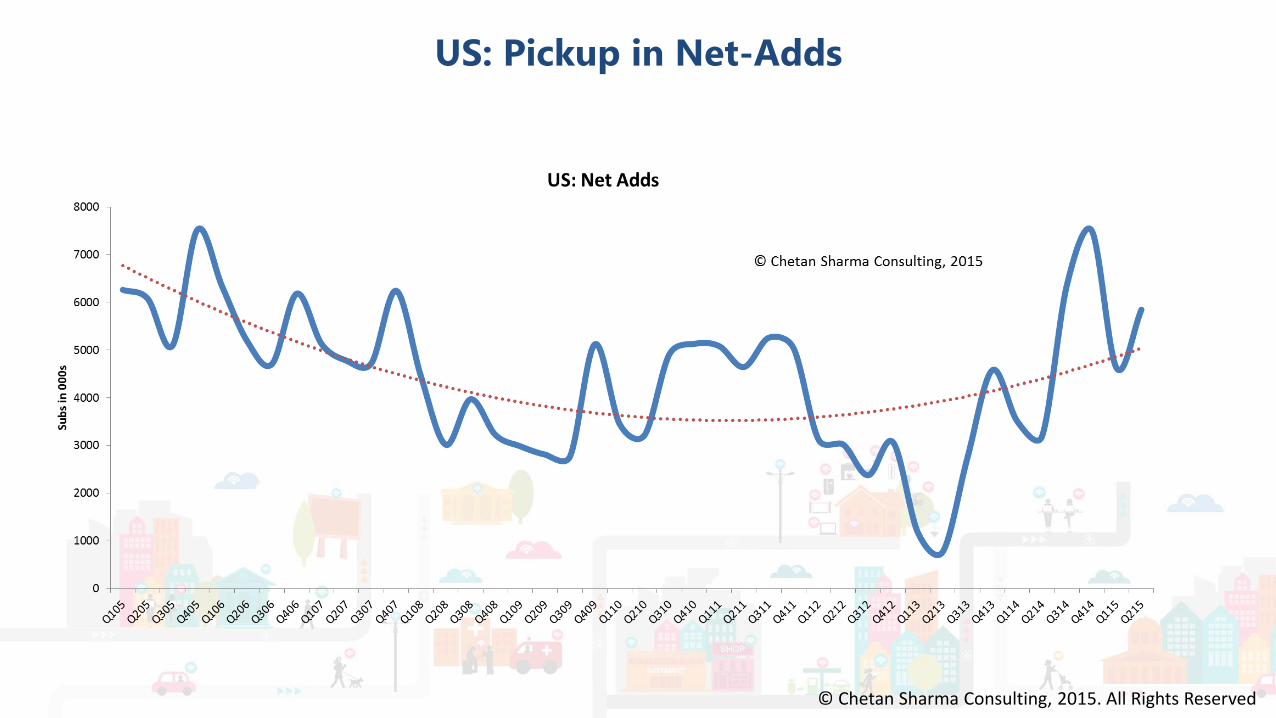

• The US market increased its net-adds to 5.8M. AT&T and T-Mobile led with 2M+ net-adds.

• Verizon led in postpaid net-adds though a bulk of the net-adds are coming from tablets.

• AT&T added 1M cars to its tally to reach 4.5M in connected cars on their network – probably the highest of any mobile operator in the world.

Shared Data Plans

• Shared data plans launched by Verizon and AT&T have been quite successful. The attachment rates have increased tremendously over the course of last two years with more consumers opting for cellular tablets and connected devices. 77% of postpaid accounts at AT&T are now on shared plans.

• Some more granular data plans for tablets have also spurred interest as the cellular broadband is becoming available on demand vs. expensive on premise Wi-Fi solutions.

• The number of accounts on 15 GB or more have quadrupled over the last year for AT&T.

Page Title Goes HereUS Mobile Market Update Q2 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

4th Wave Progress

• The number of players making $250M/quarter on mobile continues to increase rapidly and these aren’t your traditional wireless players. For example, Mobile is now contributing 76% (up from 30% in Q1 2013) to Facebook’s quarterly revenues. Latest addition to the club is Twitter which is now doing 88% in mobile (of the total advertising revenue) up from 60% in 2013. Even traditional players like Hertz, Sears, and Starbucks are generating meaningful revenues from mobile. There are now dozens of such players and the list is just growing. (for more discussion on the topic please see: “Mobile 4th Wave: Evolution of the Next Trillion Dollars”)

• The cloud and security segments have also gained significant traction with incumbents as well as startups launching new initiatives and technologies.

• Verizon reported $165 million revenue from M2M and Telematics. At the current run-rate, this will be a billion dollar business by 2016. The current annualized run rate is $650M.

• AT&T reported 1M net-adds on the connected car platform.

Connected Devices

• Connected devices (non-phones) accounted for almost 62% of the net-adds in Q2 2015. This means that while there is a healthy smartphone sales pipeline, it is for the existing subs and as such net-adds for the phone business is tapering off and we can expect that new net-adds will continue to be dominated by the connected devices segment.

