valuation of double barrier options in heston’s...

TRANSCRIPT

Valuation of Double Barrier Options in Heston’s Stochastic Volatility Model

Using Finite Element Methods

Copyright © Changwei Xiong 2010 - 2017

Jan. 2010

last update: October 31, 2017

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

2

ABSTRACT

Heston stochastic volatility moded has been widely used in financial derivative pricing and risk

management. One of the reasons for that is that vanilla options in Heston model have close form solutions.

This makes the calibration of the model computationally much efficient and accurate. To understand these

closed form formulas, this essay in the first half will introduce the Fourier transform method for option

pricing and its application to the Heston model. Additionally, a characteristic function based method is

also discussed, which extends the Heston model to have piecewise time-dependent parameters.

Finite element method (FEM) has been developed for decades to solve partial differential

equations arise from science and engineering problems. It is well known for requiring a low order storage

and for its capability to handle complicated irregular computational domains comparing to finite

difference method (FDM). This characteristic advantage makes FEM an ideal numerical method for

valuation of exotic options. This essay in the second half will present a detailed implementation of FEM

and its application to pricing a double barrier knock-out option with an underlying asset modeled by

Heston stochastic volatility process.

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

3

TABLE OF CONTENTS

Abstract ........................................................................................................................................................2

Table of Contents .........................................................................................................................................3

1. Kolmogorov Forward and Backward Equations ..................................................................................5

1.1. Kolmogorov Forward Equation ....................................................................................................5

1.2. Kolmogorov Backward Equation ..................................................................................................8

2. Heston Model .....................................................................................................................................10

2.1. Heston Stochastic Volatility Model .............................................................................................10

2.1.1. Market Price of Risk ....................................................................................................... 10

2.1.2. Radon-Nikodym Derivative ............................................................................................ 15

2.1.3. Feller Condition ............................................................................................................... 16

2.2. Probability Distribution of Spot Returns .....................................................................................16

2.2.1. Derivation of the Transition Probability .......................................................................... 17

2.2.2. Moment Generating Function (in progress…) ................................................................ 20

2.3. Analytical Solution of Vanilla Options .......................................................................................21

2.3.1. Fourier Transform and Characteristic Function .............................................................. 21

2.3.2. Characteristic Function ................................................................................................... 25

2.3.3. Vanilla Option Prices ....................................................................................................... 29

2.3.3.1. Analogy to Cumulative Density Function ....................................................................... 29

2.3.3.2. Analogy to Probability Density Function ........................................................................ 31

2.3.3.3. Heston’s Original Solution .............................................................................................. 32

2.4. Piecewise Time Dependent Heston Model ..................................................................................35

3. Heston Model: PDE by Finite Element Method ................................................................................38

3.1. The Partial Differential Equation ................................................................................................39

3.2. Numerical Solution of the PDE ...................................................................................................42

3.2.1. Temporal Discretization .................................................................................................. 42

3.2.2. Two-Dimensional Finite Element Method ...................................................................... 43

3.2.2.1. Weak Formulation ........................................................................................................... 43

3.2.2.2. Boundary Conditions....................................................................................................... 44

3.2.2.3. Mesh and Basis Functions ............................................................................................... 46

3.2.2.4. Affine Transformation ..................................................................................................... 48

3.2.2.5. Stiffness and Mass Matrix ............................................................................................... 48

3.2.2.6. Computation of Integrals ................................................................................................. 51

3.2.3. Iterative Linear Solvers ................................................................................................... 53

3.2.3.1. Implementation of Sparse Matrix .................................................................................... 53

3.2.3.2. Iterative Methods for Asymmetric Sparse Matrix ........................................................... 54

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

4

3.2.4. Interpolation of Numerical Solution ............................................................................... 54

3.3. Solutions and Discussions ...........................................................................................................55

3.3.1. Vanilla Call ...................................................................................................................... 55

3.3.2. Vanilla Put ....................................................................................................................... 58

3.3.3. Double Barrier Knock-out Call ....................................................................................... 59

3.3.4. Double Barrier Knock-out Put ........................................................................................ 61

3.3.5. Numerical Solutions of Double Barrier Knock-out Options ........................................... 63

3.4. Conclusions .................................................................................................................................64

References ..................................................................................................................................................65

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

5

This note is to summarize Heston stochastic volatility model. It was started as my degree essay for

the M.S. in Mathematical Finance, which only covered the barrier option pricing by solving PDE using

finite element method, i.e. the Chapter 3 in this note. I have been continuously expanding it with more

mathematical background, such as the derivation of market price of spot/volatility risk, the Fourier

transform method for option pricing, the derivation of characteristic function of the joint spot-variance

process, the probability distribution of spot return, the piecewise time dependent Heston parameters, etc.

At first, let’s start from the Kolmogorov forward and backward equations, which fundamentally govern

the transition probability density function of a diffusion process.

1. KOLMOGOROV FORWARD AND BACKWARD EQUATIONS

The time evolution of the transition probability density function is governed by Kolmogorov

forward and backward equations, which will be introduced as follows, without loss of generality, in multi-

dimension.

1.1. Kolmogorov Forward Equation

Let’s consider the following 𝑚-dimensional stochastic spot process 𝑆𝑡 ∈ ℝ𝑚 driven by an 𝑛-

dimensional Brownian motion 𝑊𝑡 whose correlation matrix 𝜌 is given by 𝜌𝑑𝑡 = 𝑑𝑊𝑡𝑑𝑊𝑡′

𝑑𝑆𝑡𝑚×1

= 𝐴(𝑡, 𝑆𝑡)𝑚×1

𝑑𝑡1×1

+ 𝐵(𝑡, 𝑆𝑡)𝑚×𝑛

𝑑𝑊𝑡𝑛×1

(1)

We derive the dynamics of ℎ, where ℎ:ℝ𝑚 ⟶ℝ in this case is a scalar-valued Borel-measurable function

only on variable 𝑆𝑡

𝑑ℎ(𝑆𝑡)1×1

= 𝐽ℎ1×𝑚

𝑑𝑆𝑡𝑚×1

+1

2𝑑𝑆𝑡

′

1×𝑚𝐻ℎ𝑚×𝑚

𝑑𝑆𝑡𝑚×1

= 𝐽ℎ𝐴𝑑𝑡 + 𝐽ℎ𝐵𝑑𝑊𝑡 +1

2𝑑𝑊𝑡

′𝐵′𝐻ℎ𝐵𝑑𝑊𝑡 (2)

where 𝐽ℎ is the 1 × 𝑚 Jacobian (i.e. the same as gradient if ℎ is a scalar-valued function) and 𝐻ℎ the 𝑚 ×

𝑚 Hessian (with subscripts of 𝑆 now denoting the indices of vector components)

[𝐽ℎ]𝑖 =𝜕ℎ

𝜕𝑆𝑖 and [𝐻ℎ]𝑖𝑗 =

𝜕2ℎ

𝜕𝑆𝑖𝜕𝑆𝑗 (3)

Expanding the expression in (2), we have

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

6

𝑑ℎ =∑𝜕ℎ

𝜕𝑆𝑖𝐴𝑖𝑑𝑡

𝑚

𝑖=1

+∑𝜕ℎ

𝜕𝑆𝑖

𝑚

𝑖=1

∑𝐵𝑖𝑘𝑑𝑊𝑘

𝑛

𝑘=1

+1

2∑

𝜕2ℎ

𝜕𝑆𝑖𝜕𝑆𝑗∑𝐵𝑖𝑘𝜌𝑖𝑗𝐵𝑗𝑘𝑑𝑡

𝑛

𝑘=1

𝑚

𝑖,𝑗=1

= (∑𝜕ℎ

𝜕𝑆𝑖𝐴𝑖

𝑚

𝑖=1

+1

2∑

𝜕2ℎ

𝜕𝑆𝑖𝜕𝑆𝑗𝛴𝑖𝑗

𝑚

𝑖,𝑗=1

)𝑑𝑡 +∑𝜕ℎ

𝜕𝑆𝑖

𝑚

𝑖=1

∑𝐵𝑖𝑘𝑑𝑊𝑘

𝑛

𝑘=1

(4)

where 𝛴 = 𝐵𝜌𝐵′ is the 𝑚 ×𝑚 instantaneous variance-covariance matrix of 𝑑𝑆. Integrating on both sides

of (4) from 𝑡 to 𝑇, we have

ℎ(𝑆𝑇) − ℎ(𝑆𝑡) = ∫ (∑𝜕ℎ

𝜕𝑆𝑖𝐴𝑖

𝑚

𝑖=1

+1

2∑

𝜕2ℎ

𝜕𝑆𝑖𝜕𝑆𝑗𝛴𝑖𝑗

𝑚

𝑖,𝑗=1

)𝑑𝑢𝑇

𝑡

+∫ ∑𝜕ℎ

𝜕𝑆𝑖

𝑚

𝑖=1

∑𝐵𝑖𝑘𝑑𝑊𝑘

𝑛

𝑘=1

𝑇

𝑡

(5)

Taking expectation on both sides of (5), we get (using notation 𝔼𝑡[∙] = 𝔼[∙|ℱ𝑡])

LHS = 𝔼𝑡[ℎ(𝑆𝑇)] − ℎ(𝑆𝑡) = ∫ℎ𝑦𝑝𝑇,𝑦|𝑡,𝑥𝑑𝑦𝛺

− ℎ𝑥

RHS = 𝔼𝑡 [∫ (∑𝜕ℎ

𝜕𝑆𝑖𝐴𝑖

𝑚

𝑖=1

+1

2∑

𝜕2ℎ

𝜕𝑆𝑖𝜕𝑆𝑗𝛴𝑖𝑗

𝑚

𝑖,𝑗=1

)𝑑𝑢𝑇

𝑡

] + 𝔼𝑡 [∫ ∑𝜕ℎ

𝜕𝑆𝑖

𝑚

𝑖=1

∑𝐵𝑖𝑘𝑑𝑊𝑘

𝑛

𝑘=1

𝑇

𝑡

]⏟

=0

= ∫ ∑𝔼𝑡 [𝜕ℎ

𝜕𝑆𝑖𝐴𝑖]

𝑚

𝑖=1

𝑑𝑢𝑇

𝑡

+1

2∫ ∑ 𝔼𝑡 [

𝜕2ℎ

𝜕𝑆𝑖𝜕𝑆𝑗𝛴𝑖𝑗]

𝑚

𝑖,𝑗=1

𝑑𝑢𝑇

𝑡

(6)

where 𝑝𝑇,𝑦|𝑡,𝑥 is the transition probability density having 𝑆𝑇 = 𝑦 at 𝑇 given 𝑆𝑡 = 𝑥 at 𝑡 (i.e. if we solve

the equation (1) with the initial condition 𝑆𝑡 = 𝑥 ∈ ℝ𝑚 , then the random variable 𝑆𝑇 = 𝑦 ∈ 𝛺 has a

density 𝑝𝑇,𝑦|𝑡,𝑥 in the 𝑦 variable at time 𝑇). Differentiating (6) with respect to 𝑇 on both sides, we have

∫ ℎ𝑦𝜕𝑝𝑇,𝑦|𝑡,𝑥𝜕𝑇

𝑑𝑦𝛺

=∑𝔼𝑡 [𝜕ℎ

𝜕𝑆𝑖𝐴𝑖]

𝑚

𝑖=1

+1

2∑ 𝔼𝑡 [

𝜕2ℎ

𝜕𝑆𝑖𝜕𝑆𝑗𝛴𝑖𝑗]

𝑚

𝑖,𝑗=1

=∑∫𝜕ℎ𝑦𝜕𝑦𝑖

𝐴𝑖𝑝𝑇,𝑦|𝑡,𝑥𝑑𝑦𝛺

𝑚

𝑖=1

+1

2∑ ∫

𝜕2ℎ𝑦𝜕𝑦𝑖𝜕𝑦𝑗

𝛴𝑖𝑗𝑝𝑇,𝑦|𝑡,𝑥𝑑𝑦𝛺

𝑚

𝑖,𝑗=1

(7)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

7

If we assume 𝛺 ≡ ℝ𝑚 and also assume the probability density 𝑝 and its first derivatives 𝜕𝑝/𝜕𝑦𝑖 vanish at

a higher order of rate than ℎ and 𝜕ℎ/𝜕𝑦𝑖 as 𝑦𝑖 → ±∞ ∀ 𝑖 = 1,⋯ ,𝑚, then we can integrate by parts for

the right hand side of (7), once for the first integral and twice for the second

∫𝜕ℎ𝑦𝜕𝑦𝑖

𝐴𝑖𝑝𝑑𝑦𝛺

= ∫ ℎ𝑦𝐴𝑖𝑝|𝑦𝑖 =−∞+∞

⏟ =0

𝑑𝑦−𝑖𝛺−𝑖

−∫ ℎ𝑦𝜕(𝐴𝑖𝑝)

𝜕𝑦𝑖𝑑𝑦

𝛺

and

∫𝜕2ℎ𝑦𝜕𝑦𝑖𝜕𝑦𝑗

𝛴𝑖𝑗𝑝𝑑𝑦𝛺

= ∫𝜕ℎ𝑦𝜕𝑦𝑗

𝛴𝑖𝑗𝑝|𝑦𝑖=−∞

+∞

⏟ =0

𝑑�̅�𝑖�̅�𝑖

−∫𝜕ℎ𝑦𝜕𝑦𝑗

𝜕(𝛴𝑖𝑗𝑝)

𝜕𝑦𝑖𝑑𝑦

𝛺

= −∫ ℎ𝑦𝜕(𝛴𝑖𝑗𝑝)

𝜕𝑦𝑖|𝑦𝑗=−∞

+∞

⏟ =0

𝑑�̅�𝑗�̅�𝑗

+∫ ℎ𝑦𝜕2(𝛴𝑖𝑗𝑝)

𝜕𝑦𝑖𝜕𝑦𝑗𝑑𝑦

𝛺

where ∫ (∙)𝑑�̅�𝑖�̅�𝑖

= ∫ ⋯∫ ∫ ⋯∫(∙)𝑑𝑦1ℝ

⋯𝑑𝑦𝑖−1ℝ

𝑑𝑦𝑖+1ℝ

⋯𝑑𝑦𝑚ℝ

(8)

Plugging the results of (8) into (7), we have

∫ ℎ𝑦𝜕𝑝

𝜕𝑇𝑑𝑦

𝛺

= −∑∫ ℎ𝑦𝜕(𝐴𝑖𝑝)

𝜕𝑦𝑖𝑑𝑦

𝛺

𝑚

𝑖=1

+1

2∑ ∫ ℎ𝑦

𝜕2(𝛴𝑖𝑗𝑝)

𝜕𝑦𝑖𝜕𝑦𝑗𝑑𝑦

𝛺

𝑚

𝑖,𝑗=1

⟹∫ ℎ𝑦 (𝜕𝑝

𝜕𝑇+∑

𝜕(𝐴𝑖𝑝)

𝜕𝑦𝑖

𝑚

𝑖=1

−1

2∑

𝜕2(𝛴𝑖𝑗𝑝)

𝜕𝑦𝑖𝜕𝑦𝑗

𝑚

𝑖,𝑗=1

)𝑑𝑦𝛺

= 0

(9)

By the arbitrariness of ℎ, we conclude that for any 𝑦 ∈ 𝛺

𝜕𝑝

𝜕𝑇+∑

𝜕(𝐴𝑖𝑝)

𝜕𝑦𝑖

𝑚

𝑖=1

−1

2∑

𝜕2(𝛴𝑖𝑗𝑝)

𝜕𝑦𝑖𝜕𝑦𝑗

𝑚

𝑖,𝑗=1

= 0, 𝛴 = 𝐵𝜌𝐵′ (10)

This is the Multi-dimensional Fokker-Planck Equation (a.k.a. Kolmogorov Forward Equation) [1]. In this

equation, the 𝑡 and 𝑥 are held constant, while the 𝑇 and 𝑦 are variables (called “forward variables”). In

the one-dimensional case, it reduces to

𝜕𝑝

𝜕𝑇+𝜕(𝐴𝑝)

𝜕𝑦−1

2

𝜕2(𝐵2𝑝)

𝜕𝑦2= 0 (11)

where 𝐴 = 𝐴(𝑇, 𝑦) and 𝐵 = 𝐵(𝑇, 𝑦) are then scalar functions.

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

8

1.2. Kolmogorov Backward Equation

Let’s express conditional expectation of ℎ(𝑆𝑡) by 𝑔(𝑡, 𝑆𝑡) = 𝔼𝑡[ℎ(𝑆𝑇)]. Because for 𝑜 ≤ 𝑡 ≤ 𝑇

we have

𝑔(𝑜, 𝑆𝑜) = 𝔼𝑜[ℎ(𝑆𝑇)] = 𝔼𝑜[𝔼𝑡[ℎ(𝑆𝑇)]] = 𝔼𝑜[𝑔(𝑡, 𝑆𝑡)] (12)

the 𝑔(𝑡, 𝑆𝑡) is a martingale by the tower rule (i.e. If ℋ holds less information than 𝒢 , then

𝔼[𝔼[𝑋|𝒢]|ℋ] = 𝔼[𝑋|ℋ]). The dynamics of the 𝑔(𝑡, 𝑆𝑡) is given by

𝑑𝑔 =𝜕𝑔

𝜕𝑡𝑑𝑡 + 𝐽𝑔

1×𝑚

𝑑𝑆𝑡𝑚×1

+1

2𝑑𝑆𝑡

′

1×𝑚𝐻𝑔𝑚×𝑚

𝑑𝑆𝑡𝑚×1

=𝜕𝑔

𝜕𝑡𝑑𝑡 + 𝐽𝑔𝐴𝑑𝑡 + 𝐽𝑔𝐵𝑑𝑊𝑡 +

1

2𝑑𝑊𝑡

′𝐵′𝐻𝑔𝐵𝑑𝑊𝑡

(13)

where 𝐽𝑔 is the Jacobian (i.e. the same as gradient if 𝑔 is a scalar-valued function) and 𝐻𝑔 the Hessian of

𝑔 with respect to 𝑆 (with subscripts denoting the indices of vector components)

𝐽𝑔 = (𝜕𝑔

𝜕𝑆1⋯

𝜕𝑔

𝜕𝑆𝑚) , 𝐻𝑔 =

(

𝜕2𝑔

𝜕𝑆12 ⋯

𝜕2𝑔

𝜕𝑆1𝜕𝑆𝑚⋮ ⋱ ⋮𝜕2𝑔

𝜕𝑆𝑚𝜕𝑆1⋯

𝜕2𝑔

𝜕𝑆𝑚2 )

(14)

Expanding (13), we have

𝑑𝑔 = (𝜕𝑔

𝜕𝑡+∑

𝜕𝑔

𝜕𝑆𝑖𝐴𝑖

𝑚

𝑖=1

+1

2∑

𝜕2𝑔

𝜕𝑆𝑖𝜕𝑆𝑗𝛴𝑖𝑗

𝑚

𝑖,𝑗=1

)𝑑𝑡 +∑𝜕𝑔

𝜕𝑆𝑖

𝑚

𝑖=1

∑𝐵𝑖𝑘𝑑𝑊𝑘

𝑛

𝑘=1

(15)

Since 𝑔(𝑡, 𝑆𝑡) is a martingale, the 𝑑𝑡-term must vanish, which gives

𝜕𝑔

𝜕𝑡+∑

𝜕𝑔

𝜕𝑆𝑖𝐴𝑖

𝑚

𝑖=1

+1

2∑

𝜕2𝑔

𝜕𝑆𝑖𝜕𝑆𝑗𝛴𝑖𝑗

𝑚

𝑖,𝑗=1

= 0 (16)

This is the multi-dimensional Feynman-Kac formula1.

