utility m&a presentation slides - erg consulting

TRANSCRIPT

Utility M&A:A Case Study in the Sale of a Utility’s Service Area

NARUC Accounting and Finance Meeting, March 8, 2016

Victor Prep, P.E.

Byron S. Watson, CFA

Energy & Resource Consulting Group, LLC

Denver, Colorado

www.ergconsulting.com

© 2016, Energy & Resource Consulting Group, LLC

Introduction

o Victor Prep, P.E. – Executive Consultant

BSME from OU, MBA from Univ. of PA, Wharton

Registered P.E. in CO, LA, and PA, and Certified Energy Manager

Retired Nuclear Submarine Naval Officer

o Byron S. Watson, CFA, CRRA – Senior Consultant

BSEE from SMU, MBA from Emory University

o Members of the Firm act as Advisors to the Council of the Cityof New Orleans (“Council”). Our Services as Advisors are inCertain Ways Comparable to Those of a Commission’s Staff

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

1

Introduction: Background

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

2

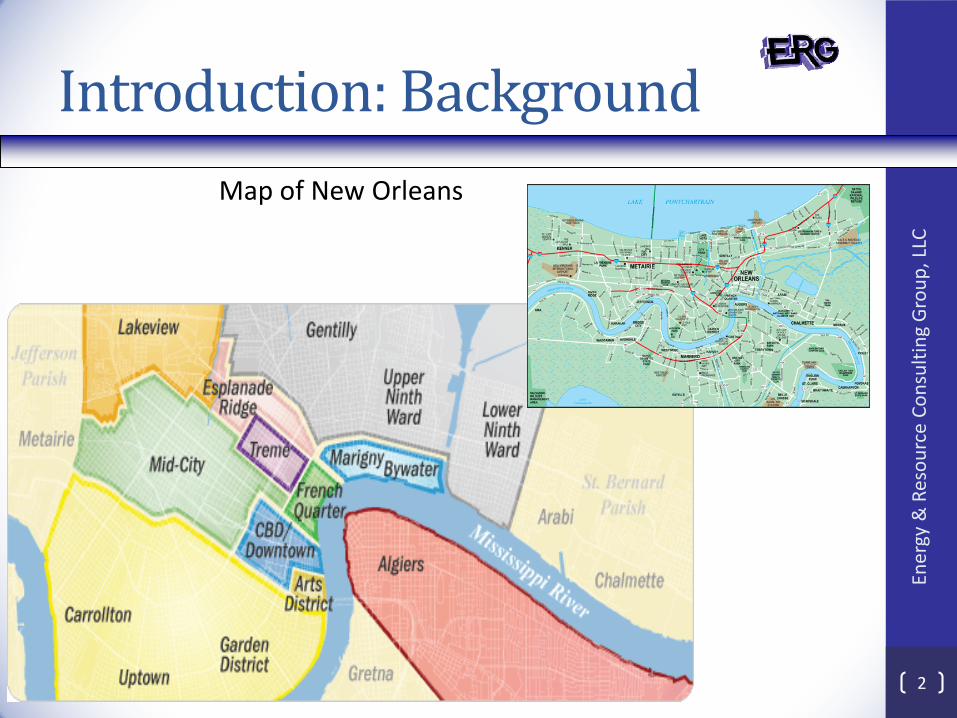

Map of New Orleans

Introduction: Background

o Prior to September 1, 2015, Retail Electric Service in the City of NewOrleans was Provided by two Separate Entergy Operating Companies

In the 15th Ward of New Orleans (a.k.a. “Algiers” or the “West Bank”),Entergy Louisiana, LLC (“ELL” or “Seller”) Provided Retail ElectricService to 22,187 Customers

In New Orleans, Except for Algiers, Entergy New Orleans, Inc. (“ENO”or “Seller”) Provided Retail Electric Service to 169,856 Customers

o The Council was the Retail Regulator of both Utilities

Each Utility had Separate and Different Rates, a Different AllowedROE, and Separate Rate Actions Before the Council

Each Utility Owned or Contracted for its own Generating Capacity,Largely From Different Generating Units

Each Utility had Separate Transmission and Distribution Plant

O&M-Related Services Were Provided to Both Utilities by a SingleEnergy Subsidiary (Entergy Services, Inc.)

