valuation kpmg ivca

TRANSCRIPT

Valuation

August 2009

CORPORATE FINANCE

ADVISORY

2© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Agenda

Valuation theory – a brief reminder

Valuation in practice

Case studies

The vendor’s perspective

The buyer’s perspective

3© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

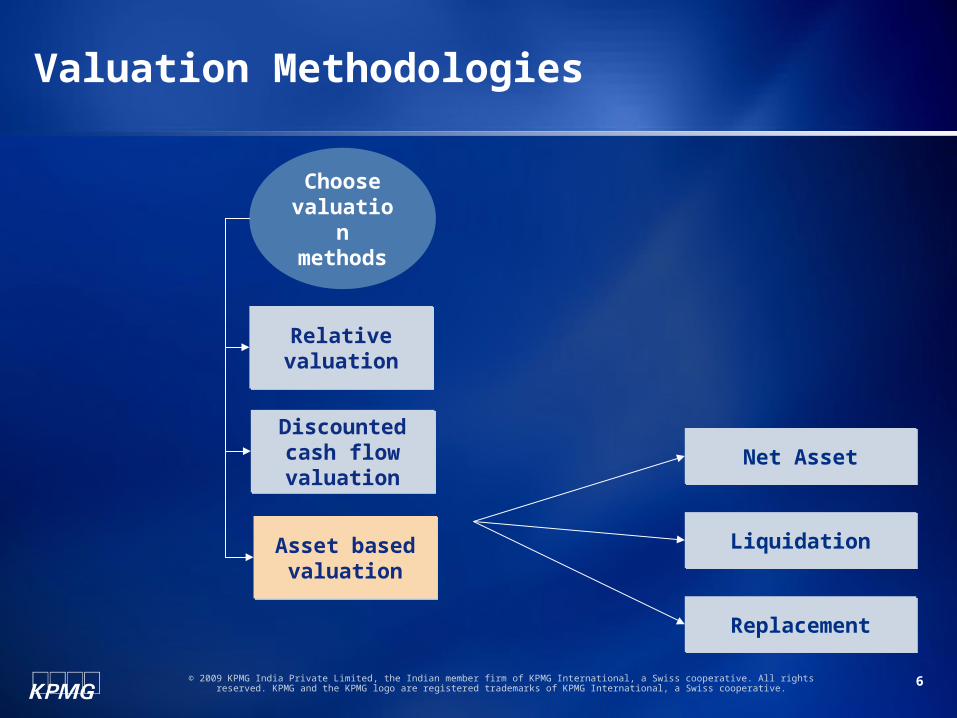

Choose valuation methods

Relative valuationRelative valuation

Asset based valuation

Asset based valuation

Discounted cash flow valuation

Discounted cash flow valuation

Valuation Methodologies

4© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

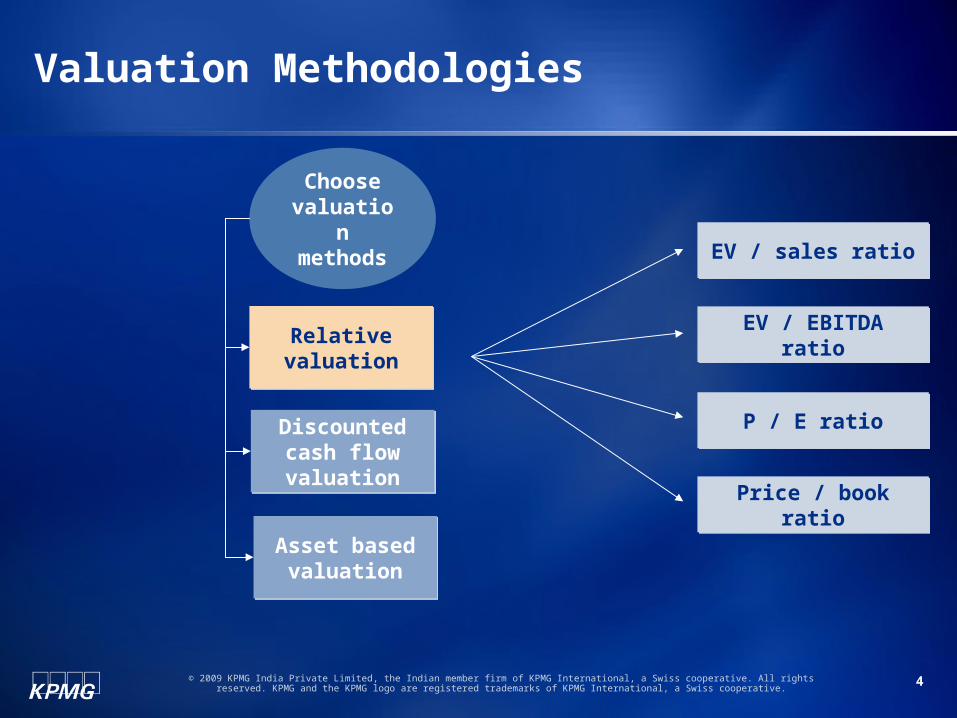

Choose valuation methods

Relative valuationRelative valuation

Asset based valuation

Asset based valuation

Discounted cash flow valuation

Discounted cash flow valuation

P / E ratioP / E ratio

Price / book ratioPrice / book ratio

EV / sales ratioEV / sales ratio

EV / EBITDA ratioEV / EBITDA ratio

Valuation Methodologies

5© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

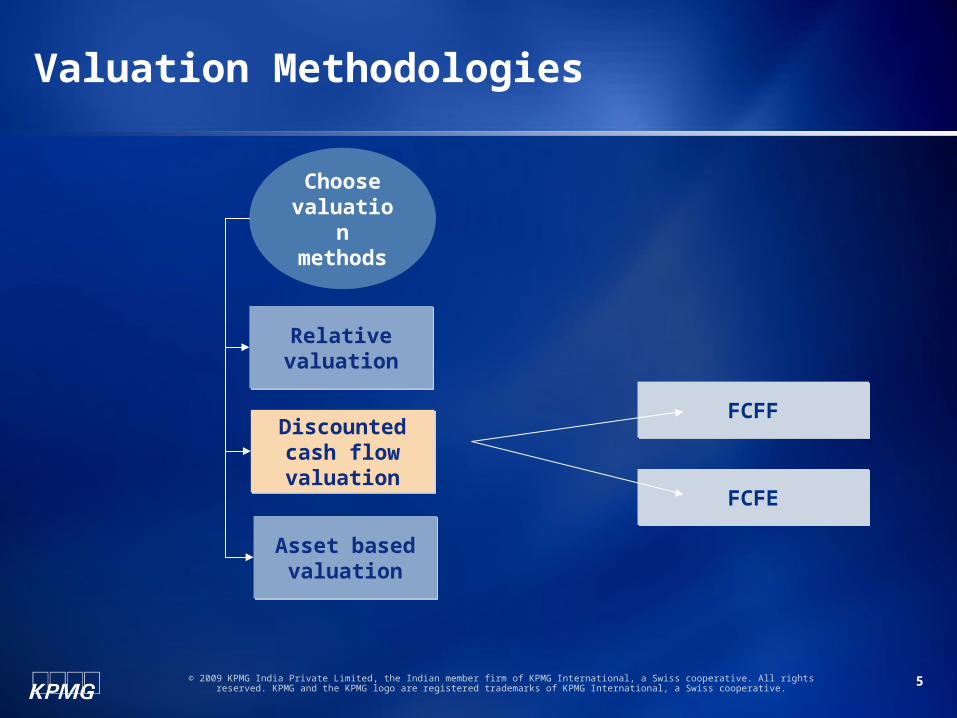

Choose valuation methods

Relative valuationRelative valuation

Asset based valuation

Asset based valuation

Discounted cash flow valuation

Discounted cash flow valuation

Valuation Methodologies

FCFFFCFF

FCFEFCFE

6© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Choose valuation methods

Relative valuationRelative valuation

Asset based valuation

Asset based valuation

Discounted cash flow valuation

Discounted cash flow valuation

Valuation Methodologies

Net AssetNet Asset

LiquidationLiquidation

ReplacementReplacement

7© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Relative Valuation

8© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Value of an asset compared to the values assessed by the market for

‘similarsimilar’ or ‘comparablecomparable’ assets

Commonly used multiples for relative valuation are the ‘Comparable

Company’ (“CoCos”) and ‘Comparable Transaction’ (“CoTrans”)

multiples

What you need to do:

• Identify comparable universe

• Use standard variables e.g. Sales, EBITDA, PAT, etc

• Apply multiples to the variables for the asset being analysed

• Ensure any differences or exceptions are eliminated to ascertain multiples are

obtained on a ‘normalised’ basis

Relative Valuation - introduction

9© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Enterprise value is the sum of market value of equity and market value of debt and securities