Using the transition probability density 𝑝𝑇,𝑦|𝑡,𝑥, we can write the expectation as

1 https://en.wikipedia.org/wiki/Feynman-Kac_formula

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

9

𝑔𝑡,𝑥 = 𝔼𝑡[ℎ(𝑆𝑇)] = ∫ℎ𝑦𝑝𝑇,𝑦|𝑡,𝑥𝑑𝑦𝛺

(17)

The formula (16) defines that

𝜕

𝜕𝑡∫ℎ𝑦𝑝𝑑𝑦𝛺

+∑𝐴𝑖𝜕

𝜕𝑥𝑖∫ℎ𝑦𝑝𝑑𝑦𝛺

𝑚

𝑖=1

+1

2∑ 𝛴𝑖𝑗

𝜕2

𝜕𝑥𝑖𝜕𝑥𝑗∫ℎ𝑦𝑝𝑑𝑦𝛺

𝑚

𝑖,𝑗=1

= 0

⟹∫ ℎ𝑦 (𝜕𝑝

𝜕𝑡+∑𝐴𝑖

𝜕𝑝

𝜕𝑥𝑖

𝑚

𝑖=1

+1

2∑ 𝛴𝑖𝑗

𝜕2𝑝

𝜕𝑥𝑖𝜕𝑥𝑗

𝑚

𝑖,𝑗=1

)𝑑𝑦𝛺

= 0

(18)

By the arbitrariness of ℎ, we have

𝜕𝑝

𝜕𝑡+∑𝐴𝑖

𝜕𝑝

𝜕𝑥𝑖

𝑚

𝑖=1

+1

2∑ 𝛴𝑖𝑗

𝜕2𝑝

𝜕𝑥𝑖𝜕𝑥𝑗

𝑚

𝑖,𝑗=1

= 0, 𝛴 = 𝐵𝜌𝐵′ (19)

This is the multi-dimensional Kolmogorov Backward Equation. In this equation, the 𝑇 and 𝑦 are held

constant, while the 𝑡 and 𝑥 are variables (called “backward variables”). In the 1-D case, it reduces to

𝜕𝑝

𝜕𝑡+ 𝐴

𝜕𝑝

𝜕𝑥+1

2𝐵2𝜕2𝑝

𝜕𝑥2= 0 (20)

where 𝐴 = 𝐴(𝑡, 𝑥) and 𝐵 = 𝐵(𝑡, 𝑥) are then scalar functions.

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

10

2. HESTON MODEL

In this chapter, we will briefly introduce the Heston stochastic volatility model, which has become

quite popular in industry to model volatility smiles. One of the reasons for that is that vanilla options in

Heston model have close form solutions. This makes the calibration of the model computationally much

efficient and accurate. To understand these closed form formulas, we will introduce the Fourier transform

method for option pricing and its application to the Heston model. Additionally, a characteristic function

based method is also discussed, which extends the Heston model to have piecewise time-dependent

parameters.

2.1. Heston Stochastic Volatility Model

The stochastic volatility in Heston’s model is a mean-reverting square-root process defined by the

following stochastic differential equations (SDE)

𝑑𝑆𝑡𝑆𝑡= (𝜇 − 𝑞)𝑑𝑡 + √𝑣𝑡𝑑𝑊1,𝑡

𝑑𝑣𝑡 = 𝜖(𝜗 − 𝑣𝑡)𝑑𝑡 + 𝜉√𝑣𝑡𝑑𝑊2,𝑡

𝑑𝑊1,𝑡𝑑𝑊2,𝑡 = 𝜌𝑑𝑡

(21)

where 𝑡 denotes the time, 𝑆𝑡 the spot process, 𝜇 and 𝑞 the drift and dividend of the spot, 𝑣𝑡 the variance

process, 𝜖 the mean reversion rate, 𝜗 the mean variance, 𝜉 the volatility of the variance and 𝑑𝑊1,𝑡, 𝑑𝑊2,𝑡

the two Brownian motions correlated by 𝜌 under physical measure ℙ. All the parameters 𝜇, 𝑞, 𝜖, 𝜗 and 𝜌

are time and state homogenous (invariant).

2.1.1. Market Price of Risk

In the Black-Scholes model, a contingent claim is dependent on one or more tradable assets 𝑆𝑡.

The randomness in the option value is solely due to the randomness of these tradable assets. Therefore,

the option can be hedged by continuously trading the underlying. This makes the market complete (i.e.

every contingent claim can be replicated). In a stochastic volatility model, a contingent claim is dependent

on both the randomness of the asset 𝑆𝑡 and the randomness associated with the instantaneous volatility 𝑣𝑡

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

11

of the asset. Since the volatility is not a traded asset, this renders the market incomplete and has many

implications to the pricing of options.

Firstly let’s consider two arbitrary derivative securities (presume they are available in the traded

markets) whose prices can be written as functions 𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡) and 𝑉(𝑡, 𝑆𝑡 , 𝑣𝑡) of variables 𝑡, 𝑆𝑡 and 𝑣𝑡

respectively. We construct a self-financing portfolio with a price process 𝑋𝑡 by having long one share of

𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡), short 𝛤𝑡 shares of 𝑉(𝑡, 𝑆𝑡 , 𝑣𝑡) and short 𝛥𝑡 shares of 𝑆𝑡, that is

𝑋𝑡 = 𝑈𝑡 − 𝛤𝑡𝑉𝑡 − 𝛥𝑡𝑆𝑡 (22)

Following the Ito’s lemma, we can derive the price dynamics of the derivative as

𝑑𝑈 =𝜕𝑈

𝜕𝑡𝑑𝑡 +

𝜕𝑈

𝜕𝑆𝑑𝑆 +

1

2

𝜕2𝑈

𝜕𝑆2𝑑𝑆𝑑𝑆 +

𝜕𝑈

𝜕𝑣𝑑𝑣 +

1

2

𝜕2𝑈

𝜕𝑣2𝑑𝑣𝑑𝑣 +

𝜕2𝑈

𝜕𝑣𝜕𝑆𝑑𝑣𝑑𝑆

=𝜕𝑈

𝜕𝑡𝑑𝑡 +

𝜕𝑈

𝜕𝑆(𝜇 − 𝑞)𝑆𝑑𝑡 +

𝜕𝑈

𝜕𝑆𝑆√𝑣𝑑𝑊1 +

𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2𝑑𝑡 +

𝜕𝑈

𝜕𝑣𝜖(𝜗 − 𝑣)𝑑𝑡 +

𝜕𝑈

𝜕𝑣𝜉√𝑣𝑑𝑊2

+𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2𝑑𝑡 + 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆𝑑𝑡

(23)

and derive the price dynamics of the self-financing portfolio as

𝑑𝑋 = 𝑑𝑈 − 𝛤𝑑𝑉 − 𝛥𝑑𝑆 − 𝛥𝑆𝑞𝑑𝑡

= (𝜕𝑈

𝜕𝑡+𝜕𝑈

𝜕𝑆(𝜇 − 𝑞)𝑆 +

𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2+𝜕𝑈

𝜕𝑣𝜖(𝜗 − 𝑣) +

𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆)𝑑𝑡

−𝛤 (𝜕𝑉

𝜕𝑡+𝜕𝑉

𝜕𝑆(𝜇 − 𝑞)𝑆 +

𝑣𝑆2

2

𝜕2𝑉

𝜕𝑆2+𝜕𝑉

𝜕𝑣𝜖(𝜗 − 𝑣) +

𝑣𝜉2

2

𝜕2𝑉

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑉

𝜕𝑣𝜕𝑆) 𝑑𝑡

+(𝜕𝑈

𝜕𝑆− 𝛥 − 𝛤

𝜕𝑉

𝜕𝑆) 𝑆√𝑣𝑑𝑊1 + (

𝜕𝑈

𝜕𝑣− 𝛤

𝜕𝑉

𝜕𝑣) 𝜉√𝑣𝑑𝑊2 − 𝛥(𝜇 − 𝑞)𝑆𝑑𝑡 − 𝛥𝑆𝑞𝑑𝑡

(24)

In order to eliminate both spot and volatility risk, we must have

𝜕𝑈

𝜕𝑆− 𝛥 − 𝛤

𝜕𝑉

𝜕𝑆= 0 and

𝜕𝑈

𝜕𝑣− 𝛤

𝜕𝑉

𝜕𝑣= 0 (25)

and therefore

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

12

𝑑𝑋 = (𝜕𝑈

𝜕𝑡+𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2+𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆−𝜕𝑈

𝜕𝑆𝑆𝑞)𝑑𝑡

− 𝛤 (𝜕𝑉

𝜕𝑡+𝑣𝑆2

2

𝜕2𝑉

𝜕𝑆2+𝑣𝜉2

2

𝜕2𝑉

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑉

𝜕𝑣𝜕𝑆−𝜕𝑉

𝜕𝑆𝑆𝑞)𝑑𝑡

(26)

In this case, the portfolio is riskless and must have a return at risk free rate in order to avoid arbitrage

𝑑𝑋 = 𝑟𝑋𝑑𝑡 = 𝑟(𝑈 − 𝛤𝑉 − 𝛥𝑆)𝑑𝑡 = 𝑟𝑈𝑑𝑡 − 𝑟𝛤𝑉𝑑𝑡 − 𝑟𝜕𝑈

𝜕𝑆𝑆𝑑𝑡 + 𝑟𝛤

𝜕𝑉

𝜕𝑆𝑆𝑑𝑡 (27)

which in turn gives

𝜕𝑈𝜕𝑡+𝑣𝑆2

2𝜕2𝑈𝜕𝑆2

+𝑣𝜉2

2𝜕2𝑈𝜕𝑣2

+ 𝑆𝑣𝜉𝜌𝜕2𝑈𝜕𝑣𝜕𝑆

+𝜕𝑈𝜕𝑆𝑆(𝑟 − 𝑞) − 𝑟𝑈

𝜕𝑈𝜕𝑣

=

𝜕𝑉𝜕𝑡+𝑣𝑆2

2𝜕2𝑉𝜕𝑆2

+𝑣𝜉2

2𝜕2𝑉𝜕𝑣2

+ 𝑆𝑣𝜉𝜌𝜕2𝑉𝜕𝑣𝜕𝑆

+𝜕𝑉𝜕𝑆𝑆(𝑟 − 𝑞) − 𝑟𝑉

𝜕𝑉𝜕𝑣

≡ 𝜂

(28)

In the above equation, the left-hand side is a function of 𝑈 only and the right-hand side is a function of 𝑉

only. The only way for the equality to hold is for both sides to equal a common function 𝜂 of the

independent variables 𝑡, 𝑆𝑡 and 𝑣𝑡.

Now let’s consider a delta-neutral portfolio 𝑌𝑡 by having long one share of 𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡) and short

𝛥𝑡 shares of 𝑆𝑡

𝑌𝑡 = 𝑈𝑡 − 𝛥𝑡𝑆𝑡 (29)

The price dynamics of the portfolio is

𝑑𝑌 = 𝑑𝑈 − 𝛥𝑑𝑆 − 𝛥𝑆𝑞𝑑𝑡

= (𝜕𝑈

𝜕𝑡+𝜕𝑈

𝜕𝑆(𝜇 − 𝑞)𝑆 +

𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2+𝜕𝑈

𝜕𝑣𝜖(𝜗 − 𝑣) +

𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆)𝑑𝑡

+ (𝜕𝑈

𝜕𝑆− 𝛥) 𝑆√𝑣𝑑𝑊1 +

𝜕𝑈

𝜕𝑣𝜉√𝑣𝑑𝑊2 − 𝛥(𝜇 − 𝑞)𝑆𝑑𝑡 − 𝛥𝑆𝑞𝑑𝑡

(30)

Since delta-neutral implies 𝜕𝑈

𝜕𝑆− 𝛥 = 0, we are able to derive the dynamics of the discounted portfolio, a

martingale under risk neutral measure, as

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

13

𝑑(𝐷𝑡𝑌𝑡)

𝐷𝑡= 𝑑𝑌 − 𝑟𝑌𝑑𝑡 = 𝑑𝑈 − 𝛥𝑑𝑆 − 𝛥𝑆𝑞𝑑𝑡 − 𝑟𝑈𝑑𝑡 + 𝑟𝛥𝑆𝑑𝑡

= (𝜕𝑈

𝜕𝑣𝜖(𝜗 − 𝑣) +

𝜕𝑈

𝜕𝑡+𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2+𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆+𝜕𝑈

𝜕𝑆𝑆(𝑟 − 𝑞) − 𝑟𝑈)𝑑𝑡

+𝜕𝑈

𝜕𝑣𝜉√𝑣𝑑𝑊2

=𝜕𝑈

𝜕𝑣(𝜖(𝜗 − 𝑣) + 𝜂)𝑑𝑡 +

𝜕𝑈

𝜕𝑣𝜉√𝑣𝑑𝑊2 =

𝜕𝑈

𝜕𝑣𝜉√𝑣𝑑�̃�2

(31)

by defining

𝑑�̃�2 = 𝑑𝑊2 + 𝜙2𝑑𝑡 and 𝜙2 = 𝜖(𝜗 − 𝑣) + 𝜂

𝜉√𝑣 (32)

In the above, the �̃�2 is a Brownian motion under risk neutral measure ℚ and 𝜙2 is the market price of

volatility risk.

We next consider a vega-neutral portfolio 𝑍𝑡 by having long a share of 𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡) and short 𝛤𝑡

shares of 𝑉(𝑡, 𝑆𝑡 , 𝑣𝑡)

𝑍𝑡 = 𝑈𝑡 − 𝛤𝑡𝑉𝑡 (33)

The dynamics of the portfolio reads

𝑑𝑍 = 𝑑𝑈 − 𝛤𝑑𝑉

= (𝜕𝑈

𝜕𝑡+𝜕𝑈

𝜕𝑆(𝜇 − 𝑞)𝑆 +

𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2+𝜕𝑈

𝜕𝑣𝜖(𝜗 − 𝑣) +

𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆)𝑑𝑡

−𝛤 (𝜕𝑉

𝜕𝑡+𝜕𝑉

𝜕𝑆(𝜇 − 𝑞)𝑆 +

𝑣𝑆2

2

𝜕2𝑉

𝜕𝑆2+𝜕𝑉

𝜕𝑣𝜖(𝜗 − 𝑣) +

𝑣𝜉2

2

𝜕2𝑉

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑉

𝜕𝑣𝜕𝑆) 𝑑𝑡

+(𝜕𝑈

𝜕𝑆− 𝛤

𝜕𝑉

𝜕𝑆) 𝑆√𝑣𝑑𝑊1 + (

𝜕𝑈

𝜕𝑣− 𝛤

𝜕𝑉

𝜕𝑣) 𝜉√𝑣𝑑𝑊2

(34)

Since vega-neutral implies 𝜕𝑈

𝜕𝑣− 𝛤

𝜕𝑉

𝜕𝑣= 0, we can derived the dynamics of the discounted portfolio as

𝑑(𝐷𝑡𝑍𝑡)

𝐷𝑡= 𝑑𝑍 − 𝑟𝑍𝑑𝑡 = 𝑑𝑈 − 𝛤𝑑𝑉 − 𝑟𝑈𝑑𝑡 + 𝑟𝛤𝑉𝑑𝑡 (35)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

14

= (𝜕𝑈

𝜕𝑡+𝜕𝑈

𝜕𝑆(𝜇 − 𝑞)𝑆 +

𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2+𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆− 𝑟𝑈)𝑑𝑡

− 𝛤 (𝜕𝑉

𝜕𝑡+𝜕𝑉

𝜕𝑆(𝜇 − 𝑞)𝑆 +

𝑣𝑆2

2

𝜕2𝑉

𝜕𝑆2+𝑣𝜉2

2

𝜕2𝑉

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑉

𝜕𝑣𝜕𝑆− 𝑟𝑉)𝑑𝑡

+ (𝜕𝑈

𝜕𝑆− 𝛤

𝜕𝑉

𝜕𝑆) 𝑆√𝑣𝑑𝑊1

= (𝜕𝑈

𝜕𝑡+𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2+𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆− 𝑟𝑈)𝑑𝑡

− 𝛤 (𝜕𝑉

𝜕𝑡+𝑣𝑆2

2

𝜕2𝑉

𝜕𝑆2+𝑣𝜉2

2

𝜕2𝑉

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑉

𝜕𝑣𝜕𝑆− 𝑟𝑉)𝑑𝑡 + (

𝜕𝑈

𝜕𝑆− 𝛤

𝜕𝑉

𝜕𝑆) 𝑑𝑆

= (𝜂𝜕𝑈

𝜕𝑣−𝜕𝑈

𝜕𝑆𝑆(𝑟 − 𝑞) − 𝛤𝜂

𝜕𝑉

𝜕𝑣+ 𝛤

𝜕𝑉

𝜕𝑆𝑆(𝑟 − 𝑞))𝑑𝑡 + (

𝜕𝑈

𝜕𝑆− 𝛤

𝜕𝑉

𝜕𝑆) 𝑑𝑆

= (𝜕𝑈

𝜕𝑆− 𝛤

𝜕𝑉

𝜕𝑆) (𝑑𝑆 − 𝑆(𝑟 − 𝑞)𝑑𝑡) = (

𝜕𝑈

𝜕𝑆− 𝛤

𝜕𝑉

𝜕𝑆) 𝑆 ((𝜇 − 𝑟)𝑑𝑡 + √𝑣𝑑𝑊1)

= (𝜕𝑈

𝜕𝑆− 𝛤

𝜕𝑉

𝜕𝑆) 𝑆√𝑣𝑑�̃�1

by defining

𝑑�̃�1 = 𝑑𝑊1 + 𝜙1𝑑𝑡 and 𝜙1 = 𝜇 − 𝑟

√𝑣 (36)

where 𝑑�̃�1 is a Brownian motion under risk neutral measure ℚ and 𝜙1 is the market price of spot risk.

