v ice president—portfolio specialist: u.s. equities v ice...

TRANSCRIPT

US LARGE-CAP GROWTH EQUITY STRATEGY12 APRIL 2017

FOR EXISTING CLIENT IN STRATEGY ONLY. NOT FOR FURTHER DISTRIBUTION.

Presentation to:

T. ROWE PRICE 78

Client Service

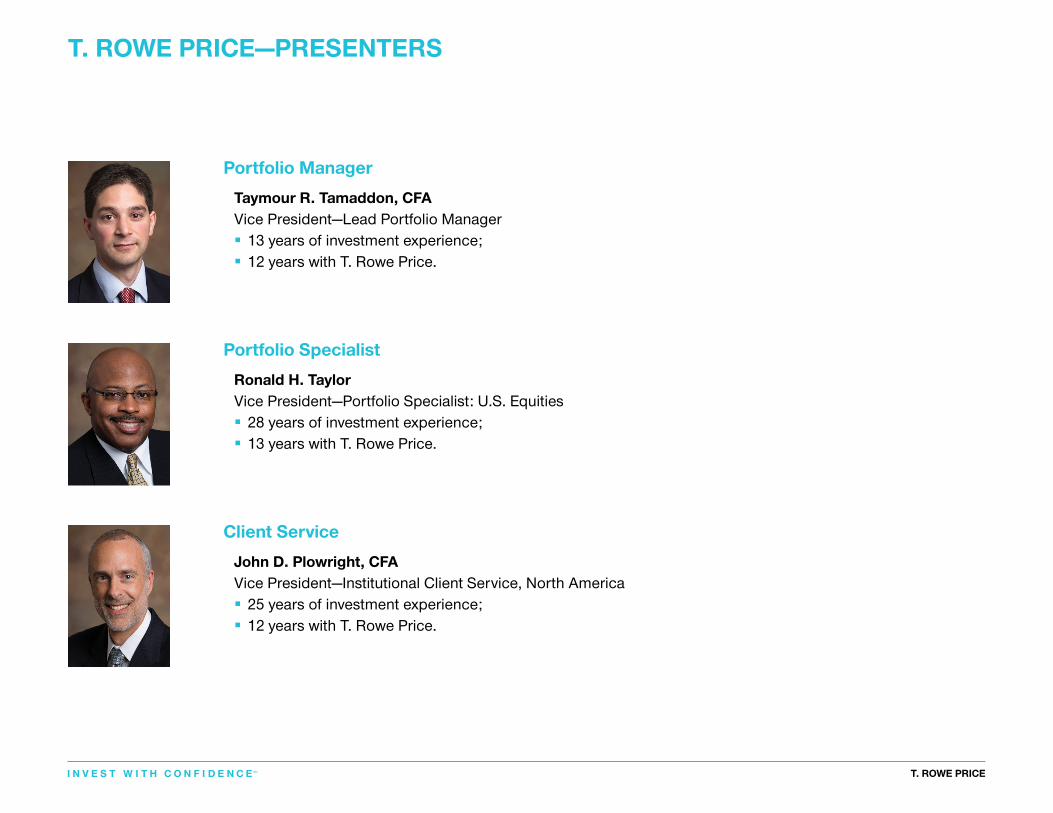

John D. Plowright, CFA Vice President—Institutional Client Service, North America § 25 years of investment experience; § 12 years with T. Rowe Price.

John D. Plowright, CFAInstitutional Client Service, North America

JOHN D. PLOWRIGHT, CFA

T. ROWE PRICE 64

Portfolio Specialist

Ronald H. Taylor Vice President—Portfolio Specialist: U.S. Equities§ 28 years of investment experience;§ 13 years with T. Rowe Price.

Ronald H. TaylorPortfolio Specialist

RONALD H. TAYLOR

T. ROWE PRICE 60

Portfolio Manager

Taymour R. Tamaddon, CFA Vice President—Lead Portfolio Manager (Eff ective 1 January 2017)§ 13 years of investment experience;§ 12 years with T. Rowe Price.

Taymour R. Tamaddon, CFAPortfolio Manager

TAYMOUR R. TAMADDON, CFA

T. ROWE PRICE

Australia Level 31120 Collins StreetMelbourne VIC 3000Australia+61.03.9225.5434

Australia Level 50, Governor Phillip Tower1 Farrer Place, Suite 50BSydney NSW 2000Australia+61.2.8667.5700

Canada Suite 4240, 77 King Street WestTD North TowerP.O. Box 87Toronto, ON M5K 1G8Canada+1.416.360.5777

Denmark Tuborg Havnevej 19DK-2900 HellerupDenmark+45.33.36.05.00

Germany Bockenheimer Landstraße 17/1960325 Frankfurt am MainGermany+49.69.71045.5218

Hong Kong 21/F Jardine House1 Connaught PlaceCentral, Hong Kong+852.2536.7800

ItalyVia Torino 220123, MilanItaly+39.02.72546615

Japan GranTokyo South Tower 7F9-2, Marunouchi 1-chome,Chiyoda-ku, Tokyo100-6607, Japan+81.3.6758.3800

Luxembourg 35 Boulevard Prince HenriL-1724 LuxembourgGrand Duchy of Luxembourg+352.27.47.251

Netherlands Strawinskylaan 10471077 XX AmsterdamNetherlands+31.20.333.62.00

Singapore 501 Orchard Road10-02 Wheelock PlaceSingapore 238880+65.6836.0098

SpainTorre EuropaPaseo de la Castellana 95–1528046 MadridSpain+34.91.418.69.50

Sweden Ôstermalmstorg 1114 42 StockholmSweden+46-85-025-65-93

Switzerland Talstrasse 65, 6th Floor8001 ZurichSwitzerland+41.44.227.1550

United Arab Emirates Dubai InternationalFinancial CentreThe Gate, Level 15, Offi ce 24PO Box 482023DubaiUnited Arab Emirates+971.4.4019266

United Kingdom 60 Queen Victoria StreetLondon, EC4N 4TZUnited Kingdom+44.20.7651.8200

United States 100 East Pratt StreetBaltimore, MD 21202United States+1.410.345.2000

T. ROWE PRICE

T. ROWE PRICE 64

Portfolio Specialist

Ronald H. Taylor Vice President—Portfolio Specialist: U.S. Equities§ 28 years of investment experience;§ 13 years with T. Rowe Price.

Ronald H. TaylorPortfolio Specialist

RONALD H. TAYLOR

T. ROWE PRICE—PRESENTERS

T. ROWE PRICE 60

Portfolio Manager

Taymour R. Tamaddon, CFA Vice President—Lead Portfolio Manager (Eff ective 1 January 2017)§ 13 years of investment experience;§ 12 years with T. Rowe Price.

Taymour R. Tamaddon, CFAPortfolio Manager

TAYMOUR R. TAMADDON, CFA

T. ROWE PRICE 78

Client Service

John D. Plowright, CFA Vice President—Institutional Client Service, North America § 25 years of investment experience; § 12 years with T. Rowe Price.

John D. Plowright, CFAInstitutional Client Service, North America

JOHN D. PLOWRIGHT, CFA

T. ROWE PRICE

TABLE OF CONTENTS

201703-129460

1 Section A: Company Overview

2 Section B: Investment Discipline and Process

3 Section C: Market Overview

4 Section D: Performance Review

5 Section E: Portfolio Review and Characteristics

6 Section F: Fee Schedules

7 Section G: Additional Information and Disclosures

8 Section H: Glossary of Investment Terms

9 Section I: Biographical Backgrounds

1T. ROWE PRICE

COMPANY OVERVIEW

2 T. ROWE PRICE6 T. ROWE PRICE

INDEPENDENT INVESTMENT ORGANIZATION

§ We are focused solely on investment management and related services

ALIGNMENT OF INTERESTS

§ We are a publicly owned company with substantial employee ownership

FINANCIAL STRENGTH

§ We carry no outstanding long-term debt and maintain substantial cash reserves

GLOBAL INVESTMENT PLATFORM

§ We off er a full range of Equity, Fixed Income, and Asset Allocation solutions

STABLE LEADERSHIP TEAM

§ Our Management Committee averages 16 years with T. Rowe Price3

A GLOBAL ASSET MANAGEMENT FIRM—FOCUSED ON CLIENT SUCCESS

1 The combined assets under management of the T. Rowe Price group of companies in USD as of December 31, 2016. The T. Rowe Price group of companies includes T. Rowe Price Associates, Inc., T. Rowe Price International Ltd, T. Rowe Price Hong Kong Limited, T. Rowe Price Singapore Private Ltd., and T. Rowe Price (Canada), Inc.

2 78 portfolio managers, 19 associate portfolio managers, 10 regional portfolio managers, 11 sector portfolio managers, 140 investment analysts/credit analysts, 47 quantitative analysts, 4 solutions associates, 45 associate analysts, 28 portfolio specialists/generalists, 2 strategists, 5 specialty analysts, 53 traders, 11 trading analysts, 2 economists, 31 portfolio modeling associates, and 22 management associates.

3 As of Decemer 31, 2016.

Founded in

1937810.81

billion USD in assets under management1

508investment professionals worldwide2,3

Local presence in

16 countries3

Over

6,000 associates worldwide3

as of 31 December 2016.

As of 31 December 2016.

3T. ROWE PRICE 7T. ROWE PRICE

WE INVEST IN OUR GLOBAL INVESTMENT RESOURCESAs of December 31, 2016

EQUITY PROFESSIONALSASSET ALLOCATION PROFESSIONALS

FIXED INCOME PROFESSIONALS

172 FIXED INCOMEProfessionals

30135

EQUITY Professionals

ASSET ALLOCATIONProfessionals

15 YEARSPortfolio Manager Average Tenure

20YEARSPortfolio Manager Average Investment Experience

35|190|133

UNITED STATES

356PROFESSIONALS

66|33

UNITED KINGDOM

99PROFESSIONALS

2PROFESSIONALS

25|6

HONG KONG

31PROFESSIONALS

5

JAPAN

5PROFESSIONALS

9

AUSTRALIA

9PROFESSIONALS

6

SINGAPORE

6PROFESSIONALS

78 portfolio managers, 19 associate portfolio managers, 10 regional portfolio managers, 11 sector portfolio managers, 140 investment analysts/credit analysts, 47 quantitative analysts, 4 solutions associates, 45 associate analysts, 28 portfolio specialists/generalists, 2 strategists, 5 specialty analysts, 53 traders, 11 trading analysts, 2 economists, 31 portfolio modeling associates, and 22 management associates.

As of 31 December 2016

4T. ROWE PRICE 8T. ROWE PRICE

PERSPECTIVES AND RESEARCHAs of December 31, 2016

Global Equities VOLATILITY, UNCERTAINTY, AND THE AGING BULL MARKET

Scott Berg, CFA Portfolio Manager, Global Growth Equity Strategy

PRICEPOINTOctober 2016

Timely intelligence and analysis for our clients.

KEY POINTS

Top-down macroeconomic and political news is dominating markets like never before.

The uneven nature of global economic health and a now more uncertain investing environment has raised questions over whether the equity cycle is coming to an end, or are we merely entering a new phase?

For patient long-term investors, such uncertainty typically creates buying opportunities in durable growth stocks, especially those with perceived cyclicality. Importantly, although profits growth and earnings have been poor at an aggregate level, there remain compelling pockets of growth in the world, and this remains a perennial opportunity throughout a cycle.

While the rally in oil and commodity prices has brought about a debate on the potential for a value cycle to form, we believe that long-term growth stocks are likely to continue to command a sustainable premium in a challenging macroeconomic environment.