Can be used for loss making and troubled companies

Less impact of accounting policies

Eliminates the impact of financial leverage

EV to Sales multiples are not as volatile as P/E multiples

Relative Valuation- EV to Sales

10© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

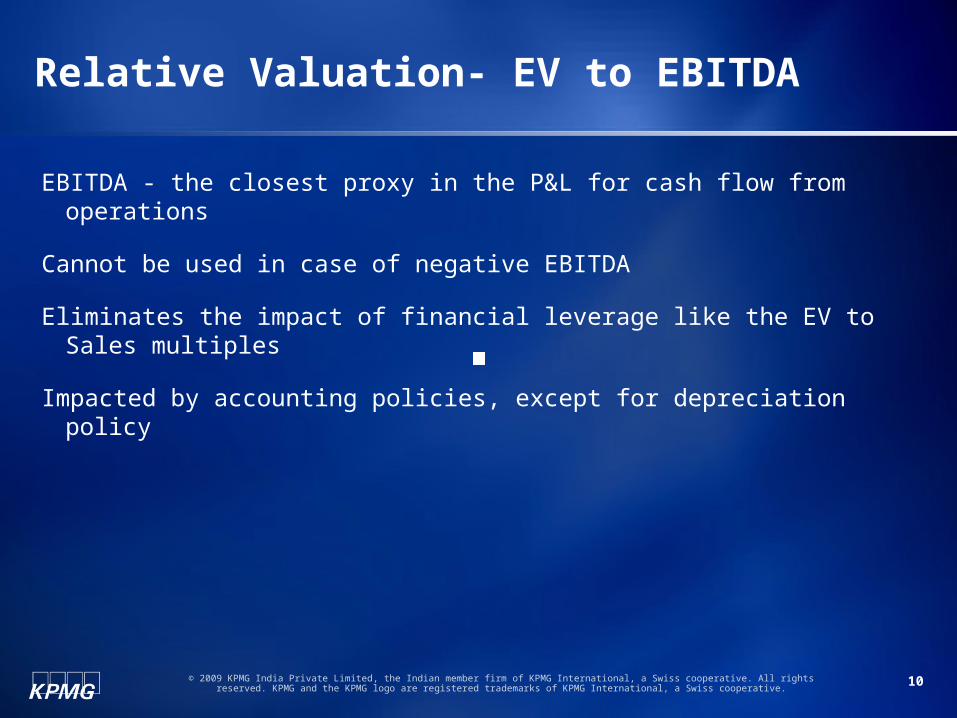

EBITDA - the closest proxy in the P&L for cash flow from operations

Cannot be used in case of negative EBITDA

Eliminates the impact of financial leverage like the EV to Sales multiples

Impacted by accounting policies, except for depreciation policy

Relative Valuation- EV to EBITDA

11© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

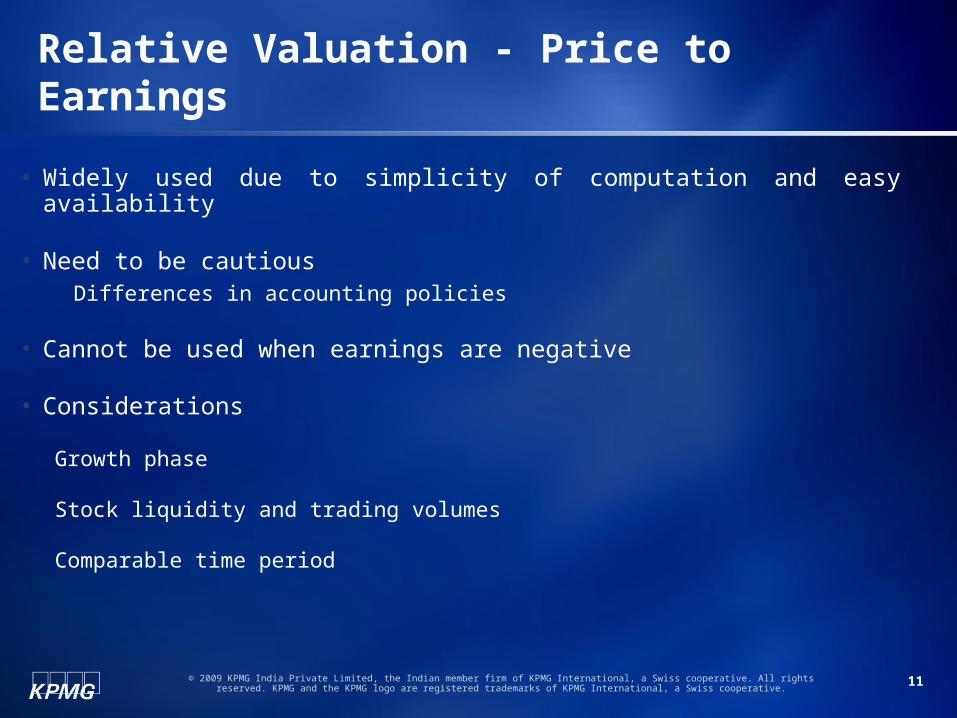

• Widely used due to simplicity of computation and easy availability

• Need to be cautious Differences in accounting policies

• Cannot be used when earnings are negative

• Considerations

Growth phase

Stock liquidity and trading volumes

Comparable time period

Relative Valuation - Price to Earnings

12© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

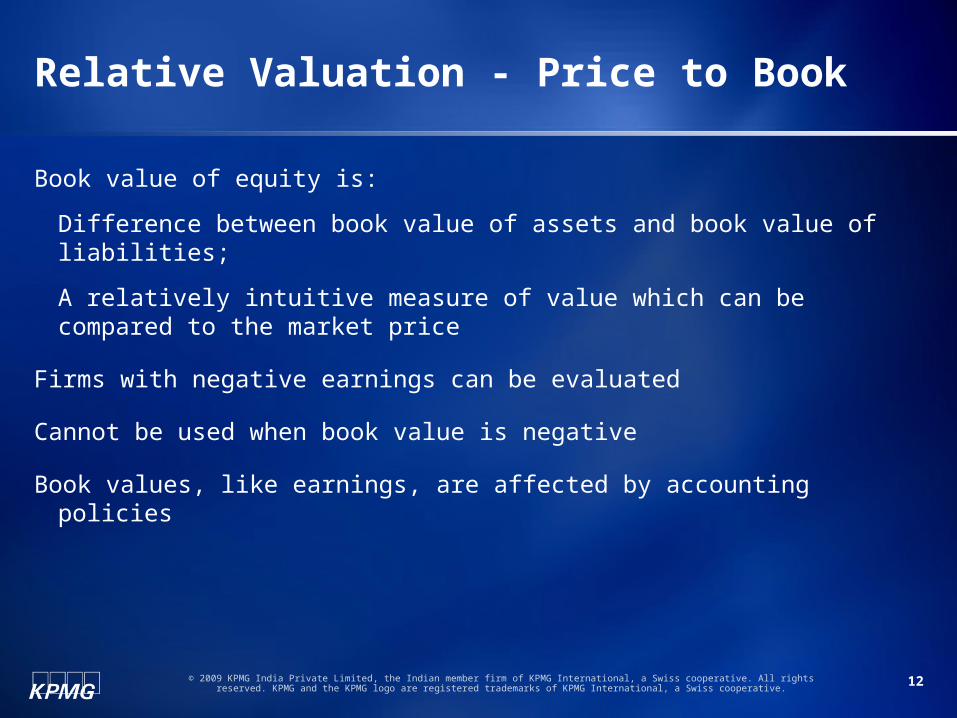

Book value of equity is:

Difference between book value of assets and book value of liabilities;

A relatively intuitive measure of value which can be compared to the market price