According to (32) and (36), the Heston SDE (21) can be written under risk neutral measure as

𝑑𝑆𝑡𝑆𝑡= (𝜇 − 𝑞)𝑑𝑡 + √𝑣𝑡(𝑑�̃�1,𝑡 − 𝜙1𝑑𝑡) = (𝑟 − 𝑞)𝑑𝑡 + √𝑣𝑡𝑑�̃�1,𝑡

𝑑𝑣𝑡 = 𝜖(𝜗 − 𝑣𝑡)𝑑𝑡 + 𝜉√𝑣𝑡(𝑑�̃�2,𝑡 − 𝜙2𝑑𝑡) = (𝜖(𝜗 − 𝑣𝑡) − 𝜙2𝜉√𝑣𝑡)𝑑𝑡 + 𝜉√𝑣𝑡𝑑�̃�2,𝑡

(37)

Based on the Consumption-based Capital Asset Pricing Model, Heston [22] assumes that the market price

of volatility risk is proportional to volatility, that is

𝜙2 = 𝑐√𝑣 for a constant 𝑐 ⟹ 𝜙2𝜉√𝑣 = 𝑐𝜉𝑣 = 𝜆𝑣 where 𝜆 = 𝑐𝜉 (38)

If we define

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

15

𝜅 = 𝜖 + 𝜆 and 𝜃 =𝜖𝜗

𝜅 (39)

then the Heston SDE under risk neutral measure ℚ becomes

𝑑𝑆𝑡𝑆𝑡= (𝑟 − 𝑞)𝑑𝑡 + √𝑣𝑡𝑑�̃�1,𝑡 , 𝑑𝑣𝑡 = 𝜅(𝜃 − 𝑣𝑡)𝑑𝑡 + 𝜉√𝑣𝑡𝑑�̃�2,𝑡 , 𝑑�̃�1,𝑡𝑑�̃�2,𝑡 = 𝜌𝑑𝑡 (40)

which retains the form of the equation under the transformation from the physical measure ℙ to the risk

neutral measure ℚ.

Since the volatility is not a traded asset, the incompleteness of the market implies the risk neutral

measure is not unique and depends on the value of the market price of volatility risk 𝜙2. To estimate the

model parameters, one may calibrate the Heston’s model using historical spot data, however the historical

calibration does not allow for the estimation of 𝜙2. Instead of using the spot data, one may also calibrate

the model to the volatility smile (i.e. prices of vanilla options). In this case, the market price of volatility

risk has already been implied in the market smile, and consequently embedded into the calibrated model

parameters 𝜅 and 𝜃 through (39).

2.1.2. Radon-Nikodym Derivative

The change of measure from ℙ to ℚ is achieved through Radon-Nikodym derivative via multi-

dimensional Girsanov’s theorem [2]. To derive this derivative, we may write correlated 𝑛-dimensional

Brownian motions as 𝑑𝑊𝑡 and 𝑑�̃�𝑡 under physical measure ℙ and risk neutral measure ℚ respectively.

The matrix 𝜌 denotes the instantaneous correlation, e.g. 𝑑𝑊𝑡𝑑𝑊𝑡′ = 𝜌𝑑𝑡. It should be noted that 𝑑𝑊𝑡 and

𝑑�̃�𝑡 possess the same correlation structure only if each is under its own probability measure, ℙ or ℚ,

otherwise this property does not hold. From (32) and (36), we represent the market price of risk by

correlation matrix an 𝑛-dimensional vector 𝜙 such that

𝑑�̃�𝑡 = 𝑑𝑊𝑡 + 𝜌𝜙𝑡𝑑𝑡 (41)

The Radon-Nikodym derivative is then given for 𝑡 > 𝑜 by

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

16

𝑑ℚ

𝑑ℙ= exp(−

1

2∫ 𝜙𝑢

′ 𝜌𝜙𝑢𝑑𝑢𝑡

𝑜

−∫ 𝜙𝑢′ 𝑑𝑊𝑢

𝑡

𝑜

) (42)

To check this, let’s assume under ℚ we have a martingale process

𝑋𝑡 = 𝑋𝑜 exp(−1

2∫ 𝜎𝑢

′𝜌𝜎𝑢𝑑𝑢𝑡

𝑜

+∫ 𝜎𝑢′𝑑�̃�𝑢

𝑡

𝑜

) (43)

where 𝜎𝑢is a vector representing an adapted volatility process. According to (41) we have

𝑋𝑡 = 𝑋𝑜 exp(−1

2∫ 𝜎𝑢

′𝜌𝜎𝑢𝑑𝑢𝑡

𝑜

+∫ 𝜎𝑢′𝑑𝑊𝑢

𝑡

𝑜

+∫ 𝜎𝑢′𝜌𝜙𝑢𝑑𝑢

𝑡

𝑜

) and

𝑋𝑡𝑑ℚ

𝑑ℙ= 𝑋𝑜 exp(−

1

2∫ 𝜎𝑢

′𝜌𝜎𝑢𝑑𝑢𝑡

𝑜

+∫ 𝜎𝑢′𝜌𝜙𝑢𝑑𝑢

𝑡

𝑜

−1

2∫ 𝜙𝑢

′ 𝜌𝜙𝑢𝑑𝑢𝑡

𝑜

+∫ (𝜎𝑢 − 𝜙𝑢)′𝑑𝑊𝑢

𝑡

𝑜

)

= 𝑋𝑜 exp(−1

2∫ (𝜎𝑢 − 𝜙𝑢)

′𝜌(𝜎𝑢 − 𝜙𝑢)𝑑𝑢𝑡

𝑜

+∫ (𝜎𝑢 − 𝜙𝑢)′𝑑𝑊𝑢

𝑡

𝑜

)

(44)

The 𝑋𝑡𝑑ℚ

𝑑ℙ is a martingale under ℙ. Hence we have the following equation

�̃�𝑜[𝑋𝑡] = 𝔼𝑜 [𝑋𝑡𝑑ℚ

𝑑ℙ] = 𝑋𝑜 (45)

as expected.

2.1.3. Feller Condition

Feller observed that the variance process 𝑣𝑡 in (40) remains strictly positive with probability one

for all times 𝑡 > 𝑜, if 𝑣𝑜 > 0 and the Feller condition [3] [4] is satisfied

2𝜅𝜃 ≥ 𝜉2 (46)

If the condition is not satisfied, i.e. 0 < 2𝜅𝜃 < 𝜉2, the variance will visit zero recurrently but will not stay

at zero, i.e. the zero boundary is strongly reflecting. In typical applications, the Feller condition is often

violated due to the convexities of volatility smiles typically encountered in practice. Indeed the process

𝑣𝑡 often has a strong affinity for the area around the origin. However, this is not a complete disaster, as

the process 𝑣𝑡 can only hit zero for an infinitesimally small amount of time.

2.2. Probability Distribution of Spot Returns

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

17

In this section, we present a derivation of the distribution of the spot returns in Heston’s model [5].

Let’s firstly make a change of variable from (21) to have a centered log-spot for 𝑡 > 𝑜

𝑥𝑡 = ln𝑆𝑡𝐹𝑜,𝑡

= ln𝑆𝑡

𝑆𝑜 exp((𝑟 − 𝑞)(𝑡 − 𝑜))= ln

𝑆𝑡𝑆𝑜− (𝑟 − 𝑞)(𝑡 − 𝑜) (47)

The Heston’s model (40) under ℚ can then be converted by Ito’s lemma to the following form

𝑑𝑥𝑡 = −𝑣𝑡2𝑑𝑡 + √𝑣𝑡𝑑�̃�1,𝑡 , 𝑑𝑣𝑡 = 𝜅(𝜃 − 𝑣𝑡)𝑑𝑡 + 𝜉√𝑣𝑡𝑑�̃�2,𝑡 , 𝑑�̃�1,𝑡𝑑�̃�2,𝑡 = 𝜌𝑑𝑡 (48)

This defines a 2-D stochastic process characterized by a joint transition probability density function

𝑝𝑡,𝑥,𝑣|𝑣𝑜, which is the probability having log-spot 𝑥𝑡 and instantaneous variance 𝑣𝑡 at time 𝑡, conditional

on 𝑣𝑜 at time 𝑡 = 𝑜 (independent on 𝑥𝑜 because 𝑥𝑜 = 0 almost surely).

2.2.1. Derivation of the Transition Probability

We may rewrite (48) in terms of a 2-D Brownian motion 𝑑�̃�𝑡

𝑑𝑍𝑡 = 𝐴𝑡𝑑𝑡 + 𝐶𝑡𝑑�̃�𝑡 with

𝑍𝑡 = (𝑥𝑡𝑣𝑡) , 𝐴𝑡 = (

−𝑣𝑡2

𝜅(𝜃 − 𝑣𝑡)) , 𝐶𝑡 = (

√𝑣𝑡 0

0 𝜉√𝑣𝑡) , 𝑑�̃�𝑡𝑑�̃�𝑡

′ = (1 𝜌𝜌 1

)𝑑𝑡 (49)

The instantaneous covariance matrix of 𝑑𝑍𝑡 becomes

𝛴𝑡 = 𝐶𝑡 (1 𝜌𝜌 1

)𝐶𝑡 = (𝑣𝑡 𝜌𝜉𝑣𝑡𝜌𝜉𝑣𝑡 𝜉2𝑣𝑡

) (50)

The 2-D Markov process is characterized by the transition probability 𝑝𝑡,𝑥,𝑣|𝑥𝑜,𝑣𝑜 . The Fokker-Planck

equation that governs the time evolution of the transition probability is given by (10)

𝜕𝑝

𝜕𝑡−1

2

𝜕(𝑣𝑝)

𝜕𝑥+𝜕(𝜅(𝜃 − 𝑣)𝑝)

𝜕𝑣−1

2

𝜕2(𝑣𝑝)

𝜕𝑥2− 𝜌𝜉

𝜕2(𝑣𝑝)

𝜕𝑥𝜕𝑣−𝜉2

2

𝜕2(𝑣𝑝)

𝜕𝑣2= 0

𝜕𝑝

𝜕𝑡−𝑣

2

𝜕𝑝

𝜕𝑥+ 𝜅(𝜃 − 𝑣)

𝜕𝑝

𝜕𝑣−𝑣

2

𝜕2𝑝

𝜕𝑥2− 𝜌𝜉

𝜕2(𝑣𝑝)

𝜕𝑥𝜕𝑣−𝜉2

2

𝜕2(𝑣𝑝)

𝜕𝑣2= 0

𝜕2(𝑣𝑝)

𝜕𝑥𝜕𝑣=𝜕

𝜕𝑥

𝜕(𝑣𝑝)

𝜕𝑣=𝜕

𝜕𝑥(𝑝 + 𝑣

𝜕𝑝

𝜕𝑣) =

𝜕𝑝

𝜕𝑥+ 𝑣

𝜕2𝑝

𝜕𝑥𝜕𝑣

(51)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

18

with initial condition 𝑝𝑡=𝑜,𝑥,𝑣|𝑣𝑜 = 𝛿𝑥−𝑥𝑜𝛿𝑣−𝑣𝑜 = 𝛿𝑥𝛿𝑣−𝑣𝑜 , where 𝛿 is the Dirac delta function. The

marginal probability density of the variance alone

𝜁𝑡,𝑣|𝑣𝑜 = ∫𝑝𝑡,𝑥,𝑣|𝑣𝑜𝑑𝑥ℝ

(52)

satisfies the following Fokker-Planck equation obtained from (51) by integration over 𝑥

𝜕𝜁

𝜕𝑡=𝜕(𝜅(𝑣 − 𝜃)𝜁)

𝜕𝑣+𝜉2

2

𝜕2(𝑣𝜁)

𝜕𝑣2 (53)

Feller has shown that this equation is well defined on the interval 𝑣 ∈ [0,+∞) as long as 𝜃 > 0. Equation

(53) has a stationary solution, which is a Gamma distribution

𝜁𝑣∗ =

𝛼𝛼

𝛤(𝛼)

𝑣𝛼−1

𝜃𝛼exp (−

𝛼𝑣

𝜃) and 𝛼 =

2𝜅𝜃

𝜉2 (54)

Since 𝑥 appears in (51) only in the derivative operator, it is convenient to take the Fourier

transform, such that

�̂�𝑡,𝜔,𝑣|𝑣𝑜 = ∫𝑒−𝑖𝜔𝑥𝑝𝑡,𝑥,𝑣|𝑣𝑜𝑑𝑥

ℝ

and 𝑝𝑡,𝑥,𝑣|𝑣𝑜 =1

2𝜋∫𝑒𝑖𝜔𝑥�̂�𝑡,𝜔,𝑣|𝑣𝑜𝑑𝜔ℝ

(55)

Inserting (55) into (51), we have

𝜕�̂�

𝜕𝑡=𝜕(𝜅(𝑣 − 𝜃)�̂�)

𝜕𝑣+𝑖𝜔 − 𝜔2

2𝑣�̂� + 𝑖𝜌𝜉𝜔

𝜕(𝑣�̂�)

𝜕𝑣+𝜉2

2

𝜕2(𝑣�̂�)

𝜕𝑣2 (56)

Since (56) is linear in 𝑣 and quadratic in 𝜕

𝜕𝑣, it can be simplified by taking the Laplace transform over 𝑣

�̃�𝑡,𝜔,𝜆|𝑣𝑜 = ∫ 𝑒−𝜆𝑣�̂�𝑡,𝜔,𝑣|𝑣𝑜𝑑𝑣ℝ+

(57)

The PDE satisfied by �̃�𝑡,𝜔,𝜆|𝑣𝑜 is of the first order

𝜕�̃�

𝜕𝑡= (

𝜔2 − 𝜉2𝜆2 − 𝑖𝜔

2− 𝛾𝜆)

𝜕�̃�

𝜕𝜆− 𝜅𝜃𝜆�̃� (58)

with initial condition �̃�𝑡=𝑜,𝜔,𝜆|𝑣𝑜 = 𝑒−𝜆𝑣𝑜, where 𝛾 = 𝜅 + 𝑖𝜌𝜉𝜔. The solution of this PDE is given by the

method of characteristics

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

19

�̃�𝑡,𝜔,𝜆|𝑣𝑜 = exp(−�̃�𝑜𝑣𝑜 − 𝜅𝜃∫ �̃�𝑢𝑑𝑢𝑡

𝑜

) (59)

where the function �̃�𝑡 is the solution of the characteristic (ordinary) differential equation

𝑑�̃�𝑢𝑑𝑢

= 𝛾�̃�𝑢 +𝜉2

2�̃�𝑢2 −

𝜔2 − 𝑖𝜔

2 (60)

With a boundary condition �̃�𝑡 = 𝜆 specified at time 𝑡 , the (60) is a Riccati equation with constant

coefficients and its solution is

�̃�𝑢 =2𝛺

𝜉21

𝛹𝑒𝛺(𝑡−𝑢) − 1−𝛾 − 𝛺

𝜉2 with 𝛺 = √𝛾2 + 𝜉2(𝜔2 − 𝑖𝜔), 𝛹 = 1 +

2𝛺

𝜉2𝜆 + 𝛾 − 𝛺 (61)

Plugging (61) into (59), we have

�̃�𝑡,𝜔,𝜆|𝑣𝑜 = exp(−�̃�𝑜𝑣𝑜 +𝜅𝜃(𝛾 − 𝛺)𝑡

𝜉2−2𝜅𝜃

𝜉2ln𝛹 − 𝑒−𝛺𝑡

𝛹 − 1 ) (62)

Normally we are interested only in distribution of log-spot 𝑥𝑡 and do not care about variance 𝑣𝑡.

Therefore we derive the marginal probability density for 𝑥𝑡 with 𝜆 = 0

𝑝𝑡,𝑥|𝑣𝑜 = ∫ 𝑝𝑡,𝑥,𝑣|𝑣𝑜𝑑𝑣ℝ+

=1

2𝜋∫ ∫𝑒𝑖𝜔𝑥�̂�𝑡,𝜔,𝑣|𝑣𝑜𝑑𝜔

ℝ

𝑑𝑣ℝ+

=1

2𝜋∫ 𝑒𝑖𝜔𝑥∫ �̂�𝑡,𝜔,𝑣|𝑣𝑜𝑑𝑣

ℝ+𝑑𝜔

ℝ

=1

2𝜋∫𝑒𝑖𝜔𝑥�̃�𝑡,𝜔,0|𝑣𝑜𝑑𝜔ℝ

=1

2𝜋∫ exp(𝑖𝜔𝑥 −

𝜔2 − 𝑖𝜔

𝛾 + 𝛺 coth𝛺𝑡2

𝑣𝑜 +𝜅𝜃𝛾𝑡

𝜉2−2𝜅𝜃

𝜉2ln (cosh

𝛺𝑡

2+𝛾

𝛺sinh

𝛺𝑡

2) )𝑑𝜔

ℝ

(63)

where the last step comes from substitution of �̂�𝑡,𝜔,0|𝑣𝑜 in (59) into (55). The derived density function

𝑝𝑡,𝑥|𝑣𝑜 in (63) is still dependent on the unknown initial variance 𝑣𝑜. To remove the dependence, the 𝑣𝑜 is

assumed to have the stationary distribution density as in (54). Thus the unconditional transition density

function 𝑝𝑡(𝑥), is derived by averaging (63) over 𝑣𝑜 with the weight 𝜁∗

𝑝𝑡,𝑥 = ∫ 𝑝𝑡,𝑥|𝑧𝜁𝑧∗𝑑𝑧

ℝ+ (64)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

20

The integral over 𝑣𝑜 is similar to the one of the Gamma function and can be taken explicitly. The final

result is the Fourier integral

𝑝𝑡,𝑥 =1

2𝜋∫𝑒𝑖𝜔𝑥+𝐹𝑡,𝜔𝑑𝜔ℝ

, 𝐹𝑡,𝜔 =𝜅𝜃𝛾𝑡

𝜉2−2𝜅𝜃

𝜉2ln (cosh

𝛺𝑡

2+𝛺2 − 𝛾2 + 2𝜅𝛾

2𝜅𝛺sinh

𝛺𝑡

2) (65)

It is easy to check that 𝑝𝑡,𝑥 is real, because ℜ[𝐹𝑡,𝜔] is an even function of 𝜔 and ℑ[𝐹𝑡,𝜔] is an odd one.