MACROECONOMIC HEADLINES DOMINATE IN 2016

Macro and top-down events are dominating markets like never before in 2016. Rising uncertainty is to be expected when you combine the fact that we are eight years into the second longest bull market in history, in a U.S. election year, and in an environment where so many of the pillars of past return are evolving. The result ofthe UK referendum on European Union (EU) membership has added to the list of macroeconomic and political risks facing markets.

Realistically, the Brexit result will impact the UK economy in the near term as companies hold back investment in the face of uncertainty surrounding the UK’s relationship with Europe. Continental Europe may suffer a similar fate, an unwelcome outcome for a region that is growing slowly and still at the beginning of its economic recovery. Ongoing stimulus from the European Central Bank to support the European economy is highly likely and affirms the view that interest rates are likely to remain low

FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR FURTHER DISTRIBUTION.

Post-Brexit Vote BRITAIN LEANS TOWARD A CLEAN BREAK FROM THE EU

PRICEPOINTOctober 2016

Timely intelligence and analysis for our clients.

KEY POINTS

New UK Prime Minister Theresa May has announced that Britain will begin the process of leaving the European Union by the end of March 2017.

This removes some of the uncertainty about how the country will extricate itself from the EU but has also heightened concerns about the potential ramifications of a so-called hard Brexit.

In our view, May’s announcement and the tone she used to make it signals less market-friendly government policies, potentially harming the UK’s growth prospects and weakening the sterling.

The continuing market uncertainty, however, will provide opportunities for patient investors with a long-term investment horizon.

May’s statement on October 2 at her first Conservative Party conference as Prime Minister was by far the strongest indication that she prefers the “hard’’ option of disentangling Britain from the EU, meaning a full withdrawal from the customs union and single European market.

“There will be no unnecessary delays in invoking Article 50. We will invoke it when we are ready. And we will be ready soon. We will invoke Article 50 no later than the end of March next year,” May said.

Quentin Fitzsimmons, a portfolio manager in T. Rowe Price’s fixed income team, says, “The Brexit vote was won by people who haven’t been doing well with the status quo. May is out to win their support and confidence in order to win the next general election. A more hardline approach to Brexit now seems more likely as May’s government regards the referendum result as a clear signal that border and migration controls are nonnegotiable in the coming Brexit negotiations.”

Global Fixed Income SHOULD I STAY OR SHOULD I GO? BOND INVESTORS FACE DIFFICULT CHOICES AHEAD

Arif Husain Head of International Fixed Income

PRICEPOINTOctober 2016

Timely intelligence and analysis for our clients.

KEY POINTS

Bond investors face a very difficult investment environment: Yields are near record lows, central bank actions have caused widespread volatility, and concerns persist over the prospects for the global economy.

Yields are likely to remain low, protecting existing portfolios against sudden declines in value, but weak U.S. corporate balance sheets could signal volatility.

It is still possible to make money in this environment, but rising correlations between equities and certain bond assets are complicating matters.

Ultimately, investors need to decide whether they want to access the higher yields available from emerging market, high yield, and corporate debt (which means accepting higher correlations with equities) or the greater diversification available from developed market sovereigns (which will mean accepting lower yields).

Every asset in a portfolio needs to justify its place. As investors, therefore, it is important that we frequently ask ourselves a basic question: Why am I holding this product? If we can’t provide a clear answer, then it is time to rethink our approach. Investing in a security for the wrong reasons can prove to be an expensive mistake.

The question is particularly important for fixed income investors at the moment. Yields in developed market sovereigns remain close to record lows, with some USD $13 trillion1 currently estimated to be in negative territory. Unconventional central bank actions have caused markets to be volatile and unpredictable, leaving participants in a near-permanent state of anxiety about when and where the next hike or cut may be coming from. Concerns over Chinese growth, the UK’s exit from the European Union, and an increasingly fractious Middle East are only adding to a prevailing climate of uncertainty. Faced with such difficult terrain, bond investors can be forgiven for not knowing which way to turn.

FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR FURTHER DISTRIBUTION.

1 Source: Financial Times as of August 12, 2016.

MARKET TRENDS

PLAN SPONSORS STRATEGYMEDIA

NEWSLETTERS

Defi ned Contribution § The PPA, 10 Years In. A Retirement

Revolution Ready for Evolution § Financial Wellness: Household

Financial Capability

Defi ned Benefi t § LDI: Customization Does Not Lead

to Higher Turnover § Using an LDI Completion Manager

Global Equity § A Case for Inclusion: International

Small-Cap Equity § Steering A Path Through Uncertainty § Investment Opportunities in a Low-

Growth World

Global Fixed Income § Emerging Markets Corporate Bonds:

Seeking Yield and Ineffi ciencies in Emerging Credit Markets

§ Is the UK About To Switch To Fiscal Stimulus?

§ Should I Stay or Should I Go? Bond Investors Face Diffi cult Choices Ahead

Video § Investors Have A Choice to Make

Blogs § Central Banks: Tiptoeing Toward

Tighter Policy § Global Growth Lifts Amid a Benign

Outlook for Global Infl ation

Webinars § T. Rowe Price Webcast: A Post-

Election Point of View § Fixed Income: Should I Stay

or Should I Go?

Press § Barron’s: Interview with Shawn

Driscoll—Get Ready for the Great Oil Bust of 2017

§ Bloomberg TV Interview Ziad Bakri— Health Policy Under the Trump Administration

§ Global Market Outlook 2017 Press Briefi ng

§ Pension Curve Insider § Fixed Income Sector Pulse § In Focus § DCIO § Quarterly Investment Updates

§ Global Market Outlook: The right side of change

§ The Benefi ts of Active Management at T. Rowe Price

§ Brexit: Britain leans toward a clean break from EU

§ Global Capital Market Updates

As of 31 December 2016

5T. ROWE PRICE

LOS ANGELES DEPARTMENT OF WATER AND POWER—RELATIONSHIP MANAGEMENT TEAM

§ Coordinates overall relationship management activities

§ Primary point of contact providing access to broad firm resources

§ Ultimate accountability for client satisfaction

Institutional Client Service:

A dedicated team helping you meet your overall objectives.

Institutional Client Operations:

Institutional Sales:

§ Key contact during initial onboarding and for future cash flows

§ Operational liaison with legal, investments, and custodian

§ Coordinates review of legal agreements and contracts

§ Partners with client service team to share intellectual capital, industry insights, etc.

§ Leads investment solutions dialogue in areas beyond current mandate(s)

§ Partners on relationship management activities

§ Assists with coordination of portfolio reviews and reporting

§ Supports client-specific requests and day-to-day servicing

38T. ROWE PRICE

JOHN D. PLOWRIGHT

Footnote Nimbus Sans Novus Condensed 10/10

After updating please save EPS in: GROUPS\KitBP\TRP_MKTG_KITS\TRP_ExbTRPGen\_EPS Presenters as: Your inst Client Plowright.eps

John D. Plowright, CFAPhone: 415-772-1117

E-mail: [email protected]

14T. ROWE PRICE

MEREDITH EMPIE

Footnote Nimbus Sans Novus Condensed 10/10

After updating please save EPS in: GROUPS\KitBP\TRP_MKTG_KITS\TRP_ExbTRPGen\_EPS Presenters as: Your inst Client Empie.eps

Meredith EmpiePhone: 415-772-1118

E-mail: [email protected]

56T. ROWE PRICE

ANNE FADER

Footnote Nimbus Sans Novus Condensed 10/10

After updating please save EPS in: GROUPS\KitBP\TRP_MKTG_KITS\TRP_ExbTRPGen\_EPS Presenters as: OP Fader.eps

Anne M. FaderPhone: 410-345- 2268

E-mail: [email protected]

6T. ROWE PRICE

KEN BROOKS

Footnote Nimbus Sans Novus Condensed 10/10

After updating please save EPS in: GROUPS\KitBP\TRP_MKTG_KITS\TRP_ExbTRPGen\_EPS Presenters as: Your inst Client Brooks.eps

Ken BrooksPhone: 415-772-1104

E-mail: [email protected]

6T. ROWE PRICE

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

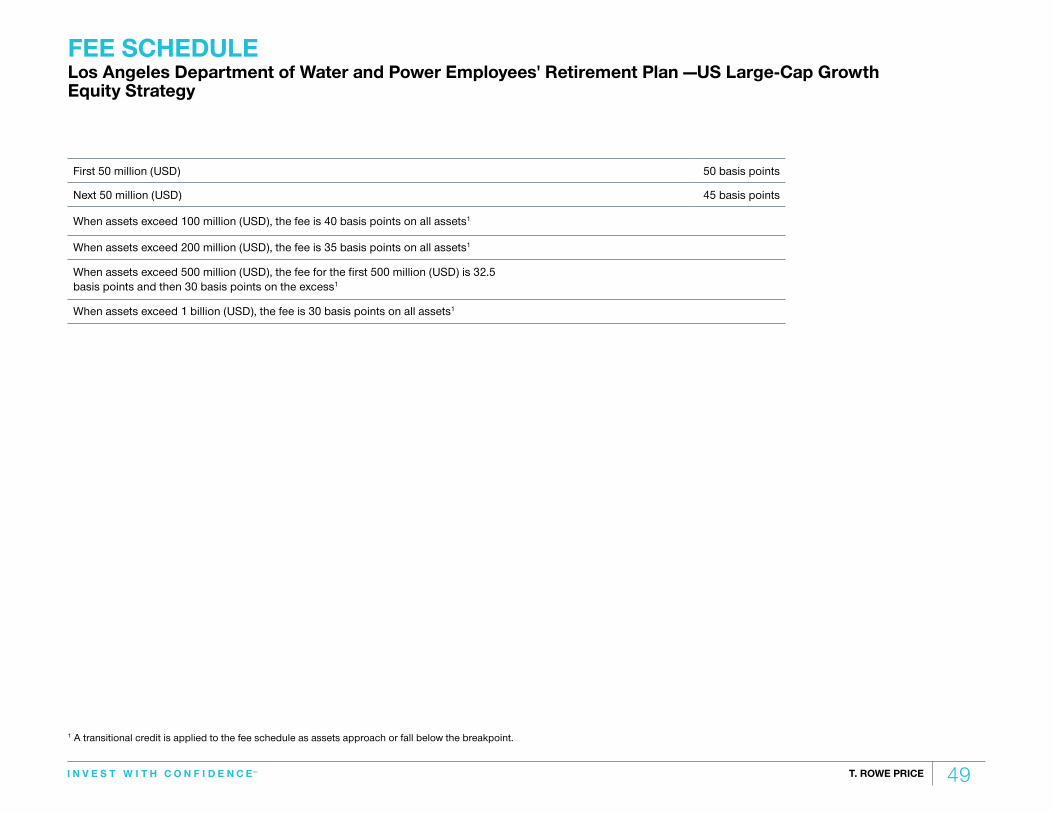

Objective

§ Seeks to provide long-term capital appreciation by investing primarily in common stocks of large growth companies.

Mandate

§ US Large-Cap Growth Equity Strategy: Separately Managed Portfolio Strategy Assets as of 31 December 2016: 30.8 Billion USD

Benchmark

§ Russell 1000 Growth Index

Investment Guidelines

§ No more than 5% of portfolio may be invested in any one issue, unless it represents more than 5% of index, in which case the portfolio may invest up to 125% of index weight.

§ All foreign securities, except for Benefit Driven Incorporations (BDIs) included in the Russell indices, are prohibited.