Firms with negative earnings can be evaluated

Cannot be used when book value is negative

Book values, like earnings, are affected by accounting policies

Relative Valuation - Price to Book

13© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

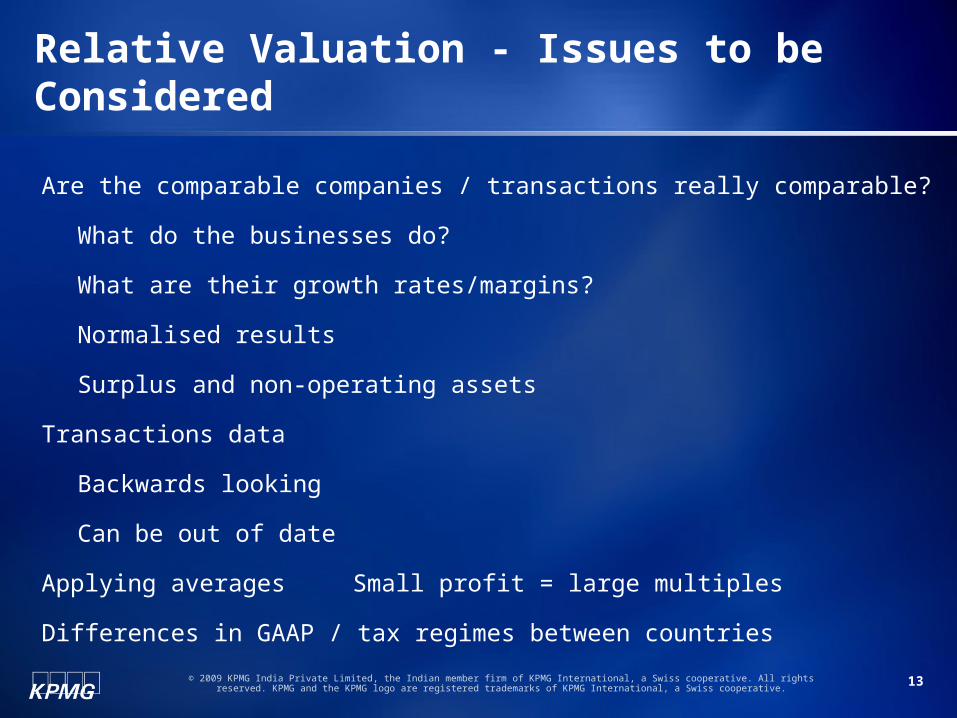

Are the comparable companies / transactions really comparable?

What do the businesses do?

What are their growth rates/margins?

Normalised results

Surplus and non-operating assets

Transactions data

Backwards looking

Can be out of date

Applying averages Small profit = large multiples

Differences in GAAP / tax regimes between countries

Relative Valuation - Issues to be Considered

14© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Discounted Cash Flow Valuation

15© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

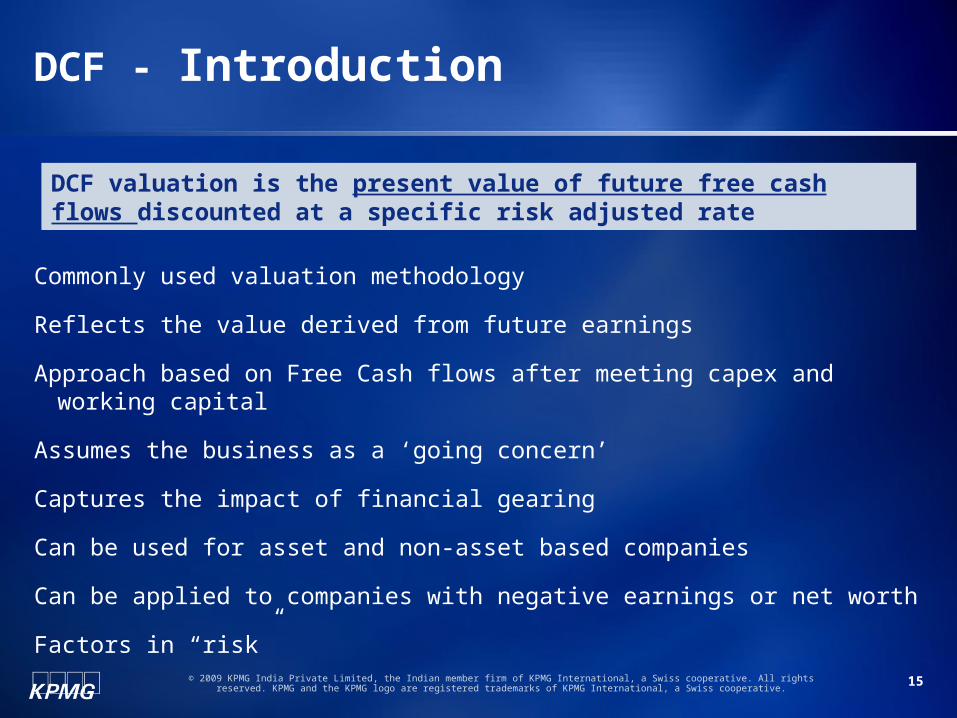

Commonly used valuation methodology

Reflects the value derived from future earnings

Approach based on Free Cash flows after meeting capex and working capital

Assumes the business as a ‘going concern’

Captures the impact of financial gearing

Can be used for asset and non-asset based companies

Can be applied to companies with negative earnings or net worth

Factors in “risk”

DCF valuation is the present value of future free cash flows discounted at a specific risk adjusted rate