One can also check that 𝐹𝑡,𝜔=0 = 0, which implies that 𝑝𝑡,𝑥 is correctly normalized at all times.

2.2.2. Moment Generating Function (in progress…)

We can integrate (48) over time from 𝑜 to 𝑡 to get

𝑥𝑡 = 𝑥𝑜 −1

2∫ 𝑣𝑢𝑑𝑢𝑡

𝑜

+∫ √𝑣𝑢𝑑�̃�1,𝑢

𝑡

𝑜

, 𝑣𝑡 = 𝑣𝑜 + 𝜅𝜃𝜏 − 𝜅∫ 𝑣𝑢𝑑𝑢𝑡

𝑜

+ 𝜉∫ √𝑣𝑢𝑑�̃�2,𝑢

𝑡

𝑜

(66)

where 𝜏 = 𝑡 − 𝓈 and 𝑑�̃�1,𝑡 = 𝜌𝑑�̃�2,𝑡 + 𝜂𝑑�̃�𝑡 for 𝜂 = √1 − 𝜌2 and the Brownian motion 𝑑�̃�𝑡 is

independent of 𝑑�̃�2,𝑡. Defining a function ℎ𝑡;𝛼,𝛽 such that

ℎ𝑡;𝛼,𝛽: = �̃�𝑜[exp(𝛼𝑥𝑡 + 𝛽𝑣𝑡)] = �̃�𝑜 [exp (𝛼𝑥𝑡 + (𝛽 +𝛼𝜌

𝜉) 𝑣𝑡 −

𝛼𝜌

𝜉𝑣𝑡)]

= �̃�𝑜 [exp(𝛼𝑥𝑜 − 𝛼𝜌𝑣𝑜 + 𝜅𝜃𝜏

𝜉+ (𝛽 +

𝛼𝜌

𝜉) 𝑣𝑡 + (

𝛼𝜌𝜅

𝜉−𝛼

2)∫ 𝑣𝑢𝑑𝑢

𝑡

𝑜

+ 𝛼𝜂∫ √𝑣𝑢𝑑�̃�𝑢

𝑡

𝑜

)]

= exp (𝛼𝑥𝑜 − 𝛼𝜌𝑣𝑜 + 𝜅𝜃𝜏

𝜉) �̃�𝑜 [exp((𝛽 +

𝛼𝜌

𝜉) 𝑣𝑡 + (

𝛼𝜌𝜅

𝜉−𝛼

2)∫ 𝑣𝑢𝑑𝑢

𝑡

𝑜

+ 𝛼𝜂∫ √𝑣𝑢𝑑�̃�𝑢

𝑡

𝑜

)]

= 𝑒𝛼𝑥𝑜−𝛼𝜌

𝑣𝑜+𝜅𝜃𝜏𝜉 �̃�𝑜 [𝑒

(𝛽+𝛼𝜌𝜉)𝑣𝑡+(

𝛼𝜌𝜅𝜉−𝛼2)∫ 𝑣𝑢𝑑𝑢

𝑡𝑜 �̃�𝑜 [𝑒

𝛼𝜂 ∫ √𝑣𝑢𝑑�̃�𝑢𝑡𝑜 ]] (𝑣𝑡 is independent of �̃�𝑡)

= exp (𝛼𝑥𝑜 − 𝛼𝜌𝑣𝑜 + 𝜅𝜃𝜏

𝜉) �̃�𝑜 [exp((𝛽 +

𝛼𝜌

𝜉) 𝑣𝑡 + (

𝛼𝜌𝜅

𝜉−𝛼

2+𝛼2𝜂2

2)∫ 𝑣𝑢𝑑𝑢

𝑡

𝑜

)]

(67)

we can derive the differential of exp(𝛼𝑥𝑡 + 𝛽𝑣𝑡) as

𝑑(𝑒𝛼𝑥𝑡+𝛽𝑣𝑡) = 𝑒𝛼𝑥𝑡+𝛽𝑣𝑡 (𝑑(𝛼𝑥𝑡 + 𝛽𝑣𝑡) +1

2𝑑(𝛼𝑥𝑡 + 𝛽𝑣𝑡)𝑑(𝛼𝑥𝑡 + 𝛽𝑣𝑡)) (68)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

21

= 𝑒𝛼𝑥𝑡+𝛽𝑣𝑡 ((−𝛼

2+𝛼2

2+𝛽2𝜉2

2+ 𝛼𝛽𝜉𝜌 − 𝛽𝜅) 𝑣𝑡𝑑𝑡 + 𝛽𝜅𝜃𝑑𝑡 + 𝛼√𝑣𝑡𝑑�̃�1,𝑡 + 𝛽𝜉√𝑣𝑡𝑑�̃�2,𝑡)

Integrating both sides gives

𝑒𝛼𝑥𝑡+𝛽𝑣𝑡 = 𝑒𝛼𝑥𝑜+𝛽𝑣𝑜 + (−𝛼

2+𝛼2

2+𝛽2𝜉2

2+ 𝛼𝛽𝜉𝜌 − 𝛽𝜅)∫ 𝑒𝛼𝑥𝑢+𝛽𝑣𝑢𝑣𝑢𝑑𝑢

𝑡

𝑜

+ 𝛽𝜅𝜃∫ 𝑒𝛼𝑥𝑢+𝛽𝑣𝑢𝑑𝑢𝑡

𝑜

+ 𝛼∫ 𝑒𝛼𝑥𝑢+𝛽𝑣𝑢√𝑣𝑢𝑑�̃�1,𝑢

𝑡

𝑜

+ 𝛽𝜉 ∫ 𝑒𝛼𝑥𝑢+𝛽𝑣𝑢√𝑣𝑢𝑑�̃�2,𝑢

𝑡

𝑜

(69)

Taking expectation, we find

ℎ𝑡;𝛼,𝛽 = 𝑒𝛼𝑥𝑜+𝛽𝑣𝑜 + (−

𝛼

2+𝛼2

2+𝛽2𝜉2

2+ 𝛼𝛽𝜉𝜌 − 𝛽𝜅)∫ �̃�𝑜[𝑣𝑢𝑒

𝛼𝑥𝑢+𝛽𝑣𝑢]𝑑𝑢𝑡

𝑜

+ 𝛽𝜅𝜃∫ ℎ𝑢;𝛼,𝛽𝑑𝑢𝑡

𝑜

⟹ ℎ𝑡;𝛼,𝛽 = ℎ𝑜;𝛼,𝛽 + (−𝛼

2+𝛼2

2+𝛽2𝜉2

2+ 𝛼𝛽𝜉𝜌 − 𝛽𝜅)

⏟ 𝑝𝛼,𝛽

∫𝜕ℎ𝑢;𝛼,𝛽

𝜕𝛽𝑑𝑢

𝑡

𝑜

+ 𝛽𝜅𝜃∫ ℎ𝑢;𝛼,𝛽𝑑𝑢𝑡

𝑜

(70)

Differentiating with respect to 𝑡, we have the PDE

𝜕ℎ𝑡;𝛼,𝛽

𝜕𝑡− 𝑝𝛼,𝛽

𝜕ℎ𝑡;𝛼,𝛽

𝜕𝛽= 𝛽𝜅𝜃ℎ𝑡;𝛼,𝛽 (71)

(To be continued, reference [6])

2.3. Analytical Solution of Vanilla Options

Vanilla option price in Heston model can be computed semi-analytically. Shortly we will see that

the spot process in Heston model admits a closed-form characteristic function, which allows us to express

the option prices in terms of Fourier-inversion integrals that can be evaluated numerically (e.g. using

Gaussian quadratures).

2.3.1. Fourier Transform and Characteristic Function

There is no standard definition of a Fourier transform and its inverse. The one that we use for

characteristic functions follows the angular frequency definition, which is (as in 𝑛-dimensional case)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

22

Forward: 𝑓𝜔 = ∫ 𝑒𝑖𝜔′𝑥𝑓𝑥𝑑𝑥

ℝ𝑛 ∀ 𝜔 ∈ ℝ𝑛

Inverse: 𝑓𝑥 =1

(2𝜋)𝑛∫ 𝑒−𝑖𝜔

′𝑥𝑓𝜔𝑑𝜔ℝ𝑛

∀ 𝑥 ∈ ℝ𝑛

(72)

where the 𝜔 is the angular frequency and the (′) denotes matrix transpose (the dot product of two column

vectors 𝜔 and 𝑥). In fact the normalization factors multiplying the forward and inverse transforms (here

1 and 1/(2𝜋)𝑛, respectively) and the signs of the exponents are merely conventions and differ in some

treatments. The only requirements of these conventions are: 1. the forward and inverse transforms have

opposite-sign exponents, and 2. the product of their normalization factors is 1/(2𝜋)𝑛. In one-dimension,

the (72) reduces to

Forward: 𝑓𝜔 = ∫𝑒𝑖𝜔𝑥𝑓𝑥𝑑𝑥

ℝ

∀ 𝜔 ∈ ℝ

Inverse: 𝑓𝑥 =1

2𝜋∫𝑒−𝑖𝜔𝑥𝑓𝜔𝑑𝜔ℝ

∀ 𝑥 ∈ ℝ

(73)

The transform is equivalent to the case we write a periodic function 𝑓𝑥 with period 2𝜋/ℎ in terms of

Fourier series expansion

𝑓𝑥 =ℎ

2𝜋∑ 𝑐ℎ𝑘

∞

𝑘=−∞

𝑒−𝑖ℎ𝑘𝑥 where 𝑐ℎ𝑘 = ∫ 𝑓𝑥𝑒𝑖ℎ𝑘𝑥𝑑𝑥

𝜋/ℎ

−𝜋/ℎ

∀ ℎ > 0 (74)

Taking the limit ℎ → 0+, we have

limℎ→0+

𝑐ℎ𝑘 = limℎ→0+

∫ 𝑓𝑥𝑒𝑖ℎ𝑘𝑥𝑑𝑥

𝜋ℎ

−𝜋ℎ

= ∫ 𝑓𝑥𝑒𝑖𝜔𝑥𝑑𝑥

ℝ

= 𝑓𝜔 and

𝑓𝑥 = limℎ→0+

ℎ

2𝜋∑ 𝑐ℎ𝑘𝑒

−𝑖ℎ𝑘𝑥

∞

𝑘=−∞

=1

2𝜋∫ 𝑓𝜔𝑒

−𝑖𝜔𝑥𝑑𝜔ℝ

where 𝜔 = ℎ𝑘

(75)

The sum can be regarded as an approximating Riemann sum for the integral [7].

Characteristic function 𝜙𝜔 of any random variable 𝑋 complete defines its probability distribution.

On the real line the characteristic function is given by the following formula

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

23

𝜙𝜔 ≡ 𝔼[𝑒𝑖𝜔𝑋] = ∫𝑒𝑖𝜔𝑥𝑝𝑥𝑑𝑥

ℝ

= ∫𝑒𝑖𝜔𝑥𝑑𝑃𝑥Ω

∀ 𝜔 ∈ ℝ (76)

where the 𝑝𝑥 denotes the probability density function (PDF) and the 𝑃𝑥 = ∫ 𝑝𝑦𝑑𝑦𝑥

−∞ is the cumulative

density function (CDF). The characteristic function is merely a Fourier transform of the 𝑝𝑥, likewise the

𝑝𝑥 can be recovered from 𝜙𝜔 through the inverse Fourier transform [8]

𝑝𝑥 =1

2𝜋∫𝑒−𝑖𝜔𝑥𝜙𝜔𝑑𝜔ℝ

∀ 𝜔 ∈ ℝ (77)

The 𝑃𝑥 can be computed from 𝜙𝜔 through Levy’s Inversion Formula [9] [10] [11]

𝑃𝑥 =𝜙02+1

2𝜋∫

𝑒𝑖𝜔𝑥𝜙−𝜔 − 𝑒−𝑖𝜔𝑥𝜙𝜔

𝑖𝜔𝑑𝜔

ℝ+

(78)

where 𝜙0 = 1 if 𝜙𝜔 is a characteristic function of a random variable. Before proving the formula, we need

to find Fourier transform of signum function 𝒮𝑥, which is defined as

𝒮𝑥 = {−1 if 𝑥 < 01 if 𝑥 > 0

(79)

Its transform cannot be obtained via direct integration. However we can consider an odd two-sided

exponential function 𝒮𝑥ℎ with ℎ > 0

𝒮𝑥ℎ = {−𝑒

ℎ𝑥 if 𝑥 < 0𝑒−ℎ𝑥 if 𝑥 > 0

(80)

The �̂�𝜔ℎ, i.e. the Fourier transform of 𝒮𝑥

ℎ, can then be derived as

�̂�𝜔ℎ = ∫𝑒𝑖𝜔𝑥𝒮𝑥

ℎ𝑑𝑥ℝ

= −∫ 𝑒(𝑖𝜔+ℎ)𝑥𝑑𝑥ℝ−

+∫ 𝑒(𝑖𝜔−ℎ)𝑥𝑑𝑥ℝ+

= −𝑒(𝑖𝜔+ℎ)𝑥

𝑖𝜔 + ℎ|𝑥=−∞

0

+𝑒(𝑖𝜔−ℎ)𝑥

𝑖𝜔 − ℎ|𝑥=0

∞

= −1

𝑖𝜔 + ℎ−

1

𝑖𝜔 − ℎ=

2𝑖𝜔

𝜔2 + ℎ2

(81)

The parameter ℎ controls how rapidly the exponential function decays. As we let ℎ → 0, the exponential

function resembles more and more closely the signum function. This suggests that

�̂�𝜔 = limℎ→0

�̂�𝜔ℎ = lim

ℎ→0

2𝑖𝜔

𝜔2 + ℎ2= −

2

𝑖𝜔 (82)

Hence the inverse transform of the �̂�𝜔 gives

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

24

𝒮𝑥 =1

2𝜋∫𝑒−𝑖𝜔𝑥�̂�𝜔𝑑𝜔ℝ

= −1

𝜋∫𝑒−𝑖𝜔𝑥

𝑖𝜔𝑑𝜔

ℝ

= −1

𝜋∫cos𝜔𝑥 − 𝑖 sin𝜔𝑥

𝑖𝜔𝑑𝜔

ℝ

= −1

𝑖𝜋∫cos𝜔𝑥

𝜔𝑑𝜔

ℝ⏟ =0, (odd function)

+1

𝜋∫sin𝜔𝑥

𝜔𝑑𝜔

ℝ

=2

𝜋∫

sin𝜔𝑥

𝜔𝑑𝜔

ℝ+

(83)

With the help of the signum function 𝒮𝑥 in (83), the proof of (78) is given as follows

∫𝑒𝑖𝜔𝑥𝜙−𝜔 − 𝑒

−𝑖𝜔𝑥𝜙𝜔𝑖𝜔

𝑑𝜔ℝ+

= ∫𝑒𝑖𝜔𝑥 ∫ 𝑒−𝑖𝜔𝑦𝑝𝑦𝑑𝑦ℝ

− 𝑒−𝑖𝜔𝑥 ∫ 𝑒𝑖𝜔𝑦𝑝𝑦𝑑𝑦ℝ

𝑖𝜔𝑑𝜔

ℝ+

= ∫ ∫𝑒𝑖𝜔(𝑥−𝑦) − 𝑒−𝑖𝜔(𝑥−𝑦)

𝑖𝜔𝑝𝑦𝑑𝑦

ℝ

𝑑𝜔ℝ+

= ∫ ∫𝑒𝑖𝜔(𝑥−𝑦) − 𝑒−𝑖𝜔(𝑥−𝑦)

𝑖𝜔𝑑𝜔

ℝ+

𝑝𝑦𝑑𝑦ℝ

(by Fubini′s theorem)

= 2∫ ∫sin𝜔(𝑥 − 𝑦)

𝜔𝑑𝜔

ℝ+

𝑝𝑦𝑑𝑦ℝ

(by 𝑒𝑖𝑥 = cos 𝑥 + 𝑖 sin 𝑥)

= 𝜋∫𝒮𝑥−𝑦𝑝𝑦𝑑𝑦ℝ

= 𝜋 (−∫ 𝑝𝑦𝑑𝑦∞

𝑥

+∫ 𝑝𝑦𝑑𝑦𝑥

−∞

) = 𝜋 (−∫𝑝𝑦𝑑𝑦ℝ

+ 2∫ 𝑝𝑦𝑑𝑦𝑥

−∞

)

= 𝜋(−𝜙0 + 2𝑃𝑥)

(84)

The Levy Inversion Formula can also be written in the following form

𝑃𝑥 =𝜙02−1

2𝜋∫𝑒−𝑖𝜔𝑥𝜙𝜔𝑖𝜔

𝑑𝜔ℝ

(85)

which can be proved as

∫𝑒−𝑖𝜔𝑥𝜙𝜔𝑖𝜔

𝑑𝜔ℝ

= ∫𝑒−𝑖𝜔𝑥 ∫ 𝑒𝑖𝜔𝑦𝑝𝑦𝑑𝑦ℝ

𝑖𝜔𝑑𝜔

ℝ

= ∫ ∫𝑒𝑖𝜔(𝑦−𝑥)

