valuation basics part 1 -...

TRANSCRIPT

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Valuation Basics – Part 1

June 5, 2018

Valuation and Financial Statement AnalysisPeking University Guanghua School of Management

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

My Background

• My writing and speaking are on Chinese consumers and

digital China.

• #1 LinkedIn Top Voice for Finance for 2017

• Named one of 15 Global Influencers by Alibaba in 2017

• Most followed Professor in China? 2.6M Followers

• Do healthcare PE deals and M&A advisory in the US and

Asia.

• Teach at Peking University, CEIBS and others.

• MBA from Columbia, MD from Stanford, BA in Physics.

• Based in Beijing and New York.

1

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

22

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

3

• Valuation Basics 25 min

• Exercise 20 min

• Break - 15 min

• Asset Values and EPV 45 min

www.jeffreytowson.com

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Big Disclaimer and Attribution

A lot of this information is drawn from the work of:

• McKinsey & Co. Especially their book Valuation: Measuring and Managing the Valuation of Companies.

• Aswath Damodaran, NYU Professor and Valuation guru. He has many books on this subject.

• Several master investors.• Seth Klarman – special situations• Charlie Munger – great companies• Carl Icahn – problematic companies• Warren Buffett

A lot of these slides is me presenting and / or summarizing the work of others. I have tried to give attribution as much as possible.

4

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

5

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

It Starts With Ben Graham: Price is Not

Value• The economic or intrinsic valuation of a company or asset is based

upon its fundamentals (i.e., its intrinsic characteristics).

• Value is different than what someone would pay for it. Or what its price is on any market.

• Value investing per Ben Graham / Warren Buffett / Seth Klarman is based on this separation of economic / intrinsic value and price. Hence “value investing.”

• This separation was Ben Graham’s big insight in the 1920’s.

• By buying with a gap between value and price, you get a “margin of safety”

• This was the first real scientific approach to valuation. The company is worth something regardless of anyone’s opinion. You can study it.

• It offered a much needed alternative to speculation.

6

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

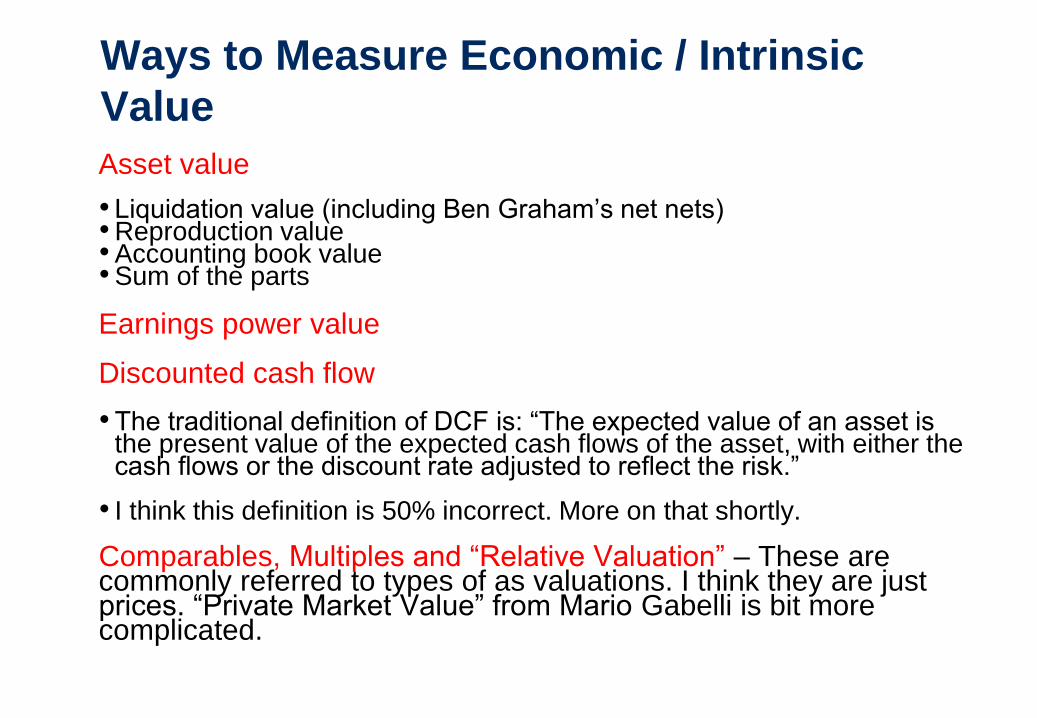

Ways to Measure Economic / Intrinsic

Value

Asset value

• Liquidation value (including Ben Graham’s net nets)• Reproduction value• Accounting book value• Sum of the parts

Earnings power value

Discounted cash flow

• The traditional definition of DCF is: “The expected value of an asset is the present value of the expected cash flows of the asset, with either the cash flows or the discount rate adjusted to reflect the risk.”

• I think this definition is 50% incorrect. More on that shortly.

Comparables, Multiples and “Relative Valuation” – These are commonly referred to types of as valuations. I think they are just prices. “Private Market Value” from Mario Gabelli is bit more complicated.

7

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Asset Value: What You Spend, Build or

Acquire

Think buying a factory, building a hotel or getting a college degree.

The assets that constitute your business can be assessed for their value.

•Some assets can be bought (land).

•Some can be built (a factory, software).

•Some accumulate naturally (brand equity, customers, knowledge).

• It is important to note that some asset values depreciate over time (a factory). But others can appreciate (customer loyalty and brand equity). And some can change unpredictably (real estate).