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

3

Introduction: Background

o As a Result of Negotiations, Seller (ELL) Agreed to Transfer itsElectric Service Operations to Buyer (ENO) and Also SellRelated Utility Plant and Rights to Generating Capacity

Buyer Would Become the Single Retail Electric Utility Provider forAll of New Orleans

The Council Would be the Retail Regulator of One Electric Utility,the Buyer, and Would No Longer Regulate the Seller

Buyer Would own, Operate, and Maintain all Electric Utility PlantPreviously Owned by Seller in Algiers

Franchise Rights to Operate in New Orleans Would be Transferredform Seller to Buyer

Buyer Would Enter into a Purchased Power Agreement (PPA) withSeller to Continue Access to an Agreed-Upon Portion of Seller’sGenerating Resources

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

4

Introduction: Background

o On October 30, 2014, Buyer and Seller Jointly Filed for Approval to:

Sell Seller’s Assets Located in Algiers to Buyer at Net Book Value

Transfer all Franchise Rights to Provide Retail Service to Buyer so thatSeller Would Have no Remaining Operations in New Orleans

Create a New PPA Providing Buyer a “Slice” of Seller’s GeneratingFleet Capacity and Energy (1.84% of Each of Seller’s Units for the Lifeof Each Unit)

Leave Retail Base Rates Unchanged (i.e., Two Separate RateStructures) Until a Later Combined Rate Case Could Set a New SingleSet of Retail Rates for All of New Orleans

Receive other Related Relief, Such as Modifications to Franchises

o The Filing’s Requested Relief was Collectively Called the “AlgiersTransaction” (“Transaction”)

o Separately, ELL (Seller) and Another Entergy Operating Company,Entergy Operating Company, Entergy Gulf States Louisiana, L.L.C.(“EGSL”) were Merging

Closing the Merger After the Transaction was Critical

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

5

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

6

I. PUBLIC GOOD – THE CASE FORREGULATORY CONSOLIDATION

Net Ratepayer Savings

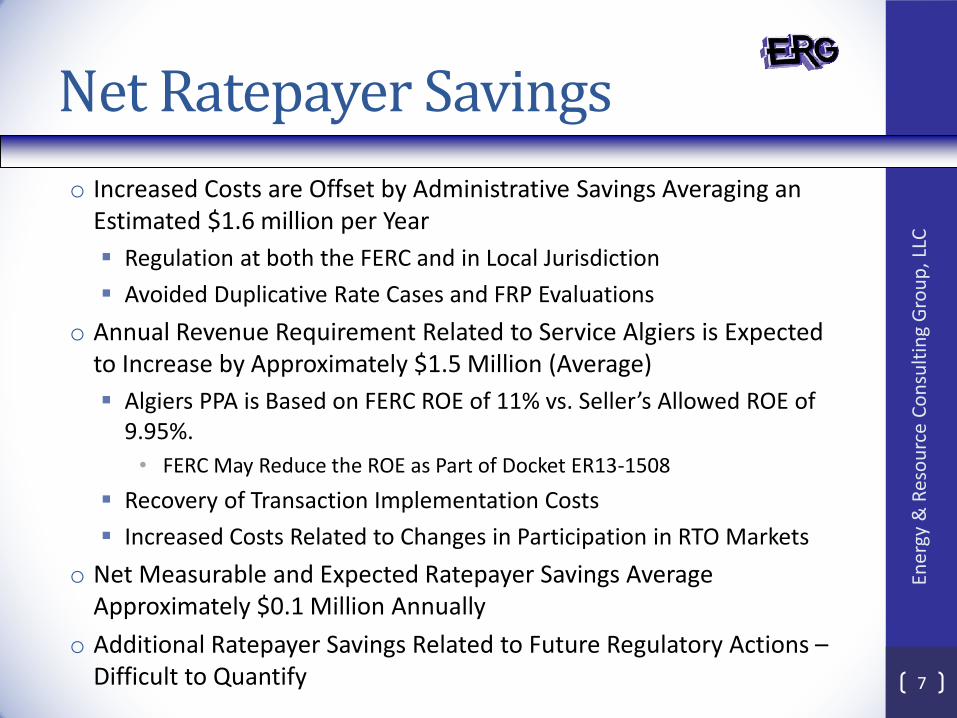

o Increased Costs are Offset by Administrative Savings Averaging an Estimated $1.6 million per Year

Regulation at both the FERC and in Local Jurisdiction

Avoided Duplicative Rate Cases and FRP Evaluations

o Annual Revenue Requirement Related to Service Algiers is Expected to Increase by Approximately $1.5 Million (Average)

Algiers PPA is Based on FERC ROE of 11% vs. Seller’s Allowed ROE of 9.95%.

• FERC May Reduce the ROE as Part of Docket ER13-1508

Recovery of Transaction Implementation Costs

Increased Costs Related to Changes in Participation in RTO Markets

o Net Measurable and Expected Ratepayer Savings Average Approximately $0.1 Million Annually

o Additional Ratepayer Savings Related to Future Regulatory Actions –Difficult to Quantify

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

7

Advantages –Other

o Reduce Customer Confusion Relating to Differing Rates and Rate Schedules in the Same City

o Eliminate Uneconomic Signals Presented by Differing Commercial and Industrial Rates in Same Geographic Area

o Eliminate any Perceived Inequity due to Different Allowed ROEs

o Reduce Administrative Burden on Local Regulators

o Fewer Interventions at FERC Proceedings

o Allow Relatively Small Algiers to Participate in Economies Available to Larger Buyer