𝑖𝜔𝑝𝑦𝑑𝑦

ℝ

𝑑𝜔ℝ

= ∫ ∫𝑒𝑖𝜔(𝑦−𝑥)

𝑖𝜔𝑑𝜔

ℝ

𝑝𝑦𝑑𝑦ℝ

= 𝜋∫𝒮𝑥−𝑦𝑝𝑦𝑑𝑦ℝ

= 𝜋(−𝜙0 + 2𝑃𝑥)

where ∫𝑒𝑖𝜔𝑥

𝑖𝜔𝑑𝜔

ℝ

= ∫𝑒𝑖𝜔𝑥

𝑖𝜔𝑑𝜔

ℝ−

+∫𝑒𝑖𝜔𝑥

𝑖𝜔𝑑𝜔

ℝ+

= ∫𝑒−𝑖𝜔𝑥

−𝑖𝜔𝑑𝜔

ℝ+

+∫𝑒𝑖𝜔𝑥

𝑖𝜔𝑑𝜔

ℝ+

= ∫𝑒𝑖𝜔𝑥 − 𝑒−𝑖𝜔𝑥

𝑖𝜔𝑑𝜔

ℝ+

= 2∫sin𝜔𝑥

𝜔𝑑𝜔

ℝ+= 𝜋𝒮𝑥

(86)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

25

Note that if 𝑝𝑥 is real-valued function (i.e. probability density function), its Fourier transform 𝜙𝜔

is then even in its real part and odd in its imaginary part [12], we therefore have 𝜙𝜔 = 𝜙−𝜔̅̅ ̅̅ ̅̅ , the inversion

formula (85) becomes identical to (78), which can be further reduced to

𝑃𝑥 =𝜙02+1

2𝜋∫

𝑒𝑖𝜔𝑥𝜙−𝜔 − 𝑒−𝑖𝜔𝑥𝜙𝜔

𝑖𝜔𝑑𝜔

ℝ+

=𝜙02+1

2𝜋∫

𝑒−𝑖𝜔𝑥𝜙𝜔̅̅ ̅̅ ̅̅ ̅̅ ̅̅ ̅ − 𝑒−𝑖𝜔𝑥𝜙𝜔𝑖𝜔

𝑑𝜔ℝ+

=𝜙02−1

𝜋∫ ℜ[

𝑒−𝑖𝜔𝑥𝜙𝜔𝑖𝜔

] 𝑑𝜔ℝ+

=𝜙02−1

𝜋∫ ℑ [

𝑒−𝑖𝜔𝑥𝜙𝜔𝜔

]𝑑𝜔ℝ+

(87)

For 𝑃𝑥𝐶 = ∫ 𝑝𝑦𝑑𝑦

∞

𝑥, the complementary of 𝑃𝑥, we can use the simple relation 𝑃𝑥

𝐶 = 𝜙0 − 𝑃𝑥

𝑃𝑥𝐶 =

𝜙02−1

2𝜋∫

𝑒𝑖𝜔𝑥𝜙−𝜔 − 𝑒−𝑖𝜔𝑥𝜙𝜔

𝑖𝜔𝑑𝜔

ℝ+

=𝜙02+1

𝜋∫ ℜ[

𝑒−𝑖𝜔𝑥𝜙𝜔𝑖𝜔

] 𝑑𝜔ℝ+

=𝜙02+1

𝜋∫ ℑ [

𝑒−𝑖𝜔𝑥𝜙𝜔𝜔

]𝑑𝜔ℝ+

(88)

2.3.2. Characteristic Function

In this section, we present a derivation of the closed form characteristic function of the spot in

Heston model [13]. The definition of the Heston joint process in (48) will be used. Suppose there exists a

payoff function 𝑔𝑥𝑇,𝑣𝑇 on 𝑥𝑇 and 𝑣𝑇, we may calculate risk neutral expectation of the payoff function as

ℎ𝑡 = �̃�𝑡[𝑔𝑥𝑇,𝑣𝑇] (89)

For example, the characteristic function of the joint distribution of 𝑥𝑇 and 𝑣𝑇 would be given by

𝜙𝑡;𝛼,𝛽 = �̃�𝑡[𝑔𝑥𝑇,𝑣𝑇;𝛼,𝛽] where 𝑔𝑥𝑇,𝑣𝑇;𝛼,𝛽 = exp(𝑖𝛼𝑥𝑇 + 𝑖𝛽𝑣𝑇) (90)

The risk neutral expectation is actually a martingale because for 𝑜 < 𝑡 < 𝑇

ℎ𝑜 = �̃�𝑜[𝑔𝑥𝑇,𝑣𝑇] = �̃�𝑜 [�̃�𝑡[𝑔𝑥𝑇,𝑣𝑇]] = �̃�𝑜[ℎ𝑡] (91)

Applying Ito’s lemma to ℎ and forcing the drift to be zero (martingale property), we end up with a PDE

𝜕ℎ

𝜕𝑡−𝑣

2

𝜕ℎ

𝜕𝑥+ 𝜅(𝜃 − 𝑣)

𝜕ℎ

𝜕𝑣+𝑣

2

𝜕2ℎ

𝜕𝑥2+𝜉2𝑣

2

𝜕2ℎ

𝜕𝑣2+ 𝜉𝜌𝑣

𝜕2ℎ

𝜕𝑥𝜕𝑣= 0 (92)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

26

To determine the solution of (92), the terminal condition ℎ𝑇 = �̃�𝑇[𝑔𝑥𝑇,𝑣𝑇] = 𝑔𝑥𝑇,𝑣𝑇 at time 𝑇 must be

specified. The terminal payoff function that we will consider has the form 𝑔𝑥𝑇,𝑣𝑇 = 𝑒𝛾+𝛿𝑣𝑇+𝑖𝛼𝑥𝑇. If 𝛾 = 0

and 𝛿 = 𝑖𝛽, the resulting payoff function becomes 𝑔𝑥𝑇,𝑣𝑇;𝛼,𝛽 in (90), corresponding to the characteristic

function of the joint distribution.

Heston [22] guessed a solution that has the form

ℎ𝑡 = �̃�𝑡[𝑔𝑥𝑇,𝑣𝑇] = 𝑒𝐶+𝐷𝑣𝑡+𝑖𝛼𝑥𝑡 where 𝐶 = 𝐶𝜏,𝛼,𝛾,𝛿 , 𝐷 = 𝐷𝜏,𝛼,𝛾,𝛿 , 𝜏 = 𝑇 − 𝑡 (93)

Substituting the tentative solution (93) in (92) yields

𝜕𝐶

𝜕𝑡+ 𝑣

𝜕𝐷

𝜕𝑡−𝑖𝛼𝑣

2+ 𝜅(𝜃 − 𝑣)𝐷 −

𝛼2𝑣

2+𝜉2𝑣

2𝐷2 + 𝑖𝛼𝐷𝜉𝜌𝑣 = 0

⟹𝜕𝐶

𝜕𝑡+ 𝜅𝜃𝐷 + (

𝜕𝐷

𝜕𝑡+𝜉2

2𝐷2 −𝑚𝐷 −−

𝛼(𝑖 + 𝛼)

2) 𝑣 = 0 where 𝑚 = 𝜅 − 𝛼𝜉𝜌𝑖

(94)

As the 𝑣 is an independent variable, (94) is zero only if

𝜕𝐶

𝜕𝑡+ 𝜅𝜃𝐷 = 0 and

𝜕𝐷

𝜕𝑡+𝜉2

2𝐷2 −𝑚𝐷 −

𝛼(𝑖 + 𝛼)

2= 0 (95)

Changing the variable 𝑡 to 𝜏 = 𝑇 − 𝑡, we have

𝜕𝐶

𝜕𝜏− 𝜅𝜃𝐷 = 0 and

𝜕𝐷

𝜕𝜏−𝜉2

2𝐷2 +𝑚𝐷 +

𝛼(𝑖 + 𝛼)

2= 0 (96)

The terminal condition for this system of equations is given by 𝐶𝜏=0 = 𝛾 and 𝐷𝜏=0 = 𝛿. The ODE for 𝐷

is a Riccati equation that only depends on 𝐷. This Riccati equation can be turned into an ODE through the

change of variable, 𝑍 = (𝐷 − �̂�)−1

, where �̂� is a particular solution to the second equation in (96)

𝜕𝑍

𝜕𝜏= −

1

(𝐷 − �̂�)2

𝜕(𝐷 − �̂�)

𝜕𝜏= −𝑍2 (

𝜉2

2𝐷2 −𝑚𝐷 −

𝜉2

2�̂�2 +𝑚�̂�)

= −𝑍 (𝜉2

2(𝐷 + �̂�) − 𝑚) = −𝑍 (

𝜉2

2(𝐷 − �̂� + 2�̂�)) + 𝑚𝑍 = −(𝜉2�̂� − 𝑚)𝑍 −

𝜉2

2

⟹𝜕𝑍

𝜕𝜏+ (𝜉2�̂� − 𝑚)𝑍 +

𝜉2

2= 0 or

(97)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

27

𝜕𝑍

𝜕𝜏+ 𝐵𝑍 + 𝐴 = 0 where 𝐴 =

𝜉2

2, 𝐵 = 𝜉2�̂� − 𝑚

The solution to (97) is given by

𝑍 = −𝐴

𝐵 + (𝑍0 +

𝐴

𝐵 ) 𝑒−𝐵𝜏 where 𝑍0 =

1

𝐷0 − �̂�=

1

𝛿 − �̂�

⟹𝐷 =1

−𝐴𝐵 + (𝑍0 +

𝐴𝐵 ) 𝑒−𝐵𝜏

+ �̂�

(98)

The particular solution �̂� can be as simple as a constant, which implies it would be the solution of the

quadratic equation

−𝜉2

2�̂�2 +𝑚�̂� +

𝛼(𝑖 + 𝛼)

2= 0 ⟹ �̂� =

𝑚 + 𝑑

𝜉2 where 𝑑 = ±√𝑚2 + 𝜉2𝛼(𝑖 + 𝛼) (99)

This particular solution for �̂� makes 𝐵 = 𝑑. The solution for 𝐷 in (98) can then be derived

𝐷 =1

−𝜉2

2𝑑+ (

−𝜉2

𝑚+ 𝑑 − 𝛿𝜉2+𝜉2

2𝑑) 𝑒−𝑑𝜏

+𝑚 + 𝑑

𝜉2

⟹ 𝜉2𝐷 = −2𝑑(𝑚 + 𝑑 − 𝛿𝜉2)

2𝑒−𝑑𝜏𝑑 + (𝑚 + 𝑑 − 𝛿𝜉2)(1 − 𝑒−𝑑𝜏)+ 𝑚 + 𝑑

= −2𝑑(𝑚 + 𝑑 − 𝛿𝜉2)

(𝑚 + 𝑑 − 𝛿𝜉2) − (𝑚 − 𝑑 − 𝛿𝜉2)𝑒−𝑑𝜏+𝑚 + 𝑑

= −2𝑑

1 − �̂�𝑒−𝑑𝜏+𝑚 + 𝑑 (by defining �̂� =

𝑚 − 𝑑 − 𝛿𝜉2

𝑚+ 𝑑 − 𝛿𝜉2)

=(𝑚 + 𝑑)(1 − �̂�𝑒−𝑑𝜏) − 2𝑑

1 − �̂�𝑒−𝑑𝜏=𝑚 − 𝑑 − (𝑚 + 𝑑)�̂�𝑒−𝑑𝜏

1 − �̂�𝑒−𝑑𝜏

= (𝑚 + 𝑑)𝑔 − �̂�𝑒−𝑑𝜏

1 − �̂�𝑒−𝑑𝜏 (by defining 𝑔 =

𝑚 − 𝑑

𝑚 + 𝑑)

⟹𝐷 =𝑚 + 𝑑

𝜉2𝑔 − �̂�𝑒−𝑑𝜏

1 − �̂�𝑒−𝑑𝜏

(100)

The 𝐷 can then be plugged into the ODE for 𝐶 in (96)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

28

𝜕𝐶

𝜕𝜏− 𝜅𝜃

𝑚 + 𝑑

𝜉2𝑔 − �̂�𝑒−𝑑𝜏

1 − �̂�𝑒−𝑑𝜏= 0 ⟹ 𝐶 = 𝜅𝜃

𝑚 + 𝑑

𝜉2∫𝑔 − �̂�𝑒−𝑑𝜏

1 − �̂�𝑒−𝑑𝜏𝑑𝜏 + 𝐾𝐶 (101)

where 𝐾𝐶 is a constant to be fixed by terminal condition. The indefinite integral in (101) can be solved

through change of variable 𝑢 = 𝑒−𝑑𝜏 where 𝜕𝑢

𝜕𝜏= −𝑢𝑑

∫𝑔 − �̂�𝑒−𝑑𝜏

1 − �̂�𝑒−𝑑𝜏𝜕𝜏 = −∫(

𝑔 − �̂�𝑢

1 − �̂�𝑢)1

𝑢𝑑𝜕𝑢 = −

1

𝑑∫(

𝑔𝑢 − �̂�

1 − �̂�𝑢)𝜕𝑢

= −1

𝑑∫(

𝑔𝑢 − �̂� −

𝑔𝑢(1 − �̂�𝑢)

1 − �̂�𝑢+𝑔

𝑢)𝜕𝑢 = −

1

𝑑∫(

(𝑔 − 1)�̂�

1 − �̂�𝑢+𝑔

𝑢)𝜕𝑢

=𝑔 − 1

𝑑ln(1 − �̂�𝑢) −

𝑔

𝑑ln 𝑢 =

𝑔 − 1

𝑑ln(1 − �̂�𝑒−𝑑𝜏) + 𝑔𝜏

(102)

which gives

𝐶 = 𝜅𝜃𝑚 + 𝑑

𝜉2(𝑔 − 1

𝑑ln(1 − �̂�𝑒−𝑑𝜏) + 𝑔𝜏) + 𝐾𝐶

=𝜅𝜃

𝜉2(−2 ln(1 − �̂�𝑒−𝑑𝜏) + (𝑚 − 𝑑)𝜏) + 𝐾𝐶

(103)

We then fix 𝐾𝐶 by 𝐶0 = 𝛾

𝐶0 = −2𝜅𝜃

𝜉2ln(1 − �̂�) + 𝐾𝐶 = 𝛾 ⟹ 𝐾𝐶 = 2

𝜅𝜃

𝜉2ln(1 − �̂�) + 𝛾 (104)

Therefore we have the solution for 𝐶

𝐶 =𝜅𝜃

𝜉2(2 ln

1 − �̂�

1 − �̂�𝑒−𝑑𝜏 + (𝑚 − 𝑑)𝜏) + 𝛾 (105)

Combining the solutions in (100) and (105), the ℎ𝑡 is of the following form

ℎ𝑡 = �̃�𝑡[𝑔𝑥𝑇,𝑣𝑇] = exp(𝐶 + 𝐷𝑣𝑡 + 𝑖𝛼𝑥𝑡) where

𝑚 = 𝜅 − 𝛼𝜉𝜌𝑖, 𝑑 = ±√𝑚2 + 𝜉2𝛼(𝑖 + 𝛼), 𝑔 =𝑚 − 𝑑

𝑚 + 𝑑, �̂� =

𝑚 − 𝑑 − 𝛿𝜉2

𝑚+ 𝑑 − 𝛿𝜉2

𝐶 =𝜅𝜃

𝜉2(2 ln

1 − �̂�

1 − �̂�𝑒−𝑑𝜏 + (𝑚 − 𝑑)𝜏) + 𝛾, 𝐷 =

𝑚 + 𝑑

𝜉2𝑔 − �̂�𝑒−𝑑𝜏

1 − �̂�𝑒−𝑑𝜏

(106)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

29

The marginal characteristic function of 𝑥𝑇 is given by 𝛾 = 0 and 𝛿 = 0 where �̂� = 𝑔

𝜙𝛼𝑥𝑇 = exp(

𝜅𝜃

𝜉2(2 ln

1 − 𝑔

1 − 𝑔𝑒−𝑑𝜏+ (𝑚 − 𝑑)𝜏) +

𝑚 − 𝑑

𝜉21 − 𝑒−𝑑𝜏

1 − 𝑔𝑒−𝑑𝜏𝑣𝑡 + 𝑖𝛼𝑥𝑡)

where 𝑚 = 𝜅 − 𝛼𝜉𝜌𝑖, 𝑑 = ±√𝑚2 + 𝜉2𝛼(𝑖 + 𝛼), 𝑔 =𝑚 − 𝑑

𝑚 + 𝑑

(107)

2.3.3. Vanilla Option Prices

Once we know the analytical form of the characteristic function 𝜙𝛼𝑥𝑇 of the centered log-spot 𝑥𝑇,

we are able to compute the vanilla option prices using inversion methods. Here, we are going to discuss

two methods, which treat the option price function analogous to the cumulative density function or the

probability density function, respectively. In addition, we also summarize the original Heston’s method

[22].