•Some are impacted by inflation over time. Some not.

8

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

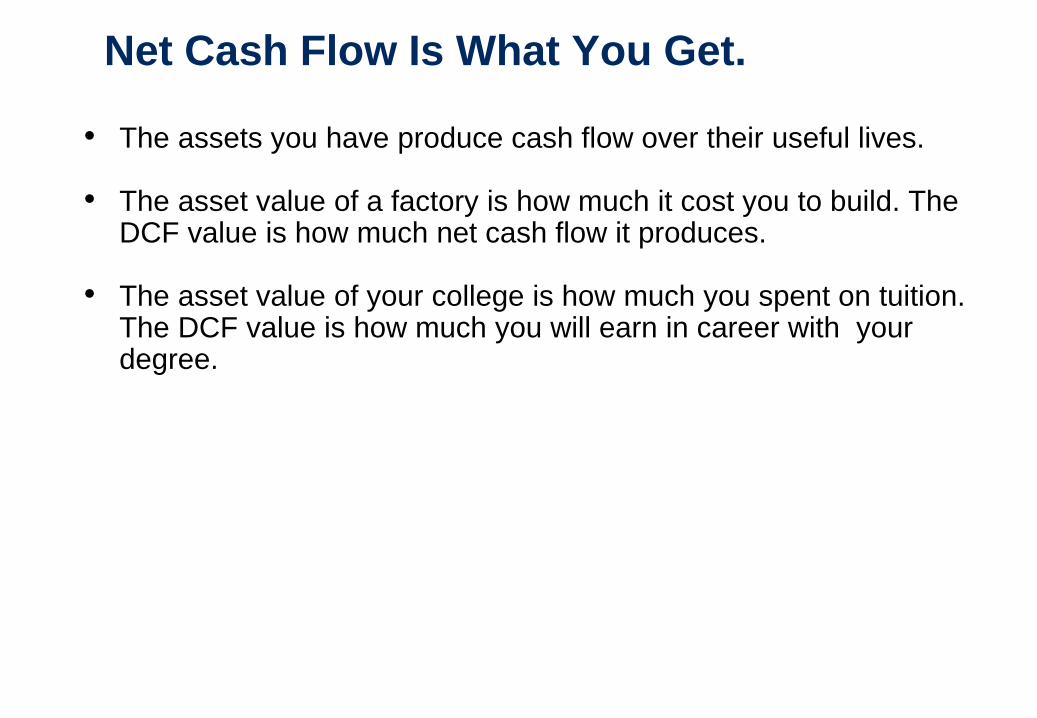

Net Cash Flow Is What You Get.

• The assets you have produce cash flow over their useful lives.

• The asset value of a factory is how much it cost you to build. The DCF value is how much net cash flow it produces.

• The asset value of your college is how much you spent on tuition. The DCF value is how much you will earn in career with your degree.

9

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Discounted Cash Flow Is the Most

Accurate Definition for Value

• The traditional definition of DCF is: “The expected value of an asset is the present value of the expected cash flows of the asset, with either the cash flows or the discount rate adjusted to reflect the risk.”

• My definitions of DCF is:

• “The true economic (or intrinsic) value is the expected cash flows of the assets over its lifetime and the uncertainty in those cash flows.

• My view: You cannot put a number on the risk of future cash flow. Don’t try and don’t pollute your calculations with made up discount factors. Think about the uncertainties your calculations, which can be measured.

• The most useful economic (or intrinsic) value as a projection of cash flows of the assets over their lifetime for a specific scenario.

10

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Other Discounted Cash Flow Stuff

•These cash flows can be from operating assets or financial assets. This is an important distinction.

• I prefer to isolate and focus on the operating assets (and operating liabilities)

•But in both cases, we are taking about productive assets.

•How would you value non-productive assets? Can you use net cash flow?

–Gold?

–Bitcoin?

–Real estate?

11

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Damodaran Says There Are Two Types of

Discounted Cash Flow Valuations

•For cash flow generating assets, the intrinsic value will be a function of the magnitude of the expected cash flows on the asset over its lifetime and the uncertainty about receiving those cash flows.

•The value of a risky asset can be estimated by discounting the expected cash flows on the asset over its life at a risk-adjusted discount rate:

where the asset has an n-year life, E(CFt) is the expected cash

flow in period t and r is a discount rate that reflects the risk of the

cash flows.