Direct Ownership of Generating Units

Securitization of Storm Costs

Access to A Large (i.e., $75 Million ) Storm Reserve

Our Review Suggested no new Procurement Economies

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

8

II. TRANSACTION SUMMARY

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

9

Transaction: Steps

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

10

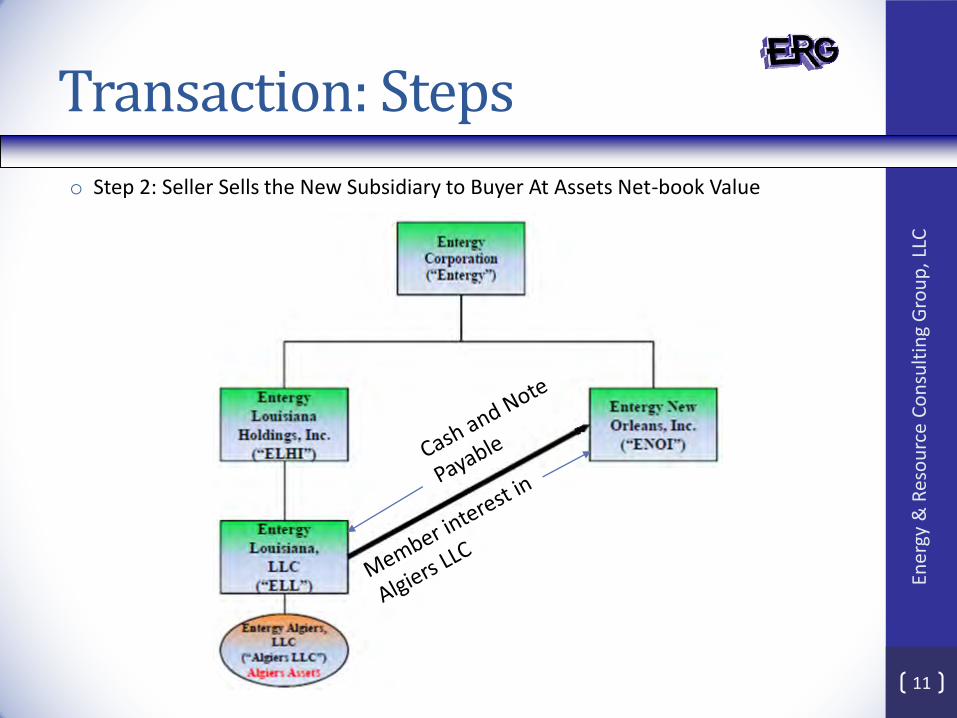

o Transaction in Three Steps, Each Occurring in Immediate Sequenceo Step 1: Create New Subsidiary to Receive Plant Located in Algiers

o A Key Transaction Objective was to Maintain Book Value Basis for Assets Sold to Buyer

Transaction: Steps

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

11

o Step 2: Seller Sells the New Subsidiary to Buyer At Assets Net-book Value

Transaction: Steps

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

12o Transaction Maintains Book Value for Assets

o Step 3: Merge New Subsidiary into Buyer

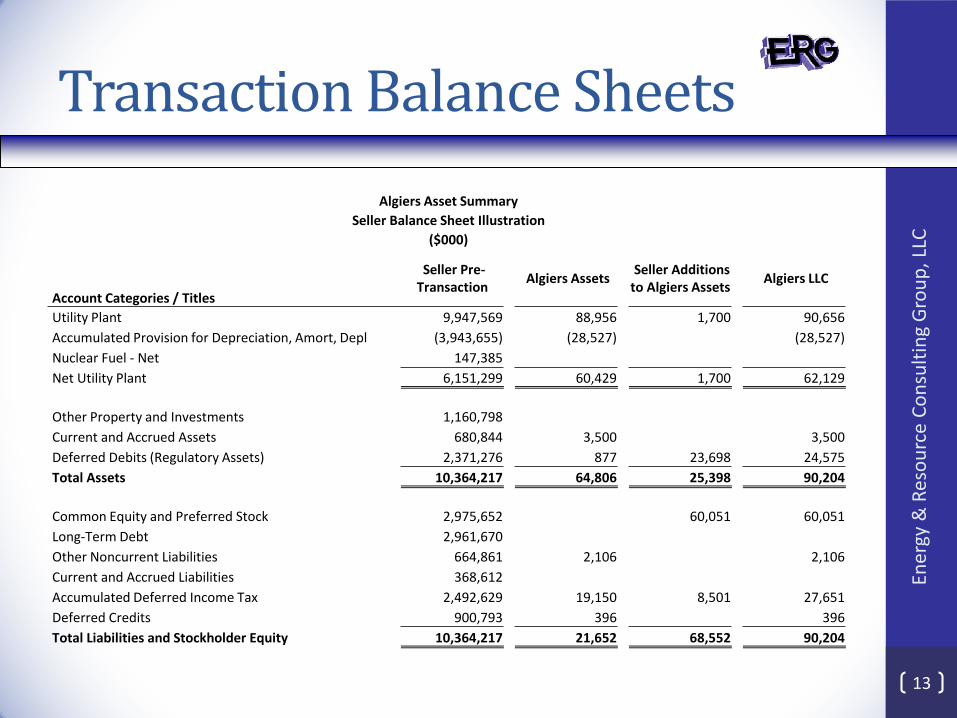

Transaction Balance Sheets

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

13

Algiers Asset Summary

Seller Balance Sheet Illustration

($000)