2.3.3.1. Analogy to Cumulative Density Function

For 𝑡 ≤ 𝑇, using a European call option as an example we change the variable to 𝑥𝑡 as in (47)

𝐶𝑇,𝐾 = �̃�𝑡 [𝑀𝑡𝑀𝑇

(𝑆𝑇 − 𝐾)+] = 𝑒−𝑟𝜏𝐹𝑡,𝑇�̃�𝑡[(𝑒

𝑥𝑇 − 𝑒𝒦)+]

with 𝜏 = 𝑇 − 𝑡, 𝜇 = 𝑟 − 𝑞, 𝐹𝑡,𝑇 = 𝑆𝑡𝑒𝜇𝜏, 𝑥𝑇 = ln

𝑆𝑇𝐹𝑡,𝑇

, 𝒦 = ln𝐾

𝐹𝑡,𝑇

(108)

where the cash account 𝑀𝑇 = 𝑀𝑡 exp (∫ 𝑟𝑢𝑑𝑢𝑇

𝑡) and the interest rate 𝑟 and dividend yield 𝑞 are assumed

constant. We then define an option forward price in percentage of the underlying forward as a function of

moneyness 𝒦 defined as the log strike over forward

𝒞𝒦 =𝐶𝑇,𝐾

𝑒−𝑟𝜏𝐹𝑡,𝑇= �̃�𝑡[(𝑒

𝑥𝑇 − 𝑒𝒦)+] = �̃�𝑡[(𝑒𝑥𝑇 − 𝑒𝒦)𝟙{𝑥𝑇 > 𝒦}]

where 𝟙{𝑥 > 𝑋} = {1 if 𝑥 > 𝑋0 otherwise

(109)

Given we know the characteristic function of the log-spot process 𝑥𝑇, we can derive the Fourier transform

of the call option, then use numerical inversion to obtain option prices directly [14]. Since 𝐶𝑇,𝐾 ∈

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

30

[0, 𝑒−𝑟𝜏𝐹𝑜,𝑇], we have 𝒞𝒦 ∈ [0,1], which can treated as a cumulative density function on 𝒦, the Fourier

transform of the option price is then given by

𝜒𝜔𝑐 = ∫ 𝑒𝑖𝜔𝒦𝑑𝒞𝒦

𝒦∈ℝ

= 𝑒𝑖𝜔𝒦𝒞𝒦|𝒦=−∞∞

−∫𝑖𝜔𝑒𝑖𝜔𝒦𝒞𝒦𝑑𝒦ℝ

= −𝑒−𝑖𝜔∞ −∫𝑖𝜔𝑒𝑖𝜔𝒦𝒞𝒦𝑑𝒦ℝ

(by 𝒞∞ = 0 and 𝒞−∞ = 1)

= −𝑒−𝑖𝜔∞ −∫ 𝑖𝜔𝑒𝑖𝜔𝒦∫(𝑒𝑥 − 𝑒𝒦)𝟙{𝑥 > 𝒦}𝑑𝑃𝑥𝑥𝑇

Ω

𝑑𝒦ℝ

= −𝑒−𝑖𝜔∞ −∫ ∫𝑖𝜔(𝑒𝑖𝜔𝒦+𝑥 − 𝑒(𝑖𝜔+1)𝒦)𝟙{𝑥 > 𝒦}𝑑𝒦ℝ

𝑑𝑃𝑥𝑥𝑇

Ω

(by Fubini′s theorem)

= −𝑒−𝑖𝜔∞ −∫ ∫ 𝑖𝜔(𝑒𝑖𝜔𝒦+𝑥 − 𝑒(𝑖𝜔+1)𝒦)𝑑𝒦𝑥

−∞

𝑑𝑃𝑥𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ −∫ (𝑒𝑖𝜔𝒦+𝑥 −𝑖𝜔𝑒(𝑖𝜔+1)𝒦

𝑖𝜔 + 1)|𝒦=−∞

𝑥

𝑑𝑃𝑥𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ −∫ (𝑒(𝑖𝜔+1)𝑥 − 𝑒−𝑖𝜔∞+𝑥 −𝑖𝜔𝑒(𝑖𝜔+1)𝑥

𝑖𝜔 + 1+𝑖𝜔𝑒−(𝑖𝜔+1)∞

𝑖𝜔 + 1⏟ =0

)𝑑𝑃𝑥𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ + 𝑒−𝑖𝜔∞∫𝑒𝑥𝑑𝑃𝑥𝑥𝑇

Ω

−∫ (𝑒(𝑖𝜔+1)𝑥 −𝑖𝜔𝑒(𝑖𝜔+1)𝑥

𝑖𝜔 + 1)𝑑𝑃𝑥

Ω

= −1

𝑖𝜔 + 1∫𝑒𝑖(𝜔−i)𝑥𝑑𝑃𝑥

𝑥𝑇

Ω

(by ∫ 𝑒𝑥𝑑𝑃𝑥𝑥𝑇

Ω

=1

𝐹𝑇�̃�0[𝑆𝑇] = 1)

= −𝜙𝜔−𝑖𝑥𝑇

𝑖𝜔 + 1

(110)

The 𝜒𝜔𝑐 is the characteristic function of the option forward price 𝒞𝒦, which is treated just as a cumulative

density function. The price is then given by the Levy’s Inversion Formula (78) [15]

𝒞𝒦 =𝜒02+1

2𝜋∫

𝑒𝑖𝜔𝒦𝜒−𝜔𝑐 − 𝑒−𝑖𝜔𝒦𝜒𝜔

𝑐

𝑖𝜔𝑑𝜔

ℝ+

(111)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

31

=1

2+1

2𝜋∫

𝑒𝑖𝜔𝒦𝜙−𝜔−𝑖𝑥𝑇

𝑖𝜔 − 1 + 𝑒−𝑖𝜔𝒦 𝜙𝜔−𝑖

𝑥𝑇

𝑖𝜔 + 1𝑖𝜔

𝑑𝜔ℝ+

(by 𝜒0𝑐 = −𝜙−𝑖 = 1)

=1

2+1

2𝜋∫ (𝑒𝑖𝜔𝒦

𝜙−𝜔−𝑖𝑥𝑇

−𝜔2 − 𝑖𝜔+ 𝑒−𝑖𝜔𝒦

𝜙𝜔−𝑖𝑥𝑇

−𝜔2 + 𝑖𝜔)𝑑𝜔

ℝ+

=1

2−1

2𝜋∫ (𝑒𝑖𝜔𝒦

𝜙−𝜔−𝑖𝑥𝑇

𝜔2 + 𝑖𝜔+ 𝑒−𝑖𝜔𝒦

𝜙𝜔−𝑖𝑥𝑇

𝜔2 − 𝑖𝜔)𝑑𝜔

ℝ+

In the integrand of (111), the 𝜙𝑢𝜔−𝑖𝑥𝑇 for 𝑢 = ±1 can be derived from the characteristic function 𝜙𝛼

𝑥𝑇 in

(107) and given as follows (note that 𝑥𝑡 = 0)

𝜙𝑢𝜔−𝑖𝑥𝑇 = exp(

𝜅𝜃

𝜉2(2 ln

1 − 𝑔

1 − 𝑔𝑒−𝑑𝜏+ (𝑚 − 𝑑)𝜏) +

𝑚 − 𝑑

𝜉21 − 𝑒−𝑑𝜏

1 − 𝑔𝑒−𝑑𝜏𝑣𝑡)

with 𝜏 = 𝑇 − 𝑡, 𝑚 = 𝜅 − 𝑢𝜔𝜉𝜌𝑖 − 𝜉𝜌, 𝑑 = ±√𝑚2 + 𝜉2𝜔(𝜔 − 𝑢𝑖), 𝑔 =𝑚 − 𝑑

𝑚 + 𝑑

(112)

The inversion formula in (111) involves evaluation of the 𝜙𝑢𝜔−𝑖𝑥𝑇 function twice, which is less efficient.

Since 𝒞𝒦 is real-valued, we may use (87) to perform the inversion

𝒞𝒦 =𝜒02−1

𝜋∫ ℑ [

𝑒−𝑖𝜔𝒦𝜒𝜔𝑐

𝜔]

ℝ+

=1

2+1

𝜋∫ ℑ [𝑒−𝑖𝜔𝒦

𝜙𝜔−𝑖𝑥𝑇

𝑖𝜔2 +ω]𝑑𝜔

ℝ+

(113)

where 𝜙𝜔−𝑖𝑥𝑇 is given in (112) with 𝑢 = 1 and the integral can be estimated numerically by Gauss-

Laguerre quadrature. Once we have 𝒞𝒦 for log-moneyness, the call option price can be computed by (109)

𝐶𝑇,𝐾 = 𝒞𝒦𝑒−𝑟𝜏𝑆𝑡𝑒

𝜇𝜏 = 𝒞𝒦𝑆𝑡𝑒−𝑞𝜏 (114)

and the put option price by call-put parity

𝐶𝑇,𝐾 − 𝑃𝑇,𝐾 = 𝑒−𝑟𝜏(𝐹𝑡,𝑇 − 𝐾) ⟹ 𝑃𝑇,𝐾 = 𝐶𝑇,𝐾 − 𝑆𝑡𝑒

−𝑞𝜏 + 𝑒−𝑟𝜏𝐾 (115)

2.3.3.2. Analogy to Probability Density Function

In this section, we treat 𝒞𝒦 analogous to a probability density [16] [17] and define in terms of

generalized Fourier transform with 𝑧 = 𝑧𝑟 − 𝑖𝑧𝑖 , 𝑧𝑟 ∈ ℝ, 𝑧𝑖 ∈ 𝒟 ⊆ ℝ+

𝜒𝑧𝑝= ∫𝑒𝑖𝑧𝒦𝒞𝒦𝑑𝒦

ℝ

= ∫𝑒𝑖𝑧𝒦�̃�𝑡[(𝑒𝑥𝑇 − 𝑒𝒦)𝟙{𝑥𝑇 > 𝒦}]𝑑𝒦

ℝ

(116)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

32

= �̃�𝑡 [∫𝑒𝑖𝑧𝒦(𝑒𝑥𝑇 − 𝑒𝒦)𝟙{𝑥𝑇 > 𝒦}𝑑𝒦

ℝ

] = �̃�𝑡 [∫ 𝑒𝑖𝑧𝒦(𝑒𝑥𝑇 − 𝑒𝒦)𝑑𝒦𝑥𝑇

−∞

]

= �̃�𝑡 [(𝑒𝑖𝑧𝒦+𝑥𝑇

𝑖𝑧−𝑒(𝑖𝑧+1)𝒦

𝑖𝑧 + 1)|𝒦=−∞

𝑥𝑇

] = �̃�𝑡 [𝑒(𝑖𝑧+1)𝑥𝑇

𝑖𝑧 − 𝑧2] (by lim

𝒦→−∞𝑒𝑖𝑧𝒦 = 0)

= �̃�𝑡 [𝑒𝑖(𝑧−𝑖)𝑥𝑇

𝑖𝑧 − 𝑧2] =

𝜙𝑧−𝑖𝑥𝑇

𝑖𝑧 − 𝑧2

For some return distributions, the return transform 𝜙𝑧−𝑖𝑥𝑇 is well-defined only when 𝑧𝑖 is in a subset of the

real line. We use 𝒟 ⊆ ℝ+ to denote the subset that both guarantees the convergence of 𝑒𝑖𝑧𝒦 and 𝑒𝑖(𝑧−𝑖)𝒦

as 𝒦 ⟶ −∞, and assures the finiteness of the transform 𝜙𝑧−𝑖𝑥𝑇 .

The option forward price 𝒞𝒦 is then given by the inverse Fourier transform

𝒞𝒦 =1

2𝜋∫ 𝑒−𝑖𝑧𝒦𝜒𝑧

𝑝𝑑𝑧

∞−𝑖𝑧𝑖

−∞−𝑖𝑧𝑖

=1

2𝜋∫ 𝑒−𝑖𝑧𝒦𝜒𝑧

𝑝𝑑(𝑧𝑟 − 𝑖𝑧𝑖)

∞−𝑖𝑧𝑖

−∞−𝑖𝑧𝑖

=1

2𝜋∫ 𝑒−𝑖𝑧𝒦𝜒𝑧

𝑝𝑑𝑧𝑟

ℝ

=1

2𝜋∫ 𝑒−𝑖𝑧𝒦

𝜙𝑧−𝑖𝑥𝑇

𝑖𝑧 − 𝑧2𝑑𝑧𝑟

ℝ

=1

𝜋∫ ℜ[𝑒−𝑖𝑧𝒦

𝜙𝑧−𝑖𝑥𝑇

𝑖𝑧 − 𝑧2] 𝑑𝑧𝑟

ℝ+

(117)

The last equality holds because 𝒞𝒦 is real, which implies that the function 𝜒𝑧𝑝 is odd in its imaginary part

and even in its real part. The functional form of 𝜙𝑧−𝑖𝑥𝑇 can be derived again from (107) in a similar way

𝜙𝑧−𝑖𝑥𝑇 = exp(

𝜅𝜃

𝜉2(2 ln

1 − 𝑔

1 − 𝑔𝑒−𝑑𝜏+ (𝑚 − 𝑑)𝜏) +

𝑚 − 𝑑

𝜉21 − 𝑒−𝑑𝜏

1 − 𝑔𝑒−𝑑𝜏𝑣𝑡) with

𝑚 = 𝜅 − (𝑧𝑖 + 1)𝜉𝜌 − 𝑧𝑟𝜉𝜌𝑖, 𝑑 = ±√𝑚2 + 𝜉2(𝑧𝑟 − 𝑖(𝑧𝑖 + 1))(𝑧𝑟 − 𝑖𝑧𝑖), 𝑔 =

𝑚 − 𝑑

𝑚 + 𝑑

(118)

2.3.3.3. Heston’s Original Solution

At time 𝑡, the price of a European call on a stock (assuming non-dividend-bearing to qualify as a

numeraire) with spot 𝑆𝑡 and strike 𝐾 is given by the no-arbitrage formula

𝐶𝑇,𝐾,𝑆𝑡 = �̃�𝑡 [𝑀𝑡𝑀𝑇

(𝑆𝑇 − 𝐾)+] = �̃�𝑡 [

𝑀𝑡𝑀𝑇

𝑆𝑇𝟙{𝑆𝑇 > 𝐾}] − 𝐾�̃�𝑡 [𝑀𝑡𝑀𝑇

𝟙{𝑆𝑇 > 𝐾}]

= 𝔼𝑡𝑆 [𝑆𝑡𝑆𝑇𝑆𝑇𝟙{𝑆𝑇 > 𝐾}] − 𝐾𝔼𝑡

𝑇 [𝐵𝑡,𝑇𝐵𝑇,𝑇

𝟙{𝑆𝑇 > 𝐾}] change numeraire 𝑀𝑡 → 𝑆𝑡 , 𝑀𝑡 → 𝐵𝑡,𝑇

(119)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

33

= 𝑆𝑡𝔼𝑡𝑆[𝟙{𝑆𝑇 > 𝐾}] − 𝐾𝐵𝑡,𝑇𝔼𝑡

𝑇[𝟙{𝑆𝑇 > 𝐾}]

= 𝑆𝑡ℙ𝑡𝑆[𝑆𝑇 > 𝐾] − 𝐾𝐵𝑡,𝑇ℙ𝑡

𝑇[𝑆𝑇 > 𝐾]

where ℙ𝑡𝑆[𝑆𝑇 > 𝐾] and ℙ𝑡

𝑇[𝑆𝑇 > 𝐾] are both conditional probabilities of spot finishing in-the-money at

maturity. The ℙ𝑡𝑆[𝑆𝑇 > 𝐾] is computed under the measure associated with the stock as the numeraire,

whereas the ℙ𝑡𝑇[𝑆𝑇 > 𝐾] is computed under 𝑇-forward measure associated with zero coupon bond 𝐵𝑡,𝑇 as

the numeraire [18]. In Black-Scholes model

𝐶𝑇,𝐾,𝑆𝑡𝐵𝑆 = 𝑆𝑡𝑁(𝑑+) − 𝐾𝐵𝑡,𝑇𝑁(𝑑−) (120)

the ℙ𝑡𝑆[𝑆𝑇 > 𝐾] and ℙ𝑡

𝑇[𝑆𝑇 > 𝐾] are computed as 𝑁(𝑑+) and 𝑁(𝑑−) respectively. Since the drift

adjustment due to change of numeraire is

𝑑𝑊𝑡ℕ

Under ℕ= 𝑑�̃�𝑡Under ℚ

− 𝜎𝑁𝑑𝑡 (121)

where ℕ denotes the measure associated with numeraire 𝑁 and ℚ the risk neutral measure. The stock

process under the measure with itself as the numeraire is given by

𝑑𝑆𝑡𝑆𝑡= 𝑟𝑑𝑡 + 𝜎𝑑�̃�𝑡 = (𝑟 + 𝜎

2)𝑑𝑡 + 𝜎𝑑𝑊𝑡𝑆 (122)

The total drift adjustment 𝜎2𝜏 for period 𝜏 = 𝑇 − 𝑡 is then normalized by the total volatility 𝜎√𝜏 of the

stock to give a shift term 𝜎√𝜏 as the difference between 𝑑+ and 𝑑− in the classic Black-Scholes formula.

Suppose we use the definition in (108) for a call option, the two conditional probabilities can be

expressed as

𝐶𝑇,𝐾 = 𝑒−𝑟𝜏𝐹𝑡,𝑇�̃�𝑡[(𝑒

𝑥𝑇 − 𝑒𝒦)+] = 𝑒−𝑟𝜏𝐹𝑡,𝑇(�̃�𝑡[𝑒𝑥𝑇𝟙{𝑥𝑇 > 𝒦}] − 𝑒

𝒦�̃�𝑡[𝟙{𝑥𝑇 > 𝒦}])

= 𝑒−𝑟𝜏𝐹𝑡,𝑇𝑃𝒦+ − 𝑒−𝑟𝜏𝐾𝑃𝒦

− with 𝑃𝒦+ = �̃�𝑡[𝑒

𝑥𝑇𝟙{𝑥𝑇 > 𝒦}], 𝑃𝒦− = �̃�𝑡[𝟙{𝑥𝑇 > 𝒦}]

(123)

Because in Heston model the 𝑃𝒦+ and 𝑃𝒦

− are not available in closed form, Heston [22] firstly derived the

characteristic functions (i.e. the Fourier transforms) of 𝑃𝒦+ and 𝑃𝒦

− by solving the PDE (92) for each of

them, and then found inverse of the two characteristic functions to obtain the option price. Since we have

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

34

already derived the characteristic function of 𝑥𝑇 as in (107), we can easily derive those for 𝑃𝒦+ and 𝑃𝒦

−.