12Slide text mostly by A Damodaran

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

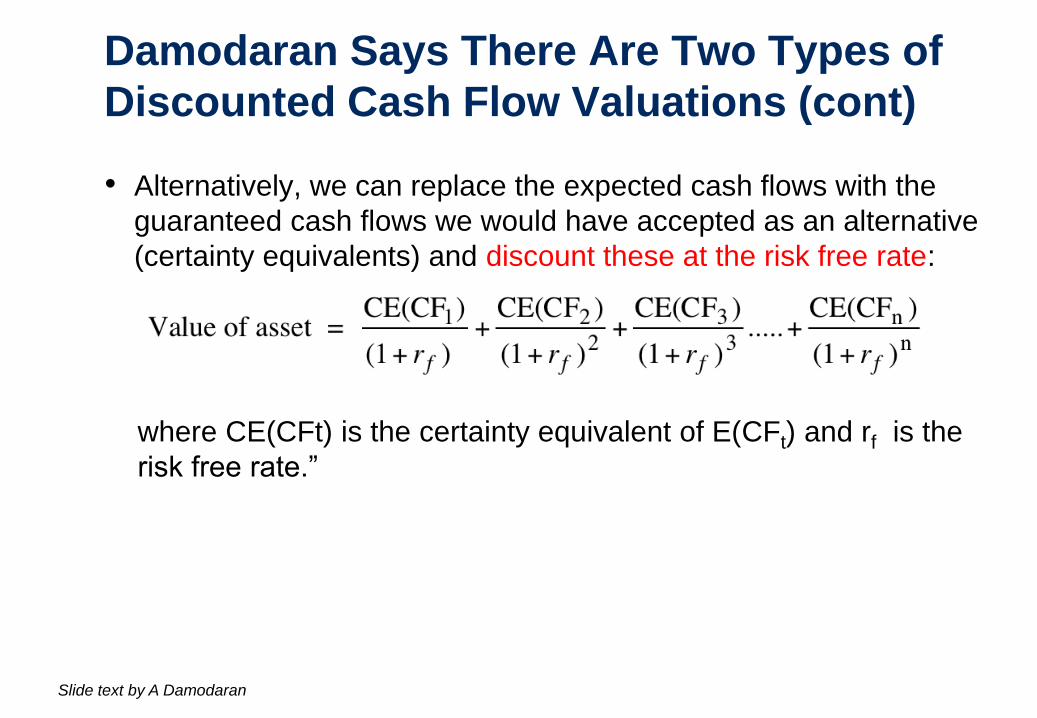

Damodaran Says There Are Two Types of

Discounted Cash Flow Valuations (cont)

• Alternatively, we can replace the expected cash flows with the

guaranteed cash flows we would have accepted as an alternative

(certainty equivalents) and discount these at the risk free rate:

where CE(CFt) is the certainty equivalent of E(CFt) and rf is the

risk free rate.”

13Slide text by A Damodaran

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

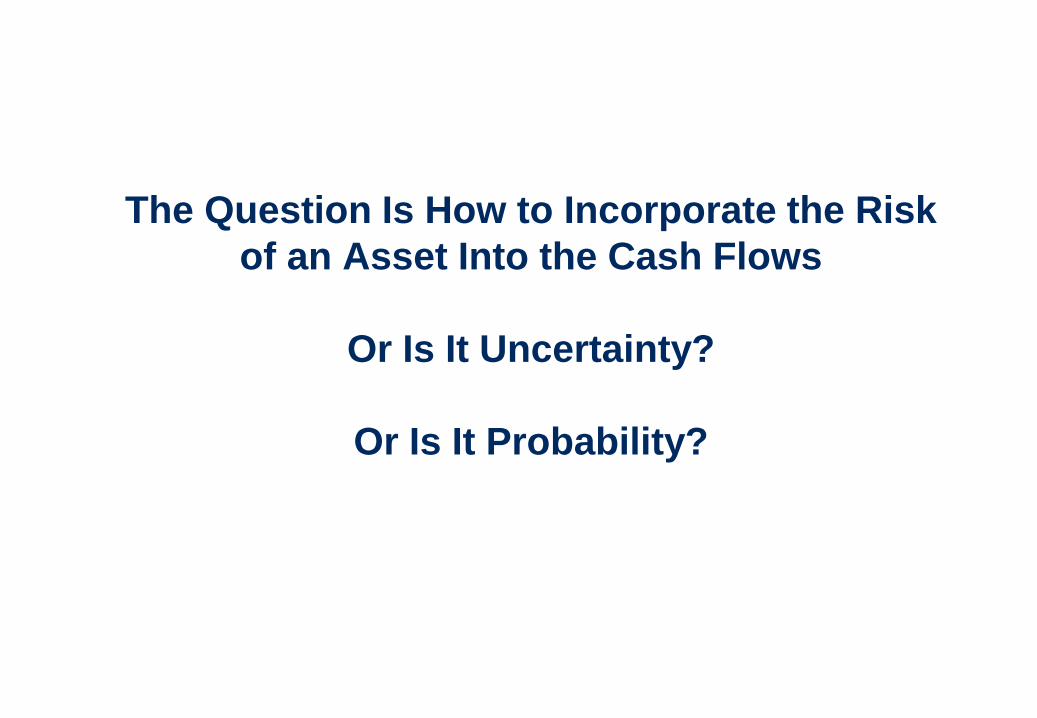

The Question Is How to Incorporate the Risk

of an Asset Into the Cash Flows

Or Is It Uncertainty?

Or Is It Probability?