CLIENT OBJECTIVELos Angeles Department of Water and Power Retirement Plan:

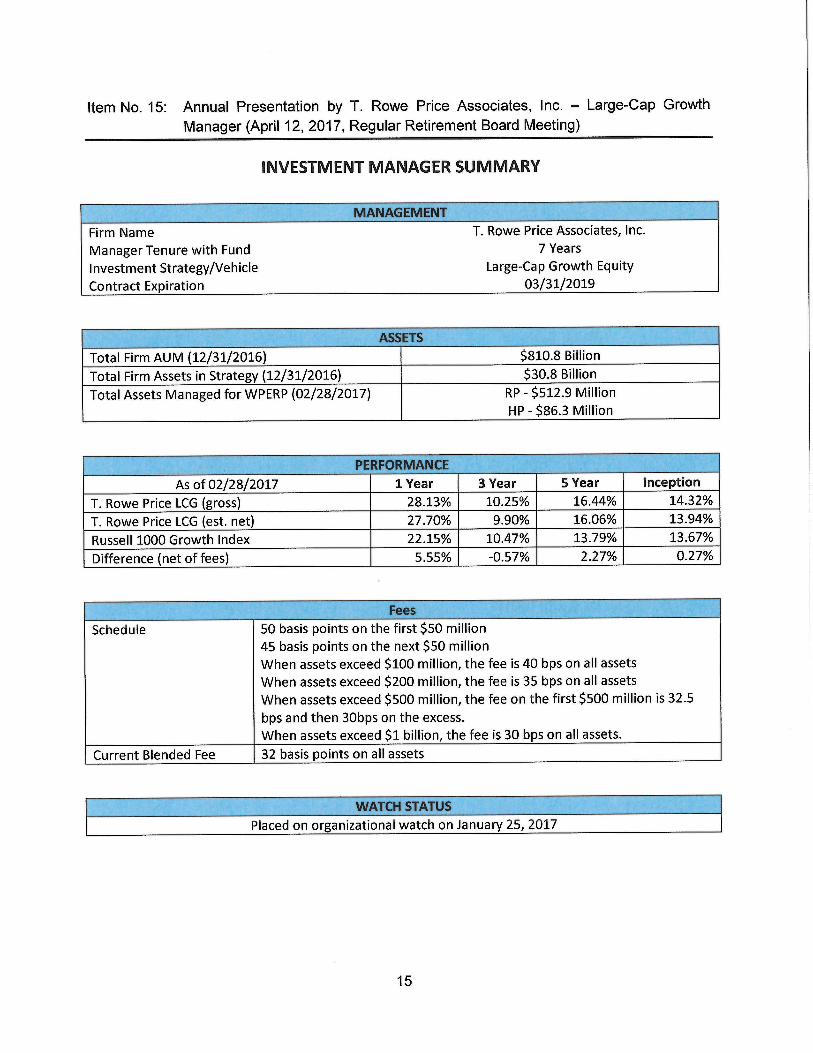

Inception value as of 16 April 2010 360,783,756 USDContributions 30,998,937 Withdrawals 343,044,405 Market Appreciation 464,152,668 Market Value as of 28 February 2017 512,890,956

Inception value as of 16 April 2010 50,894,003 USDContributions 9,455,219 Withdrawals 51,106,787 Market Appreciation 77,097,804 Market Value as of 28 February 2017 86,340,240

Los Angeles Department of Water and Power Health Benefits Plan:

7T. ROWE PRICE 33T. ROWE PRICE

1 The combined U.S. Large-Cap Growth Equity assets of the T. Rowe Price group of companies. The T. Rowe Price group of companies includes T. Rowe Price Associates, Inc., T. Rowe Price International Ltd, T. Rowe Price Hong Kong Limited, T. Rowe Price Singapore Private Ltd., and T. Rowe Price (Canada), Inc.

2 The total US Large-Cap Growth Equity Strategy assets of the T. Rowe Price group of companies. 3 Corporate, Public, Non-Profi t, Taft-Hartley, Endowments/Foundations, and Sub-Advisory clients.4 Includes a U.S.-registered mutual fund and a common trust fund. Strategy assets under management for the T. Rowe Price U.S.-registered mutual funds and common trust funds are calculated based on the closing price of the security in its respective market and may

diff er from the net asset value of the fund.

U.S. LARGE-CAP GROWTH ASSETS UNDER MANAGEMENT

Total U.S. Large-Cap Growth EquityAssets: 155.0 Billion USD1

As of 31 December 2016

US Large-Cap Growth EquityStrategy Assets: 30.8 Billion USD2

As of 31 December 2016

Large-Cap Growth investing is a signifi cant business for T. Rowe Price.

US Large-Cap CoreGrowth Equity Strategy56.5B USD

US GrowthStock Strategy

67.7B USD

US Large-CapGrowth Equity Strategy30.8B USD

Non-U.S. Commingled Fund1,265.4M USD

U.S. Separate Accounts13,270.0M USD3

Non-U.S. Separate Accounts2,915.6M USD

U.S. InstitutionalCommingled Funds13,353.8M USD4

Numbers may not total due to rounding.

8T. ROWE PRICE

INVESTMENT DISCIPLINE AND PROCESS

9T. ROWE PRICE 7T. ROWE PRICE

US LARGE-CAP GROWTH EQUITY INVESTMENT TEAMAs of 31 December 2016

Extensive collaboration among investment professionals enhances idea generation.

1 11 sector portfolio managers, 90 research analysts, 42 associate research analysts, 6 quantitative analysts, and 5 specialty analysts as of 31 December 2016. Eff ective 1 January 2017, Taymour Tamaddon assumed portfolio management responsibilities for the strategy.

US Large-Cap Growth Equity StrategyPortfolio Management Team

Stability | Depth | Collaboration

Taymour Tamaddon, CFA Portfolio Manager (LCG)

David L. Rowlett, CFA Associate Portfolio

Manager (LCG)

Joseph B. Fath, CPAPortfolio Manager (GSS)

Larry J. Puglia, CFA, CPA Portfolio Manager (LCCG)

Ronald H. Taylor Portfolio Specialist

Craig S. Watson, CPA Portfolio Specialist

§ 13 years of investment experience

§ 12 years with T. Rowe Price § B.S., Cornell

University § M.B.A., Tuck School

of Business at Dartmouth

§ 13 years of investment experience

§ 8 years with T. Rowe Price § B.B.A., University

of Georgia § M.B.A., University of

North Carolina, Kenan-Flagler Business School

§ 16 years of investment experience

§ 14 years with T. Rowe Price § B.S., University

of Illinois, Urbana-Champaign

§ M.B.A., The Wharton School, University of Pennsylvania

§ 27 years of investment experience

§ 26 years with T. Rowe Price § B.B.A., University of

Notre Dame § M.B.A., The Darden

School, University of Virginia

§ 28 years of investment experience

§ 13 years with T. Rowe Price § B.A., University

of California, Los Angeles

§ M.B.A., Harvard Business School

§ 21 years of investment experience

§ 9 years with T. Rowe Price § B.S., Hampton

University § M.B.A., The Wharton

School, University of Pennsylvania

Equity Research Team154 Research Analysts | Industry Specialists1

10 T. ROWE PRICE

As of 1 January 2017

1 Also has portfolio management responsibilities.2 11 sector portfolio managers, 90 research analysts, 42 associate research analysts, 6 quantitative analysts, and 5 specialty analysts as of 31 December 2016. Highlighted names refl ect analysts with coverage responsibilities for portfolio holdings.

EQUITY RESEARCH TEAM

BAL BaltimoreHKG Hong KongLON London

SGP Singapore SYD Sydney TOK Tokyo

154 Equity Research Professionals worldwide2

HEADS OF EQUITY DIRECTORS OF EQUITY RESEARCH ASSOCIATE DIRECTORS OF EQUITY RESEARCH

Christopher D. Alderson LONGlobal Co-HeadRobert W. Sharps BALGlobal Co-Head

Eric L. Veiel, CFA BALU.S.

Kamran Baig LONEMEA and Latin AmericaStephon Jackson, CFA BALNorth America

Jason Polun, CFA BALNorth AmericaMitchell Todd, CA LONDeveloped Europe

Kes Visuvalingam, CFA SGPAsiaThomas Watson, CFA BALNorth America

Jai Kapadia HKG AsiaTobias Mueller LON Developed Europe

Viral Patel SYD Australia

HEALTH CARE

Ziad Bakri, CFA, MD1 BALU.S. BiotechMelissa Gallagher, Ph.D. LONOUS Pharma/BiotechJohn Hall, Ph.D. BALSmall-Cap Biotech Rachel Jonas BALU.S. SMID Healthcare Adam Poussard, CFA BALU.S. Services & EquipmentKyle Rasbach, Ph.D.,Pharm.D. BALPharmaI-hung Shih, Ph.D BALU.S. Biotech Dai Wang HKGChinese HealthcareJon Wood BALU.S. Medical Devices/ToolsRouven Wool-Lewis, Ph.D. BALU.S. Services & Hospitals

INDUSTRIALS

Jason Adams BALU.S. Aerospace and Defense Peter Bates, CFA1 BALU.S. ConglomeratesAndrew Chang SGPJapan and Asia Ex Japan Auto/Steel Andrew Davis BALU.S. TransportsRyan Ferro, CFA BALU.S. SMID IndustrialsJoel Grant, CFA BALU.S. Autos & Distributors Gianluca Guicciardi, CFA LONIndustrials/Capital GoodsHiromasa Ikeda HKGJapan Small-Cap Industrials Curt Organt, CFA1 BALU.S. Small-Cap GeneralistMelanie Rizzo, CFA BALU.S. Trucking/MachineryEunbin Song, CFA HKGAsia Ex Japan Auto/C&ERupinder Vig LONIndustrials/Capital Goods

BUSINESS SERVICES

Shaun Currie, CFA BALU.S. Business ServicesJon Friar BALU.S. Business ServicesIan McDonald, CFA BALU.S. Business ServicesJared Murphy BALU.S. Bus. Serv./Industrials

TECHNOLOGY

Kennard Allen1 BALU.S. Hardware/SoftwareGreg Dunham, CFA BALU.S. SoftwareTobias Mueller, CFA LONEurope Semi./SoftwareEmily Scudder, CFA, CPA BALU.S. Hardware Joshua Spencer, CFA1 BALU.S. Semi./EquipmentAlan Tu, CFA BALU.S. SoftwareAlison Yip HKGAsia Ex-Japan Hardware

MEDIA/TELECOM

Paul Cho BALCable/Telecom Paul Greene1 BALU.S. Advertising/InternetAden Lau SGPAsia Ex-Japan Telecom/Fin.Jacqueline Liu HKGAsia Ex-Japan InternetJeff Nathan BALU.S. Advertising/Media Corey Shull, CFA BALU.S. Media/InternetChristopher Whitehouse LONEurope Media/Telecom

CONSUMER/RETAIL

Gbemi Adeniyi-Williams LONEMEA Generalist/ConsumerPaulina Amieva BALLatin America GeneralistIra Carnahan, CFA BALU.S. Consumer DiscretionaryEric DeVilbiss, CFA BALU.S. Restaurants/AgricultureAmanda Hall, CFA LONEurope ConsumerMichael Jacobs TOKJapan Retail/LeisureJacob Kann, CFA BALDiscretionaryRekha Marda BALU.S. Food Retail/Durables Sridhar Nishtala SGPAsia Ex-Japan StaplesRobert Quinn, Jr. BALU.S. Consumer StaplesSebastian Schrott LONEuropean Luxury/RetailVivian Si BALU.S. Mass Merch. / ApparelBrian Solomon, CFA BALU.S. Cruise/Lodging Konstantin Stoev, CFA LONEuropean Staples and AutoJohn Williams, CFA BALLarge-Cap Consumer StaplesEric Yuan HKGRegional Gaming