For example, the 𝑃𝒦+ can be treated as a CDF and then the characteristic function of 𝑃𝒦

+ becomes

𝜒𝜔+ = ∫ 𝑒𝑖𝜔𝒦𝑑𝑃𝒦

+

𝒦∈ℝ

= 𝑒𝑖𝜔𝒦𝑃𝒦+|𝒦=−∞

∞−∫𝑖𝜔𝑒𝑖𝜔𝒦𝑃𝒦

+𝑑𝒦ℝ

= −𝑒−𝑖𝜔∞ −∫𝑖𝜔𝑒𝑖𝜔𝒦𝑃𝒦+𝑑𝒦

ℝ

(by 𝑃∞+ = 0 and 𝑃−∞

+ = �̃�𝑡[𝑒𝑥𝑇] = 1)

= −𝑒−𝑖𝜔∞ −∫ 𝑖𝜔𝑒𝑖𝜔𝒦∫𝑒𝑥𝟙{𝑥 > 𝒦}𝑑𝑃𝑥𝑥𝑇

Ω

𝑑𝒦ℝ

= −𝑒−𝑖𝜔∞ −∫ ∫𝑖𝜔𝑒𝑖𝜔𝒦+𝑥𝟙{𝑥 > 𝒦}𝑑𝒦ℝ

𝑑𝑃𝑥𝑥𝑇

Ω

(by Fubini′s theorem)

= −𝑒−𝑖𝜔∞ −∫ ∫ 𝑖𝜔𝑒𝑖𝜔𝒦+𝑥𝑑𝒦𝑥

−∞

𝑑𝑃𝑥𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ −∫𝑒𝑖𝜔𝒦+𝑥|𝒦=−∞

𝑥𝑑𝑃𝑥

𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ −∫ [𝑒𝑖(𝜔−i)𝑥 − 𝑒−𝑖𝜔∞+𝑥]𝑑𝑃𝑥𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ + 𝑒−𝑖𝜔∞∫𝑒𝑥𝑑𝑃𝑥𝑥𝑇

Ω

−∫𝑒𝑖(𝜔−i)𝑥𝑑𝑃𝑥Ω

= −∫𝑒𝑖(𝜔−i)𝑥𝑑𝑃𝑥𝑥𝑇

Ω

(by ∫ 𝑒𝑥𝑑𝑃𝑥𝑥𝑇

Ω

= �̃�𝑡[𝑒𝑥𝑇] = 1)

= −𝜙𝜔−𝑖𝑥𝑇

(124)

Similarly, the characteristic function of 𝑃𝒦− is given by

𝜒𝜔− = ∫ 𝑒𝑖𝜔𝒦𝑑𝑃𝒦

−

𝒦∈ℝ

= 𝑒𝑖𝜔𝒦𝑃𝒦−|𝒦=−∞

∞−∫𝑖𝜔𝑒𝑖𝜔𝒦𝑃𝒦

−𝑑𝒦ℝ

= −𝑒−𝑖𝜔∞ −∫𝑖𝜔𝑒𝑖𝜔𝒦𝑃𝒦−𝑑𝒦

ℝ

(by 𝑃∞− = 0 and 𝑃−∞

− = 1)

= −𝑒−𝑖𝜔∞ −∫ 𝑖𝜔𝑒𝑖𝜔𝒦∫𝟙{𝑥 > 𝒦}𝑑𝑃𝑥𝑥𝑇

Ω

𝑑𝒦ℝ

= −𝑒−𝑖𝜔∞ −∫ ∫𝑖𝜔𝑒𝑖𝜔𝒦𝟙{𝑥 > 𝒦}𝑑𝒦ℝ

𝑑𝑃𝑥𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ −∫ ∫ 𝑖𝜔𝑒𝑖𝜔𝒦𝑑𝒦𝑥

−∞

𝑑𝑃𝑥𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ −∫𝑒𝑖𝜔𝒦|𝒦=−∞

𝑥𝑑𝑃𝑥

𝑥𝑇

Ω

(125)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

35

= −𝑒−𝑖𝜔∞ −∫(𝑒𝑖𝜔𝑥 − 𝑒−𝑖𝜔∞)𝑑𝑃𝑥𝑥𝑇

Ω

= −𝑒−𝑖𝜔∞ + 𝑒−𝑖𝜔∞∫𝑑𝑃𝑥𝑥𝑇

Ω

−∫𝑒𝑖𝜔𝑥𝑑𝑃𝑥Ω

= −𝜙𝜔𝑥𝑇

The 𝑃𝒦+ and 𝑃𝒦

− are then obtained through the inverse of 𝜒𝜔+ and 𝜒𝜔

− respectively. Given that 𝜒0+ = 𝜒0

− =

1, the Heston’s vanilla option price formula can be derived from 𝜙𝜔𝑥𝑇 in (107) and the inverse formula in

(87) directly. Here we summarize the solution as follows

HestonVanilla(𝜅, 𝜃, 𝜉, 𝜌, 𝑟, 𝑞, 𝑣𝑡 , 𝑆𝑡 , 𝐾, 𝜏, 𝜂) = 𝑒−𝑞𝜏𝑆𝑡(𝑃+ − 𝜂) − 𝑒

−𝑟𝜏𝐾(𝑃− − 𝜂)

with 𝜂 = {0 for call1 for put

, 𝑚 = {𝜅 − 𝜌𝜉𝜔𝑖 − 𝜉𝜌 for 𝑃+𝜅 − 𝜌𝜉𝜔𝑖 for 𝑃−

, 𝑢 = {1 for 𝑃+−1 for 𝑃−

𝑔 =𝑚 − 𝑑

𝑚 + 𝑑, 𝑑 = ±√𝑚2 + 𝜉2𝜔(𝜔 − 𝑢𝑖), 𝐶 =

𝜅𝜃

𝜉2(2 ln

1 − 𝑔

1 − 𝑔𝑒−𝑑𝜏+ (𝑚 − 𝑑)𝜏)

𝐷 =𝑚 − 𝑑

𝜉21 − 𝑒−𝑑𝜏

1 − 𝑔𝑒−𝑑𝜏, 𝜒𝜔 = exp(𝐶 + 𝐷𝑣𝑡 + 𝑖𝜔 ln 𝑆𝑡𝑒

(𝑟−𝑞)𝜏)

𝑃 =1

2+1

𝜋∫ ℑ [

𝑒−𝑖𝜔 ln𝐾𝜒𝜔𝜔

]𝑑𝜔ℝ+

(126)

where the 𝜂 denotes the option type with 𝜂 = 1 for calls and 𝜂 = −1 for puts. In Heston’s original

formula [22], the negative solution of 𝑑 is used, which makes the calculation of the complex logarithm

prone to numerical instabilities. This is because taking the principal value of the logarithm causes 𝐶 to

jump discontinuously each time the imaginary part of the argument of the logarithm crosses the negative

real axis (i.e. discontinuity due to branch cut of complex numbers), especially for long maturities.

Albrecher et al. [19] presents an extensive study proving that both solutions are completely equivalent

from a theoretical point of view, it is also mentioned that rather than using the negative solution of 𝑑, the

positive 𝑑 guarantees numerical stability of the resulting formula under a full dimensional and unrestricted

parameter space.

2.4. Piecewise Time Dependent Heston Model

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

36

The time-dependent Heston model we present here was proposed by Elices [20] in 2008. The

model relies on the characteristic function of the two dimensional Markov process, which we have derived

in (106). It bootstraps a series of piecewise constant Heston parameters starting from the earliest maturity,

each parameter set for a period of time, which allows the model to fit to a term structure of the implied

volatility surfaces.

Consider a Markov 𝑛-dimensional stochastic process 𝑌 (i.e. 𝑌 = (𝑥𝑡𝑣𝑡) in Heston model), we define

𝑝𝑦𝑡𝑠,𝑡

the transition probability density function for having 𝑌 = 𝑦𝑡 at time 𝑡 conditional on 𝑌 = 𝑦𝑠 at time

𝑠 where 𝑜 ≤ 𝑠 ≤ 𝑡 ≤ 𝑇. Its characteristic function 𝜙𝜔𝑠,𝑡

is the multi-dimensional Fourier transform of the

transition density 𝑝𝑦𝑡𝑠,𝑡

such that

𝜙𝜔𝑜,𝑡 = ∫ 𝑒𝑖𝜔

′𝑦𝑡𝑝𝑦𝑡𝑜,𝑡𝑑𝑦𝑡

ℝ𝑛= ∫ 𝑒𝑖𝜔

′𝑦𝑡∫ 𝑝𝑦𝑡𝑠,𝑡𝑝𝑦𝑠

𝑜,𝑠𝑑𝑦𝑠ℝ𝑛

𝑑𝑦𝑡ℝ𝑛

= ∫ ∫ 𝑒𝑖𝜔′𝑦𝑡𝑝𝑦𝑡

𝑠,𝑡𝑝𝑦𝑠𝑜,𝑠𝑑𝑦𝑠

ℝ𝑛𝑑𝑦𝑡

ℝ𝑛

= ∫ ∫ 𝑒𝑖𝜔′𝑦𝑡𝑝𝑦𝑡

𝑠,𝑡𝑑𝑦𝑡ℝ𝑛

𝑝𝑦𝑠𝑜,𝑠𝑑𝑦𝑠

ℝ𝑛= ∫ 𝜙𝜔

𝑠,𝑡𝑝𝑦𝑠𝑜,𝑠𝑑𝑦𝑠

ℝ𝑛

(127)

Consider a family of exponential characteristic functions with exponent linear in the state 𝑦𝑠 at time 𝑠

𝜙𝜔𝑠,𝑡 = exp(𝐶𝑠,𝑡(𝜔) + 𝐷𝑠,𝑡(𝜔)′𝑦𝑠) (128)

we have

𝜙𝜔𝑜,𝑡 = ∫ exp(𝐶𝑠,𝑡(𝜔) + 𝐷𝑠,𝑡(𝜔)′𝑦𝑠) 𝑝𝑦𝑠

𝑜,𝑠𝑑𝑦𝑠ℝ𝑛

= exp(𝐶𝑠,𝑡(𝜔))∫ exp(𝐷𝑠,𝑡(𝜔)′𝑦𝑠) 𝑝𝑦𝑠𝑜,𝑠𝑑𝑦𝑠

ℝ𝑛

= exp(𝐶𝑠,𝑡(𝜔))∫ exp [𝑖(−𝑖𝐷𝑠,𝑡(𝜔))′𝑦𝑠] 𝑝𝑦𝑠

𝑜,𝑠𝑑𝑦𝑢ℝ𝑛

= exp(𝐶𝑠,𝑡(𝜔))𝜙𝑜,𝑠(−𝑖𝐷𝑠,𝑡(𝜔))

= exp (𝐶𝑠,𝑡(𝜔) + 𝐶𝑜,𝑠(−𝑖𝐷𝑠,𝑡(𝜔)) + 𝐷𝑜,𝑠(−𝑖𝐷𝑠,𝑡(𝜔))′𝑦𝑜)

(129)

Identifying terms between the (128) for 𝑠 = 𝑜 and the (129), we find that

𝐶𝑜,𝑡(𝜔) = 𝐶𝑠,𝑡(𝜔) + 𝐶𝑜,𝑠(−𝑖𝐷𝑠,𝑡(𝜔)) and 𝐷𝑜,𝑡(𝜔) = 𝐷𝑜,𝑠(−𝑖𝐷𝑠,𝑡(𝜔)) (130)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

37

Formula (130) gives a recursive definition of 𝐶𝑜,𝑡(𝜔) and 𝐷𝑜,𝑡(𝜔), which can be used to bootstrap the

Heston model parameters for each time period starting from the earliest maturity. For illustrative purpose,

the first 3 periods are presented below

Period 𝐶 𝐷

𝑡0 → 𝑡1 𝐶0,1(𝜔) 𝐷0,1(𝜔)

𝑡1 → 𝑡2 𝐶1,2(𝜔) + 𝐶0,1(−𝑖𝐷1,2(𝜔)) 𝐷0,1(−𝑖𝐷1,2(𝜔))

𝑡2 → 𝑡3 𝐶2,3(𝜔) + 𝐶1,2(−𝑖𝐷2,3(𝜔)) + 𝐶0,1 (−𝑖𝐷1,2(−𝑖𝐷2,3(𝜔))) 𝐷0,1 (−𝑖𝐷1,2(−𝑖𝐷2,3(𝜔)))

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

38

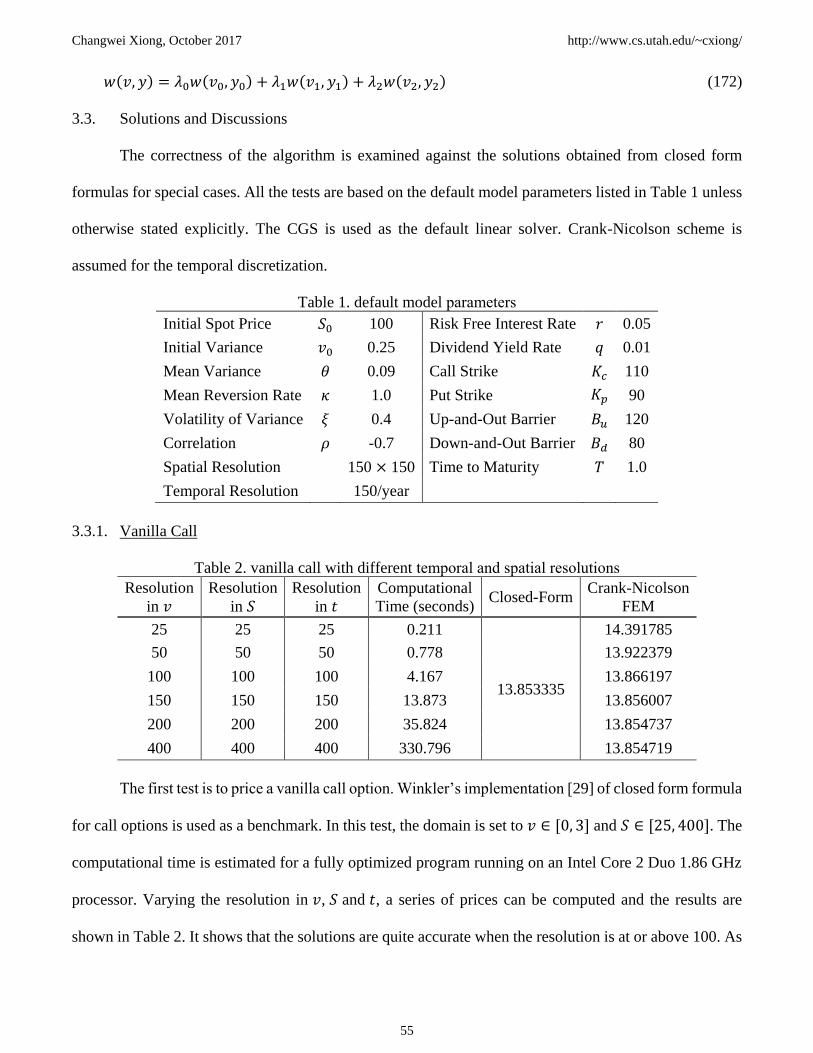

3. HESTON MODEL: PDE BY FINITE ELEMENT METHOD

Valuation of financial derivatives has become a very important subject in modern financial theory

and practice. In 1973, Black and Scholes introduced a simple formula [21] to price European-style options

under a few strong assumptions. It is the first successful attempt to provide an arbitrage free valuation of

financial derivatives. However due to limitations, it fails to capture some critical features observed in

financial markets, such as heavy tails of return, skewness and smile in implied volatility, clustering and

autocorrelation in volatility, etc. Many approaches have been proposed to address these issues. One of

them is to employ stochastic volatility models to describe the price dynamics in financial markets, in

which the volatility of the underlying is assumed to be stochastic. Heston [22] proposed a stochastic

volatility model in 1993. It extends the Black-Scholes model and includes it as a special case. One major

advantage of the Heston model is that it can be solved in closed-form for vanilla options. For exotic

options, closed-form solutions are generally not available, numerical methods must be considered for

option pricing. Monte Carlo simulations, though easy to implement, are not very suitable for computing

risk sensitivities. It turns out that solving partial differential equation (PDE) is not only more numerically

efficient but also more stable in risk sensitivity estimation. Traditionally, the PDE’s that arise from option

pricing are solved dominantly by finite difference method (FDM). FDM is straightforward to implement,

but meanwhile it also imposes many constraints, such as, sufficiently smooth terminal and boundary

conditions, rectangular domains, etc. To relax these constraints, it becomes the primary motivation of this

essay to develop an efficient finite element methods (FEM) for solving the PDE’s. Many studies have

been focused on this topic. Topper [23] provides an excellent introduction to the FEM in the context of

financial engineering applications. Previous work by Winkler et al. [24] illustrates an application of FEM

to valuation of vanilla option in Heston stochastic volatility model. Achdou and Tchou [25] Propose a

finite element analysis for Black-Scholes equation with stochastic volatility process. A recent publication

by Miglio and Sgarra [26] discusses an application of finite element method for option pricing in a

stochastic volatility model with jumps, known as the Bates model.

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

39

In this chapter, we will present an application of finite element method in the Heston model to

price exotic options (specifically, the double barrier knock-out options). It presents a detailed

implementation of the finite element method and its application in option pricing. The numerical results

and conclusions are outlined in the end.