Account Categories / Titles

Seller Pre-Transaction

Algiers Assets Seller Additions

to Algiers Assets Algiers LLC

Utility Plant 9,947,569 88,956 1,700 90,656

Accumulated Provision for Depreciation, Amort, Depl (3,943,655) (28,527) (28,527)

Nuclear Fuel - Net 147,385

Net Utility Plant 6,151,299 60,429 1,700 62,129

Other Property and Investments 1,160,798

Current and Accrued Assets 680,844 3,500 3,500

Deferred Debits (Regulatory Assets) 2,371,276 877 23,698 24,575

Total Assets 10,364,217 64,806 25,398 90,204

Common Equity and Preferred Stock 2,975,652 60,051 60,051

Long-Term Debt 2,961,670

Other Noncurrent Liabilities 664,861 2,106 2,106

Current and Accrued Liabilities 368,612

Accumulated Deferred Income Tax 2,492,629 19,150 8,501 27,651

Deferred Credits 900,793 396 396

Total Liabilities and Stockholder Equity 10,364,217 21,652 68,552 90,204

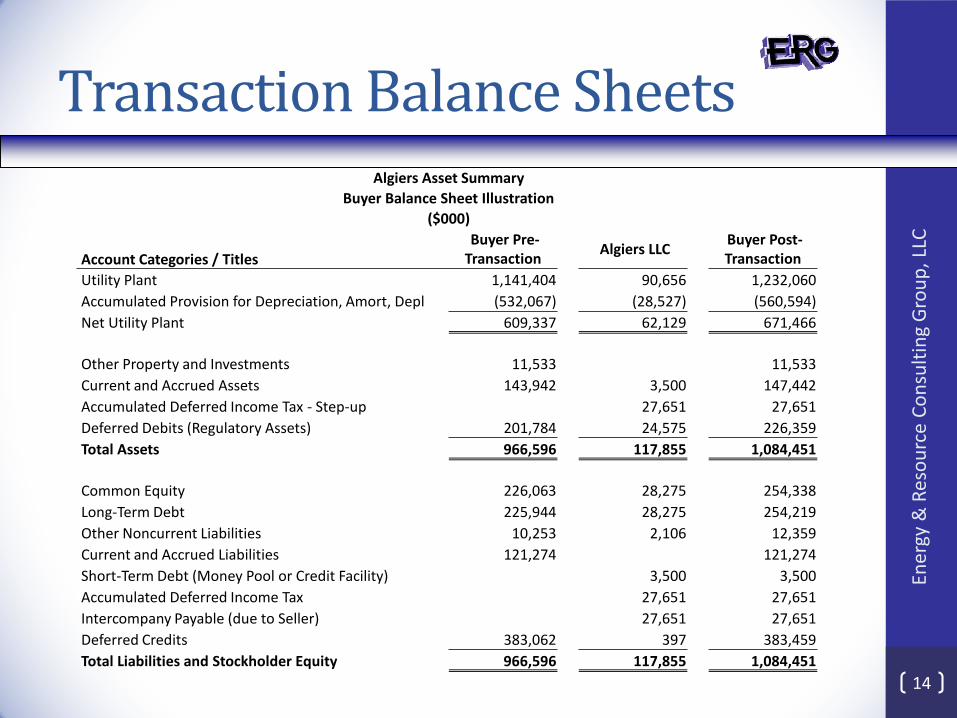

Transaction Balance Sheets

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

14

Algiers Asset Summary

Buyer Balance Sheet Illustration

($000)

Account Categories / Titles Buyer Pre-

Transaction Algiers LLC

Buyer Post-Transaction

Utility Plant 1,141,404 90,656 1,232,060

Accumulated Provision for Depreciation, Amort, Depl (532,067) (28,527) (560,594)

Net Utility Plant 609,337 62,129 671,466

Other Property and Investments 11,533 11,533

Current and Accrued Assets 143,942 3,500 147,442

Accumulated Deferred Income Tax - Step-up 27,651 27,651

Deferred Debits (Regulatory Assets) 201,784 24,575 226,359

Total Assets 966,596 117,855 1,084,451

Common Equity 226,063 28,275 254,338

Long-Term Debt 225,944 28,275 254,219

Other Noncurrent Liabilities 10,253 2,106 12,359

Current and Accrued Liabilities 121,274 121,274

Short-Term Debt (Money Pool or Credit Facility) 3,500 3,500

Accumulated Deferred Income Tax 27,651 27,651

Intercompany Payable (due to Seller) 27,651 27,651

Deferred Credits 383,062 397 383,459

Total Liabilities and Stockholder Equity 966,596 117,855 1,084,451

Tax Considerations

o Transaction had to Close Prior to The ELL/EGSL Merger to Avoid Loss of ADIT and Related Tax Recapture (i.e., Maintain Tax Deferral Represented In ADIT Balance)

o ADIT as Of Transaction Close Date Associated With Algiers Assets is Retained by Seller