FINANCIAL SERVICES

Malik Asif LONEMEA BanksJon Casper BALU.S. FinancialsVincent DeAugustino, CFA BALU.S. SMID FinancialsChristopher Fortune, CFA BALU.S. Small Cap BanksYoichiro Kai, CMA SGPAsian Banks incl. Japan and Japanese InsuranceGregory Locraft, Jr. BALU.S. P&C InsuranceJihong Min SGPSoutheast Asia BanksThibault Nardin LONEurope BanksMatt Snowling, CFA BALCapital MarketsGabriel Solomon1 BALU.S. Money Center/Insur.Zenon Voyiatzis LONEurope Insur./Financials

REAL ESTATE

Dan McCulley, CFA BALU.S. Real EstatePreeta Ragavan, CFA BALU.S. Real Estate

NATURAL RESOURCES

Haider Ali HKGAsia Ex-Japan Oil & GasSheena Barbosa, CFA HKGAsia Ex-Japan Utilities/Infra.Ryan Burgess, CFA1 BALU.S. Chemicals/IndustrialsChris Driessen BALMetals & MiningShawn Driscoll1 BALU.S. E&PRyan Hedrick, CFA BALU.S. Coal/UtilitiesJon Hussey BALU.S. Agriculture Shinwoo Kim BALU.S. Energy ServicesMatt Mahon BALU.S. Chemicals Ryan Martyn SYDAustralia Energy/IndustrialsChris O’Neill BALU.S. E&PTimothy Parker, CFA1 BALU.S. E&PVivek Rajeswaran, CFA BALU.S. Equip. & Services/WasteThomas Shelmerdine SYDAustralian Metals & MiningJohn Sherman LONEuropean Chemicals/Indus.Christopher Wheaton LONEnergy Majors

REGIONAL GENERALISTS Ulle Adamson, CFA1 LONEMEA Martin Baylac LONLatin AmericaSimon Cheng, CFA, CPA HKGGreater China Small-CapArchibald Ciganer, CFA1 TOKJapan Transports/ConsumerAnouk Dey, CFA BALU.S. Small-Cap Growth Vishnu Gopal HKGIndia & ASEAN Small-CapBen Griffi ths, CFA1 LONEurope Small-CapNabil Hanano, CFA BALEuropeTetsuji Inoue, CPA TOKJapan Small-Cap/Real Estate, Japan TechnologyRandal Jenneke1 SYDAustralia Media/ConsumerJai Kapadia HKGAsia Real Estate/Conglom.Mark Lawrence, CFA LONEMEAOxana Lyalina LONEMEAMichael Niedzielski LONEurope Small-Cap Paul O’Sullivan, ACA SYDAustralia Financials/H.C.Seun Oyegunle, CFA LONEMEAViral Patel SYDAustralia REITS/RetailAlexander Roik BALU.S. Small-Cap ValueSin Dee Tan, CFA LONEurope Small-CapVerena Wachnitz, CFA1 LONLatin America Hiroshi Watanabe, CFA1 TOKJapan SMID-CapMarta Yago LONLatin America

11T. ROWE PRICE 9T. ROWE PRICE

Extensive analyst interaction across industry groups, sectors, and asset classes promotes a broad perspective and timely decision-making.

FUNDAMENTAL RESEARCH AND ANALYSIS

Analysts are industry specialists across capitalization and investment styles

§ Evaluate impact of all competitors within an industry group

Fundamental, bottom-up approach to company research

§ Industry and company dynamics, management team quality, and fi nancial fundamentals are central considerations

“Push/pull” relationship between analysts and portfolio managers

§ Multiple signaling tools communicate analysts’ conviction and urgency

§ Portfolio managers “stress test” analysts’ recommendations to independently confi rm conclusions

§ Valuation assessment is a key consideration

Compensation of our professionals is closely linked to investment performance

§ Quantitative measurement of ratings/impact

§ Qualitative assessment of overall contribution

§ Performance-based bonuses

§ Equity participation

12T. ROWE PRICE 10T. ROWE PRICE

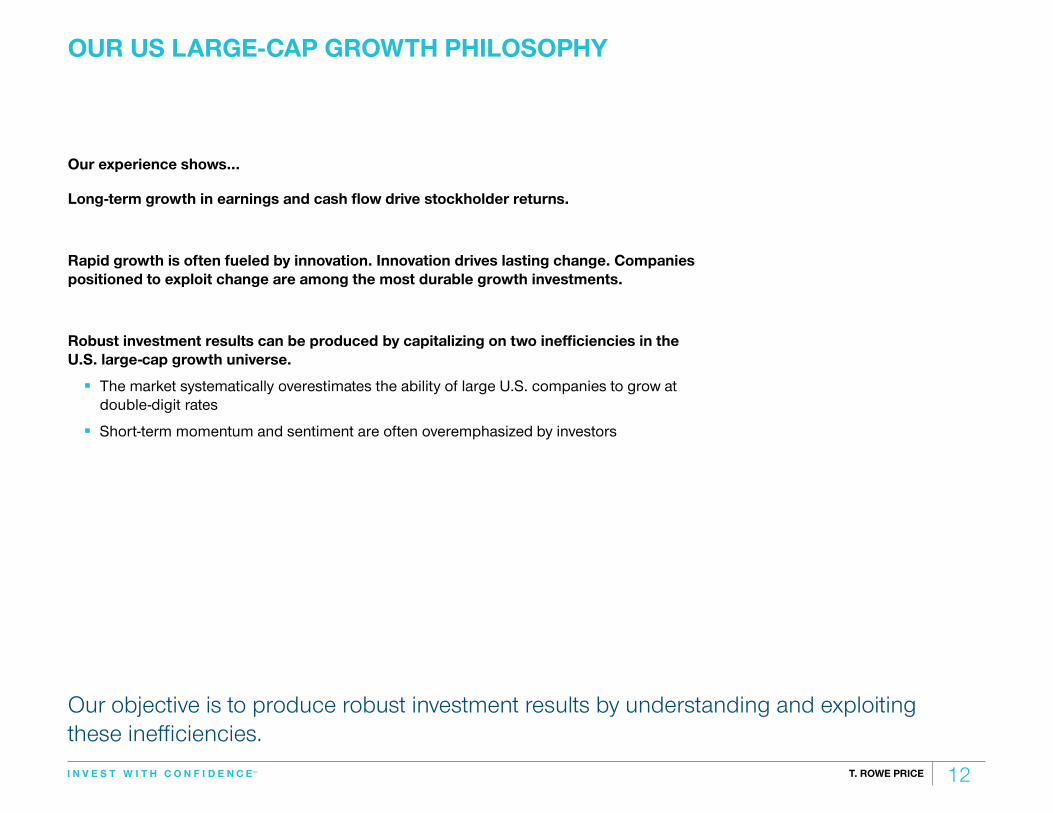

Our objective is to produce robust investment results by understanding and exploiting these ineffi ciencies.

OUR US LARGE-CAP GROWTH PHILOSOPHY

Our experience shows...

Long-term growth in earnings and cash fl ow drive stockholder returns.

Rapid growth is often fueled by innovation. Innovation drives lasting change. Companies positioned to exploit change are among the most durable growth investments.

Robust investment results can be produced by capitalizing on two ineffi ciencies in the U.S. large-cap growth universe.

§ The market systematically overestimates the ability of large U.S. companies to grow at double-digit rates

§ Short-term momentum and sentiment are often overemphasized by investors

13T. ROWE PRICE 11T. ROWE PRICE

1 Sectors representing 10%+ of the Russell 1000 Growth Index.Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

Superior information and implementation can produce robust investment results.

US LARGE-CAP GROWTH INVESTMENT PROCESS Our research-driven, bottom-up approach is the engine for our investment idea generation

§ New information or new insights alter outlook

§ Unanticipated deterioration in investment fundamentals

§ Extreme valuation

§ Most compelling, highest-conviction ideas over three-year time horizon

§ Individual position sizes typically range ±4% relative to Russell 1000 Growth Index weighting

§ Sector weightings generally limited to 0.5X–3.0X of primary1 Russell 1000 Growth Index sector weights

§ Predicted tracking error target of 400–700 basis points relative to the Russell 1000 Growth Index

§ Active risk management process to eliminate “unintended bets”

§ Proprietary industry and company analysis

§ Analyst inputs to confi rm 10%+ Real EPS Growth

§ Independent stress testing by portfolio management team

§ Confi rm analyst conclusions

§ Valuation analysis

§ Quantitative screens

§ Forecasted 10%+ Real EPS Growth

§ Historical ROE

§ Eliminates companies with slow or no long-term growth prospects

§ Generally 5B+ USDmarket cap

§ Primarily U.S. companies

Sell Discipline Portfolio

Construction and Risk Management

500Companies

150–200Companies

80–120Companies

60–75Companies

Fundamental Research and

Analysis Growth Screens Defi ning the

Universe

14T. ROWE PRICE 12T. ROWE PRICE

In-depth company analysis provides portfolio managers with sound, long-term investment ideas.

FUNDAMENTAL RESEARCH ANALYSIS154 equity research professionals1 worldwide who are industry specialists across capitalization and investment styles.

1 11 sector portfolio managers, 90 research analysts, 42 associate research analysts, 6 quantitative analysts, and 5 specialty analysts as of December 31, 2016.

Industry Analysis Company Analysis

Secular Analysis Cyclical Analysis Qualitative Analysis Quantitative Analysis Valuation Analysis

Industry Growth Prospects

§ Unit volume growth

§ Price stability/pricing power

Industry Conditions

§ Capacity additions/reductions

§ Demand drivers

Market Position

§ Market share

§ Brand/reputation, technology, intellectual property

§ Cost position/structural advantage

Management Team Quality

§ Strategy

§ Capital allocation

§ Information systems

Financial Strength

§ Free cash fl ow generation

§ Level and direction of margins

§ Level and direction of ROIC

§ Balance sheet strength

Confi rm Attractive Valuation

§ Relative valuation

§ P/FCF

§ P/E

§ PEG Ratio

§ EV/EBITDA

31 December 2016.

15T. ROWE PRICE

MARKET OVERVIEW

16 T. ROWE PRICE

5

As of 31 December 2016

Past performance is not a reliable indicator of future results. Sources: FactSet

Performance by Style and Market Capitalisation

ONE YEAR THREE YEAR

<-10% -5% to -10% 0% to -5% 0 to +5% +5% to +10% >+10% Scale:

Russell 1000 Value S&P 500 Russell 1000 Growth

Russell M

id-C

ap Grow

th

Russell 2000 Value Russell 2000 Russell 2000 Growth

FIVE YEAR TEN YEAR

17.3% 12.0% 7.1%

20.0% 13.8% 7.3%

31.7% 21.3% 11.3%

8.6% 8.9% 8.6%

9.5% 7.9% 6.2%

8.3% 6.7% 6.6%

14.8% 14.6% 14.5%

15.7% 14.7% 13.5%

15.1% 14.4% 13.7%

5.7% 6.9% 8.3%

7.6% 7.9% 7.8%

6.3% 7.1% 7.7%

Rus

sell

Mid

-C

ap V

alue

Rus

sell

Mid

-C

ap V

alue

Russell M

id-C

ap Grow

th

Russell 1000 Value S&P 500 Russell 1000 Growth

Russell 2000 Value Russell 2000 Russell 2000 Growth

Russell 1000 Value S&P 500 Russell 1000 Growth

Russell 1000 Growth S&P 500 Russell 1000 Value

Russell M

id-C

ap Grow

th

Russell M

id-C

ap Grow

th Rus

sell

Mid

-C

ap V

alue

Rus

sell

Mid

-C

ap V

alue

Russell 2000 Value

Russell 2000 Growth

Russell 2000 Growth

Russell 2000

Russell 2000

Russell 2000 Value

PERFORMANCE BY STYLE AND MARKET CAPITALISATION Periods Ended 31 December 2016

Source: FactSet.Past performance cannot guarantee future results.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

17T. ROWE PRICE

3

85

90

95

100

105

110

115

Inde

x Le

vel-R

ebas

ed

S&P 500 INDEX December 2015 – December 2016

Marching Higher Despite the Uncertainties

Past performance is not a reliable indicator of future results. Sources: FactSet, The Wall Street Journal, T. Rowe Price.