• For AT&T, Connected cars started to form a significant base of the connected devices segment with 47% of the new connections coming from cars.

Handsets

• Smartphones continued to be sold at a brisk pace accounting almost 95% of the devices sold in Q2 2015. The feature phone category is practically becoming extinct in the US market.

• The smartphone penetration in the US is now at 78%.

• Verizon continues to sell more LTE smartphones as its LTE sub tally rose to 76M making it the #2 LTE operator behind China Mobile which has more than twice LTE subs. Other three operators are also deep into their LTE deployments. Verizon reported that 87% of its total data traffic is on the LTE network now, clearly the fastest technology transitions we have seen in the US wireless industry.

Page Title Goes HereUS Mobile Market Update Q2 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Your feedback is always welcome.

Chetan Sharma

We will be keeping a close eye on the trends in the wireless data sector in our blog, twitter feeds, future research reports, articles, and our annual thought-leadership summit –Mobile Future Forward. The next US Wireless Data Market update will be released in Nov 2015.

Disclaimer: Some of the companies mentioned in this update are our clients.

We will be discussing a number of critical industry themes and future impacting topics at our annual summit Mobile Future Forward with some incredible thought-leaders from around the globe. Speakers, Sponsors, and the executives at Mobile Future Forward invite you to participate in the discussion on Sept 29th in Seattle. Join Glenn Lurie, President & CEO, AT&T Mobility, Dr. Eric Topol, Chief Academic Officer, Scripps Health, Rima Qureshi, Chief Strategy Officer, Ericsson, Hank Skorny, SVP – IoT, Neustar, Raja Rajamannar, CMO, Mastercard, Sanjiv Ahuja, Chairman, Tillman Global Holdings, Hossein Moiin, EVP and CTO, Nokia Networks, Craig Moffett, Partner, MoffettNathanson, Josh Will, SVP –Mobile, Best Buy, Tim Chang, Managing Partner, Mayfield, Prof. Shyam Gollakota, University of Washington, Mark Fernandes, Managing Director, Sierra Ventures, Erez Yarkoni, CIO and EVP, Telstra, Mark Showers, CIO and EVP, Reinsurance Group of America, Doug Suriano, SVP and GM, Oracle Communications, Vishal Gupta, Chief Products and IoT Officer, Silent Circle, Marty Cooper, Chairman, Dyna, Vijay Shekhar, Founder and CEO, Paytm, Julie Woods-Moss, CMO, CEO – Nextgen Business, Tata Communications, Andrew Hopkins, Managing Director – IoT, Accenture, Lo Toney, Partner – Catalyst Fund, Comcast Ventures, Robert Gelick, SVP and GM – Digital, CBSInteractive, Sujeet Chand, CTO and SVP, Rockwell Automation, Bob Azzi, Executive Managing Partner, Argylegriffin, Anand Chandrasekaran, Chief Product Officer, Snapdeal, Dr. Tony Yen, MD, CMIO, EvergreenHealth, and many more

Page Title Goes HereUS Mobile Data Services Revenue

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereSummary of the US Mobile Market Revenue Streams

© Chetan Sharma Consulting, 2015. All Rights Reserved

4th wave revenuessurpassed access revenues

YoY Growth

21%

Page Title Goes HereMarket will consolidate into 3 players

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereMarket will consolidate into 3 players

Page Title Goes HereRevenue will be made from existing customers, new customer

revenue approaching ZERO

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereUS Mobile Market: Data Dominant

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereUS Market: Carrier Marketshare (2015)

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereNet-Adds: Non-Phones continue to dominate

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HerePostpaid ARPU stabilized some

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HerePostpaid Net-Adds of Top 4 operators

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes Here US: Pickup in Net-Adds

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereChinese OEMs dominate the unit sales, Apple the revenue

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes Here

Page Title Goes Here

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes Here

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes Here5G: The history of the future

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereMobile Future Forward – Sept 29th 2015get inspired to fuel your mind and strategy

© Chetan Sharma Consulting, 2015. All Rights Reserved

Mobile Future Forward is the most intellectual conference – CEO and founder, Connected Watch Company

It is a terrific event. Mobile Future Forward is causing everyone to think about what’s the next big thing – CEO, Global Mobile Operator

America’s greatest gathering of the wireless minds – CEO, Future Forecasting Service

Page Title Goes HereMobile Future Forward – Sept 29th 2015get inspired to fuel your mind and strategy

© Chetan Sharma Consulting, 2015. All Rights Reserved

Ever wondered what the future of mobile looks like?Join us for an extraordinary day of executive mobile brainstorming

Contact [email protected] for sponsorship and speaking opportunitieswww.mobilefutureforward.com

Page Title Goes HereWe look forward to hearing from you

© Chetan Sharma Consulting, 2015. All Rights Reserved

Chetan Sharma

TW: @chetansharma

http://www.chetansharma.com

Mobile Future Forward

TW: @mfutureforward

http://www.mobilefutureforward.com

Research. Technology. Strategy. Intellectual Property. Thought Leadership Summits.