Seller Must Eventually Pay Taxes Equal to ADIT

Buyer Must Eventually Pay Taxes Equal to any new ADIT That Accumulates After Transaction Close

o Buyer Records Offsetting ADIT Debits And Credits Associated With Step-Up ADIT – Substantially Equal to The Algiers Assets’ ADIT as of The Transaction Close (i.e., Zero Effect on Owner Equity)

o Zero-Interest Note Payable From Buyer to Seller Equal to Step-Up ADIT.

Intercompany Payable Recreates Effect of ADIT Liability on Buyer’s Books and Compensates Seller for Increased Tax Liability

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

15

III. KEY ASPECTS OF TRANSACTION

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

16

Purchase Price

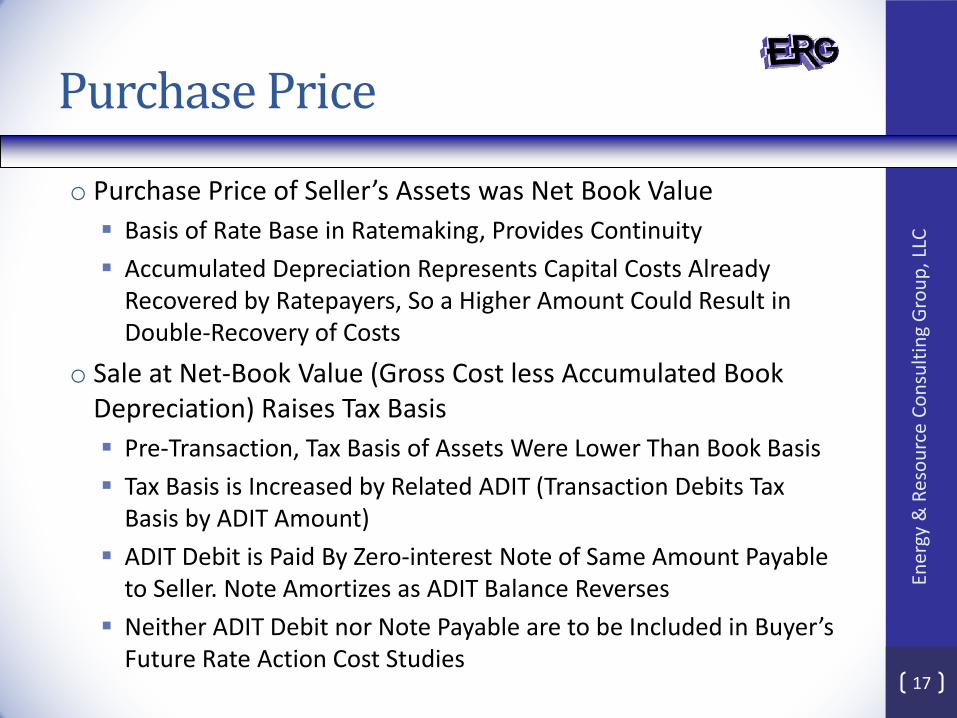

o Purchase Price of Seller’s Assets was Net Book Value

Basis of Rate Base in Ratemaking, Provides Continuity

Accumulated Depreciation Represents Capital Costs Already Recovered by Ratepayers, So a Higher Amount Could Result in Double-Recovery of Costs

o Sale at Net-Book Value (Gross Cost less Accumulated Book Depreciation) Raises Tax Basis

Pre-Transaction, Tax Basis of Assets Were Lower Than Book Basis

Tax Basis is Increased by Related ADIT (Transaction Debits Tax Basis by ADIT Amount)

ADIT Debit is Paid By Zero-interest Note of Same Amount Payable to Seller. Note Amortizes as ADIT Balance Reverses

Neither ADIT Debit nor Note Payable are to be Included in Buyer’s Future Rate Action Cost Studies