Period S&P 500 IndexReturn

1 year 12.0%

5 year 14.7%

10 year 6.9%

As of 31 December 2016

Uncertainty heightened by Brexit vote

U.S. PresidentialElection

0

5

10

15

20

25

30

Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16

VIX

1 year average

Rising/Fading Anxiety OverImpending U.S. Recession

MARCHING HIGHER DESPITE THE UNCERTAINTIESOne Year Ended 31 December 2016Figures are Calculated in U.S. Dollars

Past performance cannot guarantee future results.

Sources: FactSet, The Wall Street Journal, T. Rowe Price.Past performance cannot guarantee future results.

S&P 500 INDEXPeriod

S&P 500IndexReturn

1 year 12.0%

5 year 14.7%

10 year 6.9%

18 T. ROWE PRICE

6

1.4

5.9 6.9

-1.5

10.16.6

-2.5

-21.1

-4.8

4.7

-8.4

3.4

12.013.8

-2.7

22.8

6.0 5.4

18.9

27.4

16.3 16.7

23.5

-25%

-15%

-5%

5%

15%

25%

35%

S&P 500 Sector Returns

2015 2016

InfoTech

HealthCare Financials

ConsumDisc

ConsumStpls

Indust &Bus Svcs Energy Utilities Real Estate Materials

TelecomSvcs

S&P 500 Index Weights:

21% 14% 15% 12% 9% 10% 8% 3% 3% 3% 3%

As of 31 December 2016

Past performance is not a reliable indicator of future results. Returns in US dollars. Sources: Wilshire, FactSet

Reversal in Sector Leadership over 2016; Financials, Energy, and Materials Rebound

REVERSAL IN SECTOR LEADERSHIP OVER 2016; FINANCIALS, ENERGY, AND MATERIALS REBOUND As of 31 December 2016Figures are Calculated in U.S. Dollars

Sources: Wilshire, FactSet.Past performance cannot guarantee future results.

S&P 500 SECTOR RETURNS

T. Rowe Price uses the MSCI/S&P Global Industry Classifi cation Standard (GICS) for sector and industry reporting. Each year, MSCI and S&P review the GICS structure. The last change occurred on31 August 2016. T. Rowe Price will adhere to all future updates to GICS for prospective reporting.

19T. ROWE PRICE

EQUITY VALUATIONS AND EARNINGS GROWTH 20 Years Ended December 2016

8

Past performance is not a reliable indicator of future results. Sources: FactSet

Equity Valuations and Earnings Growth

S&P 500 Russell 1000 Value Russell 1000 Growth Russell Mid Cap Russell 2000

EPS Growth 2015 1.0 -3.9 6.6 3.2 4.5

EPS Growth 2016e 0.7 -1.2 2.7 1.4 -1.2

EPS Growth 2017e 12.0 13.1 11.0 12.4 26.2

EPS Growth 2018e 11.7 11.8 12.2 12.7 22.9

0

10

20

30

40

50

60

S&P 500 Russell 1000 Value Russell 1000 Growth Russell Mid Cap Russell 2000

MARKET INDICES: FORWARD P/E RATIOS Past 20 years, as of 31 December 2016

Current Relative P/E Ratio

Average P/E Ratio

P/E Ratio Range over past 20 years

Past performance cannot guarantee future results.

Source: FactSet.Past performance cannot guarantee future results.

MARKET INDICES: FORWARD P/E RATIOS

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

20 T. ROWE PRICE

23

BULLS

1. Near term earnings comparison arefavourable for key sectors of market

2. Compared to alternatives, valuation ofequities appears reasonable

3. Employment trends remain broadly positive

4. Sentiment and business cycle appearsupportive

BEARS 1. Profit margins have plateaued as wage

growth accelerates

2. Revenue growth remains challengedacross many segments of the market

3. Valuations are extended by historicalstandards

4. Rates and U.S. dollar expected to trendhigher

As of 31 December 2016

The Outlook for US Equities: Valid Arguments on Both Sides of Debate

Cautiously optimistic. Expect higher levels of volatility as we negotiate periods of uncertainty. Remain disciplined, value diversification, and focus on long-term opportunities.

Sources: T Rowe Price

THE OUTLOOK FOR US EQUITIES: VALID ARGUMENTS ON BOTH SIDES OF DEBATE As of 31 December 2016

Source: T. Rowe Price.

21T. ROWE PRICE

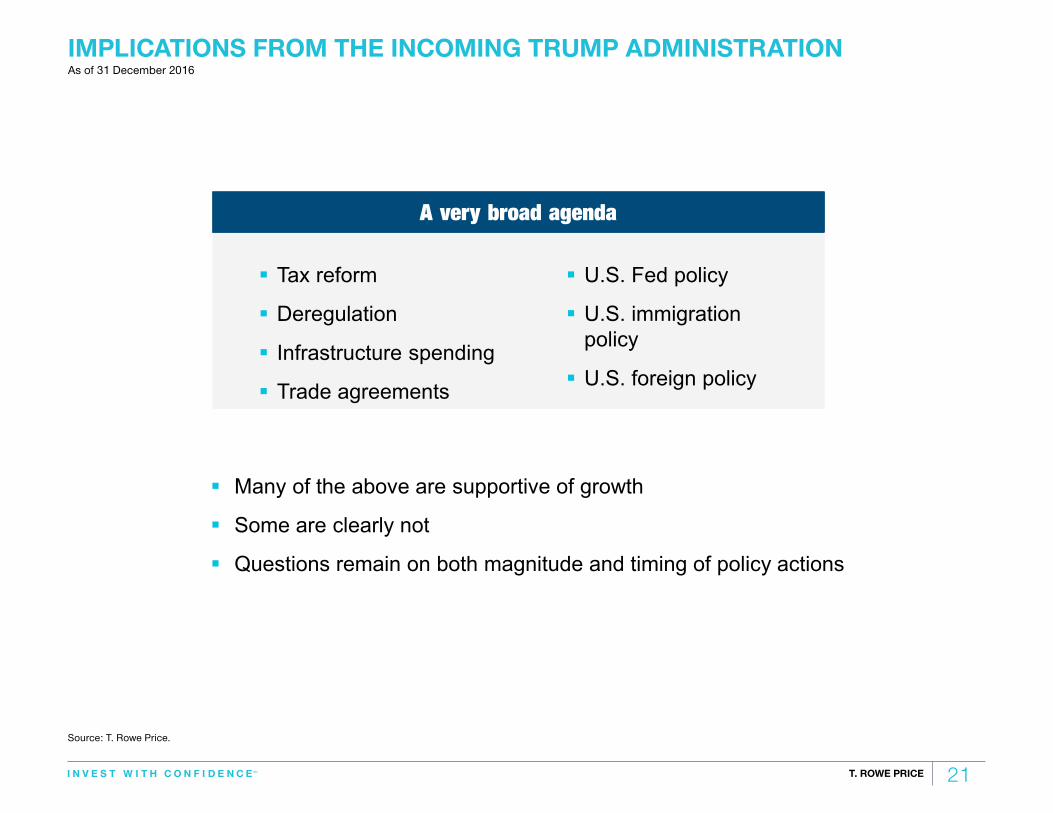

IMPLICATIONS FROM THE INCOMING TRUMP ADMINISTRATIONAs of 31 December 2016

Source: T. Rowe Price. 24

Implications from the Incoming Trump Administration

A very broad agenda

Tax reform

Deregulation

Infrastructure spending

Trade agreements

§ U.S. Fed policy

§ U.S. immigrationpolicy

§ U.S. foreign policy

Many of the above are supportive of growth

Some are clearly not

Questions remain on both magnitude and timing of policy actions

Sources: T Rowe Price

A very broad agenda

22T. ROWE PRICE

PERFORMANCE REVIEW

23T. ROWE PRICE

COMPLIANCE CERTIFICATE

24T. ROWE PRICE

COMPLIANCE CERTIFICATE

25 T. ROWE PRICE

PERFORMANCE SUMMARY AND MARKET UPDATEAs of 31 December 2016

2T. ROWE PRICE

I V. MARKET OUTLOOK

§ Modest U.S. economic growth should continue

§ Investors remain cautious amid global economic growth concerns

§ Quality, large-cap stocks off er solid risk/reward prospects

§ Equity valuations remain reasonable versus long-term averages

I. MARKET OVERVIEW

Fourth Quarter One YearS&P 500 Index 3.82% 11.96%Russell 1000 Growth Index 1.01 7.08Russell 1000 Value Index 6.68 17.34Nasdaq 1.34 7.50Russell 2000 Index 8.83 21.31

§ Large-cap stocks underperformed small-caps for the quarter

§ Growth stocks underperformed value stocks for the quarter

§ Global economic growth remains a key issue

I I. SECTOR PERFORMANCE RUSSELL 1000 GROWTH INDEX

Fourth QuarterTop Three Performers Bottom Three PerformersIndustrials & Business Services Real EstateFinancials Health CareTelecommunication Services Energy

One YearTop Three Performers Bottom Three PerformersTelecommunication Services Health CareEnergy Real Estate

Utilities Consumer Staples

V. MARKET OUTLOOK

§ Modest U.S. economic growth should continue

§ Investors remain cautious amid global economic growth concerns

§ Quality, large-cap stocks off er solid risk/reward prospects

§ Equity valuations remain reasonable versus long-term averages

As of December 31, 2016Figures are Calculated in U.S. Dollars

III. PORTFOLIO PERFORMANCE FOURTH QUARTER

Los Angeles Department of Water and Power Employees' Retirement Plan

Major Absolute Contributors Major Absolute Detractors

Morgan Stanley Amazon.com

American Airlines Facebook

Alaska Air Group Intuitive Surgical

Boeing Visa

UnitedHealth Group Workday

IV. PORTFOLIO PERFORMANCE ONE YEAR

Los Angeles Department of Water and Power Employees' Retirement Plan

Major Absolute Contributors Major Absolute Detractors

Applied Materials Alexion Pharmaceuticals

Morgan Stanley Vertex Pharmaceuticals

Amazon.com Regeneron Pharmaceuticals

UnitedHealth Group LinkedIn

Priceline Bristol-Myers Squibb

1T. ROWE PRICE

As of December 31, 2016Figures are Calculated in U.S. Dollars

I V. MARKET OUTLOOK

§ Modest U.S. economic growth should continue

§ Investors remain cautious amid global economic growth concerns

§ Quality, large-cap stocks off er solid risk/reward prospects

§ Equity valuations remain reasonable versus long-term averages

I. MARKET OVERVIEW

Fourth Quarter One YearS&P 500 Index 3.82% 11.96%Russell 1000 Growth Index 1.01 7.08Russell 1000 Value Index 6.68 17.34Nasdaq 1.34 7.50Russell 2000 Index 8.83 21.31

§ Large-cap stocks underperformed small-caps for the quarter

§ Growth stocks underperformed value stocks for the quarter

§ Global economic growth remains a key issue

I I. SECTOR PERFORMANCE S&P 500 INDEX

Fourth QuarterTop Three Performers Bottom Three PerformersFinancials Real EstateEnergy Health CareIndustrials & Business Services Consumer Staples

One YearTop Three Performers Bottom Three PerformersEnergy Real EstateTelecommunication Services Health Care

Financials Consumer Staples

V. MARKET OUTLOOK

§ Modest U.S. economic growth should continue

§ Investors remain cautious amid global economic growth concerns

§ Quality, large-cap stocks off er solid risk/reward prospects

§ Equity valuations remain reasonable versus long-term averages

(N) New holding.(E) Eliminated.