14

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

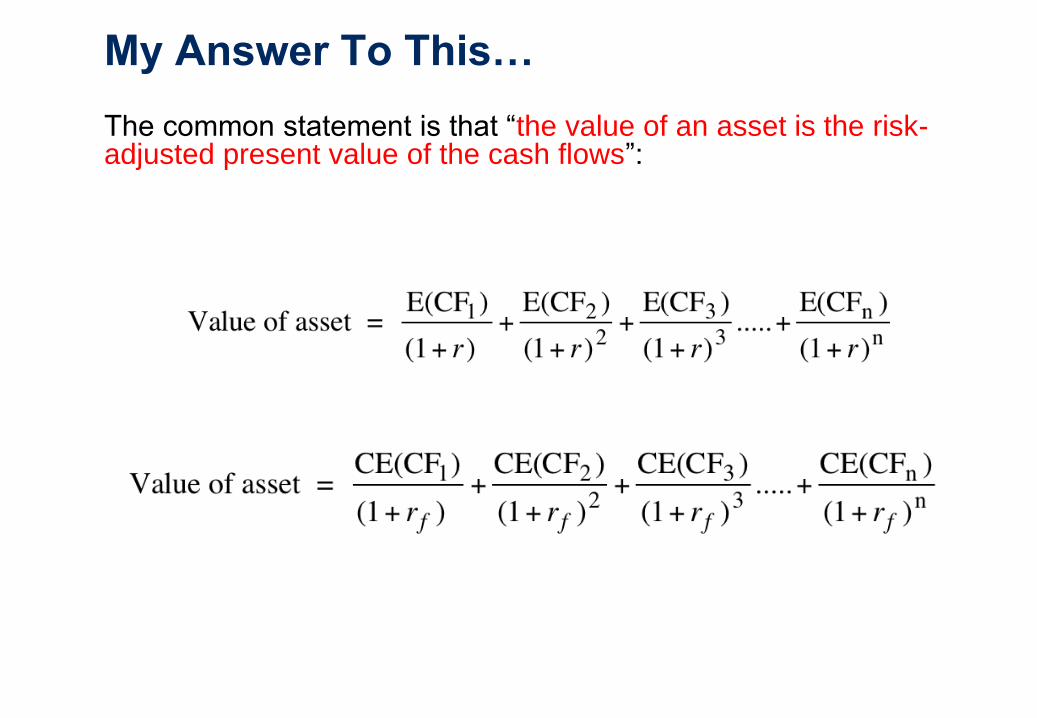

My Answer To This…

The common statement is that “the value of an asset is the risk-adjusted present value of the cash flows”:

15

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

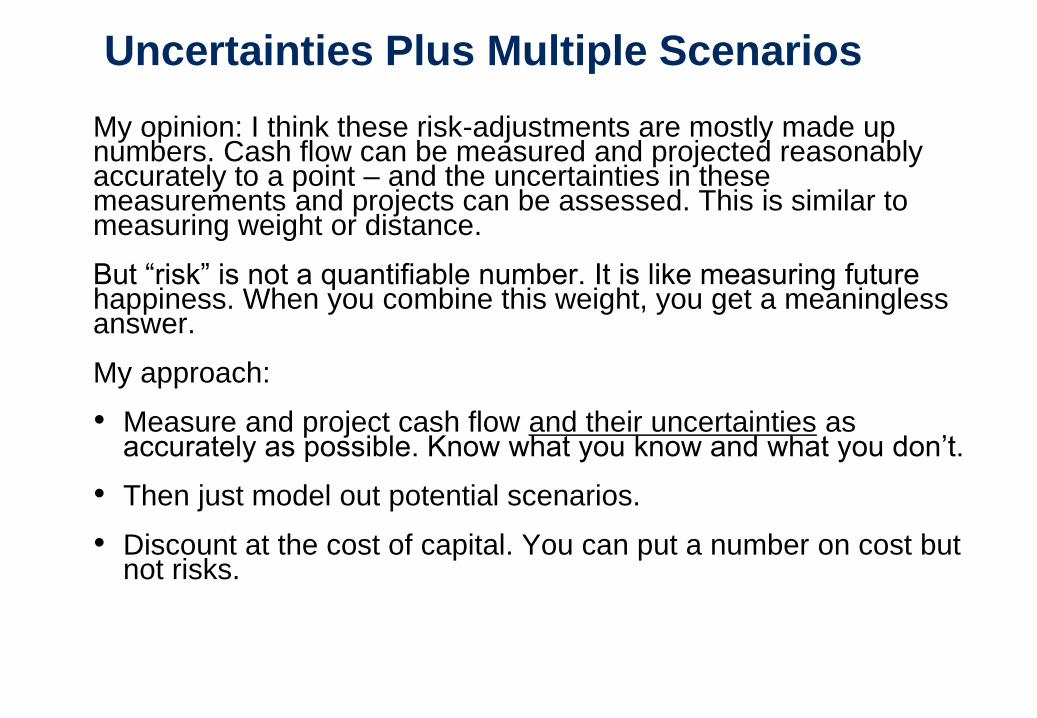

Uncertainties Plus Multiple Scenarios

My opinion: I think these risk-adjustments are mostly made up numbers. Cash flow can be measured and projected reasonably accurately to a point – and the uncertainties in these measurements and projects can be assessed. This is similar to measuring weight or distance.

But “risk” is not a quantifiable number. It is like measuring future happiness. When you combine this weight, you get a meaningless answer.

My approach:

• Measure and project cash flow and their uncertainties as accurately as possible. Know what you know and what you don’t.

• Then just model out potential scenarios.

• Discount at the cost of capital. You can put a number on cost but not risks.