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

17

Evaluation Issues

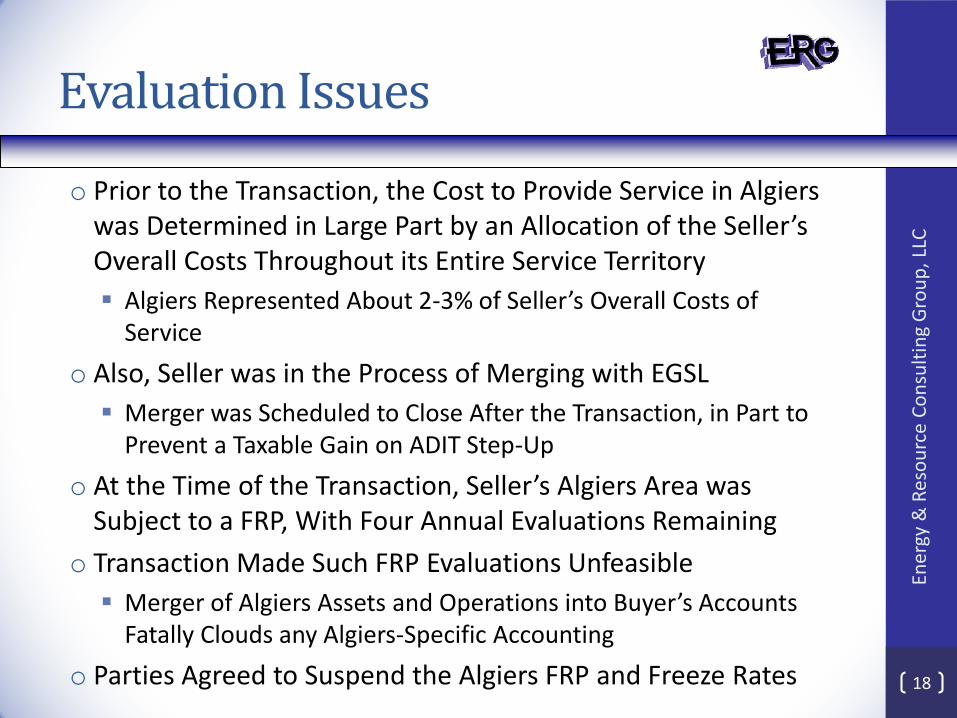

o Prior to the Transaction, the Cost to Provide Service in Algiers was Determined in Large Part by an Allocation of the Seller’s Overall Costs Throughout its Entire Service Territory

Algiers Represented About 2-3% of Seller’s Overall Costs of Service

o Also, Seller was in the Process of Merging with EGSL

Merger was Scheduled to Close After the Transaction, in Part to Prevent a Taxable Gain on ADIT Step-Up

o At the Time of the Transaction, Seller’s Algiers Area was Subject to a FRP, With Four Annual Evaluations Remaining

o Transaction Made Such FRP Evaluations Unfeasible

Merger of Algiers Assets and Operations into Buyer’s Accounts Fatally Clouds any Algiers-Specific Accounting

o Parties Agreed to Suspend the Algiers FRP and Freeze Rates

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

18

Transaction Conditions

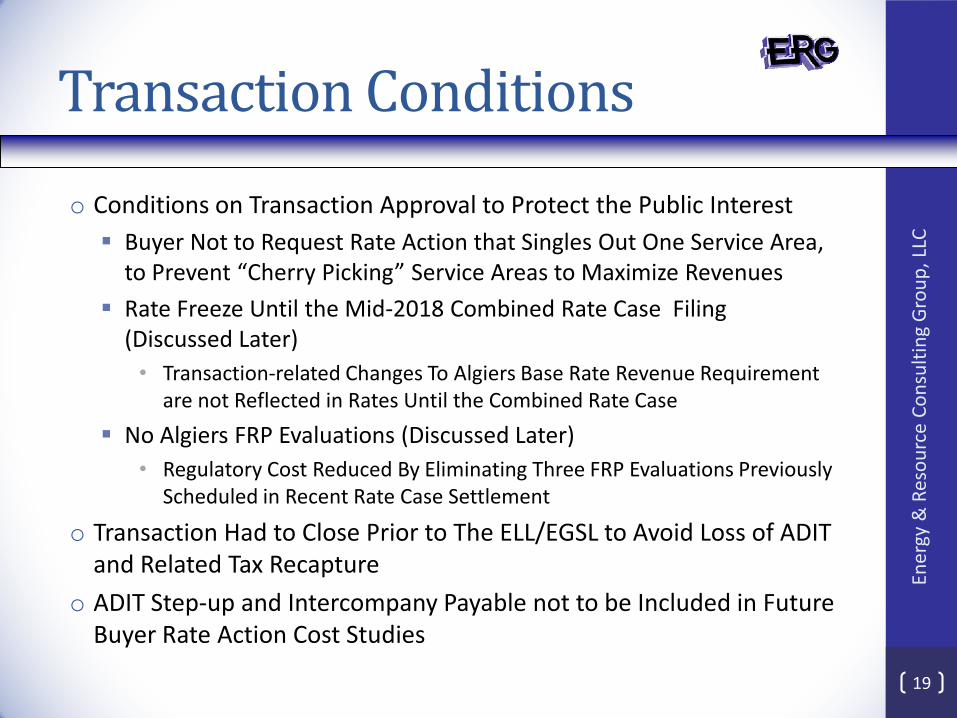

o Conditions on Transaction Approval to Protect the Public Interest

Buyer Not to Request Rate Action that Singles Out One Service Area, to Prevent “Cherry Picking” Service Areas to Maximize Revenues

Rate Freeze Until the Mid-2018 Combined Rate Case Filing (Discussed Later)