V. SIGNIFICANT TRADES FOURTH QUARTER

Los Angeles Department of Water and Power Employees' Retirement Plan

Major Purchases Major Sales

Home Depot (N) Lowe's

Red Hat (N) Danaher

Microsoft Hanesbrands (E)

Crown Castle International (N) Juniper Networks (E)

Philip Morris International Tractor Supply

Business Description sourced from Thomson Reuters Worldscope Fundamentals, Copyright©, Thomson Reuters, 1999–2017. All Rights Reserved.The specifi c securities identifi ed and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and no assumptions should be made that the securities identifi ed and discussed were or will be profi table.The information shown does not refl ect any exchange-traded funds that may be held in the portfolio.Numbers may not total due to rounding.

SA_CLIENT_TOPTEN Sep Accts with Client Performance Top Ten Holdings – Not Mutual Fund data

After updating please save EPS in: Groups/KitBP/TRP_Mtg Kits/TRP_ExbTRPGen/_EPS Footnotes as: SA_Client_TopTen

Past performance cannot guarantee future results.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

VI. MARKET OUTLOOK

26T. ROWE PRICE

TOTAL RETURN PERFORMANCELos Angeles Department of Water and Power Employees' Retirement PlanPeriods Ended 31 December 2016Figures are Calculated in U.S. Dollars

Business Description sourced from Thomson Reuters Worldscope Fundamentals, Copyright©, Thomson Reuters, 1999–2017. All Rights Reserved.The specifi c securities identifi ed and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and no assumptions should be made that the securities identifi ed and discussed were or will be profi table.The information shown does not refl ect any exchange-traded funds that may be held in the portfolio.Numbers may not total due to rounding.

SA_CLIENT_TOPTEN Sep Accts with Client Performance Top Ten Holdings – Not Mutual Fund data

After updating please save EPS in: Groups/KitBP/TRP_Mtg Kits/TRP_ExbTRPGen/_EPS Footnotes as: SA_Client_TopTen

Past performance cannot guarantee future results.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

Past performance cannot guarantee future results.1 Performance fi gures are shown gross of advisory fees. Total returns would be lower as a result of the deduction of such fees.2 Net returns refl ect the deduction of advisory fees. Source: T. Rowe Price Modifi ed Dietz Rate of Return. Total returns include all realized and unrealized gains and losses plus income. All investments are subject to risk, including the possible loss of the money you invest.

Calendar Years16 Apr 2010– 31 Dec 2010 2011 2012 2013 2014 2015 2016

Los Angeles Department of Water and Power Employees' Retirement Plan (Gross of Fees)1 4.83% -2.03% 19.91% 44.51% 9.26% 12.48% 5.27%

Los Angeles Department of Water and Power Employees' Retirement Plan (Net of Fees)2 4.59 -2.36 19.52 44.06 8.91 12.12 4.92

Russell 1000 Value Index 8.21 2.64 15.26 33.48 13.05 5.67 7.08

Value Added (Net of Fees)3 -3.62 -5.00 4.26 10.58 -4.14 6.45 -2.16

Annualized

ThreeMonths

One Year

Two Years

ThreeYears

Five Years

Since Client Inception

16 Apr 2010

Los Angeles Department of Water and Power Employees' Retirement Plan (Gross of Fees)1 2.35% 5.27% 8.82% 8.97% 17.52% 13.23%

Los Angeles Department of Water and Power Employees' Retirement Plan (Net of Fees)2 2.27 4.92 8.46 8.61 17.14 12.86

Russell 1000 Value Index 1.01 7.08 6.37 8.55 14.50 12.35

Value Added (Net of Fees)3 1.26 -2.16 2.09 0.06 2.64 0.51

3 Value Added is shown as Los Angeles Department of Water and Power Employees' Retirement Plan (Net of Fees) minus Russell 1000 Growth Index.

27T. ROWE PRICE

Annualized

Quarter-to-Date

One Year

Two Years

ThreeYears

Five Years

Since ClientInception

16 Apr 2010

Los Angeles Department of Water and Power Employees' Retirement Plan (Gross of Fees)1 8.63% 28.13% 10.11% 10.08% 16.32% 14.27%

Los Angeles Department of Water and Power Employees' Retirement Plan (Net of Fees)2 8.58 27.72 9.75 9.72 15.95 13.90

Russell 1000 Value Index 7.66 22.15 7.69 10.47 13.79 13.26

Value Added (Net of Fees)3 0.92 5.57 2.06 -0.75 2.16 0.64

TOTAL RETURN PERFORMANCELos Angeles Department of Water and Power Employees' Retirement PlanPeriods Ended 28 February 2017 Figures are Calculated in U.S. Dollars

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

Past performance cannot guarantee future results.1 Performance fi gures are shown gross of advisory fees. Total returns would be lower as a result of the deduction of such fees.2 Net returns refl ect the deduction of advisory fees. Source: T. Rowe Price Modifi ed Dietz Rate of Return. Total returns include all realized and unrealized gains and losses plus income. All investments are subject to risk, including the possible loss of the money you invest.3 Value Added is shown as Los Angeles Department of Water and Power Employees' Retirement Plan (Net of Fees) minus Russell 1000 Growth Index.

28 T. ROWE PRICE

Footnote Nimbus Sans Novus Condensed 10/10

ATTRIBUTION ANALYSISLA Dept of Water and Power Employees Retirement Plan - LCG vs. Russell 1000 Growth Index3 Months Ended 31 December 2016Figures Shown in U.S. Dollar

Total Value Added

Value Added FromSector Weight

Value Added FromStock Selection

N

Numbers may not add to 100% due to rounding; all numbers are percentages.Note: Analysis represents the equity-only performance of the portfolio as calculated by the Wilshire Atlas attribution model and is exclusive of cash, trusts, mutual funds, delisted securities, and other non-equity holdings. Returns will not match official T. Rowe Price performance because Wilshire uses different pricing and exchange rate sources and does not capture intraday trading or fair-value pricing.Performance for each security is obtained in the local currency and, if necessary, is converted using an exchange rate determined by an independent third party. Source: Wilshire Atlas, MSCI/S&P Global Industry Classification Standard (GICS) sectors; Analysis by T. Rowe Price Associates, Inc. T. Rowe Price uses the MSCI/S&P GICS for sector and industry reporting.Each year, MSCI and S&P make changes to the GICS structure. The last change occurred on 31 August 2016. T. Rowe Price will adhere to all future updates to GICS for prospective reporting. Figures areshown gross of fees. Past performance cannot guarantee future results.

BY SECTOR (TOP AND BOTTOM FIVE BY TOTAL VALUE ADDED)

TotalIndustrials &

Bus Svcs FinancialsHealth Care

Real Estate

Telecom Svcs

Consumer Staples Materials Energy Utilities

Consumer Disc

Information Technology

Over (Under) Weight -- -1.13 5.82 3.26 -2.05 -0.20 -7.64 -2.75 -0.63 -0.03 4.86 0.49

Portfolio Weight (Ending) 100.00 9.93 8.71 19.36 0.61 1.06 1.82 0.86 0.00 0.00 25.59 32.07

Index Weight (Ending) 100.00 11.06 2.88 16.10 2.66 1.26 9.46 3.61 0.63 0.03 20.73 31.57

Portfolio Performance 2.32 20.71 19.98 0.43 7.00 23.10 -1.26 10.21 0.00 0.00 -0.60 -3.37

Index Performance 1.01 6.88 6.68 -3.48 -5.28 4.55 -0.51 2.09 -0.89 3.69 2.10 1.06

Footnote Nimbus Sans Novus Condensed 10/10

ATTRIBUTION ANALYSIS (USD)Los Angeles Department of Water and Power Employees' Retirement Plan vs. Russell 1000 Growth IndexThree Months Ended 31 December 2016

Past performance cannot guarantee future results. Numbers may not add to 100% due to rounding; all numbers are percentages. Analysis represents the equity-only performance of the portfolio as calculated by the Wilshire Atlas attribution model and is exclusive of cash, trusts, mutual funds, delisted securities, and other non-equity holdings. Returns will not match offi cial T. Rowe Price performance because Wilshire uses diff erent pricing and exchange rate sources and does not capture intraday trading or fair-value pricing. Performance for each security is obtained in the local currency and, if necessary, is converted using an exchange rate determined by an independent third party.Source: Wilshire Atlas, MSCI/S&P Global Industry Classifi cation Standard (GICS) sectors; analysis by T. Rowe Price Associates, Inc. T. Rowe Price uses the MSCI/S&P GICS for sector and industry reporting. Each year, MSCI and S&P review the GICS structure. The last change occurred on 31 August 2016. T. Rowe Price will adhere to all future updates to GICS for prospective reporting.Figures are shown gross of fees.Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

29T. ROWE PRICE

KEY THREE MONTH PERFORMANCE DRIVERSThree Months Ended 31 December 2016

CONTRIBUTORS § Industrials & Business Services

§ Shares of American Airlines rallied sharply in the fourth quarter on expectations that more disciplined industry capacity growth should drive improved results. The stock benefited from mid-quarter news that Warren Buffett’s Berkshire Hathaway had accumulated shares in the company. Better than expected traffic numbers coupled with management’s raised guidance for fourth quarter revenue growth propelled the stock higher. Restrained capacity growth and improved traffic also benefited our position in Alaska Air Group.

§ Financials

§ Shares of Morgan Stanley, TD Ameritrade Holding, and State Street traded higher along with the broader financials sector during the fourth quarter. In addition to tailwinds from higher interest rates, FICC (Fixed Income, Currencies, and Commodities) activity—a key profit driver for the brokerages—continued to improve. Following the election, asset managers rallied based on expectations that the Department of Justice’s fiduciary rule could be rolled back under the incoming administration.

DETRACTORS § Information Technology

§ While Facebook reported another strong and better than consensus quarter, the stock traded lower on comments from management that 2017 would be a year of aggressive investment for the company. Also, like many internet-related names, the stock has lagged since the election as investors rotated into other segments of the market deemed to see the greatest benefits from potential policy changes.

§ Consumer Discretionary

§ Shares of Amazon.com traded lower following its latest quarterly report, as gross profits and management guidance came in lower than expected. Investors reacted negatively to higher year-over-year costs related to the build-out of its third-party distribution business. However, these non-recurring expenses are supported by the fact that growth is accelerating at Amazon’s fulfillment business, where margins are much higher than in its base retail operations. Margins for Amazon Web Services, which continues to grow at an impressive rate, also recently reached all-time highs.

§ Priceline reported another quarter of solid results, with strong growth across all geographies and channels. Key metrics, including bookings growth, gross profits, and earnings all came in ahead of consensus expectations and previous guidance. Despite the company’s healthy fundamentals the stock was roughly flat for the quarter after it sold-off along with other internet-related names as investors rotated into cyclicals and interest-rate sensitive stocks following the election.

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for clients in the portfolio and no assumptions should be made that the securities identified and discussed were or will be profitable.