DCF - Introduction

16© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

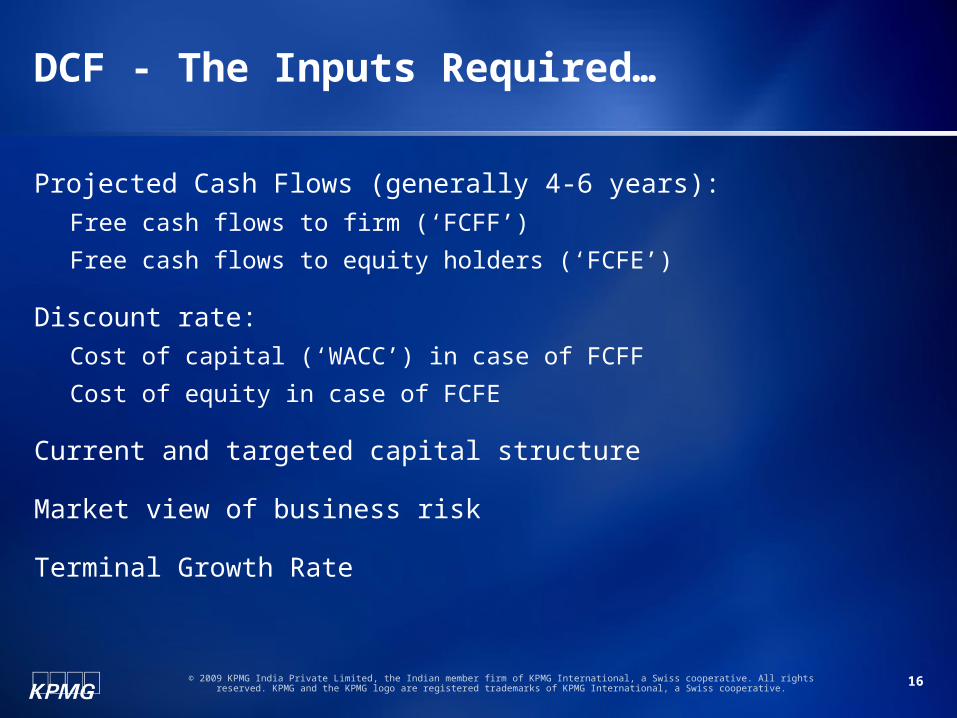

Projected Cash Flows (generally 4-6 years):

Free cash flows to firm (‘FCFF’)

Free cash flows to equity holders (‘FCFE’)

Discount rate:

Cost of capital (‘WACC’) in case of FCFF

Cost of equity in case of FCFE

Current and targeted capital structure

Market view of business risk

Terminal Growth Rate

DCF - The Inputs Required…

17© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

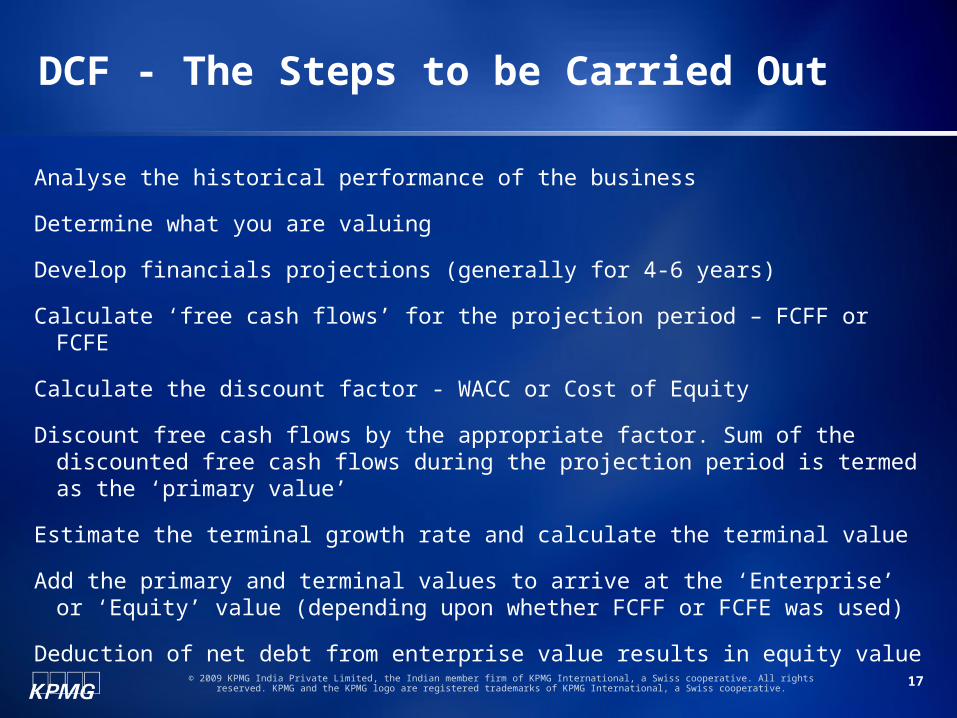

Analyse the historical performance of the business

Determine what you are valuing

Develop financials projections (generally for 4-6 years)

Calculate ‘free cash flows’ for the projection period – FCFF or FCFE

Calculate the discount factor - WACC or Cost of Equity

Discount free cash flows by the appropriate factor. Sum of the discounted free cash flows during the projection period is termed as the ‘primary value’

Estimate the terminal growth rate and calculate the terminal value

Add the primary and terminal values to arrive at the ‘Enterprise’ or ‘Equity’ value (depending upon whether FCFF or FCFE was used)