3.1. The Partial Differential Equation

Let 𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡) =1

𝐷𝑡�̃�𝑡[𝐷𝑇𝑈(𝑇, 𝑆𝑇, 𝑣𝑇)] be the price of a contingent payoff 𝑈(𝑇, 𝑆𝑇 , 𝑣𝑇) that

occur at maturity 𝑇 . Assuming deterministic interest rate, we have the dynamics of 𝐷𝑡𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡) in

Heston model (21) under risk neutral measure ℚ, that is

1

𝐷𝑡𝑑(𝐷𝑡𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡)) = 𝑑𝑈 − 𝑟𝑈𝑑𝑡

=𝜕𝑈

𝜕𝑡𝑑𝑡 +

𝜕𝑈

𝜕𝑆𝑑𝑆 +

1

2

𝜕2𝑈

𝜕𝑆2𝑑𝑆𝑑𝑆 +

𝜕𝑈

𝜕𝑣𝑑𝑣 +

1

2

𝜕2𝑈

𝜕𝑣2𝑑𝑣𝑑𝑣 +

𝜕2𝑈

𝜕𝑣𝜕𝑆𝑑𝑣𝑑𝑆 − 𝑟𝑈𝑑𝑡

=𝜕𝑈

𝜕𝑡𝑑𝑡 +

𝜕𝑈

𝜕𝑆(𝑟 − 𝑞)𝑆𝑑𝑡 +

𝜕𝑈

𝜕𝑆𝑆√𝑣𝑑�̃�1 +

𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2𝑑𝑡 +

𝜕𝑈

𝜕𝑣𝜅(𝜃 − 𝑣)𝑑𝑡 +

𝜕𝑈

𝜕𝑣𝜉√𝑣𝑑�̃�2

+𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2𝑑𝑡 + 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆𝑑𝑡 − 𝑟𝑈𝑑𝑡

(131)

Since the 𝐷𝑡𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡) is a martingale under ℚ, the 𝑑𝑡-term in (131) must vanish, which defines a PDE

that the derivative price 𝑈 must follow

𝜕𝑈

𝜕𝑡+𝑣𝜉2

2

𝜕2𝑈

𝜕𝑣2+ 𝑆𝑣𝜉𝜌

𝜕2𝑈

𝜕𝑣𝜕𝑆+𝑣𝑆2

2

𝜕2𝑈

𝜕𝑆2+ 𝜅(𝜃 − 𝑣)

𝜕𝑈

𝜕𝑣+ (𝑟 − 𝑞)𝑆

𝜕𝑈

𝜕𝑆− 𝑟𝑈 = 0 (132)

Prices of different types of derivative securities can be obtained by solving the PDE (132) under

different terminal and boundary conditions. We firstly define a rectangle domain

𝛺 ∶= {(𝑆, 𝑣) ∶ 𝑆 ∈ (𝑆min, 𝑆max), 𝑣 ∈ (𝑣min, 𝑣max)} (133)

The domain boundaries are then taken as

𝛤1 ∶= {(𝑆, 𝑣) ∶ 𝑆 ∈ (𝑆min, 𝑆max), 𝑣 = 𝑣min}

𝛤2 ∶= {(𝑆, 𝑣) ∶ 𝑆 ∈ (𝑆min, 𝑆max), 𝑣 = 𝑣max} (134)

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

40

𝛤3 ∶= {(𝑆, 𝑣) ∶ 𝑆 = 𝑆min, 𝑣 ∈ [𝑣min, 𝑣max]}

𝛤4 ∶= {(𝑆, 𝑣) ∶ 𝑆 = 𝑆max, 𝑣 ∈ [𝑣min, 𝑣max]}

The terminal condition is defined at option maturity. A vanilla call (𝜂 = 1) or put (𝜂 = −1) that matures

in 𝜏 = 𝑇 − 𝑡 would have a terminal condition defined by the maturity payoff function

𝑈(𝑇, 𝑆𝑇 , 𝑣𝑇) = (𝜂(𝑆𝑇 − 𝐾))+

(135)

Given a strike 𝐾 and a properly defined min/max range for 𝑆 and 𝑣, the Dirichlet boundary conditions for

a vanilla option can be defined as follows (here we choose Dirichlet boundary condition because it is

easier to handle. Ideally a zero gamma boundary condition should be used, however the choice of

boundary condition becomes insignificant when the domain for 𝑆 and 𝑣 gets large enough)

𝑈(𝑡, 𝑆𝑡 , 𝑣min) = (𝜂(𝑆𝑡𝑒−𝑞𝜏 − 𝐾𝑒−𝑟𝜏))

+ ∀ (𝑆, 𝑣) ∈ 𝛤1

𝑈(𝑡, 𝑆𝑡 , 𝑣max) =1 + 𝜂

2𝑆𝑡𝑒

−𝑞𝜏 +1 − 𝜂

2𝐾𝑒−𝑟𝜏 ∀ (𝑆, 𝑣) ∈ 𝛤2

𝑈(𝑡, 𝑆min, 𝑣𝑡) =1 − 𝜂

2(𝜂(𝑆min𝑒

−𝑞𝜏 − 𝐾𝑒−𝑟𝜏))+ ∀ (𝑆, 𝑣) ∈ 𝛤3

𝑈(𝑡, 𝑆max, 𝑣𝑡) =1 + 𝜂

2(𝜂(𝑆max𝑒

−𝑞𝜏 − 𝐾𝑒−𝑟𝜏))+ ∀ (𝑆, 𝑣) ∈ 𝛤4

(136)

For a European up-and-out-down-and-out double barrier call/put option, the terminal condition is of the

same form. The Dirichlet boundary conditions change a bit as the min/max value for 𝑆 is limited to the up

and down barriers

𝑈(𝑡, 𝑆𝑡 , 𝑣min) = (𝜂(𝑆𝑡𝑒−𝑞𝜏 − 𝐾𝑒−𝑟𝜏))

+ ∀ (𝑆, 𝑣) ∈ 𝛤1

𝑈(𝑡, 𝑆𝑡 , 𝑣max) = 0 ∀ (𝑆, 𝑣) ∈ 𝛤2

𝑈(𝑡, 𝑆min, 𝑣𝑡) = 0 ∀ (𝑆, 𝑣) ∈ 𝛤3

𝑈(𝑡, 𝑆max, 𝑣𝑡) = 0 ∀ (𝑆, 𝑣) ∈ 𝛤4

(137)

Equation (132) can be further simplified by change of variable, which yields

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

41

𝜕𝑤

𝜕𝑡+𝜉2𝑣

2

𝜕2𝑤

𝜕𝑣2+ 𝜌𝜉𝑣

𝜕2𝑤

𝜕𝑣𝜕𝑦+𝑣

2

𝜕2𝑤

𝜕𝑦2+ 𝜅(𝜃 − 𝑣)

𝜕𝑤

𝜕𝑣+ (𝑟 − 𝑞 −

𝑣

2)𝜕𝑤

𝜕𝑦− 𝑟𝑤 = 0 (138)

where we define 𝑦𝑡 = ln𝑆𝑡

𝐾 and 𝑤(𝑡, 𝑦𝑡 , 𝑣𝑡) = 𝑈(𝑡, 𝑆𝑡 , 𝑣𝑡). The PDE (138) is actually identical to our

previously derived (92) with variables

𝑤(𝑡, 𝑦𝑡 , 𝑣𝑡) = 𝑒𝑟𝑡ℎ(𝑡, 𝑥𝑡 , 𝑣𝑡), 𝑥𝑡 = ln

𝑆𝑡𝑆0− (𝑟 − 𝑞)𝑡 (139)

This can be shown by using the chain rule to derive partial derivatives after change of variables

𝜕𝑤

𝜕𝑡= (

𝜕

𝜕𝑡+𝜕𝑥

𝜕𝑡

𝜕

𝜕𝑥) (𝑒𝑟𝑡ℎ) = 𝑒𝑟𝑡 (𝑟ℎ +

𝜕ℎ

𝜕𝑡+𝜕𝑥

𝜕𝑡

𝜕ℎ

𝜕𝑥) = 𝑒𝑟𝑡 (𝑟ℎ +

𝜕ℎ

𝜕𝑡− (𝑟 − 𝑞)

𝜕ℎ

𝜕𝑥)

𝜅(𝜃 − 𝑣)𝜕𝑤

𝜕𝑣= 𝑒𝑟𝑡𝜅(𝜃 − 𝑣)

𝜕ℎ

𝜕𝑣,

𝜉2𝑣

2

𝜕2𝑤

𝜕𝑣2= 𝑒𝑟𝑡

𝜉2𝑣

2

𝜕2ℎ

𝜕𝑣2

(𝑟 − 𝑞 −𝑣

2)𝜕𝑤

𝜕𝑦= (𝑟 − 𝑞 −

𝑣

2)𝜕(𝑒𝑟𝑡ℎ)

𝜕𝑥

𝜕𝑥

𝜕𝑦= 𝑒𝑟𝑡 (𝑟 − 𝑞 −

𝑣

2)𝜕ℎ

𝜕𝑥

𝑣

2

𝜕2𝑤

𝜕𝑦2= 𝑒𝑟𝑡

𝑣

2

𝜕

𝜕𝑦(𝜕ℎ

𝜕𝑡

𝜕𝑡

𝜕𝑦+𝜕ℎ

𝜕𝑥

𝜕𝑥

𝜕𝑦) = 𝑒𝑟𝑡

𝑣

2

𝜕2ℎ

𝜕𝑥2

𝜌𝜉𝑣𝜕2𝑤

𝜕𝑣𝜕𝑦= 𝜌𝜉𝑣

𝜕

𝜕𝑣(𝜕(𝑒𝑟𝑡ℎ)

𝜕𝑥

𝜕𝑥

𝜕𝑦) = 𝑒𝑟𝑡𝜉𝜌𝑣

𝜕2ℎ

𝜕𝑣𝜕𝑥

(140)

For simplicity, the PDE (138) can be written in terms of the gradient and divergence operator

(𝜕𝑡 + 𝛁 ∙ 𝐀𝛁 − 𝐛 ∙ 𝛁 − 𝑟)𝑤 = 0, 𝐀 =𝑣

2(𝜉2 𝜌𝜉𝜌𝜉 1

) , 𝐛 = (

𝜉2

2− 𝜅(𝜃 − 𝑣)

𝑣 + 𝜌𝜉

2− (𝑟 − 𝑞)

) (141)

where 𝜕𝑡 = 𝜕/𝜕𝑡, the gradient operator 𝛁 = (𝜕𝑣𝜕𝑦), and the divergence operator 𝛁 ∙ = (

𝜕𝑣𝜕𝑦) ∙. Note that we

have the following identities

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

42

𝛁 ∙ 𝐀𝛁 = (𝜕𝑣𝜕𝑦)𝑇 𝑣

2(𝜉2 𝜌𝜉𝜌𝜉 1

) (𝜕𝑣𝜕𝑦) = (

𝜕𝑣𝜕𝑦)𝑇 𝑣

2(𝜉2𝜕𝑣 + 𝜌𝜉𝜕𝑦𝜌𝜉𝜕𝑣 + 𝜕𝑦

)

=𝜉2𝜕𝑣 + 𝜌𝜉𝜕𝑦

2+𝑣

2(𝜉2𝜕𝑣𝑣 + 𝜌𝜉𝜕𝑣𝑦) +

𝑣

2(𝜌𝜉𝜕𝑣𝑦 + 𝜕𝑦𝑦)

=𝜉2

2𝜕𝑣 +

𝜌𝜉

2𝜕𝑦 + 𝜌𝜉𝑣𝜕𝑣𝑦 +

𝑣𝜉2

2𝜕𝑣𝑣 +

𝑣

2𝜕𝑦𝑦

𝐛 ∙ 𝛁 = (

𝜉2

2− 𝜅(𝜃 − 𝑣)

𝑣 + 𝜌𝜉

2− (𝑟 − 𝑞)

)

𝑇

(𝜕𝑣𝜕𝑦) =

𝜉2

2𝜕𝑣 − 𝜅(𝜃 − 𝑣)𝜕𝑣 +

𝑣 + 𝜌𝜉

2𝜕𝑦 − (𝑟 − 𝑞)𝜕𝑦

𝛁 ∙ 𝐀𝛁 − 𝐛 ∙ 𝛁 = 𝜌𝜉𝑣𝜕𝑣𝑦 +𝑣𝜉2

2𝜕𝑣𝑣 +

𝑣

2𝜕𝑦𝑦 + 𝜅(𝜃 − 𝑣)𝜕𝑣 + (𝑟 − 𝑞 −

𝑣

2) 𝜕𝑦

(142)

Henceforth, we will use (∙) to denote dot product. If we think of column vectors as the standard vectors,

the divergence operator can be regarded as transpose of the gradient operator (a bit abuse of notation).

3.2. Numerical Solution of the PDE

The PDE (141) shows a 2-D dynamic problem. To solve this problem, a semi-discretization in

time is applied, which yields a series of 2-D static boundary value problems. These 2-D static boundary

value problems are then solved numerically by a 2-D finite element method as time advances.

3.2.1. Temporal Discretization

It should be noted that the time advances backwards, such that the initial value is given at the

terminal 𝑡𝑁 = 𝑇 and the solution is sought at 𝑡0 = 0. Note that the superscript is used to denote the index

of time-step. The partial derivative with respect to time is approximated by finite difference method.

According to (141), the 𝜎-weighted finite difference scheme for time is given as

𝑤𝑘+1 −𝑤𝑘

𝑡𝑘+1 − 𝑡𝑘+ (1 − 𝜎)(𝛁 ∙ 𝐀𝛁 − 𝐛 ∙ 𝛁 − 𝑟)𝑤𝑘+1 + 𝜎(𝛁 ∙ 𝐀𝛁 − 𝐛 ∙ 𝛁 − 𝑟)𝑤𝑘 = 0 (143)

In the above equation, the scheme becomes purely explicit when 𝜎 = 0, purely implicit when 𝜎 = 1, and

becomes Crank-Nicolson scheme when 𝜎 = 0.5. The computation starts backwards from 𝑡𝑁 = 𝑇 when

𝑤𝑁 is known which is given by initial condition. At each time-step, provided that the 𝑤𝑘+1 is computed

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

43

from previous step, the 𝑤𝑘 can be solved from (143) recursively. Rearrangement of (143) gives a new

equation below, in which all the 𝑤𝑘+1 terms are collected on the right hand side (RHS) and all the 𝑤𝑘

terms on the left hand side (LHS)

ℒ𝑤𝑘 = ℛ𝑤𝑘+1 where

ℒ = 𝜎(𝛁 ∙ 𝐀𝛁 − 𝐛 ∙ 𝛁) − 𝑐 and ℛ = (𝜎 − 1)(𝛁 ∙ 𝐀𝛁 − 𝐛 ∙ 𝛁) − (𝑐 − 𝑟)

𝑐 = 𝜎𝑟 +1

𝑡𝑘+1 − 𝑡𝑘

(144)

3.2.2. Two-Dimensional Finite Element Method

Finite element method is based on weak formulation. It is ideal for solving PDE when the solution

lacks smoothness and when the domain is irregular, dynamically changing, and/or unevenly spaced.

Valuation of complex exotic options can often exhibit these features, which makes FEM an ideal tool for

this type of applications.

3.2.2.1. Weak Formulation

Equation (144) can be transformed to a weak formulation by multiplying both sides with a scalar-

valued test function 𝜓 (in the subsequent sections, we will see that the 𝜓 can be constructed as a linear

combination of basis functions on the 2-D domain)

∫𝜓ℒ𝑤𝑘𝑑𝛺𝛺

= ∫𝜓ℛ𝑤𝑘+1𝑑𝛺𝛺

where

LHS = 𝜎∫𝜓𝛁 ∙ 𝐀𝛁𝑤𝑘𝑑𝛺𝛺

− 𝜎∫𝜓𝐛 ∙ 𝛁𝑤𝑘𝑑𝛺𝛺

− 𝑐∫𝜓𝑤𝑘𝑑𝛺𝛺

RHS = (𝜎 − 1)∫𝜓𝛁 ∙ 𝐀𝛁𝑤𝑘+1𝑑𝛺𝛺

− (𝜎 − 1)∫𝜓𝐛 ∙ 𝛁𝑤𝑘+1𝑑𝛺𝛺

− (𝑐 − 𝑟)∫𝜓𝑤𝑘+1𝑑𝛺𝛺

(145)

where 𝛺 is the open domain given in (133).

Assuming that 𝑢 is a scalar function and 𝐯 a vector-valued function, both are continuously

differentiable, then the integration by parts in multi-dimension is given by

Changwei Xiong, October 2017 http://www.cs.utah.edu/~cxiong/

44

∫𝑢𝛁 ∙ 𝐯𝑑𝛺𝛺

= ∮𝑢𝐯 ∙ 𝐧𝑑𝛤𝛤

−∫𝛁𝑢 ∙ 𝐯𝑑𝛺𝛺

(146)

where 𝛤 denotes the piecewise smooth boundary, and 𝐧 denotes the outward unit surface normal to 𝛤.

Applying the transformation (146) to (145) yields (here, it becomes the first Green’s identity)

∫𝜓ℒ𝑤𝑘𝑑𝛺𝛺

= ∫𝜓ℛ𝑤𝑘+1𝑑𝛺𝛺

where

LHS = 𝜎∮𝜓𝐀𝛁𝑤𝑘 ∙ 𝐧𝑑𝛤𝛤

− 𝜎∫𝛁𝜓 ∙ 𝐀𝛁𝑤𝑘𝑑𝛺𝛺

− 𝜎∫𝜓𝐛 ∙ 𝛁𝑤𝑘𝑑𝛺𝛺

− 𝑐∫𝜓𝑤𝑘𝑑𝛺𝛺

RHS = (𝜎 − 1)∮𝜓𝐀𝛁𝑤𝑘+1 ∙ 𝐧𝑑𝛤𝛤

− (𝜎 − 1)∫𝛁𝜓 ∙ 𝐀𝛁𝑤𝑘+1𝑑𝛺𝛺

− (𝜎 − 1)∫𝜓𝐛 ∙ 𝛁𝑤𝑘+1𝑑𝛺𝛺

− (𝑐 − 𝑟)∫𝜓𝑤𝑘+1𝑑𝛺𝛺

(147)

Now let’s define a few functional spaces for the trial solution 𝑤 and the test function 𝜓

𝐿2(𝛺) ∶= {𝑓: ‖𝑓‖𝐿2 < ∞} where ‖𝑓‖𝐿𝑝 = (∫ |𝑓|𝑝

𝛺

𝑑𝛺)

1/𝑝

𝐻1(𝛺) ∶= {𝑓 ∈ 𝐿2(𝛺) ∶ 𝒟1𝑓 ∈ 𝐿2(𝛺)}

𝐻01(𝛺) ∶= {𝑓 ∈ 𝐻1(𝛺) ∶ 𝑓 = 0 on 𝛤}

𝐻𝑔1(𝛺) ∶= {𝑓 ∈ 𝐻1(𝛺) ∶ 𝑓 = 𝑔 on 𝛤}

(148)

where 𝒟1𝑓 denotes the first order weak partial derivatives of function 𝑓. The 𝐿2(𝛺) is the Lebesgue space

with Euclidean norm which coincides with Hilbert space in this case. The 𝐻1(𝛺), 𝐻01(𝛺) and 𝐻𝑔

1(𝛺) are

all Sobolev space. The variational form (147) is also called the weak form. The requirements of the