30 T. ROWE PRICE

Footnote Nimbus Sans Novus Condensed 10/10

ATTRIBUTION ANALYSISLA Dept of Water and Power Employees Retirement Plan - LCG vs. Russell 1000 Growth Index1 Year Ended 31 December 2016Figures Shown in U.S. Dollar

Total Value Added

Value Added FromSector Weight

Value Added FromStock Selection

N

Numbers may not add to 100% due to rounding; all numbers are percentages.Note: Analysis represents the equity-only performance of the portfolio as calculated by the Wilshire Atlas attribution model and is exclusive of cash, trusts, mutual funds, delisted securities, and other non-equity holdings. Returns will not match official T. Rowe Price performance because Wilshire uses different pricing and exchange rate sources and does not capture intraday trading or fair-value pricing.Performance for each security is obtained in the local currency and, if necessary, is converted using an exchange rate determined by an independent third party. Source: Wilshire Atlas, MSCI/S&P Global Industry Classification Standard (GICS) sectors; Analysis by T. Rowe Price Associates, Inc. T. Rowe Price uses the MSCI/S&P GICS for sector and industry reporting.Each year, MSCI and S&P make changes to the GICS structure. The last change occurred on 31 August 2016. T. Rowe Price will adhere to all future updates to GICS for prospective reporting. Figures areshown gross of fees. Past performance cannot guarantee future results.

BY SECTOR (TOP AND BOTTOM FIVE BY TOTAL VALUE ADDED)

Total FinancialsReal Estate

Industrials &Bus Svcs

Consumer Disc

Consumer Staples Materials Utilities Energy

Telecom Svcs

Information Technology

Health Care

Over (Under) Weight -- 5.82 -2.05 -1.13 4.86 -7.64 -2.75 -0.03 -0.63 -0.20 0.49 3.26

Portfolio Weight (Ending) 100.00 8.71 0.61 9.93 25.59 1.82 0.86 0.00 0.00 1.06 32.07 19.36

Index Weight (Ending) 100.00 2.88 2.66 11.06 20.73 9.46 3.61 0.03 0.63 1.26 31.57 16.10

Portfolio Performance 5.20 26.95 7.00 24.26 6.59 15.27 32.70 0.00 0.00 47.01 5.75 -9.94

Index Performance 7.07 14.26 -6.66 15.66 6.19 3.79 11.14 17.97 22.97 23.46 11.17 -6.80

Footnote Nimbus Sans Novus Condensed 10/10

ATTRIBUTION ANALYSIS (USD)Los Angeles Department of Water and Power Employees' Retirement Plan vs. Russell 1000 Growth IndexOne Year Ended 31 December 2016

Past performance cannot guarantee future results. Numbers may not add to 100% due to rounding; all numbers are percentages. Analysis represents the equity-only performance of the portfolio as calculated by the Wilshire Atlas attribution model and is exclusive of cash, trusts, mutual funds, delisted securities, and other non-equity holdings. Returns will not match offi cial T. Rowe Price performance because Wilshire uses diff erent pricing and exchange rate sources and does not capture intraday trading or fair-value pricing. Performance for each security is obtained in the local currency and, if necessary, is converted using an exchange rate determined by an independent third party.Source: Wilshire Atlas, MSCI/S&P Global Industry Classifi cation Standard (GICS) sectors; analysis by T. Rowe Price Associates, Inc. T. Rowe Price uses the MSCI/S&P GICS for sector and industry reporting. Each year, MSCI and S&P review the GICS structure. The last change occurred on 31 August 2016. T. Rowe Price will adhere to all future updates to GICS for prospective reporting.Figures are shown gross of fees.Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

31T. ROWE PRICE

KEY ONE YEAR PERFORMANCE DRIVERSOne Year Ended 31 December 2016

CONTRIBUTORS § Financials

§ Shares of global investment bank Morgan Stanley rose sharply in the second half of the year along with the broader financials sector. The outcome of the U.S. presidential election led to a more favorable outlook for financials in light of expectations for reduced regulations, lower corporate taxes, and rising interest rates and inflation. Fundamentals have also improved, with a strong recovery in FICC (Fixed Income, Currencies, and Commodities) activity signaling that the underlying business has found its footing. Our position in TD Ameritrade Holding also benefited from the aforementioned tailwinds in the sector.

§ Consumer Discretionary

§ Despite a broader slowdown in travel trends, Priceline continued to deliver strong bookings growth by taking market share from its competition. The company’s international expansion and its move into non-hotel properties also present attractive opportunities for continued long term growth.

§ Shares of MGM Resorts International rose on reports that gambling traffic in Macau is beginning to recover after a significant slowdown in 2015. In our view, the firm is also well positioned to benefit from a deleveraging of its balance sheet via the formation of MGM Growth Properties, a real estate investment trust (REIT) designed to invest in various properties.

DETRACTORS § Health Care

§ Alexion Pharmaceuticals issued softer than expected guidance in the first quarter and later announced disappointing results from a phase III clinical trial that led to a sharp decline in the second quarter. The stock saw further volatility late in the year after delaying the filing of its quarterly financial statements and removing the CEO and CFO. Its financials have since been filed, without issue, and a new management team has been brought on board.

§ Shares of Allergan declined early on in the year when its proposed merger with Pfizer was called off after the U.S. Treasury Department issued a notice aimed at curbing the benefits of tax inversions. While we still maintain a constructive view, we subsequently trimmed our position and continue to monitor competitive pressures on the company’s dominant eye care business.

§ Information Technology

§ LinkedIn provided disappointing 2016 guidance early in the year that sent shares sharply lower. While we thought that LinkedIn’s core Talent Solutions business was a high quality asset, we had a few areas of concern including the company’s acquisition strategy, the size of its addressable market, and the impact that its planned investments would have on cash flows. We eliminated the stock in the first quarter and had begun to unwind our position before Microsoft’s takeover announcement.

§ Our overweight exposure to salesforce.com detracted from relative returns in the latter half of 2016, largely in response to a lack of clarity surrounding the company’s acquisition strategy. Sentiment further weighed on the stock following its failed pursuit of acquiring LinkedIn, rumors of the CEO’s interest in acquiring Twitter, and a leaked presentation highlighting numerous potential acquisition targets.

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for clients in the portfolio and no assumptions should be made that the securities identified and discussed were or will be profitable.

32T. ROWE PRICE

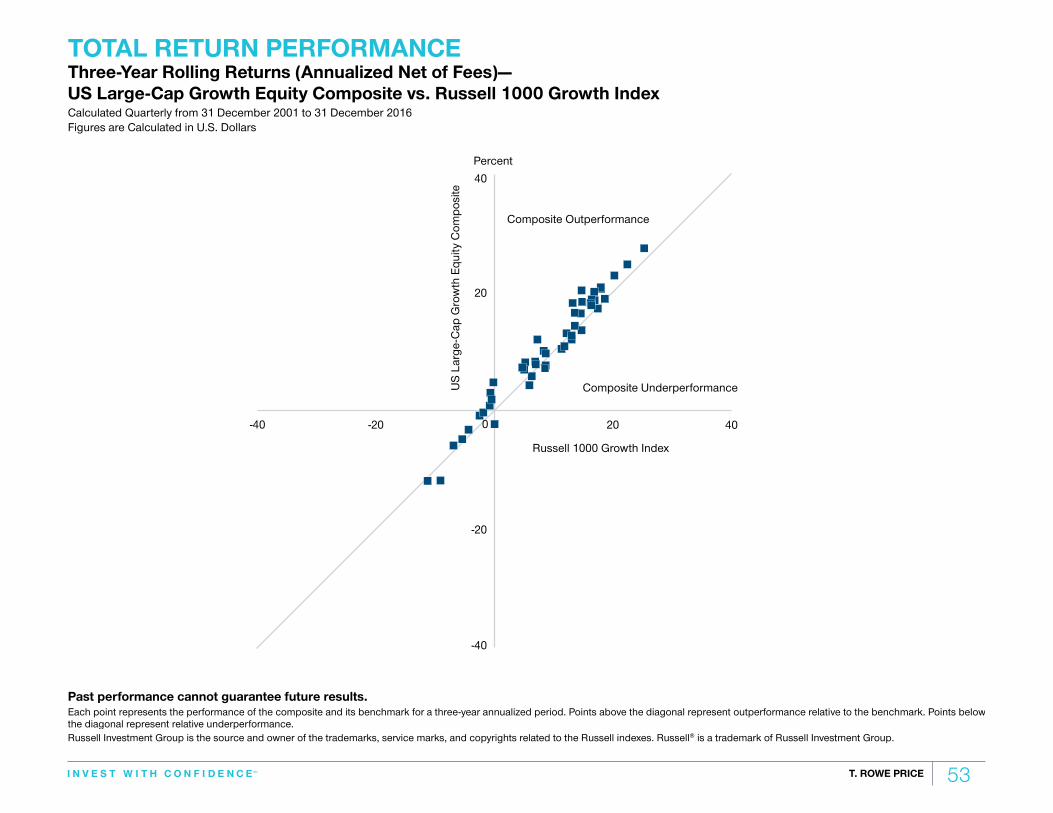

Past performance cannot guarantee future results. Each point represents the performance of the portfolio and its benchmark for a three-year annualized period. Points above the diagonal represent outperformance relative to the benchmark. Points below the diagonal represent relative underperformance. Figures shown gross of fees. Returns would have been lower as the result of the deduction of applicable fees.

TOTAL RETURN PERFORMANCEThree-Year Rolling Returns (Annualized Net of Fees)— Los Angeles Department of Water and Power Employees' Retirement Plan vs. Russell 1000 Growth IndexCalculated Quarterly from 30 June 20101 to 31 December 2016Figures are Calculated in U.S. Dollars

Percent

Portfolio Outperformance

Portfolio Underperformance

Los

Ang

eles

Dep

artm

ent o

f Wat

er

and

Pow

er E

mpl

oyee

s’ R

etire

men

t Pla

nRussell 1000 Growth Index

-40 -30 -20 -10

0

10 20 30 40

-40

-30

-20

-10

0

10

20

30

40

5334

1 Client inception date 16 April 2010.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

Past performance cannot guarantee future results. Each point represents the performance of the portfolio and its benchmark for a three-year annualized period. Points above the diagonal represent outperformance relative to the benchmark. Points below the diagonal represent relative underperformance. Figures shown gross of fees. Returns would have been lower as the result of the deduction of applicable fees.

33T. ROWE PRICE

Past performance cannot guarantee future results. This information demonstrates, in part, the fi rm’s Risk/Return analysis. This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.Statistics based on monthly gross returns. Returns would have been lower as the result of the deduction of applicable fees.Supplemental information.

1 30 April 2010. Actual client inception date is 16 April 2010.

TOTAL RETURN PERFORMANCERisk/Return CharacteristicsSince Inception1 Through 31 December 2016Figures are Calculated in U.S. Dollars

Since Inception1

Los Angeles Department of Water

and Power Employees' Retirement Plan

Russell 1000 Growth Index

Annualized Total Return 13.70% 12.76%

Annualized Standard Deviation 15.38% 13.07%

Historical Tracking Error 4.78% 0.00%

Beta 1.13 1.00

R-Squared 0.92 1.00

Alpha -0.45% 0.00%

Sharpe Ratio 0.88 0.96

Information Ratio 0.20 0.00

Russell 1000Growth Index

Los Angeles Department of Water and Power Employees’ Retirement Plan

Average Annual Standard Deviation (%)

Aver

age

Annu

al R

etur

n (%

)

The bottom axis will move whenthe graph is updated. You must realign to the guide. Sorry :(

The square around the graph is artwork

DO NOT ADJUST.

8 15 2210

13

16

r1000 Growth Index

LCGC

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

Past performance cannot guarantee future results.

34T. ROWE PRICE

PORTFOLIO REVIEW AND CHARACTERISTICS

35T. ROWE PRICE

Footnote Nimbus Sans Novus Condensed 10/10

1 Source: IBES. The specifi c securities identifi ed and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and no assumptions should be made that the securities identifi ed

and discussed were or will be profi table. The information shown does not refl ect any exchange-traded funds that may be held in the portfolio. Numbers may not total due to rounding. Statistics are investment-weighted median unless otherwise noted.