• Transaction-related Changes To Algiers Base Rate Revenue Requirement are not Reflected in Rates Until the Combined Rate Case

No Algiers FRP Evaluations (Discussed Later)

• Regulatory Cost Reduced By Eliminating Three FRP Evaluations Previously Scheduled in Recent Rate Case Settlement

o Transaction Had to Close Prior to The ELL/EGSL to Avoid Loss of ADIT and Related Tax Recapture

o ADIT Step-up and Intercompany Payable not to be Included in Future Buyer Rate Action Cost Studies

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

19

Rate Making Issues

o The Transaction Closed On September 1, 2015

o The First Full-year Test Year Available for a Cost Of Service Study on Buyer’s Combined Operations Would be CY 2016

In Our Experience, a Split-Year Test Year had Proven to be Problematic

o Seller was in The Second Step of a 4-Step Annual Algiers Retail Rate Ramp-up Scheduled to Finish In 2017

At the End of the 4-step Rate Ramp-up, Algiers Rates Will be Roughly Comparable to Those Currently Charged by Buyer

o In the Interest of Rate Stability, Parties Negotiated a Rate Freeze Through 2018, When a Combined Rate Case Based on a 2017 TY For the Buyer’s Combined Operations May Set New Rates

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

20

Interim Ratemaking Issues

o Until New Rates can be Established for all of New Orleans Through a Combined Rate Case, the Following Interim Provisions Were Adopted

A Combined Fuel Adjustment Clause

• Important Rate Differences Between Algiers and Buyer’s Original Service Area

A Combined (Blended) Environmental Adjustment Clause

Separate RTO (i.e., MISO) Cost Recovery Riders

Phase-in Of Previously Approved Rate Increases in Algiers to Continue

Separate Energy Efficiency / DSM Program Budgets and Funding Sources En

ergy

& R

eso

urc

e C

on

sult

ing

Gro

up

, LLC

21

IV. ACCOUNTING METHODOLOGIES

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

22

Accounting Methodologies

o Objective to Determine Net-book Value of Assets Sold to Buyer

o Complications

Most Distribution Assets Were Accounted for With Mass PropertyAccounting Where Individual Assets were not Identified

• The Original Cost of Most Distribution Assets Physically in Algiers wasUnknowable

• The Sales Price of Most Distribution Assets was Established by Allocatinga Portion of all Of Seller’s Distribution Assets

• Allocation was Based on the Same Factors From the Most Recent RateCase for Algiers

Some Transmission Assets Carried Across the Boundary BetweenBuyer and Seller

• Asset Purchase Price and Related O&M was Divided Between Buyer andSeller Based on Length of Transmission on Either Side of Boundary

Accounts Receivable based on Differing Billing Cycles and DifferentCollection Rates

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

23

Accounting Methodologies

o Complications (Cont.)

Seller and Buyer Have Different Depreciation Rates. Upon Closeof Transaction, Algiers Assets Begin Depreciation According toBuyer’s Approved Depreciation Rates

Regulatory Assets Were Transferred at Their Book Value net ofAmortization

Property Right to Collect Securitization Bonds’ Servicing CostsExtends to Algiers

ADIT is Substantially Eliminated on Buyer’s Books due to Tax BasisStep-up

• Effect of ADIT is Recreated Through Intercompany Note

Algiers Benefits from Buyer’s Existing Storm Reserve

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

24

Compliance Filing

o Within Three Months of Close of the Transaction, Buyer wasRequired to Make an Accounting Compliance Filing