16

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

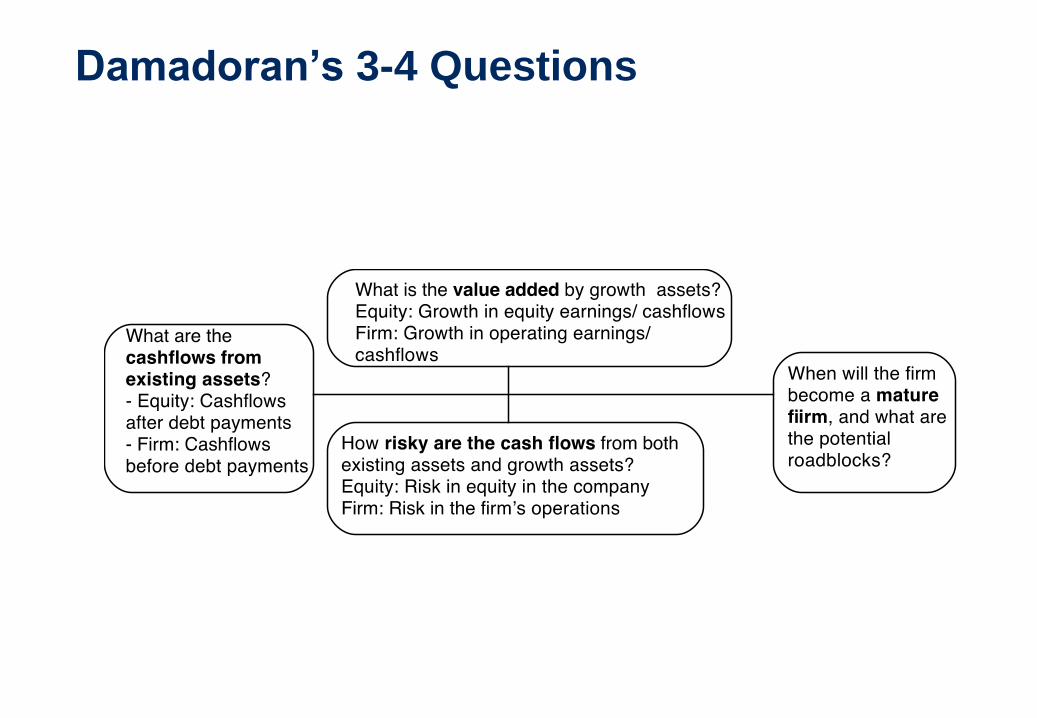

Damadoran’s 3-4 Questions

17

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Firm Valuation

Assets Liabilities

Assets in Place Debt

Equity

Discount rate reflects the cost of raising both debt and equity financing, in proportion to their use

Growth Assets

Figure 5.6: Firm Valuation

Cash flows considered are cashflows from assets, prior to any debt paymentsbut after firm has reinvested to create growth assets

Present value is value of the entire firm, and reflects the value of all claims on the firm.

18Slide by A Damodaran

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

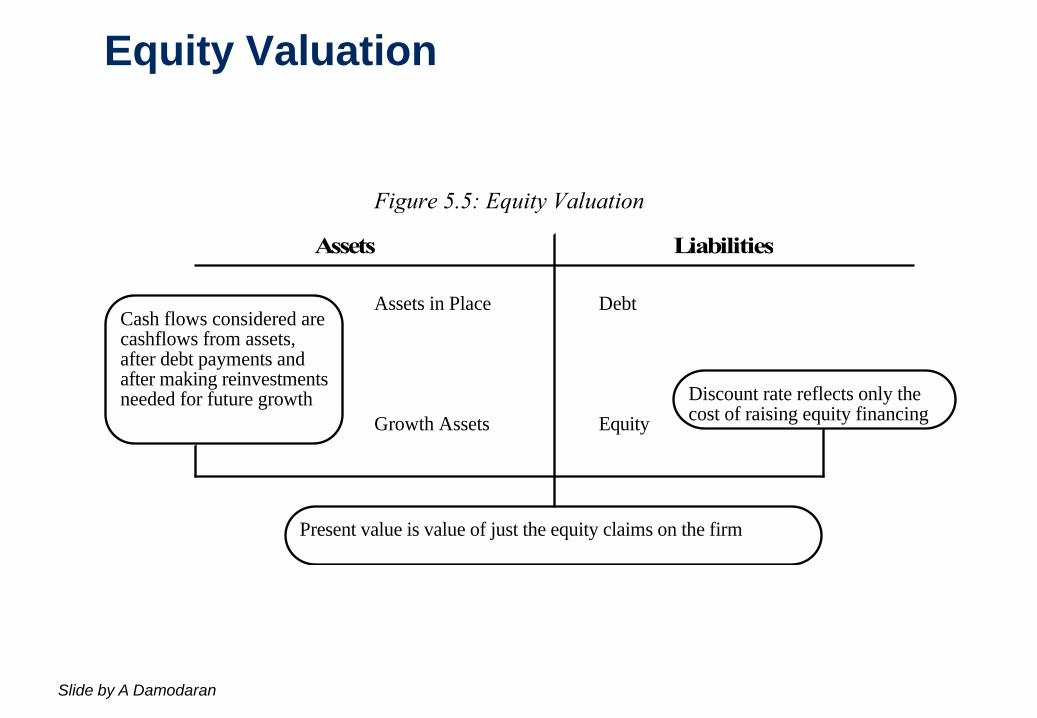

Equity Valuation

Assets Liabilities

Assets in Place Debt

Equity

Discount rate reflects only the cost of raising equity financing

Growth Assets

Figure 5.5: Equity Valuation

Cash flows considered are cashflows from assets, after debt payments and after making reinvestments needed for future growth

Present value is value of just the equity claims on the firm

19Slide by A Damodaran

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Exercise 1: Cash Flows and Discount

Rates

• A company has the following cash flows for the next five years.

Year CF to Equity Interest Exp (1-tax rate) CF to Firm

1 $ 50 $ 40 $ 90

2 $ 60 $ 40 $ 100

3 $ 68 $ 40 $ 108

4 $ 76.2 $ 40 $ 116.2

5 $ 83.49 $ 40 $ 123.49

Terminal Value $ 1603.0 $ 2363.008

• Assume also that the cost of equity is 13.625% and the firm can borrow long term

at 10%. (The tax rate for the firm is 50%.)