PORTFOLIO SNAPSHOTAs of 31 December 2016

SECTOR WEIGHTINGS

-15

0

15

30

45dif

Rus

LADWP

UtilitiesTelecomSvcs

Real Estate

MaterialsInfoTech

Indust &Bus Svcs

HealthCare

FinancialsEnergyConsumStpls

ConsumDisc

Percent

Russell 1000 Growth IndexOver/Underweighting

Los Angeles Department of Water and Power Employees’ Retirement Plan

Los Angeles Department of Water andPower Employees' Retirement Plan Russell 1000 Growth Index

Projected Earnings Growth Rate1 15.7% 10.8%

Price to Earnings (12 Months Forward)1 21.3X 20.0X

Investment-Weighted Average Market Capitalization (Millions USD) 155,198 154,034

Number of Holdings 65 595

20 Largest Holdings 62.7% 37.7%

Portfolio Turnover (Last 12 Months) 40.1% N/A

Active Share 68.1% N/A

Company % of Portfolio

Amazon.com 8.5%

Alphabet 6.7

Priceline 5.2

Facebook 4.9

Visa 3.9

Microsoft 3.9

Qualcomm 3.1

Boeing 2.8

Morgan Stanley 2.7

UnitedHealth Group 2.5

Total 44.2%

TOP 10 HOLDINGS

PORTFOLIO CHARACTERISTICS

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

Active Share is a holdings-based measure of active management representing the percentage of a portfolio’s holdings that diff er from those in its benchmark. Compared with tracking error, which measures the standard deviation of the diff erence in a manager’s returns versus the index returns, Active Share allows investors to get a clearer understanding of what a manager is doing to drive performance, rather than drawing conclusions from observed returns. The greater the diff erence between the asset composition of a product and its benchmark, the greater the active share is.

T. Rowe Price uses the MSCI/S&P Global Industry Classifi cation Standard (GICS) for sector and industry reporting. Each year, MSCI and S&P review the GICS structure. The last change occurred on31 August 2016. T. Rowe Price will adhere to all future updates to GICS for prospective reporting.

1 Source: IBES. The specifi c securities identifi ed and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and no assumptions should be made that the securities identifi ed

and discussed were or will be profi table. The information shown does not refl ect any exchange-traded funds that may be held in the portfolio. Numbers may not total due to rounding. Statistics are investment-weighted median unless otherwise noted.

36T. ROWE PRICE

Business Description sourced from Thomson Reuters Worldscope Fundamentals, Copyright©, Thomson Reuters, 1999–2017. All Rights Reserved.The specifi c securities identifi ed and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and no assumptions should be made that the securities identifi ed and discussed were or will be profi table.The information shown does not refl ect any exchange-traded funds that may be held in the portfolio.Numbers may not total due to rounding.

SA_CLIENT_TOPTEN Sep Accts with Client Performance Top Ten Holdings – Not Mutual Fund data

After updating please save EPS in: Groups/KitBP/TRP_Mtg Kits/TRP_ExbTRPGen/_EPS Footnotes as: SA_Client_TopTen

10 LARGEST OVER/UNDERWEIGHTSLos Angeles Department of Water and Power Employees' Retirement Plan Relative to the Russell 1000 Growth IndexAs of 31 December 2016

10 Largest Overweights % of Portfolio

% of Index Difference

Amazon.com 8.5% 2.8% 5.7%

Priceline 5.2 0.7 4.6

Qualcomm 3.1 0.2 2.9

Morgan Stanley 2.7 0.0 2.7

Facebook 4.9 2.5 2.5

Visa 3.9 1.4 2.5

Alphabet 6.7 4.4 2.3

American Airlines 2.2 0.0 2.2

MGM Resorts International 2.1 0.0 2.1

Danaher 2.1 0.1 2.0

10 Largest Underweights % of Portfolio

% of Index Difference

Apple 1.1% 5.5% -4.4%

Walt Disney 0.0 1.6 -1.6

Comcast 0.0 1.5 -1.5

Altria Group 0.0 1.3 -1.3

PepsiCo 0.0 1.2 -1.2

Coca-Cola 0.0 1.1 -1.1

Amgen 0.0 1.0 -1.0

Verizon Communications 0.0 1.0 -1.0

3M 0.0 1.0 -1.0

AbbVie 0.0 1.0 -1.0

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

37T. ROWE PRICE

RECENT PORTFOLIO CHANGESLos Angeles Department of Water and Power Employees' Retirement Plan Three Months Ended 31 December 2016

Major Purchases% of

Portfolio Business DescriptionHome Depot1 0.9% Home Depot is a home improvement retailer.

Red Hat1 0.8 Red Hat provides open source software solutions, using a community-powered approach to develop and offer operating system, virtualization, management, middleware, cloud, mobile and storage technologies.

Microsoft 3.9 Microsoft is a technology company. The Company develops, licenses, and supports a range of software products, services and devices.

Crown Castle International1 0.6 Crown Castle International is a real estate investment trust.Phlip Morris International 1.1 Philip Morris International is a holding company engaged in the manufacture and sale of cigarettes, other tobacco products

and other nicotine-containing products in markets outside of the United States.

Major Sales% of

Portfolio Business DescriptionLowe's 0.4% Lowe's is a home improvement retailer. Danaher 2.1 Danaher designs, manufactures and markets professional, medical, industrial and commercial products and services.Hanesbrands2 0.0 Hanesbrands is a marketer of basic innerwear and activewear apparel in the Americas, Europe, Australia and Asia/Pacific

under apparel brands, such as Hanes, Champion, Maidenform, DIM, Bali, Playtex, Bonds, JMS/Just My Size, Nur Die/Nur Der, L'eggs, Lovable, Wonderbra, Flexees, Gear for Sports and Berlei.

Juniper Networks2 0.0 Juniper Networks designs, develops and sells products and services for high-performance networks to enable customers to build networks for their businesses.

Tractor Supply 0.8 Tractor Supply is an operator of rural lifestyle retail stores in the United States.

Business Description sourced from Thomson Reuters Worldscope Fundamentals, Copyright©, Thomson Reuters, 1999–2017. All Rights Reserved.The specifi c securities identifi ed and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and no assumptions should be made that the securities identifi ed and discussed were or will be profi table.The information shown does not refl ect any exchange-traded funds that may be held in the portfolio.Numbers may not total due to rounding.

SA_CLIENT_TOPTEN Sep Accts with Client Performance Top Ten Holdings – Not Mutual Fund data

After updating please save EPS in: Groups/KitBP/TRP_Mtg Kits/TRP_ExbTRPGen/_EPS Footnotes as: SA_Client_TopTen

1 New Holding. 2 Eliminated.

38 T. ROWE PRICE

PORTFOLIO BY MARKET CAPITALIZATIONLos Angeles Department of Water and Power Employees' Retirement Plan As of 31 December 2016

0–10 Billion USD 2%

10–25 Billion USD 20%

25–50 Billion USD 21%

50+ Billion USD 57%

CenteneTractor Supply

Alaska Air GroupAmerican AirlinesCitizens FinancialDollar GeneralFirst Republic BankFortiveHilton Worldwide HoldingsIlluminaIncyteIntuitive SurgicalMGM Resorts InternationalPalo Alto NetworksRed HatServiceNowTD Ameritrade HoldingTextronVertex PharmaceuticalsVulcan MaterialsWorkdayYum! Brands

AetnaAlexion PharmaceuticalsAnthemCignaCME GroupCrown Castle InternationalFedExHumanaIntercontinental ExchangeIntuitO'Reilly AutomotivePayPal HoldingsRoss StoresSalesforce.comState StreetStrykerTeslaT-Mobile US

AlphabetAmazon.comAppleBiogenBoeingBristol-Myers SquibbCelgeneCostco WholesaleDanaherFacebookHome DepotLowe'sMerckMicrosoftMorgan StanleyNetflixNVIDIAPhilip Morris InternationalPricelineQualcommStarbucksUnitedHealth GroupVisa

Business Description sourced from Thomson Reuters Worldscope Fundamentals, Copyright©, Thomson Reuters, 1999–2017. All Rights Reserved.The specifi c securities identifi ed and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and no assumptions should be made that the securities identifi ed and discussed were or will be profi table.The information shown does not refl ect any exchange-traded funds that may be held in the portfolio.Numbers may not total due to rounding.

SA_CLIENT_TOPTEN Sep Accts with Client Performance Top Ten Holdings – Not Mutual Fund data

After updating please save EPS in: Groups/KitBP/TRP_Mtg Kits/TRP_ExbTRPGen/_EPS Footnotes as: SA_Client_TopTen

The securities mentioned above represent 100% of the publicly traded common equity securities held by the portfolio.

39T. ROWE PRICE

MARKET CAPITALIZATION RANGELos Angeles Department of Water and Power Employees' Retirement Plan As of 31 December 2016

0

12

24

36

48

60

Russell 1000 Growth

4950

50+25–5010–250–10

Percent

Russell 1000 Growth IndexLos Angeles Department of Water and Power Employees’ Retirement Plan

Billions USD

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell indexes. Russell® is a trademark of Russell Investment Group.

40T. ROWE PRICE

FULL PORTFOLIO HOLDINGSLos Angeles Department of Water and Power Employees' Retirement Plan As of 31 December 2016

Rounding may cause figures to vary from 100.00%.

As of December 31, 2016Portfolio Holdings

Security Name %Assets+Accrd

CONSUMER DISCRETIONARY 25.24 %

Automobiles 1.40 %

TSLA Tesla 1.40

Hotels Restaurants & Leisure 4.34 %

HGV Hilton Grand Vacations 0.09

MGM MGM Resorts International 2.13

SBUX Starbucks 0.67

TC551OBB Hilton Worldwide Holdings 1.04

YUM Yum! Brands 0.42

Internet & Direct Marketing Retail 14.72 %

AMZN Amazon.com 8.48

NFLX Netflix 0.99

PCLN Priceline 5.25

Multiline Retail 1.30 %

DG Dollar General 1.30

Specialty Retail 3.48 %

Security Name %Assets+Accrd

HD Home Depot 0.93

LOW Lowe's 0.39

ORLY O'Reilly Automotive 0.57

ROST Ross Stores 0.76

TSCO Tractor Supply 0.82

CONSUMER STAPLES 1.78 %

Food & Staples Retailing 0.69 %

COST Costco Wholesale 0.69

Tobacco 1.09 %

PM Philip Morris International 1.09

FINANCIALS 8.51 %

Banks 0.67 %

CFG Citizens Financial 0.48

FRC First Republic Bank 0.20

Capital Markets 7.84 %

AMTD TD Ameritrade Holding 1.56

Rounding may cause figures to vary from 100.00%.

41T. ROWE PRICE

FULL PORTFOLIO HOLDINGSLos Angeles Department of Water and Power Employees' Retirement Plan As of 31 December 2016

Rounding may cause figures to vary from 100.00%.

As of December 31, 2016Portfolio Holdings

Security Name %Assets+Accrd

CME CME Group 0.71

ICE Intercontinental Exchange 1.47

MS Morgan Stanley 2.71

STT State Street 1.38

HEALTH CARE 18.92 %

Biotechnology 4.81 %

ALXN Alexion Pharmaceuticals 1.53

BIIB Biogen 1.15

CELG Celgene 0.91

INCY Incyte 0.27

VRTX Vertex Pharmaceuticals 0.95

Health Care Equipment & Supplies 5.36 %

DHR Danaher 2.08

ISRG Intuitive Surgical 2.06

SYK Stryker 1.22

Health Care Providers & Services 6.95 %

AET Aetna 1.02

ANTM Anthem 0.52

Security Name %Assets+Accrd

CI Cigna 0.82

CNC Centene 0.70

HUM Humana 1.42