Deduction of net debt from enterprise value results in equity value

DCF - The Steps to be Carried Out

18© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

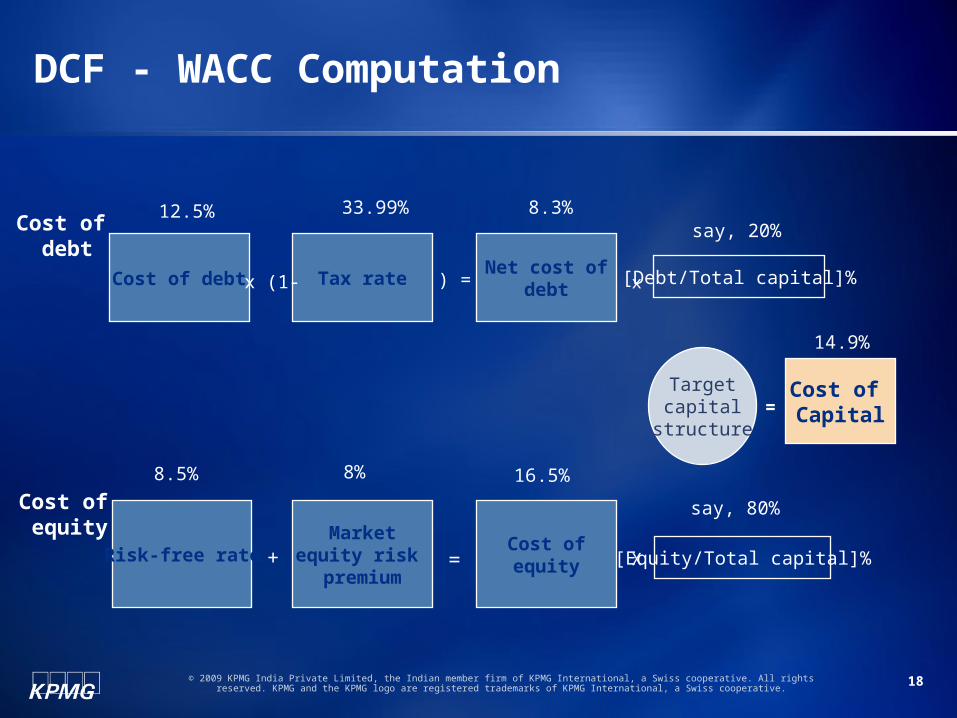

Cost of debt Tax rateNet cost of

debt[Debt/Total capital]%

Risk-free rateMarket

equity risk premium

Cost ofequity [Equity/Total capital]%

Cost of Capital

Targetcapital

structure

Cost of debt

Cost of equity

x (1- ) = x

X

=

=+

12.5% 33.99% 8.3%say, 20%

say, 80%

8.5% 8% 16.5%

14.9%

DCF - WACC Computation

19© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

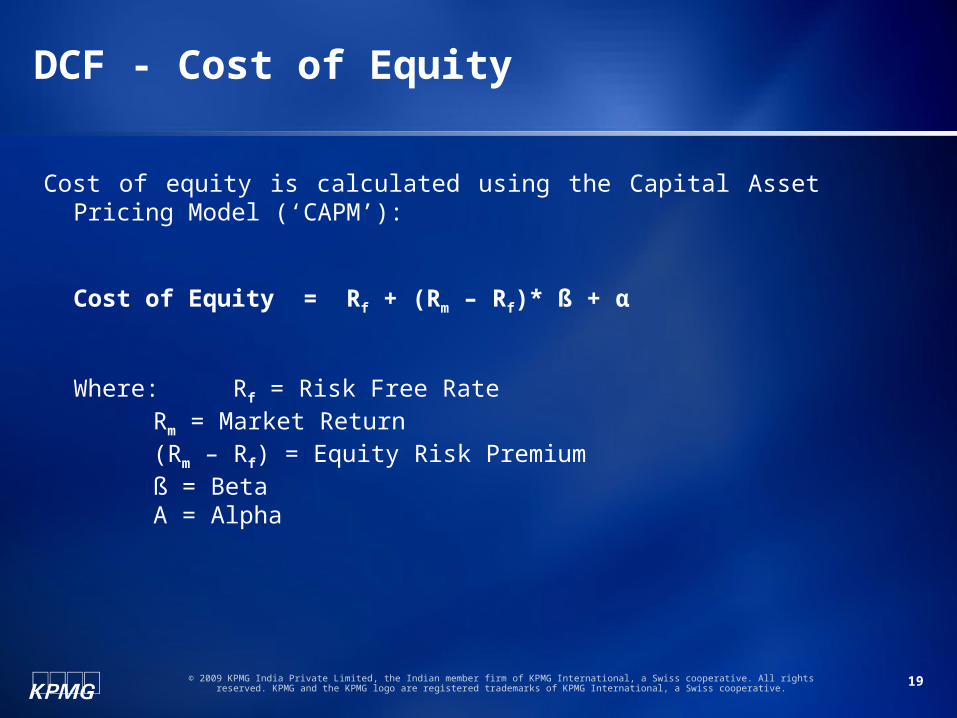

Cost of equity is calculated using the Capital Asset Pricing Model (‘CAPM’):

Cost of Equity = Rf + (Rm – Rf)* ß + α

Where:Rf = Risk Free RateRm = Market Return(Rm – Rf) = Equity Risk Premiumß = BetaΑ = Alpha

DCF - Cost of Equity

20© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Measures the value of the business after the projected cash flow period ie, cash flows into perpetuity