• The current market value of equity is $1,073 and the value of debt outstanding is

$800.

20Slide by A Damodaran

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Exercise 1: Equity Valuation

• Method 1: Discount CF to Equity at Cost of Equity to get value of equity

• Cost of Equity = 13.625%

• Value of Equity = 50/1.13625 + 60/1.136252 + 68/1.136253 + 76.2/1.136254 +

(83.49+1603)/1.136255 = $1073

21Slide by A Damodaran

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

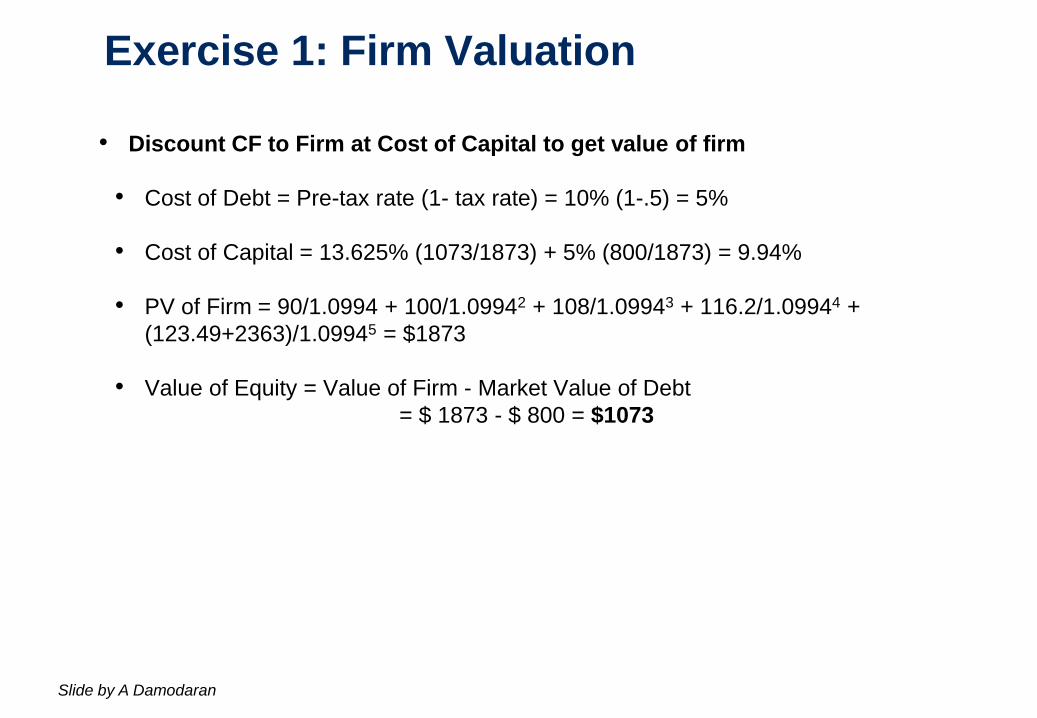

Exercise 1: Firm Valuation

• Discount CF to Firm at Cost of Capital to get value of firm

• Cost of Debt = Pre-tax rate (1- tax rate) = 10% (1-.5) = 5%

• Cost of Capital = 13.625% (1073/1873) + 5% (800/1873) = 9.94%

• PV of Firm = 90/1.0994 + 100/1.09942 + 108/1.09943 + 116.2/1.09944 +

(123.49+2363)/1.09945 = $1873

• Value of Equity = Value of Firm - Market Value of Debt

= $ 1873 - $ 800 = $1073

22Slide by A Damodaran

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Final Stuff To Keep In Mind

• Never mix and match cash flows and discount rates.