Identifying and Valuing the Algiers Assets as of Transaction Close

Showing Supporting Data

Showing all Assumptions and Computations, and Formulae

o 60-day Review Period Following Filing of AccountingCompliance Filing

Upon Completion of Review Period, Parties may File List ofUnresolved Issues

o 6-month Period to Resolve Issues With AccountingCompliance Filing

Unresolved Issues may Call for Supplemental Procedural Schedule

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

25

V. OBSERVATIONS and Q&A

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

26

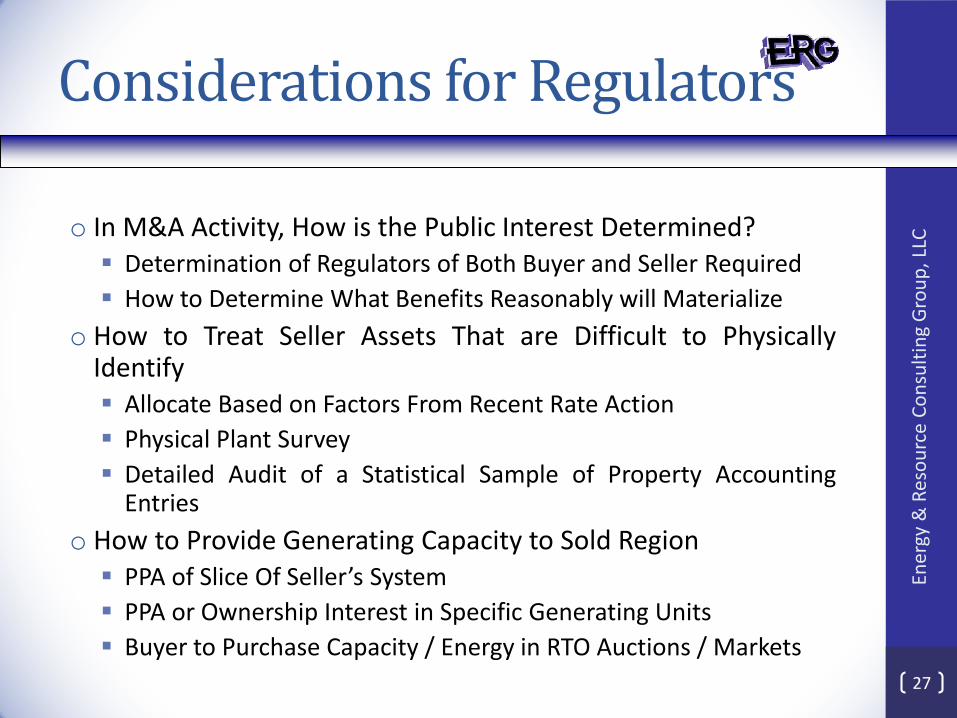

Considerations for Regulators

o In M&A Activity, How is the Public Interest Determined? Determination of Regulators of Both Buyer and Seller Required

How to Determine What Benefits Reasonably will Materialize

o How to Treat Seller Assets That are Difficult to PhysicallyIdentify Allocate Based on Factors From Recent Rate Action

Physical Plant Survey

Detailed Audit of a Statistical Sample of Property AccountingEntries

o How to Provide Generating Capacity to Sold Region PPA of Slice Of Seller’s System

PPA or Ownership Interest in Specific Generating Units

Buyer to Purchase Capacity / Energy in RTO Auctions / Markets

Ener

gy &

Res

ou

rce

Co

nsu

ltin

g G

rou

p, L

LC

27

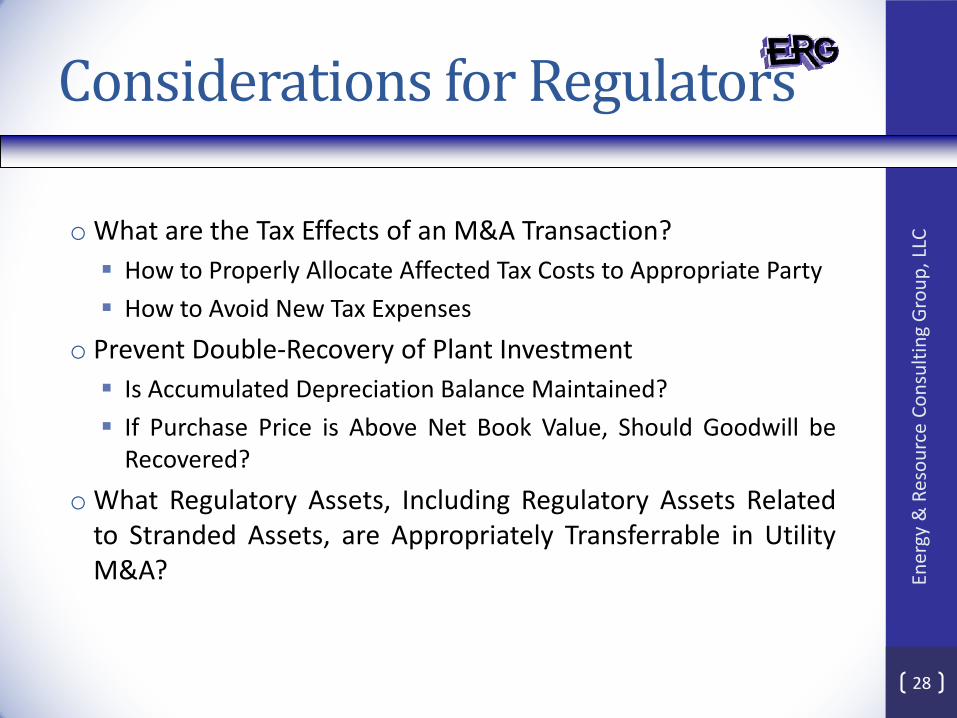

Considerations for Regulators

o What are the Tax Effects of an M&A Transaction?

How to Properly Allocate Affected Tax Costs to Appropriate Party

How to Avoid New Tax Expenses

o Prevent Double-Recovery of Plant Investment

Is Accumulated Depreciation Balance Maintained?

If Purchase Price is Above Net Book Value, Should Goodwill beRecovered?

o What Regulatory Assets, Including Regulatory Assets Relatedto Stranded Assets, are Appropriately Transferrable in UtilityM&A? En

ergy

& R

eso

urc

e C

on

sult

ing

Gro

up

, LLC

28