Estimation of the growth rate is critical - it is a valuation call

DCF - Terminal Value

21© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Asset Based Valuation

22© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

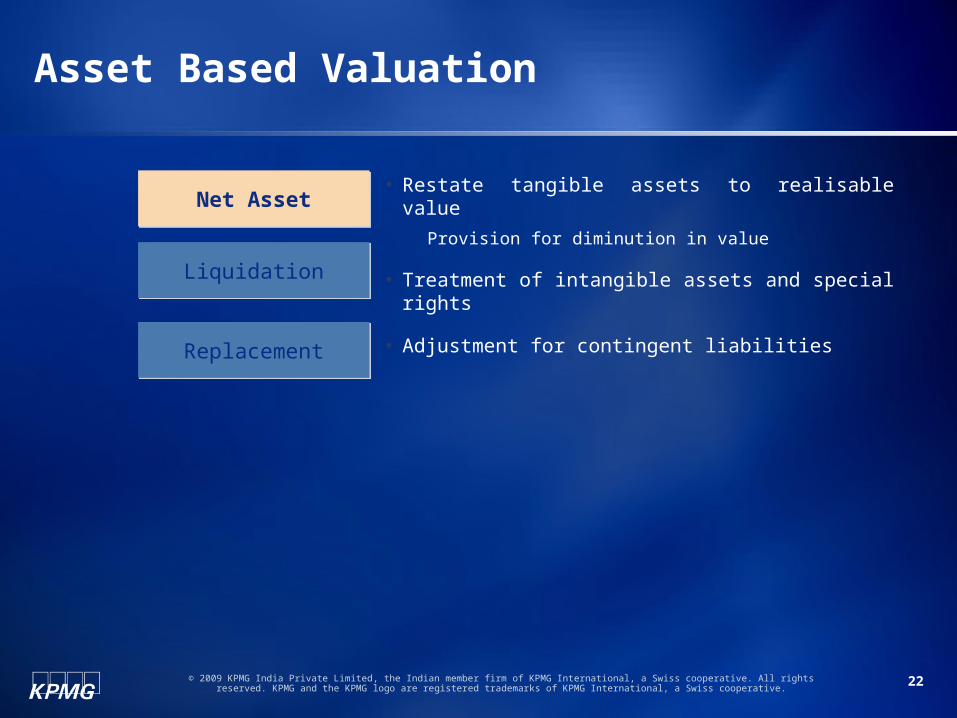

Asset Based Valuation

• Restate tangible assets to realisable value Provision for diminution in value

• Treatment of intangible assets and special rights

• Adjustment for contingent liabilities

Net AssetNet Asset

LiquidationLiquidation

ReplacementReplacement

23© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

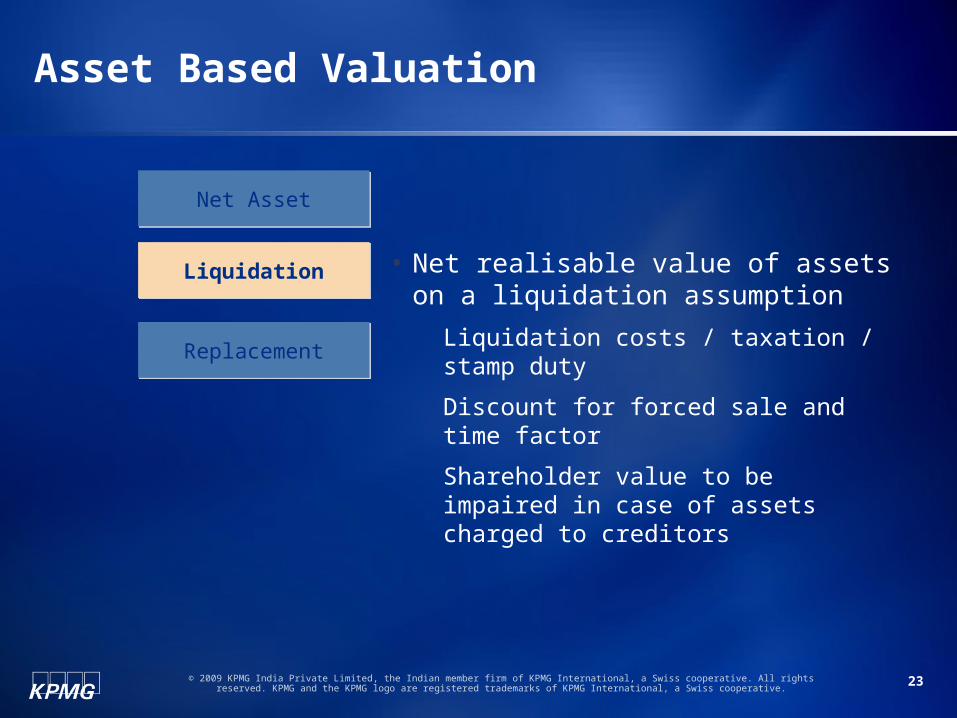

Asset Based Valuation

• Net realisable value of assets on a liquidation assumption Liquidation costs / taxation / stamp duty

Discount for forced sale and time factor

Shareholder value to be impaired in case of assets charged to creditors

Net AssetNet Asset

LiquidationLiquidation

ReplacementReplacement

24© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

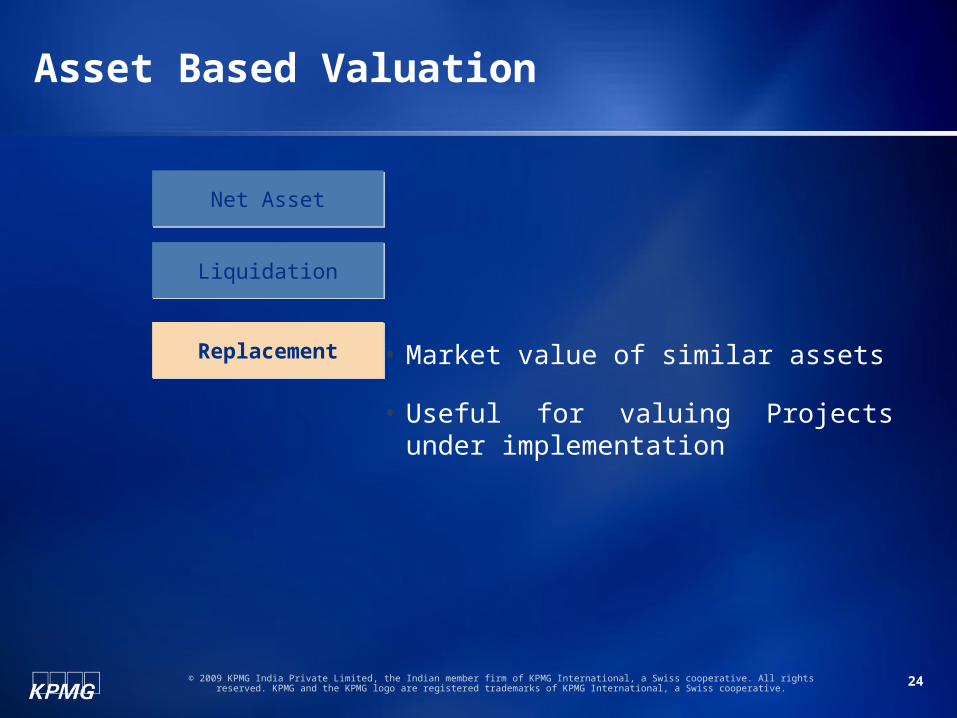

Asset Based Valuation

• Market value of similar assets

• Useful for valuing Projects under implementation

Net AssetNet Asset

LiquidationLiquidation

ReplacementReplacement

25© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Valuation in practice

Case studies

The problem with averages

Dangerous DCFs

Sensitive DCFs

The market return ‘paradox’