• If using pre-debt cash flow (cash flows to the company), then

use weighted cost of capital

• If using after debt cash flow (equity cash flows), use cost of

equity

23

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

This is 90% About Net Cash Flow

from Operating Assets Minus

Operating Liabilities

Page 24

24

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

25

• Valuation Basics 25 min

• Exercise 20 min

• Asset Values and EPV 45 min

• Break - 15 min

• Napkin Valuation 1 30 min

• DCF 15 min

• Discount Rate 10 min

www.jeffreytowson.com

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

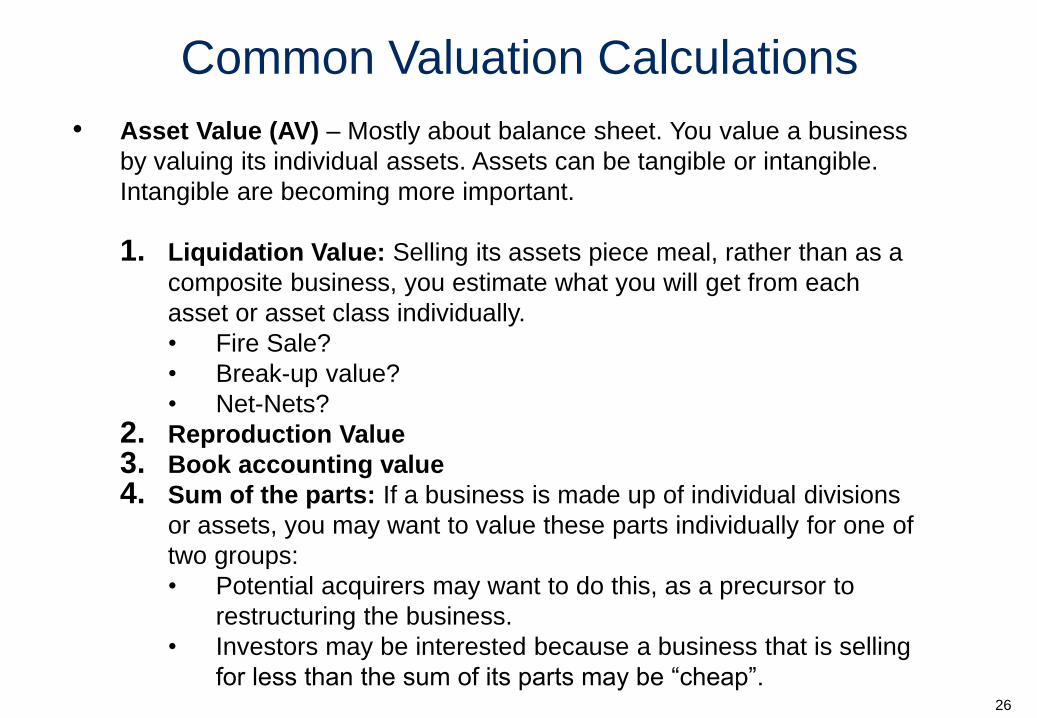

Common Valuation Calculations

26

• Asset Value (AV) – Mostly about balance sheet. You value a business

by valuing its individual assets. Assets can be tangible or intangible.

Intangible are becoming more important.

1. Liquidation Value: Selling its assets piece meal, rather than as a

composite business, you estimate what you will get from each

asset or asset class individually.

• Fire Sale?

• Break-up value?

• Net-Nets?

2. Reproduction Value

3. Book accounting value

4. Sum of the parts: If a business is made up of individual divisions

or assets, you may want to value these parts individually for one of

two groups:

• Potential acquirers may want to do this, as a precursor to

restructuring the business.

• Investors may be interested because a business that is selling

for less than the sum of its parts may be “cheap”.

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Common Valuation Calculations (cont)

27

5. Earnings Power Value (EPV)

• About current and recent earnings

• Good for reversion to mean

• Changes in balance sheet over time

6. Discounted Cash Flow (DCF)

• Value a business based upon the cash flows you expect that

business to generate over time.

• Value of growth?

• Discount rate?

• Relative valuation: You value a business based upon how

similar businesses are priced. Really just a market price.

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

I. Liquidation Valuation

• Should you price the assets or value them?

• For assets that are separable and traded (example: real estate), pricing is easy to do.

• For assets that are not, you often see book value used either as a proxy for liquidation value or as a basis for estimating liquidation value.

• In declining businesses where liquidation is often used, the assets can decline in value faster than you think.

28

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Liquidation Value

29

• The idea: Sell it for parts. Garage sale. Think of a factory

• Cash plus marketable securities $10M ± ____

• Land $50M ± ____

• Plant and Equipment $50M ± ____

• How specialized?

• Inventory $50M ± ____

• Goodwill $15M ± _____

• Liquidation Value _____

www.jeffreytowson.com

25%

2%

10%

25%

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Ben Graham Liked Liquidation Value

30

• Ben Graham’s “Net-Nets”

• Cash plus marketable securities $10M ± 3%

• Inventory $3M ± 30%

• Accounts Receivable $1M ± 30%

• Subtract All Liabilities $5M ± ??%

• Net Net Value $8M ± ??%

www.jeffreytowson.com

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

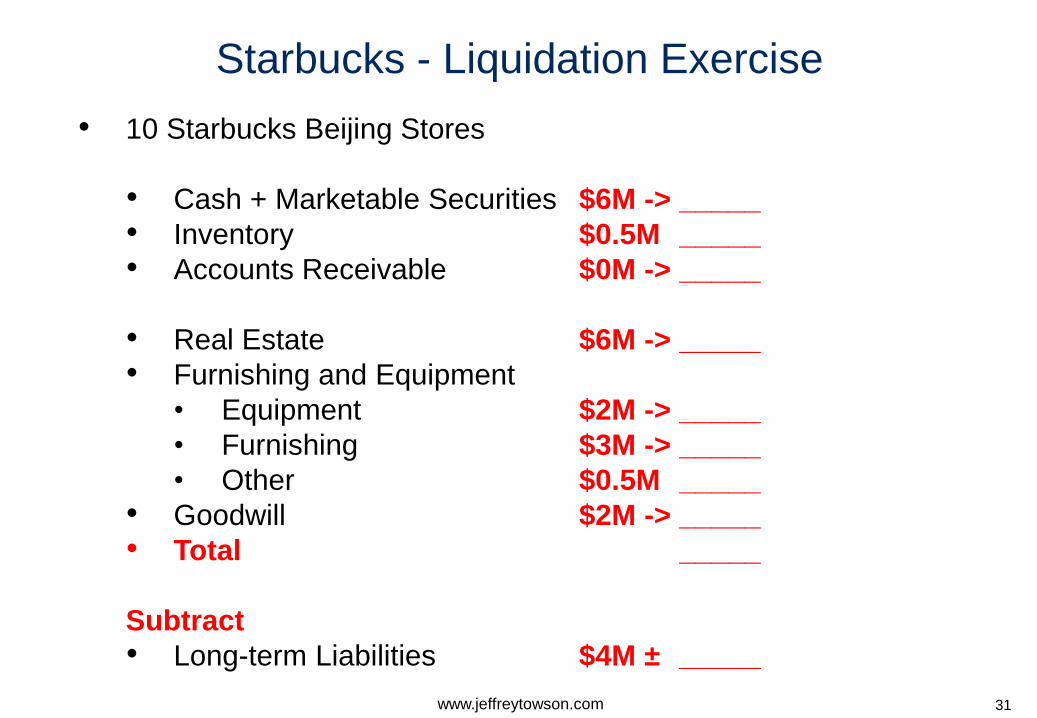

Starbucks - Liquidation Exercise

31www.jeffreytowson.com

• 10 Starbucks Beijing Stores

• Cash + Marketable Securities $6M -> _____

• Inventory $0.5M _____

• Accounts Receivable $0M -> _____

• Real Estate $6M -> _____

• Furnishing and Equipment

• Equipment $2M -> _____

• Furnishing $3M -> _____

• Other $0.5M _____

• Goodwill $2M -> _____

• Total _____

Subtract

• Long-term Liabilities $4M ± _____

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

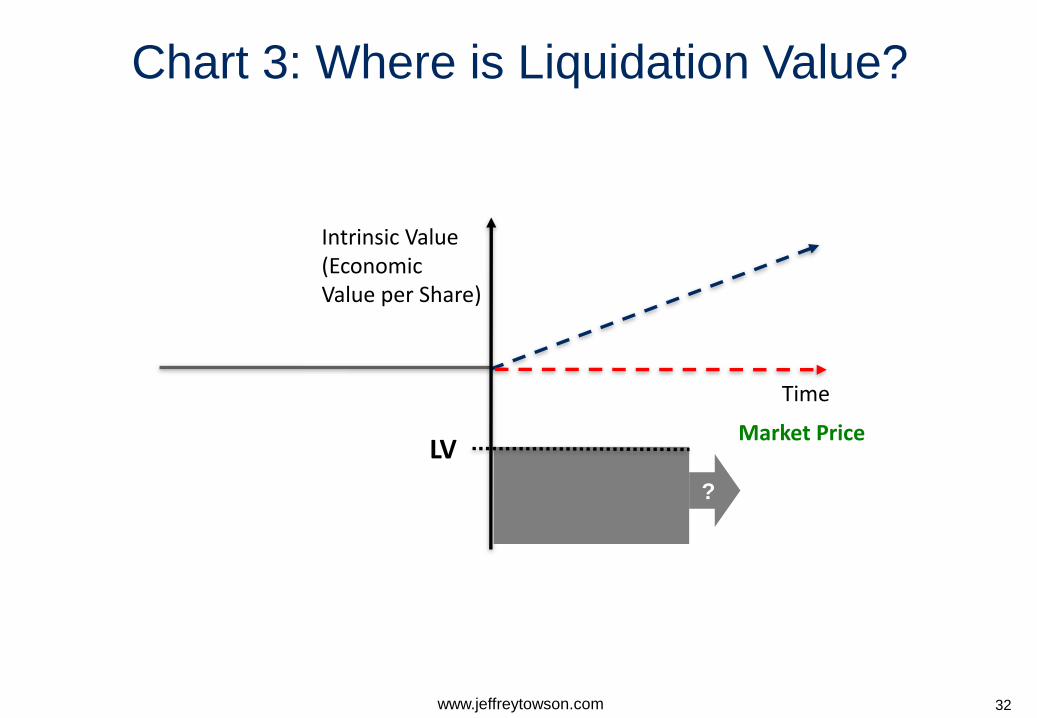

Time

Intrinsic Value (Economic Value per Share)

32www.jeffreytowson.com

LV

?

Market Price

Chart 3: Where is Liquidation Value?

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

How Good of a Measure for Value is

This?

33www.jeffreytowson.com

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Reproduction Value

34

• Cost to rebuild from scratch. To replicate or reproduce it.

• Assumes no competitive advantage or barriers to entry.

• Focused on balance sheet – but includes intangible assets.

• How much do we adjust each item on balance sheet?

• Cash plus marketable securities

• Inventory

• Accounts Receivable

• Land

• Do you need the land? What cost now?

• Plant and Equipment

• Customer base?

• Brand loyalty?

• Products, designs, technologies?

• Accounting vs. Economic Goodwill?

www.jeffreytowson.com

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Reproduction Value

35www.jeffreytowson.com

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Starbucks – Reproduction Exercise

36www.jeffreytowson.com

• 10 Starbucks Beijing Stores

• Cash + Marketable Securities $6M -> _____

• Inventory $0.5M _____

• Accounts Receivable $0M -> _____

• Real Estate $6M -> _____

• Furnishing and Equipment

• Equipment $2M -> _____

• Furnishing $3M -> _____

• Other $0.5M _____

• Goodwill $2M -> _____

• Customer base? _____

• Brand loyalty? _____

• Products, designs, technologies? _____

• Accounting vs. Economic Goodwill? _____

• Total _____

Subtract

• Long-term Liabilities $4M ± _____

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Time

Intrinsic Value (Economic Value per Share)

37www.jeffreytowson.com

RV?

LV

?

Chart 3: Where is Reproduction Value?

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

How Good of a Measure for Value is

This?

38www.jeffreytowson.com

Wo

rkin

g D

raft -

La

st M

od

ified

04

/23

/20

08

11

:49

:19

AM

Prin

ted

4/2

1/2

00

8 4

:27

:01

PM

Contact Information:

Jeffrey Towson

www.jeffreytowson.com

Wechat: a555666777aa

LinkedIn: Jeffrey Towson