Private equity pricing

26© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

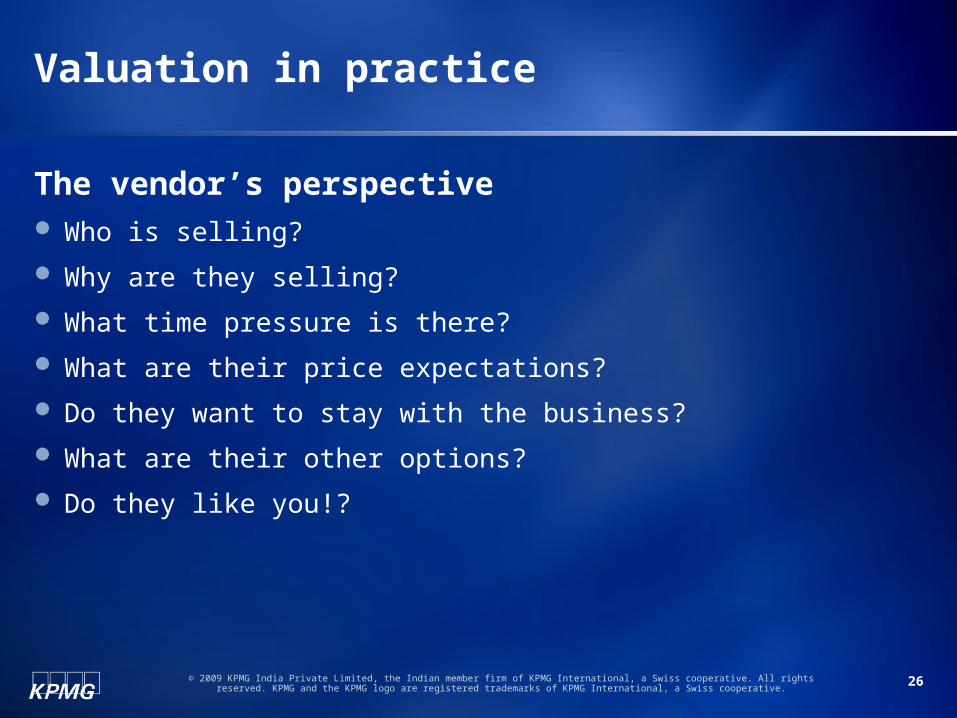

Valuation in practice

The vendor’s perspective Who is selling?

Why are they selling?

What time pressure is there?

What are their price expectations?

Do they want to stay with the business?

What are their other options?

Do they like you!?

27© 2009 KPMG India Private Limited, the Indian member firm of KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

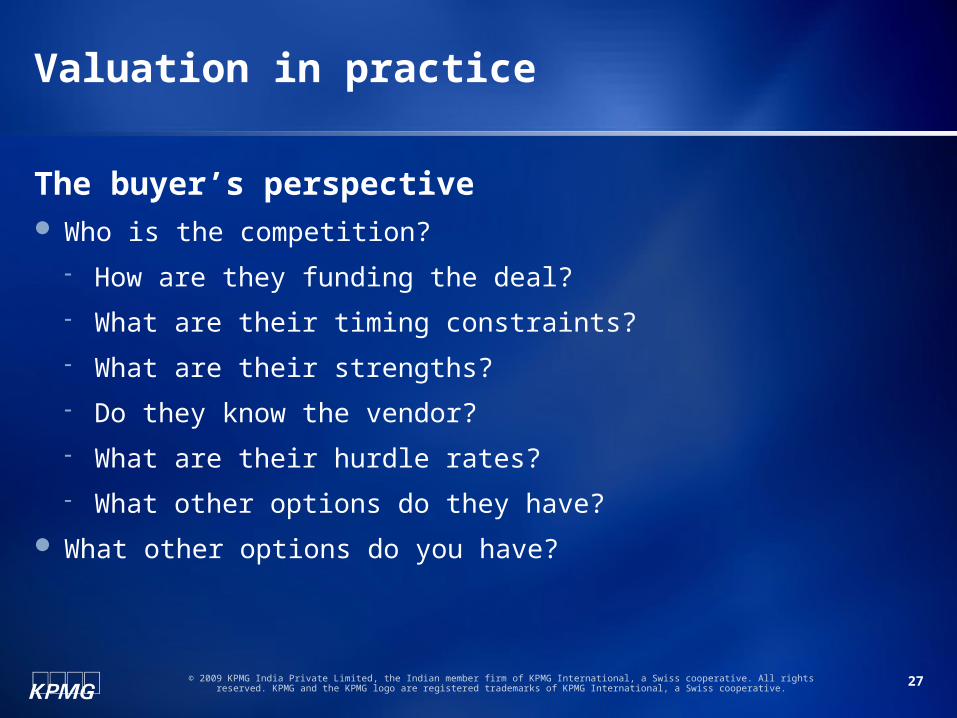

Valuation in practice

The buyer’s perspective Who is the competition?

How are they funding the deal?

What are their timing constraints?

What are their strengths?

Do they know the vendor?

What are their hurdle rates?

What other options do they have?

What other options do you have?